Embed Size (px)

Citation preview

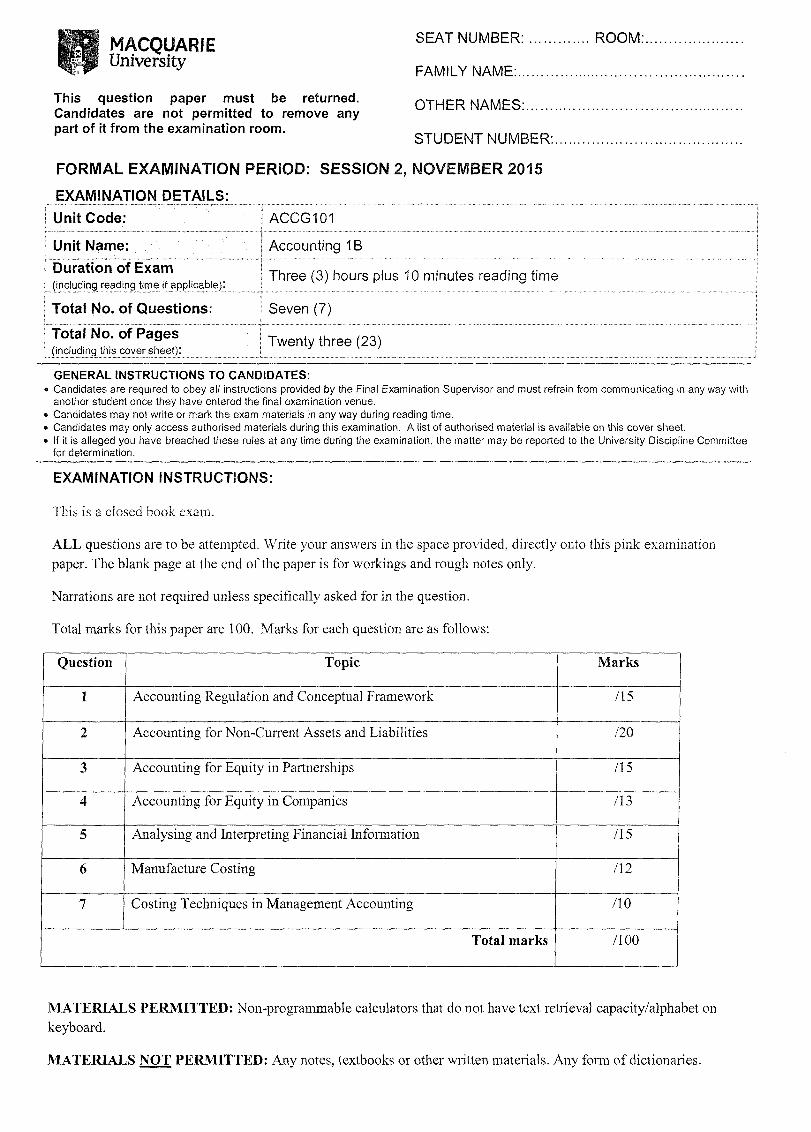

ROOM:MACQUARIEUniversity

SEAT NUMBER:

FAMILY NAME:..

This question paper must be returned. Candidates are not permitted to remove any part of it from the examination room.

OTHER NAMES:......

STUDENT NUMBER:

FORMAL EXAMINATION PERIOD: SESSION 2, NOVEMBER 2015

EXAMINATION DETAILS:Unit Code; ACCG101

Unit Name: Accounting 1BDuration of Exam(including reading time if applicable):

Three (3) hours plus 10 minutes reading time

Total No. of Questions: Seven (7)

Total No. of Pages(including this cover sheet):

Twenty three (23)

GENERAL INSTRUCTIONS TO CANDIDATES:• Candidates are required to obey all instructions provided by the Final Examination Supervisor and must refrain from communicating in any way with

another student once they have entered the final examination venue.• Candidates may not write or mark the exam materials in any way during reading time,• Candidates may only access authorised materials during this examination. A list of authorised material is available on this cover sheet.• If it is alleged you have breached these rules at any time during the examination, the matter may be reported to the University Discipline Committee

for determination.

EXAMINATION INSTRUCTIONS:

This is a closed book exam.

ALL questions are to be attempted. Write your answers in the space provided, directly onto this pink examination paper. The blank page at the end of the paper is for workings and rough notes only.

Narrations are not required unless specifically asked for in the question.

Total marks for this paper are 100. Marks for each question are as follows:

Question Topic Marks

1 Accounting Regulation and Conceptual Framework /15

2 Accounting for Non-Current Assets and Liabilities /20

3 Accounting for Equity in Partnerships /15

4 Accounting for Equity in Companies /13

5 Analysing and Interpreting Financial Information /15

6 Manufacture Costing HI

7 Costing Techniques in Management Accounting /10

Total marks /100

MATERIALS PERMITTED: Non-programmable calculators that do not have text retrieval capacity/alphabet on keyboard.

MATERIALS NOT PERMITTED: Any notes, textbooks or other written materials. Any form of dictionaries.

QUESTION 1: ACCOUNTING REGULATION & CONCEPTUAL FRAMEWORK (15 MARKS)

Part A (5 Marks)

1. Explain the two (2) main objectives of General Purpose Financial Reporting. (4 marks)2. Who are General Purpose Financial Reports prepared for? (1 mark)

Part B (4 Marks)

List four (4) of the concepts/ guidance within the Conceptual Framework that support the development of accounting standards.

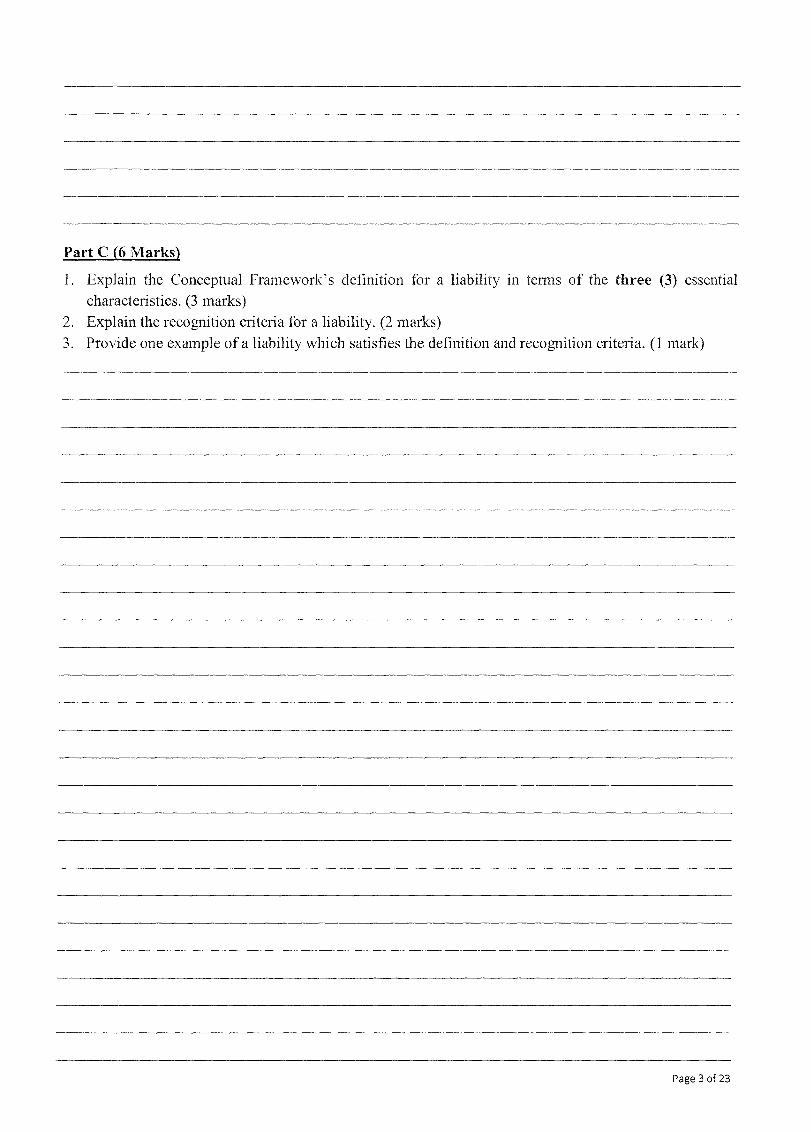

Page 2 of 23

1. Explain the Conceptual Framework’s definition for a liability in terms of the three (3) essential characteristics. (3 marks)

2. Explain the recognition criteria for a liability. (2 marks)3. Provide one example of a liability which satisfies the definition and recognition criteria. (1 mark)

Part C (6 Marks)

Page 3 of 23

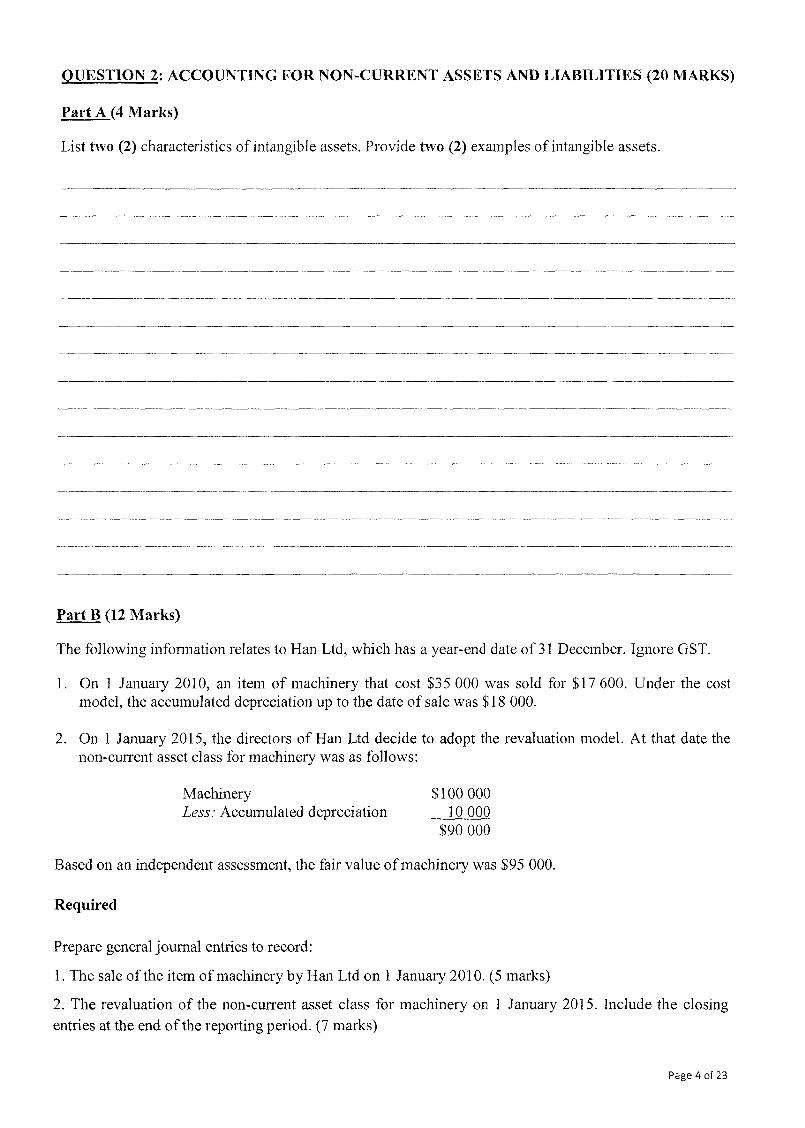

QUESTION 2: ACCOUNTING FOR NON-CURRENT ASSETS AND LIABILITIES (20 MARKS)

List two (2) characteristics of intangible assets. Provide two (2) examples of intangible assets.

Part A (4 Marks)

Part B (12 Marks)

The following information relates to Han Ltd, which has a year-end date of 31 December. Ignore GST.

1. On 1 January 2010, an item of machinery that cost $35 000 was sold for $17 600. Under the cost model, the accumulated depreciation up to the date of sale was $ 18 000.

2. On 1 January 2015, the directors of Han Ltd decide to adopt the revaluation model. At that date the non-current asset class for machinery was as follows:

Machinery $100 000Less: Accumulated depreciation 10 000

$90 000

Based on an independent assessment, the fair value of machinery was $95 000.

Required

Prepare general journal entries to record:

1. The sale of the item of machinery by Han Ltd on 1 January 2010. (5 marks)

2. The revaluation of the non-current asset class for machinery on 1 January 2015. Include the closing entries at the end of the reporting period. (7 marks)

Page 4 of 23

General JournalDR

$CR

$

_

Page 5 of 23

Fart C (4 Marks)

GL Ltd manufactures ovens. As at 30 June 2015:

1. The Provision for Warranties needs to be adjusted so that it equals 10% of sales for the year ended on

that date. Sales for the year ended 30 June 2015 were $1 250 000 and the Provision for Warranties

before the adjustment was $25 000.

2. Payment of $3 500 needs to be made to a customer on a successful warranty claim.

Required

Prepare the general journal entry to:

1. adjust the Provision for Warranties to the required level. (2 marks)

2. record the payment of the successful warranty claim. (2 marks)

General JournalDR

$CR

$

Page 6 of 23

QUESTION 3: ACCOUNTING FOR EQUITY IN PARTNERSHIPS (15 MARKS)

Part A (4 Marks)Explain the purposes of the partnership agreement and the Partnership Act. Explain why it is advisable to prepare a partnership agreement when fonning a partnership, even though the Partnership Act exists.

Page 7 of 23

Part B (11 Marks)On 1 July 2014, Cassie and Zane fonned a partnership, C&Z.

Some business assets and liabilities of Cassie were assumed by the partnership, and these are listed below at both carrying amounts and fair value.

Carrying amount Fair valueCash at Bank $ 28 000 $ 28 000Accounts Receivable 47 000 47 000Inventory 146 600 152 200Equipment 38 500 230 000Accounts Payable 36 000 36 000

Zane contributed a building and land with fair values of $820 000 and $350 000, respectively, and a $456 000 mortgage, which was taken over by the partnership.

During the first year of the partnership, Cassie invested an additional $60 000 in the business and made drawings of $45 000. Zane invested an additional $ 115 200 and made drawings of $ 17 200. The partnership had a profit of $88 460. Cassie and Zane agreed to share profits in the ratio of 1:2.

Required

1. Prepare the journal entries to record the initial investments of both partners. Ignore GST. (5 marks)

2. Prepare a Statement of Changes in Partners' Equity for C&Z for the year ended 30 June 2015.Retained Earnings accounts are not used. (6 marks)

1. General JournalDR

$CR$

Page 8 of 23

2.

Page 9 of 23

QUESTION 4: ACCOUNTING FOR EQUITY IN COMPANIES (13 MARKS)

Part A (9 Marks)

On 1 April 2015, Paprika Ltd was incorporated and a prospectus was issued inviting applications for 200 000 shares, at an issue price of $20, payable $10 on application, $5 on allotment and the remainder in one call when required.

By 30 April, applications for 240 000 shares had been received together with the application money due on each share. One applicant for 5 000 shares had forwarded $100 000 in full payment of the shares. The remaining applicants only paid the application price.

On 3 May, the directors proceeded to allot 200 000 shares on the following basis. 5 000 shares were allotted to the applicant who paid for the shares in full. The other applicants were allotted the remaining shares. The surplus application money was offset against the amount payable on allotment. The balance of the allotment money was received by 10 May.

On 3 September, the remaining call on the shares was made, and all cash was received on the call by 15 October, except for 20 000 shares.

Required

Prepare journal entries to record the transactions for the period from 1 April 2015 to 15 October 2015.

General JournalDR

$CR$

Page 10 of 23

General JournalDR

$CR

$

Page 11 of 23

Explain four (4) attributes of a company, comparing to a sole trader or partnership.

Part B (4 Marks)

Page 12 of 23

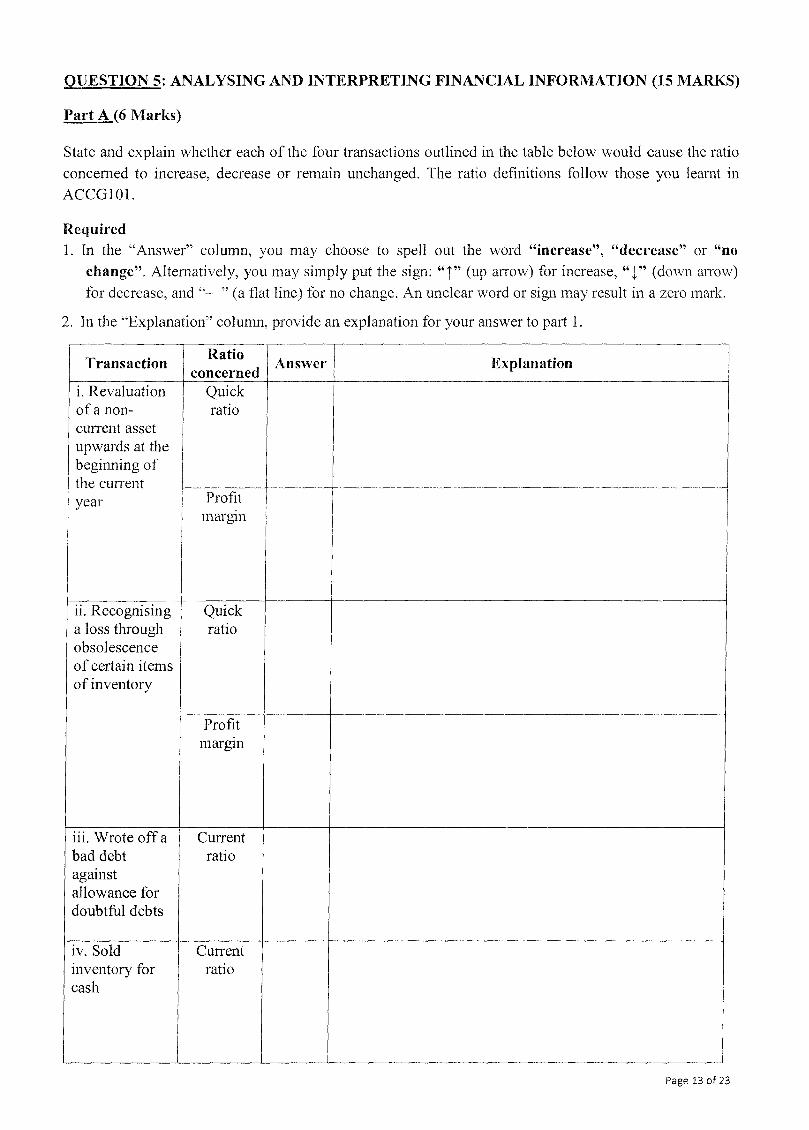

QUESTION 5: ANALYSING AND INTERPRETING FINANCIAL INFORMATION (15 MARKS)

Part A (6 Marks)

State and explain whether each of the four transactions outlined in the table below would cause the ratio concerned to increase, decrease or remain unchanged. The ratio definitions follow those you learnt in ACCG101.

Required1. In the “Answer” column, you may choose to spell out the word “increase”, “decrease” or “no

change”. Alternatively, you may simply put the sign: “|” (up arrow) for increase, “f” (down arrow) for decrease, and “—” (a flat line) for no change. An unclear word or sign may result in a zero mark.

2. In the “Explanation” column, provide an explanation for your answer to part 1.

Transaction Ratioconcerned Answer Explanation

i. Revaluation of a noncurrent asset upwards at the beginning of the current year

Quickratio

Profitmargin

ii. Recognising a loss through obsolescence of certain items of inventory

Quickratio

Profitmargin

iii. Wrote off a bad debt against allowance for doubtful debts

Currentratio

iv. Sold inventory for cash

Currentratio

Page 13 of 23

Part B (4 Marks)

After calculating the current ratio for an entity and finding that the ratio’s value was 1.5:1, a student analyst decided that the company was in a sound position to pay its current liabilities.

Required

Discuss the shortcomings of making such a conclusion by providing at least three (3) factors, which may be considered in analysing the entity’s liquidity position.

Page 14 of 23

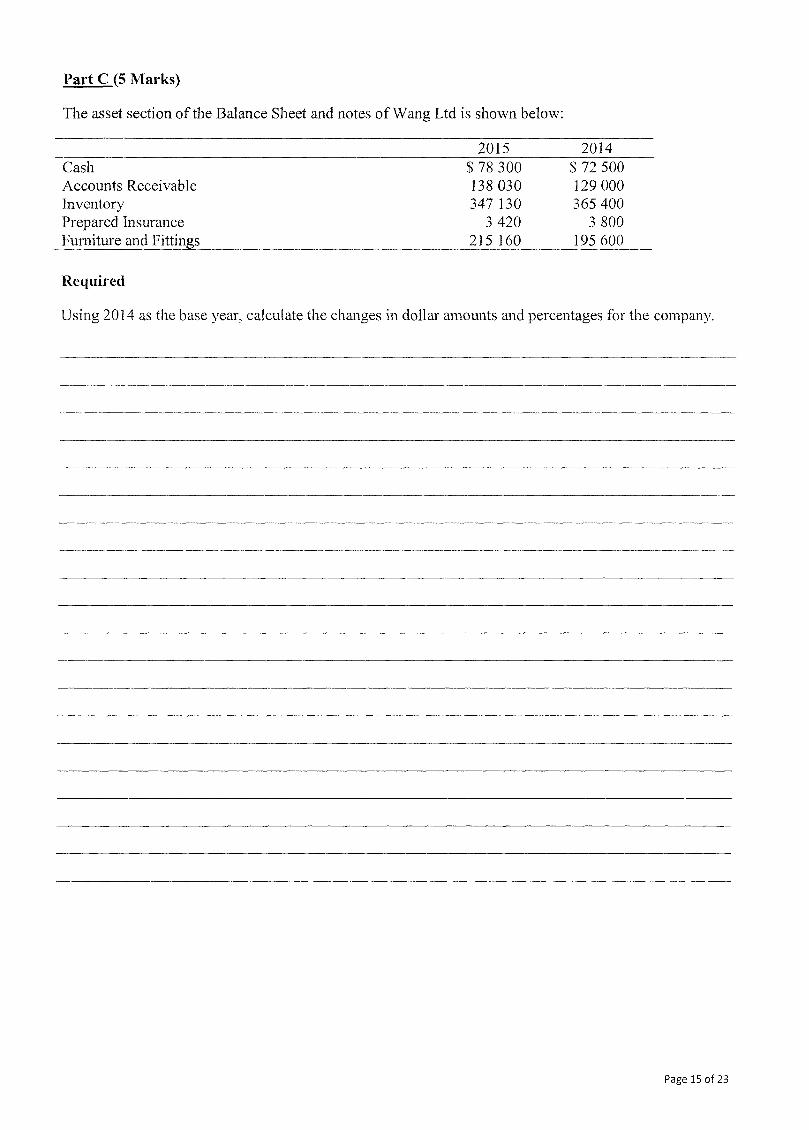

Part C (5 Marks)

The asset section of the Balance Sheet and notes of Wang Ltd is shown below:

2015 2014Cash $ 78 300 $ 72 500Accounts Receivable 138 030 129 000Inventory 347 130 365 400Prepared Insurance 3 420 3 800Furniture and Fittings 215 160 195 600

Required

Using 2014 as the base year, calculate the changes in dollar amounts and percentages for the company.

Page 15 of 23

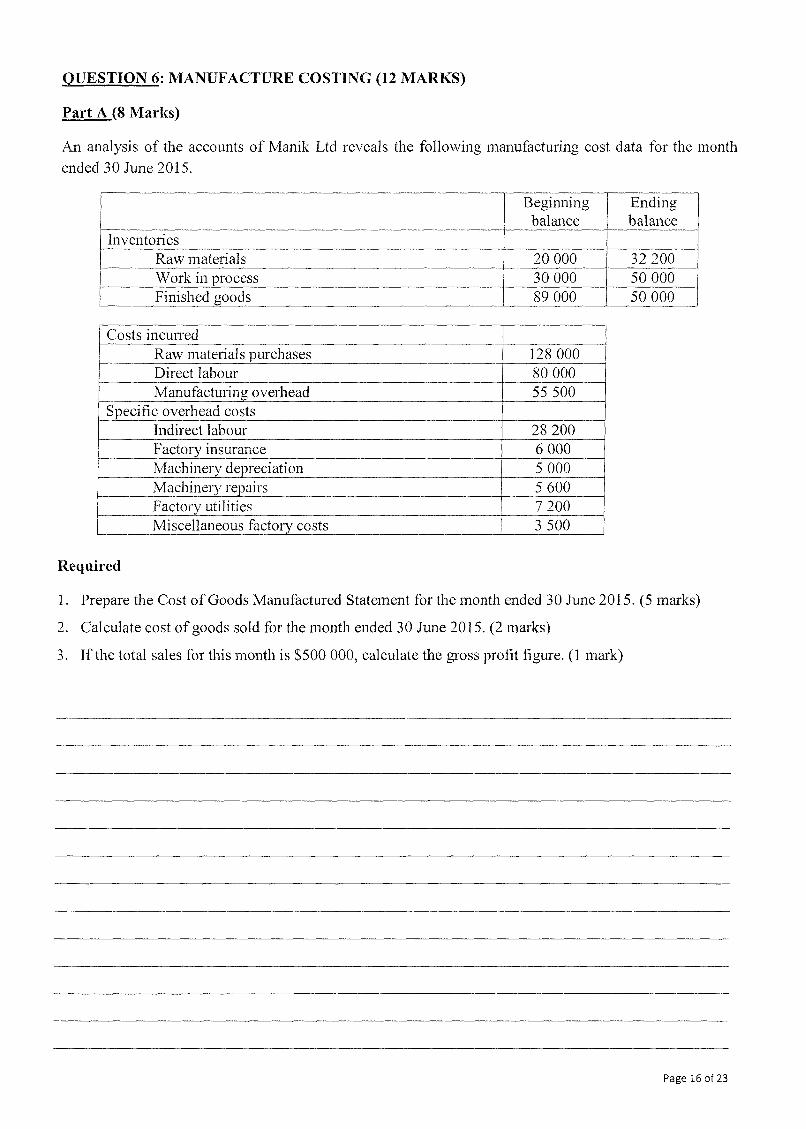

QUESTION 6: MANUFACTURE COSTING (12 MARKS)

Part A (8 Marks)

An analysis of the accounts of Manik Ltd reveals the following manufacturing cost data for the month ended 30 June 2015.

Beginningbalance

Endingbalance

InventoriesRaw materials 20 000 32 200Work in process 30 000 50 000Finished goods 89 000 50 000

Costs incurredRaw materials purchases 128 000Direct labour 80 000Manufacturing overhead 55 500

Specific overhead costsIndirect labour 28 200Factory insurance 6 000Machinery depreciation 5 000Machinery repairs 5 600Factory utilities 7 200Miscellaneous factory costs 3 500

Required

1. Prepare the Cost of Goods Manufactured Statement for the month ended 30 June 2015. (5 marks)

2. Calculate cost of goods sold for the month ended 30 June 2015. (2 marks)

3. If the total sales for this month is $500 000, calculate the gross profit figure. (1 mark)

Page 16 of 23

Page 17 of 23

Page 18 of 23

Part B (4 Marks)

Explain the difference between product and period costs. Is labour cost a period cost, a product cost, or can it be both? Explain your answer.

Page 19 of 23

QUESTION 7: COSTING TECHNIQUES IN MANAGEMENT ACCOUNTING (10 MARKS)

Part A (7 Marks)

University Pizza delivers pizzas to the residential colleges and flats near a major university. The company’s annual fixed costs are $70 000. The sales price of a pizza is $12, and it costs the company $5 to make and deliver each pizza.

Required

1. Calculate the break-even point in units (pizzas) and in sales dollars. (2 marks)

2. What is the contribution margin ratio? (1 mark)

3. How many pizzas must the company sell to earn a target net profit of $70 000? (1 mark)

Page 20 of 23

4. The sales manager believes that a reduction in the sales price of a pizza to $ 10 will result in orders for 3 000 more pizzas each year. What will the break-even point in units be if the sales price is changed? Should the sales price change be made? Explain your answer (2 marks)

5. What will the new break-even point in units be if annual fixed costs increase by 10 percent? (assuming the sales price of a pizza is still $12, and it costs the company $5 to make and deliver each pizza) (1 mark)

Page 21 of 23

Part B (3 Marks)

Explain cost estimation, cost behaviour, cost prediction and then their relationship.

ADDITIONAL WORKING PAPER

(This will NOT be marked)

Page 23 of 23

![Optical filtering properties of inhomogeneous isotropic ...asatid.tabrizu.ac.ir/PDF/637_0c4903b8-4a89-4f25-a... · [4–7]. The optical layered media can be divided into two groups](https://img.pdfslide.us/doc/110x75/5f935f7aabeb684e7251d88b/optical-iltering-properties-of-inhomogeneous-isotropic-4a7-the-optical.jpg)