Embed Size (px)

DESCRIPTION

explains how to create cashflow statements

Citation preview

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 1

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 1

IntroductionLearning objective

prepare a statement of cash flows using the direct method

prepare a statement of cash flows using the indirect method

usefulness of cash flow information interpret a statement of cash flows

all the above will is for a single entity as per IAS 7

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 2

Definition of Cash flow statementIt is a financial statement that

shows how changes in thestatement of financial position andincome affect cash and cashequivalents, and breaks the analysisdown to operating, investing, andfinancing activities.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 3

Definition of other terms1. Cash comprises cash on hand and demand

deposits2. Cash equivalents are short-term, highly

liquid investments that are readilyconvertible to known amounts of cash andwhich are subject to an insignificant risk ofchanges in value. Eg treasury bills

3. Cash flows are inflows and outflows of cashand cash equivalents.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 4

Definition of other termsOperating activities are the principal revenue-

producing activities of the entity and other activities that are not investing or financing activities.

5. Investing activities are the acquisition and disposal of non-current assets and other investments not included in cash equivalents.

6. Financing activities are activities that result in changes in the size and composition of the equitycapital and borrowings of the entity.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 5

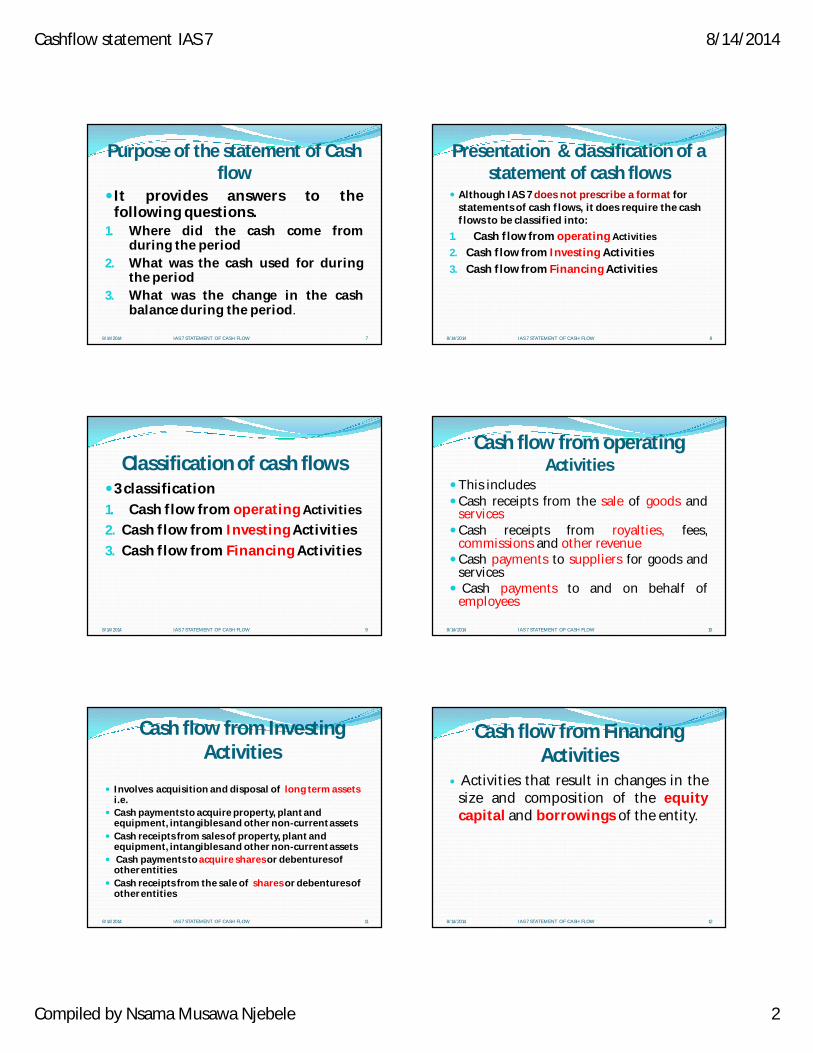

Purpose of the statement of Cash flow

The Primary purpose is to provide information about an entity's cash receipts and cash payment.Provide information on cash basis

about the operating ,investing andfinancing activities of the company

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 6

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 2

Purpose of the statement of Cash flow

It provides answers to thefollowing questions.

1. Where did the cash come fromduring the period

2. What was the cash used for duringthe period

3. What was the change in the cashbalance during the period.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 7

Presentation & classification of a statement of cash flows

Although IAS 7 does not prescribe a format for statements of cash flows, it does require the cash flows to be classified into:

1. Cash flow from operating Activities

2. Cash flow from Investing Activities3. Cash flow from Financing Activities

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 8

Classification of cash flows3 classification1. Cash flow from operating Activities2. Cash flow from Investing Activities3. Cash flow from Financing Activities

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 9

Cash flow from operating Activities

This includesCash receipts from the sale of goods and

servicesCash receipts from royalties, fees,

commissions and other revenueCash payments to suppliers for goods and

services Cash payments to and on behalf of

employees

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 10

Cash flow from Investing Activities

Involves acquisition and disposal of long term assets i.e.

Cash payments to acquire property, plant and equipment, intangibles and other non-current assets

Cash receipts from sales of property, plant and equipment, intangibles and other non-current assets

Cash payments to acquire shares or debentures of other entities

Cash receipts from the sale of shares or debentures of other entities

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 11

Cash flow from Financing Activities

Activities that result in changes in thesize and composition of the equitycapital and borrowings of the entity.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 12

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 3

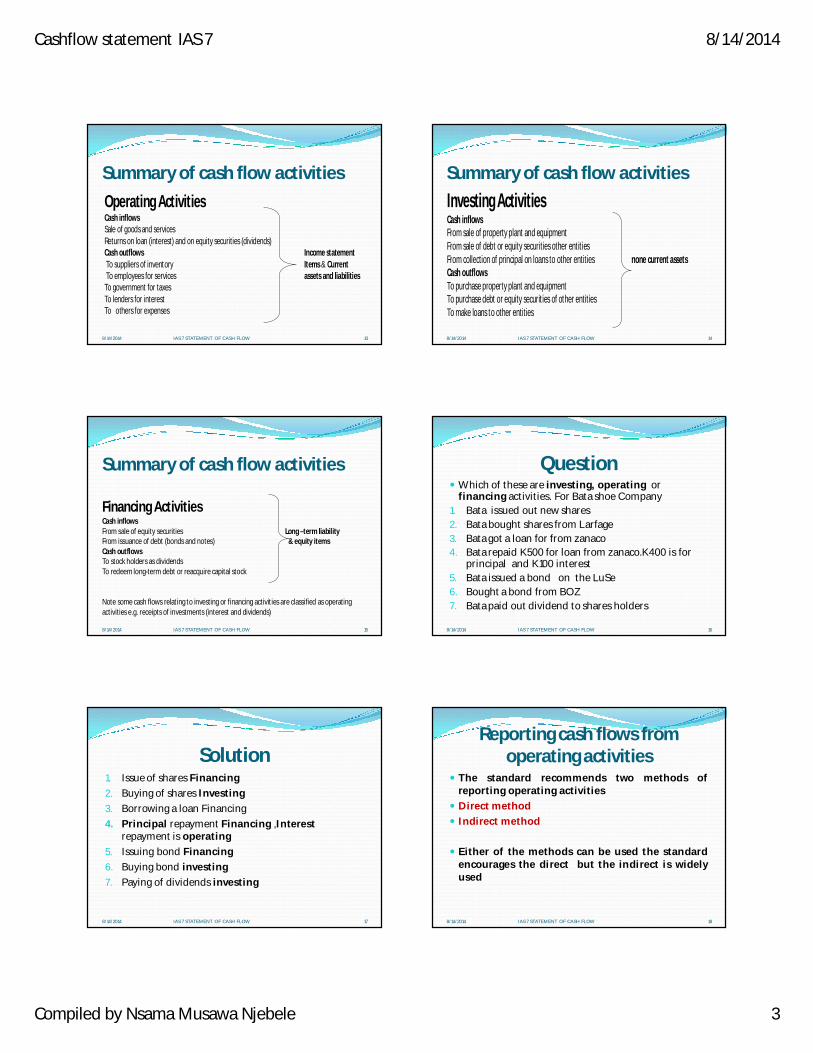

Summary of cash flow activities

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 13

Operating Activities Cash inflows Sale of goods and services Returns on loan (interest) and on equity securities (dividends) Cash outflows Income statement To suppliers of inventory Items & Current To employees for services assets and liabilities To government for taxes To lenders for interest To others for expenses

Summary of cash flow activities

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 14

Investing Activities Cash inflows From sale of property plant and equipment From sale of debt or equity securities other entities From collection of principal on loans to other entities none current assets Cash outflows To purchase property plant and equipment To purchase debt or equity securities of other entities To make loans to other entities

Summary of cash flow activities

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 15

Financing Activities Cash inflows From sale of equity securities Long –term liability From issuance of debt (bonds and notes) & equity items Cash outflows To stock holders as dividends To redeem long-term debt or reacquire capital stock Note some cash flows relating to investing or financing activities are classified as operating activities e.g. receipts of investments (interest and dividends)

Question Which of these are investing, operating or

financing activities. For Bata shoe Company1. Bata issued out new shares2. Bata bought shares from Larfage3. Bata got a loan for from zanaco4. Bata repaid K500 for loan from zanaco.K400 is for

principal and K100 interest5. Bata issued a bond on the LuSe6. Bought a bond from BOZ7. Bata paid out dividend to shares holders

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 16

Solution1. Issue of shares Financing2. Buying of shares Investing3. Borrowing a loan Financing4. Principal repayment Financing ,Interest

repayment is operating5. Issuing bond Financing6. Buying bond investing7. Paying of dividends investing

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 17

Reporting cash flows from operating activities

The standard recommends two methods ofreporting operating activities

Direct method Indirect method

Either of the methods can be used the standardencourages the direct but the indirect is widelyused

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 18

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 4

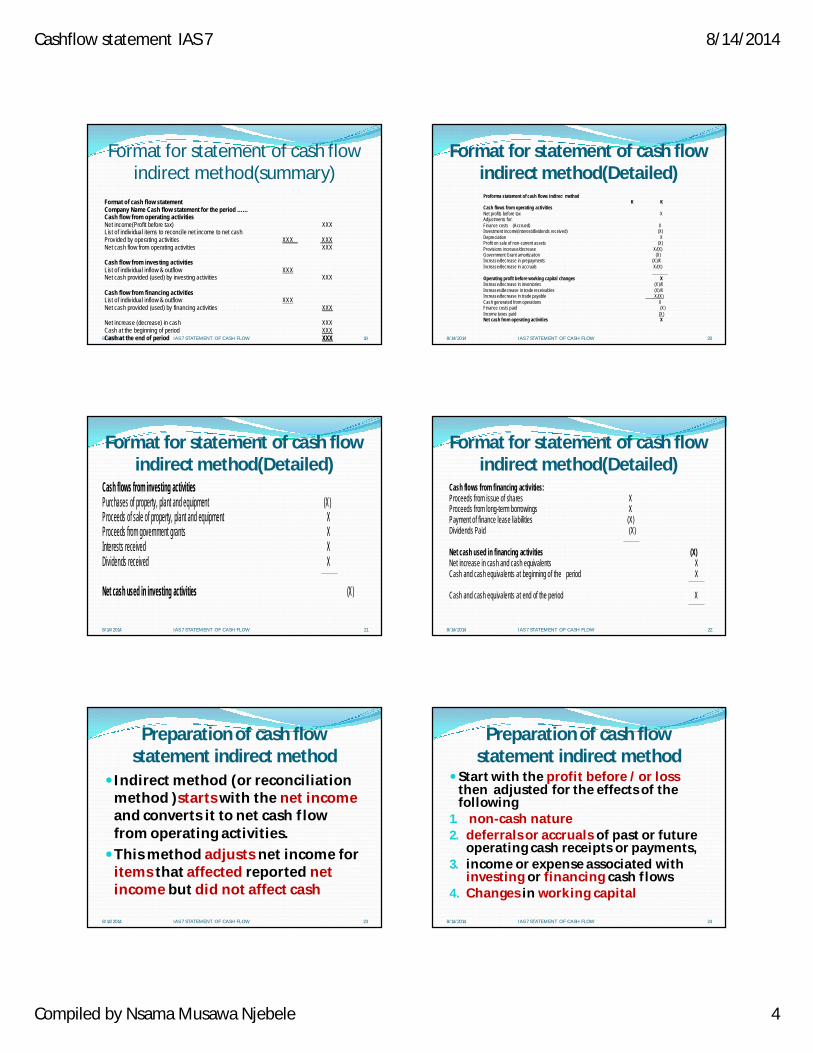

Format for statement of cash flow indirect method(summary)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 19

Format of cash flow statement Company Name Cash flow statement for the period …… Cash flow from operating activities Net income(Profit before tax) XXX List of individual items to reconcile net income to net cash Provided by operating activities XXX XXX Net cash flow from operating activities XXX Cash flow from investing activities List of individual inflow & outflow XXX Net cash provided (used) by investing activities XXX Cash flow from financing activities List of individual inflow & outflow XXX Net cash provided (used) by financing activities XXX Net increase (decrease) in cash XXX Cash at the beginning of period XXX Cash at the end of period XXX

Format for statement of cash flow indirect method(Detailed)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 20

Proforma statement of cash flows indirect method K K Cash flows from operating activities Net profits before tax X Adjustments for: Finance costs (Accrued) X Investment income(interest/dividends received) (X) Depreciation X Profit on sale of non-current assets (X) Provisions increase/decrease X/(X) Government Grant amortization (X) Increase/decrease in prepayments (X)/X Increase/decrease in accruals X/(X) _______ Operating profit before working capital changes X Increase/decrease in inventories (X)/X Increases/decrease in trade receivables (X)/X Increase/decrease in trade payable X/(X) Cash generated from operations X Finance costs paid (X) Income taxes paid (X) Net cash from operating activities X

Format for statement of cash flow indirect method(Detailed)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 21

Cash flows from investing activities Purchases of property, plant and equipment (X) Proceeds of sale of property, plant and equipment X Proceeds from government grants X Interests received X Dividends received X Net cash used in investing activities (X)

Format for statement of cash flow indirect method(Detailed)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 22

Cash flows from financing activities: Proceeds from issue of shares X Proceeds from long-term borrowings X Payment of finance lease liabilities (X) Dividends Paid (X) Net cash used in financing activities (X) Net increase in cash and cash equivalents X Cash and cash equivalents at beginning of the period X Cash and cash equivalents at end of the period X

Preparation of cash flow statement indirect method

Indirect method (or reconciliation method )starts with the net income and converts it to net cash flow from operating activities.This method adjusts net income for

items that affected reported net income but did not affect cash

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 23

Preparation of cash flow statement indirect method

Start with the profit before / or loss then adjusted for the effects of the following

1. non-cash nature2. deferrals or accruals of past or future

operating cash receipts or payments, 3. income or expense associated with

investing or financing cash flows4. Changes in working capital

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 24

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 5

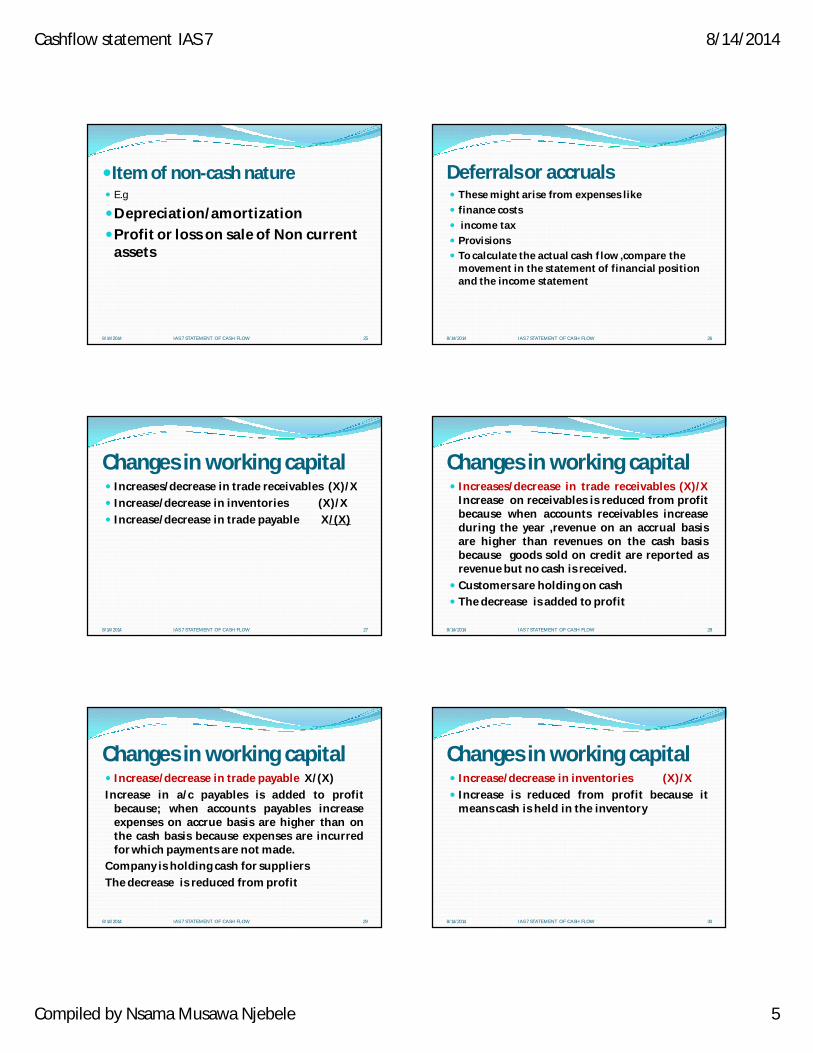

Item of non-cash nature E.g

Depreciation/amortizationProfit or loss on sale of Non current

assets

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 25

Deferrals or accruals These might arise from expenses like finance costs income tax Provisions To calculate the actual cash flow ,compare the

movement in the statement of financial position and the income statement

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 26

Changes in working capital Increases/decrease in trade receivables (X)/X Increase/decrease in inventories (X)/X Increase/decrease in trade payable X/(X)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 27

Changes in working capital Increases/decrease in trade receivables (X)/X

Increase on receivables is reduced from profitbecause when accounts receivables increaseduring the year ,revenue on an accrual basisare higher than revenues on the cash basisbecause goods sold on credit are reported asrevenue but no cash is received.

Customers are holding on cash The decrease is added to profit

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 28

Changes in working capital Increase/decrease in trade payable X/(X)Increase in a/c payables is added to profit

because; when accounts payables increaseexpenses on accrue basis are higher than onthe cash basis because expenses are incurredfor which payments are not made.

Company is holding cash for suppliersThe decrease is reduced from profit

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 29

Changes in working capital Increase/decrease in inventories (X)/X Increase is reduced from profit because it

means cash is held in the inventory

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 30

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 6

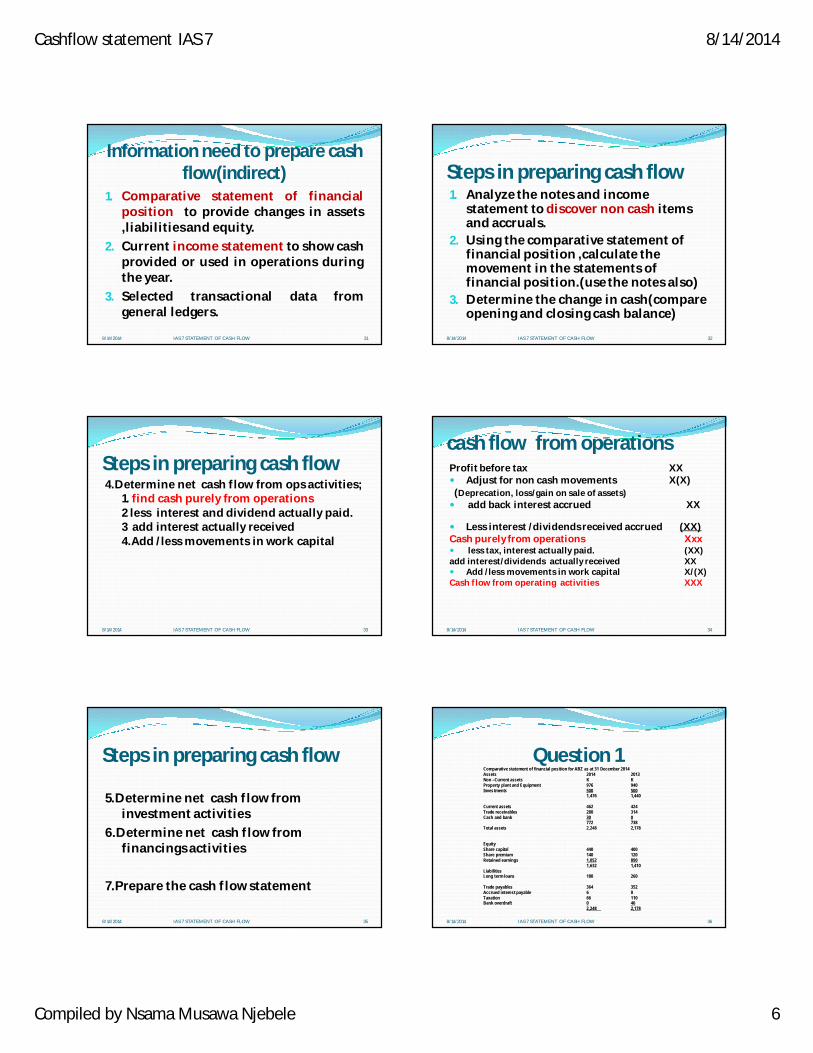

Information need to prepare cash flow(indirect)

1. Comparative statement of financialposition to provide changes in assets,liabilitiesand equity.

2. Current income statement to show cashprovided or used in operations duringthe year.

3. Selected transactional data fromgeneral ledgers.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 31

Steps in preparing cash flow1. Analyze the notes and income

statement to discover non cash items and accruals.

2. Using the comparative statement of financial position ,calculate the movement in the statements of financial position.(use the notes also)

3. Determine the change in cash(compare opening and closing cash balance)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 32

Steps in preparing cash flow4.Determine net cash flow from ops activities;

1. find cash purely from operations2 less interest and dividend actually paid.3 add interest actually received 4.Add /less movements in work capital

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 33

cash flow from operationsProfit before tax XX Adjust for non cash movements X(X)(Deprecation, loss/gain on sale of assets) add back interest accrued XX

Less interest /dividends received accrued (XX)Cash purely from operations Xxx less tax, interest actually paid. (XX)add interest/dividends actually received XX Add /less movements in work capital X/(X)Cash flow from operating activities XXX

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 34

Steps in preparing cash flow

5.Determine net cash flow from investment activities

6.Determine net cash flow from financings activities

7.Prepare the cash flow statement

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 35

Question 1

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 36

Comparative statement of financial position for ABZ as at 31 December 2014 Assets 2014 2013 Non –Current assets K K Property plant and Equipment 976 940 Investments 500 500 1,476 1,440 Current assets 462 424 Trade receivables 280 314 Cash and bank 30 0 772 738 Total assets 2,248 2,178 Equity Share capital 440 400 Share premium 140 120 Retained earnings 1,052 890 1,632 1,410 Liabilities Long term loans 180 260 Trade payables 364 352 Accrued interest payable 6 0 Taxation 66 110 Bank overdraft 0 46 2,248 2,178

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 7

Question 1

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 37

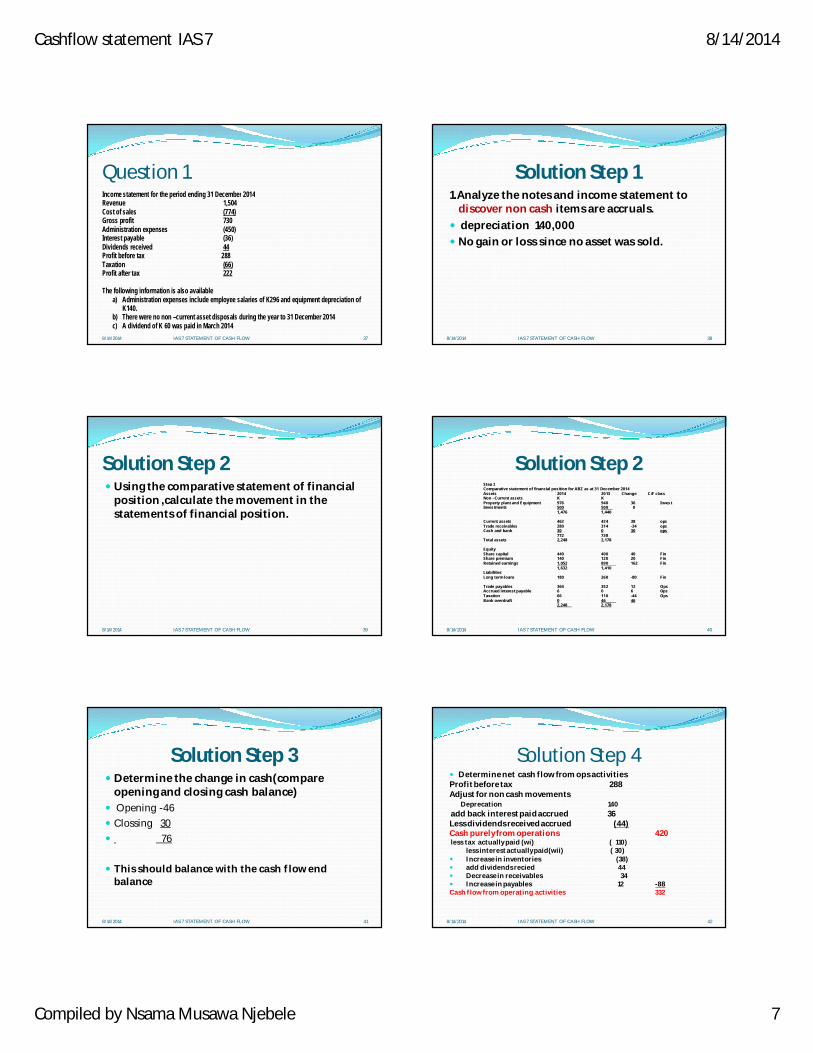

Income statement for the period ending 31 December 2014 Revenue 1,504 Cost of sales (774) Gross profit 730 Administration expenses (450) Interest payable (36) Dividends received 44 Profit before tax 288 Taxation (66) Profit after tax 222 The following information is also available

a) Administration expenses include employee salaries of K296 and equipment depreciation of K140.

b) There were no non –current asset disposals during the year to 31 December 2014 c) A dividend of K 60 was paid in March 2014

Solution Step 11.Analyze the notes and income statement to

discover non cash items are accruals. depreciation 140,000 No gain or loss since no asset was sold.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 38

Solution Step 2 Using the comparative statement of financial

position ,calculate the movement in the statements of financial position.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 39

Solution Step 2

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 40

Step 2 Comparative statement of financial position for ABZ as at 31 December 2014 Assets 2014 2013 Change C/F class Non –Current assets K K Property plant and Equipment 976 940 36 Invest Investments 500 500 0 1,476 1,440 Current assets 462 424 38 ops Trade receivables 280 314 -34 ops Cash and bank 30 0 30 ops 772 738 Total assets 2,248 2,178 Equity Share capital 440 400 40 Fin Share premium 140 120 20 Fin Retained earnings 1,052 890 162 Fin 1,632 1,410 Liabilities Long term loans 180 260 -80 Fin Trade payables 364 352 12 Ops Accrued interest payable 6 0 6 Ops Taxation 66 110 -44 Ops Bank overdraft 0 46 46 2,248 2,178

Solution Step 3 Determine the change in cash(compare

opening and closing cash balance) Opening -46 Clossing 30 76

This should balance with the cash flow end balance

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 41

Solution Step 4 Determine net cash flow from ops activitiesProfit before tax 288Adjust for non cash movements

Deprecation 140add back interest paid accrued 36Less dividends received accrued (44)Cash purely from operations 420less tax actually paid (wi) ( 110)

less interest actually paid(wii) ( 30) Increase in inventories (38) add dividends recied 44 Decrease in receivables 34 Increase in payables 12 -88Cash flow from operating activities 332

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 42

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 8

Solution Step 4 workings1. Working (i) taxation 0pening tax payable 110 Charge for year(i/s) 66 Payment (bal fig) ( 110) Closing tax payable 662. Working (ii) interest 0pening interest payable 0 Charge for year(i/s) 36 Payment (bal fig) (30) Closing interest payable 6

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 43

Solution Step 5 5.Determine net cash flow from investment

activities Acquisition of PPE(w3) (176)

Working 3 Opening balance 940 Less dep (140) Acquistion( bal fig) 176 Closing 976

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 44

Solution Step 6 6.Determine net cash flow from Financing

activities Proceeds from issues of new shares(40+20) 60 Repayment of debt (80) Dividend paid (60)

-80

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 45

Solution step 7 7.Prepare the cash flow statement Cash flow from operating activities 332 Cash flow from investing activities (176) Cash flow from financing activities (-80) Net increase in cash and cash equiv 76 Cash and cash equiv at beginning (46) Cash and cash equiv at end 30(Net increase in cash and cash equiv should = step 2

Cash and cash equiv at at end = that in financial position)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 46

Question 2

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 47

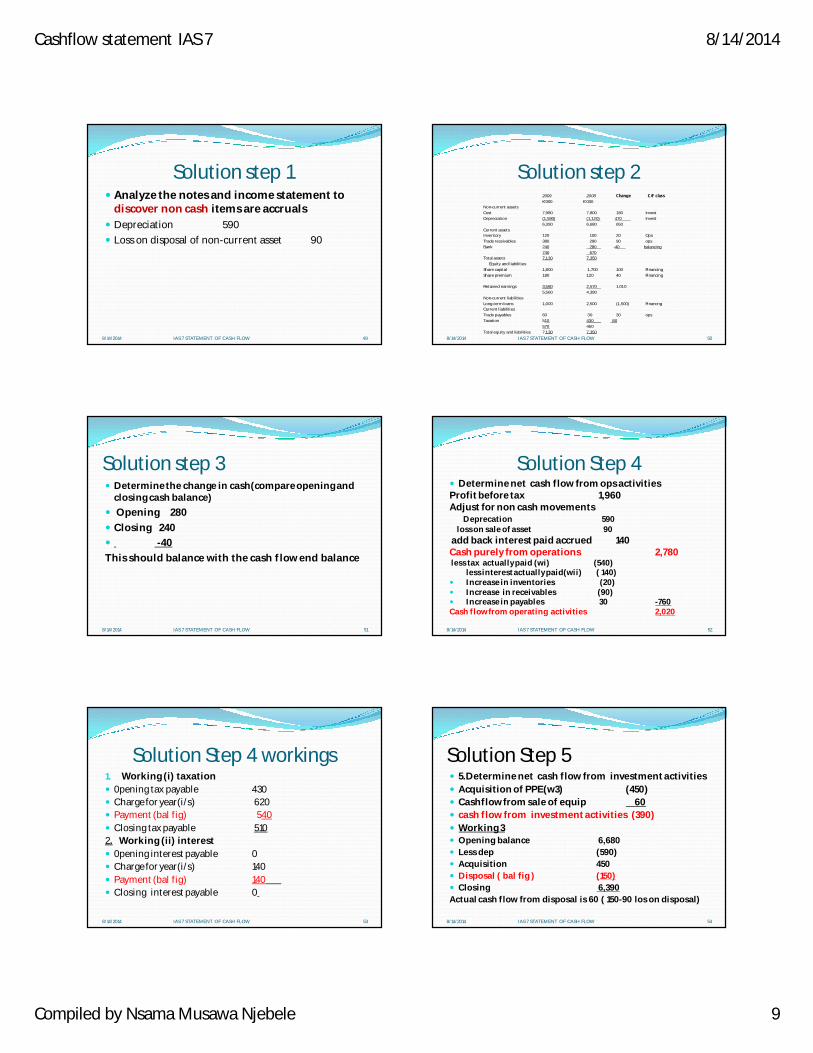

Chambishi Metals Co's income statement for the year ended 31 December 2008 and statements of financial position at 31 December 2008 and 31 December 2009 were as follows. CHAMBISHI METALS INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2009

K'000 K'000 Sales 3,600 Raw materials consumed 350 Staff costs 4,70 Depreciation 590 Loss on disposal of non-current asset 90

1,500 Operating profit 2,100 Interest payable 140 Profit before tax 1,960 Taxation 620 Profit for the year 1,340

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 48

CHAMBISHI METALS STATEMENTS OF FINANCIAL POSITION AS AT 31 DECEMBER 2009 2008 K'000 K'000

Non-current assets Cost 7,980 7,800 Depreciation (1,590) (1,120)

6,390 6,680 Current assets Inventory 120 100 Trade receivables 380 290 Bank 240 280

740 670 Total assets 7,130 7,350 FA Equity and liabilities Equity Share capital 1,800 1,700 Share premium 180 120 Retained earnings 3,580 2,570

5,560 4,390 Non-current liabilities Long-term loans 1,000 2,500 Current liabilities Trade payables 60 30 Taxation 510 430

570 460 Total equity and liabilities 7,130 7,350 Dividends paid were K330, 000 During the year, the company paid K450, 000 for a new piece of machinery. Required Prepare a statement of cash flows for Chambishi Metals Co for the year ended 31 December 2009 in accordance with the requirements of IAS 7, using the indirect method.

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 9

Solution step 1 Analyze the notes and income statement to

discover non cash items are accruals Depreciation 590 Loss on disposal of non-current asset 90

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 49

Solution step 2

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 50

2009 2008 Change C/F class K'000 K'000

Non-current assets Cost 7,980 7,800 180 Invest Depreciation (1,590) (1,120) 470 Invest

6,390 6,680 650 Current assets Inventory 120 100 20 Ops Trade receivables 380 290 90 ops Bank 240 280 -40 balancing

740 670 Total assets 7,130 7,350 FA Equity and liabilities Share capital 1,800 1,700 100 Financing Share premium 180 120 40 Financing Retained earnings 3,580 2,570 1,010

5,560 4,390 Non-current liabilities Long-term loans 1,000 2,500 (1,500) Financng Current liabilities Trade payables 60 30 30 ops Taxation 510 430 80

570 460 Total equity and liabilities 7,130 7,350

Solution step 3 Determine the change in cash(compare opening and

closing cash balance) Opening 280 Closing 240 -40This should balance with the cash flow end balance

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 51

Solution Step 4 Determine net cash flow from ops activitiesProfit before tax 1,960Adjust for non cash movements

Deprecation 590loss on sale of asset 90

add back interest paid accrued 140Cash purely from operations 2,780less tax actually paid (wi) (540)

less interest actually paid(wii) ( 140) Increase in inventories (20) Increase in receivables (90) Increase in payables 30 -760Cash flow from operating activities 2,020

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 52

Solution Step 4 workings1. Working (i) taxation 0pening tax payable 430 Charge for year(i/s) 620 Payment (bal fig) 540 Closing tax payable 5102. Working (ii) interest 0pening interest payable 0 Charge for year(i/s) 140 Payment (bal fig) 140 Closing interest payable 0

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 53

Solution Step 5 5.Determine net cash flow from investment activities Acquisition of PPE(w3) (450) Cashflow from sale of equip 60 cash flow from investment activities (390) Working 3 Opening balance 6,680 Less dep (590) Acquisition 450 Disposal ( bal fig ) (150) Closing 6,390 Actual cash flow from disposal is 60 ( 150-90 los on disposal)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 54

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 10

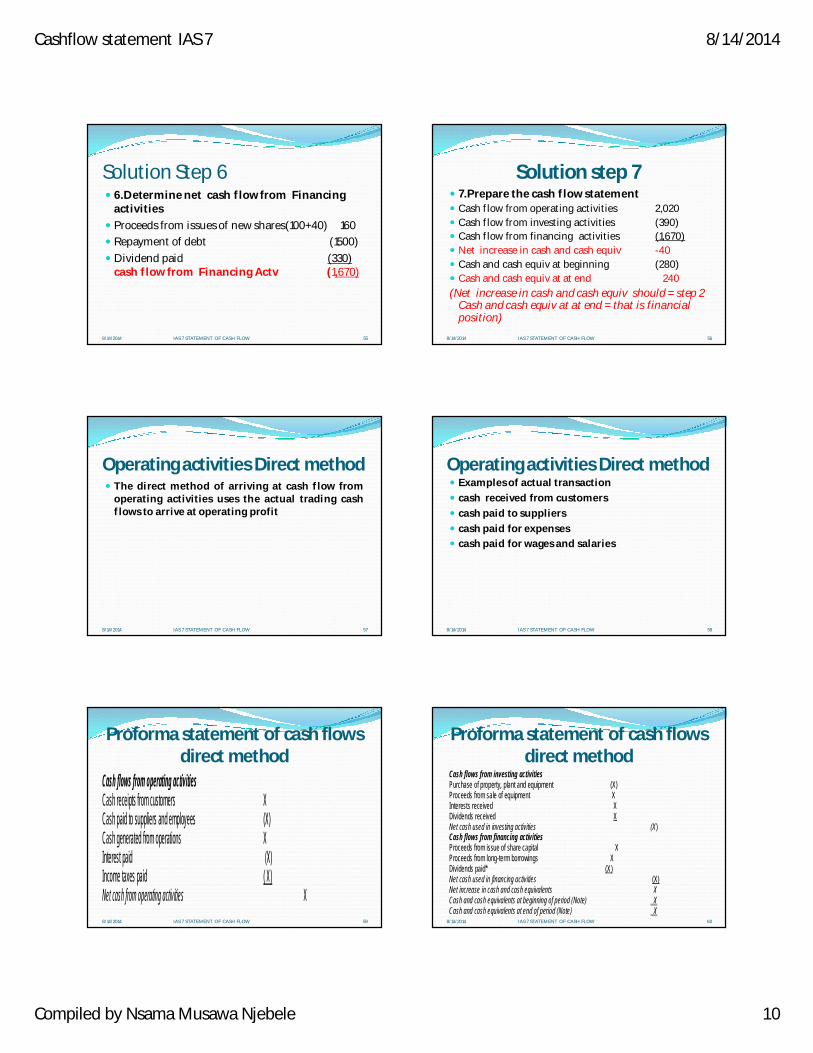

Solution Step 6 6.Determine net cash flow from Financing

activities Proceeds from issues of new shares(100+40) 160 Repayment of debt (1500) Dividend paid (330)

cash flow from Financing Actv (1,670)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 55

Solution step 7 7.Prepare the cash flow statement Cash flow from operating activities 2,020 Cash flow from investing activities (390) Cash flow from financing activities (1,670) Net increase in cash and cash equiv -40 Cash and cash equiv at beginning (280) Cash and cash equiv at at end 240(Net increase in cash and cash equiv should = step 2

Cash and cash equiv at at end = that is financial position)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 56

Operating activities Direct method The direct method of arriving at cash flow from

operating activities uses the actual trading cashflows to arrive at operating profit

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 57

Operating activities Direct method Examples of actual transaction cash received from customers cash paid to suppliers cash paid for expenses cash paid for wages and salaries

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 58

Proforma statement of cash flows direct method

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 59

Cash flows from operating activities Cash receipts from customers X Cash paid to suppliers and employees (X) Cash generated from operations X Interest paid (X) Income taxes paid ( X) Net cash from operating activities X

Proforma statement of cash flows direct method

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 60

Cash flows from investing activities Purchase of property, plant and equipment (X) Proceeds from sale of equipment X Interests received X Dividends received X Net cash used in investing activities (X) Cash flows from financing activities Proceeds from issue of share capital X Proceeds from long-term borrowings X Dividends paid* (X) Net cash used in financing activities (X) Net increase in cash and cash equivalents X Cash and cash equivalents at beginning of period (Note) X Cash and cash equivalents at end of period (Note) X

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 11

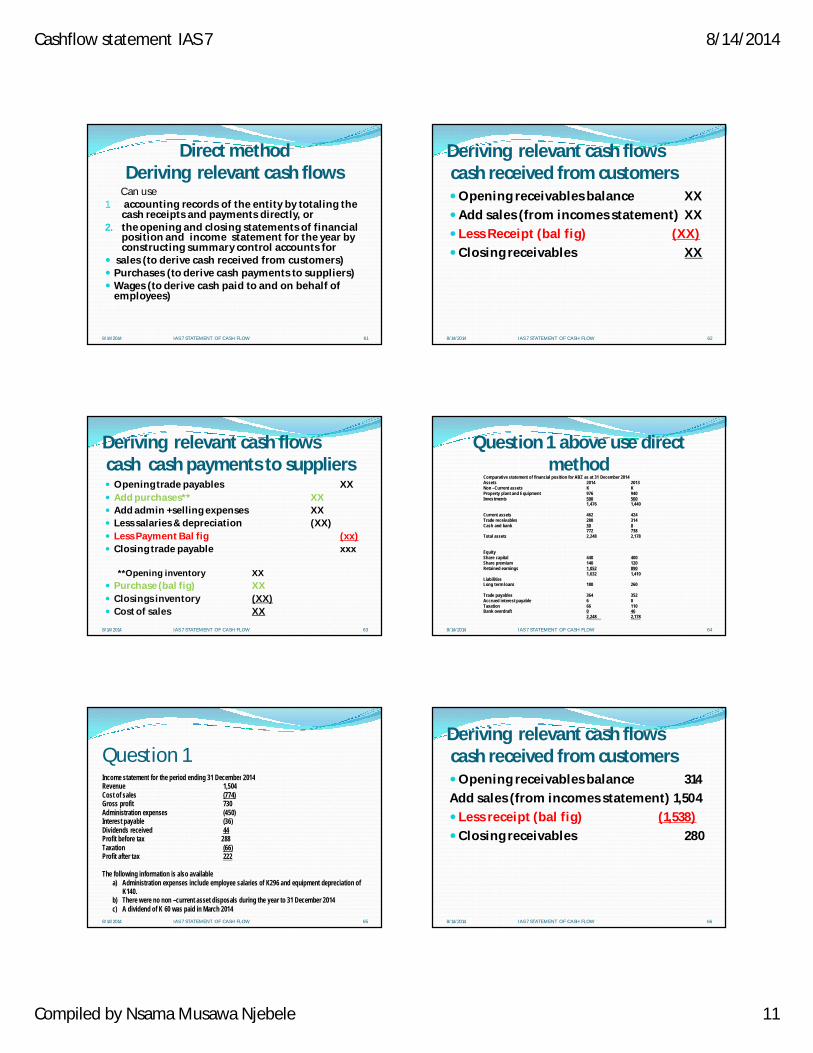

Direct method Deriving relevant cash flows

Can use1. accounting records of the entity by totaling the

cash receipts and payments directly, or 2. the opening and closing statements of financial

position and income statement for the year by constructing summary control accounts for

sales (to derive cash received from customers) Purchases (to derive cash payments to suppliers) Wages (to derive cash paid to and on behalf of

employees)

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 61

Deriving relevant cash flowscash received from customersOpening receivables balance XXAdd sales (from incomes statement) XXLess Receipt (bal fig) (XX)Closing receivables XX

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 62

Deriving relevant cash flowscash cash payments to suppliers Opening trade payables XX Add purchases** XX Add admin +selling expenses XX Less salaries & depreciation (XX) Less Payment Bal fig (xx) Closing trade payable xxx

**Opening inventory XX Purchase (bal fig) XX Closings inventory (XX) Cost of sales XX

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 63

Question 1 above use direct method

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 64

Comparative statement of financial position for ABZ as at 31 December 2014 Assets 2014 2013 Non –Current assets K K Property plant and Equipment 976 940 Investments 500 500 1,476 1,440 Current assets 462 424 Trade receivables 280 314 Cash and bank 30 0 772 738 Total assets 2,248 2,178 Equity Share capital 440 400 Share premium 140 120 Retained earnings 1,052 890 1,632 1,410 Liabilities Long term loans 180 260 Trade payables 364 352 Accrued interest payable 6 0 Taxation 66 110 Bank overdraft 0 46 2,248 2,178

Question 1

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 65

Income statement for the period ending 31 December 2014 Revenue 1,504 Cost of sales (774) Gross profit 730 Administration expenses (450) Interest payable (36) Dividends received 44 Profit before tax 288 Taxation (66) Profit after tax 222 The following information is also available

a) Administration expenses include employee salaries of K296 and equipment depreciation of K140.

b) There were no non –current asset disposals during the year to 31 December 2014 c) A dividend of K 60 was paid in March 2014

Deriving relevant cash flowscash received from customersOpening receivables balance 314Add sales (from incomes statement) 1,504Less receipt (bal fig) (1,538)Closing receivables 280

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 66

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 12

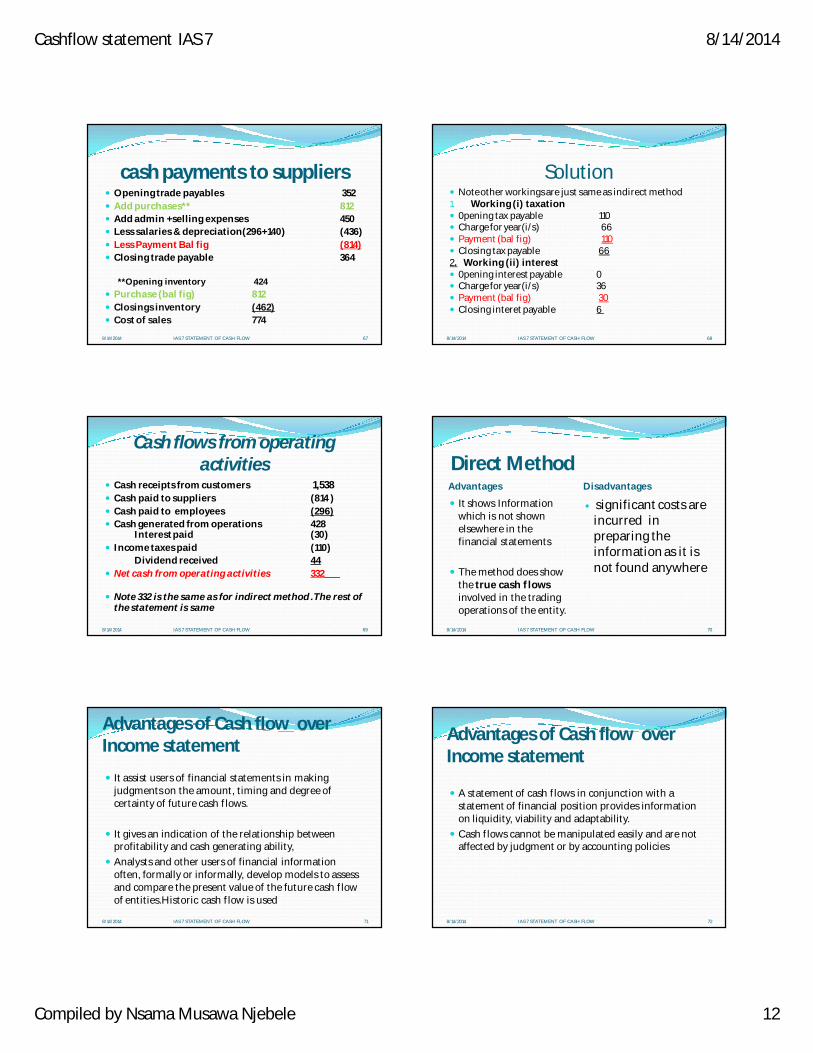

cash payments to suppliers Opening trade payables 352 Add purchases** 812 Add admin +selling expenses 450 Less salaries & depreciation(296+140) (436) Less Payment Bal fig (814) Closing trade payable 364

**Opening inventory 424 Purchase (bal fig) 812 Closings inventory (462) Cost of sales 774

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 67

Solution Note other workings are just same as indirect method1. Working (i) taxation 0pening tax payable 110 Charge for year(i/s) 66 Payment (bal fig) 110 Closing tax payable 662. Working (ii) interest 0pening interest payable 0 Charge for year(i/s) 36 Payment (bal fig) 30 Closing interet payable 6

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 68

Cash flows from operating activities

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 69

Cash receipts from customers 1,538 Cash paid to suppliers (814 ) Cash paid to employees (296) Cash generated from operations 428

Interest paid (30) Income taxes paid (110)

Dividend received 44 Net cash from operating activities 332

Note 332 is the same as for indirect method .The rest of the statement is same

Direct MethodAdvantages Disadvantages

It shows Information which is not shown elsewhere in the financial statements

The method does show the true cash flows involved in the trading operations of the entity.

significant costs are incurred in preparing the information as it is not found anywhere

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 70

Advantages of Cash flow over Income statement

It assist users of financial statements in making judgments on the amount, timing and degree of certainty of future cash flows.

It gives an indication of the relationship between profitability and cash generating ability,

Analysts and other users of financial information often, formally or informally, develop models to assess and compare the present value of the future cash flow of entities.Historic cash flow is used

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 71

Advantages of Cash flow over Income statement

A statement of cash flows in conjunction with a statement of financial position provides information on liquidity, viability and adaptability.

Cash flows cannot be manipulated easily and are not affected by judgment or by accounting policies

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 72

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 13

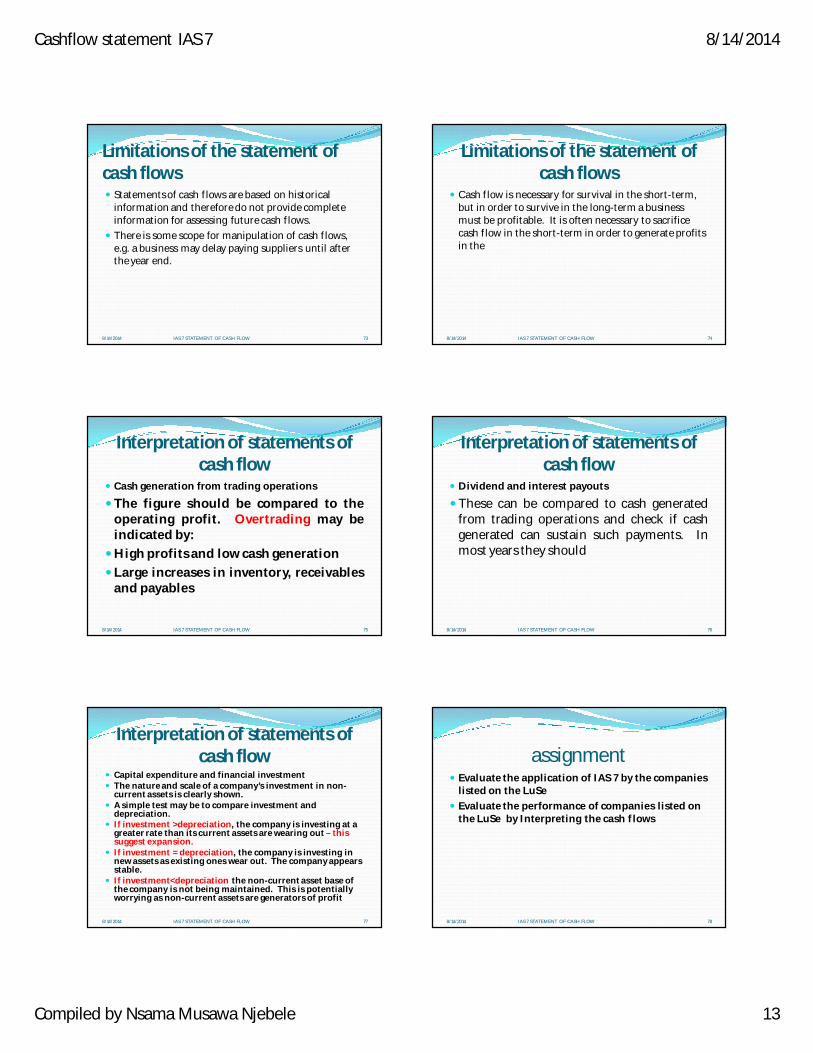

Limitations of the statement of cash flows Statements of cash flows are based on historical

information and therefore do not provide complete information for assessing future cash flows.

There is some scope for manipulation of cash flows, e.g. a business may delay paying suppliers until after the year end.

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 73

Limitations of the statement of cash flows

Cash flow is necessary for survival in the short-term, but in order to survive in the long-term a business must be profitable. It is often necessary to sacrifice cash flow in the short-term in order to generate profits in the

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 74

Interpretation of statements of cash flow

Cash generation from trading operations

The figure should be compared to theoperating profit. Overtrading may beindicated by:

High profits and low cash generationLarge increases in inventory, receivables

and payables

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 75

Interpretation of statements of cash flow

Dividend and interest payouts

These can be compared to cash generatedfrom trading operations and check if cashgenerated can sustain such payments. Inmost years they should

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 76

Interpretation of statements of cash flow

Capital expenditure and financial investment The nature and scale of a company’s investment in non-

current assets is clearly shown. A simple test may be to compare investment and

depreciation. If investment >depreciation, the company is investing at a

greater rate than its current assets are wearing out – this suggest expansion.

If investment = depreciation, the company is investing in new assets as existing ones wear out. The company appears stable.

If investment<depreciation the non-current asset base of the company is not being maintained. This is potentially worrying as non-current assets are generators of profit

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 77

assignment Evaluate the application of IAS 7 by the companies

listed on the LuSe Evaluate the performance of companies listed on

the LuSe by Interpreting the cash flows

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 78

Cashflow statement IAS 7 8/14/2014

Compiled by Nsama Musawa Njebele 14

8/14/2014 IAS 7 STATEMENT OF CASH FLOW 79