Embed Size (px)

Citation preview

Flash Memory Summit

OPEN Session 303G: Market Research

Flash Memory Summit 2016 Santa Clara, CA

1

© Copyright 2006 SASI, LLC. All rights reserved

Flash Memory Venture Funding &

M&A Insights August 11, 2016

John Rotchford, Managing Director, SASI, LLC

3

Violin Memory, $50M 6th Nimble Storage, $40.7M 5th

Pure Storage, $40M 4th STT, $36M 1st

Avalanche Technology, $30M 3rd

Pure Storage, $150M 5th Skyera, $52M 2nd

Crocus Technology, $45M Later

Tegile, $35M 3rd SolidFire, $31M 4th

Tintri, $75M 5th Pure Storage, $225M 6th

PernixData, $35M 3rd Reduxio, $15M 2nd

NVMDurance, $1M 1st

Top Five Rounds Tegile, $70M 4th

Crossbar, $35M 4th Nantero, $31.5M 5th

Everspin Tech., $29M 2nd Crocus, $21M 5th

$335M

$388M $351M

$230M

$92M

$0

$50

$100

$150

$200

$250

$300

$350

$400

2012 2013 2014 2015 1H 2016

Tota

l Fun

ding

($M

) 12 Rds.

Avg. $32.3M 5 Rds.

Avg. $70.2M

12 Rds.

Avg. $27.9M

9 Rds.

Avg. $25.5M

Year

Flash Memory Venture Funding

Elastifile, $35M 2nd Avalanche Tech, 23M 6th

Diablo Tech, $19M 3rd E8 Storage, $12M 2nd

NVM Durance, $2.5M 1st

5 Rds.

Avg. $18.3M

We are seeing a shift from larger, later stage rounds to smaller, earlier stage rounds. This is the second wave of innovation and will ramp into 2017 and 2018….

4

Flash Memory M&A Transactions

$860M

$2.04B

$1.72B

$0

$1

$2

$3

2012 2013 2014 2015

Tota

l Con

side

ratio

n ($

B)

9 Deals

Median Deal Size: $213M 6 Deals

Median Deal Size: $450M

9 Deals

Median Deal Size: $80M

4 Deals

Median Deal Size: $870M

Year

$20 $19.93B

EMC/XtremIO, $430M IBM/Texas Memory Systems $250M

NetApp/CacheIQ, $90M

SanDisk/FlashSoft, $70M

WD/Virident Systems, $645M

Cisco/WhipTail, $415M WD/STEC, $340M

SanDisk/SMART Storage Systems, $307M

Fusion-io/NextGen, $119M

SanDisk/Fusion-io, $1.1B

Seagate/LSI, $450M EMC/DSSD, $150M

Top Deals WD/SanDisk, $19.0B

NetApp/SolidFire, $870M Silicon Motion/Shannon Sys, $57.5M

Micron/Tidal Systems, ND

2016 is off to a slow start with one trade but we see M&A picking up in 2nd half of 2016, into 2017….

Flash Market Consolidation

Buyer

Software

Systems

Sub-Systems

Hybrid

SSDs/ Controllers

Cisco Whiptail (2013)

EMC DSSD (2014)

XtremIO (2012)

IBM Texas Memory (2012)

Intel Nevex (2012)

NetApp SolidFire (2015)

CacheIO (2012)

Toshiba OCZ (2013)

OCZ (2013)

Samsung Proximal Data (2014)

NVELO (2012)

Seagate LSI (2014)

LSI/ (2014)

Violin Memory

GridIron (2013)

Western Digital

SanDisk (2015) Velobit (2013)

Skyera (2014)

SanDisk (2015) Virident (2013)

SanDisk (2015)

SanDisk (2015) STEC (2013)

Micron Tidal Systems (2015)

5

We expect market leaders to fuel further consolidation in 2017…

Flash Memory Venture Market Map

Systems

Our market map has expanded across all segments…..

Sub-Systems

Hybrid

Memory/Controllers

(MRAM)

(CBRAM)

(NMV)

Software

(MRAM)

(NRAM)

6

(MRAM)

(RRAM)

(PCIe)

(NVMe)

(NVMe)

(NVMe

Flash Memory Summit

Chris DePuy, Dell’Oro Group

Flash Memory Summit 2016 Santa Clara, CA

7

GROUP DELL'ORO

Agenda

Flash Memory Summit 2016 Santa Clara, CA

8

§ Forecast of flash growth in storage infrastructure market

§ The role storage will play in transition from on-premise data centers to clouds

§ Discussion about external storage system architectures

§ Acquisition candidates in converged trend

Flash as % of Total Capacity in External Storage Systems

Flash Memory Summit 2016 Santa Clara, CA

9

0%

30%

60%

2015 2016 2017 2018 2019 2020

GROUPDELL'ORO

External Systems – Cloud vs Enterprise

Flash Memory Summit 2016 Santa Clara, CA

10

Ports on External Storage Systems and Their Connected Servers

Flash Memory Summit 2016 Santa Clara, CA

11

0%

30%

60%

2015 2016 2017 2018 2019 2020

Fibre Channel

SAS and Other

Ethernet

Ports

GROUPDELL'ORO

Share – Converged Components

Flash Memory Summit 2016 Santa Clara, CA

12

*2015 data; Data Center (DC) Switch from Ethernet Switch Deployment Location Report, Mar. 2016; Servers from 4Q15 Server Report

Branded Vendor Storage Servers DC Switch

EMCHPEDELLNetAppIBMHuaweiHitachiLenovoCiscoOracleArista & Juniper

Others

GROUPDELL'ORO

OBJECTIVE ANALYSIS

Big Changes For 2016 & Beyond

Jim Handy

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

OBJECTIVE ANALYSIS

Profound Analysts

Custom Consulting

Reports & Services

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

Objective Analysis Semiconductor Forecast Accuracy

Year Forecast Actual 2008 Zero growth at best. -3%

2009 Growth in the mid teens -9%

2010 Should approach 30% 32%

2011 Muted revenue growth: 5% 0%

2012 Revenues drop as much as -5% -2.7%

2013 Revenues increase nearly 10% 4.9%

2014 Revenues up 20%+ 9.9%

2015 Revenues up ~10% -0.2%

2016 Revenues up ~10% TBD

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

Outlook

• 3D NAND stall through 2017 – Breakthrough will occur in 2018

• Big collapse after that

• 3D XPoint won’t hurt NAND sales – DRAM is threatened

• China will begin huge CapEx spend • SSD unit growth steady

– But revenues will cycle

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

The Longer The Shortage, The Bigger The Collapse!

Collapse

Flat Pricing

Pric

e pe

r Gig

abyt

e

Time

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

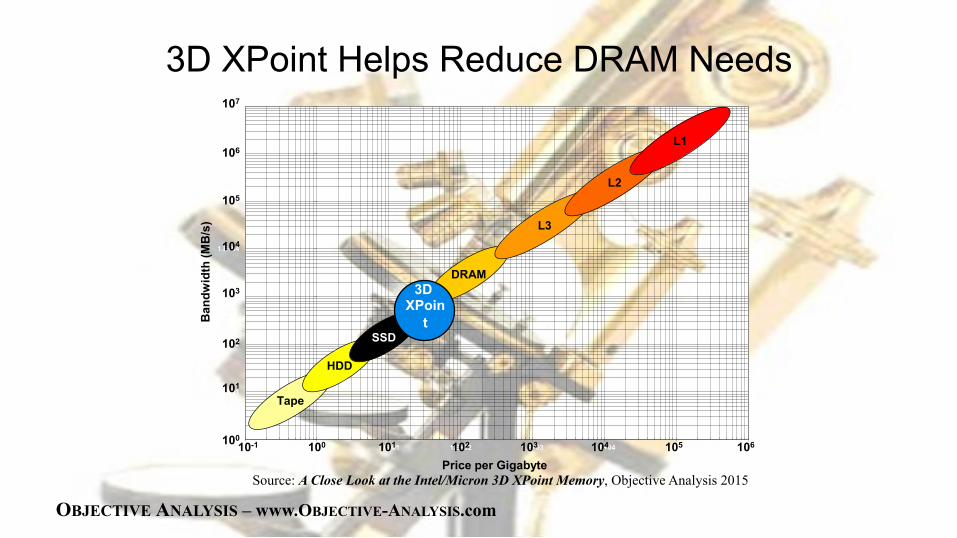

3D XPoint Helps Reduce DRAM Needs

1.E+00

1.E+01

1.E+02

1.E+03

1.E+04

1.E+05

1.E+06

1.E+07

1.E-01 1.E+00 1.E+01 1.E+02 1.E+03 1.E+04 1.E+05 1.E+06

Ban

dwid

th (M

B/s

)

Price per Gigabyte

Tape

HDD

SSD

DRAM

L3

L2

L1

101

100

102

103

104

105

106

107

101 102 103 104 105 10610010-1

3DXPoint

Source: A Close Look at the Intel/Micron 3D XPoint Memory, Objective Analysis 2015

3D XPoin

t

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

China Spending About to Begin

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

Steady SSD Unit Growth, But A Revenue Rollercoaster

$0

$10

$20

$30

$40

0

100

200

300

400

Rev

enue

s ($

B)

Uni

t Shi

pmen

ts (

Mu)

Units Revenues Source: Objective Analysis SSD Market Update 2015

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

Average IOPS by Application

0 500,000

1,000,000 1,500,000 2,000,000 2,500,000 3,000,000 3,500,000

Database OLTP Cloud Science & Eng

IOPS

Req

uire

d

From: How Many IOPS Do You Really Need? Objective Analysis & Coughlin Assoc.

OBJECTIVE ANALYSIS – www.OBJECTIVE-ANALYSIS.com

Summary

• 3D NAND Stall will break through to an oversupply • 3D XPoint is a threat to DRAM • Major China CapEx coming • SSD units grow, but revenues gyrate

OBJECTIVE ANALYSIS

Thank You!

Jim Handy

Beyond Traditional NAND Flash Marketing Research

Brian Dargel

Santa Clara, CA August 2016

The views expressed here are solely those of the author in his private capacity and do not in any way represent the views of Micron Technology Inc.

Traditional Flash Market Research

Financial Research

Market Share Predictions

Technology Trends

Application / end-Market trends

Geopolitics / Industrial Policy / National Initiatives ¶

Santa Clara, CA August 2016

Santa Clara, CA August 2016

Source: Wikipedia

Source: CNN

Source: WSJ

~1997~

Source:AOL Source: Wikipedia

Source: Time

Source: Wikipedia

Source: Time

Santa Clara, CA August 2016

Other

Source: ICE, Memory 1997

1997 Publication of 1996 Flash Memory Market Data (Start of the NAND ramp)

Santa Clara, CA August 2016

80 70 60 50 40 30 20 10 0

100 90

1992 1995 1999 2005 2010 2015

Other Other Other Other

Source: ICE, Web-Feet Research

Santa Clara, CA August 2016

Industry ‘Pivot’

Santa Clara, CA August 2016

Information Flow Industrial Policy

Santa Clara, CA August 2016

• Chaebols • Korean Peninsula •Abenomics • The IT decline

• Cross-strait relations • IT dependence • National Initiatives • Socialism with Chinese characteristics

• Presidential Election • CFIUS

Where is the rest of the world

Flash/SSD Markets

Mark Webb MKW Ventures Consulting, LLC

Flash Memory Summit 2016 Santa Clara, CA

32

Flash Market Projections

Flash Memory Summit 2016 Santa Clara, CA

33

§ Market Summary § SSD Units § SSD Adoption Rates

§ Predictions § What will not happen

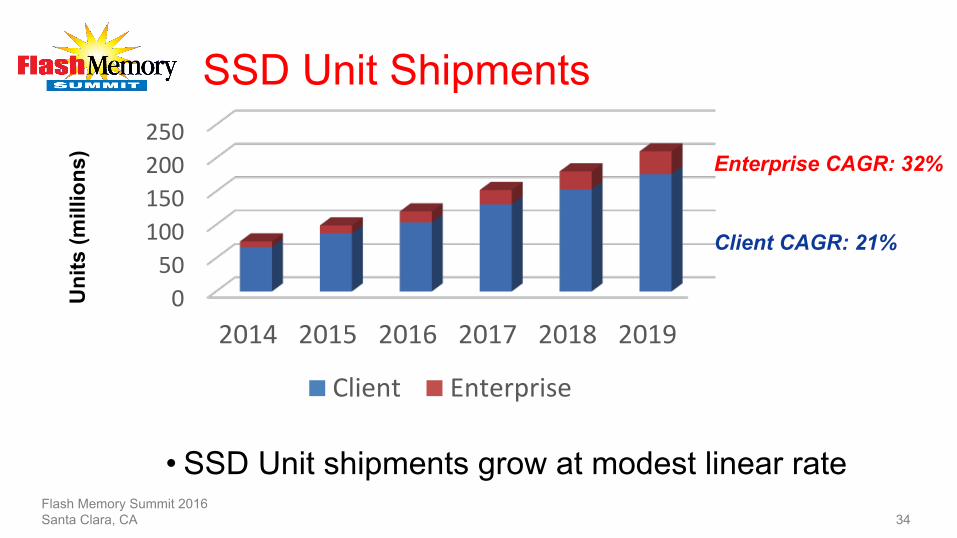

SSD Unit Shipments

Flash Memory Summit 2016 Santa Clara, CA

34

050100150200250

2014 2015 2016 2017 2018 2019

SSDUnitShipments(M)

Client Enterprise

Enterprise CAGR: 32%

Client CAGR: 21%

Uni

ts (m

illio

ns)

• SSD Unit shipments grow at modest linear rate

SSD Market Penetration

• SSDs are growing but still trail HDD

• Notebook: still TBD

• Tipping if cloud storage is first storage for 100% of notebooks

• Saturating if hybrid HDD or HDD still primary storage

• Enterprise: continues linear • 100% of performance

enterprise • <5% of capacity enterprise

Flash Memory Summit 2016 Santa Clara, CA

Predictions • SSD cost/GB drop 25% per year

• Prices 25% or more • TLC becomes dominant in all SDDs

• Client and Enterprise/Datacenter • Cloud/Hyperscale becomes dominate SSD market • Formfactors cost optimized for SSD applications

• M.2 for all applications • BGA for Phone/ultramobile, Notebooks

• SCM memory has multiple suppliers and technologies for >$1B market

Flash Memory Summit 2016 Santa Clara, CA

36

What Will NOT Happen

• HDDs will NOT go away • SCM memory will not replace DRAM or

NAND • No new major 3D NAND companies will arise

Flash Memory Summit 2016 Santa Clara, CA

37