Embed Size (px)

Citation preview

Ramsay Health Care UBS Australian Healthcare Conference 2012

7 June 2012

Christopher Rex, Managing Director

For

per

sona

l use

onl

y

OVERVIEW, GROWTH STORY &

FORMULA FOR SUCCESS

Ramsay Health Care

2

For

per

sona

l use

onl

y

Australia’s largest private hospital operator & growing global

company

− 117 hospitals & facilities across three continents; circa 10,000 beds

− Over 30,000 staff: 22,000+ in Australia including 13,500 nursing staff, 650

doctors

− 143 accredited specialist medical training positions

− Approaching 3 million patient days per annum

− Extensive education and training, including Ramsay Training Institute,

Graduate Employment Programme and Future Leaders Programme

Market capitalisation approximately $4 billion

Enterprise value approximately $5 billion

3

RAMSAY HEALTH CARE – OVERVIEW F

or p

erso

nal u

se o

nly

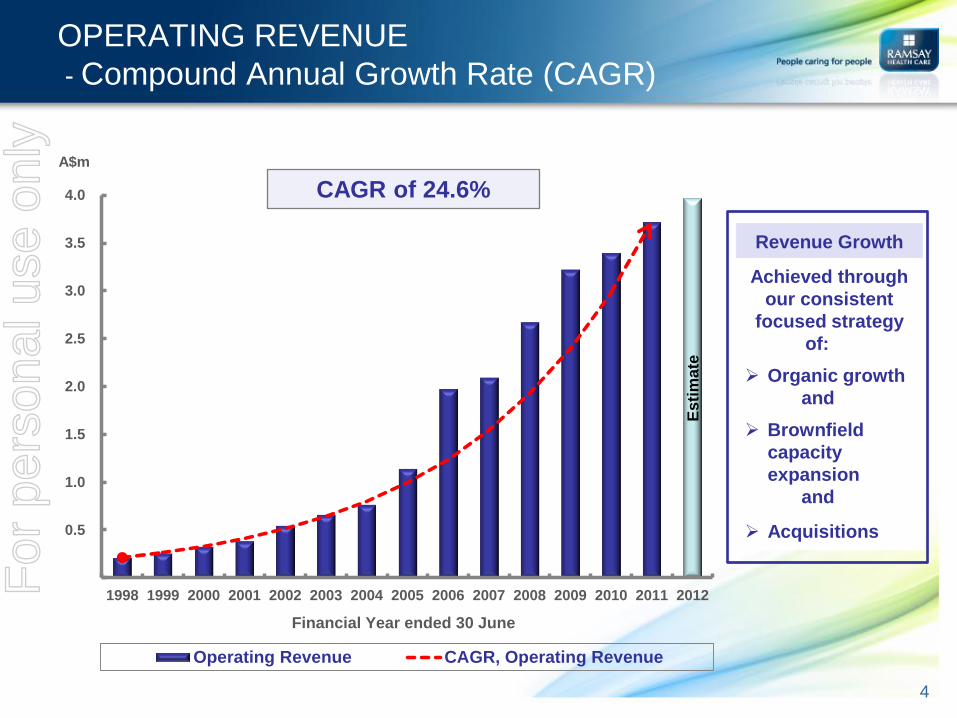

OPERATING REVENUE

- Compound Annual Growth Rate (CAGR)

Es

tim

ate

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Operating Revenue CAGR, Operating Revenue

Financial Year ended 30 June

A$m

CAGR of 24.6%

4

Revenue Growth

Achieved through

our consistent

focused strategy

of:

Organic growth

and

Brownfield

capacity

expansion

and

Acquisitions

For

per

sona

l use

onl

y

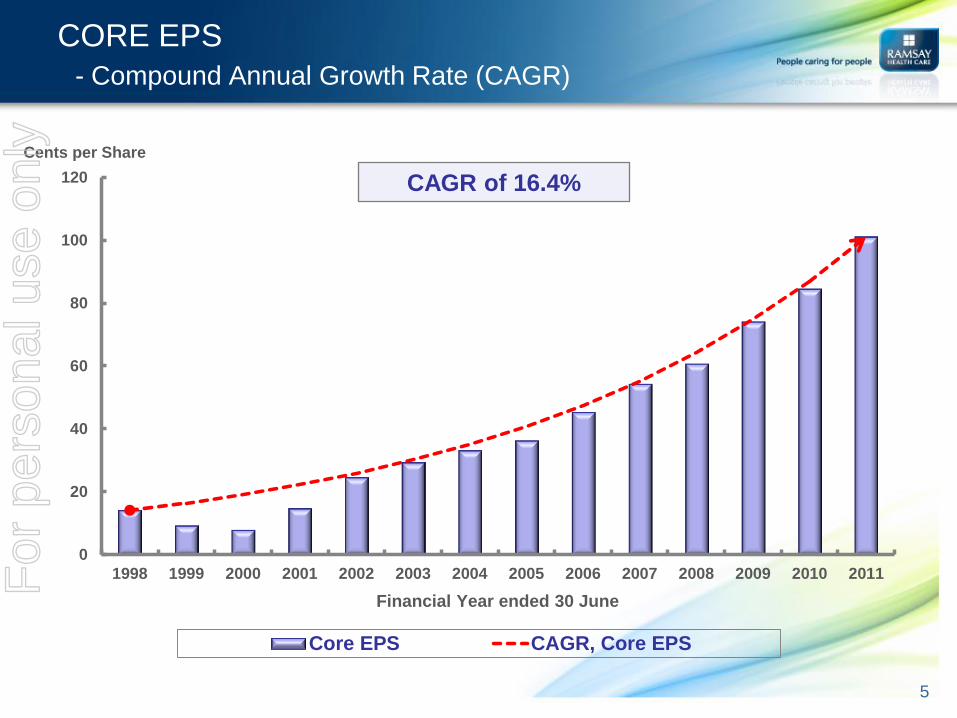

CORE EPS

- Compound Annual Growth Rate (CAGR)

0

20

40

60

80

100

120

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Cents per Share

Core EPS CAGR, Core EPS

Financial Year ended 30 June

5

CAGR of 16.4%

For

per

sona

l use

onl

y

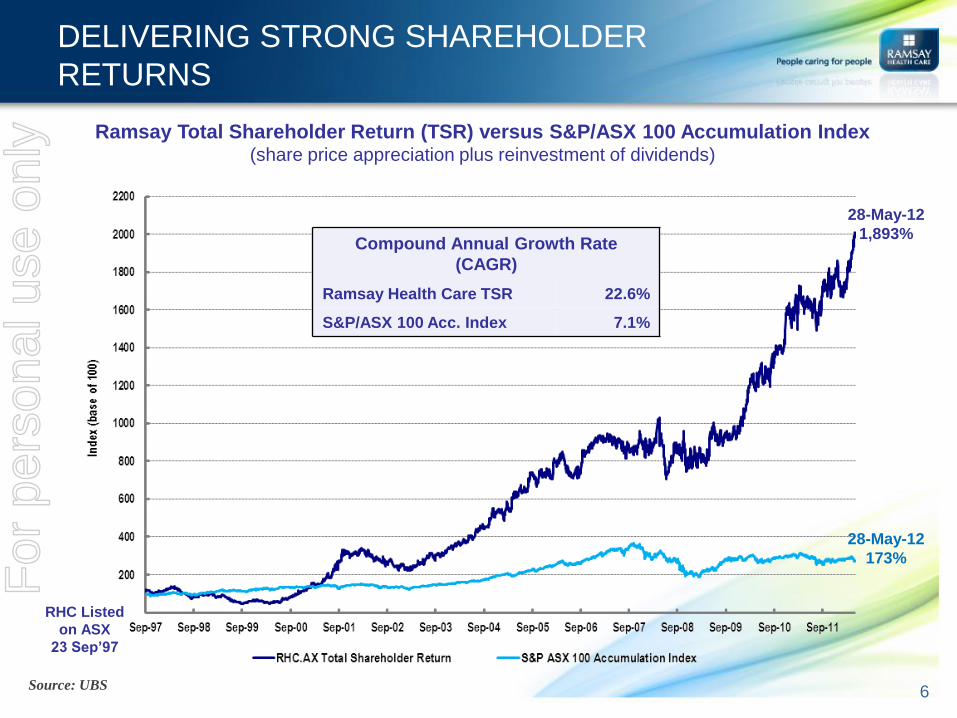

DELIVERING STRONG SHAREHOLDER

RETURNS

Ramsay Total Shareholder Return (TSR) versus S&P/ASX 100 Accumulation Index (share price appreciation plus reinvestment of dividends)

Source: UBS

Compound Annual Growth Rate

(CAGR)

Ramsay Health Care TSR 22.6%

S&P/ASX 100 Acc. Index 7.1%

RHC Listed

on ASX

23 Sep’97

6

28-May-12

173%

28-May-12

1,893%

For

per

sona

l use

onl

y

RAMSAY HEALTH CARE

Share Price 1 July 11 to 18 May 12

7

S&P ASX100 Index 3749 3309 11.7%

15.7% Share Price $20.80

Share Price $17.97

For

per

sona

l use

onl

y

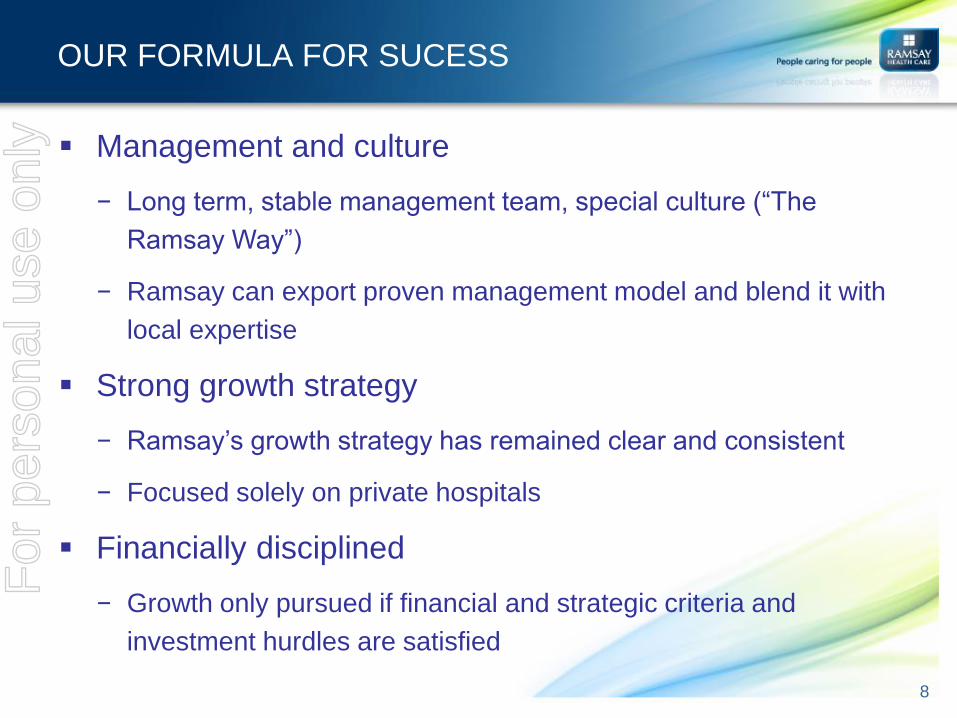

Management and culture

− Long term, stable management team, special culture (“The

Ramsay Way”)

− Ramsay can export proven management model and blend it with

local expertise

Strong growth strategy

− Ramsay’s growth strategy has remained clear and consistent

− Focused solely on private hospitals

Financially disciplined

− Growth only pursued if financial and strategic criteria and

investment hurdles are satisfied

OUR FORMULA FOR SUCESS

8

For

per

sona

l use

onl

y

9

RAMSAY HEALTH CARE IN 2012

Strong growth in our Australian business continues

Operating leverage continues to drive margin growth

Completed brownfield projects adding to EBIT & EPS

PHI membership continues to grow, with approximately

50,000 people joining in the Dec quarter

Means testing of the PHI rebate commences 1 July 2012

Private hospitals integral to healthcare system treating

41% of all patients (3.5m per annum)

State governments increasingly looking to involve the

private sector in service delivery for publicly funded

patients

For

per

sona

l use

onl

y

10

RAMSAY HEALTH CARE IN 2012 (cont)

Construction of new Public/Private hybrid Sunshine Coast

hospital commenced 1 Sept 2011

Continued growth in treating publicly funded patients in

UK - NHS patients now represent 65% our UK

admissions.

Ramsay Santé (France) is performing to expectations

under tough economic conditions

In 2012, Ramsay Health Care was selected in the “Global

100 Most Sustainable Companies in the world”. (One of

only 6 Australian companies)

For

per

sona

l use

onl

y

GLOBAL MARKET TRENDS IN

HEALTHCARE

Industry Fundamentals

11

For

per

sona

l use

onl

y

Demand for healthcare driven by:

Ageing population (first of boomers

turned 65 in 2010)

Increasing chronic disease burden:

− Coronary artery disease & heart failure

− Diabetes

− Obstructive pulmonary disease

Higher patient expectations

Increased capabilities

Longer life expectancy

AIHW Report 2010/2011 confirms the

trend

STRONG GLOBAL INDUSTRY

FUNDAMENTALS

12

For

per

sona

l use

onl

y

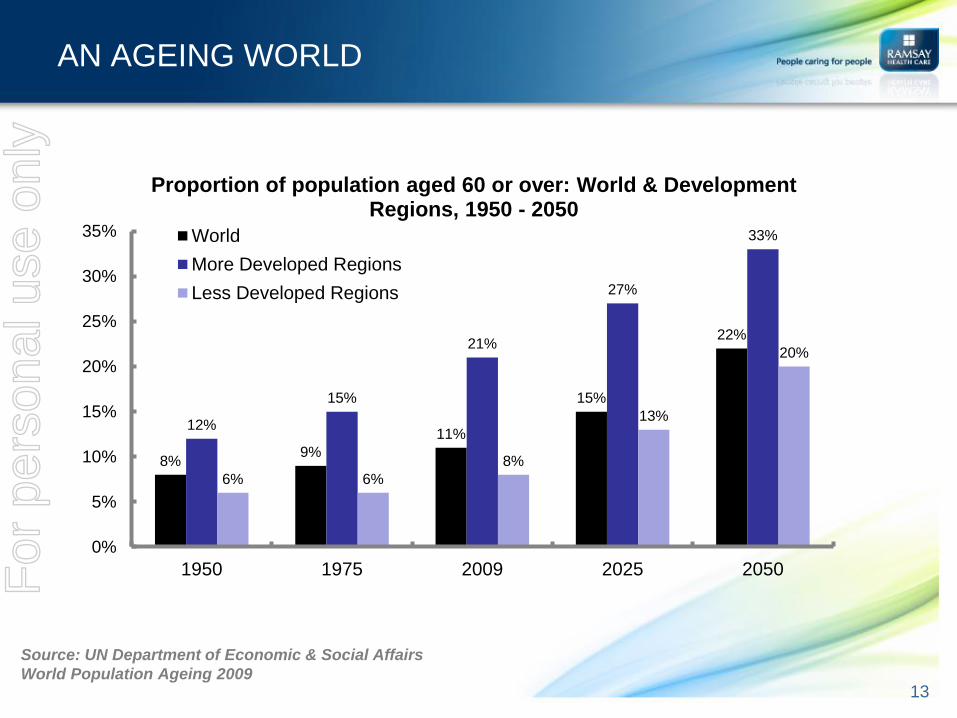

AN AGEING WORLD

8% 9%

11%

15%

22%

12%

15%

21%

27%

33%

6% 6%

8%

13%

20%

0%

5%

10%

15%

20%

25%

30%

35%

1950 1975 2009 2025 2050

Proportion of population aged 60 or over: World & Development Regions, 1950 - 2050

World

More Developed Regions

Less Developed Regions

Source: UN Department of Economic & Social Affairs

World Population Ageing 2009 13

For

per

sona

l use

onl

y

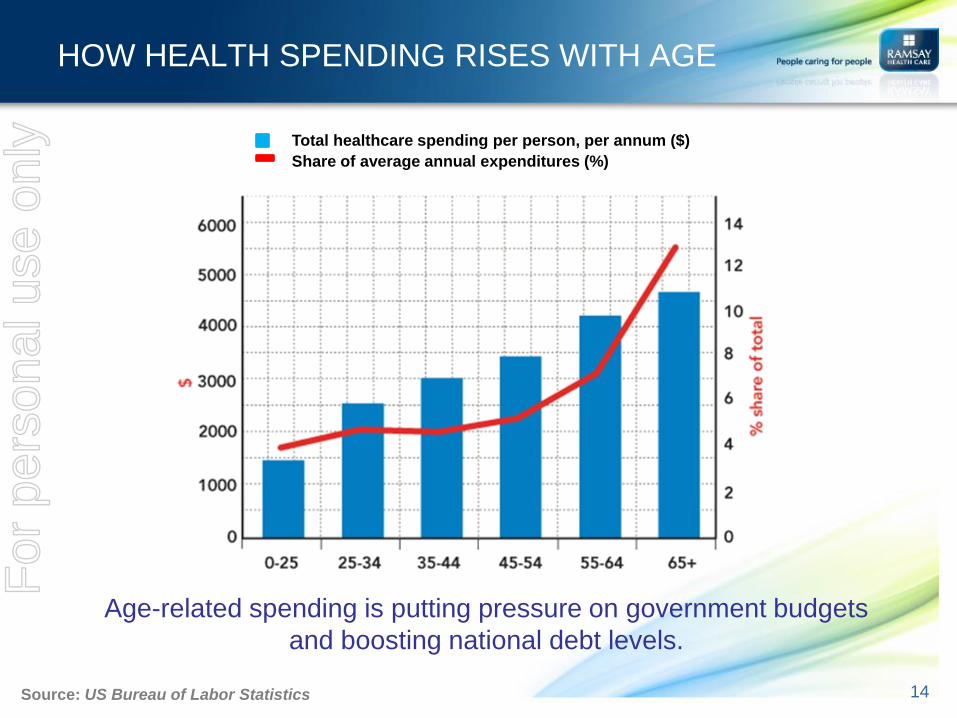

HOW HEALTH SPENDING RISES WITH AGE

Age-related spending is putting pressure on government budgets

and boosting national debt levels.

Source: US Bureau of Labor Statistics 14

Total healthcare spending per person, per annum ($)

Share of average annual expenditures (%)

For

per

sona

l use

onl

y

MARKET TRENDS IN HEALTHCARE

Growing & ageing population will continue to drive

demand for healthcare

Governments increasingly concerned about the rising

costs of healthcare, looking to private sector for solutions

Patients looking for & willing to pay for higher quality

healthcare

Increasing GDP and reducing public services, driving

growth for private operators

Significant growth in healthcare spend expected in

emerging markets

15

For

per

sona

l use

onl

y

THE FUTURE

Ramsay Health Care

16

For

per

sona

l use

onl

y

SUCCESSFUL & SUSTAINABLE GROWTH

STRATEGY

Organic

• Underpinned by demographics, quality portfolio of hospitals, ongoing business improvement

Brownfields

• Unmet demand driving Ramsay’s ongoing investment in capacity expansion

Public/Private Collaborations

• Potential for more partnerships to develop/manage/ provide hospital services in changing political landscape

Acquisitions

• Exploring further acquisitions in existing and other markets

• Ramsay has proved it can export its management model

• Must add long-term value to shareholders

17

For

per

sona

l use

onl

y

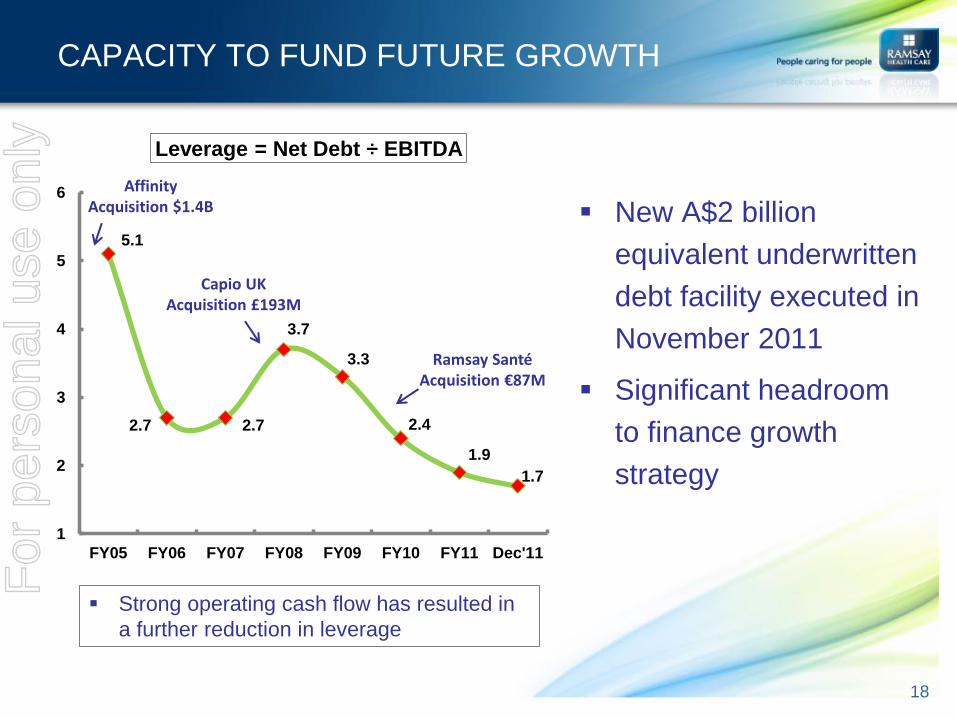

CAPACITY TO FUND FUTURE GROWTH

5.1

2.7 2.7

3.7

3.3

2.4

1.9

1.7

1

2

3

4

5

6

FY05 FY06 FY07 FY08 FY09 FY10 FY11 Dec'11

Leverage = Net Debt ÷ EBITDA

Affinity Acquisition $1.4B

Capio UK Acquisition £193M

Ramsay Santé Acquisition €87M

18

Strong operating cash flow has resulted in

a further reduction in leverage

New A$2 billion

equivalent underwritten

debt facility executed in

November 2011

Significant headroom

to finance growth

strategy

For

per

sona

l use

onl

y

BROWNFIELD DEVELOPMENTS AUSTRALIA

Proven track record of undertaking successful

brownfield expansion

Extensive program of hospital redevelopments &

expansions currently underway (>$800 million

approved since 2007)

Expect ongoing investment of approx. $100 million pa

Completed brownfield developments adding to

earnings at the EBIT & EPS level & on track to achieve

15% ROI

19

For

per

sona

l use

onl

y

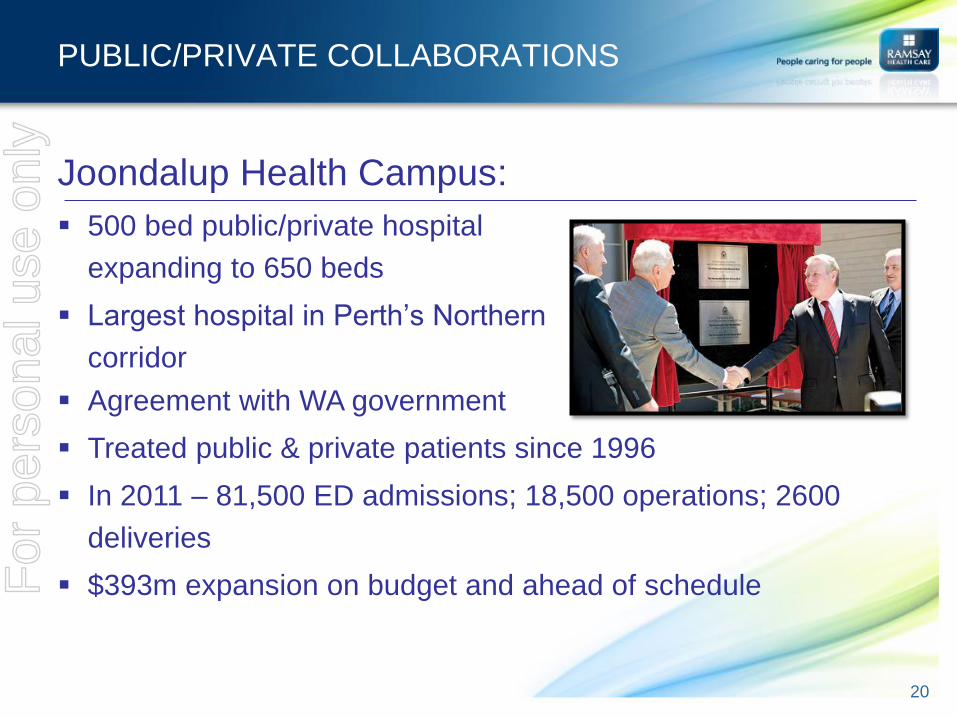

PUBLIC/PRIVATE COLLABORATIONS

Joondalup Health Campus:

500 bed public/private hospital

expanding to 650 beds

Largest hospital in Perth’s Northern

corridor

Agreement with WA government

Treated public & private patients since 1996

In 2011 – 81,500 ED admissions; 18,500 operations; 2600

deliveries

$393m expansion on budget and ahead of schedule

20

For

per

sona

l use

onl

y

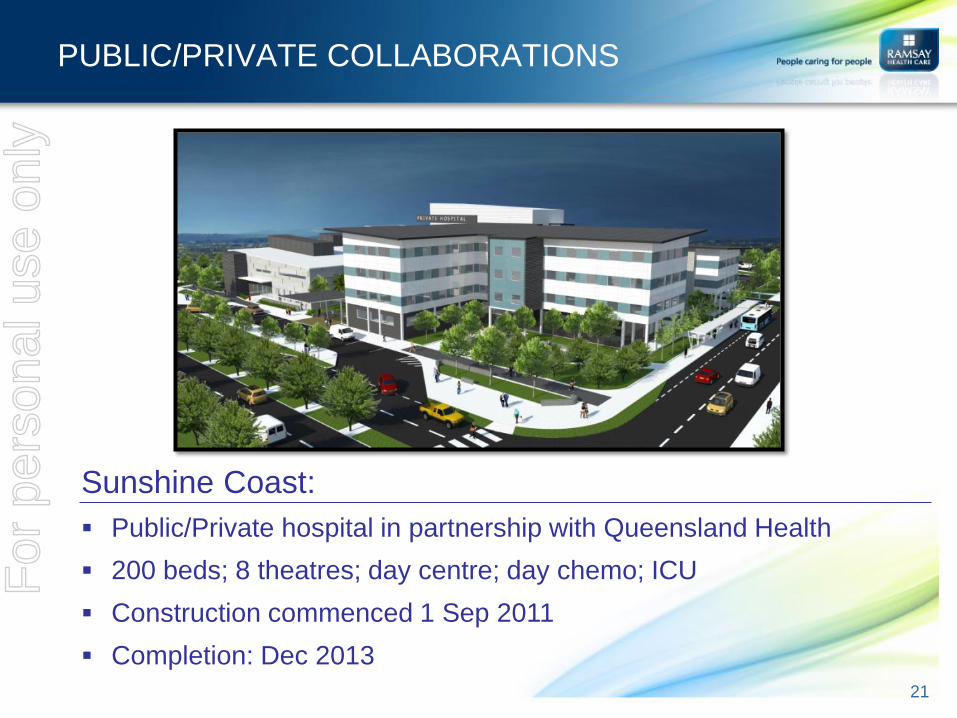

Sunshine Coast:

Public/Private hospital in partnership with Queensland Health

200 beds; 8 theatres; day centre; day chemo; ICU

Construction commenced 1 Sep 2011

Completion: Dec 2013

PUBLIC/PRIVATE COLLABORATIONS

21

For

per

sona

l use

onl

y

OUTLOOK

Rising demand for health care driving substantial

ongoing investment in brownfield projects

Completed brownfield projects adding to earnings at

EBIT and EPS level

Economic conditions in the UK and France remain

challenging but health care sector remains stable with

growth opportunities

Continuing to explore bolt-on acquisitions in the UK and

France

22

For

per

sona

l use

onl

y

QUESTIONS

For

per

sona

l use

onl

y