Embed Size (px)

Citation preview

FOOL‟S GOLD

1

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

STRONG SELL – TARGET PRICE: $15.00

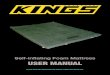

ACTUAL NANJING R&D CENTER PHOTO

NANJING R&D CENTER AS PORTRAYED BY MINDRAY

Photo taken by J Capital on 5/17/13 of Mindray's Nanjing Facility Mindray's Nanjing Facility – photo from 5/07/13 Investor pres – pg 9

By reading this report, you agree that use of OTTOMAN BAY RESEARCH‟s research is at your own risk. In no

event will you hold OTTOMAN BAY RESEARCH‟s or any affiliated party liable for any direct or indirect trading

losses caused by any information in this report. This report is not investment advice or recommendation or

solicitation to buy any securities. OTTOMAN BAY RESEARCH is not registered as an investment advisor in any

jurisdiction.

You agree to do your own research and due diligence before making any investment decision with respect to securities covered

herein. You represent to OTTOMAN BAY RESEARCH that you have sufficient investment sophistication to critically assess

the information, analysis and opinions in this report. You further agree that you will not communicate the contents of this

report to any other person unless that person has agreed to be bound by these same terms of service. You should assume that

as of the publication date of this report, OTTOMAN BAY RESEARCH stands to profit in the event the issuer‘s stock

declines. We may buy, sell, cover or otherwise change the form or substance of its position in the issuer. OTTOMAN BAY

RESEARCH disclaims any obligation to notify the market of any such changes.

Our research and report includes forward-looking statements, estimates, projections, and opinions prepared with respect to,

among other things, certain accounting, legal, and regulatory issues the issuer faces and the potential impact of those issues on

its future business, financial condition and results of operations, as well as more generally, the issuer‘s anticipated operating

performance, access to capital markets, market conditions, assets and liabilities. Such statements, estimates, projections and

opinions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond

OTTOMAN BAY RESEARCH control.

Our research and report expresses our opinions, which we have based upon generally available information, field research,

inferences and deductions through our due diligence and analytical process. OTTOMAN BAY RESEARCH believes all

information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and

reliable. However, such information is presented ―as is,‖ without warranty of any kind, whether express or implied.

OTTOMAN BAY RESEARCH, makes no representation, express or implied, as to the accuracy, timeliness, or completeness

of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to

change without notice, and OTTOMAN BAY RESEARCH is not obligated to update or supplement any reports or any of the

information, analysis and opinion contained in them.

You should assume that OTTOMAN BAY RESEARCH has and/or will file as a whistleblower with the Securities Exchange

Commission.

2

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Ottoman Bay Research – Disclaimer

Table of Contents

3

O T T O M A N B A Y R E S E A R C H

I SHORT INVESTMENT THESIS 4

II UNEXPLAINED DISCREPANCIES 13

III QUESTIONABLE ACQUISITIONS 27

IV PHANTOM CASH 42

V EARNINGS ARE OVERSTATED 49

VI IMPLAUSIBLE SHORT TERM INVESTMENT BALANCES & RETURNS 59

VII DETERIORATING BUSINESS FUNDAMENTALS 64

IX FIELD RESEARCH 88

APPENDIX 96

I Short Investment Thesis

4

O T T O M A N B A Y R E S E A R C H

Short Investment Thesis

Earnings Are Overstated – We believe Mindray is inflating revenues by 30% and real gross margins are in line with peer levels

of 45%-50% vs. the ~60% MR claims. To compound matters, recent SEC correspondences reveal MR has lost money in its ex

China businesses (55% of sales) since 2008, when it acquired Datascope‘s money losing PMD business. MR appears to manage

earnings through a myriad of accounting shenanigans, including moving cash through its complex maze of offshore subsidiaries

to inflate sales, margins and cover expanding losses, significantly overstating the earnings power latent in the business.

Phantom Cash – We do not believe Mindray has the cash it claims. Despite what appears to be a rich balance sheet ($1bn as of

9/30/13), MR is a serial capital raiser and borrows from capital markets any time the company needs to pay out cash, much like a

typical Chinese fraud. A company reporting over $1bn dollars in cash should not have to rely on debt or equity financing to fund

its recurring annual dividend or a $101m acquisition. Evidence further suggests that in 2010, MR would have likely defaulted on

its debt if the company had not misled investors regarding its 2010 equity offering.

Short Term Investment Returns Are Implausible – We question the nature of Mindray‘s speculative, off balance sheet, level 2

ST investments. MR's ex-cash net income has grown at a 5yr CAGR of just 11% vs. a 102% CAGR for short term investments

over the same period. Furthermore, MR generates well-above-average returns on its ST investments and investors cannot audit

these returns due to MR‘s overtly opaque disclosures. More alarmingly, we find little evidence as to how MR accounts for the

income from its ―investments‖, which can be used to inflate earnings. We question the sanctity of the reported cash & short term

investment balances.

A Series of Questionable Acquisitions – We believe Mindray‘s largest acquisition - Datascope - was significantly overstated.

Evidence suggests Datascope was worth far less than the $208.6m in shareholder cash MR paid. To cover up the fraudulent

acquisition, MR significantly stepped up the accounting value of the assets. The following year MR wrote off the entire value of

the acquisition to ZERO, rendering it worthless. Along with another $408m of China long-lived assets which simply vanished

from the company's financials – note MR has yet to take an impairment charge for this write-off. Furthermore, striking similarities

exist with the recent purchase of Zonare Medical (acquired 7/2013), which was recently accused of ―intentional fraud‖ by HDX,

a significant manufacturer and distributor (filed 11/1/2013)

Dubious Accounting Reporting – We find large discrepancies and outright deception in MR's filings that we cannot reconcile.

We believe Mindray Medical will restate several years of filings as a result of the issues covered.

SEC Action – We have submitted our documents to the SEC for further review. We believe Mindray Medical's Board has the

fiduciary responsibility to form a special ―independent‖ committee to examine the discrepancies covered in this report. 5

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

…And The Corporate Governance + Regulatory Overhangs?

Multiple regulatory overhangs

SEC has had 6 correspondences with MR since FY12

FDA product investigations which have led to product recalls in the U.S. (2nd largest geography), as well as a scathing letter from

the FDA in November 2012 that illuminates numerous concerning issues with the U.S. manufacturing facility

Masimo (MR supplier) is suing MR for patent infringement (multiple patents)

HDX Corp.(Zonare distributor) is suing Zonare Medical for ―intentional fraud‖ (filed 11/1/2013)

PRC government has recently begun investigating pricing practices in the medical devices industry (they had previously focused

on pharmaceuticals which led to significant fines)

SEC is suing 5 of the largest accounting firms in PRC, including PWC, MR‘s auditor

Abundant corporate governance issues

Co-CEO and co-founder, Xu Hang abruptly resigned in 4q12. The Company‘s official statement qualifies the move saying it was

done for the ―strengthening in corporate governance‖

Mindray has had 4 CFOs in 4 years ( Joyce Hsu, Ronald Ede, Jie Liu & Alex Lung)

David Gibson, former President of NA and a legacy employee of Datascope (acquired in 2008), abruptly resigned at the end of

2012, along with the majority of his senior team

MR fired auditor Deloitte in October 2008 without cause (same yr as questionable Datascope acquisition) and brought in PWC

In September, just a month earlier, MR added recently-retired and long-time PWC partner to its Board, including a position

on the auditing committee. This is highly troubling and creates potential for abuse (see page 24 for further detail)

PCAOB has been unable to review Mindray‘s auditor‘s work, investors should question the sanctity of MR's financial statements

Shortly before and after raising FY13 guidance in 2q13, insiders sold more shares in 5 months than in 1h13, 2012, 2011, 2010,

and 2008 COMBINED (see slide 8) before substantially cutting FY13 revenue guidance in its 3q13 release (from 18% to 13%)

3 insiders control greater than 60% of voting shares as class A shares only possess one vote vs. five for B shares

MR has a poison pill and staggered board with 3-year terms (pages 21 and 22 of 2012 20-F, respectively)

6

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

But Wait – There‟s More…

What does a rich FY14E consensus PE multiple of ~20x (vs. comps ~14x) valuation get you?

MR is an expensive OEM-turned med-tech manufacturer that effectively copies competitor products and makes low quality goods in

commoditized, replacement markets. We believe MR faces execution risk in attempting multiple initiatives simultaneously, has

questionable balance sheet issues, and faces significant LT headwinds. Furthermore, investors receive a call option on fraud

Mindray‟s core value category is a hypercompetitive one with significant pricing and competitive pressures

Pricing competition has increased from smaller players (Edan (PMD + Ultrasound), Biolight (PMD), KHB (IVD)) reaching

scale & moving upstream, and MNCs (GE, Siemens, Philips, Fujifilm, Samsung et al) shifting downstream to target Tier I+II

hospitals. Our hospital checks suggest the battle between incumbents for China growth will be fought on price

Slowing secular growth story in Chinese healthcare

In January 2012, the Ministry of Science and Technology announced intent to create 10 R&D centers and 10-15 large medical

device companies, creating further competition across hospitals tiers in China. The govt‘s focus is to make affordable

healthcare for its citizens, NOT to enrich local manufacturers

The Chinese government has pushed for overcapacity in certain strategic industries in the past (solar, for example) to

drive down prices and enable widespread affordability

Broken growth story in developed markets (55% of sales)

Mature, replacement markets, controlled by group purchasing orgs. (―GPOs‖) with limited growth and margin opportunities

Evidence of channel stuffing & long-term negative trends in CCC

Opaque/chaotic distribution network with numerous levels results in lower gross margins than direct sales

Newly added ―capital investors‖ in China are creating an extra layer in the distribution network, cutting into margins

Poor expense management - SG&A continues to outpace sales growth and has done so for the last 5 years

Mindray has consistently lost market share since 2009 as cited by the company's OWN investor presentations

A brand slowly losing its identity with end-users as it attempts to stretch across hospital tiers for growth

A top-line story that hasn‟t translated into any FCF generation 7

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

MR SHARE PRICE FOLLOWING INSIDER SALES IN 2009

Dubious Insider Selling

8

Shortly before and after raising guidance in 2q13, insiders sold more shares in 5 months than in 1h13, 2012, 2011, 2010, and 2008

COMBINED before substantially cutting 3q13 revenue guidance by 5% (from 18% to 13%)

Note: this activity comes on the heels of MR closing its questionable Zonare acquisition. We remain skeptical of the Zonare

purchase and MR‘s overall growth and management‘s share sales imply that they agree with our sentiment…

Note: investors saw similar insider sales in 2009. The following year, Mindray's stock plunged -25%

Mindray

-25%

MINDRAY – INSIDER SHARE SALES (THOUSANDS OF SHARES SOLD)

477.3

4,271.3

290.0 305.2 3.0

1,892.5

2008 2009 2010 2011 2012 May '13 - Oct '13

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

What's it Worth – Valuing Mindray Medical

We believe fair value for Mindray Medical is $15 and investors get the call option on fraud

Assuming Mindray has margins more inline with its med-tech peer group alone suggests a ~60% haircut to current prices

We believe real earnings (adjusted for fraud) for FY14 will be $1.10. Assigning a peer-aligned 14x multiple gives us a price of $15.40, or 61.5% downside from current levels

9

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Capital Structure

Current Price ($) $ 40.00

Shares Outstanding (mn) 121

Equity Market Cap ($mn) $ 4,829

Net Cash ($mn) (end of current FY) $ (711)

Minority Interest ($mn) $ (1.2)

Enterprise Value ($mn) $ 4,116

We believe it should be managements goal to be transparent about its core operations with investors

We believe management should disclose sales, gross margins, & operating income by segment (PMD, IVD, MIS, Other) and by major

countries & regions over the last 5 years, as many of the company's peers do. Our core belief is that Mindray's margins from its core

operations are far slimmer than is widely appreciated

We ask management to detail the asset composition of its short-term investments, and exactly where these liquid investments with

maturities less than 1 year are /were being allocated to generate such impressive returns over the last 5 years (interest income

consistently above 5% on ―bank deposits‖). We ask management to disclose where the company accounted for the ―income‖ produced

We ask management to reveal the addresses of ALL of the company's Manufacturing and ―R&D‖ facilities as any public company

would willingly do – compelling evidence suggests at least one does not exist, we question whether all 18 of Mindray's manufacturing

and R&D facilities exist

We ask management to disclose the financial statements of its shell company ―Mindray Medical International‖ as well as the

undistributed earnings held by all subsidiaries and affiliates, as was done for the years 2008 and 2009. We believe this will support our

view that Mindray holds significant liabilities off balance sheet and that there has been cash leakage

We ask management to disclose recent figures for distributor sales vs. direct sales as was done from the periods ‗09 –‘11 in MR's July

27, 2012 correspondence with the SEC. We believe this disclosure will support our view that nearly all of MR's sales growth has come

from channel stuffing distributors

We challenge management to disclose the contributions of each of the 9 acquisitions the company has done since 2011 (p.10). We

believe it is important to provide transparency on how shareholder cash is being spent, how returns have been, and allow investors to

evaluate organic growth. This is a very reasonable request as many U.S. companies provide this information without investor demand

We ask management to disclose the organizational structure of the company over the last 5 years in a manner which is legible. Investors

should be concerned that the last legible structure was produced in 2007. Recent org. charts are intentionally blurred & difficult to

construe

10

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

1

2

3

4

5

6

7

7 Disclosures Investors Deserve To Know

Why The Opportunity Exists – Hope, Hype & Reality

The big picture – justified optimism?

Long held perception that MR is a marquee brand name in Chinese medtech and one of the best pure plays on the

secular growth story in Chinese healthcare

Consensus believes MR will be the logical beneficiary of perceived growing secular trends in China

With a continued focus on improving its citizens‘ access to healthcare, the Chinese government is investing in

improving its hospitals, especially in MR‘s core category (plans to upgrade 9,600+ county-level hospitals in

China to Class 2+ hospitals in 2012-15)

Belief that MR has a substantial cost advantage vs. both domestic and international peers that allows the company to

maintain near-impermeable ~60% GMs despite underpricing competitors by 30-40% (company claims 10-30% under

pricing) and utilizing distributors who further cut into margins vs. MNCs who have a higher mix of direct sales teams

Longs have held on to the China growth story despite blatant signs of an increasingly competitive & fragmented China

med-tech environment, slowing government tenders, MR's decelerating China sales growth and margin compression

Rose colored glasses – DD top line growth overshadows MR's highly capital intensive / low FCF business model

Assumption that MR will continue to sustain reverse economies of scale

Consensus assumes roughly flat-line peak margin profile into foreseeable future

Inherent complexity of MR's story/business model is high

Opaque distributor channels

Assets across geographies + industries

Lack of open and honest management communication

Belief that MR can simultaneously penetrate high & lower tier markets with little to no impact on GMs

Consensus believes Zonare acquisition offers MR a runway to take advantage of secular shifts towards color &

portable ultrasounds, as well as help turn around US sales growth rates

Management defections, 4 CFOS in 4 years, Masimo IP lawsuit, Zonare distributor lawsuit, and FDA issues not a major

concern 11

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Mindray Today

Mindray Medial (“MR”) is China‟s largest developer, manufacturer and exporter of medical devices to hospitals,

health clinics & government health bureaus. MR is known as a “value” brand within the medical devices category.

Mindray is the largest medical device exporter in China with ~55% of revenue generated outside of China

MR's business today can be broken into 4 segments:

Patient Monitoring & Life Sciences: Patient Monitoring (FY12 - 42% of sales)- mature replacement business -

used to track heart rate, blood pressure, respiration, temperature

Life Sciences: products include anesthesia devices, defibrillators, surgical beds, surgical lights, ventilators, syringes,

and infusion pumps

In-Vitro Diagnostics: (27% of sales) – instruments & reagents for the analysis of blood, urine & bodily fluid

samples

Reagents: offers 150+ reagents for use on diagnostic instruments. Reagents account for the vast majority of MR‘s

high margin recurring consumable revenues, in direct contrast the vast majority of the rest of MR‘s business,

which includes one-time sales of hardware loaded with largely undifferentiated software

Medical Imaging Systems: (24% of sales) ultrasound & digital radiography systems (replace X-rays). Acquired

Zonare Medical in FY13, a California maker of high-end ultrasounds

Other (Non-Core): (7% of sales) - endoscopy, orthopedic products and healthcare IT solutions. Also includes

warranty, shipping, and other non-product related revenue

~88% of MR‘s sales come from capital equipment and 12% from consumables and services. An OEM without

meaningful high margin recurring service revenues, minimal IP, and high price competition is not deserving of a 20x

multiple, nor

78% of total sales and >80% of Chinese sales go through opaque distribution channels as of 2011 (data revealed through

7/27/12 SEC correspondence)

China is the largest market (43% of sales), followed by North America (16%), Latin America (11%), Europe (10%), Other

Asia (5%), and the remainder in other developed and developing nations

12

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

II Unexplained Discrepancies

13

O T T O M A N B A Y R E S E A R C H

Investors Should Review Mindray's Filings With a High Level of Skepticism

We find numerous discrepancies in Mindray's reported filings and public documents which suggest that the company has

intentionally attempted to deceive investors

Phantom facilities

We find evidence which suggests Mindray has spent millions of dollars on capex, yet at least two ―facilities‖ were actually a

substantial overpayment for empty fields of grass. See next two slide for greater detail

$656m in assets simply vanished

Post Mindray's acquisition of Datascope, $656m in long lived assets simply vanished from Mindray's financial statements. If

Mindray wrote off the assets, the company hid this impairment charge from investors as we find no record of it. As we will

cover in this report we believe this impairment was related to MR's dubious acquisition of Datascope

Registrant vs. consolidated filings do NOT reconcile

For 2008 & 2009 ONLY, Mindray released the filings of its shell company ―Mindray Medical International‖ before it was

hidden beginning in 2010. The public documents reveal a cash & investments discrepancy of 111% in FY09. the last known

year. Investors should fear whether MR carries a significant amount of cash or liabilities off BS or if the cash even exists

MR explicitly lied to the SEC regarding its return policy

In FY12, the SEC inquired into Mindray's return policy and Mindray responded that the company did not accept returns.

However, company issued product manuals and our call with the Company‘s customer service department suggest otherwise.

This suggests a blatant lie to the SEC

What SEC correspondence?

To compound matters, MR hides its SEC correspondences from investors. Under the ―SEC filings‖ section of the investor

relations website, Mindray knowingly eliminates any and all traces of correspondences with the SEC. The only place to find

these correspondences is on SEC.gov

PCAOB has been unable to review Mindray's auditors‟ work

In a 6/13/2013 SEC correspondence, it was brought to investor attention that the company's auditor‘s work had not been

reviewed by The Public Company Accounting Oversight Board or (―PCAOB‖) and MR had not disclosed this risk factor for

nearly 5 years. The PCAOB is responsible for validating the work of auditors to prevent fraudulent behavior 14

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

ACTUAL NANJING R&D CENTER PHOTO

NANJING R&D CENTER AS PORTRAYED BY MINDRAY

Perception vs. Reality – This is Mindray Medical

15

Photo taken by J Cap Research on 5/17/13 of Mindray's Nanjing Facility Mindray's Nanjing Facility – photo from 5/07/13 Investor pres – pg 9

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Management should reveal the addresses of ALL of the company's 18 Manufacturing & R&D centers, as its peers willingly

do - evidence suggests that at least two do not exist

In 2006 MR stated, ―Pursuant to an agreement with the Government of the Nanjing Jiangning Development Zone, we intend to

invest up to $150 million over three and one- half years to build a research and development and manufacturing facility in

Nanjing…that is expected to be operational in 2009‖

Subsequently, in 2010, Mindray booked ~$21m in shareholder cash to upgrade the Nanjing facility. Allegedly adding 158K of

GFA for what appears to be 2 parcels and patches of grass.

Mindray has spent hundreds of millions of dollars on R&D and Capex. We would like to see where the cash has gone, as the

Nanjing and Zhongguancun examples raise serious concerns

Further Shareholder Millions Wasted on Grass

16

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

PHOTO OF MINDRAY‟S ZHONGGUANGGCUN LOCATION

Photo taken on 4/15/13 by J Cap Research

2008 Long-Lived Assets Long Lived Assets

2008 - ('08 20F) 2008 - ('09 20F) Delta 2009 2010 2011 2012

PRC 503.1 95.14 -408.0 143.5 219.5 259.7 289.0

United States 238.0 29.8 -208.2 30.6 29.2 28.3 28.5

Other countries 44.1 4.2 -39.8 5.4 5.1 5.2 7.4

Total LL Assets 785.2 129.1 -656.0 179.5 253.7 293.2 324.9

% of Total Assets 100% 16% 19% 22% 20% 17%

Total Assets Reported 785.8 785.8 966.3 1,150.6 1,459.0 1,857.0

It appears that $656m in assets simply disappeared from MR's financials in 2009 without explanation

MR's 2008 vs. 2009 filing reveals MR's 2008 long-lived assets were significantly revised/impaired downward (-$656m or ~80%) – a

majority of the assets being in China

If Mindray wrote off the assets, the company hid this impairment charge from investors as we find no record of it. We

believe management will be forced to take this impairment charge in the future

MINDRAY 2009 20F (PG F-32)

MINDRAY 2008 20F (PG F-31)

?

$656m in Long Lived Assets Simply Vanished

17

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

?

In MR's 2008 and 2009 20-Fs ONLY, Mindray revealed the financial statements of its registrant “Mindray Medical

International” or its shell company (vs. consolidated) providing real insight into MR's financial position

Some perplexing items:

In MR's last registrant filing (2009) the filing indicated a cash & investment discrepancy of nearly 74%/$274m (Consolidated at

$372.5m vs. Registrant at $647.2m), suggesting that MR's financial statements are not fully consolidated. Does this suggest

dubious off balance sheet activity?

MR's YoY increase in loans and investments to subsidiaries from FY07 to FY08 is in line with MR's reported retained earnings

for the period ($183.1m vs. $183.8m)

MR somehow continued with uninterrupted growth in cash in 2008 (consolidated & registrant) despite MR having to pay

Datascope $211m. Furthermore, they spent $70m on capex and paid out $20m in dividends

We worry that MR has deceptively used intercompany transactions to inflate sales & margins, and understate liabilities as we find

irregularities that are nearly impossible to reconcile

Mindray has intentionally discontinued this disclosure in subsequent filings (post 2009)

Alarming Discrepancies in MR's Registrant vs. Consolidated Filings

18

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

2008 Exhibits: 2008 20F – PG. F32, F33

2009 Exhibits: 2009 20F – PG. F35, F36

Note: MR's

inter-company

loans/investments

make up 74% of MR's

reported assets. We

question whether

MR accounts for

loans to subsidiaries

as ST investments.

Discrepancies in Assets

2007 2008 2009

MR Consolidated Cash

Cash & Cash Equiv. 189.0 96.4 204.2

ST Investments 55.9 36.8 91.6

R. Cash - 119.7 76.7

Total Reported Consolidated Cash 244.9 252.9 372.5

MR Registrant Cash

Cash & Cash Equiv. 88.4 15.4 12.0

Short Term Investments 0.0 0.0 0.0

Loans to subsidiaries/affiliates 96.0 173.4 237.9

Investment in subsidiaries 170.4 276.2 397.3

Total Cash in Subsidiaries 354.8 464.9 647.2

Delta vs Registrant (109.86) (212.08) (274.73)

% of Cash + Investments Unaccounted For In Subs 45% 84% 74%

Discrepancies in Assets

Total Registrant Assets 357.8 465.7 647.8

Total Consolidated Assets 446.7 785.8 966.3

Delta 88.9 320.0 318.4

% of Assets Unaccounted For In Subs 25% 69% 49%

If Mindray Can Lie To The SEC…

19

In an SEC correspondence dated 7/27/2012, the SEC inquired into Mindray's aging accounts receivable balances and unusually low

allowance for doubtful accounts given the company's increasing A/R balances and sales. Mindray noted that the company did not

accept returns and believed their current estimations were sufficient

Note: increasing doubtful accounts to more reasonable & conservative levels impacts earnings due to increased bad debt expense

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

JULY 27, 2012 CORRESPONDENCE TO SEC

MINDRAY REVENUE RECOGNITION POLICY – 2012 20F

Why Not Investors?

20

While Mindray claims to not accept returns from customers, the company's owners product manuals suggest otherwise

We found the ambiguous nature of the language particularly interesting, so we called customer service ourselves claiming to want

to buy an ultrasound device, but were concerned that we wouldn‘t be able to return it if the doctors weren‘t satisfied. The customer

service representative assured us that we could return the product as long as we were able to get management authorization, which

we could reasonably expect to receive. This is in direct contrast to management‟s claim to the SEC that they do NOT

accept returns

MINDRAY'S PRODUCT MANUAL

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Mindray's organizational structure is a complex matrix with many layers which are difficult to trace. Like a typical Chinese fraud,

we believe this structure can enable a fraudster to perpetrate and conceal misdeeds

As noted on earlier slides, we find large discrepancies in MR's consolidated assets vs. its registrant data (“Mindray

Medical International”), suggesting assets/liabilities could be held off balance sheet

Lack of transparency – Mindray intentionally blurs the details of its organizational structure and has done so for

the last 5 years

MINDRAY MEDICAL‟S ORG. STRUCTURE – 2012

21

MINDRAY MEDICAL‟S ORG. STRUCTURE - 2008

Complex Organizational Matrix

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

22

Increasingly Complex Org. Structure = Less Disclosure?

O T T O M A N B A Y R E S E A R C H

2008 ORG. STRUCTURE DETAILS

D E C - 2 0 1 3

2012 ORG. STRUCTURE DETAILS

SEC.GOV

MINDRAY MEDICAL'S WEBSITE

Perception vs. Reality – There Are 2 Sides to Every Story

23

The SEC has sent MR numerous inquiries since 6/2012 about irregularities in MR's filings. Interestingly, under “SEC

Filings” on MR‟s website, these correspondences are nowhere to be found. One must go SEC.GOV to find them

Note: Red bubbles designate correspondence between SEC & MR

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

In October of 2008, MR fired its auditor Deloitte and hired PWC. This is alarming for several reasons:

Auditor change means that PCAOB can no longer review auditor work – Deloitte was PCAOB compliant (meaning the

PCAOB could review the auditor‘s work) while their new auditor PWC was and is not

MR failed to disclose the PCAOB non-compliance to investors for nearly 5 years, until a recent SEC correspondence

mandated that MR include this information as a risk factor in the FY2013 20-F

Blow to corporate governance and auditing checks & balances – MR placed Mr. Peter Wan—an ex-PWC partner—on its

Board and audit committee just one month prior to firing Deloitte and hiring PWC, creating a relationship ripe for potential abuse

Relationships play an especially large role in Chinese business dealings. It is entirely possible that the PWC auditors and Mr.

Wan have prior long-standing relationships and that these can be used to influence the auditors‘ behavior. We are not

suggesting that Mr. Wan has used his hypothetical influence, as we have no definitive proof. However, we believe this is

material information that investors should be aware of.

The subsequent 2008 20-F contained concerning discrepancies – detailed further throughout the deck

MR substantially reduced its transparency after the 2008 filing and engaged in numerous questionable practices post

auditor transition

In September of 2008, MR added Peter Wan, a former PWC partner to its Board

Mr. Wan had retired from PWC just three months prior in June 2008 after spending 33 years total—including 16 as a partner—at

PWC and its HK predecessor firm

In October of 2008, just one month after Mr. Wan‘s hiring, MR‘s long-standing auditor Deloitte was fired and PWC was hired in their

place

Why did MR fire its auditor so late into the fiscal year ? Note that MR‘s fiscal year runs in line with the calendar year,

meaning a December year end. They never provided a good explanation for this change to investors

MR‟s 2008 20-F (which PWC signed off on) had numerous discrepancies

A Troubling Conflict of Interest

24

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

PCAOB Has Been Unable To Review Mindray's Filings

25

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

MR kept this information from investors for nearly 5 years. The SEC only recently brought it to public attention

SEC Correspondence dated 6/13/2013

As a publicly listed company with the SEC, MR's auditor is required by law to undergo regular Public Company Accounting

Oversight Board (PCAOB) inspections to assess its compliance with U.S. law and professional standards in connection with

its audits of financial statements filed with the SEC. However the PCAOB has been unable to audit Mindray's auditor work.

Mindray's ―Risk‖ section in FY13 will note:

―Our independent registered public accounting firm‘s audit documentation related to their audit report included in this

annual report may be located in the Peoples‘ Republic of China. The Public Company Accounting Oversight Board

currently cannot inspect audit documentation located in China and, as such, you may be deprived of the

benefits of such inspection

Auditors of companies that are registered with the United States Securities and Exchange Commission and traded

publicly in the United States, including our independent registered public accounting firm, must be registered with the

U.S. Public Company Accounting Oversight Board (United States) (―the ―PCAOB‖) and are required by the laws of the

United States to undergo regular inspections by the PCAOB to assess their compliance with the laws of the United

States and professional standards. Because we have substantial operations within the Peoples‘ Republic of China and the

PCAOB is currently unable to conduct inspections of the work of our auditors as it relates to those operations without

the approval of the Chinese authorities, our auditor‘s work related to our operations in China is not currently inspected

by the PCAOB.

This lack of PCAOB inspections of audit work performed in China prevents the PCAOB from regularly evaluating audit

work of any auditors that was performed in China including that performed by our auditors. As a result, investors may

be deprived of the full benefits of PCAOB inspections.

The inability of the PCAOB to conduct inspections of audit work performed in China makes it more difficult

to evaluate the effectiveness of our auditor‟s audit procedures as compared to auditors in other jurisdictions

that are subject to PCAOB inspections on all of their work.‖

Why Does This Matter?

26

On 12/3/2012, the SEC began investigating alleged accounting fraud in China. Notably the SEC charged the

Chinese affiliates of five major accounting firms for refusing to produce audit work

Note: Mindray's auditor Pricewaterhouse Coopers is among the five firms being sued by the SEC

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

III Questionable Acquisitions

27

O T T O M A N B A Y R E S E A R C H

Mindray Makes Dubious Acquisitions

28

MR has a record of committing fairly egregious fraud in the past. We question the rapid 9 acquisitions MR has made since

2011. Like outed frauds Olympus & CMED, we believe MR must continuously make dubious acquisitions to prop up its

deteriorating business

Datascope Acquisition

Mindray‘s largest acquisition Datascope was significantly overstated. Evidence suggests Datascope was worth far less than the

$209m in shareholder cash and bank borrowings MR paid

Aggressive asset mark ups

To justify its fraudulent acquisition, evidence shows Mindray significantly stepped up the value of the assets it acquired to

justify the $209m acquisition price

$656m in long-lived assets simply vanished

The following year Mindray inexplicably wrote down the entire value of its acquired PMD assets to ZERO (this impairment was

not disclosed to investors). Notably on the face of it, $656m in total long-lived assets simply vanished from MR's financials

We believe management will be forced to restate its historical filings and ultimately take the $656m impairment charge

Evidence further suggests Datascope's PMD contribution to MR sales were inflated and acquired assets were inflated by +72%

Zonare – MR paid 1.6x sales for a business which recently lost nearly 25% of its revenues, is growing more slowly than a peer 5x its

size, has had substantial management turnover with 3 CEOs in the last few years, and which is facing a lawsuit by an OEM and

distributor to the tune of $50mn for intentional fraud

Dragonbio – MR acquired this orthopedics equipment manufacturer for $35m despite them only generating $4.6m in sales and

$0.185m in profit. This is a company that not only doesn‘t have meaningful IP, it‘s in an entirely different product and customer set.

One has to question why MR would possibly need to pay such a substantial amount of money for such a sub-par asset

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

The Dubious Acquisition of Datascope

29

In May 2008, Mindray proclaimed to become a global med-tech company when it acquired the Patient Monitoring assets of

Datascope in the United States for a consideration of $208m

Despite consensus perception, it was a very limited purchase. MR acquired only some of the PM assets and a restricted right to use the

name through 2009 on certain products as well as to co-brand the same set of products from 2010-2015

Notable restrictions: the rights were only conveyed to Mindray DS USA, with Mindray International specifically excluded.

Manufacturers had to be approved and certified by Datascope and Mindray DS USA‘s Chinese affiliates were specifically barred

from manufacturing the equipment. The name Datascope was not conveyed, just the right to continue using the Datascope name

on specific products

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

We Question The Price Mindray Actually Paid For Datascope

30

While the street was quick to superficially praise the move, we decided to look deeper into this alliance with a highly questionable

business partner

Mindray's association with Datascope began in 2003, when Datascope began distributing a Mindray patient monitor, with modifications,

under the Datascope name called the ―Duo‖, the two also collaborated on a later monitor called the ―Trio‖

Fire sale?

At the time of Mindray's PMD acq. Datascope appeared to be in a rush to sell its entire business

The company had come under scrutiny by regulators, its employees & its top shareholder Ramius Capital

Ramius alleged that (1) there were irregularities in the Chairman's expense reports (2) a senior executive was improperly using

Company funds to finance an affair he was conducting with another Company employee (3) the same executive and the Chairman of

the Company had engaged in irregular transactions with distributors (4) a member of the Chairman's family employed by the

Company did not perform services (5) the Chairman had engaged in unspecified 'sweet heart‗ deals (6) the Chairman paid himself

dividends (7) the Chairman was mentally unfit to manage the Company and (8) outside counsel had assisted the Chairman in

concealing some of the above activities

MR paid 1.5x ($209m cash + $30m receivables) sales for a money losing (FY08 PMD sales were $138m and with a loss of $5.7m),

45% margin patient monitoring business in a market growing at an abysmal 2-3% rate

Investors thought it was a bad purchase. MR shares underperformed the MSCI China index by 12% in March after the purchase, while

Datascope‘s shares were up 13.8% as ―investors cheer divestiture‖

At the time of the acquisition, all of Datascope was on the block

The profitable and more sophisticated portion of Datascope was purchased by Getinge for $618m, or 2.7x sales and 12.9x EBITDA

Mindray violated Datascope trademarks and was sued

MR had limited access to the Datascope brand through 2015 (only U.S. and only on certain products), yet violated this agreement in

order to drive sales and was sued by Datascope, eventually paying $7m (p. 15 2011 20F)

Case Study: OSI buys Spacelab for $57m

Spacelabs Medical had an offering in PMDs similar to that of Datascope. In 2004, it was acquired by OSI for ~0.4x sales ($57m

acquisition price on $150m in LTM sales) despite being both profitable and slightly larger than the Datascope's assets MR acquired

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

We Believe Datascope's PMD Business Was Worth Far Less Than MR Paid

31

In Datascope's 2008 10k (6/30), the Company recorded the assets & liabilities of its discontinued PMD operations. We find

large discrepancies between Datascope's accounting and what Mindray claims to have received.

Note: Datascope's PMD business recorded a loss of $5.7m and carried just $5m in assets, despite selling for $209m

Spacelabs held tangible net assets at a book value in excess of $70m and was acquired for just $57m

-14% YoY

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Fair Value DScope Dec-08 Dec-08

PMD Assessment Jun-08 Step Up MR

Current Assets 5,773 6x 33,211

PP&E 2,253 15x 34,900

Intangible Assets 13,413 5x 60,900

Liabilities -959 11x -10,166

Goodwill NA - 96,327

Total 20,480 - 215,172

% of Transaction - MR Accounting

Tangible Assets 30% 68,111

Intangible Assets/Goodwill 70% 157,227

Total Assets Acquired 100% 225,338

Less: Liabilities -10,166

Net Assets Acquired 215,172

Mindray Significantly Stepped Up the Value of Datascope's Assets

32

It is clear that Mindray overpaid for Datascope's PMD business, then significantly stepped up the value of the assets to justify a $209m

acquisition price. It is even harder to justify this premium given that Datascope's PMD sales were decelerating and the business was

unprofitable (FY2008 sales of $134.1m (-14% YoY) and PBT loss of $5.7m)

Traditionally we see assets receive a slight step up post-acquisition, but not to the egregious level of over-inflation of MR‘s accounting

Note: MR was the only bidder for DSCP‘s PMD business, which DSCP was looking to unload given its underperformance

Notable Step-Ups

Current Assets: Datascope reported having $5.7m in current assets for its PMD business and Mindray stepped up the value 6x to

$33.2m

PP&E: Datascope reported having $2.2m in PPE (net of 2.8m in accum. depreciation) and MR stepped up the value 15x to $34.9m

Intangible assets & goodwill ($60.9 + $96.3) accounted for 70% of the transaction

Intangible assets: Datascope reported having $13.4m in intangible assets and Mindray stepped up the value 5x to $60.9m

FAIR VALUE ASSESSMENT MINDRAY / DATASCOPE PURCHASE ACCOUNTING (12/31/2008)

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Post Acquisition MR's Long-Lived Assets Jump

33

Post Mindray's acquisition of Datascope the company's long-lived assets jumped by $234.2m in the U.S., despite Mindray claiming it

acquired $225.3m total assets from Datascope, not all of which were U.S. based

Mindray reported long-lived assets of $785.2m vs. total Assets of $785.8 (effectively allocating all of its assets to long lived assets)

Note: Mindray appears to take a $47.1m impairment on its long lived assets, yet we find no record of this impairment on the

company's reported financials

MR's 2007 20F clearly contradicts its reporting in 2008. In „07, MR claimed it did not have any LL assets outside of

China, yet in „08 the company reports having $95m assets (21%of total) ex-China in 2007

MINDRAY 2008 20F (PG F-31)

Long-Lived Assets Acquired (2008 20f, pg. F-31)

2007 2008 Delta

PRC 351.6 503.1 151.6

United States 3.8 238.0 234.2

Other countries 91.4 44.1 -47.4Total LL Assets 446.7 785.2 338.4

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

MINDRAY 2007 20F (PG F-26)

MINDRAY 2009 20F (PG F-32)

MR Wrote Down $208m, or The Entire Consideration for Datascope To Zero

34

MR wrote off $208.2m in LL assets in the US, effectively the entire $208.6m (net of the $397k cash retained) cost of the

Datascope acquisition to ZERO

As we noted previously, MR's 2008 vs. 2009 filing reveals MR's 2008 long-lived assets were significantly revised & impaired

downward– a majority of the assets being in China and the U.S., with China realizing greater absolute declines vs. U.S. seeing

substantially higher percentage decreases

We question the dubious purpose behind Mindray's acquisition of Datascope and whether Datascope may have carried a significant

amount of Mindray's channel stuffed inventory

MINDRAY 2008 20F (PG F-31)

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

2008 Long-Lived Assets Long Lived Assets

2008 - ('08 20F) 2008 - ('09 20F) Delta 2009 2010 2011 2012

PRC 503.1 95.14 -408.0 143.5 219.5 259.7 289.0

United States 238.0 29.8 -208.2 30.6 29.2 28.3 28.5

Other countries 44.1 4.2 -39.8 5.4 5.1 5.2 7.4

Total LL Assets 785.2 129.1 -656.0 179.5 253.7 293.2 324.9

% of Total Assets 100% 16% 19% 22% 20% 17%

Total Assets Reported 785.8 785.8 966.3 1,150.6 1,459.0 1,857.0

?

MR's Auditor Confirms Our Belief That Datascope Was Overstated

35

In MR's 2008 20F, PWC noted that they excluded Datascope's PMD business from the company's assessment of internal

control of financial reporting and noted Datascope's assets and revenues as a % of MR's 2008 financials – both of which

were significantly lower than MR reported to the street

Mindray's long lived assets increased from 2007 to 2008 by $338m. Yet Mindray's purchase accounting suggested the company

acquired $225m in assets from Datascope

In the same filing MR's auditor PWC, noted in its ―Report of Independent Registered Public Accounting Firm‖ that

Datascope's assets only accounted for 16.7% of assets

This implies Datascope's assets were $131.2m of the $339m increase, suggesting nearly 61% of the asset increase was related to

Mindray‘s historical business. We believe MR took this as an opportunity to purge $656m of stale assets in China

MANAGEMENT'S ANNUAL REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING (MR 2008 20F P. 84)

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Asset Contribution2007 2008 Delta

PRC 351.6 503.1 151.6United States 3.8 238.0 234.2Other countries 91.4 44.1 -47.4Other Undefined Assets 0.0 0.6

Total Assets 446.7 785.8 339.1% growth 36% 76%

% of Assets Delta PRC 79% 64% -15%United States 1% 30% 29%Other countries 20% 6% -15%

Datascopes Contribution Auditors Ex Dscope% of Assets 16.7% 83%Assets 131.2 654.5Contribution to '08 increase 131.2 207.8

Contribution to increase 39% 61%Note: in MRs 2009 20F MR seemingly revised its 2008 long lived assets to 129.1m

Asset Discrepancies2008

Purchase Accounting ('08 20f p.F-17)Current Assets 33.2PP&E 34.9Intangible Assets 60.9Goodwill 96.3Total Assets Acquired 225.3Implied % Of 2008 Total Assets 29%

Total Assets 785.8

PWC Assesment ('08 20f p.84) 2008Actual % Of Total Assets 16.7%Actual Datascope Assets 131.2

$ value difference +94.1

% inflated vs $225m Assets Acquired 72%

Questionable Zonare Acquisition

We question management‟s logic in acquiring Zonare as we find numerous core issues which imply significant headwinds

MR paid 1.6x sales for a total consideration of $101m for an unprofitable business whose growth has substantially slowed and

whose competitors are becoming increasingly larger

Despite a reported ~$800m in ―cash‖ on its balance sheet, MR largely funded the acquisition with debt, as they borrowed

$120m in 3q13 (the quarter the acquisition closed), which is more than they borrowed in all of 1h13

Jon Brubaker, Senior Analyst at MDBuyline, has been ―tracking ZONARE for years and the activity levels have not shown

much growth.‖

Compounding issues at Zonare Medical

3 CEOs in 5 years: Zonare‘s management team appears to be a revolving door. Donald Southard (former CEO of

Datascope's PMD business), Jay Miller and Timothy Marcotte have held CEO positions over the last 5 years

Fraud accusations: Zonare allegedly engaged in intentional fraud, according to an 11/1/2013 lawsuit by distributor HDX

Patent infringement lawsuit: In 2008, Zonare agreed to pay $3.25m to settle (not including legal fees) a patent infringement

suit initially brought by competitor Sonosite in 2007

Failed IPO: Zonare had a failed IPO bid in 2008, as they desperately needed cash. We question whether the Sonosite

settlement had anything to do with it

Share loser: Zonare is growing more slowly than portable ultrasound market leader Sonosite, which is ~5x Zonare‘s size

Burning through cash: Zonare had already raised ―$171m in funding since it was founded in 1999‖ from various backers

Evidence suggests that the sales lost from Zonare‟s Japan disruption will be extremely difficult to regain

In a press release dated 3/2/12, Zonare recorded $70m in sales and guided for 15-20% growth in 2012, implying that sales

would be $80.5 to $84.0m. The Company also claimed that they would achieve an operating profit for the year

Actual performance was just $64m and the company lost money

CIO May Li noted: "In 2012 there was a disruption in the Japan market as a result of contract discontinuation, was one of

the key distributors there. So it is a one-time event. We don‘t expect such disruption to continue going into 2013, 2014.‖

This is highly deceptive at minimum. In the next few slides, we detail our findings

36

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

The Anatomy of a Lie

37

First, MR noted that the contract disruption was only ―one of [Zonare‘s] key distributors [in Japan].‖ This appears to

be a lie

Zonare‘s website clearly lists all of its distributors in each country by region, but does not include any in Japan

Meanwhile, they include the tiny 115-island nation of Seychelles, located some ~1,000 miles east of mainland

Africa, which boasts a population 87,785 (according to the World Bank)

They also include HDX Corp, which was Zonare‘s South Korean and Vietnamese distributor. As of

11/1/2013, they are suing Zonare for breach of contract, intentional fraud and fraudulent concealment

Either MR lost multiple Japanese distributors in 2012 or MR‟s CIO managed to lie multiple times to

investors in the span of one sentence

It appears that Fujifilm and Zonare had an exclusive distribution agreement in Japan (detailed further

on slide 39) and MR felt the need to lie about this to investors

Where is the Japanese Distributor?

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

The Anatomy of a Lie (cont‟d) – Full Page Screenshot

38

D E C - 2 0 1 3

Where is the Japanese Distributor?

O T T O M A N B A Y R E S E A R C H

What Happened With Fujifilm?

39

Mindray‟s lies – Zonare lost its exclusive distribution partnership with FUJIFILM in 2012. This was not a small one-

time disruption to ―one of ‖ the key Japanese distributors as management would lead investors to believe, as:

Japan accounted for nearly 25% of revenue. These sales are not small nor are they easily replaceable

As detailed in slide 37, Zonare has not added new Japanese distributors, so this disruption has clearly continued

through all of 2013, contrary to MR management‘s claims

FUJIFILM was not ―one of ‖ several key distributors. They were the key distributor – the only one

The product was marketed under a different brand and proprietary distribution network. How does MR propose to

regain all the lost sales?

On November 28, 2006, Fujifilm and Zonare entered into an OEM agreement

Zonare had an exclusive distribution agreement with Fuji – According to p.63 of Zonare‘s S-1 filing, ―under

the agreement…[Zonare] agreed to sell [its] z.one ultrasound system in Japan only through Fuji‖

According to the S-1, the agreement was set to expire at the end of 2010, ―with automatic renewals for

subsequent one year periods upon agreement of minimum purchase commitments for each subsequent period‖

Zonare‟s systems were sold under a different brand name in Japan – ―Under the agreement, FUJIFIM will

market ZONARE‘s z.one ultrasound system…under the FUJIFILM brand FAZONE M throughout Japan‖

On August 15, 2011, FUJIFILM launched the FAZONE M in the U.S.

On December 15, 2011, FUJIFILM announced an offer to acquire portable ultrasound market leader Sonosite for

$995mn or ~3.3x 2011 sales of $306m

In 2012, Zonare lost its Japanese ―distributor.‖ Given the above information, it would be easy to make that case

that this ―distributor‖ was in fact its OEM partner FUJIFILM, and the agreement fell apart in 2012 when the

Sonosite deal closed

Furthermore, we question the strength of Zonare‘s business given that FUJIFILM, who had a very deep insight

into the product and its marketability, chose to allow MR to walk away with a deal at 1.6x sales when FUJIFILM

paid 3.3x sales for Sonosite

Finally, note that in 2008, Zonare agreed to pay $3.25mn to settle a patent infringement suit brought by Sonosite

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Intentional Fraud – A Recurring Theme

40

On 11/1/2013, Zonare distributor HDX Corp. filed a lawsuit against the company for breach of contract, intentional fraud and

fraudulent concealment

According to p.11 of the lawsuit, HDX believes that compensatory damages for fraud will exceed $50m

HDX and Zonare‘s relationship began on January 29, 2005, with the two entering into an International Distribution Agreement

On July 22, 2009, Zonare proposed that HDX also become its local manufacturer

To summarize, Zonare and HDX entered into an exclusive manufacturing and distribution agreement whereby HDX was to (1)

invest $3m in Zonare stock (they did so in December 2009) and (2) construct a factory to produce Zonare‘s product (HDX

spent millions on this as well)

Zonare lied in order to [allegedly] offset a major liquidity crunch at Zonare

Note that they only had ~$8m in cash in March of 2008 (according to their S-1). They then (1) had to scrap IPO plans

(2) settled a lawsuit with Sonosite for $3.25m in mid-2008 and (3) continued to be unprofitable, burning millions in cash

D E C - 2 0 1 3

HDX COMPLAINT – PG. 8

O T T O M A N B A Y R E S E A R C H

With Just 3% Share, Zonare Isn‟t As Meaningful As the Street Believes

41

D E C - 2 0 1 3 O T T O M A N B A Y R E S E A R C H

IV Phantom Cash

42

O T T O M A N B A Y R E S E A R C H

Phantom Cash – Is the Cash Real?

43

We question why a company reporting over $1bn in cash has consistently relied on debt or equity financing as its primary

funding source. We have not seen this behavior in any legitimate business or Mindray's Chinese peers

Acquisitions

Both Datascope and Zonare, $208m and $101m, respectively, were primarily funded with debt

Debt funded dividends?

On 4/26/11 (p.69 2011 20-F), MR took out a two-year term of $35m at L+210bps to fund its FY11 dividend

On 3/26/12, (p.F-23 2012 20-F), MR took out another two-year term loan of $50m at L+355bps (notice the increase in cost of

funding) to fund its FY12 dividend

Working capital

On 7/18/2011 (p.69 2011 20-F), MR entered into a revolving credit facility to fund the working capital requirements of its

Mahwah, NJ facility at $50m at L+180bps. The facility was fully drawn just 4 days later on July 22, 2011

Mindray generates 55% of its sales outside of China – does the company not keep cash overseas? Does Mindray borrow

to pay taxes as well?

2010 Equity Offering is a glimpse into MR's significant cash flow issues

In 2010, we find evidence which suggests that Mindray came dangerously close to defaulting on its $141m loan with the Bank of

China and its $25m working capital loan with HBSBC, despite alleging the company had $305m in cash

We believe Mindray nearly avoided default by purposely misleading US investors as to the REAL cash position of the

company and deceived investors regarding the company's 2010 equity offering

In 2008, Mindray borrowed $141m of Datascope's purchase price from the Bank of China and opened a $25m revolver to

finance its WC. Both borrowings were collateralized with MR's alleged balance sheet cash and, strangely, the key man life

insurance of one of the Co-CEOs

Despite reporting $305m in cash the previous qtr, we question whether Mindray actually had the cash it claimed The

company missed its loan payments to the BOCHK, so the loan was subsequently modified. MR also could not pay

its minor $25m WC facility which was also modified

The company was able to pay both loans once it raised equity from US investors in 2010 (note: MR deceptively claimed the

equity raise was for ―business development and for general corporate purposes‖ per S-1)

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Mindray Medical Balance Sheet

Q4 Q1

12/31/2007 3/31/2008

Assets

Cash & Equivalents 189.0 212.0

Short Term Investments 55.9 93.8

Total Cash & ST Investments 244.9 305.8

% QoQ Growth - 25%

MINDRAY'S LOAN AGREEMENT

MR Claimed To Borrow a ST Loan To Finance the Acquisition…

44

Despite what appeared to be a rich balance sheet, Mindray borrowed a “short term loan” through its shell company (MR

Investments & MR Holdings) to finance the acquisition

On April 23rd 2008 (p. 78 2009 20-F), MR Investments entered into an agreement with the Bank of China to borrow $141.4m,

payable in three installments of $47m due in June, August & November 2009

Note: The BOC required MR‘s co-CEOs to guarantee the loans, as well as provide additional insurance through one of the co-

CEOs‘ key man life insurance policies. This amounted to $29.3m (RMB200m) per 2009 20-F, p. F-21

MR over collateralizes the $141.4m loan with $146.5m in cash in an BOCHK ―investment account‖ to be held as collateral, yet we

cannot reconcile why MR inconsistently reported $141.4m on the BS as collateral

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

MR Also Borrowed $25m To Finance its Working Capital Facility…

45

Financing working capital requirements?

MR ironically also entered into a $25m revolving facility to finance its working capital, then PAID back the $10m used facility

– again this is a company with +300m in reported cash

Again, MR pledged $11.7m or ~45% of the working capital facility with cash

Note: Total collateral for the BOCHK acq. loan and WC facility is $158.3m ( $11.7m+ $146.5m)

In 2009, MR also raised an unexplained $54m. Note: MR did not cite what the funds were for or where the cash went

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

In April 2009, MR was only able to pay $31.4m (p. F-21 2009 20-F) of the $47.1m due (oddly MR paid 2 mos. before the 1st

payment was due in June) and the loan was subsequently modified

At 12/31/09, MR's loan was modified with $110m still outstanding (p. 64 2009 20-F), implying MR missed its Aug &

November payment (the new terms were incredibly generous: $44m became due in June 2010 & $66m due in June 2011)

MR paid a reasonable combined $928k for an ―arrangement fee‖ and ―finance charges‖

Further alarming is that in June 2009, MR attempted to renew its 2008 $25m revolver with HSBC, but the bank cut the revolver

capacity from $25m to $13m (p. 64 2009 20-F) . The expiration was extended to March 2010

As we noted in the slide before, we question how MR was able to raise an additional $54m (which was also collateralized with $54m

in alleged cash) on April 2009, when it appeared MR could not pay back its existing loan balances

Given the influx of cash, why was MR unable to make the full installment payment and avoid the heavy fees?

We also question how MR was able to collateralize the $54m ST loan when its appears MR couldn‘t even make its $47.1m

payment

The 6-K was filed on May 11, 2009, so clearly MR knew at this point that they wouldn‟t be able to (or chose not to?) pay off

the coming debt payment fully, yet still falsely told investors that the “loans can be fully repaid”

MINDRAY 2009 20F

Loan Payment Missed!

46

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

We find it hard to believe that Mindray could miss a $47.1m payment to the Bank of China and cost shareholders additional

fees which amounted to $928k

Mindray missed payments on both its $25m working capital facility and $141.4m Bank of China loan

In MR's 2008 20F the company claimed that they had enough cash to fund its operations through 6/2010 and make

payments to its acquisition loan through the company's restricted cash funds, its deposited collateral, and cash

Note: As depicted below, MR made it appear to investors that they were well-capitalized in both 2008 and 2009 and

fully able to pay off their debt – we question whether the company had the cash it claimed or whether the cash had

alternative purposes

On March 31, 2009, MR reported $103.1m in cash & equivalents and $158m in restricted cash. In that 1q09 6-K, MR

defined restricted cash as follows:

―Restricted as the security package required for the bank loans as of March 31, 2009... As of March 31, 2009, the

short-term bank loans can be fully repaid from such short-term restricted cash‖

Mindray gave the impression to investors that the business was well capitalized despite its inability to make a

$47.1m loan payment or having its $25m HSBC working capital loan cut

MINDRAY 2009 20F (PG F-21)

MR Falsely Claimed it Had Sufficient Cash to Make Loan Payments

47

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Investors Were Misled Regarding Mindray's 2010 Equity Raise

We believe MR misled investors as to the intention of its equity offering. We believe the company did not have the cash it

claimed and would have likely defaulted on its China loan had it not raised equity from US investors

On 3/4/10 MR priced a secondary offering of 4 million American depositary shares at $38.20, raising 152.8m in new cash – MR

claimed the cash was for “for business development and general corporate purposes”

The street took it as a sign that the company was preparing for another large acquisition. In reality, it appears that the

Company raised equity to pay back loans it owed to the Bank of China and HSBC, despite claiming a well-funded

balance sheet

Coincidentally, MR repaid its full $110m balance and HSBC WC loan in March 2010, the same month as the offering. They only

had to repay $44m in June of 2010 and the remaining $66m was coming due a full 15 months later in June of 2011. MR also repaid

their $54m TL facility in 4/2010, bringing its bank balance to zero

Note: MR published its 4Q09 and FY2009 results on 3/1/2010, just 3 days before its offering

48 - Mindray 2009 20F

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

V Earnings Are Overstated

49

O T T O M A N B A Y R E S E A R C H

We Question Mindray‟s Reported European Sales

In a video dated 12/6/2012, David Yin, the head of MR Europe says, ―We keep investing in Europe, and we will see in the future

if our business over here can be over 100 million or even 500 million US Dollars. That‟s our target we‟d like to achieve in

the next 5 or 10 years.”

Video support: http://www.oostnv.com/testimonial-extra/mindray

In its FY2012 20-F, MR reported $101m in European sales, up ~11% from the $91m reported in 2011 (p. 60 FY2012 20-F)

We question why MR‘s head of Europe would use $100m as a ―5 or 10 year‖ target when the Company was on the verge of

reporting $100m of sales in just a few months – note in 2011 MRs European business reported $91m

Mindray appears to run its entire European operations through its location in the Netherlands (Europe headquarters),

which services 30 countries out of what is a 3,080 square meter office and a leased 1,380 square meter warehouse

Does MR really have the European sales they claim?

50

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Mindray claims its ex-China business (55% of sales) has not been profitable since the company acquired Datascope's

money losing PMD Business

Either these disclosures are accurate and MR‘s acquisitions have been a horrid drain of shareholder capital, or MR is

aggressively attempting to avoid taxes outside of China

A higher tax rate would significantly impair MR‟s earnings and share price and could result in significant

fines, penalties, and back taxes

This could also indicate transfer pricing, which both the PRC & the US have strict laws against

Note: All US based distributors say payments for sales are made to Mindray in Mahwah, NJ, not to Shenzhen, China.

Either MR is highly inefficient in the U.S. or one of two other options: (1) they‘re using the U.S. as a tax center to shield

themselves from U.S. taxes or (2) they‘re using transfer pricing to deflate U.S. earnings, again to evade taxes

MR's eliminated its PBT disclosures post-2008. It wasn‘t until a 5/30/2013 SEC correspondence that MR was forced to reveal

updated figure

SEC CORRESP. (7/2013) REVEALS EX-CHINA HAS RECORDED A LOSS SINCE

MINDRAY 2008 20F (PG F- 26)

Aggressive Transfer Pricing

51

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

SEC Disclosure Implies China Has 60% PBT Margins

52

We question whether Mindray is using such disclosures to evade US taxes

China has represented ALL of the group‘s PBT over the last 3 years

China‘s PBT margin was 60% vs. the group‘s total gross margin of 57%

The loss (PBT) in the ex-China business was magnified in FY12 by 178% to -$66m from -$24m in FY11

This ridiculously implies that ex-Chinas gross margins are significantly lower than group GMs despite being a higher % of sales

This trend is in stark contrast to how management has been guiding investors

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

China vs Ex China (SEC Correspondence)

2010 2011 2012

China 293,435 374,312 472,991

Ex - China 410,874 506,431 587,063

Total Sales 704,309 880,743 1,060,054

Profit Before Tax

China PBT 200,424 213,272 285,595

% growth -- 6% 34%

% margin 68% 57% 60%

Ex - China PBT (27,327) (23,700) (65,944)

% growth -- -13% 178%

% margin -7% -5% -11%

Total PBT 173,097 189,572 219,651

% margin 25% 22% 21%

Note: PBT financials were disclosed as a result of SEC

correnspondence on 5/30/13 MR INCOME STATEMENT - AS REPORTED

Questionable Dividend Payments

53

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

We question whether Mindray's dividend payments are truly one time

In 3q13, MR revealed that the company was taking a ―one time‖ withholding charge for an intra-group fund transfer to remit

cash overseas which amounted to $20.8m – note MR operates 55% of its business overseas

Management did not disclose how much cash was being remitted and what the cash was being used for

Note: when asked by Bin Li (MS analyst) regarding the significant withholding tax, CFO Alex Lung noted:

―…Well the nature of this is actually emulation to our overall cash planning to relocate part of our cash from

China to outside China. And the mechanism from that we are doing it just by way of having our Shenzhen

subsidiary to pay a dividend to the Hong Kong holding company. And based on the regulations, we are obliged to

pay a withholding tax as a result of this dividend payment to the Hong Kong company as it is our internal policy

that we don‟t generally pay dividend out of subsidiaries. And for China, we haven‘t really paid dividend out in 4-5

years already. So to us, it‘s the fund transfer is really one time. We do not anticipate a recurring dividend payment coming

out from our China entity. As such, we have treat this expenses in relation to this fund transferred as a one-time

expenses and as such excluded from our non-GAAP presentations‖

Alex Lung, CFO, Q3-13 Earnings call

Dubious Dividend Payments

54

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

In MR's 3q13, Alex Lung noted the last time the company paid its hold co. a dividend was ―4-5 years‖ ago

Luckily, in 2008 and 2009 only, MR released its shell company's filings to US investors – which suggests MR's dividend had ill purposes

In 08, MR recorded ―equity earnings from subsidiaries‖ in the amount of $119.7m. Note in 2008 MR moved $119.7m, (from Nil

in 2007) in restricted cash to its BVI subsidiary on its BS to be held as collateral for its BOCHK loan – as we noted earlier -despite

claiming to have the cash MR missed its BOCHK installment payments entirely

MR's 2008 reported op. income of $117.5m was lower than the dividend MR claimed to receive from its subsidiary - $119.7m

Even more questionable is on pg F26 of MR's 20F, MR claimed to have moved $117.5m (contradicting the 119.7m in

restricted cash reported on its balance sheet) – in line with the company's reported operating income of $117.5m

We question why a ―wholly owned‖ subsidiary would pay a dividend to its parent and why the income was not consolidated

We find no evidence that MR took a withholding on its dividend paid to its holding company, as the company claimed in Q3-13

We cannot find the taxes that was paid by the holding company

We Find Numerous Contradictory Restricted Cash Amounts

55

We find numerous restricted cash amounts in MR's 2008 filing suggesting Mindray was trying to obfuscate clarity

In 2008, MR moved $117.5m to restricted cash, claiming it would be held as collateral for its Datascope loan (we find evidence

that the $117.5m was used for more dubious purposes)

Curiously, restricted cash was recorded as $119.7m on the balance sheet. We have been unable to reconcile the discrepancy

We find numerous contradictory restricted cash & collateral amounts suggesting MR was attempting to obfuscate clarity

MINDRAY 2008 20F

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

So, Which is it?

On 7/27/12, as part of its correspondence with the SEC, Mindray disclosed the company's sales by channel and

geography. Note the disclosure is not reported in Mindray's SEC filings

China

Distributors accounted for ALL of Mindray's domestic growth from 2009 – 2011 period (the only disclosed periods)

Distributor sales have outpaced direct sales in China by a margin of 2,100bps, with CAGRs at 18% & (3% )

Ex -China

Sales to distributors have outpaced direct sales channels ex-China by a margin of 1,400bps, where Mindray claims to have

an established direct sales force

To compound matters, in MR's correspondence with the SEC on 6/28/12, investors learned that Mindray began using

―equipment leasing agents‖ to normalize its rising A/R balances

Note: Mindray recognizes revenue from equipment leasing companies as ―International Direct Sales‖ despite these

businesses operating like distributors

Sales To Distributors Account For a Disproportionate Amount of Growth

56

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

DISTRIBUTOR VS. DIRECT SALES % Employees

Channel By Geography 2009 2010 2011 CAGR

China distributor sales 221.7 244.3 307.1 17.7%

China direct sales 70.9 49.2 67.2 -2.6%

Intl. Distributor sales 241.1 303.5 381 25.7%

Intl. direct sales 100.5 107.3 125.4 11.7%

Total by Channel

Distributors 462.8 547.8 688.1 21.9%

Direct Sales 171.4 156.5 192.6 6.0%

% of Sales

China distributor sales 76% 83% 82%

China direct sales 24% 17% 18%

Intl. China sales 71% 74% 75%

Intl. direct sales 29% 26% 25%

Total Revenue 634.2 704.3 880.7 17.8%

Inflated Gross Margins

57

We believe Mindray's gross margins are more in line with peer levels of 45%-50% vs. the impermeable 60% the company

claims

Contradictory to management‟s public claims, in MR's OWN investor presentation show that it has lost significant

market share in the majority of its key products in China to multinational and domestic competitors since 2009

Mindray‘s core value category is a miserable, fragmented and hyper-competitive one in China, where companies have to

give away margins to hospital administrators and compete with well financiered multi national companies and domestic

players reaching scale + moving upstream

If MR hopes to stem share losses, they will have to sacrifice GMs

MR's value proposition is to continually under price MNCs by 20-40%. How is it, then, that MR boasts the highest margins

among all peers?

Within China, Mindray has purchase with small, poorly financed county hospitals and must increasingly pay its way in via a

layer cake of tiny distributors who don‘t have the cash to take inventory risk

Labor and manufacturing costs have risen across the board in China

Developed markets are operated through GPOs, who take significant margin from manufacturers

We spoke with numerous multi-national and local distributors who noted they were “unable to piece together how

Mindray gets the kind of gross margins they do…it is unheard of in their segments”

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

Mindrays Market Share by Product in China

Mindray key products 2009 2011 2012 DELTA

Patient Monitoring & Anesthesia Devices (PMD) 31.0% 27.9% 27.2% (3.8%)

Hematology Analyzers (IVD) 34.0% 20.4% 20.6% (13.4%)

Biochemistry Analyzers (IVD) 18.0% 16.2% 19.3% 1.3%

Ultrasound Systems (MIS) 14.0% 10.9% 10.1% (3.9%)

Reported gross margin by product 2009 2011 2012 DELTA

Patient Monitoring Devices (PMD) 55.8% 54.9% 56.5% 0.7%

In-vitro Diagnostics (IVD) 56.3% 55.8% 58.3% 2.0%

Medical Imaging Systems (MIS) 63.3% 65.2% 65.3% 2.0%

Group Gross Margins 55.8% 55.2% 56.7% 0.9%

2009A

2012A

2011A

Mindray's China Business Has Reported Losing Market Share Since 2009

Mindray has consistently misled regarding its growth and market share position in China. The Company's OWN

investor presentation contradict MR's communication to the street

Patient Monitoring & Anesthesia Machines: This is MRMR reported share of 31% share in FY09 in China, its largest

segment. As of FY12 MR owns 27.2% of the market, a 3,800bp decline

IVD – Hematology + Biochemistry Analyzers: MR noted that IVD is a key growth area. A look at share gains across key

products gives a different impression

Hematology analyzers: MR reported share of 34% in FY09. As of FY12 MR owns 20.6%, a 13,400bp decline

Biochemistry Analyzers: Share has been extremely inconsistent. In FY09, MR's share was a healthy 18%, then in FY11

share declined to 16.2% a 2,200bp decline. As of FY12 , the company reported share of 19.3%, but this was primarily

due to fraud finding against market leader Olympus

Ultrasounds (B/W + Color): Another key growth area for MR. MR reported share of 14% in FY09 and as of FY12 MR

owns 10.1% of the market, a 3,900bp decline

Note: 2010 presentations did not report market share figures. Coincidentally Mindray's China business grew 0% YoY

58

O T T O M A N B A Y R E S E A R C H D E C - 2 0 1 3

VI Implausible Short Term Investment Balances & Returns

59

O T T O M A N B A Y R E S E A R C H

Short Term Investments Are Growing…And Are Growing FAST

60

Mindray Medical‟s short term investments have grown at a faster rate than any other line item on the balance sheet

MR's product mix is heavily levered to capital equipment, ~90% of sales (relies on new equipment orders) + lacks a steady stream

of high margin disposables, hindering cash flow generation