Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES AND

ANALYST CERTIFICATIONS.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

Global Securitized Products Weekly Securitized Products Strategy

Agency MBS

We maintain our short basis recommendation based on weak risk/reward. The Basel

committee softened its leverage ratio proposal, which reduces the SLR denominator and

would be incrementally positive for bank MBS demand if US regulators follow with similar

rules. We explore valuations in Agency CMOs across the curve and compare them with

pass-throughs and CMBS AAA.

Non-Agency MBS

For the last few years, the defining, and at times lone, driver of prepayment speeds in the

non-agency space has been equity position, but another variable remains: a potentially

expanding credit box. Using data provided by current mortgage issuance, we believe the

credit box is slowly beginning to open. We see this effect most amplified in post-reset Alt-A

ARMs, where always current speeds doubled in the second half of 2013, controlling for IO

status. We believe this is likely to continue into 2014.

CMBS

Market activity slowed to a near halt over the past two days, with many members of the

CMBS community attending the semi-annual CREFC conference. We thought the overall

tone was fairly optimistic. While there were definitely some concerns that were highlighted

and frequently discussed, our sense was at the market consensus remains reasonably

bullish. We discuss some of the more prevalent themes. We also take a look at the CMBS

exposure to JCP’s store closure announcement, CRE price changes in November, fourth

quarter real estate fundamentals and news on the 11 Madison Avenue loan.

Modeling and Analytics

Monthly Locus non-agency model report: high actual house price appreciation in 3Q 2013

leads to lower cumulative defaults and severities projections for January 2014; model

default rates undershot for Option ARM due to lower REO to liquidation rates; modification

rates for subprime loans continue to drop while share of principal forgiveness among all

modification types is increasing.

Research Analysts

GLOBAL HEAD

Roger Lehman +1 212 325 2123 [email protected]

AGENCY MBS

Mahesh Swaminathan +1 212 325 8789 [email protected]

Qumber Hassan +1 212 538 4988 [email protected]

Vikram Rao +1 212 325 0709 [email protected]

NON-AGENCY MBS/CONSUMER ABS

Marc Firestein +1 212 325 4379 [email protected]

CMBS

Roger Lehman +1 212 325 2123 [email protected]

Sylvain Jousseaume, CFA +1 212 325 1356 [email protected]

Serif Ustun, CFA +1 212 538 4582 [email protected]

EUROPEAN UPDATE

Carlos Diaz +44 20 7888 2414 [email protected]

MODELING AND ANALYTICS

David Zhang +1 212 325 2783 [email protected]

Table of Contents

Core Views 2

Agency MBS 3

Non-Agency MBS 10

CMBS 13

Modeling and Analytics 30

Focus on Locus 39

16 January 2014

Fixed Income Research

http://www.credit-suisse.com/researchandanalytics

FOR INSTITUTIONAL CLIENT USE ONLY

Focus on Locus New! CLO Bid List Calendar

www.credit-suisse.com/ locus

16

Ja

nu

ary

20

14

Glo

bal S

ecuritiz

ed

Pro

ducts

Weekly

2

Core Views Sector Trends Trade Ideas

Agency MBS Short MBS basis

Sell FN 3.5 vs. 5-yr and 10-yr swaps

Sell G2/FN 3.5 swap

Buy IOS 4.5 2010 versus rates

Housing

The rebound in housing should continue, albeit at a more moderate pace; we project gains of roughly 5% (FHFA all transaction) and 10% (Case Shiller) in 2014. We expect most of the major drivers behind the recent recovery in home prices to remain in place in 2014. We believe the slowdown in momentum is largely driven by two factors: a decline in affordability and a decline in distressed supply.

Prepayment We project roughly 20% and 18% drops in 30-year and 15-year speeds in January, respectively, driven by higher rates and weaker seasonality.

Non-Agency MBS

BWIC volumes were once again high heading into the ING list, with over $500MM out for bid on Tuesday and Wednesday. Prices across all sectors were modestly stronger. Post-reset Alt-A prepayment speeds, on the back of slightly more credit availability, are picking up across all LTV buckets.

We are slightly cautious at these levels, though we believe the next short-term move is slightly tighter. The credit curve remains flat.

We prefer a barbelling strategy of higher- and lower-beta sectors.

We prefer post reset clean Prime/Alt-A hybrids and fixed rate Alt-As among low-beta sectors. Longer reset clean Alt-A hybrids offer prepay and housing upside among lower-beta bonds.

CMBS

Market activity slowed to a near halt over the past two days, with many members of the CMBS community attending the semi-annual CREFC conference. We thought the overall tone was fairly optimistic. While there were definitely some concerns that were highlighted and frequently discussed, our sense was at the market consensus remains reasonably bullish. We discuss some of the more prevalent themes. We also take a look at the CMBS exposure to JCP’s store closure announcement, CRE price changes in November, fourth quarter real estate fundamentals and news on the 11 Madison Avenue loan.

Wider trading AMs remain our favorite trade and appear attractive to corporates, and other legacy CMBS. We also believe that some better quality AJs should be considered.

Differentiation is needed on premium super-seniors but some shorter duration bonds, like the A1As, are attractive.

Single-borrower deals have widened relative to new issue conduit and look attractive

We are concerned about newly issued BBB- bonds given the coming supply. Single-A bonds and super-seniors appear relatively more attractive.

Source: Credit Suisse

16 January 2014

Global Securitized Products Weekly 3

Agency MBS Strategy

We maintain our short basis recommendation based on weak risk/reward. MBS

valuations have richened to near six-month highs catalyzed by continued 100+% Fed

takeout and more recently a sharp drop in volatility. This could reverse heading into

FOMC at month-end. The possibility of a deferral of the Fed’s next decrement in MBS

purchases is a risk to our view.

The Basel committee softened its leverage ratio proposal from last year this week.

These changes reduce the SLR denominator and would be incrementally positive for

bank MBS demand if US regulators follow with similar rules. However, they are not a

game changer because SLR is only one factor in a multi-dimensional investment

decision process for banks.

We explore valuations in Agency CMOs across the curve and compare them with

pass-throughs and CMBS AAA. In short-duration CMOs, we find value in bonds backed

by HARP-eligible collateral compared to jumbo collateral, and substantially tighter

valuations on PACs compared to busted PACs. Intermediate PACs offer significant

yield, OAS and total return pick-up compared to shorter cashflows, and have positive

returns when hedged with pass-throughs. Longer duration bonds are trading at attractive

valuations, but are likely to remain cheap until investors gain more comfort with rates.

Trade recommendations

Hold short MBS basis (sell $75MM FN 3.5, receive on $30MM 5-yr and $43.8MM 10-yr

swap) at a loss of 13 ticks (3 December 2013, MBS Trade Note).

Took partial profits on buy IOS 4.5 2010 versus 10-yr swap (buy $25MM IOS 4.5

2010 hedged with 10-yr swap using a 66% hedge ratio). Closed half the trade at a profit

of 30+ ticks with carry (15 January 2013, MBS Trade Note).

Hold sell G2/FN 3.5 swap ($50MM), based on rich valuations relative to a deteriorating

supply/demand outlook (21 November 2013, MBS Trade Note). This trade is down

4 ticks since initiation.

Hold buy FN 4 fly ($50MM), based on cheap valuations (2 January 2014, MBS Trade

Note). This trade is up 5 ticks since initiation.

Exhibit 1: Current trade recommendations

Actual P&L of open trades should be slightly lower as this does not reflect bid/offer spread

Trade Idea Start Date P&L

P&L

(ticks)

Short MBS basis (Sell $75MM FN 3.5, receive on $30MM 5-

yr and $43.8MM 10-yr swap)21-Aug-13 (305,086) (13)

Sell G2/FN 3.5 swap ($100MM) 21-Nov-13 (128,906) (4)

Long FN 4.0 fly ($50MM) 2-Jan-14 74,218 5

Total P&L of open trades (359,774)

Total P&L of trades closed YTD 358,125

Note: Pricing date: Jan 14, 2014.

Source: Credit Suisse

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at the original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments may be subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. The P&L results shown do not include relevant costs, such as commissions, interest charges, or other applicable expenses

Mahesh Swaminathan

+1 212 325 8789

Qumber Hassan

+1 212 538 4988

Vikram Rao

+1 212 325 0709

16 January 2014

Global Securitized Products Weekly 4

Weak NFP potentially a fluke, Vol decline has helped MBS, but could reverse, stick with basis underweight

We maintain an underweight stance on the MBS basis. Our reasons (rich valuations, low

carry, and more downside than upside) remain in place. The sharp drop in last Friday’s

NFP is inconsistent with all other economic data, suggesting that it may have been

either a statistical fluke or simply erroneous. We place a high probability that it will be

revised away next month. Such an outcome could catalyze a meaningful sell-off/spread

widening, in our view.

Exploring drivers of recent MBS performance, we find that the first leg of post FOMC

tightening was an outright narrowing of OAS (Exhibit 2), which was potentially driven by a

continued high Fed takeout (Exhibit 3). More recently, a sharp drop in volatility has likely

been an additional catalyst (Exhibit 4).

This decline in volatility has arguably encouraged investors to infer a narrow trading

range in spreads. However, this could reverse sharply if rate volatility picks up,

potentially heading into FOMC at month end. Therefore, risk/reward in MBS longs

remains weak, in our view.

The risk to our view is a scenario in which the FOMC defers additional reductions at the

January meeting to await actual post-taper implementation economic data (please see last

week’s publication for a detailed discussion). The impact of such a step could be a another

leg of rally/tightening given the near consensus view among market participants

(supported by comments by several Fed officials) that the FOMC will announce the next

decrement this month. Although we share the consensus view as the base case, we place

a roughly 20% probability of the risk scenario being realized.

Exhibit 2: The initial outperformance following December FOMC was an outright OAS tightening

30 Oct 13 30 Nov 13 30 Dec 13

-0-240

-0-160

-0-080

0-000

0-080

5.0

7.5

10.0

12.5

15.0

17.5

20.0

Perf

orm

ance (

32nds)

Vol (b

p/y

r, R

EV

ER

SE

SC

ALE

)

FN 3.5 hedged perf FN 3.5 LOAS

December

FOMC

Source: Credit Suisse

16 January 2014

Global Securitized Products Weekly 5

Exhibit 3: Expected Fed takeout exceeding 100% during Q1 arguably supported the first leg of the post FOMC tightening

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Fe

d's

ta

ke

ou

t

FN 30

Total MBS

Actual Projection

Source: Credit Suisse

Exhibit 4: The sharp drop in vol in 2014 has further catalyzed MBS performance

30 Oct 13 30 Nov 13 30 Dec 13

-0-240

-0-160

-0-080

0-000

0-080

92.5

95.0

97.5

Pe

rfo

rma

nce

(32

nd

s)

Vo

l (b

p/y

r, R

EV

ER

SE

SC

AL

E)

FN 3.5 hedged perf 3y10y annual bp vol

December

FOMC

Source: Credit Suisse

16 January 2014

Global Securitized Products Weekly 6

Softened Basel leverage ratio framework an incremental positive MBS, but not a game changer

The Basel Committee (BCBS) issued an updated Basel III leverage ratio framework on

12 January 2014 after incorporating comments on the consultative document released in

June 2013.

This newly released BCBS framework softens the originally proposed leverage ratio

requirements by reducing the expansion of the denominator due to off-balance sheet

items. US rules proposed last August suggest that regulators may adjust the calculation of

the SLR denominator based on this BCBS framework, although the overall ratio

requirement is likely to remain higher for US GSIBs. .

These changes are incrementally positive for bank MBS demand because they diminish

the pressure on banks to scale back their balance sheet. However, they are not a game

changer because SLR is only one factor (often not the gating factor) in the multi-

dimensional investment decision process for banks. Other important factors include OCI

volatility, risk weighted capital ratios and LCR requirements. At the margin, this softening

of leverage ratio requirements (assuming US regulators follow BCBS) should diminish the

potentially heavy bias in favor loans over MBS that we cited in our 2014 Outlook.

Key changes to the BCBS framework and impact:

1) Limited netting of repos and reverse repos: The final standard allows netting of

repos in calculating with the same counterparty when specific conditions are met. This

brings it in line with US SLR, which allows netting of repos for same

counterparty/same collateral/same maturity transactions.

This change is most beneficial for non-US banks, but only benefits US GSIBs to the

extent that it removes the overhang of adverse treatment under international rules.

Please see notes from the September 2013 meeting of the Federal Advisory Council

and Board of Governors for a detailed discussion of this issue.

We note that some market participants have inaccurately assumed that US SLR does

not offer netting and pointed to this as a threat to MBS repo availability (and attendant

negative consequences to REIT MBS demand). We have never subscribed to this

thesis, but the latest BCBS change may cause a revision of such views.

2) Use credit conversion factors from Basel Standardized Approach for credit risk

instead of a fixed 100% multiplier to convert off balance sheet exposure to on balance

sheet equivalent.

This should help reduce the denominator broadly, but especially favor lower risk

weight exposures.

3) Cash variation margin associated with derivative exposures may be used to

reduce the exposure measure for leverage ratio. This should incrementally reduce

the denominator for SLR.

4) A clearing member's trade exposures to qualifying central counterparties

(QCCPs) associated with client-cleared derivatives transactions may be

excluded when the former does not guarantee the latter’s performance. This should

help reduce the balance sheet impact of such transactions.

16 January 2014

Global Securitized Products Weekly 7

Relative value in CMOs across the curve We explore valuations in Agency CMOs across the curve and compare them with pass-

throughs and CMBS AAA. In short duration CMOs, we find value in bonds backed by

HARP-eligible collateral compared to jumbo collateral, and substantially tighter valuations

on PACs compared to busted PACs. In comparison to short duration CMOs, higher

coupon 30-year passthroughs look attractive and 15-years passthroughs look fair to rich.

Intermediate PACs offer significant yield, OAS and total return pick-up compared to

shorter cashflows, and have positive returns when hedged with pass-throughs. We

recommend intermediate PACs for investors willing to moderately extend out the curve.

Longer duration bonds are trading at attractive valuations, but are likely to remain cheap

until investors gain more comfort with rates.

Short duration CMOs off HARP-eligible collateral looks attractive

In short-duration conventional CMOs, we recommend buying bonds backed by HARP-

eligible collateral due to attractive valuations and significant burnout in HARP speeds over

the last few months. These bonds offer attractive yield, OAS and total return compared to

other short duration CMOs, and the total return profile remains attractive in +50bp/-50bp

rate scenarios (Exhibits 5, 6 and 7). We believe that short-duration bonds off HARP-

eligible collateral are especially attractive compared to those backed by jumbo collateral

which have a worse convexity profile.

In short-duration Ginnie CMOs, there is a significant spread differential between PACs and

busted PACs/sequentials (for similar collateral). Investors are paying up for the extension

protection offered by a PAC structure given the selloff bias in the market, in our view. For

investors with a range-bound view on rates, we recommend buying short duration busted

PACs/sequentials over PAC structures.

Higher coupon 30-year TBA look attractive compared to short duration CMOs

In comparison to short duration CMOs, higher coupon 30-year passthroughs look cheap.

For example, FN 5.5s offer significant yield and OAS pick-up compared to similar duration

CMOs. We note that FN 5.5s are relatively unaffected by an extension of the HARP cutoff

date and have experienced significant burnout in speeds over the last few months. In

contrast to 30-years, similar duration 15-year passthroughs look fair to rich compared to

short duration CMOs.

Intermediate PACs offer attractive yield, OAS and total return pick-up

We recommend buying intermediate PACs for investors looking to go further out the curve.

We believe that these bonds offer meaningful yield and spread pick-up compared to

shorter cashflows, in addition to attractive total returns. Furthermore, projected returns

remain positive even after after hedging out duration with TBA. For example, the 4/Gold 4

PAC bond in Exhibit 5 has a base case total return of 4.4% and a 9 year OAD. If this bond

is hedged at 125% versus FN 3.5s, the 12-month hedged return is marginally positive

(4.4% - 3.2%*125% = 0.4%).

Longer duration CMOs offer attractive valuations, but likely to remain cheap in the

short term

Longer duration CMOs offer significant yield, spread total return pick-up. In particular, the

Z bond in Exhibit 5 (with roughly 20 OAD) has an 8.9% 12-month return in the base case.

However, the key risk in these bonds is a sharp selloff, which can erode returns

significantly. These longer cashflows are likely to remain cheap while investors are

concerned about a selloff, and can tighten subsequently.

We note that compared to new issue CMBS AAA, similar average life CMOs are trading at

only marginally lower yields. For example, the 11.5 average life VADM (4s off CQ 4s) only

concedes roughly 10bp of yield to its new issue CMBS counterpart (10-year average life).

Adjusting for the slightly longer average life of this VADM, the effective yield concession is

roughly 30bp. Given the GSE guarantee, Agency CMOs potentially offer an attractive

alternative at current valuations, in our view.

16 January 2014

Global Securitized Products Weekly 8

Exhibit 5: Relative value in CMOs compared to passthroughs

Valuations as of 1/13/2014 close; +50bp/-50bp scenarios based on gradual rate shock

Sector Security WALA Avg Life Yield

1-yr CPR

(projected) OAS OAD

-50bp base +50bp

Short Ginnie 3/G2SF 5, BPAC 44 2.4 1.4 15 5 2.4 2.2 1.5 0.8

3.5/G2SF 5, PAC 32 3.9 1.9 17 (26) 4.4 3.8 2.2 0.4

Short conventional 3.5/CK 4, BPAC 28 2.7 1.8 14 3 1.9 2.0 2.8 -0.5

4.5/Gold 5, BPAC 98 3.8 2.4 21 13 3.2 4.9 4.1 2.4

Intermediate 4/Gold 4, PAC 40 8.9 3.4 9 39 9.0 8.4 4.4 0.2

LCF 4/4, BPAC 26 20.0 4.1 10 47 14.2 11.2 4.4 -2.2

3/LLB Gold 4.5, BPAC 40 20.6 4.1 10 50 15.2 11.9 4.5 -2.6

VADM 4/CQ 4, VADM 9 11.5 3.7 6 37 10.2 9.0 4.4 -0.3

Z 3.5/G2 3.5, Z 13 18.5 4.4 5 37 20.6 18.8 8.9 -0.7

30-yr TBA FNCL 3.5 9 9.0 3.4 6 18 7.2 6.2 3.2 0.0

FNCL 4 5 7.8 3.3 7 10 6.2 5.4 3.1 0.4

FNCL 4.5 31 6.3 3.2 20 11 4.5 4.1 2.6 0.7

FNCL 5 66 4.7 2.8 24 18 3.5 3.4 2.4 1.0

FNCL 5.5 72 3.9 2.6 28 30 2.8 3.0 2.3 1.2

15-yr TBA FNCI 3 3 5.6 2.4 7 (16) 4.7 4.3 2.6 0.7

FNCI 3.5 10 4.7 2.3 13 (19) 3.9 3.5 2.3 0.8

FNCI 4 47 3.7 2.1 18 9 3.2 3.2 2.2 1.0

Constant Forward

TRR (%)

(12-mo horizon)

Source: Credit Suisse

Exhibit 6: Yield/average life comparison in CMOs, passthroughs and CMBS

Valuations as of 1/13/2014 close

BPAC

SEQBPAC

BPAC

PAC

LCF

LCF

VADM

Z

FN3.5 FN4

FN4.5

FN5FN5.5

DW3

DW3.5DW4

CMBS AAA 30%CE

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

- 5.0 10.0 15.0 20.0 25.0

Yie

ld (

%)

WAL

Source: Credit Suisse

16 January 2014

Global Securitized Products Weekly 9

Exhibit 7: OAS/OAD comparison in CMOs and passthroughs

Valuations as of 1/13/2014 close

BPAC

PAC

BPAC

BPAC

PAC LCF

LCF

VADM Z

FN3.5

FN4 FN4.5

FN5

FN5.5

DW3

DW3.5

DW4

(40)

(30)

(20)

(10)

-

10

20

30

40

50

60

- 5.0 10.0 15.0 20.0 25.0

OA

S (

bp

)

OAD

Source: Credit Suisse

16 January 2014

Global Securitized Products Weekly 10

Non-Agency MBS Speeding up: post-reset Alt-A ARMs and an expanding credit box

For the last few years, the defining, and at times lone, driver of prepayment speeds in

the non-agency space has been equity position. While that remains the major driver of

prepayment speeds, in our view, the sustained rate selloff of the last six months

provides an opportunity to see which collateral might withstand higher mortgage rates.

However, another variable remains an important piece of the puzzle: a potentially

expanding credit box.

Using data provided by current mortgage issuance, we believe the credit box is slowly

beginning to open. We see this effect most amplified in post-reset Alt-A ARMs, where

always current speeds doubled in the second half of 2013, controlling for IO status

(Exhibit 8). Given their currently low WAC but comparatively higher margins, we believe

this trend is likely to continue in 2014 and provide support for Alt-A ARMs.

Exhibit 8: Always current post-reset Alt-A ARMs vCPRs have doubled recently

Always current on an OTS basis, three-month averages

2

4

6

8

10

12

vC

PR

Amortizing

IO

Source: Credit Suisse, Loan Performance

Mortgage Credit – Data suggest the box is slightly expanding

To see how much the mortgage credit box is expanding, we turn to the Ellie Mae

Origination Insight Report to look at both loan closings as well as rejected application

characteristics. The data included in the report cover almost 10% of mortgage originations

in the US, as well as breaking out loan type and purpose.

While the credit quality of purchase loans remains fairly steady since the start of 2013,

refinance loans, both FHA and conventional, have seen declines from their lofty peaks. In

conventional loans, we note noticeable declines in FICO to 734 and increases in back-end

DTI to 40. In addition, the average rejected loan has seen a similar change in FICO,

implying that formerly rejected loans are beginning to close. FHA refinances have seen a

similar story, although the DTI has remained fairly constant around 40.

Marc Firestein

+1 212 325 4379

Mahesh Swaminathan

+1 212 325 8789

16 January 2014

Global Securitized Products Weekly 11

Exhibit 9: The average FICO of closed refi applications has dropped 30 points this year …

Exhibit 10: And the back-end DTI has increased in recent months

Conventional refinancing applications only Conventional refinancing applications only

680

700

720

740

760

780

FIC

O

Closed

Denied

30

34

38

42

46

Back-E

nd D

TI

Closed

Denied

Source: Credit Suisse, Ellie Mae Source: Credit Suisse, Ellie Mae

Alt-A ARM prepayment speeds – increases across LTV buckets

In the last six months, we believe a combination of rising rates pulling forward prepays and

the opening credit box has led to faster Alt-A ARM prepay speeds. To properly control the

effect, we have separated IO and amortizing borrowers. Both cohorts have shown

significant increases over the last 12 months; of particular note, 80-100 LTV borrowers

have seen increases of nearly 4 CPR over the last 24 months.

Exhibit 11: vCPRs on post-reset, amortizing Alt-A borrowers has increased across all LTV buckets …

Exhibit 12: With a similar trend in post-reset, IO Alt-A borrowers

Always current on an OTS basis, mark-to-market LTV Always current on an OTS basis, mark-to-market LTV

0

2

4

6

8

10

12

14

16

2012:H1 2012:H2 2013:H1 2013:H2

vC

PR

<=80 LTV

80-100 LTV

>100 LTV

0

2

4

6

8

10

12

2012:H1 2012:H2 2013:H1 2013:H2

vC

PR

<=80 LTV

80-100 LTV

>100 LTV

Source: Credit Suisse, Loan Performance Source: Credit Suisse, Loan Performance

We have seen a modest amount of slowdown in these borrowers in the last two months,

due in part to daycount and the pull-forward effect of the May/June rate increases.

However, we believe this general upward trend is likely to continue as borrowers gain

more and more access to credit. In addition, Alt-A ARM borrowers stand to benefit from

further LTV gains, with a large portion of the always current universe between 80 and

100 LTV.

16 January 2014

Global Securitized Products Weekly 12

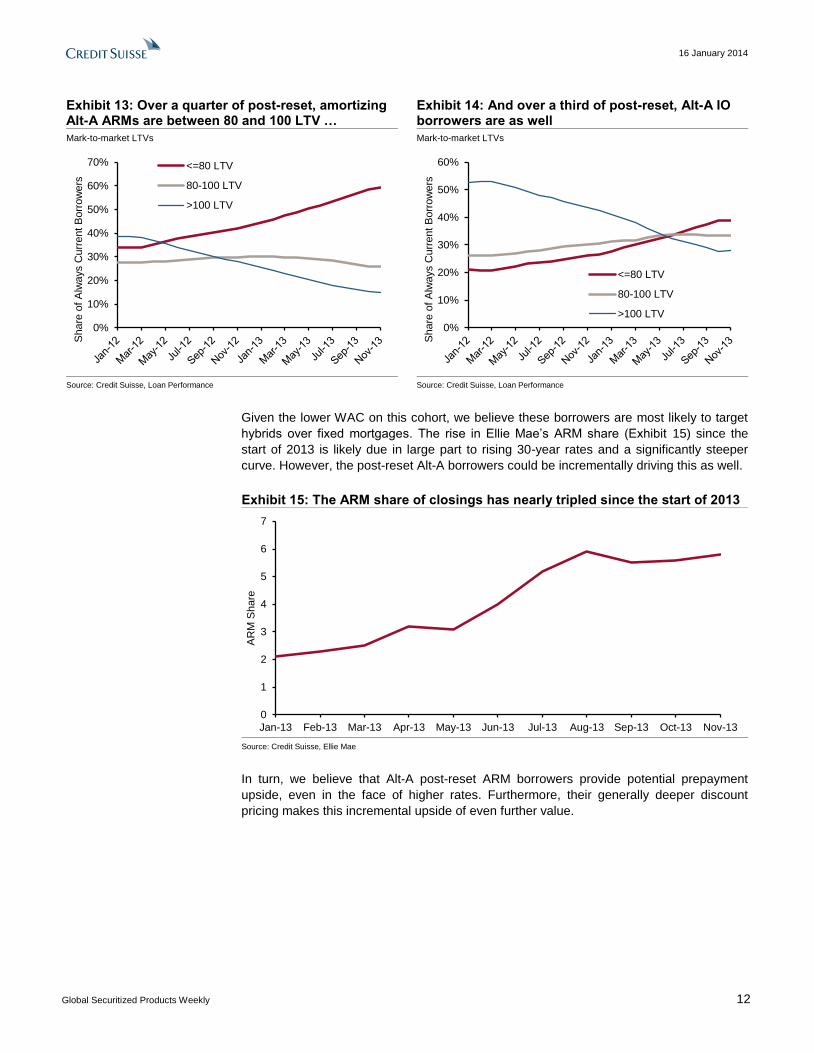

Exhibit 13: Over a quarter of post-reset, amortizing Alt-A ARMs are between 80 and 100 LTV …

Exhibit 14: And over a third of post-reset, Alt-A IO borrowers are as well

Mark-to-market LTVs Mark-to-market LTVs

0%

10%

20%

30%

40%

50%

60%

70%

Share

of

Alw

ays C

urr

ent

Borr

ow

ers

<=80 LTV

80-100 LTV

>100 LTV

0%

10%

20%

30%

40%

50%

60%

Share

of

Alw

ays C

urr

ent

Borr

ow

ers

<=80 LTV

80-100 LTV

>100 LTV

Source: Credit Suisse, Loan Performance Source: Credit Suisse, Loan Performance

Given the lower WAC on this cohort, we believe these borrowers are most likely to target

hybrids over fixed mortgages. The rise in Ellie Mae’s ARM share (Exhibit 15) since the

start of 2013 is likely due in large part to rising 30-year rates and a significantly steeper

curve. However, the post-reset Alt-A borrowers could be incrementally driving this as well.

Exhibit 15: The ARM share of closings has nearly tripled since the start of 2013

0

1

2

3

4

5

6

7

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13

AR

M S

hare

Source: Credit Suisse, Ellie Mae

In turn, we believe that Alt-A post-reset ARM borrowers provide potential prepayment

upside, even in the face of higher rates. Furthermore, their generally deeper discount

pricing makes this incremental upside of even further value.

16 January 2014

Global Securitized Products Weekly 13

CMBS

Market activity and relative value Notes from the CREFC conference Market activity slowed to a near halt over the past two days, with many members of the

CMBS community attending the semi-annual CREFC conference. Despite the lull in

trading activity, the market continued to rally over the past week. The positive sentiment at

this week’s conference helps explain the rally since the start of the year (and probably vice

versa too).

We discussed the start of the year rally, last week, which continued in the few final few

days leading up to the conference. Wider trading legacy AMs are in approximately 20 bp,

over the last week. New issue triple-Bs also tightened. We noted in last week’s edition that

this tranche off of the new issue COMM 2014-CR14 was likely to tighten from the initial

price talk of S+385 bp. The bond wound up pricing at S+360 bp and is in another 10 bp

since then.

There has been net CMBS buying, by investors, every day since the Fed’s tapering

announcement four weeks ago (19 trading days), according to TRACE data. While

volumes were low some days, due to holidays and the conference, the direction has been

consistent. Investors have added a net of $2.1 billion over this time period.

Turning back to the conference, we thought the overall tone was fairly optimistic.

While there were definitely some concerns that were highlighted and frequently discussed,

our sense was that the market consensus remains reasonably bullish, and far from

complacent, at least over the near term. This sentiment came from the overall conference

conversations but was reinforced by both the large turnout as well as the pure number of

meeting requests that we and other attendees were receiving. We highlight some of the

more prevalent themes.

Traditional CMBS investors are growing their allocation and their mix of assets

The record high attendance likely sparked one of the several often-raised questions: “are

the number of investors in the sector expanding?”. Our sense is that there are a few new

investors to the CMBS space but their participation is relatively minor compared to the

expansion of interest of the existing buyer base.

Traditional CMBS buyers seem to be expanding not only their allocation to the sector but

also the type of CMBS investments they are willing to look at. We believe that, so far, this

expansion has been a far bigger drive of demand than new entrants to the market. Most of

the expansion is centered on trying to increase yield. This includes moving further down

the credit stack in securitizations as well as a heightened interest in the mezzanine loan

market, expressed by a variety of investors and investor types.

While such demand may prove fleeting, to the extent it can be maintained, it should help

absorb the increase in supply that is expected (we are forecasting new issuance to be

$110 to $115 billion in 2014). It is also, at least near term, a positive for spreads.

Demand and supply of leverage is increasing

It also appears that there is an increased appetite for, and availability of, leverage for

CMBS. In our outlook we discussed how leverage was likely to be increasingly applied.

The ability to leverage 10-year new issue bonds drove spreads to all-time tights several

years ago.

While we are not forecasting spreads will return to those lows, we believe a little additional

leverage could go a long way in increasing demand. The yield curve has steepened quite

a bit over the past year and with the short end remaining low, funding costs are likely to

remain attractive.

Roger Lehman

+1 212 325 2123

Sylvain Jousseaume, CFA

+1 212 325 1356

Serif Ustun, CFA

+1 212 538 4582

16 January 2014

Global Securitized Products Weekly 14

In particular, the ability to leverage new issue triple-As will help investors increase their

yield as well as create additional demand for the increased supply, in our view. This and

the relative cheapness of CMBS, to corporate bonds, were two reasons we thought new

issue super-seniors could tighten slightly from levels at the end of last year.

The deterioration of credit quality is a concern

There seemed to be little disagreement in the view that the credit quality of deals has

slipped over the past year, and is likely to slip further, over the course of 2014. There was

a little less consensus on the impact this would have.

One popular – albeit imprecise – measure discussed is to equate today’s underwriting

standards to that of a specific legacy cohort. We did this, in more detail, in our Outlook and

then proceeded to overlay the projected losses of those seasoned deals onto today’s

subordination levels. The opinion of many, who we spoke to, pegged current underwriting

similar to that of 2005, or maybe early-2006. We did speak to some who argued that we

had not gotten near those level yet, while others were mindful of the use of IOs,

subordinated debt and pro forma loans and believed standards were worse than seen in

those years. While the use of pro forma underwriting has crept back in, it has not gotten

anywhere near the levels that prevailed in later legacy vintages.

Our own concerns about underwriting quality led us to be cautious on the triple-B minus

sector at the end of last year. On an absolute basis and over the short term, that concern

has been misplaced. However, we believe that over the longer-term, there remains better

relative value in the middle of the capital stack or in slightly more seasoned deals.

More origination and more originators indicate that this trend is likely to continue

The deterioration in quality seems likely to continue over the coming deals as the

competition to originate grows. Conversations indicated that as many as 30 to

35 originators were now actively making loans to securitize. Moody’s estimate of LTVs is

expected to be more than 105.0 percent on deals coming in the first quarter, compared to

103.5 percent in the prior period, according to a Bloomberg news article.

While higher leverage and more risky loans seem inevitable, the question remains whether

subordination levels will be adjusted upward and / or if spreads will rise to compensate for

the potential increase in risk.

In addition, we heard indications that average conduit deal sizes will not increase. The

thought is that originators, especially the smaller and newer entrants, will want to keep the

securitization velocity up and warehouse time down. If this proves to be the case, it will

potentially give investors more deals to go through, making it even more difficult to

properly assess the credit. As a point of reference, last year there were 45 conduit deals

brought to market (totaling $53 billion). In 2007 there were 58 deals (totaling $189 billion).

We believe conduit issuance could potentially hit $80 billion (a 51% rise). While we still

believe that average deal size will increase it may not increase proportionately.

Greater tiering should be the result of changes in quality

The result of declining credit quality should be greater tiering between vintages and

between deals. We have periodically delved into our view of the increasing risks of newer

origination (on average) and continue to believe that there should be a greater spread,

down the conduit credit, between cohorts.

There should also be further distinctions between deals. On recent origination those

quality distinctions are more difficult to make, but these should become more apparent

over time.

Lastly, given the increase in the number of originators, we believe it very likely that this

inter-deal differentiation will only become more important.

16 January 2014

Global Securitized Products Weekly 15

New CMBX indices may help drive the distinctions

The introduction of CMBX.7 was also a very popular topic throughout our various

discussions. The credit quality differential between 2012 and 2013 deals will carry through

to this and will, in part, influence the basis between these two indices. The basis, of

course, will trade differently at each level of the capital stack.

The differential will not only be driven by fundamental value but will likely be heavily

influenced by technical factors, especially in the early stages of trading, as originators may

be more inclined to use the newest index to hedge their pipeline.

More concerned about volatility than rates

When rates started to rise in the middle of last year, the market appeared very concerned

about the impact of higher rates on lending, cap rates and property prices. Since then, the

focus has seemingly, and we believe rightfully, shifted. The market is now more focused on

the volatility of rates rather than the level. In Exhibit 16, we show the updated relationship

between CMBX spreads and interest rate volatility as reflected by the CIRVE index.

Exhibit 16: CMBX.3 AAA and interest rate volatility (CIRVE)

60

80

100

120

140

160

180

40

50

60

70

80

90

100

110

120

Ma

y-1

3

Jun

-13

Jul-

13

Aug-1

3

Se

p-1

3

Oct-

13

Nov-1

3

Dec-1

3

Jan

-14

CIRVE (left)

CMBX.3 AAA (right)

Source: Credit Suisse, Markit

Volatility is currently relatively low by recent measures. It is not apparent to us what the

catalyst may be, that could send volatility higher, but we do believe the performance of

CMBS will suffer if there is a spike in volatility, such as we have seen at various periods

over the past several years.

The health of the retail sector was another concern

An ongoing concern for the CMBS market is the heavy exposure to retail and especially to

some specific names, such as JC Penney. The company today announced they were

closing 33 stores across the country. We discuss the exposure below.

As we have discussed previously, we believe store closures by some retailers are very likely

over the coming quarters and years and these will have certain repercussions in the CMBS

market. While a large scale closure is possible, these chains may instead continue to trim,

incrementally, over time, with today’s JCP announcement being an example of that.

Any closures, if they do occur, would probably be concentrated on the

underperforming stores with lower sales figures, in our opinion. This is likely to be

highly correlated with stores situated in lower-quality malls and less well located

retail centers, which we already have the greatest credit concerns about, from a loan

performance point of view.

16 January 2014

Global Securitized Products Weekly 16

To the extent these weaker retailers decide to close stores in higher-quality and

better-located retail centers, the risk to the underlying loan is far less, in our view.

The CW Auction results should come soon

There was also significant interest and discussion on the results of CWCapital’s liquidation

of distressed CMBS assets. The bids were due last December and, so far, there has been

very little information disseminated. However, we would anticipate that more information

will be coming soon.

A story in Commercial Real Estate Direct states that CBRE will “soon start closing sales

with as many as 10 investor groups”. Depending on the speed of these closings, we may

see some of the liquidations flow through in the next remittance period. Even before that,

however, we should start to hear about some of the successful buyers and, more

importantly, the purchase price.

Back in October, when the transaction was first announced, we took a close look at the

original triple-A stack from the GSMS 2007-GG10 transaction, which had fairly large

exposure. We concluded that the GG10 AMs and A1A looked relatively attractive and saw

the potential for the AJs to trade higher as well, post liquidation. This was based in part on

our outlook for the auction to go better than the expected.

Exposure and reaction to JCP store closings

Various Deals

JC Penney (JCP) announced, on Wednesday, that it was closing 33 stores as part of its

turnaround effort. It categorized these are underperforming stores. We believe that 10 of

these locations have either direct or indirect exposure to CMBS. We show this exposure in

Exhibit 17, ordered by deal. None of the deals had exposure to CMBX.6.

We have excluded from this list the Saks – Stratford Square loan in COMM 2000-C1.

While JCP is in the same mall as the Saks store, backing the loan, this is a credit tenant

lease loan and has no credit exposure to the closing JCP store.

Exhibit 17: JC Penney CMBS exposure for announced store closings *

Center Name Deal CMBX City, State

Loan bal

($mn)

Loan (% of deal)

JCP (% of loan)

JCP-weighted exp (%)

JCP lease

exp date

MR DSCR (NCF)

MR Occ.

SpcSrv Transfer

date Other Major Tenants

Bristol Mall BACM 2006-5 2 Bristol, VA 17.3 0.9% 17.7% 0.2% Aug 2017 1.04x 88 na Sears. Belk

Hickory Point Mall BSCMS 2006-PW11 Forsyth, IL 29.0 1.9% 12.2% 0.2% Oct 2015 1.00x 92 na Bergner’s, Sears

Laurel Mall BSCMS 2007-PW15 3 Hazleton, PA 36.8 1.7% 8.9% 0.2% Oct 2014 n/a n/a May 2012 Boscov’s, Sears

Marketplace of Warsaw CGCMT 2004-C2 Warsaw, IN 6.4 0.9% 12.2% 0.1% Feb 2017 n/a n/a na Elder Beernan, Dunham’s

Natchez Mall CGCMT 2006-C4 2 Natchez, MS 7.9 0.5% 22.2% 0.1% May 2014 n/a n/a na Belk

Military Circle Mall GMACC 2004-C2 Norfolk, VA 52.9 9.8% - 0.0% - 1.05x 67 Aug 2013 Hecht’s, Sears (closed)

Lincoln Plaza GSMS 2006-GG6 Rhinelander, WI 1.8 0.1% 51.0% 0.0% Mar 2017 1.39x 100 na Dollar Tree, Payless Shoe

Centre At Salisbury JPMCC 2006-LDP7 2 Salisbury, MD 115.0 3.7% 11.7% 0.4% Jul 2015 1.31x 97 na Macy’s, Boscov’s

Wayne Town Plaza MSC 2007-IQ15 4&5 Wooster, OH 9.6 0.6% 23.3% 0.2% Mar 2014 1.28x 100 na Elder Beernan,Fashion Bug

Wausau Center WFRBS 2011-C4 Wausau, WI 18.8 1.3% 36.4% 0.5% Aug 2014 1.34x 98 na -

Source: Credit Suisse, Trepp, Bloomberg * We have excluded the Saks – Stratford Sqyare loan in COMM 2000-C1. As a CTL it has no exposure to the closing of the nearby JCP location.

The largest exposed loan on the list, in dollar terms, is the Centre at Salisbury ($115

million and 3.7% of JPMCC 2007-LDP7). This was one of two properties that Rouse

recently purchased from Macerich, toward the end of last year. The loan has a reasonably

high DSCR (1.3x) and occupancy (97%) as of the latest set of financials, dated last

September. However, as we noted in our discussion of the purchase, it appeared the

transaction implied a very high LTV for that property. The inline stores generated sales of

$321 per square foot, in 12 months ending last September.

16 January 2014

Global Securitized Products Weekly 17

The other larger exposure is to the Gallery at Military Circle loan ($52.9 million and 9.8%

of GMACC 2004-C2). The JCP store does not appear to be part of the collateral but the

mall still has indirect exposure to it. In addition, the Sears location at this property closed in

May 2012 (although it is still paying rent) and the loan was sent to the special servicer last

year, as the borrower was seeking a modification.

Only one property has exposure to a recent CMBS transaction, Wausau Center. The

loan was securitized in WFRBS 2011-C4 ($18.8 million and 1.3% of the deal) but,

because it is not one of the top loans, there was not any additional information provided

in the term sheet.

As we discussed in our last JC Penney update (October 3, 2013), store closures seemed

likely and we believed would probably be concentrated on the underperforming stores,

with lower sales figures.

While store closures were expected at some point, we were a little surprised the company

only announced 33 affected locations. Our colleagues in equity research note that these

stores have, on average, a smaller footprint than typical JCP locations (they are 3.0% of

the store base but only 2.5% of the total square footage) and that store size and

productivity may have entered into the firm’s decision.

Our equity analysts go on to that this round is just “scratching the surface of what needs to

be done” but is a step in the right direction (see their January 15, 2014 article for more

information).

While we do not have information on the stores outside of CMBS, we also thought it worth

noting that four of the ten closures that were within CMBS have near-term lease

expirations. We believe that this may have also been a factor in choosing locations to

target. Sears also announced, in October, that it will evaluate closing additional stores and

highlighted they will potentially make their adjustments as leases roll.

The store closing headline caused fluctuations in the CMBX market and demonstrates

how sensitive market participants are to perceived JCP risk (this was one of the topics at

the CREFC conference discussed above as well).

Prior to the announcement, late day Wednesday, CMBX.6 BBB- and BBs were tighter on

the day. Soon after the headline came across, they moved approximately 8 and 11 bp

wider, in fairly quick order. Once the market realized that there was no CMBS exposure in

series 6, the indices rallied most of the way back leaving them, on net, only a few wider on

the day.

Moody’s price index up marginally in November The Moody’s/Real Capital Analytics commercial property price index (Moody’s CPPI)

increased 0.1% in November, on a national basis. Although the index moved higher, in

November, the move was far more modest than the prior five months, each which brought

an increase of 1.2% to 1.8%. However, it is not only the sixth straight rise but, after last

month’s revisions, the index has been up in all but one month since January 20101.

This month, the multifamily sector (up 0.6%) outpaced the core commercial property types

(which were relatively flat). That has been the case for the past two months, a reversal of

the June to September period.

The Moody’s CPPI is now up 12.5% through the first 11 months of the year. At the start of

the year, it appeared that price rises were beginning to moderate, but the mid-year rally

negated that view. Unless an unexpected drop occurs in December, the 2013 move is

poised to surpass the annual gains of the prior three years of 8.1%, 12.4% and 9.5% in

2012, 2011 and 2010, respectively.

1 The national index has been slightly restated this month, reversing a monthly drop reported for January 2013 in the previous

editions.

16 January 2014

Global Securitized Products Weekly 18

Since reaching its cyclical low, US CRE prices are now up 50%, retracing nearly three-

quarters (74%) of its decline from the peak in December 2007. We show the Moody’s

CPPI in Exhibit 18 and the three month percentage change in Exhibit 19.

Exhibit 18: Moody’s CPPI Index Exhibit 19: Three-month rolling percentage change

80

90

100

110

120

130

140

150

160

170

180

190

No

v-0

1

No

v-0

2

No

v-0

3

No

v-0

4

No

v-0

5

No

v-0

6

Nov-0

7

No

v-0

8

No

v-0

9

No

v-1

0

No

v-1

1

No

v-1

2

No

v-1

3

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Nov-0

1

Nov-0

2

Nov-0

3

Nov-0

4

Nov-0

5

Nov-0

6

Nov-0

7

Nov-0

8

Nov-0

9

Nov-1

0

Nov-1

1

Nov-1

2

Nov-1

3

Source: Credit Suisse, Moody’s Source: Credit Suisse, Moody’s

Performance by property sector

As we noted in our Year Ahead Outlook, we believe real estate investors are likely to

migrate away from seeking returns through cap rate compression and more toward

fundamental performance, income growth and operational improvements. This indicates

to us that sectors that have lagged in the upswing may start to catch up.

We show Moody’s CPPI performance, by property type, over various time frames in

Exhibit 20. Mimicking October’s results, the only sector that is down on the month is the

Office-CBD subsector, which fell 1.0%. However the two month decline follows a near

5% rise in September. The drop in this sub-index was large enough to negate the small

rises in the other core commercial sectors, the largest of which was in the industrial sub-

index (0.6%). Industrial properties have been the laggard over the year with the index up

just 5.7%, compared to double-digit increases for the other sectors. The star performer

over has been the retail area where prices are up nearly 21%, year-to-date, according to

the index.

Exhibit 20: Index performance by property type (percentage change)

1 month 3 month YTD 12 month

Peak to trough

Peak to Nov-13

Trough to Nov-13

Apartment 0.6 1.6 10.7 11.9 -40.4 0.0 67.8

Retail 0.3 4.5 20.9 22.9 -42.5 -17.5 43.3

Industrial 0.6 4.0 5.7 5.8 -33.2 -21.8 17.2

Office - CBD -1.0 3.7 12.0 11.2 -49.2 -2.0 92.9

Office -Suburban 0.3 2.5 12.3 12.8 -44.9 -27.6 31.4

All Property 0.1 3.1 12.5 13.1 -40.4 -10.6 49.9

Source: Credit Suisse, Moody’s

Since reaching their local troughs, individual sub-indices have performed very differently.

As Exhibit 21 shows, the best performers, since the local lows, have been in the apartment

and CBD office sectors.

16 January 2014

Global Securitized Products Weekly 19

Exhibit 21: Property sub-indices over time

70

90

110

130

150

170

190

210

No

v-0

1

Ma

y-0

2

No

v-0

2

Ma

y-0

3

No

v-0

3

Ma

y-0

4

No

v-0

4

May-0

5

No

v-0

5

Ma

y-0

6

No

v-0

6

Ma

y-0

7

No

v-0

7

May-0

8

No

v-0

8

Ma

y-0

9

No

v-0

9

Ma

y-1

0

No

v-1

0

May-1

1

No

v-1

1

Ma

y-1

2

No

v-1

2

Ma

y-1

3

No

v-1

3

Retail

Industrial

Office - CBD

Office - Suburban

Apartment

Hotels (qtrly)

Source: Credit Suisse, Moody’s

Some of the sectors that reversed the quickest have seen more moderate price growth

recently, as they approach their pre-crisis levels. The apartment sector provides an

example of this.

The apartment sector was up 0.6% in in November as it moves even higher above its pre-

crisis peak. Nevertheless, over the past three months it is up 1.6%, far less than all of the

core sectors (up 2.5% to 4.5%). We may be seeing a similar story emerge with CBD-office

which has dropped for two consecutive months. This is the only other index that is near its

pre-crisis peak and currently sits 2% below that level.

The reverse holds for the property sectors that are further away from their respective

peaks. As noted above, retail has been the best performing sector this year, rising 20%.

As the exhibit shows, it lagged the recovery in the other sectors prior to 2013.

Major versus non-major markets

The Moody’s indices divide properties geographically into major and non-major markets.

The major markets include what used to be called the “six city trophy” markets of Boston,

Chicago, Los Angeles, New York, San Francisco and Washington DC.

Similar to the reversal on property type

level, we are seeing some shift in the

leadership between major and non-major

markets. Exhibit 22 shows the significant

divergence between the performance of

the major and non-major markets.

The recovery of the major market segment

outpaced that of the non-major markets

since the end of 2009 but the pace of

recovery appears to have slowed and

even declined slightly in mid-2012, before

resuming its rise toward the end of 2012.

Since the trough, the major market sector

has improved 63.0% while the non-major

market index is up 39.7%.

Exhibit 22: Major and non-major markets

80

100

120

140

160

180

200

220

No

v-0

1

No

v-0

2

No

v-0

3

No

v-0

4

No

v-0

5

No

v-0

6

No

v-0

7

Nov-0

8

No

v-0

9

No

v-1

0

No

v-1

1

No

v-1

2

Nov-1

3

Major markets

National

Non-majormarkets

Source: Credit Suisse, Moody’s

16 January 2014

Global Securitized Products Weekly 20

In November, the major market sub-index was up 0.8% while prices in non-major markets

were down 0.4%. Year-to-date, we have seen a comparatively similar performance

between these two sectors with non-major markets having a very slight edge (up 12.6%

compared to 12.4%). We believe the performance of the non-major market index is, at

least in part, attributable to the changing proportion of distressed property transactions

included in the index.

Proportions of distressed transactions matter

We believe part of the reason for the difference in performance between the various

sectors lies in the proportion of distressed transactions. A higher proportion of distressed

transactions will lower repeat sales indices, such as these, even if there is absolutely no

price change in a given months, while a lower proportion of distressed trades will help to

inflate such indices.

Moody’s does not generally provide detailed data on the proportion of distressed

transactions but does show a chart with the percentage of the total. It is clear from this that

the vast majority of the decline in distressed transactions, over the past year, is in the non-

major markets. By contrast, the proportion of distressed transactions in major markets is

not only lower but has also been more consistent. We believe this disparity explains part of

the recent non-major market’s relative improvement.

Special topic on market and property size

On occasion Moody’s will focus on a special topic from the data. This month, they looked

at the impact of office property size and market size on performance from the most recent

trough levels. Some of their findings included:

Manhattan, the biggest US office market, was the best performer. The market has more

than doubled in price since the trough.

Manhattan slightly outpaced the major market CBD office index which is up 97% since

the trough. This includes both large properties and large markets.

Within the suburban CBD office market, the larger properties outpaced the recovery of

smaller properties. This held in major markets and was especially pronounced in the

non-major markets.

Moody’s also found that the recovery of the medical office sector has lagged the overall

office recovery and is up only 20% from the trough, compared to the national office

recovery of 60%.

Preliminary Q4 2013 CRE fundamentals Commercial real estate markets have, in general, been recovering since the bottom of the

cycle; however, the extent of recovery across the various property sectors remains uneven.

This is not only due to the different dynamics of each sector but also to the varying lags to

the economic cycle. We saw this when we looked the price performance of commercial

real estate, in the preceding section. The same holds when we look at the path of real

estate fundamentals..

The multifamily and hotel sectors have posted strong increases, in both occupancy

rates and rent growth, for four consecutive years, as both have a reasonably short

lag to changes in the economic climate (Exhibit 23). In contrast, the pace of recovery

for the office and retail sectors has been quite slow as occupancy and rental rates have

only improved slightly, reflecting the slow US economic growth environment.

16 January 2014

Global Securitized Products Weekly 21

Exhibit 23: Year-over-year changes in rents and vacancy rates

Effective Rents (%)* Vacancy Rate (bps)

Year Multifamily Hotel Office Retail Year Multifamily Hotel Office Retail

2009 -2.9% -16.7% -8.9% -3.7% 2009 130 520 250 170

2010 2.3% 5.1% -1.5% -1.4% 2010 -140 -240 60 40

2011 2.4% 8.2% 2.0% -0.1% 2011 -140 -260 -20 0

2012 3.9% 6.4% 2.0% 0.5% 2012 -60 -120 -30 -30

2013 3.2% 5.7% 2.2% 1.5% 2013 -50 -110 -20 -30

* Change in RevPAR for the hotel sector Source: Credit Suisse, REIS, STR

One of the factors we thought would be a big positive for commercial real estate’s

recovery was the lack of new construction, which has kept the overall supply low. The

reduction in new space, coming online, has been a universal positive, so far, across all

property types.

In the next few sections, we review the trends across the major property types based on

the preliminary 4Q 2013 data released by REIS, CoStar, and Smith Travel Research, and

compare conduit CMBS performance for each property sector.

Multifamily Multifamily sector fundamentals continued to show improvement in the fourth quarter. The

multifamily sector, along with hotels, are outperforming the rest of the commercial real

estate market coming out of the recent real estate downturn. Vacancies have been

declining and rents increasing, materially and consistently, since early 2010, albeit to a

varying degree.

The vacancy rate dropped another 10 bp, to 4.1%, in the fourth quarter of 2013. Vacancies

have been declining (or stable) for 16 consecutive quarters now. The pace of improvement

has naturally slowed, as the market got tighter. Vacancies are now in the low single-digits,

the tightest levels since 3Q 2001.

Vacancies fell 50 bp since last year and are down 390 bp since the cyclical peak, in late

2009. Effective rents increased by 0.8% over the quarter, bringing the year-over-year

increase to 3.2% (see Exhibits 24 and 25).

A testament to the market’s strength can be seen in the total net absorption, of 165k

units over the year, We note that 127k new units were completed across the multifamily

markets REIS tracks – the most in the last four years.

Exhibit 24: Multifamily vacancies declined by 10 bp to 4.1% and effective rents increased by 0.8% in the fourth quarter of 2013

Exhibit 25: Multifamily completions reverted back to pre-crisis levels

2%

3%

4%

5%

6%

7%

8%

9%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2007

Q4

2008

Q2

2008

Q4

2009

Q2

2009

Q4

2010

Q2

2010

Q4

2011

Q2

2011

Q4

2012

Q2

2012

Q4

2013

Q2

2013

Q4

Vac R

ate

Chg

in R

ents

QoQ Rent Change MF Vacancies

2%

3%

4%

5%

6%

7%

8%

9%

0k

20k

40k

60k

80k

100k

120k

140k

160k

2007

Q4

2008

Q2

2008

Q4

2009

Q2

2009

Q4

2010

Q2

2010

Q4

2011

Q2

2011

Q4

2012

Q2

2012

Q4

2013

Q2

2013

Q4

Vac R

ate

Com

plet

ions

(uni

ts)

MF Completions (12-mo change)

MF Vacancies

Source: Credit Suisse, REIS Source: Credit Suisse, REIS

16 January 2014

Global Securitized Products Weekly 22

Construction activity is expected to pick up further and REIS expects 165k units to be

delivered this year. To put that in perspective, we note that places construction near the

historical average. This is consistent with Census Bureau Data.

The Census Bureau data shows that permits and starts for 5+ unit buildings have been

trending higher and have more than doubled since the recession ended. Both series are

now near their respective historical averages (Exhibits 26 and 27). That said, we think the

forecasted increase in multifamily supply is manageable, given how undersupplied the

sector has been in recent years, and should not lead to a spike in vacancies.

Exhibit 26: Multifamily building permits … Exhibit 27: … and building starts are back to historical averages

0K

100K

200K

300K

400K

500K

600K

200

1

200

2

2003

200

4

200

5

200

6

200

7

200

8

200

9

2010

201

1

201

2

2013

Building permits (5+units)

12 per. Mov. Avg. (Buildingpermits (5+units))

0K

50K

100K

150K

200K

250K

300K

350K

400K

450K

200

1

200

2

2003

200

4

200

5

200

6

200

7

200

8

200

9

2010

201

1

201

2

2013

Starts (5+units)

12 per. Mov. Avg. (Starts(5+units))

Source: Credit Suisse, US Census Bureau Source: Credit Suisse, REIS

Multifamily markets have been the beneficiary of the ongoing weakness in the single-

family housing market as well as robust funding alternatives from the GSEs. In addition to

the increased difficulty in getting a residential mortgage, lack of any meaningful increase in

incomes, uncertainty about economic growth and housing prices still lead many to favor

renting over buying. Exhibit 28 shows that homeownership continues to decline, and this is

another positive for the multifamily sector. That said, housing prices have shown strong

gains over the past year and this too should also serve to diminish one of the positives

propelling the multifamily market.

Exhibit 28: Multifamily vacancy rates and homeownership

2%

3%

4%

5%

6%

7%

8%

9%

63%

64%

65%

66%

67%

68%

69%

70%

200

7 Q

3

200

7 Q

4

200

8 Q

1

200

8 Q

2

200

8 Q

3

200

8 Q

4

200

9 Q

1

200

9 Q

2

200

9 Q

3

200

9 Q

4

201

0 Q

1

201

0 Q

2

2010

Q3

201

0 Q

4

201

1 Q

1

201

1 Q

2

201

1 Q

3

201

1 Q

4

201

2 Q

1

201

2 Q

2

201

2 Q

3

201

2 Q

4

201

3 Q

1

201

3 Q

2

201

3 Q

3

Homeownership Rate (LHS) Multifamily Vacancy Rate (RHS)

Source: Credit Suisse, REIS, US Census Bureau, the BLOOMBERG PROFESSIONAL™ service

16 January 2014

Global Securitized Products Weekly 23

Improving sector fundamentals are helping CMBS multifamily loans and leading to fewer

new credit problems. The 60+day delinquency rate for the sector dropped from 16.3% in

early 2011, to 11.8% as of last month (Exhibit 29). In addition, our proprietary Mod-CLIR

metric, which accounts for delinquencies, liquidations, and modifications, has been

increasing at the slowest pace since the recession began. This would imply fewer new

credit problems, which is also confirmed by our first-time delinquency series, shown in

Exhibit 30.

Exhibit 29: Multifamily: Delinquency rate is down, CLIR is stable Exhibit 30: Fewer new delinquencies for multifamily

19.0%

11.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

De

c-0

8

Jun

-09

De

c-0

9

Jun

-10

De

c-1

0

Jun

-11

De

c-1

1

Jun

-12

De

c-1

2

Jun

-13

De

c-1

3

Multifamily Mod-CLIR

Multifamily 60+day

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Dec-1

0

Ma

r-1

1

Jun

-11

Se

p-1

1

Dec-1

1

Ma

r-1

2

Jun

-12

Se

p-1

2

Dec-1

2

Ma

r-1

3

Jun

-13

Se

p-1

3

Dec-1

3

Loans becoming 60+dayfor the first time

6-mth moving avg

$bn

Source: Credit Suisse, Trepp Source: Credit Suisse, Trepp

Hotel

Key performance indicators for the hotel sector show a pattern similar to that of the

multifamily sector. Occupancy rates and revenue per available room (RevPAR) metrics

have grown consistently month-over-month (adjusting for seasonality) since early 2010,

but occupancy rates have only seen marginal increases lately. Monthly occupancies were

up 1.1% in Q4 2013 and RevPARs increased at a respectable rate of 5.3%, suggesting

that most of the RevPAR gain is due to higher room prices (Exhibits 31 and 32).

Exhibit 31: Hotel occupancy improved slightly Exhibit 32: However RevPARs continued to increase

40%

45%

50%

55%

60%

65%

70%

75%

Jan

Fe

b

Mar

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

2013

2012

2011

2010

$40

$45

$50

$55

$60

$65

$70

$75

$80

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

2013

2012

2011

2010

Source: Credit Suisse, STR Source: Credit Suisse, STR

16 January 2014

Global Securitized Products Weekly 24

The improved fundamentals have also started to carry over to CMBS performance. The

60+day delinquency rate for hotels peaked at 16.7% in January 2011 and has declined

since. Delinquencies reached 11.3% in December 2013 (Exhibit 33). First-time

delinquencies are also trending down, as shown in Exhibit 34.

With the improved sector fundamentals, we have seen a commensurate rise of securitized

hotel loans in both conduit and single-borrower CMBS deals. On the single-borrower side,

about 50% of single-borrower CMBS issuance last year ($12.6 billion out of $25.7 billion)

has been backed by hotels, including the $3.5 billion Hilton deal, which priced in Q4 2013.

On the conduit side, the proportion of hotel loans in 2013 issuance has risen to 16%,

compared to 13% for the 2012 cohort.

Exhibit 33: Hotel delinquency rate is down, CLIR is stable Exhibit 34: Fewer first-time delinquencies for hotels

20.7%

11.3%

0%

5%

10%

15%

20%

25%

De

c-0

8

Jun-0

9

De

c-0

9

Jun

-10

De

c-1

0

Jun

-11

De

c-1

1

Jun-1

2

De

c-1

2

Jun

-13

De

c-1

3

Hotel Mod-CLIR

Hotel 60+day

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

De

c-1

0

Ma

r-1

1

Jun

-11

Se

p-1

1

De

c-1

1

Ma

r-1

2

Jun

-12

Se

p-1

2

De

c-1

2

Ma

r-1

3

Jun

-13

Se

p-1

3

De

c-1

3

Loans becoming 60+dayfor the first time

6-mth moving avg

$bn

Source: Credit Suisse, Trepp Source: Credit Suisse, Trepp

Office

The lackluster recovery in the office sector continued in the fourth quarter. The national

vacancy rate remained unchanged at 16.9%, bringing the year-over-year change down by

only 20 bp. This shows a continued, but rather gradual, improvement from the cyclical high

of 17.6%, in the fourth quarter of 2010. Vacancy rates remain near levels last experienced

a decade ago and are only about 2% lower than the peak levels of early 1990s.

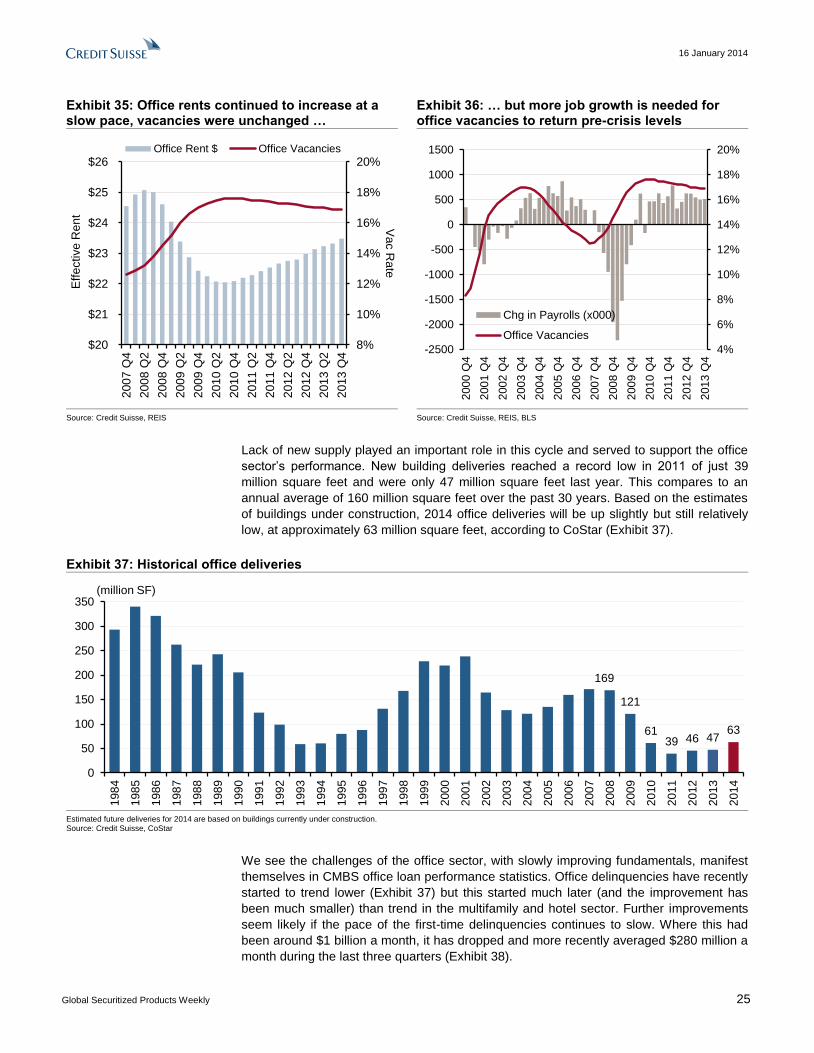

Effective rents increased by 0.7% on the quarter, bringing the year-over-year increase to

2.2% (Exhibit 35). These statistics bear out our thesis that we should see a moderate

improvement in vacancy rates and rental growth due to increasing demand in a slow

growth economy and a drop in construction activity.

While we believe that all property sectors are impacted by the health of the labor market,

the office market clearly has the closest and most direct ties. The payroll numbers shown

in Exhibit 36 reveal the extent of job losses at the height of the recession, as well as the

tame increases, even as job growth resumed. We reiterate our view that unless

employment prospects meaningfully change in upcoming quarters, office vacancies are

likely to stay at the 16%-17% level for a while.

16 January 2014

Global Securitized Products Weekly 25

Exhibit 35: Office rents continued to increase at a slow pace, vacancies were unchanged …

Exhibit 36: … but more job growth is needed for office vacancies to return pre-crisis levels

8%

10%

12%

14%

16%

18%

20%

$20

$21

$22

$23

$24

$25

$26

200

7 Q

4

200

8 Q

2

200

8 Q

4

200

9 Q

2

200

9 Q

4

201

0 Q

2

201

0 Q

4

201

1 Q

2

201

1 Q

4

201

2 Q

2

201

2 Q

4

201

3 Q

2

201

3 Q

4

Va

c R

ate

Eff

ective

Re

nt

Office Rent $ Office Vacancies

4%

6%

8%

10%

12%

14%

16%

18%

20%

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

200

0 Q

4

2001

Q4

200

2 Q

4

200

3 Q

4

2004

Q4

200

5 Q

4

200

6 Q

4

200

7 Q

4

200

8 Q

4

200

9 Q

4

201

0 Q

4

201

1 Q

4

201

2 Q

4

201

3 Q

4

Chg in Payrolls (x000)

Office Vacancies

Source: Credit Suisse, REIS Source: Credit Suisse, REIS, BLS

Lack of new supply played an important role in this cycle and served to support the office

sector’s performance. New building deliveries reached a record low in 2011 of just 39

million square feet and were only 47 million square feet last year. This compares to an

annual average of 160 million square feet over the past 30 years. Based on the estimates

of buildings under construction, 2014 office deliveries will be up slightly but still relatively

low, at approximately 63 million square feet, according to CoStar (Exhibit 37).

Exhibit 37: Historical office deliveries

169

121

6139 46 47

63

0

50

100

150

200

250

300

350

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

(million SF)

Estimated future deliveries for 2014 are based on buildings currently under construction. Source: Credit Suisse, CoStar

We see the challenges of the office sector, with slowly improving fundamentals, manifest

themselves in CMBS office loan performance statistics. Office delinquencies have recently

started to trend lower (Exhibit 37) but this started much later (and the improvement has

been much smaller) than trend in the multifamily and hotel sector. Further improvements

seem likely if the pace of the first-time delinquencies continues to slow. Where this had

been around $1 billion a month, it has dropped and more recently averaged $280 million a

month during the last three quarters (Exhibit 38).

16 January 2014

Global Securitized Products Weekly 26

Exhibit 38: Office delinquency rate and Mod-CLIR Exhibit 39: First-time office delinquencies

18.1%

9.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Dec-0

8

Jun

-09

Dec-0

9

Jun

-10

Dec-1

0

Jun

-11

Dec-1

1

Jun

-12

Dec-1

2

Jun

-13

Dec-1

3

Office Mod-CLIR

Office 60+day

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

De

c-1

0

Ma

r-1

1

Jun

-11

Se

p-1

1

De

c-1

1

Ma

r-1

2

Jun

-12

Se

p-1

2

De

c-1

2

Ma

r-1

3

Jun

-13

Se

p-1

3

De

c-1

3

Loans becoming 60+dayfor the first time

6-mth moving avg

$bn

Source: Credit Suisse, Trepp Source: Credit Suisse, Trepp

Retail

Retail has lagged the recovery of the other property sectors, making it the worst performer

since the end of the recession. There have been tentative signs that the worst may be

over, with performance metrics for the sector starting to stabilize in 4Q 2011. However, the

progress remains slow.

The vacancy rate for neighborhood and community shopping centers dropped only 10 bps

to 10.4% in the latest quarter. This brings vacancies down by just 30 bp year over year.