Embed Size (px)

Citation preview

Document o f The World Bank

____

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. I t s contents may not otherwise be disclosed without World Bank authorization.

FOR OFFICIAL USE ONLY

Report No. 29905-ID

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED LOAN

IN THE AMOUNT OF US$SO MILLION

TO THE

REPUBLIC OF INDONESIA

FOR A

DOMESTIC GAS MARKET DEVELOPMENT PROJECT

November 10,2005

Energy and Min ing Development Sector Unit Infrastructure Unit East Asia and Pacific Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS (Exchange Rate Effective - June 30,2004)

Currency unit = Indonesian Rupiah Rp. 8700 = US$1

FISCAL YEAR January 1 - December 3 1

ABBREVIATIONS AND ACRONYMS

AAA Analytical and advisory activity ADB Asian Development Bank AMDAL Analisis Mengenai Dampak Lingkungan Hidup

(Analysis o f Impacts on the Liv ing Environment)

bbl Barrel B P H MIGAS Badan Pengatur Hilir Minyak dan Gas

(Oil and Gas Downstream Regulatory Body) BPK Supreme Audit Board CAS Country Assistance Strategy CFAA Country Financial Accountability Assessment CNG Compressed natural gas COZe Carbon dioxide equivalent ComDev Community development CQS CR Current ratio D O Development objective DSCR Debt service coverage ratio ECO Enviroilmental coordinating office EIAR Environmental impact assessment report EIB European Investment Bank EIRR EMP Environmental Management Plan EO1 Expression o f Interest EPC Engineering, procurement, and construction FMR Financial monitoring report FO Fuel o i l FY Fiscal year GO1 Government o f Indonesia GPN General Procurement Notice IBRD International Bank for Reconstruction and

Development ICB International Competitive Bidding IFC International Finance Corporation IP Implementation progress IPO Initial public offering

Selection Based on Consultants' Qualifications

Economic internal rate o f return

I T JBIC km KPKN LPG mmBtu mmcfd M O E NCB NGO NPV O&M PDO PGN PIU P M C PSC QBS QCBS RFP ROR

RVP SBD SBU SCADA SFR SO2 SPN TA tcf TGI TOR TSP VAT

RP.

Information technology Japan Bank for International Cooperation Kilometer National Treasury Offices Liquefied petroleum gas Mi l l ion British thermal unit Mi l l ion cubic feet per day (gas) Ministry o f the Environment National competitive bidding Nongovernmental organization Net present value Operation and maintenance Project development objective PT Perusahaan Gas Negara (Persero) Tbk Project implementation unit Project management consultant Production-sharing contract Quality-Based Selection Quality- and Cost-Based Selection Request for Proposal Rate o f return Indonesian rupiah Regional Vice President Standard Bidding Documents Strategic Business Unit Supervisory Control and Data Acquisition Self- financing'ratio Sulfur dioxide Special Procurement Notice Technical assistance Tri l l ion cubic feet PT TRANSGASINDO Terms o f Reference Total suspended particulate Value added tax

Vice President: Jemal-ud-din Kassum Country Director: Andrew D. Steer

Task Team Leader: Noureddine Berrah Sector Manager: Junhui Wu

A .

B .

C .

D .

INDONESIA

Domestic Gas Market Development Project

CONTENTS

STRATEGIC CONTEXT AND RATIONALE ............................................................. 1 1 . COUNTRY AND SECTOR ISSUES ....................................................................................... 1

2 . RATIONALE FOR BANK INVOLVEMENT ........................................................................... 3

3 . HIGHER LEVEL OBJECTIVES TO WHICH THE PROJECT CONTRIBUTES ............................... 3

PROJECT DESCRIPTION ............................................................................................. 4 1 . LENDING INSTRUMENT ................................................................................................... 4

2 . PROJECT DEVELOPMENT OBJECTIVE AND KEY INDICATORS ........................................... 4

3 . PROJECT COMPONENTS .................................................................................................. 4

4 . LESSONS LEARNED AND REFLECTED IN THE PROJECT DESIGN ......................................... 6

5 . ALTERNATIVES CONSIDERED AND REASONS FOR REJECTION .......................................... 6 IMPLEMENTATION ...................................................................................................... 7 1 . INSTITUTIONAL AND IMPLEMENTATION ARRANGEMENTS ............................................... 7

2 . MONITORING AND EVALUATION OF OUTCOMES/RESULTS .............................................. 7

3 . SUSTAINABILITY ............................................................................................................ 8

4 . 5 .

CRITICAL RISKS AND POSSIBLE CONTROVERSIAL ASPECTS ............................................. 8

LOAN~REDIT c ~ N D ~ T ~ ~ N S AND COVENANTS ................................................................. 9

APPRAISAL SUMMARY ............................................................................................. 11 1 . 2 . 3 . 4 . 5 . 6 . 7 . 8 .

ECONOMIC AND FINANCIAL ANALYSES ........................................................................ 11

FINANCIAL ANALYSIS .................................................................................................. 11

TECHNICAL .................................................................................................................. 12

FIDUCIARY ................................................................................................................... 12

SOCIAL ......................................................................................................................... 13

ENVIRONMENT ............................................................................................................. 14

SAFEGUARD POLICIES .................................................................................................. 15 POLICY EXCEPTIONS AND READWESS .......................................................................... 15

FOR OFFIcI[AE USE ONLY

This document has a rest r ic ted distribution and may be used by recipients only in the performance of their official duties. I t s contents may not be otherwise disclosed without Wor ld Bank authorization.

ANNEXES

Annex 1:

Annex 2:

Annex 3:

Annex 4:

Annex 5:

Annex 6:

Annex 7:

Annex 8:

Annex 8(A):

Annex 8(B):

Annex 9:

Annex 10:

Annex 11:

Annex 12:

Annex 13:

Annex 14:

Annex 15:

Country and Sector or Program Background ........................................................ 17

Major Related Projects Financed b y the Bank andor other Agencies ................. 20

Results Framework and Monitoring ..................................................................... 22

Detailed Project Description ................................................................................. 26

Project Costs ......................................................................................................... 34

Implementation Arrangements .............................................................................. 36

Financial Management and Disbursement Arrangements .................................... 40

Procurement Arrangements .................................................................................. 49

Clarifications Relating To National Competitive Bidding (NCB) Procedures ..... 54

An tic ormp ti on P1 an ............................................................................................... 56

Economic and Financial Analyses ........................................................................ 62

Safeguard Policy Issues ........................................................................................ 75

Project Preparation and Supervision ..................................................................... 89

Documents in the Project Fi le ............................................................................... 90

Statement o f Loans and Credits ............................................................................ 9 1

Country at a Glance .............................................................................................. 93

Maps ...................................................................................................................... 95

MAPS

1.

2 . 3 . 4 .

Overall Project Coverage and Other PGN Infrastructure

Map o f Greater Jakarta Zone (Zone 1)

Map o f Banten Zone (Zone 2)

Map o f Karawang Zone (Zone 3)

INDONESIA

FY 2006 Annual $ 5.0 Cumulative 5.0

DOMESTIC GAS MARKET DEVELOPMENT PROJECT

2007 2008 2009 2010 201 1 20.0 20.0 20.0 10.0 5.0 25.0 45.0 65.0 75.0 80.0

PROJECT APPRAISAL DOCUMENT

EAST ASIA AND PACIFIC

EASEG Date: November 10,2005 Country Director: Andrew D. Steer Sectors: Oil and gas (100%) Sector Manager: Junhui Wu Themes: State enterprise restructuring and

privatization (P); Infrastructure services for private sector development (S) ; Population management and environmental health ( S ) Environmental screening category: A

Team Leader: Noureddine Berrah

Project ID: PO77175

Lending Instrument: Specific Investment Loan Safeguard screening cateeorv: S2 Full Assessment

Y Y Y

Project Financing Data El Loan 0 Credit 0 Grant 0 Guarantee 0 Other:

For Loans/Credi ts/O thers : Total Bank financing (US$m.): 80.00

DEVELOPMENT ~ ~~ I I I

Total: 32.40 I 89.90 122.30

Borrower: Republic of Indonesia

Responsible Agency: PT Perusahaan Gas Negara (Persero) Tbk. J1. K.H. Zainul Arifin No. 20 Jakarta, Indonesia, 11 140 Tel: (6221) 633-4838 Fax: (6221) 633-3080

Project implementation period: 2006-20 1 1 Expected effectiveness date: March 3 1, 2006 Expected closing date: March 3 1, 201 1

Does the project depart from the CAS in content or other significant respects? Ref. PAD A.3

nYes No

Does the project require any exceptions f rom Bank policies? Ref. PAD D. 8 Have these been approved by Bank management? [s approval for any policy exception sought from the Board?

OYes H N o OYes UNO OYes UNO

MYes UNO Does the project include any critical r isks rated “substantial” or “high”? Ref. PAD C.4 Does the project meet the Regional criteria for readiness for implementation? Ref. PAD 0 . 8 H Y e s UNO

Project development objective Ref. PAD B.2, Technical Annex 3 Natural gas utilization expanded and air pollutant emissions reduced in West Java.

Project description Ref. PAD B.3.a, Technical Annex 4 The project comprises two components:(a) Distribution Infrastructure Expansion to increase gas use in West Java and (b) Capacity Building to upgrade PGN’s capabilities in management, infrastructure planning, marketing, distribution system safety and integrity management, etc.

Which safeguard policies are triggered, i f any? Ref. PAD 0.6, Technical Annex 10 Environmental Assessment (OP/BP/GP 4.01) i s triggered

Significant, non-standard conditions, if any, for: Ref. PAD C.5

Board presentation: None

Loadcredit effectiveness: Dissemination o f Financial Management Manual

Covenants applicable to project implementation: None

A. S T R A T E G I C CONTEXT AND R A T I O N A L E

1. Country and Sector Issues

1.1. Indonesia’s proved reserves o f natural gas, estimated at more than 2.5 tr i l l ion cubic meters (about 90 trillion cubic feet), are among the largest in the region. In 2003, gas production amounted to about 87 bi l l ion cubic meters (about 3 tr i l l ion cubic feet), o f which 58 percent was exported, mainly to countries in the region.’ However, gas consumption by power and small and medium size industries as proportion o f total energy consumption i s among the lowest in the region. Until recently, the laws and regulations governing the hydrocarbon sector sanctioned the dominance o f PT Pertamina’s (Persero) and PT Perusahaan Gas Negara (Persero) Tbk (PGN). They also allowed the government to interfere in the sector in ways that inhibited efficient operation and limited participation o f the private sector. Many o f the issues the sector faced under the previous legislative framework have been addressed by the 2001 Oil and Gas Law and the 2004 implementation rules and regulations. The law and regulations created an environment conducive to the removal o f the barriers to competition and private sector entry and to the development o f the gas sector and the domestic gas market. However, the sector i s s t i l l facing the fol lowing interrelated issues that hamper the rapid development o f a domestic gas market (see Annex 1 for details).

0 The structure of gas pricing in Indonesia i s distorted and results in inefficient resource allocation. The price of natural gas in the domestic market i s below i t s economic and market value reducing producers’ interest in developing this abundant resource for domestic use. The negative economic impact o f this inadequate pricing system i s compounded by the subsidized prices o f petroleum products. The implementation of the new Oil and Gas L a w i s proceeding slowly because of delayed issuance of the implementation regulations. The law has provided the basis for a progressive liberalization o f the gas market. However, i t s implementation has been slow because o f the delayed issuance o f the implementing rules and regulations. The Bank engaged the government on this pressing issue and the implementation regulations were enacted on October 18, 2004 paving the way for effective implementation o f the law. PGN is not fully prepared to operate in the emerging competitive gas market.

Under the new Oil and Gas Law, the three major segments o f the o i l and gas industry (production, transmission and distribution) w i l l be unbundled, open access to network services w i l l be allowed and eventually, a competitive gas market w i l l be developed. T o face these challenges, PGN i s planning for (a) further restructuring including strategic partnership with private sector to increasingly meet new investment requirements f rom i t s financial resources and standings, a major objective assigned to i t by the government; and (b) strengthening i t s management and operational practices and corporate governance to be ready to operate in the future competitive market.

0 Production-sharing contracts (PSCs) are not conducive to gas development. More than 90 percent o f Indonesia’s o i l and gas i s produced by the private sector, mostly by international o i l companies. Private sector investment in the sector i s almost totally governed by PSCs. The fiscal and nonfiscal terms o f Indonesia’s PSCs are mostly in l ine

0

0

’ Statistics of DG MIGAS, provided by PGN.

1

with international practice. However, many existing contracts s t i l l do not have provisions for gas discoveries and therefore no predictable basis for forecasting the value to the producers o f possible gas discoveries for domestic markets.

0 The transmission and distribution infrastructure i s underdeveloped. The country’s transmission and distribution infrastructure i s underdeveloped and constrains the development and expanded utilization o f this economically and environmentally attractive fuel. Progress toward a competitive gas market, as envisaged by the new Oil and Gas Law, requires further development o f gas transmission and distribution systems.

1.2. The broad objectives o f the Government o f Indonesia’s (GOI’s) policy to reform the energy sector are: (a) efficiency and reliability; (b) transparency and competition; (c) minimization of the use of public funds; and (d) environmental soundness. GOI’s strategy with respect to the above gas sector issues includes the following:

0 Phasing out of the subsidies and rationalization of energy prices. The prices o f petroleum products in Indonesia are heavily subsidized. Prior to the recent increase in o i l prices, the GO1 has implemented phased increases in fuel prices that led to a reduction in fuel subsidies and more rational energy product prices. Fol lowing a Presidential Decree in December 2002, the subsidies for al l products-with the exception o f kerosene-were to be fully eliminated b y the end o f 2004. However, the recent unprecedented surge in o i l prices has again widened the gap between domestic prices and current international prices and increased the amount o f fuel subsidies. The new government remains fully committed to addressing the o i l product subsidy and gas pricing issues and to developing and implementing a rational gas pricing policy. Full removal of fuel subsidies w i l l require more time than earlier planned and substitution o f domestic gas for imported fuels w i l l contribute to resolving this issue and benefit the economy and the environment. Recently the GO1 increased o i l product prices between 9 and 25 percent which resulted in a weighted average increase o f 12.5 percent. Establishment of an appropriate legislative and regulatory framework. Many o f the sectoral issues have stemmed from the previous inadequate legislative framework governing the energy sector. In November 2001, the government enacted a new O i l and Gas Law. The law gave Indonesia i t s f i rs t modern legal framework to fundamentally reform the o i l and gas sector, through (a) the gradual development o f a competitive market; (b) the establishment of an implementing body for upstream activities and an independent regulatory agency for downstream activities; and (c) the unbundling o f the traditionally vertically integrated o i l and gas businesses. The issuance o f the implementing rules and regulations on October 18, 2004 wil l l ikely speed up the opening o f the o i l and gas sectors to competition and further private investments. Restructuring of the Gas Sector. PGN has already unbundled i t s key transmission activities f rom i t s distribution operation. I t associated wi th several strategic partners to create a gas transmission subsidiary, and listed, in December 2003, about 39 percent of i t s shares in the Jakarta and Surabaya stock exchange markets. Further restructuring o f PGN to allow greater private sector participation in i t s operation and preparation for future sales o f i t s shares and assets i s under way. Production-sharing contracts. The new law and regulations provide for a competitive environment under which all gas producers could have direct access to consumers. The

0

2

absence o f a provision for gas discovery in the existing contracts w i l l be resolved gradually, on a case-by-case basis.

2. Rationale for Bank Involvement

2.1. Bank involvement and assistance to PGN significantly contribute to adequate and effective implementation o f the sound legal framework and policies developed with Bank support during the preparation o f the project. During project implementation, the Bank w i l l continue the ongoing policy dialogue and cooperation with GO1 and PGN on deepening the reform o f the energy sector to ensure adequate implementation o f the recommendations of the analytical and advisory and technical assistance activities joint ly carried out to date. The project w i l l focus mainly on (a) designing and implementing an effective gas pricing pol icy and, (b) further restructuring o f PGN to bring i t s corporate structure in l ine wi th the new Oil and Gas Law. Appropriate policies in gas pricing and the restructuring of PGN must be addressed “to improve the climate for high quality investments” to develop gas use in the domestic market. The Bank’s involvement would also assure that these two issues are addressed in a timely manner to meet the market needs according to international best practice and the government reform objectives. This would pave the way to further opening o f the sector and attract private sector financing to meet the sizeable investment needs to develop it.

2.2. The development o f a comprehensive gas pricing framework in relation to the cost o f production, transmission and distribution o f gas w i l l improve the transparency o f payment and allocation o f the rent. The revenues generated by the development of natural gas f rom the f ield to the final users w i l l allow the government and the regulator to make informed decisions in setting prices, taking into account efficiency and equity.

2.3. The GO1 has secured US$500 mi l l ion f rom private investors to Pertamina for further field development and US$485 mi l l ion f rom the Japan Bank for International Cooperation (JBIC) to PGN for a transmission project to increase gas supply to West Java. However, the government and JBIC agree that additional investment alone i s not enough to develop the domestic gas market. The Bank’s strong global knowledge and experience would be instrumental in addressing long term pol icy issues to develop and sustain the domestic gas market, I t was agreed that the JBIC would rely on the Bank to address gas pricing issues to support i t s project.

3. Higher level Objectives to which the Project Contributes

3.1. The most recent full Country Assistance Strategy (CAS), approved by the Board on October 29, 2003 (Report No. 27108-IND), focuses on assistance to Indonesia to overcome the l o w rate o f investment and to improve the weak public service, two major impediments to reducing poverty. The objectives o f the proposed project are fully consistent with, and give substantial support to, two of the five areas identified as essential to raise investment and improve (energy) services: fostering a competitive private sector and expanding Indonesia’s infrastructure.

3.2. The development and implementation o f a rational gas pricing pol icy wi l l improve the efficiency o f gas utilization, increase transparency, and create a more attractive environment for private sector participation, and thereby increase investment in the supply and utilization o f

3

natural gas. The restructuring o f PGN i s essential to ease entry into the growing gas market and to increase private investment in the gas sector. I t w i l l align PGN’s corporate structure wi th the new law and recent regulations, and prepare i t to operate in a competitive environment.

3.3. The physical expansion o f the gas infrastructure under the proposed project w i l l have a significant impact on alleviating infrastructure bottlenecks in Indonesia and improving quality o f gas service in West Java. The project supports the reinforcement o f PGN’s distribution system to increase potential supply to about 550 mmcfd, more than three times PGN’s gas sales in the region.

B. PROJECT DESCRIPTION

1. Lending Instrument

1.1. The proposed project involves expansion o f the gas distribution system in West Java and capacity building activities for PGN during the project’s implementation period. Most o f the loan funds w i l l be used to procure goods for system expansion through International Competitive Bidding (ICB). Lending instruments such as SECAL and APL were considered but were rejected b y the GOI. Based on i t s past cooperation with the Wor ld Bank, PGN selected a Specific Investment Loan as the most appropriate lending instrument. The variable-rate single currency loan selected by PGN during appraisal was confirmed by the Indonesian Delegation during negotiations.

2. Project Development Objective and Key Indicators

2.1. The proposed project would expand the use o f natural gas in the West Java market. The objective i s to improve economic efficiency and reduce pollution by substituting gas for more expensive and more polluting fuels, such as diesel, fuel o i l and coal.

2.2. In addition, to achieve this objective efficiently and sustainably, PGN wil l carry out and prepare for implementation o f ongoing studies focusing on: (a) rationalization o f the natural gas pricing system to induce efficiency; and (b) restructuring o f PGN to meet the requirements o f the new law, ease market entry and increase private sector involvement. The major related projects financed by the Bank and other agencies are listed in Annex 2.

2.3.

a a a

a

3.

3.1.

The key performance indicators, presented in Annex 3, focus on the following:

An increase in utilization o f natural gas; The reduction of air pollutant emissions; Finalization of the gas pricing study and development and implementation o f a rational natural gas pricing pol icy according to a schedule acceptable to the Bank; and Finalization of the PGN’ s restructuring study and development and implementation o f a restructuring strategy according to a schedule acceptable to the Bank.

Project Components

The project, described in detail in Annex 4, comprises two components:

4

Distribution Infrastructure Expansion: This component to be implemented b y PGN includes: (i) construction o f class 300 steel pipelines 4-16 inches in diameter wi th a cumulative length o f about 185 km along with control valves and corrosion control facilities; (ii) construction o f class 150 steel pipelines o f 4 to 16 inches in diameter with a cumulative length o f about 71 km, along with control valves and corrosion control facilities; (iii) installation o f five off-take and two pressure regulation stations; (iv) installation o f about 210 customer metering and regulating stations; (v) installation o f a Supervisory Control and Data Acquisition (SCADA) system; and (vi) provision o f radio and telecommunications equipment, information technology (IT) support, and emergency response equipment. The total cost o f this component i s US$108.50 mi l l ion including contingencies and value added tax (VAT), wi th IBRD financing o f US$76.80 million. Capacity Building: This component, to be implemented by PGN, involves assistance to PGN in upgrading i t s capabilities and staff s k i l l s in financial management, infrastructure planning, gas marketing, gas utilization, distribution system safety and integrity management, and gas transmission and compression. The total cost o f this component i s US$6.20 million, wi th IBRD financing o f US$3.00 million.

The total cost o f the project i s provided in Annex 5.

3.2. project:

Three o f the issues mentioned in section A-1.1 w i l l be addressed under the proposed

Pricing. The Bank has provided funding to PGN under i t s power sector loan approved in June 2003 (Loan No. 4712-IND) to conduct a study to develop a gas pricing pol icy to: (i) establish sound pricing and regulatory principles compatible with the government’s reform and macroeconomic objectives to increase the market orientation o f the sector, foster competition where feasible and safeguard consumers f rom monopoly abuses; and (ii) develop detailed transitional arrangements for a phased implementation o f these principles in l ine wi th the implementing rules and regulations. The consultants for the study have been selected and the study i s expected to be completed on or before March 2006. The important findings o f the study w i l l be used by PGN to prepare a pricing policy framework and gas transmission and distribution pricing principles and methodologies to be submitted to the government and the Regulator for review and consideration for approval2; PGN Restructuring. PGN has taken several actions to initiate unbundling of i t s structure (consistent wi th the Bank’s recommendation in previous operations and the new Oil and Gas Law), to include strategic partners in i t s transmission operation, and to offer equity shares to the public through init ial public offering (PO). The Bank, under i t s power sector loan approved in June 2003 (Loan No. 4712-IND), i s providing assistance to PGN to study alternatives to further i t s restructuring and be prepared to operate in the future liberalized market envisioned by the new Oil and Gas Law. The consultants for

* The implementation of a rationalized pricing policy for most part falls under the purview o f the newly established regulatory body. PGN wi l l consult and closely coordinate with the regulatory body concerning the principles and implementation o f the new pricing policy. As part the Pricing Study, the consultants w i l l provide P G N with international experience on price setting, open access and other mechanisms to increase the market orientation o f the sector. The experience w i l l be shared and discussed with the regulatory body and should lead to informed decisions during the implementation o f the agreed pricing policy.

5

the Restructuring Study have been selected, and the study i s expected to be completed before the end o f June 2006. The key findings o f the study w i l l be implemented under the proposed project, as part o f the policy conditions discussed and agreed with PGN and concerned government agencies; and

(c) Infrastructure. The proposed loan w i l l finance the expansion o f the gas distribution network. Although the amount o f the loan i s relatively small (US$80 million), the proposed project w i l l have a significant impact in helping to alleviate gas infrastructure bottlenecks in Indonesia. The Bank’s involvement in the project leveraged more than US$l .O bi l l ion o f investment. This investment w i l l expand substantially the gas infrastructure for development, transmission and distribution o f natural gas, wi th potential supply of up to 550 mmcfd, or three times of current gas sales o f PGN in the West Java region.

4. Lessons Learned and Reflected in the Project Design

4.1 The objectives o f the Bank’s previous gas distribution projects in Indonesia were to expand the physical network as well as to enhance the efficiency and the financial position o f the implementing agency, PGN. Although these objectives were successfully achieved, ex post reviews o f these projects stressed that gas pricing and further restructuring o f PGN should be addressed to accelerate the development o f the domestic gas market. The current project addresses these sectoral issues after the government passed the Oil and Gas L a w and related regulations that paved the way for further opening o f the sector to new entrants and for increasing i t s market orientation.

5. Alternatives Considered and Reasons for Rejection

5.1 preparation:

The fol lowing alternatives were sequentially considered during the project design and

“Without Project” Alternative. Prior to engaging in this important investment program, PGN considered a less aggressive strategy o f converting small industries and businesses to gas, which entailed l o w growth of the Banten-West Java gas market and no expansion o f i t s distribution system. The “without project” alternative has been rejected for three reasons: (a) the expansion o f the gas market was in l ine wi th the government energy strategy to develop the domestic gas market because o f i t s economic and environmental advantages over o i l products and coal; (b) a market scoping study showed a strong preference o f small industries and businesses for gas; and (c) expansion o f the gas market would sustain the growth and strengthen the financial situation o f the company and reduce the need for petroleum products subsidies. Choice of Gas Supply. T w o alternatives were considered for gas supply: gas fields in South Sumatra, or small onshore and offshore fields in West Java. An Asian Development Bank (ADB) study found that delivering gas f rom the South Sumatra fields to the West Java market was preferable to relying on closer but limited and more costly to develop fields in West Java onshore and offshore. The gas reserves in the South Sumatra fields have been formally certified by a reputable international company at a level o f 3.85 tcf in the Proven and Risk Adjusted categories. These reserves can supply up to 500

6

mmcfd o f gas for at least 20 years. The option o f transmitting gas f rom South Sumatra to West Java was selected.

5.2 Expansion of the Distribution System. PGN considered alternatives for the expansion of i t s distribution system by taking into account (a) the capacity o f the existing system; (b) the location and demand o f potential consumers (demand nodes); (c) the quantities and input locations o f gas (supply nodes); and (d) severe constraints on the right o f way in highly urbanized areas. The latter reduced the number o f alternatives for expansion to two, mainly differentiated by the pipeline diameters along the same routes to satisfy a demand o f 500 mmcfd in the first case and a demand o f 800 mmcfd in the second case. The f i rs t option would have required further reinforcement o f the system after 5-7 years to meet the full potential demand o f 800 mmcfd by 2016. I t was rejected because i t was less cost effective and would have entailed greater temporary negative environmental and social impacts.

C. IMPLEMENTATION

1. Institutional and Implementation Arrangements

1.1. PGN w i l l be responsible for the implementation o f both components of the project. I t has established a project implementation unit (PIU) with overall responsibility for managing and coordinating al l aspects o f the project. The PIU w i l l be supported by PGN’s central departments.

1.2. Funds for this project w i l l be borrowed b y the Republic o f Indonesia and on-lent to PGN in the currency o f the loan, in l ine wi th current government pol icy and on the same terms and conditions plus an additional “administrative” fee not exceeding one percent (1%). A Subsidiary Loan Agreement i s expected to be finalized between the GO1 and PGN for this purpose, as a condition for loan effectiveness.

1.3. Financial management and disbursement arrangements, discussed and agreed wi th PGN, are detailed in Annex 7. Procurement arrangements, discussed and agreed with PGN, are detailed in Annex 8.

Institutional and implementation arrangements are provided in Annex 6.

1.4. Furthermore, PGN has agreed to hire (a) a project management consultant to assist in the design and engineering, procurement, construction supervision, inspection of materials and works, and testing and commissioning, as wel l as overall project management related to the distribution component; and (b) a long-term technical advisor to assist in customer conversion and connection, system integrity management and technical s k i l l development and enhancement.

2. Monitoring and Evaluation of Outcomes/Results

2.1. PGN maintains a statistical system with sufficient data to monitor most of the outcomes of the project such as gas sales and number o f consumers converted to gas. Major pollutant and greenhouse gas emissions w i l l be calculated according to a methodology agreed with PGN and summarized in Annex 3. Results indicators such as progress o f construction work and progress on the restructuring and pricing studies, w i l l be monitored b y the PIU and reported in periodic progress reports to be submitted to the Bank.

7

3. Sustainability

Risk

3.1 PGN has taken several actions to ensure the sustainability o f the project by contracting gas supplies f r o m different sources, preparing a customer conversion and ramping-up program, and committing to the implementation of gas sector reforms (including rationalization o f gas pricing system) to ensure optimal use of resources and further opening o f the gas market. Appropriate measures to mitigate the minor social and environmental impacts associated with the proposed and l inked projects have been developed by PGN and agreed by the Bank. These w i l l ensure the social and environmental sustainability o f the project, the safety o f the workers, PGN staff and the population during the construction period and the operation o f the system.

Risk Minimization Measure I RiskRating

4. Critical Risks and Possible Controversial Aspects

To Project Development

expected. Gas supply lower than

Customer conversion slower than planned.

The objectives of energy price rationalization not achieved because of lack of government commitment

Inherent risks arising from weaknesses in country control environment and financial accountability systems. To Component Results a) Insufficient counterpart funds available. b) Construction not completed on time

c) Procurement delays

Overall Risk Rating Risk Rating - H (High), S

4.1. The project’s overall risk i s expected to be modest.

Objective The gas source for th is project i s estimated at total proven and risk-adjusted reserves of about N 3.85 tcf, which would be sufficient to maintain a supply of 500 mmcfd for at least 20 years. PGN has signed a 12-year gas purchase contract with Pertamina, the gas supplier, for 250 mmcfd, which could deplete only 1 tcf of the above-mentioned reserves. PGN also signed a contract with Conoco-Phillips for 400 mmcfd to increase supply to West Java.

department, and a gas sale ramp-up plan was prepared at the Bank’s request. According to the study, more than 500 industrial customers who were surveyed expressed interest in switching to gas. The demand of these customers i s more than 600 mmcfd. However, because a lead time of about 12 months i s required for consumer conversion, the Bank suggested, and PGN agreed, start customer preparation as soon as possible prior to project appraisal.

system, and phasing out subsidies on the prices of oil products. Actions already taken, especially the enactment of the implementing ru les and regulations in October 2004 and the important increase of oil products prices in 2005, are clear indications of the government’s commitment.

project specific measures such as enhanced financial reporting and additional payment validation procedures.

A study on development of the gas market has been undertaken by PGN’s marketing M

The government i s committed to reforming the energy sector, rationalizing the energy pricing M

Continue country dialogue to expedite public financial management reforms and introduce S

PGN has secured financing from the JBIC for the transmission pipelines. I t has enough cash

PGN has a demonstrated management capability to plan and implement large infrastructure

N

M from i t s recent IPO to cover the capital cost not financed by the Bank.

projects. The transmission component i s well prepared and its construction commenced in 2005. Preparation of the distribution component i s also progressing well. A project management consultant (PMC) i s being hired to help PGN prepare and manage the project, and construction will be outsourced to qualified engineering, procurement and construction (EPC) contractors.

time to procurement tasks and to speed up the hiring of the PMC.

(Substantial), M (Modest), N (Negligible or Low Risk)

A procurement committee has been established. PGN committed to assign a core team full M

M

4.2. The project i s not expected to face any controversial aspects.

8

5. Loadcredit Conditions and Covenants

5.1, Concerning pricing, PGN shall:

(a) (i) Prepare a draft gas pricing framework based on the findings and recommendations o f the Gas Pricing Study carried out under the Java-Bali Power Sector Restructuring and Strengthening Project; (ii) not later than March 31, 2006, furnish to the Bank for i t s comments said draft gas pricing framework; and (iii) promptly after receipt o f said comments, finalize said draft, taking into account said comments, and submit i t to BPH M I G A S (downstream regulator) for review, amendment, i f needed and consideration in view o f adoption; and

(b) (i) Prepare draft methodology and implementation rules for transmission and distribution tar i f fs based on the findings and recommendations o f the Gas Pricing Study carried out under the Java-Bali Power Sector Restructuring and Strengthening Project; (ii) not later than September 30, 2006, furnish to the Bank for i t s comments said draft methodology and implementation rules for transmission and distribution tariffs; and (iii) promptly after receipt o f said comments, finalize said draft, taking into account said comments, and submit it to BPH MIGAS and other concerned authorities for review, amendment, i f needed, and consideration in view o f adoption.

5.2. Concerning the restructuring plan, PGN shall:

(c) (i) Prepare a draft set o f procedures and implementation plans for “Third Party Access” consistent with the regulations o f the Republic o f Indonesia No. 36 o f 2004 regarding downstream business activities o f o i l and natural gas, which draft set shall include a standard contract form to be entered into wi th al l users o f PGN’s transmission and distribution network; (ii) not later than December 31, 2005, furnish to the Bank for i t s comments said draft set o f procedures and implementation plans; and (iii) promptly after receipt of said comments, finalize and adopt said set of procedures and implementation plans, taking into account said comments

(d) (i) Prepare a draft time-bound restructuring plan based on the findings and recommendations o f the Restructuring Study carried out under the Java-Bali Power Sector Restructuring and Strengthening Project; (ii) not later than March 31, 2006, furnish to the Bank for i t s comments said draft plan; and (iii) promptly after receipt o f said comments, finalize said plan, taking into account said comments, and thereafter implement said plan in accordance wi th i t s terms.

5.3. Concerning the investment program, PGN shall:

(e) Review with the Bank annually, commencing September 30, 2005, i t s rolling three-year investment program, and thereafter take al l measures required to ensure a rational investment program.

5.4. Concerning the financial performance, PGN shall:

i t s average three-year capital expenditures. ( f ) Generate sufficient revenue f rom i t s internal sources equivalent to at least 25 percent o f

9

(8) Demonstrate that a reasonable forecast o f i t s revenues and expenditures for each fiscal year would produce sufficient net revenue to be at least 1.5 times i t s estimated debt service requirements.

(h) No t incur any debt, if after the incurrence o f such debt the ratio o f debt to equity shall be greater than 75/25 during 2006-2009 and 70/30 thereafter.

5.5. shall:

Concerning the financial management issues and financial monitoring report, PGN

(i) Furnish to the Bank an FMR, in substance satisfactory to the Bank, on a quarterly basis. The f i rs t FMR shall be furnished to the Bank not later than 45 days after the first quarter after the effective date, and thereafter at quarterly intervals not later than 45 days after the end o f each quarter.

5.6. Concerning the audit and accounting, PGN shall:

(j) Have i t s annual financial statements duly audited by public accounting f i r m s appointed by i t s shareholders in shareholders’ general meetings, in accordance wi th the provisions o f i t s articles o f association and prevailing laws and regulations in Indonesia.

(k) Furnish to the Bank as soon as available, but in any case not later than six months after the end o f each fiscal year audited the following: a certified copy o f the audited financial statements of PGN audited by the above auditor, including the auditor’s opinion on such statements, and management letters issued by the statutory auditor. Such audited financial statements shall include appropriate disclosures in the notes appended thereto on the amounts of Bank funding utilized during the period under audit, and copies o f project related internal audit reports issued to i t s management by i t s internal audit department, as wel l as other financial information as the Bank shall deem necessary.

Concerning the environmental and social aspects, PGN shall:

(1) Undertake the implementation of the project in accordance wi th the project’s Environmental Management Plan, the Environmental Monitoring Plan, and the Land Acquisition and Resettlement Policy Framework, al l in a manner satisfactory to the Bank.

Concerning the project implementation unit, PGN shall: (m)Maintain until completion o f the project, a PIU, staffed wi th qualified and experienced

officers, and provided wi th adequate funds and other resources as shall be necessary to accomplish i t s objectives.

5.7.

5.8.

5.9. Concerning the monitoring project performance, PGN shall:

(n) Maintain policies and procedures adequate to enable i t to monitor and evaluate on an ongoing basis, in accordance wi th the indicators set forth in para. 2.3 under section B (Project Description) the project objective achievements.

(0) Prepare an annual report on the above monitoring results and review it wi th the Bank three months after completion o f each report.

5.10. Concerning the progress report, PGN shall:

10

(p) Furnish to the Bank not later than March 31 in each year, commencing March 31, 2007, and until completion o f the project, annual progress reports on the implementation o f the project.

D. APPRAISAL SUMMARY

1. Economic and Financial Analyses

1.1. Cost Effectiveness. A least-cost study on expansion o f the gas distribution network in West Java was undertaken b y PGN during the project preparation. The study considered different scenarios and configurations o f the distribution system expansion to achieve the optimal expansion plan to meet the future gas demand in the region. The proposed project i s part o f the least-cost plan to expand the distribution system for West Java region to supply up to 800 mmcfd o f natural gas by 2015. This demonstrates the cost-effectiveness o f the project.

1.2. Cost-Benefit Analysis. In addition, a cost-benefit analysis (without considering environmental externalities) was carried out to estimate the economic internal rate o f return (EIRR) o f the proposed project. The EIRR was estimated at 20 percent, i f benefits were valued at prevailing tar i f fs (base case), and at 59 percent, i f benefits were valued at future market value of displaced fuels. Net present values (NPV) at 12 percent are US$169 mi l l ion in the first case and US$1,152 mi l l ion in the second case. Sensitivity and risk analyses were carried out to assess the robustness of the economic viability o f the project in relation to the major perceived risks, such as increase in investment cost, delay in construction, reduction in benefits, and slow progress in consumer conversions. The sensitivity and r i s k analyses indicate that changes in the important variables w i l l not fundamentally affect the economic viability o f the project. Details are provided in Annex 9.

2. Financial Analysis

2.1 Overall, PGN’ s financial position in the past has been sound, including during the regional financial crisis. PGN’s current financial position based on 2003 audited financial statements i s presented in Annex 9 and summarized below:

(a) Revenues and Expenditures. In 2003, PGN generated a total revenue o f US$425 million, comprising: (i) US$350 mi l l ion (82.4 percent o f the total revenue) f rom sales o f natural gas through i t s distribution networks; (ii) US$74 mi l l ion (17.4 percent o f the total revenue) f rom fees earned for gas transmission services; and (iii) less than US$500,000 (less than 0.2 percent o f the total revenue) f rom sales o f liquefied petroleum gas (LPG);

(b) Assets. PGN’s total assets in 2003 were about US$l.08 billion, including current assets o f US$418 million. Cash and cash equivalent represented 54 percent o f i t s current assets, and short-term investments represented an additional 19 percent. The large cash account was the result o f proceeds f rom the multilateral or bilateral loan borrowing, a US$ l50 mi l l ion Eurobond issue, and a December 2003 public offering o f about 39 percent o f i t s shares;

(c) Liabilities. PGN’s long-term debt in 2003 was about US$330 million, mostly consisting o f “two-step loans,” owed to the government for the funds borrowed f rom the ADB, JBIC, European Investment Bank (EIB), and Wor ld Bank for i t s capital expenditures; and

PGN’s Financial Performance and Current Financial Position.

11

(d) Equity. PGN’s total equity in 2003 was about US$390 million.

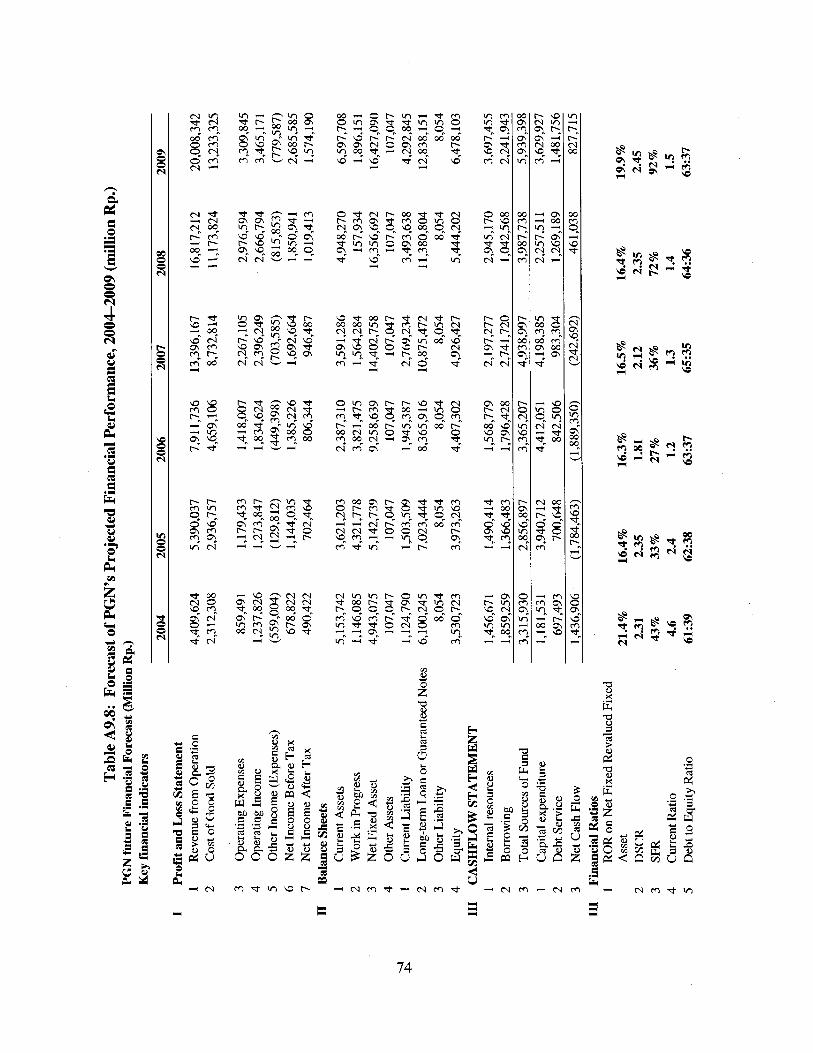

2.2 PGN’s Future Finances. Under the new O i l and Gas Law, PGN lost i t s self-regulated quasi-monopoly on gas transmission and distribution and, as the market progressively opens, w i l l operate in an increasingly competitive market. The newly established Regulator w i l l determine and regulate the tariff for natural gas distribution and transmission services. Further, the new law allows direct access o f gas suppliers to consumers, creates a healthier environment for competition and provides for a more efficient operation o f the sector in the future. It, however, has the potential to increase competitive pressure on PGN and reduce i t s current prof i t margin. For this reason, PGN’s financial forecasts are based on mutually agreed assumptions about growth scenarios for natural gas demand, constraints on PGN’s planned investment program, and pressure on i t s expected profit margin for gas distribution and transportation activities. Table A9.6 (Annex 9) provides a summary forecast o f PGN’s financial performance for 2004-09, including estimated income statements, balance sheets, and cash f low statement. Initial, unaudited figures for 2004 indicate that PGN i s on track to achieve i t s development and financial objectives. Revenues increased b y more than 20 percent as expected through the sale of nearly 300 mmcfd o f gas and the transportation o f another 420 mmcfd. Consequently, PGN had an operating income o f US$113 million, total income before taxes o f US$74 million, and after taxes o f US$55 mil l ion. Going forward, PGN needs to monitor their expansion plans carefully so that any adverse changes can be quickly mitigated with adjustments in their expansion plans.

2.3 taking into account the critical areas that warrant closer monitoring o f PGN’s future finances.

The financial performance covenants described in C 5.4 (f), (g) and (h) were determined

3. Technical

3.1. The project has been designed and w i l l be built in accordance w i th international standards and best practice to assure adequate security o f supply, operational flexibility, and safety o f operations. I t w i l l be provided wi th modem facilities for gas f low and pressure control, gas dispatch, gas flow measurement, gas quality monitoring, corrosion protection, IT support, and radio and telecommunications instrumentation. 3.2. PGN has implemented two gas distribution projects wi th Bank support and two gas transmission projects with ADB financing. I t developed a reliable database o f material and construction costs, which i s being regularly updated. The project costs are considered realistic and take into account recent variation in and escalation o f prices o f goods and services. The physical and price contingencies are based on PGN’s experience and are similar to those found in other developing countries in the region.

3.3. distribution system safety and integrity management up to international standards.

4. Fiduciary

The capacity building component of the project w i l l upgrade PGN’s capabilities in

4.1. PGN became a partially public company fol lowing listing o f about 39 percent of i t s share in December 2003. The company has successfully completed a due diligence process o f i t s internal processes, including financial management processes, that i s normally associated wi th an PO. I t i s also subjected to the financial reporting and auditing discipline normally applied to

12

publicly listed companies in Indonesia, which i s relatively more rigorous than those applied to state-owned enterprises or government agencies.

4.2. The financial management assessment for this project has concluded that overall, financial management r isks are moderate and that i t would be appropriate to accept the entity annual audited financial statements for Bank purposes, wi th appropriate disclosures on the use o f the Bank funds. T o mitigate r isks associated with this project, several measures have been suggested in an action plan agreed with PGN, including the adoption o f quarterly F M R s , external audits b y leading private sector accounting f i rms, and strengthened procedures for validating and approving payments to contractors. With the implementation o f this plan, the financial management arrangements for this project would be acceptable. Results o f the financial management assessment and agreed arrangements are provided in Annex 7.

4.3. A procurement capacity assessment has been carried out and concluded that PGN has adequate experience and capacity to carry out the procurement activities related to the proposed project. The procurement risk i s rated as “average.” However, given the size and complexity o f procurement packages, as well as the relatively tight implementation schedule, external assistance (part o f the project management consultant’s services) w i l l be provided to PGN during the entire procurement cycle, including preparation o f bidding documents, bid evaluation, and contract execution. A brief summary o f the procurement capacity assessment and more details on the procurement arrangements are provided in Annex 8 and the report i s available in the project files. Clarifications relating to National Competitive Bidding (NCB) providers and an anticomption plan are attached in Annexes 8(A) and 8(B).

5. Social

5.1. There wil l be no involuntary resettlement and no impact on indigenous people or cultural property under the project. The adverse environmental and social impacts o f the project are minor. The gas pipelines of the project w i l l be built primarily in largely urbanized or industrial areas, all alongside existing roads. Businesses, residents and other facilities along the roadsides could suffer some temporary (up to one day) disruption caused by construction activities. In addition, there could be increased risk o f pedestrian injury f rom traffic accidents during construction because of physical obstruction or removal o f walkways. T o minimize these disruptions, PGN has standard operating procedures and prevention and mitigation measures in place. I t also agreed to compensate any affected businesses for loss o f income according to the Land Acquisition and Resettlement Framework agreed with the Bank during project preparation, In addition, PGN has a strong commitment to social responsibility and has supported the communities along i t s transmission and distribution right-of-way. In 2002, a Master Plan for Community Development was drafted to provide corporate guidelines on community development (ComDev) programs. In conducting i t s ComDev program, PGN has worked closely with universities, nongovernmental organizations (NGOs), and local governments, These institutions w i l l help PGN assess local need and play important roles in project implementation and in monitoring social outcomes.

5.2. The proposed project w i l l expand the supply and utilization o f natural gas and further competition in the domestic energy market and stimulate small industry development. During the project construction period, short-term employment opportunities for local unskilled labors

13

wil l be created, and the revenues o f local small businesses may increase temporarily, because of expenditures on the part o f construction workers. The project w i l l also create permanent jobs in the project areas.

5.3. Consultation with the public at the local level i s an important component o f Indonesia’s AMDAL (Analisis Mengenai Dampak Lingkungan Hidup) process. During the project preparation, PGN convened three public consultations in Jakarta and several consultations in project affected areas with representatives from most o f the stakeholder groups: government agencies, property owners, local businesses, NGOs and academia. During the project implementation, consultation w i l l be governed by the AMDAL and Environmental Management Plan (EMF) processes. Subcomponents o f the project wi l l be screened b y PGN’s project team with the support f rom the environmental coordinating office (ECO) in order to determine their status under Indonesia’s AMDAL requirements and the Wor ld Bank’s safeguard policies and procedures. For al l the subcomponents and activities to be conducted under the project, public consultation w i l l be further carried out at the local level in the subdistricts where the project activities w i l l take place, as required by Indonesia’s AMDAL process.

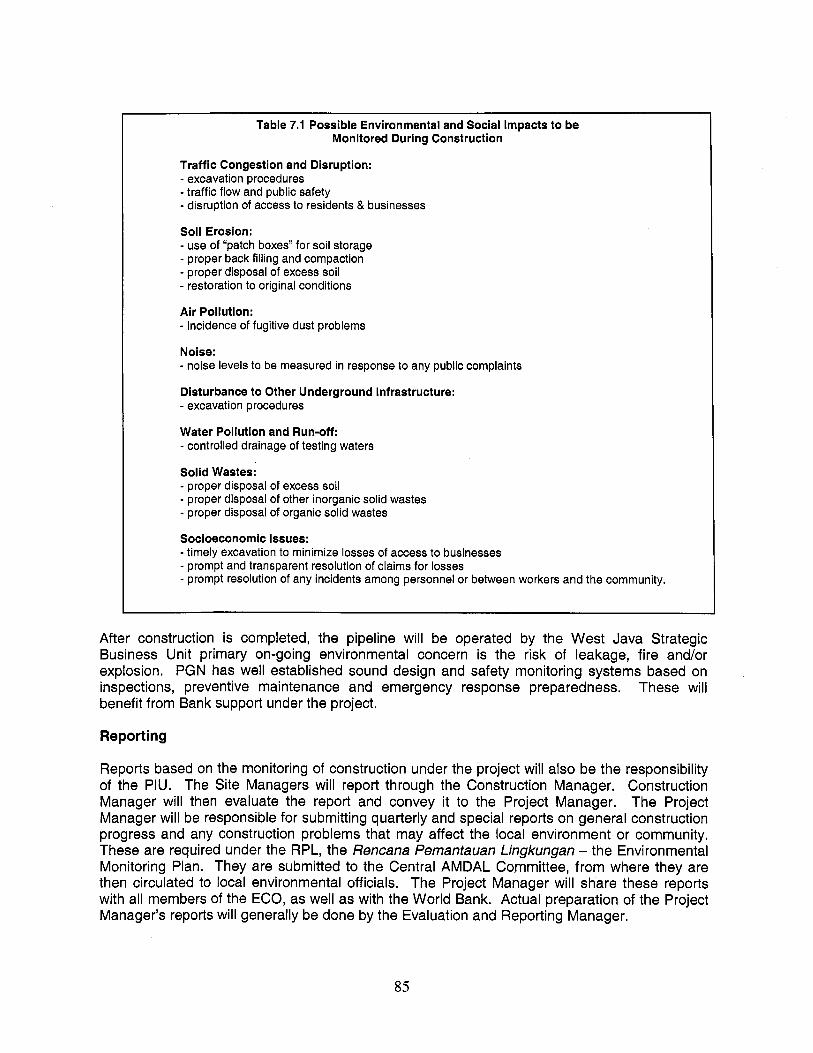

5.4. In general, the social project team o f the PIU w i l l be responsible for monitoring the project performance in terms o f social development outcomes. The project team leader w i l l receive copies o f quarterly and special reports on general construction progress and any construction problems that may affect the local environment and community. In addition, PGN’s ComDev programs and external institutions involved in the programs w i l l help the project team monitor the social development outcomes.

6. Environment

6.1. Based on the Environmental Impact Assessment Report (EIAR) prepared b y PGN wi th the assistance o f local and international consultants, the project (classified A because o f i t s link to the JBIC transmission project) i s not expected to have any significant impact on natural habitats, forests or protected or sensitive areas. None o f the impacts f rom the construction or operation o f the pipelines i s l ikely to be sustained or irreversible. The major negative environmental impacts w i l l be temporary interference with the traffic in the project area and some temporary air and water pollution, as wel l as the removal o f vegetation during the construction o f the project. None o f them, however, i s l ikely to be major, sustained or irreversible.

6.2. The proposed project w i l l provide important positive environmental benefits. Natural gas i s regarded as the “cleanest” fossil fuel, producing considerably lower amounts o f particulates or oxides o f carbon, nitrogen, sulfur, and other emissions per unit o f energy provided than other fossil fuels. Most o f the targeted consumers are currently using other fossil fuels. So ambient air quality should improve and, in some cases, the air quality within factories should improve, with direct health benefits for the workers. In addition, Indonesia’s greenhouse gas emissions w i l l be reduced.

6.3 The proposed project i s linked to a transmission project financed by the JBIC. Preparations for the construction o f the JBIC project are wel l under way wi th construction planned to commence in first quarter o f 2005. The EIAR was prepared and approved by the Ministry o f the Environment (MOE) in 1999. It has been discussed and approved b y the JBIC,

14

and was disclosed to the public fol lowing the AMDAL and JBIC's disclosure procedures. The approval o f MOE was reconfirmed in December 2003, and copies o f the EIAR, the EMP and the minutes o f discussions held between the JBIC and PGN were provided to the Bank during the preparation o f the proposed project. The EIAR and the process are considered as adequate.

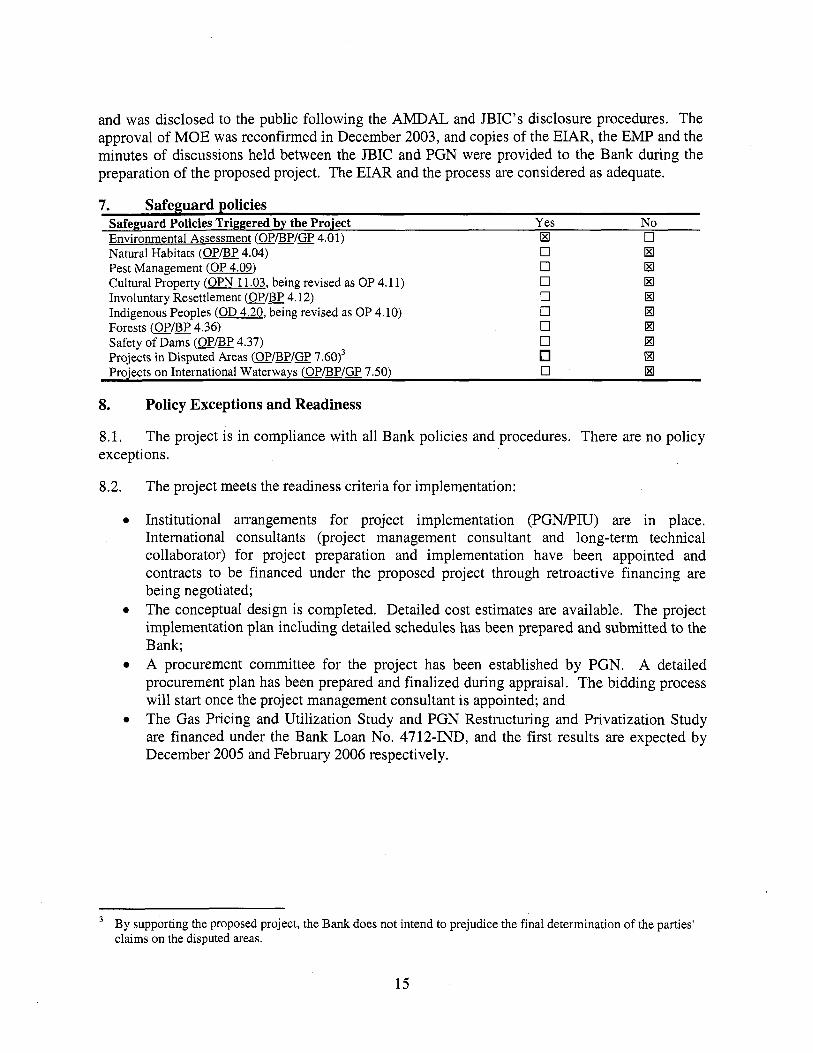

7. Safeguard policies Safeguard Policies Triggered by the Project Yes No Environmental Assessment (OP/BP/GP 4.01) H 0 Natural Habitats (OPIBP 4.04) 0 H Pest Management (OP 4.09) 0 H Cultural Property (OPN 1 1.03, being revised as OP 4.1 1) Involuntary Resettlement (OPIBP 4.12) 0 H Indigenous Peoples (OD 4.20, being revised as OP 4.10) Forests (OPIBP 4.36) 0 H Safety of Dams (OP/BP 4.37) 0 H Projects in Disputed Areas (OPIBPIGP 7.60)3 El Projects on International Waterways (OPIBP/GP 7.50) 0 El

0 H

0 H

8. Policy Exceptions and Readiness

8.1. exceptions.

The project i s in compliance with all Bank policies and procedures. There are no policy

8.2. The project meets the readiness criteria for implementation:

0 Institutional arrangements for project implementation (PGNPIU) are in place. International consultants (project management consultant and long-term technical collaborator) for project preparation and implementation have been appointed and contracts to be financed under the proposed project through retroactive financing are being negotiated;

0 The conceptual design i s completed. Detailed cost estimates are available. The project implementation plan including detailed schedules has been prepared and submitted to the Bank;

0 A procurement committee for the project has been established by PGN. A detailed procurement plan has been prepared and finalized during appraisal. The bidding process w i l l start once the project management consultant i s appointed; and

0 The Gas Pricing and Utilization Study and PGN Restructuring and Privatization Study are financed under the Bank Loan No. 4712-IND, and the first results are expected by December 2005 and February 2006 respectively.

By supporting the proposed project, the Bank does not intend to prejudice the final determination of the parties' claims on the disputed areas.

15

Annex 1: Country and Sector or Program Background INDONESIA: Domestic Gas Market Development Project

Indonesia has one o f the largest natural gas reserves in East Asia, roughly 20 percent o f the region’s total. Estimates put the total proved reserves at about 2.56 tr i l l ion cubic meters. However, the domestic gas infrastructure i s remarkably underdeveloped. In fact, Indonesia’s gas consumption by power and small and medium size industries as proportion of total energy consumption i s among the lowest in the region.

This reality i s particularly relevant since the country’s o i l reserves are declining, and the environment i s deteriorating because o f the use o f petroleum products and coal to meet the country’s industrial and power sector needs. Given i t s ample gas resources, Indonesia can stem this depletion and degradation-thus gaining significant economic and environmental benefits- i f i t moves faster to develop i t s natural gas sector and to expand the supply and utilization o f this fuel for the domestic gas market.

Indonesia needs to address the main issues impeding the development o f the gas sector and prepare a coherent and sustainable gas sector strategy to increase the use of this fuel substantially in the country. The fol lowing briefly discusses the substance o f the issues facing the sector, the government’s strategy to address them, and the Bank’s interventions to help the government in i t s efforts.

Pricing

The flawed natural gas pricing structure i s the first and the most important obstacle to gas development. However, the gas pricing issue cannot be addressed in isolation f rom the major issue o f petroleum product pricing subsidization. Therefore, the government agreed to give priority to phasing out the subsidies o f petroleum product first, and then begin to address the gas pricing issues.

The prices o f petroleum products in Indonesia are significantly below the economic cost o f supply and thus are heavily subsidized. In fact, the domestic price o f several products i s even below the cost of production. The Bank, under the “Indonesia Oil and Gas Sector Study,” provided a detailed analysis and recommendations for phasing out the subsidies for the f ive important petroleum products, while at the same time protecting the poor and avoiding disruptive macroeconomic impacts.

Since 2001, the government has taken major steps to reduce these subsidies considerably. However, soaring o i l prices in late 2003 and 2004 negated a l l the progress made to date and the ballooning subsidies regained the attention o f the government and the country and are now considered as one of the highest priorities o f the new government. Promotion o f gas and the implementation of a rational gas pricing pol icy became a central part of the strategy to reduce reliance on o i l products and phase out subsidies to create a fiscal space for funding the development o f the lagging areas.

17

Legal Framework

Many o f the o i l and gas sector issues in Indonesia stemmed from the legal framework, which was in place until the end o f 2002: (a) Pertamina had a supervisory function on the activities of the private companies operating in upstream segment o f the industry and was, at the same time, supposed to compete with them, entailing a clear conflict o f interest, and (b) i t enjoyed (and s t i l l does) a virtual monopoly over a huge market in downstream petroleum activities. These issues led to inefficient operation and non-optimal exploration and production o f o i l and gas. They heavily contributed to the slow development o f the gas domestic market. Indonesia clearly needed new and transparent Oil and Gas Law (and the associated regulations) to improve sector efficiency, to provide incentives for greater utilization o f gas in the domestic market and to provide incentives for greater participation o f the private sector in downstream activities.

With substantial inputs from the Bank and ADB, the government prepared a comprehensive draft law and implementing regulations in early 2000. The law, enacted in 2002, opened the sector to competition, increased transparency and provided incentives for further involvement o f the private sector.

The law explicitly eliminates the conflicting roles and functions o f Pertamina, by removing i t s supervisory functions and transfening these to an upstream supervisory agency. Pertamina’s monopoly has been eliminated although de facto i t s monopolistic position continues given i t s market dominance. However, i t w i l l need to improve i t s efficiency and compete wi th new entrants to keep a market share in the sector.

With respect to the gas sector, the new law provides for (a) third party access to the transmission and distribution pipelines (to the extent they are wi l l ing to pay the regulated tariff); and (b) a new regulatory body (BPH Migas) for al l downstream activities, including regulating the transport fees for transmission and distribution pipelines, the gas price for household and small commercial entities, and the open tendering for new transmission and distribution investment.

PGN Restructuring

Prior to the enactment o f the 2002 Law, Pertamina was the only upstream supplier o f gas for the domestic market-either from i t s own concession areas or, as the government’s sole agent, f rom the concession areas of other production-sharing contractors. Further, until 1998, Pertamina was also the only transporter o f gas. In 1999 the government authorized PGN to also transport gas to meet the increasing demand; particularly by the small to medium-size industrial consumers (Pertamina s t i l l continues to be the supplier to the large industries such as steel, fertilizer, power and cement). Under the new law, PGN wil l ultimately operate in a competitive environment, including allowing third party access to i t s transmission and distribution network, to provide gas producers direct access to consumers. PGN (a) began to unbundle i t s structure, both functionally and geographically, and (b) took several steps to secure private capital, including jo in ing with several strategic partners for i t s gas transportation business and listing about 39 percent o f i t s shares through an PO. However, to meet the law’s requirements, PGN needs to further i t s restructuring and increase the transparency o f the accounts o f i t s different subsidiaries to implement third party access, a prerequisite for the development o f a competitive gas market.

18

Production-Sharing Contracts

More than 90 percent o f Indonesia’s o i l and gas i s produced by the private sector, mostly by international o i l companies, and governed by production sharing arrangements. Although the fiscal and nonfiscal terms o f Indonesia’s PSCs are comparable to PSCs in other countries, one issue i s that many existing contracts s t i l l have no provision for gas discovery and therefore no predictable basis for forecasting the value to the producers o f possible gas discoveries for the domestic market.

The government has not yet began to address the issues relating to the existing contracts, considering that any change in terms and condition o f the contracts need to b e mutually agreed. With respect to new contracts, provisions o f the new law and regulations aim at creating a competitive environment that provides producers direct access to consumers. The issue o f absence o f gas discovery provisions in the existing contracts can only be resolved gradually, and on a case-by-case basis.

Infrastructure

The issues discussed above hampered the development o f an adequate gas infrastructure and constrained the development o f the domestic gas market. Given the economic and environmental benefits o f gas and Indonesia’s declining o i l reserves, i t i s essential to expand the gas infrastructure. The government’s strategy fully supports market based expansion o f the gas infrastructure wi th greater involvement o f the private sector.

19

Annex 2: Major Related Projects Financed by the Bank and/or other Agencies INDONESIA: Domestic Gas Market Development Project

Table A2.1

Sector Issue

Bank-financed

Natural gas market development in Jakarta-Bogor (West Java) and in Medan (North Sumatra)

Natural gas market development in Surabaya and other towns in the vicinity (East Java)

Fuel subsidies, oil-gas legislative framework

Power sector restructuring and preparation o f domestic gas sector restructuring Other development agencies Gas sector regulatory environment

Natural gas market development

IPDO Ratings: H S (Highly Satisfactory),

Project

Gas Distribution Project (completed 7/1994)

Gas Utilization Project (completed 12/ 199 8)

Second Policy Reform Support Loan (completed 12/1999)

Java-Bali Power Sector Restructuring and Strengthening Project

Implementation Progress

(IP) H S

S

S

S

Development Objective

(DO) HS

S

S

S

ADB Gas Transmission and I Distribution Project JBIC South Sumatra to West I Java Gas Transmission Project I :Satisfactory), U (Unsatisfactory), HU (Highly Unsatisfactory)

These projects are briefly reviewed as follows.

a. Gas Distribution Project (Ln. 2690-ZND) completed in July 1994 at a total cost of US$89 million. I t covered development of gas market and expansion of distribution infrastructure in the cities of Jakarta and Bogor in West Java and in Medan in North Sumatra, and PGN’ s institutional development. Zt was recognized as having been exceptional throughout the project cycle by the Operations Evaluation Department in its Annual Review of Evaluation Results, 1995. The performance covenants under the project were exceeded in all cases.

b. Gas Utilization Project (Ln. 3209-ZND) completed in December 1998 at a total cost of US$119 million. I t covered development o f gas market and expansion of distribution infrastructure in Surabaya and twelve other towns in i t s vicinity in East Java, and in Medan in North Sumatra in parallel with the upgrading of Indonesian expertise to manage this process. Until the onset of Asian financial crisis (July 1997), project implementation was rated as highly satisfactory. All targets were either achieved or

20

surpassed. Thereafter, despite the crisis, the project was satisfactorily completed in December 1998.

c. Grissik-Duri Gas Transmission Project, with ADB support, completed in 1998 at a total cost o f US$530 million. I t consisted o f a 28 inch diameter, 536 km long high-pressure gas transmission pipeline from gas fields near Grissik in South Sumatra to the o i l fields near Duri in Central Sumatra, along with ancillary facilities, for the transport o f 300 mmcfd natural gas for enhanced o i l recovery at Duri. Despite the Asian financial crisis, the project was completed on schedule and within the estimated cost.

d. Grissik-Singapore Gas Export Pipeline Project, with ADB support, completed in 2003, at a total cost o f US$470 million. I t comprised a 28 inch diameter, 485 km long high- pressure gas transmission pipeline from gas fields in South Sumatra to a power station in Singapore, along with ancillary facilities, for the export o f 150 mmcfd natural gas. This project was also completed on schedule and within the estimated cost.

Lessons learned and reflected in project design

The objectives o f the Banks previous gas distribution projects in Indonesia were to expand the physical network as wel l as to enhance the efficiency and the financial position o f the implementing agency, PGN. Although these objectives were successfully achieved, ex post reviews o f these projects made it clear that the pricing o f natural gas, and the corporate structure o f PGN, also needed to be addressed in order to accelerate the development o f the domestic natural gas industry. The current project addresses these sectoral issues after the government passed the Oil and Gas Law paving the way for further opening o f the sector to new entrants and increasing i t s market orientation.

21

Natural gas utilization expanded and air pollutant emssions reduced in West Java.

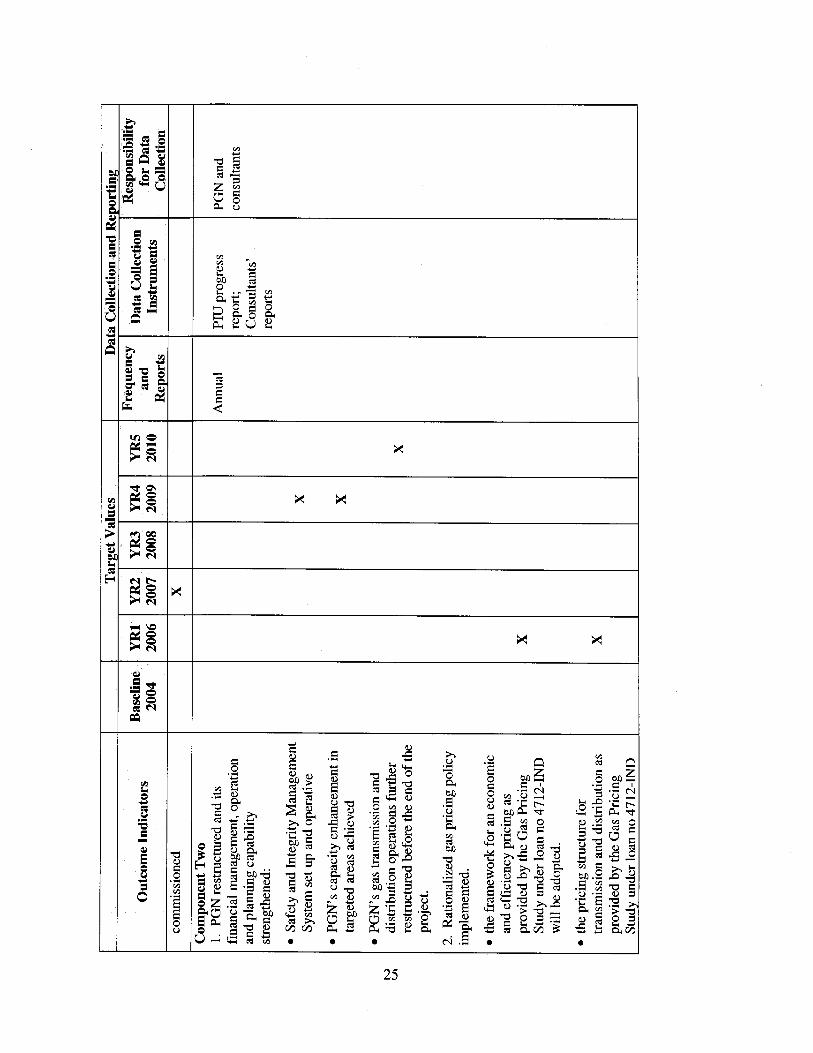

Component One: 1. West Java gas distribution network expanded

Component Two: Capacity Building of PGN 2. PGN restructured and its financial management, operation and planning capability strengthened.

3. Third Party Access 4. Rationalized gas pricing policy implemented.

ote: Estimates of Emis

Annex 3: Results Framework and Monitoring INDONESIA: Domestic Gas Market Development Project

Table A3.1: Results Framework

PGN’s gas sales in the region bmcfd):

Year 2004 2007 2010 Gassales 168 373 423 Cumulative number of consumers converted to gas: Year 2004 2007 2010 Number 0 95 120 Maior air Dollutant and greenhouse gas emissions reductions (1000 tons Der vear)

2004 2007 2010 so* 0 45 56 NO, 0 54 68 TSP 0 26 32 COze 0 1,323 1,653

Maior milestones of the distribution uroiect: Banten supply man line completed by October 2006; Banten reticulation mains completed by mid-2007;

Maior milestones for TA comuonents:

not later than June 20, 2006, PGN restructuring plan adopted Safety and Integrity Management System set up and operational by mid-2009 PGN’s capacity enhancement in targeted areas achieved by mid-2009 PGN’s gas transmission and distnbution operations further restructured before the end of the project.

not later than June 30, 2006, procedures and implementation plan of “Third Party Access”

not later than March 31,2006, the framework for an economic and efficiency pricing as adopted by PGN.

provided by the Gas Pricing Study under loan no 4712-IND wil l be developed by PGN and submitted to the Bank for comments.

the Ministry of Energy and Mining Resources for adoption.

transmission and distribution tariffs developed and submtted to the Bank for comments.

BPH Migas for consideration in view of adoption.

not later than June 30,2006, the framework (pricing policy) should be submitted by PGN

not later than September 30,2006, draft methodology and implementation rules for

not later than December 3 1, 2006, methodology and implementation ru les presented to

n Reduction Indicators.

22

e e

e

Natural gas i s the “cleanest” fuel among all the conventional fossil fuels. According to the market analysis by PGN, the gas supply from the proposed project will substitute for oil to be consumed mainly by industrial consumers in the project region. The emission reduction i s therefore estimated by the difference between the air pollutants from burning gas and oil. The simple and widely accepted method to calculate pollutant emissions i s to multiply emission coefficients o f pollutants by energy to be consumed. The emission coefficients of pollutants used here are from different sources as below:

SO2, NO,: Sasmojo et al, 1997, the “ALGAS Study Report for Indonesia”. TSP: Energy Technology Characterizations Handbook, US Department of Energy, 1983 C02: Revised 1996 IPCC Guideline Reference Manual.

1 Emission Type Oil Gas

SO2 (kg/mmBtu) 0.6464 0.0002

NO, (kg/mmBtu) 1.2009 0.4202

TSP (kg/mmBtu) 0.4100 0.0429

COZ (kg/mmBtu) 78.1459 59.1897

23

m o g 2 cc

ir: W c o N Z m w m

m o g 2

cc ir:

W W N C m w m -

m o g 2

cc v: W " N 5 m w m

o o o c

I

w

w

I w w w

a . a .

w

w w

w w

c 0

.I e,

.I Y

Y * E

E .I .I t?

& .I 3 & 3

- u .I

M

e

25

Annex 4: Detailed Project Description INDONESIA: Domestic Gas Market Development Project

Background

PGN’s natural gas marketing and distribution operations in Banten and West Java account for about 50 percent of i t s gas sales. These operations are spread over six districts, namely, Banten (recently upgraded to province status), Jakarta, Bogor, Bekasi, Karawang and Cirebon. About 163 mmcfd natural gas i s being supplied by PGN to industrial, commercial and household consumers in these areas.