Embed Size (px)

Citation preview

United StatesSecurities and Exchange Commission

Washington, D.C. 20549

FORM 10-Q

x Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended March 31, 2005

or

o Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ___________ to ___________

Commission file number 1-8291

GREEN MOUNTAIN POWER CORPORATION

(Exact name of registrant as specified in its charter)

(802) 864-5731 Registrant's telephone number, including area code

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Exchange Act). Yes xNo o

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

Vermont 03-0127430 (State or other jurisdiction ofincorporation or organization

(I.R.S. EmployerIdentification No.)

163 Acorn Lane

Colchester, Vermont(Address of Principal Executive Offices)

05446

(Zip Code)

Class - Common Stock Outstanding at April 22, 2005$3.33 1/3 Par Value 5,179,507

This report contains statements that may be considered forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934. You can identify these statements by forward-looking words such as "may," "could", "should," "would," "intend," "will," "expect," "anticipate," "believe," "estimate," "continue" or similar words. We intend these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Reform Act of 1995 and are including this statement for purposes of complying with these safe harbor provisions. You should read statements that contain these words carefully because they discuss the Company’s future expectations, contain projections of the Company’s future results of operations or financial condition, or state other "forward-looking" information.

There may be events in the future that we are not able to predict accurately or control and that may cause actual results to

differ materially from the expectations described in forward-looking statements. Investors are cautioned that all forward-looking statements involve risks and uncertainties, and actual results may differ materially from those discussed in this document, including the documents incorporated by reference in this document. These differences may be the result of various factors, including changes in general, national, regional, or local economic conditions, changes in fuel or wholesale power supply costs, regulatory or legislative action or decisions, and other risk factors identified from time to time in our periodic filings with the Securities and Exchange Commission.

The factors referred to above include many, but not all, of the factors that could impact the Company’s ability to achieve the

results described in any forward-looking statements. You should not place undue reliance on forward-looking statements. You should be aware that the occurrence of the events described above and elsewhere in this document, including the documents incorporated by reference, could harm the Company’s business, prospects, operating results or financial condition. We do not undertake any obligation to update any forward-looking statements as a result of future events or developments.

AVAILABLE INFORMATION

Our Internet website address is: www.greenmountainpower.biz. We make available free of charge through the website our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after such documents are electronically filed with, or furnished to, the SEC. The information on our website is not, and shall not be deemed to be, a part of this report or incorporated into any other filings we make with the SEC.

2

PART I FINANCIAL INFORMATIONGREEN MOUNTAIN POWER CORPORATION

INDEX TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS AND SCHEDULESAt and for the Three months Ended March 31, 2005 and 2004

The accompanying notes are an integral part of the consolidated financial statements.

Part I.

Financial Information

PageNumber

Item 1. Financial Statements - Consolidated Statements of Income and Comprehensive Income (unaudited) 4

- Consolidated Statements of Cash Flows (unaudited) 5

- Consolidated Balance Sheets (unaudited) 6

- Consolidated Statements of Retained Earnings (unaudited) 8

- Notes to Consolidated Financial Statements (unaudited) 8

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations 18Item 3. Quantitative and Qualitative Disclosures About Market Risk And Other Risk Factors 25Item 4. Controls and Procedures 27Part II. Other Information 29 - Exhibits 29

- Signatures 30

- Certifications 31

3

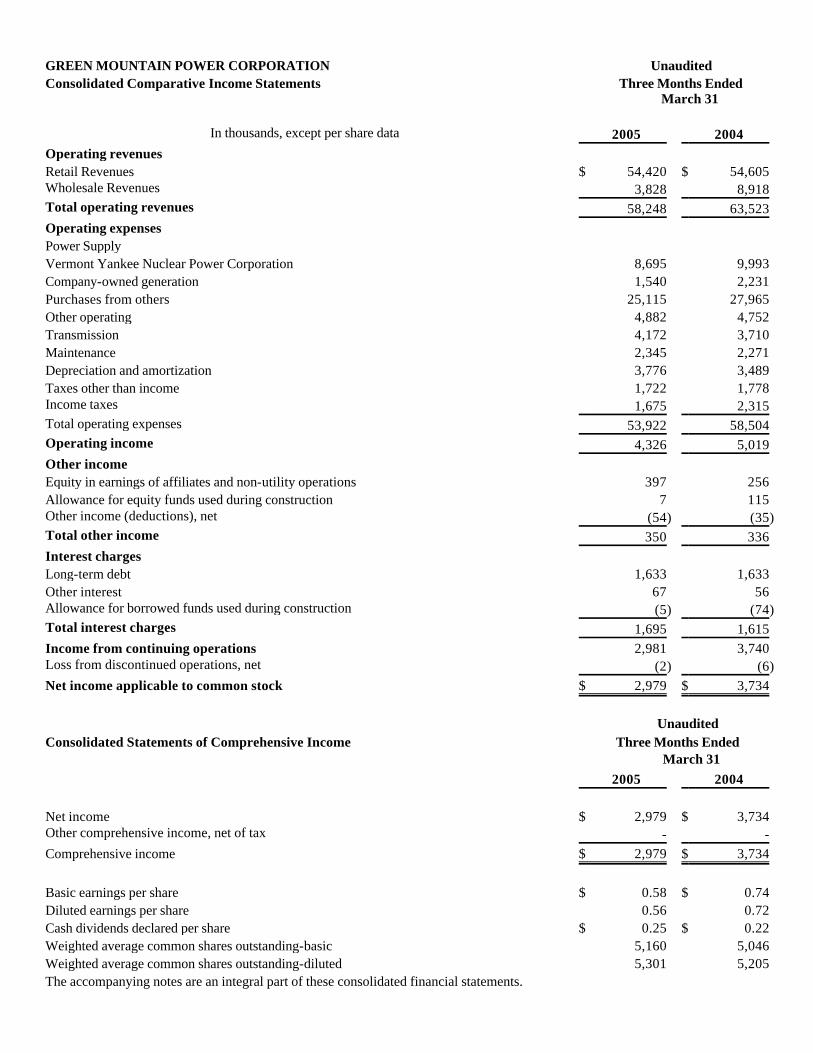

GREEN MOUNTAIN POWER CORPORATION UnauditedConsolidated Comparative Income Statements Three Months Ended

March 31

In thousands, except per share data 2005 2004

Operating revenues Retail Revenues $ 54,420 $ 54,605 Wholesale Revenues 3,828 8,918 Total operating revenues 58,248 63,523 Operating expenses Power Supply Vermont Yankee Nuclear Power Corporation 8,695 9,993 Company-owned generation 1,540 2,231 Purchases from others 25,115 27,965 Other operating 4,882 4,752 Transmission 4,172 3,710 Maintenance 2,345 2,271 Depreciation and amortization 3,776 3,489 Taxes other than income 1,722 1,778 Income taxes 1,675 2,315 Total operating expenses 53,922 58,504 Operating income 4,326 5,019 Other income Equity in earnings of affiliates and non-utility operations 397 256 Allowance for equity funds used during construction 7 115 Other income (deductions), net (54) (35)Total other income 350 336 Interest charges Long-term debt 1,633 1,633 Other interest 67 56 Allowance for borrowed funds used during construction (5) (74)Total interest charges 1,695 1,615 Income from continuing operations 2,981 3,740 Loss from discontinued operations, net (2) (6)

Net income applicable to common stock $ 2,979 $ 3,734

Unaudited Consolidated Statements of Comprehensive Income Three Months Ended

March 31 2005 2004 Net income $ 2,979 $ 3,734 Other comprehensive income, net of tax - - Comprehensive income $ 2,979 $ 3,734 Basic earnings per share $ 0.58 $ 0.74 Diluted earnings per share 0.56 0.72 Cash dividends declared per share $ 0.25 $ 0.22 Weighted average common shares outstanding-basic 5,160 5,046 Weighted average common shares outstanding-diluted 5,301 5,205 The accompanying notes are an integral part of these consolidated financial statements.

4

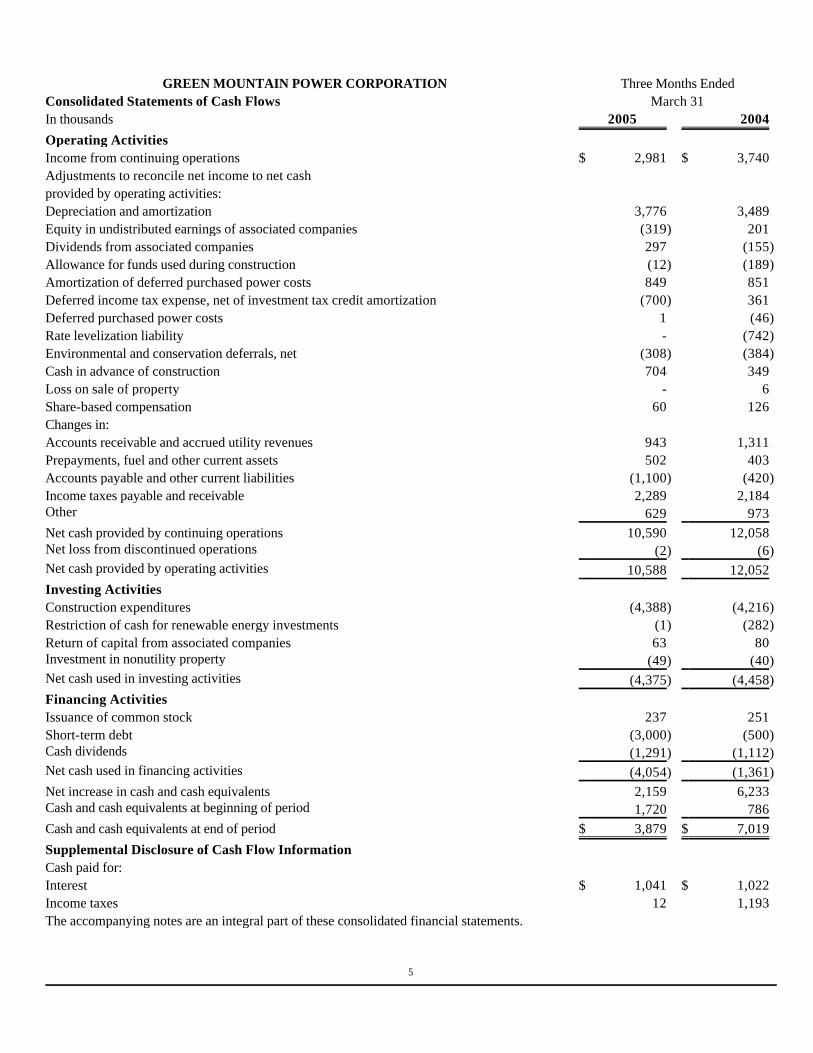

GREEN MOUNTAIN POWER CORPORATION Three Months Ended Consolidated Statements of Cash Flows March 31In thousands 2005 2004 Operating Activities Income from continuing operations $ 2,981 $ 3,740 Adjustments to reconcile net income to net cash provided by operating activities: Depreciation and amortization 3,776 3,489 Equity in undistributed earnings of associated companies (319) 201 Dividends from associated companies 297 (155)Allowance for funds used during construction (12) (189)Amortization of deferred purchased power costs 849 851 Deferred income tax expense, net of investment tax credit amortization (700) 361 Deferred purchased power costs 1 (46)Rate levelization liability - (742)Environmental and conservation deferrals, net (308) (384)Cash in advance of construction 704 349 Loss on sale of property - 6 Share-based compensation 60 126 Changes in: Accounts receivable and accrued utility revenues 943 1,311 Prepayments, fuel and other current assets 502 403 Accounts payable and other current liabilities (1,100) (420)Income taxes payable and receivable 2,289 2,184 Other 629 973 Net cash provided by continuing operations 10,590 12,058 Net loss from discontinued operations (2) (6)Net cash provided by operating activities 10,588 12,052 Investing Activities Construction expenditures (4,388) (4,216)Restriction of cash for renewable energy investments (1) (282)Return of capital from associated companies 63 80 Investment in nonutility property (49) (40)Net cash used in investing activities (4,375) (4,458)

Financing Activities Issuance of common stock 237 251 Short-term debt (3,000) (500)Cash dividends (1,291) (1,112)Net cash used in financing activities (4,054) (1,361)

Net increase in cash and cash equivalents 2,159 6,233 Cash and cash equivalents at beginning of period 1,720 786 Cash and cash equivalents at end of period $ 3,879 $ 7,019 Supplemental Disclosure of Cash Flow Information Cash paid for: Interest $ 1,041 $ 1,022 Income taxes 12 1,193 The accompanying notes are an integral part of these consolidated financial statements.

5

GREEN MOUNTAIN POWER CORPORATION Consolidated Balance Sheets Unaudited

March 31 December 31 In thousands 2005 2004 2004 ASSETS Utility plant

Utility plant, at original cost $ 339,671 $ 324,685 $ 339,269 Less accumulated depreciation 121,911 112,589 119,633 Utility plant, net of accumulated depreciation 217,760 212,096 219,636 Property under capital lease 4,731 5,047 4,731 Construction work in progress 11,126 12,494 8,345 Total utility plant, net 233,617 229,637 232,712

Other investments Associated companies, at equity 10,138 5,771 10,179 Other investments 8,938 8,236 8,780 Total other investments 19,076 14,007 18,959

Current assets Cash and cash equivalents 3,879 7,019 1,720 Accounts receivable, less allowance for doubtful accounts of $470, $690 and $621 18,559 17,131 18,216 Accrued utility revenues 5,678 5,618 6,964 Fuel, materials and supplies, average cost 4,681 4,301 4,848 Prepayments 1,384 1,640 1,674 Income tax receivable - 422 1,717 Other 278 82 323 Total current assets 34,459 36,213 35,462

Deferred charges Demand side management programs 6,928 6,853 7,293 Purchased power costs 1,485 1,769 2,322 Pine Street Barge Canal 13,250 12,954 13,250 Net power supply deferral 12,903 16,438 12,085 Power supply derivative asset 12,555 9,382 10,736 Other regulatory assets 6,538 8,236 6,932 Other deferred charges 886 1,325 1,113 Total deferred charges 54,545 56,957 53,731

Non-utility Other current assets - - - Property and equipment 247 248 247 Other assets 482 605 508 Total non-utility assets 729 853 755

Total assets $ 342,426 $ 337,667 $ 341,619 The accompanying notes are an integral part of these consolidated financial statements.

6

GREEN MOUNTAIN POWER CORPORATION Consolidated Balance Sheets Unaudited

March 31 December 31 In thousands except share data 2005 2004 2004 CAPITALIZATION AND LIABILITIES Capitalization Common stock, $3.33 1/3 par value, authorized 10,000,000 shares (issued 6,002,344, 5,891,827 and 5,968,118 $ 20,008 $ 19,640 $ 19,894 Additional paid-in capital 79,036 76,355 78,852 Retained earnings 31,577 25,406 29,889 Accumulated other comprehensive income (2,353) (1,787) (2,353)Treasury stock, at cost (827,639 shares) (16,701) (16,701) (16,701)

Total common stock equity 111,567 102,913 109,581 Long-term debt, less current maturities 93,000 93,000 93,000 Total capitalization 204,567 195,913 202,581 Capital lease obligation 4,450 4,930 4,493 Current liabilities Short-term debt - - 3,000 Accounts payable, trade and accrued liabilities 7,632 6,436 9,437 Accounts payable to associated companies 6,756 7,512 7,391 Rate levelization liability - 2,228 - Accrued taxes 1,778 2,817 1,290 Customer deposits 1,027 969 1,063 Interest accrued 1,775 1,788 1,136 Other 1,887 1,486 1,151 Total current liabilities 20,855 23,236 24,468 Deferred credits Power supply derivative liability 25,457 25,820 22,821 Accumulated deferred income taxes 31,676 30,429 32,223 Unamortized investment tax credits 2,493 2,780 2,564 Pine Street Barge Canal cleanup liability 6,150 6,972 6,458 Accumulated cost of removal 20,422 21,521 19,806 Deferred compensation 8,783 8,708 8,872 Other regulatory liabilities 4,287 6,287 4,012 Other deferred liabilities 11,115 9,002 11,150 Total deferred credits 110,383 111,519 107,906 COMMITMENTS AND CONTINGENCIES, Note 3 Non-utility Net liabilities of discontinued segment 2,171 2,069 2,171 Total non-utility liabilities 2,171 2,069 2,171 Total capitalization and liabilities $ 342,426 $ 337,667 $ 341,619 The accompanying notes are an integral part of these consolidated financial statements.

7

GREEN MOUNTAIN POWER CORPORATION NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2005 Part I — ITEM 1 1. SIGNIFICANT ACCOUNTING POLICIES

It is our opinion that the financial information contained in this report reflects all normal, recurring adjustments necessary to present a fair statement of results for the periods reported, but such results are not necessarily indicative of results to be expected for the year due to the seasonal nature of our business and include other adjustments discussed elsewhere in this report necessary to reflect fairly the results of the interim periods. Certain information and footnote disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been condensed or omitted in this Form 10-Q pursuant to the rules and regulations of the Securities and Exchange Commission. However, the disclosures herein, when read with the Green Mountain Power Corporation (the "Company" or "GMP") annual report for 2004 filed on Form 10-K, are adequate to make the information presented not misleading. The preparation of financial statements in conformity with generally accepted accounting principles requires the use of estimates and assumptions that affect assets and liabilities, and revenues and expenses. Actual results could differ from such estimates. Regulatory Accounting. The Company's utility operations, including accounting records, rates, operations and certain other practices of its electric utility business, are subject to the regulatory authority of the Federal Energy Regulatory Commission ("FERC") and the Vermont Public Service Board ("VPSB"). The Vermont Department of Public Service ("DPS" or the "Department") is the public advocate for utility customers.

The accompanying consolidated financial statements conform to accounting principles generally accepted in the United States of America applicable to rate-regulated enterprises in accordance with Statement of Financial Accounting Standards No. ("SFAS") 71 ("SFAS 71"), "Accounting for Certain Types of Regulation." Under SFAS 71, the Company accounts for certain transactions in accordance with permitted regulatory treatment. As such, regulators may permit incurred costs, typically treated as expenses by unregulated entities, to be deferred and expensed in future periods when recovered in future revenues. Revenues. The VPSB, sets the rates we charge our customers for their electricity. In periods prior to April 2001, we charged our customers higher rates for billing cycles in December through March and lower rates for the remaining months. These were called seasonally differentiated rates. Seasonal rates were eliminated in April 2001, and generated approximately $8.5 million of revenues deferred in 2001 pursuant to VPSB order (the "Deferred Revenues"), of which $3.0 million, $1.1 million and $4.5 million were recognized during 2004, 2003 and 2002, respectively. At December 31, 2004, the Company has recognized all the Deferred Revenues.

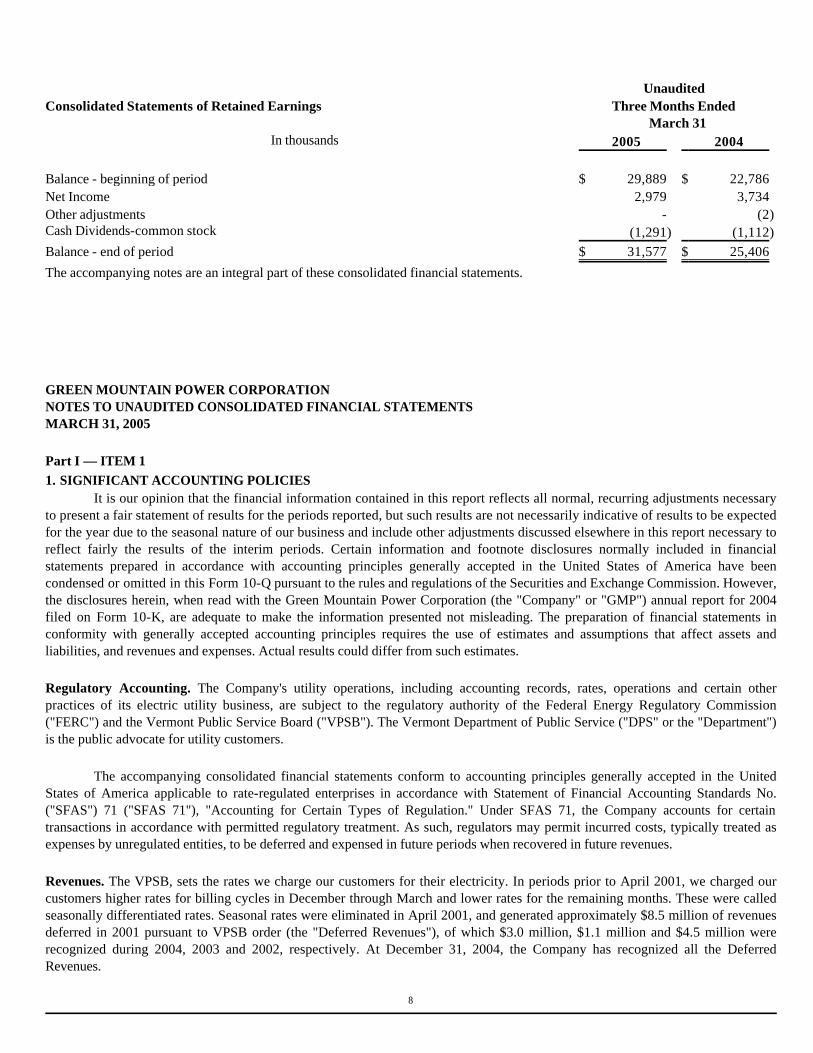

Unaudited Consolidated Statements of Retained Earnings Three Months Ended

March 31 In thousands 2005 2004

Balance - beginning of period $ 29,889 $ 22,786 Net Income 2,979 3,734 Other adjustments - (2)Cash Dividends-common stock (1,291) (1,112)

Balance - end of period $ 31,577 $ 25,406 The accompanying notes are an integral part of these consolidated financial statements.

8

Electricity sales to customers are based on monthly meter readings. Estimated unbilled revenues are recorded at the end of each monthly accounting period. In order to determine unbilled revenues, the Company makes various estimates including 1) energy generated, purchased and resold, 2) losses of energy over transmission and distribution lines, 3) kilowatt-hour usage by retail customer mix (residential, small commercial and industrial), and 4) average retail customer pricing rates.

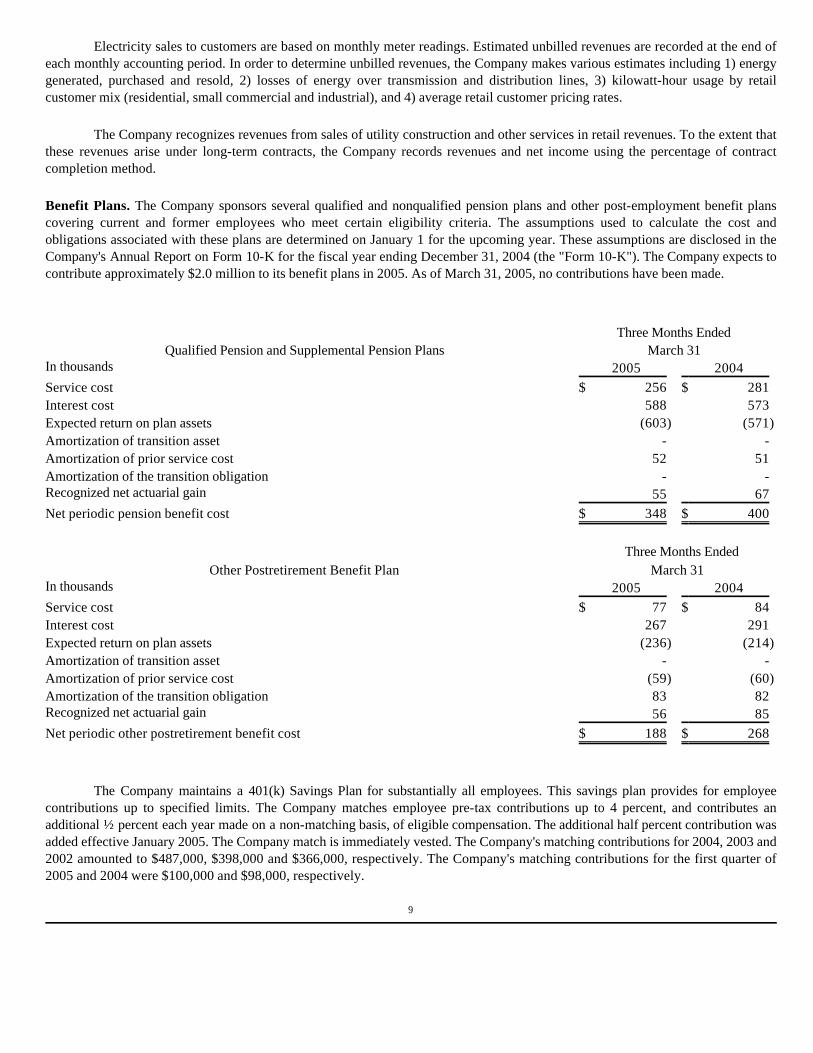

The Company recognizes revenues from sales of utility construction and other services in retail revenues. To the extent that these revenues arise under long-term contracts, the Company records revenues and net income using the percentage of contract completion method. Benefit Plans. The Company sponsors several qualified and nonqualified pension plans and other post-employment benefit plans covering current and former employees who meet certain eligibility criteria. The assumptions used to calculate the cost and obligations associated with these plans are determined on January 1 for the upcoming year. These assumptions are disclosed in the Company's Annual Report on Form 10-K for the fiscal year ending December 31, 2004 (the "Form 10-K"). The Company expects to contribute approximately $2.0 million to its benefit plans in 2005. As of March 31, 2005, no contributions have been made.

The Company maintains a 401(k) Savings Plan for substantially all employees. This savings plan provides for employee

contributions up to specified limits. The Company matches employee pre-tax contributions up to 4 percent, and contributes an additional ½ percent each year made on a non-matching basis, of eligible compensation. The additional half percent contribution was added effective January 2005. The Company match is immediately vested. The Company's matching contributions for 2004, 2003 and 2002 amounted to $487,000, $398,000 and $366,000, respectively. The Company's matching contributions for the first quarter of 2005 and 2004 were $100,000 and $98,000, respectively.

Three Months Ended Qualified Pension and Supplemental Pension Plans March 31

In thousands 2005 2004 Service cost $ 256 $ 281 Interest cost 588 573 Expected return on plan assets (603) (571)Amortization of transition asset - - Amortization of prior service cost 52 51 Amortization of the transition obligation - - Recognized net actuarial gain 55 67 Net periodic pension benefit cost $ 348 $ 400

Three Months Ended

Other Postretirement Benefit Plan March 31 In thousands 2005 2004 Service cost $ 77 $ 84 Interest cost 267 291 Expected return on plan assets (236) (214)Amortization of transition asset - - Amortization of prior service cost (59) (60)Amortization of the transition obligation 83 82 Recognized net actuarial gain 56 85 Net periodic other postretirement benefit cost $ 188 $ 268

9

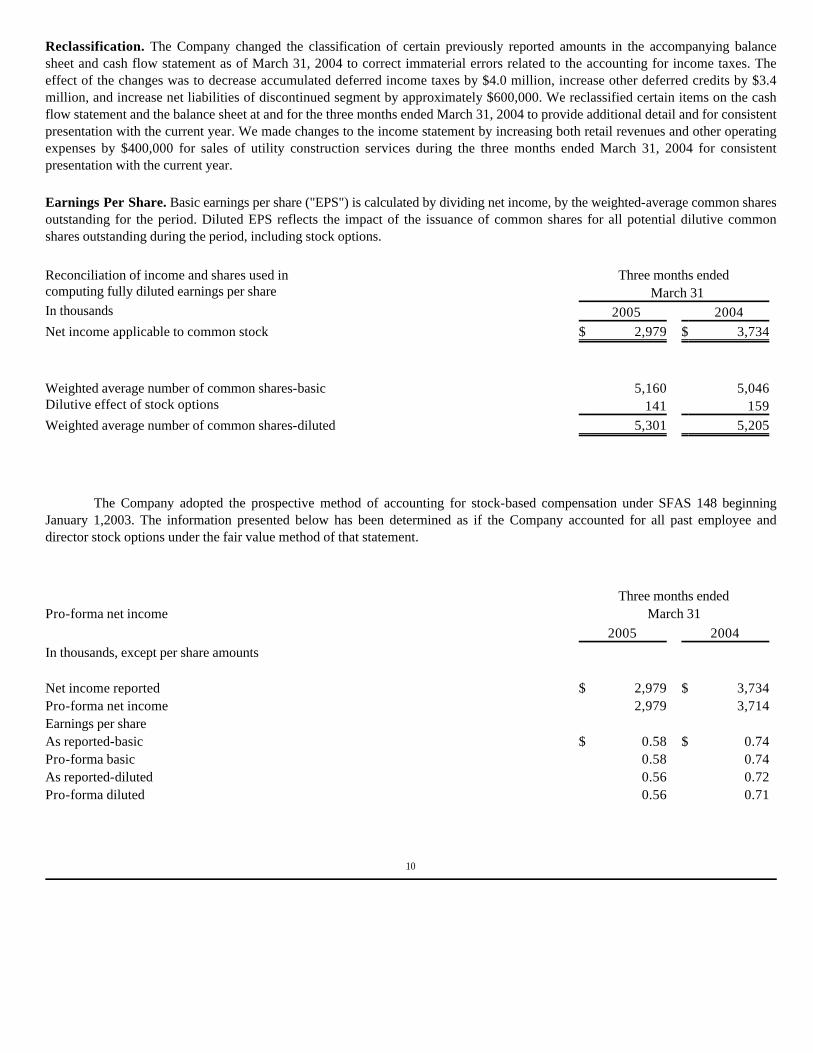

Reclassification. The Company changed the classification of certain previously reported amounts in the accompanying balance sheet and cash flow statement as of March 31, 2004 to correct immaterial errors related to the accounting for income taxes. The effect of the changes was to decrease accumulated deferred income taxes by $4.0 million, increase other deferred credits by $3.4 million, and increase net liabilities of discontinued segment by approximately $600,000. We reclassified certain items on the cash flow statement and the balance sheet at and for the three months ended March 31, 2004 to provide additional detail and for consistent presentation with the current year. We made changes to the income statement by increasing both retail revenues and other operating expenses by $400,000 for sales of utility construction services during the three months ended March 31, 2004 for consistent presentation with the current year. Earnings Per Share. Basic earnings per share ("EPS") is calculated by dividing net income, by the weighted-average common shares outstanding for the period. Diluted EPS reflects the impact of the issuance of common shares for all potential dilutive common shares outstanding during the period, including stock options.

The Company adopted the prospective method of accounting for stock-based compensation under SFAS 148 beginning January 1,2003. The information presented below has been determined as if the Company accounted for all past employee and director stock options under the fair value method of that statement.

Reconciliation of income and shares used in Three months ended computing fully diluted earnings per share March 31 In thousands 2005 2004 Net income applicable to common stock $ 2,979 $ 3,734 Weighted average number of common shares-basic 5,160 5,046 Dilutive effect of stock options 141 159 Weighted average number of common shares-diluted 5,301 5,205

Three months ended Pro-forma net income March 31

2005 2004 In thousands, except per share amounts Net income reported $ 2,979 $ 3,734 Pro-forma net income 2,979 3,714 Earnings per share As reported-basic $ 0.58 $ 0.74 Pro-forma basic 0.58 0.74 As reported-diluted 0.56 0.72 Pro-forma diluted 0.56 0.71

10

Unregulated operations. Our wholly owned subsidiaries include GMP Real Estate Corporation and Green Mountain Power Investment Company ("GMPIC"). Green Mountain Resources, Inc. and Green Mountain Propane Gas Company Limited were dissolved in March and May 2004, respectively, with no gain or loss resulting from dissolution. We also have a rental water heater program that is not regulated by the VPSB. The results of these subsidiaries, and the Company’s unregulated rental water heater program, are included in earnings of affiliates and non-utility operations in the Other Income (Deductions) section of the Consolidated Statements of Income.

Discontinued Operations. The Company accounts for its wholly-owned subsidiary, Northern Water Resources, Inc. ("NWR"), as a discontinued operation. NWR's assets and liabilities consist primarily of deferred tax assets and liabilities relating to a number of investments that the company has discontinued, inactivated, sold in part or retains as passive minority interests. Remaining holdings include a minority equity investment in a wind project that usually, but not always, generates tax losses; a minority interest in a manufacturer of waste treatment equipment; and non-performing loans. Substantially all of NWR's investments have been written off, except for associated deferred tax amounts, net of applicable valuation allowances. 2. INVESTMENT IN ASSOCIATED COMPANIES

We recognize net income from our affiliates (companies in which we have ownership interests) listed below based on our percentage ownership (equity method). Vermont Yankee Nuclear Power Corporation ("VYNPC") Percent ownership: 33.6% common

Summarized unaudited financial information for VYNPC follows:

Entergy Nuclear Vermont Yankee, LLC ("ENVY"), the owner of the Vermont Yankee Nuclear Plant, has announced that, under current operating parameters, it will exhaust the capacity of its existing nuclear waste storage pool in 2007 or 2008 and will need to store nuclear waste in so-called "dry fuel storage" facilities to be constructed on the site. Current Vermont law appears to require ENVY to obtain approval of the Vermont State legislature, in addition to VPSB approval, to construct and use such dry fuel storage facilities. If ENVY is unsuccessful in receiving favorable legislative action and/or regulatory approval, ENVY has announced that it would be required to shut down the Vermont Yankee plant. If the Vermont Yankee plant is shut down, we would have to acquire substitute baseload power resources, comprising approximately 35 percent of our estimated total power supply needs. At currently projected market prices, we estimate the annual incremental cost (in excess of the projected costs of power under our power supply contract for output from the Vermont Yankee facility) would be approximately $15 million annually. Recovery of those increased costs in rates would require a rate increase of approximately seven percent.

Three Months Ended March 31 In thousands 2005 2004 Gross Revenue $ 42,349 $ 49,146 Net Income Applicable 162 143 to Common Stock Equity in Net Income 54 48 Amounts due to VYNPC 2,740 3,178

11

On June 18, 2004, a fire in the electrical conduits leading to a transformer outside the Vermont Yankee plant resulted in a shutdown of the plant. The outage ended on July 7, 2004. In response to the Company's request, the VPSB issued a final accounting order allowing the Company to defer its incremental replacement power costs during the outage totaling approximately $500,000. The order also instructs the Company to apply any proceeds received under a Ratepayer Protection Proposal ("RPP") to reduce the balance of deferred replacement power costs.

The RPP was a part of ENVY's request to uprate or increase the output of the Vermont Yankee plant that was approved by the VPSB. Under the RPP, we have indemnification rights to between approximately $550,000 and $1.6 million to recover uprate-related reductions in output for the three-year period beginning in May 2004 and ending after completion of the uprate (or a maximum of three years), depending on future wholesale energy market prices. The Company and ENVY dispute whether the fire was uprate-related, and therefore whether the associated outage is subject to indemnification under the RPP. The Company has petitioned the VPSB to resolve the dispute.

Vermont Electric Power Company, Inc. ("VELCO") Percent ownership: 29.2% common

30.0% preferred

VELCO and its wholly-owned subsidiary, Vermont Electric Transmission Company, own and operate the transmission system in Vermont over which bulk power is delivered to all electric utilities in the state. The Company plans to make capital investments of up to $20 million in VELCO through 2007 in support of various transmission projects, including a $4.6 million investment made in the last quarter of 2004.

Summarized unaudited financial information for VELCO is as follows:

The cost of transmission services provided by VELCO included in the Company's transmission expenses in the accompanying Consolidated Statements of Income amounted to $3.4 million in the first quarter 2005, compared with $3.0 million in first quarter 2004, respectively.

Vermont Electric Power Company Three Months Ended

March 31 In thousands 2005 2004 Gross Revenue $ 7,982 $ 6,333 Net Income 730 310 Equity in Net Income 210 46 Amounts due to VELCO 4,016 4,338

12

3. COMMITMENTS AND CONTINGENCIES Environmental Matters

The electric industry typically uses or generates a range of potentially hazardous products in its operations. We must meet various land, water, air and aesthetic requirements as administered by local, state and federal regulatory agencies. We believe that we are in substantial compliance with these requirements, and that there are no outstanding material complaints about our compliance with present environmental protection regulations, except as described below under the caption "Pine Street Barge Canal Superfund Site." Pine Street Barge Canal Superfund Site - In 1999, the Company entered into a United States District Court Consent Decree constituting a final settlement with the United States Environmental Protection Agency ("EPA"), the State of Vermont and numerous other parties of claims relating to a federal Superfund site in Burlington, Vermont, known as the "Pine Street Barge Canal." We have estimated total future costs of the Company’s future obligations under the consent decree to be approximately $6.5 million. The estimated liability is not discounted, and it is possible that our estimate of future costs could change by a material amount. We have recorded a regulatory asset of $13.3 million to reflect unrecovered past and future Pine Street costs. Pursuant to the Company’s 2003 Rate Plan approved by the VPSB, the Company will begin to amortize past unrecovered costs in 2005. The Company will amortize the full amount of incurred costs over 20 years without a return. The amortization is expected to be allowed in future rates, without disallowance or adjustment, until fully amortized. Rates - Management believes that fair regulatory treatment, including adequate and timely rate relief, is required to maintain the Company's financial strength. Retail Rate Cases - On December 22, 2003, the VPSB approved our 2003 Rate Plan, jointly proposed by the Company and the Department. The 2003 Rate Plan covers the period from 2003 through 2006 and includes the following principal elements:

· The Company’s rates remained unchanged through 2004. The 2003 Rate Plan allows the Company to raise rates 1.9 percent, effective January 1, 2005, and an additional 0.9 percent, effective January 1, 2006, if the increases are supported by cost of service schedules submitted 60 days prior to the effective dates. We submitted a cost of service schedule supporting the 1.9 percent rate increase for 2005 in accordance with the plan. The increase became effective on January 1, 2005 in accordance with the plan. If the Company’s cost of service filing for 2006 established that a rate increase of less than 0.9 percent is required for the Company to meet its revenue requirements, the Company would implement the lesser rate increase. The VPSB retains the discretion to open an investigation of the Company’s rates at any time, at the request of the DPS, the request of ratepayers, or on its own volition. Certain ratepayers requested the VPSB to open such an investigation in connection with the Company’s 1.9 percent rate increase for 2005. The VPSB granted the request in December 2004, and then, at our request, closed and terminated its investigation in January 2005, with no adverse impact on the Company’s rates.

· The Company may seek additional rate increases in extraordinary circumstances, such as severe storm repair costs, natural disasters, extended unanticipated unit outages, or significant losses of customer load.

· The Company’s annual allowed return on equity is 10.5 percent for the period January 1, 2003 through December 31, 2006. During the same period, the Company’s earnings on core utility operations are capped at 10.5 percent. The Company did not experience excess earnings in 2004. Excess earnings in 2005 or 2006 will be refunded to customers as a credit on customer bills or applied to reduce regulatory assets, as the Department directs.

13

Other Regulatory MattersOn March 29, 2005, the VPSB issued its Order in a retail rate proceeding filed by Central Vermont Public Service

Corporation (“CVPS”), the largest Vermont electric utility. The CVPS Order included a determination that CVPS had incorrectly calculated the amount of its utility earnings under a voluntary earnings cap to which CVPS had agreed as part of a 2001 rate case settlement. The VPSB required CVPS to recalculate its earnings cap retroactively to 2001, after removing expenses and assets that would not be included in its cost of service or rate base. Under the 2003 Rate Plan, GMP calculated its earnings cap in 2003 in the same manner as CVPS. GMP does not have substantial net assets on its balance sheet that would normally be excluded from rate base. We have also calculated, and submitted to the DPS, earnings cap calculations for 2003 applying the methodology ordered by the VPSB in the CVPS rate case. The calculations indicate that the Company did not exceed its earnings cap in 2003 under either calculation method, a conclusion with which the DPS has agreed. The Company submitted to the DPS and VPSB an earnings cap report for 2004, applying the new Board-ordered calculation method. Our 2004 report shows that the Company's 2004 earnings did not exceed the earnings cap in our 2003 Rate Plan (10.5 percent allowed return on equity).

The CVPS Order also provided CVPS with an allowed rate of return of 10 percent as compared with the 10.5 percent return on equity allowed in our 2003 Rate Plan. The CVPS Order found that CVPS's risk profile differs from GMP's in several ways, including the absence of significant customer concentration risk, cost of capital and other considerations. Power Supply Risks and Contingencies

All of the Company’s power supply contract costs are currently being recovered through rates approved by the VPSB. The Company’s most significant power supply contracts are the Hydro Quebec Vermont Joint Owners ("VJO") Contract (the "VJO Contract") and the VYNPC Contract, which together supply approximately 70 percent of our retail load. The Company has a contract with Morgan Stanley Capital Group, Inc. (the "Morgan Stanley Contract"), that we estimate supplies 16 percent of our load.

· The Company carried forward into 2004 $3.0 million in Deferred Revenue remaining at December 31, 2003, from a previous VPSB order. These revenues were applied in 2004 to offset increased costs.

· The Company has begun to amortize (recover) certain regulatory assets, including Pine Street Barge Canal environmental site costs and past demand-side management program costs, beginning in January 2005, with those amortizations to be allowed in future rates. Pine Street costs will be recovered over a twenty-year period without a return.

· The Company filed with the VPSB in 2004 a new fully-allocated cost of service study and rate re-design, which allocates the Company’s revenue requirement among all customer classes on the basis of current costs. The new rate design is subject to VPSB approval and is not expected to adversely affect operating results.

· The Company and the Department have agreed to work cooperatively to develop and propose an alternative regulation plan as authorized by legislation enacted in Vermont in 2003. If the Company and Department agree on such a plan, and it is approved by the VPSB, the alternative regulation plan would supersede the 2003 Rate Plan.

14

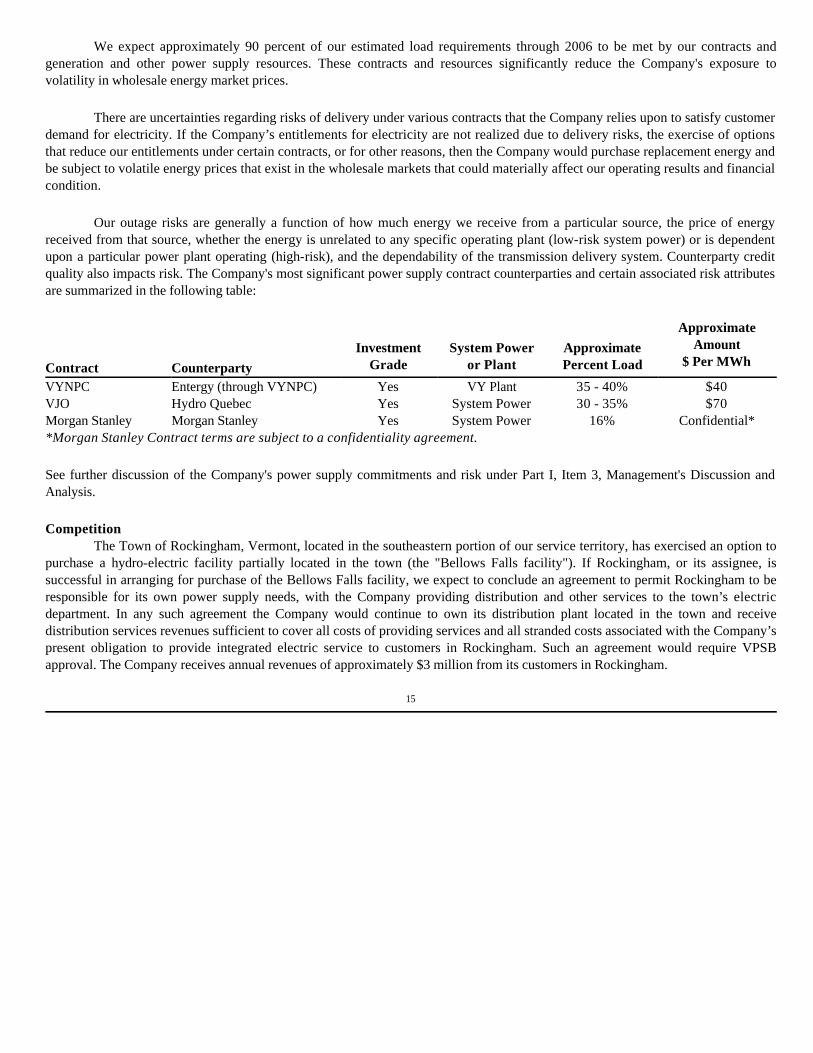

We expect approximately 90 percent of our estimated load requirements through 2006 to be met by our contracts and generation and other power supply resources. These contracts and resources significantly reduce the Company's exposure to volatility in wholesale energy market prices.

There are uncertainties regarding risks of delivery under various contracts that the Company relies upon to satisfy customer

demand for electricity. If the Company’s entitlements for electricity are not realized due to delivery risks, the exercise of options that reduce our entitlements under certain contracts, or for other reasons, then the Company would purchase replacement energy and be subject to volatile energy prices that exist in the wholesale markets that could materially affect our operating results and financial condition.

Our outage risks are generally a function of how much energy we receive from a particular source, the price of energy

received from that source, whether the energy is unrelated to any specific operating plant (low-risk system power) or is dependent upon a particular power plant operating (high-risk), and the dependability of the transmission delivery system. Counterparty credit quality also impacts risk. The Company's most significant power supply contract counterparties and certain associated risk attributes are summarized in the following table:

*Morgan Stanley Contract terms are subject to a confidentiality agreement. See further discussion of the Company's power supply commitments and risk under Part I, Item 3, Management's Discussion and Analysis. Competition

The Town of Rockingham, Vermont, located in the southeastern portion of our service territory, has exercised an option to purchase a hydro-electric facility partially located in the town (the "Bellows Falls facility"). If Rockingham, or its assignee, is successful in arranging for purchase of the Bellows Falls facility, we expect to conclude an agreement to permit Rockingham to be responsible for its own power supply needs, with the Company providing distribution and other services to the town’s electric department. In any such agreement the Company would continue to own its distribution plant located in the town and receive distribution services revenues sufficient to cover all costs of providing services and all stranded costs associated with the Company’s present obligation to provide integrated electric service to customers in Rockingham. Such an agreement would require VPSB approval. The Company receives annual revenues of approximately $3 million from its customers in Rockingham.

Contract

Counterparty

Investment

Grade

System Power

or Plant

ApproximatePercent Load

ApproximateAmount

$ Per MWh

VYNPC Entergy (through VYNPC) Yes VY Plant 35 - 40% $40VJO Hydro Quebec Yes System Power 30 - 35% $70Morgan Stanley Morgan Stanley Yes System Power 16% Confidential*

15

Other Legal Matters In 2002, the owners of property along the shoreline of Joe's Pond, an impoundment located in Danville, Vermont, created by

the Company's West Danville hydro-electric generating facility, filed an inquiry with the VPSB seeking review of certain dam improvements made by the Company in 1995, alleging that the Company did not obtain all necessary regulatory approvals for the 1995 improvements and that the Company's improvements and subsequent operation of the dam have caused flooding of the shoreline and property damage. The Company received VPSB approval for, and has made additional dam improvements at, the facility. The VPSB has pending a regulatory proceeding to determine whether to impose regulatory penalties in connection with the 1995 dam improvements. The Company and the DPS have stipulated to a penalty amount of $50,000. The stipulation has been submitted to the VPSB for approval. In addition, numerous owners of shoreline property on Joe's Pond have filed a lawsuit in Vermont superior court seeking damages for property damage allegedly caused by the Company's negligent conduct in making dam improvements and operating the dam facilities. The Company is defending against these claims. The Company does not expect the litigation to result in a material adverse effect on its operating results or financial condition. 4. DERIVATIVE INSTRUMENTS

The Company utilizes derivative instruments primarily to reduce power supply risk. The Company does not hold derivative trading positions. The Company has continued to record expense related to derivatives in the period settled consistent with an accounting order issued by the VPSB which allows for changes in fair values of derivatives to be recorded as regulatory assets or liabilities.

SFAS 133, as amended, establishes accounting and reporting standards requiring that every derivative instrument (including

certain derivative instruments embedded in other contracts) be recorded on the balance sheet as either an asset or liability measured at its fair value.

We currently have an agreement (the "9701 agreement") that grants Hydro Quebec an option to call power at prices below

current and estimated future market rates. This agreement is a derivative and is effective through 2015. The Morgan Stanley Contract is used to hedge against increases in fossil fuel prices. The Morgan Stanley Contract is a

derivative and expires December 31, 2006. At March 31, 2005, the Company had a power supply derivative liability in deferred credits of $25.5 million reflecting the

fair value of the 9701 agreement, and a power supply derivative asset of $12.6 million, reflecting the fair value of the Morgan Stanley Contract. A corresponding net regulatory asset of $12.9 million is also recorded in deferred charges. At December 31, 2004, the Company had a liability of $22.8 million, reflecting the fair value of the 9701 agreement, and an asset of $10.7 million, reflecting the fair value of the Morgan Stanley Contract. A corresponding net regulatory asset of $12.1 million was also recorded. The Company believes that the net regulatory asset is probable of recovery in future rates. The net regulatory asset is based on current estimates of future market prices that are likely to change by material amounts.

If a derivative instrument were terminated early because it is probable that a transaction or forecasted transaction will not

occur, any gain or loss would be recognized in earnings immediately. For derivatives held to maturity, the earnings impact would be recorded in the period that the derivative is sold or matures. 5. SEGMENTS AND RELATED INFORMATION

The Company's electric utility operation is its only operating segment. The electric utility is engaged in the procurement, generation, distribution and sale of electrical energy in the State of Vermont and also reports the results of its wholly owned unregulated subsidiaries (GMPIC and GMP Real Estate) and the rental water heater program as a separate line item in the Other Income section in the Consolidated Statement of Income.

16

6. NEW ACCOUNTING STANDARDS On May 19, 2004, the FASB issued FASB Staff Position No. FAS 106-2, "Accounting and Disclosure Requirements Related

to the Medicare Prescription Drug, Improvement and Modernization Act of 2003," (the "Act") which requires employers to provide certain disclosures regarding the effect of the federal subsidy provided by the Act. The effect of the federal subsidy under the Act, accounted for as an actuarial gain, resulted in a reduction of $3.5 million to the Company's accumulated postretirement benefit obligation at December 31, 2004, and will reduce net periodic cost by approximately $368,000 in 2005.

In December 2004, the FASB issued a revision to SFAS No. 123R, "Share-Based Payments," which replaces SFAS No. 123,

"Accounting for Stock-Based Compensation." The revision determines how the Company will measure the cost of employee services received in exchange for share-based payments. The cost of share-based payments will be based on the grant date fair value of the award. The guidance is effective for the Company as of the beginning of 2006. The Company has not yet determined what the impact of this new standard will be on its financial position or results of operations.

In December 2004, the FASB issued FASB Staff Position 109-1 ("FSP 109-1"), which was effective upon issuance, to

provide guidance of the application of SFAS No. 109, "Accounting for Income Taxes" ("SFAS 109"), to the provision within the American Jobs Creation Act of 2004 ("Jobs Act") that provides a tax deduction on qualified production activities. The Jobs Act includes a tax deduction of up to 9 percent (when fully phased-in) of the lesser of (a) "qualified production activities income," as defined in the Jobs Act, or (b) taxable income (after the deduction for the utilization of any net operating loss carryforwards). The tax deduction is limited to 50 percent of W-2 wages paid by the taxpayer. FSP 109-1 clarifies that the manufacturer's deduction provided for under the Jobs Act should be accounted for as a special deduction in accordance with SFAS 109 and not as a tax rate reduction. The adoption of FSB 109-1 had no impact on the Company's financial statements in 2004. The Company estimates that in 2005 earnings will benefit by approximately $0.03 per share as a result of the Jobs Act.

In March 2005, the FASB issued FASB Interpretation No. 47 ("FIN 47") Accounting for Conditional Asset Retirement

Obligations, an interpretation of FASB 143, Accounting for Asset Retirement Obligations. FIN 47 clarifies that the term conditional asset retirement obligation as used in FASB 143 refers to a legal obligation to perform an asset retirement activity in which the timing or method of settlement is conditional on a future event that may or may not be within the control of the reporting entity. An entity is required to recognize a liability for the fair value of a conditional asset retirement obligation if the fair value can be reasonably estimated, and should be recognized when incurred. FIN 47 is effective for the Company in 2005. The Company has not yet determined what the impact of this new standard will be on its financial position or results of operations.

17

GREEN MOUNTAIN POWER CORPORATION Part I — ITEM 2 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIALCONDITION AND RESULTS OF OPERATIONS March 31, 2005Executive Overview -- Green Mountain Power Corporation (the "Company") generates virtually all of its earnings from retail electricity sales. Our retail electricity sales typically grow at an average annual rate of between one and two percent, about average for most electric utility companies in New England. While wholesale revenues are substantial, they have relatively minor impact on our operating results and financial condition. The Company is regulated and cannot adjust prices of retail electricity sales without regulatory approval from the Vermont Public Service Board ("VPSB").

Fair regulatory treatment is fundamental to maintaining the Company’s financial stability. Rates must be set at levels to recover costs, including a market rate of return to equity and debt holders in order to attract capital. In December 2003, the Company received approval from the VPSB of a new rate plan covering the period 2003 through 2006 (the "2003 Rate Plan"), which sets rates at levels the Company believes will provide improved opportunities to recover costs and to earn its allowed rate of return. In accordance with the rate plan, the VPSB approved, and the Company implemented, a 1.9 percent rate increase, effective January 1, 2005.

Power supply expenses were equivalent to approximately 61 percent of total revenues in the first quarter of 2005. The

Company’s need to seek rate increases from its customers frequently moves in tandem with increases in our power supply costs. We have entered into long-term power supply contracts for most of our energy needs. All of our power supply contract costs are currently included in the rates we charge our customers.

Growth opportunities beyond the Company’s normal investment in its infrastructure include a planned increase in our equity

investment in Vermont Electric Power Company, Inc. ("VELCO") and a planned increase in sales of utility services.

In this section, we explain the general financial condition and the results of operations for the Company and its subsidiaries. This explanation includes:

Management believes its most critical accounting policies include the timing of expense and revenue recognition under the

regulatory accounting framework within which we operate; the manner in which we account for certain power supply arrangements that qualify as derivatives; the assumptions that we make regarding defined benefit plans and contingency reserves; and revenue recognition, particularly as it relates to unbilled and deferred revenues. These accounting policies, among others, affect the Company's significant judgments and estimates used in the preparation of its consolidated financial statements.

· factors that affect our business; · our earnings and costs in the periods presented and why they changed between periods; · the source of our earnings; · our expenditures for capital projects and what we expect they will be in the future; · where we expect to get cash for future capital expenditures; and · how all of the above affect our overall financial condition.

18

There are statements in this section that contain projections or estimates that are considered to be "forward-looking" as defined by the Securities and Exchange Commission (the "SEC"). In these statements, you may find words such as believes, expects, plans, or similar words. These statements are not guarantees of our future performance. There are risks, uncertainties and other factors that could cause actual results to be different from those projected. Some of the reasons the results may be different include:

We address these items in more detail below.

These forward-looking statements represent our estimates and assumptions only as of the date of this report. As you read this section it may be helpful to refer to the consolidated financial statements and notes in Part I - ITEM 1.

RESULTS OF OPERATIONS Earnings Summary - Overview

In this section, we discuss our earnings and the principal factors affecting them.

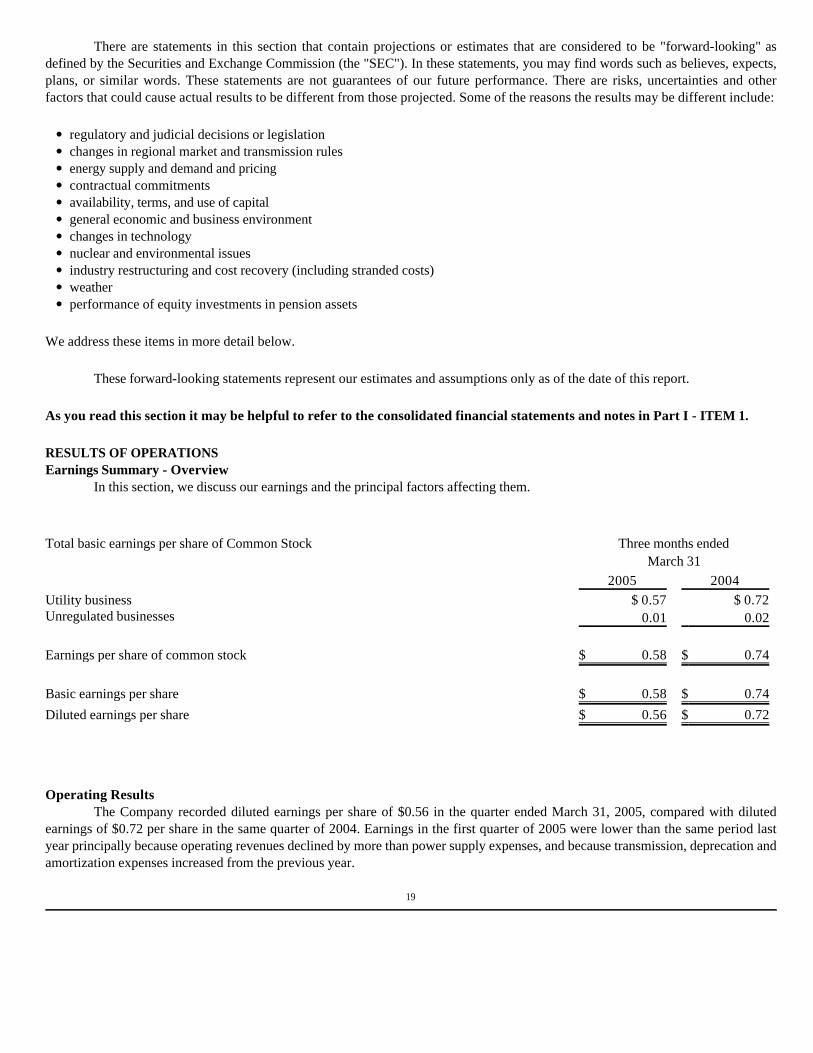

Operating Results The Company recorded diluted earnings per share of $0.56 in the quarter ended March 31, 2005, compared with diluted

earnings of $0.72 per share in the same quarter of 2004. Earnings in the first quarter of 2005 were lower than the same period last year principally because operating revenues declined by more than power supply expenses, and because transmission, deprecation and amortization expenses increased from the previous year.

· regulatory and judicial decisions or legislation · changes in regional market and transmission rules · energy supply and demand and pricing · contractual commitments · availability, terms, and use of capital · general economic and business environment · changes in technology · nuclear and environmental issues · industry restructuring and cost recovery (including stranded costs) · weather · performance of equity investments in pension assets

Total basic earnings per share of Common Stock Three months ended

March 31 2005 2004

Utility business $ 0.57 $ 0.72 Unregulated businesses 0.01 0.02 Earnings per share of common stock $ 0.58 $ 0.74 Basic earnings per share $ 0.58 $ 0.74 Diluted earnings per share $ 0.56 $ 0.72

19

Company operating revenues declined by $5.3 million while power supply expenses decreased by $4.8 million in the first quarter of 2005, compared with the same period last year. The reduced margins (operating revenues less cost of power) caused first quarter 2005 earnings per share to decrease by approximately $0.05. Reductions in sales to residential customers and decreased output from the Company’s low cost hydroelectric facilities both contributed to lower margins on the sale of electricity. Transmission expenses increased by approximately $462,000, reducing earnings per share by $0.05 in the first quarter of 2005, reflecting increased transmission expense resulting from expanded transmission investment by VELCO, which owns and operates transmission systems in Vermont for all Vermont utilities. In addition, first quarter 2005 depreciation and amortization expenses increased by $287,000 reducing earnings per share by $0.03 compared with the first quarter of 2004.

Retail operating revenues for the first quarter of 2005 decreased by $186,000 over the comparable 2004 period, reflecting

decreased recognition of revenues deferred under a previous regulatory order, that was substantially offset by a 1.9 percent rate increase authorized by the VPSB and effective as of January 1, 2005. The Company recognized $749,000 or $0.09 earnings per share of deferred revenue during the first quarter of 2004, compared with no deferred revenues recognized during the first quarter of 2005.

In December 2003, the VPSB approved a rate plan for the period 2003 through 2006 (the "2003 Rate Plan"), jointly proposed by the Company and the Vermont Department of Public Service (the "Department" or the "DPS"). The 2003 Rate Plan calls for no retail rate increases in 2003 or 2004, then scheduled increases of 1.9 percent (generating approximately $4 million in added annual revenues) effective January 1, 2005, and 0.9 percent (generating approximately $2 million in added annual revenues) effective January 1, 2006. The first of these rate increases has been implemented effective January 1, 2005. The 2003 Rate Plan sets the Company’s allowed return on equity from core utility operations at 10.5 percent, effective with 2003, and provides for an earnings cap at that level through 2006. The 2003 Rate Plan is summarized in more detail in Part I, Item 1, Note 3 "Retail Rate Cases".

The VPSB’s January 2001 rate order (the "2001 Settlement Order") allowed the Company to defer revenues of

approximately $8.5 million, generated by leveling winter/summer rates during 2001, to help offset costs and realize our allowed rate of return during the 2001-2003 period. The 2003 Rate Plan permitted us to continue to defer and recognize these revenues in 2004. We recognized approximately $3.0 million of these deferred revenues during the year in 2004, compared with approximately $1.1 and $4.5 million recognized annually in 2003 and 2002, respectively.

20

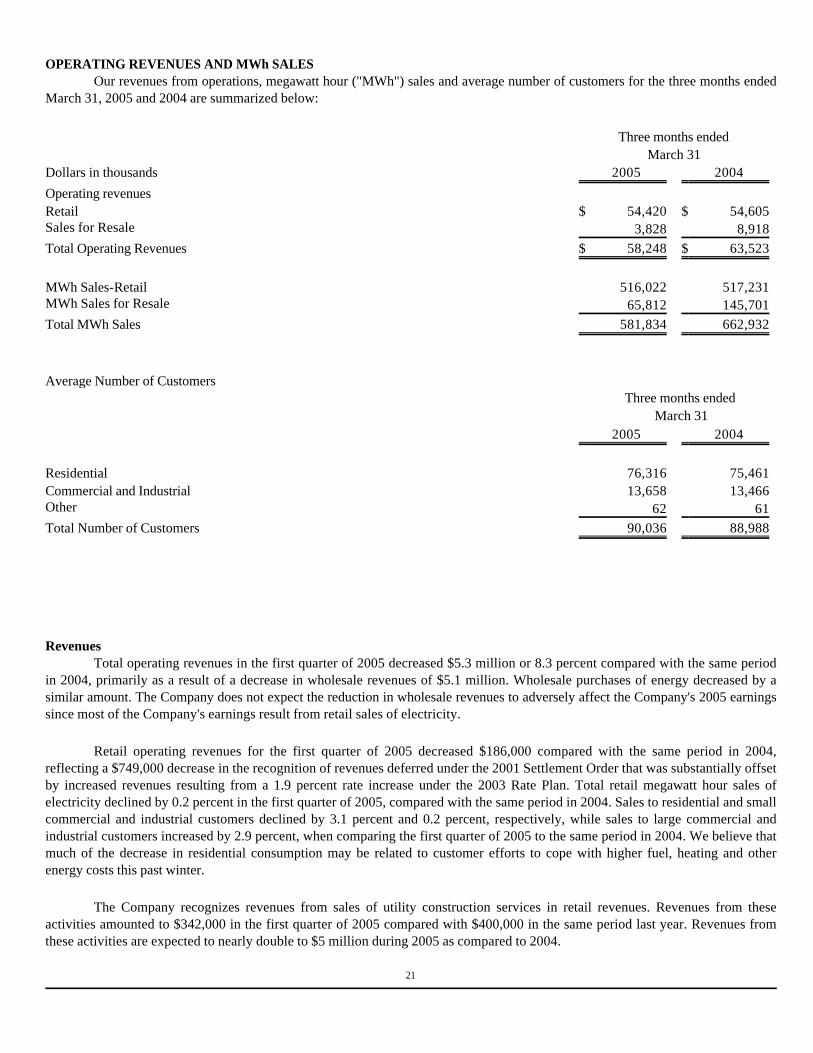

OPERATING REVENUES AND MWh SALES Our revenues from operations, megawatt hour ("MWh") sales and average number of customers for the three months ended

March 31, 2005 and 2004 are summarized below:

Revenues

Total operating revenues in the first quarter of 2005 decreased $5.3 million or 8.3 percent compared with the same period in 2004, primarily as a result of a decrease in wholesale revenues of $5.1 million. Wholesale purchases of energy decreased by a similar amount. The Company does not expect the reduction in wholesale revenues to adversely affect the Company's 2005 earnings since most of the Company's earnings result from retail sales of electricity.

Retail operating revenues for the first quarter of 2005 decreased $186,000 compared with the same period in 2004,

reflecting a $749,000 decrease in the recognition of revenues deferred under the 2001 Settlement Order that was substantially offset by increased revenues resulting from a 1.9 percent rate increase under the 2003 Rate Plan. Total retail megawatt hour sales of electricity declined by 0.2 percent in the first quarter of 2005, compared with the same period in 2004. Sales to residential and small commercial and industrial customers declined by 3.1 percent and 0.2 percent, respectively, while sales to large commercial and industrial customers increased by 2.9 percent, when comparing the first quarter of 2005 to the same period in 2004. We believe that much of the decrease in residential consumption may be related to customer efforts to cope with higher fuel, heating and other energy costs this past winter.

The Company recognizes revenues from sales of utility construction services in retail revenues. Revenues from these

activities amounted to $342,000 in the first quarter of 2005 compared with $400,000 in the same period last year. Revenues from these activities are expected to nearly double to $5 million during 2005 as compared to 2004.

Three months ended March 31

Dollars in thousands 2005 2004 Operating revenues Retail $ 54,420 $ 54,605 Sales for Resale 3,828 8,918 Total Operating Revenues $ 58,248 $ 63,523 MWh Sales-Retail 516,022 517,231 MWh Sales for Resale 65,812 145,701 Total MWh Sales 581,834 662,932 Average Number of Customers

Three months ended March 31

2005 2004

Residential 76,316 75,461 Commercial and Industrial 13,658 13,466 Other 62 61 Total Number of Customers 90,036 88,988

21

Customer Concentration Risk The Company’s major industrial customer, International Business Machines ("IBM"), accounted for 16.4 percent and 16.6

percent of retail revenue in 2004 and 2003, respectively. The Company currently estimates, based on a number of projected variables, the retail rate increase required from all retail customers by a hypothetical shutdown of the IBM facility to be approximately five percent, inclusive of projected related declines in sales to residential and commercial customers. OPERATING EXPENSES Power supply expenses

Power supply expenses decreased $4.8 million or 12.0 percent in the first quarter of 2005 compared with the same period in 2004, primarily as a result of an estimated $5.1 million decline in wholesale purchases for resale, and reductions in power supply expenses for VYPNC, offset in part by higher energy prices and an increase in purchases to replace reduced output from Company hydro-electric facilities.

Power supply expenses from VYNPC decreased $1.3 million or 13.0 percent during the first quarter of 2005 compared with

the same period of 2004, primarily due to a scheduled price reduction under VYNPC's contract with Entergy, and to decreased output at the Vermont Yankee nuclear power plant.

Company-owned generation expenses decreased $691,000 or 31.0 percent in the first quarter of 2005 compared with the

same period in 2004, primarily due to decreased production at peak generation facilities. Peak generation facilities are run only to maintain system reliability or when wholesale energy prices are extremely high.

The cost of power that we purchased from other companies decreased $2.9 million or 10.2 percent in the first quarter of

2005 compared with the same period in 2004, primarily due to reduced wholesale purchases for resale, offset in part by increased purchases to replace reduced output from Company hydro-electric facilities. Reduced output from Company hydro-electric facilities required the Company to purchase substantially higher-cost replacement energy. Other operating expenses

Other operating expenses increased $130,000 or 2.7 percent in the first quarter of 2005 compared with the same period in 2004 due primarily to increased regulatory expenses. Transmission expenses

Transmission expenses increased by approximately $462,000 or 12.5 percent for the three months ended March 31, 2005 compared with the same period in 2004, due to increased expenses from VELCO, reflecting increased transmission investment in Vermont. The Company's relative share of transmission expenses allocated from VELCO varies with the Company's relative share of the peak demand recorded on Vermont's transmission system.

The Independent System Operator for New England ("ISO-NE") was created to manage the New England Power Pool. ISO-NE implemented its Standard Market Design ("SMD") plan governing wholesale energy sales in New England on March 1, 2003. SMD includes a system of locational marginal pricing of energy, under which prices are determined by zone, and based in part on transmission congestion experienced in each zone. Currently, the State of Vermont constitutes a single zone under the plan, although pricing could eventually be determined on a more localized ("nodal") basis. FERC's affirmation of zonal pricing in December 2004 substantially reduced the likelihood that nodal pricing would replace zonal pricing. There are no current initiatives to impose nodal pricing or to change Vermont's use of zonal pricing to allocate congestion costs. We believe that nodal pricing, if it were ever adopted, could result in a material adverse impact on our power supply and/or transmission costs. Transmission projects, such as the recently approved Northwest Reliability Project ("NRP"), will reduce congestion and potential nodal pricing differences within Vermont, when they are completed. The NRP is not expected to be completed prior to 2007.

22

Maintenance expensesMaintenance expenses increased $74,000 or 3.3 percent for the three months ended March 31, 2005 compared with the

same period in 2004, primarily due to an increase in software maintenance costs. Depreciation and amortization expenses

Depreciation and amortization expenses for the quarter ended March 31, 2005 increased $287,000 or 8.2 percent compared with the same period in 2004, reflecting an increase in the depreciation of utility plant due to increased investment, and the amortization of regulatory assets in accordance with the 2003 Rate Plan. Taxes other than income taxes

Other tax expense for the first quarter of 2005 decreased by $56,000 or 3.2 percent compared with the same period in 2004 due to reductions in property taxes. Income taxes

Income taxes decreased $640,000 or 27.8 percent in the first quarter of 2005 compared with the same period in 2004 due to a decrease in pretax book income and use of additional income tax credits. The Company expects to recognize an income tax benefit of approximately three cents per share as a result of an income tax credit and deduction available in 2005 under the American Jobs Creation Act of 2004. The credit and deduction arise from our ownership interest in a biomass generation plant and from the production of electricity at Company hydro and fossil fuel plants. Interest Charges

Interest charges increased $80,000 or 4.9 percent in the first quarter of 2005 compared with the same period in 2004, due to a decrease in interest capitalized on utility plant construction. LIQUIDITY AND CAPITAL RESOURCES

At December 31, 2004, we had cash and cash equivalents of $1.7 million. In the first quarter of 2005, cash and cash equivalents increased $2.2 million primarily reflecting net cash provided by operating activities. Operating cash flows declined by $1.5 million from the same period last year primarily as the result of a decrease in net income and decreased deferred income tax liabilities. Net cash used by investing activities amounted to $4.4 million principally for investments to construct utility plant. We expect to spend approximately $18.4 million during the remainder of 2005, primarily for improvements in transmission, distribution and generation plant, and environmental expenditures. The Company plans to invest up to $20 million in VELCO through 2007 in support of various transmission projects, including a $4.8 million investment made in the last quarter of 2004. The Company also intends to contribute approximately $2.0 million in additional funds to its defined benefit plans in 2005.

On February 14, 2005, the annual dividend rate was increased from $0.88 to $1.00 per share, a payout ratio of approximately 48 percent based on 2004 earnings from continuing operations. On February 9, 2004, the annual dividend rate was increased from $0.76 per share to $0.88 per share, a payout ratio of approximately 44 percent based on 2003 earnings. The Company expects to increase the dividend on a consistent basis in the first quarter of each year to the middle of a payout ratio that falls between 50 percent and 70 percent of anticipated earnings, so long as financial and operating results permit. We believe this payout ratio to be consistent with that of other electric utilities having similar risk profiles.

23

We expect most of our construction expenditures and dividends to be financed by net cash provided by operating activities. We anticipate that we will issue long-term debt of up to $25 million in 2005 and/or 2006 for scheduled first mortgage bonds redemptions of $14 million and to finance increased investment in VELCO and generation. The Company has no plans at present to issue additional equity and seeks to maintain equity at between fifty and fifty-five percent of its capital structure. Material risks to cash flow from operations include regulatory risk, our customer concentration risk with IBM, slower than anticipated load growth, unfavorable economic conditions and increases in net power costs.

During June 2004, the Company negotiated a 364-day revolving credit agreement with Fleet Financial Services, Bank of America, successor joined by Sovereign Bank (the "BOA-Sovereign Agreement"). The BOA-Sovereign Agreement is for $30.0 million, unsecured, and allows the Company to choose any blend of a daily variable prime rate and a fixed term LIBOR-based rate. There was no short-term debt outstanding in the BOA-Sovereign Agreement at March 31, 2005, compared with $3.0 million outstanding at December 31, 2004. The BOA-Sovereign Agreement expires June 15, 2005. The Company expects to renew the BOA-Sovereign Agreement on similar terms and conditions.

The credit ratings of the Company's first mortgage bonds at March 31, 2005 were:

Moody's affirmed the Company's senior secured debt rating at Baa1, with a stable outlook on June 18, 2004.

On November 3, 2004, Standard and Poor's Ratings Services upgraded the Company's issuer credit rating to BBB from

BBB-.

In the event of a change in the Company's first mortgage bond credit rating to below investment grade, scheduled payments under the Company's first mortgage bonds would not be affected. Such a change would require the Company to post what would currently amount to a $4.3 million bond under our remediation agreement with the EPA regarding the Pine Street Barge Canal site. The Morgan Stanley Contract requires credit assurances if the Company's first mortgage bond credit ratings are lowered to below investment grade by any one of the two credit rating agencies listed above.

Moody's Standard &

Poor's First mortgage bonds Baa1 BBB

24

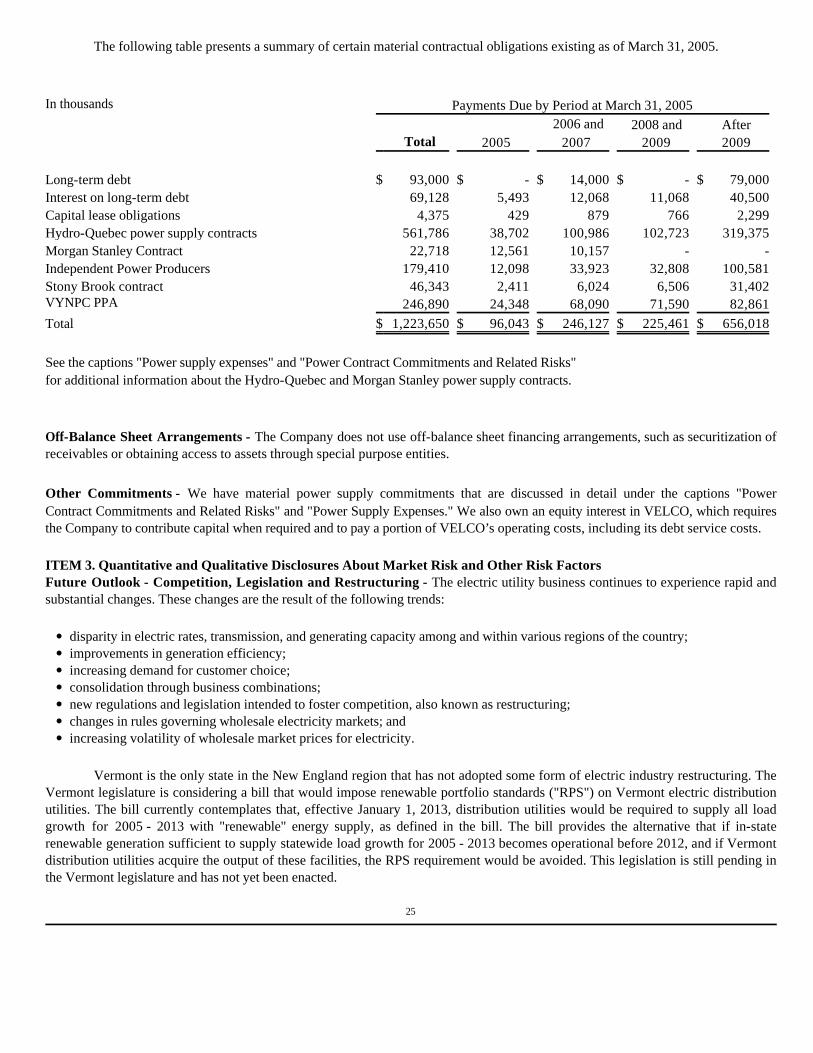

The following table presents a summary of certain material contractual obligations existing as of March 31, 2005.

Off-Balance Sheet Arrangements - The Company does not use off-balance sheet financing arrangements, such as securitization of receivables or obtaining access to assets through special purpose entities. Other Commitments - We have material power supply commitments that are discussed in detail under the captions "Power Contract Commitments and Related Risks" and "Power Supply Expenses." We also own an equity interest in VELCO, which requires the Company to contribute capital when required and to pay a portion of VELCO’s operating costs, including its debt service costs.

ITEM 3. Quantitative and Qualitative Disclosures About Market Risk and Other Risk Factors Future Outlook - Competition, Legislation and Restructuring - The electric utility business continues to experience rapid and substantial changes. These changes are the result of the following trends:

Vermont is the only state in the New England region that has not adopted some form of electric industry restructuring. The Vermont legislature is considering a bill that would impose renewable portfolio standards ("RPS") on Vermont electric distribution utilities. The bill currently contemplates that, effective January 1, 2013, distribution utilities would be required to supply all load growth for 2005 - 2013 with "renewable" energy supply, as defined in the bill. The bill provides the alternative that if in-state renewable generation sufficient to supply statewide load growth for 2005 - 2013 becomes operational before 2012, and if Vermont distribution utilities acquire the output of these facilities, the RPS requirement would be avoided. This legislation is still pending in the Vermont legislature and has not yet been enacted.

In thousands Payments Due by Period at March 31, 2005 2006 and 2008 and After Total 2005 2007 2009 2009

Long-term debt $ 93,000 $ - $ 14,000 $ - $ 79,000 Interest on long-term debt 69,128 5,493 12,068 11,068 40,500 Capital lease obligations 4,375 429 879 766 2,299 Hydro-Quebec power supply contracts 561,786 38,702 100,986 102,723 319,375 Morgan Stanley Contract 22,718 12,561 10,157 - - Independent Power Producers 179,410 12,098 33,923 32,808 100,581 Stony Brook contract 46,343 2,411 6,024 6,506 31,402 VYNPC PPA 246,890 24,348 68,090 71,590 82,861 Total $ 1,223,650 $ 96,043 $ 246,127 $ 225,461 $ 656,018 See the captions "Power supply expenses" and "Power Contract Commitments and Related Risks" for additional information about the Hydro-Quebec and Morgan Stanley power supply contracts.

· disparity in electric rates, transmission, and generating capacity among and within various regions of the country; · improvements in generation efficiency; · increasing demand for customer choice; · consolidation through business combinations; · new regulations and legislation intended to foster competition, also known as restructuring; · changes in rules governing wholesale electricity markets; and · increasing volatility of wholesale market prices for electricity.

25

Power Contract Commitments and Related Risks A primary factor affecting future operating results is the volatility of the wholesale electricity market. Periods frequently

occur when weather, availability of power supply resources and other factors cause significant differences between customer demand and electricity supply. Because electricity cannot be stored, in these situations the Company must buy or sell the difference into a marketplace that has experienced volatile energy prices. Volatility and market price trends also make it more difficult to extend or enter into new power supply contracts at prices that avoid the need for rate relief.

We have developed a power supply portfolio that meets approximately 90 percent of our estimated customer demand ("load") requirements through 2006. Our power supply contracts and resources significantly reduce the Company's exposure to volatility in wholesale energy market prices.

Vermont does not have a fuel or purchased-power adjustment clause that would allow increases in power supply costs to be recovered immediately in the rates we charge customers. Historically, however, the VPSB has allowed electric utilities to defer material unexpected increases in power supply costs to future periods to permit recovery in future rates. Vermont law also allows electric utilities to seek temporary rate increases if deemed necessary by the VPSB to provide adequate and efficient service or to preserve the viability of the utility.

Vermont Yankee - We have a 20 percent entitlement in Vermont Yankee plant output sold by Entergy to Vermont Yankee Nuclear Power Corporation ("VYNPC"), through a long-term purchase contract with Vermont Yankee (the "VYNPC Contract"). We generally purchase between 35 and 40 percent of our annual load requirements from VYNPC at rates that are presently well below market. We are responsible for the purchase of replacement power to serve our load requirements when the plant is not operating due to scheduled or unscheduled outages. In the first quarter of 2005, we purchased $8.7 million from VYNPC based on our entitlement share of plant output, compared to $10 million for the same period in 2004, reflecting price reductions and reduced deliveries under Vermont Yankee’s contract with Entergy.

Hydro Quebec - We purchase varying amounts of power from Hydro Quebec under the Vermont Joint Owners ("VJO")

Contract negotiated between the Company and Hydro Quebec. There are specific contractual provisions that provide that in the event any VJO member fails to meet its obligation under the contract with Hydro Quebec, the remaining VJO participants, including the Company, must "step-up" to the defaulting party's share on a pro rata basis. The Company is not aware of any instance where this provision has been invoked by Hydro Quebec. In the first quarter of 2005, we purchased $12.3 million of energy and related capacity under the existing contracts with Hydro Quebec, compared to $12.1 million for the same period in 2004.

Under the VJO Contract, Hydro Quebec had the right to reduce the load factor from 75 percent to 65 percent a total three

times over the life of the contract. Hydro Quebec exercised its third and last option in 2004 for deliveries occurring principally during 2005. Hydro Quebec retains the right to reduce the load factor by 10 percent up to five times, over the 2001 to 2015 period, if documented drought conditions exist in Quebec.

26

Morgan Stanley - We purchase approximately 16 percent of our load requirements under a contract with Morgan Stanley Capital Group, Inc. (the "Morgan Stanley Contract"), designed to manage some of the price risks associated with changing fossil fuel prices. The Morgan Stanley Contract price is substantially below current market prices and expires on December 31, 2006. The Company is unable to predict the price, contract duration or terms of any future power supply contract that could replace the Morgan Stanley Contract after it expires. Defined Benefit Plans

Due to sharp declines in the equity markets during 2001 and 2002, the relative funding level of defined benefit plan obligations decreased. The Company’s defined benefit plan assets are primarily made up of public equity and fixed income investments. Fluctuations in actual equity market returns as well as changes in general interest rates may result in increased or decreased defined benefit plan costs in future periods.

The Company’s funding policy is to make voluntary contributions to its defined benefit plans before ERISA or Pension Benefit Guaranty Corporation requirements mandate such contributions under minimum funding rules, and so long as the Company’s liquidity needs do not preclude such investments. The Company expects to contribute to defined benefit plans approximately $2.0 million during 2005. Power Supply Derivatives

The Morgan Stanley Contract is used to hedge our power supply costs against increases in fossil fuel prices. The Morgan Stanley Contract is a derivative under Statement of Financial Accounting Standards No. 133 ("SFAS 133"). Management has estimated the fair value of the future net benefit of this agreement at March 31, 2005 to be approximately $12.6 million.

We currently have an agreement that grants Hydro Quebec an option (the "9701 agreement") to call power at prices that are expected to be below estimated future market rates. This agreement is a derivative and is effective through 2015. Management’s estimate of the fair value of the future net cost for the 9701 agreement at March 31, 2005 is approximately $22.8 million. We sometimes use forward contracts to hedge forecasted calls by Hydro Quebec under the 9701 agreement.

The table below presents the Company’s market risk of the Morgan Stanley Contract and the 9701 agreement derivatives, estimated as the potential loss in fair value resulting from a hypothetical ten percent adverse change in wholesale energy prices, which nets to approximately $1.8 million. Actual results may differ materially from the table illustration. Under an accounting order issued by the VPSB, changes in the fair value of derivatives are deferred.

New Accounting Standards

See Part I-Item 1, Note 5, "New Accounting Standards" for information on the adoption of new accounting standards and the impact, if any, on the Company's financial position and operating results. ITEM 4. Disclosure Controls and Procedures

Pursuant to Rule 13a-15(b) under the Securities Exchange Act of 1934, the Company carried out an evaluation, with the participation of the Company's management, including the Company's President and Chief Executive Officer, and Chief Financial Officer and Treasurer, of the effectiveness of the Company's disclosure controls and procedures (as defined under Rule 13a-15(e) under the Securities Exchange Act of 1934) as of the end of the period covered by this report. Based upon that evaluation, the Company's President and Chief Executive Officer, and Chief Financial Officer and Treasurer, concluded that the Company's disclosure controls and procedures are effective.

Commodity Price Risk March 31, 2005In thousands Fair Value(Cost) Market RiskMorgan Stanley Contract $ 12,554 $ 1,873 9701 agreement (25,457) (3,680)

$ (12,903) $ (1,807)

27

Management’s report on the Company’s internal control over financial reporting was included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2004 and concluded that, as of December 31, 2004, the Company did not maintain effective internal control over financial reporting due to a material weakness as a result of deficiencies in both the design and operating effectiveness of controls associated with the Company’s accounting for income taxes. During the first quarter of 2005, management conducted testing and enhancement of the Company’s internal controls associated with accounting for income taxes and engaged a public accounting firm to assist management with its review of all income tax entries for the quarter, the statutory rate reconciliation, the Company's treatment of new tax credits and deductions, if applicable, and timing differences. These ongoing efforts, which required certain changes to the Company’s internal controls associated with accounting for income taxes, and which are subject to audit by the Company’s independent registered accounting firm at year-end, have improved the design and operational effectiveness of the Company's control processes and systems for financial reporting. Based on these efforts, management believes that the deficiencies in both the design and operating effectiveness of controls associated with the Company’s accounting for income taxes have been remedied and that the Company no longer has a material weakness in its internal control over financial reporting. It should be noted that the design of any system of controls is based, in part, on certain assumptions about the likelihood of future events, and that only reasonable assurance can be given that any internal control system will succeed in achieving its stated goals against all potential future conditions, regardless of how remote.

Except as described above, there has been no change in our internal control over financial reporting during the quarter ended March 31, 2005, that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting

28

GREEN MOUNTAIN POWER CORPORATIONMarch 31, 2005

PART II - OTHER INFORMATION

ITEM 6. ExhibitsExhibit 31.1, Certification by Christopher L. Dutton, President and Chief Executive Officer of Green Mountain Power Corporation, pursuant to Rules 13a-14(a) and Rule 15d-14(a) promulgated under the Securities Exchange Act of 1934, as adopted pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. Exhibit 31.2, Certification by Robert J. Griffin, Chief Financial Officer, Vice President, Treasurer and Principal Accounting Officer of Green Mountain Power Corporation, pursuant to Rules 13a-14(a) and Rule 15d-14(a) promulgated under the Securities Exchange Act of 1934, as adopted pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. Exhibit 32.1, Certification by Christopher L. Dutton, President and Chief Executive Officer of Green Mountain Power Corporation, and Robert J. Griffin, Chief Financial Officer, Vice President Treasurer and Principal Accounting Officer of Green Mountain Power Corporation, pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002.

Item 1. Legal Proceedings See Note 3 of Notes to Consolidated Financial Statements Item 2. Unregistered Sales of Equity Securities and Use of Proceeds NONE Item 3. Defaults Upon Senior Securities NONE Item 4. Submission of Matters to a Vote of Security Holders NONE Item 5. Other Information NONE

29

GREEN MOUNTAIN POWER CORPORATIONSIGNATURES