Embed Size (px)

Citation preview

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext.1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Sales and Use Tax Fundamentals: Mastering Tax Base,

Compliance, Nexus, and Other Essential Multistate Concepts

TUESDAY, JANUARY 29, 2019, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

Jan. 29, 2019

Sales and Use Tax Fundamentals

Joseph F. Geiger, Jr., CPA, Consulting Tax Manager

Vertex, Berwyn, Pa.

Monika Miles, President

Miles Consulting Group, San Jose, Calif.

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

VertexSales and Use Tax Fundamentals

January 29, 2019 | 1:00 pm – 2:50 pm EST

• Joseph F. Geiger, Jr., Esq., CPA, MST, MSA

• Senior Tax Consultant, Vertex

• Over 30 years in accounting, audit and tax

• Public accounting and industry experience

• Specializing in indirect taxation, consulting and automation

• Represented audit clients at local, state and federal levels, including U.S. Tax Court

Presenter

7

© Miles Consulting Group, Inc. 2018

Presenter: Monika Miles

Founder - Miles Consulting GroupWebsite: MilesConsultingGroup.com;

www.JumpstartRain.comEmail: [email protected]

Professional Affiliations: AICPA, Texas Society of CPAs, CalCPA NAWBO - Silicon Valley, AFWA (Past National President)

Honored To Be Recognized As:

• “25 Most Powerful Women in Accounting” by CPA Practice Advisor

(2012, 2013, 2014 and 2015)

• “Women of Influence” by San Jose Silicon Valley Business Journal

(2014)

• Woman of Influence – AFWA National 2016

Tax Types

Tax Type: Sales Tax

Sales Tax – General Definition?

• Sales tax applies when seller has nexus and is subject to the state taxing authority

• A tax on the sale of tangible personal property or service

• Seller may pass tax on to the consumer; must be separately stated on the invoice

• Applies only to intrastate transactions

10

Tax Type: Sales Tax

Five states without a sales tax:

• NOMAD States:

• New Hampshire

• Oregon

• Montana

• Alaska (local jurisdictions may impose a tax)

• Delaware

11

Tax Type: Privilege Tax

Privilege tax – General Definition?

• Imposed on seller’s gross receipts for privilege of doing business in state

• Seller is liable for tax, but can pass tax on to the purchaser

• Can be included in the sales price or, separately stated on the invoice

12

Tax Type: Transaction Tax

Transaction tax – General Definition?

• Tax imposed on the sale of tangible personal property or services

• The purchaser is liable to the seller for the tax due

• The tax must be separately stated on the invoice

• If the seller is not registered in the state where goods are received, the purchaser is liable under audit for tax due on their purchases

• Examples: Colorado, Florida, Texas, and Virginia

13

Tax Type: Gross Receipts

Gross Receipts – General Definition?

• Similar to transaction tax, but with fewer exemptions or exclusions to the taxable base

• Hawaii - if the tax is passed on to the purchaser, the tax becomes part of the gross receipts for tax calculation

• The tax must be separately stated on the invoice

• In some states it is like the income tax and cannot be passed on (Washington B&O, Ohio CAT, Texas Margins)

14

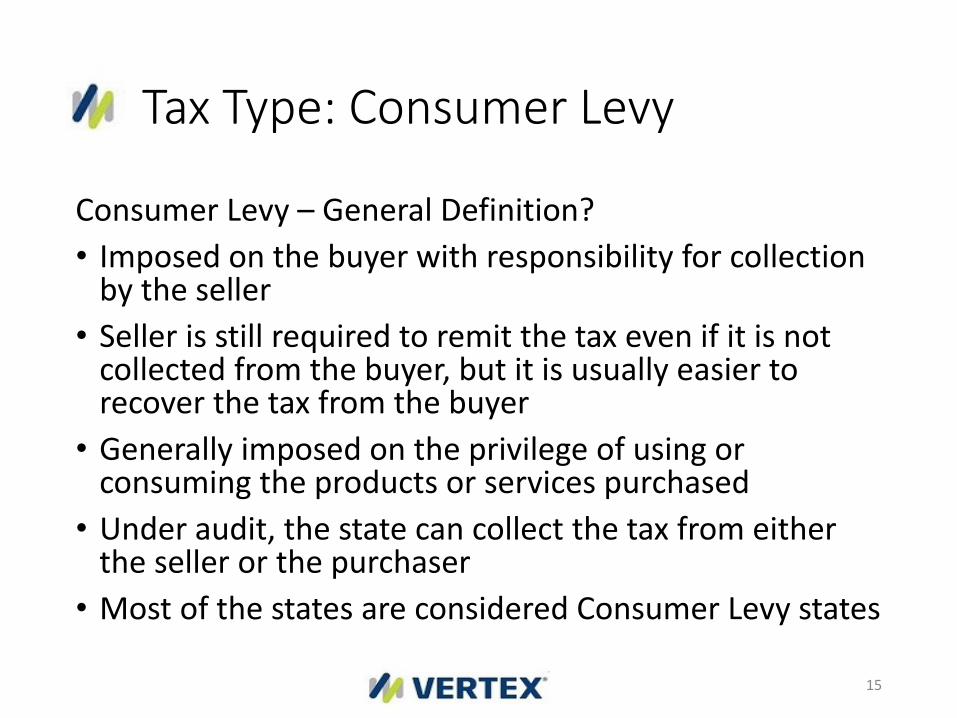

Tax Type: Consumer Levy

Consumer Levy – General Definition?

• Imposed on the buyer with responsibility for collection by the seller

• Seller is still required to remit the tax even if it is not collected from the buyer, but it is usually easier to recover the tax from the buyer

• Generally imposed on the privilege of using or consuming the products or services purchased

• Under audit, the state can collect the tax from either the seller or the purchaser

• Most of the states are considered Consumer Levy states

15

Definition: Use Tax

Use Tax – General Definition?

• Imposed on the storage, use, or consumption of a taxable item or service on which no sales tax has been included on the invoice

• Complementary to sales tax

• Purchases made outside the taxing jurisdiction but used in the taxing jurisdiction

16

Tax Type: Use Tax

Types of Use Tax

• Seller’s use – tax collected by registered vendor on interstate sales

• Consumer’s use – tax owed by the purchaser when the vendor does not include tax on the invoice

17

Illustration: Intrastate Sales Tax vs Interstate Seller’s Use• Sales tax applies to supplies of taxable goods and

services when the transaction occurs within a state.

• Vendor has a physical location in the state of the buyer – warehouse, branch location, corporate office

18

Illustration: Intrastate Sales Tax vs Interstate Seller’s Use • Seller’s use tax applies to supplies of taxable goods and

services when transaction occurs between two states

• Vendor shipping product out of state

• Vendor approving order out of state

• Customer receipt of goods or service from out of state vendor

19

Intrastate Sales Tax vs. Interstate Seller’s Use Tax

• Some locals within a state impose sales tax, but not seller’s use tax

• Examples include:• Alaska: no state sales tax, but local sales tax rates

• Arizona: many cities impose a sales tax, but not seller’s use tax

• Colorado: many home rule cities impose a seller’s use tax (intrastate transactions) while state administered cities do not

• Illinois: Chicago imposes a sales and consumer’s use tax, but not seller’s use tax

20

Intrastate Sales Tax vs. Interstate Seller’s Use Tax

• Some locals within a state impose sales tax, but not seller’s use tax.

• Examples in Pennsylvania:• Allegheny County is the only county in the state that

imposes tax at the county level. Allegheny county imposes sales and consumer’s use tax, but not seller’s use tax.

• Philadelphia City is the only city in the state that imposes tax at the city level. Philadelphia imposes sales and consumer’s use tax, but does not impose seller’s use tax.

21

Tax Type: Summary

• Intrastate Transactions - What tax type applies?• Sales tax

• Interstate Transactions – What tax type applies?• Seller’s use

• Purchase Transactions – What tax type applies?• Consumer’s use

22

© Miles Consulting Group, Inc. 2018

Nexus:

Some (Very)Hot Topics

© Miles Consulting Group, Inc. 2018

Nexus – Then & Now

• General Sales Tax Concepts

• Physical Presence Nexus

• Economic Nexus

• South Dakota v. Wayfair (2018)

• Wayfair Q&A

© Miles Consulting Group, Inc. 2018

The concept of sales tax is prevalent

in daily conversations because:

• States Need Revenue

• Increased On-line Transactions

• Smaller companies are able to expand their sales

footprints quickly because of increased

technology.

• There’s been some national media and a US

Supreme Court Case!

© Miles Consulting Group, Inc. 2018

Recapping What Joe said…

• Sales tax and complementary use tax are

imposed by state and local jurisdictions on

retailers for the privilege of selling “tangible

personal property” and certain services in the

jurisdiction.

• 45 states and DC impose a sales tax.Sales Tax

© Miles Consulting Group, Inc. 2018

How About Some History?

Let’s call it “Recent History”!

© Miles Consulting Group, Inc. 2018

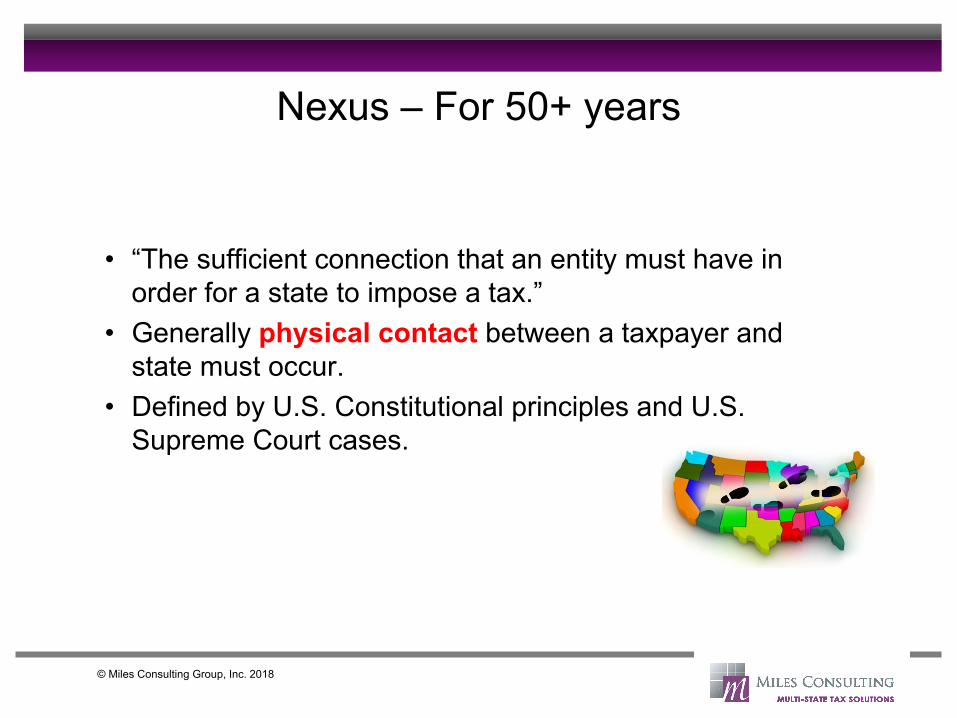

Nexus – For 50+ years

• “The sufficient connection that an entity must have in

order for a state to impose a tax.”

• Generally physical contact between a taxpayer and

state must occur.

• Defined by U.S. Constitutional principles and U.S.

Supreme Court cases.

© Miles Consulting Group, Inc. 2018

Nexus – OK! Now What?

• Once nexus is established, seller is obligated to collect sales tax.

• Unless there is a specific exemption.

© Miles Consulting Group, Inc. 2018

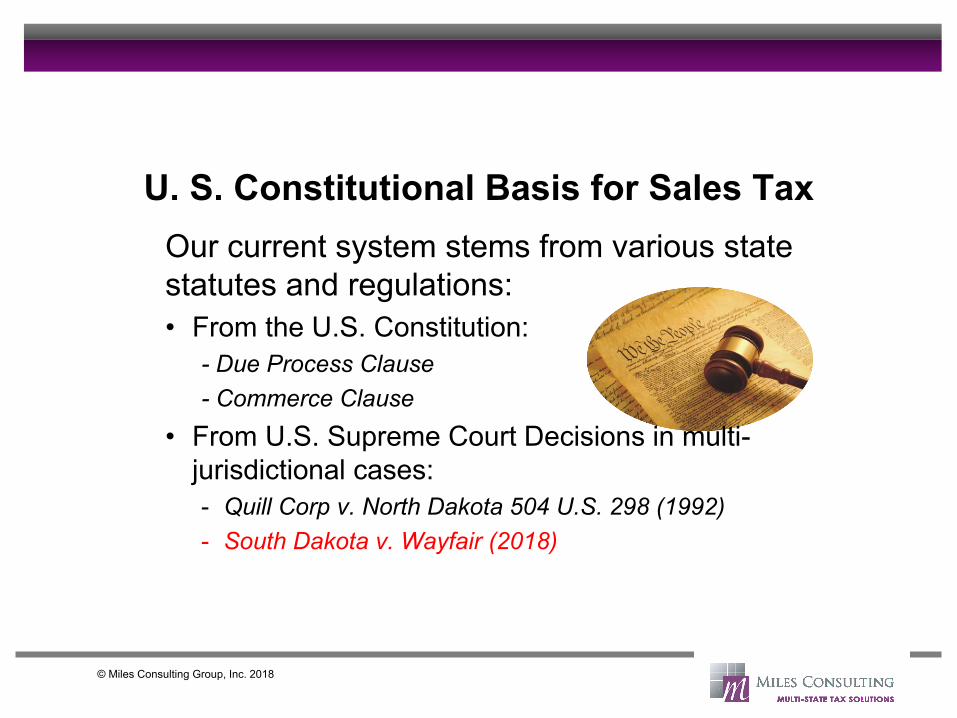

U. S. Constitutional Basis for Sales Tax

Our current system stems from various state

statutes and regulations:

• From the U.S. Constitution:

- Due Process Clause

- Commerce Clause

• From U.S. Supreme Court Decisions in multi-

jurisdictional cases:

- Quill Corp v. North Dakota 504 U.S. 298 (1992)

- South Dakota v. Wayfair (2018)

© Miles Consulting Group, Inc. 2018

Quill

In Quill (in 1992) the U.S. Supreme Court concluded that in

addition to any minimum connection with a state (Due

Process Clause), a business must have substantial

physical presence nexus (under the Commerce Clause)

before the state could impose sales/use tax collection

requirements.

© Miles Consulting Group, Inc. 2018

Catalog vs. the Internet

VS

© Miles Consulting Group, Inc. 2018

The Growth of Internet Sales

• Non-existent when the High Court decided Quill.

• No tax collection obligation on seller without a

physical presence in a state (like catalog sellers).

• Large part of the problem has been uncollected

use tax

– Complementary to sales tax

– Paid by purchaser directly

– Protects in state companies (if remitted)

© Miles Consulting Group, Inc. 2018

Uncollected Use Tax – Pop Quiz

The National Conference of State Legislators

(NCSL) recently calculated the estimated amount

of uncollected use tax in 2015 to be:

a. $2.6 Million

b. $26 Million

c. $2.6 Billion

d. $26 Billion

e. $260 Billion

© Miles Consulting Group, Inc. 2018

Uncollected Use Tax – Pop Quiz

The NCSL recently calculated the estimated

amount of uncollected use tax in 2015 to be:

a. $2.6 Million

b. $26 Million

c. $2.6 Billion

d. $26 Billion

e. $260 Billion

© Miles Consulting Group, Inc. 2018

“Economic Nexus”

• A minimum amount of sales $$ or transactions

creates nexus

• Even before Wayfair ruling, a growing number of

states had passed these laws – some examples:

– South Dakota, Alabama, Indiana, Rhode Island,

Wyoming, Maine, Massachusetts

© Miles Consulting Group, Inc. 2018

South Dakota: A “good fact pattern”

• Wayfair and other retailers sold more than $100K or 200

transactions to SD customers;

• State said that its economic nexus law applied and wanted

them to collect sales tax;

• Companies disagreed and appealed all the way to South

Dakota Supreme Court; and the state lost

• South Dakota appealed to US Supreme Court

• Early 2018 USSC granted certiorari – agreed to hear case

© Miles Consulting Group, Inc. 2018

US Supreme Court: Agrees to hear South Dakota case

• South Dakota v. Wayfair

• Court heard the case in April 2018; rendered its

decision on June 21, 2018

• We knew it would be close…

© Miles Consulting Group, Inc. 2018

US Supreme Court – Wayfair Decision

Overturned Quill• Ruled 5-4 in favor of South Dakota

• Sales in excess of $100,000 or 200 transactions

can create economic nexus

• Physical presence test under Quill no longer has to

be met (in South Dakota)

• So…nexus will be easier to trip into

Nexus?

Taxability of

Product?

Exemptions?

Sales Tax Quick Decision Tree

Register &

File (maybe)

Register &

File (maybe)Copyright © Miles Consulting Group, Inc. 2018

Materiality?

South Dakota v. Wayfair

Some Relevant Q&A

© Miles Consulting Group, Inc. 2018

Question 1:

Q: Since this case is about “economic nexus”,

does that mean physical presence doesn’t

matter anymore?

A: No. Physical presence DOES still matter.

© Miles Consulting Group, Inc. 2018

Question 2:

Q: Do we need to start filing in the 45 states

that have a sales tax immediately?

A: You may not have to file in all states

immediately, but it’s time to do some serious

analysis.

© Miles Consulting Group, Inc. 2018

Question 3:

Q: Does this case address retroactivity? Are

we going to have to go back many years and

pay prior years’ taxes?

A: The South Dakota statutes (and most

others) were written for no retroactivity.

But…there’s still some retroactive exposure to

consider.

© Miles Consulting Group, Inc. 2018

Question 3 (continued):

Q: Does this case address retroactivity?

A1: If you had physical presence before and

ignored it, it’s not going away and you may

have exposure.

A2: It’s January 2019. Many states have

required filing since late 2018. Now you MAY

have retroactive exposure!

© Miles Consulting Group, Inc. 2018

Question 4:

Q: Does this case relate to internet sellers

only?

A: It sounds like it does, but the answer is NO.

© Miles Consulting Group, Inc. 2018

Question 5:

Q: If we are a SaaS, software, or services

company, could we be affected by this

decision?

A: Absolutely! The ruling made it easier to

have nexus – it doesn’t impact the taxability of

the product.

© Miles Consulting Group, Inc. 2018

Question 6:

Q: Have other states already jumped on the “Wayfair

bandwagon” and crafted similar legislation?

A: Yes. As of 01/15/19 – the following 37 states have

indicated they have economic nexus statutes similar to

Wayfair:

HI, ME, VT (7/1/18); MS (9/1/18); NC, NJ, SC, SD (11/1/18); CO, CT (12/1/18)

AL, IN, IL, KY, MD, MI, MN, ND, WA, WI (all 10/1/18);

GA, IA, LA, NE, UT, WV (1/1/19);

CA (4/1/19); TX (10/1/19)

Officially “Pending”: NV, TN, WY

Some special states: MA, OH, OK, PA, RI, NY (varying dates & thresholds)

© Miles Consulting Group, Inc. 2018

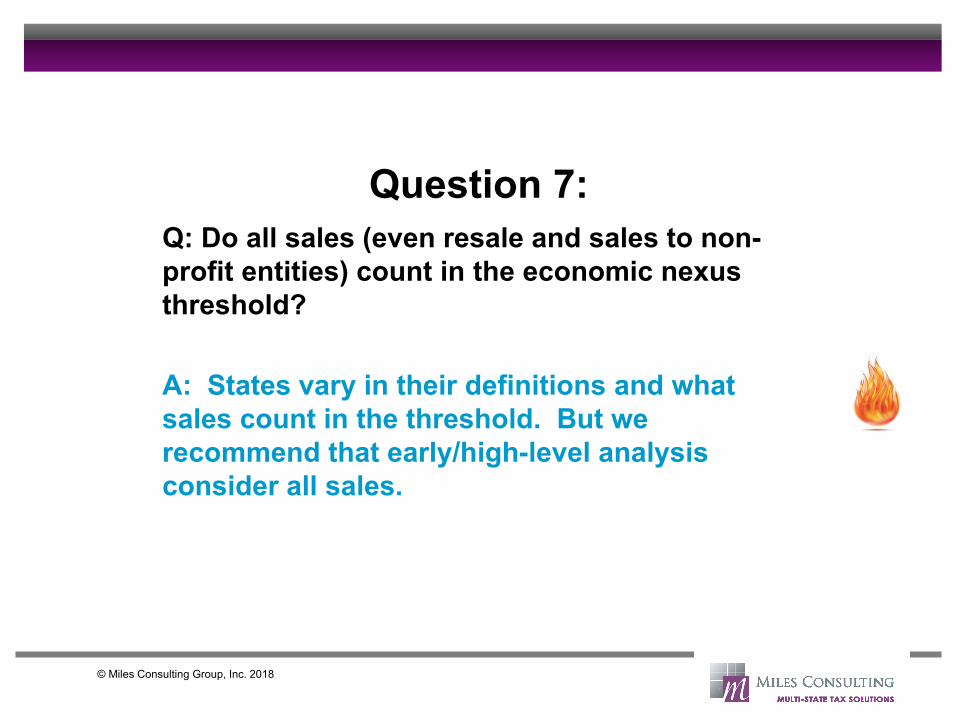

Question 7:

Q: Do all sales (even resale and sales to non-

profit entities) count in the economic nexus

threshold?

A: States vary in their definitions and what

sales count in the threshold. But we

recommend that early/high-level analysis

consider all sales.

© Miles Consulting Group, Inc. 2018

Question 8:

Q: How do you count a “transaction” to get to

the 200 transactions? By invoice, or line item,

or some other way?

A: While some interpretation by state is still

recommended, it appears that most states will

defer to: an invoice = a transaction.

© Miles Consulting Group, Inc. 2018

Question 9:

Q: What’s likely to happen next at the state or

federal level?

A1: At the state level, we anticipate the

remainder of the states to enact economic nexus

laws. (Most already have.)

A2: Congress could still go back and

codify Quill or enact other legislation.

But will they? It’s unlikely!

© Miles Consulting Group, Inc. 2018

Question 10:

Q: What do we recommend as next steps for

clients?

• Begin the nexus/taxability question TODAY

(or yesterday!)

• Perform a nexus study

• Track upcoming economic nexus legislation

• Be prepared to develop a compliance

system

© Miles Consulting Group, Inc. 2018

Why It’s Important?

“Sales tax is a pass through tax. The thing that

concerns most companies is the burden and cost

of collection and remittance of the taxes”

© Miles Consulting Group, Inc. 2018

Collecting & Remitting = Compliance

Compliance 101

• Nexus?

• Rate?

• Exemptions?

• Registration

• Forms - Electronic vs. Paper

• Due Dates (vary)

© Miles Consulting Group, Inc. 2018

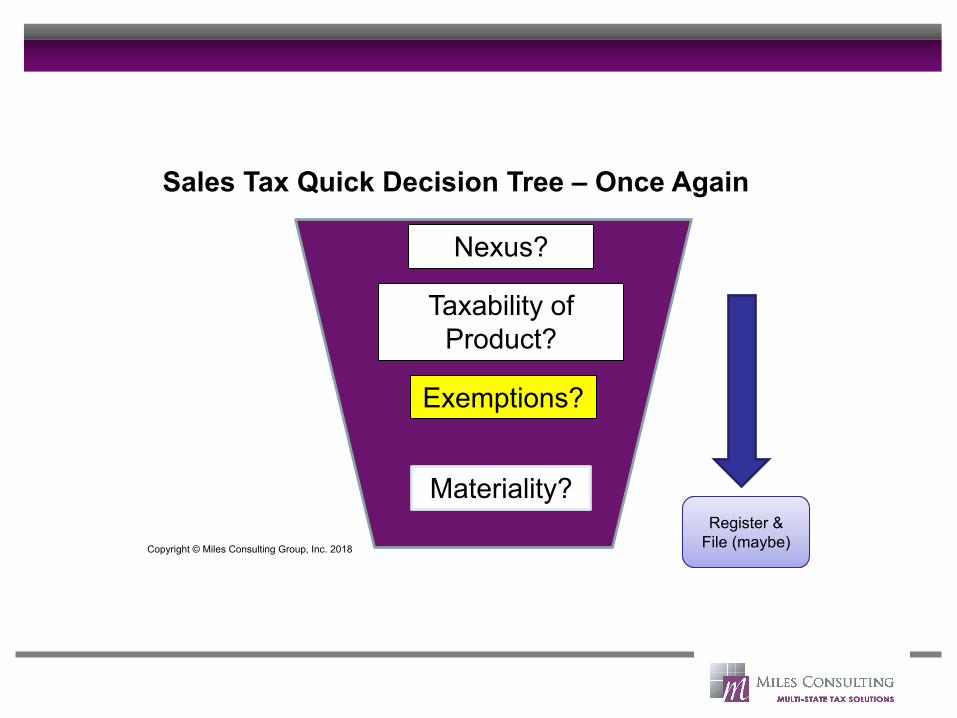

Sales Tax Exemptions

Nexus?

Taxability of

Product?

Exemptions?

Sales Tax Quick Decision Tree – Once Again

Register &

File (maybe)

Register &

File (maybe)Copyright © Miles Consulting Group, Inc. 2018

Materiality?

© Miles Consulting Group, Inc. 2018

Sales of TPP & Services

• In general, unless otherwise exempt,

sales of TPP are subject to sales tax.

• In general, unless specifically

enumerated, sales of services are

exempt

BUT

• States are increasing enumerated

services or broadening the definitions

© Miles Consulting Group, Inc. 2018

Sales Tax Exemptions

• Due to the nature of the buyer

• Nature of the property/service

transferred/performed

• Intended use by the purchaser

• Nature of the transaction

© Miles Consulting Group, Inc. 2018

Sales Tax Exemptions

Due to the nature of the buyer:

• US Government

• Some state governments

• Some exempt entities

© Miles Consulting Group, Inc. 2018

Sales Tax Exemptions

Due to the nature of the property or service

transferred/performed:

• Food

• Medical

• Manufacturing

© Miles Consulting Group, Inc. 2018

Sales Tax Exemptions

Due to the intended use by the purchaser:

• Resale

• Manufacturing

• Construction

• Pollution Control

© Miles Consulting Group, Inc. 2018

Sales Tax Exemptions

Due to the nature of the transaction:

• Load & Leave Software

• Cloud applications (SaaS)

© Miles Consulting Group, Inc. 2018

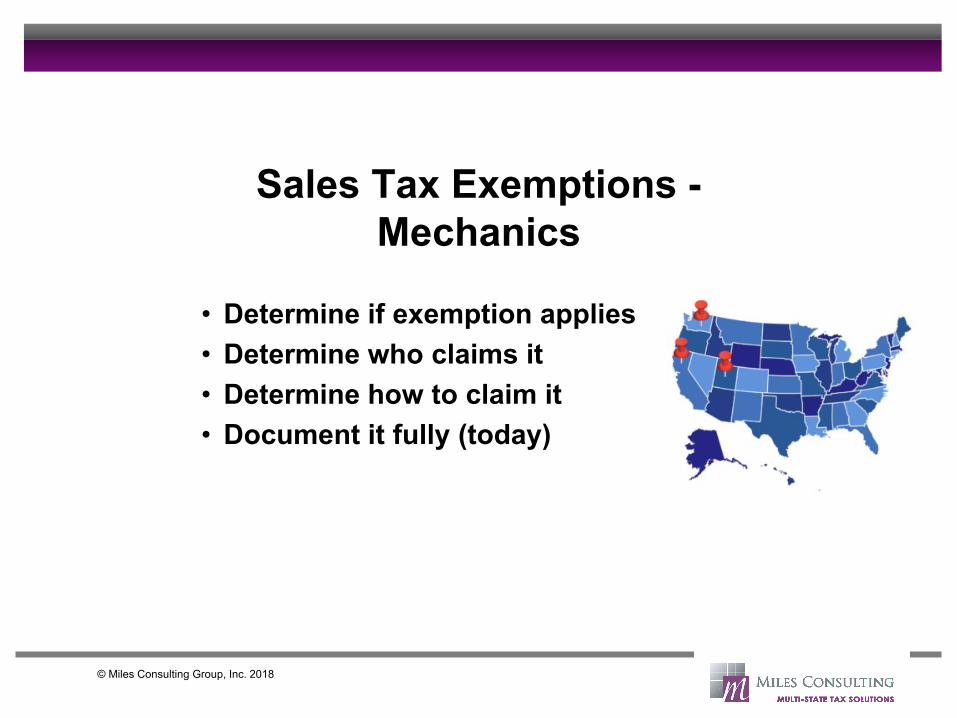

Sales Tax Exemptions -

Mechanics

• Determine if exemption applies

• Determine who claims it

• Determine how to claim it

• Document it fully (today)

Situs and Sourcing Transactions

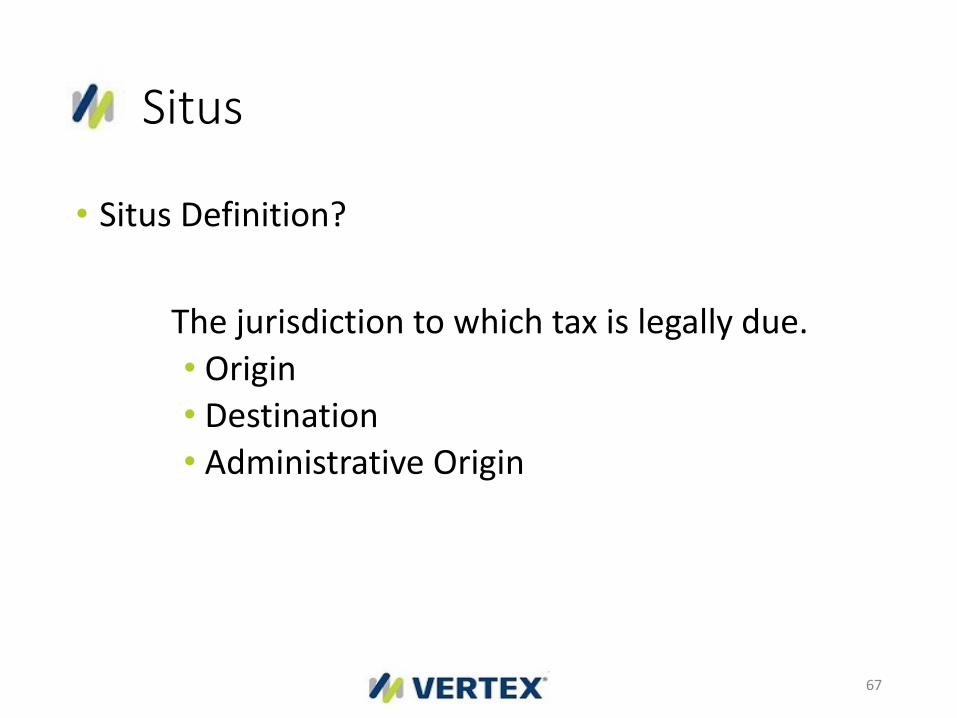

Situs

• Situs Definition?

The jurisdiction to which tax is legally due.

• Origin

• Destination

• Administrative Origin

67

Situs on Goods vs. Service

• Situs rules are different for sales of Tangible Personal Property (goods) vs. sale of services.

68

This Photo by Unknown Author is licensed under CC BY-NC-ND

Situs Rules on Goods vs. Service

• Situs Rule on Goods• Interstate Transactions

- Situs determination is ship to location

• Intrastate Transactions- Situs determination depends on state

• Destination states

• Origin states

• Modified origin states

69

• Situs Rule on Services• Situs is determined by:

• Where received

• Where performed

• Where enjoyed

Situs on Interstate Transactions

• Goods shipped from one state and delivered across state lines to another state

• Taxing situs is where the goods are consumed

70

List of Origin and Modified Origin States

71

Situs: Intrastate Transaction on Sale of Goods in Origin State

72

• Ship-to is Erie, PA and physical origin is Philadelphia, PA

• Pennsylvania is an origin state

• Taxing Situs is?

• Origin: Philadelphia, PA

• Tax type is?

• Sales Tax

Situs – Some Things to Keep in Mind

Once you registered with a state:

• Review whether or not the state is an origin or

destination state (for local tax application)

• Review whether or not you have any physical presence

in the state

• Determine software requirements for correct situs

determination outcomes

73

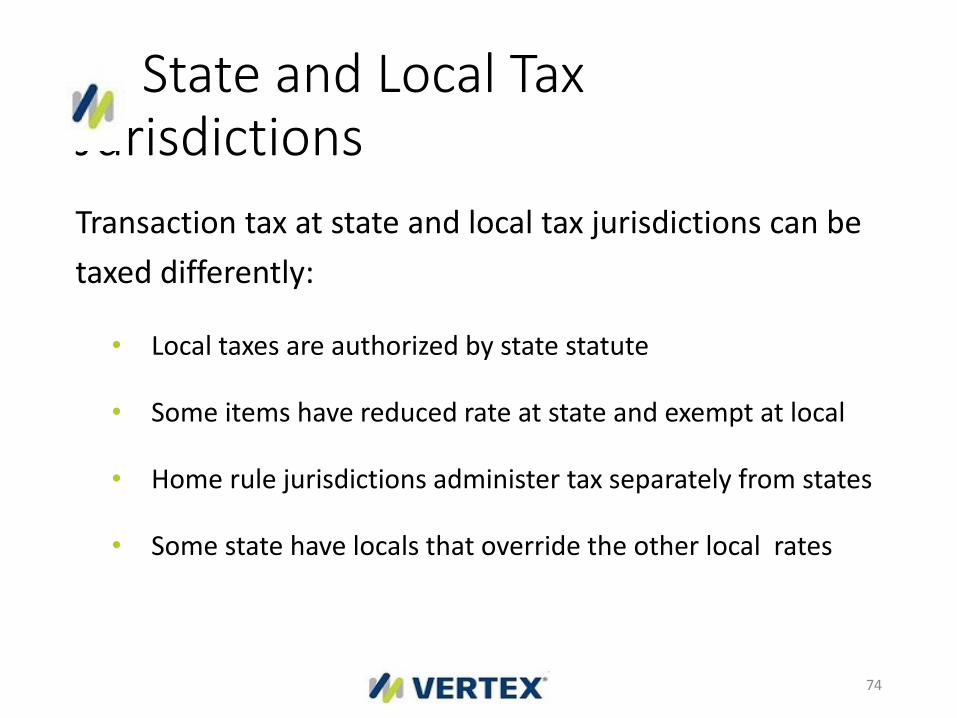

State and Local Tax Jurisdictions

Transaction tax at state and local tax jurisdictions can be

taxed differently:

• Local taxes are authorized by state statute

• Some items have reduced rate at state and exempt at local

• Home rule jurisdictions administer tax separately from states

• Some state have locals that override the other local rates

74

Situs Determination for Intrastate Transactions in Colorado

Colorado wants to know the vendor’s relationship with the buyer

• Does the vendor have a physical location in the same county as the buyer?

• Does the vendor have a physical location in the same city as the buyer?

• If yes, collect sales tax in destination

• If no, collect seller’s use tax in destination

75

Revenue Agency Administration of Sales Tax

Filing Frequency

• State and local filing frequencies• Monthly, quarterly, semi-annually or annually

• Each jurisdiction has its own guidelines – frequency can change

• Thresholds• Dollar amounts

• Time period

• Registrations• Initial frequency

77

E- Electronic Filing (E-Filing)

• State and local jurisdictions may require e-filing of returns

• Automated solutions – save time and money

• Manual filing – takes more time and increase risk of error

• Third-party providers• Reduce compliance burden

• Simplify filing process

• Provide reconciliations

78

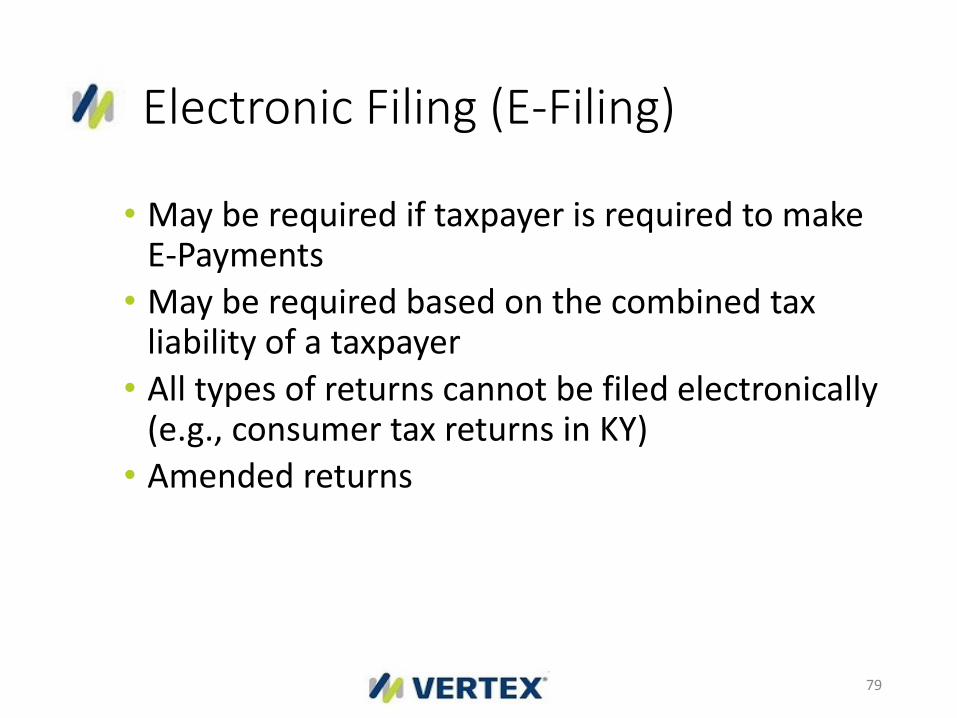

Electronic Filing (E-Filing)

• May be required if taxpayer is required to make E-Payments

• May be required based on the combined tax liability of a taxpayer

• All types of returns cannot be filed electronically (e.g., consumer tax returns in KY)

• Amended returns

79

E- Payment

• State and local jurisdictions may require E-Payments

• Dollar amount thresholds

• May be required based on the combined tax liability of a taxpayer

• Automated solutions – save time and money

• Manual filing – takes more time and increase risk of error

• Third-party providers

• Reduce compliance burden

• Simplify payment process

• Provide reconciliations

80

V Vendor Compensation

• Some states offer vendor compensation or a “discount” to taxpayers

• Timely filing (due date in most states is the 20th of the month following reporting period)

• Compensation is calculated on the amount of tax the vendor has collected

• Compensation/Discount may be limited by dollar amount per return or period (See Federation of Tax Administrators – State Sales Tax rates and Vendor Discounts List - January 2019)

81

States with Sales Discounts

• The following states have sales tax discounts:

• AL, AZ, AR, FL, GA, IL, IN, KY, LA, MD, MI, MS, MO, NE, NV, NY, ND, OH, PA, SC, TN, TX, UT, VA, WI, WY

82

Vendor Compensation Example

• Calculate the amount of tax the vendor has collected for the state of Georgia.

• Multiply the total tax collected by 3 percent, or ".03."

• Subtract $90 from the total, and multiply the remaining total by .167. The vendor compensation in Georgia only applies to 3 percent of the total tax collected up to $90, which is based on collecting the first $3,000. Anything collected above $3,000 is based on 1/2 of 1 percent, or .005, of the tax collected. This compensation is accrued on a monthly basis.

83

© Miles Consulting Group, Inc. 2018

Some Final Thoughts…

© Miles Consulting Group, Inc. 2018

Some Final Thoughts

• Don’t be on Defense (Offense is

always better)

• Wayfair developments don’t change

retroactive exposure that might exist

as a result of prior physical presence

nexus

• Income tax questions will arise as

well!

© Miles Consulting Group, Inc. 2018

Some Final Thoughts…

Miles Consulting is a resource:

• Monthly Newsletter

• Weekly topical blog

• ½ hour Complimentary Consultations

© Miles Consulting Group, Inc. 2018

How Can Miles Consulting Help You

Provide Client Value?

• Perform Nexus Reviews

• Perform Taxability Studies

• Determine Appropriate Exemptions

• Wayfair/economic nexus navigation

• M&A Due Diligence

© Miles Consulting Group, Inc. 2018

Sign up for our newsletter &

Preview our State Tax Checklist Here

http://www.milesconsultinggroup.com/CPA-checklist-signup.html

© Miles Consulting Group, Inc. 2018

In Summary

It’s a crazy, interesting time

• States are aggressively pursuing

revenue (really!)

• Wayfair ruling has changed the game

• Multi-state companies have interesting

issues (and usually need help)

• Don’t go it alone!

© Miles Consulting Group, Inc. 2018

Questions

© Miles Consulting Group, Inc. 2018

Thank You!

Monika Miles(408) 266-2259

http://www.milesconsultinggroup.com

C Contact

• Joseph F. Geiger, Jr., Esq., CPA, MST, MSA• Vertex Consulting

• Telephone: 484.595.6353

• Email: [email protected]

https://www.vertexinc.com

92

Questions?