Embed Size (px)

Citation preview

SP

O-Z

WL7

58-2

0080

325

Dev

elop

men

t of I

T an

d IT

ES

O

ffsho

ring

–O

ppor

tuni

ties

for C

ount

ries

The

Wor

ld B

ank

and

Inte

rnat

iona

l Fin

ance

C

orpo

ratio

n –

Glo

bal I

nfor

mat

ion

and

Com

mun

icat

ions

Tec

hnol

ogie

s D

epar

tmen

t

info

Dev

Don

ors’

Mee

ting

19 J

une

2008

This

repo

rt is

sol

ely

for t

he u

se o

f clie

nt p

erso

nnel

. N

o pa

rt of

it m

ay b

e ci

rcul

ated

, qu

oted

, or r

epro

duce

d fo

r dis

tribu

tion

outs

ide

the

clie

nt o

rgan

izat

ion

with

out p

rior

writ

ten

appr

oval

from

McK

inse

y &

Com

pany

. Thi

s m

ater

ial w

as u

sed

by M

cKin

sey

&

Com

pany

dur

ing

an o

ral p

rese

ntat

ion;

it is

not

a c

ompl

ete

reco

rdof

the

disc

ussi

on.

CO

NFI

DE

NTI

AL

SP

O-Z

WL7

58-2

0080

325 1

CO

NTE

NTS

•IT/

ITE

S v

alue

pro

posi

tion

•Cou

ntry

ass

essm

ent

–LR

I des

ign

prin

cipl

es

–In

done

sia

asse

ssm

ent

•Pol

icy

obse

rvat

ions

•Pot

entia

l eco

nom

ic im

pact

•Im

plic

atio

ns fo

r inf

oDev

don

ors

SP

O-Z

WL7

58-2

0080

325 2

*In

clud

es P

hilip

pine

s, C

hina

, Rus

sia,

Eas

tern

Eur

ope,

Irel

and,

Mex

ico;

**

Incl

udes

add

ress

able

mar

kets

in c

urre

ntly

offs

horin

g in

dust

ries

***

Fina

ncia

l yea

rS

ourc

e:M

cKin

sey

Out

sour

cing

& O

ffsho

ring

prac

tice;

McK

inse

y G

loba

l Ins

titut

e; G

artn

er 2

005

data

base

; ID

C; N

AS

SC

OM

Stra

tegi

c R

evie

w 2

007

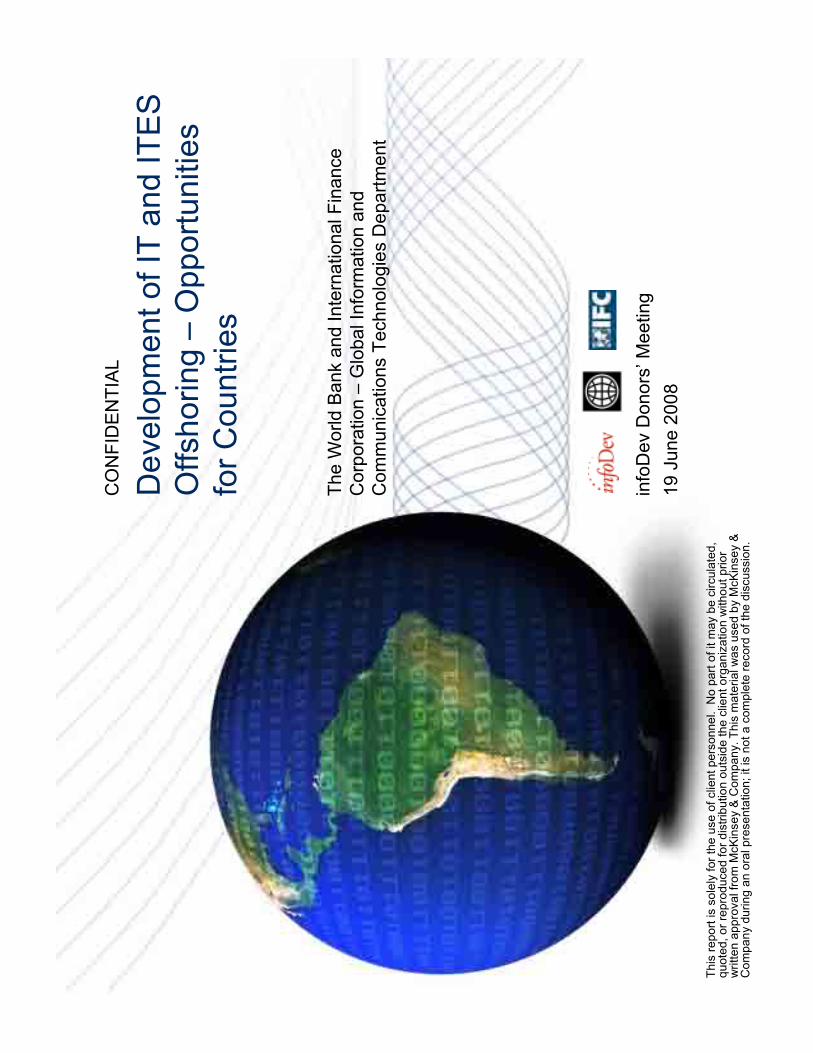

Pote

ntia

l mar

ket f

or o

ffsho

re IT

, BPO

and

R&

D

serv

ices

is a

t lea

st U

S $4

50 b

illio

n

ES

TIM

ATE

S

Oth

ers*

Indi

a

Glo

bal o

ffsho

re IT

exp

orts

, FY

*** 2

007

US

$ bi

llion

18.0

9.0

Cur

rent

si

ze

~190

-220

Add

ress

able

mar

ket

27.08x

Glo

bal B

PO e

xpor

ts**

, FY

2007

US

$ bi

llion 8.2

9.8

Cur

rent

si

ze

~150

18.08x

Add

ress

able

mar

ket

R&

D/e

ngin

eerin

g se

rvic

es

expo

rts,

FY

2007

US

$ bi

llion 4.6

20.0

5.4-

10.4

Cur

rent

si

ze

~115

-135

Add

ress

able

m

arke

t

10-1

5

10x

SIZE

OF

THE

OFF

SHO

RE

IT, B

PO A

ND

R&

D S

ERVI

CES

MA

RK

ET IS

PR

OJE

CTE

D T

O B

E VE

RY

LAR

GE;

CU

RR

ENTL

Y O

NLY

A S

MA

LL

FRA

CTI

ON

HA

S B

EEN

REA

LIZE

D

SP

O-Z

WL7

58-2

0080

325 3

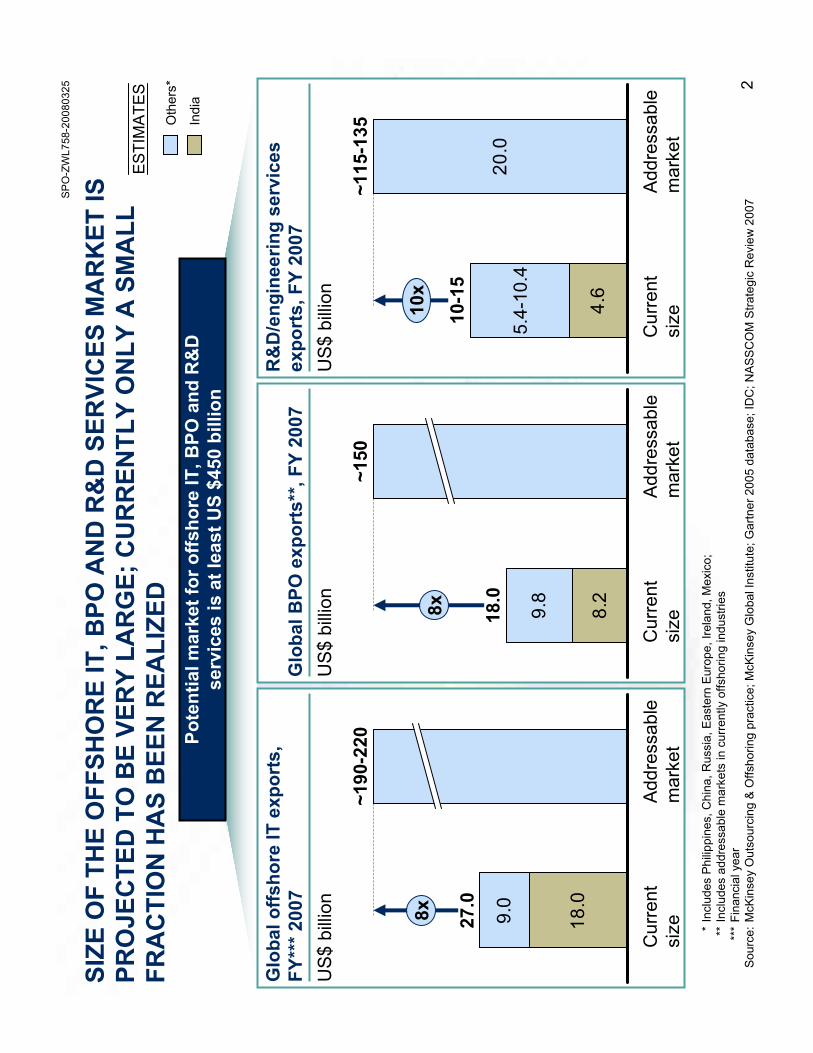

IT S

ECTO

R G

RO

WTH

HA

S H

AD

PO

SITI

VE E

CO

NO

MIC

IMPA

CT

ON

DEV

ELO

PIN

G N

ATI

ON

S (1

/2)

Indi

aPh

ilipp

ines

•Em

ploy

men

t:Th

e P

hilip

pine

s ra

pidl

y gr

owin

g B

PO

sec

tor e

mpl

oyed

thre

e tim

es

as m

any

peop

le in

200

7 as

in 2

004

100

2004

2007

300

Empl

oyee

s ‘0

00

•GD

P:O

ver t

he la

st te

n ye

ars

IT-IT

ES in

In

dia

has

grow

n fro

m a

nas

cent

sec

tor t

o re

pres

entin

g m

ore

than

5%

of t

he n

atio

n’s

GD

P

1.2

2007

1998

5.4

% o

f GD

P

•Exp

orts

: Las

t yea

r Ind

ia’s

IT-IT

ES

sec

tor

cont

ribut

ed o

ver $

30 b

illion

of t

he n

atio

n’s

expo

rts

$ bi

llion

1.8

1998

31.9

2007

•Em

pow

erm

ent o

f wom

en:W

omen

ac

coun

t for

65

perc

ent o

f the

tota

l pr

ofes

sion

al a

nd te

chni

cal w

orke

rs in

the

Philip

pine

s

SP

O-Z

WL7

58-2

0080

325 4

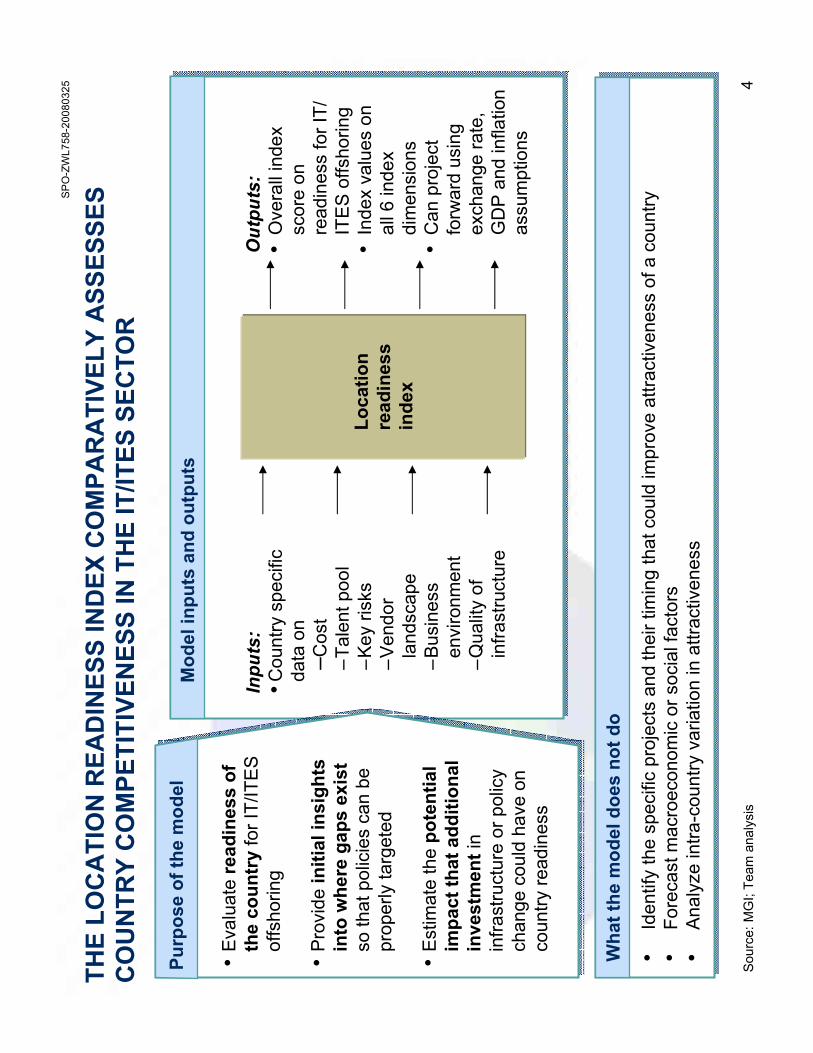

Mod

el in

puts

and

out

puts

THE

LOC

ATI

ON

REA

DIN

ESS

IND

EX C

OM

PAR

ATI

VELY

ASS

ESSE

S C

OU

NTR

Y C

OM

PETI

TIVE

NES

S IN

TH

E IT

/ITES

SEC

TOR

Sour

ce:M

GI;

Team

ana

lysi

s

Loca

tion

read

ines

s in

dex

Wha

t the

mod

el d

oes

not d

o

•Id

entif

y th

e sp

ecifi

c pr

ojec

ts a

nd th

eir t

imin

g th

at c

ould

impr

ove

attra

ctiv

enes

s of

a c

ount

ry•

Fore

cast

mac

roec

onom

ic o

r soc

ial f

acto

rs•

Ana

lyze

intra

-cou

ntry

var

iatio

n in

attr

activ

enes

s

Purp

ose

of th

e m

odel

Inpu

ts:

•Cou

ntry

spe

cific

da

ta o

n –C

ost

–Tal

ent p

ool

–Key

risk

s–V

endo

r la

ndsc

ape

–Bus

ines

s en

viro

nmen

t–Q

ualit

y of

in

frast

ruct

ure

Out

puts

: •

Ove

rall

inde

x sc

ore

on

read

ines

s fo

r IT/

IT

ES

offs

horin

g•

Inde

x va

lues

on

all 6

inde

x di

men

sion

s•

Can

pro

ject

fo

rwar

d us

ing

exch

ange

rate

, G

DP

and

infla

tion

assu

mpt

ions

•Eva

luat

e re

adin

ess

of

the

coun

try

for I

T/IT

ES

of

fsho

ring

•Pro

vide

initi

al in

sigh

ts

into

whe

re g

aps

exis

t so

that

pol

icie

s ca

n be

pr

oper

ly ta

rget

ed

•Est

imat

e th

e po

tent

ial

impa

ct th

at a

dditi

onal

in

vest

men

tin

infra

stru

ctur

e or

pol

icy

chan

ge c

ould

hav

e on

co

untry

read

ines

s

SP

O-Z

WL7

58-2

0080

325 5

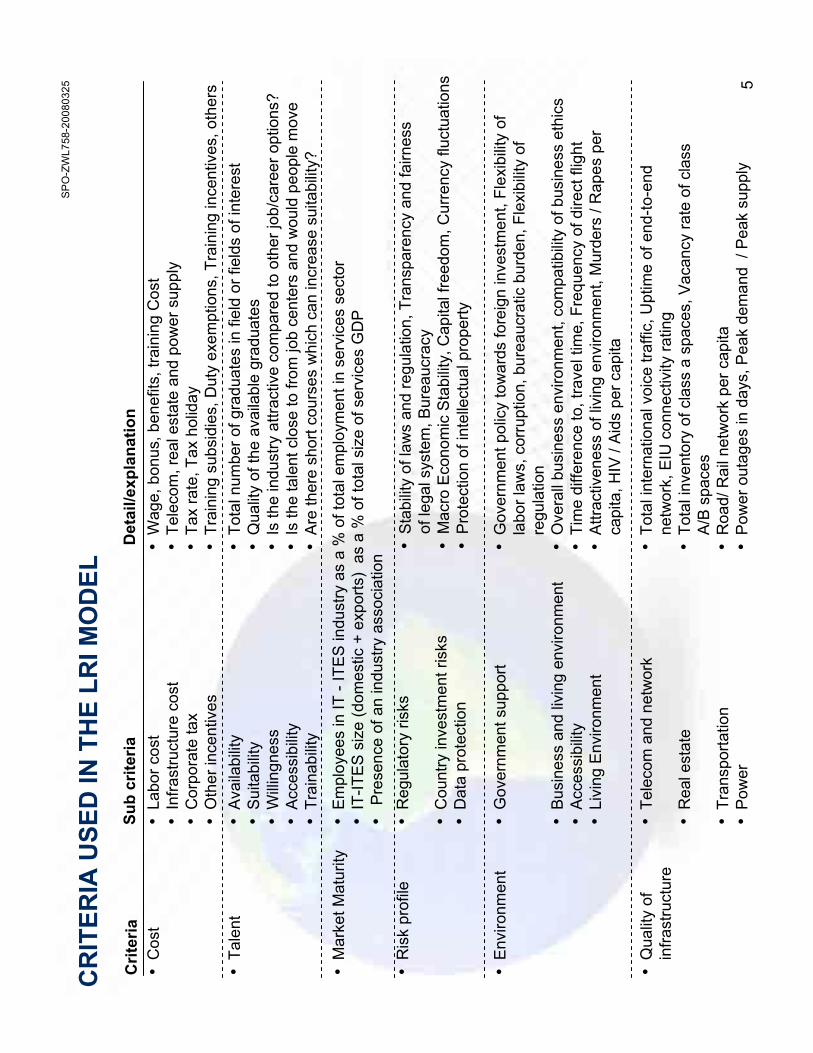

CR

ITER

IA U

SED

IN T

HE

LRI M

OD

ELC

riter

iaSu

b cr

iteria

•M

arke

t Mat

urity

•E

mpl

oyee

s in

IT -

ITE

S in

dust

ry a

s a

% o

f tot

al e

mpl

oym

ent i

n se

rvic

es s

ecto

r •

IT-IT

ES

siz

e (d

omes

tic +

exp

orts

) as

a %

of t

otal

siz

e of

ser

vice

sG

DP

•P

rese

nce

of a

n in

dust

ry a

ssoc

iatio

n•

Ris

k pr

ofile

•R

egul

ator

y ris

ks

•C

ount

ry in

vest

men

t ris

ks•

Dat

a pr

otec

tion

•Ta

lent

•Av

aila

bilit

y•

Suita

bilit

y•

Willi

ngne

ss•

Acc

essi

bilit

y•

Trai

nabi

lity

Det

ail/e

xpla

natio

n•

Cos

t•

Labo

r cos

t•

Infra

stru

ctur

e co

st

•C

orpo

rate

tax

•O

ther

ince

ntiv

es

•W

age,

bon

us, b

enef

its, t

rain

ing

Cos

t•

Tele

com

, rea

l est

ate

and

pow

er s

uppl

y•

Tax

rate

, Tax

hol

iday

•Tr

aini

ng s

ubsi

dies

, Dut

y ex

empt

ions

, Tra

inin

g in

cent

ives

, oth

ers

•E

nviro

nmen

t•

Gov

ernm

ent s

uppo

rt

•Bu

sine

ss a

nd li

ving

env

ironm

ent

•A

cces

sibi

lity

•Li

ving

Env

ironm

ent

•G

over

nmen

t pol

icy

tow

ards

fore

ign

inve

stm

ent,

Flex

ibilit

y of

la

bor l

aws,

cor

rupt

ion,

bur

eauc

ratic

bur

den,

Fle

xibi

lity

of

regu

latio

n•

Ove

rall

busi

ness

env

ironm

ent,

com

patib

ility

of b

usin

ess

ethi

cs•

Tim

e di

ffere

nce

to, t

rave

l tim

e, F

requ

ency

of d

irect

flig

ht

•A

ttrac

tiven

ess

of li

ving

env

ironm

ent,

Mur

ders

/ R

apes

per

ca

pita

, HIV

/ A

ids

per c

apita

•Q

ualit

y of

in

frast

ruct

ure

•Te

leco

m a

nd n

etw

ork

•R

eal e

stat

e

•Tr

ansp

orta

tion

•Po

wer

•To

tal i

nter

natio

nal v

oice

traf

fic, U

ptim

e of

end

-to-e

nd

netw

ork,

EIU

conn

ectiv

ity ra

ting

•To

tal i

nven

tory

of c

lass

a s

pace

s, V

acan

cy ra

te o

f cla

ss

A/B

spa

ces

•R

oad/

Rai

l net

wor

k pe

r cap

ita•

Pow

er o

utag

es in

day

s, P

eak

dem

and

/ P

eak

supp

ly

•S

tabi

lity

of la

ws

and

regu

latio

n, T

rans

pare

ncy

and

fairn

ess

of le

gal s

yste

m, B

urea

ucra

cy

•M

acro

Eco

nom

ic S

tabi

lity,

Cap

ital f

reed

om, C

urre

ncy

fluct

uatio

ns•

Pro

tect

ion

of in

telle

ctua

l pro

perty

•To

tal n

umbe

r of g

radu

ates

in fi

eld

or fi

elds

of i

nter

est

•Q

ualit

y of

the

avai

labl

e gr

adua

tes

•Is

the

indu

stry

attr

activ

e co

mpa

red

to o

ther

job/

care

er o

ptio

ns?

•Is

the

tale

nt c

lose

to fr

om jo

b ce

nter

s an

d w

ould

peo

ple

mov

e•

Are

ther

e sh

ort c

ours

es w

hich

can

incr

ease

sui

tabi

lity?

SP

O-Z

WL7

58-2

0080

325 6

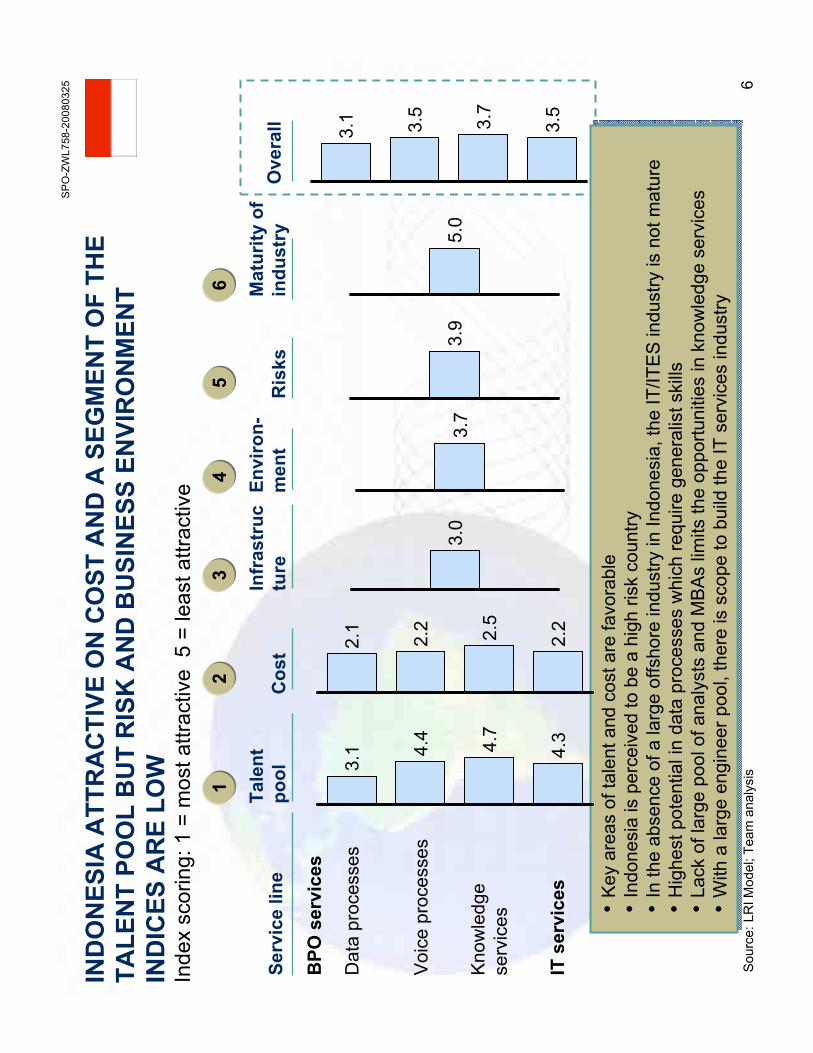

Sour

ce:L

RI M

odel

; Tea

m a

naly

sis

Cos

tTa

lent

pool

Ove

rall

2.1

2.2 2.5

2.2

3.1 4.

4 4.7

4.3

•Key

are

as o

f tal

ent a

nd c

ost a

re fa

vora

ble

•Ind

ones

ia is

per

ceiv

ed to

be

a hi

gh ri

sk c

ount

ry

•In

the

abse

nce

of a

larg

e of

fsho

re in

dust

ry in

Indo

nesi

a, th

e IT

/ITE

S in

dust

ry is

not

mat

ure

•Hig

hest

pot

entia

l in

data

pro

cess

es w

hich

requ

ire g

ener

alis

t ski

lls•L

ack

of la

rge

pool

of a

naly

sts

and

MB

As

limits

the

oppo

rtuni

ties

in k

now

ledg

e se

rvic

es•W

ith a

larg

e en

gine

er p

ool,

ther

e is

sco

pe to

bui

ld th

e IT

ser

vice

s in

dust

ry

BPO

ser

vice

s

Infr

astr

uctu

reEn

viro

n-m

ent

Ris

ksM

atur

ity o

f in

dust

rySe

rvic

e lin

e

3.7

3.9

5.0

3.1 3.5

3.7

3.5

Dat

a pr

oces

ses

Voi

ce p

roce

sses

Kno

wle

dge

serv

ices

IT s

ervi

ces

3.0

13

45

62

Inde

x sc

orin

g: 1

= m

ost a

ttrac

tive

5 =

leas

t attr

activ

e

IND

ON

ESIA

ATT

RA

CTI

VE O

N C

OST

AN

D A

SEG

MEN

T O

F TH

E TA

LEN

T PO

OL

BU

T R

ISK

AN

D B

USI

NES

S EN

VIR

ON

MEN

T IN

DIC

ES A

RE

LOW

SP

O-Z

WL7

58-2

0080

325 7

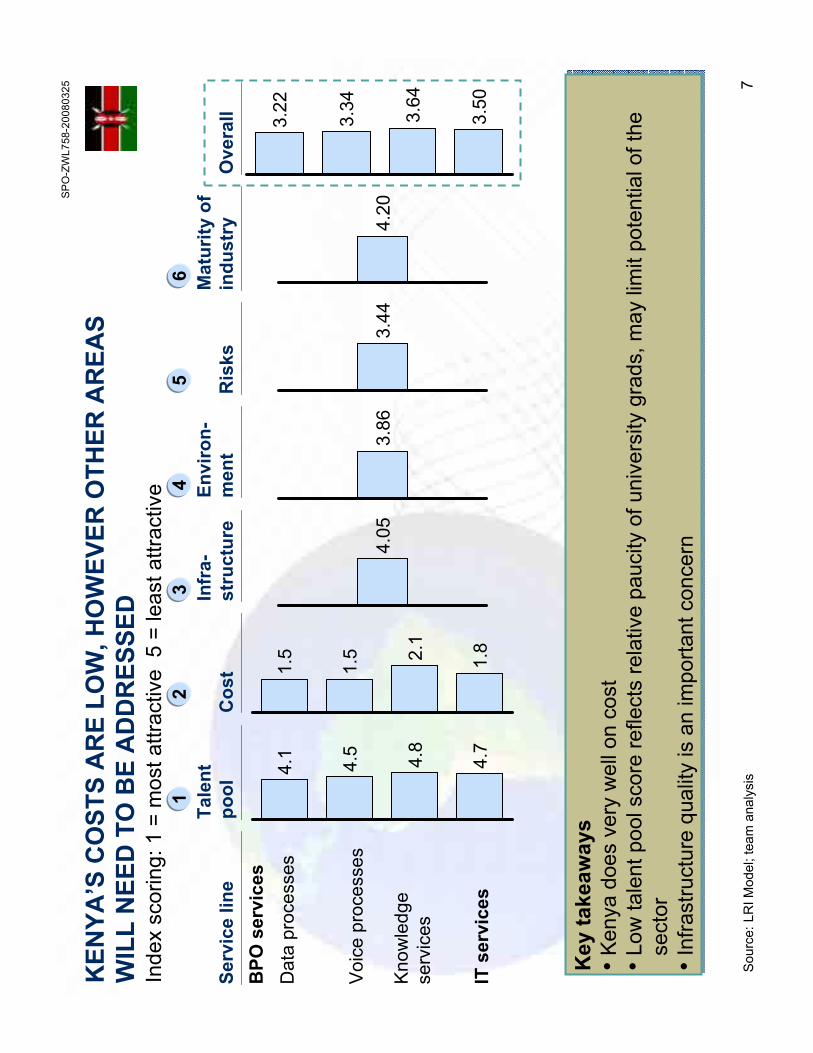

Sour

ce:L

RI M

odel

; tea

m a

naly

sis

Cos

tTa

lent

pool

Ove

rall

1.5

1.5 2.

1

1.8

4.1

4.5 4.8

4.7

BPO

ser

vice

s

Infr

a-st

ruct

ure

Envi

ron-

men

tR

isks

Mat

urity

of

indu

stry

Serv

ice

line

3.86

3.44

4.20

3.22

3.34 3.64

3.50

Dat

a pr

oces

ses

Voi

ce p

roce

sses

Kno

wle

dge

serv

ices

IT s

ervi

ces

4.05

13

45

62

Inde

x sc

orin

g: 1

= m

ost a

ttrac

tive

5 =

leas

t attr

activ

e

KEN

YA’S

CO

STS

AR

E LO

W, H

OW

EVER

OTH

ER A

REA

S W

ILL

NEE

D T

O B

E A

DD

RES

SED

Key

take

away

s•K

enya

doe

s ve

ry w

ell o

n co

st•L

ow ta

lent

poo

l sco

re re

flect

s re

lativ

e pa

ucity

of u

nive

rsity

gra

ds, m

ay li

mit

pote

ntia

l of t

he

sect

or•I

nfra

stru

ctur

e qu

ality

is a

n im

porta

nt c

once

rn

Key

take

away

s•K

enya

doe

s ve

ry w

ell o

n co

st•L

ow ta

lent

poo

l sco

re re

flect

s re

lativ

e pa

ucity

of u

nive

rsity

gra

ds, m

ay li

mit

pote

ntia

l of t

he

sect

or•I

nfra

stru

ctur

e qu

ality

is a

n im

porta

nt c

once

rn

SP

O-Z

WL7

58-2

0080

325 8

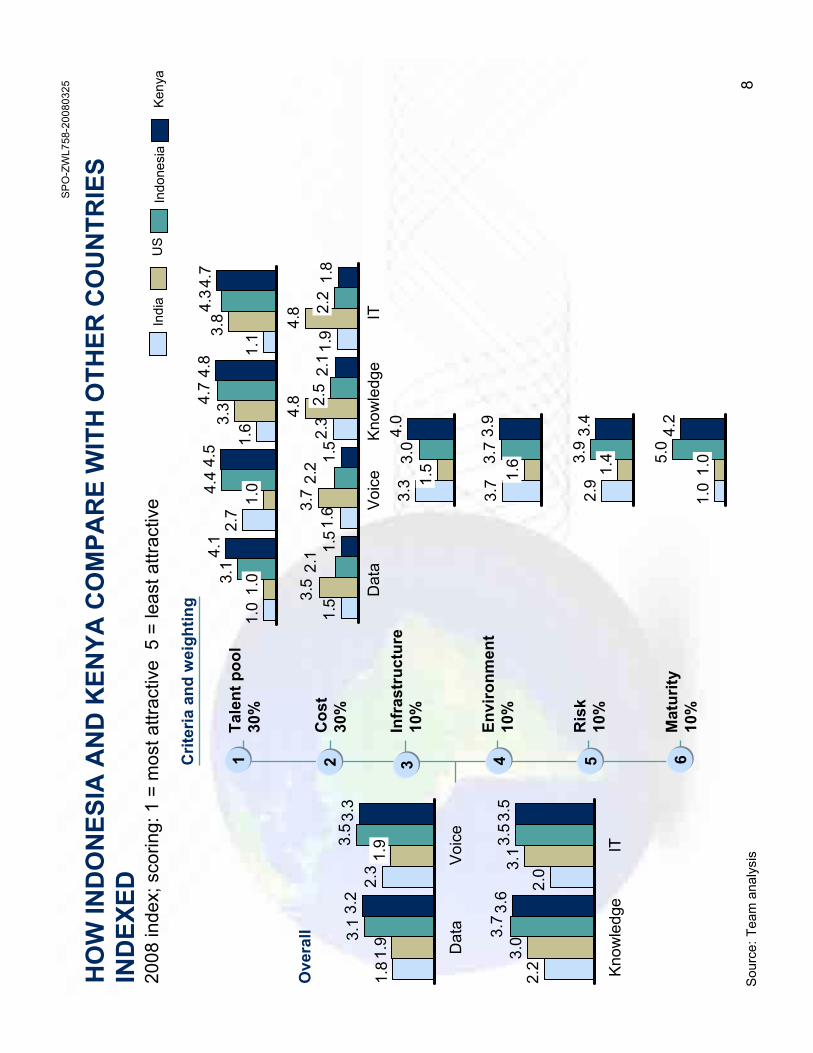

HO

W IN

DO

NES

IA A

ND

KEN

YA C

OM

PAR

E W

ITH

OTH

ER C

OU

NTR

IES

IND

EXED

Sour

ce:T

eam

ana

lysi

s

2008

inde

x; s

corin

g: 1

= m

ost a

ttrac

tive

5 =

leas

t attr

activ

eIn

dia

US

2.2

3.03.

73.

6

Know

ledg

e

2.03.

13.

53.

5

IT

Ove

rall

2.9

1.43.

93.

4

1.0

1.05.

04.

2

3.7 1.

63.7

3.9

1.0

1.03.

14.

12.

71.

04.4

4.5 1.

63.34.

74.

8 1.13.

84.

34.

7

3.3 1.

53.0

4.0

1.9

2.3

1.6

1.5

4.8

4.8

3.7

3.5

2.2

2.1

1.8

2.1

1.5

1.5

2.5

2.2

Cos

t30

%

Tale

nt p

ool

30%

Infr

astr

uctu

re10

%

Envi

ronm

ent

10%

Ris

k10

%

Mat

urity

10%

Crit

eria

and

wei

ghtin

g

1 2 3 4 5 6

Indo

nesi

a Ke

nya

Dat

aVo

ice

Know

ledg

eIT

1.8

1.93.

13.

2

Dat

a

2.3

1.93.

53.

3

Voi

ce

SP

O-Z

WL7

58-2

0080

325 9

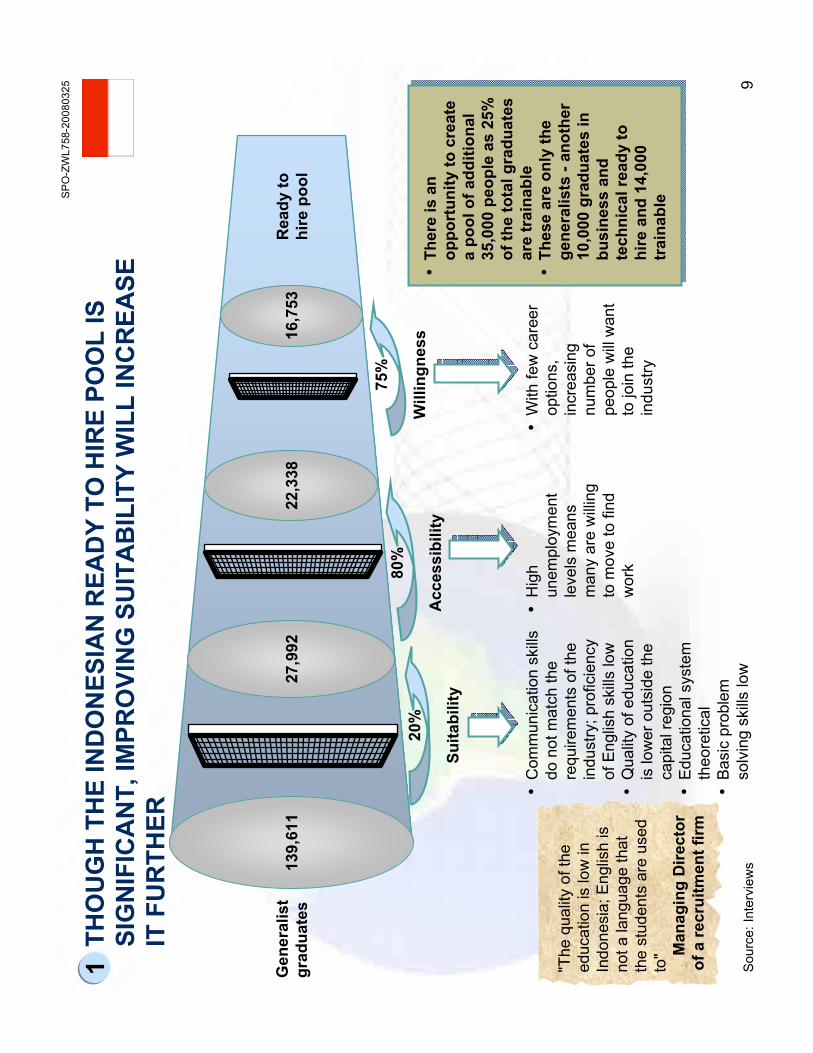

75%

Will

ingn

ess

139,

611

22,3

3816

,753

27,9

92

•H

igh

unem

ploy

men

t le

vels

mea

ns

man

y ar

e w

illing

to

mov

e to

find

w

ork

•C

omm

unic

atio

n sk

ills

do n

ot m

atch

the

requ

irem

ents

of t

he

indu

stry

; pro

ficie

ncy

of E

nglis

h sk

ills lo

w•

Qua

lity

of e

duca

tion

is lo

wer

out

side

the

capi

tal r

egio

n•

Edu

catio

nal s

yste

m

theo

retic

al•

Bas

ic p

robl

em

solv

ing

skills

low

•W

ith fe

w c

aree

r op

tions

, in

crea

sing

nu

mbe

r of

peop

le w

ill w

ant

to jo

in th

e in

dust

ry

THO

UG

H T

HE

IND

ON

ESIA

N R

EAD

Y TO

HIR

E PO

OL

IS

SIG

NIF

ICA

NT,

IMPR

OVI

NG

SU

ITA

BIL

ITY

WIL

L IN

CR

EASE

IT

FU

RTH

ER

20%

Suita

bilit

y

80%

Acc

essi

bilit

y

Rea

dy to

hi

re p

ool

Gen

eral

ist

grad

uate

s

•Th

ere

is a

n op

port

unity

to c

reat

e a

pool

of a

dditi

onal

35

,000

peo

ple

as 2

5%

of th

e to

tal g

radu

ates

ar

e tr

aina

ble

•Th

ese

are

only

the

gene

ralis

ts -

anot

her

10,0

00 g

radu

ates

in

busi

ness

and

te

chni

cal r

eady

to

hire

and

14,

000

trai

nabl

e

"The

qua

lity

of th

e ed

ucat

ion

is lo

w in

In

done

sia;

Eng

lish

is

not a

lang

uage

that

th

e st

uden

ts a

re u

sed

to" M

anag

ing

Dire

ctor

of

a re

crui

tmen

t firm

1 Sour

ce:I

nter

view

s

SP

O-Z

WL7

58-2

0080

325

10

25,4

3313

,734

10,9

8715

,260

•Pe

ople

are

w

illing

to

relo

cate

to p

lace

of

wor

k if

give

n th

e op

portu

nity

•G

ood

Eng

lish

lang

uage

ski

lls•

How

ever

sec

tor

spec

ific

skills

gap

s e.

g. p

robl

em

solv

ing

•IT

indu

stry

is

view

ed a

s a

good

car

eer

optio

n an

d gr

adua

tes

are

willi

ng to

join

th

is in

dust

ry

IN K

ENYA

, A L

AR

GE

PER

CEN

TAG

E O

F G

RA

DU

ATE

S C

OU

LD

BE

HIR

EDB

YD

ATA

SER

VIC

ES

"Peo

ple

are

very

co

mfo

rtabl

e co

mm

unic

atin

g in

E

nglis

h, th

is is

an

adva

ntag

e fo

r K

enya

" M

anag

ing

Dire

ctor

of

a B

PO

85%

Will

ingn

ess

60%

Suita

bilit

y

90%

Acc

essi

bilit

y•

Shor

t tra

inin

g co

urse

s to

Impr

ove

skill

s ca

n yi

eld

an

addi

tiona

l 3,0

00

grad

uate

s a

year

•Th

ese

are

only

the

gene

ralis

ts -

anot

her

5,00

0 gr

adua

tes

in

busi

ness

and

te

chni

cal r

eady

to

hire

and

5,0

00

trai

nabl

e

Gen

eral

ist

grad

uate

sR

eady

to

hire

poo

l

1

Sour

ce:I

nter

view

s; te

am a

naly

sis

DA

TA P

RO

CES

SIN

G E

XAM

PLE

SP

O-Z

WL7

58-2

0080

325

11

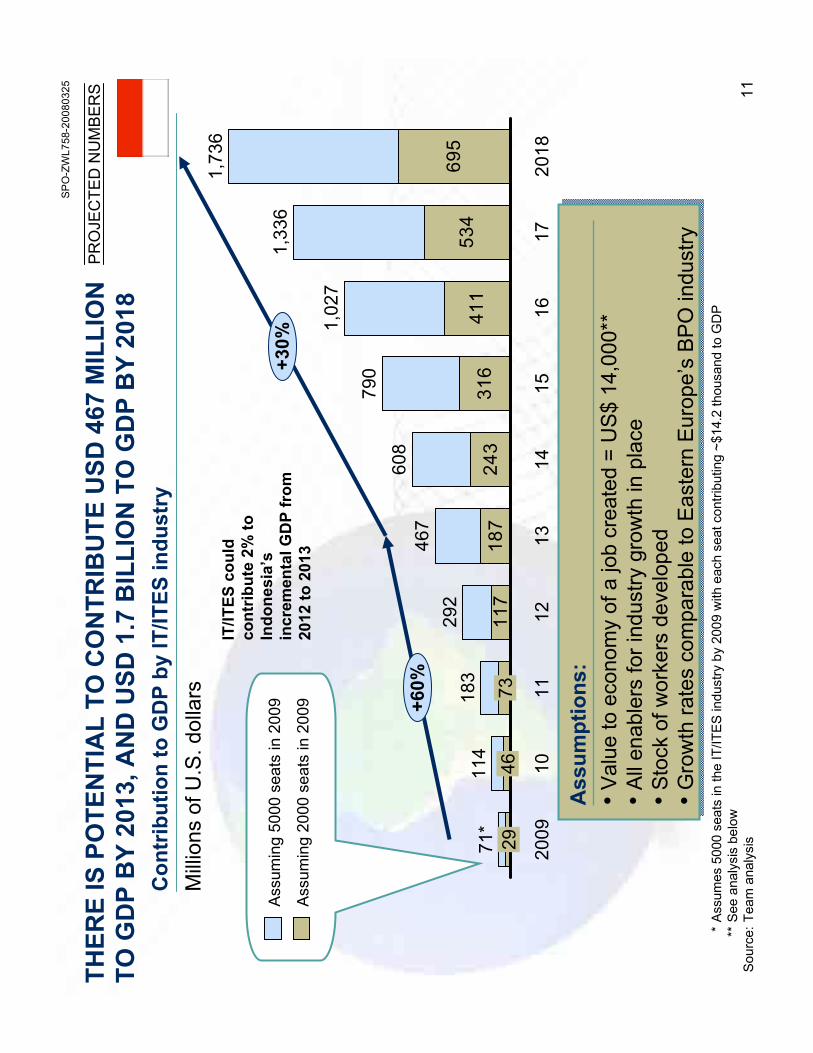

THER

E IS

PO

TEN

TIA

L TO

CO

NTR

IBU

TE U

SD 4

67 M

ILLI

ON

TO

GD

P B

Y 20

13, A

ND

USD

1.7

BIL

LIO

N T

O G

DP

BY

2018

*As

sum

es 5

000

seat

s in

the

IT/IT

ES in

dust

ry b

y 20

09 w

ith e

ach

seat

con

tribu

ting

~$14

.2 th

ousa

nd to

GD

P**

See

anal

ysis

bel

owSo

urce

:Tea

m a

naly

sis

117

187

243

316

411

534

695

1,33

6

17

Assu

min

g 20

00 s

eats

in 2

009 +6

0%

1,73

6

2018

Assu

min

g 50

00 s

eats

in 2

009

+30%

2009

46114

29

10

71*

73183

11

608

292

1312

467

14

1,02

7

790

1615

Con

trib

utio

n to

GD

P by

IT/IT

ES in

dust

ryM

illion

s of

U.S

. dol

lars

•Val

ue to

eco

nom

y of

a jo

b cr

eate

d =

US

$ 14

,000

**•A

ll en

able

rs fo

r ind

ustry

gro

wth

in p

lace

•Sto

ck o

f wor

kers

dev

elop

ed•G

row

th ra

tes

com

para

ble

to E

aste

rn E

urop

e’s

BP

O in

dust

ry

Ass

umpt

ions

:

PR

OJE

CTE

D N

UM

BE

RS

IT/IT

ES c

ould

co

ntrib

ute

2% to

In

done

sia’

s in

crem

enta

l GD

P fr

om

2012

to 2

013

SP

O-Z

WL7

58-2

0080

325

12So

urce

:tea

m a

naly

sis

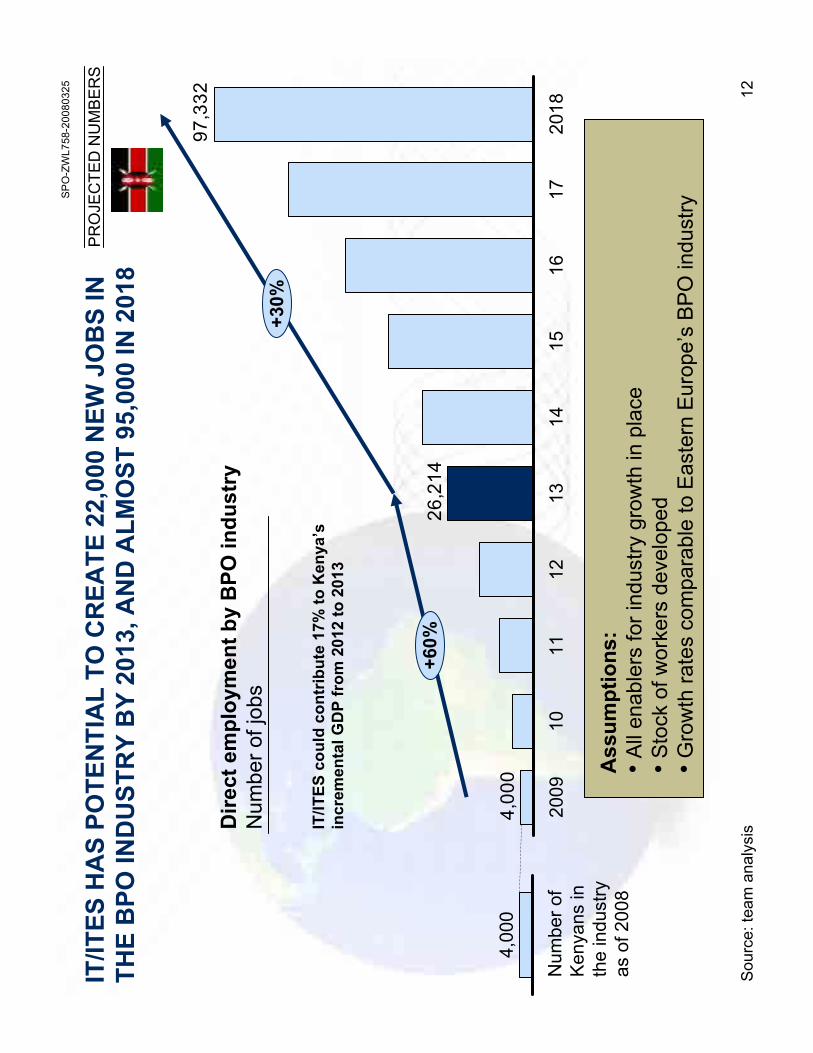

97,3

32

26,2

14

4,00

0

1314

1516

1011

2009

12

+60%

17

+30%

2018

Num

ber o

f K

enya

ns in

th

e in

dust

ry

as o

f 200

8

4,00

0

Dire

ct e

mpl

oym

ent b

y B

PO in

dust

ry

Num

ber o

f job

s

Ass

umpt

ions

:•A

ll en

able

rs fo

r ind

ustry

gro

wth

in p

lace

•Sto

ck o

f wor

kers

dev

elop

ed•G

row

th ra

tes

com

para

ble

to E

aste

rn E

urop

e’s

BP

O in

dust

ry

IT/IT

ES H

AS

POTE

NTI

AL

TO C

REA

TE 2

2,00

0 N

EW J

OB

S IN

TH

E B

PO IN

DU

STR

Y B

Y 20

13, A

ND

ALM

OST

95,

000

IN 2

018

PR

OJE

CTE

D N

UM

BE

RS

IT/IT

ES c

ould

con

trib

ute

17%

to K

enya

’s

incr

emen

tal G

DP

from

201

2 to

201

3

SP

O-Z

WL7

58-2

0080

325

13

KEY

MES

SAG

ES A

ND

NEX

T ST

EPS

FOR

IND

ON

ESIA

• Dev

elop

ing

the

IT/IT

ES

offs

hore

ser

vice

sec

tor i

n In

done

sia

coul

d re

sult

in m

eani

ngfu

lly

fast

er e

cono

mic

gro

wth

•Ind

ones

ia h

as re

ason

ably

goo

d po

tent

ial a

nd th

e ba

rrie

rs to

cap

turin

g th

e op

portu

nity

ar

e no

t stru

ctur

al

•With

in th

e sh

ort t

erm

(1-3

yea

rs) I

ndon

esia

can

incr

ease

its

attra

ctiv

enes

s to

com

pani

es

with

in th

e se

ctor

prim

arily

by

addr

essi

ng it

s in

fras

truc

ture

qua

lity,

bus

ines

s en

viro

nmen

t and

risk

per

cept

ion

•To

rem

ain

com

petit

ive

in th

e m

ediu

m to

long

term

the

coun

try n

eeds

to

–Im

prov

e la

bor s

uita

bilit

y fo

r the

poo

l alre

ady

grad

uate

d–

Impr

ove

qual

ity o

f edu

catio

nif

it w

ants

to b

e a

play

er a

t hig

her e

nd o

f the

IT/IT

ES

mar

ket

•We

reco

mm

end

as n

ext s

teps

that

the

WB

eng

age

with

the

coun

try to

:–

Ref

ine

the

asse

ssm

ent

–D

esig

n th

e ro

adm

ap to

sec

tor g

row

th (p

olic

y an

d in

vest

men

ts)

–S

uppo

rt im

plem

enta

tion

as n

eede

d

Sour

ce:T

eam

ana

lysi

s

SP

O-Z

WL7

58-2

0080

325

14

KEY

MES

SAG

ES A

ND

NEX

T ST

EPS

FOR

KEN

YA

•Dev

elop

ing

the

IT/IT

ES

offs

hore

ser

vice

sec

tor i

n K

enya

cou

ld re

sult

in s

igni

fican

tly

fast

er e

cono

mic

gro

wth

(17%

of i

ncre

men

tal G

DP

yea

r-on-

year

201

2-20

13)

•Ken

ya’s

mai

n ba

rrie

r to

capt

urin

g th

e op

portu

nity

, nam

ely

tale

nt p

ool s

ize,

will

be d

iffic

ult

to o

verc

ome

as it

is s

truc

tura

l

•With

in th

e sh

ort t

erm

(1-3

yea

rs) K

enya

can

incr

ease

its

attra

ctiv

enes

s to

com

pani

es

prim

arily

by

addr

essi

ng in

fras

truc

ture

qua

lity,

bus

ines

s en

viro

nmen

t and

risk

perc

eptio

n

•To

rem

ain

com

petit

ive

in th

e m

ediu

m to

long

term

the

coun

try n

eeds

to fi

nd w

ay to

ad

dres

s ta

lent

poo

l iss

ue–

Incr

ease

tale

nt p

ool e

.g.,

tapp

ing

non-

univ

ersi

ty s

ourc

es–

Con

side

r oth

er s

ecto

r str

uctu

res

e.g.

, bec

omin

g th

e E

ast A

frica

regi

onal

hub

for O

&O

–Fi

nd n

iche

mar

ket

•How

ever

, giv

en th

e hi

gh p

oten

tial i

mpa

ct o

f the

sec

tor t

o ec

onom

ic d

evel

opm

ent i

n K

enya

,we

reco

mm

end

as n

ext s

teps

that

the

WB

eng

age

with

the

coun

try to

:–

Ref

ine

the

asse

ssm

ent t

o id

entif

y ho

w to

add

ress

the

key

stru

ctur

al b

arrie

r

SP

O-Z

WL7

58-2

0080

325

15

HO

W C

AN

INFO

DEV

AN

D D

ON

OR

S EN

GA

GE?

Are

aIs

sue/

desc

riptio

nPo

tent

ial i

nfoD

ev /

dono

r rol

e

Inve

stm

ent d

ecis

ion

mak

ing

•Ass

essi

ng re

adin

ess

•For

mul

atin

g a

stra

tegi

c pl

an•F

undi

ng th

e di

agno

stic

stu

dy•A

naly

tics

•Exp

ertis

e in

pro

ject

man

agem

ent

•Ens

ure

ther

e is

a c

ham

pion

rela

tivel

y in

sula

ted

from

pol

itica

l tre

nds

Edu

catio

n &

trai

ning

•Tra

inin

g co

urse

s•C

urric

ulum

revi

sion

s•I

ncre

ased

pla

ces

at u

nive

rsity

•Tap

oth

er ta

lent

sou

rces

•Bro

ader

edu

catio

nal r

efor

ms

•Par

tner

with

priv

ate

sect

or fo

r con

tent

•Coo

rdin

ate

educ

atio

nal r

efor

ms

•Ext

end

for o

ther

soc

ial e

nds

e.g.

to

disa

dvan

tage

d/un

der-r

epre

sent

ed

•Tra

in tr

aine

rs•O

ther

cap

acity

bui

ldin

g ex

erci

ses

Lega

l & re

gula

tory

refo

rm•R

efor

m re

gula

tion

e.g.

–

IP la

ws

–Te

leco

m d

ereg

ulat

ion

–“D

oing

bus

ines

s”fa

ctor

s–

Land

and

title

refo

rm

•Tec

hnic

al a

dvic

e•A

dvis

e on

gov

erna

nce

issu

es

Infra

stru

ctur

e•P

rovi

de in

dust

ry n

eces

sary

tool

s e.

g.–

Rea

l est

ate

–bu

ild IT

par

ks–

Band

wid

th –

lay

cabl

e–

Tran

spor

tatio

n –

impr

ove

road

s,

build

airp

orts

–Po

wer

•Adv

ice

•Fun

ding