Embed Size (px)

Citation preview

For

per

sona

l use

onl

y

Contents

1 Chairman and Managing Director’s Review

6 Providing customers with global reach

8 Corporate Social Responsibility

10 Board of Directors

Toll Group structure and Senior Management

13 Directors’ Report

39 Corporate Governance Statement

49 Income Statements

50 Statements of Recognised Income and Expenses

51 Balance Sheets

52 Statements of Cash Flows

53 Notes to the Financial Statements

130 Directors’ Declaration

131 Independent Audit Report

133 Shareholder Information

134 Ten Year Summary

For

per

sona

l use

onl

y

TOLL – ANNUAL REPORT 2008 1

It’s been another big year for the Toll Group. In the last 12 months,

we have restructured the company into three major operating divisions,

reduced our exposure to Virgin Blue Australia (VBA) through a special

in specie dividend, sold our New Zealand rail and ferry operations back

to the New Zealand government and achieved another year of strong

underlying organic revenue and earnings growth for continuing business

operations across the Group. As we look forward to the coming year we

are very excited by what we see ahead: our core Australian business is

extremely sound, our Asian businesses are growing, our powerful organic

growth engine remains strong, and new business wins across the Group

are solid and consistent. But before we discuss this in more detail, let’s

briefl y recap the past year.

Following our decision to distribute our stake in Virgin Blue

Australia on a 1 for 1 basis to shareholders by way of a special

in specie dividend, we booked a one-off non-cash charge to the

current year’s profi t of approximately $1.2 billion.

When offset by adjustments including the $225 million gain from

the sale of the New Zealand rail and ferry operations, and the

year’s underlying net profi t fi gure of $258 million, the net effect

is an after tax reported loss of $694.7 million for the 2007-08

fi nancial year.

However, when we focus on the company’s annual earnings for

the continuing business operations of the Group, the strength

of Toll’s performance is clear — across the Group all our key

measures are up, core operations are strong and vibrant, and

the story we have to tell is a good one.

Our 2007-08 revenue grew from $4.86 billion to $5.60 billion,

an increase of 15 percent; EBITDA grew from $471 million to

$570 million, a rise of 21 percent; EBIT grew from $365 million

to $429 million, an increase of 18 percent; and our normalised

net profi t after tax for continuing operations increased 24 percent

to $258 million.

Shareholder returns from continuing operations were

likewise strong: on a like-for-like basis our EPS (fully diluted)

was 42.7 cents per share compared to 35.5 cents per share

for the previous year, and the fi nal full-year dividend was

25 cents per share.

Of course, a feature of Toll’s powerful and unique business

model is the consistent generation of strong cash fl ow, and

this last year was no exception. In 2007-08, our net cash from

DEAR FELLOW INVESTOR,

CHAIRMAN AND MANAGING DIRECTOR’S REVIEWF

or p

erso

nal u

se o

nly

2

continuing operations was $496 million. Compellingly, our ‘unique

integrated logistics model’ has allowed us to generate signifi cant

cash fl ow over the past fi ve years — an undeniable barometer

of Toll’s fi nancial strength.

This impressive cash fl ow profi le has again enabled us to grow

the business through strategic acquisitions and focused capital

expenditure. In the last 12 months, we have spent $796 million

acquiring new businesses that broaden the scale and capabilities

of our evolving and unique global supply chain model, taking our

acquisition tally to over 63 in the last 22 years.

Capital expenditure topped $380 million for the year with the

key areas of focus being new facilities, technology and fl eet

upgrades.

Equally important is the strength of our balance sheet, and

we are pleased to tell you it’s in great shape: total assets exceed

$4.8 billion, net debt is a very manageable $650 million and total

equity is $2.1 billion. We have a gearing ratio of only 24 percent

and interest cover is very strong at around 12 times.

Add it all up, and the company is fi nancially strong,

underpinned by consistent organic growth and in a very powerful

position to take advantage of any new strategic opportunities.

As we have said before in previous annual reports, achieving

such results over one, two or even fi ve years as many great

companies have done, is not really that unique. What’s gratifying

is to achieve consistent underlying performance over long

periods and through different economic cycles. It’s precisely this

point of consistent underlying performance over long periods

through differing economic cycles that is an important part of

any discussion today, and as Toll enters this new fi nancial year

with momentum, some are asking whether the fl uctuating global

economic factors are going to affect us going forward?

This is a legitimate question: certainly future economic conditions

are not easy to predict, and there are many factors that will

always be beyond our control, but Toll is a company with a clear

strategic vision, a powerful and time-tested business model,

driven by an enthusiastic group of energised people, and

if you don’t read any further in this annual report, know this,

Toll is in great shape and excited by the opportunities ahead.

To help you better understand the sources of our confi dence

let’s look at the key points in a little more detail.

First, we’ve greatly simplifi ed the structure of the business

following the in specie VBA dividend and sale of the New

Zealand rail and ferry assets, and established three operating

divisions — Australia and New Zealand Integrated Transport

and Logistics, Toll Asia Contract Logistics and Toll Global

Forwarding. Second, we’re exceptionally strong fi nancially,

with powerful cash fl ows, solid growth in underlying EBIT

margins and a balance sheet the envy of many. Third, we’re

very well positioned in the key trade markets of the Asian

region, where trade has never been stronger. Fourth, we’re

generating revenue from a diversifi ed range of strong industry

sectors across our extensive geographic markets. Fifth, we’re

insulated against rising fuel costs and have most contracts

structured around effective fuel recovery surcharges, proven

and tested to minimise increasing costs to Toll. And sixth,

we’re underpinned by strong, consistent organic growth,

a cornerstone of Toll’s year-on-year revenue story.

Put it all together, and we’re talking powerful competitive

advantages in uncertain economic times, and the foundations

of our confi dence about what lies ahead for Toll and our three

new operating divisions.

1. Australia and New Zealand Integrated Transport

and Logistics is the largest of the three divisions, contributing

over 80 percent of the Group’s revenue and EBIT, and on a

comparable basis for continuing operations, trading results

for 2007-08 were excellent.

0

1

2

3

4

5

65.6

05 06 07 08

0

100

200

300

400

500

429

05 06 07 08

0

100

200

300

400

500

600 570

05 06 07 08

REVENUE*Billion dollars

EBIT*Million dollars

EBITDA*Million dollars

CHAIRMAN AND MANAGING DIRECTOR’S REVIEWF

or p

erso

nal u

se o

nly

TOLL – ANNUAL REPORT 2008 3

Revenue from Australian operations grew 9.2 percent to

$4.42 billion, EBIT grew 18 percent from $294 million to

$347 million, and EBIT margins maintained the powerful

upward trends of prior years, increasing from 7.21 percent

to 7.84 percent.

These are fi rst-class results, and signifi cantly organic growth

again played a starring role. There is no doubt, organic growth

is one of Toll’s most powerful growth engines, confi rming year-

on-year just how much more business our customers continue

to bring us.

Highlights for the year were many, including the fi nalisation

of the long-term domestic freight operations agreement with

Virgin Blue, the winning of signifi cant new contracts in retail,

mining and automotive, the establishment of Toll Dnata, our

aviation logistics joint venture with Emirates, the transferral

of the Jetcare maintenance facilities to Virgin Blue and the

continuation of the integration and rationalisation of the

ex-Patrick warehousing and logistics activities.

We also acquired a number of smaller businesses including

Victorian Express, Westrans, Extra Transport, Golden Riverland

Express, SkyNet Worldwide Express and the Western Australian-

based, Courier Australia to expand and grow our capabilities.

Across the Tasman, New Zealand continued to perform well.

Revenue was NZ$255 million, up from NZ$234 million, with

EBIT substantially increasing from NZ$7.3 million to the

NZ$9.4 million for the year. These are very good results in

what can only be considered a fl at economy and we are keen

to grow our presence in New Zealand.

Following the sale of the rail and ferry operations, the focus

in New Zealand is fi rmly on contract logistics and road and rail

forwarding, leveraging our scale and volume to generate the

lowest possible linehaul cost to strengthen our position in the

higher-value spaces of supply chain management. That’s why

we continue to build our services, and the recent acquisition

of United Carriers, one of Northland’s largest freight companies

with annual sales of NZ$40 million, is an example of our

ongoing commitment. Expect to see more acquisition activity

from Toll in New Zealand’s freight forwarding sector, as we

reaffi rm our commitment to this important market.

A major strength of Toll’s business model in our core Australian

and New Zealand markets, especially in uncertain economic

times, is the level of diversifi cation of our customer base and

the industry sectors in which we operate. This is an important

point, for there is the mistaken belief that we are signifi cantly

exposed to a slowdown in discretionary spend, and while there

is a general softening in the economy, we believe, Toll is well

insulated to minimise any effects.

We compete in a number of key dynamic market sectors, the

majority of which are pretty resilient. For example, 80 percent of

our Australian retail and Fast Moving Consumer Goods (FMCG)

business is non-discretionary, defence and government spending

remains strong, the mining and resources sector is booming,

automotive is still performing, and the steel and industrial sector

is powering ahead, exporting to Asia and beyond. The exception

to the rule is the manufacturing sector, where the obvious

slowdown in the local market is countered in many cases, by

moves to offshore production. Of course, with our signifi cant and

ever expanding presence in the Asian region we don’t greatly

suffer, as we benefi t from this growing two-way trade as well.

Add to that the fact that our top 20 sector customers represent

less than 30 percent of the Group’s total revenue, and Toll’s

business model is best regarded as highly sustainable in both

good times and bad.

But we have another core strength, one that is increasingly

playing a pivotal role in differentiating Toll’s unique competitive

advantages, and that’s our diverse and integrated multi-modal

operational profi le. Providing more fl exibility and greater

diversity in end-to-end supply chain solutions, customers can,

for example, now trade-off service for price, shifting from road

0

1

2

3

4

5

6

7

8 7.65

05 06 07 08

EBIT MARGIN*Percent

* Continuing operations for years 2007, 2008Adjusted to refl ect continuing operations post restructure following sale of New Zealand rail and ferry operations and demerger of Virgin Blue Australia.

TOTAL ORDINARY DIVIDENDSMillion dollars

0

50

100

150

200

161.6

05 06 07 08

For

per

sona

l use

onl

y

4

to rail, air express to road express or rail to sea. Not only do

our customers have more choice, but this collective multi-modal

approach presents Toll with huge cross-selling opportunities,

driving greater sector revenues and improved EBIT margins

throughout the Group.

In summary, our core Australian market is extremely strong and

stable. We see no reason for increased concern in the coming

year, and in fact, we look forward to the opportunities ahead.

Now, let’s turn our attention to our expanding Asian businesses.

We have moved quickly in the last few months to consolidate

and unify our growing and powerful collection of Asian logistics

assets under the Toll brand, an essential move for a company

that today does business in over 45 countries and enjoys an

increasingly broad-based geographic distribution of revenue.

2. Toll Asia Contract Logistics, the second of our three

divisions, is of course, the amalgamation of our 2006

acquisition of SembCorp Logistics, and our October 2007

takeover of Sembawang Kimtrans, the Singapore-based

integrated logistics and marine transportation specialist.

With a new management structure and the appointment

of Wayne Hunt, a long-standing and senior Toll executive,

as CEO, Toll Asia performed very well in 2007-08. Revenues

were S$777 million compared to S$563 million for the year

previous; EBIT increased 12 percent, from S$73 million to

S$82 million. On a like-for-like basis, and excluding the impact

of the Sembawang Kimtrans acquisition, underlying revenue

grew 12.5 percent, driven in part by excellent growth in

offshore marine and mining logistics operations, government

defence logistics, and major contract wins or renewals for

customers like Yamaha, Hawley and Hazel, Pfi zer, St Medical,

Samsung, Proctor & Gamble, Coca-Cola Amatil, Johnson &

Johnson, Michelin and Nestlé. This strong growth in underlying

revenue is an important point, for it is a clear indication of

Toll’s increasing momentum in Asia.

We’re also investing in key assets. Take SOPS (Singapore

Offshore Petroleum Services), our offshore oil and gas logistics

division, for example. Strategically headquartered at the

sprawling 52 hectare Loyang Offshore Supply Base — and

home to nearly 200 established oil and gas services-related

companies and the region’s integrated offshore logistics

hub — SOPS is at the very heart of this one-stop resource

centre for oilfi eld services, equipment and supplies. That’s why

we’re investing signifi cant capital as part of a redevelopment

strategy and securing 40-year leases to ensure our long-term

foundations, for its potential is as much global as it is regional.

Which brings us to the third division in the Group.

3. Toll Global Forwarding has been formed as a direct response

to customers’ growing global logistics needs. It is important to

understand that customers of all kinds are increasingly making

their decisions at a regional or global level. This is being driven

by the very international nature of trade today, and in particular,

the meteoric rise of Asia as the ‘world’s factory’.

That’s why our most recent acquisitions — the Hong Kong-

based BALtrans in March 2008, and the Australian-based Gluck

in June 2008 — are strategically so very important to Toll.

With a network spanning 65 major cities across Asia, US,

Europe, Africa and the Middle East, BALtrans is one of

Asia’s largest global forwarders, adding extensive worldwide

capabilities and annual revenues of approximately $700 million

to Toll’s operations. And Gluck, whose strong, long-term

relationship with BALtrans, strategically strengthens our

Australian-Asian based freight forwarding capabilities.

We have appointed Hugh Cushing, previously Toll’s Director of

International Development, as CEO of Toll Global Forwarding, to

ensure the swift and accurate alignment of BALtrans operations

with Toll’s unique business model.

CHAIRMAN AND MANAGING DIRECTOR’S REVIEWF

or p

erso

nal u

se o

nly

TOLL – ANNUAL REPORT 2008 5

Importantly, the formation of Toll Global Forwarding means we

now have a consolidated offering across the Group, true end-to-

end international supply chain capabilities, all underpinned by

one point of contact across all operational components.

The strength and breadth of Toll’s international service

capabilities is a huge competitive advantage, and one that

fi rmly catapults Toll’s unique integrated business model into

global prominence. From this base, we can leverage not

only our scale and network capacities to drive superior cost

structures, but also our cross-group capabilities to maximise

cross-group sales and revenues.

And we’re pleased to say we’re already seeing results:

revenues and earnings are growing steadily, we’ve won

important new global freight forwarding contracts including

GMC, Shandong SEM Machinery Co., Ltd. (a Caterpillar

subsidiary), Danks, Supercheap, Spotlight and the Apparel

Group; and we’re expanding capabilities for customers like

Proctor & Gamble, Colgate, Ford and Holden.

Year-after-year, our results consistently confi rm we have the

right business model, that we are in the right businesses in the

right segments of the industry, and that we compete in one of

the most dynamic industries there is, for global trade is perhaps

the world’s most powerful economic engine.

On pages 6 to 7 of this report, you’ll see demand for logistics

in our region is supported by powerful trends — trends that are

constantly working in our favour.

Importantly, this one fact remains constant: customers continue

to outsource more and more of their logistics. We’ve said on

many occasions, our greatest opportunities for growth are right

in front of us: if we execute our business model successfully,

we earn more of our customers’ business.

This is illustrated in the strong and consistent organic growth

we experience year-in-and-year-out; in the mushrooming

internationalism of Australian business where customers are

increasingly expanding their two-way trade between Australia

and Asia; and in the growing sophistication of our intra- and

inter-Asian trade.

We believe our differentiating capabilities — our vision

of a single source for global supply chain management, our

strategy, our values, our focus on being the best at what we

do, our famous can-do attitude, and our belief in people as

a competitive advantage — are powerful drivers of strong

and profi table growth in both good times and bad.

As a result, we know that Toll has excellent opportunities in

2008 and beyond. In an environment that presents signifi cant

challenges for some, we possess signifi cant strengths: a

powerful balance sheet, signifi cant cash reserves and available

undrawn facilities, little net debt, low gearing and strong

interest cover. Our acquisition capacity is strong, and thanks to a

well-executed business model, we’re far less subject to volatility

in uncertain economic conditions. We’re in excellent shape —

and remain very optimistic about the future of our company.

In closing, we want to sincerely thank the 25,000+ Toll

people for their outstanding accomplishments and strong

results. Another great year by a truly great team! We thank

our customers for entrusting us with more of their business.

And we thank you, our owners, for your confi dence in Toll

as we begin yet another exciting year.

Ray Horsburgh AM

Chairman

Paul Little

Managing Director

For

per

sona

l use

onl

y

6

Toll’s global integration

Ten to fi fteen years ago the typical supply chain

was domestic, but today many businesses are either

directly sourcing overseas, or their suppliers are.

And more and more companies are selling their

goods in international markets.

Consequently, customers have come to realise that

if they’re going to respond rapidly and effectively

to today’s marketplace, they need to do more

to re-engineer their supply chains, and not just

domestically, but globally.

That’s why Toll’s three main areas of focus, include:

• the strong and powerful Australia and

New Zealand integrated domestic transport

and logistics business;

• Toll Asia Contract Logistics, the Asian logistics

business headquartered in Singapore; and,

• the recently created Toll Global Forwarding

business focused on international freight

forwarding and supply chain services,

headquartered in Hong Kong.

These powerful and strategically located logistics

capabilities combined with the advantages of

our formidable technical capabilities is enabling

customers to comprehensively optimise effi ciencies

in their global logistics and supply chains,

synchronising multiple partners in multiple countries

in multiple time zones. Which adds up to strong

growth for Toll.

PROVIDING CUSTOMERS

WITH GLOBAL REACH

WHERE WE DO BUSINESS IN 2008 – BY REGION

Today, Toll does business from over 700 sites in over 45 countries and enjoys an

increasingly broad-based geographic distribution of revenue. Of course, our focus is the

Asian region, the fastest growing and most dynamic logistics marketplace there is.

Why operating in high growth areas is good for Toll

Because it’s where trade happens. Countries like China, India and Vietnam are growth

markets; people are becoming consumers; they’re joining the middle class. Hundreds of

millions of people are opening their fi rst bank accounts, getting their fi rst cell phones,

using their fi rst credit cards. Tens of millions are buying their fi rst televisions, their fi rst

refrigerators and their fi rst automobiles. Now consider what has to happen to deliver all

of those people cell phones, televisions and cars. Every item has to travel through a

complex integrated logistics network involving supply chain management optimised for

both time and cost. That’s why Toll operates in high growth areas — because we’re

at the crucial intersection of supply and demand.

AUSTRALIA AND NEW ZEALAND

Revenue: AUD$4.64 billion

• Express/Courier

• Domestic Freight Forwarding

• Specialist Logistics

• Coastal Shipping

• Distribution, Warehousing and

Logistics Management

• Defence Logistics

• AutoLogistics

• Road, Rail & Air Freight Forwarding

TOLL GROUP

AMERICAS EUROPE

WHO WE ARE IN 2008

We are an Asian region focused integrated logistics group with extensive global reach.

With over 25,000 people we operate in over 45 countries and have revenues in excess

of $5.6 billion. We are headquartered in Australia.

Moscow

IstanbulRome

MilanZurich

Madrid

MontrealToronto

BostonNew York

Chicago

St Louis

Memphis

Atlanta

Miami

Lima

Co-owned branch

Agency branch Santiago

Sao Paulo

Buenos Aires

Dallas

Los Angeles

San Francisco

Vancouver ParisBrusselsLondon

Basildon

OsloStockholm

AlvestaRotterdam

Hamburg

DusseldorfHannover

Amsterdam

FrankfurtMunich

Goteborg

Manchester

Southampton

Stuttgart

Barcelona

Tel Aviv

Kuwait

Manama

Doha

Dubai

Muscat

Karachi

New Delhi

Mumbai

Colombo

Durban

Port Elizabeth

Cape Town

Johannesburg

Cairo

ASIA CONTRACT LOGISTICS

Revenue: AUD$602 million

• Oil and Gas Logistics

• Supply Chain Management

• Distribution of Bulk Materials

• Defence Logistics

• Project Logistics

• Specialist Logistics

• Marine Logistics

For

per

sona

l use

onl

y

TOLL – ANNUAL REPORT 2008 7

OUR REVENUE MIX IN 2008

A major strength of the business, particularly in relation to challenging economic environments is the level

of diversifi cation across industry segments and also across the customer base. The fact that the company

is not heavily reliant on specifi c discretionary consumer spending is positive in both diffi cult and strong

economic periods. And when you combine the profi le of our customers with our variable cost structure

relating to sub-contractor fl eet, Toll’s business model is sustainable no matter what the economic conditions.

*Excludes Virgin BlueDefence and

Government 15%

Mining and

Resources 13%

Automotive 9%

Retail and

FMCG 50%

Manufacturing 8%

Steel and Industrial 5%

REVENUE

CONTRIBUTION

BY

INDUSTRY

Strong market alignment between Australia, New Zealand and Asia

INDUSTRY AUSTRALIA NZ ASIA

Retail and FMCG (50%) Customers include: Coca-Cola Amatil, Foster’s Group, Palmolive, Unilever, Wesfarmers, Woolworths

4 4 4

Defence and Government (15%)Customers include: Australian Defence Force, Australian Taxation Offi ce, NT Government, QLD Purchasing

4 4 4

Mining and Resources (13%)Customers include: Rio Tinto, Xstrata, Zinifex 4 4

Automotive (9%)Customers include: Bridgestone, Ford Motor Co, General Motors, Holden, Mercedes Benz, Toyota Motor Co

4 4

Manufacturing (8%)Customers include: Amcor, Fletcher Building Group, Qenos, Viridian Glass 4 4 4

Steel and Industrial (5%)Customers include: BlueScope Steel, OneSteel, Orica 4 4

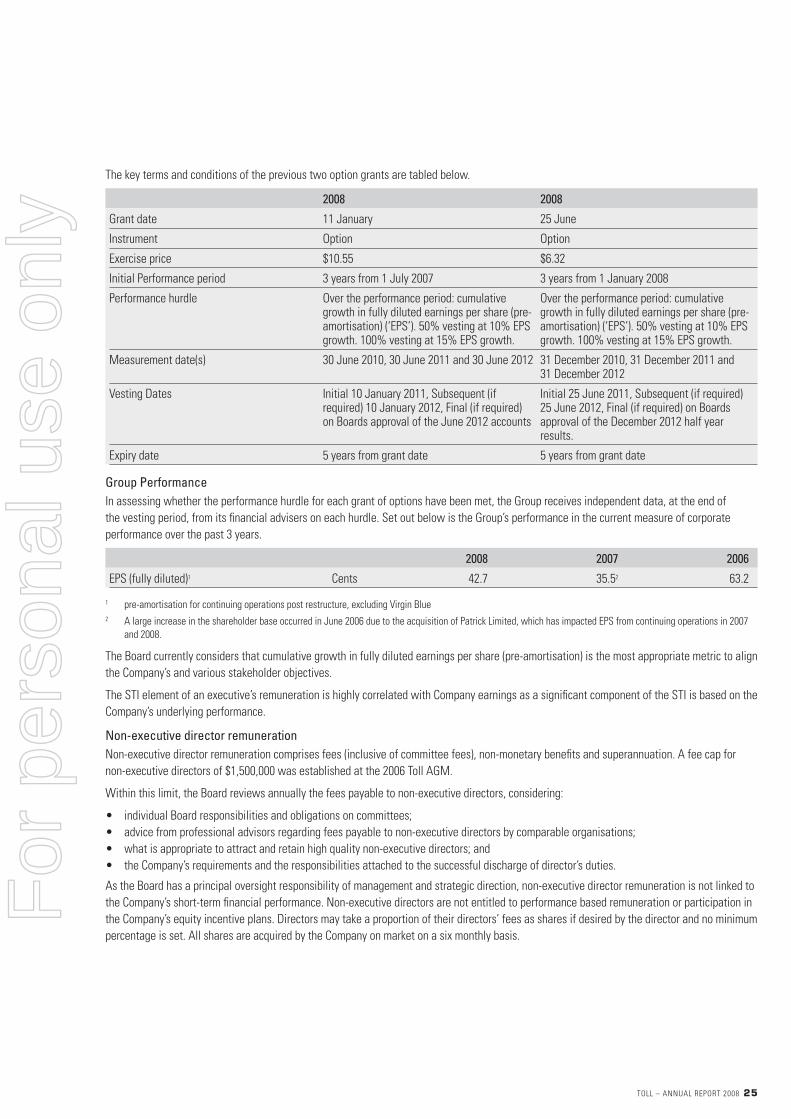

2008 GDP growth rates

China 9.3%

India 7.9%

Vietnam 7.3%

Cambodia 7.2%

Indonesia 6.1%

Thailand 5.3%

Malaysia 5.0%

Singapore 4.0%

Australia 3.2%

ASIA

Committed to optimising outcomes

MANAGING A COMPLEX ARRAY OF LOGISTICS SERVICES

Toll’s integrated logistics offering is developed from an array of complex service offerings, utilising all

modes of transport, a specialised range of integrated logistics services, an extensive range of freight

profi les, and covers all major territories and regions.

MODE

• Road

• Rail

• Sea

• Air

SERVICE

• Network transport

• Contract logistics

• 4PL

• Freight-Forwarding

FREIGHT PROFILE

• Satchels

• Packages

• Pallets

• FTLs

• Bulk

TERRITORY

• Australia

• New Zealand

• Japan

• China

• India

• Singapore

• Other

+ + +

Moscow

Dubai

Muscat

Karachi

New Delhi

Dhaka

MumbaiChennai

Colombo

Perth

AdelaideMelbourne

Hobart

CanberraSydney

Brisbane

Wellington

Auckland

Jakarta

Singapore

Kuala LumpurIpoh

Penang

BangkokBurma

Macau

ShenzhenGuangzhou

Chengdu

Hong Kong

XiamenFuzhou

Shanghai/Ningbo

Tokyo

SeoulBeijing

Tianjin

Dalian

Quingdao

Surabaya Darwin

Manila

Ho Chi Minh City

Taipei/Taichung/Kaohsiung/Hsinchu

TOLL GLOBAL FORWARDING

Revenue: AUD$358 million (four months trading)

• Air Freight

• Ocean Freight

• Consolidation and Deconsolidation

• Supplier Management

• Order Management

• Customs Brokerage

• Visibility and Information Management

For

per

sona

l use

onl

y

8

CORPORATE SOCIAL RESPONSIBILITY

Of course, Toll exists to deliver solid fi nancial results, and healthy returns to

our investors. But it’s not all we do, or all we are. In a world too frequently

beset by intolerance, fear, hunger and illiteracy, some of us are in a position

to help. We count ourselves among the fortunate — not only able to help,

but having the responsibility and the desire to help.

COMMUNITY

We are pleased to tell you that once again the company’s largest

ongoing community commitment is our support of First Step, a small

but successful non-profi t organisation assisting people who have a

dependency on drugs, particularly heroin.

For the eighth consecutive year we have provided not only fi nancial

assistance but time and expertise to help First Step do what they

do best, design and deliver treatment and management programs

for drug addiction and recovery. According to individual needs,

treatments may vary and include counselling, buprenorphine/

methadone maintenance programs, rapid detoxifi cation, naltrexone

tablets and slow release naltrexone implants.

Our connection with First Step has lead directly to the development

of the Second Step program.

Second Step

Begun in 2001, Second Step was designed to offer employment

opportunities to people who, as a result of previous drug or

incarceration issues, fi nd diffi culty in obtaining or retaining suitable

employment. The program provides a period of supported employment

and aims to help people to: replace their previous life style with a

safer and more constructive one; re-establish themselves within the

working world; develop strategies for coping with diffi culties in daily

life; establish a life style and work habit that will help them avoid

resuming previous self destructive behaviours; and move on to the

next stage of their life with skills, experience and a solid reference

for future employment.

We are very proud of our ongoing involvement and indeed in March

of this year, our participation in the Second Step program was

recognised when featured on a popular Australian television show the

7:30 Report. The response to the program aired was overwhelming,

and thousands of enquiries have been received at head offi ce. The

great thing was the high number of Australian corporations who

contacted us for further information.

There is no doubt First Step and Second Step are growing in

importance and infl uence and it is now our goal to develop the

programs to encourage the involvement of other corporations who

are as keen to support people coping with what would otherwise

be an overwhelming problem.

…At 4am on a cold winter’s day 18 months

ago, recovering drug addict Second Stepper

set off on an arduous ride into a new life.

She’d recently been released from jail

with no money, no possessions and no one

to turn to, except welfare agencies that

gave her clothes, a bike, and a place in

a supported employment program run by

Toll Holdings. Every day for the next three

months, she spent three hours travelling

each way by bike and train, from a boarding

house in Melbourne’s northern suburbs to a

job hauling boxes at a warehouse in the west.

Every day I used to think “What the hell am

I doing? This sucks, I hate it, I don’t wanna

do this” but I kept going, every day. They

offered me something nobody ever would.

They believed that I could do it. They trusted

me, so, and I promised them I would do it.

So I had to.

…It gives people like me hope. Hope that

someone will believe in them. That they are

willing to change. You can get out. And live

a normal life.

“

”7:30 Report – Australian Broadcasting Corporation

For

per

sona

l use

onl

y

TOLL – ANNUAL REPORT 2008 9

“Convoy for Kids

Operating across the Asian region, Convoy for Kids assists in the

welfare of sick and disabled children and for the tenth year we are

happy to be part of the programs conducted by this great organisation.

Surf Life Saving

Like most Australians we have an affi nity with beach culture,

and in particular the very important role surf life saving plays in

ensuring our beaches are safer for all beach goers. That’s why our

long-standing association with Sorrento Surf Life Saving Club is

now in its seventh year.

ENVIRONMENT

Toll is now into its third year of an enhanced focus on environmental

climate change. Since 2006, we have met the requirements of key

government environmental programs, that will lead Australia into

the Carbon Pollution Reduction Scheme.

In Australia, the focus at Toll has been to progressively improve

reporting and management processes. At the hub of this approach

is our Toll web-based management system, GEMS (Greenhouse

Emission Management System). Simply, GEMS converts all energy

sources to specifi c program units measuring the progress and

impact of Toll’s generated greenhouse gases.

Our focus on improving operational effi ciency has identifi ed

many aspects that impact fuel use throughout our fl eet. Vehicle

specifi cations will be further refi ned to ensure that the best

fl eet investments are implemented to maximise fuel savings and

return on investment. In addition, Toll will continue exploring the

use of alternative fuels and technologies based on research and

development results from its own and international trials.

Toll’s ongoing commitment to designing energy effi cient depots,

warehouses and distribution centres includes trials on improving

lighting systems, building design and potential implementation

of alternate energy sources such as solar power. In addition, Toll

recognises the need to maximise the use of rain water and seeks

to where possible capture multiple facility rain water to supply

truck cleaning facilities and toilet fl ushing systems.

Furthermore, Toll prefers to reduce emissions in place of acquiring

carbon credits through trading. We will seek additional emission

reduction opportunities to ensure the greatest savings are made

to meet our strategic goals and support our customers.

One of the common themes I see wherever I go,

is that governments either can’t or choose not to

support these sorts of programs as aggressively

as I think they should, and so business needs

to step up to the plate.

Paul Little – Managing Director

At Toll, we know that being a company in the community in which we

work means stepping up to real problems we face as people. And as a big

corporation we are in a position to help. Around the Asian region we actively

support a range of worthy initiatives, of which we are justly proud, including:

Foodbank Australia

For the fourth consecutive year we have continued our long-standing support

of Foodbank Australia. By providing transport services for the collection and

distribution of donated grocery and beverage products to more than 1,500

state-based accredited welfare agencies — The Salvation Army, Mission

Australia, St Vincent’s, The Smith Family and school Breakfast Clubs around

Australia — we help Foodbank feed more than 20,000 Australians daily.

Toll was proud to receive the 2008 Foodbank Partnership Award – for being

a pivotal partner in helping Foodbank achieve its vision of ‘an Australia

without hunger’.

Cancer Support

Supporting cancer research makes a difference, and Toll has a long history

of supporting cancer research groups across the country including Australia’s

Biggest Morning Tea, Shave for a Cure and Swinging for NZ Cancer Society

(Golf Day).

TLC for Kids

Toll is proud to support TLC for Kids Distraction Box Program which provides

urgent attention and immediate distractions to sick children and young

people, as well as support for families via an additional program, RAPID

TLC. Since the organisation was established ten years ago TLC for Kids

has helped over 13,500 people.

”

For

per

sona

l use

onl

y

10

BOARD OF DIRECTORS

Ray Horsburgh AMHon D Univ, FAICD, B.Chem Eng

Chairman from 14 September 2007Independent Non Executive Director

Director since 24 November 2004.

Extensive management experience in the glass and steel industries, mergers and acquisitions, managing businesses overseas especially in the SE Asian countries and building businesses in mainland China. Former Managing Director of Smorgon Steel Group Limited from 1998 to 30 June 2007. Non Executive Director of CSR Limited, National Can Industries Limited and Traffic Technologies Limited.

Age 65.

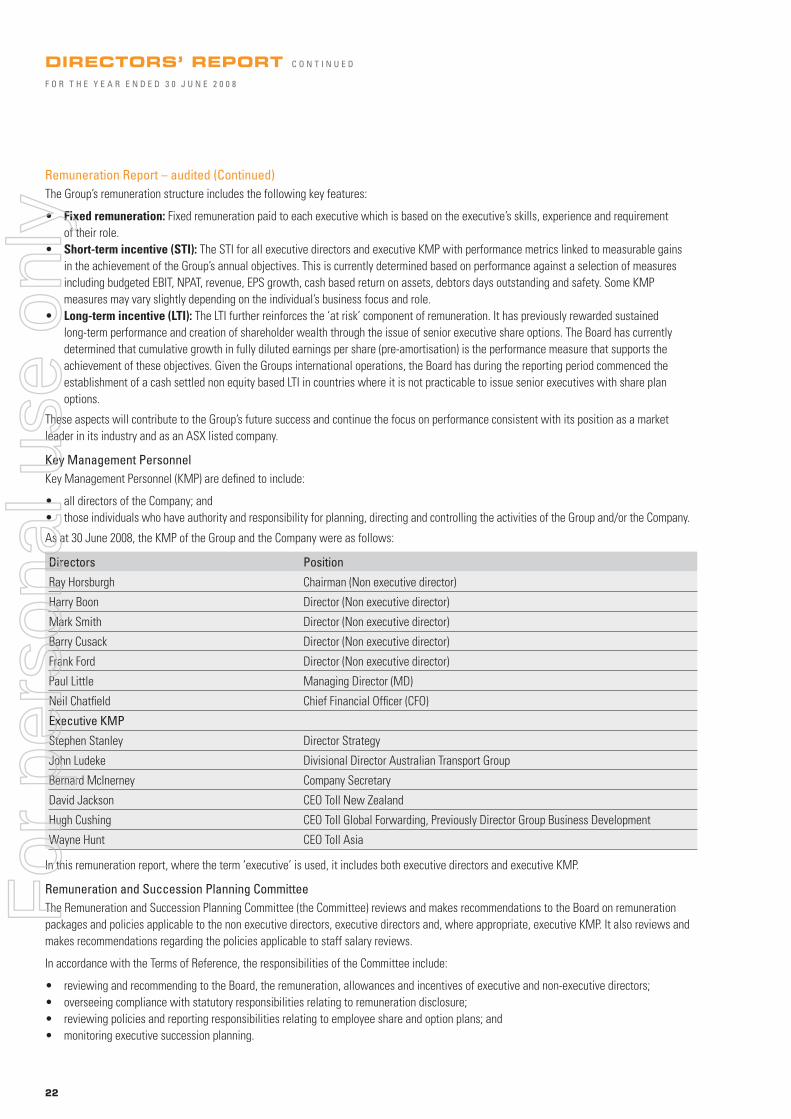

Special Responsibilities: Chairman of Board of Directors and the Nomination and Corporate Governance Committee. Member of the Remuneration and Succession Planning and Audit and Financial Risk Committees.

Paul LittleFAICD, FCIT

Managing Director

Managing Director since 1 May 1986.

Extensive experience and management in the logistics industry. Director of Virgin Blue Holdings Limited from May 2006 to August 2008. Age 60.

Special Responsibilities: Member of the Nomination and Corporate Governance Committee.

Harry BoonLLB (Hons), B Com (Melb)

Independent Non Executive Director

Director since 1 November 2006.

Extensive experience in global marketing and sales, large scale manufacturing operations, and product development. Chairman of Tatts Group Limited and Gale Pacific Limited and Non Executive Director of Hastie Group Limited, and former Director PaperLinX Limited and Funtastic Limited. Former Chief Executive Officer and Managing Director of Ansell Limited. Age 60.

Special Responsibilities: Chairman of the Remuneration and Succession Planning Committee. Member of the Nomination and Corporate Governance

Committee.

Mark SmithFAMI, CPM, FAIM, MAICD

Independent Non Executive Director

Director since 1 July 2007.

Extensive experience in senior roles including marketing with Unilever and Uncle Toby’s. Managing Director of Cadbury Schweppes Australia and New Zealand from 2003 to 2007. Former Managing Director of Confectionery ANZ and prior to that, three years as Director of Marketing for Cadbury Trebor Basset in the UK and senior positions in Cadbury Schweppes’ North American and Australian operations. Age 53.

Special Responsibilities: Chairman of the Audit and Financial Risk Committee. Member of the Nomination and Corporate Governance Committee.

TOLL GROUP STRUCTURE

Managing Director/CEO

Paul Little

Global Forwarding

Hugh Cushing

Acting CFO

Mal Grimmond

Strategy M&A

Stephen Stanley

Company Secretary

Bernard McInerney

Asia Contract Logistics

Wayne Hunt

Australia

John Ludeke

New Zealand

David Jackson

For

per

sona

l use

onl

y

TOLL – ANNUAL REPORT 2008 11

Barry CusackBE (Hons), M. Eng. Sci, FTSE, FAusIMM, FAIM, MAICD

Independent Non Executive Director

Director from 1 October 2007.

In an executive career of 40 years in the minerals industry with the Rio Tinto Group, held positions of Managing Director of Dampier Salt, Hlsmelt Corporation, Hamersley Iron Operations and Rio Tinto Australia and was Chairman of Rio Tinto Asia and Rio Tinto Shipping.

Chairman of 0Z Minerals Limited and a Non Executive Director of MacMahon Holdings Limited. Past President of the Minerals Council of Australia, 2001 to 2003.Age 66.

Special Responsibilities: Member of the Nomination and Corporate Governance and Remuneration and Succession Planning Committees.

Frank Ford M. Tax(Melb), B Bus (Acc), FCA

Independent Non Executive Director

Director since 14 January 2008.

Former Managing Director Deloitte

Victoria after a long and successful

career as a professional advisor

spanning some 35 years. During that

period, Mr Ford was also a member

of the Deloitte Global Board, Deloitte

Global Governance Committee and also

the Deloitte National Management

Committee.

Director of Citigroup Pty Limited and

Tarrawarra Museum of Art Limited.

Age 62.

Special Responsibilities: Member

of Audit and Financial Risk and the

Nomination and Corporate Governance

Committees.

Bernard McInerneyAICS, CPA, AICD, B Bus (Acc)

Company Secretary

Company Secretary since 1994. Also held the position of General Manager Finance and Administration from 1994 until late 1997. Extensive experience in business acquisitions and accounting and financial management within the logistics industry over the last 24 years. Director of Virgin Blue Holdings Limited from September 2006 to August 2008. Age 50.

Special Responsibilities: Member of the Risk Management Committee.

Neil Chatfield FCPA, FAICD

Chief Financial Officer to September 2008

Director from 1998 to 18 September 2008.

Over 30 years experience in the resources and transport sectors. Extensive experience in financial management, capital markets, mergers and acquisitions and risk management. Non Executive Director of Seek Limited since 2005 and Non Executive Director of Whitehaven Coal since 2007. Chairman of Virgin Blue Holdings Limited since June 2007 and Director of Virgin Blue Holdings Limited since May 2006. Age 54.

SENIOR MANAGEMENT

John LudekeGroup Director – Toll Australia and New Zealand

Joined Toll 1996. Current position since May 2007.

Previously, Group Director Toll Australia Group since June 2006 and Group Director Long Distance/ Networks Divisions since 1997.

Extensive experience over 26 years in a number of senior management positions within the transport and logistics industry.

Age 59.

Chairman of Toll NZ Limited from January 2007 to June 2008.

Director of Virgin Blue Holdings Limited from June 2007 to August 2008.

Stephen StanleyDirector, Strategy, Mergers and Acquisitions

Joined Toll 1999. Current position since 1999. Extensive experience in the transport industry and management. Responsible for strategy, portfolio review, marketing growth initiatives involving acquisitions, joint ventures and major business developments. Age 50.

Wayne HuntPresident/CEO – Toll Asia

Joined Toll 1990. Current position since August 2007. Previously held positions as Group General Manager Intermodal at Pacific National and Divisional GM Toll AutoLogistics, General Manager Group Development, National Sales & Marketing Manager Toll Express and NSW Marketing Manager.

Twenty-four years experience in the logistics industry. Age 56.

Member of the Chartered Institute of Logistics and Transport Australia.

Hugh CushingCEO – Toll Global Forwarding

Joined Toll in 1997 with the acquisition of the TNT Australia businesses. In current position since 1 July 2008. Previously Director Business Development and was responsible for the Toll Solutions technology development team.

Thirty-two years experience in operational, commercial and general management positions. Age 51.

David JacksonChief Executive Officer – Toll NZ Limited

Joined Toll 1996. Current position since October 2003. Previously, General Manager of Toll SPD.

Thirty years experience in various management roles in the transport and logistics industry. Age 51.

Director of Toll NZ Limited from October 2003 to August 2008.

Trustee of Chris Cairns Foundation.

Director of WNC 2007 Limited.

Malcolm GrimmondActing Chief Financial OfficerDirector, Business Solutions and Chief Information Officer

Joined Toll 1997. Acting CFO since September 2008. Current position, CIO since 2006. Previously CFO Pacific National and Divisional Financial Controller Toll Logistics.

Thirteen years experience in financial, commercial and management positions in the transport and logistics industry.Age 45.

After 11 years with Toll, Neil has decided to pursue private interests and concentrate on his Non Executive Director roles. Neil leaves Toll in March 2009. We thank him for his valued contribution and wish him well.

For

per

sona

l use

onl

y

12

F INANCIAL STATEMENTS AND

DIRECTORS’ REPORT

FOR THE YEAR ENDED 30 JUNE 2008

For

per

sona

l use

onl

y

TOLL – ANNUAL REPORT 2008 13

The directors present their report together with the fi nancial report of

Toll Holdings Limited (‘the Company’) and the consolidated fi nancial

report of the consolidated entity, being the Company and its controlled

entities (‘the Group’), for the year ended 30 June 2008 and the

auditors’ report thereon.

Directors

The following persons held offi ce as directors of the Company during

or since the end of the fi nancial year:

Ray Horsburgh AM (Chairman) Director since 2004

John Moule AM Director since 1995

(Retired 14 September 2007)

Paul Little (Managing Director) Director since 1986

Neil Chatfi eld Director since 1998

Harry Boon Director since 2006

Mark Smith Appointed 1 July 2007

Barry Cusack Appointed 1 October 2007

Frank Ford Appointed 14 January 2008

Principal Activities

The principal activities of the Group during the year consisted of:

• Less than full load express and economy freight forwarding

service using all modes of transport;

• Full load road and rail freight forwarding service including rail

linehaul operation;

• Temperature controlled transport service for full load and less

than full load clients;

• Warehousing and distribution of bulk dry and refrigerated goods;

• Wharf cartage, container handling and storage;

• Contract distribution services;

• Time sensitive parcel freight distribution services;

• Specialised international forwarding services;

• Removals and relocation brokerage service;

• Vehicle transport and distribution;

• Bulk liquid transportation;

• Shipping linehaul operations for freight and passengers;

• Rail passenger operations; and

• Air passenger operations.

Consolidated Result

The consolidated profi t from ordinary activities for the year

attributable to the members of the Company was:

2008$M

2007$M

Net profi t/(loss) attributable to members of the Company (694.7) 1,278.7

Earnings per share

Basic earnings per share (107.41¢) 202.52¢

Diluted earnings per share (107.41¢) 197.39¢

Continuing operations

Basic earnings per share 38.72¢ 4.36¢

Diluted earnings per share 38.70¢ 4.33¢

Review of Operations

Toll Holdings, the Asian region’s leading integrated transport and

logistics provider, has reported after tax earnings for the year to

30 June 2008 of $258 million in relation to continuing businesses.

This result excludes discontinuing businesses ($945m loss) and net

one-off items ($7m), refl ecting a total loss of $952 million relating

mainly to the non-cash restructure of the Virgin Blue investment

and gain on sale of the New Zealand rail and ferry operations.

Revenue from continuing businesses was $5.6 billion for the year

with EBIT, pre-acquisition accounting amortisation of $429 million.

This compares to $4.9 billion and $365 million respectively on a

like for like basis in the previous year.

Divisional Performance

Following the in specie Virgin Blue special dividend and sale of the

New Zealand rail and ferry operations, the Company has established

three major operating divisions, namely Australia and New Zealand

Integrated Transport and Logistics, Toll Asia Contract Logistics and

Toll Global Forwarding.

Comparative results have been restated for consistency into the three

divisions and all references to divisional EBIT are pre-amortisation of

charges arising from acquisition accounting and one-off items.

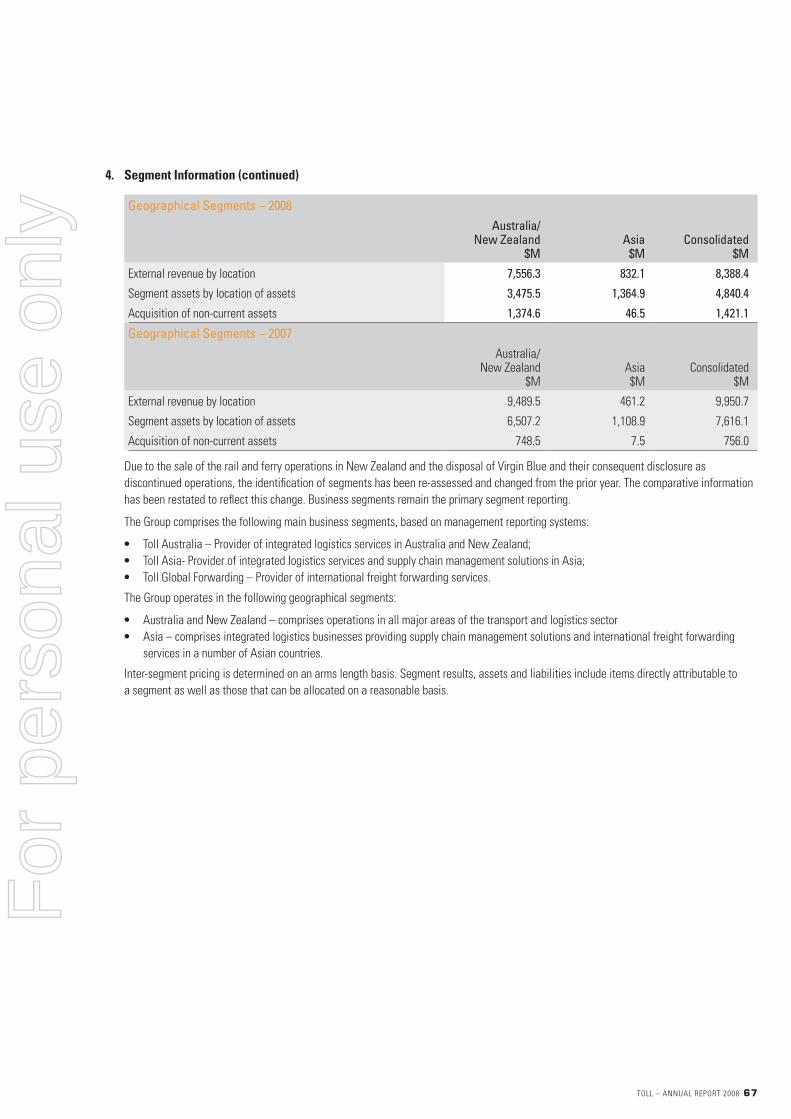

Toll Australia and New Zealand

Trading results across the Australian division continued to

demonstrate strong revenue and earnings growth. EBIT margin

expansion also continued, as improved effi ciencies and cost control

were achieved.

Revenue for Australia for the year was $4.42 billion, which after

eliminating the impact of acquisitions and incremental fuel

surcharges, represented an underlying organic increase of 7.5%

over the previous year of $4.05 billion.

EBIT for Australia grew over 18% to $347 million compared to

$294 million previously. This resulted in the EBIT margin increasing

from 7.21% to 7.84% maintaining the margin expansion evident

over the past few years.

DIRECTORS’ REPORT

F O R T H E Y E A R E N D E D 3 0 J U N E 2 0 0 8

For

per

sona

l use

onl

y

14

Review of Operations (continued)

There were numerous other highlights in the Australian division over

the year, these included:

• completion of a long term domestic freight operations agreement

with Virgin Blue;

• acquisitions of the Victorian Express, Couriers Australia and

SkyNet businesses;

• signifi cant new contract wins in the retail, mining and automotive

sectors;

• establishment of a Joint Venture with Dnata;

• transfer of Jetcare maintenance facilities to Virgin Blue; and

• continued integration and rationalisation of Patrick warehousing

and logistics activities.

Trading conditions generally remained strong throughout the year. In

particular, the resource, food, beverage and retail sectors experienced

solid volumes. Defence logistics also recorded strong activity.

The Company continued to invest heavily in technology, infrastructure

and new fl eet, providing increased cost effi ciency and capacity to

facilitate future growth.

The express and time sensitive operations of the Company grew

strongly throughout the year, supported by investment in a new

national air linehaul network and targeted acquisitions. These express

operations represent approximately 35% of divisional revenue and

are pivotal in servicing increased volumes arising from Asian direct

sourcing activities of Australian customers.

Toll IPEC, the Company’s road parcel express business, performed

strongly during the year, benefi ting from integrating services with

group warehousing and distribution operations and utilising its

comprehensive network to grow market share.

Toll Priority, our air express operator, also performed well and

completed the acquisition of SkyNet, an international air express

operator. Whilst the cost of additional investment in the air linehaul

network impacted results, it is expected that potential integration with

the developing international Asian air network will drive additional

profi table growth for Toll Priority.

The Toll Dnata aviation logistics joint venture with Emirates,

established early in the year, continued to secure additional growth

including the acquisition of the Skystar and Aerocare businesses.

Toll Express and Toll SPD, the Company’s road and rail forwarding

operation, traded well with increased volumes and achieved

effi ciencies through technology and fl eet investments.

NQX had a strong result from increased activity in the resource sector,

as well as enhanced national trade emanating from Queensland.

Our Queensland rail forwarder, QRX, had a diffi cult year with major

fl ooding and derailments disrupting services.

In the automotive sector, domestic manufactured vehicles continued

to experience fl at conditions as the high Australian dollar favoured

imports. Notwithstanding these conditions, Toll Automotive performed

well, growing market share and supporting customers with Asian

based sourcing arrangements.

PDL Toll, the Group’s defence logistics operator, traded strongly and

extended its capability in both aviation and marine services. PDL Toll

is currently furthering its defence and United Nations footprint into

developing countries.

Looking at economic conditions and the likely impact on operations

within Australia, no major deterioration is evident, notwithstanding

a number of challenging factors including increased interest rates,

high fuel prices and currency volatility.

Following the sale of the rail and ferry operations back to the

NZ Crown, Toll New Zealand now consists of contract logistics and

road and rail forwarding operations under the Tranzlink brand. The

sale, which was effective 30 June 2008, will enable the Company

to focus on accelerating growth in forwarding and logistics within

New Zealand.

New Zealand revenue for the year was NZ$255 million compared

to NZ$234 million previously whilst EBIT was NZ$9.4 million against

NZ$7.3 million previously.

Results for the year benefi ted from increased rail linehaul and

warehousing effi ciencies. Investment in technology and new facilities

is expected to assist growth in the next 12 months.

Effective 30 June 2008, the Company acquired the United Carriers

business. This business further expands our road and rail forwarding

base in New Zealand, particularly into Northland where the Company

previously had a limited presence.

Whilst the New Zealand economy remains subdued, we are

increasing our focus on acquisition opportunities, to add further

scale and capability to existing operations.

Toll Asia

The Group’s presence in Asia within the contract and marine

logistics sectors continued to grow strongly throughout the year.

The integration of Sembawang Kimtrans is now complete and has

proceeded very well.

Total revenue for Toll Asia for the year was S$777 million compared

to S$563 million in the prior year. On a like for like basis and excluding

the impact of the Sembawang Kimtrans acquisition, underlying

revenue grew 12.5% continuing the successful growth rates in

new business established over the past 18 months.

EBIT for the year (including share of associates) was S$82 million,

a 12% increase over the S$73 million recorded in the prior year.

Underlying revenue and EBIT growth accelerated in the second half

of the fi nancial year.

Highlights for Toll Asia during the course of the year included:

• full takeover of the Sembawang Kimtrans operations;

• strong growth in offshore supply operations;

• strong contract retention rates; and

• management restructure and appointment of Toll CEO.

Revenue grew strongly across most of the business, in particular the

offshore marine and mining logistics operations which benefi ted from

high levels of activity in the energy sector.

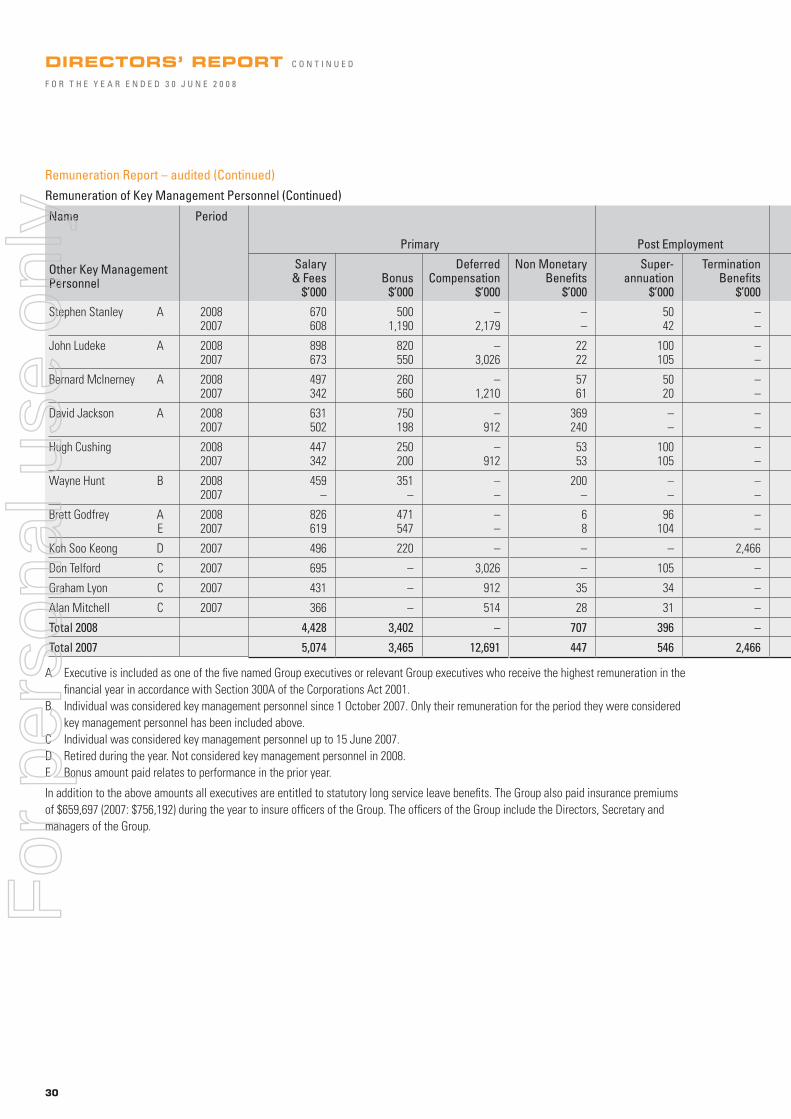

DIRECTORS’ REPORT C O N T I N U E D

F O R T H E Y E A R E N D E D 3 0 J U N E 2 0 0 8

For

per

sona

l use

onl

y

TOLL – ANNUAL REPORT 2008 15

Solid revenue growth was experienced in Malaysia, Thailand, Vietnam

and China, with higher revenue from existing customers and new

contracts providing the increase.

The Government defence logistics operations continued to perform

well and traded up on plan. As expected, additional opportunities to

leverage the defence logistics capability in Singapore to other group

operations has created further growth in this important sector.

During the year the contribution from associates reduced from

S$13.9 million to S$3 million, partially due to the acquisition of

previous associates Sembawang Kimtrans and Thailand and disposal

of associates in the prior year. Equity accounted results from 38%

owned Footwork Express reduced signifi cantly due to continued

depressed economic conditions in Japan, high levels of competition

and a one-off income tax charge.

The Group is currently reviewing its investment in Footwork Express

in order to maximise value and determine the optimum way for the

Company to leverage the comprehensive Japanese network within

Footwork Express.

The growth now being experienced in our Toll Asia businesses is

expected to be further enhanced by the integration of services with

Toll Global Forwarding, creating tailored solutions for customers

seeking cross border supply chain solutions.

Toll Global Forwarding (TGF)

The TGF division has been developed to consolidate capabilities

across the Group in order to offer customers end-to-end international

supply chain solutions.

The global footprint for TGF has been established with the successful

takeover of BALtrans, a Hong Kong based listed company, effective

1 March 2008.

The strategic rationale for the BALtrans transaction and the

establishment of TGF was to develop a service offering, which

when combined with in-country transport capabilities, would deliver

effi ciencies to customers’ international supply chains.

TGF has not only enhanced the Group’s global air and ocean freight

forwarding capabilities, but provided a global network including

operations in Europe, North America and the Middle East as well

as Asia Pacifi c.

In June 2008 the Group acquired a 100% interest in Gluck, an

Australian based international forwarder with a close long term

relationship with BALtrans in Asia. The acquisition of Gluck enables

all the Australian forwarding operations to be consolidated, thereby

providing scale and additional capability.

In the year to 30 June 2008, TGF recorded revenues of $358 million

compared to the prior year, which related only to the Australian

operations of $145 million. EBIT for the year was $10.9 million

against $4.9 million in the previous period.

During the period since the acquisition of BALtrans in March 2008, the

business has seen strong improvement in both revenue and earnings

compared to the corresponding period in the previous year. This was

refl ective of a more stable leadership team and increased focus on

business development.

TGF has a detailed integration plan to ensure that all international

forwarding operations across the Group are co-ordinated under one

infrastructure, and to ensure that the assets, both in Australia and

Asia, are leveraged to provide a wholly integrated service to customers.

A number of management changes have been made in order to

align the BALtrans operations with the Toll business model, and the

Group’s Director of International Development, Mr Hugh Cushing has

been appointed CEO of the TGF business. A number of other positive

management changes have also been affected.

To date the integration of TGF is proceeding very well and a number

of new customer contracts have been secured with a very promising

pipeline of prospective opportunities.

Discontinuing Operations

Effective 30 June 2008, Virgin Blue became a discontinued operation

as a consequence of the decision to distribute Virgin Blue shares to

shareholders via a special in specie dividend.

Revenue for the year for Virgin Blue was $2.35 billion compared

to $2.17 billion, while profi t after tax was $97.7 million compared

to $215.8 million. Earnings were impacted by high fuel costs, a

competitive market place and investment in new operations.

Also effective 30 June 2008 was the New Zealand rail and ferry

sale to the Crown, and these operations became characterised as

discontinued. Revenue for the year in relation to these operations

was NZ$555 million compared to NZ$543 million previously. EBIT

for the year was NZ$56 million compared to NZ$52 million in the

previous period.

Finance

Net debt at 30 June 2008 was $1.27 billion, including Reset

Preference Shares of $250 million. Following the settlement of the

New Zealand rail and ferry sale after balance date, net debt fell to

approximately $650 million. Based on net debt of $650 million, gearing

(measured on a net debt to equity plus net debt basis) was 24%.

Interest cover remained very strong at over 12 times.

Cashfl ow from continuing operations was $496 million, which

refl ected the ongoing strength of the core activities of the Group.

Throughout the year the Group continued to invest heavily in growth.

Investment in acquisitions amounted to $796 million, whilst net

capital expenditure was $380 million. The acquisition investments

which included BALtrans and Sembawang Kimtrans also included

a number of smaller strategic acquisitions designed to broaden

the Group’s capability and scale. The availability of value adding

acquisitions is particularly strong as smaller industry players in both

Australia and Asia come under increasing pressure, both fi nancially

and in their ability to meet service demands.

For

per

sona

l use

onl

y

16

Review of Operations (continued)

Earnings per share (fully diluted) from continuing operations for the

year was 42.7 cents per share, pre acquisition amortisation charges

and one-off items, compared to 35.5 cents per share in the prior

period.

The Company has declared a fi nal dividend of 11.5 cents per ordinary

share, bringing the full year dividend to 25 cents per share. The

dividend, on continuing operations represents a 20% increase over

the previous year, on a constant payout ratio basis.

Industry Conditions

Over the past year, the industry has continued to consolidate both on

a domestic and global scale. However, there is a consistent theme

of enhanced focus on international supply chain management.

Notwithstanding slowing economic conditions in some regions,

trade-fl ows both by air and sea remained robust with Asia being

central to global logistics.

In Australia, as more and more companies look to direct international

sourcing in order to remain competitive, opportunities to work with

these groups is increasing. Toll has assembled a strong capability in

terms of technology and operational expertise and this is expected

to drive growth over the long term.

Industry conditions for contract logistics businesses throughout the

world have remained challenging and companies with limited supply

chain focus are likely to come under increasing pressure. In contrast,

companies with the ability to provide highly integrated solutions are

increasingly better positioned to gain market share, higher margins

and to benefi t from increased outsourcing.

High fuel prices have remained a challenge for the industry, with

most industry players adopting fuel surcharging mechanisms. At Toll,

we have a rigorous system of surcharging to ensure that the volatility

of fuel costs is appropriately managed and communicated to our

customer base. In addition, fuel conservation programs are in place

around the Group to promote reduced fuel usage where possible.

In the next twelve months, we expect industry rationalisation to

continue with many larger and smaller players under pressure due

to excess gearing, unsustainable business models and poor execution.

As industry valuation multiples also reduce, it is likely that a range of

acquisition opportunities will present themselves to the Company.

Environment

Toll is now into its third year of an enhanced focus on environmental

climate change.

Since 2006 we have met the requirements of key government

environmental programs that will lead Australia into the Carbon

Pollution Reduction Scheme.

In Australia the focus at Toll has been to progressively improve

reporting and management processes. At the hub of this approach

is our previously reported Toll web based management system,

GEMS (Greenhouse Emission Management System). Simply, GEMS

converts all energy sources to specifi c program units measuring the

progress and impact of Toll’s generated greenhouse gases.

Our focus on improving operational effi ciency has identifi ed

many aspects that impact fuel use throughout our fl eet. Vehicle

specifi cations will be further refi ned to ensure that the best fl eet

investments are implemented to maximise fuel savings and return

on investment.

In addition, Toll will continue exploring the use of alternative fuels

and technologies based on research and development results from

its own and international trials.

Toll’s ongoing commitment to designing energy effi cient depots,

warehouses and distribution centres includes trials on improving

lighting systems, building design and potential implementation

of alternate energy sources such as solar power. In addition, Toll

recognises the need to maximise the use of rain water and seeks

to where possible capture multiple facility rain water to supply

truck cleaning facilities and toilet fl ushing systems.

Finally, Toll prefers to reduce emissions in place of acquiring carbon

credits through trading. We will seek additional emission reduction

opportunities to ensure the greatest savings are made to meet our

strategic goals and support our customers.

Economic Conditions

Generally economic conditions remained solid in the regions in which

the Company participates. In Australia, there has been no noticeable

slowdown and, although much current economic data is pointing to

a slowdown in consumption, the Company does not expect a serious

deterioration in conditions.

In New Zealand conditions remain fl at. Most Asian countries in which

the Group operates continue to demonstrate solid growth.

Whilst considerable volatility exists in global energy prices and on global

debt and equity markets, fundamentals in the logistics sector remain

favourable as global trade and the trend to outsourcing continues.

DIRECTORS’ REPORT C O N T I N U E D

F O R T H E Y E A R E N D E D 3 0 J U N E 2 0 0 8

For

per

sona

l use

onl

y

TOLL – ANNUAL REPORT 2008 17

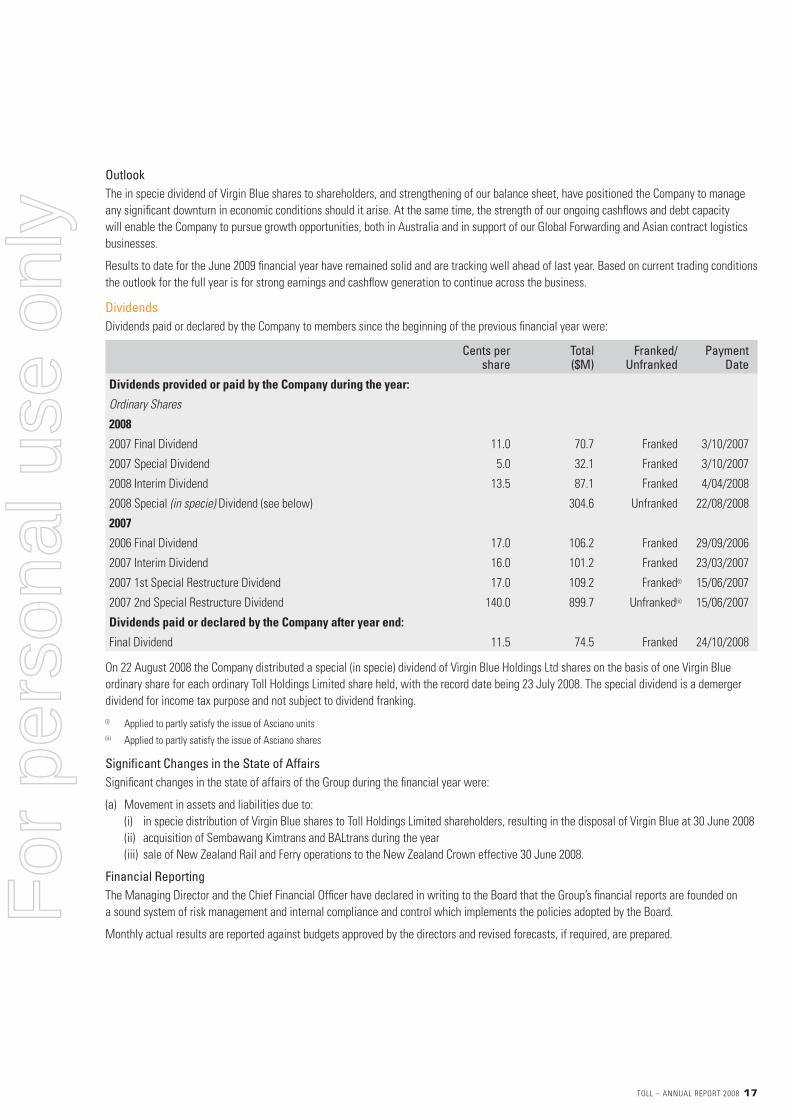

Outlook

The in specie dividend of Virgin Blue shares to shareholders, and strengthening of our balance sheet, have positioned the Company to manage

any signifi cant downturn in economic conditions should it arise. At the same time, the strength of our ongoing cashfl ows and debt capacity

will enable the Company to pursue growth opportunities, both in Australia and in support of our Global Forwarding and Asian contract logistics

businesses.

Results to date for the June 2009 fi nancial year have remained solid and are tracking well ahead of last year. Based on current trading conditions

the outlook for the full year is for strong earnings and cashfl ow generation to continue across the business.

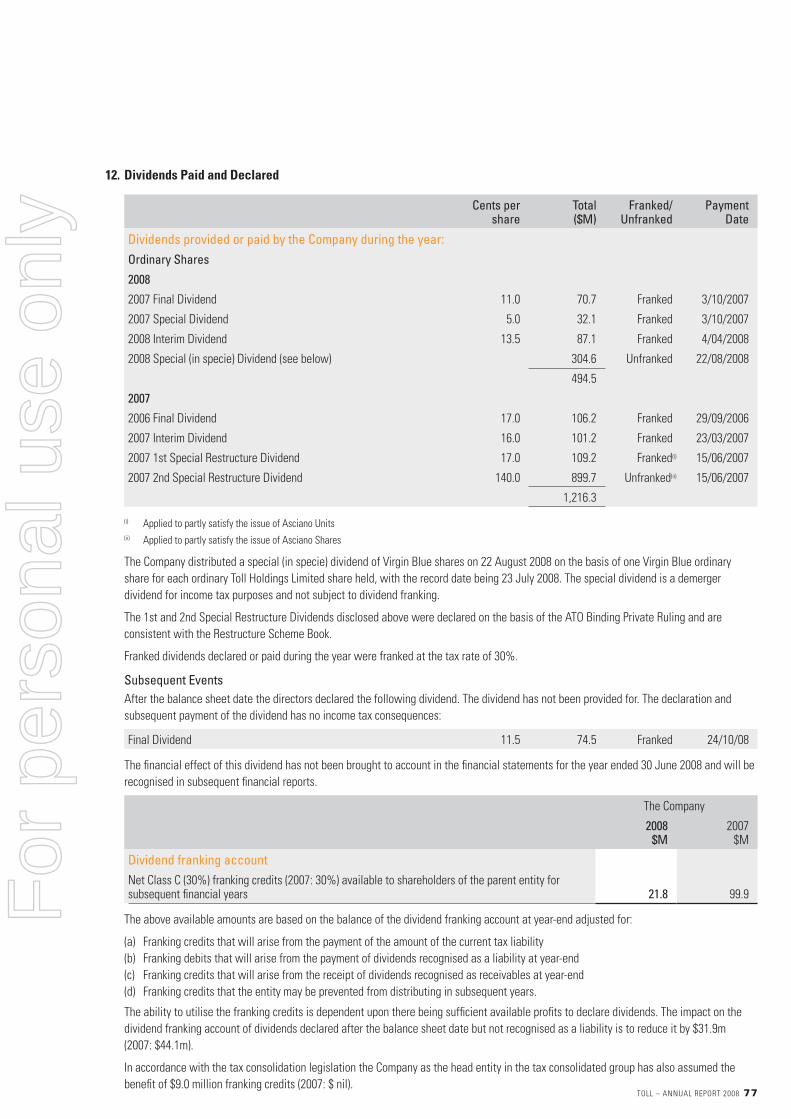

Dividends

Dividends paid or declared by the Company to members since the beginning of the previous fi nancial year were:

Cents per

share Total ($M)

Franked/Unfranked

Payment Date

Dividends provided or paid by the Company during the year:

Ordinary Shares

2008

2007 Final Dividend 11.0 70.7 Franked 3/10/2007

2007 Special Dividend 5.0 32.1 Franked 3/10/2007

2008 Interim Dividend 13.5 87.1 Franked 4/04/2008

2008 Special (in specie) Dividend (see below) 304.6 Unfranked 22/08/2008

2007

2006 Final Dividend 17.0 106.2 Franked 29/09/2006

2007 Interim Dividend 16.0 101.2 Franked 23/03/2007

2007 1st Special Restructure Dividend 17.0 109.2 Franked(i) 15/06/2007

2007 2nd Special Restructure Dividend 140.0 899.7 Unfranked(ii) 15/06/2007

Dividends paid or declared by the Company after year end:

Final Dividend 11.5 74.5 Franked 24/10/2008

On 22 August 2008 the Company distributed a special (in specie) dividend of Virgin Blue Holdings Ltd shares on the basis of one Virgin Blue

ordinary share for each ordinary Toll Holdings Limited share held, with the record date being 23 July 2008. The special dividend is a demerger

dividend for income tax purpose and not subject to dividend franking.

(i) Applied to partly satisfy the issue of Asciano units

(ii) Applied to partly satisfy the issue of Asciano shares

Signifi cant Changes in the State of Affairs

Signifi cant changes in the state of affairs of the Group during the fi nancial year were:

(a) Movement in assets and liabilities due to:

(i) in specie distribution of Virgin Blue shares to Toll Holdings Limited shareholders, resulting in the disposal of Virgin Blue at 30 June 2008

(ii) acquisition of Sembawang Kimtrans and BALtrans during the year

(iii) sale of New Zealand Rail and Ferry operations to the New Zealand Crown effective 30 June 2008.

Financial Reporting

The Managing Director and the Chief Financial Offi cer have declared in writing to the Board that the Group’s fi nancial reports are founded on

a sound system of risk management and internal compliance and control which implements the policies adopted by the Board.

Monthly actual results are reported against budgets approved by the directors and revised forecasts, if required, are prepared.

For

per

sona

l use

onl

y

18

Environmental Regulation

The operations of the Group in Australia are subject to various environmental regulations under both Commonwealth and State legislation.

In making this report, the directors note that the Group’s operations frequently involve the use or development of land, the transport of goods and

people, the storage, transport and disposal of waste and the use of transportation equipment. Some of these activities require a licence, consent

or approval from Commonwealth or State regulatory bodies. This regulation of the Group’s activities is typically of a general nature, applying to

all persons carrying out such activities, and does not in the directors’ view comprise particular and signifi cant environmental regulation.

Based upon enquiries within the Group, the directors are not aware of any breaches of particular and signifi cant environmental regulation

affecting the Group’s operations.

The directors believe the environmental performance of the Group is sound and that the Group has appropriate systems in place for the

management of its ongoing corporate environmental responsibilities.

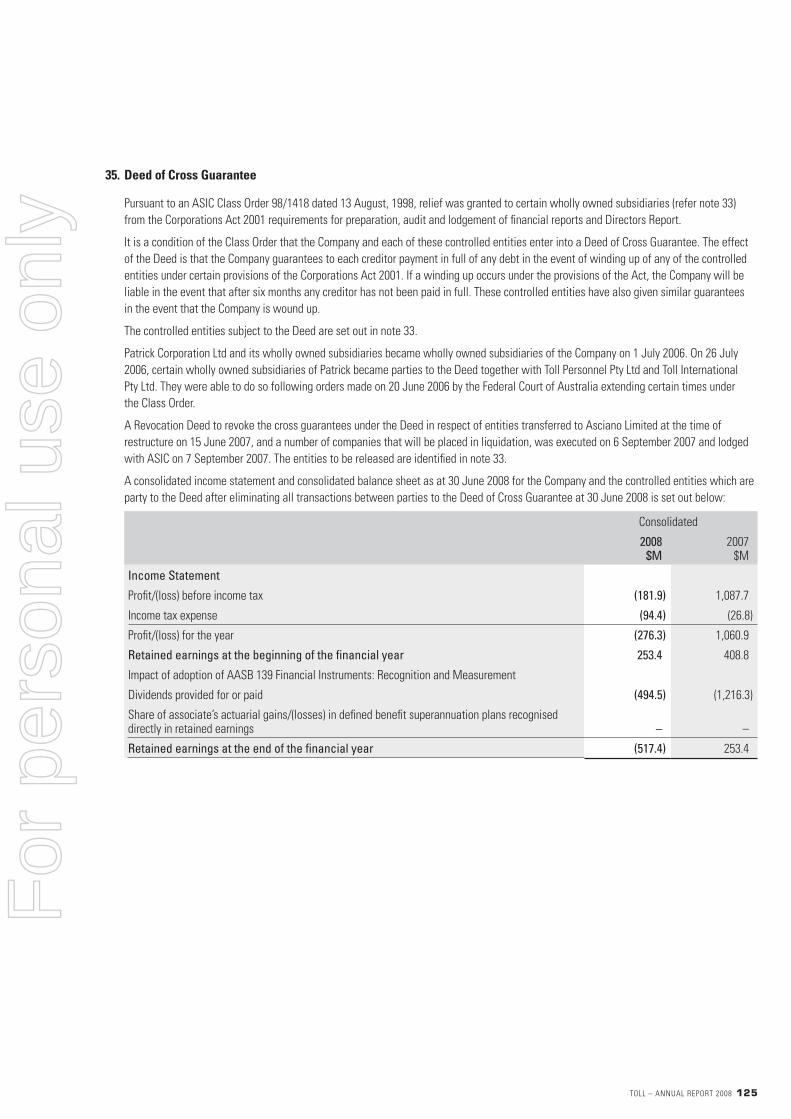

Events Subsequent to Balance Date

Dividends

A fi nal dividend of 11.5 cents per share has been declared by the directors.

On 22 August 2008 the Company distributed a special (in specie) dividend of Virgin Blue Holdings Ltd shares on the basis of one Virgin Blue

ordinary share for each ordinary Toll Holdings Limited share held , with the record date being 23 July 2008. The special dividend is a demerger

dividend for income tax purpose and not subject to dividend franking.

Likely Developments and Expected Results of Operations

The Group will continue to pursue its policy of increasing the profi tability and market share of its businesses during the next fi nancial year.

Information as to likely developments in the operations of the Group and the expected results of those operations in future fi nancial years has

not been included in this report because, the directors believe on reasonable grounds, that to include such information would be likely to result

in unreasonable prejudice to the Group.

DIRECTORS’ REPORT C O N T I N U E D

F O R T H E Y E A R E N D E D 3 0 J U N E 2 0 0 8

For

per

sona

l use

onl

y

TOLL – ANNUAL REPORT 2008 19

Information on Directors

Director Experience & Qualifi cations Age Special Responsibilities*

R Horsburgh AMHon D Univ, FAICD,BChem EngIndependent Non Executive Director

Extensive management experience in the glass and steel industries, in mergers and acquisitions, managing businesses overseas especially in the SE Asian countries and building businesses in mainland China. Director since 2004. Appointed Chairman from 14 September 2007.Former Managing Director of Smorgon Steel Group Limited from 1998 to June 2007. Non Executive Director of CSR Limited , National Can Industries Limited and Traffi c Technologies Limited since 2006.

65 Chairman of Board of Directors Chairman of the Nomination and Corporate Governance Committee and Member of the Remuneration and Succession Planning Committee and Audit and Financial Risk Committee. Chairman of the Audit and Financial Risk Committee up to February 2008.

P A LittleFAICD, FCITManaging Director

Extensive experience and management in the logistics industry. Managing Director for 20 years. Director since 1986. Director of Virgin Blue Holdings Limited from May 2006 to August 2008.

60 Member of the Remuneration and Succession Planning and Nomination and Corporate Governance Committees.

N Chatfi eldFCPA, FAICDChief Financial Offi cer

Over 30 years experience in the resources and transport sectors. Extensive experience in fi nancial management, capital markets, mergers and acquisitions and risk management. Director since 1998. Non Executive Director of Seek Limited since 2005 and of Whitehaven Coal Limited since 2007. Chairman of Virgin Blue Holdings Limited since June 2007 and Director of Virgin Blue Holdings Limited since May 2006.

54 Member of the Risk Committee.

H BoonLLB(Hons), BCom(Melb)Independent Non Executive Director

Extensive experience in global marketing and sales, large scale manufacturing operations, and product development. Director since 1 November 2006. Currently Chairman of Tatts Group Limited and Gale Pacifi c Limited and Non Executive Director of Hastie Group Limited since 2005, PaperlinX Limited since May 2008 and of Funtastic Limited from 2004 to 2007. Former Chief Executive Offi cer and Managing Director of Ansell Limited.

60 Chairman of the Remuneration and Succession Planning Committee from March 2008. Member of Nomination and Corporate Governance Committee. Member of the Audit and Financial Risk Committee up to February 2008.

M SmithFAMI, CPM, FAIM, MAICD Independent Non Executive Director

Extensive experience in senior roles including marketing with Unilever and Uncle Toby’s. Director since 1 July 2007. Managing Director of Cadbury Schweppes Australia and New Zealand from 2003 to 2007. Former Managing Director of Confectionery ANZ and prior to that, three years as Director of Marketing for Cadbury Trebor Basset in the UK and senior positions in Cadbury Schweppes’ North American and Australian operations.

53 Chairman of Audit and Financial Risk Committee from March 2008. Member of Nomination and Corporate Governance Committee and a Member of the Remuneration and Succession Planning Committee up to February 2008.

B CusackBE(Hons),M.Eng.Sci., FTSE, FAusIMMFAIM, MAICD,Independent Non Executive Director

Extensive experience in management and resource industries. Director since October 2007. He joined Rio Tinto Australia (formerly CRA) in 1966 and retired as Managing Director of Rio Tinto Australia in 2001. Non Executive Director of MacMahon Holdings Limited since 2002, Chairman of Oz Minerals Limited and was President of the Minerals Council of Australia from 2001 to 2003 (member since 1996).

66 Member of the Remuneration and Succession Planning and Nomination and Corporate Governance Committees.

F FordM.Tax (Melb), B.Bus(Acc), FCA Independent Non Executive Director

Extensive experience in fi nancial and risk management. Director since January 2008. Former Managing Director of Deloitte Victoria as a professional advisor for 35 years. A past member of the Deloitte Global Board, Deloitte Global Governance and Deloitte National Management Committees. Director of Citigroup Pty Limited and Tarrawarra Museum of Art Limited.

62 Member of the Audit and Financial Risk and Nomination and Corporate Governance Committees.

* Refer to Meetings of Directors as detailed on the following page.

For

per