Embed Size (px)

Citation preview

The Week in Review For the period May 21, 2018 – May 25, 2018

News This Week

Foreign reserves reach below USD17bn mark

Current account deficit widens 50% to USD14.04bn in July-April

Moody’s reaffirms Pakistan’s rating, but vulnerabilities remain

July-March period external debt servicing reaches USD5bn

ECC approves fresh borrowing of PKR50bn to pay circular debt

Pakistan's textile exports jump 8%

DG Khan Cement announces completion of Pakistan’s biggest

USD300mn plant

Meezan Bank plans to raise PKR7bn through Tier 1 Sukuk

Domestic auto makers halt fresh booking from non-filers

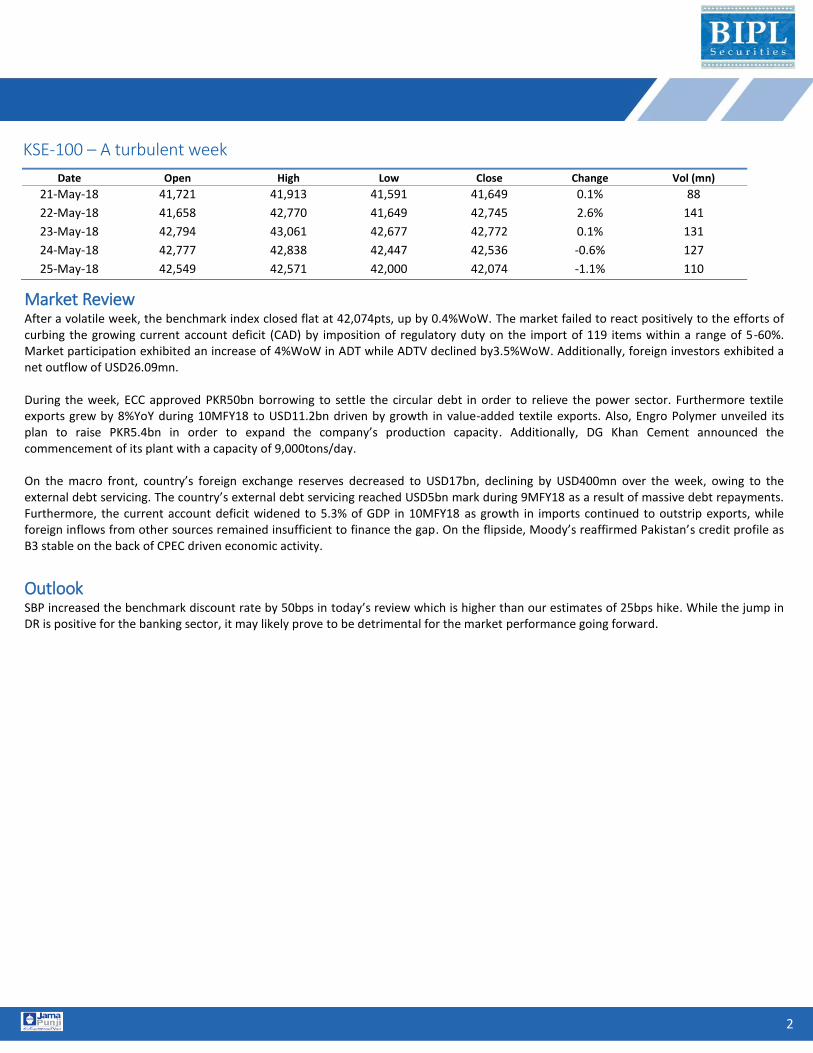

KSE-100 – A turbulent week

Stock Market Overview

After a volatile week, the benchmark index closed flat at 42,074pts, up by 0.4%WoW. The market failed to react positively to the efforts of curbing the growing current account deficit (CAD) by imposition of regulatory duty on the import of 119 items within a range of 5-60%. Market participation exhibited an increase of 4%WoW in ADT while ADTV declined by3.5%WoW. Additionally, foreign investors exhibited a net outflow of USD26.09mn.

UNITY, PSX, PAKT, FML and EFOODS were the major gainers while BATA, NATF, SHFA, COLG, and IBFL were the major losers in the benchmark KSE-100 this week.

REP 039 BIPL Securities Limited 5thFloor, Trade Centre, I.I. Chundrigar Road, Karachi 1

www.jamapunji.pk

Market Review After a volatile week, the benchmark index closed flat at 42,074pts, up by 0.4%WoW. The market failed to react positively to the efforts of curbing the growing current account deficit (CAD) by imposition of regulatory duty on the import of 119 items within a range of 5-60%. Market participation exhibited an increase of 4%WoW in ADT while ADTV declined by3.5%WoW. Additionally, foreign investors exhibited a net outflow of USD26.09mn. During the week, ECC approved PKR50bn borrowing to settle the circular debt in order to relieve the power sector. Furthermore textile exports grew by 8%YoY during 10MFY18 to USD11.2bn driven by growth in value-added textile exports. Also, Engro Polymer unveiled its plan to raise PKR5.4bn in order to expand the company’s production capacity. Additionally, DG Khan Cement announced the commencement of its plant with a capacity of 9,000tons/day. On the macro front, country’s foreign exchange reserves decreased to USD17bn, declining by USD400mn over the week, owing to the external debt servicing. The country’s external debt servicing reached USD5bn mark during 9MFY18 as a result of massive debt repayments. Furthermore, the current account deficit widened to 5.3% of GDP in 10MFY18 as growth in imports continued to outstrip exports, while foreign inflows from other sources remained insufficient to finance the gap. On the flipside, Moody’s reaffirmed Pakistan’s credit profile as B3 stable on the back of CPEC driven economic activity.

Outlook SBP increased the benchmark discount rate by 50bps in today’s review which is higher than our estimates of 25bps hike. While the jump in DR is positive for the banking sector, it may likely prove to be detrimental for the market performance going forward.

KSE-100 – A turbulent week

Date Open High Low Close Change Vol (mn)

21-May-18 41,721 41,913 41,591 41,649 0.1% 88

22-May-18 41,658 42,770 41,649 42,745 2.6% 141

23-May-18 42,794 43,061 42,677 42,772 0.1% 131

24-May-18 42,777 42,838 42,447 42,536 -0.6% 127

25-May-18 42,549 42,571 42,000 42,074 -1.1% 110

2 2

3

News This Week

Economic highlights & Data points

Foreign reserves reach below USD17bn mark | (BR): Following the massive external debt servicing, Pakistan's total liquid foreign reserves further declined over USD400mn to reach below USD17bn mark end of last week. Current account deficit widens 50% to USD14.04bn in July-April | (The News): Current account deficit widened to 5.3% of gross domestic product, or USD14.04bn, in 10MFY18 as merchandise imports continued to broadly outstrip exports, while foreign inflows from other sources remained insufficient to finance the gap, the central bank data showed on Friday. Moody’s reaffirms Pakistan’s rating, but vulnerabilities remain | (Dawn): Moody’s Investors Service continues to expect solid economic activity, driven by investments related to the China-Pakistan Economic Corridor (CPEC) while it reaffirmed Pakistan’s credit profile as B3 stable. July-March period external debt servicing reaches USD5bn | (BR): The country's external debt servicing has reached some USD5bn mark during 9MFY18 due to massive repayments of public debt. Economists said the higher external debt servicing is mainly due to scheduled repayments to Paris Club and other financial institutions under the public debt.

Sector and Corporate highlights

Meezan Bank plans to raise PKR7bn through Tier 1 Sukuk | (The News): Meezan Bank Limited was planning to raise up to PKR7bn by issuing Tier 1 Islamic bond or Sukuk in the coming few months, industry officials said on Wednesday. According to the details of the structure as provided by the source, the total issue would be PKR5bn with a green show option of PKR2bn. The minimum investment is set to be PRK1mn. DG Khan Cement announces completion of Pakistan’s biggest USD300mn plant | (The News): DG Khan Cement on Wednesday announced the start of the country’s biggest cement plant with around 9,000 tons/day capacity at an estimated cost of over USD300mn. The largest vertical cement grinding mill with cope drive has started trial operations together with cement silos and packaging plant. Also, successful commissioning has been completed in raw material crushing, transportation and storage departments. Domestic auto makers halt fresh booking from non-filers | (The News): Local automobile manufacturers have sent a strong warning to their respective buyers supporting the government’s move to widen the tax net by starting to refuse purchase or booking of new cars by non-filers. ECC approves fresh borrowing of PKR50bn to pay circular debt | (Tribune): The federal government quietly approved on Thursday another loan of PKR50bn from commercial banks to retire circular debt in the power sector, taking total bank borrowings to PKR230bn in two months to manage liquidity. The decision was taken just one week before the tenure ends of the current government that failed to address the power sector’s bottlenecks despite declaring it as its top priority. Engro Polymer plans to raise PKR5.4bn for expansion| (The News): Engro Polymer and Chemicals (EPCL) on Friday unveiled a plan to raise PKR5.4bn to expand the company’s production capacity. EPCL decided to issue right shares amounting to 37% – approximately 37 shares for every 100 shares held by the shareholders of the company. The company is to increase the volume of shares by 245.45mn through the issuance of right shares. Its price would be PKR22/sh including PKR12/sh as the premium. Pakistan's textile exports jump 8%| (Dawn): Exports of textile and clothing products recorded 8% growth year-on-year to USD11.2bn in 10MFY18, the Pakistan Bureau of Statistics (PBS) reported on Monday.

4

Stock Market – Last week in pictorals

Chart 1: KSE-100 Index

Source: PSX

Chart 2: KSE Advance/Decline Ratio

Source: PSX

Chart 3: Pak Foreign Portfolio Flows (US$mn; US$=PKR115)

Source: NCCPL

Chart 4: KSE- Volumes & Values

Source: PSX

Chart 5: Price to Money Ratio

Source: NCCPL

Chart 6: Off market activity

Source: PSX

Economy Watch

Chart 7: Revenue Collection (PKRbn)

Source: SBP

Chart 8: Forex Reserves (US$mn)

Source: SBP

Chart 9: Import & Export (US$mn)

Source: SBP

Chart 10: Foreign Exchange Rate (PKR/US$)

Source: SBP

Chart 11: 6-mth T-Bill Yield (%)

Source: SBP

Chart 12: Yield Curve (%)

Source: SBP

5

Stock Market Synopsis Last week This Week %Change 1M 3M 12M

Mkt. Cap (US $ bn) 74.7 75.5 1.0% 81.5 81.3 99.6

Avg. Dly T/O (mn. shares) 114.9 119.5 4.0% 147.7 180.9 185.3

Avg. Dly T/O (US$ mn.) 44.4 42.9 -3.5% 52.9 68.1 82.3

No. of Trading Sessions 5.0 5.0 0.0 22.0 64.0 250.0

KSE 100 Index 41,623.5 42,074.1 1.1% 45,718.3 43,267.2 52,869.0

KSE ALL Share Index 30,397.7 30,718.7 1.1% 33,091.3 31,238.0 36,224.4

Chart 13: KSE-100 Active Issues (ADTO-million shares)

Source: PSX

Chart 14: KSE-100 Least Traded Issues (ADTO- shares)

Source: PSX

Chart 15: KSE-100 Top Gainer (% change)

Source: PSX

Chart 16: KSE-100 Top Losers (% change)

Source: PSX

6

Disclaimer

This research report is for information purposes only and does not constitute nor is it intended as an offer or solicitation for the purchase or sale of securities or other financial instruments. Neither the

information contained in this research report nor any future information made available with the subject matter contained herein will form the basis of any contract. Information and opinions contained

herein have been compiled or arrived at by BIPL Securities Limited from publicly available information and sources that BIPL Securities Limited believed to be reliable. Whilst every care has been taken in

preparing this research report, no research analyst, director, officer, employee, agent or adviser of any member of BIPL Securities Limited gives or makes any representation, warranty or undertaking,

whether express or implied, and accepts no responsibility or liability as to the reliability, accuracy or completeness of the information set out in this research report. Any responsibility or liability for any

information contained herein is expressly disclaimed. All information contained herein is subject to change at any time without notice. No member of BIPL Securities Limited has an obligation to update,

modify or amend this research report or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or

subsequently becomes inaccurate, or if research on the subject company is withdrawn. Furthermore, past performance is not indicative of future results.

The investments and strategies discussed herein may not be suitable for all investors or any particular class of investor. Investors should make their own investment decisions using their own

independent advisors as they believe necessary and based upon their specific financial situations and investment objectives when invest ing. Investors should consult their independent advisors if they

have any doubts as to the applicability to their business or investment objectives of the information and the strategies discussed herein. This research report is being furnished to certain persons as

permitted by applicable law, and accordingly may not be reproduced or circulated to any other person without the prior written consent of a member of BIPL Securities Limited. This research report may

not be relied upon by any retail customers or person to whom this research report may not be provided by law. Unauthorized use or disclosure of this research report is strictly prohibited. Members of

BIPL Securities and/or their respective principals, directors, officers, and employees and their families may own, have positions or affect transactions in the securities or financial instruments referred

herein or in the investments of any issuers discussed herein, may engage in securities transactions in a manner inconsistent with the research contained in this research report and with respect to

securities or financial instruments covered by this research report, may sell to or buy from customers on a principal basis and may serve or act as director, placement agent, advisor or lender, or make a

market in, or may have been a manager or a co-manager of the most recent public offering in respect of any investments or issuers of such securities or financial instruments referenced in this research

report or may perform any other investment banking or other services for, or solicit investment banking or other business from any company mentioned in this research report. Investing in Pakistan

involves a high degree of risk and many persons, physical and legal, may be restricted from dealing in the securities market of Pakistan. Investors should perform their own due diligence before investing.

No part of the compensation of the authors of this research report was, is or will be directly or indirectly related to the specific recommendations or views contained in the research report. By accepting

this research report, you agree to be bound by the foregoing limitations.

BIPL Securities Limited and / or any of its affiliates, which operate outside Pakistan, do and seek to do business with the company(s) covered in this research document. Investors should consider this

research report as only a single factor in making their investment decision. BIPL Securities Limited prohibits research personnel from disclosing a recommendation, investment rating, or investment

thesis for review by an issuer/company prior to the publication of a research report containing such rating, recommendation or investment thesis.

BIPL Securities Limited endeavors to make all reasonable efforts to disseminate its publication to all eligible clients in a timely manner through either physical or electronic distribution such as mail, fax

and/or email. Nevertheless, not all clients may receive the material at the same time.

![HBL MobileHabib Bank Limited Habib Bank Plaza I.I. Chundrigar Road, Karachi-75650, Pakistan Phone: (92-21) 32418000 [50 lines] Registered Office Habib Bank Limited 9th Floor, Habib](https://img.pdfslide.us/doc/110x75/60d994921b247557bf192842/hbl-mobile-habib-bank-limited-habib-bank-plaza-ii-chundrigar-road-karachi-75650.jpg)