Embed Size (px)

Citation preview

Daconient of

The World Bank

FOR OMCIAL USE ONLY

Report Me. 4932-GE

STAFF APPRAISAL REPORT

GHANA

POWER SYSTEM REHABILITATION PROJECT

August 26, 1985

Western Arica Projects DepartmentEnergy Division

II& documt ha a aldud asugutm ad my be wed by re_ipet only in The peufru.mce oftbir o l doom. lb cmmtb y ino odmermwie be dbdhsed widhou WVod DBnk auihrize.bL l

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

- CURRENCY EQUIVALENTS

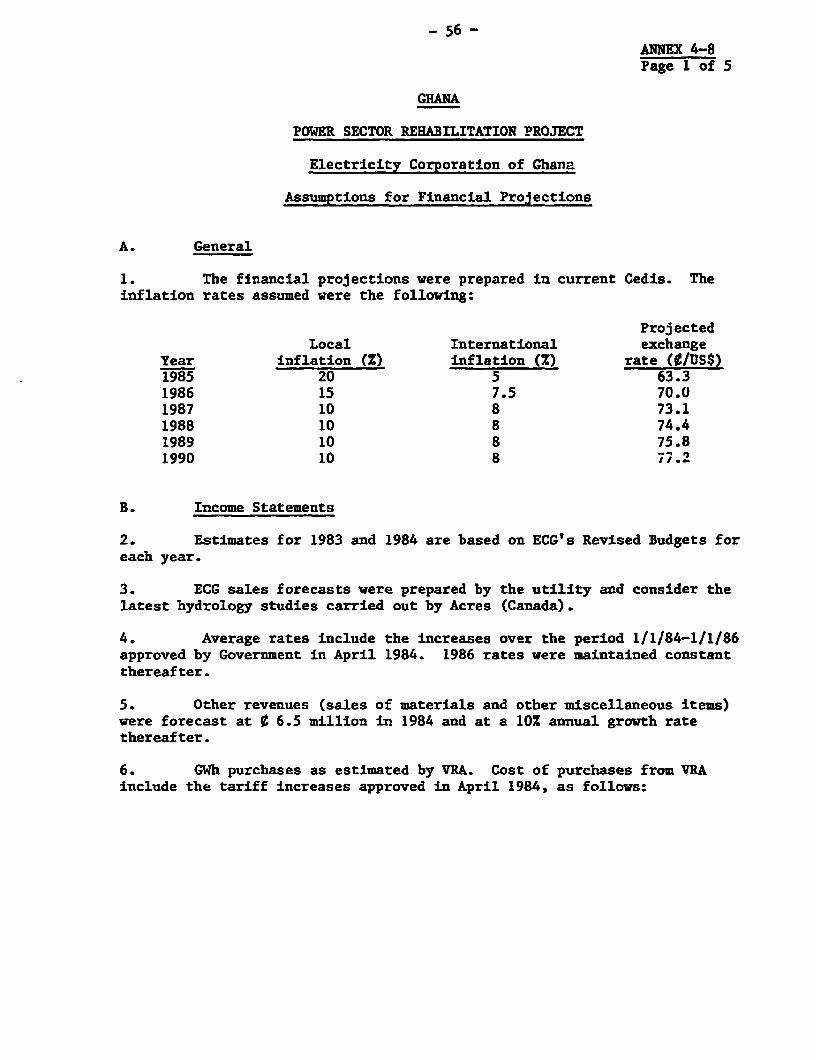

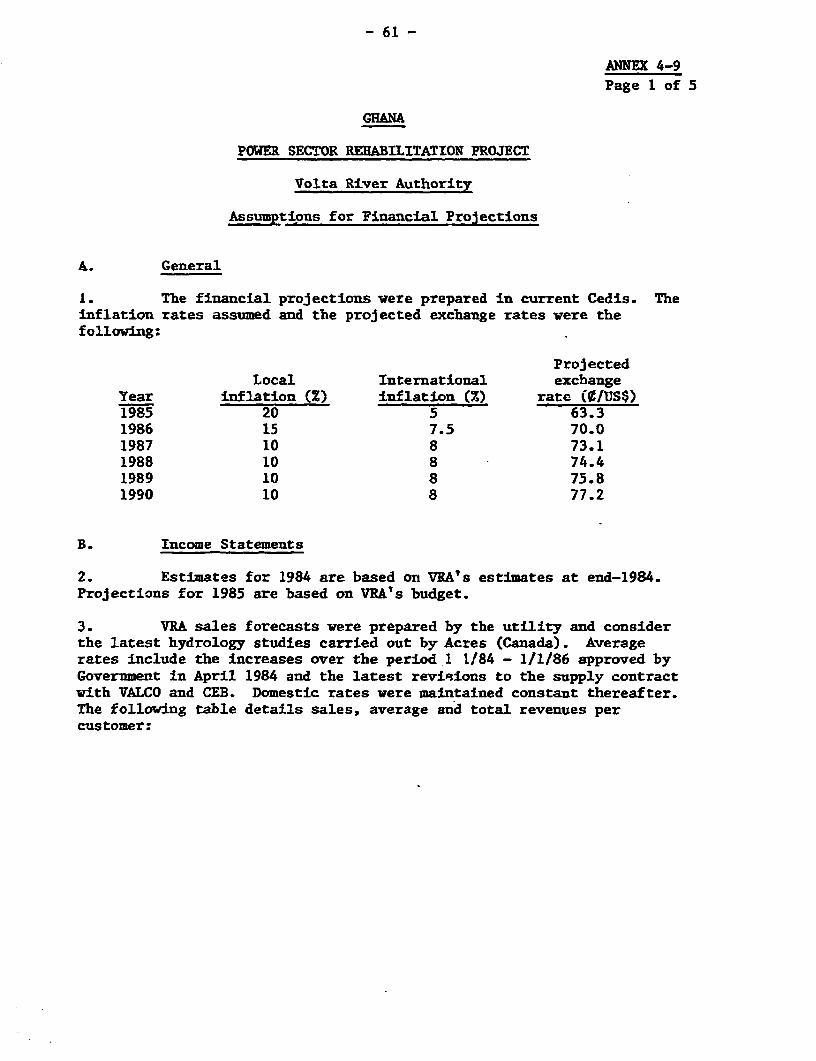

Currency Unit Cedis (¢)US$1 57.0 Cedis1 Cedi = US$0.018US$1 - SDR 1.037

ABBREVIATIONS AND ACRONYNS

CEB = Communaute Electrique du BeninECG = Electricity Corporation of GhanaEECI = Energie Electrique de la Cote d'IvoireESB = Electricity Supply Board of IrelandPPF = Project Preparation Facility of the World Bank Group-VALCO = Volta Aluminum CompanyVRA = Volta River AuthorityMFP = Ministry of Fuel and PowerNEB = National Energy BoardUNDP = United Nations Development ProgramPNDC = Provisional National Defence Council

MEASURES AND EQUIVALENTS

One kilovolt (kV) = 1,000 voltsOne megawatt (MW) = 1,000 kilowatts (kW)One gigawatt hour (GWh) = 1 million kilowatt hours (kWh)One barrel (bbl) = 0.16 cubic metersOne tone of oil equivalent (toe) = about 7 bbl of crude oil

FISCAL YEAR

January 1 - December 31

FOR OFFICUIL USE ONLY

GHANA

STAFF APPRAISAL REPORT

POWER SYSTEM REHABILITATION PROJECT

TABLE OF CONTENTS

Page No.

I. THE ENERGY SECTOR.......... 1

A. Energy Resources and Uses................. ...... ........ . 1B. Sector Institutions....................................... 1C. The Renewable Energy Sector.. 2............. 2D. The Petroleum Sector... ....................................* *. ; 2E. Investment Requirements ........ . ......... ............... .. 3F. Organization of the Pover Sub-sector ............ 4Go Power Facilities .... o ...... ....... . 5H. Access to Service, Electricity Consumption and Exports.... 6I. Power Developmrent and Planning .................... o..... 7

II. THE BORROWER AND EXECUTING AGENCIES .................. ........ o. 8

A. Electricity Corporation of Ghana (ECG) ............... o. 91. Organization and Managee...... 92. Manpower...... 93. Training.r. .... . . .. . . o. .. 10

4. Accounting and Audit .... 105. Insurance.............. 10

B. Volta River Authority (RA) . .10

1. Organization and Management. 102. Manpower and Traininga.. . .n..- 113. Accounting and Audit. . 114. Insurance ... ; 11

C. History of Bank Group Involvement with the Power Sector... 11D. Bank Group Objectives, Strategy and Rationale for

Invovmet...... ...... m .... 6400 t00 12

III. THE PROJECT ..... 12

A. Project Cost .......................... ...... 14B. Project Financing ......... . 16C. Procurement .................................... ....... 16D. Status of Project ............................................... . .. 18E. Project Implementation .................... . 18F. Disbursements ........................................... 18G. Environment ....................................... 19

This report was prepared by Messrs. C. F. Mena and S. Contreras based onthe findings of an IDA appraisal mission consisting of Messrs. J. Sneddon, C. F. Mena,and B. Dahlborg who visited Ghana in May, 1983, and a subsequent mission by Messrs.Mena and Contreras in November 1984. Secretarial assistance for this report vasprovided by Miss Mary Jackson.

Thi document ha a rusutcedidstibution and may be mnd by recipien only in tm perform"eor their oIlci.l ftduti Its countents amy sou ouduwbei be dhsckod withot World kink authiorinm.

IV. FINANCIAL ANALYSIS............................... 19

A. Past Finances .. .................................... . 191. Background .................... * ... 19

2. Past Earnings > ......... 20

3. Financing Performance. . .. ......... .. 21

4. Capitalization .... . . ... ......... 23

B. Billing and Collectionl l e c t i on.. ...... ....... 24

C. Tariffss... .... ... . ......... 24

1. Present Arrangementsrangemens.. .......... 24

2. Future Tariffs ....................s........ 25D. Financing Plan .................................................... 25E. Future Finances ......... 27

V. PROJECT JUSTIFICATION ....... * .............. . 29

A. Background ............................................. . . . 29

B. Least-Cost Solution .............. ......... 29C. Return on Inveetment . . . . .................................. 29

D. Project Risks..... ...................................... 30

VI. AGREEMENTS REACHED AND RECONMENDATIONS .......................... 30

List of Annexes

l-1 Existing Power Facilities .......... . 321-2 Electricity Consumption and Exports 1970-1983 ........... 33

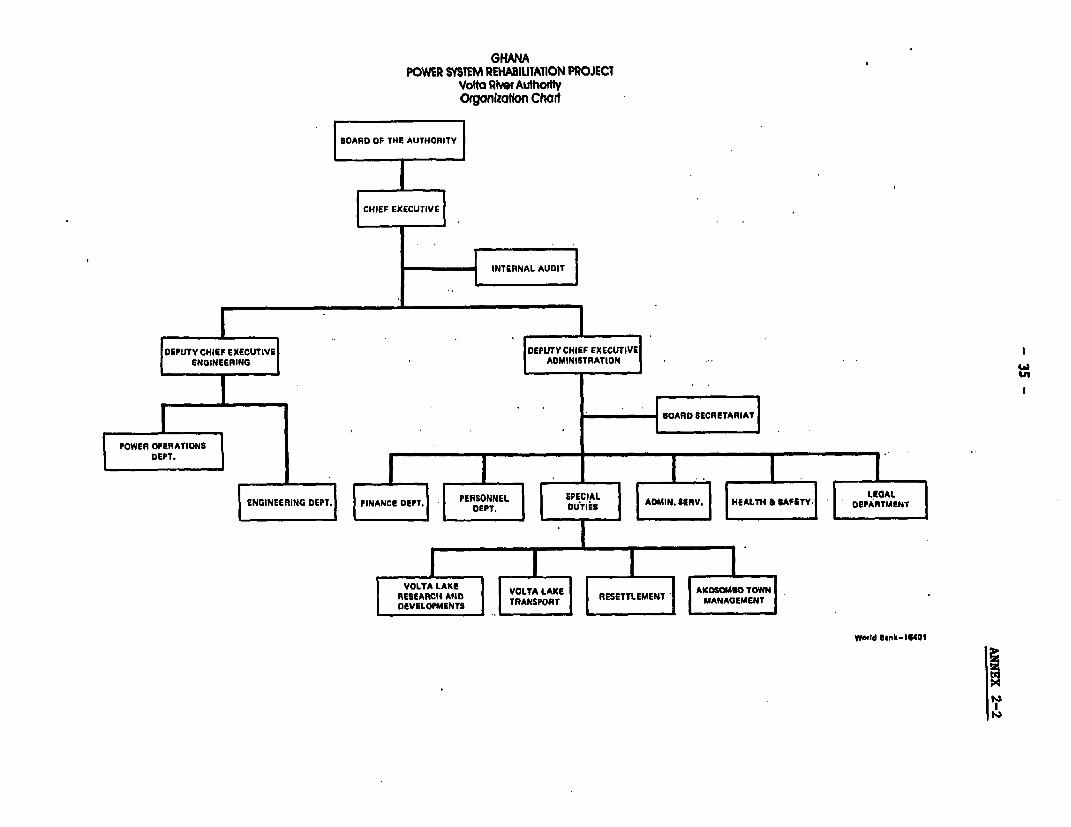

2-1 ECG - Organization Chart .............................. o.. 342-2 VRA - Organization Chart ............ o .................... 35

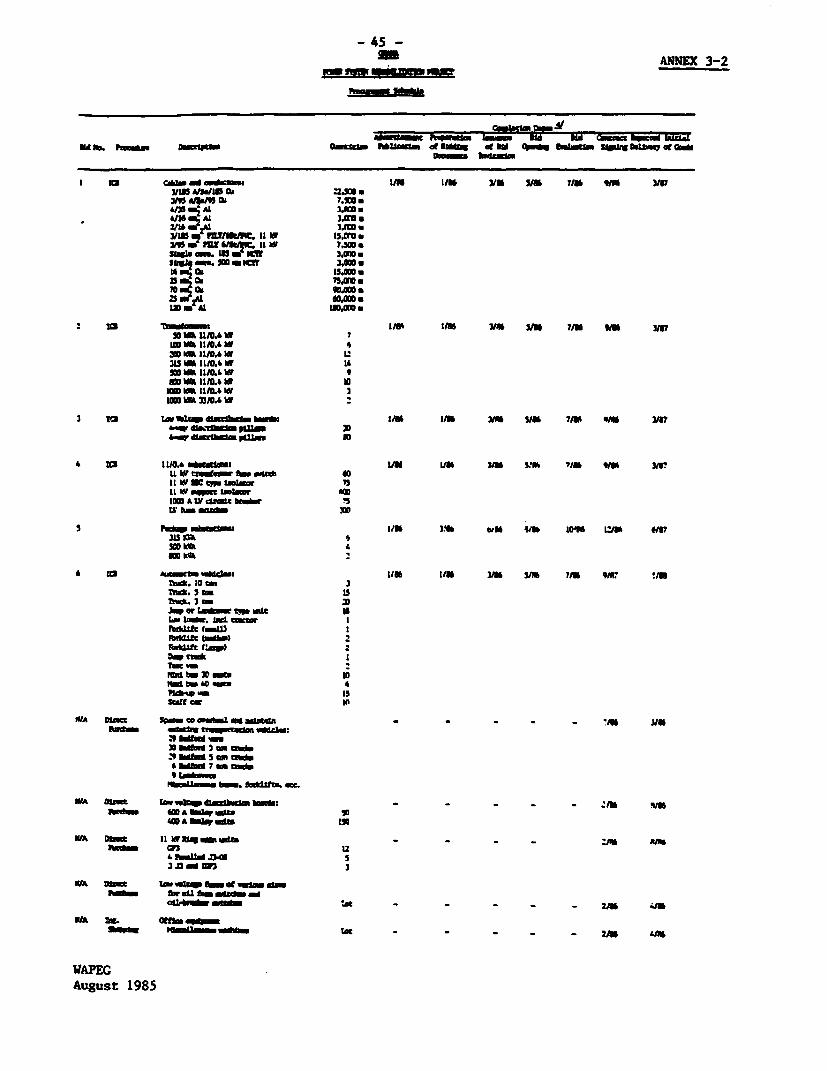

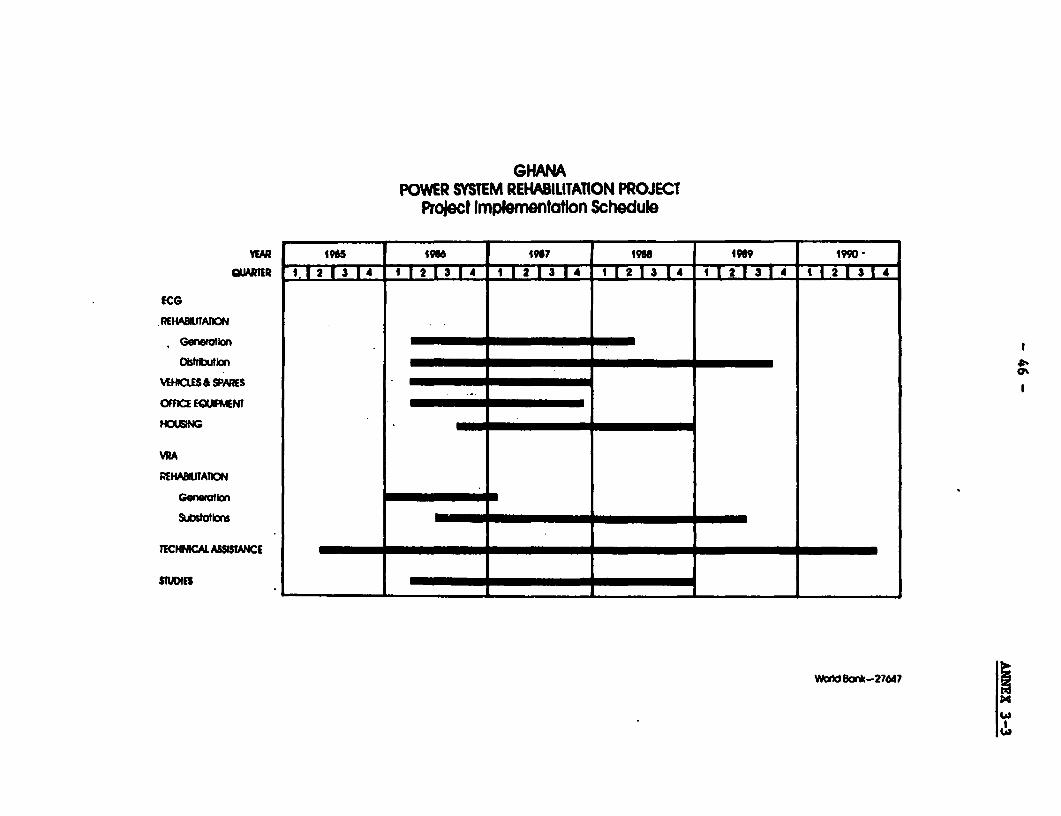

3-1 Equipment and Materials for ECG's and VRA's Systems ...... 363-2 Procurement Schedule . . .. .. .. 453-3 Project Implementation Schedule ......................... . 463-4 Estimated Credit Disbursements . . . . 47

4-1 ECG Actual, Estimated and Projected Income Statements,1981-1990 ....................................... o ....... 48

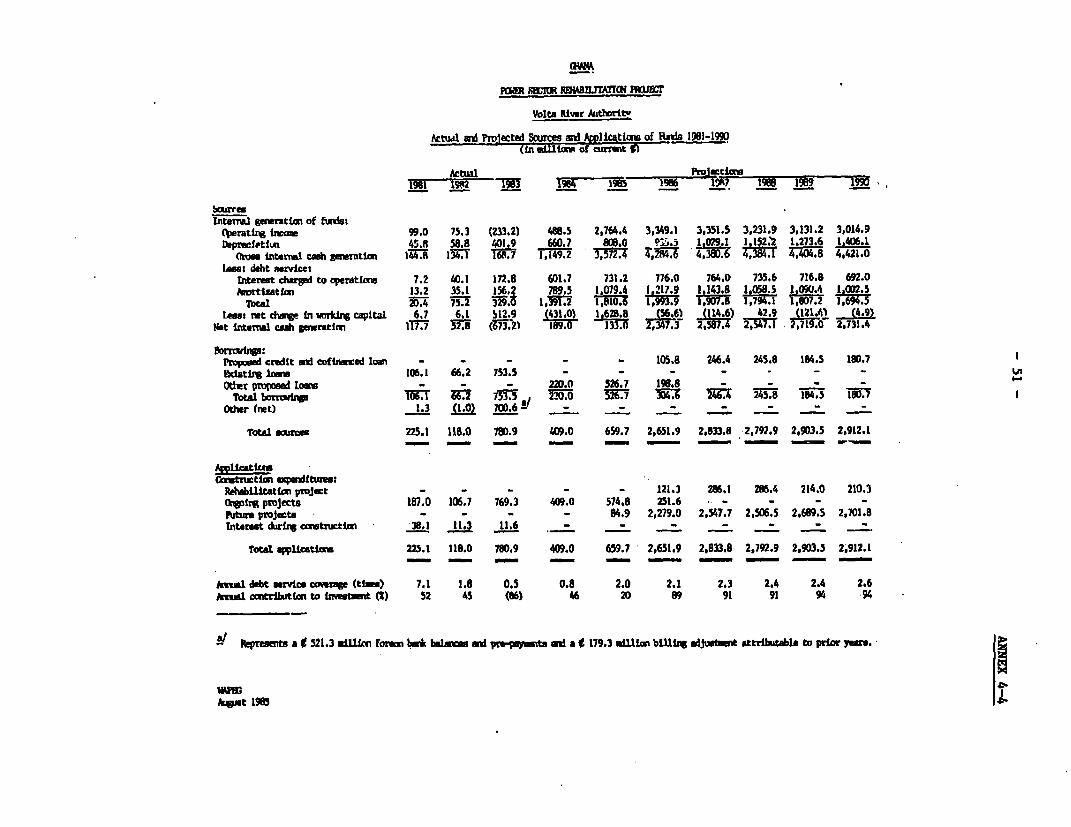

4-2 VRA Actual and Projected Income Statements, 1981-1990 .... 494-3 ECG Actual, Estimated and Projected Sources and

Applications of Funds, 1981-1990 .................... 504-4 VRA Actual and Projected Sources and Applications of

Funds, 1981-1990 ...... .... .000.... .............................. 51

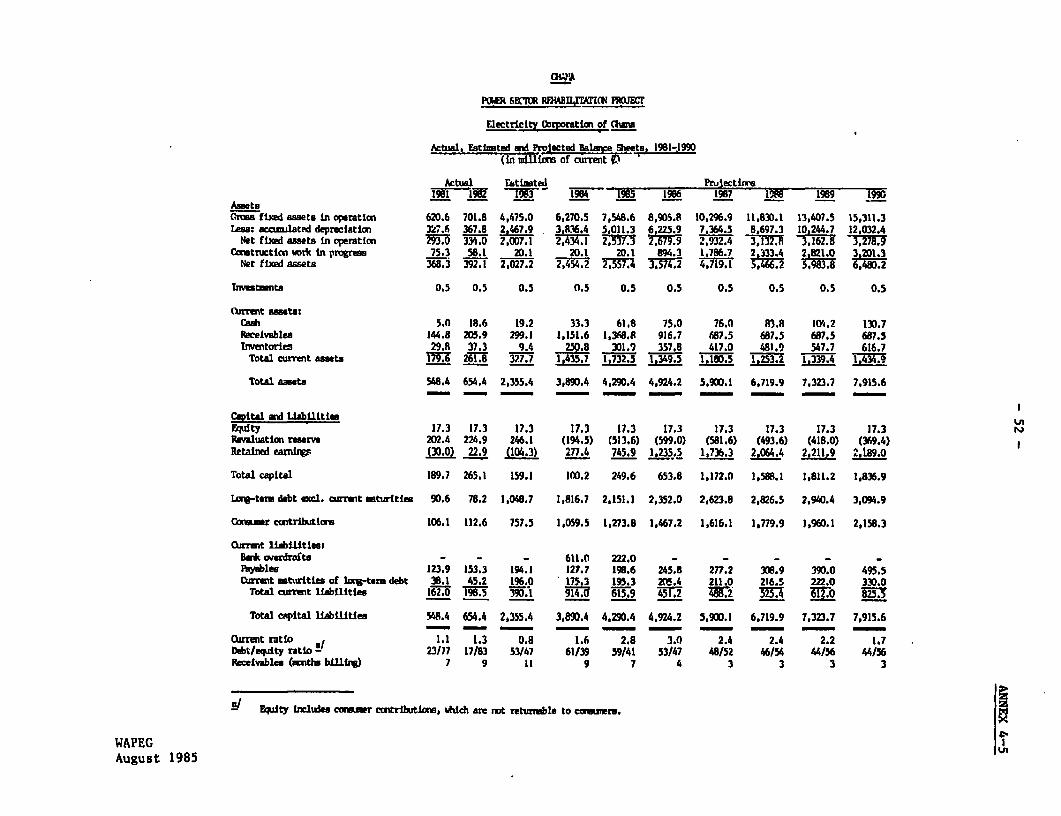

4-5 ECG Actual, Estimated and Projected Balance Sheets,1981-1990 ............................ o.................. 52

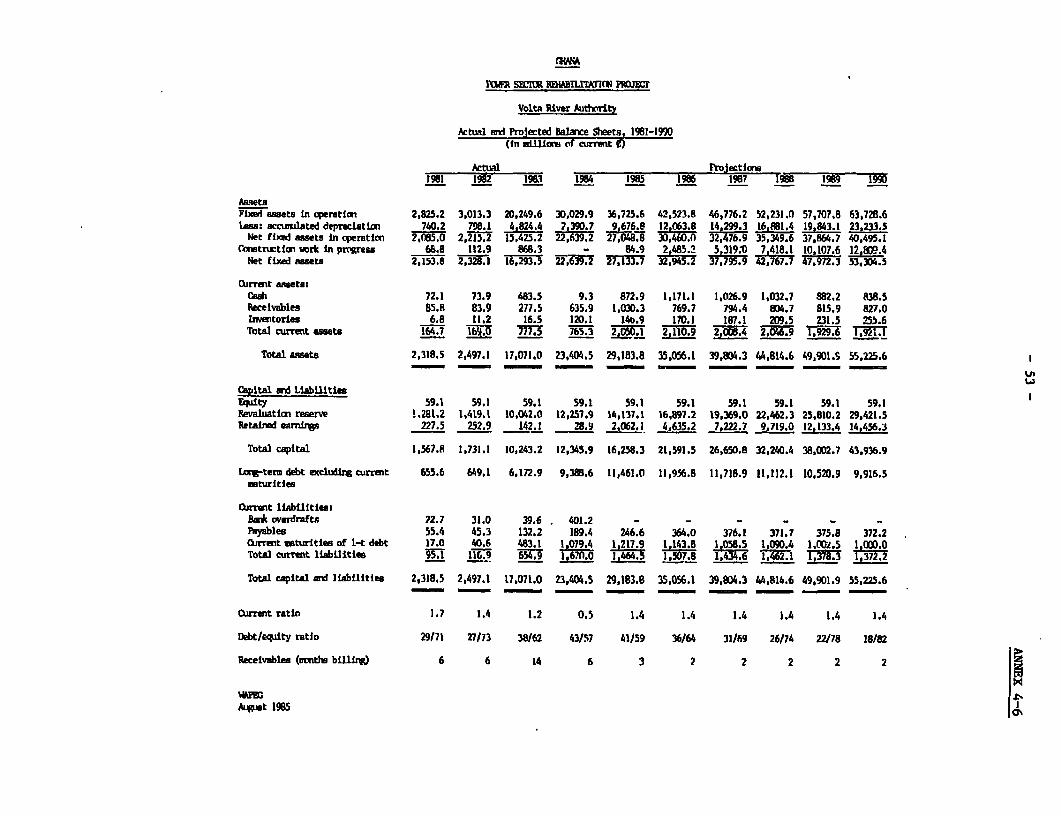

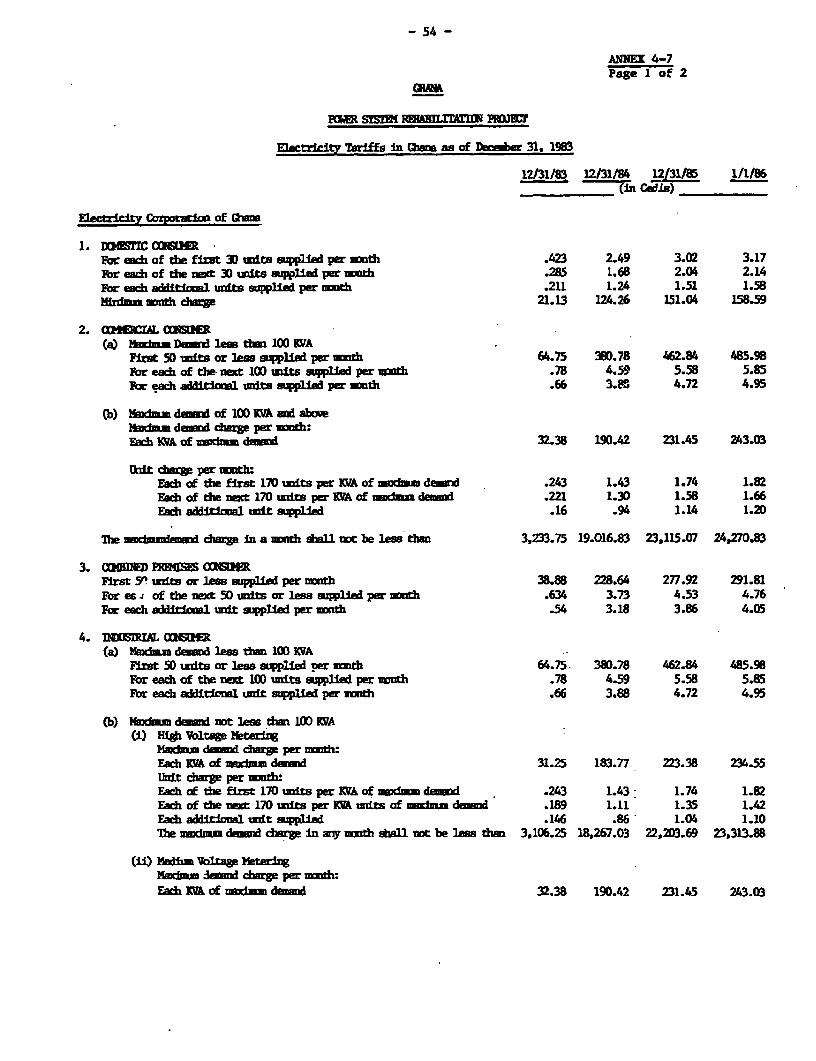

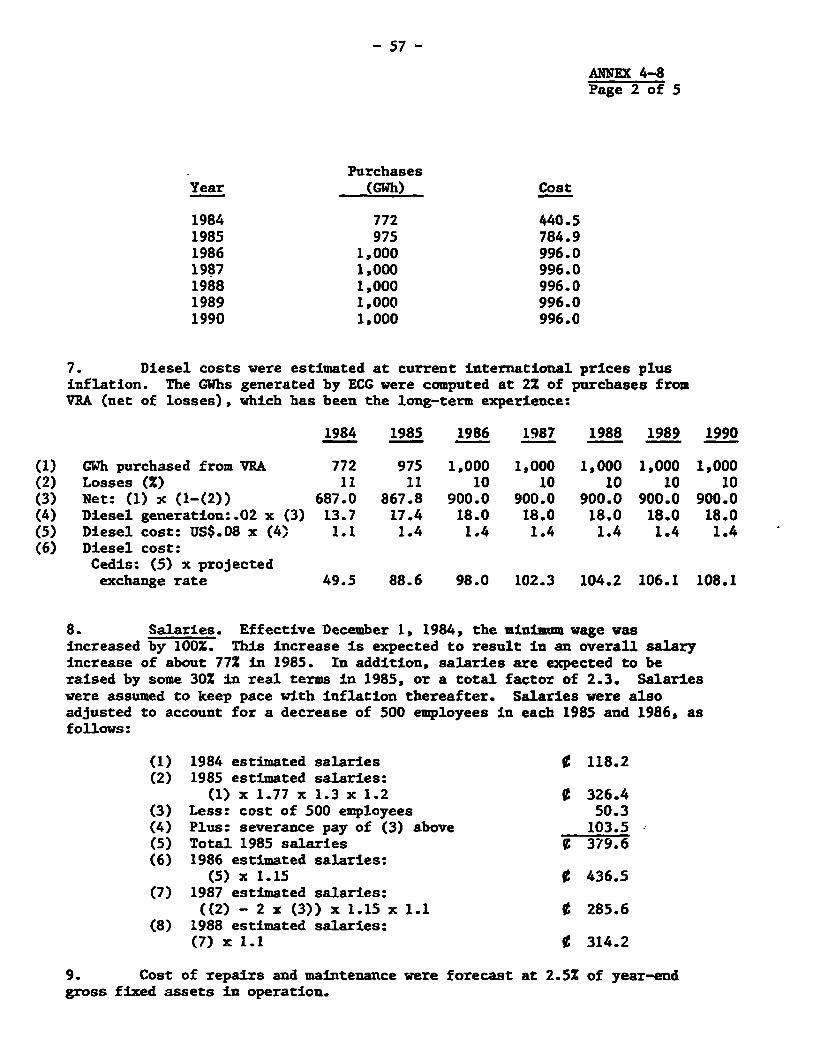

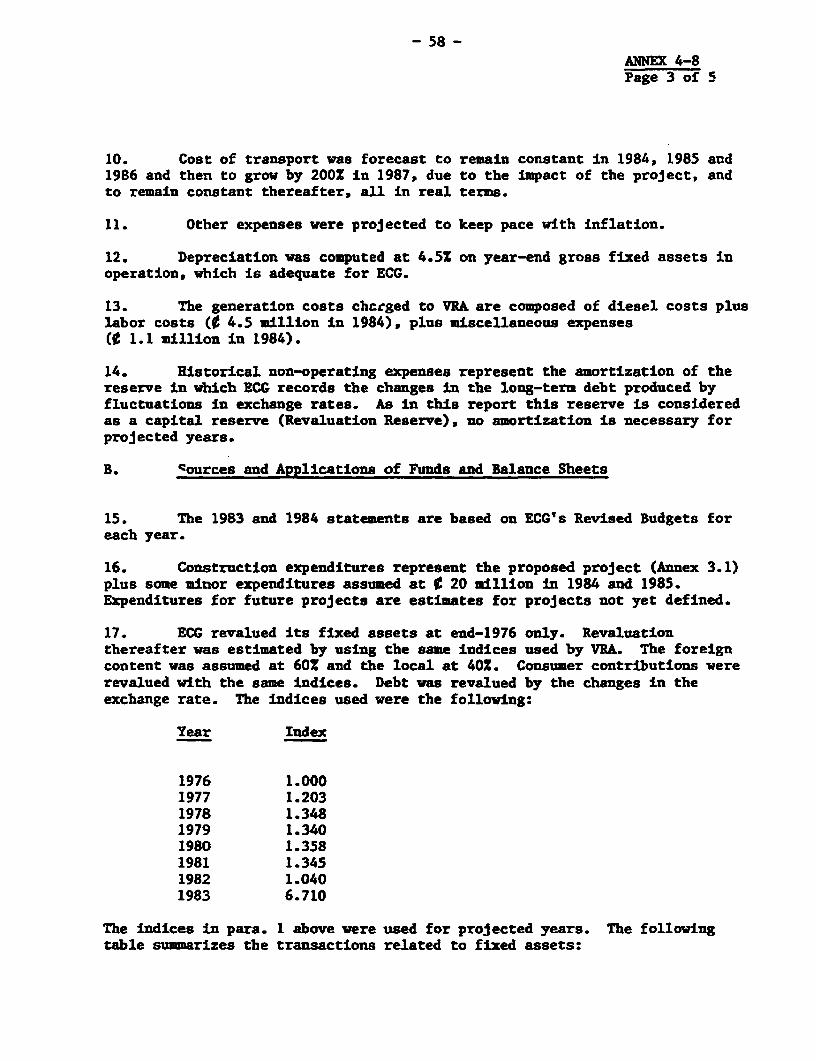

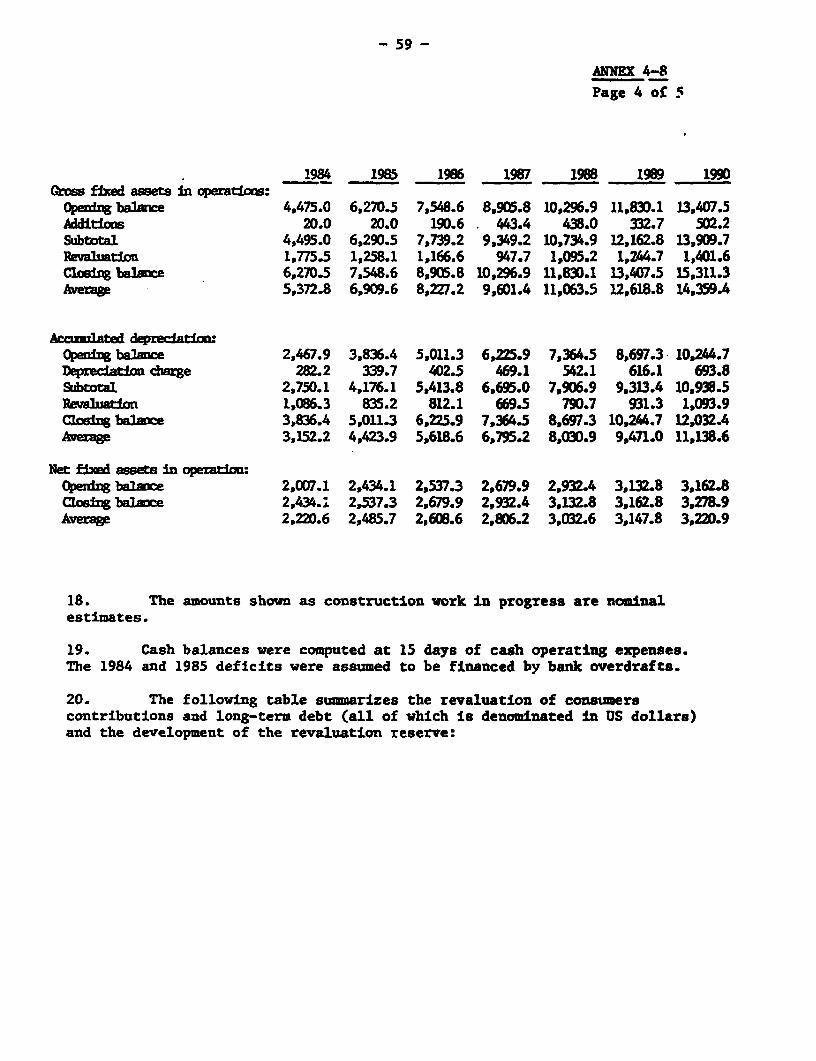

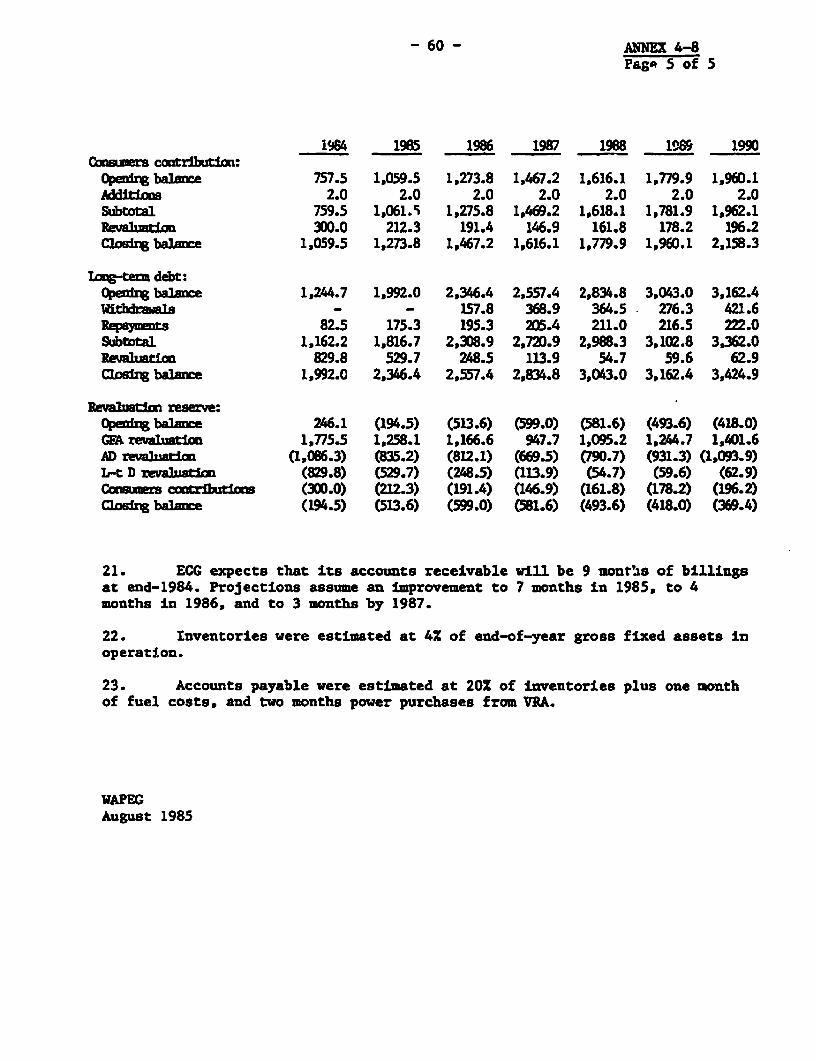

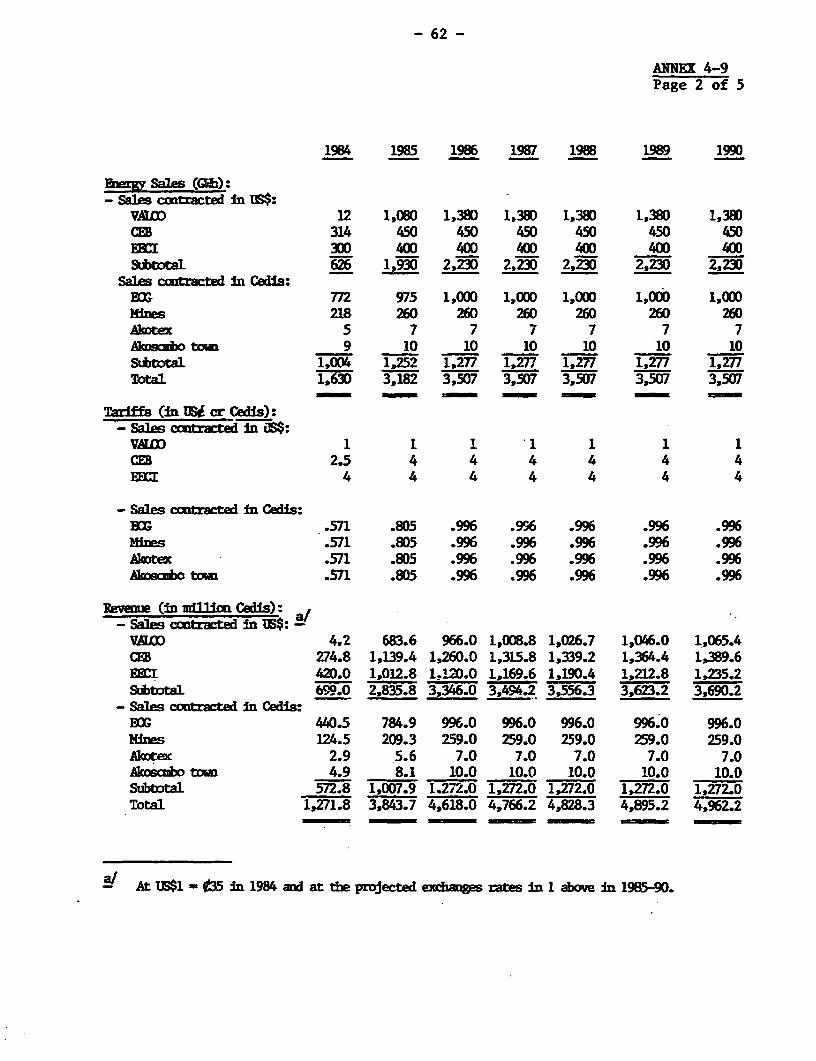

4-6 VRA Actual and Projected Balance Sheets, 1981-1990 ... 534-7 Electricity Tariffs in Ghana as of December 31, 1983 ... 544-8 ECG Assumptions for Financial Projections . . 564-9 VRA Assumptions for Financial Projections. . 61

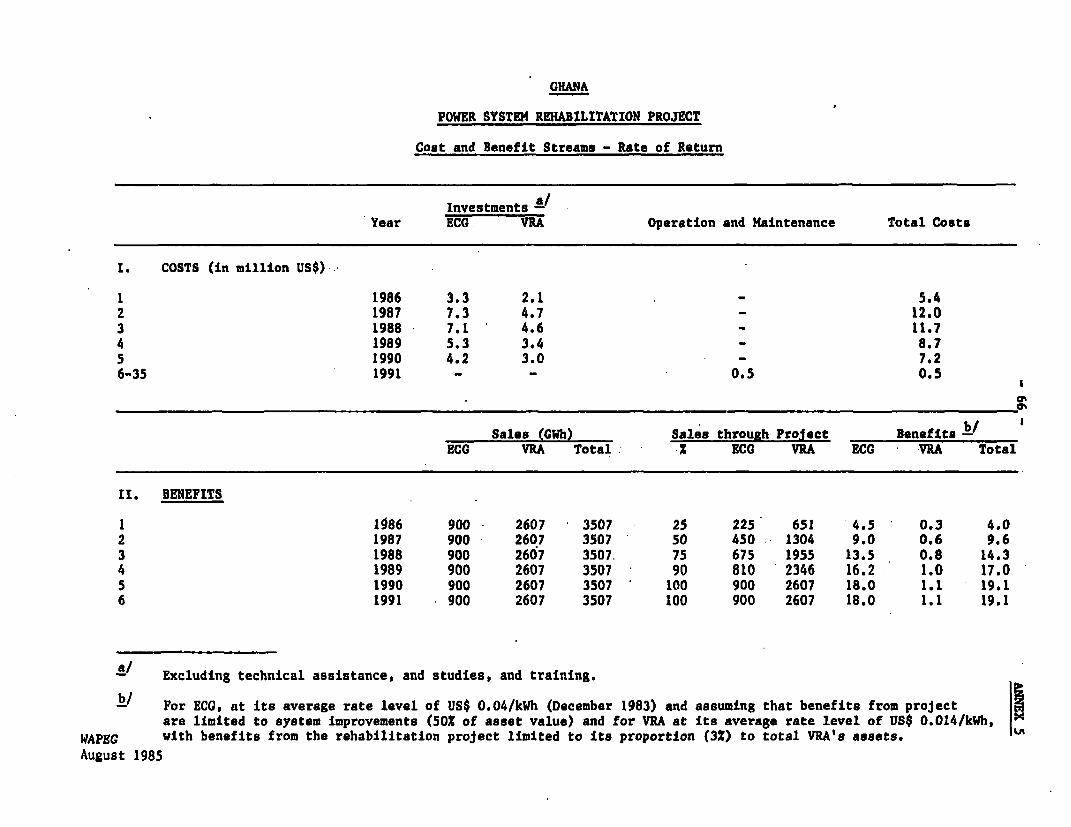

5 Cost and Benefit Streams - Rate of Return .66

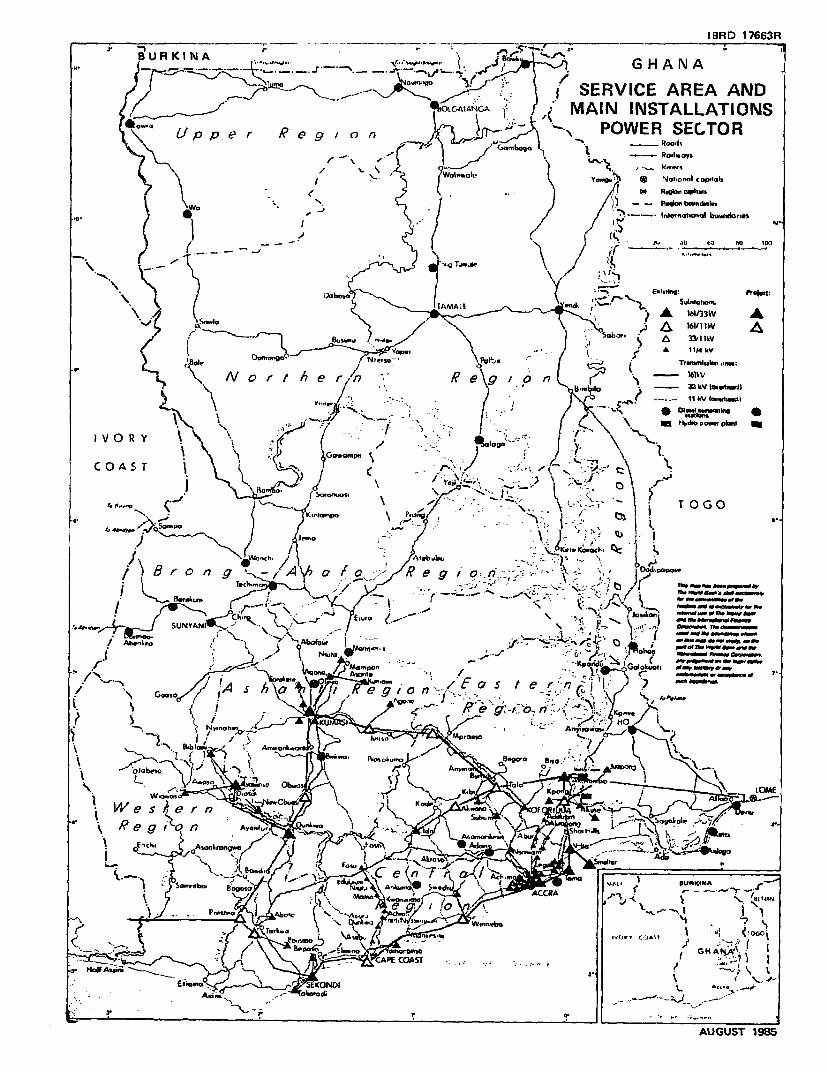

MAP Ghana: Service Area and Main Installations(IBRD Map No. 17663R)

(iM

GHANA

POWER SYSTEM RE9ABILITATION PROJECT

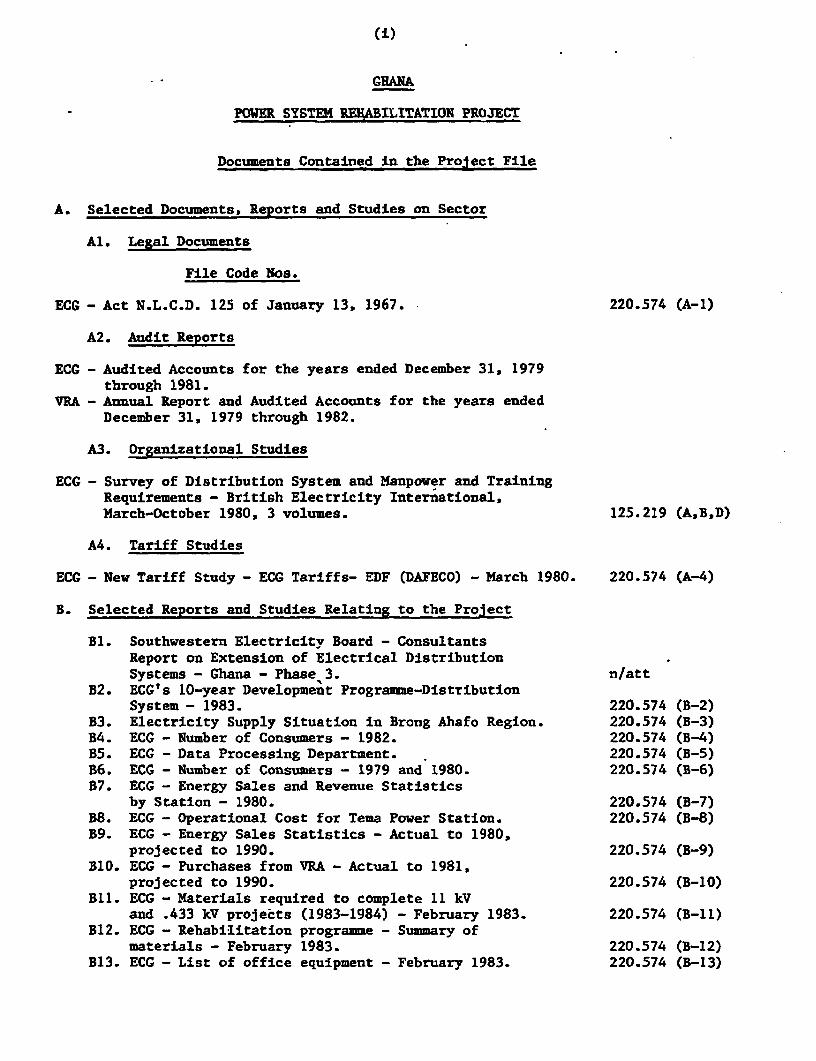

Documents Contained in the Project File

A. Selected Documents, Reports and Studies on Sector

Al. Legal Documents

File Code Nos.

ECG - Act N.L.C.D. 125 of January 13, 1967. 220.574 (A-1)

A2. Audit Reports

ECG - Audited Accounts for the years ended December 31, 1979through 1981.

VRA - Annual Report and Audited Accounts for the years endedDecember 31, 1979 through 1982.

A3. Organizational Studies

ECG - Survey of Distribution System and Manpower and TrainingRequirements - British Electricity International,March-October 1980. 3 volumes. 125.219 (A,B,D)

A4. Tariff Studies

ECG - New Tariff Study - ECG Tariffs- EDF (DAFECO) - March 1980. 220.574 (A-4)

B. Selected Reports and Studies Relating to the Project

E1. Southwestern Electricity Board - ConsultantsReport on Extension of Electrical DistributionSystems - Ghana - Phase 3. n/att

B2. ECG's 10-year Development Programme-DistributionSystem - 1983. 220.574 (B-2)

B3. Electricity Supply Situation in Brong Ahafo Region. 220.574 (B-3)B4. ECG - Number of Consumers - 1982. 220.574 (B-4)B5. ECG - Data Processing Department. 220.574 (B-5)B6. ECG - Number of Consumers - 1979 and 1980. 220.574 (B-6)B7. ECG - Energy Sales and Revenue Statistics

by Station - 1980. 220.574 (B-7)B8. ECG - Operational Cost for Tema Power Station. 220.574 (B-8)B9. ECG - Energy Sales Statistics - Actual to 1980,

projected to 1990. 220.574 (B-9)B10. ECG - Purchases from VRA - Actual to 1981,

projected to 1990. 220.574 (B-10)B11. ECG - Materials required to complete 11 kV

and .433 kV projects (1983-1984) - February 1983. 220.574 (B-11)B12. ECG - Rehabilitation programme - Summary of

materials - February 1983. 220.574 (B-12)B13. ECG - List of office equipment - February 1983. 220.574 (B-13)

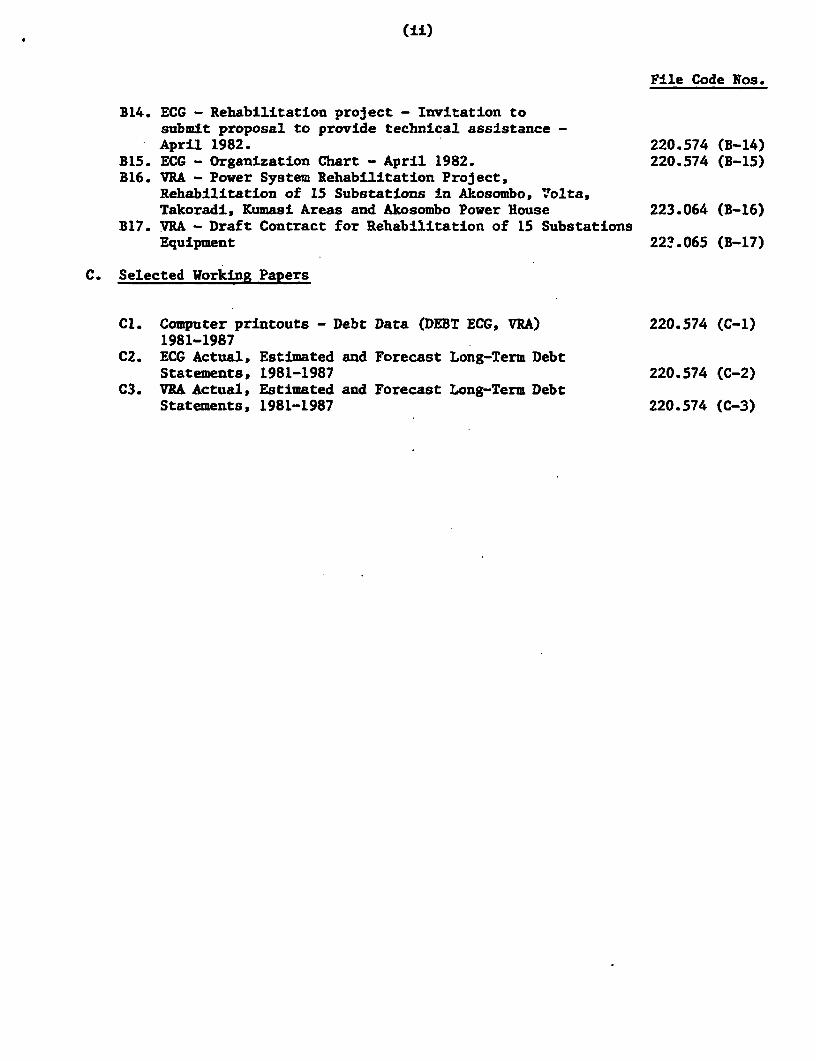

(ii)

File Code Nos.

B14. ECG - Rehabilitation project - Invitation tosubmit proposal to provide technical assistance -April 1982. 220.574 (B-14)

B15. ECG - Organization Chart - April 1982. 220.574 (B-15)B16. VRA - Power System Rehabilitation Project,

Rehabilitation of 15 Substations in Akosombo, Volta,Takoradi, Kumasi Areas and Akosombo Power House 223.064 (B-16)

B17. VRA - Draft Contract for Rehabilitation of 15 SubstationsEquipment 22!.065 (B-17)

C. Selected Working Papers

Cl. Computer printouts - Debt Data (DEBT ECG, VRA) 220.574 (C-1)1981-1987

C2. ECG Actual, Estimated and Forecast Long-Term DebtStatements, 1981-1987 220.574 (C-2)

C3. VRA Actual, Estimated and Forecast Long-Term DebtStatements, 1981-1987 220.574 (C-3)

(iii)

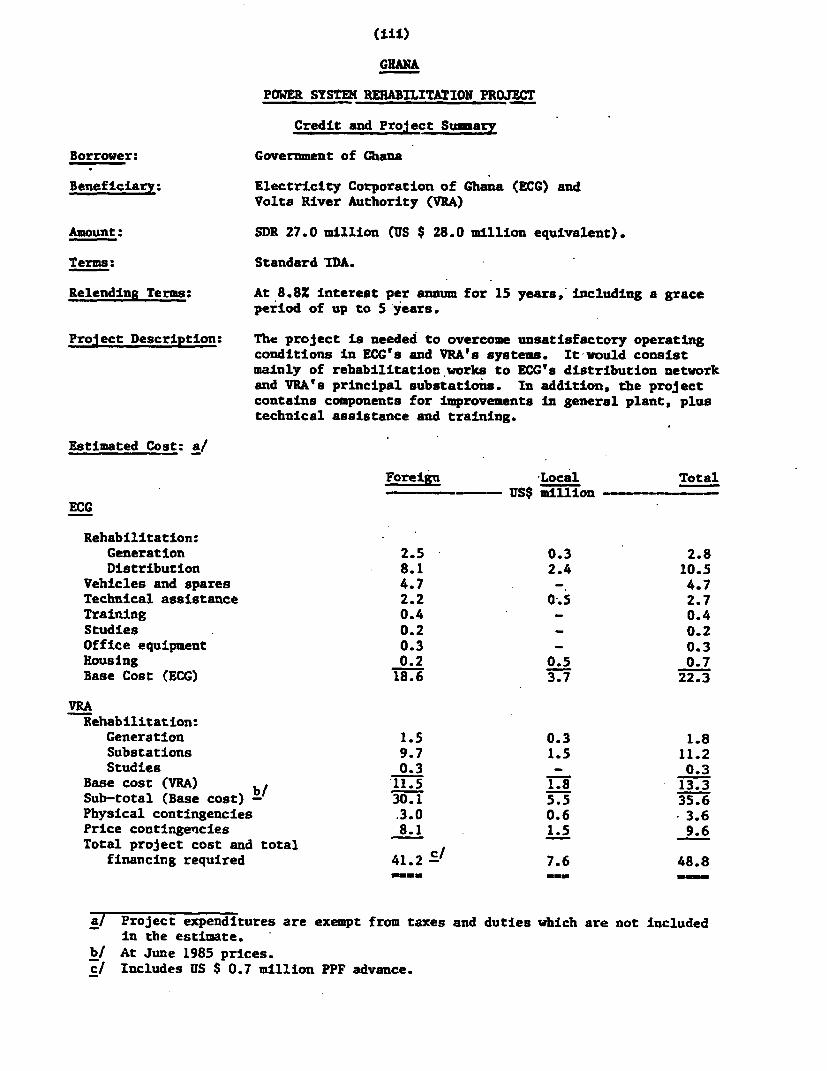

GHANA

P0IER SYSTEM REHABILITATION PROJECT

Credit and Project Su_ arv

Borrower: Government of Ghana

Beneficiary: Electricity Corporation of Ghana (ECG) andVolta River Authority (VRA)

Amount: SDR 27.0 million (US $ 28.0 million equivalent).

Terms: Standard'IDA.

Relending Terms: At 8.8X interest per annum for 15 years,'including a graceperiod of up to 5 years.

Project Description: The project is needed to overcome unsatisfactory operatingconditions in ECG's and VRA's systems. It-would consistmainly of rehabilitation works to ECG's distribution networkand VRA's principal substations. In addition, the projectcontains components for improvements in general plant, plustechnical assistance and training.

Estimated Cost: a/

Foreign Local Total-- c-= - WUS$ million -

ECG

Rehabilitation:Generation 2.5 0.3 2.8Distribution 8.1 2.4 10.5

Vehicles and spares 4.7 4.7Technical assistance 2.2 0.5 2.7Training 0.4 - 0.4Studies 0.2 0.2Office equipment 0.3 _ 0.3Housing 0.2 0.5 0.7Base Cost (ECG) 18.6 3.7 22.3

VRARehabilitation:

Generation 1.5 0.3 1.8Substations 9.7 1.5 11.2Studies 0.3 - 0.3

Base cost (VRA) b/ '11.5 1.8 13.3Sub-total (Base cost) - 30.1 5.5 35.6Physical contingencies .3.0 0.6 3.6Price contingencies 8.1 1.5 9.6Total project cost and total

financing required 41.2 c, 7.6 48.8

a/ Project expenditures are exempt from taxes and duties which are not includedin the estimate.

b/ At June 1985 prices.c/ Includes US $ 0.7 million PPF advance.

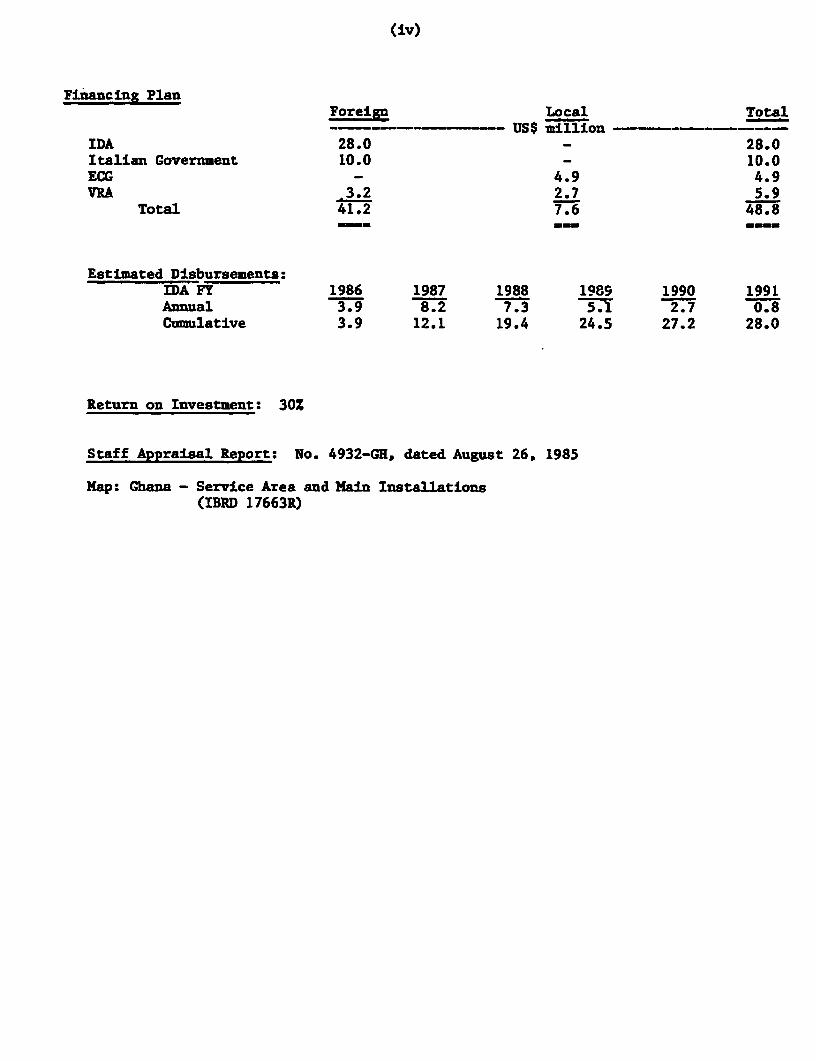

(iv)

Financing PlanForeign Local Total- - - - US$ million

IDA 28.0 28.0Italian Government 10.0 - 10.0ECG - 4.9 4.9VRA 3.2 2.7 5.9

Total 41.2 7.6 48.8=m _.

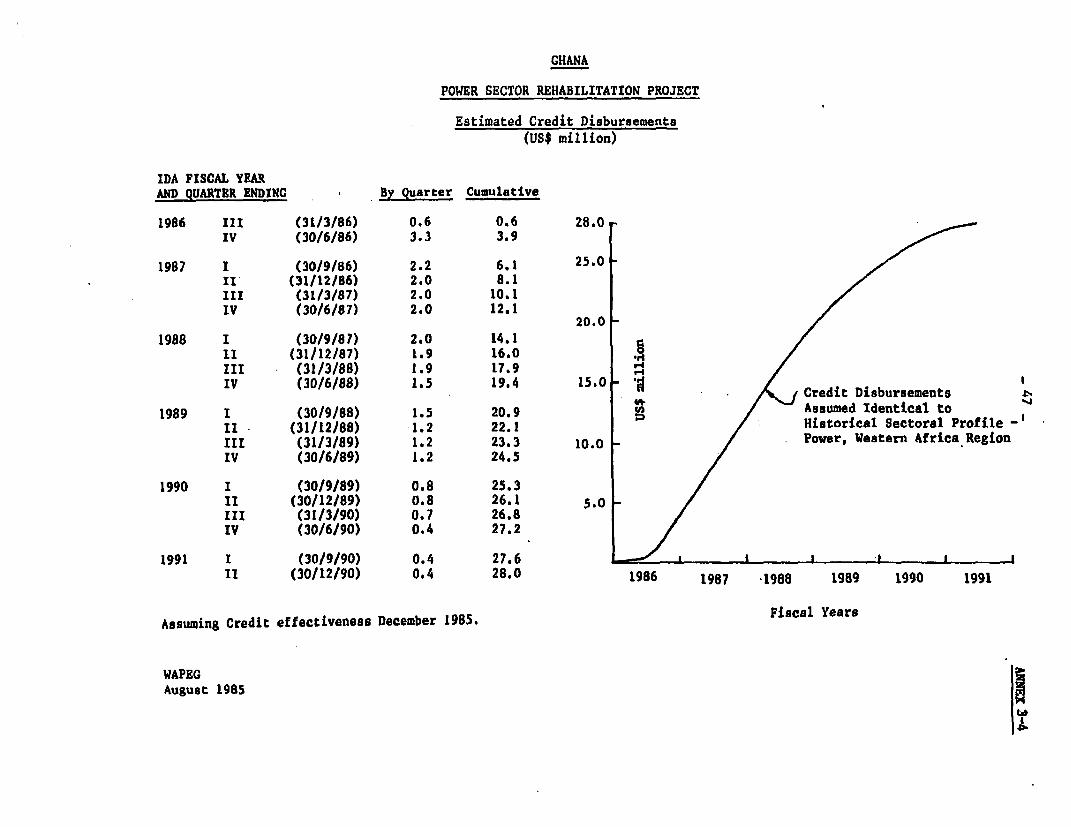

Estimated Disbursements:IDA FY 1986 1987 1988 1989 1990 1991Annual 3.9 8.2 7.3 2.7 0.8Cumulative 3.9 12.1 19.4 24.5 27.2 28.0

Return on Investment: 30Z

Staff Appraisal Report: No. 4932-GH, dated August 26, 1985

Map: Ghana - Service Area and Main Installations(IBRD 17663R)

I. THE ENERGY SECTOR

A. Energy Resources and Uses

1.01. Ghana has substantial energy resources. Wood is plentiful in thehigh forest zone which covers 34% of the total lantd area (8.2 millionhectares). Hydropower resources are also abundant, particularly in theCentral and Western regions of the country. The economically useablepotential is estimated at 2,000 MW, about twice the presently installedcapacity. Estimates of proven reserves of oil vary from 1 to 5 millionbarrels but the potential is considered to be larger. Recent drillings in theTano basin confirm the existence of large quantities of oil and natural gas.There are no known coal, lignite or peat deposits.

1.02. Energy demand of 4.2 million toe per year, or 360 kg per capita isrelatively low in comparison with other African countries. Domestic output ofenergy consisting primarily of wood and, to a lesser extent, hydropower andpetroleum, Is estimated at 3.6 million tons of oil equivalent (toe) and coversnearly 86% of Ghana's energy requirements. Wood meets some 73% of primaryenergy demand, petroleum 17X, and hydropower 10%. The sectoral breakdown offinal energy demand is estimated to be as follows: residential (urban andrural), over 67Z; industry and commerce, 15%; transport, 12Z; and agriculture,less than 6%. Despite the economic decline during most of the 1970's, energydemand during 1971-79 increased by almost 5% p.a. Between 1980 and 1984,however, the consumption of petroleum products decreased by about 20% becausethe scarcity of foreign exchange limited the import of petroleum products.During the same period, the severe drought, combined with breakdowns inelectrical distribution systems contributed to a reduction by 33% inelectricity consumption.

B. Sector Institutions

1.03. The principal responsibility for the energy sector lies with theMinistry of Fuel and Power (MFP). Government entities in the petroleum sectorinclude the Geological Survey Department which monitors petroleum exploration,the Ghana Italian Petroleum Company Limited which operates the refinery andthe Ghana Oil Company Limited which distributes petroleum products. In thepower sector, the Volta River Authority (VRA) owns and operates the hydroplants and high voltage transmission facilities, sells and exports bulkelectricity. The Electricity Corporation of Ghana (ECG) purchases power fromVRA for distribution throughout the country, and owns and operates dieselplants supplying isolated systems.

1.04. The Government has recently taken several steps to strengthenmanagement of the energy sector. First, it established the National EnergyBoard (NEB) as the advisory body to the MPP. NEB is responsible for gatheringstatistical data on energy resources, production, transformation andconsumption, for developing energy policies, conducting energy studies, andcoordinating activities in the renewable energy field. Second, the Governmenthas streamlined the organization of the petroleum sub-sector by establishingthe Ghana National Petroleum Corporation (GNPC) which has responsibility forexploration, development, production and disposal of petroleum. GNPC has also

taken on the responsibility for crude and petroleum product procurement, afunction previously performed by the Petroleum Department in the MFP. Andfinally, in the power sub-sector, the Government has hired the ElectricitySupply Board of Ireland (ESB) to examine the organization of the sector andprovide technical assistance to ECG and VRA.

C. The Renewable Energy Sector

1.05. More than 95% of Ghanaian households depend on wood or charcoal forcooking fuel. Forest-based products also meet a substantial proportion ofenergy needs in activities such as food processing, post-harvest drying andbeverage making. Total wood demand by 1990 is expected to be around 17million m3 of fuelwood and 7 million m3 of commercial foreetry cut.Projections of the forest resource balance through 1990 show an annualallowable cut of about 23 million =3. Although these aggregate figuresindicate that Ghana is not likely to face a forest depletion problem over thenext decade, there are serious prospects of regional fuelwood scarcity in someareas, particularly in the extreme Northeast.

1.06. Possibilities may exist in Ghana to develop small and mini hydropowersites in rural areas but the schemes so far identified are not economicallyattractive. There is potential for transformation of solar energy. A largeamount of research is being done in the renewable energy field by variousGhanaian institutions with the assistance of public and private aid agencies.To coordinate these research efforts and promote the use of renewable energyso that it could reduce the use of petroleum, particularly in the rural areas,the Government has decided to establish a renewable energy unit as part of NEB'and has created an Energy Fund, replenished through a special levy onpetroleum products. The IDA financed Energy Project (Credit 1373-GB of June1983), provides for experts, training, and equipment to assist NEE in thecoordination and preparation of programs for investment in renewable energyand help attract foreign financing. At Government's request the Bank has alsoagreed to provide a staff member on a temporary assignment in Ghana to provideassistance in renewable energy matters.

D. The Petroleum Sector

1.07. Ghana is a minor petroleum producer, producing about 650 barrels perday from the Saltpond field, some 15 km offshore and 100 km west of Accra.This represented about 52 of 1984 domestic consumption of about 0.6 millionmetric tons. The remainder is imported. Although not a petroleum intensiveeconomy by international standards (50 kg per capita in 1984), Ghana's heavydependence on imported petroleum for commercial energy has strained itsforeign exchange position. In 1976, US$ 48 million was spent on oil,representing no more than 6% of export of goods and services. In 1984imported oil cost about US$ 240 million, or over 40Z of Ghana's exportearnings.

1.08. Oil and gas have been found in the offshore Tano area near theborder with Ivory Coast. Recoverable reserves are roughly estimated at about

- 3 -

50 million barrels of oil and one TCF 1/ of gas. On the basis of a gas marketstudy financed under Credit 1373-GH of June 1983 the most promising market forthe gas appears to be power generation. However, the economic merits andfinancial costs of exploiting the gas reserves remain to be established. As afirst step, the Government has hired consultants to prepare reliable estimatesof the gas reserves of the Saltpond field where 10 million cubic feet of gasper day are flared, as well as of the other discoveries. Should gas reservesprove to be sufficient and economically exploitable, a gas thermal generatingplant may be justifiable.

1.09. Under the Energy Project (Credit 1373-GH) the Government is activelypromoting petroleum exploration. Offshore areas have been made available tothe petroleum industry and several proposals for exploration/production havealready been received from international oil companies.

1.10. Petroleum product consumption in Ghana diminished by 20% from 1980 to1984 to about 600,000 tons. Diesel accounts for the largest consumption share(35%), followed by gasoline (34%). The largest consuming sector is transport(75% of total consumption). The remainder covers the residential sector, 16%,and the combined industrial and agricultural sectors, 9%. Petroleum productprices have been raised substantially following the exchange rate adjustmentsin 1983 and 1984. The Energy Project includes the financing of a study todevise a sound pricing policy and a mechanism for revising prices in thepetroleum field. A plan of action based on the study is expected to beavailable by December 31, 1985.

E. Investment Requirements

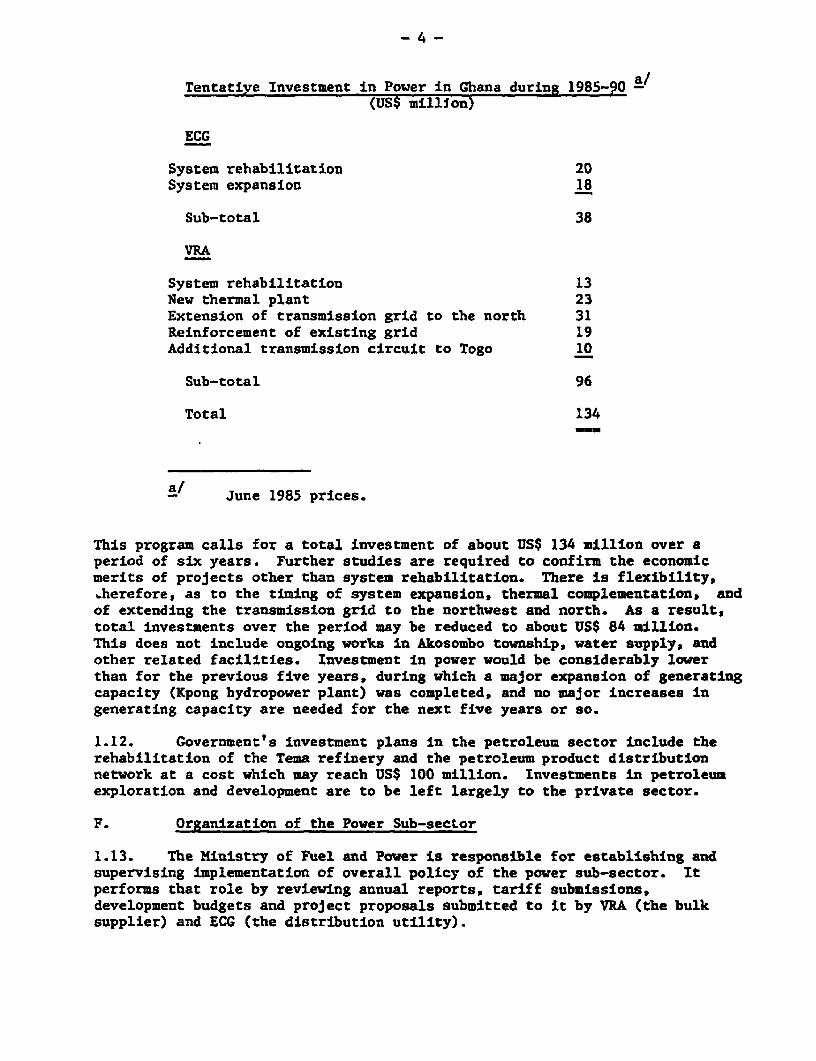

1.11. Government and the Bank are carrying out a review of publicinvestments which will be completed by September 1985. Investments in energyprojects during the period 1985-1990 will be conceutrated in power andpetroleum. Government proposals for investments in power would be mainly forrehabilitation of existing facilities, for extension of the high voltage gridand for small additions in thermal generating capacity to complement operationof the hydro plants, as follows:

1/ TCF - Trillion cubic feet.

- 4 -

Tentative Investment in Power in Ghana during 1985-90(US$ million)

ECG

System rehabilitation 20System expansion 18

Sub-total 38

VRA

System rehabilitation 13New thermal plant 23Extension of transmission grid to the north 31Reinforcement of existing grid 19Additional transmission circuit to Togo 10

Sub-total 96

Total 134-mm

June 1985 prices.

This program calls for a total investment of about US$ 134 million over aperiod of six years. Further studies are required to confirm the economicmerits of projects other than system rehabilitation. There is flexibility,.herefore, as to the timing of system expansion. thermal complementation, andof extending the transmission grid to the northwest and north. As a result,total investments over the period may be reduced to about US$ 84 million.This does not include ongoing works in Akosombo township, water supply, andother related facilities. Investment in power would be considerably lowerthan for the previous five years, during which a major expansion of generatingcapacity (Kpong hydropower plant) was completed, and no major increases ingenerating capacity are needed for the next five years or so.

1.12. Government's investment plans in the petroleum sector include therehabilitation of the Tema refinery and the petroleum product distributionnetwork at a cost which may reach US$ 100 million. Investments in petroleumexploration and development are to be left largely to the private sector.

F. Organization of the Power Sub-sector

1.13. The Ministry of Fuel and Power is responsible for establishing andsupervising implementation of overall policy of the power sub-sector. Itperforms that role by reviewing annual reports, tariff submissions,development budgets and project proposals submitted to it by VRA (the bulksupplier) and ECG (the distribution utility).

- 5 -

1.14. Since its foundation in 1961 VRA has operated as a quasi enclavewithin Ghana, has been well managed and has fully met its responsibilitieswithin the sector. VRA has therefore enjoyed the confidence of Government andhas its views and proposals accepted. ECG, on the other hand, with operationswhich are much more complex than those of VRA, has suffered from ;neffectivemanagement, has not met its sector responsibilities in recent years, and doesnot have full confidence of Government or the consumers. The contrast betweenthe highly efficient, albeit simpler, management and operations of VRA and thepoor, although more complex, management and operations of ECG have promptedGovernment and IDA to consider ways to achieve a more effective sectororganization. A study of the merits of a merger of VRA and ECG as well asother institutional arrangements in the sector is being carried out byElectricity Supply Board of Ireland (ESB) and financed by a PPF advanceapproved by the Bank on August 15, 1983.

1.15. The study is being carried out in three stages. The first stage tobe cc-Ir?leted by August 1985 consists of a diagnosis of the sector withrecommendations on future sector organization, and in particular an analysisof the merits of merging ECG and VRA. This stage also includes a work plan,staffing plan and schedule for execution of the second step. Government andIDA will review ESB's work and agree on a schedule to carry out the necessarymeasures by December 1985. In the second stage, expected to require 6 months,ESB will review existing legislation governing the sub-sector, and inparticular legislation govern-ing the management and operations of theutilities. ESB will review the utilities' organizations, objectives,functions, financial practices, maintenance programs, and training provisions.The study will also define the roles of the responsible Ministry, theboard(s), the chief executives, the department heads and their deputiesincluding as appropriate job descriptions, delegation of responsibility andreporting requirements. Government and IDA will review ESB's recommendationsbefore December 1986 and agree on a schedule to carry out the necessarymeasures. For the third stage, ESB will prepare a detailed institutionalrehabilitation plan and assist in its implementation which should lead tobuilding strong, efficient and autonomous organization(s) capable of meetingthe country's electric power requirements economically. During negotiationsGovernment agreed to carry out necessary sector organization measures on aschedule satisfactory to the Association and to initiate them no later thanDecember 31, 1985.

G. Power Facilities

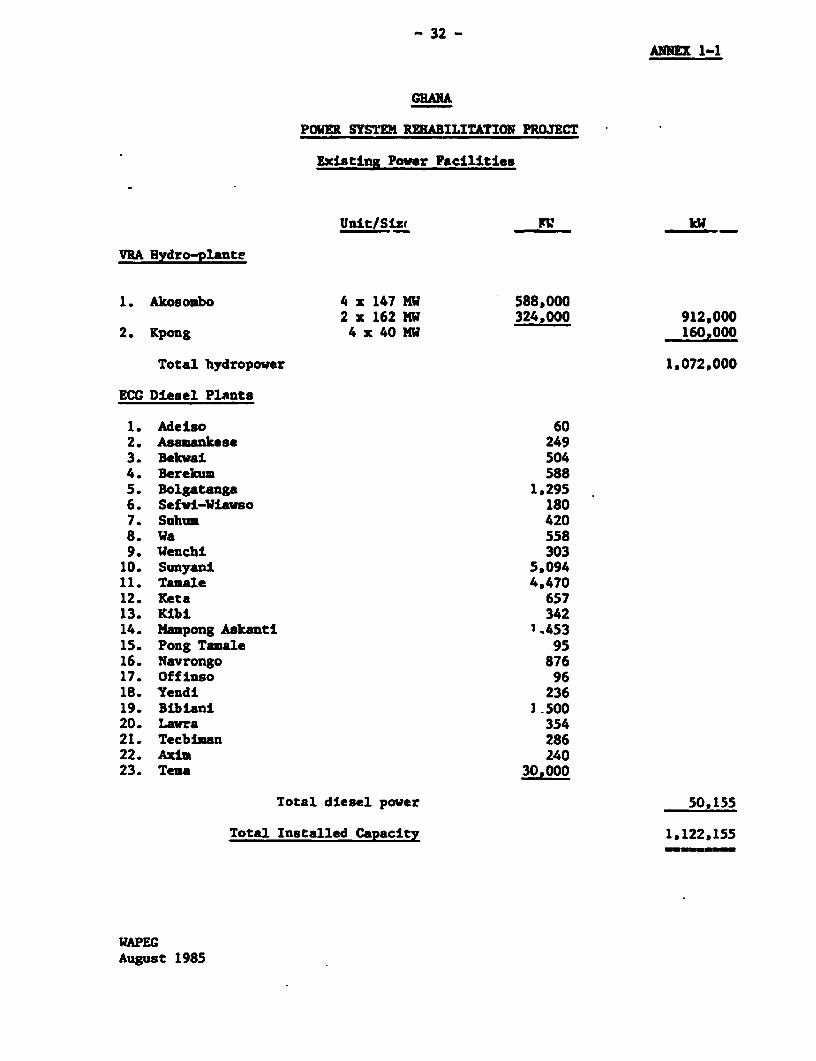

1.16. The total installed generating capacity in Ghana is about 1,130 MW ofwhich 1,072 MW (95%) is hydroelectric. The remainder comprises diesel unitsinstalled in 28 stations varying in size from 51 kW to 30 MW which aregenerally in poor condition. Hydro capacity is installed in two stationsowned by VRA on the Volta River - the Akosombo plant (912 MW), commissioned inthe mid-1960's, and the Kpong plant (160 MW), commissioned in 1982. Bothhydro plants are in good condition and well maintained. Because of age, theAkosombo plant efficiency has fallen, but it could be restored and probablyimproved. VRA would study this further, under the proposed project. Ghana'sinstalled capacity is described in greater detail in Annex 1-1.

- 6 -

1.17. The VRA 161 kV transmission system totals over 1,200 km. Eightcircuits of 67 km connect the Akosombo and Kpong plants to the VALCO smelterat Tema and other industrial loads. A 650 km transmission loop supplies ECGareas and mines in Southern Ghana. A 161 kV interconnection with CommunauteElectrique du Benin (CEB) connects Akosombo to Lome (Togo). In 1983, theIvory Coast was also interconnected through a 225 kV transmission line (seeMap). Under the proposed project these substations will be repaired andupgraded.

1.18. ECG's distribution facilities comprise 33 kV and 11 kV lines andunderground cables with 33/11/0.4 kV substations feeding power from VRA'stransmission system or ECG's diesel plants. ECG distributes power in the maincities - Accra, Tema, Kumasi, and Sekondi-Takoradi - and in other urbancenters located within the interconnected grid which covers the southern partof Ghana. About 95% of ECG's electricity requirement is purchased from VRA.ECG also operates a number of isolated stations on behalf of the Governmentwhich subsidizes the operation of these facilities. The quality of service isgenerally poor as the system has been inadequately maintained and consumershave been allowed to install service connections of varying materials andconstruction standards. Distribution losses average at least 15%. In view ofthe configuration of the system and the voltages involved, losses could bereduced to about 10%. In recent years service within the interconnected gridhas deteriorated due largely to poor maintenance and inadequate reinforcementof the distribution system. The isolated diesel plant systems serving smalltowns have even more serious problems. Many operate less than half the daybecause of inadequate supply of diesel fuel, in part due to poor roadconditions and the poor state of the contractor's tanker fleet.

R. Access to Service, Electricity Consumption and Exports

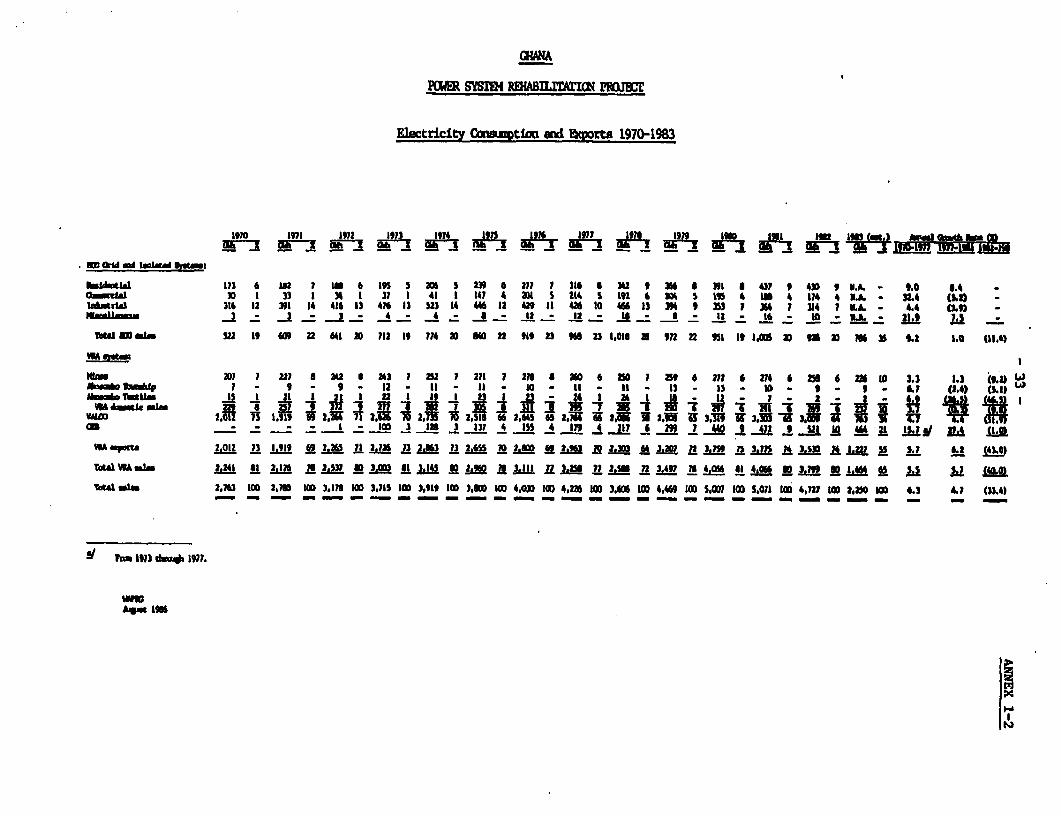

1.19. Ghana, with a population of about 12.5 million had about 230,000electricity consumers in 1983, indicating that no more than 10% of thepopulation 2/ had access to electricity. The cities of Accra, Tema, Takoradi,Kumasi, and Cape Coast accounted for 162,000 (70%) of the total number ofconsumers, with the remainder spread over other urban areas. Excluding salesto VALCO and CEB, per capita electricity consumption reached a high of 110 kWhin 1981 (this compares with 217 kWh in Ivory Coast, 124 kWh in Senegal).Sector sales grew steadily at an annual rate of 6.3Z between 1970 and 1977(from 2,763 GWh to 4,226 GWh), but slowed down to an annual pace of 5.0% overthe period 1977-1981 (from 4,226 GWh to 5,181 GWh), as economic activitydeclined. Between 1981 and 1983, however, sales dropped by 33.4Z becausehydro generation decreased from 5,650 GWh in 1981 to 2,650 GWh in 1983 asconsequence of the drought which started in 1981. In June 1983 VALCO wasforced to shut down its aluminum smelter which only resumed operations on areduced scale in April 1985. In 1984, VRA had to restrict supply to Ghana'sdomestic market to 1,000 GWh and to CEB to about 300 GWh. During the secondhalf of 1984 it began exports to Ivory Coast at an annual rate of 300 GWh.

2/ Based on average size household of 5 persons.

- 7 -

Details on Ghana's consumption pattern and rates of growth over 1970-1983 aregiven in Annex 1-2.

I. Power Development and Planning

1.20. Ghana's power sector is at a crossroads. The recent drought haddepleted the Volta lake (Akosombo reservoir), with the result that normaloperation of the reservoir is not certain before, say 1988. With domesticelectricity sales expected to grow between 2% to 5% p.a., new generatingcapacity would be needed primarily as reserve and to increase flexibility inreservoir management. According to an expansion plan prepared by AcresInternational Ltd. (Canada) all new capacity to the year 2000 would bethermal, as none of the hydro options is economic. The attractiveness ofthermal generation has been enhanced by recent offshore discoveries of gas.In all expansion schemes prepared by the consultants, rehabilitation of theTema diesel plant (10 x 3 MW) defers by about two years investments in newthermal capacity. The Tema plant would serve as standby and complement thehydro capacity. Rehabilitation.of Tema would cost about US$ 2.5 million andis included in the proposed project. f

1.21. In July 1984, Government and VALCO renegotiated the 1962 contract.The most significant change to the contract is the provision for reviews everyfive years and an increase in the price for power paid by VALCO, whichoriginally had been set at 2.625 US mills per kWh. The new rate is atapproximately the world average price for power supplied to smelters (aboutUS 20 mills/kWh). Also under the amended contract, VRA's supplies to VALCOare determined by a formula which guarantees that the domestic market getspriority over VALCO. The maximum energy assigned to VALCO is now 2,760 GWh(enough for only four out of five potlines). If VALCO requires more energy torun its fifth potline, it has the right of first refusal over any additionalenergy that may be available after VRA has met its other obligations but at aprice to be negotiated at that time. The new contract gives VRA considerableflexibility to supply customers other than VALCO, particularly the exportmarkets to Energie Electrique de la C^ote d'Ivoire (EECI) and CEB, and toincrease significantly its revenues. Since VRA no longer needs to guarantee afixed amount of power to VALCO, it can manage its reservoir in such a way asto maximize sales and reduce the likelihood of spilling water in wet years.

1.22. Other important changes to the agreement between Ghana and VALCOinclude an increase in the fee VALCO earns from its foreign shareholders onprocessing alui-na into aluminium and an increase in the tax rate on VALCO'sincome. Government now also has the right to nominate two directors to theVALCO board and the option to buy 20% of VALCO's equity during the next fiveyears. The effect on Government's revenues from the change in contract issignificant. For the maximum contracted amount (2,760 GWh/year) VRA'srevenues from sales to VALCO would be about US$ 39 million, at an aluminiumprice of USJ55/pound, as against US$ 15.5 million under the previousagreement. Similarly, tax revenues will increase significantly.

1.23. VRA has pioneered electrical supply across national boundaries inwestern Africa. It has supplied power to CEB starting in 1972 and to theIvory Coast since 1984. The interconnection has worked well and VRA, CEB, andBECI support a West Africa Power System Interconnection (WAPSI) within the

- 8 -

Union des Producteurs, Transporteurs et Distributeurs d'Energie Electriqued'Afrique (UPDEA). WAPSI, in a first stage, would aim at linking the powersystems of Benin, Ghana, Ivory Coast, Nigeria, and Togo. The presentlyinterconnected facilities would then be linked to the 330 kV Nigerian grid viaa 330 kV transmission line from the Ikeja West substation near Lagos to theVolta substation in Ghana. A Danish/Swedish joint venture was retained toprepare an interconnection feasibility study, which was financed with aScandinavian grant, and was completed in July 1984. The African DevelopmentBank (AfDB) was the executing agency and CEB supervised the study, with theBank providing advice. The feasibility study concluded that a West Africainterconnection (including Nigeria) was economic. The study assumed that gaswould be available to supply the 1,320 MW Egbin thermal plant near Lagos.However, the pipeline project to supply that plant is now stalled and thissituation casts doubts on the timing of interconnection with Nigeria.

1.24. The nature of the power systems and resource base in the regionsuggests that many benefits would be reaped from a Nigeria to Ivory Coastinterconnection. Ghana and Ivory Coast have largely hydro generation, whileNigeria is planning for large scale development of gas-fired thermalgeneration. Future interchanges might consist of firming up VRA hydrocapacity with NEPA thermal capacity and seasonal excess hydro energy transfersto effect fuel savings at NEPA in exchange for NEPA thermal energy support toVRA in dry periods. Another possibility is optimization of capacity use bytaking advantage of peak load diversity. Because utilities wish to retainindependence, and resolution of administration complexities takes time, anyinterconnection benefits are likely to be realized only in successive stagesof cooperation. The CEB - VRA - EECI portion of the interconnection hasbecome more attractive with the discovery of gas in Ghana and Ivory Coast,which could fuel gas-fired thermal plants to provide the requiredcomplementation for hydro, and with the increased flexibility provided by thenew VALCO/VRA agreement. As a consequence, reinforcement of VRA's existinggrid and additional transmission circuit to Togo and increased capacity oftransmission to Ivory Coast will likely proceed within the next two to threeyears. Given the uncertainty of future conditions on the Nigerian powersystem and, therefore, the economic attractiveness of the Nigerian portion ofthe West Africa interconnection, VRA has planned a back-up alternative tothermal support from Nigeria. The Acres study determined that a small amountof thermal capacity, 50 to 100 MT, would increase substantially the amount ofenergy VRA could sell while reducing the probability of spilled water byproviding a standby source to meet energy deficits in dry years. VRA shouldprepare such a thermal project for execution in case full interconnection doesnot proceed. The project would therefore include site investigations,engineering and bidding document preparation for a VRA thermal plant tocomplement existing hydro. The type, oil versus gas versus coal and sizewould be finalized in the continuing Acres study.

II. THE BORROWER AND EXECUTING AGENCIES

The borrower of the IDA and cofinanced funds would be the Governmentof Ghana and the beneficiaries would be ECG and VRA.

- 9 -

A. Electricity Corporation of Ghana (ECG)

2.01. ECG was established in 1967 to succeed the Electricity Division ofthe Ministry of Works and Housing and is responsible for the distribution ofelectricity throughout Ghana and for the country's diesel power plants and theoperations of Government's rural electrification works. Over the last fiveyears, ECG could not discharge its responsibilities satisfactorily due toineffective management and lack of foreign exchange to purchase spare partsand equipment. The quality of its service is poor with interrupted andintermittent supply and ECG has been unable to provide either for newconnections or for system reinforcement to maintain voltage levels.

1. Organization and Management

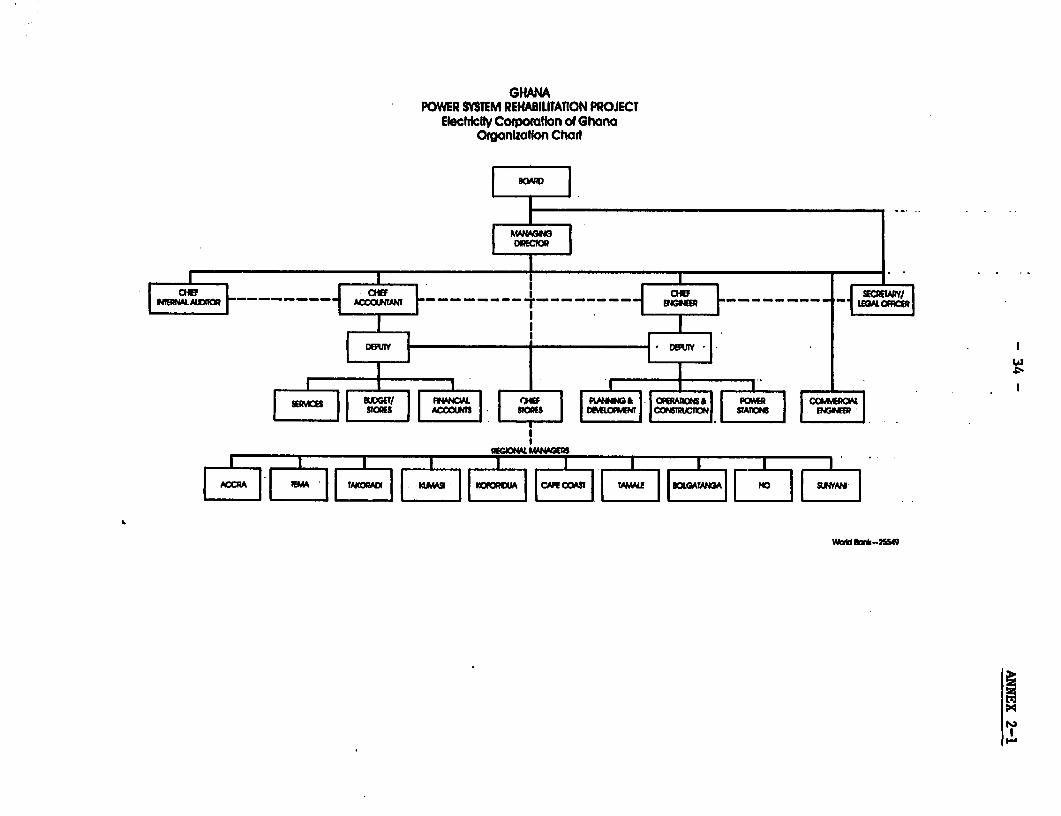

2.02. ECG is organized along typical utility lines. Its organization cLiartis shown in Annex 2-1. ECG has had organization and management problems forseveral years, such as poor administrative links with provincial centers, lackof effective administrative procedures, and a weak managerial team. In May1982 EeG's Board was replaced by a committee comprising the Managing Director,the Financial Controller or Chief accountant, the Chief Engineer of ECG, amiddle management representative, a trade -anion representative, and tworepresentatives of ECG's Workers Defense Committee. This committee provedineffective because it was concerned primarily with political matters andinterfered in the day to day operations of the utility. The committee wasdissolved in December 1984 and the old system reinstated. As part of itssecond stage work (para. 1.15) ESB will examine the composition andresponsibilities of ECG and its new board. Any necessary action will beincluded in ESB's third stage work.

2. Manpower

2.03. At year-end 1979, ECG had close to 6,200 employees (or 37 customersper employee, compared to 90 in Ivory Coast and 80 in Senegal) when it frozehirings. By the end of 1984 the number of employees had declined to 4,800.The pace of employee resignations has accelerated over the last year to about45 per month, as an increasing number of people are cashing in on theiraccrued benefits. Although an appropriate overall staff level will be reachedin the near future, ECG will still be overstaffed at the lower levels and willnot have qualified and trained personnel in sufficient numbers at all levels.ECG has had problems in recruiting and retaining suitably qualified staff,partly because of image problems and partly because employees are notadequately compensated. As a result, ECG has vacancies in about 50% of themanagement and professional cadres and many incumbents appear unsuitable forthe positions they hold. ESB will examine in detail ECG's manpower problemslncluding compensation and make recommendations and would assist ECG infinding suitable managerial staff from within ECG and Ghana and from overseasif necessary (para. 1.14). IDA and the Government will discuss theirrecommendations and agree by December 1986, on a plan to implement themeasures that should be taken in this area. In the meantime, and given theseriousness of the probleu, housi.ng would be financed under the project andassigned to senior staff to complement their remuneration.

- 10 -

3. Training

2.04. ECG is building its own training center at Tema for its technical,commercial and administrative training needs. Due to a shortage of importedmaterials, however, the workshop building is not yet completed. The centeralso lacks equipment, materials, and technical instructors. Staff trainingabroad has been curtailed due to cuts in bilateral aid and foreign exchangeproblems. Consequently, there is a backlog of training needs for managers,engineers and accountants who need exposure to utility operations overseas.In addition, ECG must develop the ability to continuousiv assess its manpowerneeds and plan all its training activities. The technical assistance programunder the proposed project would review all matters relating to training.Completion of the training center, including acquisition of remainingequipment would be financed under the proposed credit. ESB would review theutilities' training provisions and prepare a training program by December1986.

4. Accounting and Audit

2.05. Like other parts of ECG, its accounting department lacks qualifiedstaff. Financial management is almost non-existent and its accounting systemneeds redesign. Information is both sparse and unreliable. ECG keepsseparate accounts for the operation of rural electrification networks onGovernment's behalf. At end-1982, rural net fixed assets represented about 5Xof ECG's own assets. ECG's accounts are audited by Coopers and Lybrand. Forsome years now the auditors have heavily qualified their certificates for ECGdue to the unreliability of its accounting. As part of its assignment, ESBwould assist ECG overcome its accounting and financial management problems.

5. Insurance

2.06. ECG insures for protection against losses of goods-in-transit, fire,third party claims on vehicles and other property and workmen's compensationalong accepted public utility practices.

B. Volta River Authority (VRA)

2.07. VRA is a modern, well operated public utility with a high degree ofautonomy, and is responsible for hydropower generation and power exports toTogo-Benin and Ivory Coast, bulk power supplies to ECG, the Volta AluminumCompany's (VALCO) smelter at Tema, to gold and diamond mines, and the Akosombotextiles and township. VRA was established in 1961 to construct and operatethe Akosombo hydro-plant on the Volta River, which was the first hydroelectricproject in Ghana and was partly financed by the Bank (Loan 310-GH of February1962). In addition to Akosombo, VRA owns the Kpong hydroplant downstream ofAkosombo and the 161 kV grid in Ghana with extensions to Togo and the IvoryCoast.

1. Organization and Management

2.08. VRA's charter, the 1961 Volta River Development Act, charges VRA notonly to operate its hydroelectric plants according to sound public utilitypractices, but also to develop the Volta Lake which involves lake research and

- 11 -

transport. VRA is governed by a Board which is appointed by the Head ofState, who is Chairman ex-officio. The Board is composed of a Chairman andseven other members, including VRA's Chief Executive and representatives ofECG and VALCO. Its organization chart is shown in Annex 2-2.

2. Manpower and Training

2.09. As of December 1984, VRA had about 2,500 employees of which about 95%are engaged in electricity services and 5% in other activities. VRA has beenable to build up and retain good staff because of its financial and managerialindependence, relatively good working conditions and in spite of itsrelatively low salaries. As a result, the morale of VRA's staff is muchhigher than that of ECG's staff. VRA has recently installed its own trainingcenter at Akuse (Kpong) which is functioning well. VRA is receiving financialassistance (about US$ 3 million) on concessional terms from CIDA (Canada) tofinance equipment and expatriate instructors for its training center. TheAkuse center does not yet have all intended training specializations (notably,mechanical maintenance training), but VRA plans to provide these opportunely.

3. Accounting and Audit

2.10. VRA's accounting system is good. Financial forecasting is done on amicro-computer and production of accounting, budgeting and forecasting data istimely. VRA maintains separate accounts for activities unrelated toelectricity services. The accounting and finance departments have qualifiedstaff but appear understaffed. VRA's accounts are also audited by Coopers andLybrand. The accounts of VRA have always been certified without qualificationby the auditors.

4. Insurance

2.11. VRA insures against most common risks associated with hydrogeneration and transmission, fire, third party claims on vehicles and otherproperty and workmen's compensation along accepted public utility practices.

C. History of Bank Group Involvement with the Power Sector

2.12. Three projects financed by three IDE credits and one IBRD Loan havebeen made to assist the expansion of ECG's distribution system: a credit ofUS$ 10 million in 1968, US$ 2 million in 1971 and US$ 9 million in 1977together with a loan of US$ 9 million. The first two projects were completedsatisfactorily. The Third Power Project was completed in 1982 after athree-year delay, due in part to Ghana's economic situation and in part toECG's poor project administration. Although the project was successful inproviding new facilities, it was not successful in improving the management orthe operations of ECG. A Project Performance Audit Report (PPAR) of June 6,1985, presents in detail the effects of the project and the main lesson to belearned from it which is that in economies where growth prospects areuncertain, more emphasis should be placed on ensuring full utilization ofcapacity of existing facilities, rather than investing in extensicns of suchsystems.

- 12 -

2.13. Three loans have been made to VRA: the first for US$ 47 million toassist in financing the Volta River Hydroelectric Project (Akosombo) in 1961;the second for US$ 6 million for the Volta Expansion Project in 1968; and thethird for US$ 39 million to help finance the Kpong Hydro-Project in 1977. Thefirst two projects were completed satisfactorily. The Kpong projectexperienced cost overruns of about 140% in local costs and 14% in foreign costand two years delay, and was completed 1982. The cost overruns were due toGhana's poor economic condition which caused shortages and delays in obtaininglocally purchased equipment and materials and by the very high inflation thatprevailed at that time. The PPAR of June 6, 1985, points out, among others,that for hydro projects in the Sahel, extensive drought periods must beconsidered in structuring the hydrological design and operation criteria.

D. Bank Group Objectives, Strategy and Rationale for Involvement

2.14. The principal objective of the Bank in the power sector in Ghana isto improve the reliability, reduce the cost of electric power supplies andsupport economic grid extensions within Ghana, while at the same time reducingthe demands imposed by the sector on Government resources and maintaining thesector's export capability. The Bank's past lending has helped Ghana achievesome of these objectives, and by assisting VRA, has helped build one of thebetter managed utilities in West Africa. The Bank has not, however, succeededin introducing institutional and organizational reforms in ECG which wouldhave helped improve reliability and reduce costs. During the preparation ofthis project, IDA and the Government have agreed on a two front approach totackle the sector's problems. First, ESB's work and follow-up actions willprovide the basis for the reorganization and institutional rehabilitation ofthe sector. Second, the physical rehabilitation of the sector's facilitieswill improve service and consolidate finances. These actions would preparethe sector for future development and enhance its capacity to fulfill itsstrategic role in the economic growth both in Ghana and in its neighbors.

III. THE PROJECT

3.01. The project proposed for IDA financing is an important component ofthe 1986-90 investment program and will concentrate on the rehabilitation ofECG's and VRA's systems. It includes priority facilities that would permitthe sector to provide reliable service by 1990. Implementation of the projectis expected to begin by January 1, 1986, and be completed by December 31,1990.

- 13 -

3.02. Project Descrlption. The project comprises the following:

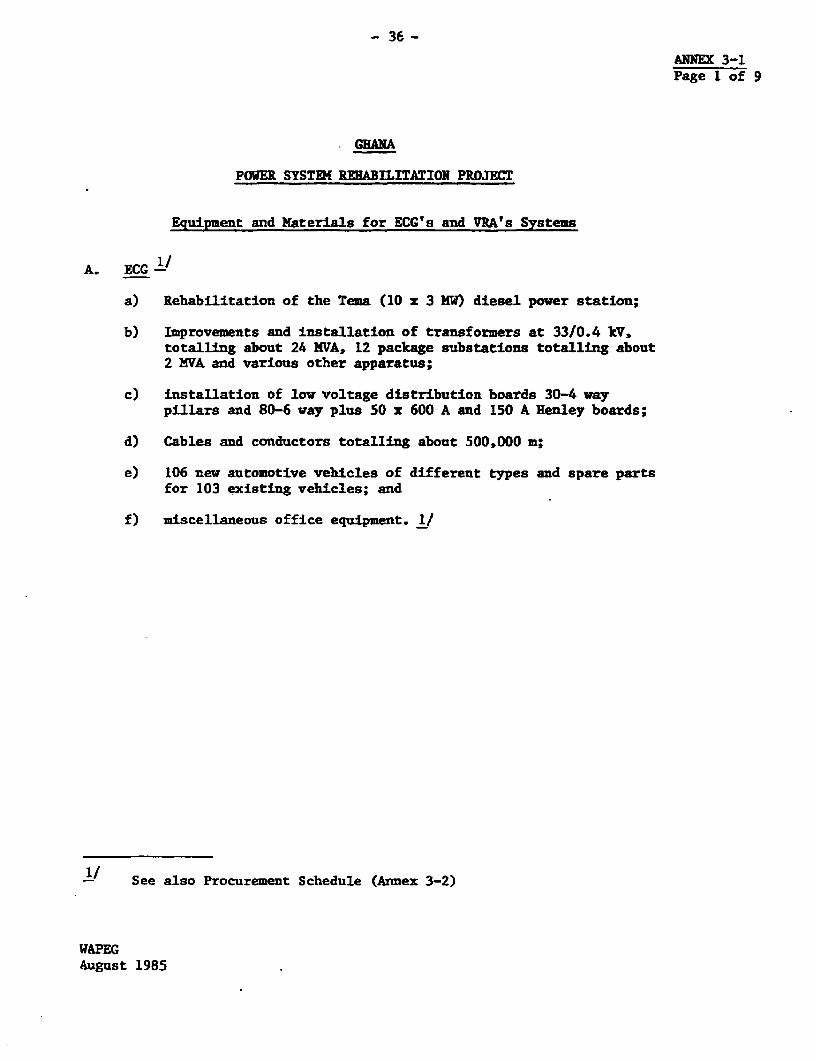

A. ECG

(a) Generationrehabilitation of the Tema diesel plant (10 x 3 MW). 3/

(b) Distribution 4/(i) improvements and installation of transformers at 33/0.4 kV,

33/11 kV, and 11/0.4 kV.

(ii) installation of low voltage distribution boards.

(c) General Plantprovision of about 100 new motor vehicles and spare parts for about120 existing ones, about 10 houses for ECG's senior staff, andmiscellaneous office equipment;

(d) Institutionaltechnical assistance and trainin- to be provided by an operatingutility. Government and ECG have retained the Electricity SupplyBoard of Ireland (ESB) who will perform the following:

(i) a diagnosis of the sector with recommendations on future sectororganization, and in particular on analysis of the merits ofmerging ECG and VRA and also include preparation of a workplan, staffing plan and schedule for execution of the followingwork stage;

(ii) review existing legislation governing the sub-sector, and inparticular legislation governing the management and operationof the utilities;

(iii) prepare a detailed institutional rehabilitation plan and assistin its implementation. ESB's services would entail about 168man-months; and

(iv) technical assistance through operational support, also to beprovided by ESB.

(e) Trainingtraining overseas of 6 mid-level professionals has been included,plus 6 scholarships.

3/ To be executed by VRA.

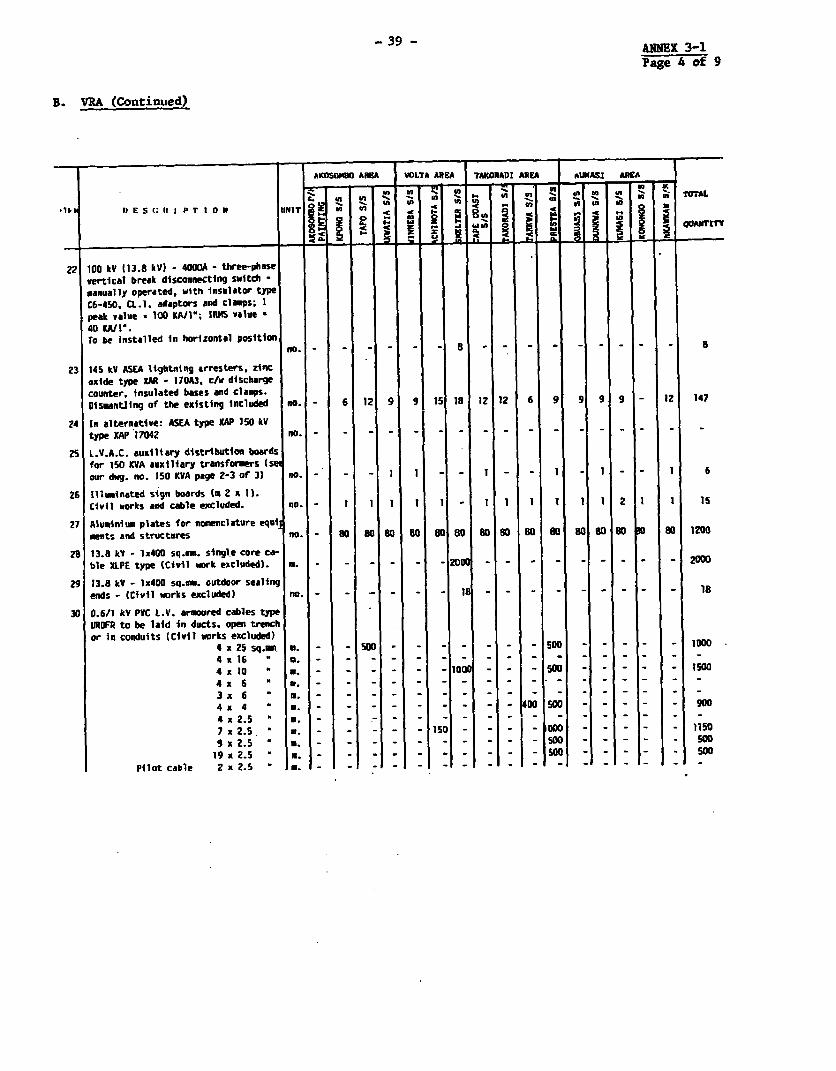

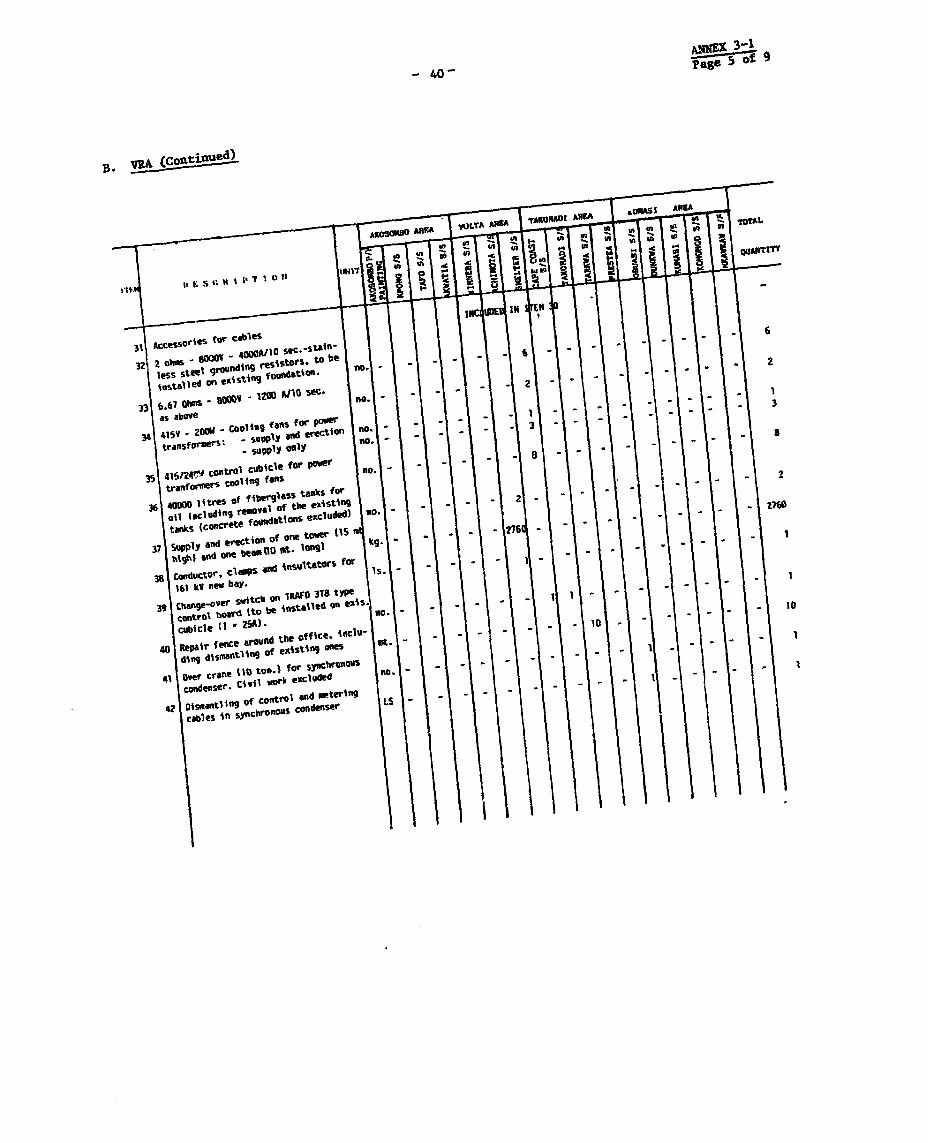

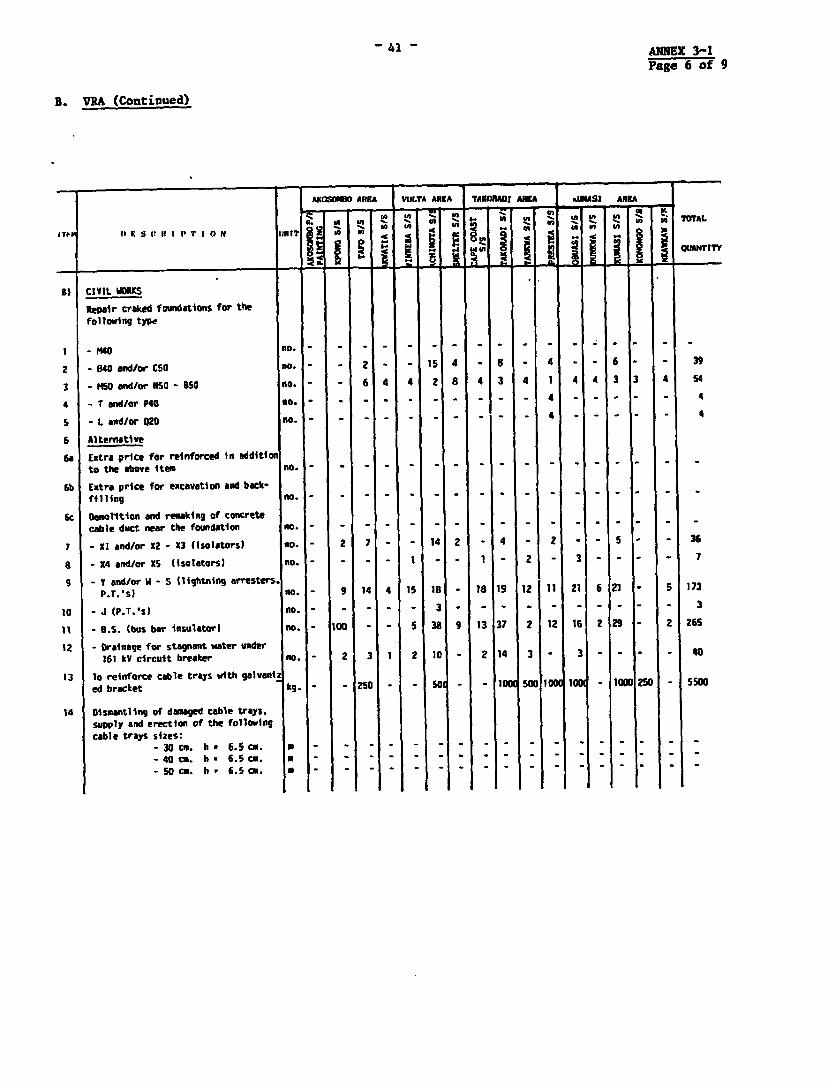

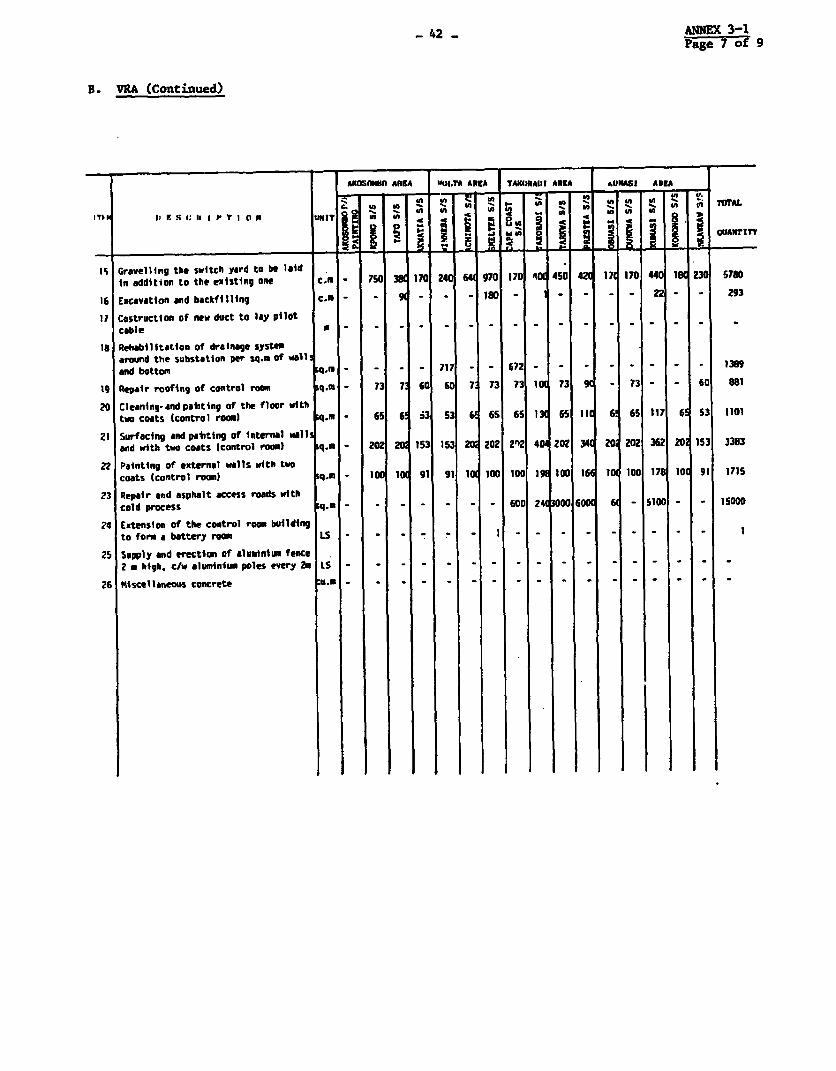

4/ For details see Annex 3-1.

- 14 -

B. VRA

(a) Generationanticorrosive painting of all exposed metal parts of the Akosombohydro plant;

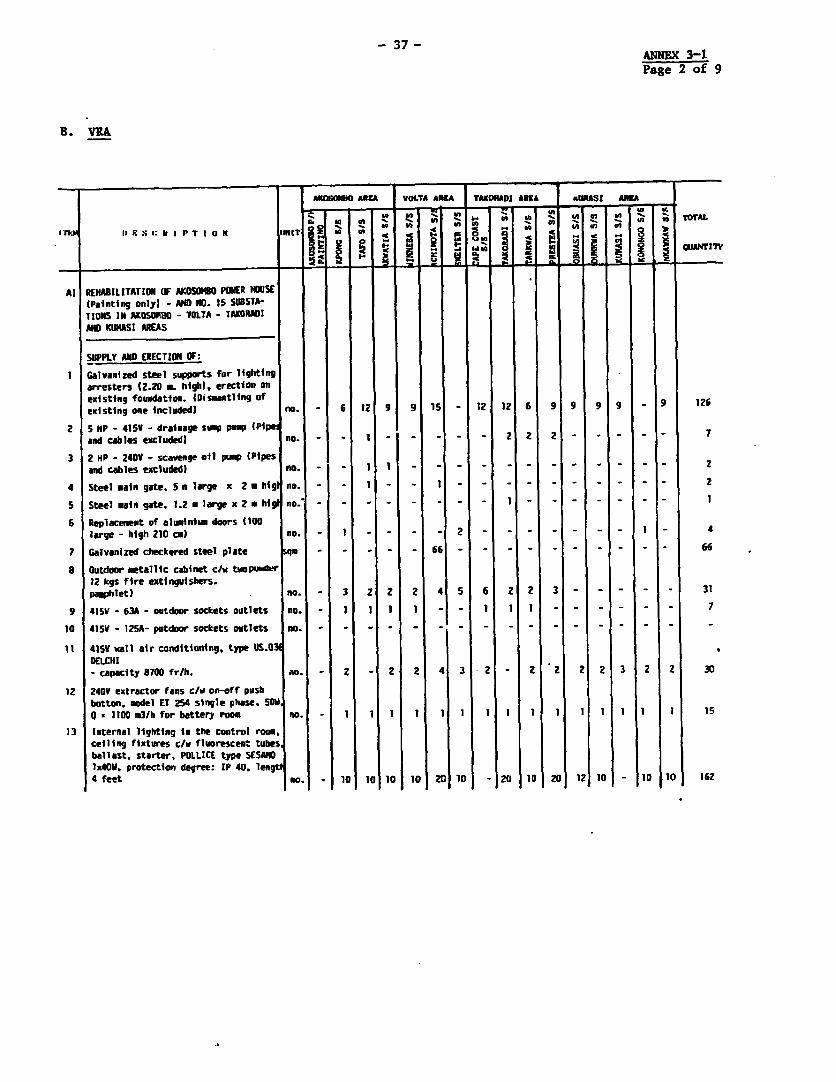

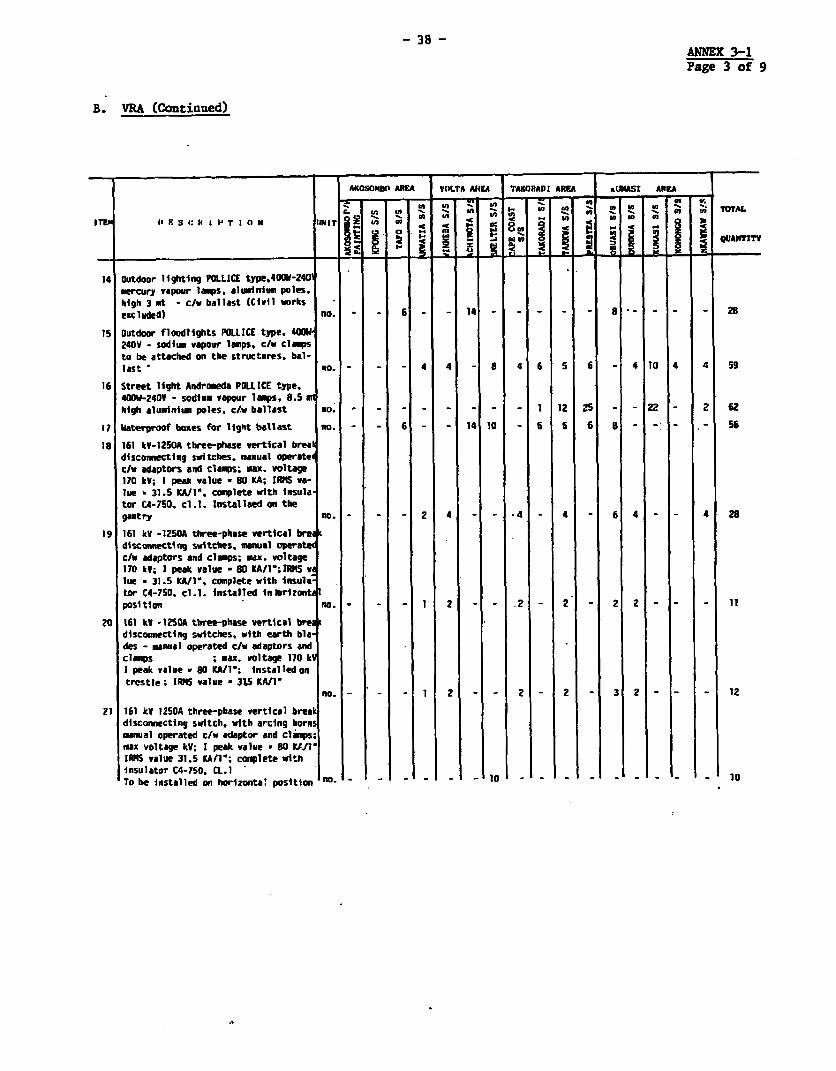

(b) general improvements and renovation of miscellaneous electricalapparatus in the following substations: 5/

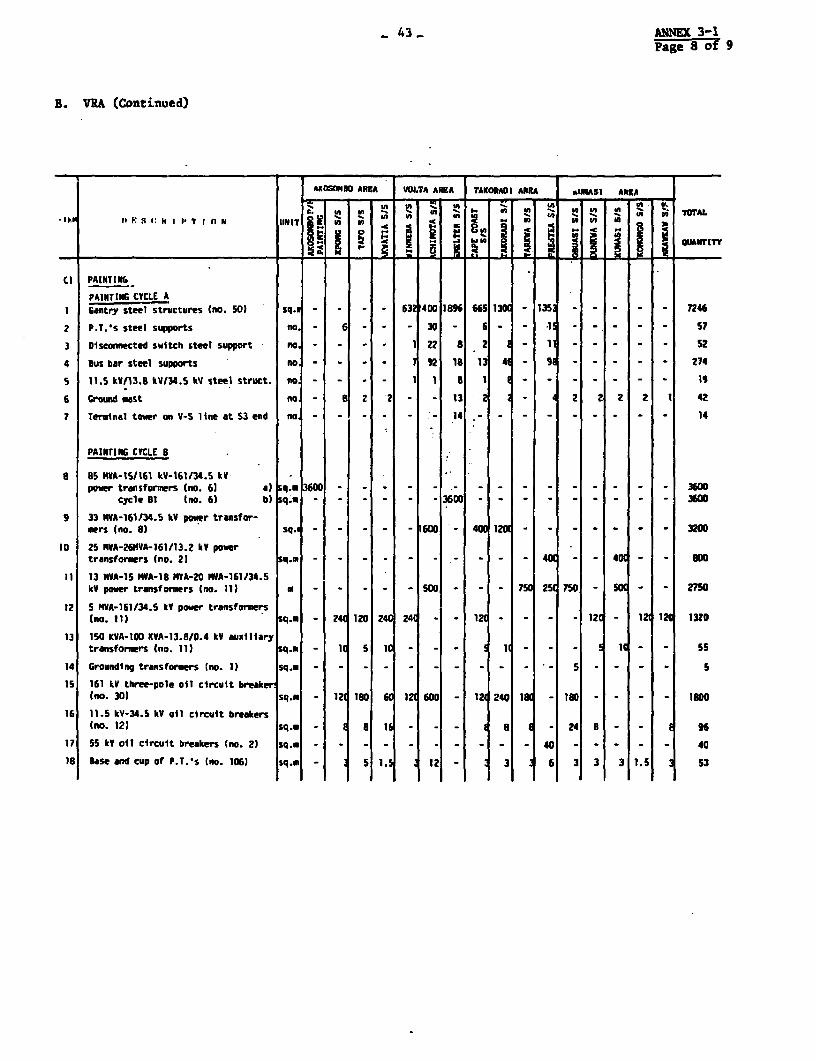

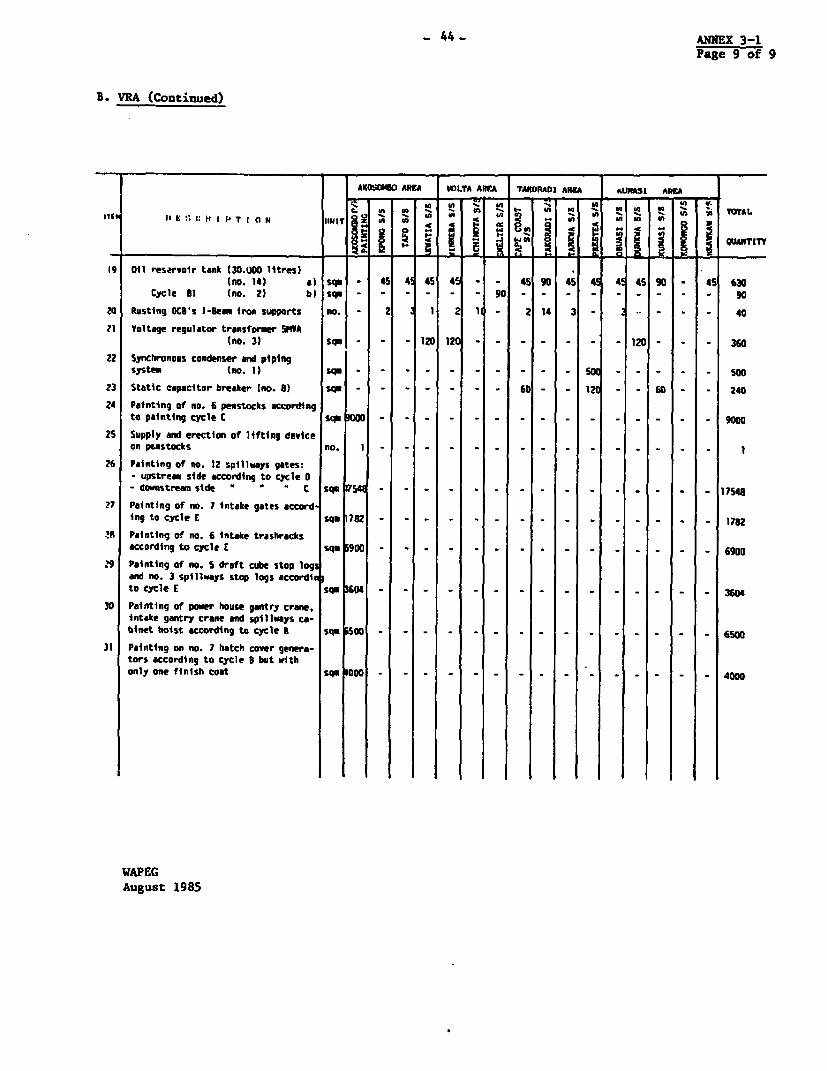

- Akosombo Area - Kpong, Tafo and Akwatia;- Volta Area - Winneba, Achimota, and Smelter;- Takoradi Area - Cape Coast, Takoradi, Tarkwa, and Prestea; and- Kumasi Area - Obuasi, Dunkwa, Kumasi, Konongo, and Nkawkaw; and

C. Studies

- Improvement in efficiency of the Akosombo hydro plant.

- Distribution expansion plans.

- Market surveys and economic analyses of the high voltage lineextensions to the northwest and northern parts of Ghana.

- Detailed and updated economic analyses of the proposedgeneration expansion plan and detailed engineering studies forthe next power plant.

- Tariff study (discussed in para. 4.12).

A. Project Cost

Project costs are summarized below:

5/ For details see Annex 3-1.

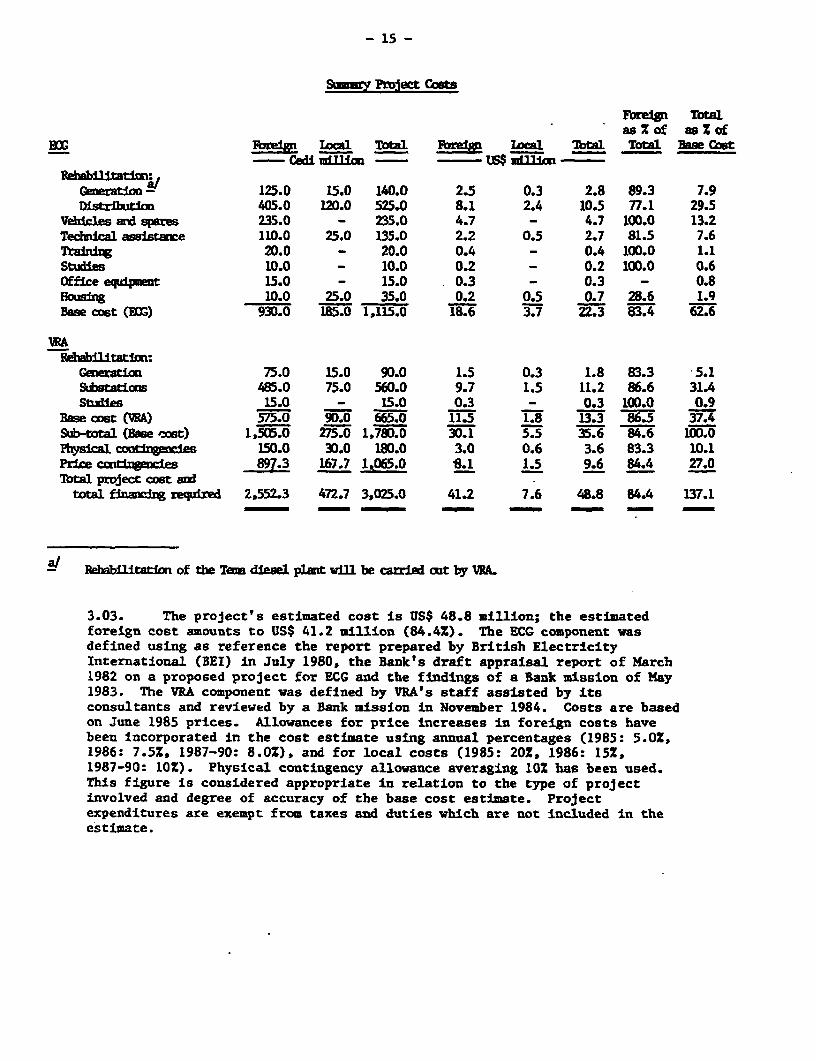

- 15 -

-mnory Project Costs

Foreign Totalas % of as % of

_~~~~~~~~~~~~~~oa Ikcal Toaltal_ceBOO FCMVIW Tool Toa Fr4p local Total Total Base cost- Cedi mink - !aLfLt -

Re*ibflitatlixnG8 125.0 15.0 140.0 2.5 0.3 2.8 89.3 7.9

Distrlbutim 405.0 120.0 525.0 8.1 2.4 10.5 77.1 29.5Vehicles and spares 235.0 - 235.0 4.7 - 4.7 100.0 13.2Technical assistance 110.0 25.0 135.0 2.2 0.5 2.7 81.5 7.6Training 20.0 - 20.0 0.4 - 0.4 100.0 1.1Studies 10.0 - 10.0 0.2 - 0.2 100.0 0.6Office eqipment 15.0 - 15.0 0.3 - 0.3 - 0.8Hbusing 10.0 25.0 35.0 0.2 0.5 0.7 28.6 1.9Base cost (BOG) 930.0 185.0 1,115.0 18.6 3.7 22.3 83.4 62.6

RAEdbfltticx:

Geeaticu 75.0 15.0 90.0 1.5 0.3 1.8 83.3 5.1Substations 485.0 75.0 560.0 9.7 1.5 11.2 86.6 31.4Studies 15.0 - 15.0 0.3 - 0.3 100.0 0.9

Base cost 3) 575.0 90.0 665.0 11.5 1.8 13.3 86.5 37.4Sub-total (Base cost) 1,505.0 275.0 1,780.0 30.1 5.5 35.6 84.6 100.0Phyical contignes 150.0 30.0 180.0 3.0 0.6 3.6 83.3 10.1Price cltfrgmEie 897.3 167.7 1065.0 8.1 1.5 9.6 84.4 27.0Total project cost andtotal finaxn requried 2,552.3 472.7 3,025.0 41.2 7.6 48.8 84.4 137.1

a/ Re litt of the Ta diesl plait wi be crried out by WA.

3.03. The project's estimated cost is US$ 48.8 million; the estimatedforeign cost amounts to US$ 41.2 million (84.4%). The ECG component wasdefined using as reference the report prepared by British ElectricityInternational (BEI) in July 1980, the Bank's draft appraisal report of March1982 on a proposed project for ECG and the findings of a Bank mission of May1983. The VRA component was defined by VRA's staff assisted by itsconsultants and reviewed by a Bank mission in November 1984. Costs are basedon June 1985 prices. Allowances for price increases in foreign costs havebeen Incorporated in the cost estimate using annual percentages (1985: 5.0%,1986: 7.5%. 1987-90: 8.0%), and for local costs (1985: 202. 1986: 15Z,1987-90: 10%). Physical contiugency allowance averaging 10% has been used.This figure is considered appropriate in relation to the type of projectinvolved and degree of accuracy of the base cost estimate. Projectexpenditures are exempt from taxes and duties which are not included in theestimate.

- 16 -

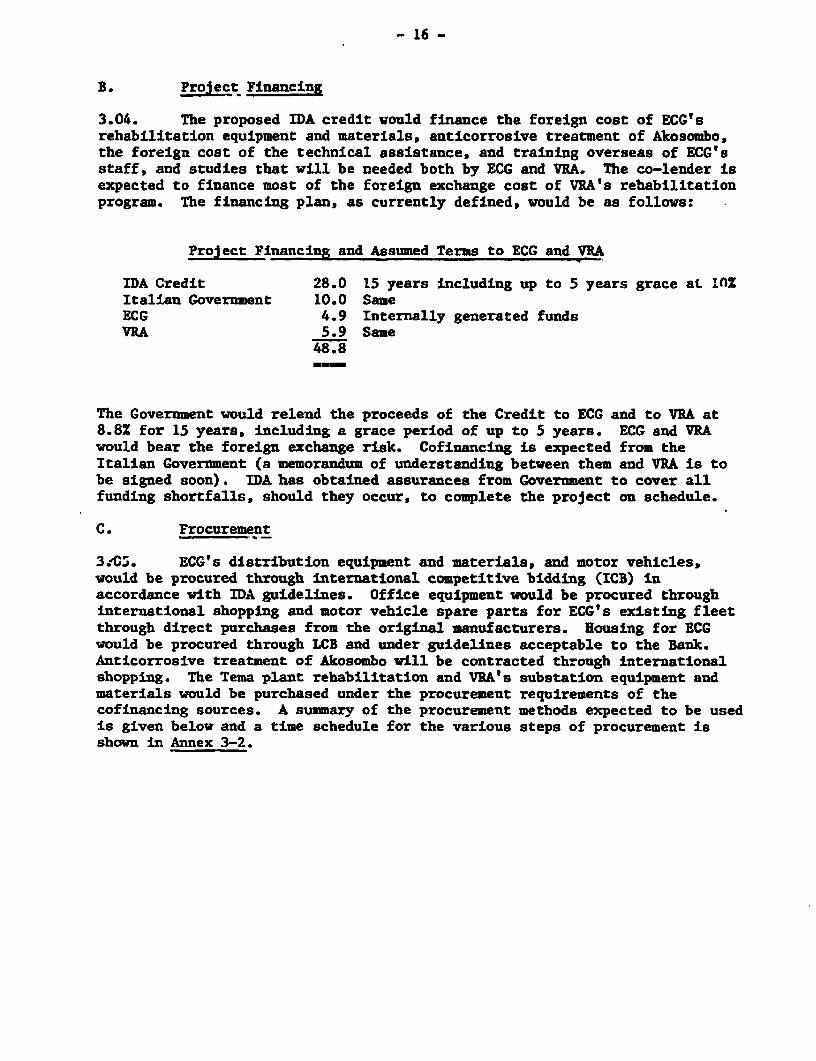

B. Project Financing

3.04. The proposed IDA credit would finance the foreign cost of ECG'srehabilitation equipment and materials, anticorrosive treatment of Akosombo,the foreign cost of the technical assistance, and training overseas of ECG'sstaff, and studies that will be needed both by ECG and VRA. The co-lender isexpected to finance most of the foreign exchange cost of VRA's rehabilitationprogram. The financing plan, as currently defined, would be as follows:

Project Financing and Assumed Terms to ECG and VRA

IDA Credit 28.0 15 years including up to 5 years grace at lnZItalian Government 10.0 SameECG 4.9 Internally generated fundsVRA 5.9 Same

48.8

The Government would relend the proceeds of the Credit to ECG and to VRA at8.8% for 15 years, including a grace period of up to 5 years. ECG and VRAwould bear the foreign exchange risk. Cofinancing is expected from theItalian Government (a memorandum of understanding between them and VRA is tobe signed soon). IDA has obtained assurances from Government to cover allfunding shortfalls, should they occur, to complete the project on schedule.

C. Procurement

3.,05. ECG's distribution equipment and materials, and motor vehicles,would be procured through international competitive bidding (ICB) inaccordance with IDA guidelines. Office equipment would be procured throughinternational shopping and motor vehicle spare parts for ECG's existing fleetthrough direct purchases from the original manufacturers. Housing for ECGwould be procured through LCB and under guidelines acceptable to the Bank.Anticorrosive treatment of Akosombo will be contracted through internationalshopping. The Tema plant rehabilitation and VRA's substation equipment andmaterials would be purchased under the procurement requirements of thecofinancing sources. A summary of the procurement methods expected to be usedis given below and a time schedule for the various steps of procurement isshown in Annex 3-2.

- 17 -

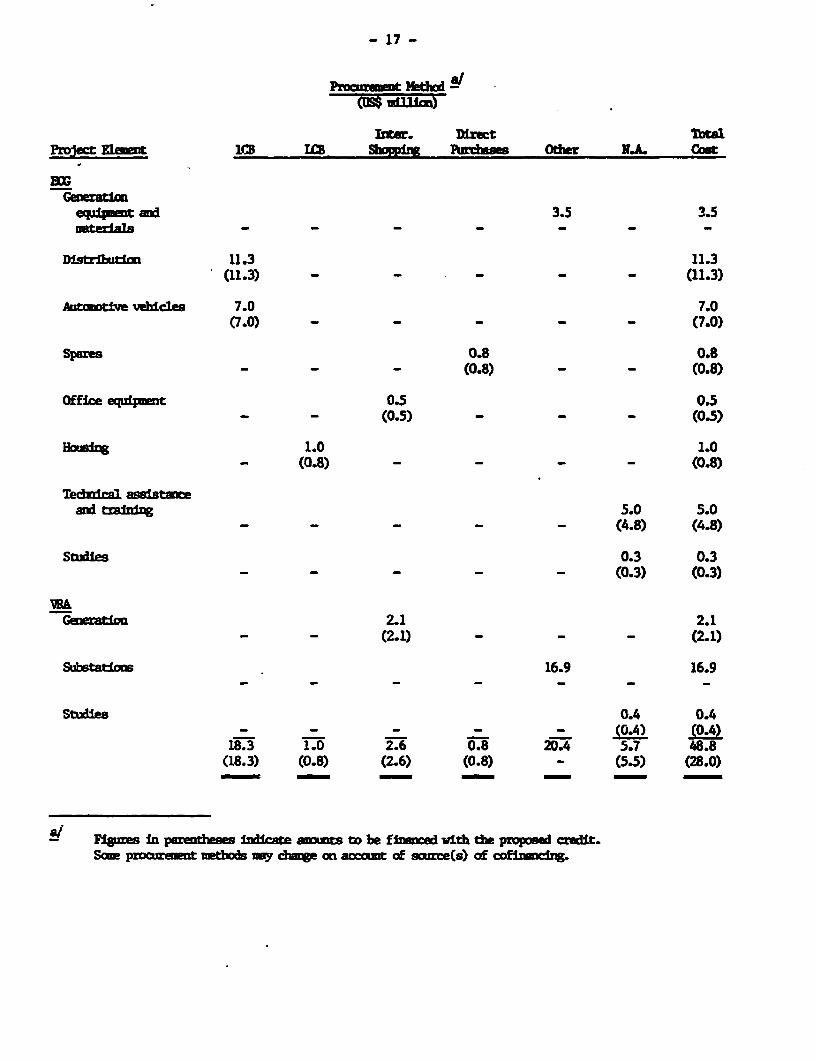

Proart Nt(t1$ ui

Inter. Dirct TbtelProject E.ent 11:1 IQ pSxt Pewdis Other NJL Coat

equ1pt an 3.5 3.5aterial - - -_

Disriti 11.3 11.3(11.3) - - _ _ _ (11.3)

AhvtiVe vebidls 7.0 7.0(7.0) - - - - - (7.0)

Spares 0.8 0.8- - - (0.8) - - (0.8)

Office enur[mt 0.5 0.5= - (0.5) - - - (0.5)

Houizg 1.0 1.0- (0.8) - - - - (0.8)

Tedmica1 a8stuieand traini 5.0 5.0

- - - - - (4.8) (4.8)

Stlial 0.3 0.3_ _ - - - (0.3) (0.3)

INAGoierat1on 2.1 2.1

- - (2.1) _ _ _ (2.1)

Substati= 16.9 16.9

Sties 0.4 0.4- - - - - (0.4) (0.4)

18.3 1.0 2.6 0.8 20.4 5.7 48.8(18.3) (0.8) (2.6) (0.8) - (5.5) (28.0)

a/ F1gLires in pid s diae mts to be fined ith the propsed credit.Scm pcuremnt tbods uuy dhwge on accmt of swume(s) of cofizdrg.

- 18 -

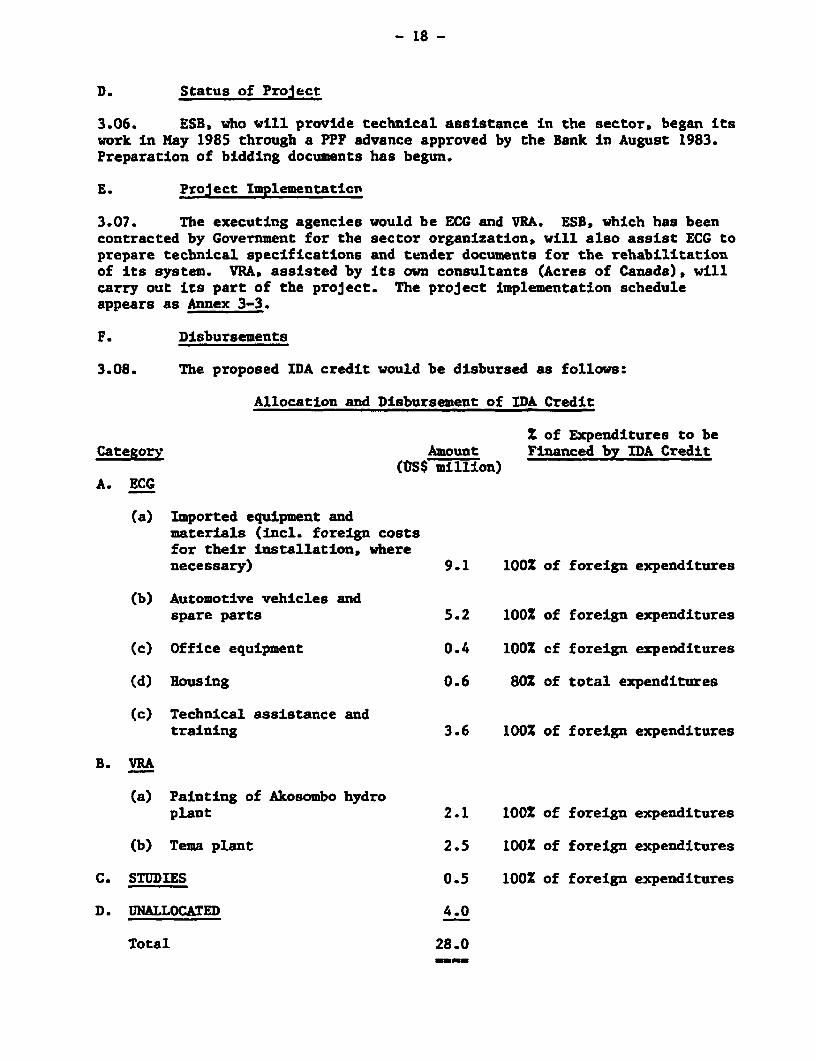

D. Status of ProJect

3.06. ESB, who will provide technical assistance in the sector, began itswork in May 1985 through a PPF advance approved by the Bank in August 1983.Preparation of bidding documents has begun.

E. Project ImplementatioT

3.07. The executing agencies would be ECG and VRA. ESB, which has beencontracted by Government for the sector organization, will also assist ECG toprepare technical specifications and tender documents for the rehabilitationof its system. VRA, assisted by its own consultants (Acres of Canada), willcarry out its part of the project. The project implementation scheduleappears as Annex 3-3.

F. Disbursements

3.08. The proposed IDA credit would be disbursed as follows:

Allocation and Disbursement of IDA Credit

Z of Expenditures to beCategorab Amount Financed by IDA Credit

(tS$ million)A. ECG

(a) Imported equipment andmaterials (incl. foreign costsfor their installation, wherenecessary) 9.1 100% of foreign expenditures

(b) Automotive vehicles andspare parts 5.2 1002 of foreign expenditures

(c) Office equipment 0.4 100X cf foreign expenditures

(d) Housing 0.6 80% of total expenditures

(c) Technical assistance andtraining 3.6 100Z of foreign expenditures

B. VRA

(a) Painting of Akosombo hydroplant 2.1 100% of foreign expenditures

(b) Tema plant 2.5 100% of foreign expenditures

C. STUDIES 0.5 10O2 of foreign expenditures

D. UNALLOCATED 4.0

Total 28.0

- 19 -

3.09. The estimated schedule of disbursements is based on the SectoralDisbursements Profile in West Africa and is shown in Annex 3-4. Arrangementsto establish a-Special Account, to be maintained in foreign currency in acommercial bank, were agreed during negotiations. Withdrawals will be madeagainst full documentation, with the exception of contracts of less thanUS$ 10,000 equivalent and training overseas; reimbursement for expenditureswill be made on the basis of statements of expenditures (SOEs) for -whichsupporting documentation will be retained by the implementing agenciesconcerned. Amoxnis withdrawn on the basis of SOEs will be subject to specialauditing arrangements, including a separate opinion covering the use of thesefunds.

G. Environment

3.10. The project is not expected to produce any adverse environmentaleffects.

IV. FINANCIAL ANALYSIS

A. Past Finances

1. Backround

4.01. ECG's charter mandates it to operate commercially and to setelectricity charges at levels sufficient to cover annual operating costs, debtservicing requirements, fund a reasonable proportion of its expansion programand contribute to reserves. According to its charter, VRA has to operatecommercially and make profits. The actual financial performance of Ghana'spower sector in recent years must be seen in context with the deterioration ofthe economy, the drought that has affected Ghana since 1981 and the economicmeasures (Economic Recovery Program) undertaken since April 1983.

4.02. The deterioration of the economy has adversely affected thefinancial position of the sector as high inflation produced cost increaseswhich were not offset by timely and adequate rate Increases; industrial demandfor electricity declined and the sector lacked needed foreign exchange.Simultaneously, the drought has reduced hydroelectric generation, furtherrestricting sector revenues, particularly foreign exchange earniugs. As partof the Economic Recovery Program, Government devalued the Cedi by 11 times inOctober 1983, and by a further 60% in several stages in 1984. The Cedidevaluations resulted in additional cost increases and made critical thesector's financial position. To remedy this situation Government increasedelectricity rates by about 500% in 1984, and authorized further increases ofabout 20% for 1985, and about 15% for 1986. These measures, which were takenin the most adverse circumstances, are expected to put the sector on e soundfinancial footing.

4.03. The consequences of the economic measures are still rippling throughthe economy and make the analysis of data and their projection difficult. Inaddition, ECG's information is scant, inaccurate and tardy.

- 20 -

2. Past Earnings

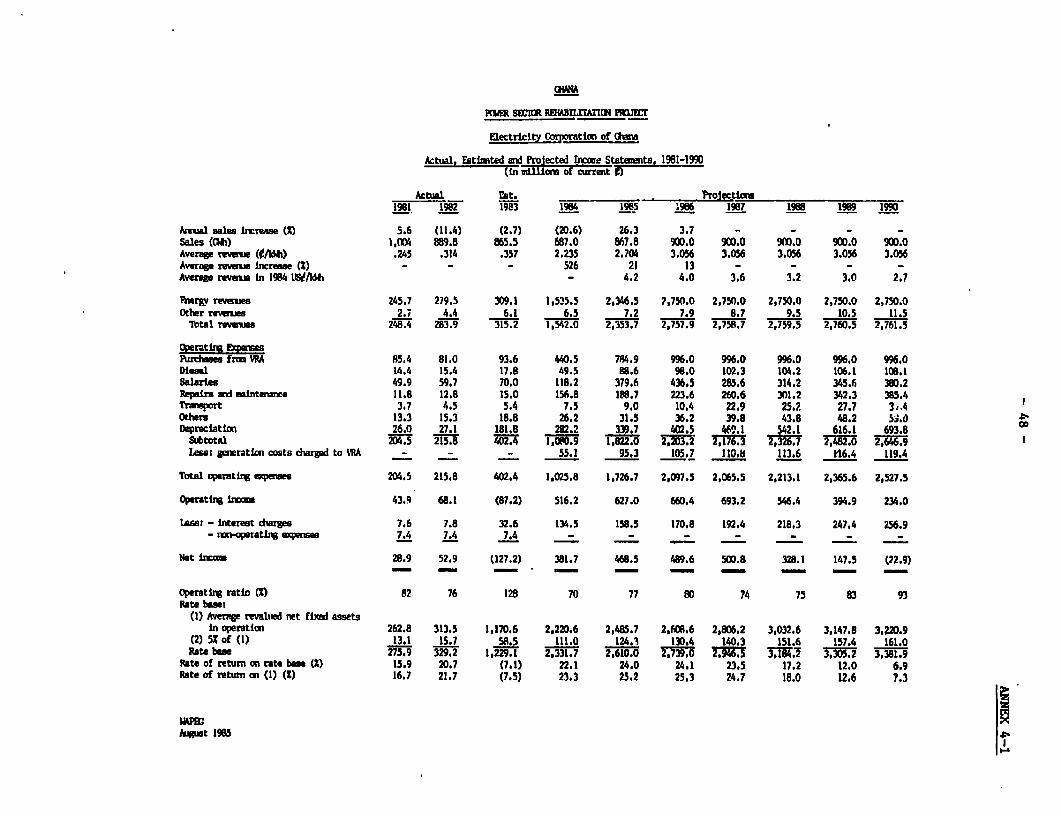

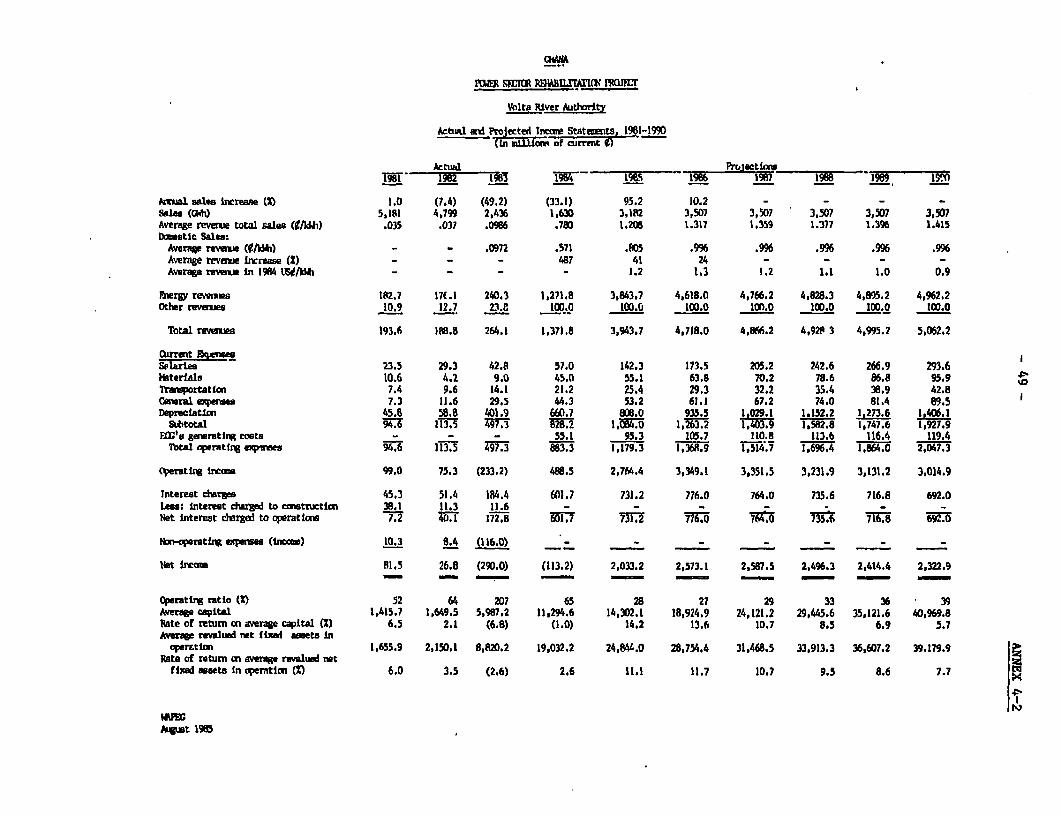

4.04. Detailed Income Statements for ECG are shown in Annex 4-1.and forVRA in Annex 4-2; the table below summarizes their earnings over the period1981-1984:

Gand VRA - Past Frnrs 1961-M14(in mffIi-i O

BOG - ~~~~~VRAEst. Est.

FIscal Year 1981 1982 1983 1984 1981 1982 1983 1984

Sales (GWh) 1,004 890 866 687 5,181 4,799 2,436 1,63D

Average reva3m (t/Ib) .245 .314 .357 2.235 .035 .037 .099 .780

Totalreverms 248 284 315 1,542 194 189 264 1,372

Total expenes 22D 231 442 1,160 112 162 554 1.485

Net inxcme 28 53 (127) 382 82 27 (290) (113)

Ope Elrig ratio 82 76 128 70 52 64 207 65

Revalued rate b bs 2-76 329 1,229 2.332 1,416 1.650 5,987 11,295

Rate of returX C/

-nralued ratebase - 15.9 20.7 (7.1) 22.1 6.5 2.1 (6.8) (1.0)

Average revalued met fi Ldassets in operation 263 314 1,171 2.221 1.656 2,150 8,820 19,032

Rate of return o average revahednet fixed assets in operatim 16.7 21.7 (7.5) 23.3 6.0 3.5 (2.6) 2.6

Incbzles interest dhages and non-perating annde losses.

or FbOG, rate base is the sun of average revaled net fixed assets in peration plus 5% on it aswoking capital allcumce. Revalued assets are uissim estimtes, dbich may be uiderstated(para. 4.08). For VRA, rate base is average capital (equity, retaied earnings and revaluation reserve).

-/ F¢or EG, the rate of retumn is dbtaied by dividing net qprating inore by the rate base. For VEA, therate of return is obtaied by dividing net inccoe by the rate base.

Credit 689-GE and Loan 1381-GE earnings covenant requires ECG to earn a rateof return equivalent to 6.2% of its rate base (average revalued net fixedassets in operation plus 5% working capital allowance). Following two years

- 21 -

(1981 and 1982) of excellent earnings provided by substantial rate increases(183Z for 1981-1982), ECG did not cover its costs in 1983. In 1983, theGovernment granted ECG rate increases which yielded a 14% increase in itsrevenue while the utility's total costs (including interest charges) increasedby about 92%, mostly as a result of the devaluatic-: of the currency. The 500%rate increase granted to ECG in 1984 is expected to have produced again a veryhigh return; more than 20%.

4.05. Loan 1380-GH requires VRA to earn a rate of return equivalent to7.3% of average owner's equity (net income over average equity). VRA'searnings in 1981 were close to those required by Loan 1380-GH but deterioratedsteadily as a result of the drought until they bottomed out in 1983. In1981-1982 the Government authorized VRA rate increases of about 68% to itsdomestic consumers and VRA was able to increase the price on its exports toCEB by about 48%, while the utility's operating costs increased by about 47%.In 1983, the 15% rate increases granted VRA on its domestic sales andincreases in the Cedi equivalent of its exports - resulting from the Cedidevaluation - were much lower than the 240% increase in its total costs. The1984 hefty rate increases approved by the Government are expected to haveresulted still in a negative return figure on average capital but with a clearimproving trend.

3. Financing Performance

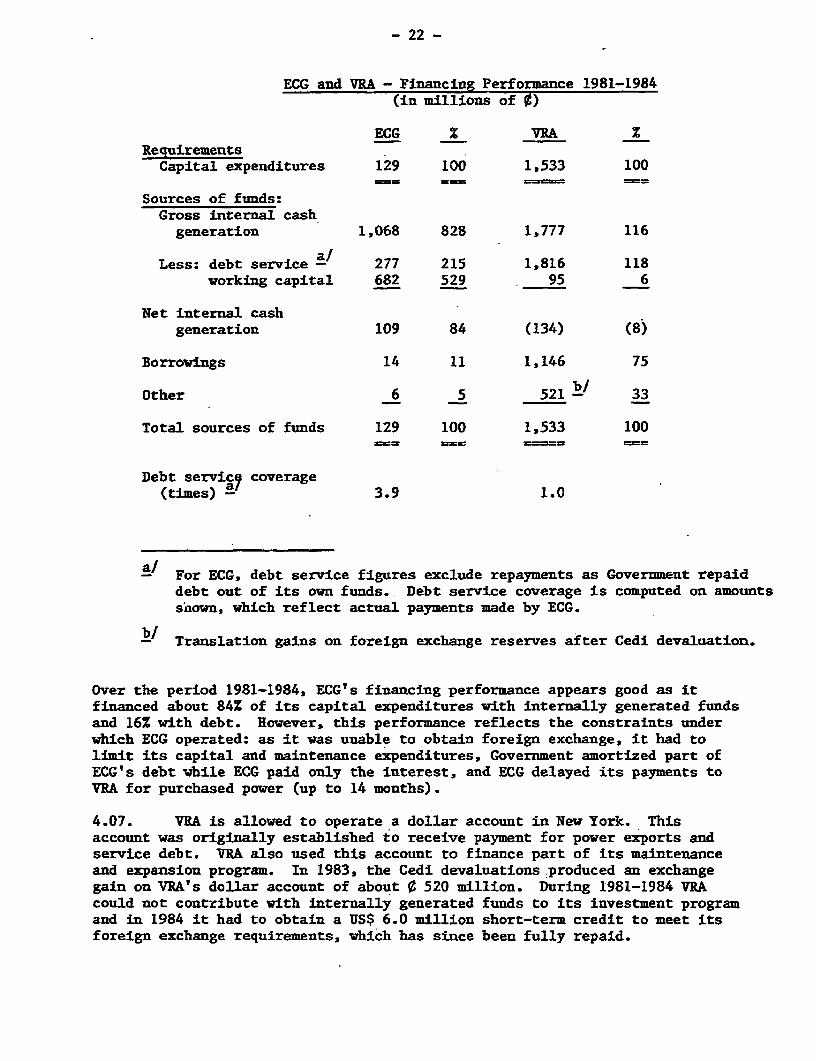

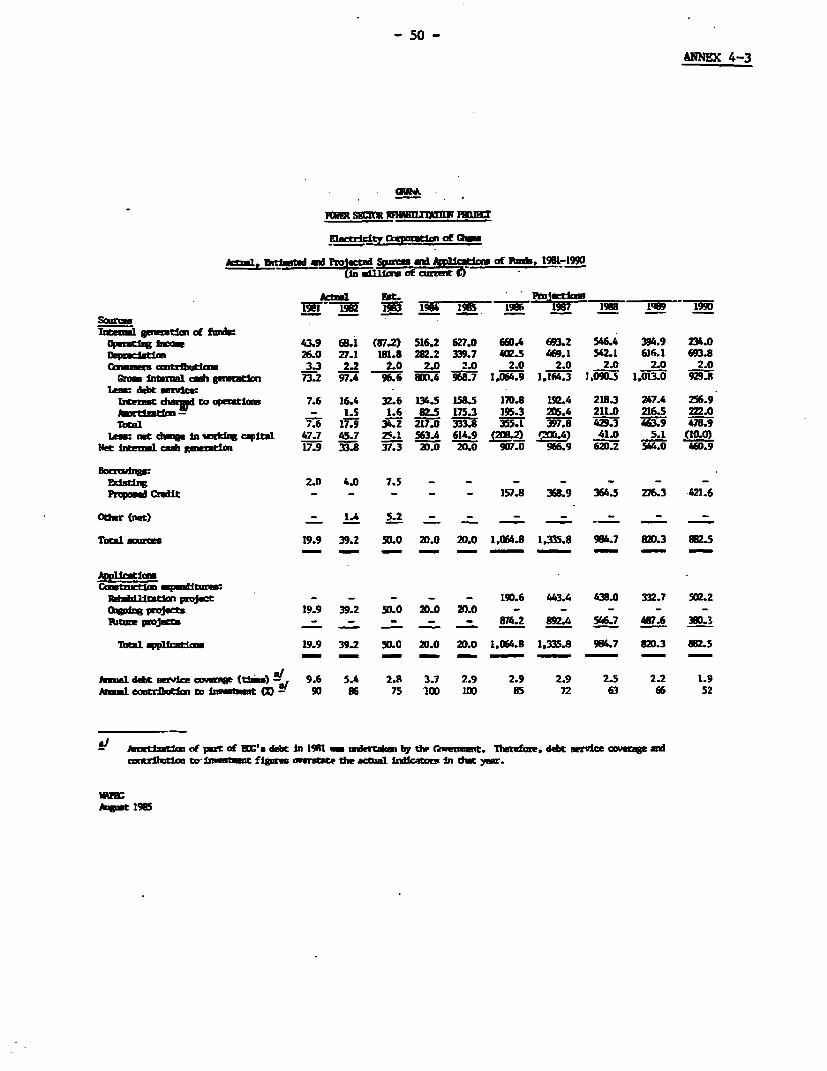

4.06. Detailed Sources and Applications of Funds Statements for ECG (since1981) are shown in Annex 4-3 and for VRA in Annex 4-4 and summarized asfollows:

- 22 -

ECG and VRA - Financing Performance 1981-1984(in millions of 0)

ECG % VRA ZRequirementsCapital expenditures 129 100 1,533 100

Sources of funds:Gross internal cash

generation 1,068 828 1,777 116

Less: debt service a/ 277 215 1,816 118working capital 682 529 95 6

Net internal cashgeneration 109 84 (134) (8)

Borrowings 14 11 1,146 75

Other 6 5 5 2 1 k' 33

Total sources of funds 129 100 1.533 100

Debt servic 7 coverage(times) - 3.9 1.0

-/ For ECG, debt service figures exclude repayments as Government repaiddebt out of its own funds. Debt service coverage is computed on amountssLnown, which reflect actual payments made by ECG.

b/ Translation gains on foreign exchange reserves after Cedi devaluation.

Over the period 1981-1984, ECG's financing performance appears goad as itfinanced about 84Z of its capital expenditures with internally generated fundsand 16Z with debt. However, this performance reflects the constraints underwhich ECG operated: as it was unable to obtain foreign exchange, it had tolimit its capital and maintenance expenditures, Government amortized part ofECG's debt while ECG paid only the interest, and ECG delayed its payments toVRA for purchased power (up to 14 months).

4.07. VRA is allowed to operate a dollar account in New York. Thisaccount was originally established to receive payment for power exports andservice debt. VRA also used this account to finance part of its maintenanceand expansion program. In 1983, the Cedi devaluations produced an exchangegain on VRA's dollar account of about ¢ 520 million. During 1981-1984 VRAcould not contribute with internally generated funds to its investment programand in 1984 it had to obtain a US$ 6.0 million short-term credit to meet itsforeign exchange requirements, which has since been fully repaid.

- 23 -

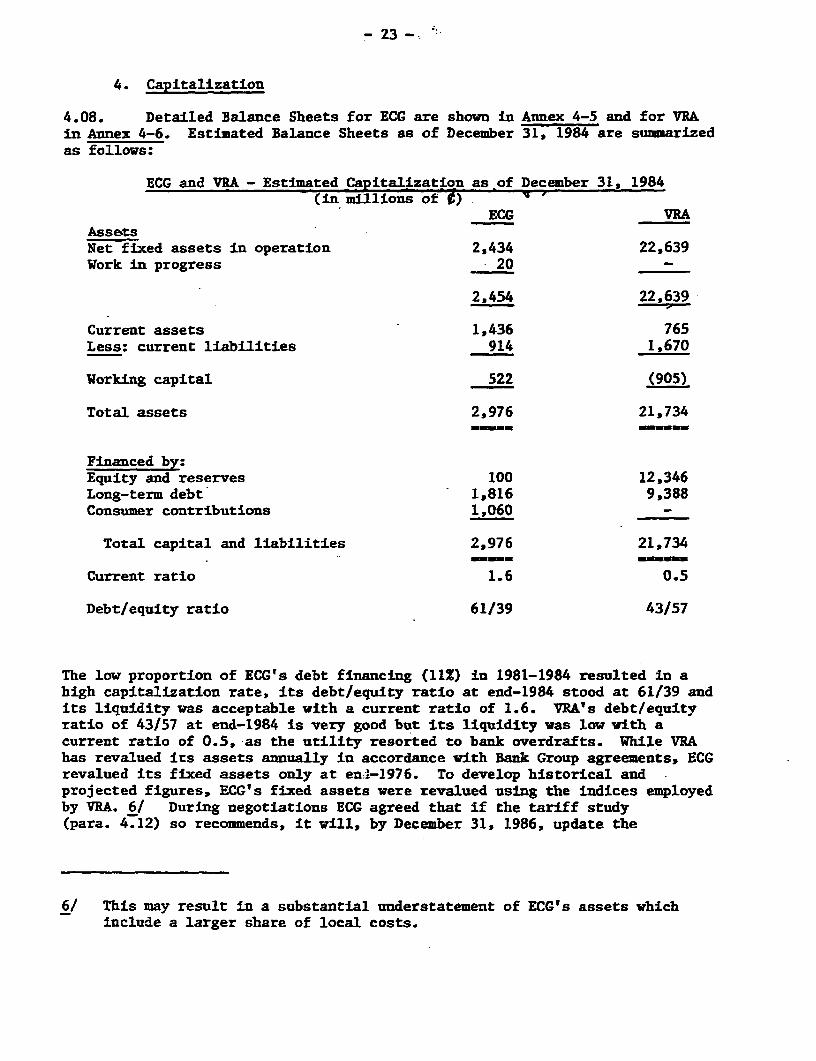

4. Capitalization

4.08. Detailed Balance Sheets for ECG are shown in Annex 4-5 and for VRAin Annex 4-6. Estimated Balance Sheets as of December 31, 1984 are summarizedas follows:

ECG and VRA - Estimated Capitalization as of December 31, 1984(in millions of 0 )

ECG VRAAssetsNet fixed assets in operation 2,434 22,639Work in progress - 20 -

2,454 22,639

Current assets 1,436 765Less: current liabilities 914 1,670

Working capital 522 (905)

Total assets 2,976 21,734

Financed by:Equity and reserves 100 12,346Long-term debt 1,816 9,388Consumer contributions 1,060 -

Total capital and liabilities 2,976 21,734

Current ratio 1.6 0.5

Debt/equity ratio 61/39 43/57

The low proportion of ECG's debt financing (11%) in 1981-1984 resulted in ahigh capitalization rate, its debt/equity ratio at end-1984 stood at 61/39 andits liquidity was acceptable with a current ratio of 1.6. VRA's debt/equityratio of 43/57 at end-1984 is very good but its liquidity was low with acurrent ratio of 0.5, as the utility resorted to bank overdrafts. While VRAhas revalued irs assets annually in accordance with Bank Group agreements, ECGrevalued its fixed assets only at en'-1976. To develop historical andprojected figures, ECG's fixed assets were revalued using the indices employedby VRA. 6/ During negotiations ECG agreed that if the tariff study(para. 4.12) so recommends, it will, by December 31, 1986, update the

6/ This may result in a substantial understatement of ECG's assets whichinclude a larger share of local costs.

- 24 -

revaluation of its assets to 1985 and will continue to revalue them every yearthereafter. VRA will continue to revalue its assets every year.

B. Billing and CollectionB. ~~~~~~~~~~~~~P

4.09. ECG has serious billing and collection problems. Receivables haverisen from almost 6 months billing in 1978 to 11 months by 1983. ESB, underproject financing, is assisting in improving ECG's billing and collection toreduce receivables to no more than 3 months billing by end-1987. On the otherhand, VRA's main collection problem has been ECG's overdues (para. 4.06). Itis expected that VRA would be able to reduce its receivables to 2 monthsbilling by end-1986 as ECG's finances improve and ECG pays its overdues. Amajor reason for ECG's overdues to VRA (over C 450 million) is ECG'sreceivableb from Government and parastatals (Government overdues stand atabout e 200 million and the Water and Sewerage Corporation's at about C 250million). Government is now paying its overdues under a plan agreed with ECG.To ensure that this plan is carried out in a timely manner, it was agreedduring negotiations that ECC will improve its collections so that byDecember 31, 1986, it will have no more than 120 days of billing outstandingand by December 31, 1987, and thereafter, no more than 90 days of billing.During negotiations it was also agreed that interlocking overdues amongGovernment, ECG and VRA will be settled not later than December 31, 1986.

C. Tariffs

1. Present Arrangements

4.10. Both ECG and VRA request rate increases to the MFP. After theproposal has been reviewed by X4EB, MEP makes a final decision on behalf ofGovernment. ECG's tariffs comprise demand and energy charges 7/ forcommercial and industrial customers. Its average selling price by end-1984was 9/kWh 2.235 or USi/kWh 4.47. 8/ Despite the recent rate increasesGhana's average revenue per kWh at the retail level is low compared to mostother West African countries (in USI/kWh: Benin: 14; Togo: 12; Ivory Coast:10; Senegal: 11; Burkina: 19), which reflects primarily Ghana's cheap hydrogeneration. VRA's tariffs are also two-part, comprising demand and energycharges. VRA's power sales to VALCO are now billed at over USJ 1 per kWh(para. 1.21). The price of VRA sales to CEB is USJ 4 per kWh from April 1,1985 to March 31, 1988, when it is scheduled to be renegotiated. The pricecurrently charged Ivory Coast is USi 4 per kWh but a long-term contract hasnot yet been agreed. VRA's total estimated average revenue for 1984 was

7/ Energy charge is that portion of the billed charge for electric servicewhich is based upon the elec.ric energy (kilowatt-hours) supplied; demandcharge is the portion of the billed charge which is based on billingdemand (power, which is measured in kilowatts).

8/ Cedis 50.0 = US$ 1.00.

- 25 -

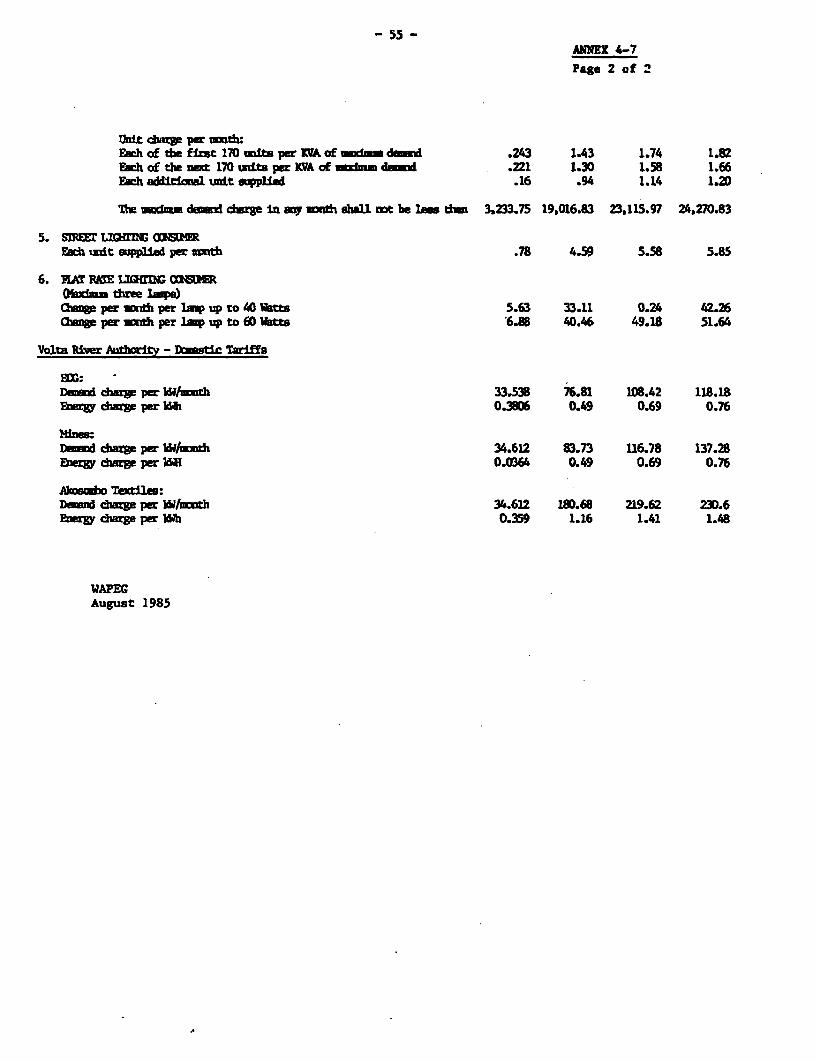

9 0.78/kWh or USi/kWh 1.56 and its average cost ¢ 0.54/kWh or USi 1.1. 9/Annex 4-7 shows ECG's and VRA's domestic rate schedule.

4.11. ECG used to bear all diesel generation costs of the provincialstations, which it passed to consumers through a standard rate schedule. Toensure equity in sharing generation costs among all consumers, ECG hasrecently been authorized to charge all generation costs to VRA, who passesthem on to all domestic consumers at the bulk level, including ECG. However,the procedure for computing these charges is not yet finalized. Furthermore,to ensure that additional costs will be passed on to consumers on time, bothECG and VRA should incorporate fuel and bulk power cost adjustment clauses intheir tariff schedules and power supply contracts. During negotiations,Government, ECG and VRA agreed to confirm a procedure for computing andinvoicing ECG's generation costs to VRA for recovery in the charges to allbulk power consumers and agreed that ECG and VRA would incorporate fuel andbulk power cost adjustment clauses in their tariff schedules and power supplycontracts under procedures to be agreed with IDA.

2. Future Tariffs

4.12. Now that the Acres generation planning has been completed, sectortariffs should be examined. During negotiations, ECG and VRA agreed that theywill hire consultants, to be financed by the proposed credit, to carry out astudy of the sector tariffs and to discuss with IDA the findings of such a.study. This study will, among others, recommend an appropriate financial goalfor the sector. On the basis of such study. Government and IDA will agree onthe criteria and schedule for adjusting electricity rates. The study will setelectricity prices after consideration of the long-run marginal cost (LRMC,currently estimated at between USi 5 and 6 per kWh at the generation level),and a level sufficient to cover costs, service debt and make an adequatecontribution to expansion program. The revised agreement between VALCO andVRA provides flexibility to supply domestic markets for the foreseeable futurewith low cost power from Akosombo. Tariffs based on LRMC may tlus providelarge surpluses. The study will also make recommendations on the allocationof surpluses between retention at the utilities or payment of dividends. Thefinal results of the study should be available for discussion with IDA bymid-1986.

D. Financing Plan

4.13. The financial projections take into account the rate increasesalready allowed by Government (para. 4.02), and rates were assumed to remainunchanged at their 1986 level until 1990. VRA prices on its exports ofelectricity were kept constant throughout 1985-1990. VRA sales to VALCO wereconservatively valued at the minimum selling price of USJ 1 per kWh. ECG andVRA tentative investment plans are shown in para. 1.11. ECG's and VRA's

91 This cost is an inflated estimate due to the reduced sales that resultedfrom the drought.

- 26 -

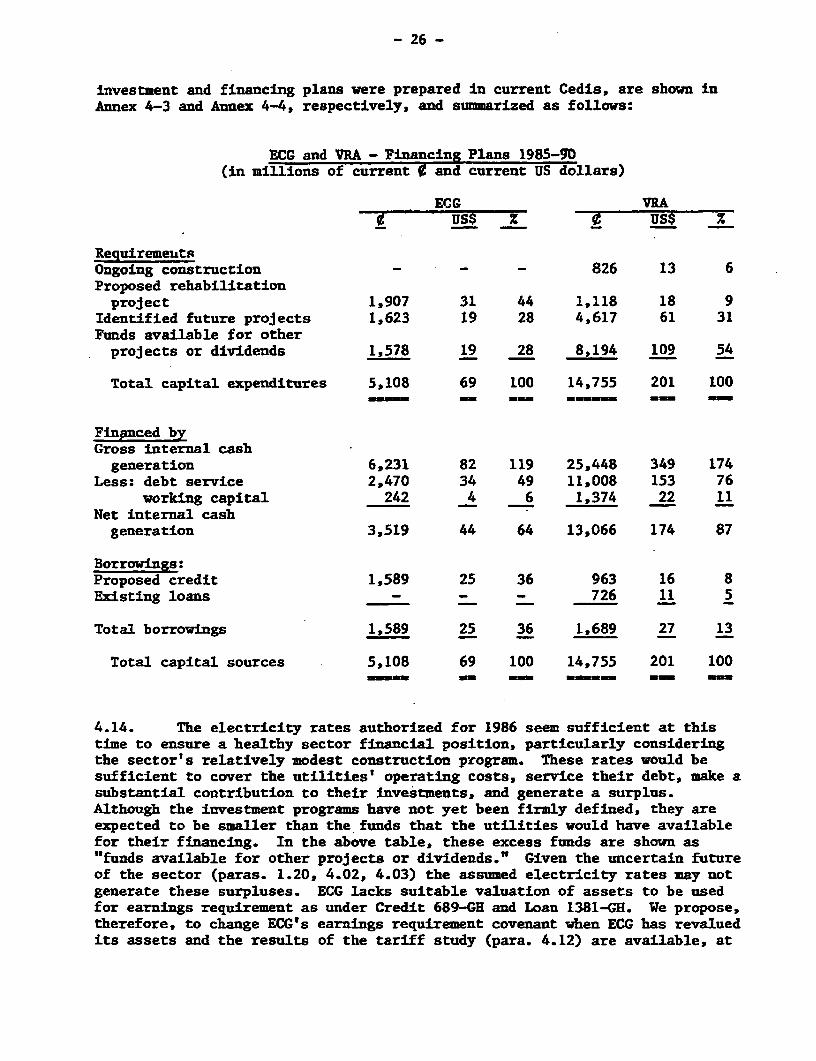

investment and financing plans were prepared in current Cedis, are shown inAnnex 4-3 and Annex 4-4, respectively, and summarized as follows:

ECG and VRA - Financing Plans 1985-90(in millions of current ¢ and current US dollars)

ECG VRAUS$ % ¢ USS z

RequiremeutsOngoing construction - - - 826 13 6Proposed rehabilitationproject 1,907 31 44 1,118 18 9

Identified future projects 1,623 19 28 4,617 61 31Funds available for otherprojects or dividends 1,578 19 28 8,194 109 54

Total capital expenditures 5,108 69 100 14,755 201 100

Financed byGross internal cashgeneration 6,231 82 119 25,448 349 174

Less: debt service 2,470 34 49 11,008 153 76working capital 242 4 6 1,374 22 11

Net internal cashgeneration 3,519 44 64 13,066 174 87

Borrowings:Proposed credit 1,589 25 36 963 16 8Existing loans - - - 726 11 5

Total borrowings 1,589 25 36 1,689 27 13

Total capital sources 5,108 69 100 14,755 201 100

4.14. The electricity rates authorized for 1986 seem sufficient at thistime to ensure a healthy sector financial position, particularly consideringthe sector's relatively modest construction program. These rates would besufficient to cover the utilities' operating costs, service their debt, make asubstantial contribution to their investments, and generate a surplus.Although the investment programs have not yet been firmly defined, they areexpected to be smaller than the funds that the utilities would have availablefor their financing. In the above table, these excess funds are shown as"funds available for other projects or dividends." Given the uncertain futureof the sector (paras. 1.20, 4.02, 4.03) the assumed electricity rates may notgenerate these surpluses. ECG lacks suitable valuation of assets to be usedfor earnings requirement as under Credit 689-GH and Loan 1381-GH. We propose,therefore, to change ECG's earnings requirement covenant when ECG has revaluedits assets and the results of the tariff study (para. 4.12) are available, at

- 27 -

which time the covenant would.be reviewed. Likewise, we propose to changeVRA's earnings requirement until the results of the tariff study areavailable. Although VRA's earningF requirement (para. 4.05) has worked wellin the past, it may not-be effective over the'next years if rains do notreturn to normal. Consequently, during negotiations, Government, ECG, and VRAagreed that:

(a) pending the results of the tariff study, ECG's and VRA'sdomestic rates would be reviewed annually and adjusted asnecessary to ensure that they would be the higher of either therates approved to be in effect by January 1, 1986 or sufficientto produce revenues to cover operating expenses, debt service,and working capital and produce a contribution to investment ofnot less than 25Z; and

(b) after completion of the tariff study, but not later thanJune 30, 1986, Government, the power entities, and IDA willagree on a financial objective and review the provision onearnings requirements.

4.15. Under the above conditions, in 1985-1990 ECG and VRA would not needborrowings other than the proposed Credit and cofinanced loan, and VRA woulddrawdown the remaining funds on existing loans (mostly contractors' andsuppliers' credits) to finance its ongoing construction program.

E. Future Finances

4.16. Under the above assumptions, the finances of ECG and VIA areimproving, as highlighted in the following table:

- 28 -

BOG axd WA - HiliAt:s of Fautre Pines 1985-1990(in CUrrent terni unless otherWIe noted)

BCG_ WA1_qa 1986 1987 1988 1989 1990 1985 1986 1987 1968 1989 1990

Sales (CWh) 868 900 900 900 900 900 3,182 3,507 3.507 3.507 3.507 3.507Average revenue (KWMh) 2.7 3.1 3.1 3.1 3.1 3.1 1.2 1.3 1.4 1.4 1.4 1.4Average.revenue (1984 UEU/kWh) - 4.2 4.0 3.6 3.2 3.0 2.7 1.2 1.3 1.2 1.1 1.0 0.9

Total revenues (i ndULni) b/ 2.354 2.758 2,759 2.760 2,761 2,762 3.944 4,718 4.866 4,928 4.995 5.062Total xipenses (O udUlm) - 1,885 2.268 2,258 2.432 2,613 2,785 1.911 2,145 2,279 2,432 2.581 2.739Net Inn ( mUllion) 469 490 501 328 148 (23) 2,033 2,573 2,587 2,496 2,414 2,323

Operating ratio (Z) 77 80 74 75 83 93 28 27 29 33 36 39Debt/equity ratio 59/41 53/47 48/52 46/54 44/56 44/56 41/59 36/64 31/69 26/74 22W78 18/82Debt service coverage (tims) 2.9 2.9 2.9 2.5 2.2 1.9 2.0 2.1 2.3 2.6 2.8 3.3ChrrTnt ratio 2.8 3.0 2.4 2.4 2.2 1.7 1.4 1.4 1.4 1.4 1.4 1.4Annul contribution c

to investment (Z) 10D 85 72 63 66 52 20 89 91 91 94 94Rate of return on average revalued

net fixBd assets in operatio (Z) 25 25 25 18 13 7 11 12 11 10 9 8

y Dazstic revenue aly.

b T1.04 interest dge.

Deffmd as net internal cash generation (operatng iTcoue plus depreciatmo and cQamr ctntrhtimzsless debt serie and net change in working capital) as proportimo of constctixm epesnditures includinginterest durig coritrutia.

4.17. ECG's capitalization would further improve to a debt/equityratio of around 45/55. In 1985-1987 some of ECG's financial indicatorsare higm:: contribution to investment is high because ECG's investmentexpenditures are kept to a minimum; the rate of return may beoverestimated because of possible undervaluation of ECG's assets. ECG'sfinancial indicators reach more normal levels in the later years; thus,by the end of the period, its annual debt service coverage ratio wouldbe around the acceptable level of 2 times, its annual contribution toconstruction would be higher than 50% and its liquidity would improve sothat its current ratio would be around 2, which is acceptable. VRA isalso expected to further improve its capitalization (debt/equity ratioof 26/74 by 1988), its annual debt service coverage would be higher than2 times and its liquidity would improve and reach acceptable levels in1985 (current ratio of 1.4, which is acceptable).

4.18. Although the financial projections show an improving trend forthe two utilities, it is prudent to maintain the utilities' expansionprograms under review. Therefore, during negotiations, it was agreedwith Government and the utilities that no major investments in the

- 29 -

sector (defined as those totalling US$ 25 million for the sector duringthe project period) would be carried out unless they are technically,economically and financially sound and satisfactory to IDA. Under lowrainfall conditions, VRA's foreign exchange deficit may continue andreach US$ 8-9 million by end-1986. If this shortage materialized, VRAexpects to cover it with short-term loans. During negotiations, ECG andVRA agreed that they would not incur long-term borrowings (andshort-term borrowings could not exceed 10% of cash operating expenses)without IDA's concurrence if forecast net revenues covered their maximumfuture debt service requirement (including the debt proposed to beincurred) less than 1.5 times.

V. PROJECT JUSTIFICATION

A. Background

5.01. Reliable public service electricity supply is vital to Ghana'seconomic recovery because of the increased dependence of mining andsmelting and other export-oriented industries in the public system andthe needs of agriculture and wood processing for reliable and economicelectricity. While the project would not involve system expansion itwould provide reliability in the infrastructure necessary for suchservice.

5.02. The purpose of the project is to restore reliable electricservice by overcoming the most serious operating problems existing inthe coastal grid and various isolated systems owing to inadequatemaintenance since the late 70's. These operating problems encompasssystem overloads with concomitant energy losses and voltage reductions,curtailment of service because of frequent outages of old thermalgenerating equipment (particularly in isolated systems) and frequentbreakdown of transportation equipment, which not only involve highmaintenance costs but also totally disrupts ECG's maintenance andoperation schedules. Since most of Ghana's industry relies onpublic-service electricity supply, the value of reliable supply to thenation's economy is very high. The justification of the project is toprovide the electrical facilities with the elements of reliabilitynecessary to render effective support to economic recovery of thecountry.

B. Least-Cost Solution