Embed Size (px)

Citation preview

4/18/2016

1

Copyright © 2014 Holland & Knight LLP. All Rights Reserved

Form 8971: A Practical Approach to Basis Reporting by Estates

Abigail O’Connor, Holland & Knight LLP

Florida Bar Tax Section April 20, 2016

Brief Outline

»New, New, New, and New

»The Crawley Estate

»Is 8971 Required?

»Preparing the 8971 Forms

2

WITH SOME SURPRISES THROWN IN

4/18/2016

2

New, New, New, and New

3

New Rules (The Surface Transportation and Veterans Health Care Choice Improvement Act of 2015)

»IRC 1014(f)

»See Supplement A for the actual rule.

» AO paraphrase:

– The basis of property received from a decedent is the value as finallydetermined for estate tax purposes.

– A “final” determination may take a while. Until it is finally determined,use the value reported on IRS Form 8971 Schedule A.

– This rule applies only to property that increases the estate tax liability.

4

4/18/2016

3

»IRC 6035

»See Supplement A for the actual rule.

» AO Paraphrase: If a 706 is required, then the executor also must provideto the beneficiaries the “final” values of the assets that they receive fromthe decedent, and must provide the same information to the IRS.

» The information is shared via IRS Form 8971 (including its Schedule A).

5

P.S. There also were changes to IRC Sections 6662, 6721, 6722, 6724, which apply penalties for failing to comply with the new rules.

New Rules (The Surface Transportation and Veterans Health Care Choice Improvement Act of 2015)

New (Proposed) Regulations

»Proposed Regulation 1.1014(f)-10

» See Supplement A for actual language.

» AO Paraphrase/Highlights:

– Beneficiary's initial basis is the “final” value for estate tax purposes. Post-death adjustments tobasis under other sections of the Code are permitted.

– Assets not subject to consistency rules: assets for which there is a marital or charitablededuction, and tangible personal property for which an appraisal is not required (under $3K invalue).

– If estate tax is due, then consistency rule applies to all assets in estate (other than thosementioned above). If no estate tax is due, then consistency rule does not apply to any assetsin the estate.

6

4/18/2016

4

New (Proposed) Regulations

»Proposed Regulation 1.1014(f)-10

» See Supplement A for actual language.

» AO Paraphrase/Highlights:

– Final value equals:

• if statute of limitations has run without an audit, the 706 value; or

• if the IRS determines a different value and the estate does not contest, then the IRS value;or

• if there is a contest, the value determined by settlement or court order.

– Until the value is “final,” the beneficiary relies on the value shown on the 8971.

7

New (Proposed) Regulations

»Proposed Regulation 1.1014(f)-10

» AO Paraphrase/Highlights Continued…

– Later discovered or omitted property is handled differently based on whether the 706 was filedand whether the statute has run.

• 706 filed

» Statute has not run: file supplemental 706 and final value is determined as usual.

» Statute has run: ZERO BASIS

• 706 not filed

» If the “new” asset yields an estate tax payable, then all assets in gross estate have ZEROBASIS until the value is “finally” determined.

» AO Inference: If the “new” asset does not yield an estate tax payable, then consistencyrules do not apply, so we don’t care.

8

4/18/2016

5

New (Proposed) Regulations

»Proposed Regulation 1.1014(f)-10

» AO Paraphrase/Highlights Continued…

– Executor means the same as in IRC 2203 and includes those required to file a 706 under6018(b).

– Good examples in Regulation.

– Applies for returns filed after 7/31/15.

9

New (Proposed) Regulations

»Proposed Regulation 1.6035-1

»See Supplement A for actual language.

»AO Paraphrase/Highlights:

»If executor is required to file a 706, the IRS Form 8971 is required.

»DON’T COUNT:

»Filing only to preserve portability.

»Filing only for GST exemption allocation.

10

4/18/2016

6

New (Proposed) Regulations

»Proposed Regulation 1.6035-1

»See Supplement A for actual language.

»AO Paraphrase/Highlights:

»All property in gross estate goes on a statement, except:

»(i) cash (other than coin collections or collectibles);

»(ii) IRD;

»(iii) tangible property that did not require an appraisal; and

»(iv) property sold or disposed of by the estate where gain/loss is recognized.

11

New (Proposed) Regulations

»Proposed Regulation 1.6035-1

»AO Paraphrase/Highlights Continued:

»Beneficiary of life estate is life tenant; beneficiary of remainder interest is remainderman; contingent beneficiaries included.

»Beneficiary that is a trust or estate – statement goes to the fiduciary.

»Beneficiary that is an entity – statement goes to the entity.

»If the executor has not decided what property will be used to fund a gift, must list all property that could be used to fund the gift.

»If a beneficiary is nowhere to be found, the executor has to demonstrate efforts to find him or her, and if found, must furnish the statement within 30 days.

12

4/18/2016

7

New (Proposed) Regulations

»Proposed Regulation 1.6035-1

»AO Paraphrase/Highlights Continued:

»Due date:

»If the 706 is due after 7/31/15: due date is earlier of:

»30 days from due date of return (w/extensions); or

»30 days from date return is filed.

»If the 706 is due prior to 7/31/15 but filed afterwards, 30 days from filing.

»Supplemental statements required for changes to values that make prior statement incorrect or incomplete.

»Due date is 30 days from the change; however, if the asset still hasn’t been distributed, 30 days from the distribution.

13

New (Proposed) Regulations

»Proposed Regulation 1.6035-1

»AO Paraphrase/Highlights Continued:

»If a beneficiary transfers an asset to a related transferee, the beneficiary/transferor provides the transferee and the IRS with a supplemental statement within 30 days.

»If before the beneficiary has received the statement from the executor, then the supplemental just reports the change in ownership.

»If after the beneficiary has received the statement from the executor, then the supplemental includes the value.

»If before the value is “final,” then the supplemental also must go to the executor in case there is a change later on.

»Related Transferee: family member under 2704(c)(2), controlled entity within 2701/2704, or a grantor trust.

»Penalties under 6721, 6722, 6724.

14

4/18/2016

8

New Notice

»IRS Notice 2016-27

IRS Forms 8971 that are due prior to June 30, 2016,

are not due until June 30, 2016.

15

New Form

»IRS Form 8971» See Supplement B

» What goes only to IRS:

– Part I: Estate & Executor information

– Part II: Beneficiary Information

» What goes to IRS and beneficiary:

– Schedule A – this is the “statement” that goes to the beneficiary.

– Each beneficiary receives his or her own Schedule A

16

4/18/2016

9

New Form

»Instructions to IRS Form 8971

» See Supplement C – highlighted according to AO’s impressions of really important info

» Includes much of what we find in the Proposed Regulations.

» Interestingly, we round to whole dollars.

» Gives penalties.

» Must give TIN for all beneficiaries (Part II, Column D).

– What about trusts that have not yet been funded?

» If beneficiary cannot be located, cannot give a date on which the 8971 is provided – does that mean the returns is incomplete?

17

Time for an example:The Crawley Estate

18

4/18/2016

10

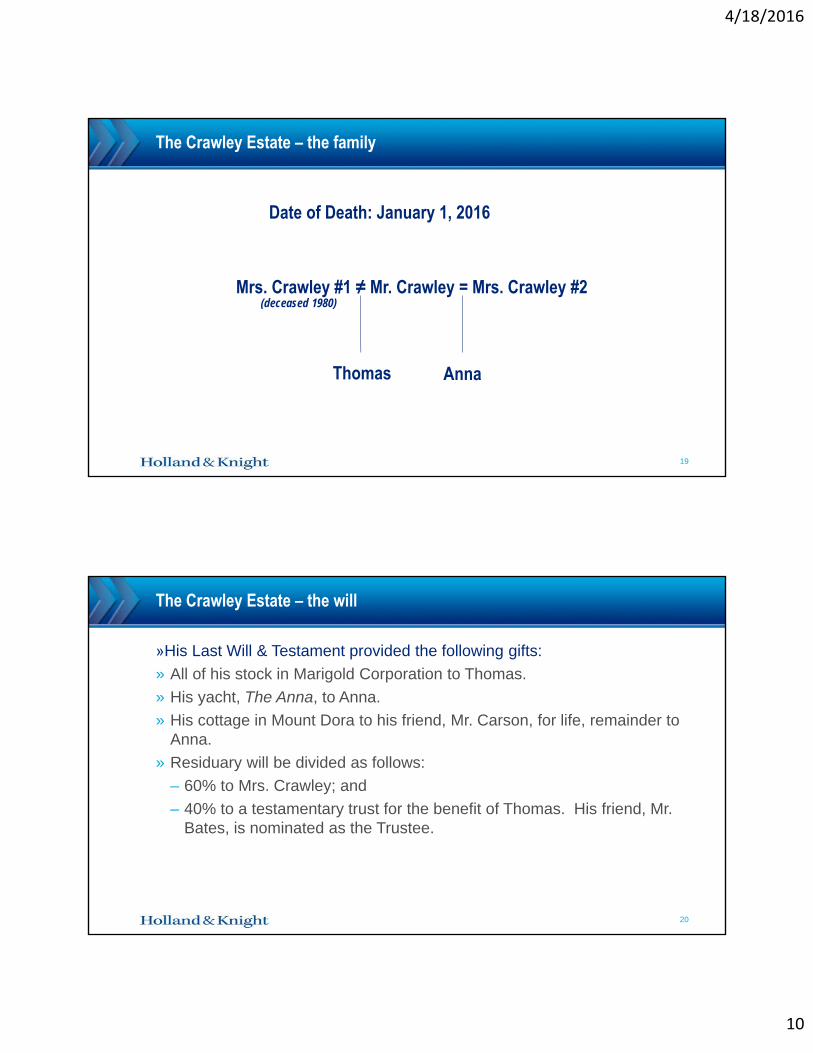

The Crawley Estate – the family

19

Mrs. Crawley #1 ≠ Mr. Crawley = Mrs. Crawley #2(deceased 1980)

Thomas Anna

Date of Death: January 1, 2016

The Crawley Estate – the will

»His Last Will & Testament provided the following gifts:

» All of his stock in Marigold Corporation to Thomas.

» His yacht, The Anna, to Anna.

» His cottage in Mount Dora to his friend, Mr. Carson, for life, remainder to Anna.

» Residuary will be divided as follows:

– 60% to Mrs. Crawley; and

– 40% to a testamentary trust for the benefit of Thomas. His friend, Mr. Bates, is nominated as the Trustee.

20

4/18/2016

11

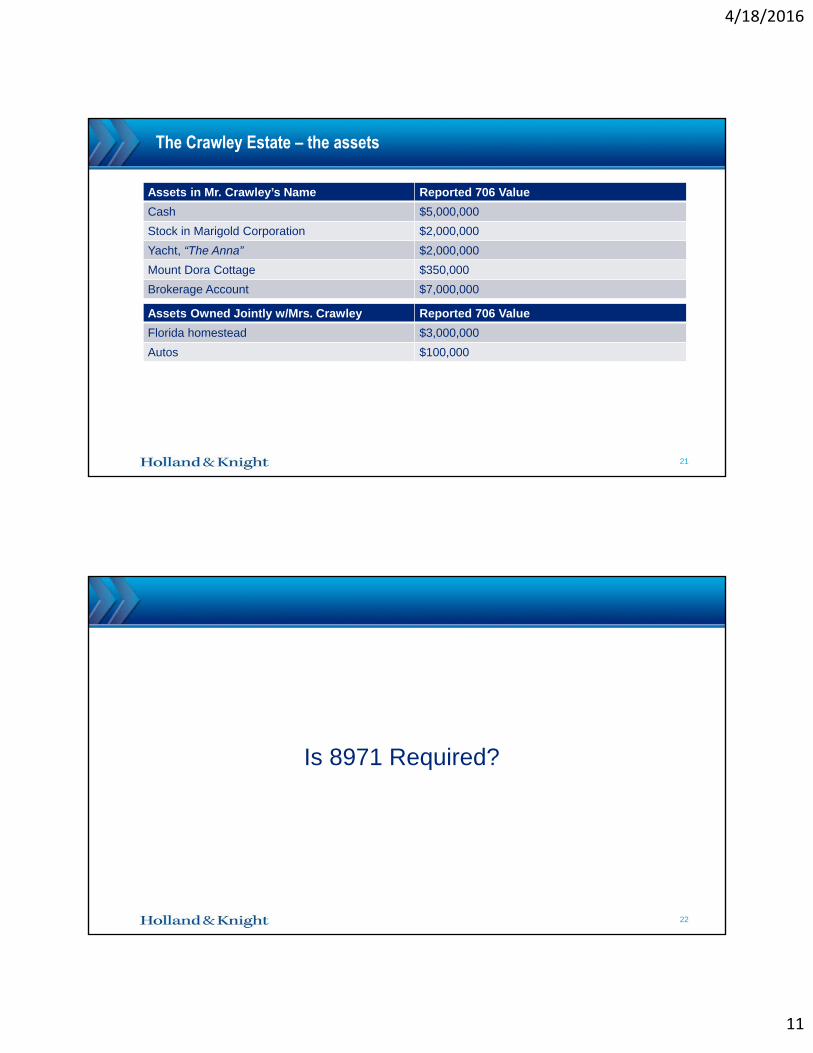

The Crawley Estate – the assets

Assets in Mr. Crawley’s Name Reported 706 ValueCash $5,000,000

Stock in Marigold Corporation $2,000,000

Yacht, “The Anna” $2,000,000

Mount Dora Cottage $350,000

Brokerage Account $7,000,000

21

Assets Owned Jointly w/Mrs. Crawley Reported 706 ValueFlorida homestead $3,000,000

Autos $100,000

Is 8971 Required?

22

4/18/2016

12

Is 8971 Required?

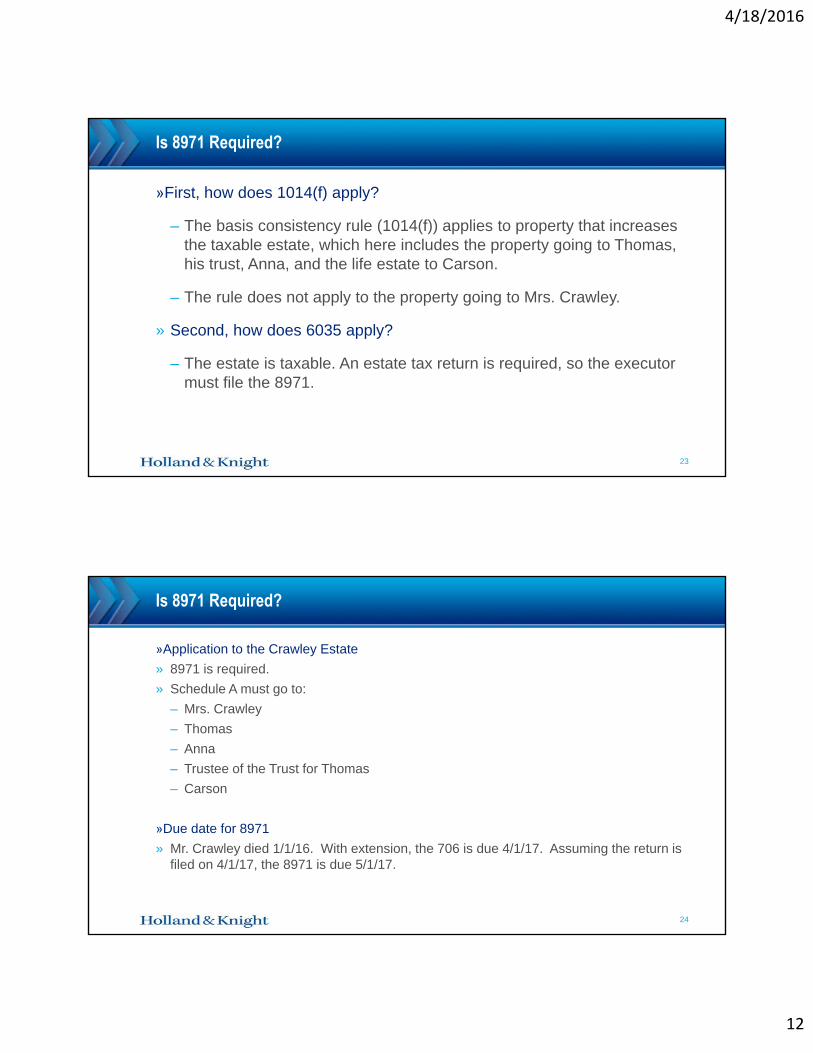

»First, how does 1014(f) apply?

– The basis consistency rule (1014(f)) applies to property that increases the taxable estate, which here includes the property going to Thomas, his trust, Anna, and the life estate to Carson.

– The rule does not apply to the property going to Mrs. Crawley.

» Second, how does 6035 apply?

– The estate is taxable. An estate tax return is required, so the executor must file the 8971.

23

Is 8971 Required?

»Application to the Crawley Estate

» 8971 is required.

» Schedule A must go to:

– Mrs. Crawley

– Thomas

– Anna

– Trustee of the Trust for Thomas

– Carson

»Due date for 8971

» Mr. Crawley died 1/1/16. With extension, the 706 is due 4/1/17. Assuming the return is filed on 4/1/17, the 8971 is due 5/1/17.

24

4/18/2016

13

SURPRISE!

25

SURPRISE!Anna takes off. Nobody knows where to find her.

Executor will have to show efforts to locate Anna.

Once she turns up, statement is due within 30 days.

Perhaps send to last known address, regardless?

Proposed Reg. 1.6035-1(c)(4).

26

4/18/2016

14

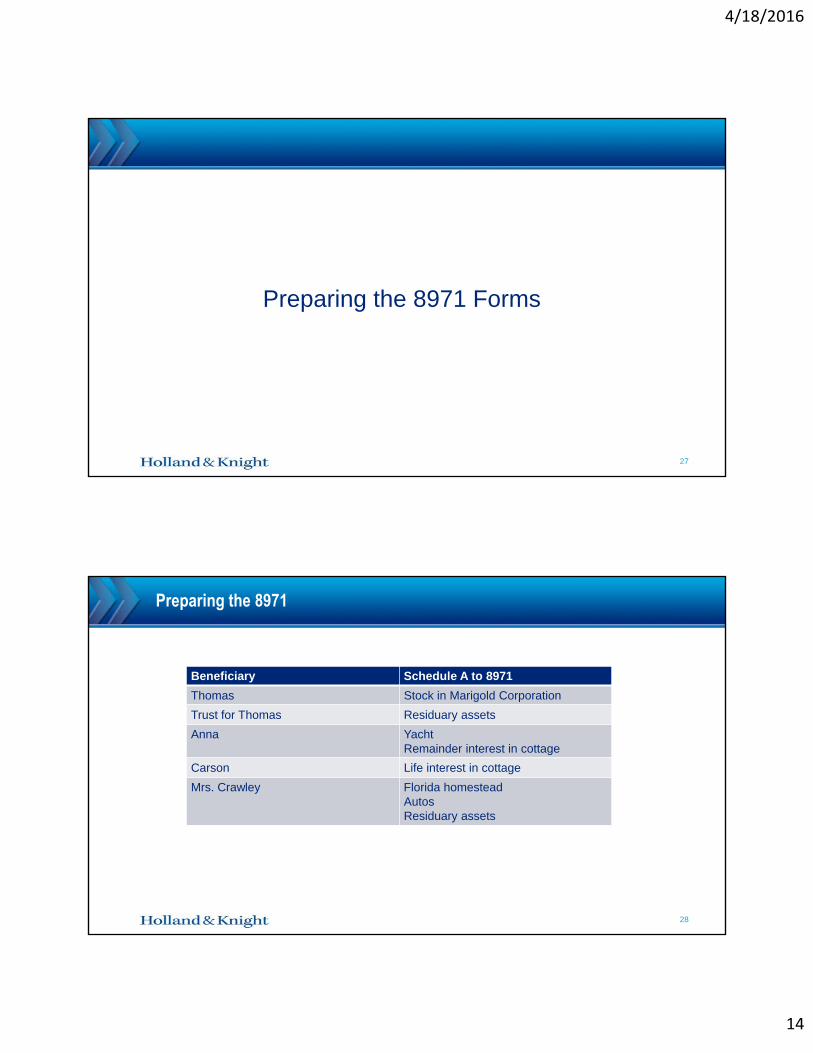

Preparing the 8971 Forms

27

Preparing the 8971

28

Beneficiary Schedule A to 8971Thomas Stock in Marigold Corporation

Trust for Thomas Residuary assets

Anna YachtRemainder interest in cottage

Carson Life interest in cottage

Mrs. Crawley Florida homesteadAutosResiduary assets

4/18/2016

15

Preparing the 8971

Residuary Assets:

Brokerage account?

Cash?

29

Preparing the 8971

GO TO SUPPLEMENT D

30

4/18/2016

16

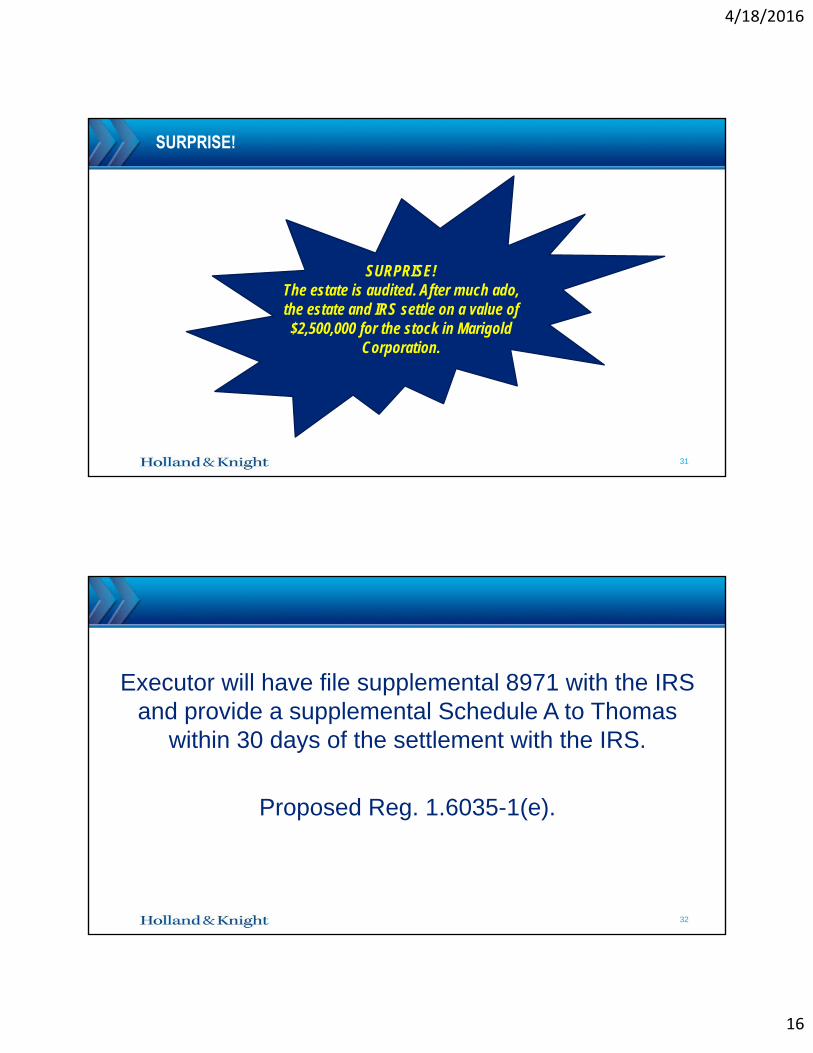

SURPRISE!

31

SURPRISE!The estate is audited. After much ado, the estate and IRS settle on a value of $2,500,000 for the stock in Marigold

Corporation.

Executor will have file supplemental 8971 with the IRS and provide a supplemental Schedule A to Thomas

within 30 days of the settlement with the IRS.

Proposed Reg. 1.6035-1(e).

32

4/18/2016

17

Preparing the 8971 Forms

GO TO SUPPLEMENT E

33

SURPRISE!

34

SURPRISE!The family just learned that Mr. Crawley inherited a

valuable fishing cabin in Alaska shortly before he died.

Value is $500,000.The statute has not yet run.

4/18/2016

18

Executor will file a supplemental 706, and then file supplemental 8971 and provide a supplemental

Schedule A to Mrs. Crawley and the Trust for Thomas within 30 days of the settlement with the IRS.

Proposed Reg. 1.6035-1(c)(3)(i)(A).

35

Preparing the 8971 Forms

GO TO SUPPLEMENT F

36

4/18/2016

19

SURPRISE!

37

SURPRISE!Thomas transfers his stock

in Marigold Corp. to an irrevocable grantor trust for

his wife and children.

Thomas already received his Schedule A (including the supplemental). He must file a form 8971 with the IRS, and give a Schedule A to the recipient trust, reflecting

the value of $2,500,000.

Proposed Reg. 1.6035-1(f).

38

4/18/2016

20

Preparing the 8971

What to tell the executor?Just some possibilities…

» Keep the 8971 and Schedules A.» Ongoing responsibilities until all values are “final.”

» Beneficiaries addresses & contact information» Audits» Potential for supplemental Schedule A» Subsequent transfers to related transferee by

beneficiaries

39

Preparing the 8971

What to tell the beneficiaries?Just some possibilities…

» Keep the Schedule A for their records.

» Share with tax professional.

» “Final” value not yet determined.

» Inclusion of an item on Schedule A does not mean the beneficiary will receive that item.

» Potential for supplemental Schedule A.

» Subsequent transfers to related transferee.

40

4/18/2016

21

Preparing the 8971

What to tell the trustees who acceptnew trusts or new trust property?

» Ask whether any trust property has a corresponding 8971 Schedule A.

» Determine whether values are “final” yet, and if not, advise of possible changes.

41

The End.(Unless there are more subsequent transfers, more

later-discovered property, or Anna shows up.)

Thank you.

42

Abigail O’[email protected]

907-263-6330

![Basis of Reporting · Basis of Reporting 2017 4 LTIFR = MAT [Number of lost time injuries x 200,000] MAT [Hours worked] MAT – Moving Annual Total 3.3 Changes from previous years](https://img.pdfslide.us/doc/110x75/5f82158f87d59c460f08cb40/basis-of-reporting-basis-of-reporting-2017-4-ltifr-mat-number-of-lost-time-injuries.jpg)