Embed Size (px)

Citation preview

2

Fit for Future? The Pharmaceutical Industry in Europe 2020

Executive Summary

Views on Europe 2020

Trend-by-Trend Results

3Executive Summary

The Study – Purpose and Coverage

A joint survey by INSEAD and MANAGEMENT ENGINEERS among top executives of leading pharmaceutical companies reveals the industry perspective on the European Pharmaceutical Industry in 2020

*IMS Health, MAT Q1 2009

Study

Setup

Joint study elaborated by INSEAD and MANAGEMENT ENGINEERS

Objective: Industry perspective on the Pharmaceutical Industryin Europe in 2020

47 Top executives from 42 pharmaceutical companies took part in the survey

These companies account for 61% of global pharmaceutical sales*

18 of the top 20 global pharmaceutical companies are represented*

35 of the respondents are Global CEOs, Global Board Members or European Region Heads; the other 12 are Global Function Headsor Country Managers

Participants stem from three industry sectors: Originals/Biopharmaceuticals, Generics, OTC

StudySetup

4

Study Results at a Glance

Executive Summary

Our survey among top executives of leading pharmaceutical companies has revealed shared as well as divergent expectations about the Pharmaceutical Industry in Europe in 2020

Shared expectations for Pharmaceutical Industry in 2020 among virtually all

participants:

Payers are in control

Generics and biosimilars are first-line treatments

Transparent health technology assessments recognize and reward the added

value of new medicines

High-channel power reduces the industry‟s profitability

70% or more of all executives expect

Higher predictability of R+D success through early proof of concept

Integrated care models to prevail

Strong differences among participants regarding expectations concerning

the industry’s

I) Stature in 2020

II) Consumer centricity in 2020

Key Findings

lead to 3 executivesegments

Harves-ters

Consu-merists

New Golden Agers

5

Fit for Future? The Pharmaceutical Industry in Europe 2020

Executive Summary

Views on Europe 2020

Trend-by-Trend Results

6

European Pharmaceutical Industry: Influencing Factors

Views on Europe 2020

Pharmaceutical companies are impacted by a total of five trend clusters

*Healthcare Powerplay: payers, prescribers, patients, distribution channel

Governmental Policies

Healthcare Powerplay*

Societal Expectations

Industry Moves and

Innovation Potential

Global Megatrends

Influencing Factors The healthcare environment is changing

Leaders of pharmaceutical companies are

challenged to position their companies for the

future

To paint a vivid andcomprehensive picture of thepharmaceutical industry inEurope 2020 the study results

Provide valuable insight on industry trends from the perspective of top executives

Lead to strategic implications and hypotheses which help business leaders to shape their companies

1

2

3

4

5

7

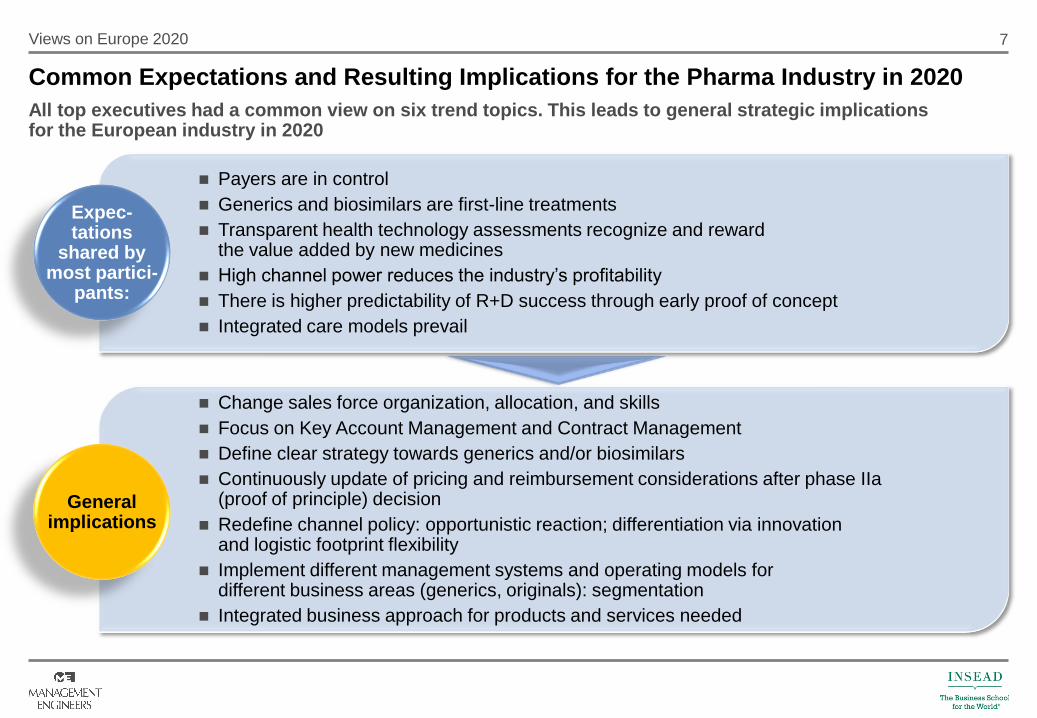

Common Expectations and Resulting Implications for the Pharma Industry in 2020

All top executives had a common view on six trend topics. This leads to general strategic implications for the European industry in 2020

Views on Europe 2020

Payers are in control

Generics and biosimilars are first-line treatments

Transparent health technology assessments recognize and reward the value added by new medicines

High channel power reduces the industry‟s profitability

There is higher predictability of R+D success through early proof of concept

Integrated care models prevail

General

implications

Expec-tations

shared by most partici-

pants:

Generalimplications

Change sales force organization, allocation, and skills

Focus on Key Account Management and Contract Management

Define clear strategy towards generics and/or biosimilars

Continuously update of pricing and reimbursement considerations after phase IIa(proof of principle) decision

Redefine channel policy: opportunistic reaction; differentiation via innovation and logistic footprint flexibility

Implement different management systems and operating models for different business areas (generics, originals): segmentation

Integrated business approach for products and services needed

8

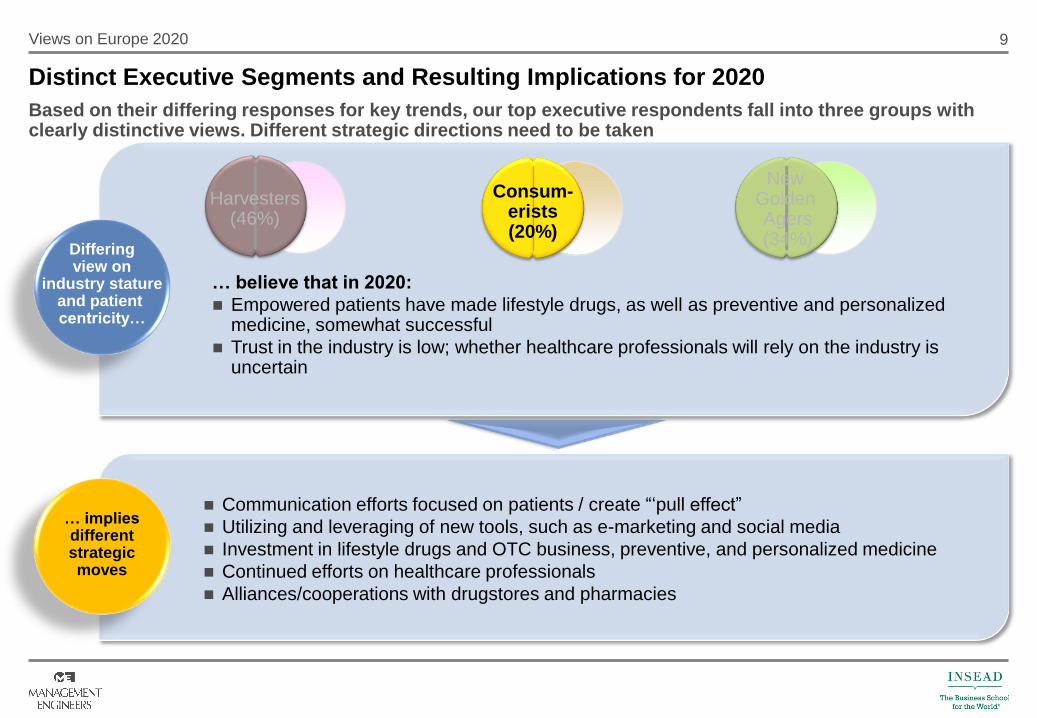

Distinct Executive Segments and Resulting Implications for 2020

Based on their differing responses for key trends, our top executive respondents fall into three groups with clearly distinctive views. Each of the three views implies different strategic moves

Views on Europe 2020

… believe that in 2020:

Biotechnology investments have paid off, but lifestyle drugs, preventive and personalized medicine have not

Patients rely on healthcare professionals who rely on the industry

Barriers to entry in biotechnology still exist but might fall in the future

Continued investment in protein research

No investment in lifestyle drugs, preventive and personalized medicine

Continued focus on healthcare professionals

… impliesdifferentstrategicmoves

Differingview on

industry statureand patient centricity…

Harvesters(46%)

Consum-erists(20%)

New Golden Agers(34%)

9

Distinct Executive Segments and Resulting Implications for 2020

Based on their differing responses for key trends, our top executive respondents fall into three groups with clearly distinctive views. Different strategic directions need to be taken

Views on Europe 2020

… believe that in 2020:

Empowered patients have made lifestyle drugs, as well as preventive and personalized medicine, somewhat successful

Trust in the industry is low; whether healthcare professionals will rely on the industry is uncertain

Communication efforts focused on patients / create “„pull effect”

Utilizing and leveraging of new tools, such as e-marketing and social media

Investment in lifestyle drugs and OTC business, preventive, and personalized medicine

Continued efforts on healthcare professionals

Alliances/cooperations with drugstores and pharmacies

… impliesdifferentstrategicmoves

Differingview on

industry statureand patient centricity…

Consum-erists(20%)

Harvesters(46%)

New Golden Agers(34%)

10

Distinct Executive Segments and Resulting Implications for 2020

Based on their differing responses for key trends, our top executive respondents fall into three groups with clearly distinctive views. Different strategic directions need to be taken

Views on Europe 2020

… believe that in 2020:

All technology bets (biotechnology, preventive and personalized medicine) have paid off; lifestyle drugs are somewhat successful

Patients rely on healthcare professionals who rely on the industry

Highest efforts put on establishment of product pipeline mix in biotechnology, preventive and personalized medicine (by inhouse R+D and/ or alliances / joint ventures)

Continued focus on healthcare professionals

Differentiated marketing approaches according to target segments and opinion leaders

… impliesdifferentstrategicmoves

Differingview on

industry statureand patient centricity…

New Golden Agers(34%)

Consum-erists(20%)

Harvesters(46%)

11

Executives’ Visions on Europe 2020: Industry Stature and Patient Centricity

Assuming that the industry currently suffers from a doubtful stature and is not consumer-centric, respondents, clustered in three groups, believe that 2020 will bring improvements for consumers, industry, or both

Views on Europe 2020

Consumer

centricity

Industry

stature

: 34% of respondents: 20% of respondents: 46% of respondents

Currentsituation in manyEU markets?

Current situationin the U.S.?

Society‟s trust is regained

Industry is main source of information for healthcare professionals

Biotechnology has paid off

Patients

decide on

pharma-

ceuticals

Lifestyle

drugs,

preventive

medicines

and perso-

nalized

medicines

are highly

profitable

Harvesters

Consu-merists New

Golden Agers

12

Executives’ Majority View

The study results provide answers about expected future scenarios

Views on Europe 2020

Governmental Policies

Healthcare Powerplay

Societal Expectations1

2

3

Industry Moves and

Innovation Potential

4

5

A slight majority is sceptical about

lifestyle drugs

Europeans livewith a two-class

medicine

Detailed patientdata is available

Trust is insufficient to avoid detailed governmental

regulations

Pricing and reimbursement

decisions reward the added value of new

medicines

The industry is themain source of

product informationfor healthcare professionals

Development costsand time reach

unprecedented highs

New retail channels

have made their mark

Greater buyer concentration drives down

industry profitability

Payers arein control

Pruning and increasing the number of indi-

cation segments are equally likely

The industryis dominated by

a few giants

Largepharmaceutical companies are unattractive for private equity

Integrated care models prevail

Biotechnology investmentshave paid off

R+D success is more predictable

Preventivemedicine is

highly profitable

Personalized medicine is highly

profitable and well accepted

Still waiting for patient empower-

ment

Generics and biosimilars are first-line treatments

Trend topics

13

Scenario A Scenario B

Lifestyle drugs are significant and highly profitable Lifestyle drug market is not significant

There is restricted access to innovative medicines Innovative medicines are accessible for all

Detailed patient data is accessible Patient data is limited to basic demographic information

Insufficient trust in industry; detailed regulations The industry has regained society‟s trust through self regulation

Transparent health technology assessmentrewards added value of new medicines Prices are based on a mere cost plus calculation

Healthcare professionals receive product information from neutral third parties

The industry is the main source of productInformation for health care professionals

Collaboration between industry and regulator has reduced development costs and time

Development costs and time are at new highs

Patients decide which pharmaceuticals to take; industry-to-patient communication is allowed

Patients rely on health care professionals; industry-patient communication is highly constrained

New retail channels have made their mark Pharmaceuticals are still sold mainly in traditional pharmacies

Profitability is reduced due to greater buying power Profit pressure can be offset by efficiency gains

Payers are in control Physicians have regained control

Generics and biosimilars are first-line treatments Patients and payers are willing to pay for brandsMost companies increase their number of indication segments Most companies reduce their indication segments

Today‟s leading pharmaceutical companies still exist in 2020

A handful of giant companies dominates

Large companies are not attractive for private equity Private equity has acquired and restructured some top 20 companies

Integrated care models succeed as new business models Most companies remain product focused

Biotechnology investments have paid off R+D investments in biotechnology have been reduced

R+D success is more predictable New technologies have not significantly increased R+D predictability

Preventive medicine is highly profitable Profits for preventive medicine are low

Personalized medicine is highly profitable Profits for personalized medicine are low

Beyond the Majority View: Consensus and Divergence

The average responses across all participants indicate the future trend expectations for the European Pharmaceutical industry

Views on Europe 2020

: Average peer responses

1.1

1.2

1.3

1.4

2.1

2.2

2.3

3.1

3.2

3.3

3.4

3.5

4.1

4.2

4.3

4.4

5.1

5.2

5.3

5.4

1 Predominantly agree 2 Partly agree

21 12

OVERVIEW

14

Fit for Future? The Pharmaceutical Industry in Europe 2020

Executive Summary

Views on Europe 2020

Trend-by-Trend Results

15

Patients not only seek treatment when they are sick, but increasingly look for ways to improve their overall well-being

Scenario A: Scenario B:

In Europe 2020, this paradigm shift has ledto lifestyle drugs becoming a significantand highly profitable part of thepharmaceutical industry. These products are available either by prescription with reimbursement, or as OTC, for which mostpatients are willing to pay

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, despite efforts of pharma-ceutical companies to react to the paradigm shift, the lifestyle drugs

market has not grown much. These products are available

only by prescription without reimbursement, and few

patients are willing to pay for them

Identify lifestyle conditions with high patient willingness to pay

Consumer marketing expertise is important

Use unbranded direct-to-consumer communication (condition branding)

Promote coverage of lifestyle drugs as an option by insurers

Organizational setup of key account and contract management towards payers

1.1 From Sick-Care to Well-Care

Societal Expectations: From Sick-care to Well-care

Trend-by-Trend Results

1

A slight majority is sceptical about lifestyle drugs as neither insurance nor patients will cover the costs

14%

37%30%

16%

A slight majority believes that the lifestyle drug market will not grow much in the future as neither insurance nor the patients themselves will be willing to cover the costs

2% undecided

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Note: Results do not total to 100% because of rounding

16

While healthcare provision is developing in the direction of a two-class system, society demands access to affordable healthcarefor all

Scenario B:Scenario A:

In Europe 2020, access to innovativemedicines for the broad public isrestricted. Growing healthcare costscause reimbursement to be limited to a selected number of products considered essential

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, access to innovative medicines for all is ensured through

public pressure against two-class medicine

Market research with payers to identify conditions and outcomes that are high priority for payers

Focus R+D activities and product portfolio on payer priorities

Demonstrate cost effectiveness

Promote insurance schemes that provide coverage for products not covered by basic insurance

Growth opportunities in Generics, Biosimilars and OTC businesses with strong regional differences

1.2 Two-Class Medicine

Societal Expectations: Two-Class Medicine1

Europeans live with a two-class medicine

The majority believes that two-class medicine seems unavoidable due to economic constraints

9%

30%25%

36%

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

17

A growing amount of patient data is gathered on e-health records, and patients are concerned about data ownership and the potential (mis)use by insurers, employers, and other parties

Scenario A: Scenario B:

In Europe 2020, patients have accepted thathealthcare professionals have access todetailed patient data including genetic information. Anonymous data isanalyzed to define (cost)effectiveand safe treatment strategiesfor different patient profiles

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, patients have control over which data is recorded and shared on

their e-health records. Most patients choose to limit the data to basicdemographic information, which

constrains the development and use of evidence-based

treatment strategies

Communicate the benefits of data sharing to patients and other key stakeholders

Promote and comply with legislation preventing data misuse

Ensure access to anonymous patient data, develop expertise in patient data mining, and integrate patient data use in development, marketing (product positioning) and sales

1.3 Patient Data Management

Societal Expectations: Patient Data Management1

Detailed patient data is available

The majority expects that by 2020 detailed patient data will be available on e-health recordsand can be analyzed as a basis for the development of improved treatment strategies

2%

30%

44%

23%

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

Note: Results do not total to 100% because of rounding

18

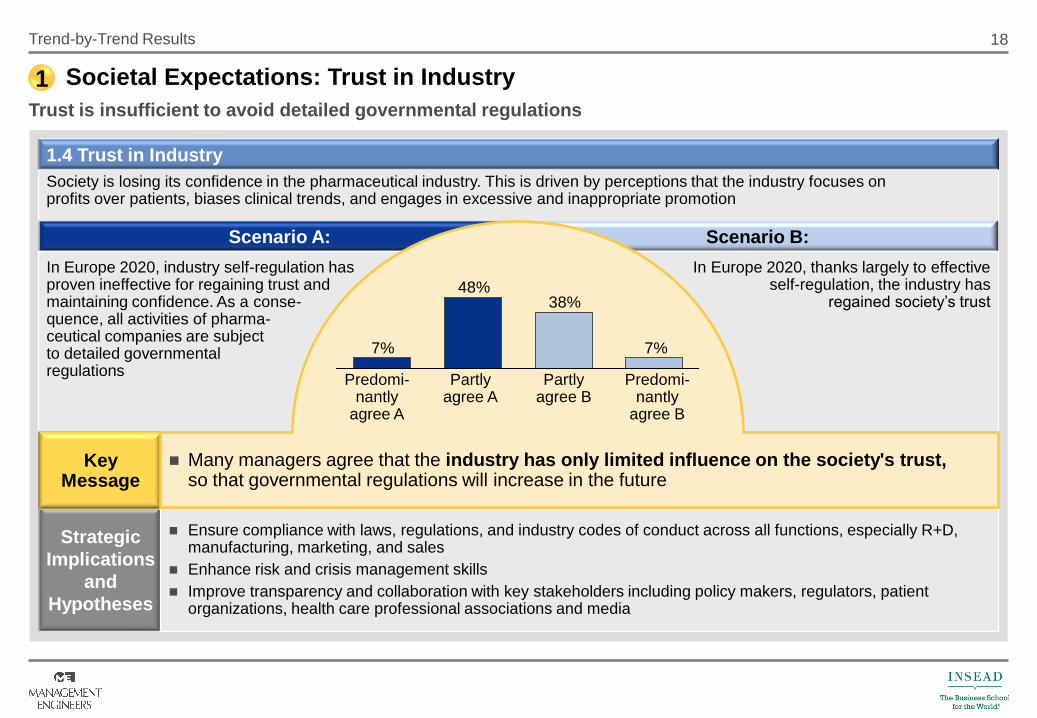

Society is losing its confidence in the pharmaceutical industry. This is driven by perceptions that the industry focuses on profits over patients, biases clinical trends, and engages in excessive and inappropriate promotion

Scenario A: Scenario B:

In Europe 2020, industry self-regulation has proven ineffective for regaining trust and maintaining confidence. As a conse-quence, all activities of pharma-ceutical companies are subject to detailed governmentalregulations

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, thanks largely to effective self-regulation, the industry has

regained society‟s trust

Ensure compliance with laws, regulations, and industry codes of conduct across all functions, especially R+D, manufacturing, marketing, and sales

Enhance risk and crisis management skills

Improve transparency and collaboration with key stakeholders including policy makers, regulators, patient organizations, health care professional associations and media

1.4 Trust in Industry

Societal Expectations: Trust in Industry1

Trust is insufficient to avoid detailed governmental regulations

Many managers agree that the industry has only limited influence on the society's trust, so that governmental regulations will increase in the future

7%

38%48%

7%

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

19

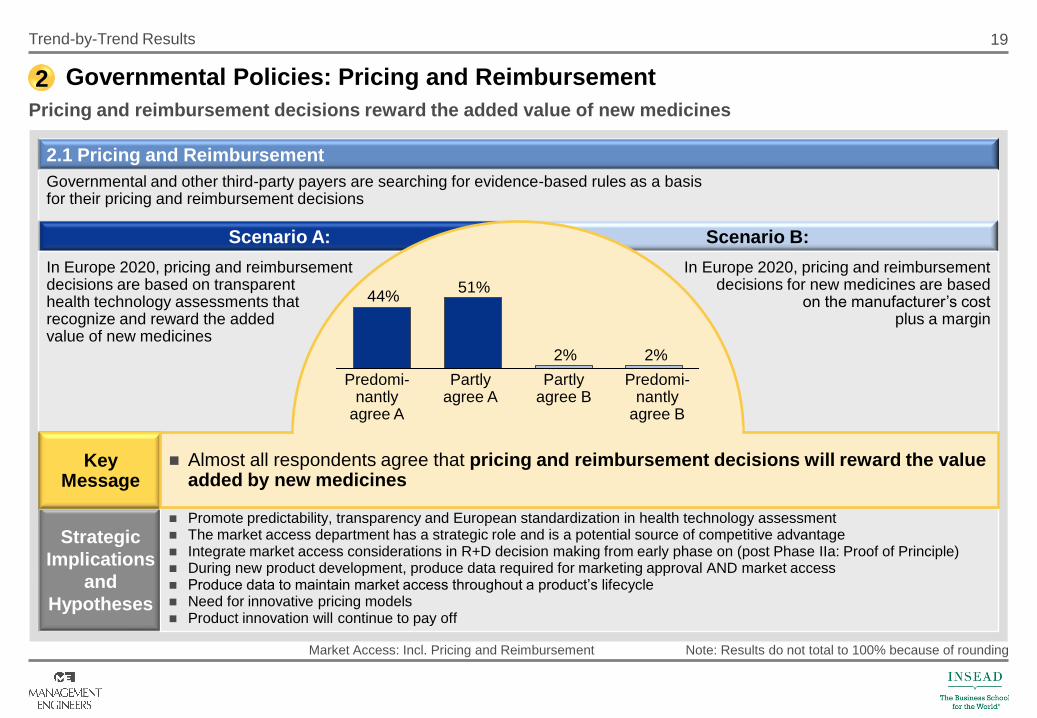

Governmental and other third-party payers are searching for evidence-based rules as a basis for their pricing and reimbursement decisions

Scenario A: Scenario B:

In Europe 2020, pricing and reimbursement decisions are based on transparenthealth technology assessments thatrecognize and reward the addedvalue of new medicines

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, pricing and reimbursement decisions for new medicines are based

on the manufacturer‟s cost plus a margin

Promote predictability, transparency and European standardization in health technology assessment The market access department has a strategic role and is a potential source of competitive advantage Integrate market access considerations in R+D decision making from early phase on (post Phase IIa: Proof of Principle) During new product development, produce data required for marketing approval AND market access Produce data to maintain market access throughout a product‟s lifecycle Need for innovative pricing models Product innovation will continue to pay off

2.1 Pricing and Reimbursement

Governmental Policies: Pricing and Reimbursement2

Pricing and reimbursement decisions reward the added value of new medicines

Almost all respondents agree that pricing and reimbursement decisions will reward the value added by new medicines

2%2%

51%44%

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

Market Access: Incl. Pricing and Reimbursement Note: Results do not total to 100% because of rounding

20

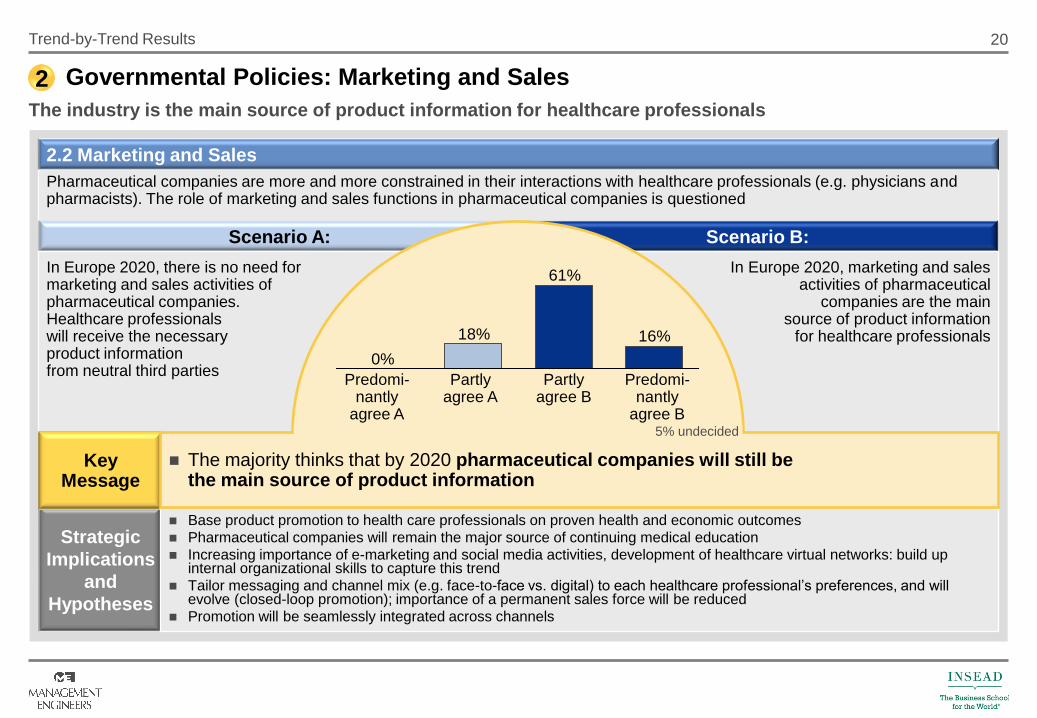

Pharmaceutical companies are more and more constrained in their interactions with healthcare professionals (e.g. physicians and pharmacists). The role of marketing and sales functions in pharmaceutical companies is questioned

Scenario A: Scenario B:

In Europe 2020, there is no need formarketing and sales activities ofpharmaceutical companies. Healthcare professionals will receive the necessary product informationfrom neutral third parties

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, marketing and sales activities of pharmaceutical

companies are the main source of product information

for healthcare professionals

Base product promotion to health care professionals on proven health and economic outcomes

Pharmaceutical companies will remain the major source of continuing medical education

Increasing importance of e-marketing and social media activities, development of healthcare virtual networks: build up internal organizational skills to capture this trend

Tailor messaging and channel mix (e.g. face-to-face vs. digital) to each healthcare professional‟s preferences, and will evolve (closed-loop promotion); importance of a permanent sales force will be reduced

Promotion will be seamlessly integrated across channels

2.2 Marketing and Sales

Governmental Policies: Marketing and Sales2

The industry is the main source of product information for healthcare professionals

16%

61%

18%

0%

The majority thinks that by 2020 pharmaceutical companies will still be the main source of product information

5% undecided

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

21

Regulatory requirements for both market authorization and post-approval monitoring are rising

Scenario A: Scenario B:

In Europe 2020, the collaboration betweenthe industry and regulators has reduced development costs and time as wellas post-monitoring costs whileguaranteeing the effectiveness and safety of new medicines

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, the increasingly stringent market authorization hurdles for new

medicines have pushed the development costs and time to unprecedented

highs

Innovation in product development technology and processes

Continuous and systematic monitoring of regulatory guideline development

Regulatory as key team member in R+D from start of concept phase on

Inclusion of product liabilities and risk assessments into project decision

Stronger focus on post-marketing surveillance programs

Early and continuous involvement of regulatory bodies, e.g. in study design considerations and post-marketing surveillance

2.3 Regulatory Hurdles

Governmental Policies: Regulatory Hurdles2

Development costs and time reach unprecedented highs

27%

55%

16%

0%

The pharmaceutical industry expects ever-increasing regulatory hurdles pushing development costs and time to unprecedented highs

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A2% undecided

Trend-by-Trend Results

22

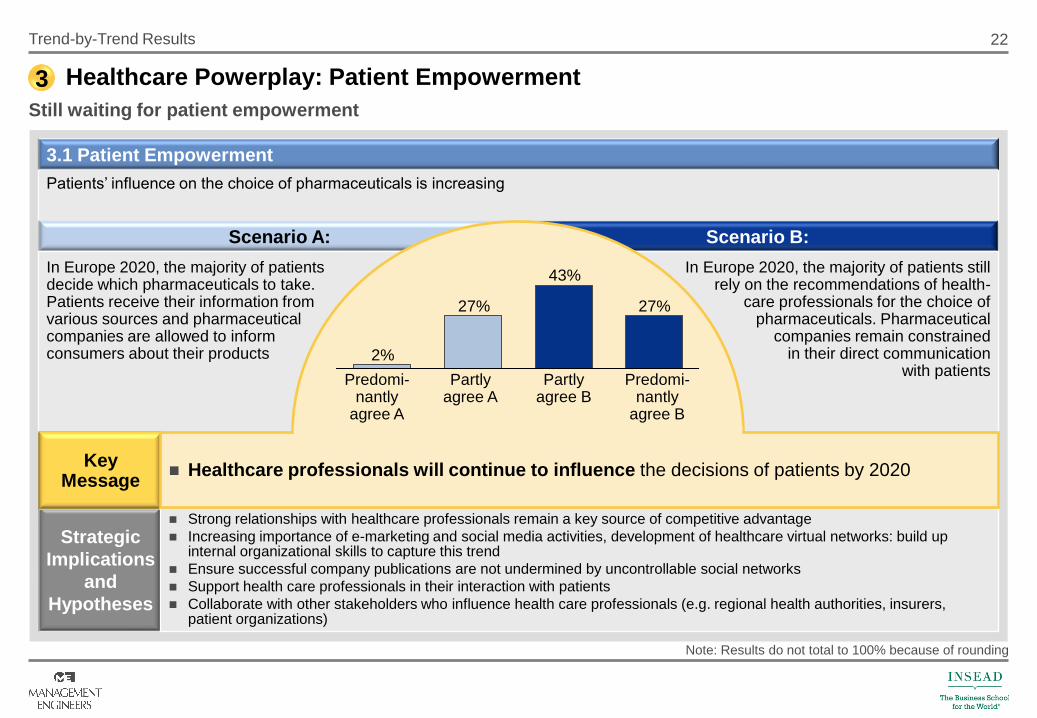

Patients‟ influence on the choice of pharmaceuticals is increasing

Scenario A: Scenario B:

In Europe 2020, the majority of patientsdecide which pharmaceuticals to take.Patients receive their information fromvarious sources and pharmaceuticalcompanies are allowed to informconsumers about their products

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, the majority of patients still rely on the recommendations of health-

care professionals for the choice of pharmaceuticals. Pharmaceutical

companies remain constrained in their direct communication

with patients

Strong relationships with healthcare professionals remain a key source of competitive advantage

Increasing importance of e-marketing and social media activities, development of healthcare virtual networks: build up internal organizational skills to capture this trend

Ensure successful company publications are not undermined by uncontrollable social networks

Support health care professionals in their interaction with patients

Collaborate with other stakeholders who influence health care professionals (e.g. regional health authorities, insurers, patient organizations)

3.1 Patient Empowerment

Healthcare Powerplay: Patient Empowerment3

Still waiting for patient empowerment

27%

43%

27%

2%

Healthcare professionals will continue to influence the decisions of patients by 2020

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Note: Results do not total to 100% because of rounding

Trend-by-Trend Results

23

Besides the traditional pharmacies, mass market retailers and internet-based shops are pushing into the distribution channel for pharmaceuticals

Scenario A: Scenario B:

In Europe 2020, a high percentage of pharmaceuticals are sold outside oftraditional pharmacies. Mass marketretailers and internet-based shopshave gained significance in thedistribution of pharmaceuticals

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, pharmaceuticals are still sold mainly through traditional

pharmacies. Mass market retailers and internet-based shops play

only a minor role in the distribution of

pharmaceuticals

Monitor the evolution of retail channels and ensure access to emerging channels

Consider the development of differentiated supply chains and commercial models to deal with different types of channels (direct-to patients, retail channels, etc.), in different countries; take into account complexity aspects

Partner with channels to enhance channel performance and efficiency (e.g. reduce working capital)

3.2 Broadening of Distribution Channel

Healthcare Powerplay: Broadening of Distribution Channel3

New retail channels have made their mark

14%18%

55%

14%

New retail channels are gaining importance and will have made their mark in 2020 for the distribution of pharmaceuticals in Europe

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

Note: Results exceed 100% because of rounding

24

There is increasing consolidation among pharmacies, wholesalers, hospitals, and physician practices which leads to higher concentration of buying power in the pharmaceutical market

Scenario A: Scenario B:

In Europe 2020, the greater concentration of buying power has driven down theprofitability of pharmaceuticals

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, greater opportunities for cost saving in supply chain and

commercialization have neutralized profit

pressure

Increasing price and margin pressure: need for critical mass / consolidation

Increasing tender offers / contract management: production and supply chain flexibility needed

Need for continuous cost management and efficiency programs

Make-or-buy analysis: what is really required to be made inhouse?

Focus on core segments (disease area, region, original / generic, OTC) to increase efficiency

3.3 Concentration of Buying Power

Healthcare Powerplay: Concentration of Buying Power3

Greater buyer concentration drives down industry profitability

2%9%

51%

37%

Most respondents support the statement that buyer consolidation will lead to

a decrease in industry profits

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

Note: Results do not total to 100% because of rounding

25

As a means of cost containment, payers are becoming increasingly influential in the product chosen by prescribers and pharmacists

Scenario A: Scenario B:

In Europe 2020, payers exercise cost containment by controlling which product physicians prescribe and pharmaciesdispense

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, physicians have regained substantial control over the product

prescribed and dispensed to a patient from a broad

range of options

Understanding payers: Stricter formulary use is becoming common practice also in Europe

Patient care programmes link with healthcare providers: Budget restrictions will especially affect chronic diseases

Assisted decision tools will be increasingly used to influence the physicians‟ choice

Trend-to-tender offers: impact on supply chain

Early collaboration with health insurances as an option to secure revenue flows

3.4 Payers as Major Powerplayers

Healthcare Powerplay: Payers as Major Powerplayers3

Influence of Payers on product choice will continue to increase

0%0%

45%55%

Increase of payer power is undisputed, driven by vast budget constraints

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

26

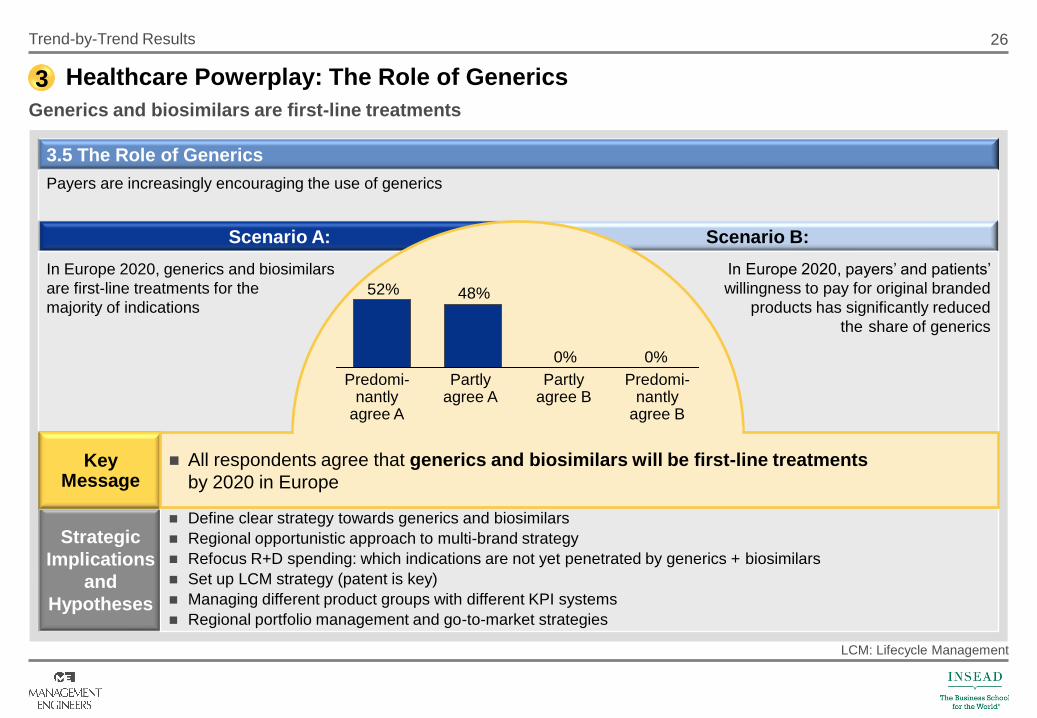

Payers are increasingly encouraging the use of generics

Scenario A: Scenario B:

In Europe 2020, generics and biosimilars

are first-line treatments for the

majority of indications

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, payers‟ and patients‟

willingness to pay for original branded

products has significantly reduced

the share of generics

Define clear strategy towards generics and biosimilars

Regional opportunistic approach to multi-brand strategy

Refocus R+D spending: which indications are not yet penetrated by generics + biosimilars

Set up LCM strategy (patent is key)

Managing different product groups with different KPI systems

Regional portfolio management and go-to-market strategies

3.5 The Role of Generics

Healthcare Powerplay: The Role of Generics3

Generics and biosimilars are first-line treatments

0%0%

48%52%

All respondents agree that generics and biosimilars will be first-line treatments

by 2020 in Europe

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

LCM: Lifecycle Management

Trend-by-Trend Results

27

A changing healthcare and greater financial pressure lead pharmaceutical companies offering originals to either diversify among or focus within indication segments

Scenario A: Scenario B:

In Europe 2020, most companies offering originals have increased the number ofindication segments in their portfolio

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, most companies offering originals have reduced the number of indication segments in their portfolio

Active portfolio management is needed: continuous review of and action on existing and desired product range

Clear strategic commitment needed on focus or differentiation: avoid being stuck in the middle

High-price niche markets will be the focus of the industry: however, they need different marketing and commercial skills

Alliance management, R+D sharing will be key

LCM: maximize potential of existing molecules across indications

4.1 Diversification vs. Focus

Industry Moves: Diversification vs. Focus4

Pruning and increasing the number of indication segments are equally likely

21%26%28%

19%

Pruning or increasing the number of indication segments are considered to be equally likely, depending on the individual company‟s situation

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A7% undecided

Trend-by-Trend Results

Note: Results exceed 100% because of roundingLCM: Lifecycle Management

28

The pharmaceutical industry is characterized by increasing consolidation through megamergers, acquisitions of niche experts, and takeovers in order to fill the R+D pipeline or for geographical expansion

Scenario A: Scenario B:

In Europe 2020, today‟s leading pharma-ceutical companies in each of theindustry segments (e.g. originals, bio-pharmaceuticals, generics, OTC) still exist

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, sales are concentrated among a handful of giant

pharmaceuticalcompanies

Consolidation yes, but not a handful; still room for specialists; clear roadmap on how to integrate and manage acquisitions

Clear strategy towards industry consolidation: actively participate; or defence strategy: avoid hostile takeovers

Continuous emergence of niche players: potential for investments / capturing promising growth opportunities

Consolidation across industry segments will increase (originals, generics, biopharmaceuticals, OTC, etc.)

4.2 Consolidation

Industry Moves: Consolidation4

The industry is dominated by a few giants

12%

47%

30%

7%

The majority expects the pharmaceutical industry in Europe to be further concentrated in a reduced number of giant companies by 2020

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A5% undecided

Trend-by-Trend Results

Note: Results exceed 100% because of rounding

29

Private equity is gaining importance in the financing of pharmaceutical companies beyond biotech start-ups

Scenario A: Scenario B:

In Europe 2020, the need for long-term investments in the pharmaceuticalindustry has reduced the attractiveness of large pharmaceutical companiesfor private equity investors

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, private equity investors have acquired pharmaceutical companies

among the top 20 and unlocked significant economic value

through restructuring

Restructuring will be mainly driven by the industry itself, not by PE; the return on capital in pharmaceuticals does not require PE

The risk reward profile and timelines are not attractive to PE: avoid lengthy discussions

The industry will have less problem to access cash compared to PE. However, need to ensure long-term financing

4.3 Private Equity Financing

Industry Moves: Private Equity Financing4

Large pharmaceutical companies are unattractive for private equity

11%23%

48%

16%

Most managers believe that large pharmaceutical companies remain unattractive for private equity

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A2% undecided

Trend-by-Trend Results

30

There is a growing demand for integrated care delivery, combining products and related services in a “one-stop shop” for convenience and expertise reasons

Scenario A: Scenario B:

In Europe 2020, many pharmaceuticalcompanies create new business models based on integrated care concepts

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, most pharmaceutical companies remain

product-focused

Integrating marketing approach for products and services

Gap analysis: which products/services are needed and still missing, which do really add value

Need to exploit new markets: what are alternative sources of revenue

Approach towards payers / other stakeholders: enlarge offerings to better negotiate – differentiate

Changing competence profile to enable added value beyond medicine

4.4 Integrated Care Delivery

Industry Moves: Integrated Care Delivery4

Integrated care models prevail

11%18%

48%

23%

Integrated care models will prevail

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

31

Biotechnology products represent a growing share of R+D investments in the pharmaceutical industry

Scenario A: Scenario B:

In Europe 2020, investments in bio-technology are the main growth driver and source of profit for the industry

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, companies have reduced their investments in biotechnology as a

percentage of their R+D spend

Invest in biopharmaceuticals and create barriers of entry

Acquire additional capabilities: internal build-up and/or joint ventures / alliances

Threat to existing products / portfolio needs to be assessed

R+D strategy: capturing biotechnology potential? Capturing threat to existing pipeline?

Biotechnology is still only one element of the portfolio and needs to be embedded into a comprehensive technology strategy

5.1 Biotechnology

Innovation Potential: Biotechnology5

Biotechnology investments have paid off

2%7%

59%

25%

The majority expects the investments in research and development for biotechnological products to have paid off by 2020

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A7% undecided

Trend-by-Trend Results

32

Companies find it increasingly difficult to fill their R+D pipeline especially with future blockbuster products. While R+D costsand complexity are rising, at the same time the number of successful new molecular entity launches has stagnated

Scenario A: Scenario B:

In Europe 2020, new technologies have increased the predictability of R+Dsuccess through early proof of concept

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, the use of new technology has not shown a significant positive

impact on the predictability of R+D success

Building a streamlined and structured R+D process: increasing the predictability

Increasing role of biomarkers: targeted innovations are possible

Further extension of co-development and in licensing to share cost and reduce risk

5.2 (Un-)predictable R+D success

Innovation Potential: (Un-)Predictable R+D Success5

R+D success is more predictable

0%

30%

50%

20%

The majority of respondents expect at least some improvement in the predictability of research and development success by 2020

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

33

Pharmaceutical companies‟ R+D investments focus not only on treatment research, but increasingly also on illness prevention, e.g. through preventive vaccines

Scenario A: Scenario B:

In Europe 2020, preventive medicine is ahighly profitable business. High prices are justified by lower treatment costs

In Europe 2020, the profitability of preventive medicine is low. The willingness of

payers and patients to pay for prevention is limited

Strategic

Implications

and

Hypotheses

Add prevention as additional target indication

Which areas of prevention seems most promising/attractive? Set up R+D focus accordingly

Establish Innovative and joint solutions together with payers and other stakeholders:If total treatment costs can be demonstrated to be lower, the costs will be born by the healthcare system

5.3 From Treatment to Prevention

Innovation Potential: From Treatment to Prevention5

Preventive medicine is a profitable business

KeyMessage

5%

32%

50%

14%

Preventive medicine is believed by many to be a highly profitable business by 2020

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A

Trend-by-Trend Results

Note: Results exceed 100% because of rounding

34

There are increasing efforts to combine diagnosis and medicine in order to make individualized and targeted treatment possible

Scenario A: Scenario B:

In Europe 2020, personalized medicine ishighly profitable and well accepted bypatients, prescribers and payers

Strategic

Implications

and

Hypotheses

KeyMessage

In Europe 2020, higher costs, limited ability to obtain price premiums and smaller

market size lead to low profitability of personalized medicine

Benefits of personalized medicine need to be promoted to the public

Build upon the possibility for differentiation and value propositions to justify higher prices

Establish early-on link of HTA model criteria and project decisions

Still underdeveloped regulatory pathway towards personalized medicine: convincing of stakeholders needed

5.4 Personalized Medicine

Innovation Potential: Personalized Medicine5

Personalized medicine is highly profitable and well accepted

7%

27%

41%

23%

The majority expects personalized medicine to be highly profitable and

well accepted in Europe 2020

Predomi-nantly

agree B

Partly agree B

Partly agree A

Predomi-nantly

agree A2% undecided

Trend-by-Trend Results

HTA: Health Technology Assessment