Embed Size (px)

Citation preview

October 8th, 2012

Biocon Ltd.

Focused on innovation

SKP Securities Ltd www.skpmoneywise.com Page 1 of 13

CMP Rs 273 Target Rs: 338 Initiating Coverage - Buy

Face Value (Rs.) 5Equity Capital (Rs.Cr) 100.0M. Cap (Rs. Cr.) 5,46052-wk High / Low (Rs.) 363/208Avg.Volume (qtrly) 61,843BSE code 532523Reuters code BION.BOBloomberg code BIOS IN

Key Share Data

Shareholding Pattern (as on June 31,2012)

40% Indian

Promoter

20% Foreign Promoter

14% Institutio

n

25% Non-Institution

Source: Company Financials (Rs In Cr.)Particulars FY11 FY12 FY13E FY14ENet Sales 1806 2087 2420 2808Sales Gr . (%) -24% 16% 17% 16%EBIDTA 522 517 582 668EBIT 422 405 428 481Adj.PAT 370 338 358 403Adj.EPS (Rs.) 18.5 17.1 17.9 20.1CEPS (Rs.) 4.9 5.1 5.6 6.5Key Ratios FY11 FY12 FY13E FY14EP/E (x) 14.8 16.0 15.2 13.6P/BV (x) 13.4 12.0 10.9 9.8P/CEPS (x) 55.6 53.2 48.5 42.1M.Cap/Sales (x) 3.02 2.62 2.26 1.94EV/EBIDTA (x) 10.2 10.2 8.9 7.6ROCE (%) 18% 16% 15% 15%ROE(%) 17% 15% 14% 14%EBIDTAM(%) 29% 25% 24% 24% Price Performa nce Biocon vs Sensex

-8%

-5%

-2%

1%

4%

Biocon Ltd. BSE_SENSEX

Company Profile

Biocon India Ltd. (incorporated in 1978) was the first Indian manufacturer and exporter of ENZYMES to U.S. & Europe, subsequently developing in Fermentation process. Biocon subsequently entered in to biopharmaceutical, statins and then moved to insulin. Biocon is the first company worldwide to develop human insulin on a Pichia expression system and is one of the Asia’s largest insulin producers, having 12% of market share, through its 7 subsidiaries globally.

Investment Rationale

Branded Formulation is expected to drive growth: Biocon’s branded formulations business has grown rapidly over the period of time, offering a large basket of products for chronic disease. Biocon recently launched its first reusable insulin delivery device which has been showing sustainable value in the company’s basket of insulin therapies in the market.

Commitment to deliver affordable, quality Insulin: push the demand: Biocon has a good talent base, low cost infrastructure and a low-cost scientific talent pool that makes it to manufacture affordable drugs. We do expect affordability of drugs is going to be the crux for the company’s growth strategies.

Upcoming Facility in Malaysian to expand Biocon’s wings: Biocon

has commenced work on its Greenfield Malaysian biopharma manufacturing facility. We expect it to commence operation by 2014. The plant is expected to be one of the largest investments in the Malaysia healthcare biotech sector and expected to cater to the global requirements for Biocon’s range of biosimilar insulin and insulin analogs for diabetes treatment.

Insulin demand is expected to increase on the broader: Biocon has strong presence in anti-diabetic segment. We expect Biocon to launch Rh insulin in FY14 in the regulated market as they have completed phase III trials in EU. Insulin & Immunosuppressant is capturing 12-18% of domestic market.

Research & Development to be backbone of future growth: Biocon spends around 8% of its revenue on its R&D which is one of the highest in the industry.

Outlook & Recommendation: We expect Biocon to report healthy growth in the top line on the back of

increasing expenditure on R&D segment and increasing demand of affordable drugs in the market. At current market price of Rs 273, Stock is trading at an EV/EBIDTA of 10.2x & 9.5x for FY13E and FY14E respectively.

We recommend BUY rating on the stock with a target of Rs. 338 (23%UPSIDE) at the EV/EBIDTA of 9.5x on FY13E earning over the period of 18month.

Analyst: Savitree Singh/ Rupali Goregaonkar Tel No.:+91 22 2281 9012; Mob: +919820501348 Email: [email protected]

Biocon Ltd.

SKP Securities Ltd. www.skpmoneywise.com Page 2 of 13

The Company: A Snap Shot

Biocon India was incorporated in 1978 to manufacture select enzymes for the breweries industry. In 1978, Biocon India was incorporated as a 70:30 Joint Venture between Indian promoter’s

with70% stake and Ireland based Biocon Biochemical Ltd. with the 30% stake to manufacture and export few enzymes for breweries.

In 1994, Biocon established Syngene International Pvt. Ltd. as a Custom research Company (CRC) to address the growing need for outsourced R&D in the pharmaceutical sector.

In 2000, Biocon established Clinigene, India’s first clinical research organization (CRO) to pursue clinical research & development.

In 2001, Biocon becomes the first Indian company to be approved by US FDA for the manufacture of lovastatin, a cholesterol-lowering molecule.

Biocon is the first company, globally to manufacture human insulin, INSUGEN, using a Pichia expression system, 2004.

Biocon is the first Indian company to manufacture and export enzymes to USA and Europe. Biocon launched BIOMAb EGFR India's first anti-cancer, therapeutic monoclonal antibody-

based drug for treating solid tumors of epithelial origin, such as head & neck cancers, in 2006. In 2010, Biocon explores investment in Malaysia in partnership with Biotech Corp. Biocon launched INSUPen, a convenient and affordable reusable insulin delivery device, 2011. Biocon is among the world’s largest producers of statins & immunosuppressant. Biocon Research Center is Asia’s largest integrated biopharmaceutical research and development

center, which inaugurated in April 2012. Syngene collaborates with Abbott Nutrition and sets up a dedicated Nutrition R&D Center at

Biocon Park, in June 2012. Manufacturing facilities: In 2006, the company established Biocon Park, India’s largest

integrated biotech hub spread over a 90 acre of land, in a SEZ (special economic zone).The company has built additional capacity by commissioning the multiproduct microbial fermentation and synthetic conversion facilities at Bioco Park. These facilities were inspected and approved by the US FDA.

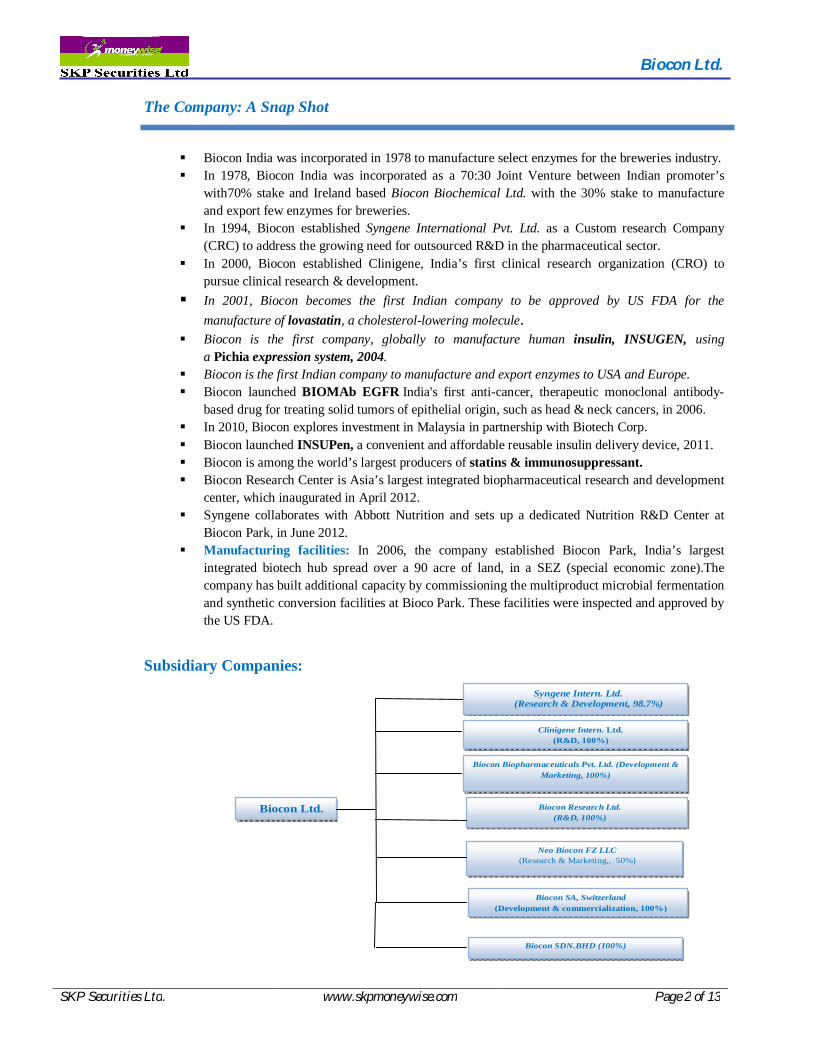

Subsidiary Companies:

Biocon SDN.BHD (100%)

Biocon Ltd.

Clinigene Intern. Ltd. (R&D, 100%)

Biocon SA, Switzerland (Development & commercialization, 100%)

Neo Biocon FZ LLC (Research & Marketing,, 50%)

Biocon Research Ltd. (R&D, 100%)

Biocon Biopharmaceuticals Pvt. Ltd. (Development & Marketing, 100%)

Syngene Intern. Ltd. (Research & Development, 98.7%)

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 3 of 13

Syngene-

Syngene, (99% subsidiary), got established in 1994 and was India’s first Contract Research

Organization (CRO). Syngene has the vision to become global leader in custom research & manufacturing by

creating value, identifying opportunities, developing a fully integrated service pipeline and delivering quality.”

In 2010, Syngene partnered with Endo Pharmaceuticals to develop a novel biological therapeutic molecule against cancer.

Syngene provides contract research services in biology in early stage of drug discovery, process development and contract manufacturing of biotheraputics.

Syngene’s customer base consists of over 60 companies consisting of big pharma, biotech, agrochemical, chemical, cosmetics and personal care companies.

Syngene provides contract research services in formulation development for oral solid as well as liquid dosage forms including injectable formulations.

Syngene is on going with the collaboration with over 60 companies worldwide. Syngene recorded a growth of 29% in top line for FY12 with revenues touching Rs 416 cr against

Rs 321.9cr in FY11. Syngene has currently 1,250 employees of which over 1,000 are scientists. About 200 scientists

are Ph.D. and around 750 are M.Sc.

Clinigene-

Clinigene, (100% subsidiary), got established in 2000 and became India’s first CAP (College of American Pathologists) accredited Central Laboratory.

Clinigene Started offering Clinical Research Services to global clients in 2005. Clinigene's services have a broad spectrum of activities including human pharmacology,

bioanalytical research, central laboratory, clinical operations, medical writing, medical monitoring, safety management, pharmacovigilance, clinical data management & biostatistics and regulatory services supporting early-phase through late-phase clinical development programs

Clinigene has strengths in oncology, diabetes , cardiology and is likely to capitalize on these segments.

Clinigene has over 165 highly skilled and experienced professionals. Clinigene offers FTF based, service fee and fixed fee contracts to suit customer requirements. Over 5,500 patients have participated in clinical trials of Clinigene. Clinigene recorded revenue of Rs 29 cr in FY12. We expect revenue to improve from here

onward.

Product Pipeline: Few of the Biocon products name are as follows.

IMMUNOSUPPRESSANTS MMF, Tacrolimus, Sirolimus, Pimecrolimus, Temsirolimus etc.

STATINS

Lovastatin, Simvastatin, Pravastatin, Atorvastatin, Rosuvastatin, Fluvastatin etc. MAbs BIOSIMILARS

Trastuzumab, Bevacizumab, rh-Insulin, Glargine, Lispro, Aspart etc. NOVEL:

Nimotuzumab, Itolizumab, BVX20, Conjugated MAbs, IN105, Phybrids etc.

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 4 of 13

INSULINS: Biocon is India’s premier Insulin Company registering the fastest growth in the insulin sector. The company markets the world’s first recombinant human insulin under the brand name Insugen. Biocon has recently introduced an innovative device called INSUPen which are showing good demand. From last two decades, there has been a marked increase in the prevalence of diabetes among both urban as well as rural India, while southern India having the sharpest increase. Biocon markets its insulin in Asia, Middle East and Latin America. We expect it to become a major player in the global insulin market. Insulin & immunosuppressant are capturing 12-18% of the domestic market.

7%10%

52%

9%5%

17%

57%

24%

7%1%

7%3%

0%

10%

20%

30%

40%

50%

60%

North America Europe BRIC-TM MENA Japan & Oceamia

RoW

Diabetic Insulin Market In Diff. Country

Diabetic Population Insulin Market

Source: Company & SKP Research

India’s Diabetes Boom: The western diet and life style that have accompanied India’s growing prosperity has brought and alarming rise in case of type 2 diabetes. Nationwide prevalence of T2D is more than 9%. The epidemic is not surprising in urban areas. However, the disease is now also becoming common in rural villages, especially in wealthy southern states.

STATINS-future growth driver:

The company is the major player in the statins business. Statins inhibit the excess production of bad cholesterol in the liver. Biocon manufactures all four statins namely: Lovastatin, Simvastatin, Pravastatin and Atorvastatin by fermentation process. Biocon has developed patented processes for the manufacture of Lovastatin and Simvastatin. The company exports over 80% of its statin production and commands over 20% MS in US and 22% in Europe. The global patents of Lovastatin, Simvastatin and Pravastatin have already expired and they have become generic. Statin is capturing 30% of the world API market and currently 25% of the revenue is being generated from the statins .

Business Verticals: Growth Accelerators:

Company has shaped its business in to five key growth verticals to deliver sustainable long term value for patients, partners, and healthcare systems across the globe and they are given as follows.

Small Molecules: This segment is driven by Active Pharmaceutical Ingredients business is reaching at its inflection point. Biocon is now seeking to enter in to the next phase of growth by front ending this business through dossiers, ANDAs and 505 (b)(2) filings.

Biosimilars: Biocon is on the rapid growth of development, regulatory and clinical expertise along with the world class manufacturing capabilities. Biocon is working on the cost reduction and high innovation of drugs. Biocon has begun penetrating in other emerging markets with rh-insulin, Insulin Analogs and Monoclonal Antibodies (MAbs).

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 5 of 13

Branded Formulations: This segment is strong growth driver for the company and considerable value builder for brand Biocon. The Indian pharmaceuticals industry is expected to attain a size of over US$ 50 billion by 2015. Novel Molecules: Biocon has the capability to bring path breaking proprietary products to the global markets. Company is planning to take its most promising novel molecules to proof-of-concept before exploring it to partnerships. Biocon’s two late stage candidates include an Oral Insulin molecule (IN-105) and Itolizumab (T1h) – an anti-CD6 MAb for autoimmune conditions which has completed a phase III psoriasis trial. Biocon with its partnered program Amylin Pharmaceuticals for AC165198, a Phybrid which has dual pharmacology addressing diabetes and obesity, currently in phase I clinical trials under a US FDA IND.

Integrated Research Service: Biocon has two research centers that is Syngene & Clinigene and they built remarkable integrated contract research capabilities to support discovery and development for both the small and large molecules. FY 12 has been one of the strongest years in Syngene’s history. Company is investing in to strengthening its scientific team. So we do expect to provide company to attract world wide customers. Syngene has recently established The Abbott Nutrition R&D center and company is also expecting to enroll other dedicated services in future as per demand.

Investor Rationale:

1. Branded Formulation is expected to drive growth: Biocon branded formulations business has

grown rapidly over the period of time, offering a large basket of products for chronic disease. In India, diabetology division has seen growth of 38%, which pushed Biocon to the no 4th position in the Insulin segment. Biocon INSUGEN ranked no. 3 in the 40 IU Insulin space.

100 IU Insulin 17%Glargine vials 85%

Biocon's Volune Market Share

Company Value gr y-o-y (%)Biocon 50%Sanofi Aventis 29%Novo Nordisk 26%

Fastest Growing Insulin Company

8

28.6

9.6

45.6

0

8

16

24

32

40

48

Developed Markets Emerging Market

Diabetic Population

Diabetic Population (2011) Diabetic Population (2030)

Source: Company presentation

Biocon is the fastest growing company with the market share of 50% in Insulin segment leaving behind the Sanofi Aventis and Novo Nordisk competitor with the market share of 29% and 26% respectively. In FY12, branded formulation grew by 39% on y-o-y basis; Biocon recently launched their first reusable insulin delivery device which has been showing sustainable value in the company’s basket of insulin therapies in the market. Company has 1700 MRs. We expect company to become the major player in these therapeutic segments.

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 6 of 13

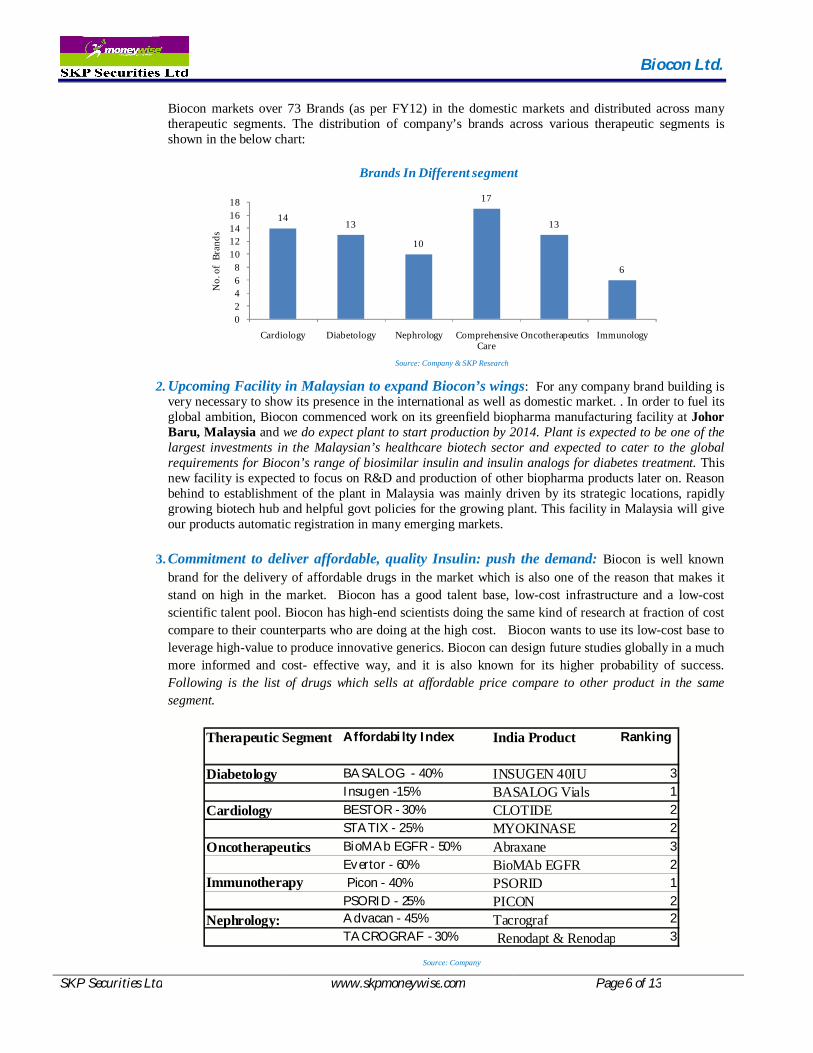

Biocon markets over 73 Brands (as per FY12) in the domestic markets and distributed across many therapeutic segments. The distribution of company’s brands across various therapeutic segments is shown in the below chart:

1413

10

17

13

6

02468

1012141618

Cardiology Diabetology Nephrology Comprehensive Care

Oncotherapeutics Immunology

No.

of

Bran

ds

Brands In Different segment

Source: Company & SKP Research

2. Upcoming Facility in Malaysian to expand Biocon’s wings: For any company brand building is very necessary to show its presence in the international as well as domestic market. . In order to fuel its global ambition, Biocon commenced work on its greenfield biopharma manufacturing facility at Johor Baru, Malaysia and we do expect plant to start production by 2014. Plant is expected to be one of the largest investments in the Malaysian’s healthcare biotech sector and expected to cater to the global requirements for Biocon’s range of biosimilar insulin and insulin analogs for diabetes treatment. This new facility is expected to focus on R&D and production of other biopharma products later on. Reason behind to establishment of the plant in Malaysia was mainly driven by its strategic locations, rapidly growing biotech hub and helpful govt policies for the growing plant. This facility in Malaysia will give our products automatic registration in many emerging markets.

3. Commitment to deliver affordable, quality Insulin: push the demand: Biocon is well known

brand for the delivery of affordable drugs in the market which is also one of the reason that makes it stand on high in the market. Biocon has a good talent base, low-cost infrastructure and a low-cost scientific talent pool. Biocon has high-end scientists doing the same kind of research at fraction of cost compare to their counterparts who are doing at the high cost. Biocon wants to use its low-cost base to leverage high-value to produce innovative generics. Biocon can design future studies globally in a much more informed and cost- effective way, and it is also known for its higher probability of success. Following is the list of drugs which sells at affordable price compare to other product in the same segment.

Therapeutic Segment Affordabilty Index India Product Ranking

Diabetology BASALOG - 40% INSUGEN 40IU 3Insugen -15% BASALOG Vials 1

Cardiology BESTOR - 30% CLOTIDE 2STATIX - 25% MYOKINASE 2

Oncotherapeutics BioMAb EGFR - 50% Abraxane 3Evertor - 60% BioMAb EGFR 2

Immunotherapy Picon - 40% PSORID 1PSORID - 25% PICON 2

Nephrology: Advacan - 45% Tacrograf 2TACROGRAF - 30% Renodapt & Renodapt S 3

Source: Company

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 7 of 13

4. Insulin demand is expected to increase on the broader level: Biocon has strong presence in anti-

diabetic segment. The company markets the world first recombinant human insulin under the brand name INSUGEN. Biocon was the first to launch the insulin the market. Biocon is expecting to launch Rh insulin in FY14 in the regulated market as they have completed phase III trial in EU. Biocon has 30+ registration in the emerging market and have tie ups with the strong regional partners in major markets including Japan & China. For the Glargine company completed phase 1 trial globally.In Fy10 market size for the insulin was USD 15~Bn and it went up to USD 17~bn in Fy12, globally .

32%Glargine

23% Aspart

20% rh insulin

14% Lispro

9% Detemir

2% Gluisine

Market breakup by Molecule

4%

43%

17%23%

13%

0%

10%

20%

30%

40%

50%

rh Insulin Glargine Lispro Aspart Others

Growth Contribution by molecles

Growth Contribution by molecles

Source: Company & SKP Research

47%

10%

25%

8%

2% 5% 3%

Break-up of patient in Therapeutic Areas

Diabetology

Oncology

Bone & Metabolic dis

Immunology

Cardiology

Dermatology

Others

Source: Company & SKP Research

Diabetic prevalence expected to go up from current level of 8% to 10% in FY30 (as per international diabetic Atlas 2011). As per research diabetes prevalence expected to rapidly increase in Africa, MENA and Urban Areas of BRIC-TM. As we know because of low penetration of medial facility as well as medicine in the rural as well as metro half of the the diabetic population remains undiagnosed. To garner the increasing opportunity, Biocon is working on increasing its penetration in the rural as well as metro areas so company can cater its increasing demand now and in future market. Company has developed relationships with regional partners for the insulin portfolio in certain markets like Latin America, Middle East and Africa.

5. Spreading its arm in the regulated market through different partnership:

Partnership with Mylan: Monoclonal Antibodies (MAbs): This partnership is exclusively for the development and commercialization of complex biosimilar. It combines Biocon’s R&D and manufacturing prowess of biologics with the Mylan’s regulatory & commercialization capabilities in the US & Europe. Market value of the portfolio in 2011 was ~33 Bn USD . Biocon and Mylan will share the development and capital costs and Mylan will have exclusive commercialization rights in the regulated

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 8 of 13

markets; and profits to be shared between them. Biocon and Mylan to have co-exclusive commercialization rights in other markets. Partnership with OPTIMER: First-in-class-Anti-infective FIDAXOMICIN: This partnership is the extension of prior relationship with the OPTIMER where Biocon assisted optimer with product development and now they got in to the exclusive agreement for the manufacture & supply of Fidaxomicin API : DIFICIDTM tablets. It combines Biocon’s R&D and manufacturing prowess of novel biologics with optimer’s proprietary molecule technology. This will be launch in US & select East European nations in first phase; with the alliances established for Japan & Brazil. Partnership with Abbott Nutrition: Maternal & Child nutrition: This partnership combines Syngene’s integrated drug development prowess with Abbott’s capabilities in maternal & child nutrition. This collaboration will focus on the development of affordable nutrition products for maternal and child nutrition and diabetes care. This product is being developed for the Indian market, are meal compliments for diabetes and pre-diabetics. This is the long term contract commencing more than 50 scientists.

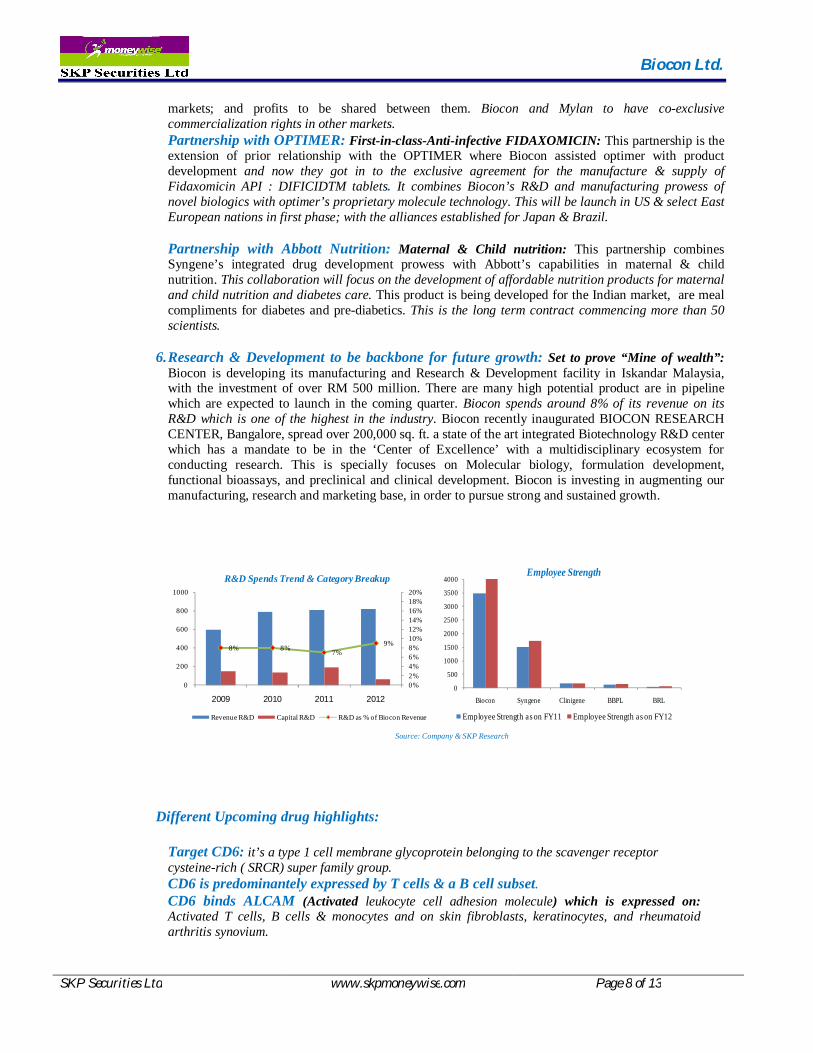

6. Research & Development to be backbone for future growth: Set to prove “Mine of wealth”:

Biocon is developing its manufacturing and Research & Development facility in Iskandar Malaysia, with the investment of over RM 500 million. There are many high potential product are in pipeline which are expected to launch in the coming quarter. Biocon spends around 8% of its revenue on its R&D which is one of the highest in the industry. Biocon recently inaugurated BIOCON RESEARCH CENTER, Bangalore, spread over 200,000 sq. ft. a state of the art integrated Biotechnology R&D center which has a mandate to be in the ‘Center of Excellence’ with a multidisciplinary ecosystem for conducting research. This is specially focuses on Molecular biology, formulation development, functional bioassays, and preclinical and clinical development. Biocon is investing in augmenting our manufacturing, research and marketing base, in order to pursue strong and sustained growth.

8% 8% 7%9%

0%2%4%6%8%10%12%14%16%18%20%

0

200

400

600

800

1000

2009 2010 2011 2012

R&D Spends Trend & Category Breakup

Revenue R&D Capital R&D R&D as % of Biocon Revenue

0

500

1000

1500

2000

2500

3000

3500

4000

Biocon Syngene Clinigene BBPL BRL

Employee Strength

Employee Strength as on FY11 Employee Strength as on FY12

Source: Company & SKP Research

Different Upcoming drug highlights:

Target CD6: it’s a type 1 cell membrane glycoprotein belonging to the scavenger receptor cysteine-rich ( SRCR) super family group. CD6 is predominantely expressed by T cells & a B cell subset. CD6 binds ALCAM (Activated leukocyte cell adhesion molecule) which is expressed on: Activated T cells, B cells & monocytes and on skin fibroblasts, keratinocytes, and rheumatoid arthritis synovium.

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 9 of 13

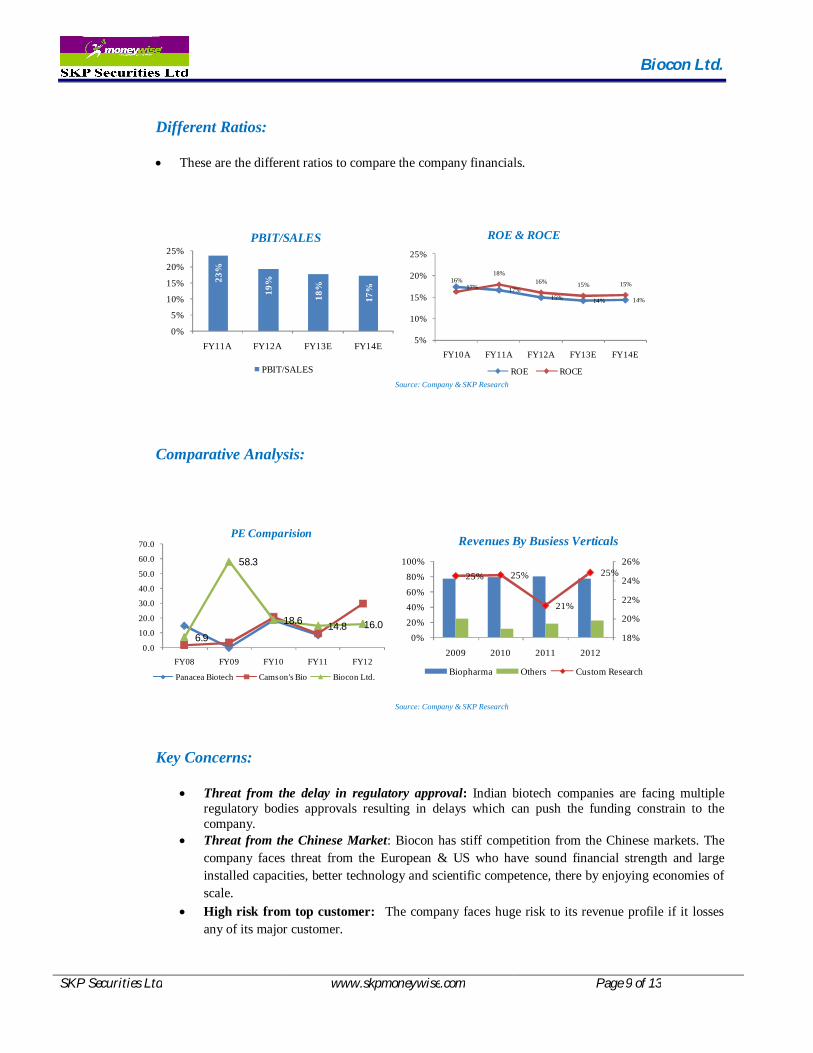

Different Ratios:

These are the different ratios to compare the company financials.

23%

19%

18%

17%

0%

5%

10%

15%

20%

25%

FY11A FY12A FY13E FY14E

PBIT/SALES

PBIT/SALES

17% 17%15% 14% 14%

16%18%

16% 15% 15%

5%

10%

15%

20%

25%

FY10A FY11A FY12A FY13E FY14E

ROE & ROCE

ROE ROCE Source: Company & SKP Research

Comparative Analysis:

6.9

58.3

18.6 14.8 16.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY08 FY09 FY10 FY11 FY12

PE Comparision

Panacea Biotech Camson's Bio Biocon Ltd.

25% 25%

21%

25%

18%

20%

22%

24%

26%

0%

20%

40%60%

80%

100%

2009 2010 2011 2012

Revenues By Busiess Verticals

Biopharma Others Custom Research

Source: Company & SKP Research

Key Concerns:

Threat from the delay in regulatory approval: Indian biotech companies are facing multiple regulatory bodies approvals resulting in delays which can push the funding constrain to the company.

Threat from the Chinese Market: Biocon has stiff competition from the Chinese markets. The company faces threat from the European & US who have sound financial strength and large installed capacities, better technology and scientific competence, there by enjoying economies of scale.

High risk from top customer: The company faces huge risk to its revenue profile if it losses any of its major customer.

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 10 of 13

Financial Outlook:

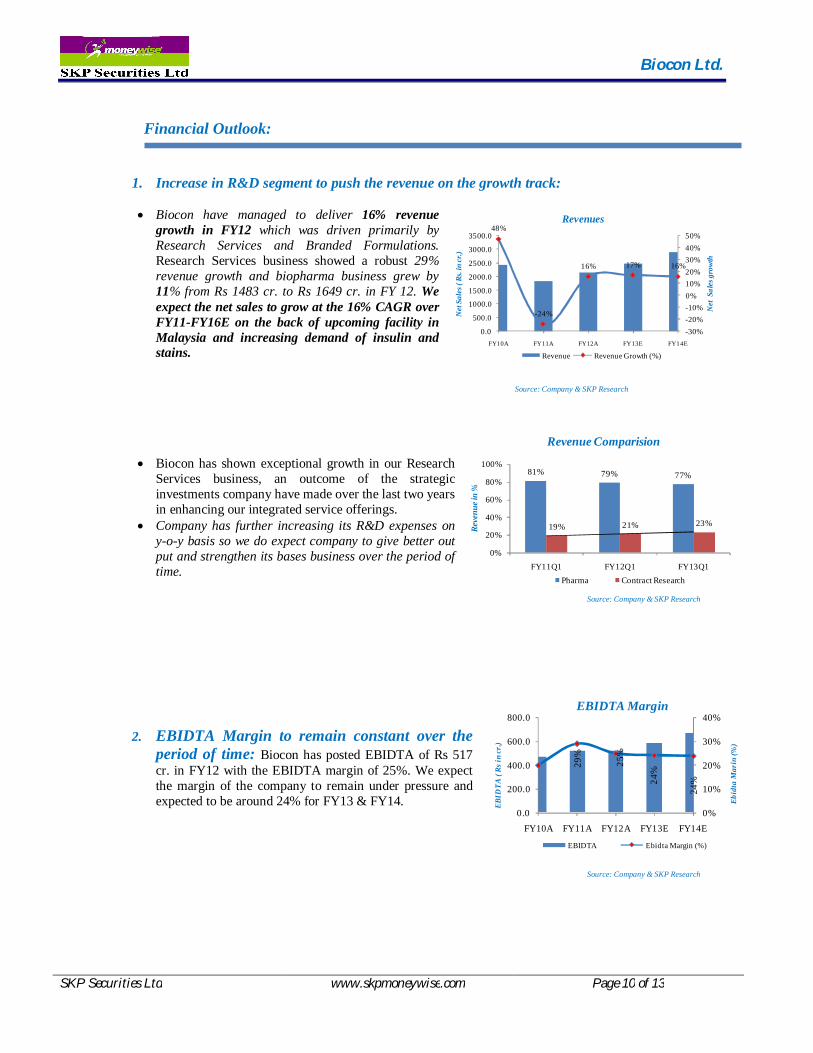

1. Increase in R&D segment to push the revenue on the growth track:

Biocon have managed to deliver 16% revenue

growth in FY12 which was driven primarily by Research Services and Branded Formulations. Research Services business showed a robust 29% revenue growth and biopharma business grew by 11% from Rs 1483 cr. to Rs 1649 cr. in FY 12. We expect the net sales to grow at the 16% CAGR over FY11-FY16E on the back of upcoming facility in Malaysia and increasing demand of insulin and stains.

Source: Company & SKP Research

Biocon has shown exceptional growth in our Research Services business, an outcome of the strategic investments company have made over the last two years in enhancing our integrated service offerings.

Company has further increasing its R&D expenses on y-o-y basis so we do expect company to give better out put and strengthen its bases business over the period of time.

Source: Company & SKP Research

2. EBIDTA Margin to remain constant over the period of time: Biocon has posted EBIDTA of Rs 517 cr. in FY12 with the EBIDTA margin of 25%. We expect the margin of the company to remain under pressure and expected to be around 24% for FY13 & FY14.

Source: Company & SKP Research

Page 11 of 15

48%

-24%

16% 17% 16%

-30%-20%-10%0%10%20%30%40%50%

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

FY10A FY11A FY12A FY13E FY14E

Net

Sal

es g

rowt

h

Net

Sal

es (

Rs. i

n cr

.)

Revenues

Revenue Revenue Growth (%)

29%

25%

24%

24%

0%

10%

20%

30%

40%

0.0

200.0

400.0

600.0

800.0

FY10A FY11A FY12A FY13E FY14E

Ebid

ta M

arin

(%)

EBID

TA (

Rs in

cr.)

EBIDTA Margin

EBIDTA Ebidta Margin (%)

81% 79% 77%

19% 21% 23%

0%

20%

40%

60%

80%

100%

FY11Q1 FY12Q1 FY13Q1

Reve

nue i

n %

Revenue Comparision

Pharma Contract Research

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 11 of 13

Valuation:

We expect Biocon to report healthy growth in the top line on the back of increasing expenditure on R&D segment and increasing demand of affordable drugs in the market. At current market price of Rs 273, Stock is trading at an EV/EBIDTA of 10.2x & 9.5x for FY13E and FY14E respectively.

010002000300040005000600070008000

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

One Year Forward looking EV/EBIDTA Band

3x 6x 9x 12x 15x EV

Source: Company & SKP Research

We recommend BUY rating on the stock with a target of Rs. 338 (23%UPSIDE) at the EV/EBIDTA of

9.5x on FY13E earning over the period of 18month.

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 12 of 13

Financial Performance:

` FY11 FY12 FY13E FY14E Cash Flow Statements FY12 FY13E FY14EFinancials (In Cr.)Net operating income 1,806 2,087 2,420 2,808 PBT (less exceptional items) 393 413 465 Operating Expenditure 1,285 1,569 1,838 2,140 Add: Dep, int. & Other Exp. 174 208 248 EBIDTA 522 517 582 668 Op. Profit before cash flow changes 492 746 598 Depreciation 152 174 208 248 Direct Tax paid (5) (58) (65)EBIT 422 405 428 481 Net cash from Operating Activities 492 746 598 Interest 23 12 15 17 Cash flow from Invstment Activities (64) (448) (448)Other Income 52 62 53 62 Net Cash from Financing Activities (156) (122) (111)PBT 398 393 413 465 Opening Cash Balance 124 523 698 Tax 59 54 58 65 Net (dec.)/inc. in cash (A+B+C) 272 175 38 Adj PAT 367 342 358 403 Closing Cash Balance 523 698 737 EPS 19 17 18 20

Balance Sheet FY11 FY12 FY13E FY14E Financial Ratios FY12 FY13E FY14E

Equity Capital 100 100 100 100 Valuation Ratios(x)Reserves & Surplus 1,936 2,168 2,407 2,691 P/E 16.0 15.2 13.6Minor ity Interest 38 4 4 4 P/CEPS 53.2 48.5 42.1Shareholder 's Fund 2,074 2,272 2,511 2,795 P/BV (x) 12.0 10.9 9.8Total Debt 313 257 299 330 EV/EBIDTA 10.2 8.9 7.6Short term borrowing 247 187 240 270 PBIT/Sales 19% 18% 17%Long term bor rowing 66 70 59 60 Deffered Tax Liabiity 50 - - - Market cap/Sales (x) 2.62 2.26 1.94Oth. Long term liabilities 339 583 600 650 EV/Sales 2.49 2.09 1.80Sources of funds 2,776 3,112 3,410 3,775 Net Fixed Assets 1,177 1,241 1,319 1,519 Capital WIP 179 286 448 448 Earning Ratios (%)Investments 460 556 629 730 EBIDTAM 24.8% 24.1% 23.8%Intangible Assets 138 123 123 123 Total Current Assets 1,607 1,728 1,956 2,180 Return Ratios (%)-Inventory 414 378 436 505 ROCE 16.0% 15.2% 15.4%-Debtors 495 491 581 674 ROE 14.9% 14.2% 14.3%-Cash & Bank Balances 442 523 698 737 -Loans & Advances 179 274 145 168 B/S RatiosOther assets 78 61 96 96 Debtors Days 86.2 80.8 81.6 Total Current Liabilities 786 823 1,066 1,226 Creditors Days 56.2 60.8 64.6 Net Current Assets 821 905 890 955 Uses of Funds 2,775 3,112 3,410 3,775

Biocon Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 13 of 13

The above analysis and data are based on last available prices and not official closing rates. SKP Research is also available on Bloomberg, Thomson First Call &InvestextMyiris, Moneycontrol, Tickerplant and ISI Securities. DISCLAIMER: This document has been issued by SKP Securities Ltd (SKP), a stock broker registered with and regulated by Securities & Exchange Board of India, for the information of its clients/potential clients and business associates/affiliates only and is for private circulation only, disseminated and available electronically and in printed form. Additional information on recommended securities may be made available on request. This document is supplied to you solely for your information and no matter contained herein may be reproduced, reprinted, sold, copied in whole or in part, redistributed or passed on, directly or indirectly, to any other person for any purpose, in India or into any other country without prior written consent of SKP. The distribution of this document in other jurisdictions may be strictly restricted and/ or prohibited by law, and persons into whose possession this document comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition. If you are dissatisfied with the contents of this complimentary document or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using the document and SKP shall not be responsible and/ or liable in any manner. Neither this document nor the information or any opinion expressed therein should be construed as an investment advice or offer to anybody to acquire, subscribe, purchase, sell, dispose of, retain any securities or derivatives related to such securities or an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an official endorsement of any investment. Any recommendation or view or opinion expressed on investments in this document is not intended to constitute investment advice and should not be intended or treated as a substitute for necessary review or validation or any professional advice. The views expressed in this document are those of the analyst which are subject to change and do not represent to be an authority on the subject. SKP may or may not subscribe to any and/ or all the views expressed herein. It is the endeavor of SKP to ensure that the analyst(s) use current, reliable, comprehensive information and obtain such information from sources, which the analyst(s) believes to be reliable. However, such information may not have been independently verified by SKP or the analyst(s). The information, opinions and views contained within this document are based upon publicly available information, considered reliable at the time of publication, which are subject to change from time to time without any prior notice. The Document may be updated anytime without any prior notice to anybody. SKP makes no guarantee, representation or warranty, express or implied; and accepts no responsibility or liability as to the accuracy or completeness or correctness of the information in this Report. SKP, its Directors, affiliates and employees do not accept any liability whatsoever, direct or indirect, that may arise from the use of the information or recommendations herein. Please note that past performance is not necessarily a guide to evaluate future performance. SKP or its affiliates, may, from time to time render advisory and other services to companies being referred to in thiss document and receive compensation for the same. SKP and/or its affiliates, directors and employees may trade for their own account or may also perform or seek to perform investment banking or underwriting services for or relating to those companies and may also be represented in the supervisory board or on any other committee of those companies or may sell or buy any securities or make any investment, which may be contrary to or inconsistent with this document. This document should be read and relied upon at the sole discretion and risk of the reader. The value of any investment made at your discretion based on this document or income there from may be affected by changes in economic, financial and/ or political factors and may go down as well as up and you may not get back the full or the expected amount invested. Some securities and/ or investments involve substantial risk and are not suitable for all investors. Neither SKP nor its affiliates or their directors, employees, agents or representatives/associates, shall be responsible or liable in any manner, directly or indirectly, for information, views or opinions expressed in this document or the contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the document or inability to use or access our service or this document or for any loss or damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits or any loss or damage that may arise from or in connection with the use of or reliance on this document or inability to use or access our service or this document.

SKP Securities Ltd Contacts Research Sales Mumbai Kolkata Mumbai Kolkata Phone 022 2281 9012 033 4007 7000 022 2281 1015 033 4007 7400 Fax 022 2283 0932 033 4007 7007 022 2283 0932 033 4007 7007 E-mail researchmum@skpmoneywis

e.com [email protected]

Member: NSE BSE NSDL CDSL NCDEX* MCX* MCX-SX FPSB*Group Entities INB/INF: 230707532, BSE INB: 010707538, CDSL IN-DP-CDSL-132-2000, DPID: 021800, NSDL IN-DP-NSDL: 222-2001, DP ID: IN302646, ARN: 0006, NCDEX: 00715, MCX: 31705, MCX-SX: INE 260707532

Equities Derivatives Commodities Currency Demat Services Mutual Funds Insurance Financial Planning Online Trading