Embed Size (px)

Citation preview

Fortune Oil PLCannual report 2012

Fortu

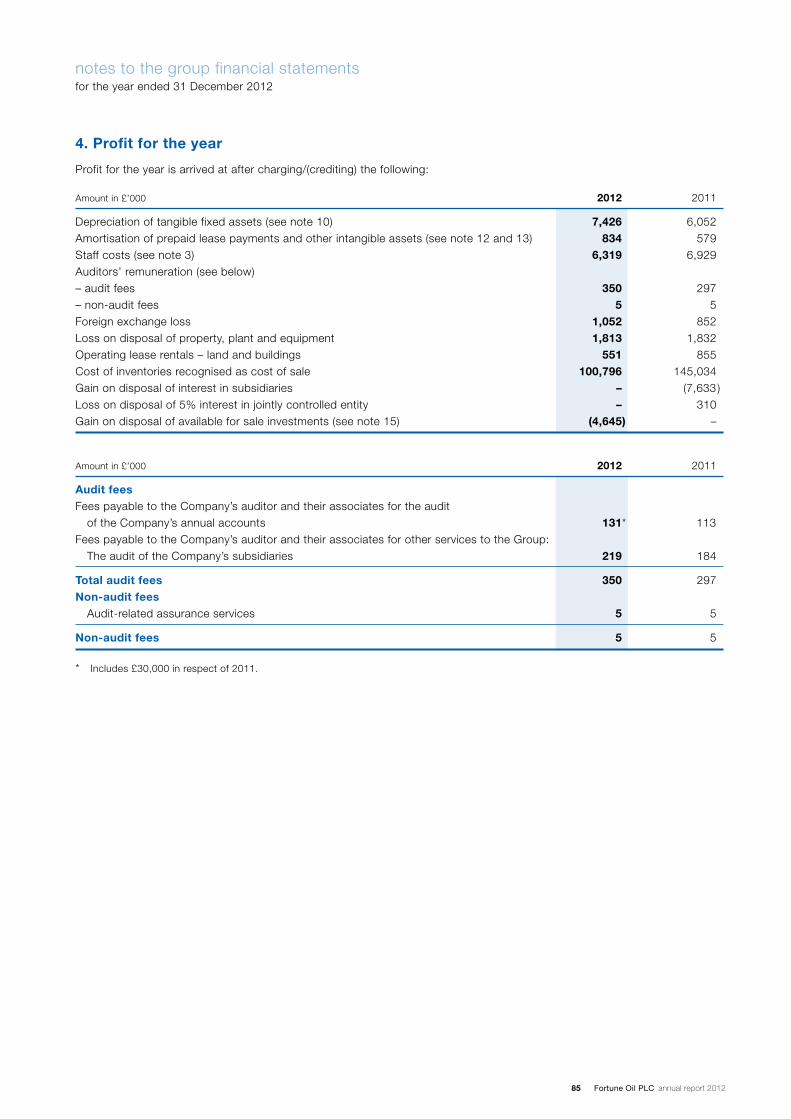

ne O

il PLC an

nu

al repo

rt 2012

BankersMorgan Stanley Asia LimitedLevel 46 International Commerce Centre1 Austin Road WestKowloon, Hong Kong

Standard Chartered Bank (Hong Kong) LimitedStandard Chartered Bank Building4 – 4A Des Voeux Road, CentralHong Kong

The Hongkong and ShanghaiBanking Corporation LimitedHSBC Main Building1 Queen’s Road CentralHong Kong

CITIC Bank International Limited80 Fl. International Commerce Centre 1 Austin Road WestKowloon, Hong Kong

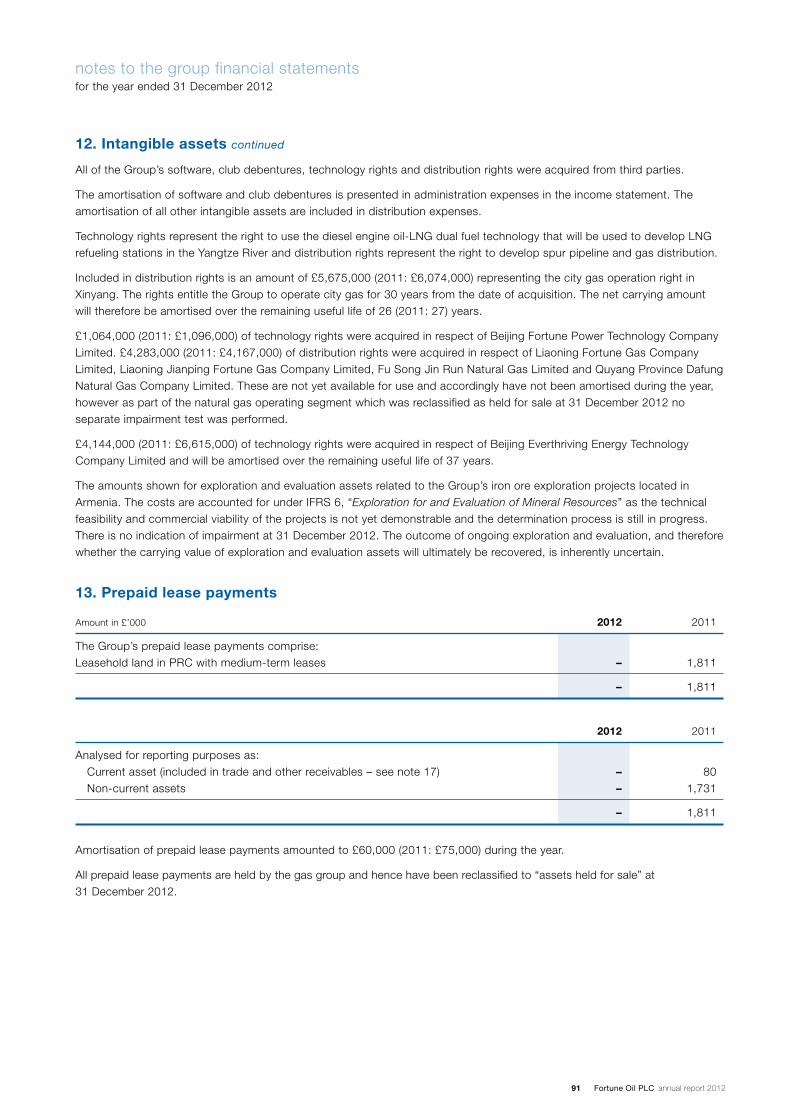

DBS Bank (Hong Kong) Limited16th Floor, The Center99 Queen’s Road Central Central, Hong Kong

Shenzhen Development Bank Co., Ltd.Guangzhou BranchNo. 66 Huacheng DadaoZhujiang Xincheng, GuangzhouChina

Barclays Bank plcKnightsbridge Business CentreP.O. Box 32014London NW1 2ZGUnited Kingdom

P R AdviserPelham Bell Pottinger5th Floor, Holborn Gate330 High HolbornLondon WC1V 7QDUnited Kingdom

Financial Adviser & Stockbroker Oriel Securities Limited150 CheapsideLondon EC2V 6ETUnited Kingdom

Corporate ConsultantS.Goschalk Limited41 MeadwayLondon NW11 7AXUnited Kingdom

Corporate AdviserVSA Capital LimitedFourth FloorNew Liverpool House15-17 Eldon StreetLondonEC2M 7LD

Investor Relations ConsultantScott Harris Victoria House1–3 College HillLondon EC4R 2RAUnited Kingdom

SolicitorsJun He Law OfficesSuite 2208, 22/F., Jardine HouseOne Connaught PlaceCentral, Hong Kong

Reed Smith LLPThe Broadgate Tower20 Primrose StreetLondon EC2A 2RSUnited Kingdom

DirectorsQIAN BenyuanChairman (Non-executive)

Daniel CHIUExecutive Vice-Chairman

TEE Kiam PoonChief Executive

LI Ching (Ms)Executive Director

Frank ATTWOODSenior Independent Director

LIN XizhongMAO TongDennis CHIULouisa HO (Ms)Ian TAYLORWANG JinjunZHI YulinNon-executive Directors

Company SecretarySandi CHOI (Ms)

Registered Office6/F., Belgrave House76 Buckingham Palace RoadLondon SW1W 9TQUnited Kingdom

Registered Number2173279

AuditorsDeloitte LLP2 New Street SquareLondon EC4A 3BZUnited Kingdom

company informationVisionTo be a leader in China’s energy and resources supply

StrategyTo invest and operate long term cost competitive assets supplying oil, gas and resources to China

1 Fortune Oil PLC annual report 2012

company profile

Fortune Oil PLC, a company listed on the London Stock Exchange focussing on the supply of crude oil, transportation fuels including petrol, diesel, aviation fuel, and natural gas in the People’s Republic of China and development of resources to capitalise on China’s growing demand for energy and resources.

Oil business; operates an off shore crude oil import terminal, refined products jetty and storage terminal, and aviation refuelling.

Trading Business; focuses on the supply and trading of oil and petrochemical products, LPG and LNG.

Natural gas business; includes the exploration, production, distribution and supply of natural gas to residential, industrial and commercial customers and the operation of natural gas vehicle refuelling stations.

Resources business; develops overseas investment opportunities to capitalise on China’s growing demand for energy and resources.

contents

1 company profile

2 operational locations

4 business highlights

4 five year summary

5 key performance indicators

6 chairman’s statement

9 chief executive’s review

12 business review • ourorganisation • ourdevelopment • ourmarket • oilbusiness • tradingbusiness • naturalgasbusiness • resources • corporatesocialresponsibility • environmentalreview • glossary

24 principal risks and uncertainties, their effects and our management strategy

26 financial review

28 board of directors

30 directors’ report

40 corporate governance

50 remuneration report

63 directors’ responsibilities statement

64 independent auditor’s report on the group financial statements

66 consolidated income statement

67 consolidated statement of comprehensive income

68 consolidated statement of financial position

69 consolidated cash flow statement

70 consolidated statement of changes in equity

71 notes to the group financial statements

113 five year summary

114 independent auditor’s report on the company financial statements

116 company statement of financial position

117 notes to the company financial statements

121 shareholder information

3027

2829

9

1011

12

16 2321

18

3

4

2

5

625

78

32

3331

2426

2014152217

1913

1

West-East Gas Pipeline

Shaanxi-Beijing Pipeline No. 1

Shaanxi-Beijing Pipeline No. 2

Chang-Hu Pipeline

Se-Ning-Lan Pipeline

Zhong-Wu Pipeline

Huai-Wu Pipeline

Ji-Ning Pipeline

North-East Pipeline connectingto Russian Gas Pipeline

Southern Pipeline

West Siberia East SiberiaSakhalin

Tashkent

2 Fortune Oil PLC annual report 2012

operational locations

Beijing municipality 1. Tongzhou

Shanxi province 2. Liulin 3. Shuozhou 4. Jinshatan 5. Changzhi 6. Jincheng

Henan province 7. Xinyang 8. Minggang

Tianjin municipality 9. Jinghai10. Daqiuzhuang11. Tuanbo

Hebei province 12. Quyang 13. Luquan 14. Jingxing 15. Luancheng 16. Xingtang 17. SJZ Airport Industrial Zone18. Wuji19. Shenze20. Gaocheng21. Xinji22. Lingshou23. Jinzhou

Shandong province 24. Qufu 25. Jining (new district)

26. Sishui

Liaoning province 27. Shenyang 28. Dashiqiao 29. Jianping

Jilin Province 30. Fusong

Chongqing Municipality 31. Ba-nan

Hubei province32. Zigui33. E-Zhou

Fortune Gas

Maoming SPMWest Zhuhai

Oil Terminals

Bluesky Airports

Baise AirportBeihai AirportChangde AirportChangsha AirportChaoshan AirportEnshi AirportGuangzhou AirportGuilin AirportLiuzhou AirportMeixian AirportNanning AirportWuhan AirportWuzhou AirportYichang AirportZhangjiajie AirportZhanjiang AirportZhengzhou Airport

3027

2829

9

1011

12

16 2321

18

3

4

2

5

625

78

32

3331

2426

2014152217

1913

1

West-East Gas Pipeline

Shaanxi-Beijing Pipeline No. 1

Shaanxi-Beijing Pipeline No. 2

Chang-Hu Pipeline

Se-Ning-Lan Pipeline

Zhong-Wu Pipeline

Huai-Wu Pipeline

Ji-Ning Pipeline

North-East Pipeline connectingto Russian Gas Pipeline

Southern Pipeline

West Siberia East SiberiaSakhalin

Tashkent

3 Fortune Oil PLC annual report 2012

4 Fortune Oil PLC annual report 2012

Financial £ million 2012 2011 Change %

Revenue including share of jointly controlled entities* 739.4 624.6 18

Profit after tax* 20.5 24.9 (18 )

Profit attributable to owners of the parent* 15.7 18.2 (14 )

Net assets 246.8 196.5 26

Net assets attributable to owners of the parent 188.4 141.1 34

Shareholders

Issued Shares, millions of shares 1,987 1,987 nil

Basic earnings per Share (pence)* 0.82 0.96 (14 )

Dividend per Share (pence) 0.16 0.18 (11 )

business highlights

five year summaryBlueskySales, million tonnes

2009 2010 201120080.0

0.40.81.21.6

2.02.4

2.83.2

2012

Profit attributable to owners of the parent* £ million

2008 2009 2010 2011 2012024

1086

1214161820

Maoming SPM ThroughputThroughput, million tonnes

2010 2011 2012200920080

2

4

6

8

10

12

West ZhuhaiThroughput, million tonnes

2010 2011 2012200920080.0

0.5

1.0

1.5

2.0

2.5

Natural GasSales, million cubic metres

0

90

180

270

360

450

540

630

2010 201120092008 2012

Connected Natural Gas customersThousands

2009 2010 20112008 20120306090120150180210240270300

* from continuing and discontinued operations.

5 Fortune Oil PLC annual report 2012

Key Performance Indicator Target Commentary

key performance indicators

Revenues including share of jointlycontrolled entities*£ million

2008 2009 2010 2011 20120

100200300400500600700800

To increase the Group’s revenues (including share of jointly controlled entities) by 10 per cent per year over the long term.

Target met:18 per cent increase over 2011.

Profit Attributable to Equity Shareholders*(Before other gains)£ million

2008 2009 2010 2011 20120

2

4

6

8

10

12

To achieve a growth of above 15 per cent per year over the long term in profit attributable to equity shareholders.

Target not met: 2 per cent increase over 2011.

Basic earnings Per Share*Pence

2008 2009 2010 2011 20120.0

0.2

0.4

0.6

0.8

1.0

To increase earnings per share (EPS) by 15 per cent per year over the long term.

Target not met year-on-year from 2011 to 2012 (there was a 14 per cent decrease).

Increase in Gas Sales %

and Gas Volume million m3

% million m3

-600

60120180240300360

0100200300400500600700

20102009 2011 20122008Target

increase in gas sales % gas volume million m3

To increase the volume sales of gas by over 30 per cent per year.

Target not met: 6 per cent increase over 2011.

2008 2009 2010 2011 2012

Lost Time Injury Frequency Rate for SubsidiariesLost time injuries per million man hours

0.0 0 0 0 0 00.5

1.0

1.5

2.0

2.5

To ensure safe operation for our personnel, as measured by Lost Time Injury Frequency Rate (LTIFR) for our subsidiary companies.

Target met as LTIFR was zero in 2012. Safety at work is critical to our business.

To minimise the accidental release of hydrocarbons to the environment from all our operating companies.

Target met as there were no significant spillages or releases. The Company is committed to environmental protection.

* from continuing and discontinued operations.

6 Fortune Oil PLC annual report 2012

chairman’s statement

Fortune Oil continued to perform strongly in 2012 and made significant progress across all core businesses, delivering on its strategy in the face of the prevailing uncertain global economic conditions.

IntroductionI am pleased to report that Fortune Oil continued to perform strongly in 2012 and made significant progress across all core businesses, delivering on its strategy in the face of the prevailing uncertain global economic conditions.

Results and OperationsThe Group’s revenues increased by 18 per cent to £739.4 million (2011: £624.6 million), and operating profits were £28.5 million, 4 per cent higher than 2011 (£27.4 million). Profit attributable to owners of the parent decreased by 14 per cent to £15.7 million (2011: £18.2 million) however, profits attributable to owners of the parent before other gains increased to £11.0 million (2011: £10.8 million).

During the year, we entered into a strategic joint venture arrangement with a view to investing in China Gas Holdings Limited (“CGH”), one of the largest independent natural gas businesses in China. This culminated in the decision, announced at the end of 2012 to enter into a transaction with CGH in relation to the Company’s natural gas business. Once complete, this will significantly strengthen the Company’s balance sheet, through the receipt of cash proceeds of US$170 million as half of the consideration for our 85% share of the natural gas business. The CGH transaction remains conditional on approval by the Anti-Monopoly Bureau of the Ministry of Commerce of the PRC and the Hong Kong Takeovers Executive or Takeovers and Merges Panel, which is expected mid-year 2013.

The Board is evaluating several options on how to best utilise the proceeds from the transaction including the potential for strategic acquisitions in the energy and resources sector that are synergistic to the Group’s strategy, and exploring other investment opportunities and gas supply options that can help to strengthen the supply of resources for the combined gas business with CGH.

Fortune Oil’s strength lies in its relationships with its joint venture partners in developing growth opportunities. This is clearly demonstrated with the CGH transaction which further strengthens our position in the Chinese natural gas market. As a result of the CGH transaction, Fortune Oil should own an enlarged stake and exercise significant influence in CGH, which will have natural gas operations in 200 cities across China. CGH recognised the complementary skills and assets of our natural gas business which ideally positions the company for success in what we expect to become an increasingly competitive market.

In 2012 we also made significant progress in a number of other key areas:

• We are in the final stages of negotiating a replacement structure for the Maoming SPM partnership.

• We obtained the government approvals to progress the construction of the gas gathering system for our CBM block in Liulin. This is a critical step towards commercialisation of gas from this block.

• We achieved a major first for China in obtaining the regulatory approvals for the commercial operation of our dual fuel LNG ship. This gives us first mover advantage in the development of a major new market for gas in China.

As a Group we will pursue attractive growth opportunities in our target markets.

7 Fortune Oil PLC annual report 2012

chairman’s statement

DividendThe Board recommends the payment of a dividend to shareholders for 2012, of 0.16p per share (2011: 0.18p per share). The dividend will be payable on 15 August 2013 to shareholders on the register as at 12 July 2013.

Management and GovernanceGiven the importance of the CGH transaction, continuity across the Board and Management team is critical during this period. We are determined to manage a smooth and efficient transition to a new combined natural gas organisation. The continued performance of all of our businesses during this period is critical and we will ensure that there is no disruption to our operations.

As a result of the CGH transaction and the proposed change of the status of the Maoming SPM joint venture, we were no longer able to maintain our Premium Listing on the London Stock Exchange but have become a Standard Listed company, with effect from 20 March 2013. Nevertheless, following this move we are committed to maintaining the high standards of corporate governance and the same reporting standards as are required for a Premium Listed company.

We will continue to evaluate options such that Fortune Oil’s listing status meets the best interests of the Company and our shareholders.

Review of China EconomyChina’s economy slowed to 7.8 per cent in 2012, its lowest annual growth rate since 1999, as a result of restrictions the Chinese government had put in place to cool China’s property market and as a result of the lower demand for Chinese goods from Europe and the United States. However, unlike in 2009, the Chinese government did not step in with a stimulus plan. The outcome is a general recognition that the days of double-digit growth in the Chinese economy have come to an end. The ten yearly transition of the Chinese leadership in 2012 is expected to lead to a wholesale revamp of government ministries aimed at reducing bureaucracy.

Energy price mechanisms are also being reformed and are moving to a more market based approach. Fortune Oil pays close attention to short-term economic conditions but also takes a long term strategic view of the Company’s development, balancing growth opportunities and investment returns whilst continuously looking to improve our competitiveness.

OutlookFortune Oil’s growth is underpinned by China’s ongoing economic growth and the associated increase in demand for energy. Although China’s GDP grew at only 7.8 per cent in 2012 the OECD is predicting growth of 8.5 per cent in 2013 and 8.9 per cent in 2014. The OECD also predicts that China will over take the United States and become the world’s biggest economy in 2016.

In line with the slowdown in China’s economic growth rate, Chinese oil demand grew by 4.2 per cent in 2012, or at about 387,000 barrels of oil per day, down from 6.3 per cent growth in 2011 and the double-digit growth in 2010. In line with signs that the economy started to expand in Q4 2012, China’s crude oil demand hit a record high of 44.8 million tonnes and refinery throughput also reached an all time high of 10.15 million bpd in December 2012.

Consumption of oil-derived products such as diesel and petrol will continue to grow to fuel the rapid expansion of the automotive and aviation sectors. Maoming SPM, West Zhuhai Terminal and the Bluesky businesses are well positioned to participate in this growth.

Looking to the future, the projects that will help drive Fortune Oil’s growth are advancing well.

In the natural gas business we anticipate completion of the gas gathering system by the middle of 2013 and this will enable commercial gas sales from our CBM block in Liulin. With the approval of our LNG ship design we will progress the development of our construction of LNG refuelling stations along the Yangtze and conversion of ships to dual fuel LNG technology.

8 Fortune Oil PLC annual report 2012

In the Oil business we are planning to increase the capacity of the SPM terminal once the replacement partnership structure is in place to meet the growing demand at Sinopec’s Maoming refinery and our Trading business is expanding into the supply and trade of other commodities including diesel, LPG and LNG.

Guangzhou airport started construction of its third runway and second terminal in August 2012, as passenger traffic has exceeded its design capacity. The airport handled 48 million passengers in 2012 but this is projected to increase to 80 million in 2020. This bodes well for the Bluesky business which supplies the aviation fuel to this airport.

The Resources business completed the feasibility study and obtained a JORC compliant resource estimate for the Hrazdan iron ore mine in Armenia and is in the process of completing a final set of studies required to obtain the regulatory approvals which are now expected in 2014.

As a Group we have clear priorities, direction and focus. I remain confident of the continued success in the coming years and see great opportunities ahead. In shaping our portfolio, our priority is to create value for our shareholders and enable them to share in China’s

growth, one of the most exciting markets in the world. I would like to thank them for their continued support and loyalty. We remain very optimistic about the future growth prospects for Fortune Oil. With its solid foundation across the oil and gas sectors in China and the anticipated rising demand for energy, the Group anticipates an even better future for its businesses in the years to come.

Finally, I would like to thank all of our employees for their efforts. This has been another demanding year and they have shown admirable dedication. Special thanks are due to management for the successful execution of the CGH transaction, the most significant in the Company’s history.

QIAN BenyuanChairman24 April 2013

chairman’s statement

Guangzhou airport started construction of its third runway and second terminal in August 2012.

9 Fortune Oil PLC annual report 2012

chief executive’s review

all operations for the year amounted to £15.7 million, a decrease of 14 per cent compared to £18.2 million in 2011 mainly as a result of an exceptional one off profit in 2011 of £7.3 million arising from the deemed divestment of the CBM business. Group profit from operations, excluding gains on disposals and deemed disposal increased by 4 per cent to £28.5 million (2011: £27.4 million). Earnings per share for the year decreased to 0.82 pence compared to 0.96 pence in 2011, a decrease of 14 per cent. Operating profit growth in 2012 was driven by a strong contribution from our Bluesky aviation and natural gas businesses. The net borrowing position stayed low at £61.1 million as at 31 December 2012 (2011: £5.7 million). During the year we invested £59.9 million which primarily consisted of the injection into China Gas Group (“CGG”) for shares acquisition purpose of £35.6 million and capital expenditure of £15.7 million, mainly to continue development of our integrated natural gas business.

I continue to be greatly encouraged by the Group’s performance. Our focus is on continuous improvement and to drive efficiency in our operations.

StrategyFortune Oil has a clear and focussed strategy: we invest in and operate long term cost competitive assets supplying oil, gas and resources to support China’s growing economy. To achieve this we focus on our portfolio of assets with the intention of:

• Becoming a leading integrated natural gas supplier across our selected regions in China via our equity investment in CGH;

• Developing opportunities in the Chinese oil sector, in particular exploiting the Company’s unique position in oil products supply and terminals; and

• Developing overseas resources supported by our strong relationships with major Chinese state owned enterprises.

2012 ResultsFortune Oil continued to make good progress in 2012. We have achieved a series of key milestones and remain on course with our growth strategy, making great strides forward across our core businesses of oil, gas and resources.

Through our transaction with CGH we will be cooperating with one of the largest natural gas companies in China supplying gas to over 200 cities with a strong platform for future growth. Fortune Oil shareholders will continue to be exposed to China’s considerable natural gas growth, through our shareholding and management position in CGH.

In our Oil business we also continue to make good progress. We are close to finalising the replacement structure to expand the Maoming SPM joint venture with Sinopec and the Bluesky aviation fuel joint venture also turned in another solid performance.

In the Resources business, we have completed the feasibility study and JORC resource statement on the Armenian iron ore asset and made good progress on other technical and environmental studies required to fulfil the necessary regulatory approvals.

In terms of financial performance, 2012 was another good year for the Company. Higher sales volumes drove a 18 per cent increase in revenues from all operations to £739.4 million in 2012 from £624.6 million in 2011. Group profit after taxation attributable to owners of the parent from

I continue to be greatly encouraged by the Group’s performance. Our focus is on continuous improvement and to drive efficiency in our operations.

10 Fortune Oil PLC annual report 2012

chief executive’s review

Our focus has resulted in the creation of the SPM, Bluesky, West Zhuhai Terminal and the natural gas business which have provided strong and consistent cash flows and most recently the potential for a significant cash inflow and the opportunity to build upon the strategic relationship with CGH.

Key Performance IndicatorsWe continue to apply the six principal Key Performance Indicators (“KPIs”) that were adopted in 2004. We feel these continue to be valuable in assessing how well the Group has been performing against its strategic objectives. In 2012 we met or exceeded three out of the six KPIs (see page 5).

2012 Key AchievementsIn 2012 the Group had four priorities. First, to conclude the renewal of the Maoming SPM joint venture; second, to reinforce the strategic direction of the natural gas business; third, to progress the commercialisation of gas from the CBM project in Liulin; and finally, progress the Armenian iron ore project towards the final investment decision point. Substantial progress has been made in meeting these priorities as detailed in this report.

The Maoming SPM was one of the original investments on which Fortune Oil was founded. The SPM arrangements with the Company’s partners were due to expire on 5 February 2013 but have continued pending completion of an alternative partnership structure. The Company is now in the final stages of concluding a replacement structure for the Maoming SPM partnership which will include the development of a new pipeline and buoy. We expect that under the new structure, the Company will no longer hold a controlling equity stake in the joint venture although the scope of the joint venture with Sinopec will be expanded.

Natural gas continues to play an increasing role in meeting the government targets in energy conservation and environmental protection and we have steadily expanded this business with our focus on growth in the higher margin sectors of LNG and CNG refuelling and gas supply to industrial zones. In 2012 our natural gas sales exceeded 500 million cubic metres and we connected an additional 67,907 new customers.

We have also become the first company in China to secure the regulatory approvals for an LNG dual fuel ship. This is a very significant milestone and demonstrates that our technology is at the leading edge of this important new market. We are already constructing our first LNG refuelling station in Chongqing and our plans for a network of stations along the Yangtze are progressing to plan. In LNG vehicle refuelling, our projects in Liaoning and Hebei province are

well advanced and our first mover advantage will ensure we access the prime locations to capture the rapidly expanding LNG fuelled bus and truck fleets in these provinces.

In Liulin our total field production from the Fortune Liulin Gas CBM wells exceeded 27,000 cubic metres per day, the Production Sharing Contract (“PSC”) was extended a further two years until March 2014, and we commenced construction of the gas gathering system which will collect the gas from the various wells and transport it to the wholesale station we have built. We are on track for commercial production of gas from Liulin in 2013.

The Company also took the strategic step to enter into the CGH transaction described in more detail below, as this was seen as the most efficient avenue to accelerate the growth and strengthen our position in China’s rapidly expanding natural gas market. Through this transaction, we will hold a significant position in a nation-wide natural gas supplier to over 200 cities with significant growth potential, positioning the combined natural gas businesses as amongst the largest natural gas companies in China.

The transaction allows Fortune Oil to become part of a much stronger business platform well positioned to capture a disproportionate share of the China natural gas market. Moreover, we anticipate this market will see more consolidation and greater competition from the major state owned gas companies. Following the completion of the transaction, we will be one of the largest shareholders in CGH, with a founder and managing director of CGH as our joint venture partner in our investment vehicle. Under the terms of the transaction, we have the right to nominate two directors to the board of CGH, one to be the managing director, thus enabling us to have significant influence in the development and strategic direction of CGH.

Outlook for 2013In 2012 we continued to put in place the solid foundations on which to build our future. Although China’s economic growth cooled from the double digit growth of previous years, there are signs that the economy has turned and with the new Chinese administration taking control, we expect to see significant steps being taken to maintain China’s strong and sustained growth as well as a continued strong demand for energy.

We constantly assess the potential impact of these factors on the Group’s plans, ensuring that the Company’s interests are protected and that our investment strategy is appropriate to the prevailing market conditions. We believe our solid foundations and strategy will enable us to continue to grow in the volatile and challenging markets.

11 Fortune Oil PLC annual report 2012

China crude oil demand reached a record high in December 2012 and we expect demand in the oil sector to remain strong. This will mean continued demand for our Oil business “engines” of Bluesky, Maoming SPM and West Zhuhai Terminal, which, although mature businesses, generate much of our cash flow. We will continue to invest to keep them running smoothly and efficiently and to extract additional value.

The news in China over the past few months has highlighted the poor air quality in several of the major cities in China, including Beijing, due to coal consumption. Natural gas will be the cornerstone to improve local air quality. Our involvement with CGH will be the ideal platform to increase our share of this rapidly expanding market. Through CGH, we are creating scale and critical mass, which are key in an increasingly competitive market. We expect to complete the transaction with CGH around the middle of 2013 and we will then work closely with CGH to enhance the development of the combined natural gas business.

The resource business made good progress on the development of the Hrazdan mine. We completed the JORC compliant mineral resource statement and the feasibility study and are working through various technical and environmental studies required to obtain the necessary regulatory approvals. Whilst it remains difficult to be definitive about the long term iron ore cost of production

curve, China Metallurgical Mines Association (“CMMA”) estimates that 42 per cent of iron ore supply to China is unprofitable at prices less than US$100/tonne, providing us a clear target for the cost of production we need to achieve to ensure the commercial success of this project.

Our EmployeesFinally I would like to join the Chairman in thanking our employees for their dedication, hard work and focus. We are very much judged on our results and our employees are responsible for helping us achieve this. Throughout the year, their commitment, talent and integrity have led to the delivery of our strong performance.

On behalf of the Board, I would also like to thank our shareholders as their continued support for Fortune Oil which has helped us achieve such a good performance in 2012.

TEE Kiam PoonChief Executive24 April 2013

The commitment, talent and integrity of our employees helped us achieve such a strong performance.

12 Fortune Oil PLC annual report 2012

business review

CAUTIONARY STATEMENTThe purpose of the Annual Report is to provide information to the shareholders of the Company. The Annual Report contains certain forward-looking statements with respect to the operations, performance and financial condition of the Company and the Group as a whole. By their nature, these statements involve uncertainties since future events and circumstances can cause results and development to differ from those anticipated. The forward-looking statements reflect knowledge and information available at the date of preparation of the Annual Report. Nothing in the Annual Report should be construed as a profit forecast.

OUR ORGANISATION

Our activities span across northern, central and southern China and include the following operations:

• The Bluesky aviation refuelling business supplies jet fuel to 17 major airports which handled 107.7 million passengers in 2012;

• The Maoming Single Point Mooring Facility supplied 11 million tonnes of crude oil to Sinopec’s Maoming Refinery in 2012, one of the largest refineries in China;

• The West Zhuhai import and distribution terminal supplies petrol and diesel to Petrochina’s downstream refuelling markets across southern China;

• The natural gas business is focussed on ten key provinces and, in 2012, supplied approximately 280,000 customers with fuel for transportation, the energy to heat their homes, and the power to drive their industries;

• The introduction of LNG dual fuel ships and associated LNG refuelling infrastructure for river borne cargo operations;

• The development and commercialisation of coal bed methane in Liulin, Shanxi Province; and

• The supply and trading of oil, gas and petrochemical products.

OUR DEVELOPMENT

Fortune Oil has always sought to exploit opportunities in the oil products and natural gas industry as the Chinese market continues to expand. In summary our aims are to:

• Work with CGH to become a leading integrated gas supplier across selected regions in China via our equity investment in CGH;

• Bring Liulin CBM to commercialisation and to integrate it with downstream markets;

• Develop opportunities for the supply and trading of fuels to China, in particular exploiting our unique position in oil products supply and terminal operations;

• Develop overseas high growth rate commodities such as oil, natural gas, coal and metals with linkage to China and the ability to generate cash flows within three years.

This Operational Review details our performance in 2012, assesses the changing economic and business environment in China, the performance of the major operating businesses, and our responsibilities to the community.

Fortune Oil PLC, a London Stock Exchange listed company with operational headquarters in Hong Kong, has supplied oil products and natural gas in the People’s Republic of China for almost twenty years. We have done this reliably and, importantly, safely.

13 Fortune Oil PLC annual report 2012

OUR MARKET

In 2012 China imported 271 million tonnes of crude oil, representing a 6.8 per cent increase on 2011, with crude oil demand reaching an all time high of 44.8 million tonnes in December 2012. The NDRC’s Energy Research Institute is predicting that China will consume over 500 million tonnes of oil products in 2013, of which 60 per cent would be imported. Oil products demand is projected to increase to 540 million tonnes by 2015, driven by increasing demand for transportation fuels such as petrol, diesel and jet fuel.

Auto vehicle sales in China, rose 4.3 per cent in 2012 to 19.3 million, a modest increase over the previous year’s pace, according to the China Association of Automobile Manufacturers (“CAAM”). CAAM is predicting an improved picture for 2013, forecasting a 7 per cent rise in total vehicle sales for the year. China is also expected to produce more cars than Europe in 2013 for the first time, a milestone in the country’s industrial history. Annual car sales growth of between 5 and 8 per cent is predicted over the next decade.

The volume of air passenger traffic reached 319 million person-trips in 2012, an increase of 9.2 per cent year- on-year, according to the Civil Aviation Administration of China (“CAAC”). Passenger traffic growth in 2012 was almost the same as in 2011. Total air passenger and freight transport increased by 6.1 percent year-on-year in 2012 to 60.8 billion ton-km, according to CAAC. The International Air Transport Association (IATA) remains optimistic about the industry’s prospects; globally air-line passenger numbers are set to rise by over a quarter in the coming years to hit 3.6 billion in 2016, with China accounting for nearly one in four new travellers.

Fortune Oil’s operations in the oil sector are primarily in infrastructure facilities for the import and supply of oil and oil derived products. Continued growth in demand for transportation fuels will ensure strong utilisation of Fortune Oil’s facilities.

According to NDRC, China saw its consumption of natural gas rise 13 per cent to 147.1 billion cubic metres in 2012. China produced 107.7 billion cubic metres of natural gas, an increase of only 6.5 per cent on 2011 production. To meet this accelerating demand, China has had to increase significantly the amount of gas it imports. In 2012 China’s natural gas imports surged 31.1 per cent from the previous year to 42.5 billion cubic metres with imports now accounting to 29 per cent of the country’s total consumption.

Although demand for natural gas continues to grow dramatically, China still lags behind developed countries in terms of infrastructure development and per capita consumption of natural gas. In Japan for example power produced from natural gas makes up 28 per cent of the country’s total domestic power generation. That percentage in the U.S. and Europe is more than 20 per cent and 30 per cent respectively, while in China, it is still under 3 per cent.

China’s rapid economic development and the growth of the predominantly coal-based energy production have resulted in a drop in the air quality in many of China’s major cities. In response, the Chinese government implemented the Ambient Air Quality Standard in February 2012 which sets to improve air quality and limit the levels of key pollutants. The introduction of this standard and the existing supportive Government policies are expected to enhance the prospects of natural gas as the energy source of choice in the urban market.

To support this expansion of the natural gas market China continues to invest heavily to increase natural gas supply with the West to East Gas Transmission pipelines constructed to bring natural gas from the Xinjiang Autonomous Region to the coastal regions of China. Construction of the second phase of the West to East Gas Transmission pipelines from Central Asia and the Sichuan to East pipelines from the gas rich Sichuan Province to coastal regions have been completed. The West to East Gas Transmission Phase 3, the Myanmar to Yunnan gas pipeline, as well as additional LNG terminals in the coastal cities of China are actively being developed to meet the anticipated growth in natural gas demand which the International Energy Agency predicts will grow by 17 per cent each year through to 2017.

China is also driving the expansion of its indigenous gas production to limit its dependency on gas imports. China’s National Energy Administration announced that it will allocate more funds and encourage private capital to exploit the country’s large reserves of coal bed methane gas and encourage the inflow of private capital into the sector. China plans to complete construction of two major coal bed methane production bases in the central and western regions by 2015 and increase the number of production bases up to five in the next 10 years. The Ministry of Land and Resources announced plans in February 2013 to produce 16 billion cubic meters per annum of coal bed methane increasing to 30 billion cubic meters by 2015. Success for Fortune Oil in the Liulin block will position us well for the future development of opportunities in CBM.

Natural gas price reforms to close the price gap between imported and local gas prices are also gradually being implemented. Once realised, these measures are expected to more than double the supply of natural gas in China in the next few years and will result in increases in the price of natural gas throughout the supply chain from the well head to the ultimate customer.

China’s demand for all the main commodities such as coal, iron ore and copper continues to grow. China imported a record 743.6 million tonnes of iron ore in 2012, up 8.4 per cent from 2011, exceeding previous projections, and many of the major iron ore companies are predicting that iron ore demand will continue to grow beyond 2020 as increased urbanisation drives construction and hence steel demand. This bodes well for the prospects of our Resources business.

14 Fortune Oil PLC annual report 2012

business review

West Zhuhai Jetty and Storage Terminal supplies gasoline and diesel to Petrochina’s retail business in southern China and part of Petrochina’s strategic oil products reserve.

China’s only off-shore oil import terminal supplying 4 per cent of China’s crude oil imports. The Maoming single point mooring (SPM) acts as a delivery point for imported crude oil and can handle Ultra Large Crude Carriers (300,000dwt) supplying the Sinopec Maoming Refinery in Guangdong Province.

We have a unique portfolio of oil activities in partnership with the leading Chinese State owned enterprises including Petrochina, Sinopec and China National Aviation Fuel Company.

South China Bluesky Aviation (Bluesky) is one of the largest aviation fuel storage, supply and logistic operations in China which owns and operates the aviation fuel storage terminals, pipelines and aviation refuelling services for 17 major airports in central and southern China.

OIL BUSINESS The oil business continues to be a strong cash generator for the Group. In 2012 we continued to expand our supply of crude oil, oil based products and jet fuel.

Aviation Refuelling (South China Bluesky Aviation Oil Company)In 2012, Bluesky’s sales of jet fuel continued to increase, rising by 15 per cent to 3.0 million tonnes, compared with 2.6 million tonnes in 2011. Joint venture revenues increased to £2,021.4 million (2011: £1,647.9 million). Bluesky achieved a net profit of £47.2 million (2011: £47.4 million) with a Fortune Oil share of £11.6 million, matching the previous years record profit (2011: £11.6 million).

Air travel demand is still expanding across China and Bluesky continues to evaluate opportunities to extend its operations to new airport developments with China National Aviation Fuels Ltd in Central and Southern China covering Guangdong, Guangxi, Hubei, Hunan and Henan provinces.In 2012 Bluesky started supplying fuel to two more airports (Wuzhou and Baise) bringing the total number of airports Bluesky supplies to 17.

Maoming Single Point Mooring (SPM)In 2012 Maoming SPM throughput matched the record performance of 2011 of 11.0 million tonnes (2011: 11.0 million tonnes) handling 57 tankers just one delivery less than last year’s record. Throughput revenues in 2012 were maintained at £16.4 million (2011: £16.3 million) with a net profit of £4.1 million, (2011: £4.0 million). Fortune Oil’s share of net profit in 2012 was £1.7 million (2011: £1.6 million).

The original SPM joint venture period expired in February 2013 and continues pending completion of the new arrangements. Fortune Oil and Sinopec are currently in discussions regarding the future cooperation on the SPM and additional developments to serve the Maoming refinery. Management is optimistic of a satisfactory outcome to such discussions and, although under the new structure, the Company will no longer hold a controlling equity stake in the joint venture, the scope of the joint venture with Sinopec will be expanded with the potential development of a new pipeline and buoy.

Products Terminal and SupplyThe West Zhuhai Products Jetty and Storage Terminal (South China Petroleum Company) performance was maintained over 2012 although the terminal is not operating at full capacity due to lower utilisation of the facility by Petrochina. The throughput increased slightly to 2.5 million tonnes (2011: 2.3 million tonnes), with a slight increase in company revenues of £7.2 million (2011: £7.0 million). The profit contribution to Fortune Oil decreased to £0.8 million compared to £1.1 million in 2011.

West Zhuhai Oil Products Terminal is now part of Petrochina’s “Strategic Oil Products Reserve facilities” underlining the strategic importance of the Company’s unique storage facility in Southern China. This will help to limit the possibility of oil products supply disruption in Southern China. More importantly it will also help to generate new revenue streams from the recently expanded facilities at West Zhuhai. Options to diversify the customer base are currently being evaluated in order to help address declining volumes.

15 Fortune Oil PLC annual report 2012

business review

The trading business continues to focus on the supply and trading of oil and petrochemical products.

TRADING BUSINESS The trading business continues to focus on the supply and trading of oil and petrochemical products.

In 2012 we traded 157,000 tonnes of petroleum products and petrochemicals, compared to 144,000 tonnes in 2011. Revenues generated by these activities increased by 2 per cent to £123.4 million (2011: £121.5 million) with an earnings contribution of £1.0 million compared to £1.0 million in 2011. The trading business continues to explore options for the expansion of products that it trades.

Fortune Oil obtained in 2012 one of the first licences issued to enable the supply and trade of diesel and other refined products. Previously this area was limited to the major state owned enterprises. Fortune Oil has completed 5 shipments with a total inventory of 23,200 tonnes of diesel in 2012.

During our negotiations with CGH we have also identified the opportunity to support their LPG supply requirements and are currently in discussions with various suppliers to develop this option further.

Fortune’s licenses will enable the Trading business to support CGH’s LPG supply requirements and this is also a clear demonstration that the Company’s strategy of developing relationships with key JV partners is allowing the Company to access markets generally closed off to the competition.

The carbon asset investment fund established with Huaneng Carbon Asset Ltd and Vitol S.A. is progressing several

carbon emission projects. During 2012 25 “Specific Project Investment Agreements” have been developed and submitted to NDRC for approval. Among these projects, 14 projects have acquired letters of approval and 3 projects have been submitted for UN registration.

Fortune Oil has established a joint venture with Tianjin Gas that will be responsible for the supply of LNG to the city of Tianjin, China’s sixth most populous city with a population of over 12 million. The joint venture company will manage, on a non-exclusive basis, the procurement, import and supply of LNG to Tianjin Gas including securing reliable and competitive overseas LNG supply. Fortune Oil holds 60 per cent and Tianjin Gas 40 per cent of the equity interest in the joint venture company. This joint venture will not form part of the CGH transaction and will remain within Fortune Oil’s trading business.

Tianjin Gas is the largest natural gas supplier in Tianjin City responsible for gas supply and operations to 18 districts and counties in Tianjin City with over 95 per cent of the market, 2 million customers and 9,000 km of gas pipelines. Tianjin Gas is one of the main shareholders in the Tianjin LNG Import and Regasification terminal which is expected to start operations in 2013. The terminal will initially import 2.2 million tonnes (3 bcm) of LNG per annum into China using a floating storage and regasification unit (“FSRU”) with the plan to expand the LNG import terminal in Tianjin to a capacity of 6 million tonnes per annum (8 bcm) from 2015.

16 Fortune Oil PLC annual report 2012

business review

We have natural gas operations in over 30 cities across 10 provinces and municipalities with approximately 280,000 connected customers where we supply gas to households, industries and clean vehicle refuelling.

NATURAL GAS BUSINESS

The natural gas business continues to benefit from China’s robust economy and thriving natural gas demand. We have been steadily expanding our upstream and midstream operations as well as our downstream city-gas and refuelling operations. Through our transaction with China Gas Holdings, we will have an ideal platform to accelerate this expansion.

PerformanceThe natural gas business strategy has built, and in combination with CGH, will continue to build an integrated natural gas business linking upstream gas production to supply our chosen downstream markets.

Fortune Oil’s natural gas business develops and operates natural gas supply and distribution infrastructure to supply natural gas to industrial, commercial, residential and transportation sectors. We are working with CGH on a combined gas strategy that will encompass the development of both upstream and downstream assets, further investment in existing city networks and selective acquisitions where these can be acquired on economically sensible terms. Pending completion of the CGH transaction we are continuing with our development plans for the natural gas business.

Revenue including the share of jointly controlled entities in the gas division in 2012 increased 30 per cent to £91.8 million (2011: £70.6 million). The operating profit for the gas business increased 51 per cent to £15.8 million (2011: £10.5 million). The natural gas business net profit

contribution to Fortune Oil increased by 76 per cent to £8.8 million (2011: £5.0 million), after taking in to account the minority interest held by Wilmar.

In 2012 Fortune Gas sales volumes increased 6 per cent to 502 million cubic metres (2011: 472 million cubic metres) and 67,907 new customers were connected in 2012 an increase in new connections by 79 per cent bringing the total number of customers up to approximately 280,000 (2011: 212,000) a 32 per cent increase.

In 2012 Fortune Oil increased its shareholding, via the CGG joint venture in CGH, the largest independent natural gas company in China in terms of city network, supplying natural gas to over 170 cities. The strategic objective of forming this joint venture was to develop cooperative opportunities combining CGH’s strengths with those of Fortune Oil and to accelerate the growth rate of Fortune Oil’s natural gas business in China.

The two companies’ natural gas businesses are highly synergistic and the proposed transaction will be the most effective means of cooperation. Through this transaction Fortune Oil and its associates will become one of the largest shareholders in and be involved in the management of CGH. As a result, Fortune Oil will continue to create value for our shareholders from the rapid growth in China’s natural gas market. This enhanced business platform will be better able to capture an increased market share in the rapidly expanding China natural gas market and create value for the shareholders of both companies. This investment advances our stated strategic objectives of developing Fortune Oil into a leading business in the Chinese natural gas supply market.

Upstream CBM ProjectOur state pilot project is deploying cutting edge in-seam drilling and advanced hydraulic fracturing technology to commercialise coal bed methane in Shanxi.

17 Fortune Oil PLC annual report 2012

business review

Natural gas will continue to be one of the growth engines of the Group. Fortune Oil and CGH have identified a number of specific expansion opportunities for the combined gas business which they will accelerate through their new partnership with the aim of CGH becoming one of the top three gas companies in China. Fortune Oil will also continue to develop new projects together with CGH.

As at April 23 2013 the Company’s joint venture CGG and its associates (including shares held directly by Mr. Liu Minghui, the Managing Director of CGH) held 911,550,000 shares in CGH representing 20.0 per cent of CGH total issued shares making the joint venture and its associates (including shares held directly by Mr Liu Minghui, the Managing Director of CGH), the second largest shareholder of CGH.

Upstream CBM ProjectThe CBM project in Liulin covers 183 square kilometres and is located in the eastern part of the Ordos basin 500km south west of Beijing. Fortune Liulin Gas Company (“FLG”) is the foreign contractor in the Production Sharing Contract (“PSC”) with China United Coal Bed Methane Corporation (“CUCBM”). FLG met its exploration drilling targets for the CBM Liulin Block and the Ministry of Commerce has approved an extension of the exploration period of the PSC for the Liulin CBM block to 29 March 2014.

Fortune Oil continues to make good progress in the development of the Liulin CBM block and first commercial gas sales are expected in 2013 following completion of the gas gathering system. Total field production from the FLG horizontal wells now exceeds 27,000 cubic metres per day with the most successful well to-date (H3) currently

producing over 12,000 cubic metres per day, a rate which exceeds all previous wells drilled by FLG. These flow rates have been achieved with a bottom hole pressure (“BHP”) of 1.6 megapascals (MPa) and gas flow rates are predicted to increase as the BHP is reduced further to a target of around 0.2 MPa.

In 2012, FLG drilled 2 more horizontal wells which are currently being dewatered and undergoing production testing. These wells, together with existing wells are expected to provide sufficient production volumes to meet the requirements of the existing Gas Sales Agreement (“GSA”) of 100,000 cubic metres per day. Pricing under the GSA, is RMB 1.58 per cubic metre which equates to gross sales revenues of RMB 52.1 million (£5.0 million) per annum (£2.5 million net to FLG). These inseam wells have been designed to optimally drain two independent coal seams from the same production well. These wells have been designed and supervised by FLG ensuring the intellectual property and technical experience remains within the FLG project team.

CUCBM have drilled a total of 145 vertical wells and 4 horizontal wells across the Liulin block. To date 40 of the vertical wells have been “fracked” to put into test production. These wells will enable reserves certification for additional coal seams across the block and development of the Overall Development Plan (“ODP”) and together with the gas produced from the lateral wells on the northern section, gas produced from the CUCBM wells will also be used to meet the gas sales agreement. The data from these wells will be used in conjunction with existing data to review the reserves estimates for Liulin in 2013.

Refuelling with GasThe Group continues to expand vehicle gas refuelling business which is core to the growth of the natural gas business.

City gas businessesOwns and operates the city networks connecting and supplying natural gas to apartment complexes and commercial buildings.

Wholesale Gas DistributionOur spur pipelines and wholesalestations connect the gas from the main transnational pipelines to our cities and supply gas to the downstream customers.

18 Fortune Oil PLC annual report 2012

business review

Fortune Oil received the regulatory approvals for the installation of the gas gathering system and construction is in progress. The gas gathering system consists of over 20 km of gas gathering pipeline which will collect the gas from the wells and transfer it to the nodal compression station. Here the gas will be purified, compressed and dispatched by an 8 km pipeline to the Shanxi CUCBM wholesale CNG station. The gas from the Liulin block will be marketed by Shanxi CUCBM, a joint venture between Fortune Oil and CUCBM and the parties have an initial gas sale agreement for 33 million cubic metres per annum. Fortune Oil is also progressing the design and planning to install the gas pipeline from the wholesale station to connect Liulin to the main national gas network. This will allow both the export of gas from Liulin as well as import gas from the national grid to the Fortune Gas wholesale station.

The ODP has been prepared for submission in 2013 and a summary ODP has been submitted to FLG’s Chinese partner CUCBM. The ODP is the final approval procedure required for full commercial operations and marks the transition of the field from exploration to development and operation and is a key step towards the commercial production of gas from Liulin.

Midstream Wholesale Gas DistributionThe wholesale gas distribution business continued to expand the natural gas pipeline network and wholesale gas stations. Our gas pipeline network increased to 1059km in 2012 (2011: 771km) and one new natural gas wholesale station was opened, bringing the number of natural gas wholesale processing stations to 5 with a daily natural gas supply capacity of 600,000 m3. In 2012 Fortune Oil supplied over 87.5 million cubic metres through its wholesale stations.

Shanxi CUCBM has completed the Liulin CNG wholesale station. This wholesale gas station will compress and distribute natural gas produced from the Liulin CBM block and supply Shanxi CUCBM refuelling stations and industrial customers across Shanxi province further demonstrating the effectiveness of Fortune Gas’s integrated natural gas business model.

Fortune Gas continues to make good progress in developing the local gas pipeline network in Dashiqiao. This includes the completion of the first phase of the development comprising the connection of the pipeline to the industrial zone of the city, where a major magnesium industry has significant gas demand.

TOP Wholesale CNG trailers distribute gas.

BOTTOM LEFT Filling a CNG trailer with high pressure gas.

BOTTOM RIGHT Producing gas from our CBM block in Liulin.

Finding, producing and distributing natural gas to serve our customers.

19 Fortune Oil PLC annual report 2012

business review

City Gas BusinessOne new city gas project was launched in Quyang, Hebei province in 2012 bringing the number of our city-gas businesses to over thirty cities in ten provinces and municipalities. This extensive city-gas network forms the core of our gas business portfolio.

During the year the Group continued to focus on boosting connections in existing projects. A further 67,907 new customers were connected in this period (2011: 38,014), representing a 79 per cent increase in the rate of connections, demonstrating the continued growth post the divestments as new city gas networks are connected to a gas supply bringing the total of connected customers to approximately 280,000 representing an increase of 32 per cent (2011: 212,000 customers). Market penetration rates remain low; typically around 25 per cent of the connectable urban populations have been added to the city network highlighting the continued opportunity for growth in this business.

The Group also provided natural gas connections for 200 new commercial/industrial (“C/I”) customers (2011: 156) an increase of 28 per cent. We continued to focus on growing this higher margin sector and at the end of 2012, we had 1,000 C/I customers covered by the Group’s projects (2011: 800).

Gas Vehicle RefuellingThis year we completed two new vehicle CNG refuelling stations, in Sishui and Mingzheng, bringing our total to 11 refuelling stations located in seven cities. In 2012 Fortune Oil supplied over 35.3 million cubic metres of CNG to refuel buses and taxis representing an increase of 22 per cent (2011: 28.8 million cubic meters). Shanxi CUCBM commenced operation of the Changzhi retail station which will sell CBM gas to refuel natural gas vehicles. The rapid expansion in the use of natural gas as a fuel for the transportation sector provides Fortune Oil an opportunity to invest in vehicle refuelling stations to supply natural gas to these vehicles.

Fortune Oil has installed two LNG refuelling stations on the route between Fushun and Shenyang to refuel a fleet of thirty LNG inter-city buses. Negotiations are underway to supply LNG fuel on the inter city bus routes between Shenyang, Liaoyang and Chaoyang across Liaoning province.

Fortune Gas has also established a joint venture in Quyang, Hebei province which will develop the city gas infrastructure and also install LNG refuelling stations along the key highway in the area. This route carries a large volume of coal through the province and the operators are looking to switch to LNG fuel to reduce their fuel costs. The initial phase will involve building five LNG stations along the main highway.

As we expect demand for LNG as a fuel for the transport sector in China to continue to grow we will continue to evaluate opportunities to increase our exposure to this market. First mover advantage will enable Fortune Oil together with our collaboration with CGH to capture the prime refuelling site locations for these vehicles.

In our joint venture to bring natural gas as a fuel for ships on the Yangtze River, the first dual fuel ship successfully completed the required river trials and we obtained the first full licence for a commercial dual fuel ship of its kind from the Chinese authorities. This will enable the start of the full scale commercialisation of this technology. The sites for the first two permanent LNG ship refuelling stations have been identified and Chinese design institutes are progressing the design and approvals prior to construction. These are the first of a number of stations Fortune Gas is planning to build along the Yangtze River. Other major companies including the major state owned companies are also planning to develop LNG refuelling for ships so first mover advantage is critical to access the prime refuelling locations along the river front.

Negotiations are progressing with a leading shipping company to commence conversion of its ships to dual fuel technology and the LNG fuel supply arrangements for these ships. Fortune Oil is uniquely placed to expand its LNG operations and develop a major, high margin and sustainable business in the important rapidly expanding gas market in China. Other provinces across China are also looking to introduce LNG ships and Fortune Oil is pursuing a number of potential opportunities.

20 Fortune Oil PLC annual report 2012

business review

Hrazdan, Armenia

RESOURCES

Fortune Oil is pursuing overseas investment opportunities to capitalise on China’s growing demand for energy and resources.

As its first move into resources Fortune Oil acquired a 77.34 per cent effective interest in three Armenian iron ore mining and exploration licenses. Fortune Oil completed a drilling programme and assay test work on the first of these, the Hrazdan mine, to develop the optimised pit design and mining plan. SRK Consulting (UK) completed the mining plan and has issued the JORC compliant Mineral Resource Statement for the Hrazdan iron ore mine. The Resource Statement confirmed a total Resource of 21.4 million tonnes consisting of an Indicated Mineral Resource of 17.3 million tonnes at an average iron ore grade of 26.0 per cent and an Inferred Mineral Resource of 4.1 million tonnes at an average iron ore grade of 29.4 per cent.

Design work has continued for a 2.5 million tonnes per annum iron ore concentration plant producing in excess of 590,000 tonnes of concentrate of approximately 66 to 68 per cent iron.

Design work has continued for a 2.5 million tonnes per annum iron ore concentration plant producing in excess of 590,000 tonnes of concentrate of approximately 66 to 68 per cent iron. Sinosteel completed the feasibility study including the flow sheet, preliminary design for the iron ore processing plant. Our in-house technical team are optimising the process design, tailings dam and waste rock site with a view to determining the viability of developing the Hrazdan mine by the end of 2013. Fortune Oil is in negotiations with a number of potential customers for the iron ore off-take from the Hrazdan mine including customer evaluations to ensure the product from the planned facility meets the customer requirements.

Fortune Oil is actively engaging and has had constructive dialogue with the local environmental groups and non-government organisations to address their concerns in relation to the mining development. Fortune Oil will continue to work closely with these organisations and the local communities throughout the project development.

21 Fortune Oil PLC annual report 2012

business review

Corporate social responsibility is at the cornerstone of all of our activities.

CORPORATE SOCIAL RESPONSIBILITY

Our EmployeesFortune Oil employed around 2,000 people in 2012, over 99 per cent of whom are citizens of the PRC. Our people are recruited, trained and recompensed according to our employment policy of attracting, developing and retaining talented people and to provide attractive long term career prospects for our employees. We have a long standing commitment to create a culture that embraces diversity and fosters inclusion. Our goal is to provide equal opportunities, career development, promotion, training and reward for all employees including those with disabilities.

All senior management of the Company are required to adhere to the Company’s code of ethics in relation to areas such as supervisory rules, insider dealing, market malpractices, whistle blowing policy, conflicts of interest, proper use of the Company’s assets and reporting requirements for listed companies. The Company ensures that all its staff follow internationally recognised governance practices in its business dealings and if staff break these rules they will face disciplinary action up to and including termination of employment. There is also a process that enables employees to report any breaches of our Company’s code of ethics confidentially.

Our CommunityThe Company’s operations are currently principally in the PRC although the Resources business has activities in Armenia. We ensure that the Company’s operations are in compliance with national and local laws and practices. Our ongoing success relies on the maintenance of excellent relationships and trust of the communities where we operate.

Fortune Oil has a proven track record of safe and reliable operation. The Company remains one of the few international companies with both oil and gas operations based onshore in China. Many of the Company’s businesses are amongst the largest foreign-invested enterprises in that area and they provide a benchmark for other local companies. As part of their social responsibility programmes in China, our companies support community activities and provide training to customers regarding the safe use of fuels. We also interact with local and national government and associations to further the development of better policies. The Company follows the same principles and practices as it develops operations elsewhere in the world.

Health and SafetyWe consider the safety of our staff and the communities that we operate in as our top priority. We manage safety risk across our businesses through rigorous controls and compliance systems combined with a safety-focused culture. We regularly inspect, test and maintain our facilities to ensure they are meeting our standards. We continue to

build our safety culture among our employees and contractors. We expect everyone working for us to intervene and stop activities that may be unsafe. We expect employees to comply with our safety regulations and if any employees break these rules they will face disciplinary action up to and including termination of employment.

In 2012 there were no Lost Time Injuries or fatal accidents in the Company’s subsidiaries (where we have operational control).

Environmental PolicyFortune Oil has a policy of minimising the impact of its operations on the environment. We aim to apply best industry practices wherever we operate to improve environmental performance and to foster close relationships with the local community. The requirements of our environmental and sustainability policy are incorporated through the planning, operations and closure of projects and this will also cover the new Resources developments outside of China.

Oil and Gas EmissionsOur primary environmental focus is to prevent the release of hydrocarbons, whether they occur through leaks in pipelines, spills or leaks during transfers, the venting of tanks or tank overflows. Fortune Oil has clear requirements and procedures to prevent spills and programmes in place to maintain and improve our facilities and pipelines to reduce the risk of any potential leak or spill. We have a number of recovery methods in place to minimise the impact in the event of any spill or release. In 2012 there were no significant spills or releases from our operations.

22 Fortune Oil PLC annual report 2012

business review

Finding, producing and distributing the gas to serve our customers.

Drilling for gas in Liulin next to the Yellow River.

Climate ChangeThe Group’s direct emissions of greenhouse gases are small, mainly being methane releases when equipment is maintained, flaring of gas from our Liulin wells (as required under NDRC guidelines for reserves certification), the combustion of gas for power production and the use of diesel and gasoline for vehicles.

Fortune Oil was one of the first operating companies in the oil and gas sector in China to measure its own emissions with the aim of bringing about awareness among staff and customers of the importance of minimising emissions, and increase the efficiency of our operations.

Equity Share of EmissionsThese are categorised in accordance with UK government (DEFRA) guidelines and the 2006 Intergovernmental Panel on Climate Change (“IPCC”) Guidelines for National Greenhouse Gas Emissions and exclude secondary emissions by customers through utilisation of our fuels:

2012 2011

Methane to Air (tonnes) 75.0 78.2Greenhouse Gases to Air (tonnes CO2 equivalent) 14,498 9,298Local Air Quality pollutants (such as NOx, SOx) Negligible NegligibleVolatile Organic Compounds to Air (tonnes) 125 129Smog Precursors (such as particulates) Negligible NegligibleChemical Waste Negligible NegligibleMetals Emissions Negligible Negligible

The increase in greenhouse gas emissions to air (14,498 tonnes CO2 equivaler) is associated with flaring at the Liulin CBM project. FLG is managing the flowing rate and dewatering of the wells to minimise greenhouse gas emissions.

Other Environmental ImpactsAvailability of water in China is an area of increasing environmental concern. The Group’s operations’ use of water is primarily for office use and cleaning vehicles. Fortune’s CBM development programme has consent levels for its water discharge from the CBM wells and the discharge is monitored to ensure we remain within the consents. We also recycle water in these operations to minimise water use.

23 Fortune Oil PLC annual report 2012

business review

GLOSSARY

bcmBillion cubic metres (1,000,000,000 m3), when converted to normal conditions of 0.1 MPa (Mega Pascal) pressure and 20 degrees Celsius temperature.

CBMCoal Bed Methane, refers to methane deposits in coal seams. CBM is generated during coal formation and adsorbed in the natural fracture surfaces in coal. CBM can be extracted by drilling prior to coal mining and can normally be utilised as natural gas (commonly referred to as an unconventional source of gas).

CMMCoal Mine Methane which is extracted during coal mining operations. It has a lower methane content than CBM because of air ingress.

Coal Seam Gas Methane gas trapped in coal seams, which may be extracted as CBM or CMM.

CNGCompressed Natural Gas, gas which has been compressed to between 4 MPa and 25 MPa of pressure, and is transported in tanks as a gas.

CO2 equivalentThe quantity of greenhouse gases emitted in million tonnes, when expressed as though it was carbon dioxide (CO2), so as to indicate the potential impact on global warming.

CUCBMChina United Coalbed Methane Corporation Ltd, the principal PRC government entity responsible for entering into PSCs with foreign companies for development of CBM fields.

dwtDead-weight tonnage, the carrying capacity of a ship.

Gas“Natural gas” for domestic supply contains over 90 per cent methane (CH4). Conventional gas is sourced from petroleum gas fields but the same quality gas could also come from unconventional sources such as coal bed methane.

GDPGross Domestic Product.

HSEHealth, Safety and Environment.

HydrocarbonsOrganic compounds sourced from crude oil or gas

JORCJoint Ore Reserves Committee of the Australasian Institute of Mining and Metallurgy, Australian Institute of Geoscientists and Minerals Council of Australia. The JORC code is an internationally recognised reporting code as defined by the Combined Reserves International Reporting Standards Committee.

KPIKey Performance Indicator, a measure of the Company’s performance.

LNGLiquefied Natural Gas, gas which has been liquefied by cooling to approximately 160 degrees Celsius below zero, and is transported in tanks as a liquid.

LPGLiquefied Petroleum Gas, a mixture of propane and butane (whereas natural gas is mostly methane). Supplied to customers under pressure in bottles as a liquid or via a pipeline network as a gas, sometimes mixed with air.

LTIFRLost Time Injury Frequency Rate. An LTI is any work-related injury or illness which prevents a person working the following day. Calculated as LTIs per million working hours.

m m3/aMillion cubic metres per year, when converted to normal conditions of 0.1 MPa (Mega Pascal) pressure and 20 degrees Celsius temperature.

NDRCNational Development and Reform Commission, the principal government entity in China for economic and energy policy.

ODPOverall Development Programme for an oil & gas field.

PRCThe People’s Republic of China.

PSCProduction Sharing Contract, an agreement between the government and a foreign company for exploration and development of a natural resource block.

RMB/m3

Renminbi per normal cubic metre of gas.

SPMSingle Point Mooring buoy, which allows an oil tanker to moor at its bow and through which oil is discharged to a sub-sea pipeline. The MKM subsidiary operates the only SPM in China for import of crude oil.

24 Fortune Oil PLC annual report 2012

principal risks and uncertainties, their effects and our management strategy

Our business is supplying China with energy and resources, principally oil and natural gas. We face many risks and whilst we can manage some, we have to accept others as part of doing business. We face the usual economic risks – prices, interest rates, supply and demand for the products we produce and deliver which we cannot control. Outlined below are the principal risk factors that may affect the Group’s business. Any of these risks, as well as the other risks and uncertainties discussed in this document, could have a material adverse effect on the business. In addition, the risks set out below may not be exhaustive, and additional risks and uncertainties may arise or become material in the future including those associated with achieving completion of the CGH transaction and the Maoming SPM cooperation.

Concentration riskOur principal assets and operations are located in China and we sell all our products and services to China. Any adverse change in the economic or political environment in China would seriously affect the profitability and possibly viability of our entire business. We seek, through maintaining high level contacts and through providing high quality services, to minimise any adverse consequences.

Pricing risksOur business sells products where we have little or no control over the price we achieve. The price we pay for product we on-sell is also largely out of our control. The interest rate we pay for debt and the interest we receive on surplus cash, and the exchange rates applying to transactions where we need to exchange currencies, are all set by international markets or by governmental regulation. Adverse movements in prices, interest rates or exchange rates can result in actual losses on transactions, increased costs or decreased revenues or losses on translation into our reporting currency. We seek to mitigate the effects of these risks through management of stocks of product in storage or transit, through currency matching of the costs of products sold to revenue produced and through holding cash in the currencies where expenditure is expected. We do not carry out hedging transactions in respect of these risks.

Regulatory and relationships risksThe energy sector in China is subject to a variety of regulatory regimes covering many of the Group’s operations, both at the national and local government levels. The regulatory environment continues to evolve but includes restrictions on foreign ownership and participation in certain activities; land use and industry permitting; and

health, safety and environmental obligations. Our operations are often carried out in joint ventures or through associated companies or, through production sharing contracts (PSC), or under mining and exploration licences, or rely on medium term and long term supply agreements with State owned enterprises. If regulations change, or we or our partners fail to abide by regulations or meet the requirements of PSC, or mining and explanation licences or supply agreements, then we may lose rights or suffer fines or other penalties. Our management aims to be aware of any prospective changes in regulation and to ensure we comply, and to seeks to maintain a positive and constructive working relationship with our partners and with State owned companies so that decisions can be taken together to ensure compliancy with regulation and PSC and supply agreements.

A significant proportion of our business is conducted through joint ventures or investment arrangements where we do not have board control or control of day-to-day operations. We are therefore dependent upon the decision making processes and internal controls, put in place by our investment partners and operated by the staff of the joint ventures or investments. If incorrect business decisions are taken or, through lack or overriding of internal controls, assets and/or revenues are lost, the value of and income from such joint ventures and investments may be materially reduced. We seek through involvement in these decision making processes, using our rights to appoint directors and/or managers, monitoring the results of internal controls, and using our rights to access trading information to reduce the risk associated with such non-controlled joint ventures and investment structures.

Health, Safety and the Environment (HSE)The Group operates facilities in the oil and gas industry where there is an inherent risk of accidents that may harm employees, assets, the community or the environment. Such accidents may have an adverse impact on the ongoing operations, revenues and profits of the Group. We seek through the Group’s HSE policies to observe all local and national legal and regulatory requirements. We also carry out pre-project and regular review risk assessments to ensure where possible that processes and procedures are in place to reduce and manage such incidents.