Embed Size (px)

Citation preview

Insights & Observations for Not-For-Profit Organizations Volume 6 :: Issue 1

Not-For-ProfitInsider

In This Issue

Capital/Major Gift GivingCampaigns and Fundraising Trends ....... 1,2

Tax Update: Is YourNon-Profit OrganizationComplying? .................... 3

Trends in ReportingOperating Metrics........4, 5

The Price of FederalFunding: MoreReporting ....................6, 7

The most successful capital/major gift giving campaigns are perpetual in nature for many Not-for-Profit (NFP) Organizations. How do they do this and what are the methods, tools and techniques that get results? Also, what are some of the recent trends on who gives, how they give and when they support charities?

First, I would like to acknowledge and credit Mr. Jim Radford, President of Holmes, Radford & Avalon, who presented several ideas and concepts on this topic at UHY’s Nonprofit Roundtable Series in St. Louis in November 2010. Some of those ideas included:

• Value of Feasibility Studies – a process to gain input and fresh, independent ideas that translate to the possible, the potential and the probable. It can be used for strategic issues and planning, campaign, annual fund, planned giving and relationship building. It shapes vision, provides a roadmap to the future, and inspires and creates destiny. The study process can take 8-10 weeks, and may involve up to 40 people in personal, confidential interviews. It will identify local and regional funding possibilities.

Continued on Page 2...

Capital/Major Gift Giving Campaigns and Fundraising Trends

The Next Level Of Service UHY LLP

2 UHY LLP Not-For-Profit Insider Volume 6 :: Issue 1

• Value of Capital Campaigns – a process that provides numerous benefits including: transformation and change, exponential revenue stream, encourages donors to “Think Big”, builds volunteer leadership fundraising veterans, increased visibility in the community, and enables donors to pledge over several years to give larger gifts. The campaign can take six months on readiness, eight months on leadership gifts and four months of community gifts.

• Value of Engaging Donors – a process of building lasting relationships, building a force for good, opening doors and creating opportunities. The value is creating a joyous process for everyone.

To further expand on the critical aspects of fundraising, the focus on relationship building with the donor is the single most important factor. A quote from Marshall Howard’s book “Let’s Have Lunch Together” states….”Without powerful relationships, it’s a constant uphill battle to develop a stronger board, impact major giving, expand grants, increase event income, or drive a successful capital campaign”.

Mr. Marshall’s book illustrates the power of relationships and how donors who are valued and understood give ten times more than other donors. Donors want to establish relationships with people they trust. Do you know the donor personally, including family and children? Mr. Howard states, “People decide emotionally and justify logically”. Many NFPs believe that donors give based on the mission and the wonderful programs. Yes, many do give, but the larger gifts are from people that have strong relationships.Finally, I would like to recap trends on how people donate (Giving

Channels – last 2 years) from a study from the NonProfit Times in April 2010 “Haiti Donations Seen as Tipping Point for Mobile Giving” :

• 52% Checkout Donation • 49% Check by Mail • 32% Gift Shop • 31% Website • 27% Fundraising Event • 26% Honor/Tribute Gift • 20% Third Party Vendor • 14% Phone • 14% Monthly Debit • 8% Mobile/Text • 5% Social Networking Site

Other research indicates that most charities receive 50% of their annual online donations during November and December. Younger donors are increasingly likely to make contributions via websites or social networking sites.

Action idea: Utilize the expertise of independent consultants to review your approach to fundraising and related activities.

Capital/Major Gift Giving Campaigns and Fundraising Trends Continued from Page 1...

For more information, please feel free to contact Patrick Rohrkaste, Partner, at (314) 615-1221 or [email protected].

UHY LLP The Next Level Of Service

Volume 6 :: Issue 1 Not-For-Profit Insider UHY LLP 3

Although FASB ASC 740-10 formerly knows as (FIN 48) - Accounting for Uncertainty in Income Taxes has been applicable to non-public and non-profit corporations for fiscal years beginning January 1, 2009, many non-profit organizations should still examine whether or not they are actively complying with the standard.

As a refresher, the guidance provides a methodology to analyze tax positions in order to create uniformity in accounting for income taxes. The purpose of FIN 48 is to promote transparency for the reader of financial statements. As a result, its application goes hand-in-hand with the recent changes in the Form 990, which promotes the same theory of full disclosure for the reader of the exempt organization tax return.

Citing their income tax exemption status, many non-profit organizations consider the guidance irrelevant to their organization. While this may be true in most circumstances, exempt organizations should still consider reviewing their operations to discuss areas where the organization may miss the application.

While a tax position is basically a position taken on a tax return, it may also include making the decision to refrain from reporting certain items or from filing certain tax returns. This would include the application of state as well as federal tax laws. For a non-profit corporation, it is important to note that the tax exempt status of the entity itself is considered a tax position.

For example, entities that claim tax exemption under section 501(c)(3) should have the documentation to substantiate their tax exempt status. In addition, the organization should document its activities that support its stated purpose or the mission of its exemption. In this regard, the organization should review whether any political activity or significant lobbying activities could rise to the level of where it could affect the tax exemption. In addition, consideration should be made whether the level or conduct of certain business activities may also affect tax exempt status.

Another major tax position category for a non-profit organization is in the area of unrelated business income. The organization should review its activities to conclude whether or not it has unrelated business activities. If so, the non-profit should review whether it is properly complying by filing Form 990-T. The organization should also analyze its activities to conclude whether it may have

nexus with other states that requires compliance with various state tax regulations.

The activities of related entities such as taxable subsidiaries should also be considered. There are many tax positions that can be created by such relationships which may result in taxable income such as rents, royalties or interest. Investment by a tax exempt entity made through partnerships or limited liability companies can lead to unrelated business income tax issues that may have not been considered.

The activities undertaken by the flow through entity affect the non-profit investor as reported on the Form K-1. The exempt entity should ensure that the flow through entity is providing sufficient information to determine if the unrelated business rules apply. Caution should also be exercised in the area of debt financed property, which the organization may own directly or through investments, in flow through entities that may lead to unrelated business income issues.

After an analysis is made of any tax issues, such as those previously mentioned, it must be determined whether there are any material amounts that may have to be recognized on the financial statement of the non-profit as the result of an uncertain position that was taken. Consequently, there could be a significant impact on the financial reporting of the organization.

This discussion should prompt organizations to consider whether or not they have actively pursued or thought of the reporting requirements or have simply ignored them on the basis that they do not believe it affects them. The non-profit should coordinate the application of ASC 740-10 with their public accountants to ensure compliance with the requirements.

If you have any questions or concerns regarding the applications of ASC 740-10, contact your UHY Advisors professional.

Tax Update: Is Your Non-Profit Organization Complying?

For more information, please contact James Daniels, Partner, at (518) 449-3166 or [email protected].

Capital/Major Gift Giving Campaigns and Fundraising Trends Continued from Page 1...

The Next Level Of Service UHY LLP

4 UHY LLP Not-For-Profit Insider Volume 6 :: Issue 1

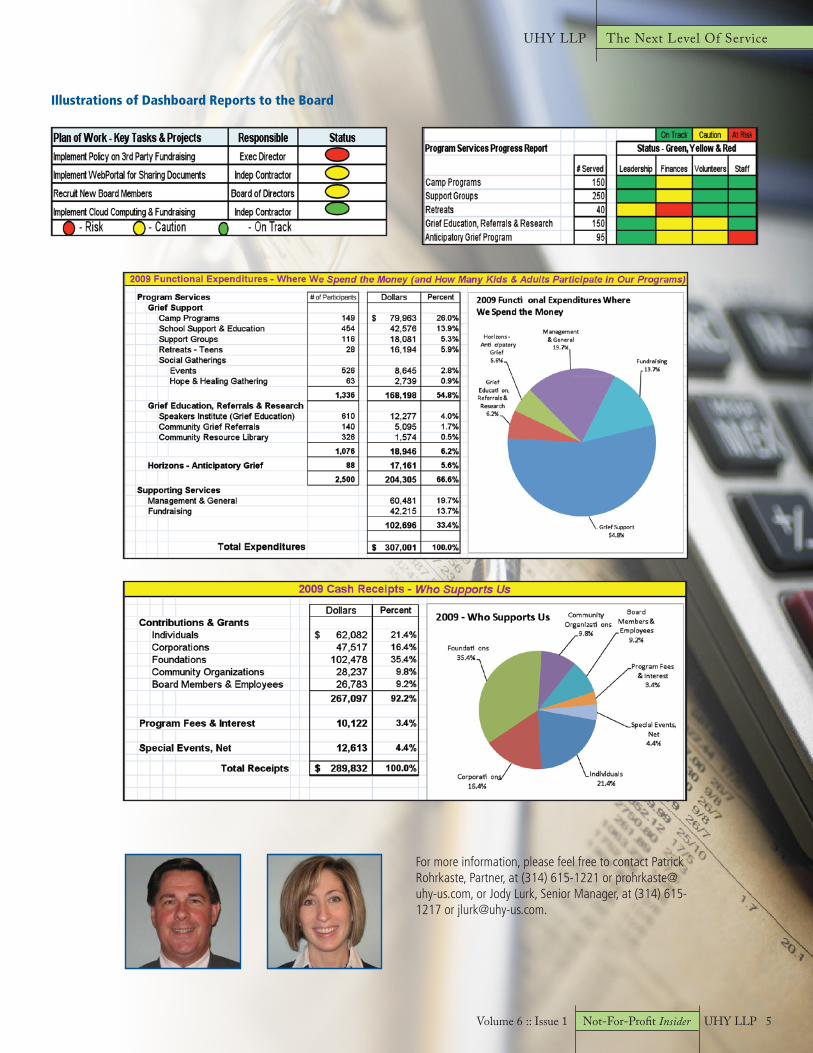

Trends in Reporting Operating MetricsPresent Data, Figures and Pictures to Maximize Action!

In the past decade, Not-for-Profit (NFP) entities have been dealing with numerous regulatory and accounting changes, including the revisions to IRS Form 990, increased reporting demands of charity watch groups and accounting changes for endowments. As a result, the nature and volume of information are comprehensive, but based on the traditional reporting formats most information is presented in figures without percentages and visuals (graphs, charts, clipart, etc.).

Operating metrics vary from basic to advanced presentations. The more advanced metrics include correlations between financial and nonfinancial operational data and incorporate pictures and graphics for those individuals who are moved/motivated by visual data. Information on program services, employees, board of directors, and volunteers that is linked to financial results can be used to showcase the activities of the entity that can be leveraged into more grants and funds. So, let’s review some of the best practices and trends in reporting operating metrics:

1. Measurement Data….are you telling your story?a. Cash position – unrestricted, designated by the

board for operations (3-6 months of annual expenditures) and restricted.

b. Net assets – unrestricted, temporarily restricted (time, program and expenditure) and permanently restricted (endowments under control and endowments held by third party trusts).

c. Statistics – program, fundraising and administrative.d. Donor – cash and noncash (dollars, number of,

segmented by giving levels).e. Volunteer data – numbers, junior boards, volunteer

hours, impact on programs and fundraising.f. Historical results – recommend five years to illustrate

trends on revenues, expenses and nonfinancial data on # of people served on programs.

g. Program successes – quantify statistics on effectiveness of programming (for example, pre-service data compared to post-service data).

h. Key targets – financial, program and capacity.i. Research and development – investment in new

program initiatives/activities.

2. Reporting Techniques – Master Scorecard & Dashboard (keep it simple & limit to 1-2 pages) a. List top three strategic directions of the entity with

the planned metrics. The metrics that are reported on a quarterly basis illustrate actual performance for the quarter and year-to-date with benchmark data for the prior year and the target for the current year.

b. List bar charts of overall revenues and expenses for actual, budget and prior year. Also, supplemental charts of key revenue and expense components and/or operating funds (excluding endowments or significant restricted funds) may contribute to the presentation.

c. Pie charts of revenues by category (United Way, Monetary, Services, and Investment) and expenses by functional area (Program and Supporting Services) will demonstrate that the Entity is accountable and transparent. Additionally, communicating the trends on volunteers, people served and the impact of the program effectiveness is extremely valuable.

d. List other benchmarks that address the key concerns of watchdog groups. For example, BBB compliance, unqualified audit, employee and/or customer satisfaction.

Action Idea – Review current reporting systems, databases, Form 990, annual reports, grant proposals for ideas on information and how it is presented. Do you need to expand or curtail information to improve your story?

UHY LLP The Next Level Of Service

Volume 6 :: Issue 1 Not-For-Profit Insider UHY LLP 5

Trends in Reporting Operating MetricsPresent Data, Figures and Pictures to Maximize Action!

Illustrations of Dashboard Reports to the Board

For more information, please feel free to contact Patrick Rohrkaste, Partner, at (314) 615-1221 or [email protected], or Jody Lurk, Senior Manager, at (314) 615-1217 or [email protected].

The Next Level Of Service UHY LLP

6 UHY LLP Not-For-Profit Insider Volume 6 :: Issue 1

If you had just become used to hearing the term ARRA without having a panic attack, there is now a new potential source of anxiety: FFATA. FFATA, the Federal Funding Accountability and Transparency Act, is not new legislation, per se; it was signed into law on September 26, 2006, by President George W. Bush. The reason FFATA is starting to make headlines again is that many of its provisions became effective on October 1, 2010.

FFATA is similar to ARRA (the American Recovery and Reinvestment Act) in its intent to make the government transparent and accountable for its spending decisions by using the newest information technology resources, but it goes beyond the ARRA reporting in several aspects. To begin, the provisions of FFATA affect all entities that receive federal awards (direct and first tier sub-recipients) regardless of the type or amount of federal funding received, and are applicable for all new awards effective October 1, 2010.

The other major difference is that FFATA reporting is going to be monthly (not quarterly, as with ARRA). The first reporting was due November 30, 2010, for the month ending October 31, 2010. The collected information on federal awards is then published and accessible through a searchable website: www.USASpending.gov.

The term federal awards used in FFATA is quite broad and includes grants, sub-grants, loans, awards, cooperative agreements and other forms of financial assistance as well as contracts, sub-contracts, purchase orders, task orders and delivery orders. ARRA grants, awards that involve classified information and benefit payments, and other awards to individuals who apply for or receive the awards as natural persons are excluded from reporting under FFATA. Other transactions that are presently exempted from reporting include individual transactions below $25,000 and credit card transactions before October 1, 2008.

Who is affected?

FFATA affects a spectrum of entities: for-profit and nonprofit corporations, associations, partnerships, limited liability companies, limited liability partnerships, sole proprietorships, any other legal business entities and states or localities. Entities with gross income of less than $300,000 for the previous tax year (from any source) are exempted from reporting.

Additionally, not-for-profit entities that do not meet the threshold subjecting them to the federal Single Audit Act may still be subject to the provisions of FFATA.

All recipients of federal awards (grants and/or contracts) are required to register in the Central Contractor Registration system at https://www.bpn.gov/ccr/. In addition, prior to submitting FFATA reports, the prime awardees must register in the new FFATA Sub-award Reporting System (FSRS) at http://www.fsrs.gov.

FSRS was created to collect the required data from the federal awardees for reportable sub-awards (grants or contracts greater than $25,000) and executive compensation. In a memo to federal agencies, the Office of Management and Budget (OMB) clarified that awardees would be required to submit data only on first-tier sub-grants and sub-contracts.

Reporting requirements

All awardees should have implemented the requirement to collect sub-award data prior to October 1, 2010. Awardees and sub-awardees (recipients, sub-recipients, contractors and sub-contractors) should be prepared to report on applicable awards (grants, contracts and orders greater than $25,000) as soon as practicable after the sub-award, or a subsequent change to the sub-award, has been made, but no more than 30 days after that event. The prime awardee has a responsibility to inform the sub-awardees at the time of the award of all reportable data elements and to monitor the completion of those requirements on a monthly basis. It is the sub-awardee’s responsibility to report to the prime awardee all information required by FSRS.

The reporting requirements are phased in for federal contracts and sub-contracts and are effective as follows:

• For contracts greater than or equal to $20,000,000, reporting started July 1, 2010,

• For contracts greater than or equal to $550,000, reporting started October 1, 2010, and

• For contracts greater than or equal to $25,000, reporting starts March 1, 2011.

There is no phase-in of the reporting requirements for federal grants and sub-grants.

The Price of Federal Funding: More Reporting

UHY LLP The Next Level Of Service

Volume 6 :: Issue 1 Not-For-Profit Insider UHY LLP 7

The Price of Federal Funding: More Reporting

Sub-award reporting

The sub-award information reported in FSRS is very similar to what is being reported under ARRA at http://www.FederalReporting.gov:

• Name of entity receiving award • Amount of award• Funding agency • NAICS code for contracts/CFDA program number for grants • Program source • Award title • Location of the entity (including congressional district) • Place of performance (including congressional district) • Unique identifier of the entity and its parent (if owned by

another entity)

Compensation and names of top five executives (prime and/or sub-awardee), limited to entities that have met all three of the following requirements:

• More than 80% of annual gross revenues are funded by the Federal government,

• Annual gross revenues are greater than $25 million in the previous fiscal year, and

• Compensation information is not already available through reporting to the SEC or some other public source (IRS Form 990).

For ARRA-funded contracts subject to FFATA reporting, the prime recipient will be required to report the contracts to both FederalReporting.gov and FSRS, if required by the contract.

However, for ARRA-funded grants subject to FFATA reporting, the prime recipient will not be required to report the grants to both FederalReporting.gov and FSRS. ARRA-funded grants will continue to be reported to FederalReporting.gov only and all non-ARRA funded federal grants will be reported to FSRS.

Making things a little easier

Some prime and sub-award information will be pre-populated in FSRS with data from the Federal Assistance Award Database System (FAADS), the Federal Procurement Data System (FPDS) and the Central Contractor Registration System (CCR) to ensure quality data and minimize unintended data entry errors by sub-recipients. The federal agency making the award will pre-populate the prime award recipient information by reporting it in FAADS for grant awards and in FPDS for contract awards. FSRS interfaces with the above three systems (FAADS, FPDS and CCR) to make the information available to the general public in USASpending.gov.

FSRS takes an “awardee-centric” approach, allowing the prime awardees to manage and report against multiple contracts and/or grants awarded to their registered DUNS number. The awardees

can sort and filter their worklist by type, i.e. contract or grant, by awarding agency and by other filter terms. Awardees will be able to see, by award number, the FFATA sub-award reports filed against that particular contract and/or grant.

Now, even though FSRS reporting is not specifically addressed in the latest A-133 audit guide, OMB considers this to be required reporting and, as such, the awardees’ timeliness and accuracy of FSRS reporting will be audited, and any non-compliance will result in a finding.

Summing things up, sub-recipient monitoring and reporting and timeliness of the reporting are expected to be the major issues in the FFATA implementation process.

Please contact Nelly Gizdova, Manager, at (410) 423-4800 or [email protected] for more information.

Not-For-Profit Industry InsightWith the increasing complexity of laws and regulations, it’s important for associations, foundations, charities, hospitals, schools and other tax-exempt entities to seek out professionals with extensive experience in not-for-profit compliance issues.

• Accounting/Assurance

• Audit, Reviews & Compilations

• Financial Management Consulting

• Internal Controls & Forensic Accounting

• Compliance/Governance Capabilities

• Accounting Policies and Procedures

Updates

• Design, Implementation & Testing

of Internal Controls

uhyllp-us.com

Our Locations

The statements contained herein are provided for informational purposes only, are not intended to constitute tax advice which may be relied upon to avoid penalties under any federal, state, local or other tax statues or regulations, and do not resolve any tax issues in your favor. Furthermore, such statements are not presented or intended as, and should not be taken or assumed to constitute legal advice of any nature, for which advice it is recommended that you consult your own legal counselors and professionals.

UHY Advisors, Inc. provides tax and business consulting services through wholly owned subsidiary entities that operate under the name of “UHY Advisors.” UHY Advisors, Inc. and its subsidiary entities provide services from offices across the United States. UHY Advisors, Inc. and its subsidiary entities are not licensed CPA firms. UHY LLP is a licensed independent CPA firm that performs attest services in an alternative practice structure with UHY Advisors, Inc. and its subsidiary entities. UHY Advisors, Inc. and UHY LLP are U.S. members of Urbach Hacker Young International Limited, an international association of legally independent professional service firms.

• Sarbanes-Oxley Education

• Tax & Management Consulting

• Cost Allocation Planning Assistance

• Financial Forecasting Analysis

• Implementation of New Accounting

Standards

• IRS Controversy

• State, Federal and Local Tax Planning

• Unrelated Business Income Tax Analysis

Additional UHY Advisors Locations

Atlanta ...................................................... 678.602.4470

Columbia - B. Jennine Anderson ................. 410.423.4800

Southfield - Cleat Spacht/Heather Raschke ....248.355.0280Sterling Heights ............................................ 586.254.8141

St. Louis - Patrick Rohrkaste ....................... 314.615.1301Oakland ..................................................... 201.337.0007

Albany - Marilyn Pendergast ....................... 518.449.3171

New York - Dan Desire................................ 212.381.4800Westchester ............................................... 914.697.4966

Dallas - Scott Lunsford................................ 214.243.2900

Houston - Louise Duble .............................. 713.561.6500

Chicago ..................................................... 312.578.9600New York ................................................... 646.746.1120Houston ..................................................... 713.548.0900Washington ............................................... 202.609.6100

GeorgiaMarylandMichigan

Missouri

New JerseyNew York

Texas

IllinoisNew York

TexasWashington DC

© 2011