Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES AND

ANALYST CERTIFICATIONS.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

Global Securitized Products Weekly Securitized Products Strategy

Agency MBS

With a somewhat dovish FOMC statement, we maintain a tactical overweight. With

ECB’s QE announcement, Greek elections and the FOMC in the rearview mirror, we

see room for volatility to decline, supporting basis performance. We expect a low

probability of base g-fee reduction, and significant probability of the 25bp upfront

adverse market delivery fee being dropped and/or a targeted reduction of LLPA for low

FICO/high LTV borrowers. STACR 2015-DN1 pricing corroborates our earlier analysis

suggesting limited room to lower base g-fees. Net issuance of GNMA MBS backed by

FHA loans has turned negative due to elevated FHA-to-conventional refi activity. We

estimate the volume at roughly $50B in 2014, 5-6 CPR in FHA speeds and roughly 3-4

CPR to overall GN speeds. The refi index should slip gradually for unchanged

mortgage rates, rise slightly (100-200 points) for a modest rate rally (~5bp), increase to

a 3800-4000 range in a 25bp rally, and rise to a 4500-5000 range for a 50bp rally.

Non-Agency MBS

Last Friday saw a fast and furious news cycle for Ocwen and HLSS. In the morning,

BlueMountain delivered a notice of default to the trustee on two HSART series; in the

afternoon, RMBS investors filed a notice of non-performance for 119 trusts and the CA

DBO settled its claims from two weeks ago. After recapping the events that have

occurred over the last week, we revisit our framework approach introduced two weeks

ago to help RMBS investors think about the ramifications of an Ocwen setback.

CMBS

The CMBS market continues to perform very well, on a relative basis, as it remains

largely immune from the macro-led volatility that has affected other financial markets,

including corporate bonds and equities. Investors are certainly attempting to

differentiate more between recently issued bonds, based on perceived credit quality,

subordination levels and rating agency assignments. The latest set of CMBX indices,

CMBX.8, started trading this past Monday and the launch was met with decent

trading volumes. The 60+-day legacy conduit delinquency rate fell 1 bp to 8.7% in

January, as the monthly changes have once again taken on a little bit of a see-saw

pattern of ups and downs. Credit seems to have stabilized, however. We count over

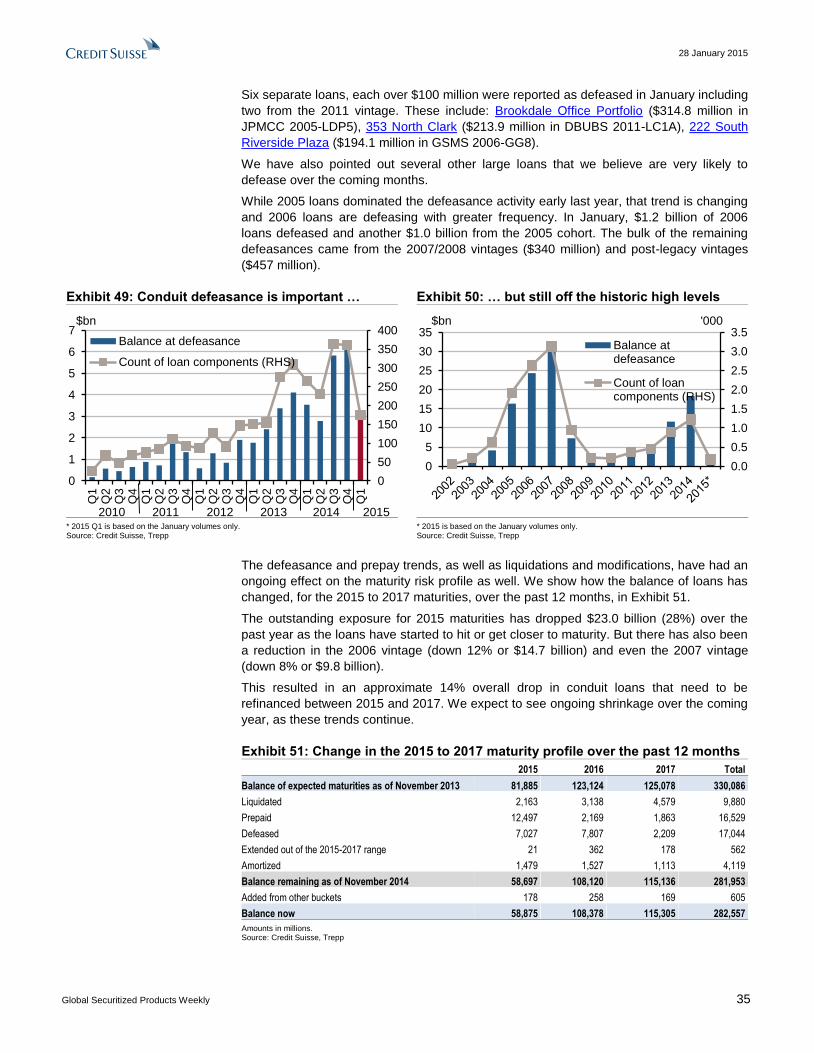

$1.3 billion of legacy loan liquidations in the January remittance period while

$3.0 billion was defeased.

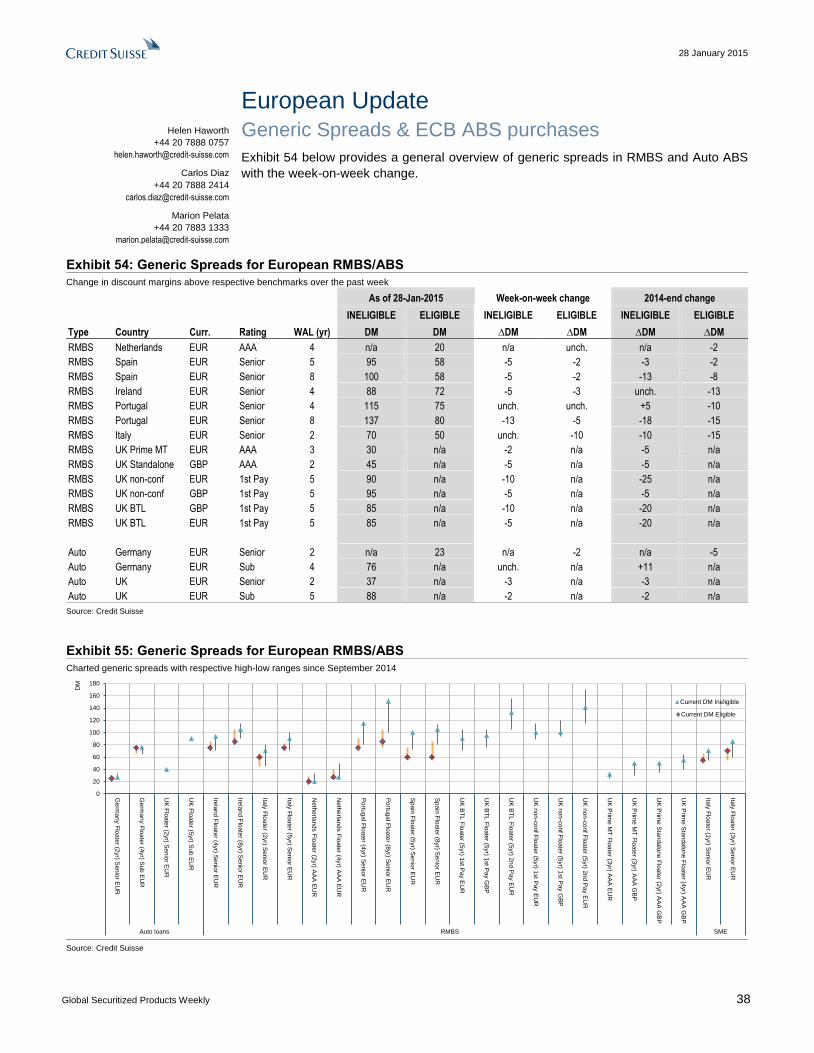

European Update

There have been no new public pricings this week with only a retained transaction

(French consumer loan ABS) being structured and pricing. The current pipeline

includes a UK auto loan ABS deal and Italian CMBS. Please refer to the European

Update for more information.

Research Analysts

GLOBAL HEAD

Roger Lehman +1 212 325 2123 [email protected]

AGENCY MBS

Mahesh Swaminathan +1 212 325 8789 [email protected]

Qumber Hassan +1 212 538 4988 [email protected]

Glenn Russo +1 212 538 6881 [email protected]

NON-AGENCY MBS/CONSUMER ABS

Marc Firestein +1 212 325 4379 [email protected]

Jonathan Corwin +1 212 538 6490 [email protected]

CMBS

Roger Lehman +1 212 325 2123 [email protected]

Sylvain Jousseaume, CFA +1 212 325 1356 [email protected]

Serif Ustun, CFA +1 212 538 4582 [email protected]

EUROPEAN UPDATE

Helen Haworth +44 20 7888 0757 [email protected]

Carlos Diaz +44 20 7888 2414 [email protected]

Marion Pelata +44 20 7883 1333 [email protected]

MODELING AND ANALYTICS

David Zhang +1 212 325 2783 [email protected]

Table of Contents

Core Views 2

Agency MBS 3

Non-Agency MBS 11

CMBS 16

European Update 38

28 January 2015

Fixed Income Research

http://www.credit-suisse.com/researchandanalytics

FOR INSTITUTIONAL CLIENT USE ONLY

28

Ja

nu

ary

20

15

Glo

bal S

ecuritiz

ed

Pro

ducts

Weekly

2

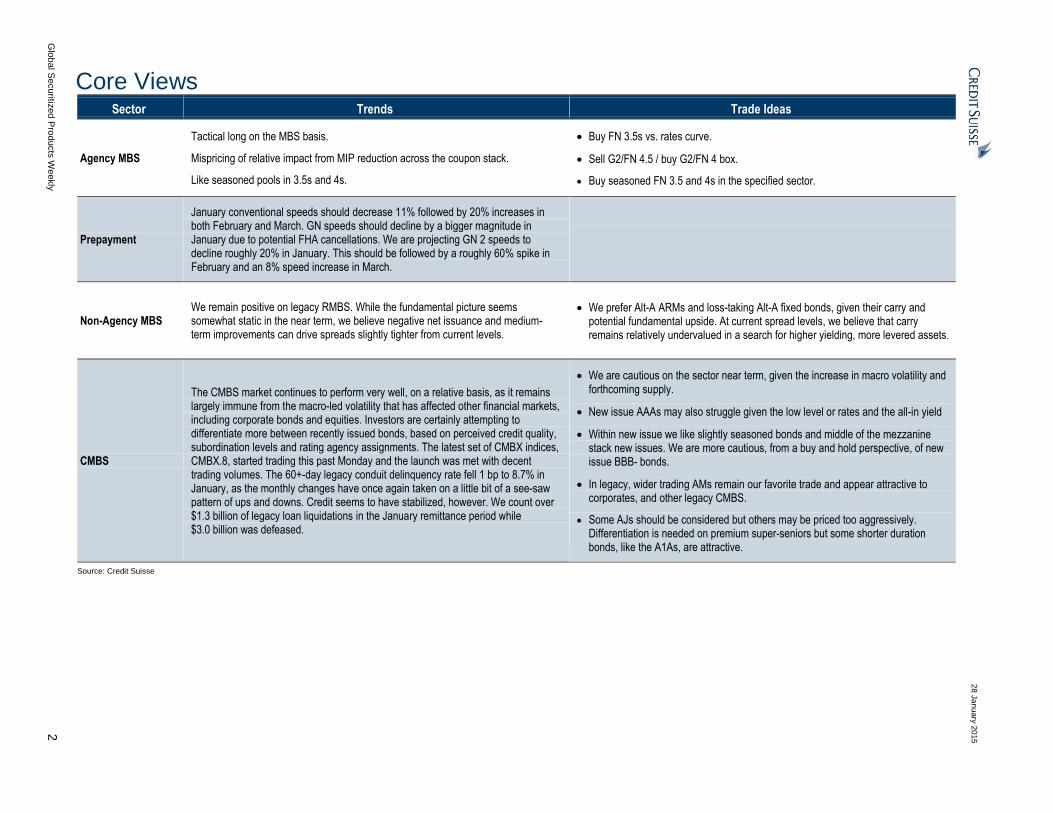

Core Views Sector Trends Trade Ideas

Agency MBS

Tactical long on the MBS basis.

Mispricing of relative impact from MIP reduction across the coupon stack.

Like seasoned pools in 3.5s and 4s.

Buy FN 3.5s vs. rates curve.

Sell G2/FN 4.5 / buy G2/FN 4 box.

Buy seasoned FN 3.5 and 4s in the specified sector.

Prepayment

January conventional speeds should decrease 11% followed by 20% increases in both February and March. GN speeds should decline by a bigger magnitude in January due to potential FHA cancellations. We are projecting GN 2 speeds to decline roughly 20% in January. This should be followed by a roughly 60% spike in February and an 8% speed increase in March.

Non-Agency MBS We remain positive on legacy RMBS. While the fundamental picture seems somewhat static in the near term, we believe negative net issuance and medium-term improvements can drive spreads slightly tighter from current levels.

We prefer Alt-A ARMs and loss-taking Alt-A fixed bonds, given their carry and potential fundamental upside. At current spread levels, we believe that carry remains relatively undervalued in a search for higher yielding, more levered assets.

CMBS

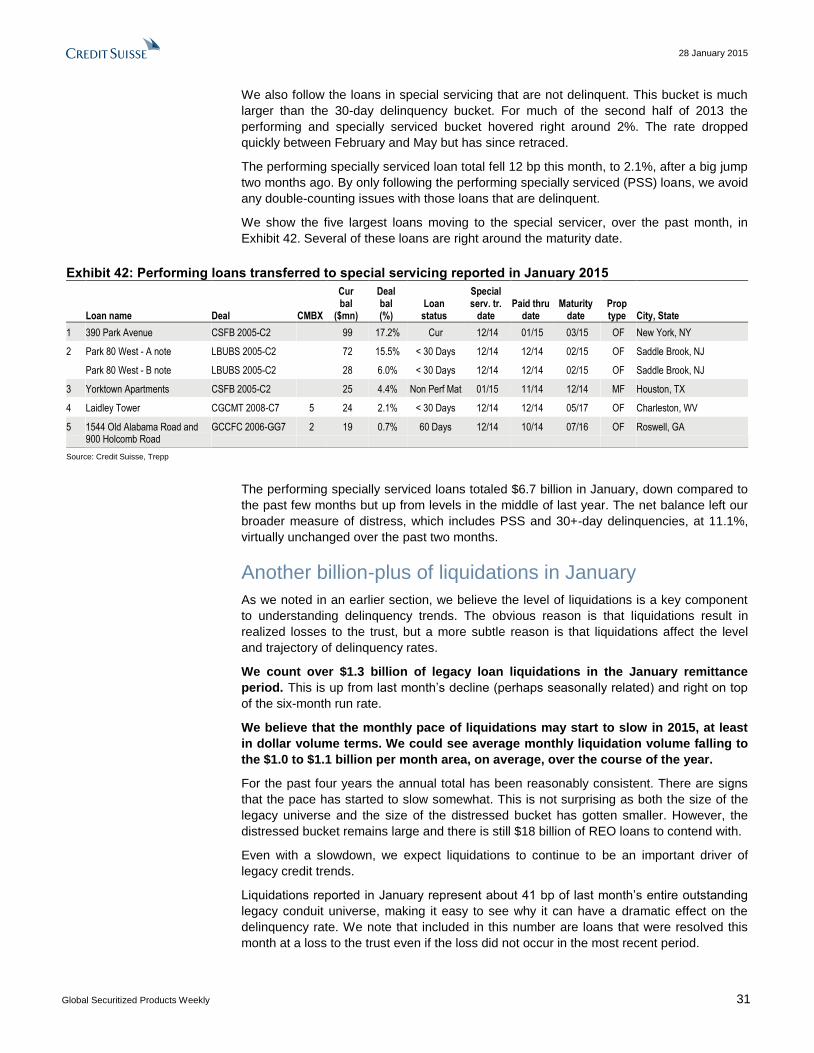

The CMBS market continues to perform very well, on a relative basis, as it remains largely immune from the macro-led volatility that has affected other financial markets, including corporate bonds and equities. Investors are certainly attempting to differentiate more between recently issued bonds, based on perceived credit quality, subordination levels and rating agency assignments. The latest set of CMBX indices, CMBX.8, started trading this past Monday and the launch was met with decent trading volumes. The 60+-day legacy conduit delinquency rate fell 1 bp to 8.7% in January, as the monthly changes have once again taken on a little bit of a see-saw pattern of ups and downs. Credit seems to have stabilized, however. We count over $1.3 billion of legacy loan liquidations in the January remittance period while $3.0 billion was defeased.

We are cautious on the sector near term, given the increase in macro volatility and forthcoming supply.

New issue AAAs may also struggle given the low level or rates and the all-in yield

Within new issue we like slightly seasoned bonds and middle of the mezzanine stack new issues. We are more cautious, from a buy and hold perspective, of new issue BBB- bonds.

In legacy, wider trading AMs remain our favorite trade and appear attractive to corporates, and other legacy CMBS.

Some AJs should be considered but others may be priced too aggressively. Differentiation is needed on premium super-seniors but some shorter duration bonds, like the A1As, are attractive.

Source: Credit Suisse

28 January 2015

Global Securitized Products Weekly 3

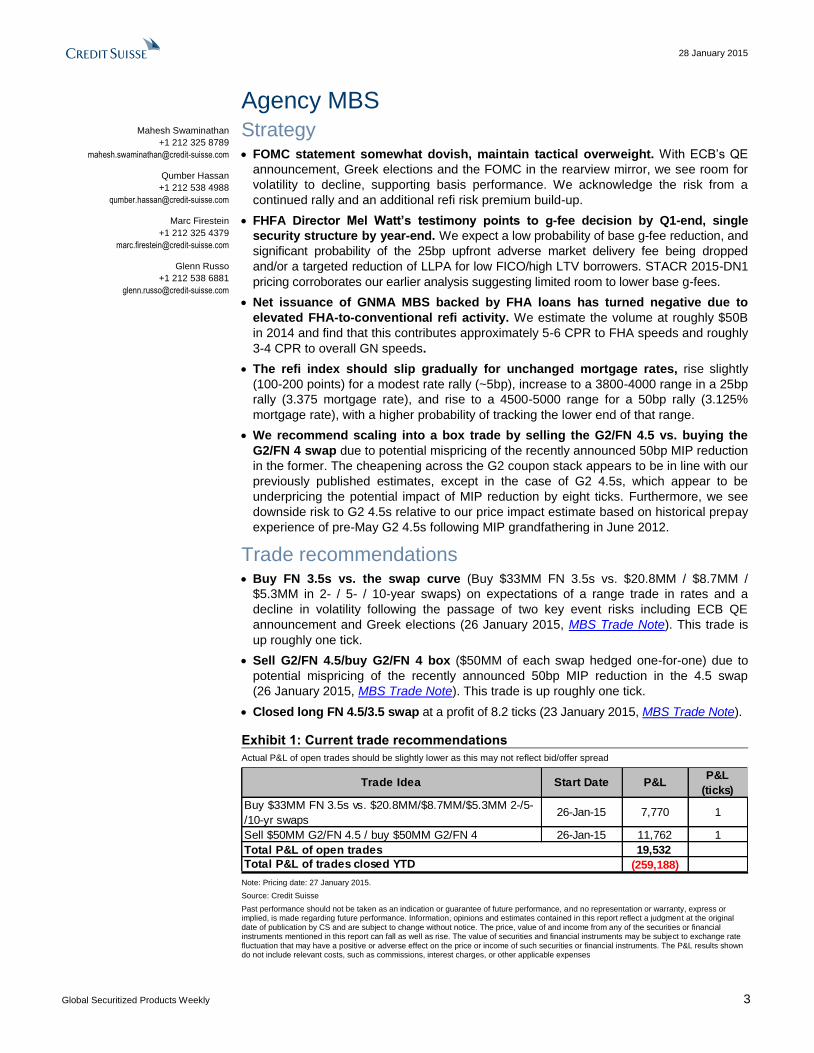

Agency MBS Strategy FOMC statement somewhat dovish, maintain tactical overweight. With ECB’s QE

announcement, Greek elections and the FOMC in the rearview mirror, we see room for

volatility to decline, supporting basis performance. We acknowledge the risk from a

continued rally and an additional refi risk premium build-up.

FHFA Director Mel Watt’s testimony points to g-fee decision by Q1-end, single

security structure by year-end. We expect a low probability of base g-fee reduction, and

significant probability of the 25bp upfront adverse market delivery fee being dropped

and/or a targeted reduction of LLPA for low FICO/high LTV borrowers. STACR 2015-DN1

pricing corroborates our earlier analysis suggesting limited room to lower base g-fees.

Net issuance of GNMA MBS backed by FHA loans has turned negative due to

elevated FHA-to-conventional refi activity. We estimate the volume at roughly $50B

in 2014 and find that this contributes approximately 5-6 CPR to FHA speeds and roughly

3-4 CPR to overall GN speeds.

The refi index should slip gradually for unchanged mortgage rates, rise slightly

(100-200 points) for a modest rate rally (~5bp), increase to a 3800-4000 range in a 25bp

rally (3.375 mortgage rate), and rise to a 4500-5000 range for a 50bp rally (3.125%

mortgage rate), with a higher probability of tracking the lower end of that range.

We recommend scaling into a box trade by selling the G2/FN 4.5 vs. buying the

G2/FN 4 swap due to potential mispricing of the recently announced 50bp MIP reduction

in the former. The cheapening across the G2 coupon stack appears to be in line with our

previously published estimates, except in the case of G2 4.5s, which appear to be

underpricing the potential impact of MIP reduction by eight ticks. Furthermore, we see

downside risk to G2 4.5s relative to our price impact estimate based on historical prepay

experience of pre-May G2 4.5s following MIP grandfathering in June 2012.

Trade recommendations Buy FN 3.5s vs. the swap curve (Buy $33MM FN 3.5s vs. $20.8MM / $8.7MM /

$5.3MM in 2- / 5- / 10-year swaps) on expectations of a range trade in rates and a

decline in volatility following the passage of two key event risks including ECB QE

announcement and Greek elections (26 January 2015, MBS Trade Note). This trade is

up roughly one tick.

Sell G2/FN 4.5/buy G2/FN 4 box ($50MM of each swap hedged one-for-one) due to

potential mispricing of the recently announced 50bp MIP reduction in the 4.5 swap

(26 January 2015, MBS Trade Note). This trade is up roughly one tick.

Closed long FN 4.5/3.5 swap at a profit of 8.2 ticks (23 January 2015, MBS Trade Note).

Exhibit 1: Current trade recommendations

Actual P&L of open trades should be slightly lower as this may not reflect bid/offer spread

Trade Idea Start Date P&LP&L

(ticks)

Buy $33MM FN 3.5s vs. $20.8MM/$8.7MM/$5.3MM 2-/5-

/10-yr swaps26-Jan-15 7,770 1

Sell $50MM G2/FN 4.5 / buy $50MM G2/FN 4 26-Jan-15 11,762 1

Total P&L of open trades 19,532

Total P&L of trades closed YTD (259,188)

Note: Pricing date: 27 January 2015.

Source: Credit Suisse

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at the original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments may be subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. The P&L results shown do not include relevant costs, such as commissions, interest charges, or other applicable expenses

Mahesh Swaminathan

+1 212 325 8789

Qumber Hassan

+1 212 538 4988

Marc Firestein

+1 212 325 4379

Glenn Russo

+1 212 538 6881

28 January 2015

Global Securitized Products Weekly 4

FOMC statement somewhat dovish, maintain tactical overweight

We maintain a tactical overweight on MBS initiated Monday (26 January 2015 MBS Trade

Note). Last week we argued that MBS had cheapened to the point that finding a trading

range would offer upside potential. We noted waiting for the passage of ECB’s QE

announcement and Greek elections before turning more constructive. With those events,

plus the FOMC in the rearview mirror, we see room for volatility to decline, supporting

basis performance. Furthermore, the relatively narrow range on 10-year Treasury yields

since mid-January opens the door for establishing a new rate range. However, we

recognize that Wednesday’s sharp rally potentially delays this process.

Wednesday’s FOMC statement mentions “solid growth” in the US economy, keeping a

June 2015 rate hike on the table. At the same time, the FOMC downgraded the

characterization of market-based inflation measures as having declined “substantially,”

and expanded the variables it is monitoring to include “international developments.” The

latter two shifts in language create optionality to delay the start of hikes if global data

worsen. Taken together, the FOMC has cast a somewhat dovish outlook.

The MBS coupon stack (FN 3s through 4.5s) has cheapened 1+ to 3 ticks vs. the swap

curve (2s/5s/10s) on Wednesday on the heels of the rally in rates. A continuation of this

rally could put further downside pressure on the basis by refocusing market attention on a

push toward lows in mortgage rates and an additional build-up of refi risk premium. That

said, considering the magnitude of the rate rally, we see the resilience of MBS on

Wednesday as a positive and hold our long recommendation.

FHFA Director Mel Watt’s testimony takeaways – g-fee decision by Q1 end, single security structure by year-end, low probability of base g-fee reduction

Director Watt on Tuesday presented to the House Financial Services Committee on the

state of GSE conservatorship and ongoing initiatives.

Key takeaways include the following:

(1) Significant progress made in 2014 on the single security initiative for Fannie and

Freddie MBS. GSEs to finalize the single security structure by 2015 end and begin a

“multi-year” implementation process.

(2) Reviewing input received on potential g-fee changes with a decision expected by end of

Q1 or potentially early Q2. The decision will incorporate safety, soundness, and credit

access considerations. The director did not explicitly suggest a direction for the decision.

(3) We think there is a low probability of changing the base g-fee (<10%), significant

probability (50%+) of the 25bp upfront adverse market delivery fee (AMDC) being

dropped. Additionally, there is potential for a targeted reduction in LLPA for high

LTV/low FICO borrowers (50+%). In addition to our detailed analysis in 15 January

2015 Global Securitized Products Weekly, the recent pricing of Freddie Mac’s STACR

2015-DN1 also supports the idea that there is little room to reduce base g-fees

(Exhibit 2).

(4) Director Watt’s answer to a question on FHLB membership rules changes noted that

the overwhelming majority of responses to a request for input favored maintaining the

status quo prior to FHFA’s recent shift. This opens the door to the possibility that he

may ease up on his restrictive guidance late last year. If such restrictions on captive

insurer membership are eased, it would most directly benefit some REITs (and would

encourage more) which access FHLB funding through this channel.

28 January 2015

Global Securitized Products Weekly 5

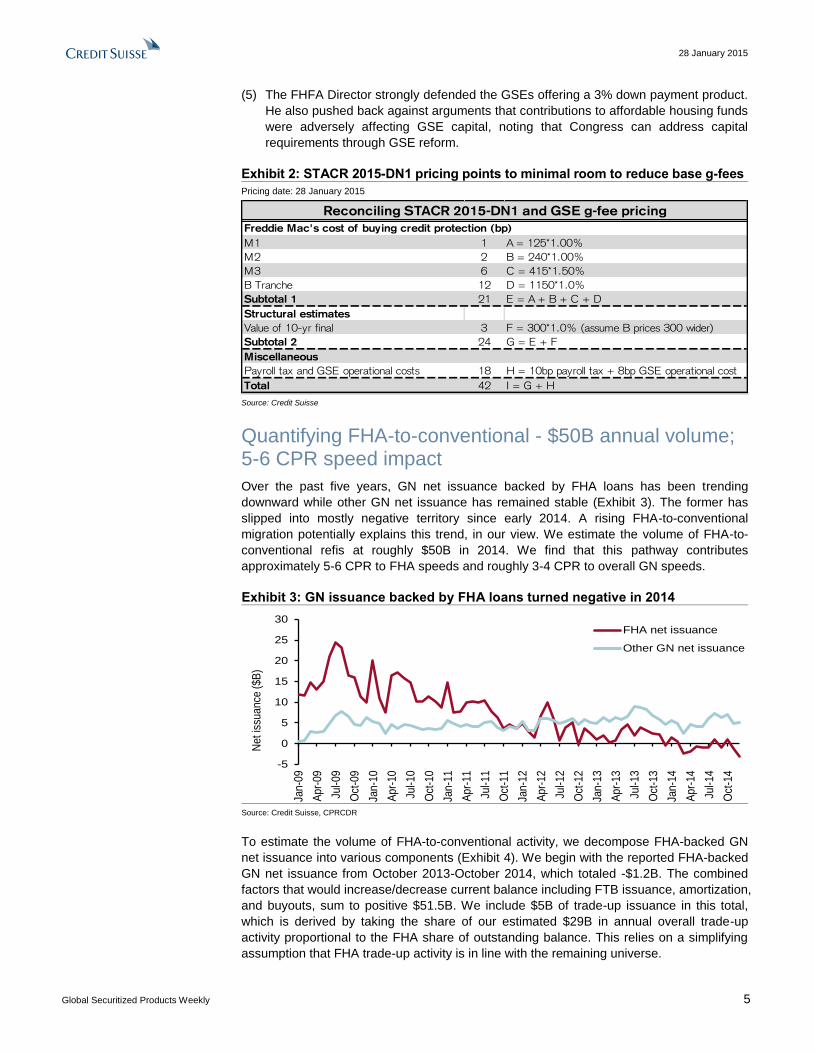

(5) The FHFA Director strongly defended the GSEs offering a 3% down payment product.

He also pushed back against arguments that contributions to affordable housing funds

were adversely affecting GSE capital, noting that Congress can address capital

requirements through GSE reform.

Exhibit 2: STACR 2015-DN1 pricing points to minimal room to reduce base g-fees

Pricing date: 28 January 2015

Freddie Mac's cost of buying credit protection (bp)

M1 1 A = 125*1.00%

M2 2 B = 240*1.00%

M3 6 C = 415*1.50%

B Tranche 12 D = 1150*1.0%

Subtotal 1 21 E = A + B + C + D

Structural estimates

Value of 10-yr final 3 F = 300*1.0% (assume B prices 300 wider)

Subtotal 2 24 G = E + F

Miscellaneous

Payroll tax and GSE operational costs 18 H = 10bp payroll tax + 8bp GSE operational cost

Total 42 I = G + H

Reconciling STACR 2015-DN1 and GSE g-fee pricing

Source: Credit Suisse

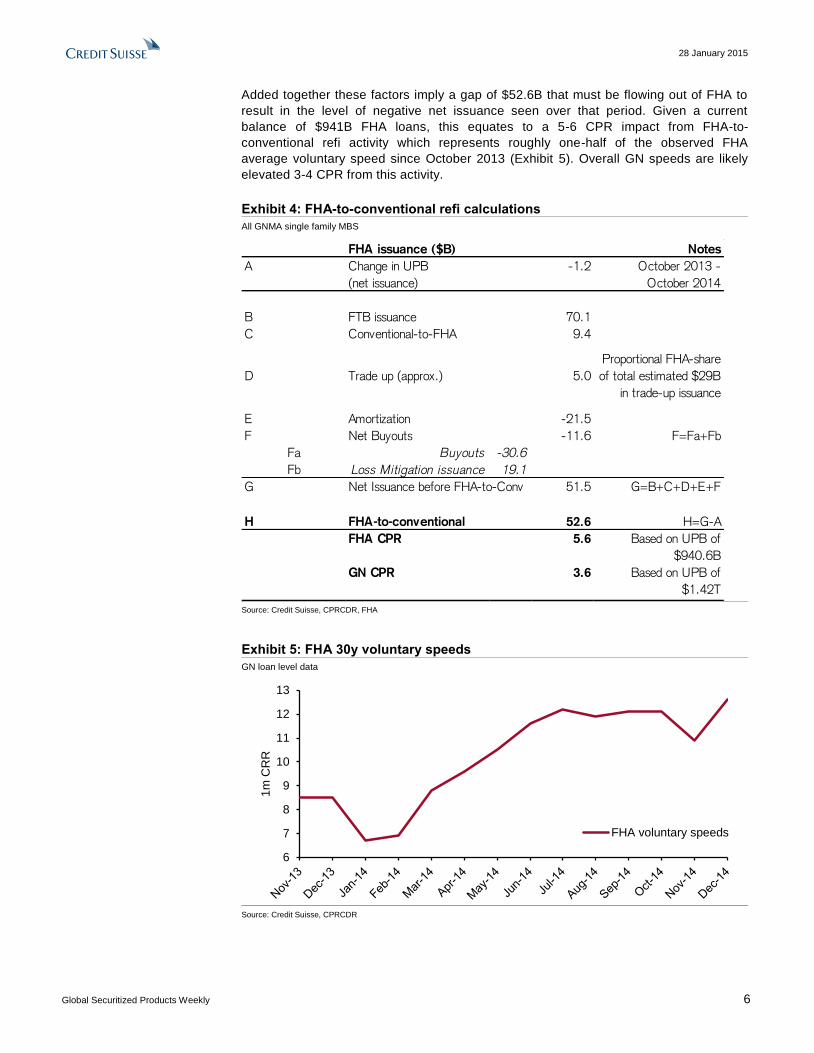

Quantifying FHA-to-conventional - $50B annual volume; 5-6 CPR speed impact

Over the past five years, GN net issuance backed by FHA loans has been trending

downward while other GN net issuance has remained stable (Exhibit 3). The former has

slipped into mostly negative territory since early 2014. A rising FHA-to-conventional

migration potentially explains this trend, in our view. We estimate the volume of FHA-to-

conventional refis at roughly $50B in 2014. We find that this pathway contributes

approximately 5-6 CPR to FHA speeds and roughly 3-4 CPR to overall GN speeds.

Exhibit 3: GN issuance backed by FHA loans turned negative in 2014

-5

0

5

10

15

20

25

30

Jan

-09

Ap

r-09

Jul-

09

Oct

-09

Jan

-10

Ap

r-10

Jul-

10

Oct

-10

Jan

-11

Ap

r-11

Jul-

11

Oct

-11

Jan

-12

Ap

r-12

Jul-

12

Oct

-12

Jan

-13

Ap

r-13

Jul-

13

Oct

-13

Jan

-14

Ap

r-14

Jul-

14

Oct

-14

Net

issu

an

ce (

$B

)

FHA net issuance

Other GN net issuance

Source: Credit Suisse, CPRCDR

To estimate the volume of FHA-to-conventional activity, we decompose FHA-backed GN

net issuance into various components (Exhibit 4). We begin with the reported FHA-backed

GN net issuance from October 2013-October 2014, which totaled -$1.2B. The combined

factors that would increase/decrease current balance including FTB issuance, amortization,

and buyouts, sum to positive $51.5B. We include $5B of trade-up issuance in this total,

which is derived by taking the share of our estimated $29B in annual overall trade-up

activity proportional to the FHA share of outstanding balance. This relies on a simplifying

assumption that FHA trade-up activity is in line with the remaining universe.

28 January 2015

Global Securitized Products Weekly 6

Added together these factors imply a gap of $52.6B that must be flowing out of FHA to

result in the level of negative net issuance seen over that period. Given a current

balance of $941B FHA loans, this equates to a 5-6 CPR impact from FHA-to-

conventional refi activity which represents roughly one-half of the observed FHA

average voluntary speed since October 2013 (Exhibit 5). Overall GN speeds are likely

elevated 3-4 CPR from this activity.

Exhibit 4: FHA-to-conventional refi calculations

All GNMA single family MBS

FHA issuance ($B) Notes

A Change in UPB

(net issuance)

-1.2 October 2013 -

October 2014

B FTB issuance 70.1

C Conventional-to-FHA 9.4

D Trade up (approx.) 5.0

Proportional FHA-share

of total estimated $29B

in trade-up issuance

E Amortization -21.5

F Net Buyouts -11.6 F=Fa+Fb

Fa Buyouts -30.6

Fb Loss Mitigation issuance 19.1

G Net Issuance before FHA-to-Conv 51.5 G=B+C+D+E+F

H FHA-to-conventional 52.6 H=G-A

FHA CPR 5.6 Based on UPB of

$940.6B

GN CPR 3.6 Based on UPB of

$1.42T

Source: Credit Suisse, CPRCDR, FHA

Exhibit 5: FHA 30y voluntary speeds

GN loan level data

6

7

8

9

10

11

12

13

1m

CR

R

FHA voluntary speeds

Source: Credit Suisse, CPRCDR

28 January 2015

Global Securitized Products Weekly 7

Where does the refi index go next?

(Originally published on 28 January 2015)

The MBA reported an 8% weekly decline (to 2572) in its seasonally adjusted conventional

refi index for the week ending 23 January 2015. This has raised questions as to whether

we have already seen the peak in refi response.

We expect the refi index to slip gradually for unchanged mortgage rates, rise slightly (100-

200 points) for a modest rate rally (~5bp), increase to a 3800-4000 range in a 25bp rally

(3.375), and rise to a 4500-5000 range for a 50bp rally (3.125% mortgage rate).

We note that applying a full one-day adjustment for MLK Day (rather than the one-half day

scaling used by the MBA) would result in roughly unchanged levels compared to the prior

week. The correct level of adjustment is uncertain, but we believe that the magnitude of

this adjustment should increase over time (to approach 1) as the holiday is more widely

observed. The other source of uncertainty arises from a 3bp decline in the Freddie Mac

PMMS for the week in contrast to a 3bp increase in the MBA’s 30-year mortgage rate

index. Using the Freddie Mac PMMS rate, our model suggests a roughly unchanged

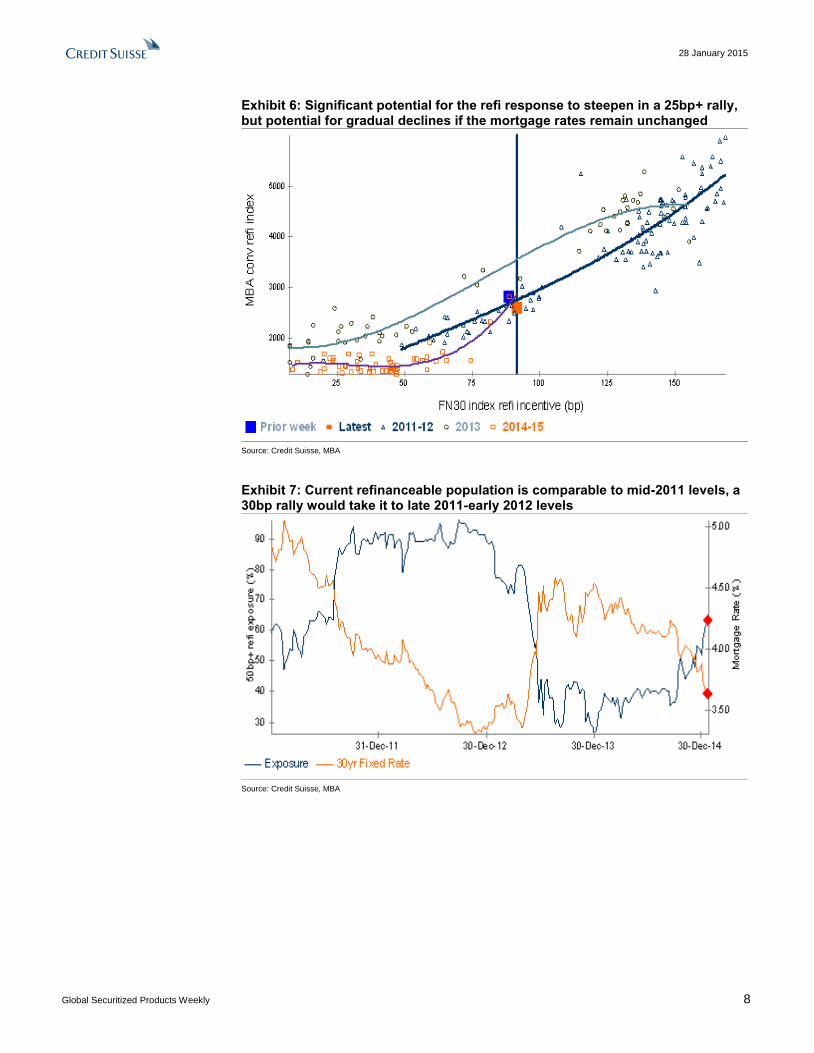

projection week over week for the 23 January report (Exhibit 6).

More interesting is what happens next. Historical data (FN30 index gross WAC minus

mortgage rate vs. refi index) from 2011 are reasonably well populated around the current

level of the FN 30-year index and suggest a roughly 300-point increase in the refi index for

a roughly 10bp mortgage rate rally (Exhibit 6). This is a realistic trajectory for small rate

movements, in our view.

However, there is a gap in historical data for the next 30bp rate rally, which raises

uncertainty as to whether the refi response will track the 2011 to early 2012 trajectory or

the late 2012 through early 2013 observations. We believe that the lower trajectory is more

likely today. Taken together, the refi index may range from 1700 for a 3.875% mortgage

rate to around 3800-4000 for a 3.375% mortgage rate. A 3.125% rate level is needed to

push the index to the 4500-5000 range, with a higher probability of tracking the lower end

of that range.

We think that for unchanged mortgage rates, the refi index may indeed start slipping

gradually and may rise modestly for small declines in rates (~5bp). We estimate that a

25bp-30bp rally (to a mid-3.30% mortgage rate) should raise the refi index to a 3800-4000

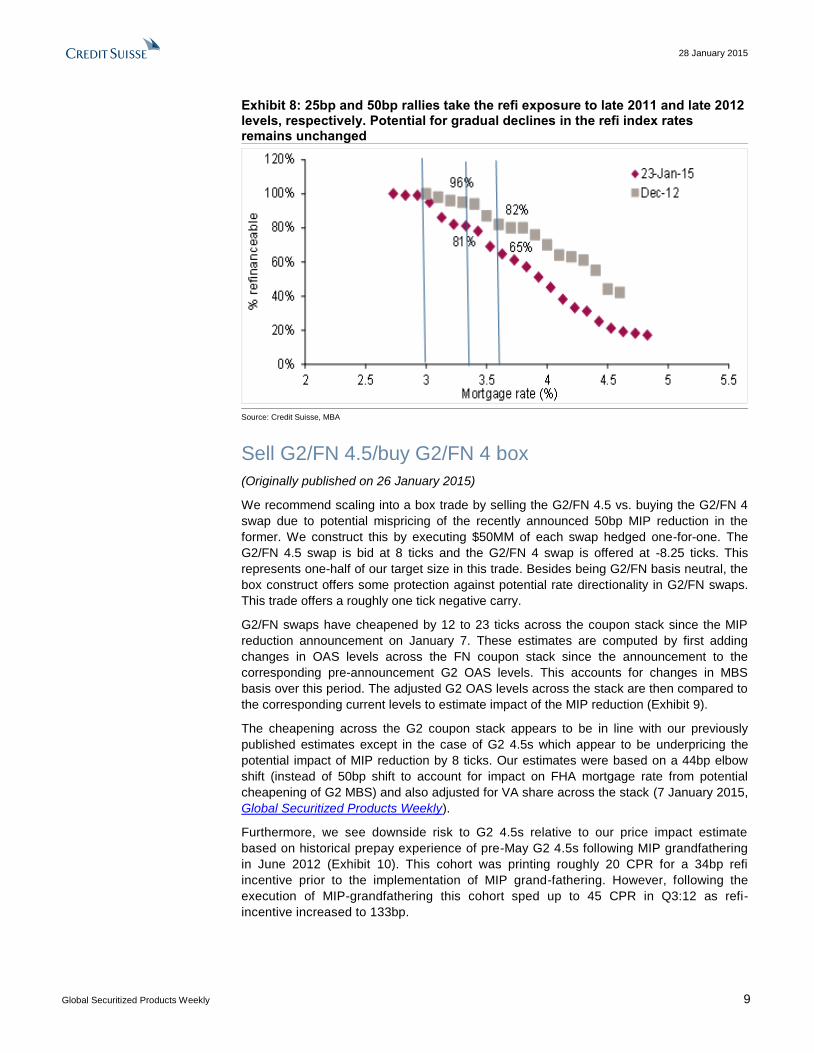

range, which is comparable to the response in fall 2011 and spring 2012. The 50bp+ in-

the-money population would rise from around 65% today to 80% in a 30bp rally. This

compares to mid-to-high 80s percent levels in H2 2011 through H1 2012 (Exhibits 7 and 8).

We estimate that in a 50bp mortgage rate rally, the refi index could reach mid-to-high

4000s. At this rate level, the market refi exposure rises into the mid-high 90s percent

range, which is comparable to late 2012 levels. That said, the response in late 2012 was

roughly 500 refi index points higher, potentially exaggerated by the full-fledged

implementation of HARP 2.0. Moreover, the overall moneyness of the index reached into

the 175bp-200bp range because of this HARP 2.0 eligible population (Exhibit 6).

This go around, the 30-year index would be roughly 140bp ITM in a 50bp rally and would

be missing the HARP boost. These factors could limit the refi index somewhat below the

H2 2012 levels. A combination of HARP impact and a possible “trying to catch the bottom

effect” potentially also helped inflate the refi index in H1 2013, although the refinanceable

population was mostly around the 80% range.

Today’s response for a comparable refi exposure is likely to be more muted due to the

absence of the HARP tailwind, in our view. Therefore, despite a sharp pick-up in the media

effect, we expect the refi index to track 2011 through early 2012 path (Exhibit 6).

28 January 2015

Global Securitized Products Weekly 8

Exhibit 6: Significant potential for the refi response to steepen in a 25bp+ rally, but potential for gradual declines if the mortgage rates remain unchanged

Source: Credit Suisse, MBA

Exhibit 7: Current refinanceable population is comparable to mid-2011 levels, a 30bp rally would take it to late 2011-early 2012 levels

Source: Credit Suisse, MBA

28 January 2015

Global Securitized Products Weekly 9

Exhibit 8: 25bp and 50bp rallies take the refi exposure to late 2011 and late 2012 levels, respectively. Potential for gradual declines in the refi index rates remains unchanged

Source: Credit Suisse, MBA

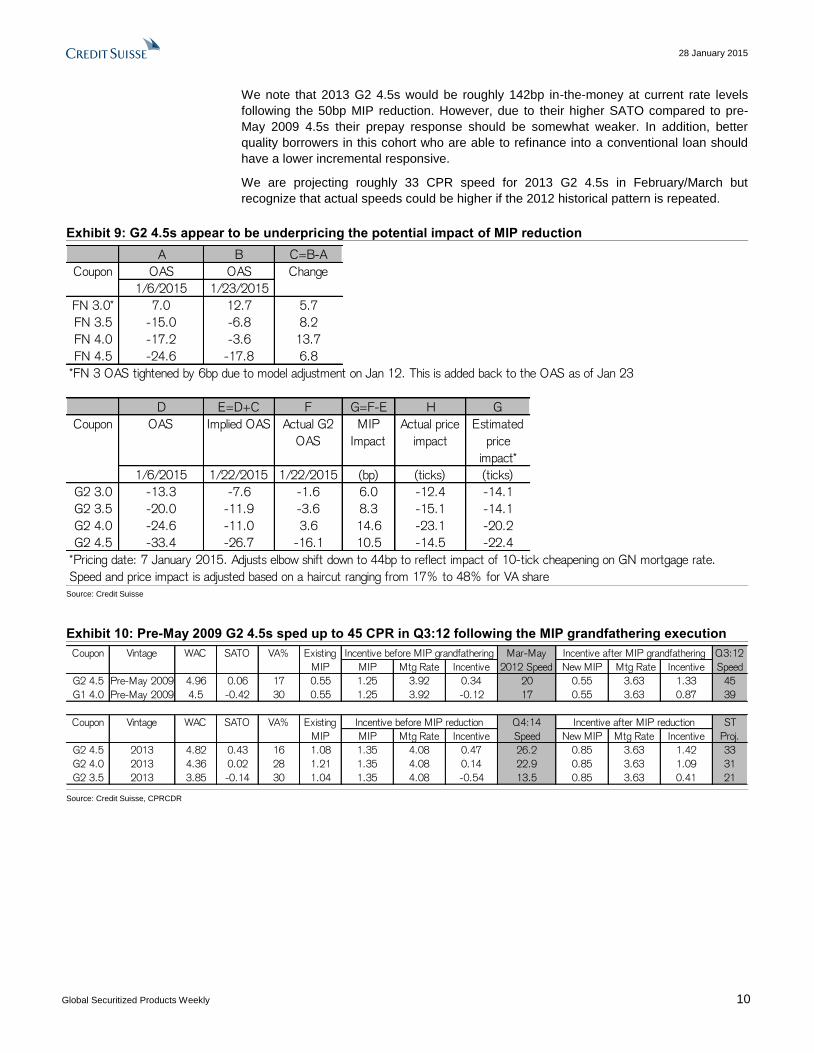

Sell G2/FN 4.5/buy G2/FN 4 box

(Originally published on 26 January 2015)

We recommend scaling into a box trade by selling the G2/FN 4.5 vs. buying the G2/FN 4

swap due to potential mispricing of the recently announced 50bp MIP reduction in the

former. We construct this by executing $50MM of each swap hedged one-for-one. The

G2/FN 4.5 swap is bid at 8 ticks and the G2/FN 4 swap is offered at -8.25 ticks. This

represents one-half of our target size in this trade. Besides being G2/FN basis neutral, the

box construct offers some protection against potential rate directionality in G2/FN swaps.

This trade offers a roughly one tick negative carry.

G2/FN swaps have cheapened by 12 to 23 ticks across the coupon stack since the MIP

reduction announcement on January 7. These estimates are computed by first adding

changes in OAS levels across the FN coupon stack since the announcement to the

corresponding pre-announcement G2 OAS levels. This accounts for changes in MBS

basis over this period. The adjusted G2 OAS levels across the stack are then compared to

the corresponding current levels to estimate impact of the MIP reduction (Exhibit 9).

The cheapening across the G2 coupon stack appears to be in line with our previously

published estimates except in the case of G2 4.5s which appear to be underpricing the

potential impact of MIP reduction by 8 ticks. Our estimates were based on a 44bp elbow

shift (instead of 50bp shift to account for impact on FHA mortgage rate from potential

cheapening of G2 MBS) and also adjusted for VA share across the stack (7 January 2015,

Global Securitized Products Weekly).

Furthermore, we see downside risk to G2 4.5s relative to our price impact estimate

based on historical prepay experience of pre-May G2 4.5s following MIP grandfathering

in June 2012 (Exhibit 10). This cohort was printing roughly 20 CPR for a 34bp refi

incentive prior to the implementation of MIP grand-fathering. However, following the

execution of MIP-grandfathering this cohort sped up to 45 CPR in Q3:12 as refi-

incentive increased to 133bp.

28 January 2015

Global Securitized Products Weekly 10

We note that 2013 G2 4.5s would be roughly 142bp in-the-money at current rate levels

following the 50bp MIP reduction. However, due to their higher SATO compared to pre-

May 2009 4.5s their prepay response should be somewhat weaker. In addition, better

quality borrowers in this cohort who are able to refinance into a conventional loan should

have a lower incremental responsive.

We are projecting roughly 33 CPR speed for 2013 G2 4.5s in February/March but

recognize that actual speeds could be higher if the 2012 historical pattern is repeated.

Exhibit 9: G2 4.5s appear to be underpricing the potential impact of MIP reduction

A B C=B-A

Coupon OAS OAS Change

1/6/2015 1/23/2015

FN 3.0* 7.0 12.7 5.7

FN 3.5 -15.0 -6.8 8.2

FN 4.0 -17.2 -3.6 13.7

FN 4.5 -24.6 -17.8 6.8

*FN 3 OAS tightened by 6bp due to model adjustment on Jan 12. This is added back to the OAS as of Jan 23

D E=D+C F G=F-E H G

Coupon OAS Implied OAS Actual G2

OAS

MIP

Impact

Actual price

impact

Estimated

price

impact*

1/6/2015 1/22/2015 1/22/2015 (bp) (ticks) (ticks)

G2 3.0 -13.3 -7.6 -1.6 6.0 -12.4 -14.1

G2 3.5 -20.0 -11.9 -3.6 8.3 -15.1 -14.1

G2 4.0 -24.6 -11.0 3.6 14.6 -23.1 -20.2

G2 4.5 -33.4 -26.7 -16.1 10.5 -14.5 -22.4

*Pricing date: 7 January 2015. Adjusts elbow shift down to 44bp to reflect impact of 10-tick cheapening on GN mortgage rate.

Speed and price impact is adjusted based on a haircut ranging from 17% to 48% for VA share Source: Credit Suisse

Exhibit 10: Pre-May 2009 G2 4.5s sped up to 45 CPR in Q3:12 following the MIP grandfathering execution

MIP Mtg Rate Incentive New MIP Mtg Rate Incentive

G2 4.5 Pre-May 2009 4.96 0.06 17 0.55 1.25 3.92 0.34 20 0.55 3.63 1.33 45

G1 4.0 Pre-May 2009 4.5 -0.42 30 0.55 1.25 3.92 -0.12 17 0.55 3.63 0.87 39

MIP Mtg Rate Incentive New MIP Mtg Rate Incentive

G2 4.5 2013 4.82 0.43 16 1.08 1.35 4.08 0.47 26.2 0.85 3.63 1.42 33

G2 4.0 2013 4.36 0.02 28 1.21 1.35 4.08 0.14 22.9 0.85 3.63 1.09 31

G2 3.5 2013 3.85 -0.14 30 1.04 1.35 4.08 -0.54 13.5 0.85 3.63 0.41 21

Existing

MIP

Incentive before MIP reduction Q4:14

Speed

Incentive after MIP reduction ST

Proj.

Vintage WAC SATO VA%Coupon

Coupon Vintage WAC SATO VA%

Mar-May

2012 Speed

Q3:12

Speed

Incentive after MIP grandfatheringIncentive before MIP grandfatheringExisting

MIP

Source: Credit Suisse, CPRCDR

28 January 2015

Global Securitized Products Weekly 11

Non-Agency MBS Ocwen, revisited – recent activity and impact on RMBS

Last Friday saw a fast and furious news cycle for Ocwen and HLSS. In the morning,

BlueMountain delivered a notice of default to the trustee on two HSART series; in the

afternoon, RMBS investors filed a notice of non-performance for 119 trusts and the CA

DBO settled its claims from two weeks ago. After recapping the events that have occurred

over the last week, we revisit our framework approach introduced two weeks ago to help

RMBS investors think about the ramifications of an Ocwen setback.

A recap of the last week’s activities

On Friday 1/23, hedge fund BlueMountain Capital Management, LLC delivered a

notice of default to the trustee of the HLSS Servicer Advance Receivables Trust

(HSART) Series 2012-T2 and 2013-T3 Notes. BlueMountain alleged that events of

defaults exist as a result of Ocwen’s material breach of Indenture covenants by failing to

“comply with applicable laws and requisite servicing obligations,” breach of warranty due

to the “adverse effect on Ocwen’s business and financial condition” from violations of law,

and inadequate collateralization levels for the Notes.

As evidence of imprudent servicing practices, BlueMountain cited Ocwen’s consent order

with the NYDFS, troubles with the California Department of Business Oversight (CA DBO),

rating agency downgrades and share price declines, among other items. BlueMountain

alleged that these events should trigger an early amortization event and a 3.0% increase

to the interest rate for each Note. In addition, BlueMountain disclosed that it holds short

positions in Ocwen and HLSS.

The press release for this notice can be found here.

Ocwen has since defended itself against the allegations in a letter to the Indenture Trustee.

Also on Friday, Gibbs & Bruns LLP filed a Notice of Non-Performance against Ocwen

for 119 trusts, stating that Ocwen failed to perform as servicer in the following ways:

“Use of Trust funds to “pay” Ocwen’s required “borrower relief” obligations under a

regulatory settlement, through implementation of modifications on Trust-owned

mortgages that have shifted the costs of the settlement to the Trusts and enriched

Ocwen unjustly.

Employing conflicted servicing practices that enriched Ocwen’s corporate affiliates,

including Altisource and Home Loan Servicing Solutions, to the detriment of the Trusts,

investors, and borrowers.

Engaging in imprudent and wholly improper loan modification, advancing, and advance

recovery practices.

Failure to maintain adequate records, communicate effectively with borrowers, or comply

with applicable laws, including consumer protection and foreclosure laws.

Failure to account for and remit accurately to the Trusts cash flows from, and amounts

realized on, Trust-owned mortgages.”

The notice states that the holders’ expert analysts determined “that Trusts serviced by

Ocwen have performed materially worse than Trusts serviced by other servicers.” The notice

also claims that these failures constitute an event of default, and that “[t]he Holders intend to

take further action to recover these losses and protect the Trusts’ assets and mortgages.”

No damage amounts were announced and how this issue would be remedied remains to

be seen. The investors could be seeking remedies such as Ocwen’s removal from the

trusts or potential damage payments. The distribution of any hypothetical payments made

related to this issue remains unclear.

Marc Firestein

+1 212 325 4379

Jonathan Corwin

+1 212 538 6490

28 January 2015

Global Securitized Products Weekly 12

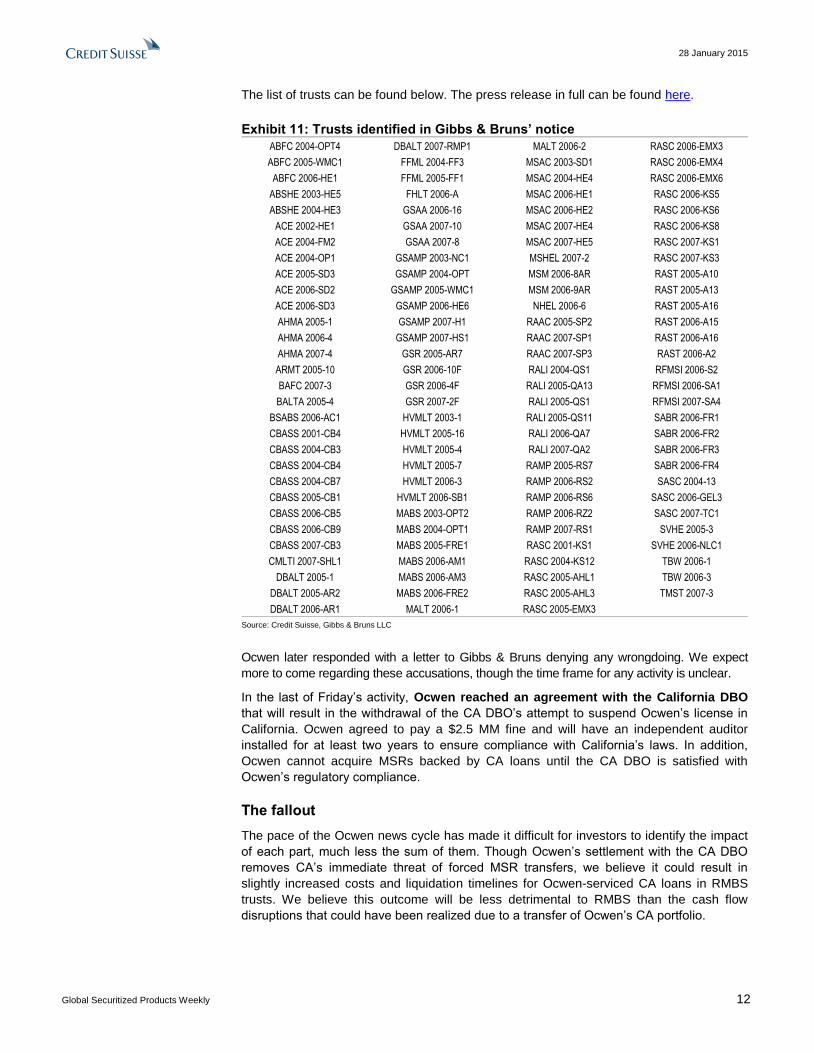

The list of trusts can be found below. The press release in full can be found here.

Exhibit 11: Trusts identified in Gibbs & Bruns’ notice

ABFC 2004-OPT4 DBALT 2007-RMP1 MALT 2006-2 RASC 2006-EMX3

ABFC 2005-WMC1 FFML 2004-FF3 MSAC 2003-SD1 RASC 2006-EMX4

ABFC 2006-HE1 FFML 2005-FF1 MSAC 2004-HE4 RASC 2006-EMX6

ABSHE 2003-HE5 FHLT 2006-A MSAC 2006-HE1 RASC 2006-KS5

ABSHE 2004-HE3 GSAA 2006-16 MSAC 2006-HE2 RASC 2006-KS6

ACE 2002-HE1 GSAA 2007-10 MSAC 2007-HE4 RASC 2006-KS8

ACE 2004-FM2 GSAA 2007-8 MSAC 2007-HE5 RASC 2007-KS1

ACE 2004-OP1 GSAMP 2003-NC1 MSHEL 2007-2 RASC 2007-KS3

ACE 2005-SD3 GSAMP 2004-OPT MSM 2006-8AR RAST 2005-A10

ACE 2006-SD2 GSAMP 2005-WMC1 MSM 2006-9AR RAST 2005-A13

ACE 2006-SD3 GSAMP 2006-HE6 NHEL 2006-6 RAST 2005-A16

AHMA 2005-1 GSAMP 2007-H1 RAAC 2005-SP2 RAST 2006-A15

AHMA 2006-4 GSAMP 2007-HS1 RAAC 2007-SP1 RAST 2006-A16

AHMA 2007-4 GSR 2005-AR7 RAAC 2007-SP3 RAST 2006-A2

ARMT 2005-10 GSR 2006-10F RALI 2004-QS1 RFMSI 2006-S2

BAFC 2007-3 GSR 2006-4F RALI 2005-QA13 RFMSI 2006-SA1

BALTA 2005-4 GSR 2007-2F RALI 2005-QS1 RFMSI 2007-SA4

BSABS 2006-AC1 HVMLT 2003-1 RALI 2005-QS11 SABR 2006-FR1

CBASS 2001-CB4 HVMLT 2005-16 RALI 2006-QA7 SABR 2006-FR2

CBASS 2004-CB3 HVMLT 2005-4 RALI 2007-QA2 SABR 2006-FR3

CBASS 2004-CB4 HVMLT 2005-7 RAMP 2005-RS7 SABR 2006-FR4

CBASS 2004-CB7 HVMLT 2006-3 RAMP 2006-RS2 SASC 2004-13

CBASS 2005-CB1 HVMLT 2006-SB1 RAMP 2006-RS6 SASC 2006-GEL3

CBASS 2006-CB5 MABS 2003-OPT2 RAMP 2006-RZ2 SASC 2007-TC1

CBASS 2006-CB9 MABS 2004-OPT1 RAMP 2007-RS1 SVHE 2005-3

CBASS 2007-CB3 MABS 2005-FRE1 RASC 2001-KS1 SVHE 2006-NLC1

CMLTI 2007-SHL1 MABS 2006-AM1 RASC 2004-KS12 TBW 2006-1

DBALT 2005-1 MABS 2006-AM3 RASC 2005-AHL1 TBW 2006-3

DBALT 2005-AR2 MABS 2006-FRE2 RASC 2005-AHL3 TMST 2007-3

DBALT 2006-AR1 MALT 2006-1 RASC 2005-EMX3

Source: Credit Suisse, Gibbs & Bruns LLC

Ocwen later responded with a letter to Gibbs & Bruns denying any wrongdoing. We expect

more to come regarding these accusations, though the time frame for any activity is unclear.

In the last of Friday’s activity, Ocwen reached an agreement with the California DBO

that will result in the withdrawal of the CA DBO’s attempt to suspend Ocwen’s license in

California. Ocwen agreed to pay a $2.5 MM fine and will have an independent auditor

installed for at least two years to ensure compliance with California’s laws. In addition,

Ocwen cannot acquire MSRs backed by CA loans until the CA DBO is satisfied with

Ocwen’s regulatory compliance.

The fallout

The pace of the Ocwen news cycle has made it difficult for investors to identify the impact

of each part, much less the sum of them. Though Ocwen’s settlement with the CA DBO

removes CA’s immediate threat of forced MSR transfers, we believe it could result in

slightly increased costs and liquidation timelines for Ocwen-serviced CA loans in RMBS

trusts. We believe this outcome will be less detrimental to RMBS than the cash flow

disruptions that could have been realized due to a transfer of Ocwen’s CA portfolio.

28 January 2015

Global Securitized Products Weekly 13

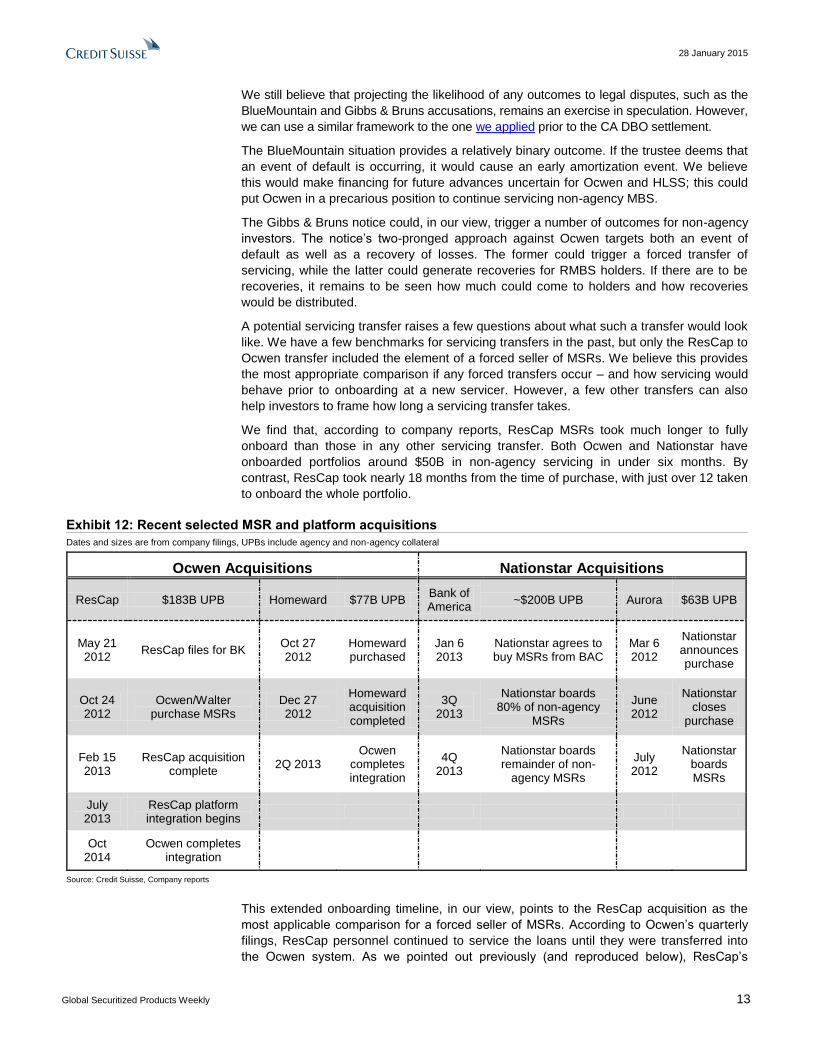

We still believe that projecting the likelihood of any outcomes to legal disputes, such as the

BlueMountain and Gibbs & Bruns accusations, remains an exercise in speculation. However,

we can use a similar framework to the one we applied prior to the CA DBO settlement.

The BlueMountain situation provides a relatively binary outcome. If the trustee deems that

an event of default is occurring, it would cause an early amortization event. We believe

this would make financing for future advances uncertain for Ocwen and HLSS; this could

put Ocwen in a precarious position to continue servicing non-agency MBS.

The Gibbs & Bruns notice could, in our view, trigger a number of outcomes for non-agency

investors. The notice’s two-pronged approach against Ocwen targets both an event of

default as well as a recovery of losses. The former could trigger a forced transfer of

servicing, while the latter could generate recoveries for RMBS holders. If there are to be

recoveries, it remains to be seen how much could come to holders and how recoveries

would be distributed.

A potential servicing transfer raises a few questions about what such a transfer would look

like. We have a few benchmarks for servicing transfers in the past, but only the ResCap to

Ocwen transfer included the element of a forced seller of MSRs. We believe this provides

the most appropriate comparison if any forced transfers occur – and how servicing would

behave prior to onboarding at a new servicer. However, a few other transfers can also

help investors to frame how long a servicing transfer takes.

We find that, according to company reports, ResCap MSRs took much longer to fully

onboard than those in any other servicing transfer. Both Ocwen and Nationstar have

onboarded portfolios around $50B in non-agency servicing in under six months. By

contrast, ResCap took nearly 18 months from the time of purchase, with just over 12 taken

to onboard the whole portfolio.

Exhibit 12: Recent selected MSR and platform acquisitions

Dates and sizes are from company filings, UPBs include agency and non-agency collateral

Ocwen Acquisitions Nationstar Acquisitions

ResCap $183B UPB Homeward $77B UPB Bank of America

~$200B UPB Aurora $63B UPB

May 21 2012

ResCap files for BK Oct 27 2012

Homeward purchased

Jan 6 2013

Nationstar agrees to buy MSRs from BAC

Mar 6 2012

Nationstar announces purchase

Oct 24 2012

Ocwen/Walter purchase MSRs

Dec 27 2012

Homeward acquisition completed

3Q 2013

Nationstar boards 80% of non-agency

MSRs

June 2012

Nationstar closes

purchase

Feb 15 2013

ResCap acquisition complete

2Q 2013 Ocwen

completes integration

4Q 2013

Nationstar boards remainder of non-

agency MSRs

July 2012

Nationstar boards MSRs

July 2013

ResCap platform integration begins

Oct 2014

Ocwen completes integration

Source: Credit Suisse, Company reports

This extended onboarding timeline, in our view, points to the ResCap acquisition as the

most applicable comparison for a forced seller of MSRs. According to Ocwen’s quarterly

filings, ResCap personnel continued to service the loans until they were transferred into

the Ocwen system. As we pointed out previously (and reproduced below), ResCap’s

28 January 2015

Global Securitized Products Weekly 14

servicing tactics were only modestly different post-filing and pre-integration. A forced seller

of MSRs would likely remain the servicer, keeping most policies in place, until the assets

could be fully transferred to the new servicer.

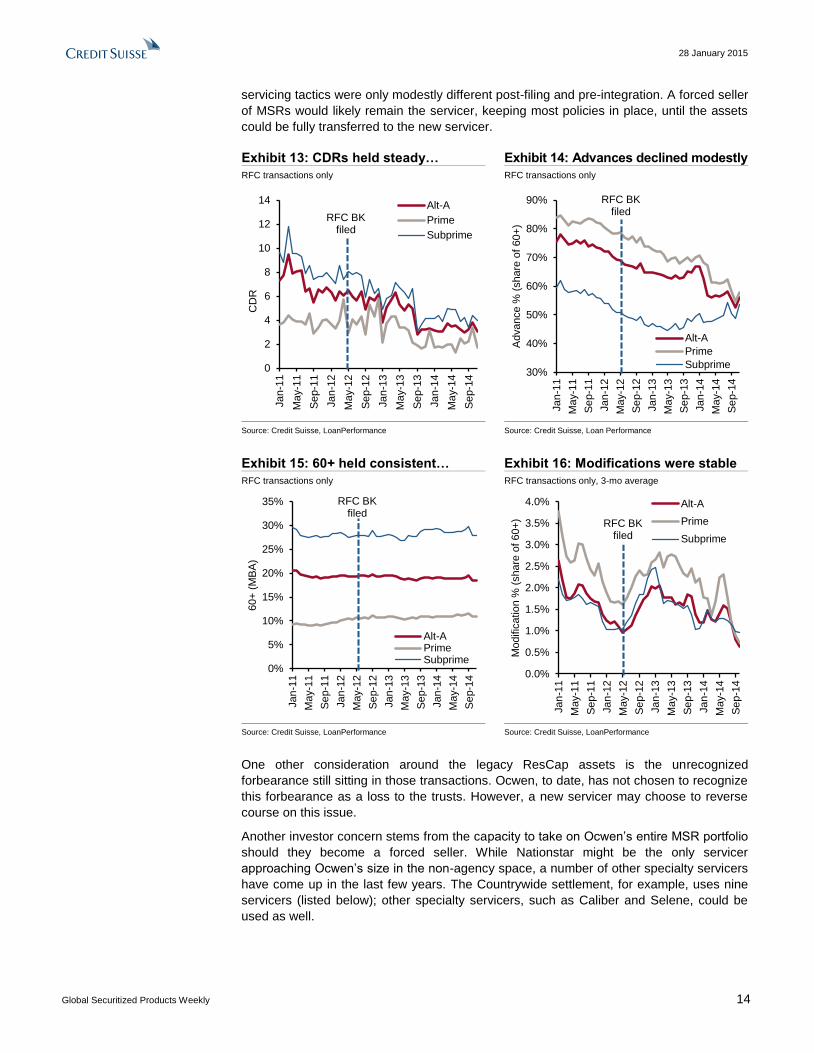

Exhibit 13: CDRs held steady… Exhibit 14: Advances declined modestly

RFC transactions only RFC transactions only

0

2

4

6

8

10

12

14

Jan

-11

May-1

1

Se

p-1

1

Jan

-12

May-1

2

Se

p-1

2

Jan

-13

May-1

3

Se

p-1

3

Jan

-14

May-1

4

Se

p-1

4

CD

R

Alt-A

Prime

Subprime

RFC BK filed

30%

40%

50%

60%

70%

80%

90%

Jan

-11

Ma

y-1

1

Se

p-1

1

Jan

-12

Ma

y-1

2

Se

p-1

2

Jan

-13

Ma

y-1

3

Se

p-1

3

Jan

-14

Ma

y-1

4

Se

p-1

4

Advance %

(share

of

60+

)

Alt-A

Prime

Subprime

RFC BK filed

Source: Credit Suisse, LoanPerformance Source: Credit Suisse, Loan Performance

Exhibit 15: 60+ held consistent… Exhibit 16: Modifications were stable

RFC transactions only RFC transactions only, 3-mo average

0%

5%

10%

15%

20%

25%

30%

35%

Jan

-11

Ma

y-1

1

Se

p-1

1

Jan

-12

May-1

2

Se

p-1

2

Jan

-13

Ma

y-1

3

Se

p-1

3

Jan

-14

Ma

y-1

4

Se

p-1

4

60+

(M

BA

)

Alt-APrimeSubprime

RFC BK filed

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Jan

-11

Ma

y-1

1

Se

p-1

1

Jan

-12

Ma

y-1

2

Se

p-1

2

Jan

-13

Ma

y-1

3

Se

p-1

3

Jan

-14

Ma

y-1

4

Se

p-1

4

Modific

atio

n %

(share

of 60+

)Alt-A

Prime

Subprime

RFC BK filed

Source: Credit Suisse, LoanPerformance Source: Credit Suisse, LoanPerformance

One other consideration around the legacy ResCap assets is the unrecognized

forbearance still sitting in those transactions. Ocwen, to date, has not chosen to recognize

this forbearance as a loss to the trusts. However, a new servicer may choose to reverse

course on this issue.

Another investor concern stems from the capacity to take on Ocwen’s entire MSR portfolio

should they become a forced seller. While Nationstar might be the only servicer

approaching Ocwen’s size in the non-agency space, a number of other specialty servicers

have come up in the last few years. The Countrywide settlement, for example, uses nine

servicers (listed below); other specialty servicers, such as Caliber and Selene, could be

used as well.

28 January 2015

Global Securitized Products Weekly 15

Exhibit 17: Approved subservicers from the Countrywide settlement

Names as of 10/2011; some subservicers now operate under another name

Bayview Loan Servicing, LLC

Residential Credit Solutions, Inc.

Resurgent Capital Services, LP (d/b/a Resurgent Mortgage Servicing)

Nationstar Mortgage LLC

Specialized Loan Servicing LLC

Select Portfolio Servicing, Inc.

Vantium Capital Inc. (d/b/a Acqura Loan Services)

Greentree Servicing LLC

FCI Lender Services, Inc.

Source: Credit Suisse, Court documents

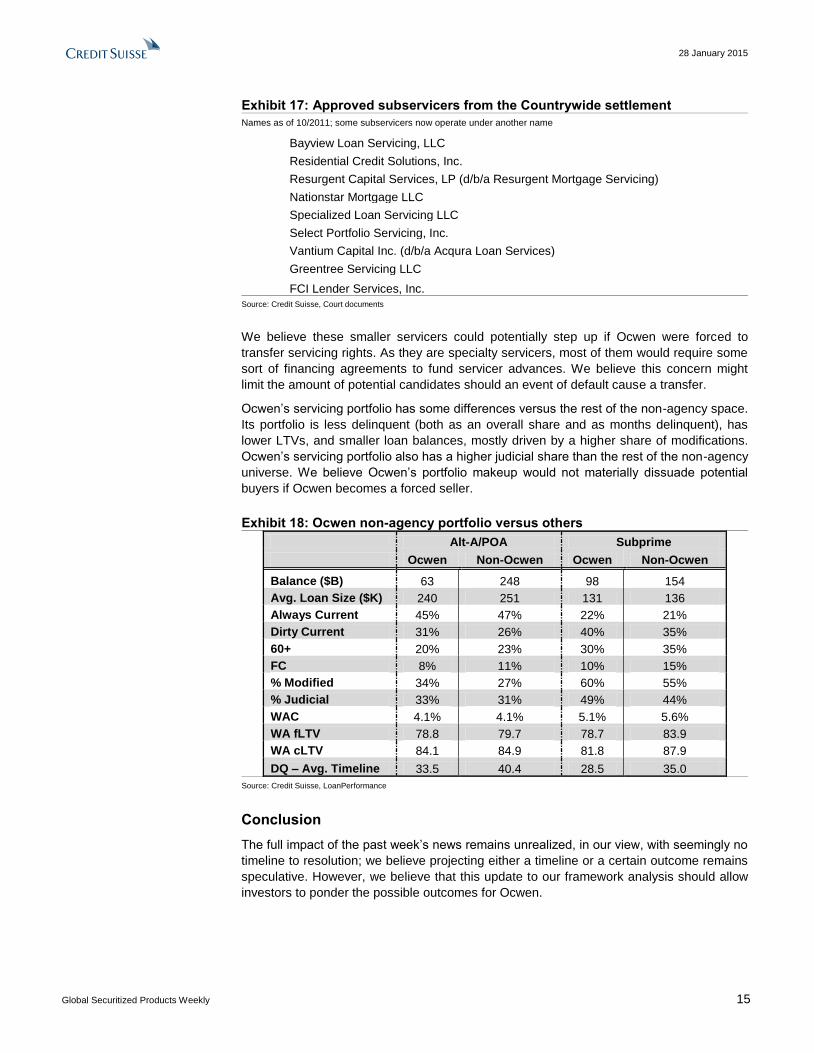

We believe these smaller servicers could potentially step up if Ocwen were forced to

transfer servicing rights. As they are specialty servicers, most of them would require some

sort of financing agreements to fund servicer advances. We believe this concern might

limit the amount of potential candidates should an event of default cause a transfer.

Ocwen’s servicing portfolio has some differences versus the rest of the non-agency space.

Its portfolio is less delinquent (both as an overall share and as months delinquent), has

lower LTVs, and smaller loan balances, mostly driven by a higher share of modifications.

Ocwen’s servicing portfolio also has a higher judicial share than the rest of the non-agency

universe. We believe Ocwen’s portfolio makeup would not materially dissuade potential

buyers if Ocwen becomes a forced seller.

Exhibit 18: Ocwen non-agency portfolio versus others

Alt-A/POA Subprime

Ocwen Non-Ocwen Ocwen Non-Ocwen

Balance ($B) 63 248 98 154

Avg. Loan Size ($K) 240 251 131 136

Always Current 45% 47% 22% 21%

Dirty Current 31% 26% 40% 35%

60+ 20% 23% 30% 35%

FC 8% 11% 10% 15%

% Modified 34% 27% 60% 55%

% Judicial 33% 31% 49% 44%

WAC 4.1% 4.1% 5.1% 5.6%

WA fLTV 78.8 79.7 78.7 83.9

WA cLTV 84.1 84.9 81.8 87.9

DQ – Avg. Timeline 33.5 40.4 28.5 35.0

Source: Credit Suisse, LoanPerformance

Conclusion

The full impact of the past week’s news remains unrealized, in our view, with seemingly no

timeline to resolution; we believe projecting either a timeline or a certain outcome remains

speculative. However, we believe that this update to our framework analysis should allow

investors to ponder the possible outcomes for Ocwen.

28 January 2015

Global Securitized Products Weekly 16

CMBS

Market activity and relative value The CMBS market continues to perform very well, on a relative basis, as it remains largely

immune from the macro-led volatility that has affected other financial markets, including

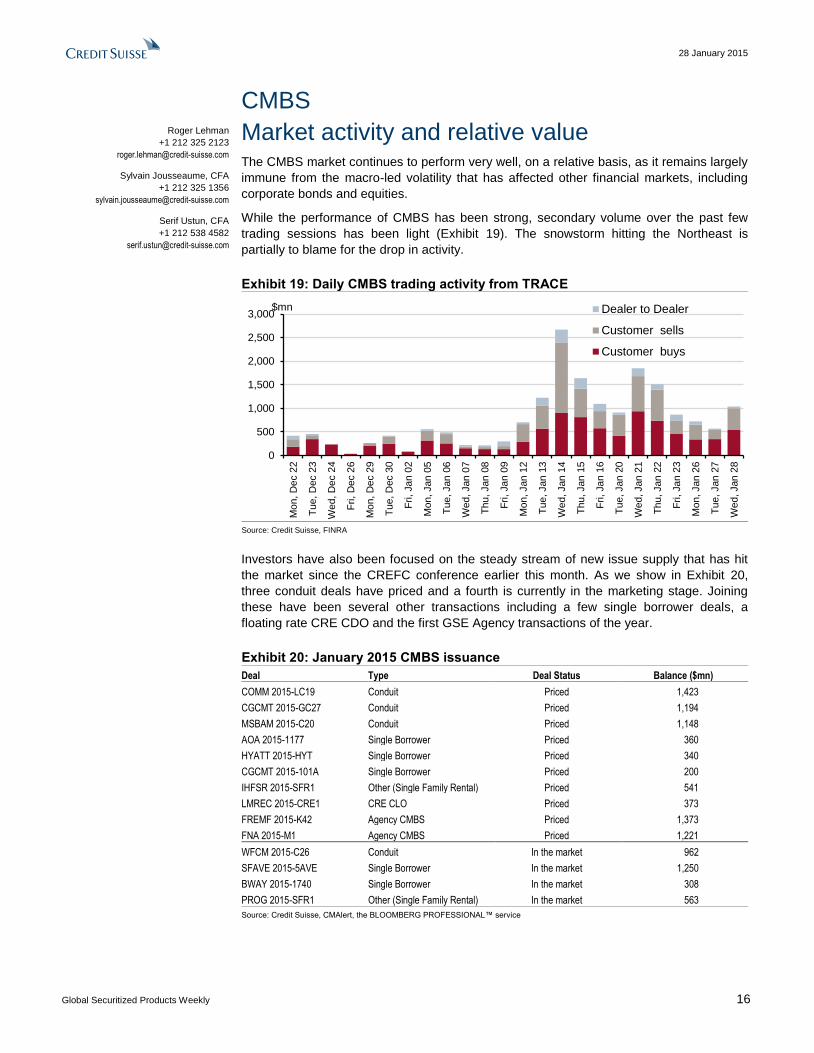

corporate bonds and equities.

While the performance of CMBS has been strong, secondary volume over the past few

trading sessions has been light (Exhibit 19). The snowstorm hitting the Northeast is

partially to blame for the drop in activity.

Exhibit 19: Daily CMBS trading activity from TRACE

0

500

1,000

1,500

2,000

2,500

3,000

Mo

n, D

ec 2

2

Tu

e, D

ec 2

3

We

d, D

ec 2

4

Fri, D

ec 2

6

Mo

n, D

ec 2

9

Tu

e, D

ec 3

0

Fri, Ja

n 0

2

Mo

n, Jan

05

Tu

e, Jan

06

We

d, Jan

07

Th

u, Jan

08

Fri, Ja

n 0

9

Mo

n, Jan

12

Tu

e, Jan

13

We

d, Jan

14

Th

u, Jan

15

Fri, Ja

n 1

6

Tu

e, Jan

20

Wed, Jan 2

1

Th

u, Jan

22

Fri, Ja

n 2

3

Mo

n, Jan

26

Tu

e, Jan

27

We

d, Jan

28

Dealer to Dealer

Customer sells

Customer buys

$mn

Source: Credit Suisse, FINRA

Investors have also been focused on the steady stream of new issue supply that has hit

the market since the CREFC conference earlier this month. As we show in Exhibit 20,

three conduit deals have priced and a fourth is currently in the marketing stage. Joining

these have been several other transactions including a few single borrower deals, a

floating rate CRE CDO and the first GSE Agency transactions of the year.

Exhibit 20: January 2015 CMBS issuance

Deal Type Deal Status Balance ($mn)

COMM 2015-LC19 Conduit Priced 1,423

CGCMT 2015-GC27 Conduit Priced 1,194

MSBAM 2015-C20 Conduit Priced 1,148

AOA 2015-1177 Single Borrower Priced 360

HYATT 2015-HYT Single Borrower Priced 340

CGCMT 2015-101A Single Borrower Priced 200

IHFSR 2015-SFR1 Other (Single Family Rental) Priced 541

LMREC 2015-CRE1 CRE CLO Priced 373

FREMF 2015-K42 Agency CMBS Priced 1,373

FNA 2015-M1 Agency CMBS Priced 1,221

WFCM 2015-C26 Conduit In the market 962

SFAVE 2015-5AVE Single Borrower In the market 1,250

BWAY 2015-1740 Single Borrower In the market 308

PROG 2015-SFR1 Other (Single Family Rental) In the market 563

Source: Credit Suisse, CMAlert, the BLOOMBERG PROFESSIONAL™ service

Roger Lehman

+1 212 325 2123

Sylvain Jousseaume, CFA

+1 212 325 1356

Serif Ustun, CFA

+1 212 538 4582

28 January 2015

Global Securitized Products Weekly 17

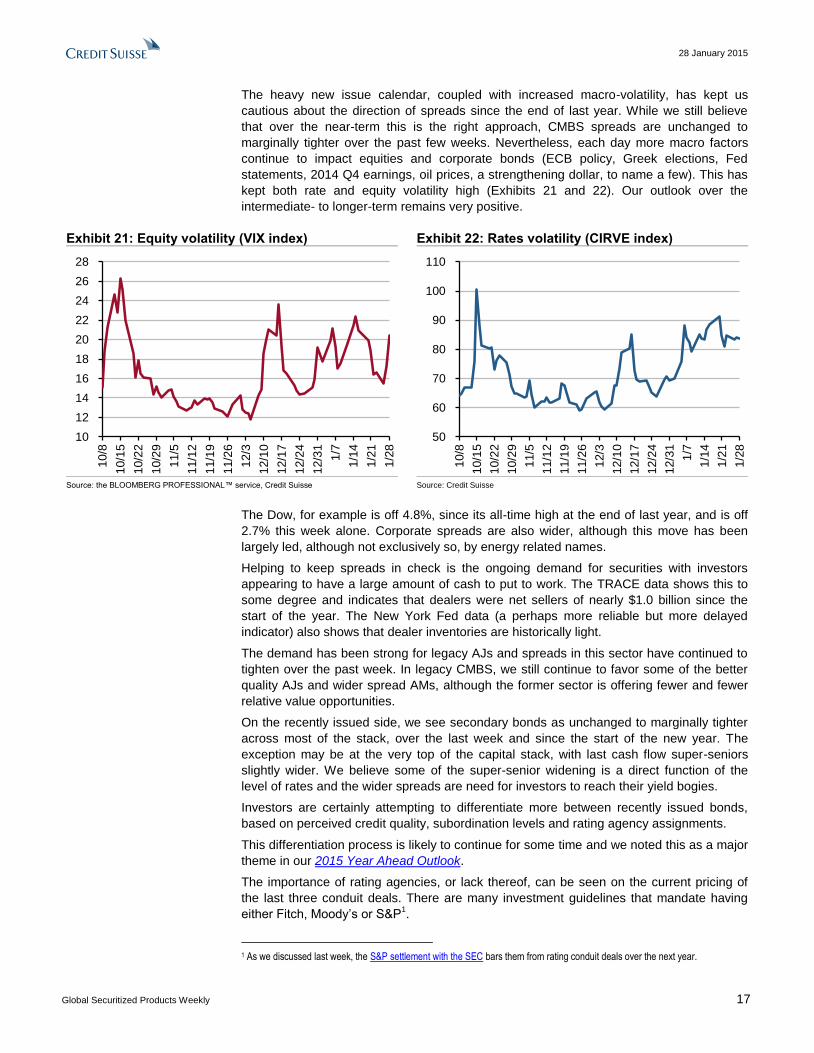

The heavy new issue calendar, coupled with increased macro-volatility, has kept us

cautious about the direction of spreads since the end of last year. While we still believe

that over the near-term this is the right approach, CMBS spreads are unchanged to

marginally tighter over the past few weeks. Nevertheless, each day more macro factors

continue to impact equities and corporate bonds (ECB policy, Greek elections, Fed

statements, 2014 Q4 earnings, oil prices, a strengthening dollar, to name a few). This has

kept both rate and equity volatility high (Exhibits 21 and 22). Our outlook over the

intermediate- to longer-term remains very positive.

Exhibit 21: Equity volatility (VIX index) Exhibit 22: Rates volatility (CIRVE index)

10

12

14

16

18

20

22

24

26

28

10/8

10/1

5

10/2

2

10/2

9

11/5

11/1

2

11/1

9

11/2

6

12/3

12/1

0

12/1

7

12/2

4

12/3

1

1/7

1/1

4

1/2

1

1/2

8

50

60

70

80

90

100

110

10/8

10/1

5

10/2

2

10/2

9

11/5

11/1

2

11/1

9

11/2

6

12/3

12/1

0

12/1

7

12/2

4

12/3

1

1/7

1/1

4

1/2

1

1/2

8

Source: the BLOOMBERG PROFESSIONAL™ service, Credit Suisse Source: Credit Suisse

The Dow, for example is off 4.8%, since its all-time high at the end of last year, and is off

2.7% this week alone. Corporate spreads are also wider, although this move has been

largely led, although not exclusively so, by energy related names.

Helping to keep spreads in check is the ongoing demand for securities with investors

appearing to have a large amount of cash to put to work. The TRACE data shows this to

some degree and indicates that dealers were net sellers of nearly $1.0 billion since the

start of the year. The New York Fed data (a perhaps more reliable but more delayed

indicator) also shows that dealer inventories are historically light.

The demand has been strong for legacy AJs and spreads in this sector have continued to

tighten over the past week. In legacy CMBS, we still continue to favor some of the better

quality AJs and wider spread AMs, although the former sector is offering fewer and fewer

relative value opportunities.

On the recently issued side, we see secondary bonds as unchanged to marginally tighter

across most of the stack, over the last week and since the start of the new year. The

exception may be at the very top of the capital stack, with last cash flow super-seniors

slightly wider. We believe some of the super-senior widening is a direct function of the

level of rates and the wider spreads are need for investors to reach their yield bogies.

Investors are certainly attempting to differentiate more between recently issued bonds,

based on perceived credit quality, subordination levels and rating agency assignments.

This differentiation process is likely to continue for some time and we noted this as a major

theme in our 2015 Year Ahead Outlook.

The importance of rating agencies, or lack thereof, can be seen on the current pricing of

the last three conduit deals. There are many investment guidelines that mandate having

either Fitch, Moody’s or S&P1.

1 As we discussed last week, the S&P settlement with the SEC bars them from rating conduit deals over the next year.

28 January 2015

Global Securitized Products Weekly 18

On the newest deals, the tranches that were missing ratings from all of these agencies

priced noticeably wider. For example, the single-A and triple-B minus tranches, of COMM

2015-LC19, came at S+205 bp and S+360 bp, respectively, with the bonds carrying a

Fitch rating. Neither the MSBAM 2015-C20 nor the CGCMT 2015-GC27 deal had ratings

from any of these three raters and the two single-A minus tranches came 40 bp wider.

While the cash markets have been somewhat immune to the heightened volatility, the

price swings are definitely more pronounced in the CMBX market, where more macro-

oriented investors tend to play a greater role.

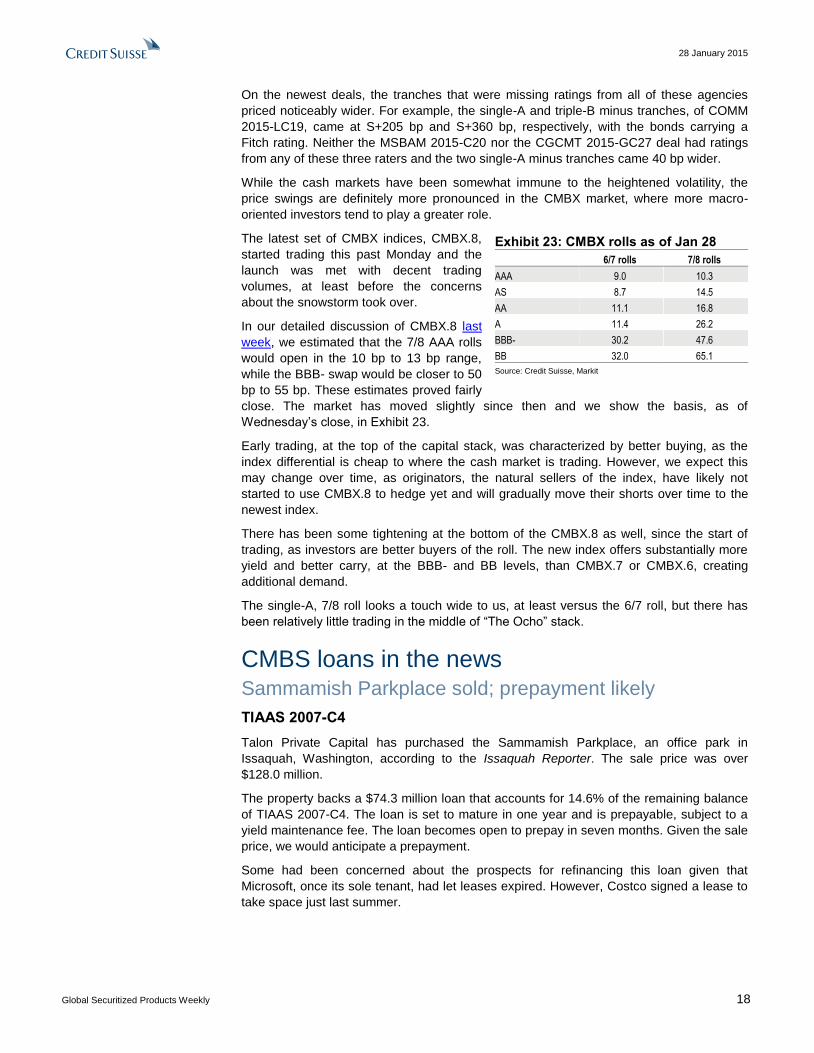

The latest set of CMBX indices, CMBX.8,

started trading this past Monday and the

launch was met with decent trading

volumes, at least before the concerns

about the snowstorm took over.

In our detailed discussion of CMBX.8 last

week, we estimated that the 7/8 AAA rolls

would open in the 10 bp to 13 bp range,

while the BBB- swap would be closer to 50

bp to 55 bp. These estimates proved fairly

close. The market has moved slightly since then and we show the basis, as of

Wednesday’s close, in Exhibit 23.

Early trading, at the top of the capital stack, was characterized by better buying, as the

index differential is cheap to where the cash market is trading. However, we expect this

may change over time, as originators, the natural sellers of the index, have likely not

started to use CMBX.8 to hedge yet and will gradually move their shorts over time to the

newest index.

There has been some tightening at the bottom of the CMBX.8 as well, since the start of

trading, as investors are better buyers of the roll. The new index offers substantially more

yield and better carry, at the BBB- and BB levels, than CMBX.7 or CMBX.6, creating

additional demand.

The single-A, 7/8 roll looks a touch wide to us, at least versus the 6/7 roll, but there has

been relatively little trading in the middle of “The Ocho” stack.

CMBS loans in the news Sammamish Parkplace sold; prepayment likely

TIAAS 2007-C4

Talon Private Capital has purchased the Sammamish Parkplace, an office park in

Issaquah, Washington, according to the Issaquah Reporter. The sale price was over

$128.0 million.

The property backs a $74.3 million loan that accounts for 14.6% of the remaining balance

of TIAAS 2007-C4. The loan is set to mature in one year and is prepayable, subject to a

yield maintenance fee. The loan becomes open to prepay in seven months. Given the sale

price, we would anticipate a prepayment.

Some had been concerned about the prospects for refinancing this loan given that

Microsoft, once its sole tenant, had let leases expired. However, Costco signed a lease to

take space just last summer.

Exhibit 23: CMBX rolls as of Jan 28

6/7 rolls 7/8 rolls

AAA 9.0 10.3

AS 8.7 14.5

AA 11.1 16.8

A 11.4 26.2

BBB- 30.2 47.6

BB 32.0 65.1

Source: Credit Suisse, Markit

28 January 2015

Global Securitized Products Weekly 19

Expansion near Green Acres Mall

COMM 2013-GAM

The owners of the Green Acres Mall, in Valley Stream, New York is building an adjacent

shopping center, according to an article in Newsday. The article states that Macerich Co

will spend an estimated $83.7 million on the new center, to be called Green Acres

Commons. In addition, the company plans to spend an estimated $79 million on

improvements to the mall.

The mall backs a $325.0 million loan that is securitized in a single borrower deal, COMM

2013-GAM. The loan is scheduled to mature in February 2021 and is subject to

defeasance until a few months prior to that date.

Improvements to the mall are already under way, according to the article, and the mall

plans to remain opening during the renovation, which is expected to take 15 years to

complete. Macerich was granted tax emptions and other incentives for the project.

Macerich purchased the Green Acres Mall in 2012 for $500 million and then purchased the

adjacent movie theater, where the new construction will take place, for $22.5 million, in 2013.

Sierra Vista Mall is now REO

COMM 2006-C8

Sierra Vista Mall was sold in a foreclosure proceeding according to ABC News and various

other news sources. The trust that owned the mortgage was the buyer, at $39 million, and

the asset is now REO. The lender was the only bidder at the auction.

The Sierra Vista Mall had backed a $77.8 million loan that accounts for 3.2% of COMM

2006-C8. The loan has been with the special servicer since September 2013. The notes

indicate that a modification was discussed but that tactic was apparently scrapped.

In addition to the outstanding loan balance the loan has accumulated $4.7 million in

servicing advances and interest as well as an additional $2.0 million in cumulative ASERs.

The property was appraised at $50.0 million a year ago and the most recent appraisal

reduction amount totals nearly $40.0 million.

The property backing the loan totaled about 405k square feet. Sears is the only one of the

anchors that is part of the collateral. Since the loan was securitized, Mervyn’s has been

replaced by Kohl’s and the MB2 Raceway has replaced the former Gottschalks.

New lease at 411 East Wisconsin

JPMCC 2006-LDP7

Northwestern Mutual has taken 56k square feet at the 411 East Wisconsin office building

in Milwaukee, according to the Milwaukee Business Journal. The lease accounts for about

8.6% of the space and should boost occupancy to 88%, the article states.

The building backs a $65.2 million loan that represents 2.1% of JPMCC 2006-LDP7. The

loan is scheduled to mature in September. The most recent financials show a DSCR of

1.2x and an occupancy of 77%.

The property sold last year for $74.3 million, to an affiliate of Five Mile Capital. This was

well below the 2006 appraised valued of $98.2 million. The buyers have begun a

$17.5 million redevelopment at the building.

28 January 2015

Global Securitized Products Weekly 20

Logistics Pointe trades for $52 million

MSC 2011-C3

Logistics Pointe, a 1.1 million square foot industrial park, sold for $52.1 million, according

to the Charlotte Business Journal. LRC Opportunity Fund and New York Life Real Estate

Investors were partners in the purchase.

The property now backs a $23.9 million loan securitized in MSC 2011-C3 (1.7% of the

deal). The property had been appraised at $40.0 million in May 2011, at securitization. The

purchase price implies a current LTV of under 46%. The loan is scheduled to mature in

June 2016 and is subject to defeasance, until early next year.

The Plaza Evergreen Park may sell for $14 million

CSMC 2006-C4

Lormax Stern has agreed to pay $14 million for The Plaza Evergreen Park, according to

Crain’s Chicago. With only four tenants remaining at the property the thinking is Lormax

would demolish it and redevelop it into a new retail operation.

The property backs a delinquent loan securitized in CSMC 2006-C4 ($18.4 million and

0.6% of the deal). The loan has been with the special servicer since October 2009.

The servicing notes indicate that a loan sale failed to close but we believe this was a prior

sale. A previous deal to sell the loan fell through and the special servicer restarted the

foreclosure process.

In addition to the outstanding balance the loan has accumulated over $9.1 million in

servicing advances and interest as well as nearly $902k in cumulative ASERs. The ASERs

have stopped growing, however, as the loan was deemed non-recoverable.

Factoring all of this in, we would expect a near total loss to the trust, with little or

no recovery.

The loss will continue to write down Class F (originally rated single-A).

January conduit credit update The 60+-day legacy conduit delinquency rate fell 1 bp in January, as the monthly changes

have once again taken on a little bit of a see-saw pattern of ups and downs. The

delinquency rate has been down in two of the past three months, but this follows four

consecutive increases, in the middle of last year. This rises brought some concerns that

the pace of credit deteriorate, in legacy loans, had started to escalate. We do not believe

that to be true, but changes are occurring.

As we have been discussing, and detailed in the 2015 CMBS Year Ahead Outlook, it

is our view that while the outlook for legacy credit has improved, over the past two

years, the pace of those gains is starting to wane and improvements will be more

gradual in 2015. From July 2012 to June 2014 the conduit delinquency rate fell in

16 months, bringing the rate from 10.6% down to 8.4%. However, since then, the rate has

increased and even with the latest drop, it is up 30 bp over the past few months.

However, we believe the legacy delinquency rate and, for that matter, other credit

metrics which rely on the current balance, may be prone to volatile and misleading

reads. In fact, over the past four months, even as the delinquency rate has been rising,

the total dollar balance of delinquent loans fell.

28 January 2015

Global Securitized Products Weekly 21

The problem is that the amount of delinquent loans fell less rapidly, relative to the amount

outstanding (the denominator), pushing up the overall delinquency rate. In a simplified

example, assume from one month to the next no conduit loans change their delinquency

status but several current loans mature and pay off. The delinquency rate will actually rise.

While the profile of the remaining universe has arguably gotten worse, it is hard to say

credit deteriorated. Generally, if the rate of pay downs is relatively faster than the rate of

resolutions (cures and liquidations) the legacy delinquency rate will rise regardless of the

pace of new delinquencies.

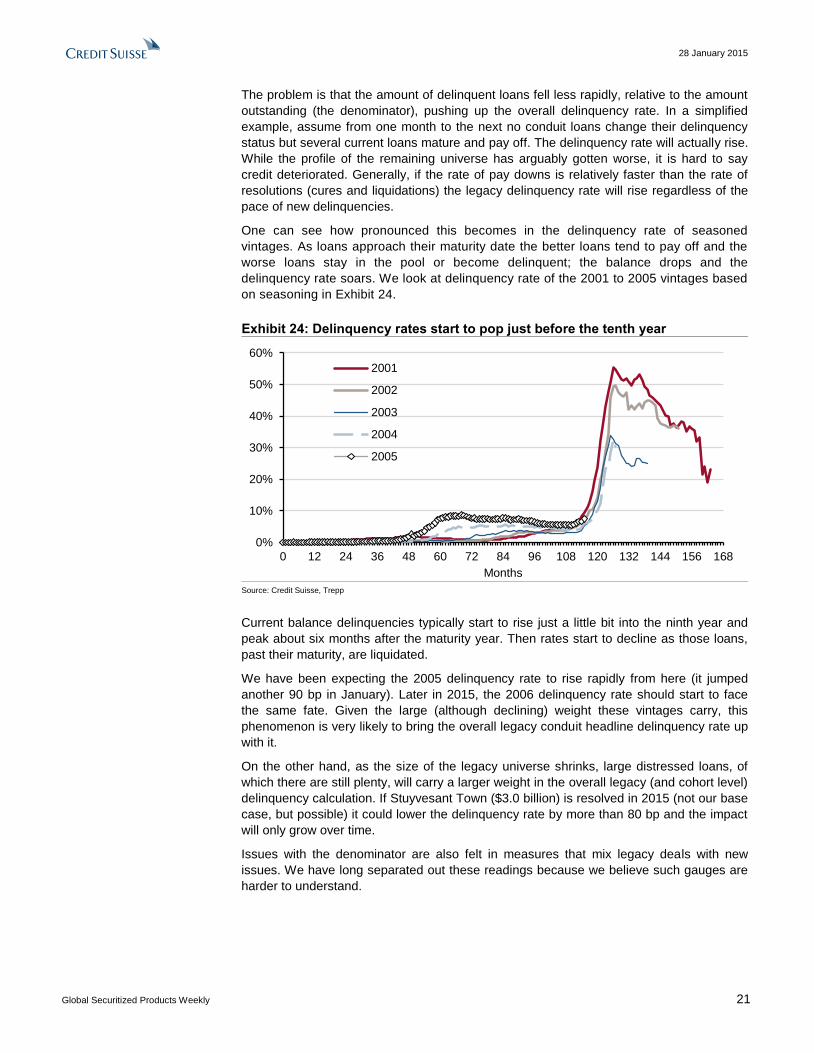

One can see how pronounced this becomes in the delinquency rate of seasoned

vintages. As loans approach their maturity date the better loans tend to pay off and the

worse loans stay in the pool or become delinquent; the balance drops and the

delinquency rate soars. We look at delinquency rate of the 2001 to 2005 vintages based

on seasoning in Exhibit 24.

Exhibit 24: Delinquency rates start to pop just before the tenth year

0%

10%

20%

30%

40%

50%

60%

0 12 24 36 48 60 72 84 96 108 120 132 144 156 168

Months

2001

2002

2003

2004

2005

Source: Credit Suisse, Trepp

Current balance delinquencies typically start to rise just a little bit into the ninth year and

peak about six months after the maturity year. Then rates start to decline as those loans,

past their maturity, are liquidated.

We have been expecting the 2005 delinquency rate to rise rapidly from here (it jumped

another 90 bp in January). Later in 2015, the 2006 delinquency rate should start to face

the same fate. Given the large (although declining) weight these vintages carry, this

phenomenon is very likely to bring the overall legacy conduit headline delinquency rate up

with it.

On the other hand, as the size of the legacy universe shrinks, large distressed loans, of

which there are still plenty, will carry a larger weight in the overall legacy (and cohort level)

delinquency calculation. If Stuyvesant Town ($3.0 billion) is resolved in 2015 (not our base

case, but possible) it could lower the delinquency rate by more than 80 bp and the impact

will only grow over time.

Issues with the denominator are also felt in measures that mix legacy deals with new

issues. We have long separated out these readings because we believe such gauges are

harder to understand.

28 January 2015

Global Securitized Products Weekly 22

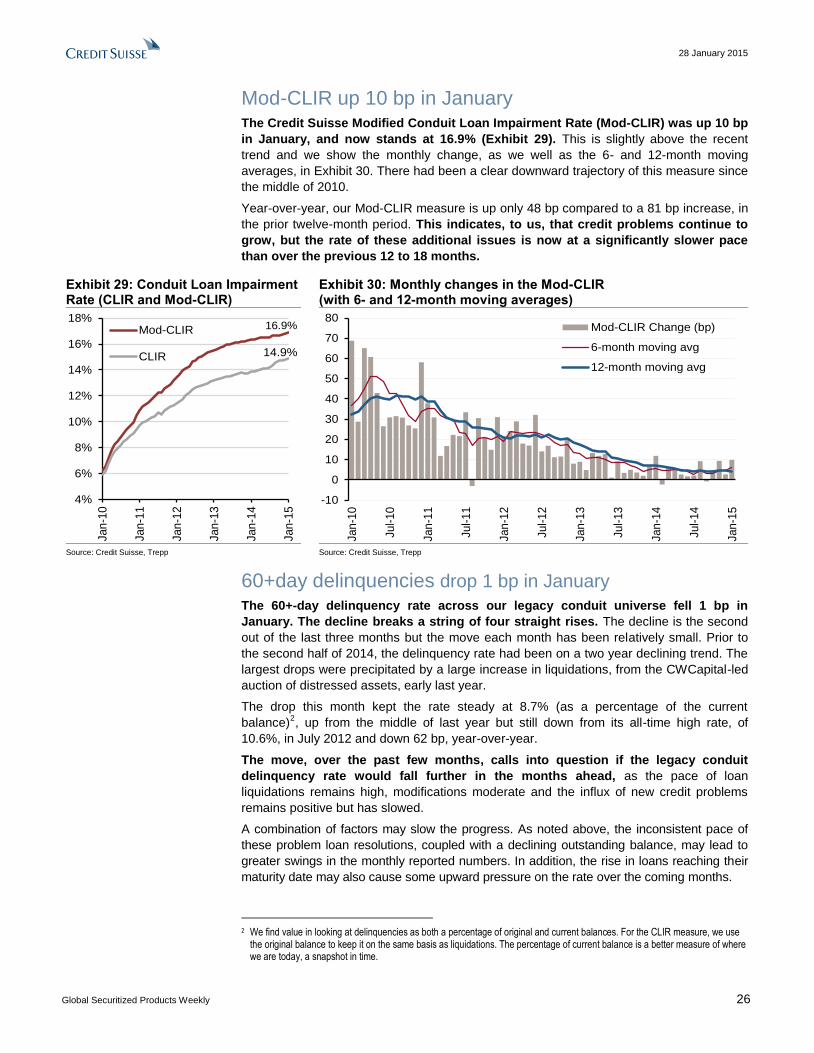

The Conduit Loan Impairment Rate (CLIR)

There are many credit metrics that can be followed and each has advantages and

disadvantages. One of the more popular headline statistics is the overall delinquency rate

(with some using 30+-day and others using 60+-day measures).

While delinquencies are an important component to understanding the current

credit picture, we do not believe that, by themselves, they tell the full story. Just as

important is how loans are transitioning in and out of their respective buckets. Loans can

cure, be modified, or liquidated (often at a loss). Not all of these are positive credit events.

We think an unchanged delinquency rate, that is accompanied by a high level of

loan liquidations or modifications, is a sign of a deteriorating, rather than a stable,

credit environment. Credit problems will first show as delinquencies in the initial stages

of a credit downturn and attract the most attention. But we firmly believe that liquidations

and mods, which only start to appear later in the cycle, should not be ignored.

As we have often seen in the past, changes in the rate of liquidations and

modifications can have a distortive effect on the delinquency rate. In a month when

delinquent loan liquidations are above the trend, there is more pressure on the overall

delinquency rate.

In order to capture the dual influence of delinquencies and liquidations, we have

adapted a simple construct in which we combine the two measures, adding together

the delinquency rate (today’s current problems) and liquidations (credit problems

that have left the CMBS universe). This combination provides what we call the

conduit loan impairment rate (CLIR).

For the delinquency rate, we have chosen to use the current balance of loans that are

60+-days delinquent (which also includes loans in the process of foreclosure, REO, and

non-performing matured balloons). To this measure, we add the balance of loans that

have been liquidated and calculate the conduit loan impairment rate, as a percentage of

the original outstanding balance of the universe we are analyzing.

We then enhanced this measure to capture the growing number of modified loans.

We have dubbed this measure Mod-CLIR. While modified loans are often reported as

current, many of them are not performing as originally intended and we believe are credit

impaired. In summary, our Mod-CLIR measure incorporates loans that have been modified

with respect to their monthly payments but would not otherwise be captured in our original

CLIR measure. Loans that have received only a maturity modification are not included.

Legacy analysis covers the pre-2010 universe

Before we go on and discuss this month’s credit statistics, we also think it is important to

understand and clearly define the universe that one is analyzing, as this can also heavily

influence the calculation of credit metrics.

We focused on the CMBS fixed-rate conduit deals and specifically legacy issuance

(those deals issued in 2008 and earlier). It is easier, in our view, to focus on a fixed set

of deals and loans to make meaningful comparisons over time than an ever-changing

universe (that is one reason why we also like to analyze vintage level information).

The set of conduit deals we used in our analysis has a current outstanding balance of

approximately $321 billion (and an original balance of $844 billion).

We have seen other measures that incorporate the larger universe of conduit deals,

including those issued over the past four years. Fortunately, at the moment, these newer

vintage deals (issued in 2010 and later) have few serious credit issues. Adding the most

recent conduit issuance, which has been accelerating, would increase the denominator in

28 January 2015

Global Securitized Products Weekly 23

our calculation and suppress the overall percentages as well as any of the changes in

percentages from month to month. Including the recent issuance would push the overall

delinquency rate significantly lower and would mute the month-over-month change.

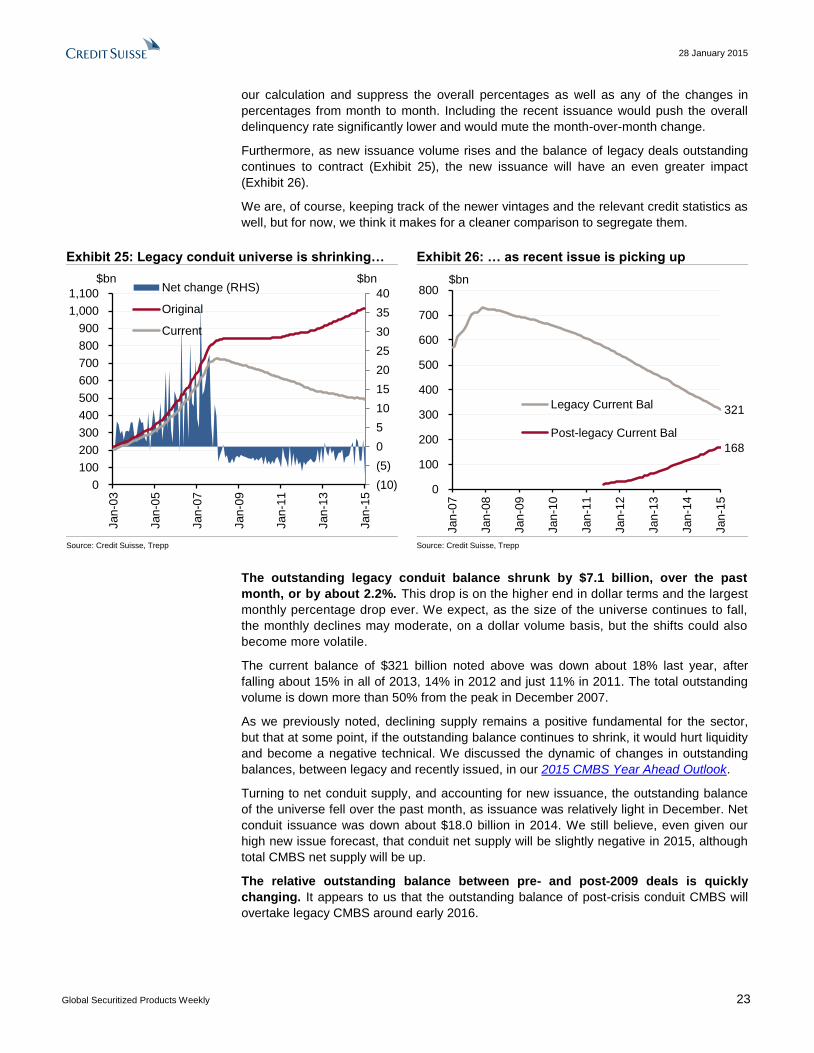

Furthermore, as new issuance volume rises and the balance of legacy deals outstanding

continues to contract (Exhibit 25), the new issuance will have an even greater impact

(Exhibit 26).

We are, of course, keeping track of the newer vintages and the relevant credit statistics as

well, but for now, we think it makes for a cleaner comparison to segregate them.

Exhibit 25: Legacy conduit universe is shrinking… Exhibit 26: … as recent issue is picking up

(10)

(5)

0

5

10

15

20

25

30

35

40

0

100

200

300

400

500

600

700

800

900

1,000

1,100

Jan

-03

Jan

-05

Jan

-07

Jan

-09

Jan

-11

Jan

-13

Jan

-15

Net change (RHS)

Original

Current

$bn $bn

321

168

0

100

200

300

400

500

600

700

800

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Legacy Current Bal

Post-legacy Current Bal

$bn

Source: Credit Suisse, Trepp Source: Credit Suisse, Trepp

The outstanding legacy conduit balance shrunk by $7.1 billion, over the past

month, or by about 2.2%. This drop is on the higher end in dollar terms and the largest

monthly percentage drop ever. We expect, as the size of the universe continues to fall,

the monthly declines may moderate, on a dollar volume basis, but the shifts could also

become more volatile.

The current balance of $321 billion noted above was down about 18% last year, after

falling about 15% in all of 2013, 14% in 2012 and just 11% in 2011. The total outstanding

volume is down more than 50% from the peak in December 2007.

As we previously noted, declining supply remains a positive fundamental for the sector,

but that at some point, if the outstanding balance continues to shrink, it would hurt liquidity

and become a negative technical. We discussed the dynamic of changes in outstanding

balances, between legacy and recently issued, in our 2015 CMBS Year Ahead Outlook.

Turning to net conduit supply, and accounting for new issuance, the outstanding balance

of the universe fell over the past month, as issuance was relatively light in December. Net

conduit issuance was down about $18.0 billion in 2014. We still believe, even given our

high new issue forecast, that conduit net supply will be slightly negative in 2015, although

total CMBS net supply will be up.

The relative outstanding balance between pre- and post-2009 deals is quickly

changing. It appears to us that the outstanding balance of post-crisis conduit CMBS will

overtake legacy CMBS around early 2016.

28 January 2015

Global Securitized Products Weekly 24

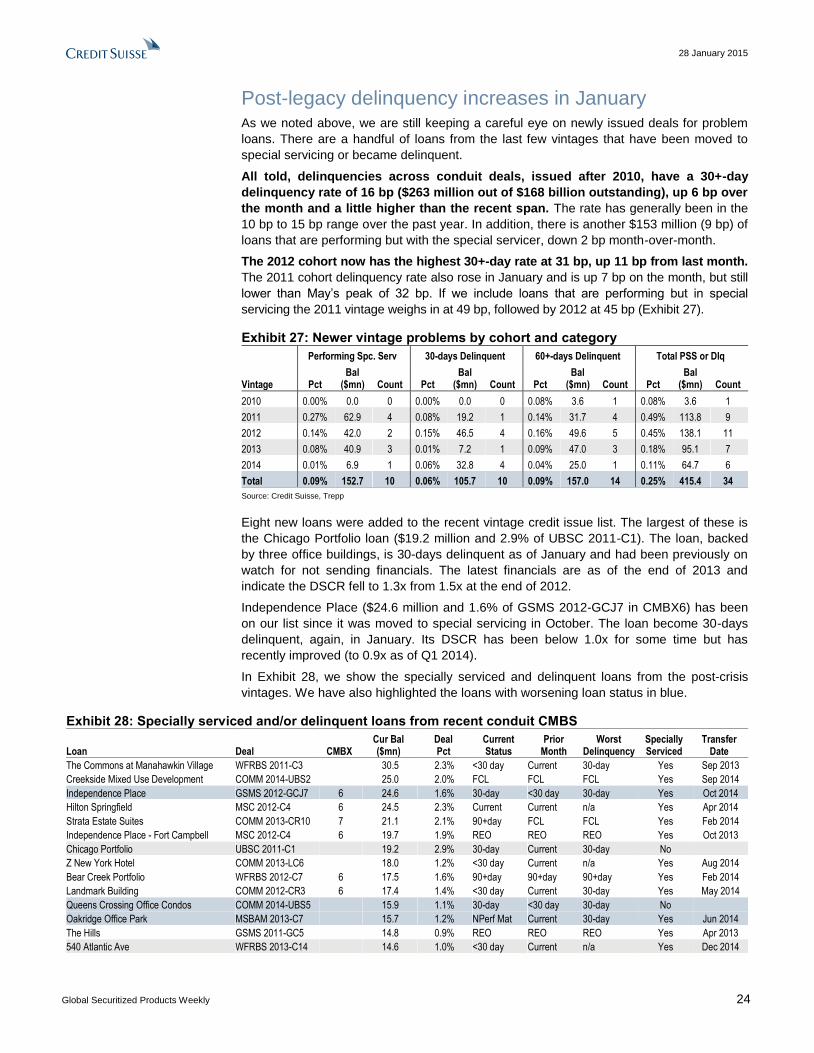

Post-legacy delinquency increases in January As we noted above, we are still keeping a careful eye on newly issued deals for problem

loans. There are a handful of loans from the last few vintages that have been moved to

special servicing or became delinquent.

All told, delinquencies across conduit deals, issued after 2010, have a 30+-day

delinquency rate of 16 bp ($263 million out of $168 billion outstanding), up 6 bp over

the month and a little higher than the recent span. The rate has generally been in the

10 bp to 15 bp range over the past year. In addition, there is another $153 million (9 bp) of

loans that are performing but with the special servicer, down 2 bp month-over-month.

The 2012 cohort now has the highest 30+-day rate at 31 bp, up 11 bp from last month.

The 2011 cohort delinquency rate also rose in January and is up 7 bp on the month, but still

lower than May’s peak of 32 bp. If we include loans that are performing but in special

servicing the 2011 vintage weighs in at 49 bp, followed by 2012 at 45 bp (Exhibit 27).

Exhibit 27: Newer vintage problems by cohort and category

Performing Spc. Serv 30-days Delinquent 60+-days Delinquent Total PSS or Dlq

Vintage Pct Bal

($mn) Count Pct Bal

($mn) Count Pct Bal

($mn) Count Pct Bal

($mn) Count

2010 0.00% 0.0 0 0.00% 0.0 0 0.08% 3.6 1 0.08% 3.6 1

2011 0.27% 62.9 4 0.08% 19.2 1 0.14% 31.7 4 0.49% 113.8 9

2012 0.14% 42.0 2 0.15% 46.5 4 0.16% 49.6 5 0.45% 138.1 11

2013 0.08% 40.9 3 0.01% 7.2 1 0.09% 47.0 3 0.18% 95.1 7

2014 0.01% 6.9 1 0.06% 32.8 4 0.04% 25.0 1 0.11% 64.7 6

Total 0.09% 152.7 10 0.06% 105.7 10 0.09% 157.0 14 0.25% 415.4 34

Source: Credit Suisse, Trepp

Eight new loans were added to the recent vintage credit issue list. The largest of these is

the Chicago Portfolio loan ($19.2 million and 2.9% of UBSC 2011-C1). The loan, backed

by three office buildings, is 30-days delinquent as of January and had been previously on

watch for not sending financials. The latest financials are as of the end of 2013 and

indicate the DSCR fell to 1.3x from 1.5x at the end of 2012.

Independence Place ($24.6 million and 1.6% of GSMS 2012-GCJ7 in CMBX6) has been

on our list since it was moved to special servicing in October. The loan become 30-days

delinquent, again, in January. Its DSCR has been below 1.0x for some time but has

recently improved (to 0.9x as of Q1 2014).

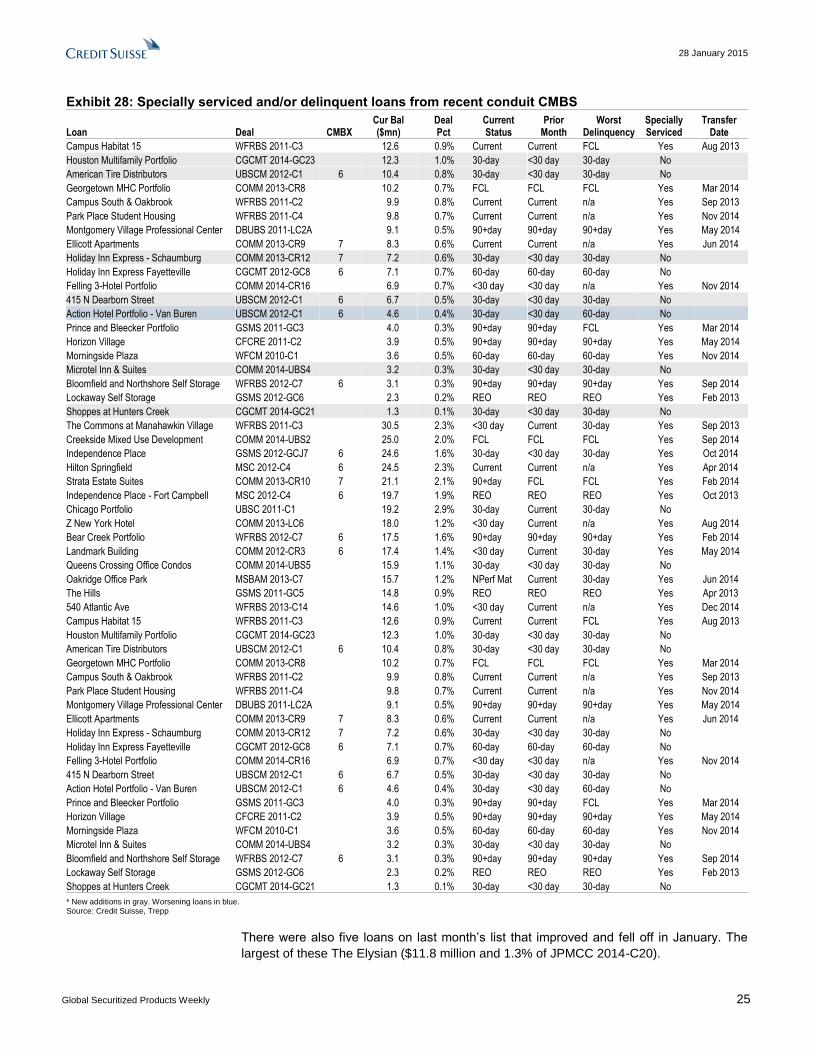

In Exhibit 28, we show the specially serviced and delinquent loans from the post-crisis

vintages. We have also highlighted the loans with worsening loan status in blue.

Exhibit 28: Specially serviced and/or delinquent loans from recent conduit CMBS

Loan Deal CMBX Cur Bal ($mn)

Deal Pct

Current Status

Prior Month

Worst Delinquency

Specially Serviced

Transfer Date

The Commons at Manahawkin Village WFRBS 2011-C3 30.5 2.3% <30 day Current 30-day Yes Sep 2013

Creekside Mixed Use Development COMM 2014-UBS2 25.0 2.0% FCL FCL FCL Yes Sep 2014

Independence Place GSMS 2012-GCJ7 6 24.6 1.6% 30-day <30 day 30-day Yes Oct 2014

Hilton Springfield MSC 2012-C4 6 24.5 2.3% Current Current n/a Yes Apr 2014

Strata Estate Suites COMM 2013-CR10 7 21.1 2.1% 90+day FCL FCL Yes Feb 2014

Independence Place - Fort Campbell MSC 2012-C4 6 19.7 1.9% REO REO REO Yes Oct 2013

Chicago Portfolio UBSC 2011-C1 19.2 2.9% 30-day Current 30-day No

Z New York Hotel COMM 2013-LC6 18.0 1.2% <30 day Current n/a Yes Aug 2014

Bear Creek Portfolio WFRBS 2012-C7 6 17.5 1.6% 90+day 90+day 90+day Yes Feb 2014

Landmark Building COMM 2012-CR3 6 17.4 1.4% <30 day Current 30-day Yes May 2014

Queens Crossing Office Condos COMM 2014-UBS5 15.9 1.1% 30-day <30 day 30-day No

Oakridge Office Park MSBAM 2013-C7 15.7 1.2% NPerf Mat Current 30-day Yes Jun 2014

The Hills GSMS 2011-GC5 14.8 0.9% REO REO REO Yes Apr 2013

540 Atlantic Ave WFRBS 2013-C14 14.6 1.0% <30 day Current n/a Yes Dec 2014

28 January 2015

Global Securitized Products Weekly 25

Exhibit 28: Specially serviced and/or delinquent loans from recent conduit CMBS

Loan Deal CMBX Cur Bal ($mn)

Deal Pct

Current Status

Prior Month

Worst Delinquency

Specially Serviced

Transfer Date

Campus Habitat 15 WFRBS 2011-C3 12.6 0.9% Current Current FCL Yes Aug 2013

Houston Multifamily Portfolio CGCMT 2014-GC23 12.3 1.0% 30-day <30 day 30-day No

American Tire Distributors UBSCM 2012-C1 6 10.4 0.8% 30-day <30 day 30-day No

Georgetown MHC Portfolio COMM 2013-CR8 10.2 0.7% FCL FCL FCL Yes Mar 2014

Campus South & Oakbrook WFRBS 2011-C2 9.9 0.8% Current Current n/a Yes Sep 2013

Park Place Student Housing WFRBS 2011-C4 9.8 0.7% Current Current n/a Yes Nov 2014

Montgomery Village Professional Center DBUBS 2011-LC2A 9.1 0.5% 90+day 90+day 90+day Yes May 2014

Ellicott Apartments COMM 2013-CR9 7 8.3 0.6% Current Current n/a Yes Jun 2014

Holiday Inn Express - Schaumburg COMM 2013-CR12 7 7.2 0.6% 30-day <30 day 30-day No

Holiday Inn Express Fayetteville CGCMT 2012-GC8 6 7.1 0.7% 60-day 60-day 60-day No

Felling 3-Hotel Portfolio COMM 2014-CR16 6.9 0.7% <30 day <30 day n/a Yes Nov 2014

415 N Dearborn Street UBSCM 2012-C1 6 6.7 0.5% 30-day <30 day 30-day No

Action Hotel Portfolio - Van Buren UBSCM 2012-C1 6 4.6 0.4% 30-day <30 day 60-day No

Prince and Bleecker Portfolio GSMS 2011-GC3 4.0 0.3% 90+day 90+day FCL Yes Mar 2014

Horizon Village CFCRE 2011-C2 3.9 0.5% 90+day 90+day 90+day Yes May 2014