Embed Size (px)

Citation preview

Fraudulent Financial Reporting and Forensic Accounting

Presented by:

Victor Hieken, UHY Advisors

Jeffrey Streif, UHY Advisors

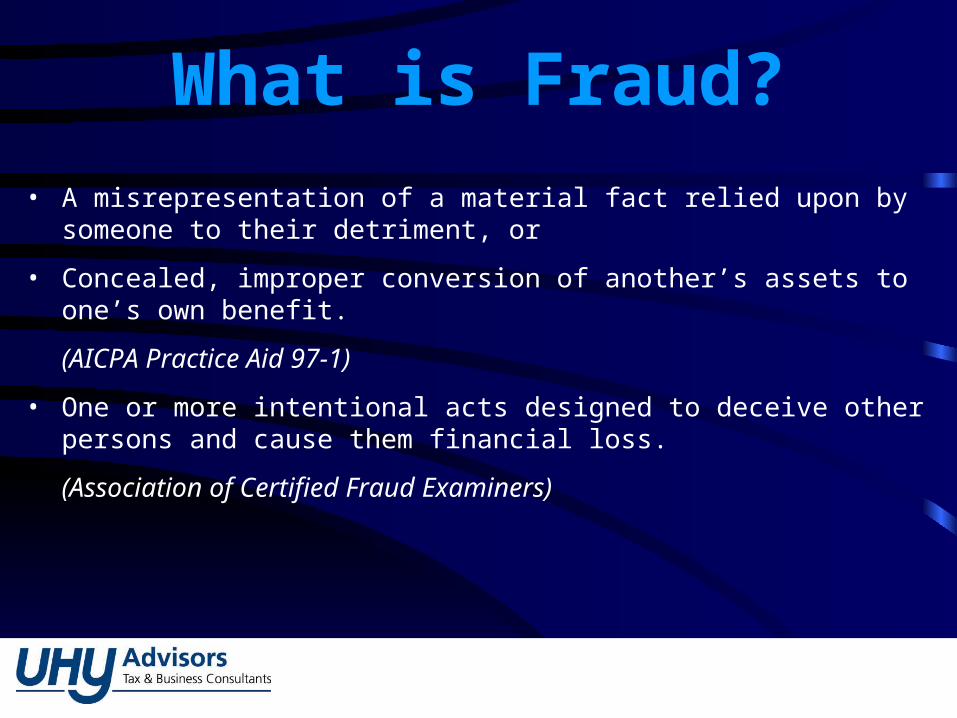

• A misrepresentation of a material fact relied upon by someone to their detriment, or

• Concealed, improper conversion of another’s assets to one’s own benefit.

(AICPA Practice Aid 97-1)

• One or more intentional acts designed to deceive other persons and cause them financial loss.

(Association of Certified Fraud Examiners)

What is Fraud?

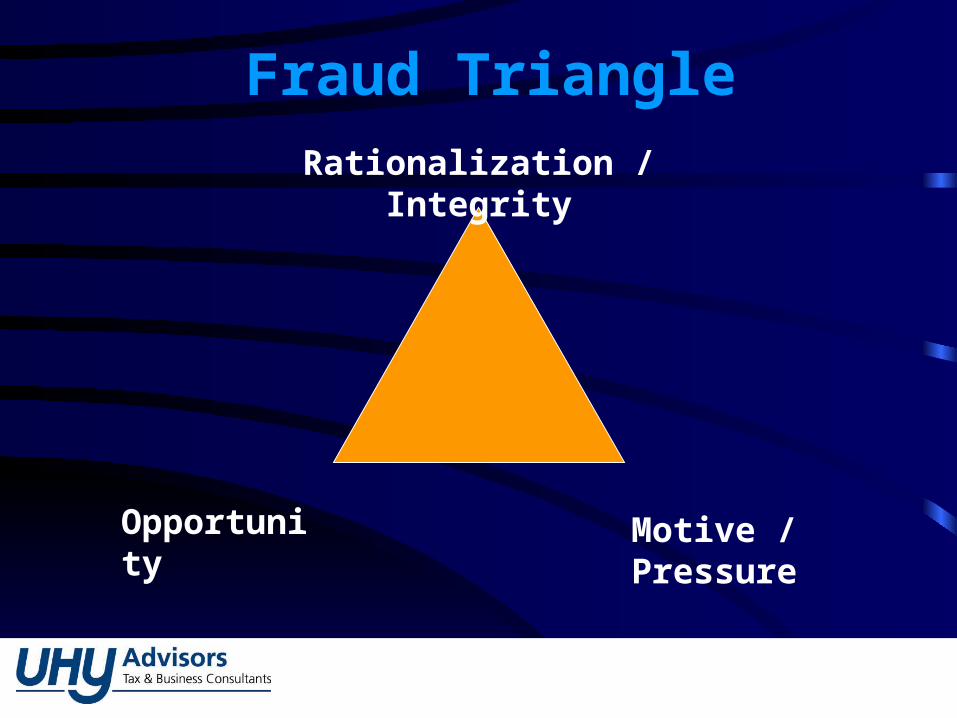

Fraud Triangle

Opportunity Motive / Pressure

Rationalization / Integrity

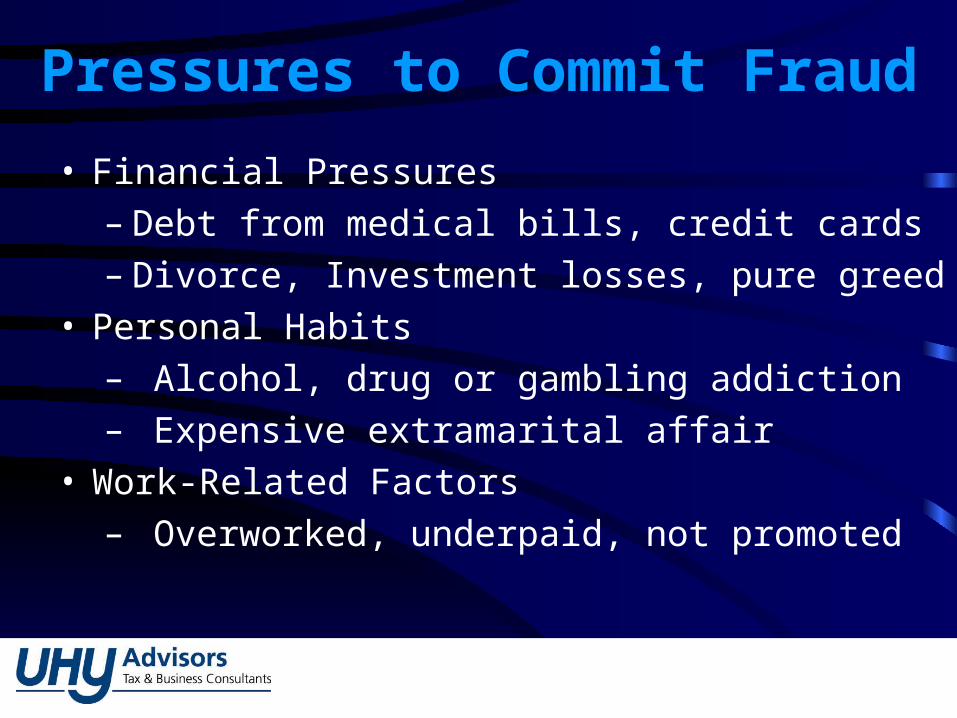

Pressures to Commit Fraud

• Financial Pressures– Debt from medical bills, credit cards– Divorce, Investment losses, pure greed

• Personal Habits– Alcohol, drug or gambling addiction– Expensive extramarital affair

• Work-Related Factors– Overworked, underpaid, not promoted

Opportunities to Commit Fraud

• Internal controls are weak

• Excessive levels of trust

Rationalization to Commit Fraud

Integrity

• Most important factor in keeping a person from misappropriating assets or committing

management fraud.

Opportunity

Where are the Opportunities?• Most common types of employee fraud include:

– Theft of cash by diverting cash receipts, manipulating accounts receivable cash postings (lapping), altering bank deposits, stealing or forging checks, stealing petty cash, etc.

– Manipulation of invoices, including fictitious or overstated vendor invoices.– Theft of inventory or equipment.– Kickbacks.– Credit card fraud.– False entries in accounts to increase performance results (management

fraud).– Abuse of travel and entertainment reimbursement to include personal

items.– Payroll schemes such as ghost employees or overstated hours.

VictimsThe smallest organizations suffer the largest median

losses because of three factors:

1. Basic accounting controls often are lacking.

2. Higher levels of trust.

3. Small companies are less likely to be audited.

Deterring Fraud

• Internal controls– Segregation of duties– Procedures manual– Timely financial reporting– Mandatory vacations

• Audits

• Financial analyses

• Corporate fraud policy

Types of Entities

• Nonprofit & Governmental

• Public companies

• Privately held companies

Types of Fraud

• Third party fraud

• Management fraud

• Employee fraud

Third Party FraudCommitted by those not involved with the organization

and normally benefits the third party, rather than the company or management.

– Overbilling Schemes– Defective Products– Bid Rigging– Bribery/Corruption– Economic Espionage/Extortion

Employee Fraud(Occupational Fraud)

Committed by employees for their own benefit and to the detriment of the organization.

- Embezzlement- Kickbacks- Ghost Employees- Theft of Inventory- Bribery/Corruption

The Cost of Occupational Fraud

• Costs U.S. organizations - $600 billion annually.

• Average 5% total annual revenues by its own

employees.

Cash Misappropriation

Over 80% of occupational fraud involves asset misappropriation –

with cash being targeted 90% of the time.

Management FraudCommitted by management for the direct benefit of the

organization. Management benefits indirectly.

– Financial Statement Fraud

Financial Statement Fraud

MOTIVATION• Economy, Business Environment• Executive incentives:

– Stock prices are tied to meeting Wall Street’s earnings forecasts– Focus is on short-term performance only– Companies are heavily punished for not meeting forecasts– Executives have been endowed with stock options—far exceeds

compensation (tied to stock price)– Performance is based on earnings & stock price

• Wall Street expectations: rewards for short-term behavior

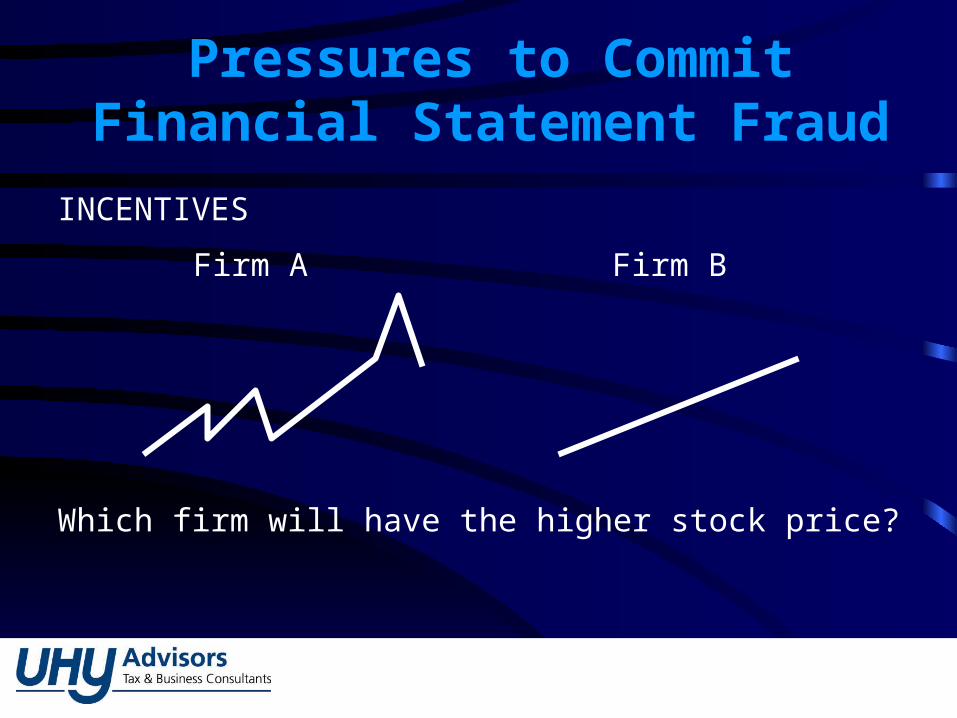

Pressures to Commit Financial Statement Fraud

INCENTIVES

Which firm will have the higher stock price?

Firm A Firm B

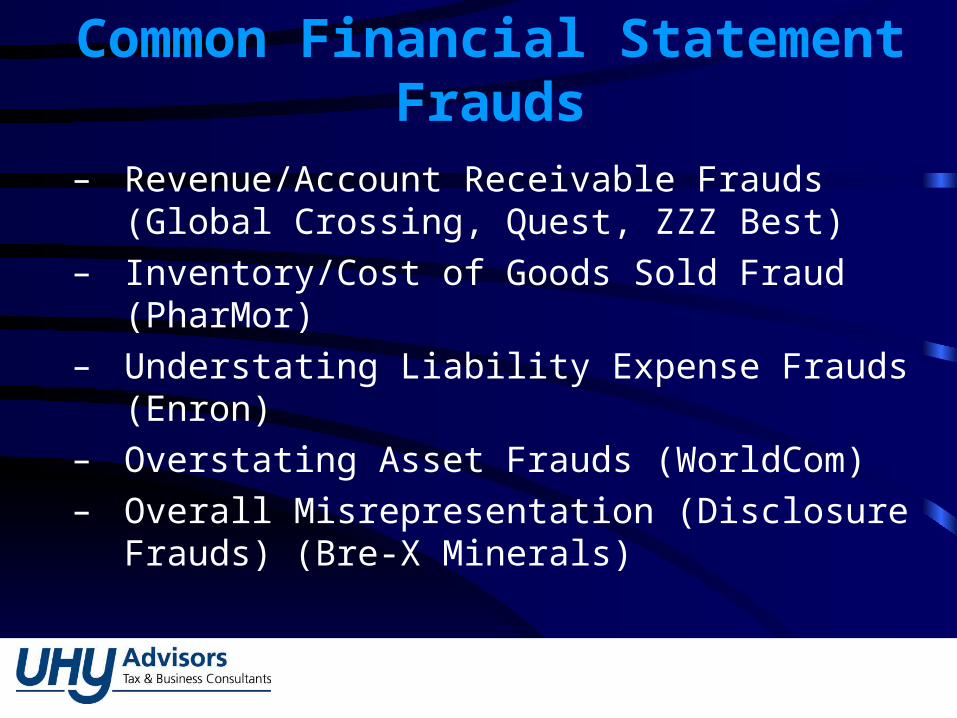

Common Financial Statement Frauds

– Revenue/Account Receivable Frauds (Global Crossing, Quest, ZZZ Best)

– Inventory/Cost of Goods Sold Fraud (PharMor)– Understating Liability Expense Frauds (Enron)– Overstating Asset Frauds (WorldCom)– Overall Misrepresentation (Disclosure Frauds)

(Bre-X Minerals)

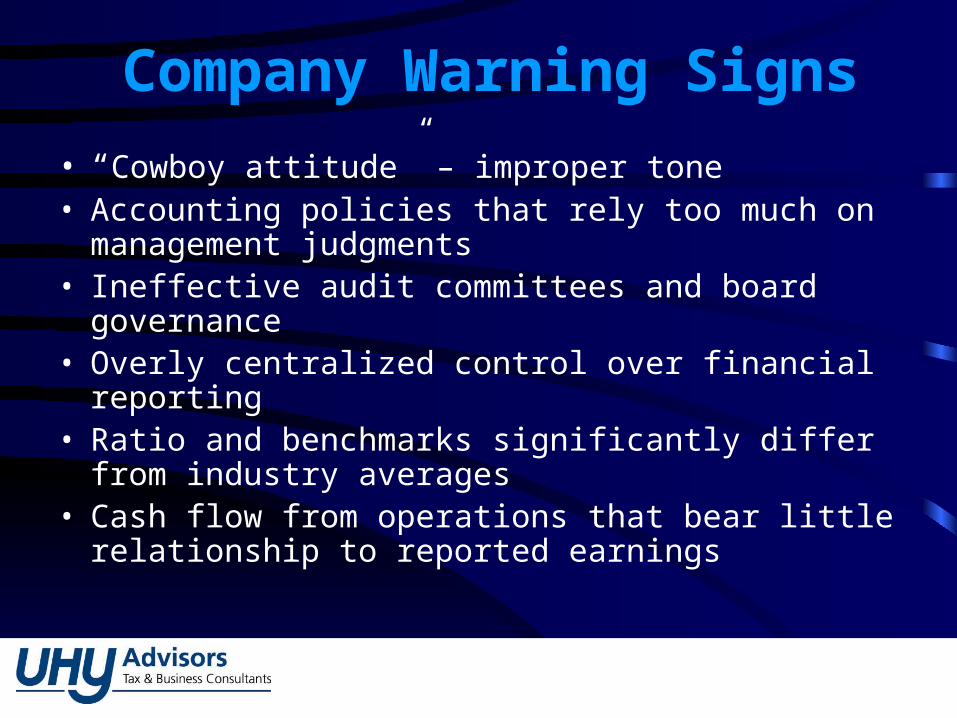

Company Warning Signs

• “Cowboy attitude” – improper tone• Accounting policies that rely too much on management

judgments• Ineffective audit committees and board governance• Overly centralized control over financial reporting• Ratio and benchmarks significantly differ from industry

averages• Cash flow from operations that bear little relationship to

reported earnings

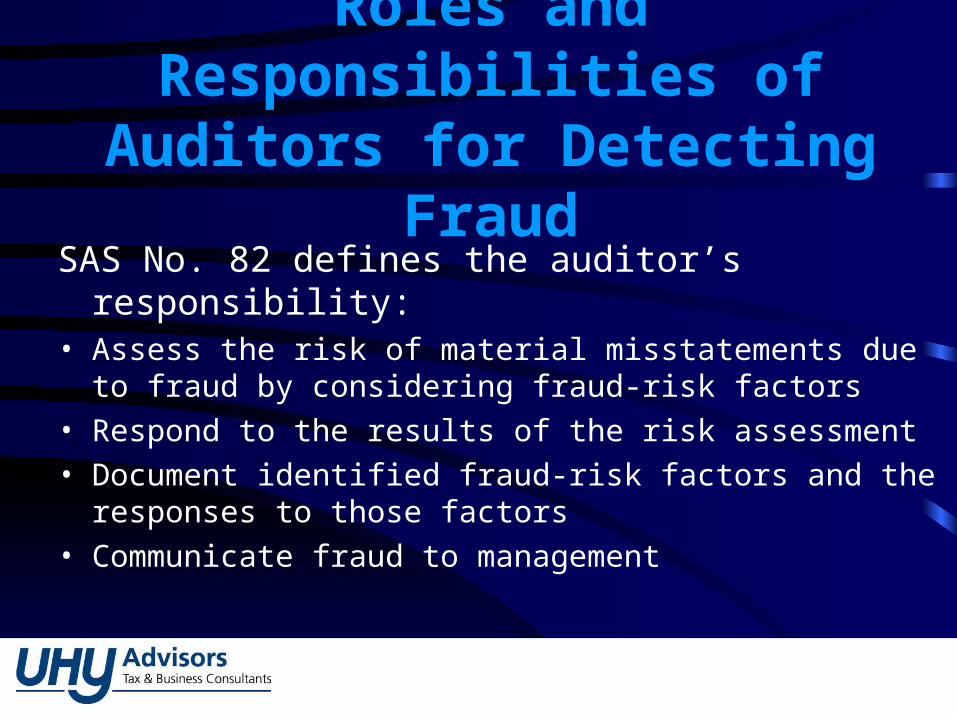

Roles and Responsibilities of Auditors for Detecting Fraud

SAS No. 82 defines the auditor’s responsibility:• Assess the risk of material misstatements due to fraud by

considering fraud-risk factors • Respond to the results of the risk assessment• Document identified fraud-risk factors and the responses to

those factors• Communicate fraud to management

Roles and Responsibilities of Auditors for Detecting Fraud

SAS 99 requires auditors to• plan the audit to provide reasonable assurance that financial

statements are free of material fraud. • adopt an attitude of professional skepticism toward clients,• conduct brainstorming sessions to assess the risk of

material fraud and how it could be concealed,• conduct an assessment of a client's overall antifraud

programs, and look for red flags that may indicate fraud.

Audit Process

• Gain understanding of clients operations and industry• Understand internal control environment – operations and IT

controls• What are outside influences or third party influences• Are there any related parties• Understand management involvement and responsibilities

Audit Process

• Brainstorming• Risk Assessment• Modification of procedures• Interviews of High and low level management• Review key internal controls to determine reliance

Audit Process

Computer Assisted Audit Tools are used more frequently in the normal audit process such as IDEA to increase coverage and quality of audit evidence

• 100% of population tested• Sampling• Automated tests

What is Forensic or Investigative Accounting?

Forensic accounting services - generally involve the application of special skills in accounting, auditing, finance, quantitative methods, certain areas of the law and research, and investigative skills to collect, analyze, and evaluate evidential matter and to interpret and communicate findings, and may involve either an attest or consulting engagement.

Definition adopted by the AICPA Business Valuation/Forensic and Litigation Services Executive Committee; January 2006

Tools Used in Forensic Audit

• IDEA or ACL are used to analyze, extract and manipulate large amounts of raw data

• Benford’s Law• Lowers scope based upon criteria• Saves time and fees

Tools Used in Forensic Audit

Forensic software such as Encase and FTK Imager are used to acquire and analyze electronic data in Computer Forensic investigations

Important to maintain proper chain of evidence in case dispute goes to litigation

Questions?