Embed Size (px)

Citation preview

Fraport @Santander EuroLatam Conference

New York September 2015

Stefan J. Rüter Head of Finance & Investor Relations

Marc Poeschmann Investor Relations

Disclaimer

This document has been prepared by Fraport solely for use in this presentation.

The information contained in this document has not been independently verified. No representation or warranty – whetherexpress or implied – is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctnessof the information or opinions contained therein. Neither the company nor any of its affiliates, advisors or representatives shallhave any liability whatsoever (in negligence or otherwise) for any loss arising from any use of this document or its content orotherwise arising in connection with this document.

This document does not constitute an offer or invitation to purchase or subscribe for any shares and neither this document norany part of it shall form the basis of, or be relied upon in connection with, any contract or commitment whatsoever.

This document contains forward-looking statements that are based on current estimates and assumptions made by themanagement of Fraport to the best of its knowledge. Such forward-looking statements are subject to risks and uncertainties,the non-occurrence or occurrence of which could cause the actual results – including the financial condition and profitability ofFraport – to differ materially from or be more negative than those expressed or implied by such forward-looking statements.This also applies to the forward looking estimates and forecasts derived from third-party studies. Consequently, neither thecompany nor its management can give any assurance regarding the future accuracy of the opinions set forth in this documentor the actual occurrence of the predicted developments.

By accepting this document, you agree with the foregoing.

Fraport @Santander EuroLatam Conference2

Fraport @Santander EuroLatam Conference3

Agenda

- Traffic Insight

- Details on T3

- International Business Development

- Appendix

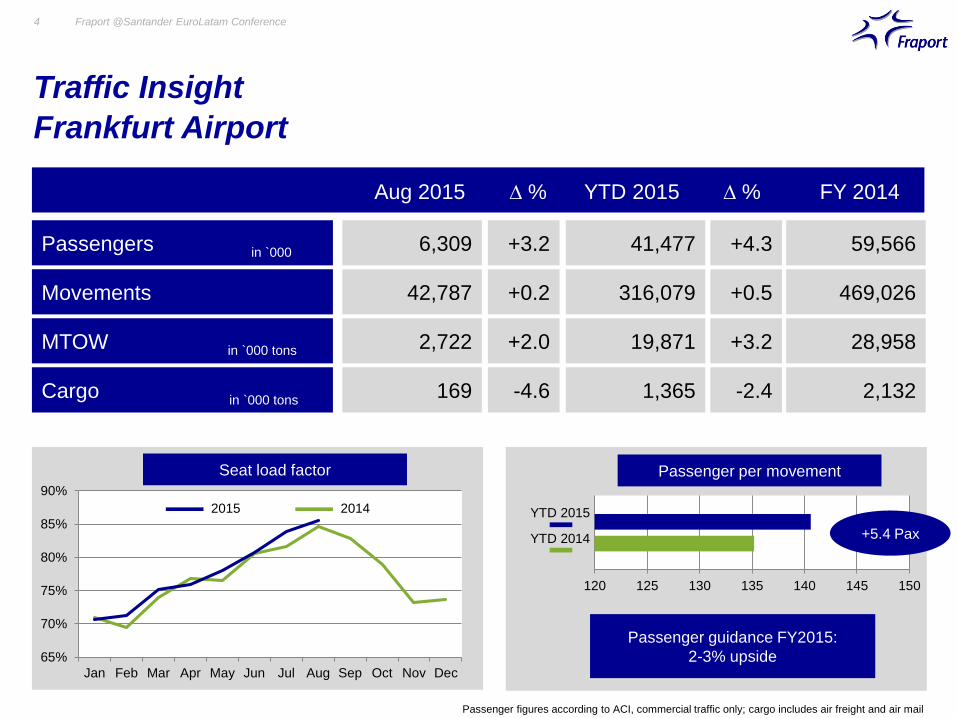

Traffic Insight

Frankfurt Airport

Fraport @Santander EuroLatam Conference4

Passengers

Movements

MTOW

Cargo

Aug 2015 YTD 2015

41,477

316,079

19,871

1,365

6,309

42,787

2,722

169

+3.2

+0.2

+2.0

-4.6

+4.3

+0.5

+3.2

-2.4

D %D %

in `000

in `000 tons

65%

70%

75%

80%

85%

90%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Seat load factor

2015 2014

FY 2014

in `000 tons

Passenger per movement

120 125 130 135 140 145 150

Passenger guidance FY2015:

2-3% upside

+5.4 Pax

YTD 2015

YTD 2014

59,566

469,026

28,958

2,132

Passenger figures according to ACI, commercial traffic only; cargo includes air freight and air mail

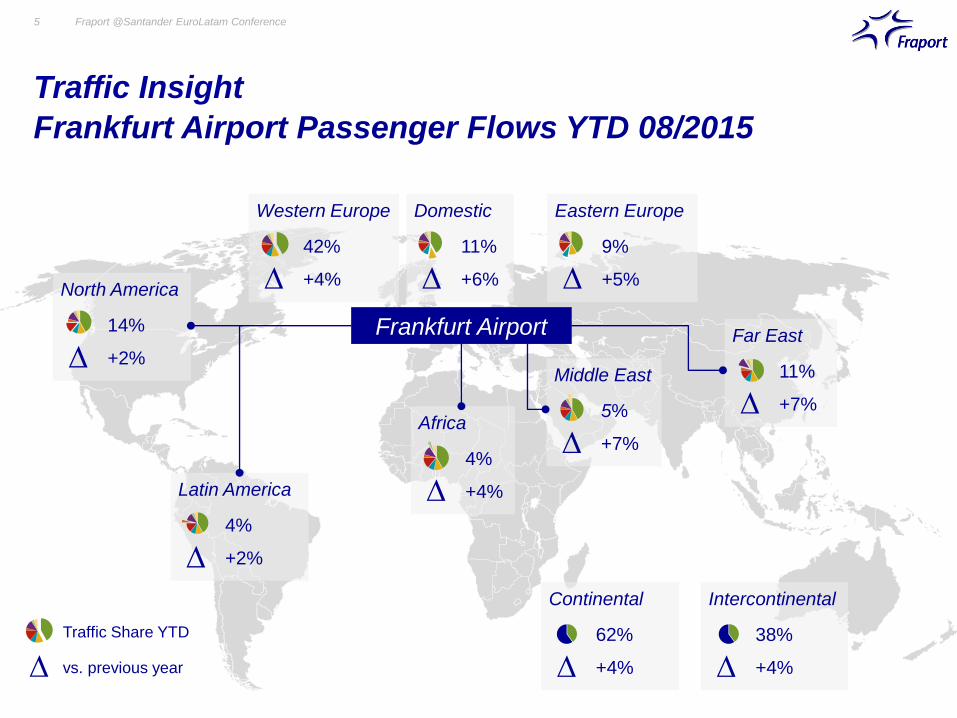

Traffic Insight

Frankfurt Airport Passenger Flows YTD 08/2015

Fraport @Santander EuroLatam Conference5

Western Europe

42%

+4%D

D

Traffic Share YTD

vs. previous year

Domestic

11%

+6%D

Eastern Europe

9%

+5%DNorth America

14%

+2%DFar East

11%

+7%DMiddle East

5%

+7%DAfrica

4%

+4%DLatin America

4%

+2%D

Continental

62%

+4%D

Intercontinental

38%

+4%D

Frankfurt Airport

Traffic Insight

Group Passenger Development (stakes above 10%)

Fraport @Santander EuroLatam Conference6

IATA

CodeAirport Share

Aug

2015

Dprevious

year

YTD

2015

Dprevious

year

FY

2014

CAGR

2010-

2014

FRA Frankfurt, Germany 100% 6,309 +3.2% 41,477 +4.3% 59,566 +3.0%

LJU Ljubljana, Slovenia 100% 180 +10.4% 978 +10.9% 1,307 -1.4%

LIM Lima, Peru 70% 1,594 +8.5% 11,160 +8.9% 15,659 +11.1%

BOJ Burgas, Bulgaria 60% 724 -3.1% 1,964 -8.5% 2,530 +7.5%

VAR Varna, Bulgaria 60% 345 -2.6% 1,082 -1.9% 1,387 +3.1%

AYT Antalya, Turkey 51% 4,496 -0.5% 19,324 -2.0% 27,979 +6.0%

LED St. Petersburg, Russia 35.5% 1,688 -3.7% 9,456 -4.2% 14,265 +14.0%

HAJ Hanover, Germany 30% 590 +3.8% 3,611 +5.3% 5,292 +1.1%

XIY Xi‘an, China 24.5% 3,127 +8.9% 21,877 +13.6% 29,177 +12.8%

Traffic Insight

Accumulated Group Passenger Development since 2009(stakes above 10%)

Fraport @Santander EuroLatam Conference7

60

80

100

120

140

160

180

200

220

2009 2010 2011 2012 2013 2014

in %

FRA +17%

LED +111%

Russia, China & Peru booming since 2009

– FRA with 17% doing well

XIY +91%

LIM +78%

AYT +50%

BUL +35%

HAJ +6%

Fraport @Santander EuroLatam Conference8

Agenda

- Traffic Insight

- Details on T3

- International Business Development

- Appendix

> 60

> 65

> 70

> 75

> 80

58

> 60> 65

> 70

> 75

> 80

45,0

50,0

55,0

60,0

65,0

70,0

75,0

80,0

85,0

90,0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

64 mil. Passengers per year

(dedicated capacity)

68 mil. Passengers per year

(temporary overload)

Capacity T1+T2

Hall C and CD-Pier (2007)

Pier A-Plus (2012)

Year

Passengers per

year in mil.

Forecast MKmetric

Forecast Intraplan

Capacity

restriction

9

Details on T3

Traffic Forecast of Passengers FRA until 2030

Fraport @Santander EuroLatam Conference

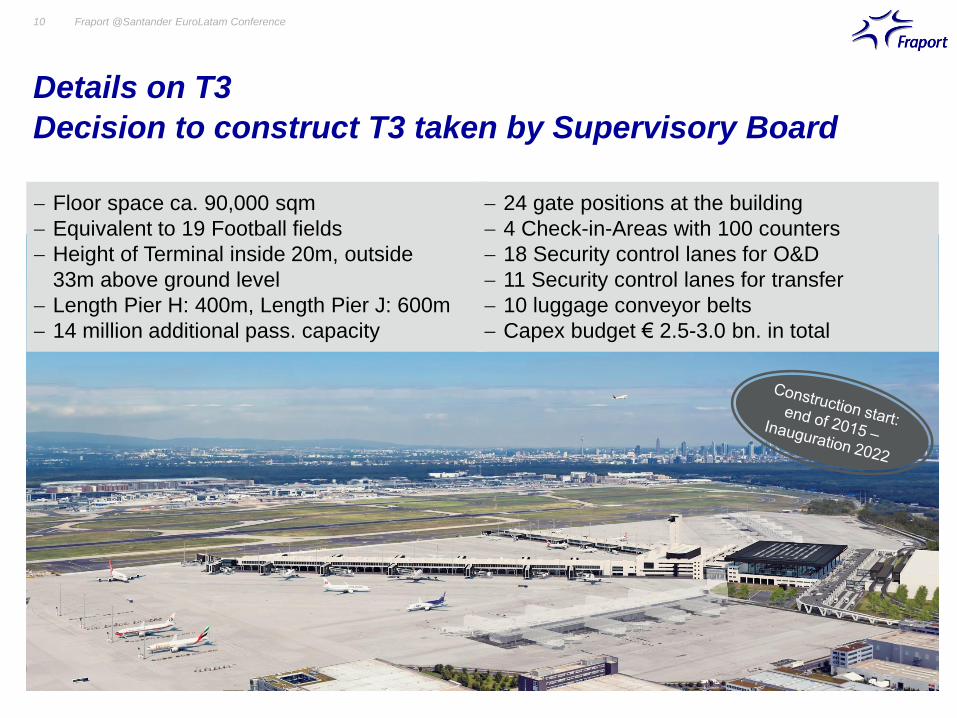

Floor space ca. 90,000 sqm

Equivalent to 19 Football fields

Height of Terminal inside 20m, outside

33m above ground level

Length Pier H: 400m, Length Pier J: 600m

14 million additional pass. capacity

24 gate positions at the building

4 Check-in-Areas with 100 counters

18 Security control lanes for O&D

11 Security control lanes for transfer

10 luggage conveyor belts

Capex budget € 2.5-3.0 bn. in total

10

Details on T3

Decision to construct T3 taken by Supervisory Board

Fraport @Santander EuroLatam Conference

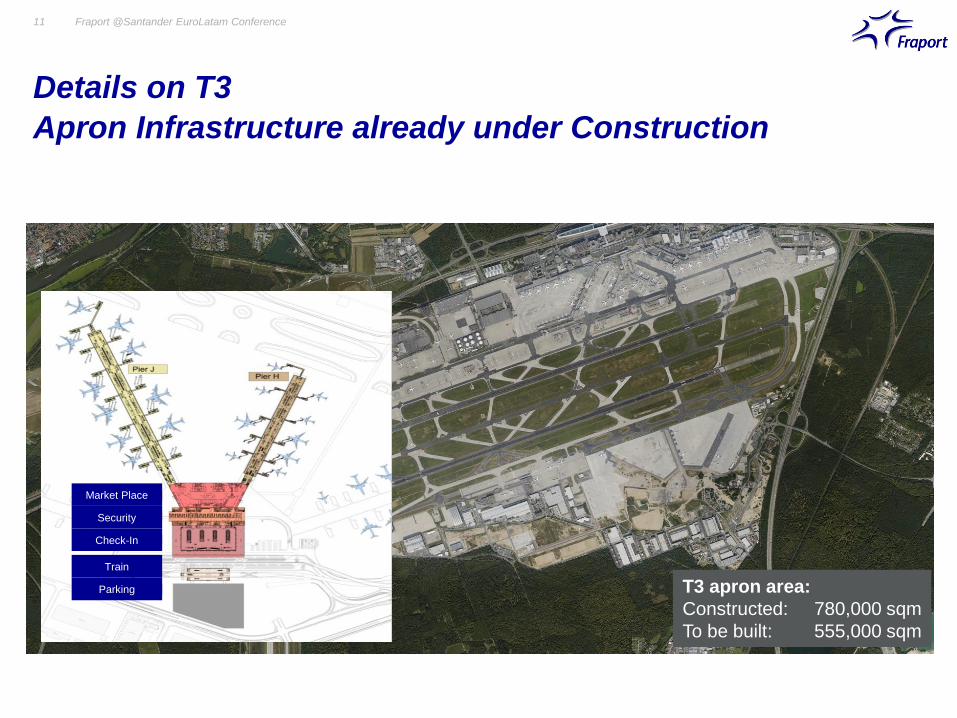

T3 apron area:

Constructed: 780,000 sqm

To be built: 555,000 sqm

Market Place

Security

Check-In

Parking

Train

11 Fraport @Santander EuroLatam Conference

Details on T3

Apron Infrastructure already under Construction

12 Fraport @Santander EuroLatam Conference

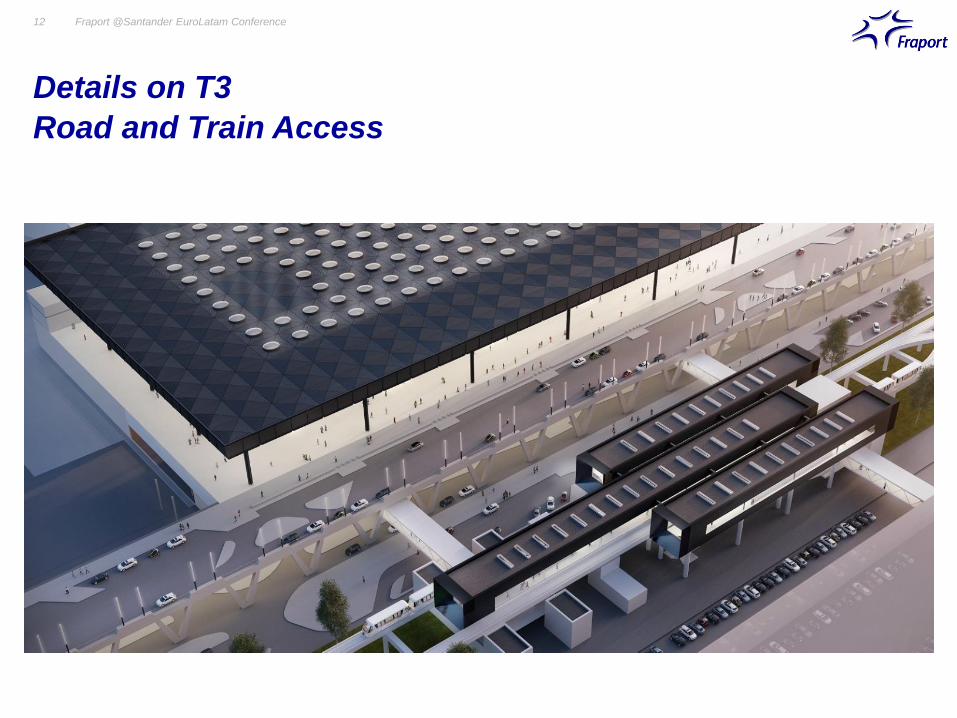

Details on T3

Road and Train Access

13 Fraport @Santander EuroLatam Conference

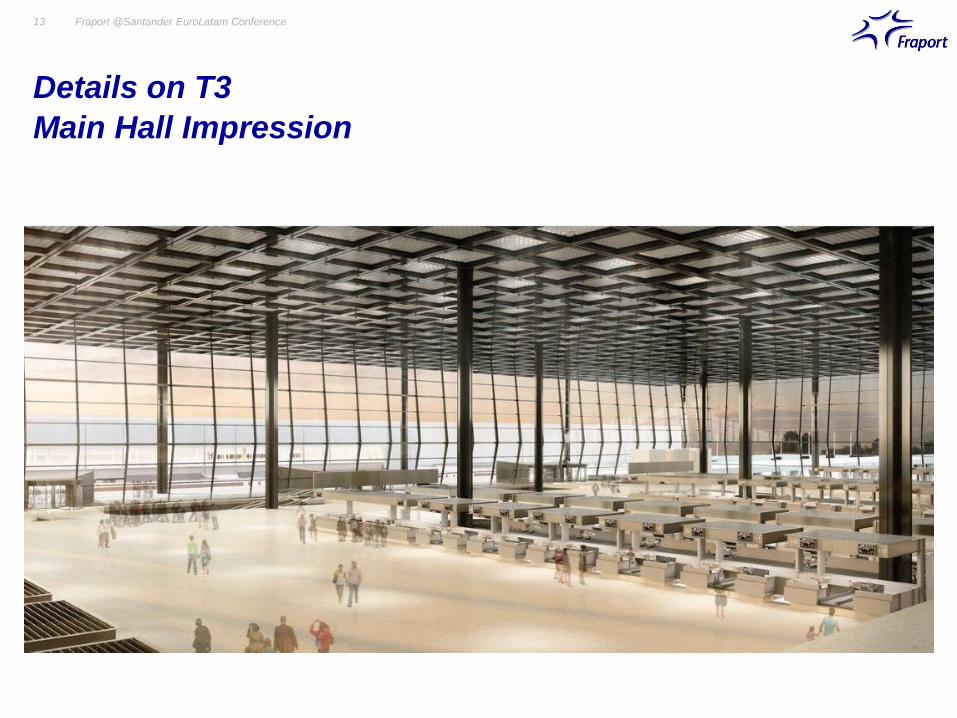

Details on T3

Main Hall Impression

Details on T3

Façade Impression

Fraport @Santander EuroLatam Conference14

2015 2016 2017 2018 2019 2020 2021 2022

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

1 2 3 4

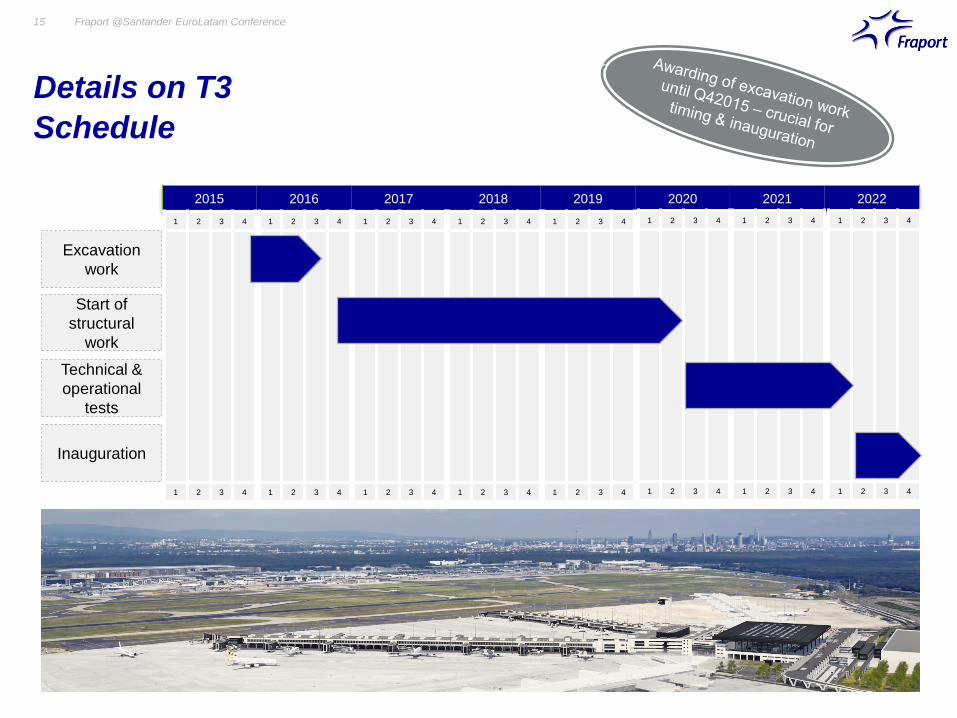

Excavation

work

Start of

structural

work

Technical &

operational

tests

Inauguration

15

Details on T3

Schedule

Fraport @Santander EuroLatam Conference

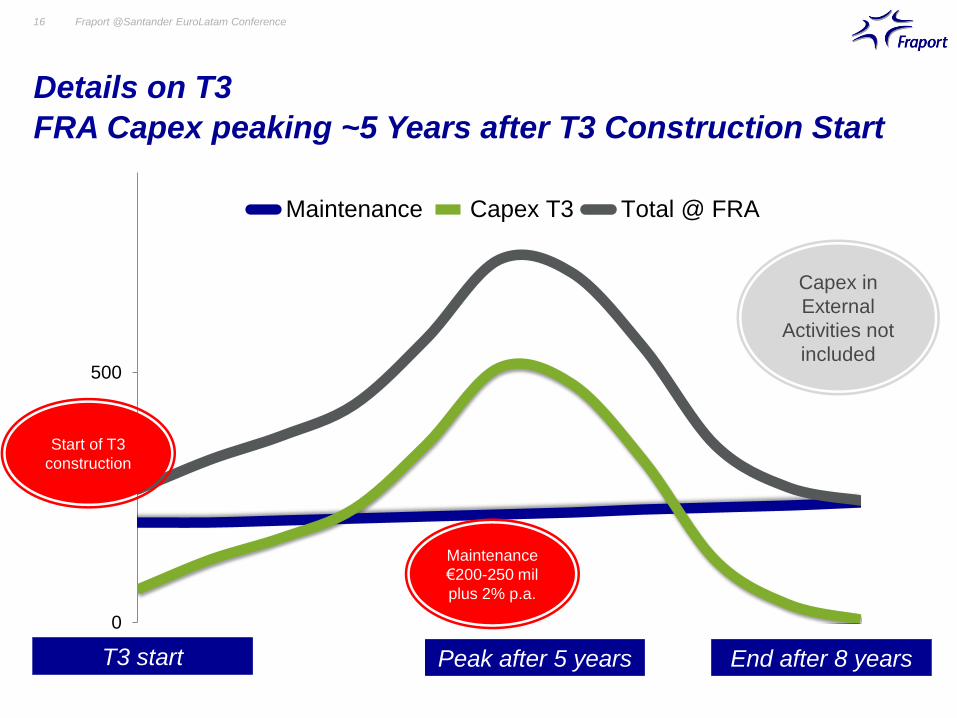

0

500

Maintenance Capex T3 Total @ FRA

Start of T3

construction

Maintenance

€200-250 mil

plus 2% p.a.

T3 start Peak after 5 years End after 8 years

Capex in

External

Activities not

included

16 Fraport @Santander EuroLatam Conference

Details on T3

FRA Capex peaking ~5 Years after T3 Construction Start

Fraport @Santander EuroLatam Conference17

Agenda

- Traffic Insight

- Details on T3

- International Business Development

- Appendix

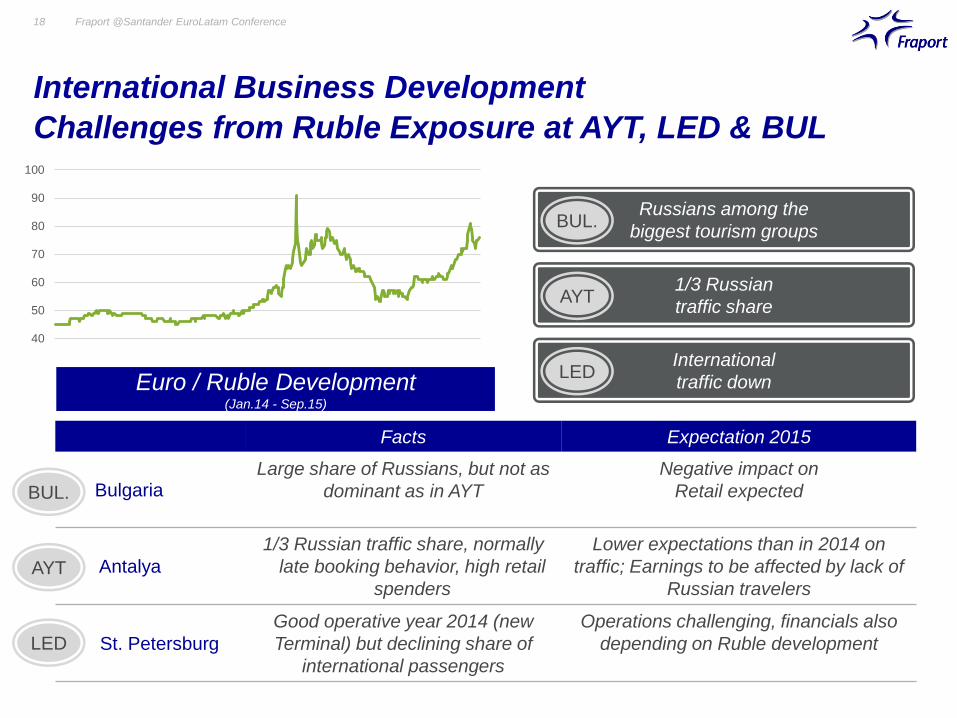

Russians among the

biggest tourism groups

1/3 Russian

traffic share

International

traffic down

Facts Expectation 2015

BulgariaLarge share of Russians, but not as

dominant as in AYT

Negative impact on

Retail expected

Antalya

1/3 Russian traffic share, normally

late booking behavior, high retail

spenders

Lower expectations than in 2014 on

traffic; Earnings to be affected by lack of

Russian travelers

St. Petersburg

Good operative year 2014 (new

Terminal) but declining share of

international passengers

Operations challenging, financials also

depending on Ruble development

Euro / Ruble Development(Jan.14 - Sep.15)

BUL.

AYT

LED

BUL.

AYT

LED

18 Fraport @Santander EuroLatam Conference

International Business Development

Challenges from Ruble Exposure at AYT, LED & BUL

40

50

60

70

80

90

100

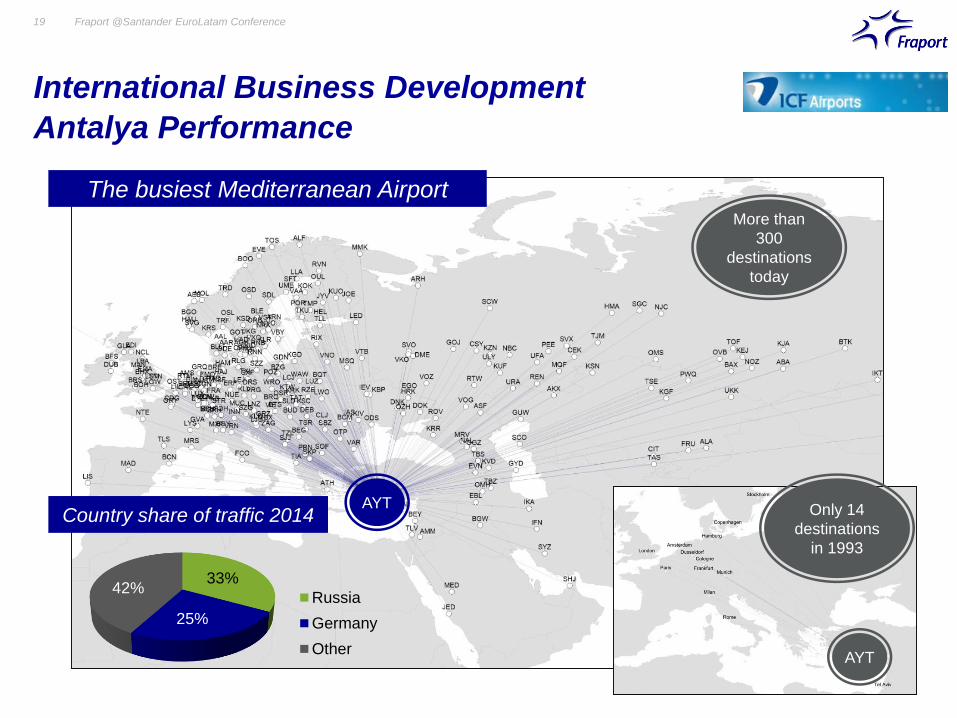

Only 14

destinations

in 1993

AYT

More than

300

destinations

today

AYT

The busiest Mediterranean Airport

33%

25%

42%Russia

Germany

Other

Country share of traffic 2014

19

International Business Development

Antalya Performance

Fraport @Santander EuroLatam Conference

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Traffic Development 2001-2014

13Y CAGR: 10.8%

in mil

Above 15

million

passengers

20 Fraport @Santander EuroLatam Conference

International Business Development

Lima Airport

› Significant traffic growth for more than a decade with nearly 11% CAGR

› Dividend payments to Fraport: € 5.2 million in 2014 (cumulated: 53.5 million €)

› Upgrade of infrastructure necessary within the next decade:

› 2nd terminal, new runway, extension of taxiways, new tower, additional access ways

to the airport

› Runway construction within 5 years after land transfer of the Peruvian state,

subsequently construction of a 2nd Terminal

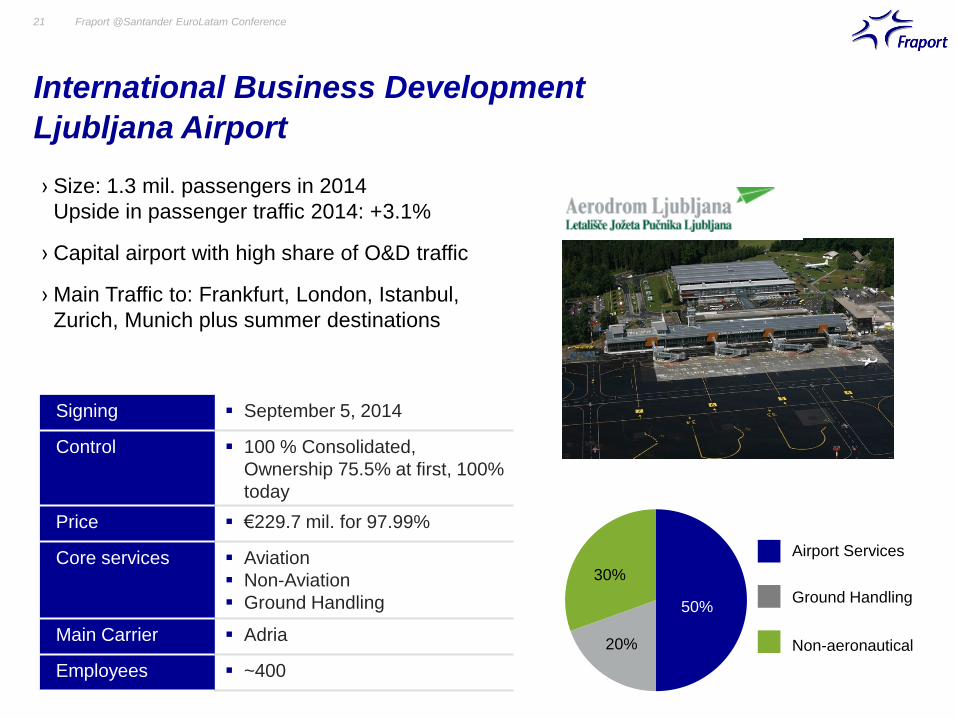

Signing September 5, 2014

Control 100 % Consolidated,

Ownership 75.5% at first, 100%

today

Price €229.7 mil. for 97.99%

Core services Aviation

Non-Aviation

Ground Handling

Main Carrier Adria

Employees ~400

50%

20%

30%

Ground Handling

Non-aeronautical

Airport Services

21 Fraport @Santander EuroLatam Conference

International Business Development

Ljubljana Airport

› Size: 1.3 mil. passengers in 2014

Upside in passenger traffic 2014: +3.1%

› Capital airport with high share of O&D traffic

› Main Traffic to: Frankfurt, London, Istanbul,

Zurich, Munich plus summer destinations

International Business Development

Update Aerodrom Ljubljana

Fraport @Santander EuroLatam Conference22

1 new carrier - 3 new routes

› The only airport subsidiary with 100%

Fraport share in Group portfolio

› Stable cash flows

› Payback already started

› Very good 6M traffic and EBITDA

performance Redesign of arrival F&B area and mobile units

Percent changes based on unrounded figures, financials according to local GAAP, IFRS figures differ

Aerodrom Ljubljana 6M Performance

6M 2015

6M 2014+9.7%+15.8%

627571

Passengers EBITDA

in ‘000 in € mil.

65

International Business Development

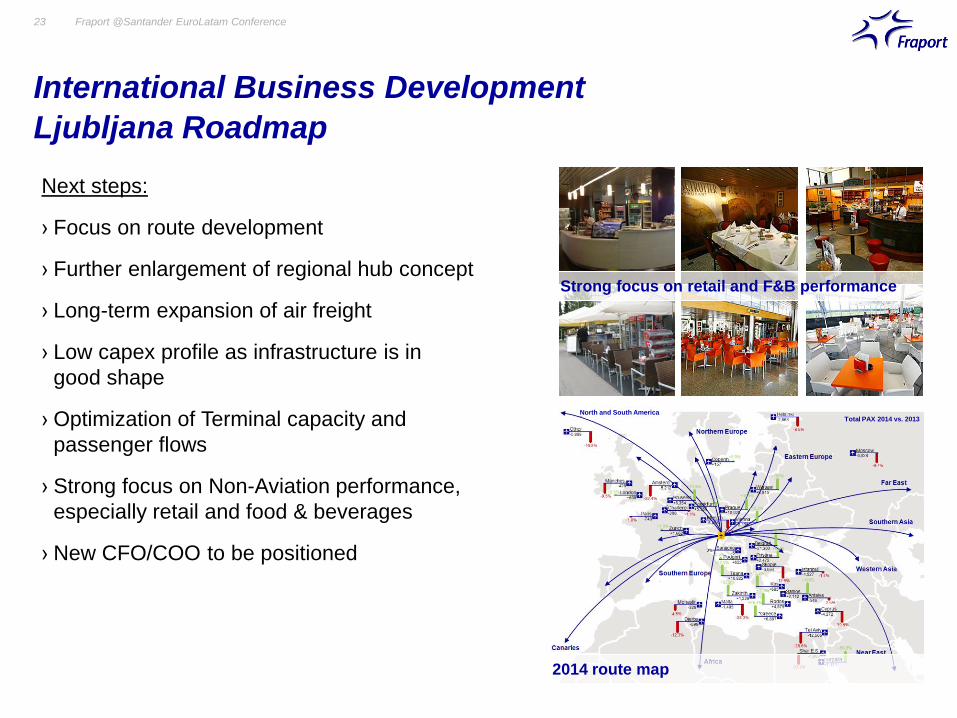

Ljubljana Roadmap

Fraport @Santander EuroLatam Conference23

Next steps:

› Focus on route development

› Further enlargement of regional hub concept

› Long-term expansion of air freight

› Low capex profile as infrastructure is in

good shape

› Optimization of Terminal capacity and

passenger flows

› Strong focus on Non-Aviation performance,

especially retail and food & beverages

› New CFO/COO to be positioned

2014 route map

North and South AmericaTotal PAX 2014 vs. 2013

Strong focus on retail and F&B performance

Signing / Closing July 23 / August 1, 2014

Control Consolidated, 100% owned

Core services Retail Property Development

Leasing

Operations Management

Branding and Marketing

Founded 1991

Employees 28

24 Fraport @Santander EuroLatam Conference

International Business Development

Airmall Retail Acquisition USA

› Core segment Retail is expanded to the largest

aviation market in the world

› Visible and continuous contribution to EBITDA

› Stable cash flows guarantee start of payback

period immediately after takeover

› Unlocking of further growth potential by Fraport

Group network expertise

International Business Development

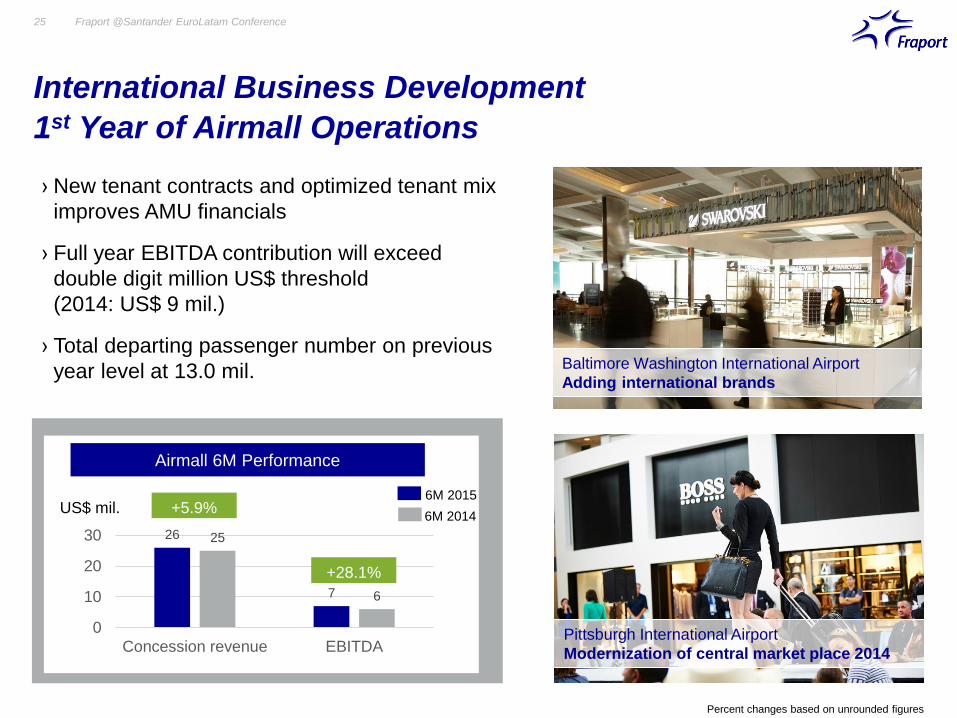

1st Year of Airmall Operations

Fraport @Santander EuroLatam Conference25

› New tenant contracts and optimized tenant mix

improves AMU financials

› Full year EBITDA contribution will exceed

double digit million US$ threshold

(2014: US$ 9 mil.)

› Total departing passenger number on previous

year level at 13.0 mil. Baltimore Washington International Airport

Adding international brands

Pittsburgh International Airport

Modernization of central market place 2014

Percent changes based on unrounded figures

Airmall 6M Performance

+5.9%

26

7

25

6

0

10

20

30

Concession revenue EBITDA

+28.1%

US$ mil.6M 2015

6M 2014

International Business Development

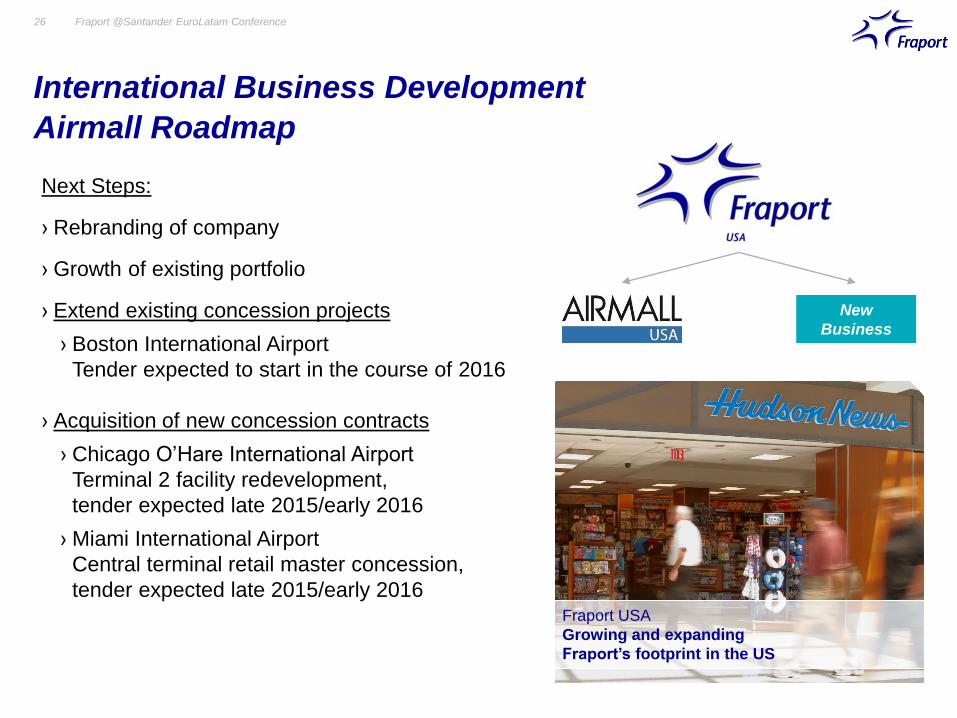

Airmall Roadmap

Fraport @Santander EuroLatam Conference26

Next Steps:

› Rebranding of company

› Growth of existing portfolio

› Extend existing concession projects

› Boston International Airport

Tender expected to start in the course of 2016

› Acquisition of new concession contracts

› Chicago O’Hare International Airport

Terminal 2 facility redevelopment,

tender expected late 2015/early 2016

› Miami International Airport

Central terminal retail master concession,

tender expected late 2015/early 2016 Fraport USA

Growing and expanding

Fraport’s footprint in the US

New

Business

Fraport @Santander EuroLatam Conference27

Agenda

- Traffic Insight

- Details on T3

- International Business Development

- Appendix

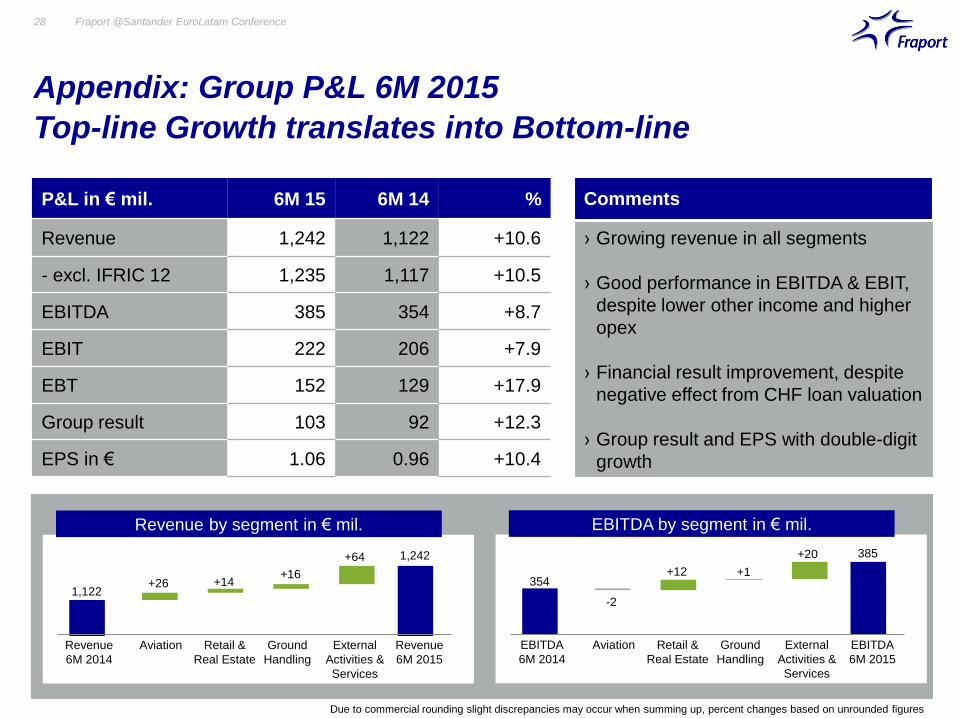

Appendix: Group P&L 6M 2015

Top-line Growth translates into Bottom-line

Fraport @Santander EuroLatam Conference28

P&L in € mil. 6M 15 6M 14 %

Revenue 1,242 1,122 +10.6

- excl. IFRIC 12 1,235 1,117 +10.5

EBITDA 385 354 +8.7

EBIT 222 206 +7.9

EBT 152 129 +17.9

Group result 103 92 +12.3

EPS in € 1.06 0.96 +10.4

› Growing revenue in all segments

› Good performance in EBITDA & EBIT,

despite lower other income and higher

opex

› Financial result improvement, despite

negative effect from CHF loan valuation

› Group result and EPS with double-digit

growth

Comments

Revenue by segment in € mil.

Revenue

6M 2014

Aviation Retail &

Real Estate

Ground

Handling

External

Activities &

Services

Revenue

6M 2015

1,122+26

+16

+64 1,242

+14

External

Activities

Services

EBITDA by segment in € mil.

EBITDA

6M 2014

Aviation Retail &

Real Estate

Ground

Handling

EBITDA

6M 2015

354+1

+20 385

+12

-2

External

Activities &

Services

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

Appendix: Group P&L 6M 2015

External Activities key Driver for lift in Group EBITDA

Fraport @Santander EuroLatam Conference29

EBITDA

6M 2014

Other

income

Cost of

materials ex.

IFRIC 12

Staff

cost

EBITDA

6M 2015

Revenue

ex. IFRIC 12

Other

opex

354-42 -34

385

+€31 mil.

-2

IFRIC 12

revenue

IFRIC 12

cost of

materials

+117

-6

29,5%

48,6%

3,2%

18,7%

Segment share in Group EBITDA 6M 2014 Segment share in Group EBITDA 6M 2015

26,6%

47,8%

3,3%

22,3%Aviation

Retail &

Real Estate

External

Activities &

Services Aviation

Retail &

Real Estate

External

Activities &

Services

Ground

Handling Ground

Handling

€ mil.

Due to commercial rounding slight discrepancies may occur when summing up

+2

-5

Appendix: Group P&L 6M 2015

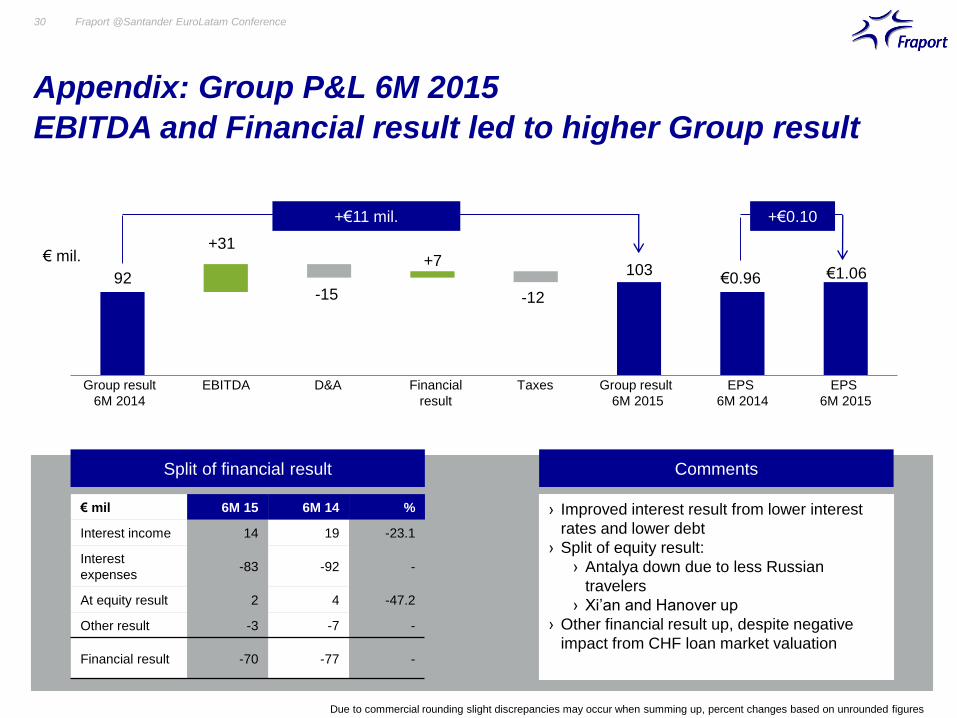

EBITDA and Financial result led to higher Group result

Fraport @Santander EuroLatam Conference30

Split of financial result Comments

Group result

6M 2014

EBITDA D&A Financial

result

Taxes Group result

6M 2015

92

+31

103

-15 -12

+€11 mil.

€1.06€0.96

EPS

6M 2014

EPS

6M 2015

+€0.10

€ mil 6M 15 6M 14 %

Interest income 14 19 -23.1

Interest

expenses-83 -92 -

At equity result 2 4 -47.2

Other result -3 -7 -

Financial result -70 -77 -

› Improved interest result from lower interest

rates and lower debt

› Split of equity result:

› Antalya down due to less Russian

travelers

› Xi’an and Hanover up

› Other financial result up, despite negative

impact from CHF loan market valuation

+7€ mil.

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

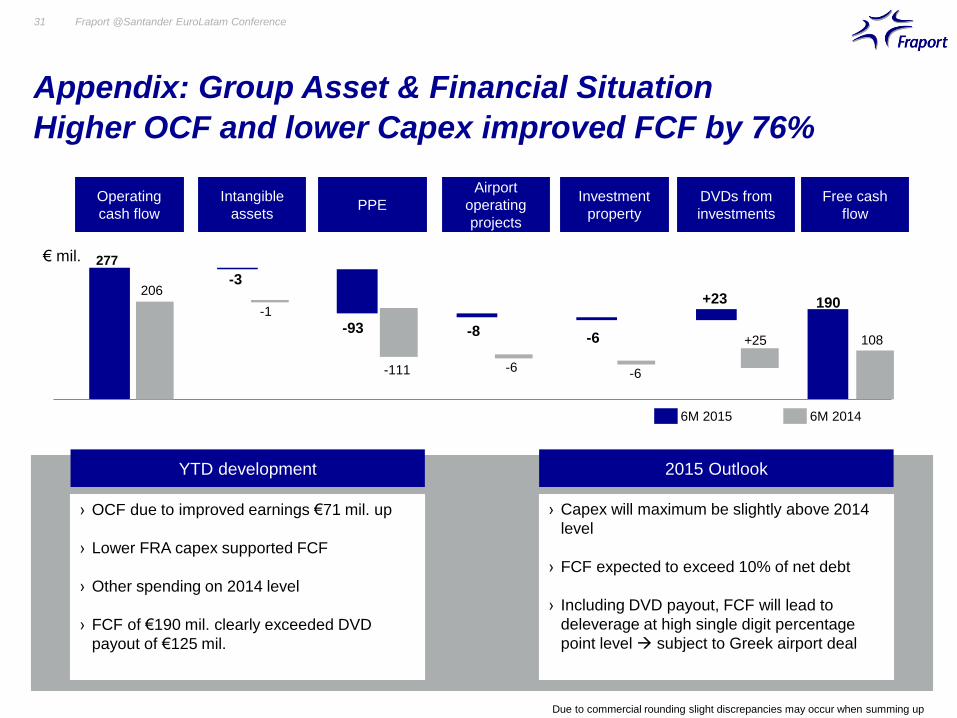

Appendix: Group Asset & Financial Situation

Higher OCF and lower Capex improved FCF by 76%

Fraport @Santander EuroLatam Conference31

2015 OutlookYTD development

PPEInvestment

property

Operating

cash flow

Intangible

assets

Airport

operating

projects

277

190206

-1

-111 -6 -6

-3

-93 -8 -6

+23

DVDs from

investments

Free cash

flow

+25 108

› Capex will maximum be slightly above 2014

level

› FCF expected to exceed 10% of net debt

› Including DVD payout, FCF will lead to

deleverage at high single digit percentage

point level subject to Greek airport deal

› OCF due to improved earnings €71 mil. up

› Lower FRA capex supported FCF

› Other spending on 2014 level

› FCF of €190 mil. clearly exceeded DVD

payout of €125 mil.

Due to commercial rounding slight discrepancies may occur when summing up

6M 2015 6M 2014

€ mil.

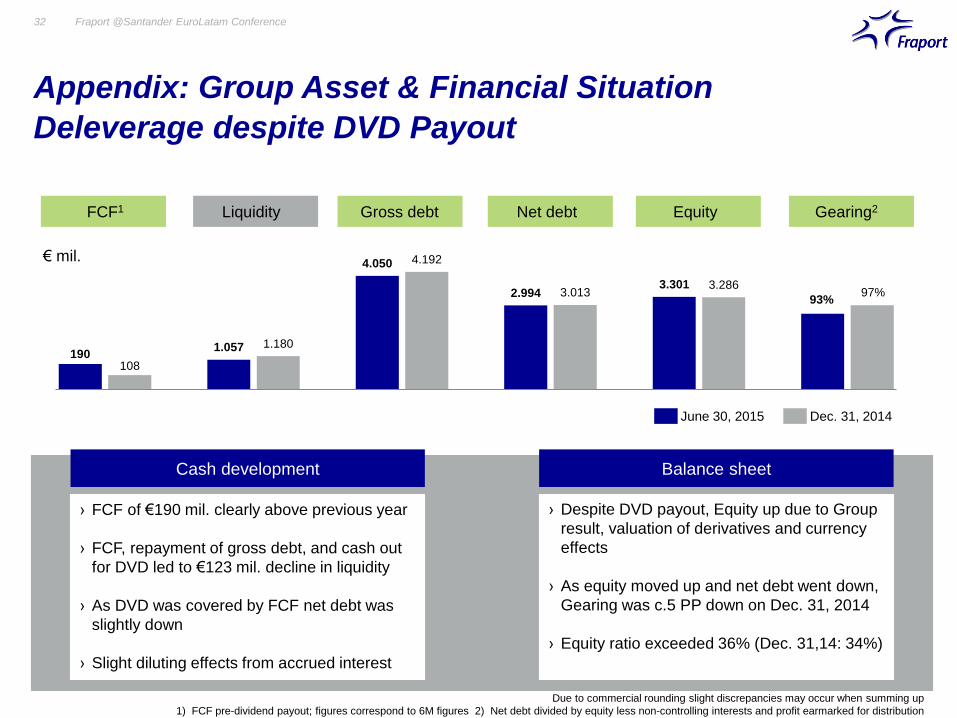

Appendix: Group Asset & Financial Situation

Deleverage despite DVD Payout

Fraport @Santander EuroLatam Conference32

Balance sheet

› Despite DVD payout, Equity up due to Group

result, valuation of derivatives and currency

effects

› As equity moved up and net debt went down,

Gearing was c.5 PP down on Dec. 31, 2014

› Equity ratio exceeded 36% (Dec. 31,14: 34%)

Cash development

› FCF of €190 mil. clearly above previous year

› FCF, repayment of gross debt, and cash out

for DVD led to €123 mil. decline in liquidity

› As DVD was covered by FCF net debt was

slightly down

› Slight diluting effects from accrued interest

190108

1.057 1.180

4.050 4.192

2.994 3.0133.301 3.286

93%97%

June 30, 2015

Liquidity Gross debt Net debt Equity Gearing2FCF1

Dec. 31, 2014

€ mil.

Due to commercial rounding slight discrepancies may occur when summing up

1) FCF pre-dividend payout; figures correspond to 6M figures 2) Net debt divided by equity less non-controlling interests and profit earmarked for distribution

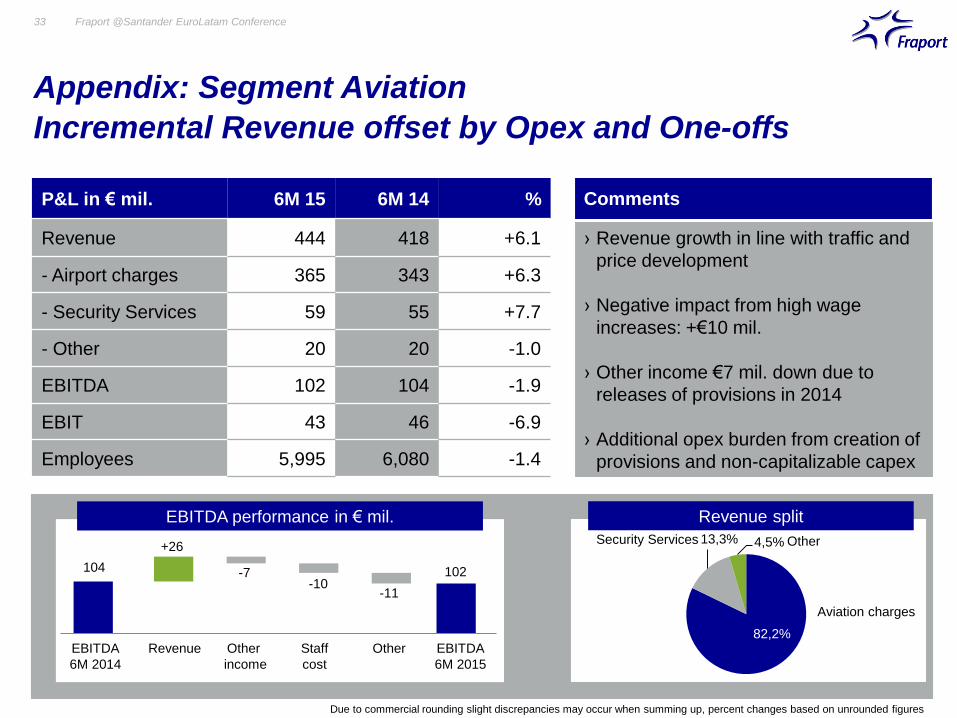

Appendix: Segment Aviation

Incremental Revenue offset by Opex and One-offs

Fraport @Santander EuroLatam Conference33

P&L in € mil. 6M 15 6M 14 %

Revenue 444 418 +6.1

- Airport charges 365 343 +6.3

- Security Services 59 55 +7.7

- Other 20 20 -1.0

EBITDA 102 104 -1.9

EBIT 43 46 -6.9

Employees 5,995 6,080 -1.4

› Revenue growth in line with traffic and

price development

› Negative impact from high wage

increases: +€10 mil.

› Other income €7 mil. down due to

releases of provisions in 2014

› Additional opex burden from creation of

provisions and non-capitalizable capex

Comments

EBITDA

6M 2014

Revenue Other

income

Staff

cost

Other EBITDA

6M 2015

104

+26

-7-10

-11

102

EBITDA performance in € mil. Revenue split

Aviation charges

OtherSecurity Services

82,2%

13,3% 4,5%

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

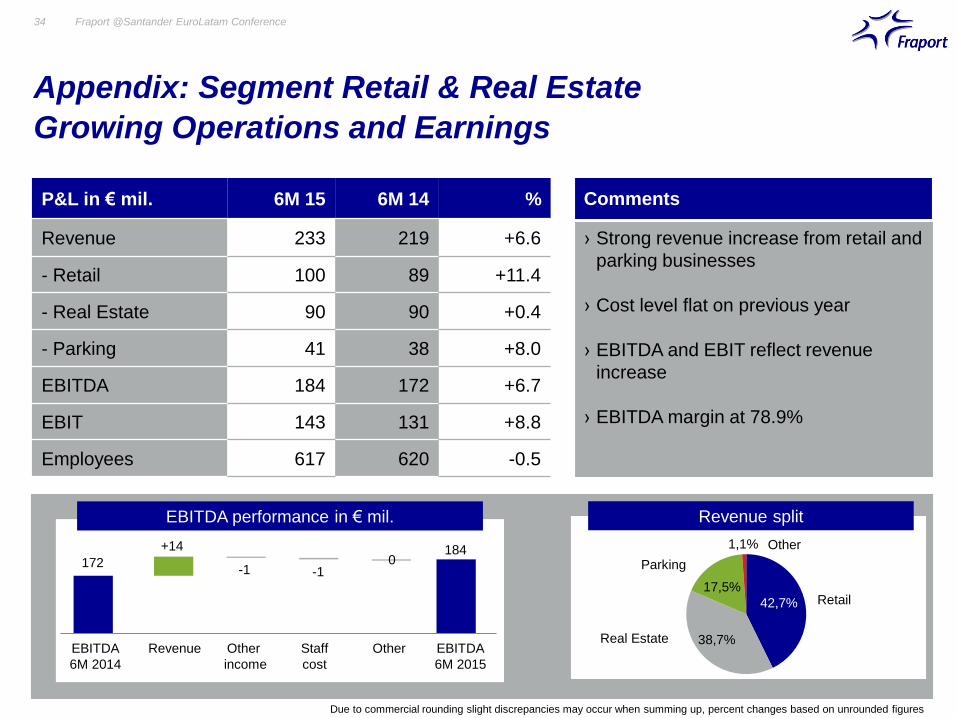

Appendix: Segment Retail & Real Estate

Growing Operations and Earnings

Fraport @Santander EuroLatam Conference34

P&L in € mil. 6M 15 6M 14 %

Revenue 233 219 +6.6

- Retail 100 89 +11.4

- Real Estate 90 90 +0.4

- Parking 41 38 +8.0

EBITDA 184 172 +6.7

EBIT 143 131 +8.8

Employees 617 620 -0.5

› Strong revenue increase from retail and

parking businesses

› Cost level flat on previous year

› EBITDA and EBIT reflect revenue

increase

› EBITDA margin at 78.9%

Comments

EBITDA

6M 2014

Revenue Other

income

Staff

cost

Other EBITDA

6M 2015

172

+14

-1 -10

184

EBITDA performance in € mil. Revenue split

Retail

Other

Parking

42,7%

38,7%

17,5%

1,1%

Real Estate

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

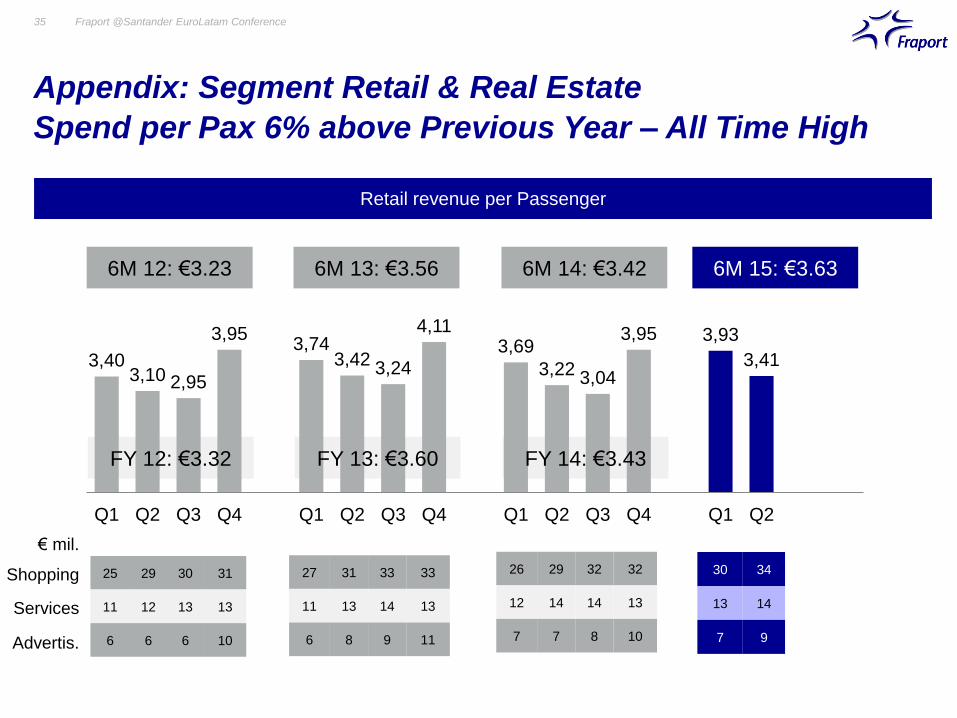

Appendix: Segment Retail & Real Estate

Spend per Pax 6% above Previous Year – All Time High

Fraport @Santander EuroLatam Conference35

Retail revenue per Passenger

25 29 30 31

11 12 13 13

6 6 6 10

3,403,10 2,95

3,953,74

3,42 3,24

4,113,69

3,22 3,04

3,95 3,93

3,41

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

6M 12: €3.23

27 31 33 33

11 13 14 13

6 8 9 11

30 34 33

13 14 13

7 9 11

€ mil.

Shopping

Services

Advertis.

6M 13: €3.56 6M 14: €3.42 6M 15: €3.63

26 29 32 32

12 14 14 13

7 7 8 10

FY 12: €3.32 FY 13: €3.60 FY 14: €3.43

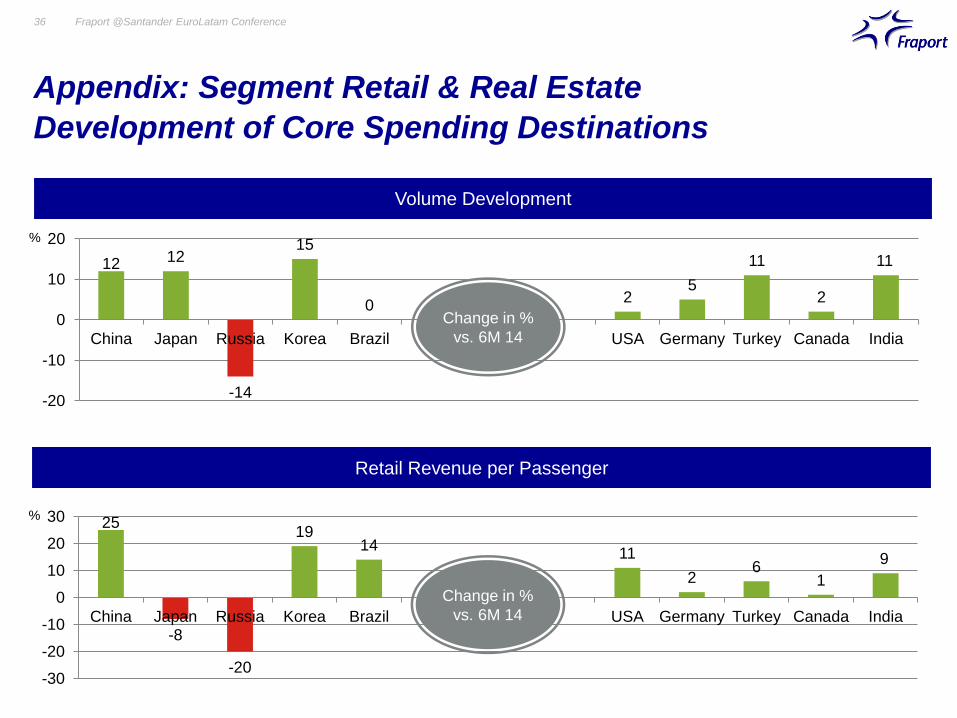

Appendix: Segment Retail & Real Estate

Development of Core Spending Destinations

Fraport @Santander EuroLatam Conference36

Volume Development

12 12

-14

15

02

5

11

2

11

-20

-10

0

10

20

China Japan Russia Korea Brazil USA Germany Turkey Canada India

%

Change in %

vs. 6M 14

Retail Revenue per Passenger

25

-8

-20

1914

11

26

1

9

-30

-20

-10

0

10

20

30

China Japan Russia Korea Brazil USA Germany Turkey Canada India

%

Change in %

vs. 6M 14

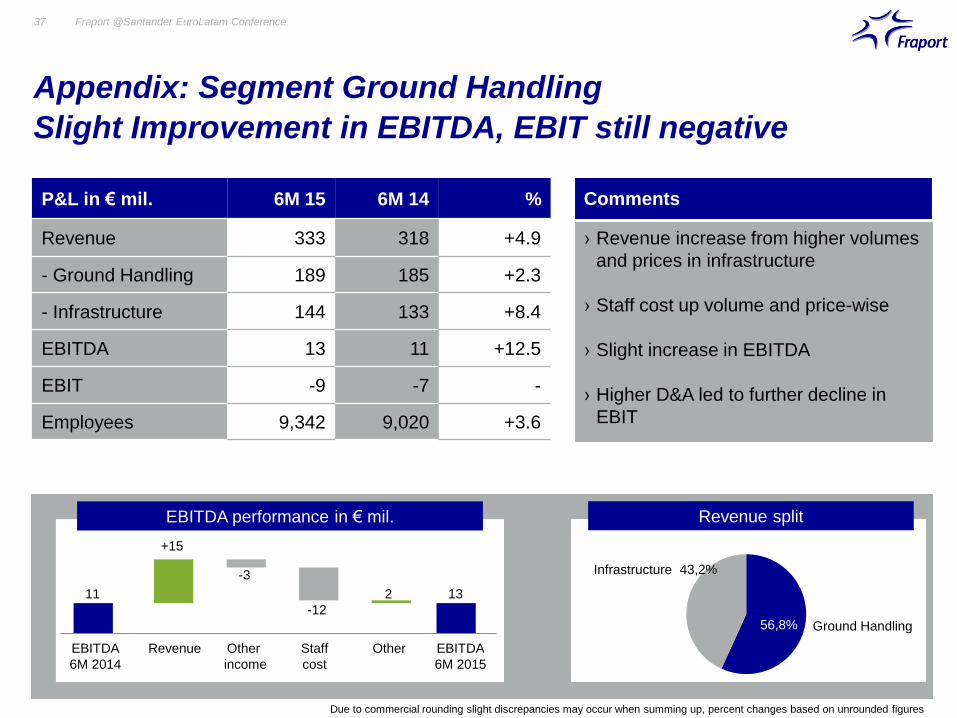

Appendix: Segment Ground Handling

Slight Improvement in EBITDA, EBIT still negative

Fraport @Santander EuroLatam Conference37

P&L in € mil. 6M 15 6M 14 %

Revenue 333 318 +4.9

- Ground Handling 189 185 +2.3

- Infrastructure 144 133 +8.4

EBITDA 13 11 +12.5

EBIT -9 -7 -

Employees 9,342 9,020 +3.6

› Revenue increase from higher volumes

and prices in infrastructure

› Staff cost up volume and price-wise

› Slight increase in EBITDA

› Higher D&A led to further decline in

EBIT

Comments

EBITDA

6M 2014

Revenue Other

income

Staff

cost

Other EBITDA

6M 2015

11

+15

-3

-12

2 13

EBITDA performance in € mil. Revenue split

Ground Handling56,8%

43,2%Infrastructure

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

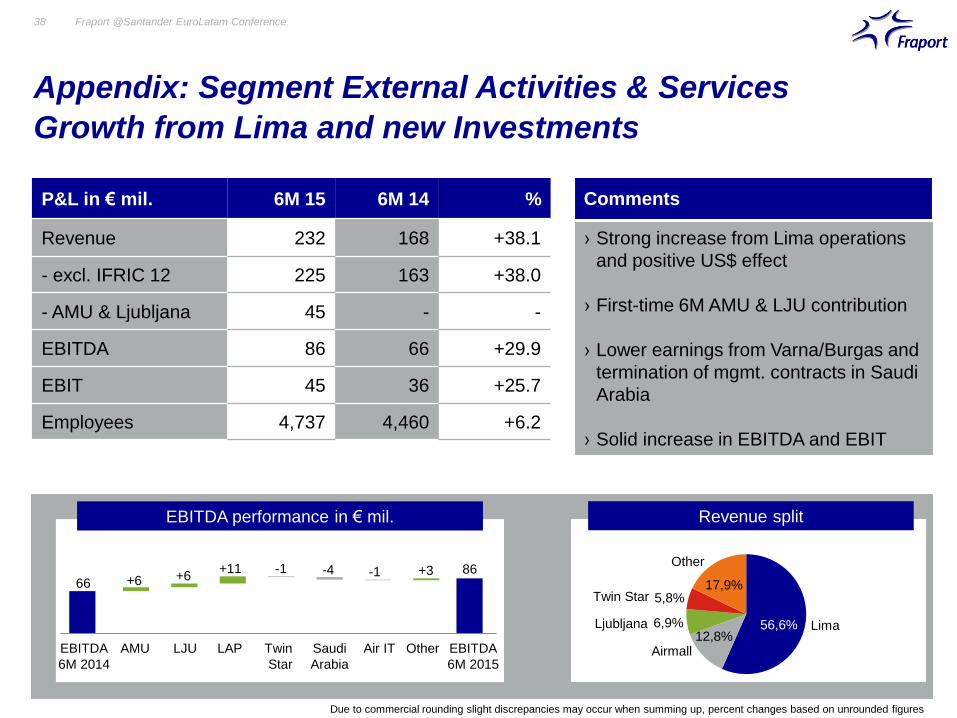

Appendix: Segment External Activities & Services

Growth from Lima and new Investments

Fraport @Santander EuroLatam Conference38

P&L in € mil. 6M 15 6M 14 %

Revenue 232 168 +38.1

- excl. IFRIC 12 225 163 +38.0

- AMU & Ljubljana 45 - -

EBITDA 86 66 +29.9

EBIT 45 36 +25.7

Employees 4,737 4,460 +6.2

› Strong increase from Lima operations

and positive US$ effect

› First-time 6M AMU & LJU contribution

› Lower earnings from Varna/Burgas and

termination of mgmt. contracts in Saudi

Arabia

› Solid increase in EBITDA and EBIT

Comments

EBITDA

6M 2014

AMU Saudi

Arabia

Other EBITDA

6M 2015

66 +6-4 86

EBITDA performance in € mil. Revenue split

56,6%12,8%

6,9%

5,8%17,9%

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

Lima

Other

Twin Star

Ljubljana

Airmall

-1+11

LJU LAP Twin

Star

Air IT

+6 -1 +3

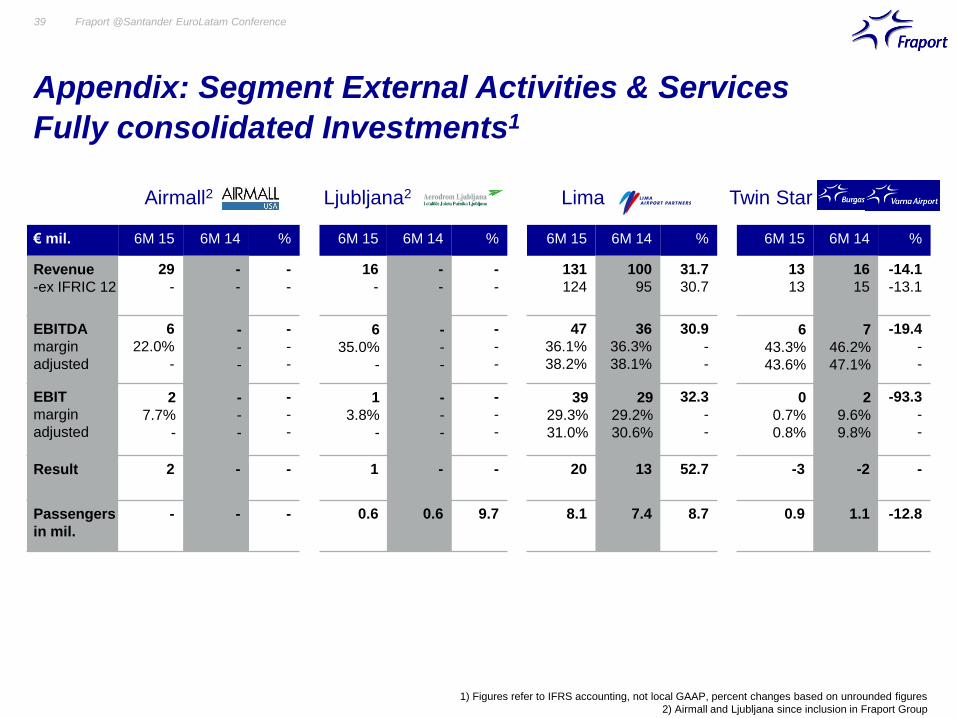

Appendix: Segment External Activities & Services

Fully consolidated Investments1

Fraport @Santander EuroLatam Conference39

1) Figures refer to IFRS accounting, not local GAAP, percent changes based on unrounded figures

2) Airmall and Ljubljana since inclusion in Fraport Group

€ mil. 6M 15 6M 14 % 6M 15 6M 14 % 6M 15 6M 14 % 6M 15 6M 14 %

Revenue

-ex IFRIC 12

29

-

-

-

-

-

16

-

-

-

-

-

131

124

100

95

31.7

30.7

13

13

16

15

-14.1

-13.1

EBITDA

margin

adjusted

6

22.0%

-

-

-

-

-

-

-

6

35.0%

-

-

-

-

-

-

-

47

36.1%

38.2%

36

36.3%

38.1%

30.9

-

-

6

43.3%

43.6%

7

46.2%

47.1%

-19.4

-

-

EBIT

margin

adjusted

2

7.7%

-

-

-

-

-

-

-

1

3.8%

-

-

-

-

-

-

-

39

29.3%

31.0%

29

29.2%

30.6%

32.3

-

-

0

0.7%

0.8%

2

9.6%

9.8%

-93.3

-

-

Result 2 - - 1 - - 20 13 52.7 -3 -2 -

Passengers

in mil.

- - - 0.6 0.6 9.7 8.1 7.4 8.7 0.9 1.1 -12.8

Airmall2 Twin StarLjubljana2 Lima

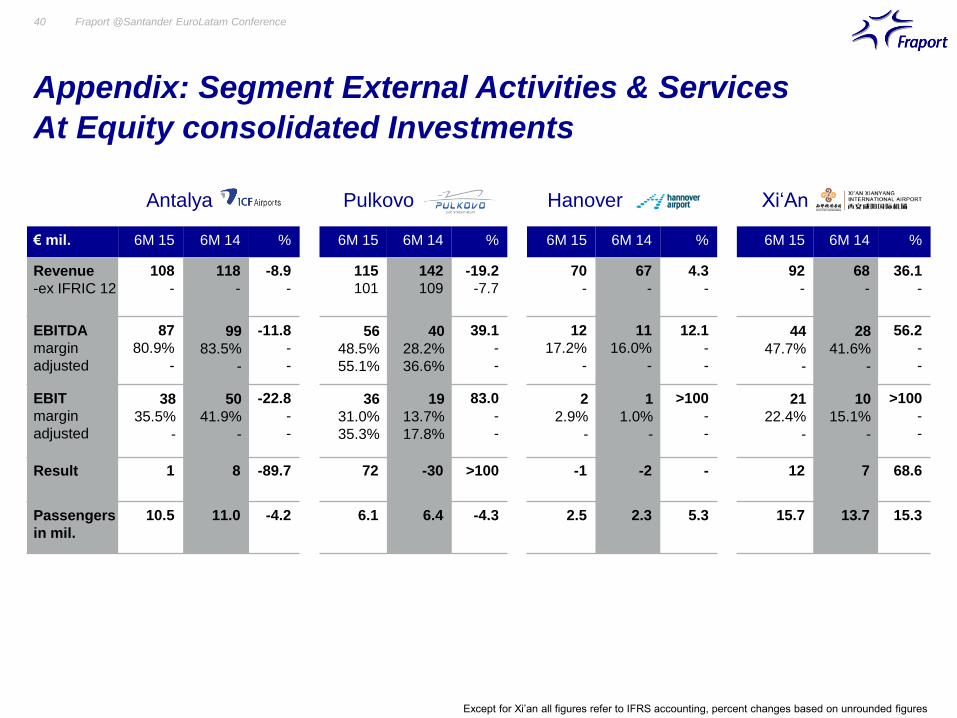

Appendix: Segment External Activities & Services

At Equity consolidated Investments

Fraport @Santander EuroLatam Conference40

Except for Xi’an all figures refer to IFRS accounting, percent changes based on unrounded figures

€ mil. 6M 15 6M 14 % 6M 15 6M 14 % 6M 15 6M 14 % 6M 15 6M 14 %

Revenue

-ex IFRIC 12

108

-

118

-

-8.9

-

115

101

142

109

-19.2

-7.7

70

-

67

-

4.3

-

92

-

68

-

36.1

-

EBITDA

margin

adjusted

87

80.9%

-

99

83.5%

-

-11.8

-

-

56

48.5%

55.1%

40

28.2%

36.6%

39.1

-

-

12

17.2%

-

11

16.0%

-

12.1

-

-

44

47.7%

-

28

41.6%

-

56.2

-

-

EBIT

margin

adjusted

38

35.5%

-

50

41.9%

-

-22.8

-

-

36

31.0%

35.3%

19

13.7%

17.8%

83.0

-

-

2

2.9%

-

1

1.0%

-

>100

-

-

21

22.4%

-

10

15.1%

-

>100

-

-

Result 1 8 -89.7 72 -30 >100 -1 -2 - 12 7 68.6

Passengers

in mil.

10.5 11.0 -4.2 6.1 6.4 -4.3 2.5 2.3 5.3 15.7 13.7 15.3

Xi‘AnPulkovo HanoverAntalya

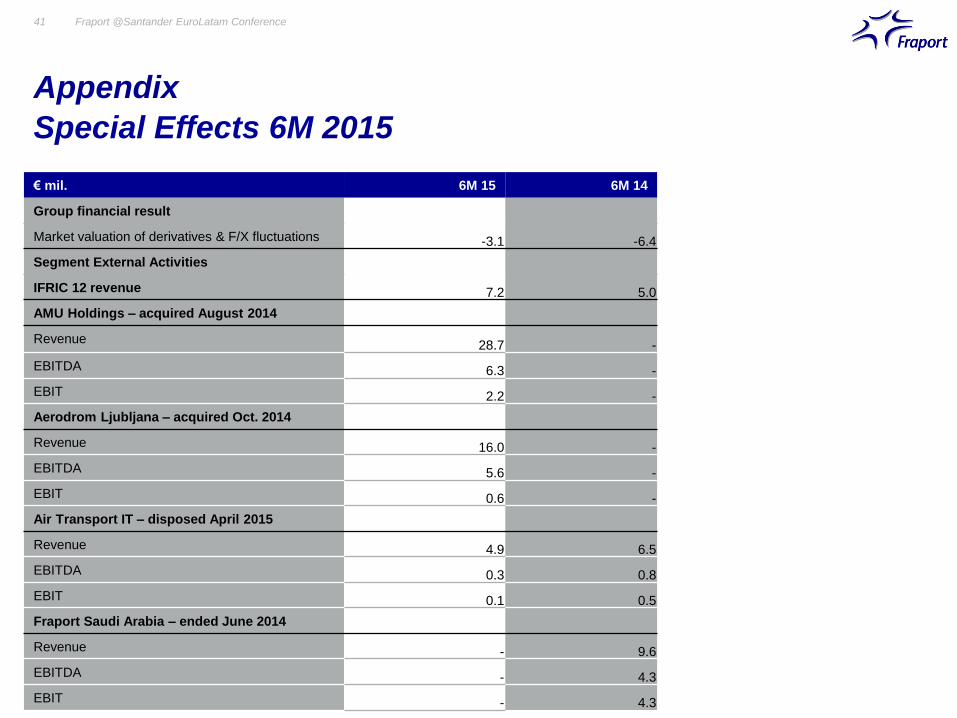

Appendix

Special Effects 6M 2015

Fraport @Santander EuroLatam Conference41

€ mil. 6M 15 6M 14

Group financial result

Market valuation of derivatives & F/X fluctuations -3.1 -6.4

Segment External Activities

IFRIC 12 revenue 7.2 5.0

AMU Holdings – acquired August 2014

Revenue28.7 -

EBITDA 6.3 -

EBIT 2.2 -

Aerodrom Ljubljana – acquired Oct. 2014

Revenue 16.0 -

EBITDA 5.6 -

EBIT 0.6 -

Air Transport IT – disposed April 2015

Revenue 4.9 6.5

EBITDA 0.3 0.8

EBIT 0.1 0.5

Fraport Saudi Arabia – ended June 2014

Revenue - 9.6

EBITDA - 4.3

EBIT - 4.3

Appendix

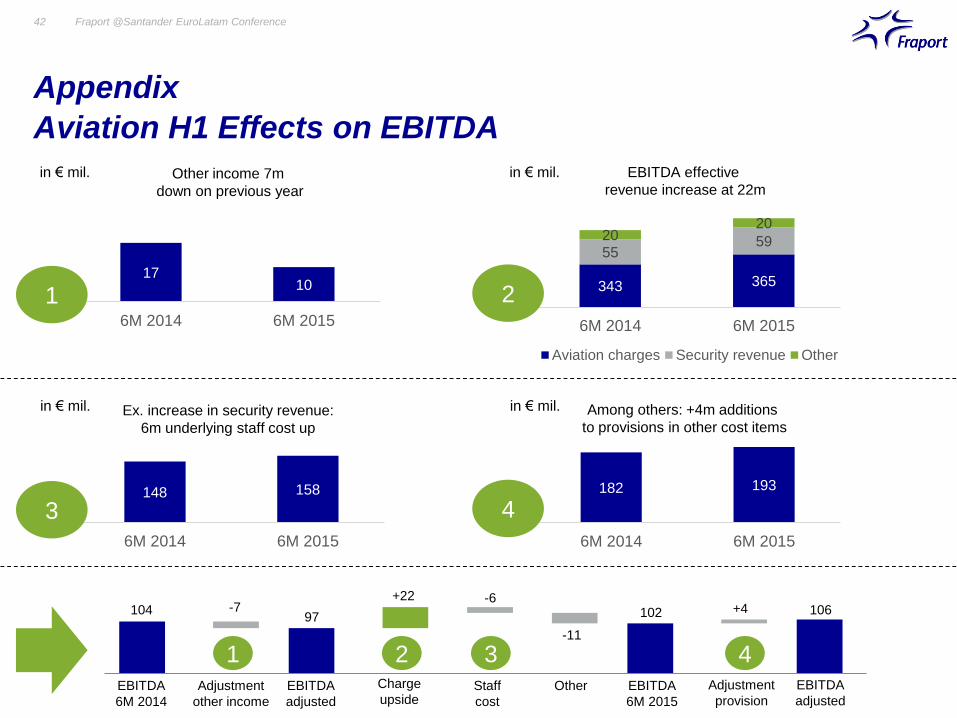

Aviation H1 Effects on EBITDA

Fraport @Santander EuroLatam Conference42

EBITDA effective

revenue increase at 22m

in € mil.

148 158

6M 2014 6M 2015

Ex. increase in security revenue:

6m underlying staff cost up

in € mil.

182 193

6M 2014 6M 2015

Among others: +4m additions

to provisions in other cost items

in € mil. in € mil.

3 4

EBITDA

6M 2014

EBITDA

adjusted

Adjustment

other income

Staff

cost

Other EBITDA

6M 2015

104+22

-797

-11

102

Charge

upside

-6106+4

EBITDA

adjusted

Adjustment

provision

1710

6M 2014 6M 2015

Other income 7m

down on previous year

343 365

55592020

6M 2014 6M 2015

Aviation charges Security revenue Other

1

1 2 3 4

2

Appendix

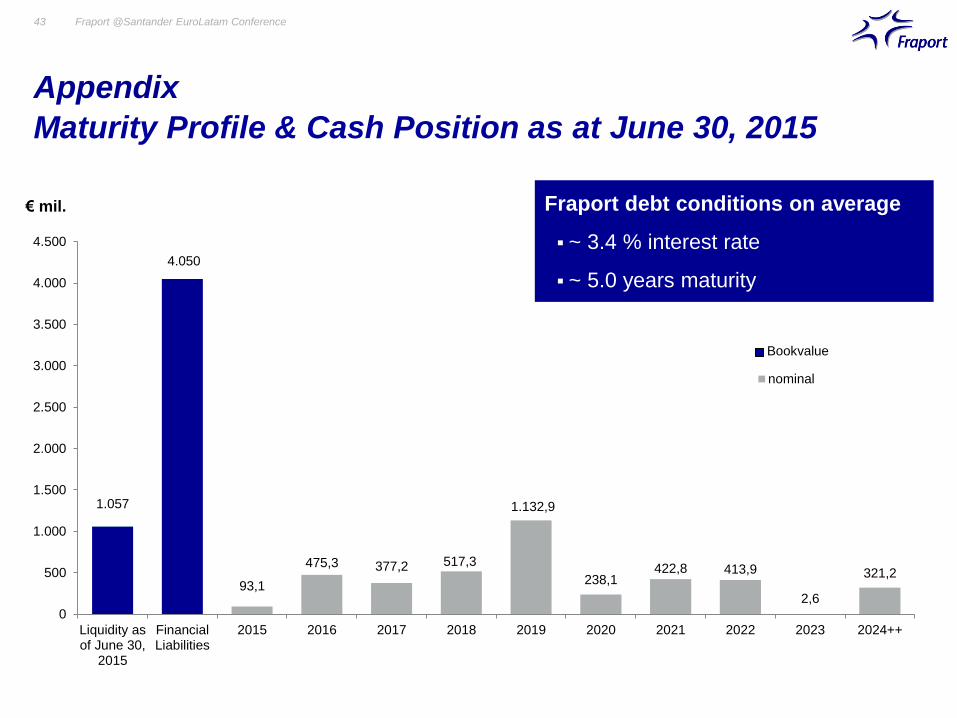

Maturity Profile & Cash Position as at June 30, 2015

Fraport @Santander EuroLatam Conference43

€ mil.

1.057

4.050

93,1

475,3 377,2 517,3

1.132,9

238,1422,8 413,9

2,6

321,2

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

Liquidity asof June 30,

2015

FinancialLiabilities

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024++

nominal

Bookvalue

Fraport debt conditions on average

~ 3.4 % interest rate

~ 5.0 years maturity

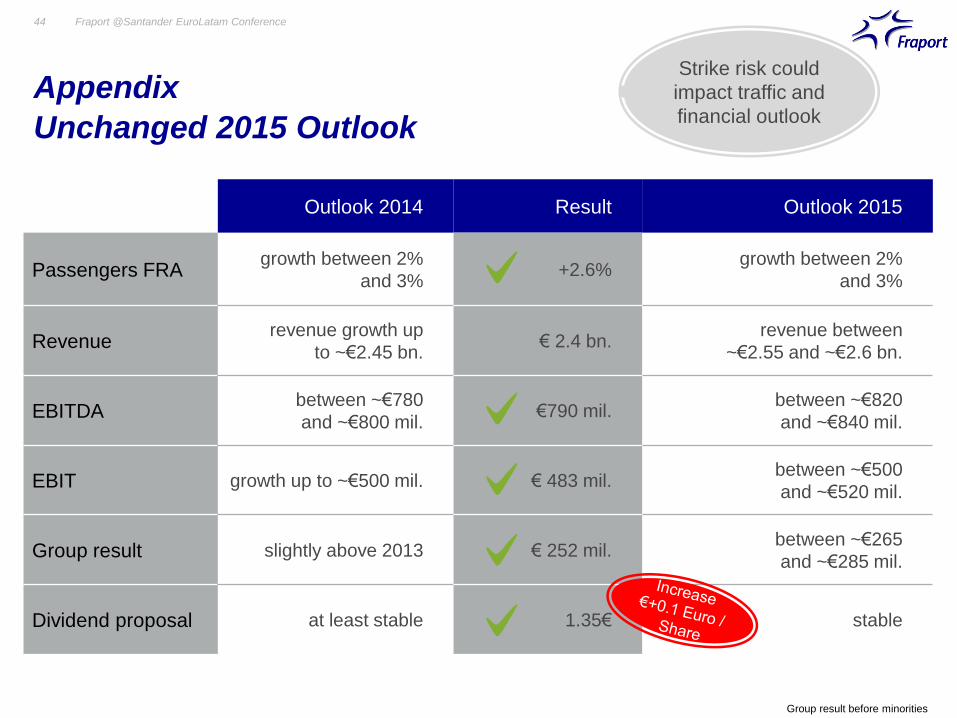

Outlook 2014 Result Outlook 2015

Passengers FRAgrowth between 2%

and 3%+2.6%

growth between 2%

and 3%

Revenuerevenue growth up

to ~€2.45 bn.€ 2.4 bn.

revenue between

~€2.55 and ~€2.6 bn.

EBITDAbetween ~€780

and ~€800 mil.€790 mil.

between ~€820

and ~€840 mil.

EBIT growth up to ~€500 mil. € 483 mil.between ~€500

and ~€520 mil.

Group result slightly above 2013 € 252 mil.between ~€265

and ~€285 mil.

Dividend proposal at least stable 1.35€ stable

Appendix

Unchanged 2015 Outlook

Fraport @Santander EuroLatam Conference44

Strike risk could

impact traffic and

financial outlook

Group result before minorities

Appendix

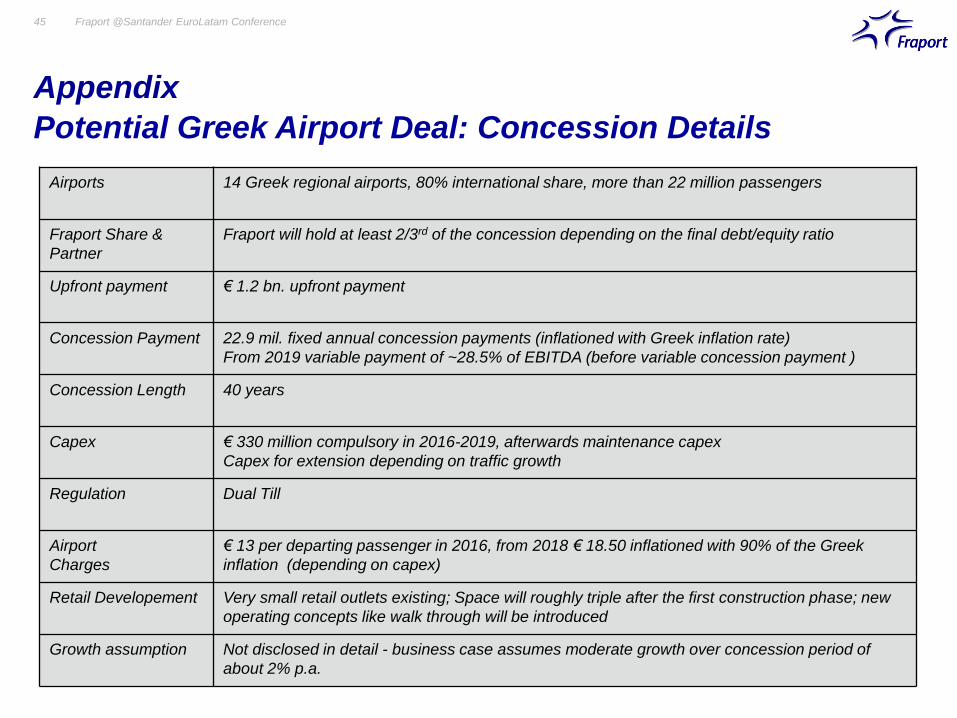

Potential Greek Airport Deal: Concession Details

Fraport @Santander EuroLatam Conference45

Airports 14 Greek regional airports, 80% international share, more than 22 million passengers

Fraport Share &

Partner

Fraport will hold at least 2/3rd of the concession depending on the final debt/equity ratio

Upfront payment € 1.2 bn. upfront payment

Concession Payment 22.9 mil. fixed annual concession payments (inflationed with Greek inflation rate)

From 2019 variable payment of ~28.5% of EBITDA (before variable concession payment )

Concession Length 40 years

Capex € 330 million compulsory in 2016-2019, afterwards maintenance capex

Capex for extension depending on traffic growth

Regulation Dual Till

Airport

Charges

€ 13 per departing passenger in 2016, from 2018 € 18.50 inflationed with 90% of the Greek

inflation (depending on capex)

Retail Developement Very small retail outlets existing; Space will roughly triple after the first construction phase; new

operating concepts like walk through will be introduced

Growth assumption Not disclosed in detail - business case assumes moderate growth over concession period of

about 2% p.a.

Appendix

IR Contact

Fraport @Santander EuroLatam Conference46

Fraport AG

Frankfurt Airport Services Worldwide

60547 Frankfurt am Main

www.meet-ir.com

+49 69 690 – 74842

Stefan J. Rüter

Head of Finance

& Investor Relations

+49 69 690-74840

Svenja Ebeling

Investor Relations Assistant

+49 69 690-74842

Marc Poeschmann

Manager Investor Relations

+49 69 690-74845

Florian Fuchs

Manager Investor Relations

& Financial Reporting

+49 69 690-74844

Thank you for your Attention!

www.meet-ir.com

Fraport @Santander EuroLatam Conference47