Embed Size (px)

DESCRIPTION

good explanantion of options

Citation preview

Section 15: Introduction to Financial Derivatives,Forward and Future Contracts

ACTS 4308

Natalia A. Humphreys

1 / 40

Acknowledgement

This work is based on the material in S. Broverman Study Guidefor SOA Exam FM/CAS Exam 2, 2011 Edition and on the notes

prepared by Professor Ryan Gill at the University of Louisville, KY.

Additionally, Study Manual for Exam FM/Exam 2, ASM 2009,10th Edition by Harold Cherry and Rick Gorvett was used to

present the material in this section.

2 / 40

Financial Derivatives

I Financial derivative: financial instrument related to someother asset and whose value is derived from that asset

I Purposes of financial derivatives: risk management (e.g.,form of insurance); speculation; reduction of transactioncosts; circumventing regulatory limitations, accountingregulations, and taxes

I Diversifiable risks: risks unrelated to other risks; can beshared through markets

3 / 40

Financial Derivatives (cont.)

I Over-the-counter (OTC) trading: trading of financialinstruments (such as forwards and swaps) made directlybetween two parties (in contrast with exchange trading ofstocks or futures)

I Market maker: firm that is ready to buy and sell a particularasset

I Credit risk: possibility of failure of payment or delivery oncontract expiration date

I Bid price: price at which an investor can sell the asset

I Ask price: price at which an investor can buy the asset

I Bid-ask spread = ask price− bid price: compensation to themarket-makers for their risk and for keeping the market liquid

4 / 40

Payoff, Profit

I The payoff at time T is the value of an investment at time T .

I The profit from time 0 to time T is the difference betweenthe payoff at time T and the amount invested at time 0.

5 / 40

Positions in the Assets

When you buy a stock (or any other asset), you are said to have along position in the stock. You enter into this position if youbelieve the stock will go up in the future.

Short position - the opposite of a long position. You enter intothis position if you believe the stock will go down in the future.

6 / 40

Essence of a short sale

I You borrow a stock whose price you expect to decline

I You immediately sell the stock and receive the current price

I At a later date, you buy the stock to repay the lender

Short-selling is a dangerous game. There is theoretically no limit toyour losses.

7 / 40

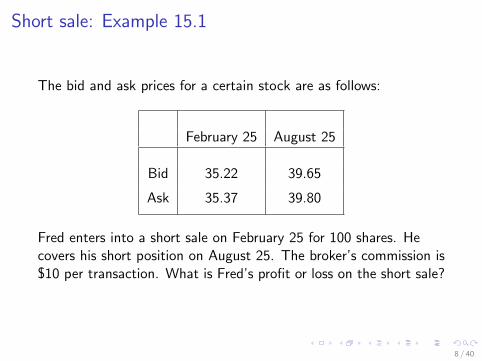

Short sale: Example 15.1

The bid and ask prices for a certain stock are as follows:

February 25 August 25

Bid 35.22 39.65

Ask 35.37 39.80

Fred enters into a short sale on February 25 for 100 shares. Hecovers his short position on August 25. The broker’s commission is$10 per transaction. What is Fred’s profit or loss on the short sale?

8 / 40

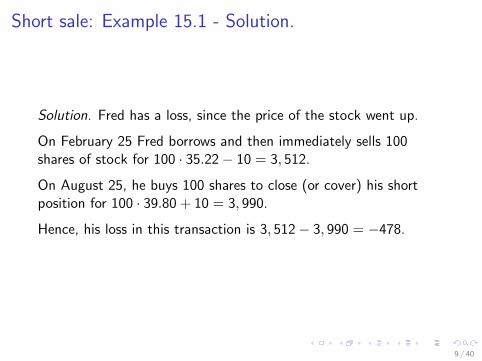

Short sale: Example 15.1 - Solution.

Solution. Fred has a loss, since the price of the stock went up.

On February 25 Fred borrows and then immediately sells 100shares of stock for 100 · 35.22− 10 = 3, 512.

On August 25, he buys 100 shares to close (or cover) his shortposition for 100 · 39.80 + 10 = 3, 990.

Hence, his loss in this transaction is 3, 512− 3, 990 = −478.

9 / 40

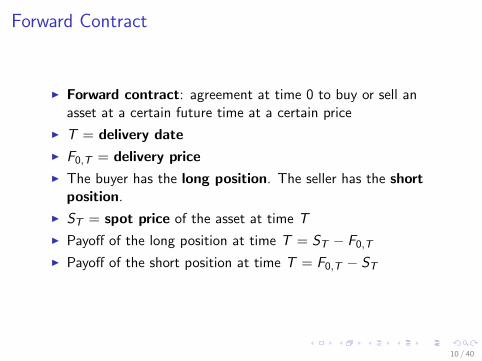

Forward Contract

I Forward contract: agreement at time 0 to buy or sell anasset at a certain future time at a certain price

I T = delivery date

I F0,T = delivery price

I The buyer has the long position. The seller has the shortposition.

I ST = spot price of the asset at time T

I Payoff of the long position at time T = ST − F0,TI Payoff of the short position at time T = F0,T − ST

10 / 40

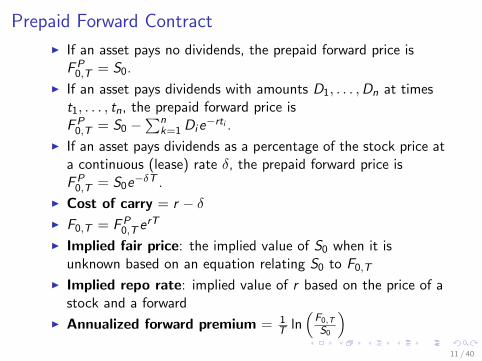

Prepaid Forward Contract

I If an asset pays no dividends, the prepaid forward price isFP0,T = S0.

I If an asset pays dividends with amounts D1, . . . ,Dn at timest1, . . . , tn, the prepaid forward price isFP0,T = S0 −

∑nk=1Die

−rti .

I If an asset pays dividends as a percentage of the stock price ata continuous (lease) rate δ, the prepaid forward price isFP0,T = S0e

−δT .

I Cost of carry = r − δI F0,T = FP

0,T erT

I Implied fair price: the implied value of S0 when it isunknown based on an equation relating S0 to F0,T

I Implied repo rate: implied value of r based on the price of astock and a forward

I Annualized forward premium = 1T ln

(F0,T

S0

)11 / 40

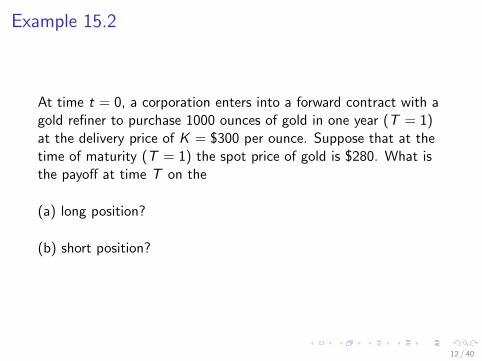

Example 15.2

At time t = 0, a corporation enters into a forward contract with agold refiner to purchase 1000 ounces of gold in one year (T = 1)at the delivery price of K = $300 per ounce. Suppose that at thetime of maturity (T = 1) the spot price of gold is $280. What isthe payoff at time T on the

(a) long position?

(b) short position?

12 / 40

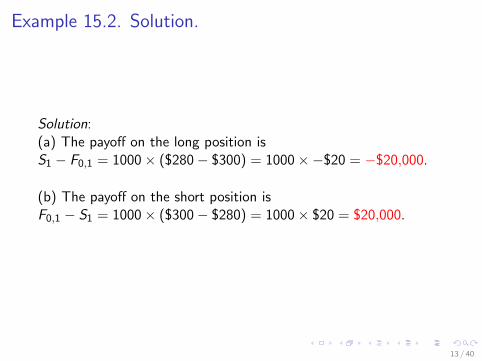

Example 15.2. Solution.

Solution:(a) The payoff on the long position isS1 − F0,1 = 1000× ($280− $300) = 1000×−$20 = −$20,000.

(b) The payoff on the short position isF0,1 − S1 = 1000× ($300− $280) = 1000× $20 = $20,000.

13 / 40

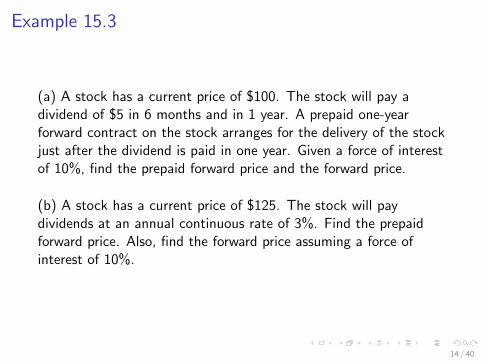

Example 15.3

(a) A stock has a current price of $100. The stock will pay adividend of $5 in 6 months and in 1 year. A prepaid one-yearforward contract on the stock arranges for the delivery of the stockjust after the dividend is paid in one year. Given a force of interestof 10%, find the prepaid forward price and the forward price.

(b) A stock has a current price of $125. The stock will paydividends at an annual continuous rate of 3%. Find the prepaidforward price. Also, find the forward price assuming a force ofinterest of 10%.

14 / 40

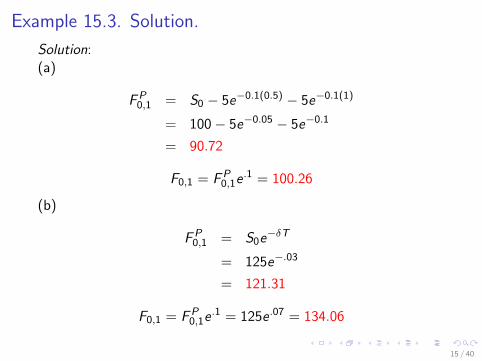

Example 15.3. Solution.

Solution:(a)

FP0,1 = S0 − 5e−0.1(0.5) − 5e−0.1(1)

= 100− 5e−0.05 − 5e−0.1

= 90.72

F0,1 = FP0,1e

.1 = 100.26

(b)

FP0,1 = S0e

−δT

= 125e−.03

= 121.31

F0,1 = FP0,1e

.1 = 125e .07 = 134.06

15 / 40

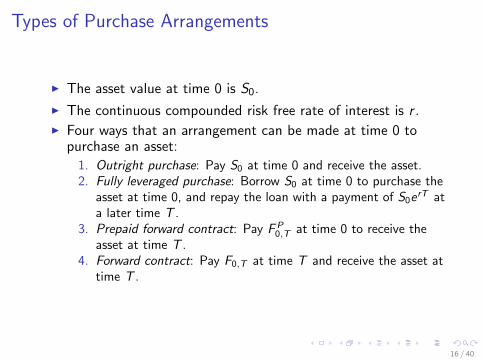

Types of Purchase Arrangements

I The asset value at time 0 is S0.

I The continuous compounded risk free rate of interest is r .I Four ways that an arrangement can be made at time 0 to

purchase an asset:

1. Outright purchase: Pay S0 at time 0 and receive the asset.2. Fully leveraged purchase: Borrow S0 at time 0 to purchase the

asset at time 0, and repay the loan with a payment of S0erT at

a later time T .3. Prepaid forward contract: Pay FP

0,T at time 0 to receive theasset at time T .

4. Forward contract: Pay F0,T at time T and receive the asset attime T .

16 / 40

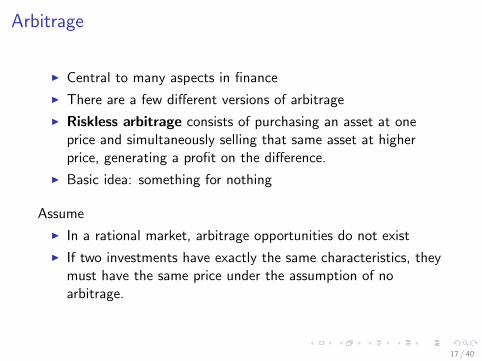

Arbitrage

I Central to many aspects in finance

I There are a few different versions of arbitrage

I Riskless arbitrage consists of purchasing an asset at oneprice and simultaneously selling that same asset at higherprice, generating a profit on the difference.

I Basic idea: something for nothing

Assume

I In a rational market, arbitrage opportunities do not exist

I If two investments have exactly the same characteristics, theymust have the same price under the assumption of noarbitrage.

17 / 40

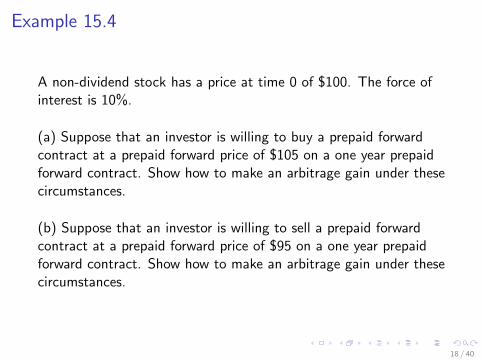

Example 15.4

A non-dividend stock has a price at time 0 of $100. The force ofinterest is 10%.

(a) Suppose that an investor is willing to buy a prepaid forwardcontract at a prepaid forward price of $105 on a one year prepaidforward contract. Show how to make an arbitrage gain under thesecircumstances.

(b) Suppose that an investor is willing to sell a prepaid forwardcontract at a prepaid forward price of $95 on a one year prepaidforward contract. Show how to make an arbitrage gain under thesecircumstances.

18 / 40

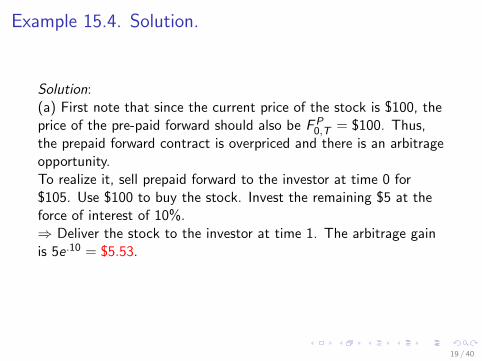

Example 15.4. Solution.

Solution:(a) First note that since the current price of the stock is $100, theprice of the pre-paid forward should also be FP

0,T = $100. Thus,the prepaid forward contract is overpriced and there is an arbitrageopportunity.To realize it, sell prepaid forward to the investor at time 0 for$105. Use $100 to buy the stock. Invest the remaining $5 at theforce of interest of 10%.⇒ Deliver the stock to the investor at time 1. The arbitrage gainis 5e .10 = $5.53.

19 / 40

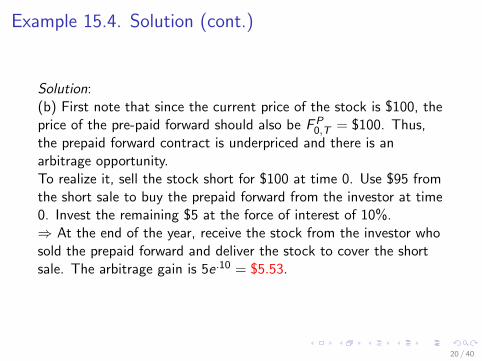

Example 15.4. Solution (cont.)

Solution:(b) First note that since the current price of the stock is $100, theprice of the pre-paid forward should also be FP

0,T = $100. Thus,the prepaid forward contract is underpriced and there is anarbitrage opportunity.To realize it, sell the stock short for $100 at time 0. Use $95 fromthe short sale to buy the prepaid forward from the investor at time0. Invest the remaining $5 at the force of interest of 10%.⇒ At the end of the year, receive the stock from the investor whosold the prepaid forward and deliver the stock to cover the shortsale. The arbitrage gain is 5e .10 = $5.53.

20 / 40

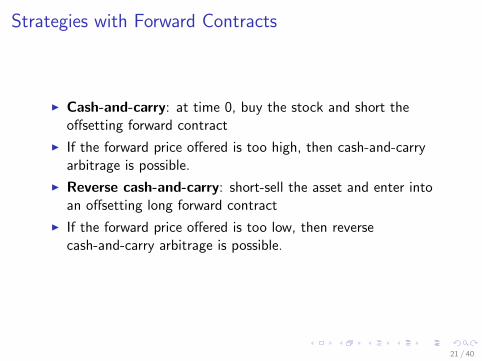

Strategies with Forward Contracts

I Cash-and-carry: at time 0, buy the stock and short theoffsetting forward contract

I If the forward price offered is too high, then cash-and-carryarbitrage is possible.

I Reverse cash-and-carry: short-sell the asset and enter intoan offsetting long forward contract

I If the forward price offered is too low, then reversecash-and-carry arbitrage is possible.

21 / 40

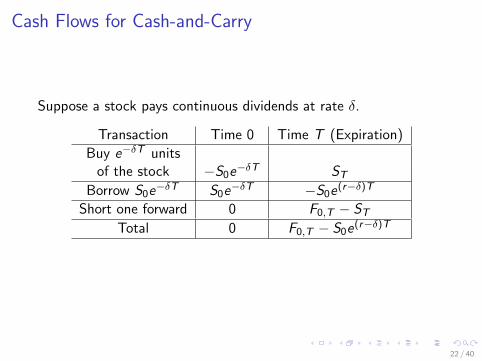

Cash Flows for Cash-and-Carry

Suppose a stock pays continuous dividends at rate δ.

Transaction Time 0 Time T (Expiration)

Buy e−δT unitsof the stock −S0e−δT ST

Borrow S0e−δT S0e

−δT −S0e(r−δ)TShort one forward 0 F0,T − ST

Total 0 F0,T − S0e(r−δ)T

22 / 40

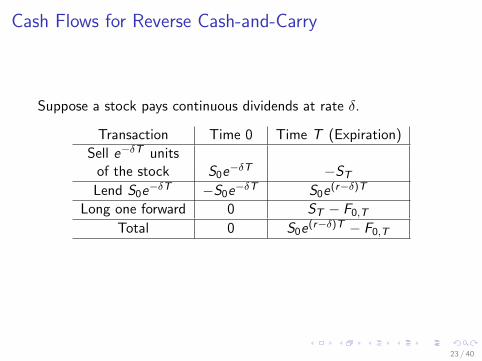

Cash Flows for Reverse Cash-and-Carry

Suppose a stock pays continuous dividends at rate δ.

Transaction Time 0 Time T (Expiration)

Sell e−δT unitsof the stock S0e

−δT −STLend S0e

−δT −S0e−δT S0e(r−δ)T

Long one forward 0 ST − F0,TTotal 0 S0e

(r−δ)T − F0,T

23 / 40

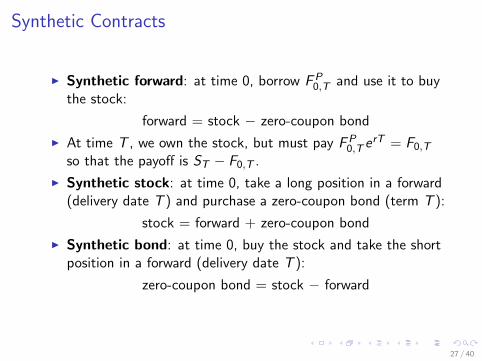

Synthetic Contracts

If two financial investments result in the same payoffs, then underthe assumption of no arbitrage they would have the same value orprice.For some types of financial contracts it is possible to replicate thepayoffs by combining alternative financial instruments.

24 / 40

Example 15.5

A stock which does not pay dividends is currently selling for S0.An investor borrows S0 to purchase the stock with the intention ofselling the stock in one year and repaying the loan. Suppose thatthe force of interest is r . Show that the payoff from thistransaction at the end of the year is the same as the payoff on along position on one year forward contract on the stock.

25 / 40

Example 15.5. Solution.

At the end of the year the stock is sold for amount S1 and theamount of the loan repayment is S0e

r . The payoff from thetransaction is S1 − S0e

r , which is the same as the payoff on a longposition on a one year forward contract on the stock.

26 / 40

Synthetic Contracts

I Synthetic forward: at time 0, borrow FP0,T and use it to buy

the stock:

forward = stock − zero-coupon bond

I At time T , we own the stock, but must pay FP0,T e

rT = F0,Tso that the payoff is ST − F0,T .

I Synthetic stock: at time 0, take a long position in a forward(delivery date T ) and purchase a zero-coupon bond (term T ):

stock = forward + zero-coupon bond

I Synthetic bond: at time 0, buy the stock and take the shortposition in a forward (delivery date T ):

zero-coupon bond = stock − forward

27 / 40

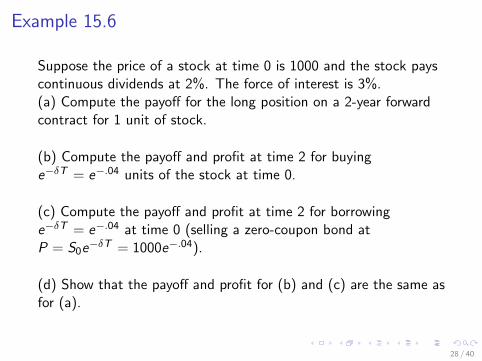

Example 15.6

Suppose the price of a stock at time 0 is 1000 and the stock payscontinuous dividends at 2%. The force of interest is 3%.(a) Compute the payoff for the long position on a 2-year forwardcontract for 1 unit of stock.

(b) Compute the payoff and profit at time 2 for buyinge−δT = e−.04 units of the stock at time 0.

(c) Compute the payoff and profit at time 2 for borrowinge−δT = e−.04 at time 0 (selling a zero-coupon bond atP = S0e

−δT = 1000e−.04).

(d) Show that the payoff and profit for (b) and (c) are the same asfor (a).

28 / 40

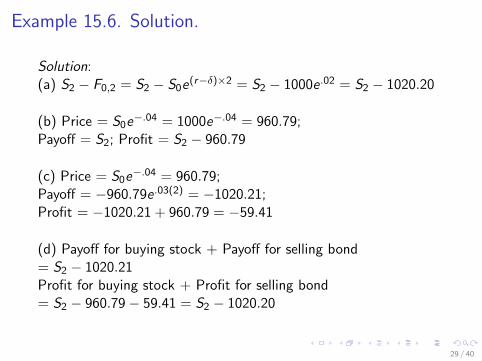

Example 15.6. Solution.

Solution:(a) S2 − F0,2 = S2 − S0e

(r−δ)×2 = S2 − 1000e .02 = S2 − 1020.20

(b) Price = S0e−.04 = 1000e−.04 = 960.79;

Payoff = S2; Profit = S2 − 960.79

(c) Price = S0e−.04 = 960.79;

Payoff = −960.79e .03(2) = −1020.21;Profit = −1020.21 + 960.79 = −59.41

(d) Payoff for buying stock + Payoff for selling bond= S2 − 1020.21Profit for buying stock + Profit for selling bond= S2 − 960.79− 59.41 = S2 − 1020.20

29 / 40

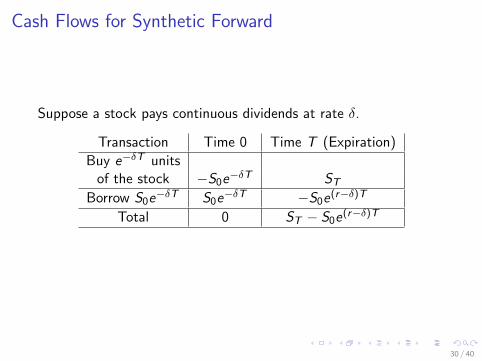

Cash Flows for Synthetic Forward

Suppose a stock pays continuous dividends at rate δ.

Transaction Time 0 Time T (Expiration)

Buy e−δT unitsof the stock −S0e−δT ST

Borrow S0e−δT S0e

−δT −S0e(r−δ)TTotal 0 ST − S0e

(r−δ)T

30 / 40

Cash Flows for Synthetic Stock

Suppose a stock pays continuous dividends at rate δ.

Transaction Time 0 Time T (Expiration)

Long one forward 0 ST − F0,TLend S0e

−δT −S0e−δT S0e(r−δ)T

Total −S0e−δT ST

31 / 40

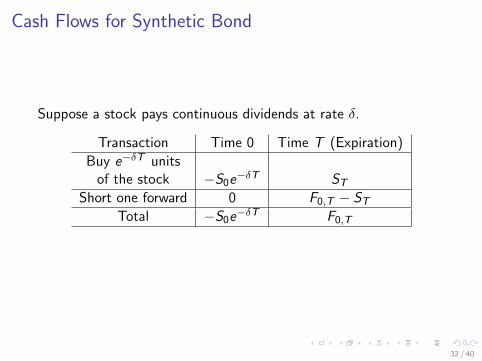

Cash Flows for Synthetic Bond

Suppose a stock pays continuous dividends at rate δ.

Transaction Time 0 Time T (Expiration)

Buy e−δT unitsof the stock −S0e−δT ST

Short one forward 0 F0,T − STTotal −S0e−δT F0,T

32 / 40

Hedging and Expected Return

I Hedging: making an investment to reduce the risk related toadverse price movements of an asset

I Reasons to hedge: taxes, avoiding bankruptcy, avoid costlyexternal financing, protect debt capacity, managerial riskaversion, non-financial risk management

I Reasons not to hedge: transaction costs, complex strategywith requires expertise, transactions must be monitored andmanaged, complicates accounting and tax reporting

I Nondiversifiable risks can be partially controlled by hedgingwith investments that are less exposed to the risks

I Expected Return (without hedging): Suppose that thereturn on an investment will be R1 with probability p1, R2

with probability p2, . . ., Rn with probability pn. Then theexpected return without hedging is

p1R1 + p2R2 + . . .+ pnRn.

33 / 40

Example 15.7

The following example is #18 in Sample Questions For DerivativesMarkets.

You are a jeweler who buys gold, which is the primary input neededfor your products. One ounce of gold can be used to produce oneunit of jewelry. Assume that the cost of all other markets isnegligible. You are able to sell each unit of jewelry for 700 plus20% of the market price of gold in one year. In one year, theactual price of gold will be in 1 of 3 possible states, correspondingto the following probability table.

34 / 40

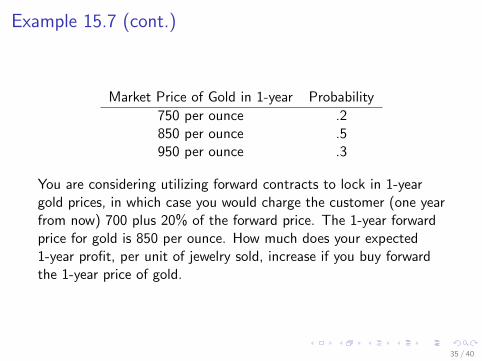

Example 15.7 (cont.)

Market Price of Gold in 1-year Probability

750 per ounce .2850 per ounce .5950 per ounce .3

You are considering utilizing forward contracts to lock in 1-yeargold prices, in which case you would charge the customer (one yearfrom now) 700 plus 20% of the forward price. The 1-year forwardprice for gold is 850 per ounce. How much does your expected1-year profit, per unit of jewelry sold, increase if you buy forwardthe 1-year price of gold.

35 / 40

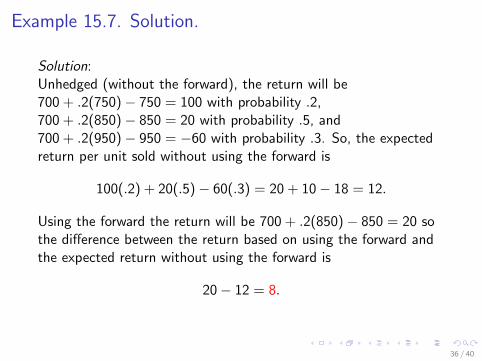

Example 15.7. Solution.

Solution:Unhedged (without the forward), the return will be700 + .2(750)− 750 = 100 with probability .2,700 + .2(850)− 850 = 20 with probability .5, and700 + .2(950)− 950 = −60 with probability .3. So, the expectedreturn per unit sold without using the forward is

100(.2) + 20(.5)− 60(.3) = 20 + 10− 18 = 12.

Using the forward the return will be 700 + .2(850)− 850 = 20 sothe difference between the return based on using the forward andthe expected return without using the forward is

20− 12 = 8.

36 / 40

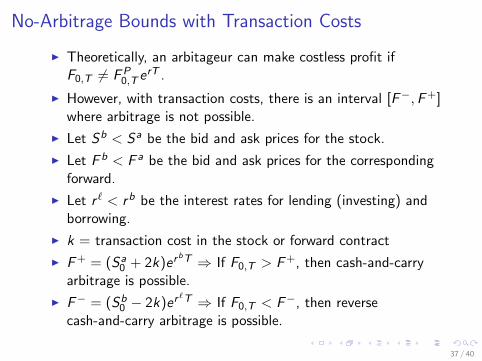

No-Arbitrage Bounds with Transaction Costs

I Theoretically, an arbitageur can make costless profit ifF0,T 6= FP

0,T erT .

I However, with transaction costs, there is an interval [F−,F+]where arbitrage is not possible.

I Let Sb < Sa be the bid and ask prices for the stock.

I Let F b < F a be the bid and ask prices for the correspondingforward.

I Let r ` < rb be the interest rates for lending (investing) andborrowing.

I k = transaction cost in the stock or forward contract

I F+ = (Sa0 + 2k)er

bT ⇒ If F0,T > F+, then cash-and-carryarbitrage is possible.

I F− = (Sb0 − 2k)er

`T ⇒ If F0,T < F−, then reversecash-and-carry arbitrage is possible.

37 / 40

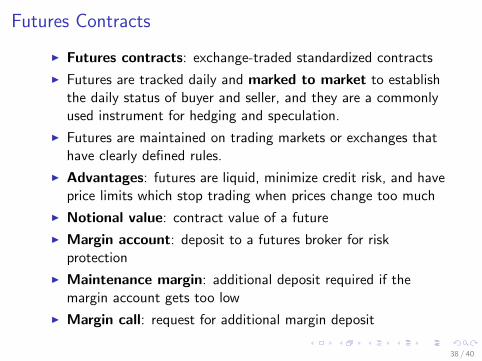

Futures Contracts

I Futures contracts: exchange-traded standardized contracts

I Futures are tracked daily and marked to market to establishthe daily status of buyer and seller, and they are a commonlyused instrument for hedging and speculation.

I Futures are maintained on trading markets or exchanges thathave clearly defined rules.

I Advantages: futures are liquid, minimize credit risk, and haveprice limits which stop trading when prices change too much

I Notional value: contract value of a future

I Margin account: deposit to a futures broker for riskprotection

I Maintenance margin: additional deposit required if themargin account gets too low

I Margin call: request for additional margin deposit

38 / 40

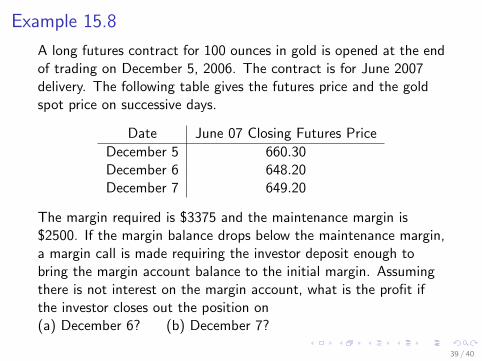

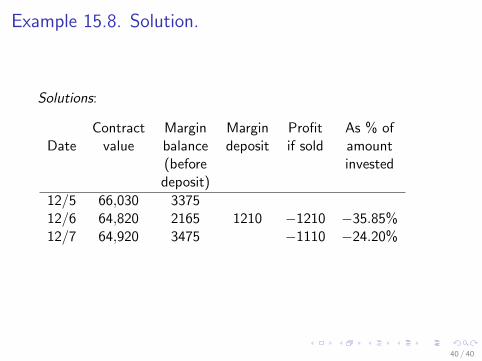

Example 15.8

A long futures contract for 100 ounces in gold is opened at the endof trading on December 5, 2006. The contract is for June 2007delivery. The following table gives the futures price and the goldspot price on successive days.

Date June 07 Closing Futures Price

December 5 660.30December 6 648.20December 7 649.20

The margin required is $3375 and the maintenance margin is$2500. If the margin balance drops below the maintenance margin,a margin call is made requiring the investor deposit enough tobring the margin account balance to the initial margin. Assumingthere is not interest on the margin account, what is the profit ifthe investor closes out the position on(a) December 6? (b) December 7?

39 / 40

Example 15.8. Solution.

Solutions:

Contract Margin Margin Profit As % ofDate value balance deposit if sold amount

(before investeddeposit)

12/5 66,030 337512/6 64,820 2165 1210 −1210 −35.85%12/7 64,920 3475 −1110 −24.20%

40 / 40