Embed Size (px)

Citation preview

Corporate Presentation

Fortescue Metals Group LtdOctober 2012

For

per

sona

l use

onl

y

Important NoticeThe purpose of this presentation is to provide general information about Fortescue Metals Group Ltd ("Fortescue"). It is not recommended that any person makes any investment decision in relation to Fortescue based on this presentation.

This presentation contains certain statements which may constitute "forward-looking statements". Such statements are only predictions and are subject to inherent risks and uncertainties which could cause actual values, results, performance or achievements to differ materially from those expressed, implied or projected in any forward-looking statements.

No representation or warranty, express or implied, is made by Fortescue that the material contained in this presentation will beachieved or prove to be correct. Except for statutory liability which cannot be excluded, each of Fortescue, its officers, employees and advisers expressly disclaims any responsibility for the accuracy or completeness of the material contained in this presentation and excludes all liability whatsoever (including in negligence) for any loss or damage which may be suffered by any person as a consequence of any information in this presentation or any error or omission therefrom. Fortescue accepts no responsibility to update any person regarding any inaccuracy, omission or change in information in this presentation or any other information madeavailable to a person nor any obligation to furnish the person with any further information.

Additional InformationThis presentation should be read in conjunction with the Annual Financial Report as at 30 June 2012, the half year financial statements together with any announcements made by Fortescue in accordance with its continuous disclosure obligations arisingunder the Corporations Act 2001.

All amounts within this presentation are stated in United States Dollars consistent with the Functional Currency of the Fortescue Metals Group Limited.

Tables contained within this presentation may contain immaterial rounding differences.

Disclaimer

2

For

per

sona

l use

onl

y

The Fortescue storyWorld’s 4th biggest seaborne exporter

Strong culturedelivers record results

57.5mtrecord shipped in FY2012

Top 25 ASX listed company

mtpacurrentrun rate

12bt resource

Target run rate

155mtpa

3

For

per

sona

l use

onl

y

See our operations in the PilbaraCorporate DVD

4

For

per

sona

l use

onl

y

A differentiated modelDelivering results

CultureFortescue’s unique culture is the key

RelationshipsDirect relationships with sub contractors and local suppliers

ChinaLeveraging China’s growth and manufacturing capability

SpeedSpeed of delivery – time is money

Planning Planning for scale today and efficiency into the future

5

For

per

sona

l use

onl

y

6

2012 in review

For

per

sona

l use

onl

y

7

Operations, 30%+ growth across all areasContinuing growth trajectory over FY13

Mining Processed Port

Ore Mined (wmt) Ore Processed (wmt) Total Ore Shipped (wmt)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY09 FY10 FY11 FY120.0

10.0

20.0

30.0

40.0

50.0

60.0

FY09 FY10 FY11 FY120.0

10.0

20.0

30.0

40.0

50.0

60.0

FY09 FY10 FY11 FY12

46% 33% 41%

Mill

ion

tonn

es

Mill

ion

tonn

es

Mill

ion

tonn

es

For

per

sona

l use

onl

y

Financial highlightsRecord FY12 performance

Fortescue tonnes shipped up 38% yoy

Revenues up 23% yoy

C1 average

EBITDA up 14% yoy

NPAT up 53%

fully franked dividend

55.8mt $6.7bn $48/wmt$3bn$1.6bnA$0.08

8

For

per

sona

l use

onl

y

9

EBITDA analysis

9

• Volume benefits offset by lower index prices• Higher costs from Christmas Creek ramp up, strip ratio and strong AUD

EBITDA Variance (US$m)

For

per

sona

l use

onl

y

10

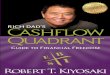

Earnings analysis

10

Return on equity

• Sustained ~ 50% ROE

Earnings and cash flow per share (US$)

• 52% increase in earnings per share

• Consistency in cash flow per share

18.9

32.9

50.142.0

89.3 90.2

2010 2011 2012

EPS CFPS

49.9% 52.1% 50.3%

2010 2011 2012

For

per

sona

l use

onl

y

11

Expansion facilities structured for flexibility

• Diversification of funding sources and maturity profiles• Early call options provide repayment flexibility

$750$600

$2,040

$600

$154

$1,000$900

$99 $100

$1,500

$1,000

$750

$866

$490

0

500

1000

1500

2000

2500

US$

m

CY2012 CY2013 CY2014 CY2015 CY2016 CY2017 CY2018 CY2019 CY2020 CY2021 CY2022

* Note the Master Finance Lease and Export Credit facilities amortises straight line to maturity

CAPEX Term Loan Revolving Credit Facility Senior Unsecured Note Unsecured Loan Note Preference Shares Master Lease Facility* Export Credit Facility*

For

per

sona

l use

onl

y

12

Market

For

per

sona

l use

onl

y

13

Iron Ore Price (62% Fe CFR – Platts IODEX China)

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

$200.00

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Jun-

12

Jul-1

2

Aug

-12

Sep

-12

History shows price volatilityStrong rebounds follow price drops

For

per

sona

l use

onl

y

14

Decisive response to market conditionsSecuring profitability and liquidity

$300m operating cost savings

FY13 capital down US$1.6bn

Chichester expansion 95mtpa Dec 2012

Solomon Firetail 20mtpa March 2013

March 2013 115mtpa

Kings and 155mtpa on market recovery

US$4.5bn debt restructureFor

per

sona

l use

onl

y

15

Fortescue cost per tonne 155mtpa $55*

Chinese cost curve to support pricesWith Fortescue products at lower end of cost curve

Source: Metalytics prepared March 2012

Cumulative mt (wet, as delivered)

US$

/dry

tonn

e C

FR e

quiv

alen

t

200

150

100

50

0

0 100 200 300 400 500 600 700 800 900 1,000

Domestic Chinese Ore

Australia

Brazil

India

South Africa

Other

Firetail cost per tonne $40*

* Estimated C1 costs at full production

For

per

sona

l use

onl

y

16

C1 costDecreasing cost profile

* Estimated C1 costs at full production^ C1 costs estimated from Metalytics industry US$/dry tonne CFR equivalent analysis

0

5

10

15

20

25

30

35

40

45

50

Fortescue Firetail* RIO^ BHP^ Vale^

$/wmt

Industry leaders^

For

per

sona

l use

onl

y

Long term confidence in ChinaLower growth rates but still strong in absolute volumes

• Strong underlying economy

• Stimulus packages

• Regime change

• Short term volatility rebound

• De-stocking

17

For

per

sona

l use

onl

y

18

Additional approvals

7 port and channel projects

13 highway projects

10 urban waste plant projects

Stimulus package announcedApproves US$157 billion infrastructure projects

urban railway projectsUS$133 billion

25Near term steel

consumption growth

infrastructure and urbanisation

For

per

sona

l use

onl

y

19

Expansion and Development

For

per

sona

l use

onl

y

2020

The quarterly milestone calendarForging ahead

Christmas Creek 2nd OPF

Train unloadersSolomon Firetail

115mtpa run rate

DEC QTR

SEP QTR

MAR QTR

JUN QTR

FY2013

For

per

sona

l use

onl

y

Financial strength will follow expansionCashflow will be harnessed for financial de-risking

Strong operations:• Expanded product range

• Low Solomon Strip Ratio < 2 : 1

• Target Solomon C1 cost of US$25 - 30/wmt*

• C1 cost in lowest 1/3rd of global cost curve

• Economies of scale + productivity gains hold wages inflation

Strong balance sheet:• Gearing reduction to follow production ramp up

• Preferred gearing range 30 – 40% by FYE14

• Balance sheet flexibility

* Assumes parity exchange rate.

21

For

per

sona

l use

onl

y

22

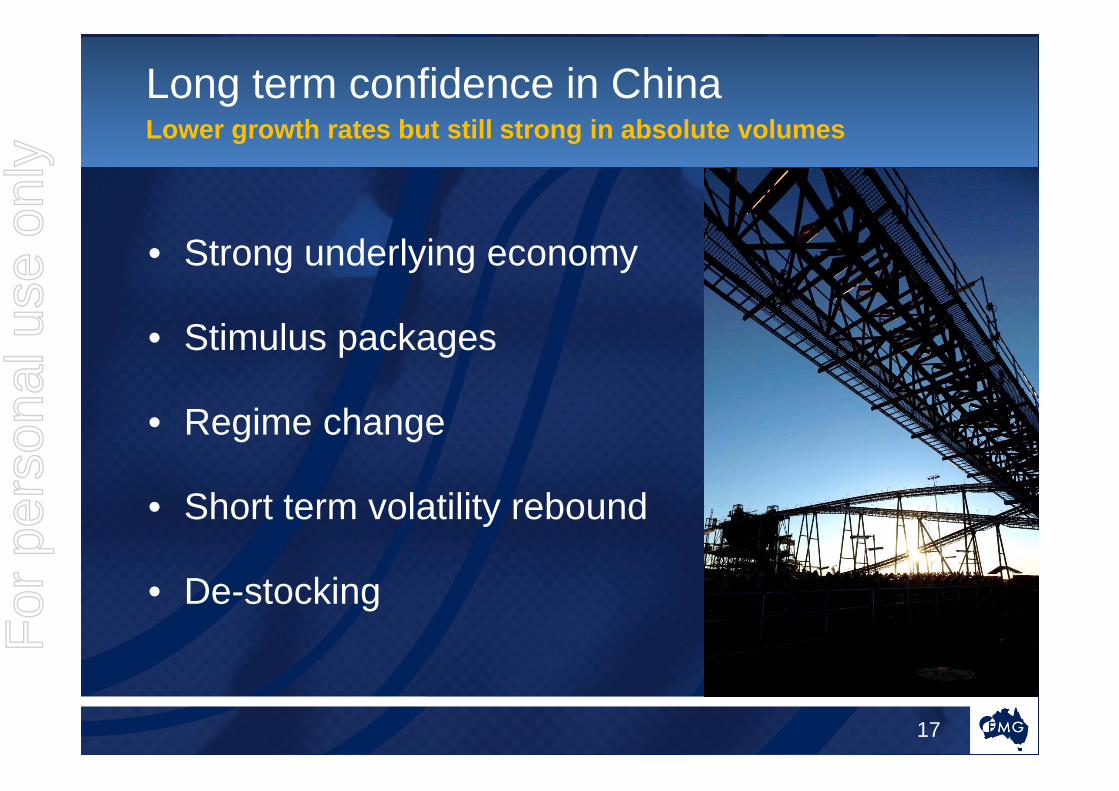

Fortescue has the dominant Pilbara land position

Fortescue: 85,000km2

Rio: 14,230km2

BHP: 8,195km2

For

per

sona

l use

onl

y

23

Fortescue

23

Flexible design for future growthFifth berth approved

* 120mtpa allocated priority capacity

For

per

sona

l use

onl

y

2424

2,266 2,227 2,143 2,550 2,550

695 695 695 695 6951,715 2,224 2,860

3,070 3,070

624 6241,032

2,013

1,2301,230

2,465

3,236

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2008 2009 2010 2011 2012

Min

eral

Res

ourc

es (M

t)

Fiscal Year Chichester Hub Chichester Other Solomon Hub Western Hub Nyidinghu Magnetite

1.5btAnnualised growth of

per annum

Resource portfolio sets expansion platformTo leverage existing assets for low cost growth

• Supports low cost Brownfield opportunities at both the Chichester and Solomon Hubs

For

per

sona

l use

onl

y

Deleverage following expansion

Expansion to 155mtpa

Strong FY2012 results

Building one of the world’s great resourcecompanies

Unique culture drives performance

Flexible growth pipeline

25

For

per

sona

l use

onl

y

26

Low cost brownfield expansion opportunities

Potential 10mtpa Chichester expansion

Low capital intensity ~US$20/t at the mine

OPF mods, debottlenecking, stockyard upgrades

Solomon brownfield opportunities to be investigated post Kings completion

For

per

sona

l use

onl

y

2727

Further low Phos opportunities in the East Chichester

• Existing resource and large exploration potential – Mt Lewin and Tongololo• Low Phos ore to support blending options

20 km

MappedMapped mineralisation

Resource outline

Proposed drilling

For

per

sona

l use

onl

y

Proudly supporting:

Sign up to alerts online:

www.fmgl.com.au

For

per

sona

l use

onl

y