Embed Size (px)

Citation preview

1

FLORIDA AND THE CLEAN POWER PLAN: A STATE, A FEDERAL

REGULATION AND A CLIMATE SITUATION

A thesis presented by

Monique N. Cunningham-Brijbasi, MBA, CESCO

To

Doctor of Law and Policy Program

In partial fulfillment of the requirements for the degree of

Doctor of Law and Policy

College of Professional Studies

Northeastern University

Boston, Massachusetts

June 2016

2

DEDICATION

This doctoral thesis is dedicated to my children, Hayden and Zoë.

3

ACKNOWLEDGEMENTS

I wish to thank all of the air and chemical engineers who have provided guidance and

support throughout this research. Thank you to Patrick Knight at Synapse Energy Economics for

teaching me how to use Synapse’s Clean Power Plan Planning Tool for my research analysis. I

especially thank John Powell, my second reader and supervisor of four years, for always

believing in me and allowing me to harass him with a ton of questions while writing my research

proposal. After all of that, he’s still agreed to be my second reader. Your insights and guidance

have guided me through this journey and made my thesis stronger.

With deep gratitude, I acknowledge the faculty and staff of Northeastern University’s

Doctor of Law and Policy program, especially Dr. Neenah Estrella-Luna, my primary advisor.

Your support and guidance have been instrumental in more ways than I can count. I would also

like to thank Northeastern University’s College of Professional Studies for embracing and

promoting practice-based doctoral level education. Moreover, I cannot go without recognizing

the inimitable and venerable Cohort VIII – my fellow students who have challenged, frustrated,

supported, and entertained me – that has made the past two years a special era in my life. I will

miss joining all of you in the “library” after class.

It would not be fair for me to neglect mentioning my coworkers, friends and family, who

have listened to me cry and vent as they have continued to support me through my journey.

Special thanks go to: Mezline Cunningham-Smith, Vijay Brijbasi, Enid Roberts, Rudolph

Roberts, Yanessy Miranda, Yvette Theodore, Majid Shah, Fadner Theodore, Juan Zamora, Mark

Rogers, and Jeremy Moodie.

4

ABSTRACT

Florida’s unique ecosystem – consisting of porous limestone, coastal property, and

abundant energy resources – is a significant reason for the state government to consider an

environmental policy to mitigate potential threats to the vitality of this ecosystem associated with

current and future climate change. Presently, Florida is already facing concurrent, and often

related, economic and environmental crises that can be linked to inadvertent climate

modifications. Based on readily available measures identified in the Environmental Protection

Agency’s Clean Power Plan to reduce carbon dioxide emissions, this study recommends the state

of Florida implements a climate disturbance and adaptation fee as a method of mitigating risks

associated with inadvertent climate modifications.

5

TABLE OF CONTENTS

Contents

Acknowledgements ......................................................................................................................... 3

Abstract ........................................................................................................................................... 4

Introduction ................................................................................................................................... 12

Changes in the Climate, Human Influence ............................................................................. 14

Climate Modifications ............................................................................................................ 15

Bangladesh .............................................................................................................................. 16

Isle de Jean Charles ................................................................................................................. 16

South Florida ........................................................................................................................... 17

Environmental Policy: Clean Power Plan ............................................................................... 18

Mitigating the Risk of Inadvertent Climate Modifications with Energy Policy ..................... 19

Methods toward Compliance: Meeting the Emission Reduction Goals ................................. 20

Florida’s Energy Future. ......................................................................................................... 20

Compliance Factors ................................................................................................................ 21

Supreme Court Litigation ....................................................................................................... 23

The Path Forward .................................................................................................................... 25

Structure of the Thesis ............................................................................................................ 25

Literature Review.......................................................................................................................... 26

Environmental Economics ...................................................................................................... 26

Impact on different Socio-Economic Groups. ........................................................................ 27

Discount Rate. ......................................................................................................................... 28

Resource Allocation ................................................................................................................ 29

6

Economics of Uncertainty....................................................................................................... 31

Method and Research Design ....................................................................................................... 33

Research Questions ................................................................................................................. 34

Research Framework .............................................................................................................. 35

Research Method .................................................................................................................... 35

Scenario Methodology. ........................................................................................................... 36

Adjusting Values for Cost Benefit Analysis. .......................................................................... 40

Incremental Benefits (PVB). ................................................................................................... 41

Incremental Costs (PVC). ....................................................................................................... 42

Cost-benefit Analysis Ratio. ................................................................................................... 42

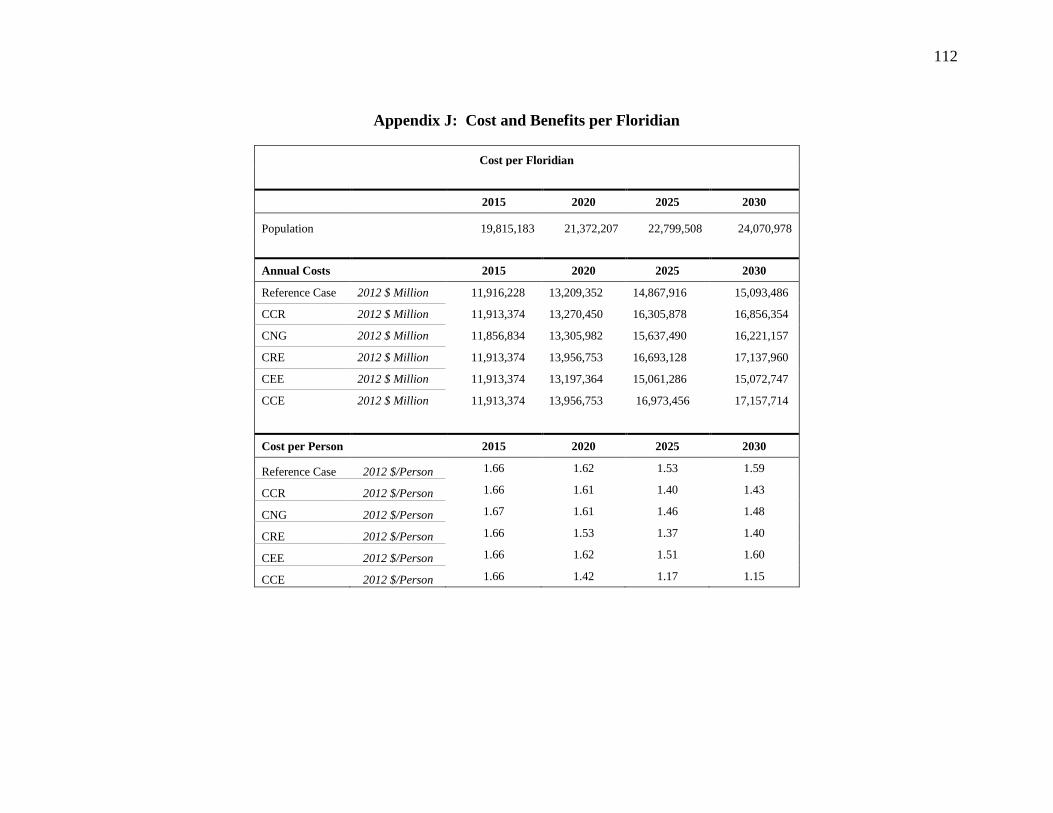

Costs and Benefits per Floridian. ............................................................................................ 42

Limitations of Study ............................................................................................................... 43

Ethical Statement .................................................................................................................... 43

Results ........................................................................................................................................... 44

Carbon Dioxide Emissions ..................................................................................................... 44

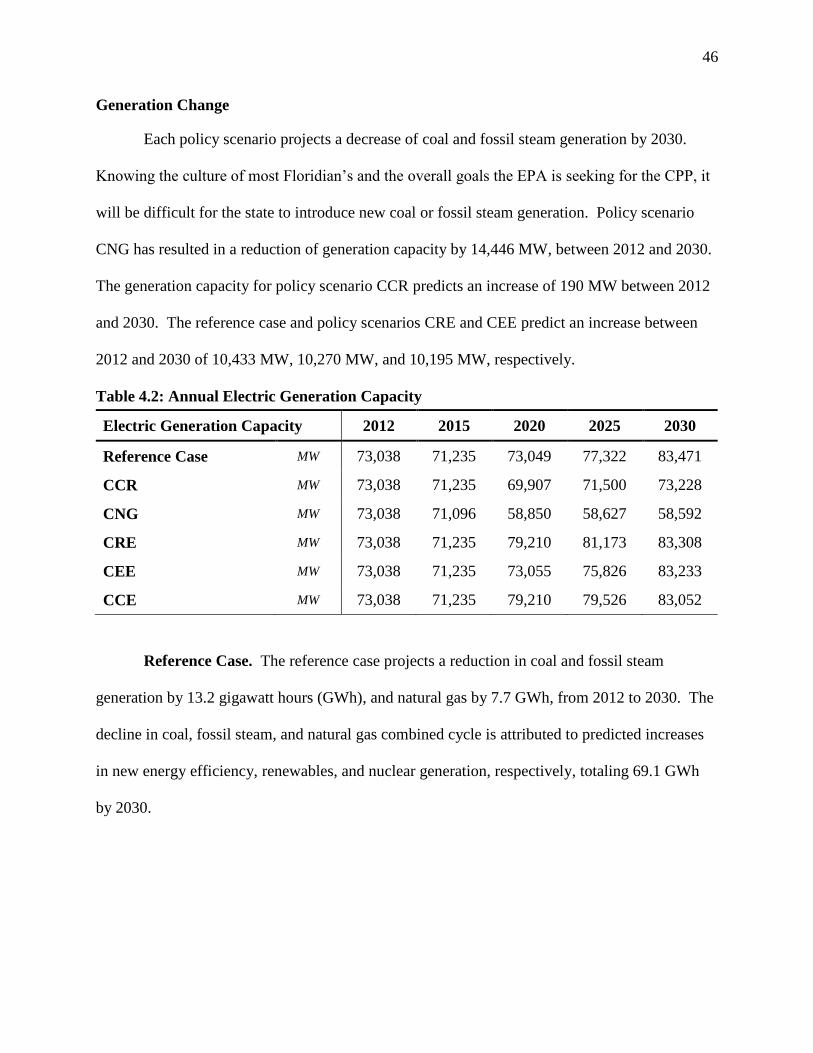

Generation Change.................................................................................................................. 46

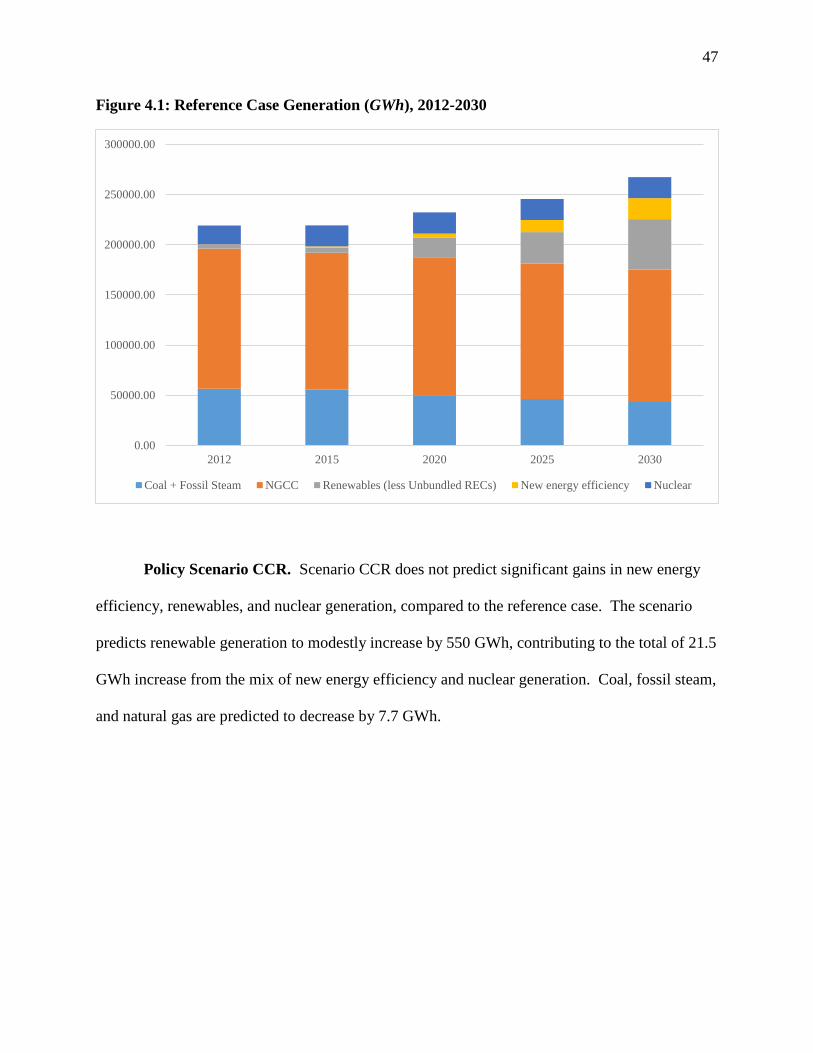

Reference Case........................................................................................................................ 46

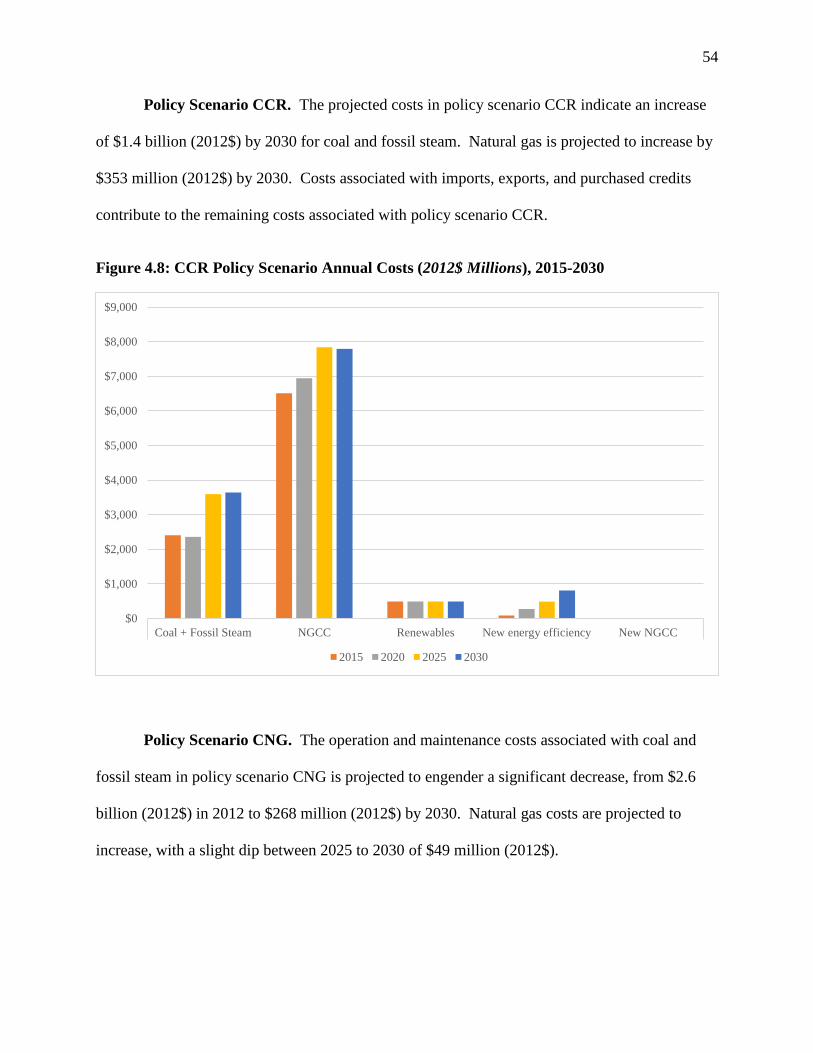

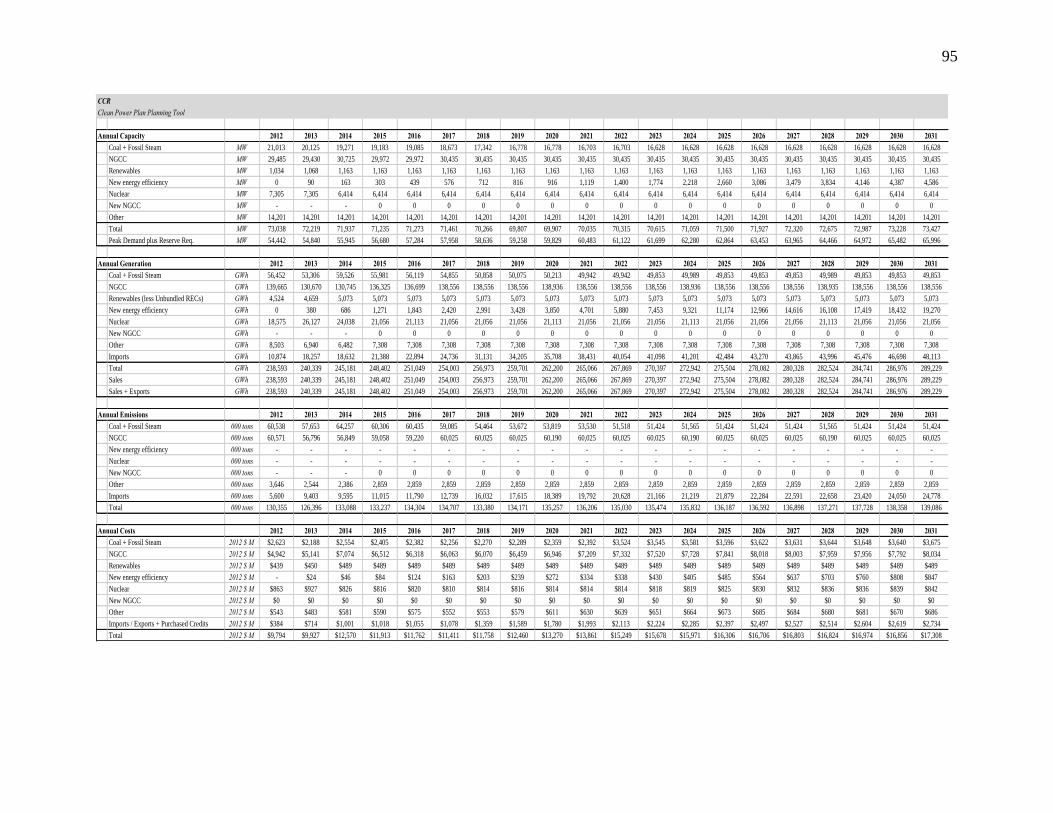

Policy Scenario CCR. ............................................................................................................. 47

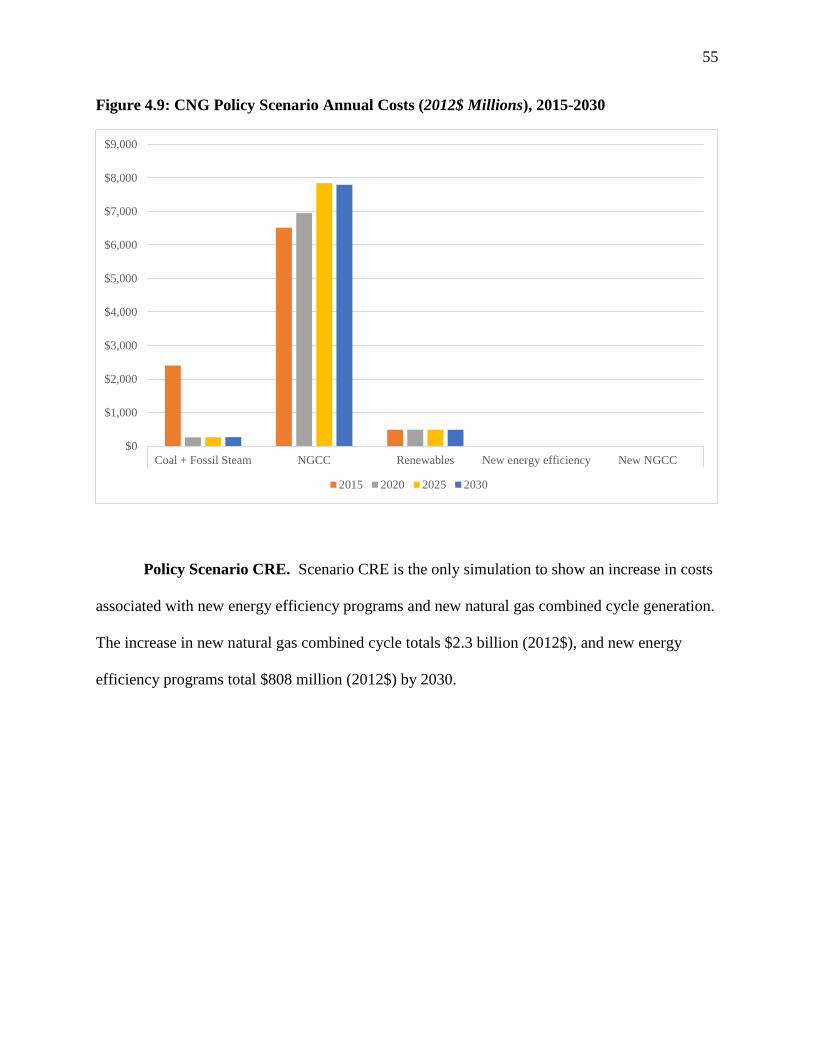

Policy Scenario CNG .............................................................................................................. 48

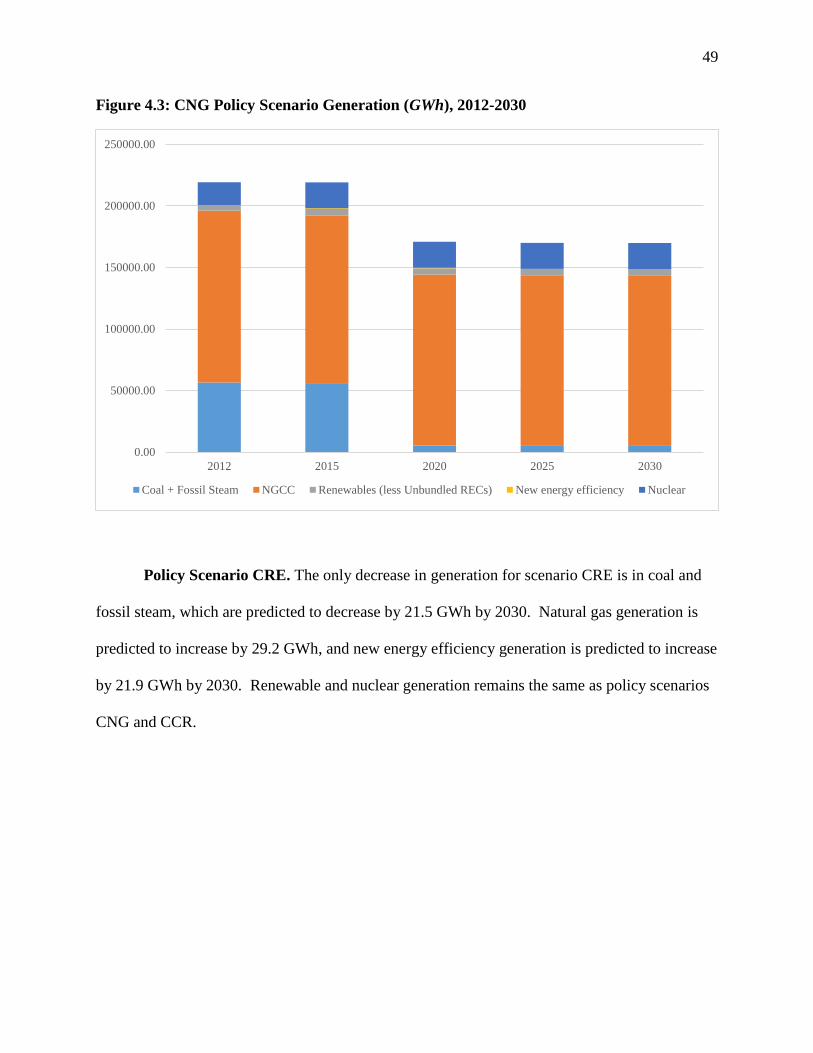

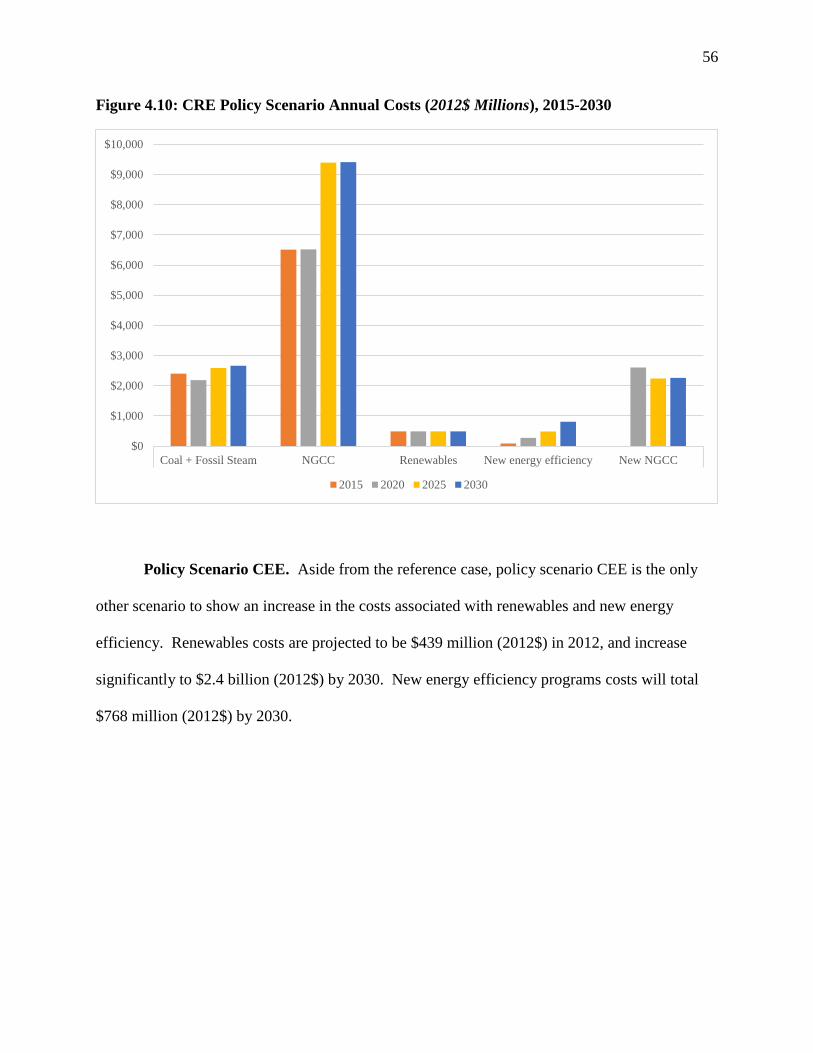

Policy Scenario CRE............................................................................................................... 49

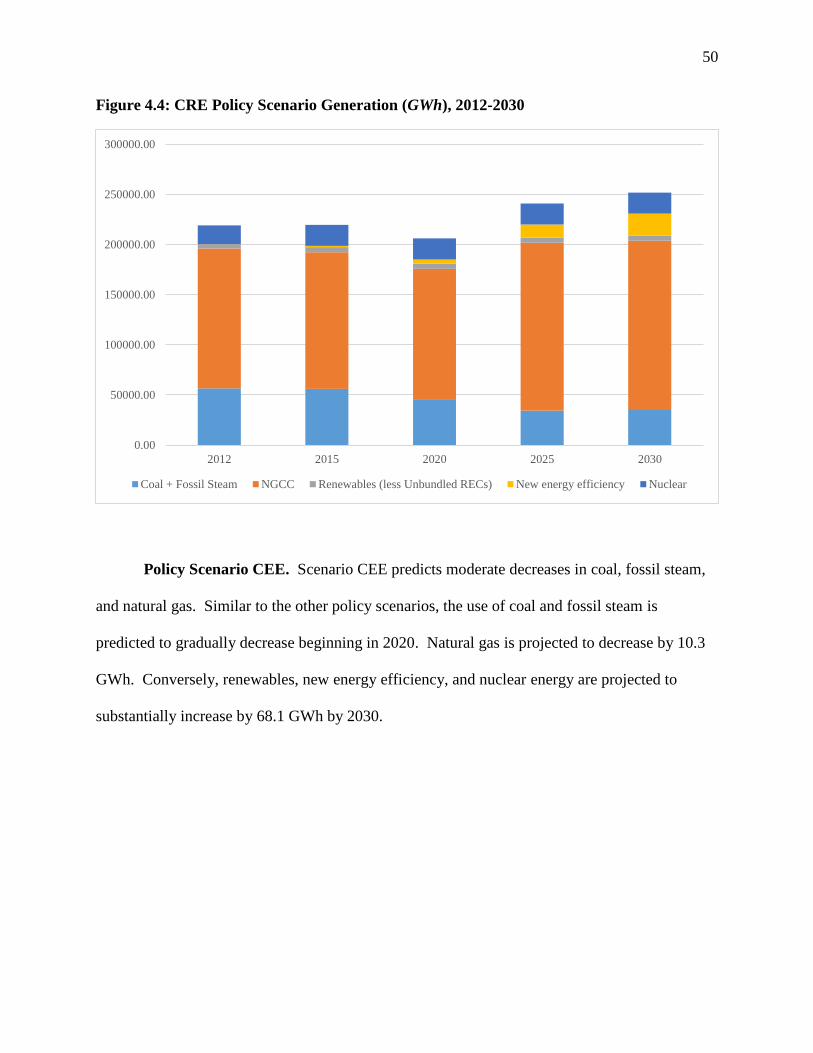

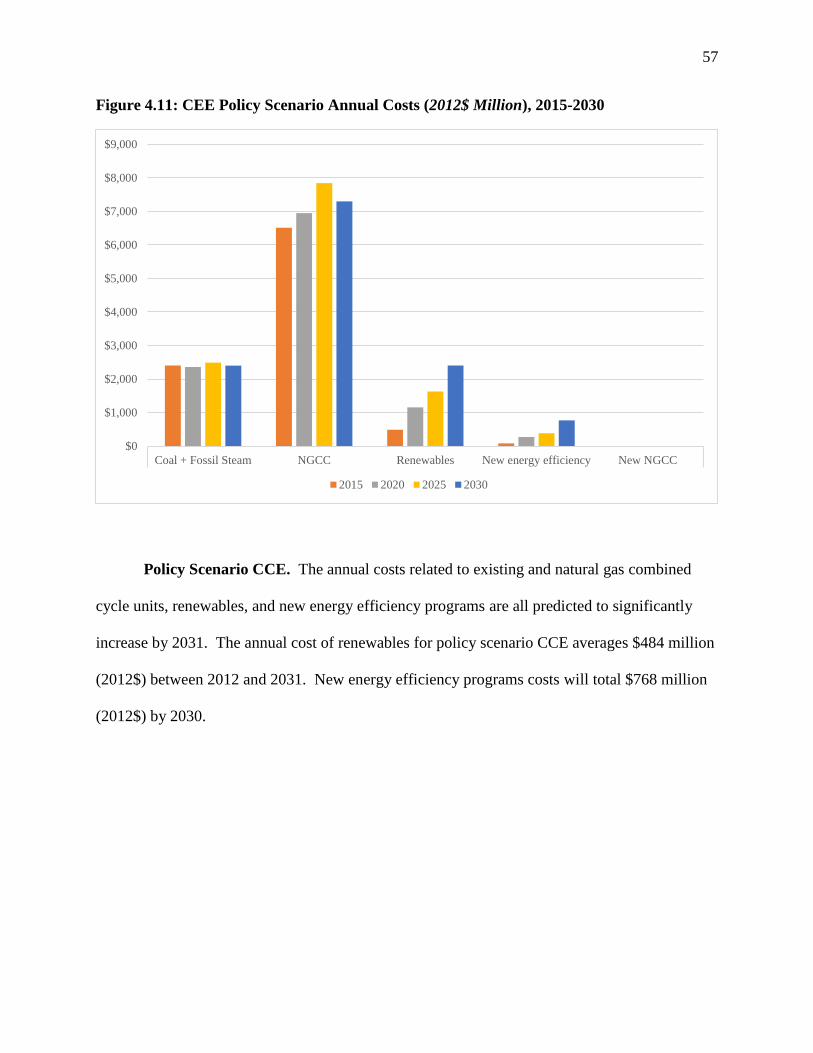

Policy Scenario CEE ............................................................................................................... 50

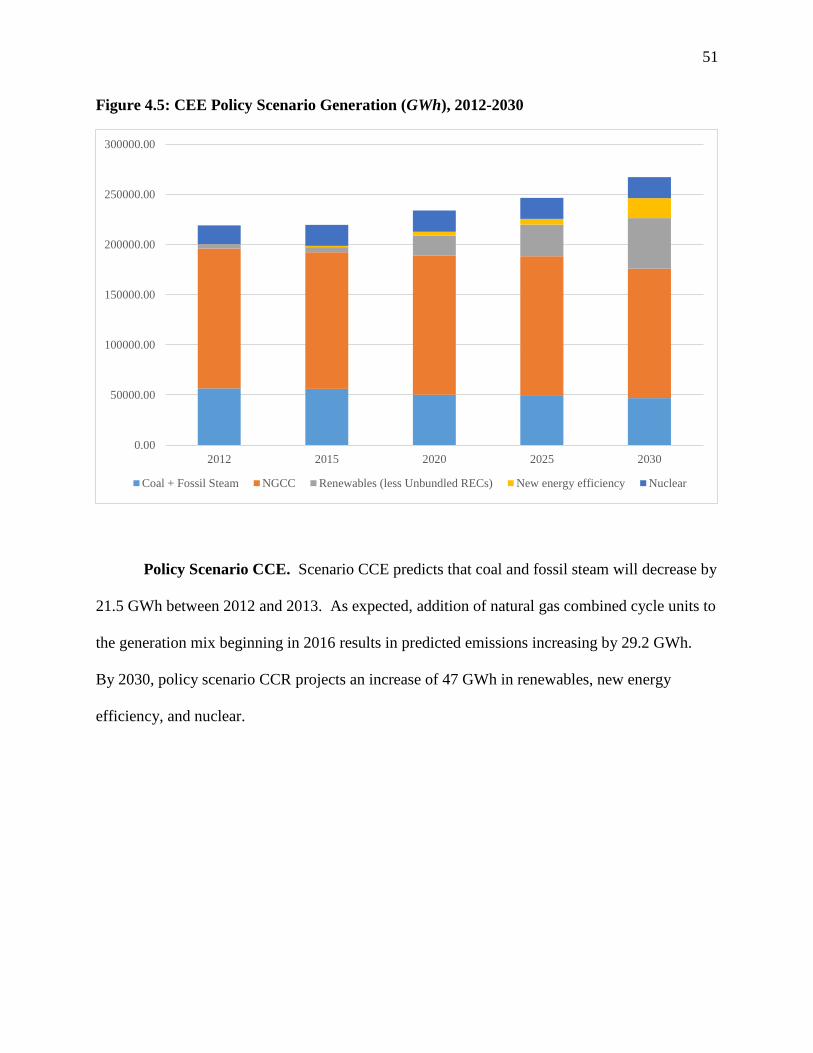

Policy Scenario CCE............................................................................................................... 51

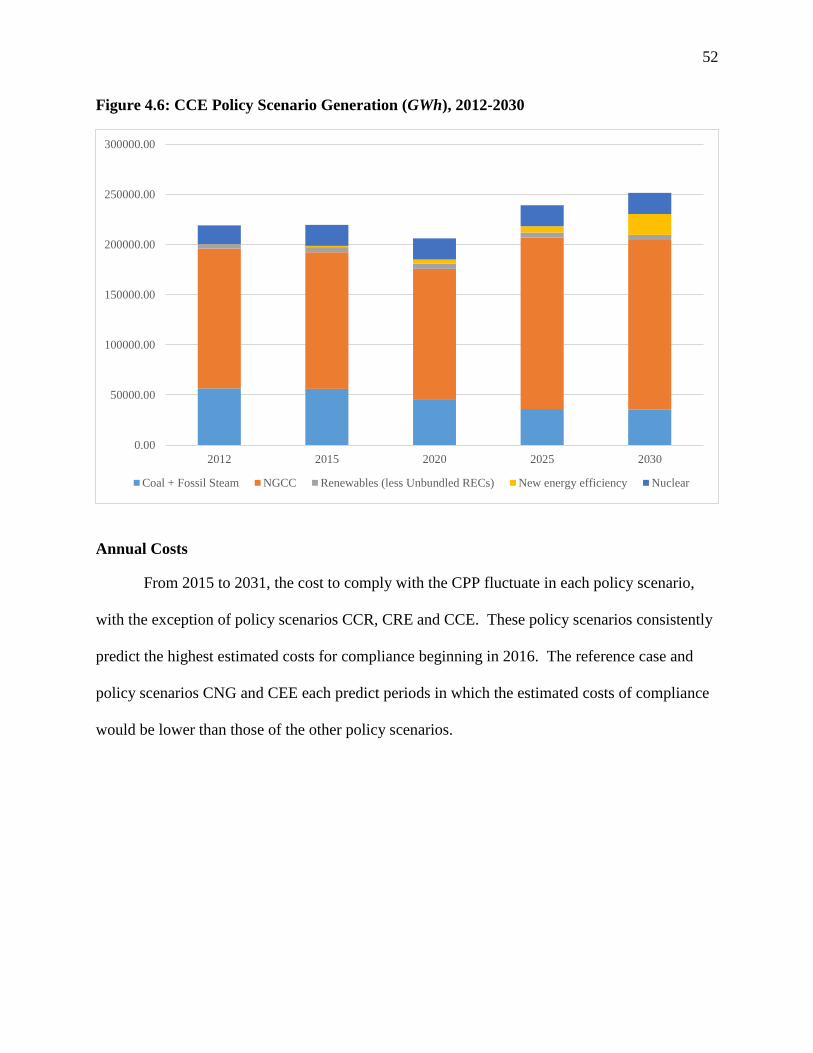

Annual Costs ........................................................................................................................... 52

7

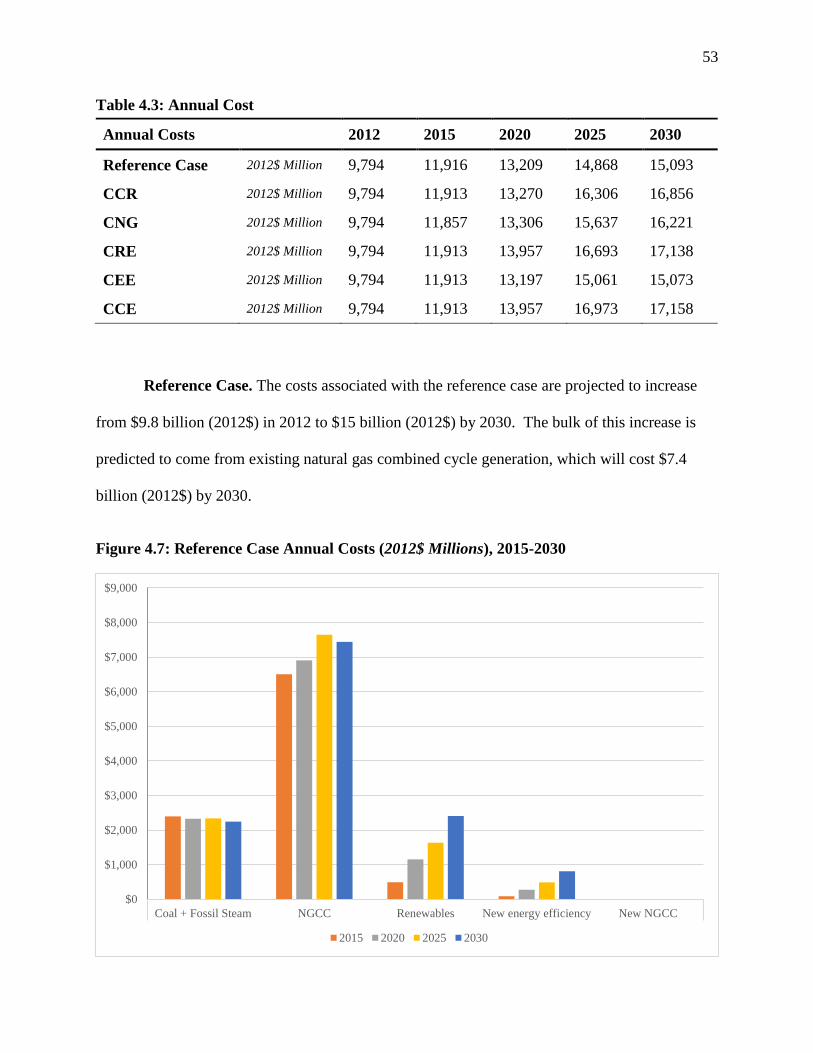

Reference Case........................................................................................................................ 53

Policy Scenario CCR .............................................................................................................. 54

Policy Scenario CNG .............................................................................................................. 54

Policy Scenario CRE............................................................................................................... 55

Policy Scenario CEE ............................................................................................................... 56

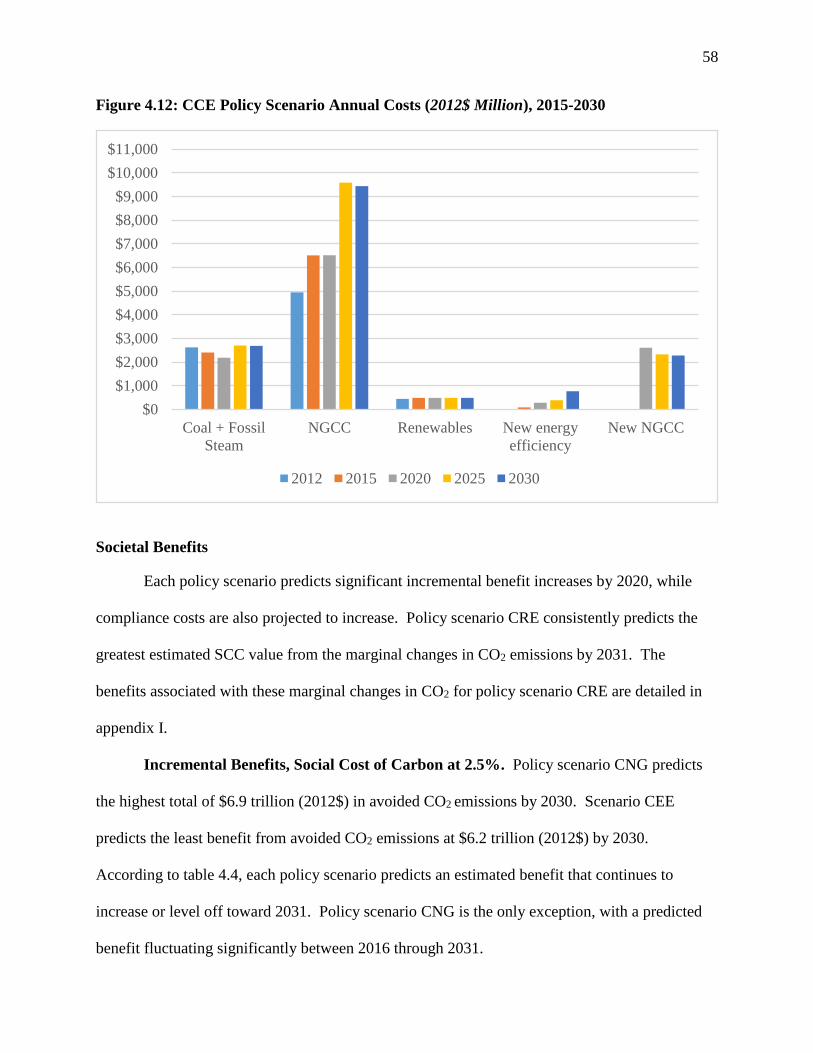

Policy Scenario CCE............................................................................................................... 57

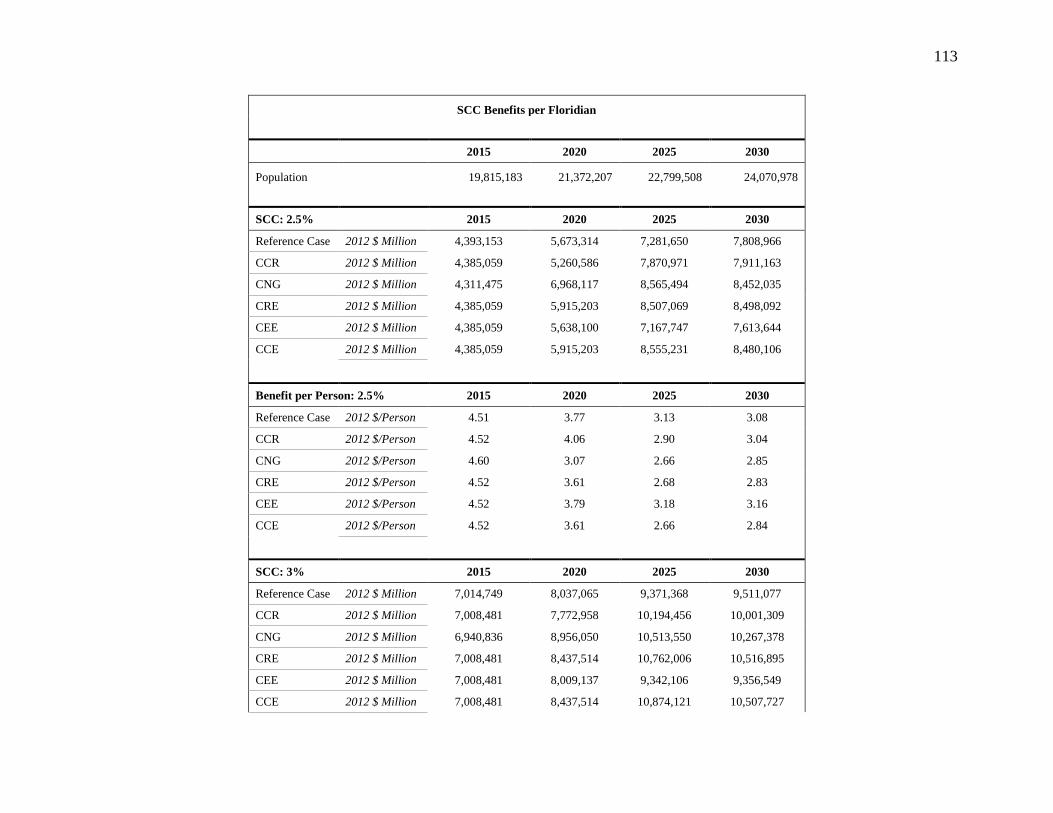

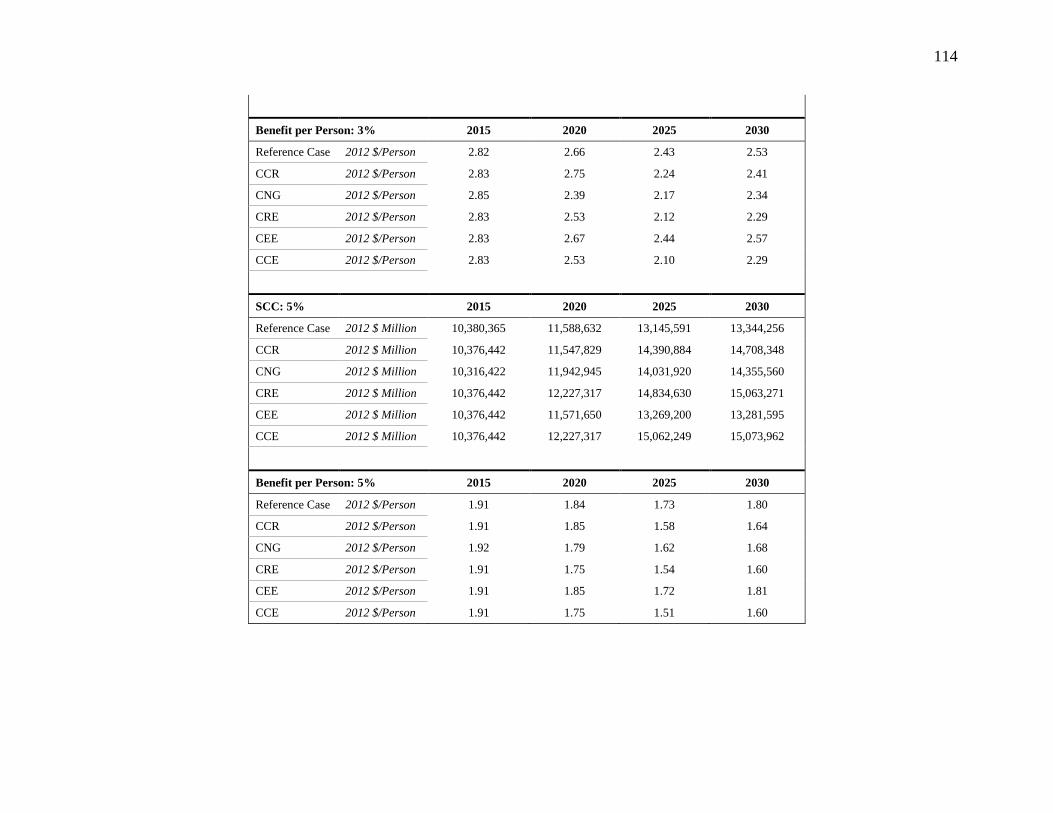

Societal Benefits ..................................................................................................................... 58

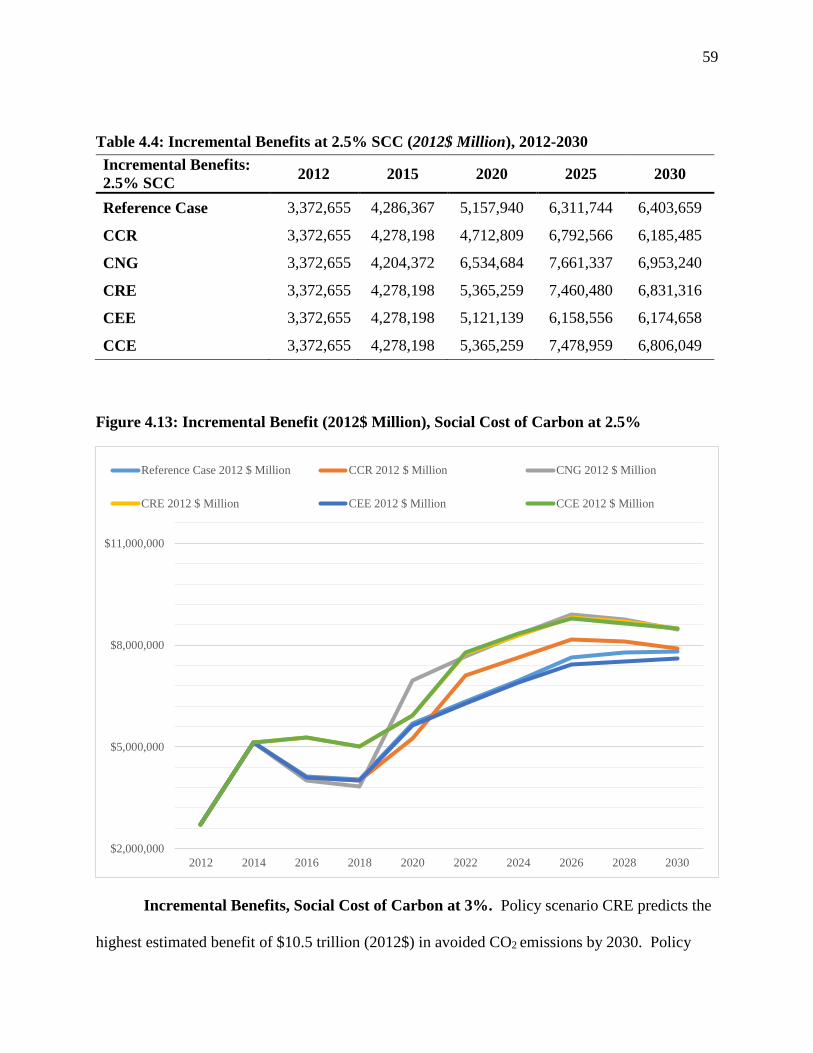

Incremental Benefits, Social Cost of Carbon at 2.5% ............................................................ 58

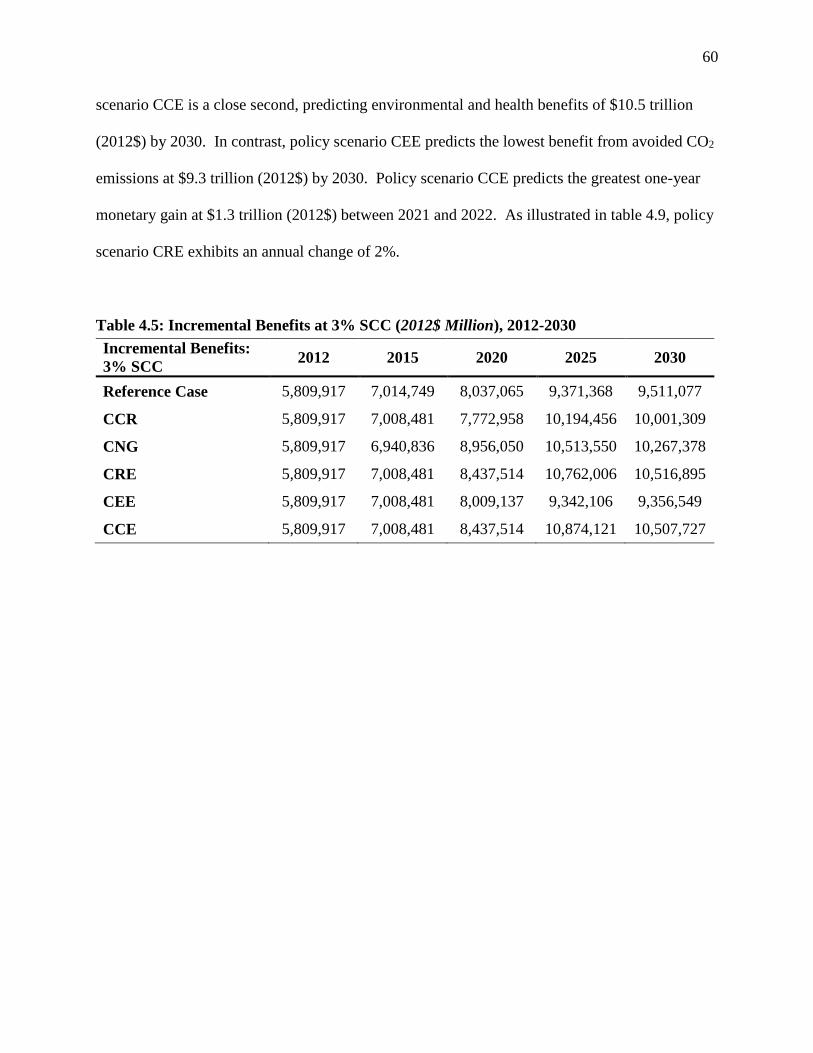

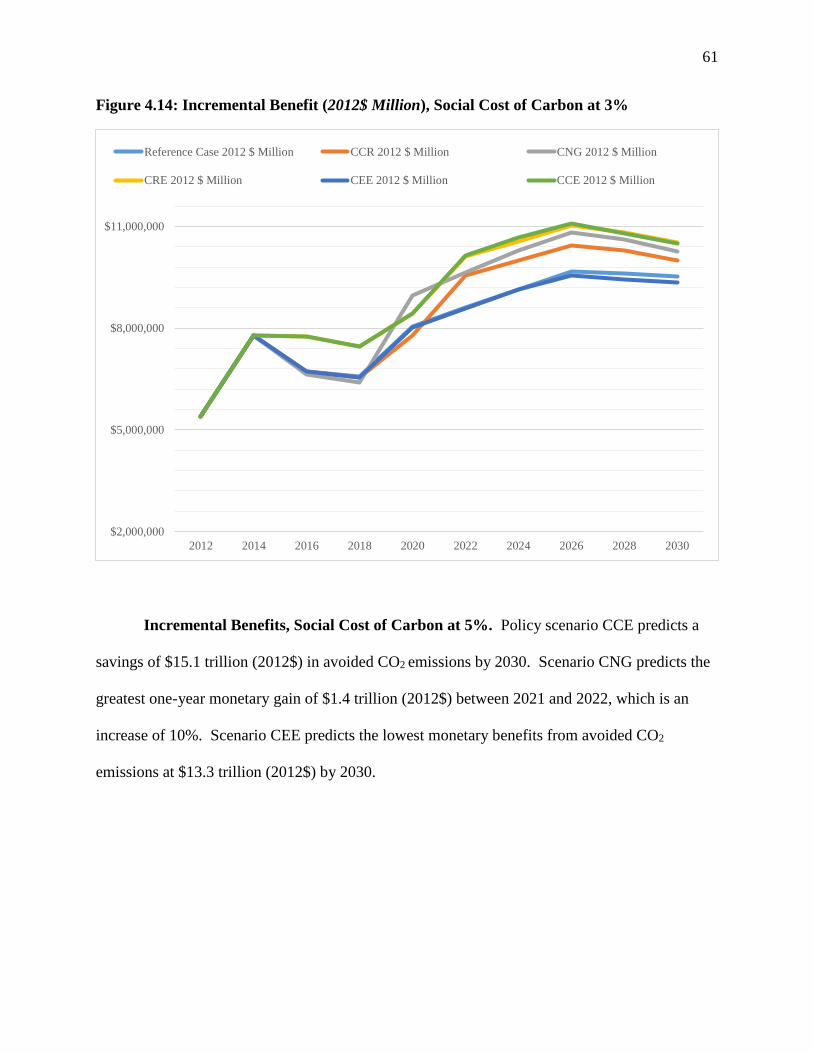

Incremental Benefits, Social Cost of Carbon at 3%. .............................................................. 59

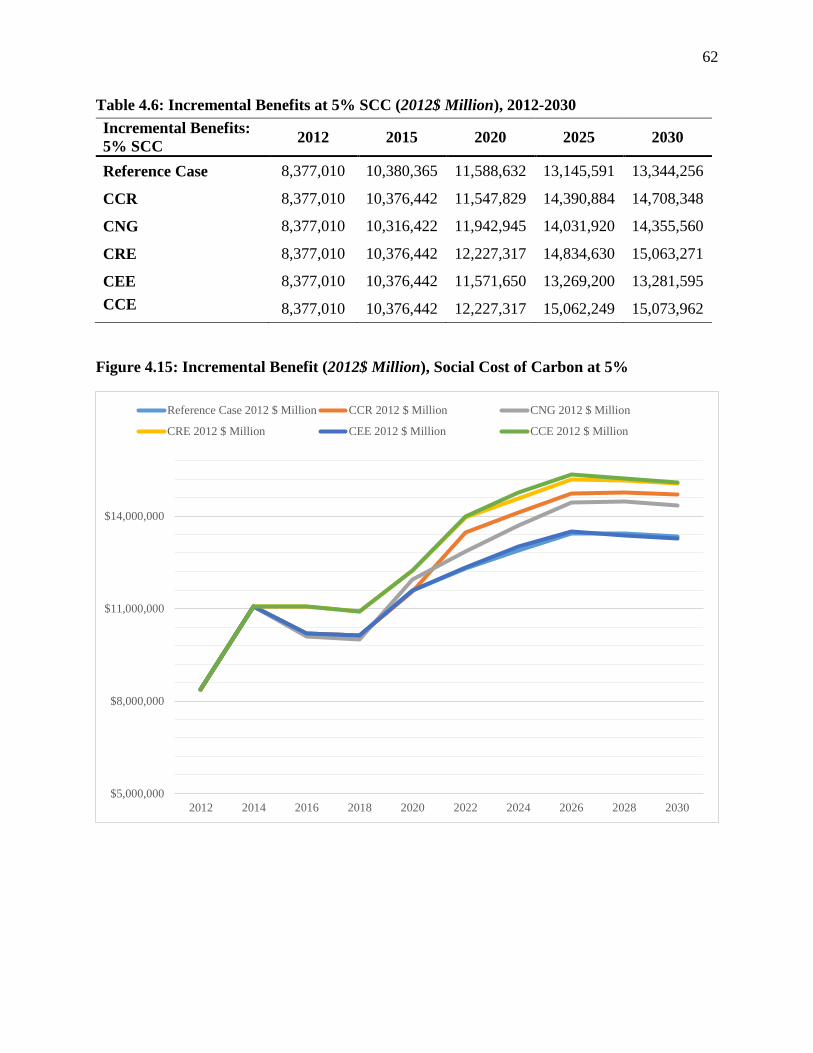

Incremental Benefits, Social Cost of Carbon at 5%. .............................................................. 61

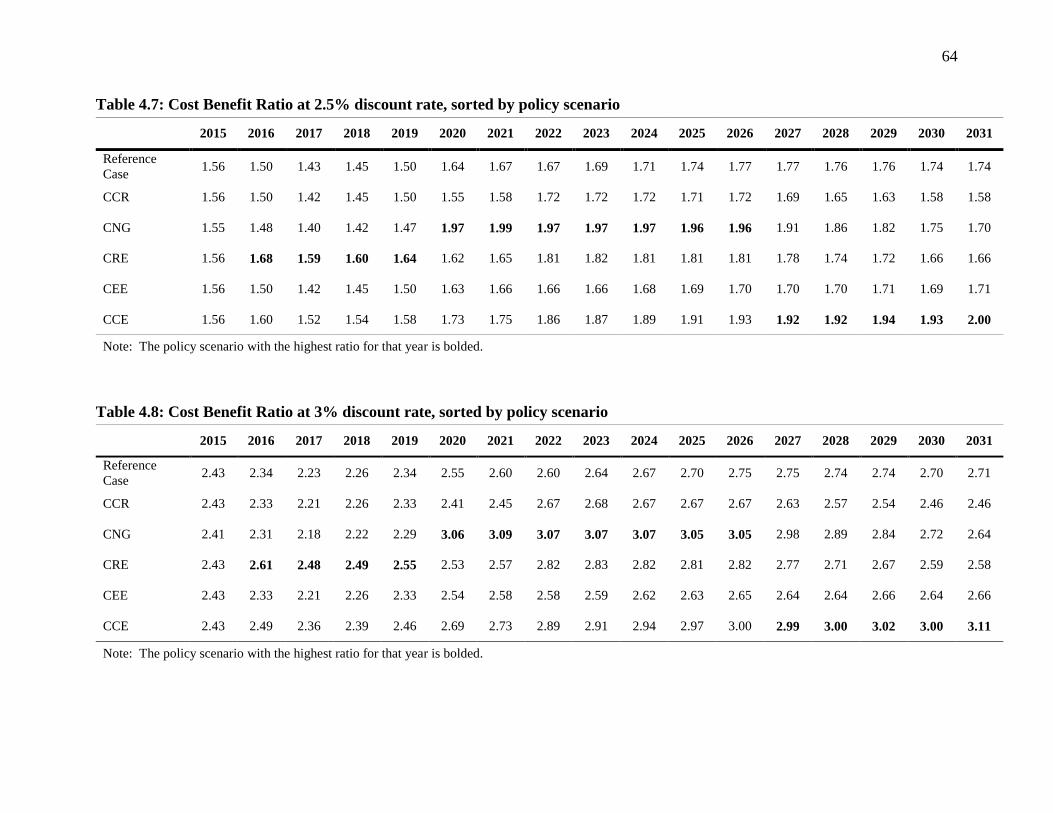

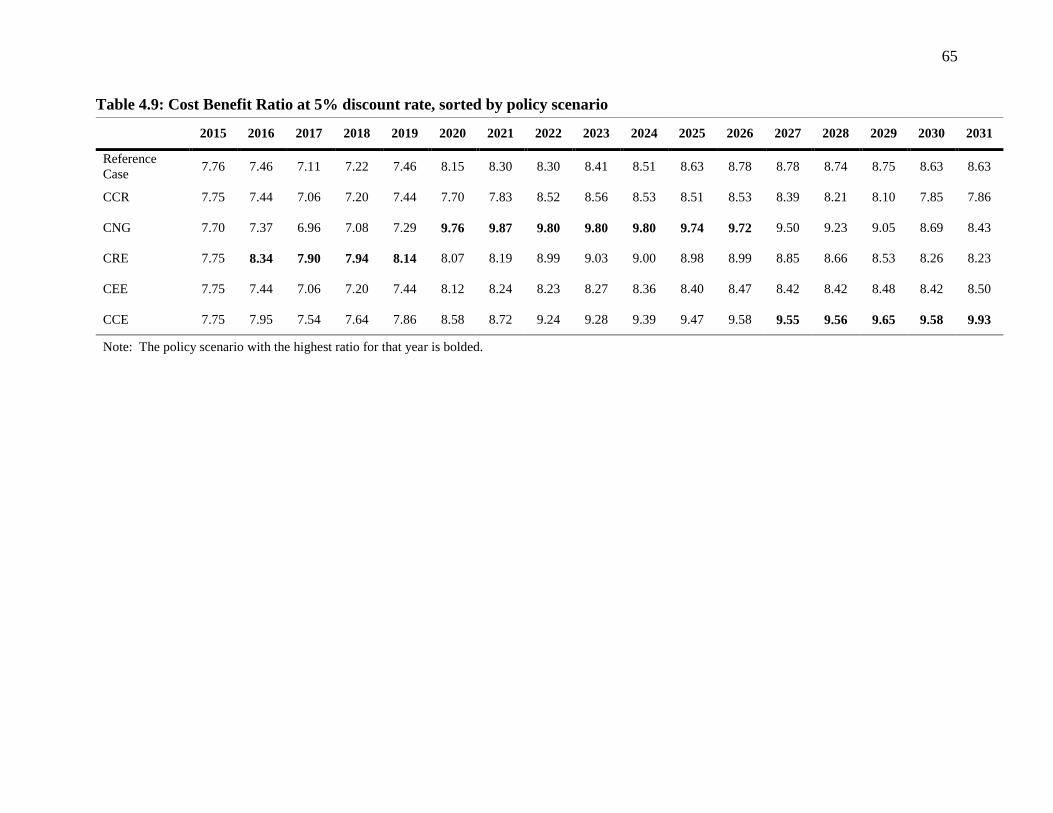

Cost-benefit Ratio ................................................................................................................... 63

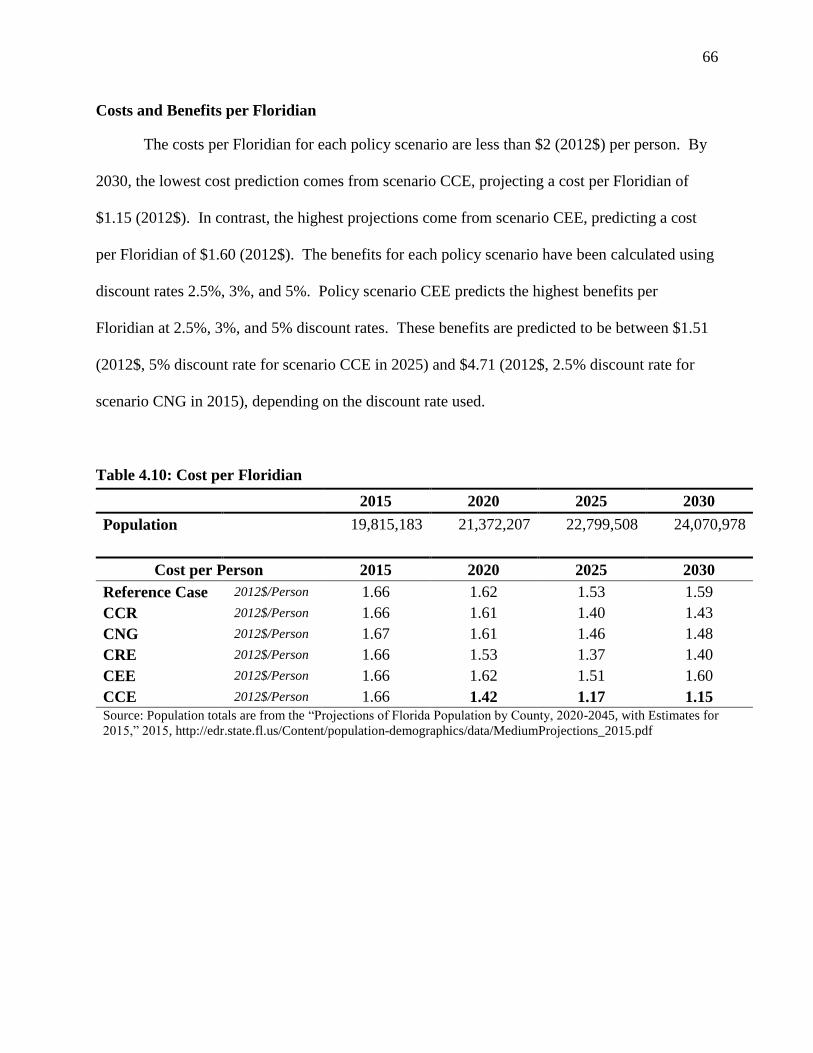

Costs and Benefits per Floridian ............................................................................................. 66

Energy and Emissions: Mitigating the Risks ................................................................................ 69

Which BSER, or Mixture of Methods, Provides the Best Economic Outcome for Florida? . 70

Which Mixture of BSER Methods are Economically Viable While Meeting EPA’s Emission

Eeduction Goals for the Development of the State Implementation Plan (SIP)? ............. 71

Energy is the Engine of Economic Growth: Generation Diversity ......................................... 72

Insuring the Future: An Insurance Premium Associated with Carbon ................................... 74

Policy Recommendation Summary......................................................................................... 76

Future Research ...................................................................................................................... 77

Conclusion .............................................................................................................................. 77

References ..................................................................................................................................... 80

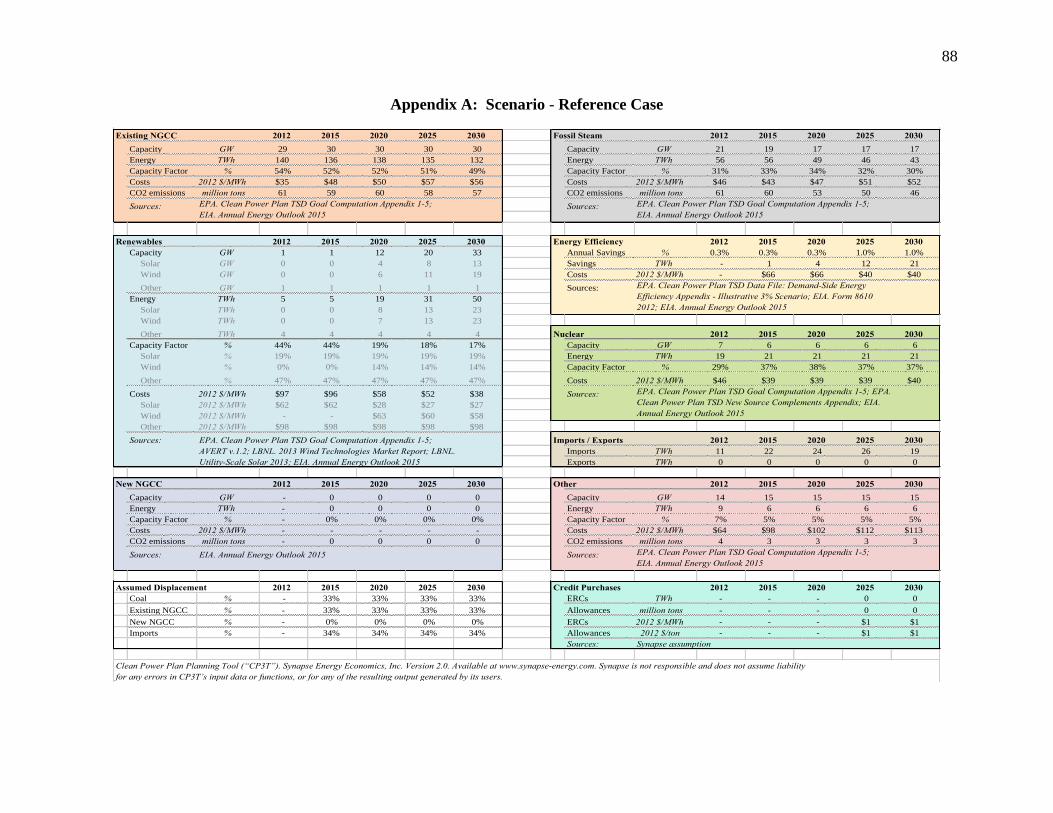

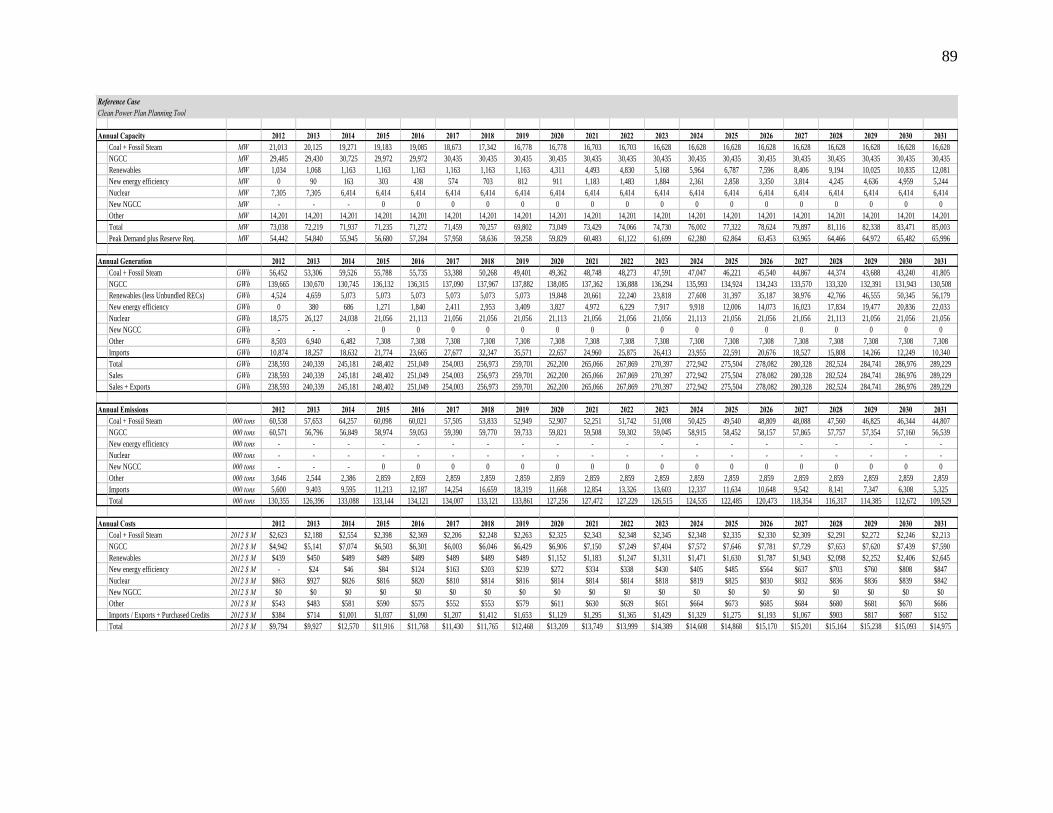

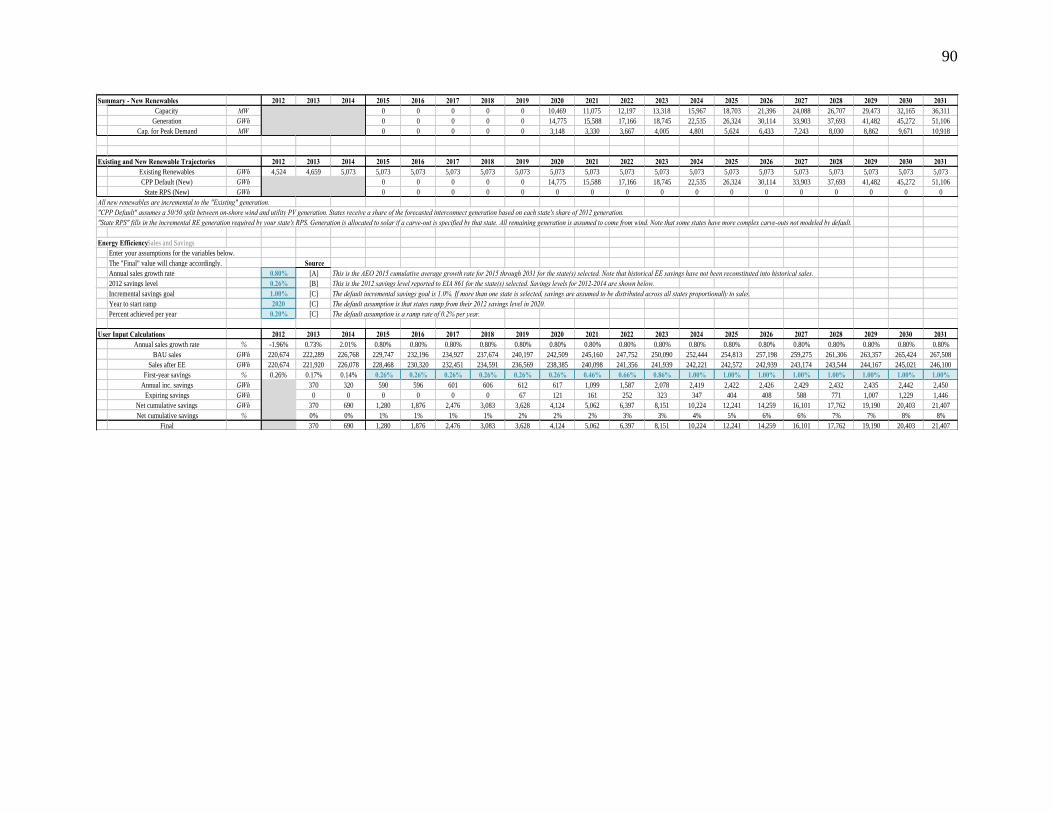

Appendix A: Scenario - Reference Case ..................................................................................... 88

8

Appendix B: Scenario - CNG ....................................................................................................... 91

Appendix C: Scenario - CCR ........................................................................................................ 94

Appendix D: Scenario - CRE ........................................................................................................ 97

Appendix E: Scenario - CEE ...................................................................................................... 100

Appendix F: Scenario - CCE ...................................................................................................... 103

Appendix G: Consumer Price Index – All Urban Consumers .................................................... 106

Appendix H: Future Value Interest Factor.................................................................................. 109

Appendix I: Analysis Tables, Summary of Results .................................................................... 110

Appendix J: Cost and Benefits per Floridian .............................................................................. 112

9

LIST OF TABLES

Table 3.1: Synapse CPP Default, Renewables Capacity and Generation .................................... 37

Table 3.2: Energy Efficiency, Sales, and Savings ........................................................................ 37

Table 3.3: Scenario Descriptions .................................................................................................. 39

Table 3.4: Social Cost of CO2, 2010 - 2050 ................................................................................ 41

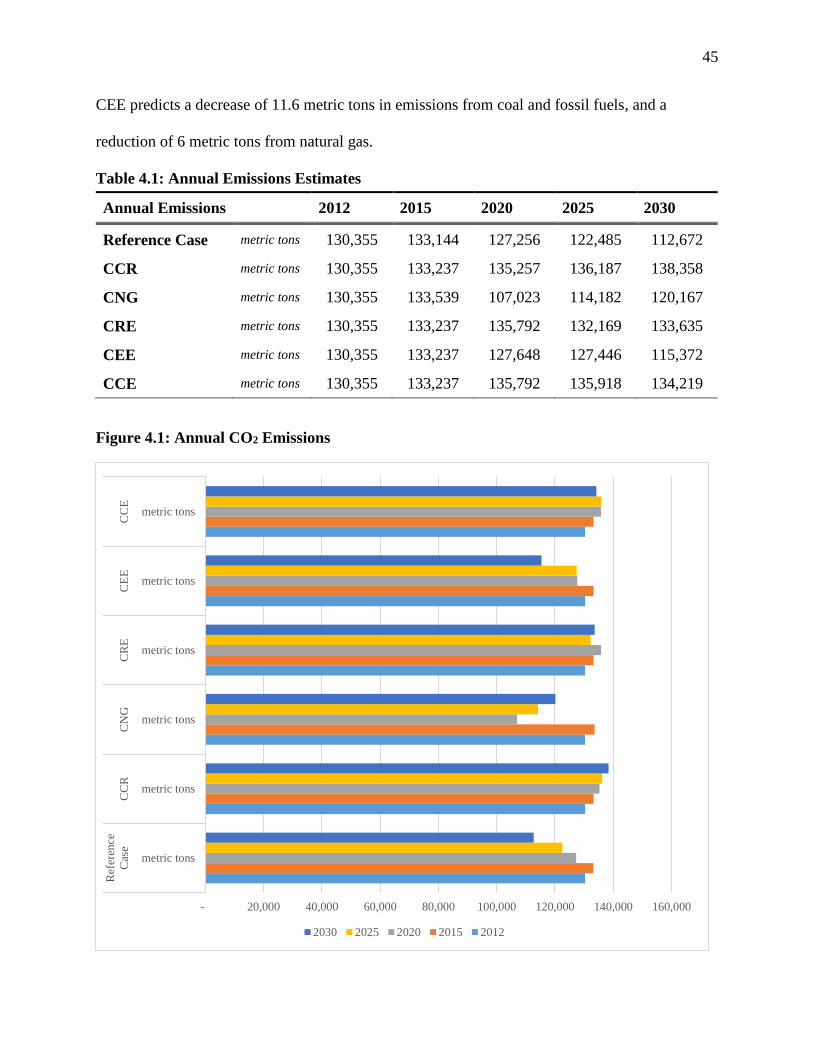

Table 4.1: Annual Emissions Estimates........................................................................................ 45

Table 4.2: Annual Electric Generation Capacity .......................................................................... 46

Table 4.3: Annual Cost ................................................................................................................. 53

Table 4.4: Incremental Benefits at 2.5% SCC (2012$ Million), 2012-2030 ................................ 59

Table 4.5: Incremental Benefits at 3% SCC (2012$ Million), 2012-2030 ................................... 60

Table 4.6: Incremental Benefits at 5% SCC (2012$ Million), 2012-2030 ................................... 62

Table 4.7: Cost-benefit Ratio at 2.5% discount rate, sorted by policy scenario ........................... 64

Table 4.8: Cost-benefit Ratio at 3% discount rate, sorted by policy scenario .............................. 64

Table 4.9: Cost-benefit Ratio at 5% discount rate, sorted by policy scenario .............................. 65

Table 4.10: Cost per Floridian ...................................................................................................... 66

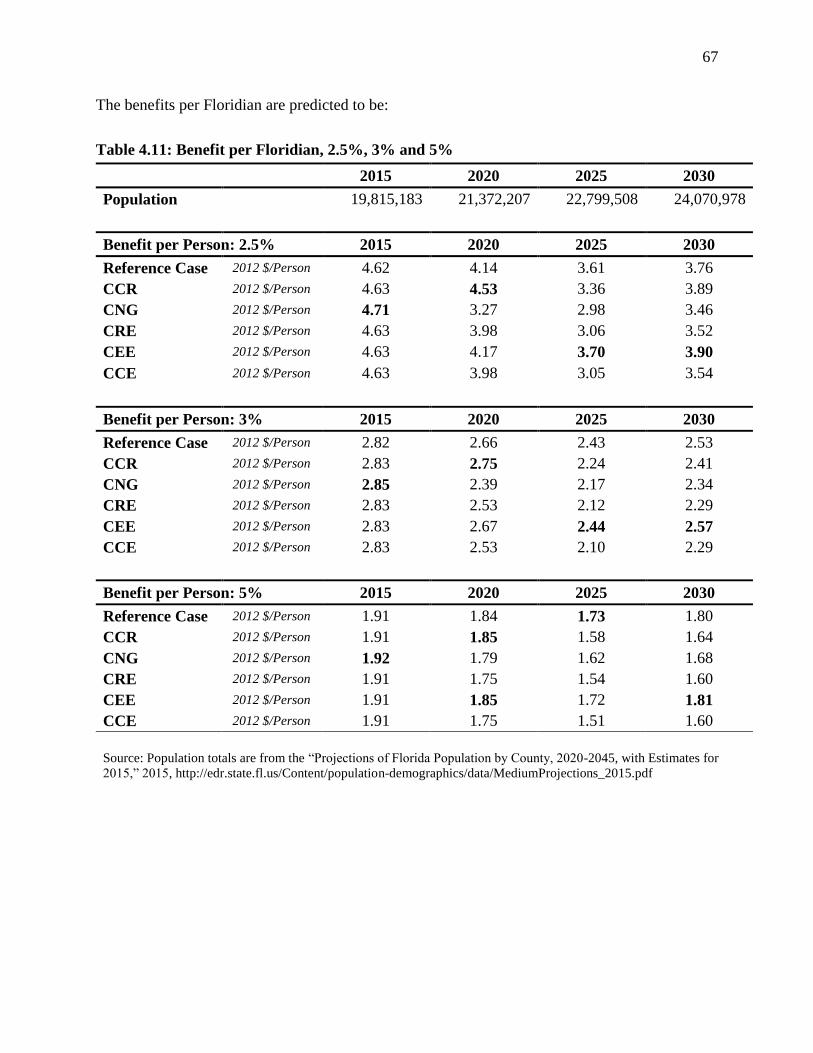

Table 4.11: Benefit per Floridian, 2.5%, 3% and 5% ................................................................... 67

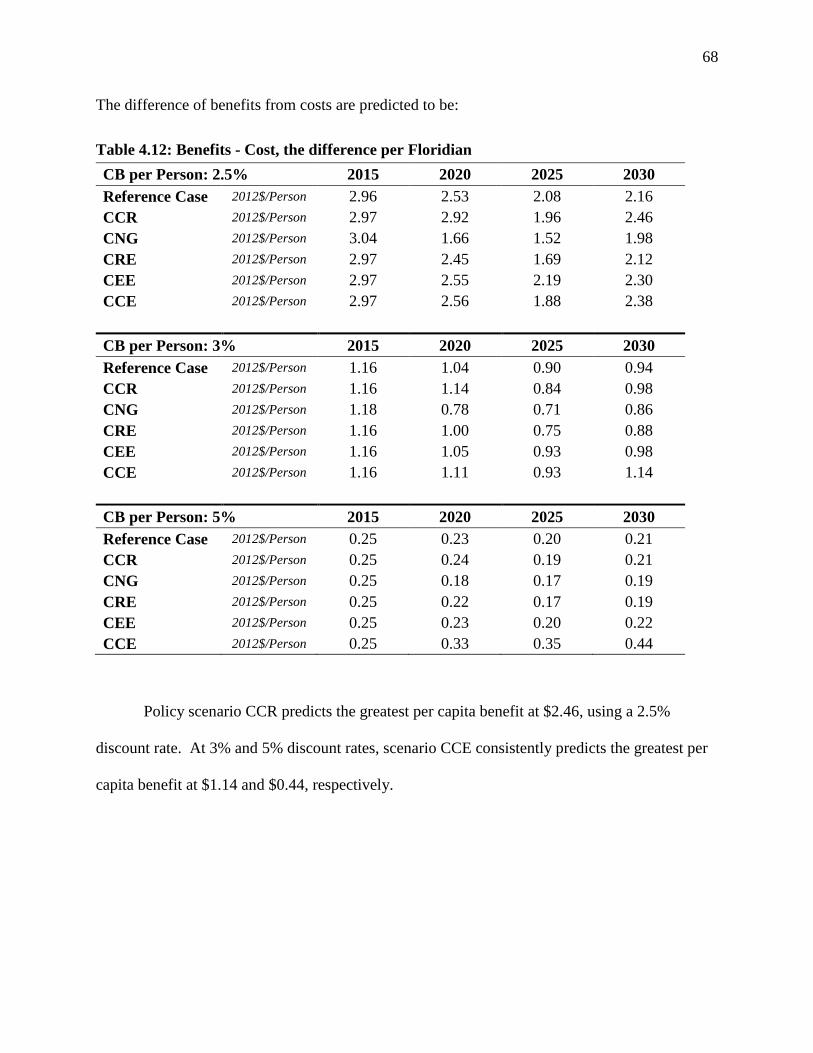

Table 4.12: Benefits- cost, the Difference per Floridian .............................................................. 68

10

LIST OF FIGURES

Figure 4.1: Annual CO2 Emissions ............................................................................................... 45

Figure 4.2: Reference Case Generation (GWh), 2012-2030 ......................................................... 47

Figure 4.3: CCR Policy Scenario Generation (GWh), 2012-2030 ................................................ 48

Figure 4.4: CNG Policy Scenario Generation (GWh), 2012-2030 ............................................... 49

Figure 4.5: CRE Policy Scenario Generation (GWh), 2012-2030 ................................................ 50

Figure 4.6: CEE Policy Scenario Generation (GWh), 2012-2030 ................................................ 51

Figure 4.7: CCE Policy Scenario Generation (GWh), 2012-2030 ................................................ 52

Figure 4.8: Reference Case Annual Costs (2012$ Millions), 2015-2030 ..................................... 53

Figure 4.9: CCR Policy Scenario Annual Costs (2012$ Millions), 2015-2030 ............................ 54

Figure 4.10: CNG Policy Scenario Annual Costs (2012$ Millions), 2015-2030 ......................... 55

Figure 4.11: CRE Policy Scenario Annual Costs (2012$ Millions), 2015-2030 .......................... 56

Figure 4.12: CEE Policy Scenario Annual Costs (2012$ Million), 2015-2030 ............................ 57

Figure 4.13: CCE Policy Scenario Annual Costs (2012$ Million), 2015-2030............................ 58

Figure 4.14: Incremental Benefit (2012$ Million), Social Cost of Carbon at 2.5% ..................... 59

Figure 4.15: Incremental Benefit (2012$ Million), Social Cost of Carbon at 3% ........................ 61

Figure 4.16: Incremental Benefit (2012$ Million), Social Cost of Carbon at 5% ........................ 62

11

LIST OF ACRONYMS

Acronym

BSER Best system for emission reductions

CAA Clean Air Act

CBA Cost-benefit analysis

CO2 Carbon dioxide

CP3T Clean Power Plan planning tool

CPI Consumer price index

CPP Clean Power Plan

DoD Department of Defense

EERS Energy efficiency resource standard

ENPV Expected net present value

EPA Environmental Protection Agency

FL DEP Florida Department of Environmental Protection

FL PSC Florida Public Service Commission

FV Future value

GDP Gross domestic product

GHG Greenhouse gas

GWh Gigawatt hours

HUD Department of Housing and Urban Development

IAM Integrated Assessment Model

IPCC Intergovernmental Panel on Climate Change

IRB Institutional Review Board

MATS Mercury and Air Toxics Standard

MW Megawatt

NEL Net energy for load

NPV Net present value

PV Present value

RPS Renewable portfolio standard

SCC Social cost of carbon

SIP State Implementation Plan

12

The climate is a common good, belonging to all and meant for all. At

the global level, it is a complex system linked to many of the essential

conditions for human life. – Pope Francis, Encyclical Letter Laudato Si’ of the

Holy Father Francis On Care for Our Common Home

Chapter 1

Introduction

As nations develop their own environmental policies to mitigate rising seas, weather

extremes, and altered precipitation patterns, the citizen response to these strategies will be

economically and politically critical. Accordingly, using tools to mitigate the risk associated

with inadvertent climate modifications can be a useful in evaluating environmental policies

needed to address these changes. An ideal environmental policy is balanced, meet the

environmental and health needs to the public while accounting against the typical business as

usual perspective (Hultman, Hassenzahl, & Rayner, 2010).

Worldwide, the economic risks associated with continued anthropogenic greenhouse gas

(GHG) emissions are beginning to manifest in both local and global environmental catastrophes.

The effects of human-induced stress on the environment have been apparent in rising coastal

water, crippling damage from storm surges, and frequent seasons of extreme heat. Between

2010 and 2015, the U.S. has spent over $242.2 billion dollars responding to weather-related

disasters.

One such disaster has been Hurricane Isaac in 2012, which cost the U.S. approximately

$2.9 billion dollars. A large, tropical cyclone, Isaac has generated storm surges and flooding

throughout many southeastern states, including Florida (National Centers for Environmental

13

Information, n.d.). Costly environmental disasters like Hurricane Isaac continue to place stress

on the national economy.

Thus, it is time for nations, especially industrialized nations, to create policies that

mitigate the risks associated with global warming. Over the last several decades, numerous

climatologists and other scientists have studied the impacts associated with increasing

greenhouse gases (GHGs) on our planet. GHGs, like carbon dioxide (CO2), do not dissipate

quickly; rather, they trap the Sun’s rays within the atmosphere, which causes the planet to get

warmer.

The impacts of this warming have altered weather patterns globally. These atmospheric

fluctuations include droughts, coastal erosion, storm intensity and location, water availability,

flooding, and changes in rainfall pattern (Nordhaus, 2013). The impacts are severe enough that

the U.S. Department of Defense (DoD) (2015) has released a report noting that continued

environmental degradation threatens the financial stability of numerous nations. The DoD

(2015) has also acknowledged that the impacts on the climate are projected to increase over time.

By reviewing case studies, the DoD has recognized that climate risks can exacerbate

socioeconomic problems, thereby generating unforeseen vulnerabilities and potentially causing

conflicts in regions not considered at risk for disturbances (Department of Defense, 2015).

Further, one does not have to leave the U.S. to find areas that are vulnerable to current

climate turmoil. The Southeast region – which includes Alabama, Arkansas, Florida, Georgia,

Kentucky, Louisiana, Mississippi, North Carolina, South Carolina, Tennessee, Texas, and

Virginia – has recently experienced the downside of growth in their manufacturing and energy

production sectors, in the form of increases in carbon emissions.

14

Florida is one of several coastal communities that has the potential to see catastrophic

losses from rising sea levels. According to a risk analysis conducted by the Risky Business

Project, existing property in Florida has the potential be damaged by global warming events,

costing the state between $5.6 billion and $14.8 billion by 2030 (Kinniburgh, Bloomberg,

Paulson, Jr, & Steyer, 2015). Significant losses of public and private property along the state’s

8,436 miles1 of coastal shoreline will negatively impact Florida’s economy, particularly the

tourism industry. At Increasing temperatures will also increase pressure on the energy industry to

meet skyrocketing demands for electricity. In order to meet the demand, the state will need to

generate exponentially growing amounts of electricity to feed the grid, which will lead to an

increase in electricity rates to cover the associated costs (Staletovich, 2015; Kinniburgh, Greer

Simonton, & Allouch, 2015).

Changes in the Climate, Human Influence

In recent decades, industrial nations have worked to reduce their contributions to

atmospheric pollution. These efforts have taken the forms of endangered species protection and

cleaner air and water, resulting in an improved quality of life. However, these policies have not

addressed a growing national dependency on fossil fuels. Environmental sinks are unable to

absorb continually increasing GHG emissions from industrial growth and depleted resources.

The severe weather events resulting from such emissions beget serious social and

economic consequences. In May, 2014, the National Climate Assessment Report found that over

1 The shoreline coastline mileage of the outer coast, offshore islands, sounds, bays, rivers, and creeks are included to

the head of tidewater or to a point where tidal waters narrow to a width of 100 feet. Source: NOAA Office for

Coastal Management, General Coastline and Shoreline Mileage of the United States:

https://coast.noaa.gov/data/docs/states/shorelines.pdf

15

the past decade, various weather-related events have caused significant disruptions and damage

to infrastructure and agriculture. Between 2013 and 2014, the U.S. experienced 17 different

weather disaster events, resulting in 166 deaths, with estimated losses of $41 billion dollars

(National Centers for Environmental Information, n.d.).

Moreover, the Intergovernmental Panel on Climate Change’s (IPCC) 2014 Climate

Change Synthesis Report finds that changes in global temperatures, specifically decreasing

occurrence of cold days and nights and increasing frequency of warm days and nights, are likely

consequences of some human influence. These climatic changes are expected to result in

changes in the frequency and intensity of temperature extremes. Population size, lifestyle

choices, energy consumption, economic activity, and land use patterns contribute to

anthropogenic GHG emissions.

Climate Modifications

The continuous debate about whether current climate patterns are a result of

anthropogenic or natural influences seems to be rhetoric with no logical purpose. Assuming that

these climate disturbances are purely natural, it still may not make sense for the world’s

population to continue to exhaust the planet’s natural resources. David Atkinson, of the Arctic

Research Center, shows that regardless of whether climatic disruptions are caused by human

activity or natural cyclical changes, there are still people who are experiencing the impacts of

such atmospheric turmoil in the present (Nash, 2010). Entire communities in the U.S., as well as

globally, are finding that they are unable to continue the ways of life they are accustomed to due

to extreme weather events, sea level rise, erosion, and the loss of natural resources on which to

survive.

16

Some communities are facing the need to either relocate due to climatic changes

impacting their ecosystems. Areas like South Florida, Isle de Jean Charles, Louisiana, and

Bangladesh are just three examples of communities dealing with worsening climate patterns.

Unlike the other two, however, South Florida is not dealing with human rights violations, like

those of the indigenous people of Isle de Jean Charles.

Bangladesh. Bangladesh is a well-known example of disappearing coastal communities.

The city’s environmental tragedies are not confined to coastal flooding; instead, impacts include

changes in precipitation, increased cyclone intensity, and increased temperature. Many families

in Bangladesh have fled their coastal communities to relocate to the capital, Dhaka. Generally,

these displaced families live in the slums of their new cities.

This migration from coastal communities to the slums has created another epidemic as a

result of inadvertent climatic modifications: the health risk crisis. In 2007, the capital of

Bangladesh was home to 13.5 million people. By 2025, it hosted 22 million people. Neither the

city nor the country of India is able to meet the demand from its growing population. Common

consequences of overcrowding include sanitation issues, poor drainage, and fresh water scarcity.

Approximately one-third of Bangladesh’s population lives below the poverty line, and

approximately 17% live in extreme poverty (Shaw, Mallick, & Islam, 2013).

Isle de Jean Charles. Isle de Jean Charles, an island south of New Orleans, Louisiana, is

home to the Biloxi-Chitimacha-Choctaw Indians. Traditionally known as a fishing, trapping,

and hunting culture in Terrebonne Parish, this community has found itself inundated with water,

making it impossible for many to stay. Moreover, oil and gas companies have spent years in this

area dredging canals to run pipelines along Louisiana’s coast. Doing so has removed the barrier

17

of marshes protecting Isle de Jean Charles from storm surges (Maldonado, Shearer, Bronen,

Peterson, & Lazrus, 2013).

The continuous loss of land from dredging, erosion, sea level rise, and storm surges has

resulted in the U.S.’ first climate refugees. The Department of Housing and Urban Development

(HUD) awarded $48 million to relocate the entire community. HUD’s program director for the

grant, Marion McFadden, has stated that the agency must be “cognizant of the obligation to

taxpayers to not throw good money after bad” (Davenport & Robertson, 2016). Every analysis

of the remaining land has shown that the problems outweigh any feasible solutions to save the

community (U.S. Army Corps of Engineers – Mississippi Valley Division, 2013). Accordingly,

the current residents must agree to relocate to drier land, losing the land they have called home

for decades.

South Florida. In 2009, Monroe, Miami-Dade, Broward, and Palm Beach counties held

their first Southeast Florida Regional Climate Leadership Summit, during which leaders from

each county came together to discuss current and future climate pattern issues impacting their

communities. This summit led to the formation of the Florida Regional Climate Change

Compact. The goal of the Compact focused on coordinating advocacy efforts towards state and

federal policies, developing programs for mitigation and adaption strategies, and keeping the

lines of communication open between the four counties so that they may identify emerging

issues around climate resiliency. Serving over 5.6 million residents, these counties decided to

develop and advocate for policy reform because the impacts of inadvertent climate modifications

were affecting their communities (Southeast Florida Regional Climate Change Compact

Counties, 2012).

18

South Florida’s beaches are currently eroding away and coastal communities are

investing millions of dollars to protect the shoreline. As noted by a local reporter, “Even if

climate change isn’t to blame for the increased local erosion that followed Hurricane Sandy,

rising sea levels and expectations for intensified future storms is already affecting the decisions

about how to reconstruct roads and shorelines” (Reid, 2013). Coastal communities throughout

the state are seeking methods for the establishment of a climate resilient infrastructure – to

address current and future shoreline damage.

In 2013, the Compact worked to identify which roads, bridges, and airports were at risk

for storm surges, flooding, and sea level rise. Once identified, the counties worked on a plan to

determine which vulnerable infrastructures should be repaired and which should be built

elsewhere. The city of Miami Beach invested $500 million to install pumps throughout the

island to raise roads and seawalls. This measure mitigated damage caused by continuous sunny

day flooding that was occurring during the seasonal high tides (Flechas & Staletovich, 2015).

Environmental Policy: Clean Power Plan

Following the 2014 Climate Assessment Report, President Obama initiated global

warming legislation at the national level. The White House crafted the President’s Climate

Action Plan, which directed the EPA to reduce CO2 emissions from the electric utility sector. In

response, the EPA drafted the Clean Power Plan (CPP) to reduce the country’s CO2 emissions

from existing electric generating units by allowing states to develop an emissions reduction plan

consistent with their specific economic conditions, energy market, and energy generation

opportunities.2 The EPA’s intention for the CPP was for compliance to be flexible,

2 The CPP focuses exclusively on existing units. This rule does not focus on new units.

19

acknowledging that different states had unique opportunities to cut carbon emissions while

satisfying their energy demands.

In order for the EPA to meet this objective, several environmental economic models have

been utilized to determine which method allows the electric utility sector to reduce CO2

emissions while providing affordable electricity to their customers. Utilizing standard

environmental economic modeling, the EPA estimate that the CPP will reduce annual CO2

emissions by 32 percent below 2005 levels by 2030 (Clean Power Plan for Existing Stationary

Sources, 2015, sec. 40 CFR Part 60). The proposed CPP utilizes three methods that provide a

roadmap toward reducing carbon pollution.3 The final CPP establishes a uniform national CO2

emission performance rate for stationary combustion turbines (natural gas combined cycle) and

fuel-fired electric steam units (coal, natural gas, or oil). The final standards comprise the

foundation for EPA’s state-specific emission reduction goals.

Mitigating the Risk of Inadvertent Climate Modifications with Energy Policy

In order to protect its citizens, each nation must evaluate how it will mitigate the risks

associated with climate change. To date, only a few countries have attempted to quantify and

develop policies to mitigate the risks associated with climate disruptions. In the U.S., the CPP

serves as a first step in mitigating the risks associated with anthropogenic GHG emissions. If

industrialized nations reduce their emissions, the continued pressures on the world’s

environmental sinks may subside significantly. This reduction may stifle global temperature

increases, normalize precipitation patterns, and reduce land erosion in coastal communities.

3 The final BSERs focus on supply-side measures that reduce emissions from power plants, and do not rely on

demand-side energy efficiency (EE) as a building block. The EPA anticipates that, due to its low costs and potential

in every state, demand-side EE will be a significant component of state plans under the Clean Power Plan.

20

However, developing an effective environmental policy requires regulators to consider

the economic viability of the policy. Mitchell Polinsky (2011) shows that economic efficiency

considers the relationship between any set of cumulative benefits and the associated costs. Thus,

the EPA has determined that the CPP will have an economic impact on the electric utility sector,

and the benefits outweigh the actual cost to comply. These benefits include public health safety

and energy security.

There are concerns, however, that the CPP will increase net costs, which will be passed

down to electric company customers. An internal EPA analysis does show that customers will

experience some increase in electricity rates; but, over time, these costs will decrease (Hibbard,

Okie & Tierney, 2014). Hence, the EPA’s challenge is in finding a balance between the costs

and benefits of maintaining clean air in growing economies. As states enter this new frontier in

energy policy, investors will have to evaluate which technologies they support to reduce

emissions from the energy sector, while maintaining strong local economies (Staff, 2007).

Methods toward Compliance: Meeting the Emission Reduction Goals

The EPA uses 2012 as the baseline year from which to make a determination of the

emission reduction goals for each state. The CPP provides both states and electric companies

numerous options for reducing CO2 emissions. The emission reduction goals are tailored to the

electricity needs and capabilities of each state. In addition, the states may utilize other methods

to achieve their emission reduction goals. These outlined options include, but are not limited to,

investing in energy efficiency programs, renewable energy, fuel switching, and reducing use of

coal-fired electricity generation.

Florida’s Energy Future. For electricity generation, Florida’s fuel of choice has long

been natural gas. In 2011, the state saw an increase of natural gas to 57.7% of the net energy for

21

load (NEL). According to Florida’s Public Service Commission’s 2012 Ten-Year Site Plan,

utility companies throughout the state are encouraged to reduce their consumption of natural gas

by substituting more renewable energy and nuclear generation. In the 2015 Ten-Year Site Plan,

renewable energy is predicted to provide 1,638 MW of generation capacity, accounting for 2.8%

of overall state generation capacity.

In addition to renewable energy, Florida’s utilities must consider how to make consumer

energy consumption more efficient, improve efficiency standards for new construction, and

encourage energy efficient appliances for residential and commercial customers (Florida Public

Service Commission, 2015). Between the inclusion of energy efficiency programs, fuel load

switch, and increasing renewable energy capacity, Florida’s electric utilities will either need to

continue their normal business operations, or make additional adjustments to achieve the

emission reduction goals set by the EPA.

Compliance Factors

The EPA has assigned each state specific emission reduction goals. However, the EPA’s

CPP does not dictate how these standards are to be reached (Oates & Jaramillo, 2015). The EPA

requires states to develop and submit a state implementation plan (SIP) that establishes carbon

dioxide performance standards for the electric utility sector (Glaser, McGuffey III, & Gaines,

n.d.). These standards can be satisfied by establishing a best system of emission reductions

(BSER), which enable states to cut carbon emissions while meeting their energy demands and

maintaining economic growth (Oates & Jaramillo, 2015).

Depending on a state’s electricity production mix, it may elect to abstain from developing

a SIP. Similar to the Affordable Care Act, if a state does not submit a SIP to the EPA, then the

22

EPA will create a federal plan in lieu of the SIP (Glaser et al., n.d.). Ideally, each state should

create an SIP that considers the most economically efficient plan to minimize cost increases to

utility customers, or at least reduce costs over time. In the process, states that make an effort to

satisfy the SCC will have a better understanding of the potential economic and health benefits

associated with the CPP.4

The final rule allows states to select which approach they will use to achieve their

emission reduction goals. This includes either an emissions standards approach or a state

measures approach. If a state pursues an emissions standards approach, it will be required to

implement the federally enforceable emissions rate standards at the affected unit level. This

approach has the potential for multi-state collaborations with an emission rate or mass-based

trading system.

The state measures approach provides states with the flexibility to achieve the equivalent

CO2 emission standards by using the emissions standards at the unit level in conjunction with

other standards that are enforceable by the state. If these enforceable plans do not achieve their

targeted emission reduction goals under the state measures approach, the federally enforceable

standards will take precedent.

4 The SCC does consider the economic and health benefits to some extent. However, these marginal economic and

health costs and benefits are only estimates. Several research studies, as well as the EPA’s Regulatory Impact

Analysis, argue that it is impossible to determine all of the economic and health benefits. What is included in the

SCC currently can only be considered a limited estimate of economic and health benefits, since there is no real

consensus on the calculations.

23

Supreme Court Litigation

On June 29, 2015, the Supreme Court, found that the EPA should have considered cost

when it published the Mercury and Air Toxics Standards (MATS) (Michigan v. EPA, 2015). The

MATS rule was designed to protect the public from mercury emissions and other air pollutants.5

The Supreme Court’s decision regarding the MATS rule played a pivotal role in the

considerations for CPP. The Court decided that the EPA could establish that a regulation was

“appropriate and necessary” if the agency considered compliance costs at the onset of the

rulemaking process. The EPA did not consider the cost of compliance when they enacted the

MATS rule. The cost concerns at the center of the mercury rule decision did not apply to the

CPP, since the CPP was drafted under a different Clean Air Act (CAA) provision that explicitly

required the EPA to consider cost. Moreover, the flexibility under the CPP allowed states to

choose the best method to reduce CO2 emissions by using the most cost effective method

available.

In early 2016, 29 states, including Florida, petitioned the Supreme Court to issue a stay

pending the D.C. Circuit’s review the CPP. The states argued that the CPP was an unattainable

and burdensome regulation (State of West Virginia, State of Texas, et. al v. United Stated

Environmental Protection Agency, and Regina McCarthy, 2016, p. 10). In an unprecedented

decision, the Supreme Court ruled in favor of the CPP. The states and industry groups asserted

that EPA’s shifting of electricity generation from fossil fuels to other sources was outside the

5 The EPA determined that “mercury is highly toxic, persistent, and bioaccumulates in food chains”, and therefore

was “appropriate and necessary” to regulate emissions under §7412. However, this decision was made without any

consideration of costs. (Brief of the Federal Respondents, State of Michigan v, Environmental Protection Agency, et

al., Utility Air Regulatory Group v. Environmental Protection Agency, et al., National Mining Association v.

Environmental Protection Agency, et al., 2015).

24

scope of the provision in the CAA. 6 Accordingly, the states were not required to begin working

towards satisfying the terms of the CPP until the D.C. Circuit completed its review. The goal in

petitioning was to prevent a similar outcome to that of the Michigan v. EPA, 135 S. Ct. 2699

(2015) decision. Because the regulation being challenged in this case was not maintained, states

were required to comply with a law that was later overturned by the Supreme Court.

The Court’s decision to order a stay suggested that a majority in the Court were

questioning whether the EPA had the authority to use the CAA to craft the CPP. The Attorney

General’s response to the motion argued that the CPP “identifies highly cost-effective and

proven emission-reduction strategies that are already widely employed by power plants”

(Respondent EPA’s Opposition to Motions to Stay Final Rule, State of West Virginia, State of

Texas, et. al v. United Stated Environmental Protection Agency, and Regina McCarthy, Docket

#1586661, 2015).

In a separate brief opposing the stay, respondents, including several South Florida

communities, asserted that any stay ordered by the Court would cause irreversible harm to many

areas in the U.S. that were already experiencing the effects of a modified climate pattern. This

legal battle seemed to utilize the same data to support different conclusions. The petitioners in

this case pointed to a decline in the nation’s coal industries as a result of the regulations placed

on the energy generating facilities, forcing them to switch to other fuel sources. The

respondents, in contrast, used the same data to argue that, as natural gas prices continued to

decline, natural gas had become a cost-competitive solution for utilities to switch to. This

6 Generation shifting, as noted in the petition, is what the EPA is employing to shift electricity generation from fossil

fuels to renewable energy. The EPA is using Section 111(d) to support its crafting of the CPP.

25

dispute among states, utilities, local government and communities, and environmental groups has

continued into the latter part of 2016.

The Path Forward

This research evaluates the opportunities associated with the implementation of the

CPP. Using standard environmental economic methods, the analysis of the CPP will help guide

states in determining the economic impacts of this energy policies. The CPP will undoubtedly

force Florida’s power generation sector to spend a significant amount of money in order to

comply with the regulation. However, doing nothing will cost future Floridians financially and

affect their communities (Kinniburgh, Greer Simonton, et al., 2015). As evidence, Miami Beach

is currently investing $400-$500 million to pump flood water associated with king tides from the

streets into the bay (Flechas & Staletovich, 2015). Thus, past ignorance of CO2 emissions is

forcing coastal communities to spend resources for pumping systems with the hope that these

systems will help save their homes.

Structure of the Thesis

In the next chapter, a brief literature review of environmental economics, resource

allocation, and the economics of uncertainty is outlined. In Chapter 3, this study’s research

methodology is described in detail, including each policy scenario and overview of the cost-

benefit analysis. Chapter 4 is a detailed analysis of the results, covering the policy consequences

from each scenario in terms of emissions, generation, costs, societal benefits, as well as the costs

and benefits per Floridian. In Chapter 5, an evaluation is made of the CPP which demonstrates

that the environmental health benefits outweigh the cost to comply. The analysis shows that

there are available methods by which Florida can combat current and future climatic change. It

is argued that the use of a carbon fee will help Florida to finance climate resilient activities.

26

Chapter 2

Literature Review

This literature review surveys various methods used when developing a policy to address

possible environmental impacts. The goal of the Clean Power Plan (CPP) is to reduce

greenhouse gas (GHG) emissions from the electric utility sector. In order for the Environmental

Protection Agency (EPA) to meet this objective, several environmental economic models have

been utilized to determine which method would allow the electric utility sector to reduce carbon

dioxide (CO2) emissions while providing affordable electricity to their customers (Clean Power

Plan for Existing Stationary Sources, 2015, sec. 40 CFR Part 60).

Environmental Economics

Evaluating environmental resources draws from two major areas: economic goods and

free goods. An economic good is “anything which yields utility to someone and which is scarce”

(Asafu-Adjaye, 2000). If the total supply is less than the demand, then it is scarce. In contrast, a

free good represents a good in enough supply “to satisfy everybody’s wants at a zero price”

(Sullivan & Arias, 1972). Air is commonly considered to be a free good. However, pollution

emitted into the air has a cost associated with it, and these costs should be accounted for in the

development of environmental and energy policy.

Executive Order 12866, issued by President William J. Clinton in 1993, requires agencies

to use a cost-benefit analysis to determine the impacts of a pending regulation. The social cost of

carbon (SCC) is one method of calculating these costs. It allows agencies to incorporate the

benefits of reducing CO2 emissions into their cost-benefit analyses of “regulatory actions that

have small, or ‘marginal’, impacts on cumulative global emissions” (Environmental Protection

Agency, 2010, p. 2).

27

More specifically, the SCC represents the “incremental damage caused by the emission

of an incremental unit of CO2” (Hatase & Managi, 2015, p. 243). These incremental increases in

GHGs include “net agricultural productivity, human health, property damages from increased

flood risk, and the value of ecosystem services due to climate change” (Environmental Protection

Agency, 2010, p. 2). For the CPP, the EPA has determined that the costs will range from $40 per

short ton of CO2 in 2020, to $48 per short ton of CO2 in 2030 (Clean Power Plan for Existing

Stationary Sources, 2015, sec. 40 CFR Part 60).7

Impact on different Socio-Economic Groups. Kaswan’s (2014) research evaluates the

benefits and drawbacks associated with policies designed to reduce emissions, and how these

policies impact various socio-economic groups. The continued increase of greenhouse gases has

the potential to negatively affect every socio-economic group, especially those without the

resources to cope with and respond to a changing climate. Accordingly, the Department of

Defense (DoD) has announced that modifications to climate patterns “will aggravate problems

such as poverty, social tensions, environmental degradation, ineffectual leadership and weak

political institutions that threaten stability in a number of countries” (Frelinghuysen, 2014). The

problems noted by the DoD are comprised of actual costs associated with anthropogenic GHG

emissions. However, the costs associated with reducing emissions while slowing the rate of

inadvertent climate modifications will require a reduction in price of many goods and services

(Nordhaus, 2013). New technologies to reduce emissions will most likely require costs to be

7 According to Table 1 of the CPP, the EPA has determined that the climate benefit estimate reflects global impacts

from CO2 emission changes and does not account for changes in non-CO2 GHG emissions. Also, discount rates

applied to SCC are different from other estimates because CO2 emissions are long-lived and damages occur over

many years. The benefit estimates in this table are based on the average SCC estimated for a 3% discount rate;

however, it is important to consider the full range of SCC values. As shown in the RIA, climate benefits are also

estimated using the other three SCC estimates (model average at 2.5 percent discount rate, 3 percent, and 5 percent;

95th percentile at 3 percent). The SCC estimates are year-specific and increase over time.

28

passed to customers, directly affecting citizens of the lower socio-economic classes. For

example, the reduction of CO2 emissions in fuel economy for equipment used for farming may

have an increased the prices of equipment and the products produced.

Discount Rate. The discount rate is an essential economic analysis tool to determine the

effectiveness of an environmental policy. The discount rate accounts for the expected net present

value (ENPV) of a project at a constant rate equivalent to the net present value (NPV) decreasing

over time. Currently, each country uses its own method of calculating discount rates. Thus,

economists are generally unable to agree on “what is the appropriate value of an uncertain

future” (Weitzman, 2001). Arrow et al. (2013) notes that in the United States, the discount has

remained constant at 3%. Other countries, like the United Kingdom and France, use a declining

discount rate that addresses the “rate at which society is willing to trade consumption in the

future for consumption today” (Arrow et al., 2013, p. 349).

Since the discount rate considers future policy implications, the use of a constant rate

versus a declining rate should be compared. Should future generations be held less accountable

for current policy decisions? The time preference accounts for societal needs to receive goods

and services right away, while deferring costs to future generations (HM Treasury, n.d.)

According to the HM Treasury’s The Green Book: Appraisal and Evaluation in Central

Government, projects with a timeframe that exceeds thirty years, like the CPP, should use a

declining discount rate. However, the EPA has utilized a constant discount rate of 3% to

determine the potential benefits from reducing emissions. In addition to the 3% discount rate,

the EPA notes that its Regulatory Impact Analysis has determined climatic benefits at 2.5 %, 3

%, and 5% values (Environmental Protection Agency, 2015).

29

Resource Allocation

The CPP attempts to achieve Pareto efficiency by dividing resources while trying to

provide equitable solutions to all stakeholders. The goal of environmental policy generally

presumes that no group of people should exploit environmental resources to the detriment of

others (Sullivan & Arias, 1972). Therefore, the goal outlined by the EPA to reduce CO2

emissions could be viewed as an attempt to achieve Pareto efficiency through careful

management of energy markets. Through the allocation of resources to improve the lives of

many.

Richard Bishop (1993) illustrates how economic efficiency is achievable through the

market. Markets and governmental policies create incentives and rules to help achieve economic

efficiency. The CPP encourages states to become more energy efficient while considering their

energy markets. Reducing emissions through energy efficiency policies is one of the most

efficient methods to effectively preserve an energy supply (Yearwood, Travezan, Harmsen, &

van Toledo, 2013).

Regulators and financial markets alike are constantly considering how weather patterns

are changing, especially storm intensity, flooding, and droughts. Under these circumstances,

environmental policies and risk management are similar in that the determination of fairness

must be distributed to all individuals. Hultman et al. (2010) details how achieving a Pareto

efficient environmental policy and risk management can be considered together:

Climate change and associated policy responses raise many

questions familiar to risk management, including the relative

importance of familiar and unfamiliar risks, the fairness of their

distribution, the credibility of different sources of knowledge and

expertise, and our attitudes toward others from whom the threat

30

originates or who are responsible for preventing or failing to

prevent the unwanted outcome.

The CPP is an example of the EPA’s attempt to achieve Pareto efficiency by searching

for equitable solutions to meet the needs of all stakeholders. As with any policy, there are

economic costs associated with the CPP’s goal to reduce emissions. These economic costs must

be taken into consideration when assessing how to comply with this regulation. Due to the

unique resources and energy demands within each state, the economic impact will vary by state.

As such, each state requires a unique framework to achieve the EPA’s emission reduction goals.

It should be noted that there are differences between energy efficiency and economic

efficiency. However, in order to be considered a sustainable policy the CPP must consider the

environment, social equity, as well as economic viability. (Gillingham, Newell, & Palmer, 2009;

Thiele, 2013). The future welfare of all stakeholders should be considered throughout the policy

development process. The continuous economic growth of society, without policies in place to

combat inadvertent climate modifications, will most likely result in damage to the planet.

Stagnant economic growth will result in less damage, but will render more members of society at

an economic disadvantage in their ability to their environment.

Balancing economic growth and reducing environmental impact is a dilemma. An

environmentally sound policy should also consider the socio-economic impacts by considering

how the policy will protect citizens who are at risk from inaction (Thiele, 2013). The growing

desire for a higher standard of living may result in a better economic future for later generations

within an environment unable to sustain itself (Nordhaus, 2013).

31

Economics of Uncertainty

Emissions from CO2 have the potential to be controlled through the implementation of

policies to reduce the potential burden on future generations. In a report completed by Risk

Business, climate change has been compared to “an interest-only loan we are putting on the

backs of future generations” (Gordon, 2014). At the current rate of continuous GHG emissions,

future generations may not have the capability to mitigate impacts from environmental

deterioration. This leaves future generations to deal with an uncertain future.

Traditionally, economic theory assumes the decisions related to the consumption,

investment, and production of materials are made by impartial experts. The uncertainty in these

decisions is “ignored or explicitly ‘assumed away’” (BORCH, 1968). Implicitly, uncertainty is

not realistic to ignore. These uncertainties are accounted for by spreading the risk. The most

common risk aversion method is known as insurance, a bond or note that is paid now for use

later, and is dependent on the occurrence of particular events. By pooling the risk associated

with flooding, fire, or weather events, the insurance carrier is able to insure millions against

unpredictable occurrences. The insurance policy places a monetary value on every positive and

negative event tied to an insurance premium. This shift in the portfolio influences an

individual’s attitude toward the risk (Arrow, 1971).

The risk-sharing contracts (i.e., insurance policies) are dependent upon proportionate

collections from everyone in the risk pool. The use of insurance as a method to mitigate the

impacts associated with climate disturbances becomes a public good; everyone benefits from

spreading the risk. As such, an insurance policy that Floridians pay into can become a cost-

sharing mechanism that could fund climate mitigation efforts throughout the state.

32

The cost of carbon is highly contested and economists continually debate how to

calculate it. While that debate continues, coastal communities are forced to address and finance

their perpetual climate uncertainty. Should a cost-benefit analysis of compliance with the CPP

show excess monetary benefits, it could serve as a basis for the state’s insurance premiums for

risks related to inadvertent climate modifications.

33

Chapter 3

Method and Research Design

This research evaluates the potential economic impacts of the Clean Power Plan (CPP) on

the state of Florida. By using a straightforward cost-benefit analysis (CBA), estimates of the

long-term effects the CPP may have on Florida stakeholders have been calculated. Similar to a

study published by the Center for Climate and Energy Solutions, the goal of this analysis is to

provide high-level insights with which to guide policymakers and stakeholders through the

implementation of the CPP, or the implementation of any carbon dioxide reduction policy for

Florida.

The underlying assumptions and calculations crafted by the Environmental Protection

Agency (EPA) have been designed to create state-specific emission reduction targets, as well as

develop a standard CO2 emission performance rate. The CPP proposes multiple methods that

states may use to reduce carbon pollution from the electric utility sector. Conversely, there are

economic costs associated with CPP’s emission reduction policy. These economic costs must be

taken into consideration when analyzing how to comply with this regulation.

Due to the unique resources and energy demands within each state, the economic impact

of complying with the CPP varies by state. Thus, it is expected that each state will develop a

unique framework to achieve the EPA’s emission reduction goals. Accordingly, this study has

two goals. The first is to determine which predictive methods have the potential to provide

Florida with the best set of tools for achieving the emission reduction goals outlined in the CPP.

The second is to determine if the potential costs outweigh the benefits, and how the

implementation of these actions may impact Floridians in the future.

34

The proposed CPP applies four best systems for emission reduction (BSER)8 standards,

using a state’s 2012 baseline emissions to derive an attainable emission threshold for each state.

The four BSER approaches are as follows: (1) heat rate/efficiency improvements to coal plants;

(2) re-dispatch from high emitting sources to low emitting sources, like natural gas combined

cycle units; (3) investing in renewable energy by generating electricity from low-to-zero

emission sources; and (4) efficiency savings from demand side energy (EPA Webinar, 2014). In

its final draft of the CPP, the EPA removed BSER 4 and significantly modified approaches 1-3.

The new BSER approaches include the following: (1) improving energy efficiency of coal and

oil-fired steam turbines; (2) shifting load from high emitting sources to low emitting sources; and

(3) increasing the amount of renewable megawatts within the generation mix (Clean Power Plan

for Existing Stationary Sources, 2015, sec. 40 CFR Part 60).

Research Questions

This research addresses the following questions: (1) Which BSER, or mixture of

methods, can provide the best economic outcome for the Florida? (2) Which mixture of BSER

methods are economically viable while meeting the EPA’s emission reduction goals for the

development of a State Implementation Plan (SIP)?

With the results from this analysis, the Florida Department of Environmental Protection

(FL DEP) and other policymakers may gain some insight on how the state might comply with the

CPP. According to the EPA, the CPP will reduce emissions of CO2 and other air pollutants from

8 Under the Clean Air Act, section 111(d), the state plans must establish standards of performance that

reflect the degree of emission limitations achievable through the application of best system for emission reduction

(BSER) that, taking into account the cost of achieving the reduction and any air quality, health and environmental

impacts, and energy requirements.

35

the electric utility sector. Since each state is able to select which method it will use to reduce

emissions, the cost of compliance will vary. Therefore, this research focuses on calculating the

cost of compliance for Florida. Ultimately, this study aims to provide recommendations to the

FL DEP, or to the EPA, in the development of Florida’s SIP.9

Research Framework

The goal of this research is to determine which compliance methods might be best for

Florida to pursue in order to comply with the CPP. The research will not consider the recent stay

by the U.S. Supreme Court, current litigation before the federal appellate court, or the possibility

of future changes to policy direction. The flexibility of the CPP provides a framework within

which states can select methods to implement in order to reduce CO2 emissions, even though it is

not through a federal mandate. Florida’s unique ecosystem of porous limestone, property along

the coast, and energy production mix are significant reasons for the state to consider an

environmental policy that may mitigate the risks associated with modifications to climate

patterns, regardless of litigation outcome.

Research Method

This study seeks to evaluate the effects of policy actions and related opportunity costs.

To do so, modeling framework is used to describe any efficiency gains and losses. Synapse’s

Clean Power Plan Planning Tool (CP3T) has been used for all methodological considerations.10

9 If the FL DEP does not create a SIP, the EPA will create one for the state. On August 3, 2015, the EPA announced

its proposed federal plan for states that fail to submit an “approvable plan”. According to the EPA, “the federal plan

is an important measure to ensure that congressionally mandated emission standards under the authority of the CAA

are implemented” (Federal Plan Requirements for Greenhouse Gas Emissions from Electric Utility Generating

Units Constructed on or Before January 8, 2014; Model Trading Rules; Amendments to Framework Regulations,

2015) 10 CP3T is completely open-source. Users are free to make any changes to any of the formulas and/or inputs. The

tool is available for download at cp3t.com.

36

This tool provides a first-run scenario analysis of expected costs, generation, capacity, and CO2

emissions in complying with the final CPP. CP3T allows users to manipulate generation rates,

capacity factors, and emissions rates by state or multiple states, until the state’s mass base and

rate base goals are met (Knight, 2015). For the purposes of this study, CP3T has been used to

enter unit retirements, change capacity factors, adjust for the increase in renewables and energy

efficiency, and add natural gas fired combined cycle or combustion turbine generators.

In order to begin scenario modeling, the first step performed was to determine a baseline

case. The baseline provides a starting point for this analysis to which the proposed policy

actions are compared. As such, it serves as a primary point of comparison for an analysis of a

proposed policy action. This reference case compares the current state of the world to the

expected state of the world after a policy or regulation is enacted. By comparing reference and

policy across various scenarios, the impacts of a policy may be approximated. The policy cases

presented here represent Florida’s compliance with the final CPP’s mass base and rate base

goals.

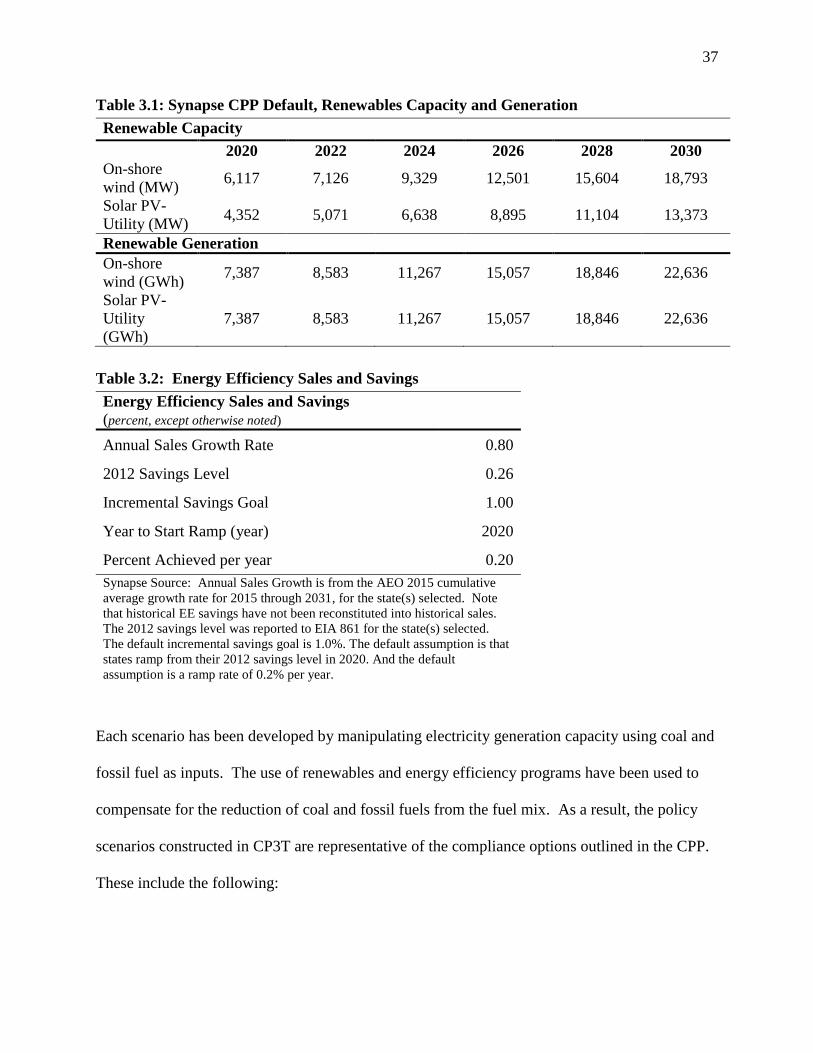

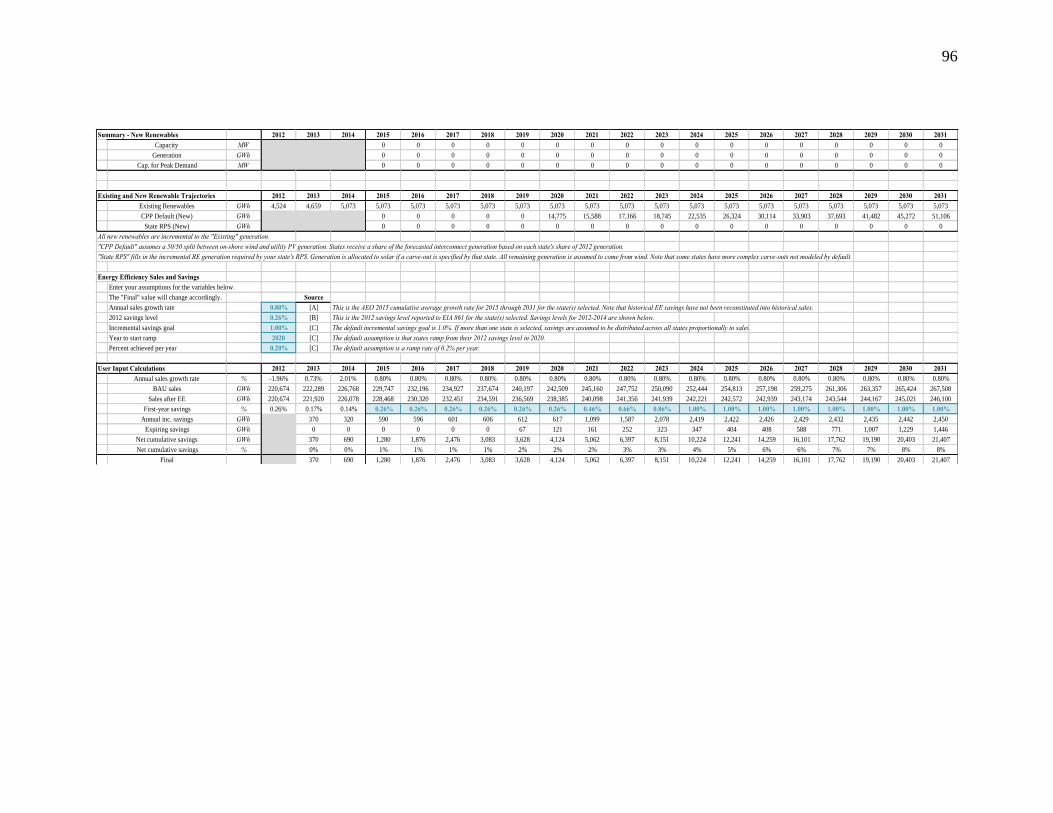

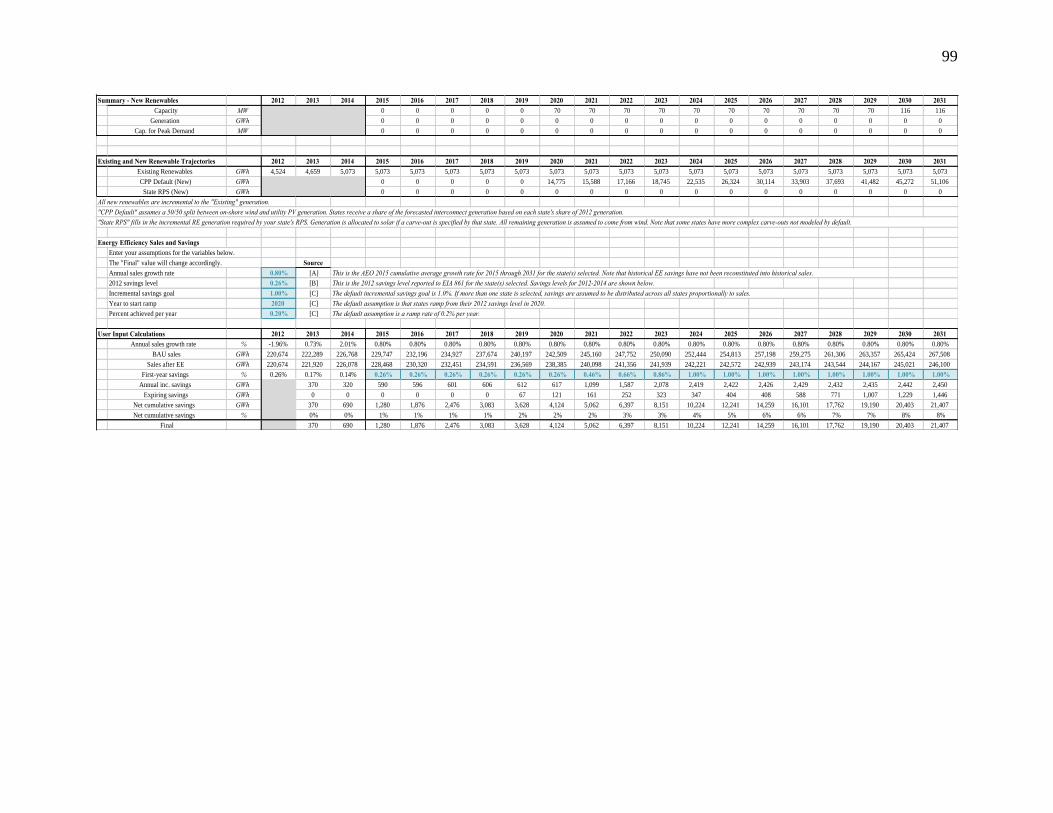

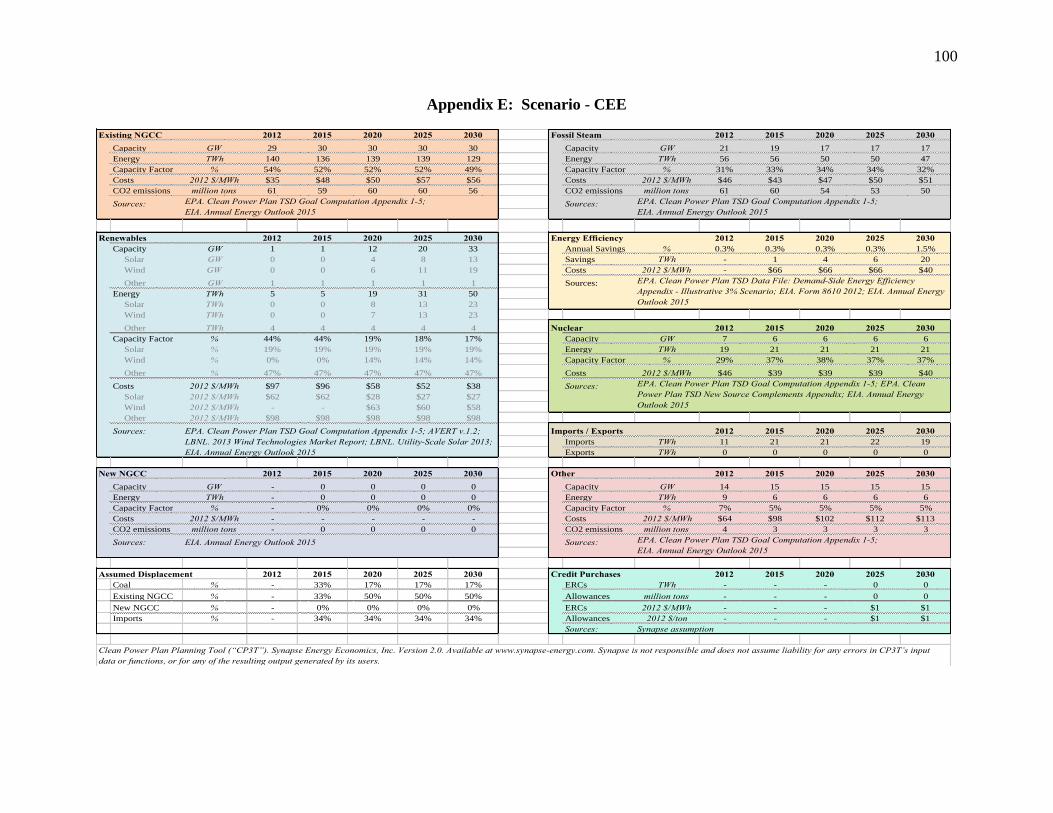

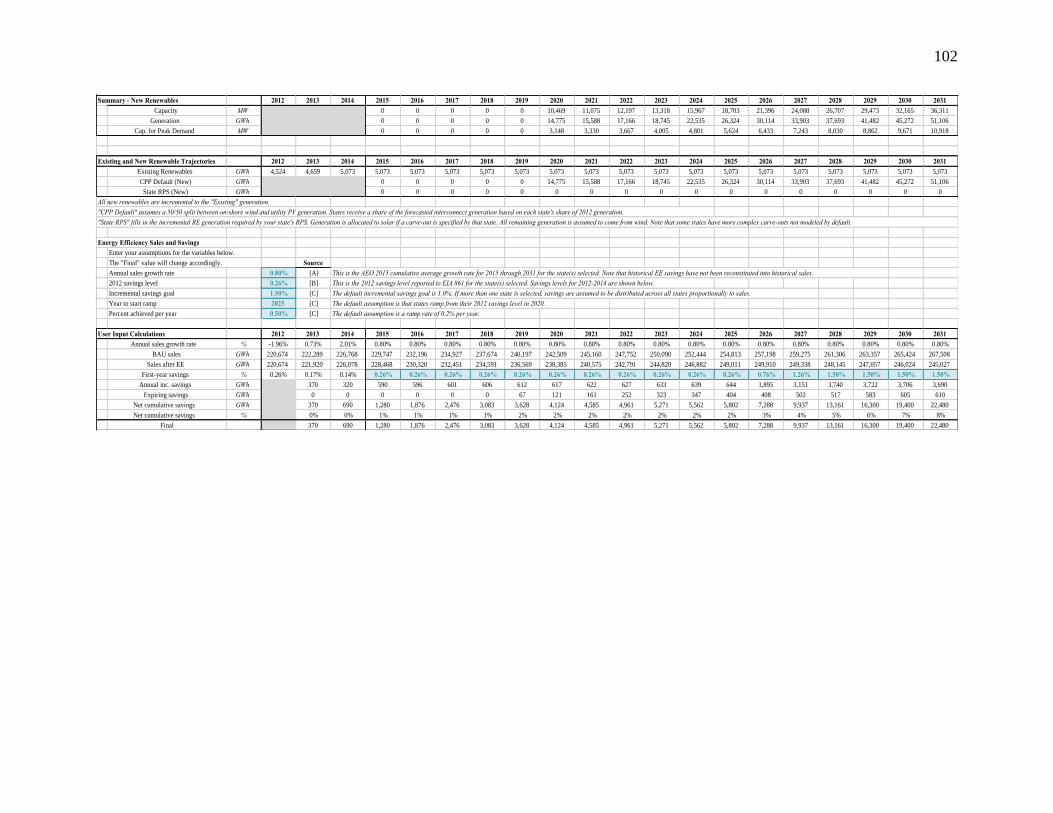

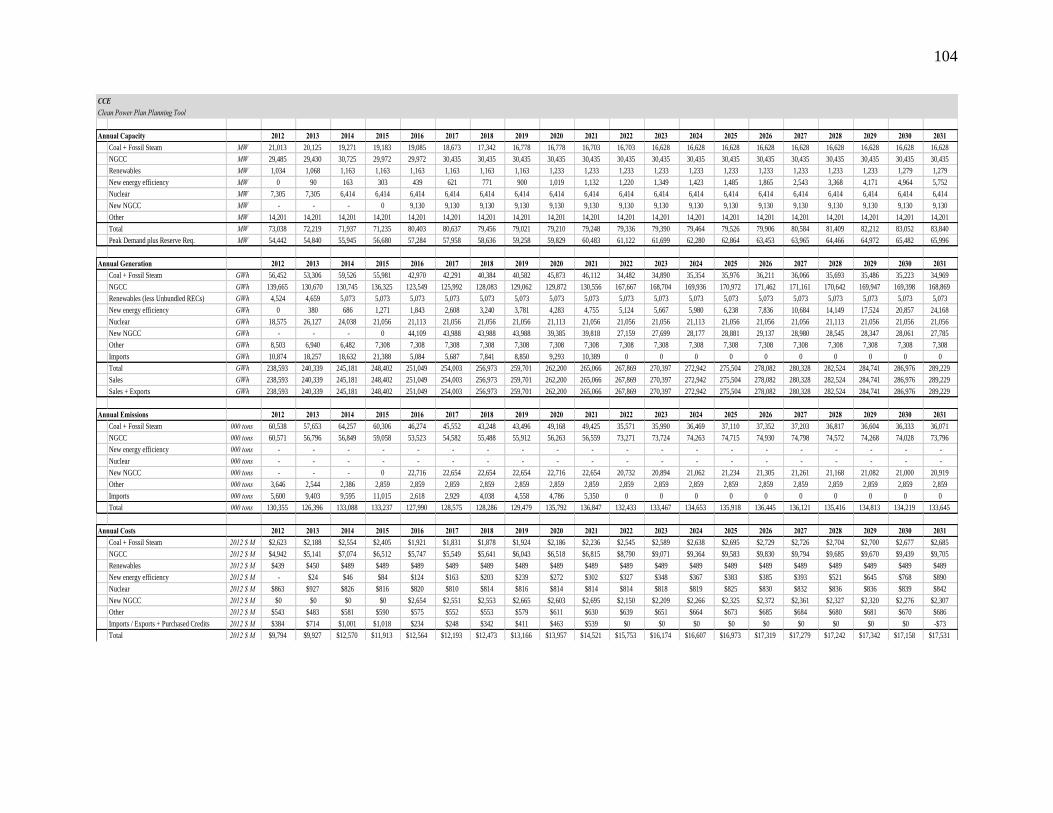

Scenario Methodology. For the reference case, Synapse’s CPP default for renewables

and state energy efficiency resource standard (EERS) for energy efficiency were used. The

renewables generation and capacity tab used in the CPP default are listed in Table 3.1. The

CP3T CPP default assumes that renewable generation from utility scale solar and on-shore wind

will be met by a 50/50 spilt. Selecting state renewable portfolio standard (RPS) or user input

switches, the renewable capacity beginning in 2020 is set to zero, thereby changing the rate and

mass base outputs significantly. The energy efficiency tab assumes Florida’s EERS will increase

by 0.2% per year until the 1% savings on sales are met, as noted in Table 3.2. This predictive

energy savings trajectory continues from 2012 into 2020.

37

Table 3.1: Synapse CPP Default, Renewables Capacity and Generation

Renewable Capacity

2020 2022 2024 2026 2028 2030

On-shore

wind (MW) 6,117 7,126 9,329 12,501 15,604 18,793

Solar PV-

Utility (MW) 4,352 5,071 6,638 8,895 11,104 13,373

Renewable Generation

On-shore

wind (GWh) 7,387 8,583 11,267 15,057 18,846 22,636

Solar PV-

Utility

(GWh)

7,387 8,583 11,267 15,057 18,846 22,636

Table 3.2: Energy Efficiency Sales and Savings

Energy Efficiency Sales and Savings

(percent, except otherwise noted)

Annual Sales Growth Rate 0.80

2012 Savings Level 0.26

Incremental Savings Goal 1.00

Year to Start Ramp (year) 2020

Percent Achieved per year 0.20

Synapse Source: Annual Sales Growth is from the AEO 2015 cumulative

average growth rate for 2015 through 2031, for the state(s) selected. Note

that historical EE savings have not been reconstituted into historical sales.

The 2012 savings level was reported to EIA 861 for the state(s) selected.

The default incremental savings goal is 1.0%. The default assumption is that

states ramp from their 2012 savings level in 2020. And the default

assumption is a ramp rate of 0.2% per year.

Each scenario has been developed by manipulating electricity generation capacity using coal and

fossil fuel as inputs. The use of renewables and energy efficiency programs have been used to

compensate for the reduction of coal and fossil fuels from the fuel mix. As a result, the policy

scenarios constructed in CP3T are representative of the compliance options outlined in the CPP.

These include the following:

38

Removing a majority of coal and fuel steam turbines from the fuel mix. A common

criticism of the CPP is that it perpetuates a war on coal. This scenario has helped to

determine if the operating costs outweigh the environmental benefits.

Adding additional energy efficiency and renewable generation to the fuel mix.

Environmental dispatch of units that consume the least amount of fuel to generate

electricity, i.e., natural gas generation.

39

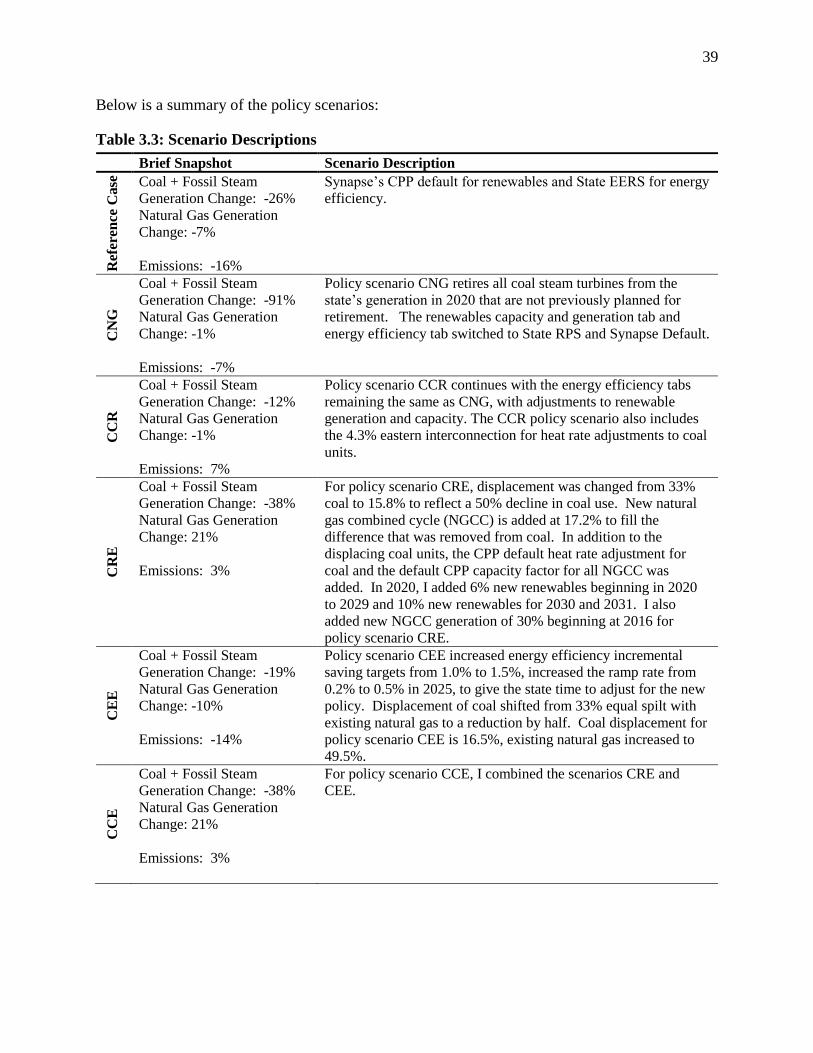

Below is a summary of the policy scenarios:

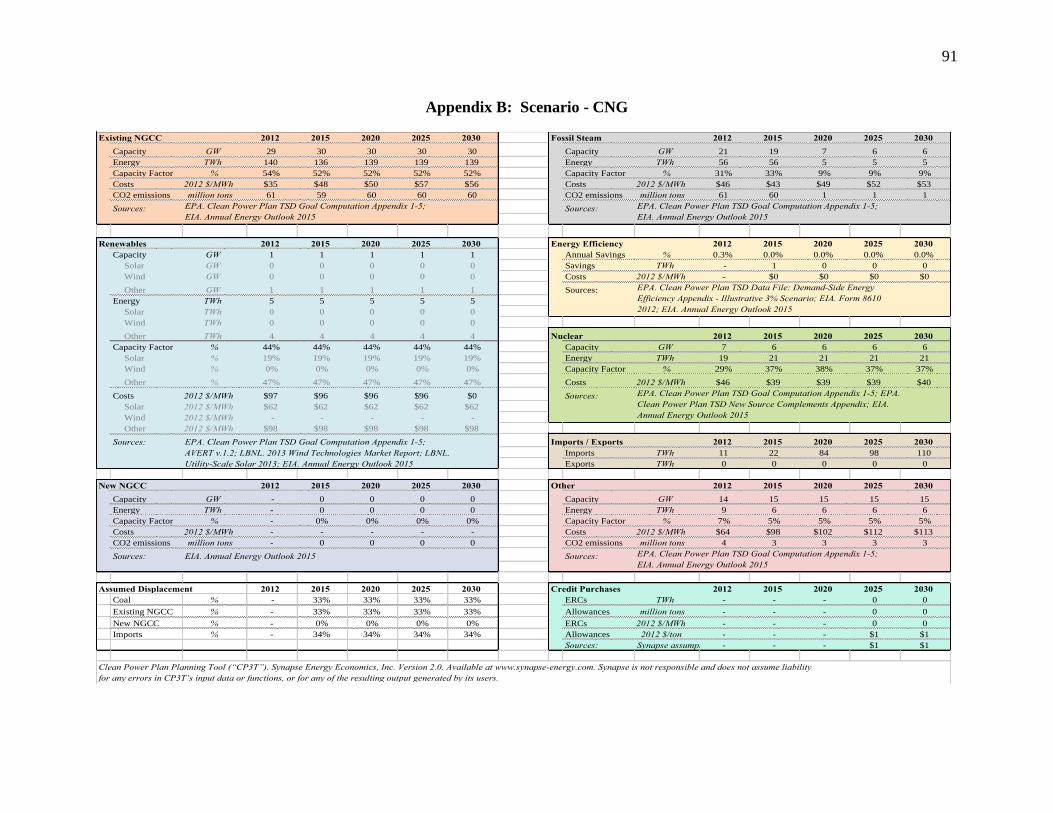

Table 3.3: Scenario Descriptions

Brief Snapshot Scenario Description

Ref

eren

ce C

ase

Coal + Fossil Steam

Generation Change: -26%

Natural Gas Generation

Change: -7%

Emissions: -16%

Synapse’s CPP default for renewables and State EERS for energy

efficiency.

CN

G

Coal + Fossil Steam

Generation Change: -91%

Natural Gas Generation

Change: -1%

Emissions: -7%

Policy scenario CNG retires all coal steam turbines from the

state’s generation in 2020 that are not previously planned for

retirement. The renewables capacity and generation tab and

energy efficiency tab switched to State RPS and Synapse Default.

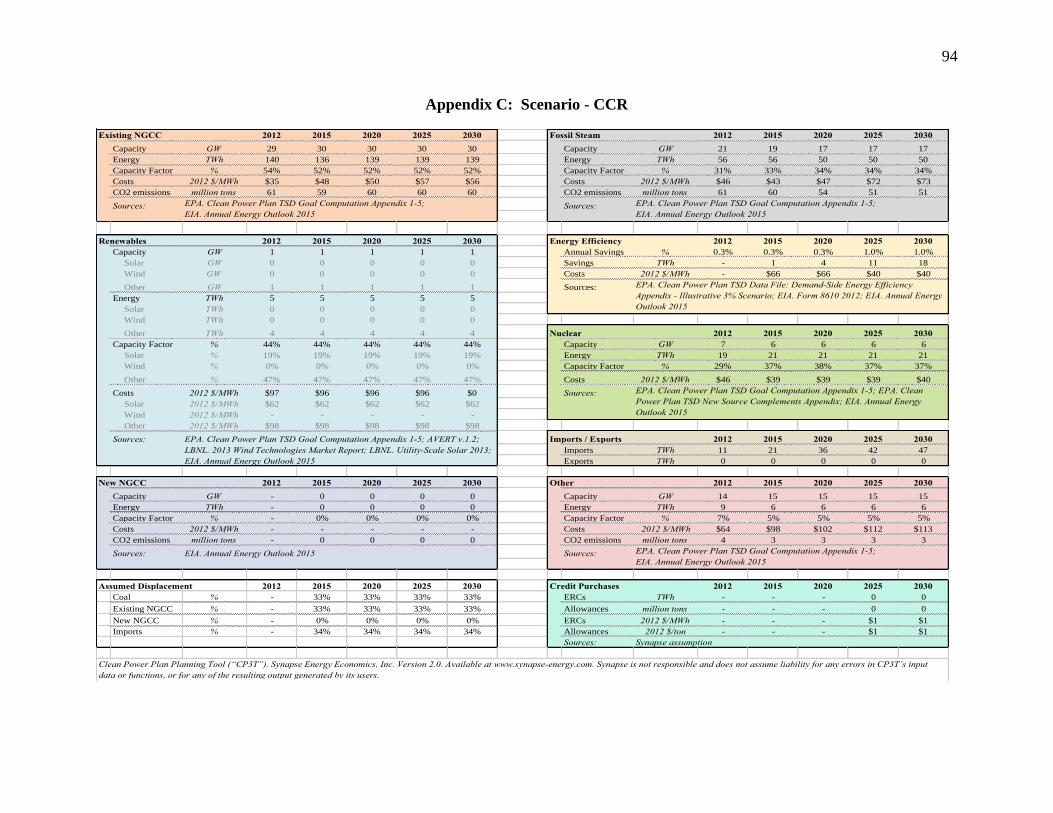

CC

R

Coal + Fossil Steam

Generation Change: -12%

Natural Gas Generation

Change: -1%

Emissions: 7%

Policy scenario CCR continues with the energy efficiency tabs

remaining the same as CNG, with adjustments to renewable

generation and capacity. The CCR policy scenario also includes

the 4.3% eastern interconnection for heat rate adjustments to coal

units.

CR

E

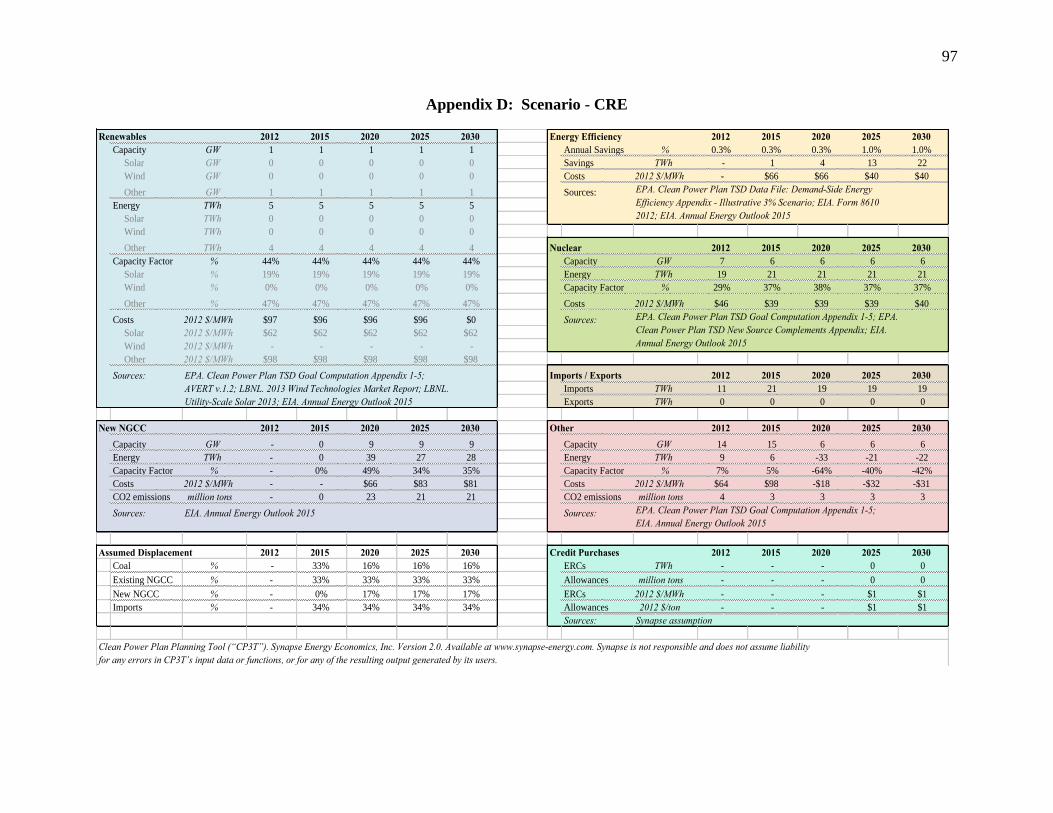

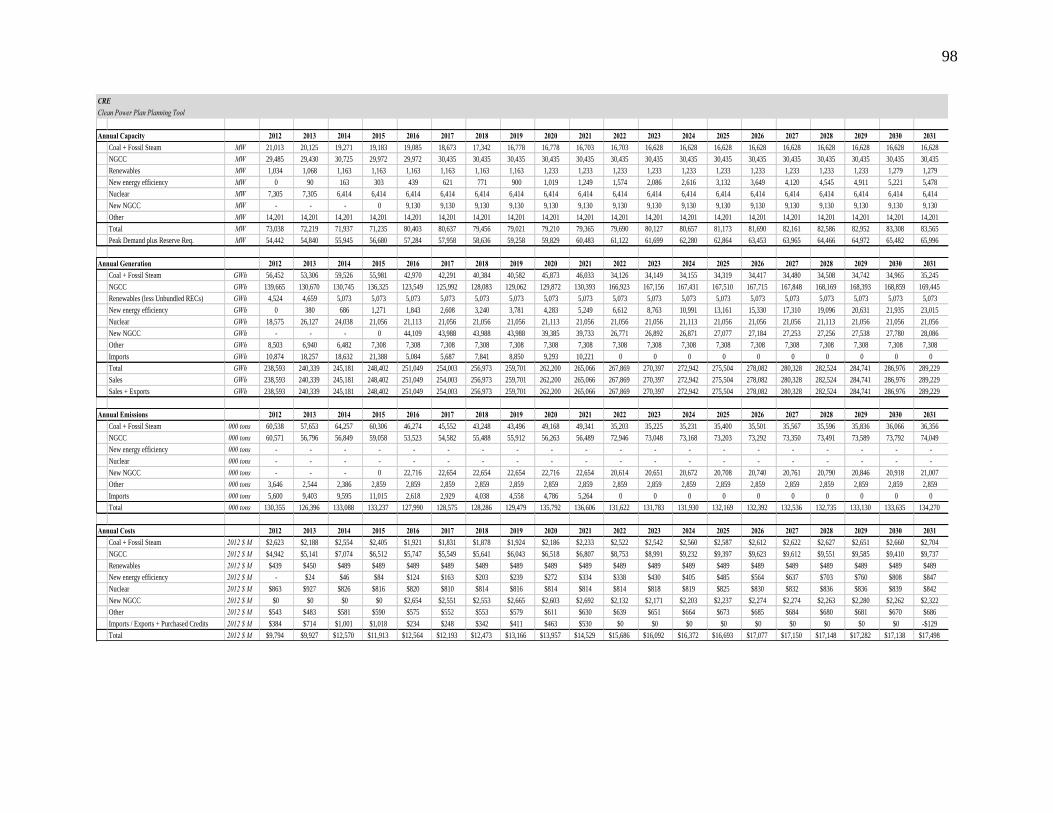

Coal + Fossil Steam

Generation Change: -38%

Natural Gas Generation

Change: 21%

Emissions: 3%

For policy scenario CRE, displacement was changed from 33%

coal to 15.8% to reflect a 50% decline in coal use. New natural

gas combined cycle (NGCC) is added at 17.2% to fill the

difference that was removed from coal. In addition to the

displacing coal units, the CPP default heat rate adjustment for

coal and the default CPP capacity factor for all NGCC was

added. In 2020, I added 6% new renewables beginning in 2020

to 2029 and 10% new renewables for 2030 and 2031. I also

added new NGCC generation of 30% beginning at 2016 for

policy scenario CRE.

CE

E

Coal + Fossil Steam

Generation Change: -19%

Natural Gas Generation

Change: -10%

Emissions: -14%

Policy scenario CEE increased energy efficiency incremental

saving targets from 1.0% to 1.5%, increased the ramp rate from

0.2% to 0.5% in 2025, to give the state time to adjust for the new

policy. Displacement of coal shifted from 33% equal spilt with

existing natural gas to a reduction by half. Coal displacement for

policy scenario CEE is 16.5%, existing natural gas increased to

49.5%.

CC

E

Coal + Fossil Steam

Generation Change: -38%

Natural Gas Generation

Change: 21%

Emissions: 3%

For policy scenario CCE, I combined the scenarios CRE and

CEE.

40

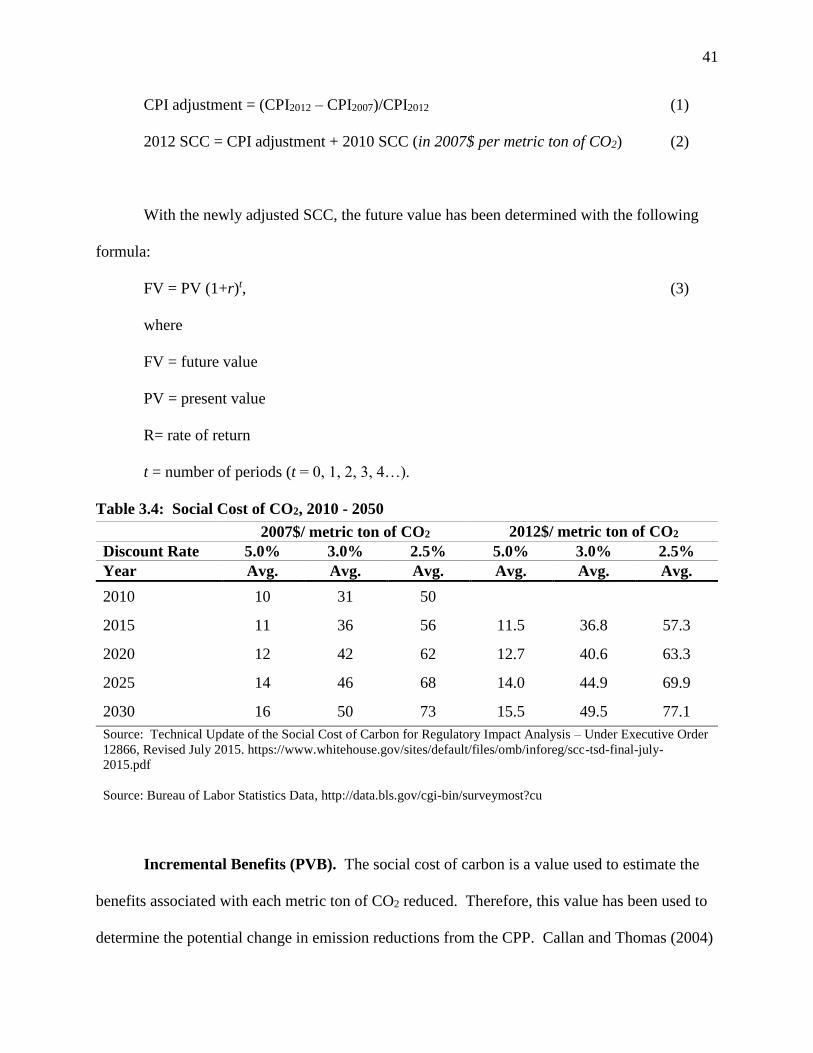

Adjusting Values for Cost Benefit Analysis. As noted in the Intergovernmental Panel

on Climate Change’s (IPCC) Climate Change 2014 Synthesis Report, effectively evaluating

policies that may cause disruptions to the climate involves “valuation and mediation among

diverse values and may be aided by the analytic methods of several normative disciplines”

(Pachauri & Mayer, 2015). Here, a CBA has been utilized. This standard method for evaluation

“reflects ethical principles, and take account of non-marketed goods, equity, behavioral biases,

ancillary benefits and cost and the differing values of money to different people” (Pachauri &

Mayer, 2015). Thus, this evaluation method enables holistic analysis of the CPP.

In order to determine if the CPP will be socially beneficial for Florida stakeholders, the

social benefits have been simulated until they reach Pareto efficiency (Asafu-Adjaye, 2000). To

determine the benefits associated with the CPP, the highly debated social cost of carbon (SCC)

estimate provided by the EPA has been used. Policy impacts to an individual’s income vary

depending on the benefits associated with an extra metric ton of emissions in a given year.

Depending on the economic tool used, the SCC varies greatly. The EPA has used three

integrated assessment models (IAMs) for estimating the SCC. The marginal social damages

associated with CO2 have not been determined to be zero. Since the debate on which

methodology to use for the SCC is outside the scope of this study, it has been determined that

using the EPA’s IAMs estimation will provide a fair representation of the predominant models

used.

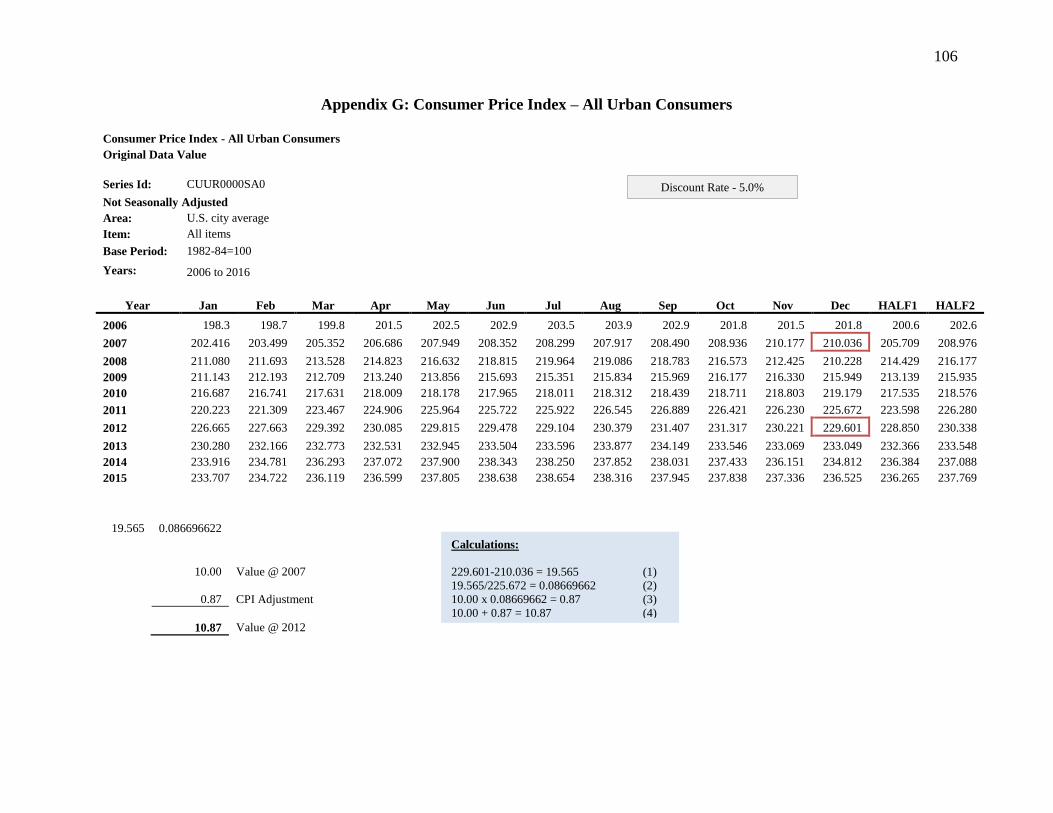

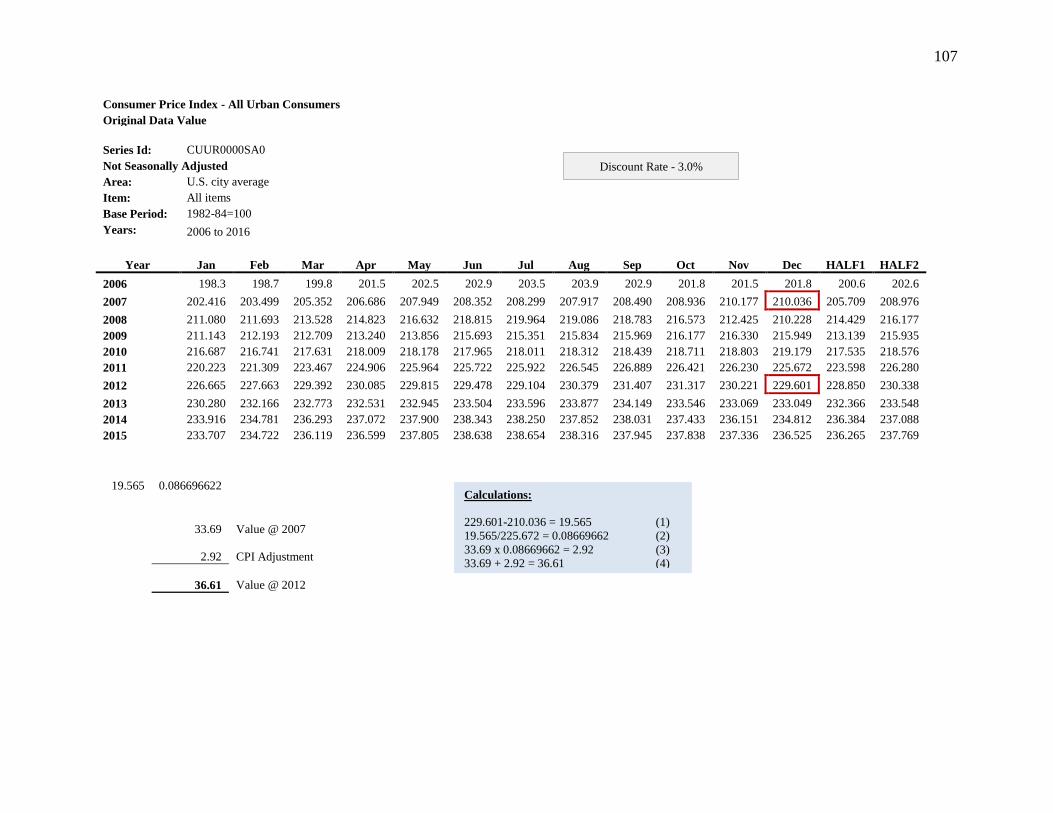

The revised SCC Technical Support Document published by the EPA for 2010-2050 has

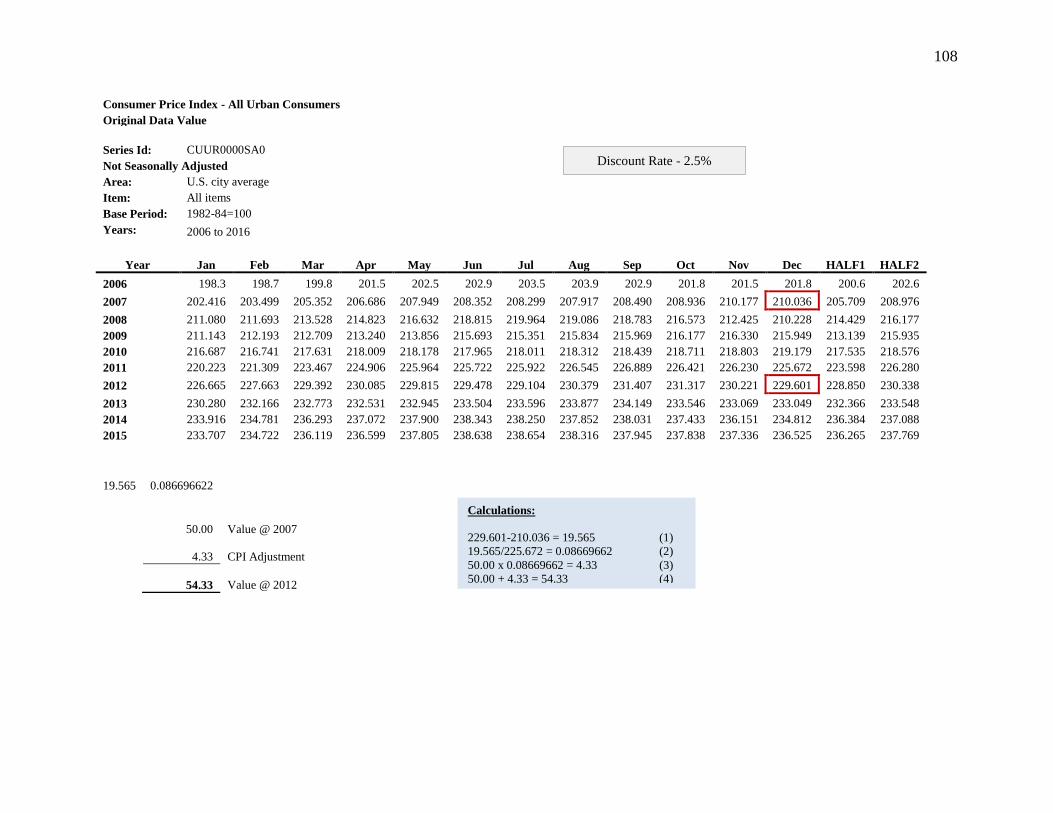

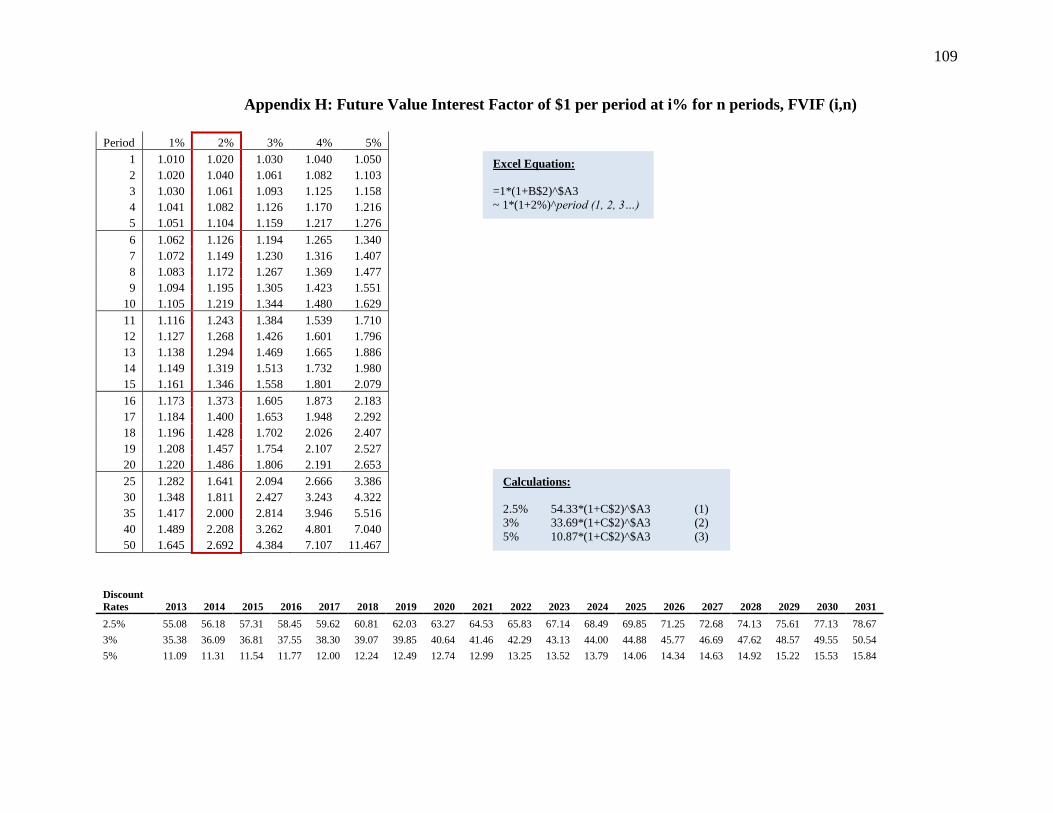

been calculated using 2007 dollars. In order to run an analysis consistently in 2012 dollars, the

Bureau of Labor Statistics’ Consumer Price Index (CPI) has been used to adjust all values. This

conversion uses the following simple formula:

41

CPI adjustment = (CPI2012 – CPI2007)/CPI2012 (1)

2012 SCC = CPI adjustment + 2010 SCC (in 2007$ per metric ton of CO2) (2)

With the newly adjusted SCC, the future value has been determined with the following

formula:

FV = PV (1+r)t, (3)

where

FV = future value

PV = present value

R= rate of return

t = number of periods (t = 0, 1, 2, 3, 4…).

Table 3.4: Social Cost of CO2, 2010 - 2050

2007$/ metric ton of CO2 2012$/ metric ton of CO2

Discount Rate 5.0% 3.0% 2.5% 5.0% 3.0% 2.5%

Year Avg. Avg. Avg. Avg. Avg. Avg.

2010 10 31 50

2015 11 36 56 11.5 36.8 57.3

2020 12 42 62 12.7 40.6 63.3

2025 14 46 68 14.0 44.9 69.9

2030 16 50 73 15.5 49.5 77.1

Source: Technical Update of the Social Cost of Carbon for Regulatory Impact Analysis – Under Executive Order

12866, Revised July 2015. https://www.whitehouse.gov/sites/default/files/omb/inforeg/scc-tsd-final-july-

2015.pdf

Source: Bureau of Labor Statistics Data, http://data.bls.gov/cgi-bin/surveymost?cu

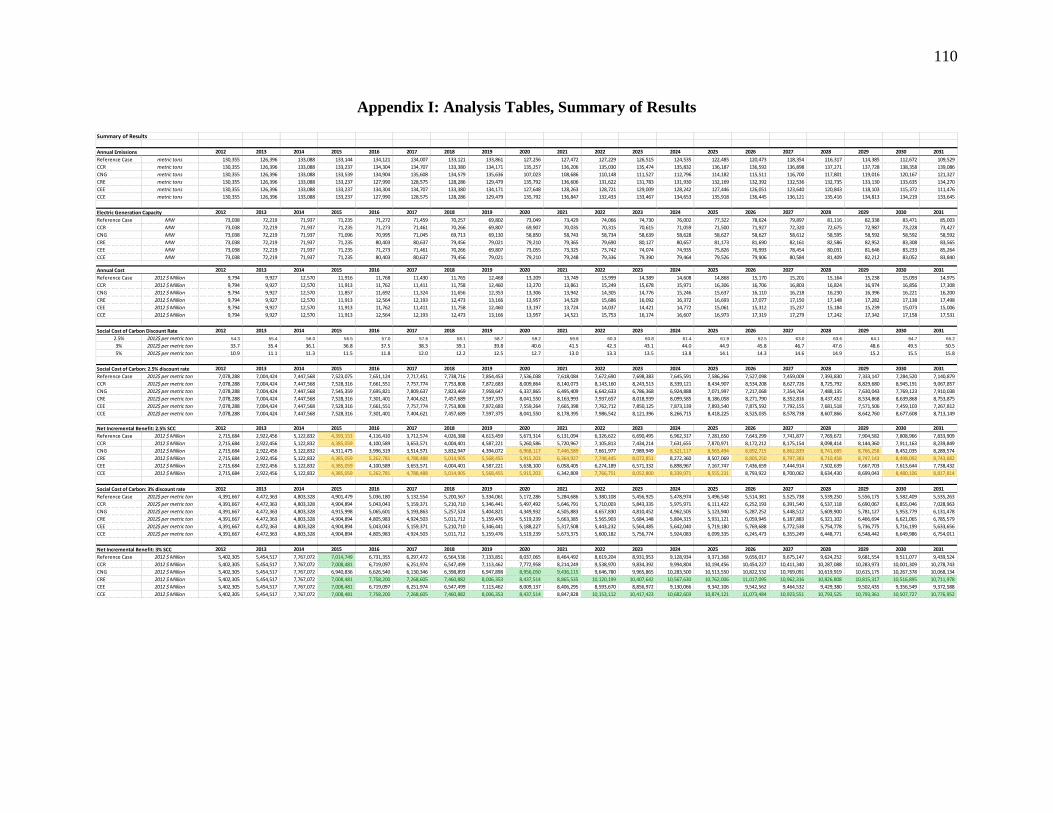

Incremental Benefits (PVB). The social cost of carbon is a value used to estimate the

benefits associated with each metric ton of CO2 reduced. Therefore, this value has been used to

determine the potential change in emission reductions from the CPP. Callan and Thomas (2004)

42

note that “the reduction in health, ecological, and property damages associated with an

environmental policy initiative” is the incremental benefit. Importantly, the evaluation of the

CPP must include the reduction of estimated damages over time in order to appropriately

measure the incremental benefits associated with the policy.

Incremental Costs (PVC). The CPP will require power generators to review their

operations in order to improve efficiency, change fuel load, or incorporate renewable resources

into their generation capacity. With these changes, explicit and implicit costs will be incurred.

These incremental costs include existing expenditures, costs after the policy is implemented, and

the difference between the two. The annual cost estimated by Synapse includes the operational

cost, fixed operational cost, and variable operational costs.

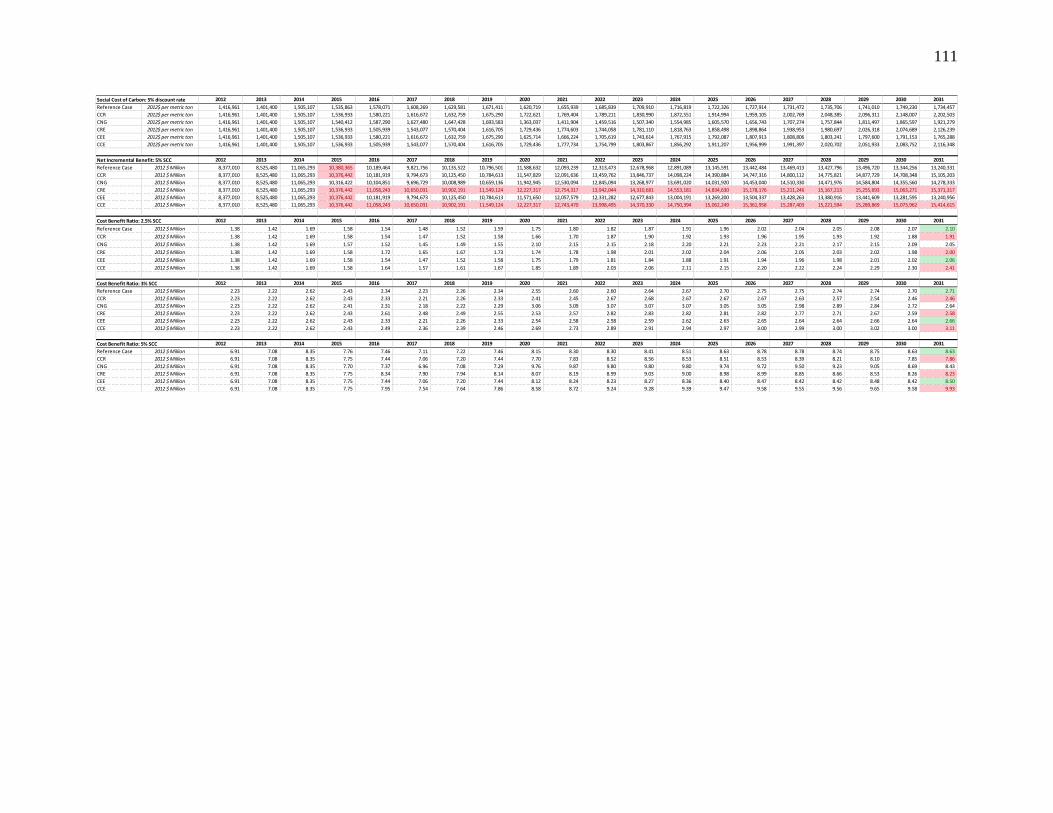

Cost-benefit Analysis Ratio. In order to distinguish which policy scenario may be the

best option, adjusted incremental costs and benefits have been compared. The PVB/PVC ratio

conveys the benefits of a policy option per dollar of costs incurred (Callan & Thomas, 2004).

Analysis with a cost-benefit ratio greater than 1 demonstrates that the benefits outweigh the

costs; hence, the net benefits are positive. A higher ratio begets larger benefits relative to costs.

If (PVB/PVC) > 1, for a given option, the option is considered feasible.

Costs and Benefits per Floridian. The costs and benefits for each policy scenario per

Floridian have been considered. To this ratio, the Florida’s Office of Economic and

Demographic Research projections for population have been used (Office of Economic and

Demographic Research, 2015). From there, the values obtained through the CBA have been

divided by Florida’s projected populations at various years to determine the potential costs and

benefits of the CPP per Floridian.

43

Limitations of Study

This research utilizes a CBA which provides a framework for quantifying and comparing

the costs and benefits associated with the CPP. The Synapse tool used for the evaluation of the

CPP as it relates to Florida has provided insights on the operating and maintenance costs

involved with this new environmental policy. Other related costs are not included. In a study

completed by Elizabeth Stanton and Frank Ackerman (2007), the cost of inaction is evaluated.

These costs are divided into (1) the loss of tourism revenue, (2) at-risk residential real estate, (3)

increase in electricity costs, and (4) damage from hurricanes. Due to time constraints, these costs

have not been incorporated into this analysis. Thus, both costs and benefits estimated here

should be viewed as conservative.