Embed Size (px)

Citation preview

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 1/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 2/105

The duration of a Plain Vanilla bond may bedefined as its average life

It is very easily defined for a zero coupon

bond In such cases there is a single cash flow at

maturity

Thus there is no difference between the average

time to maturity and the actual time to maturity The duration of a ZCB is equal to its stated time

to maturity

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 3/105

The definition is not clear cut for a couponpaying bond

Such assets give rise to a sequence of cash flows- usually on a semi-annual basis

They also give rise to a relatively large cash flowat maturity

Thus to compute the average life we need totake cognizance of the times to maturity of each

cash flow

Obviously we need to factor in the Time Value ofMoney

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 4/105

Macaulay came up with the concept ofDuration

`It is the weighted average maturity of the

bond’s cash flows where the Present Valuesof the cash flows serve as the weights’

This definition is comprehensive

It accounts for all the cash flows

It takes into account the time value of money

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 5/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 6/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 7/105

t represents the corresponding semi-annualperiod

So the final value will be in half years

It will have to be divided by two in order toannualize it

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 8/105

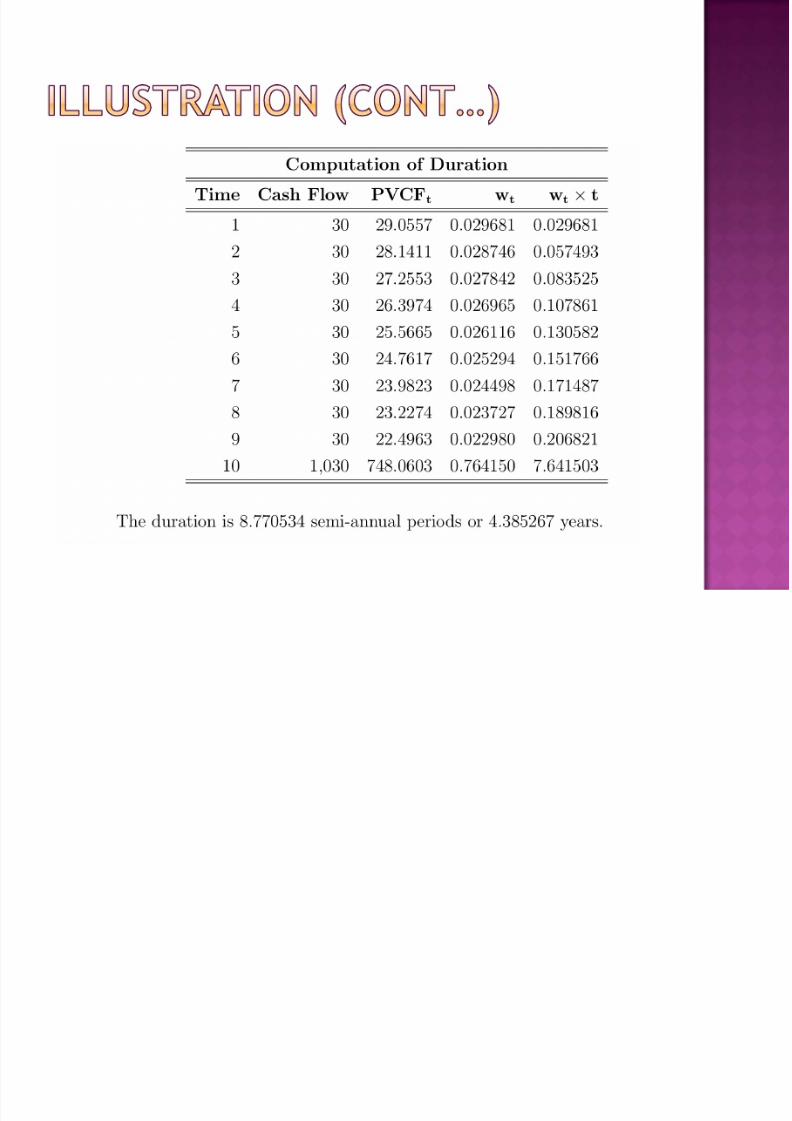

Consider a T-note with 5 years to maturity

Face value is $1,000

Coupon is 6% payable semi-annually

YTM is 6.50% per annum The dirty price is:

30xPVIFA(3.25,10) + 1,000PVIF(3.25,10) =$978.9440

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 9/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 10/105

Assume that the next coupon is k periodsaway where k < 1

k is computed using the prescribed day-count

convention

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 11/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 12/105

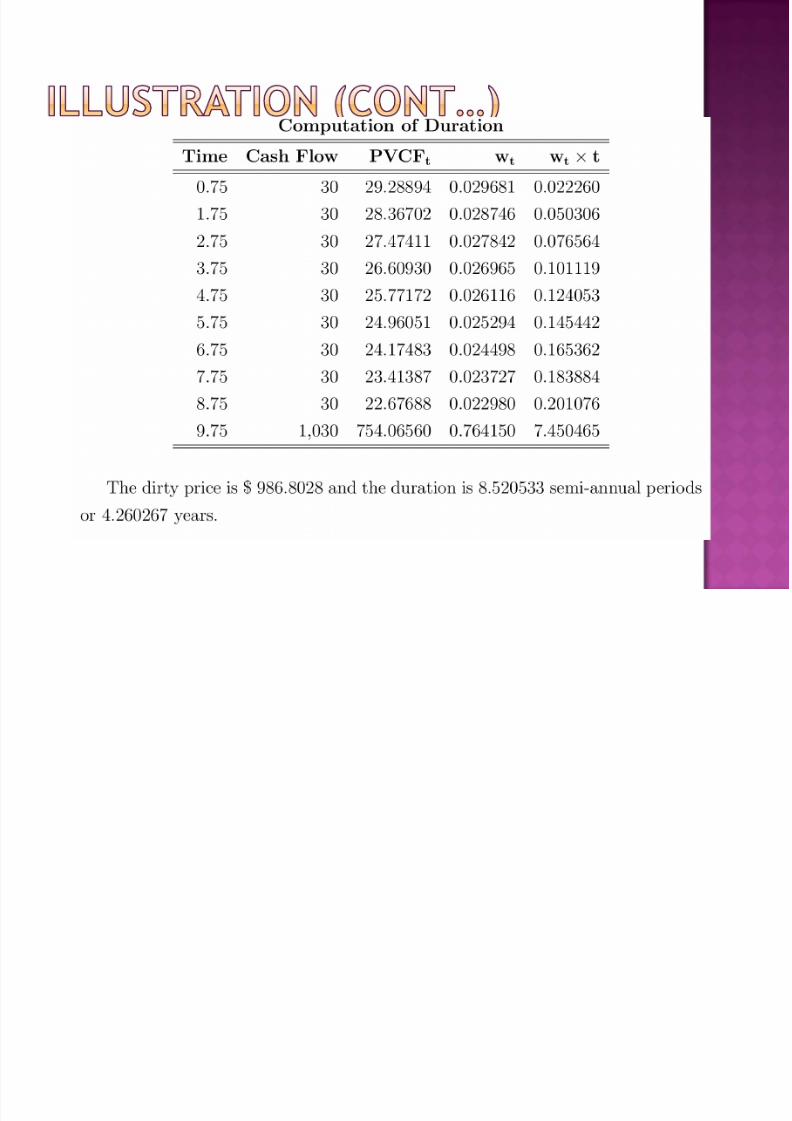

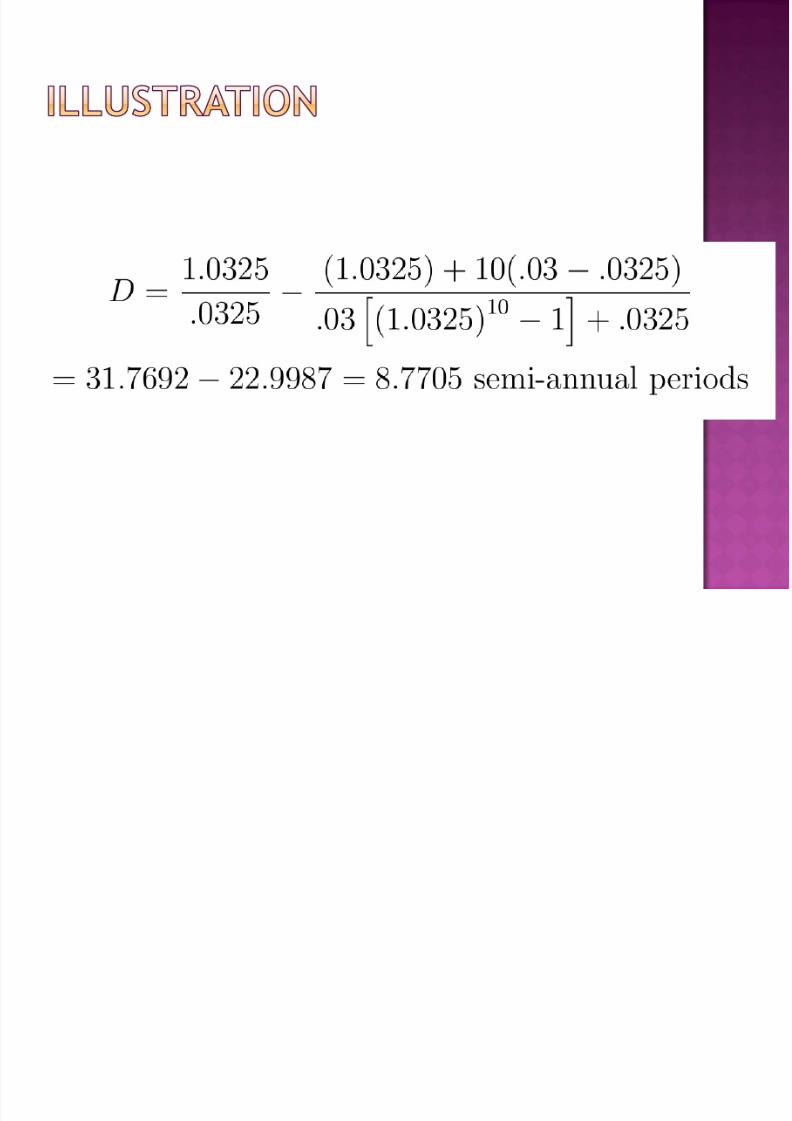

Take the five year T-note

Assume that it has 4.75 years to maturity

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 13/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 14/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 15/105

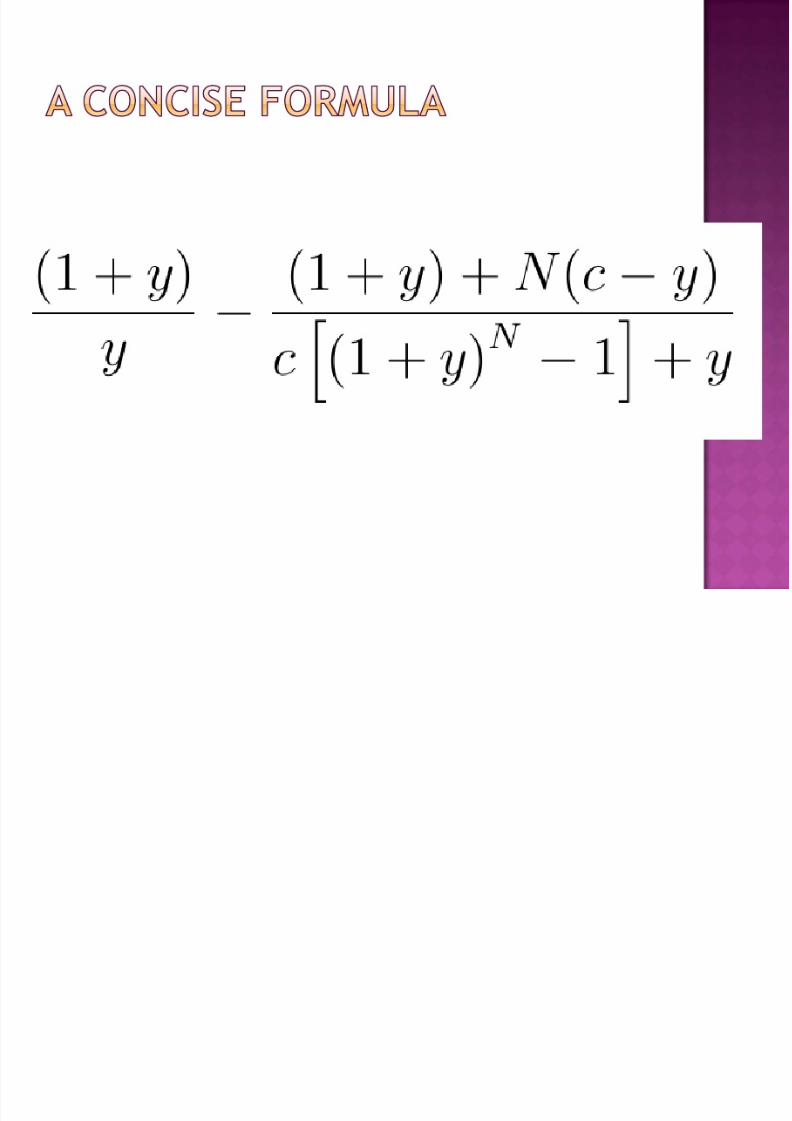

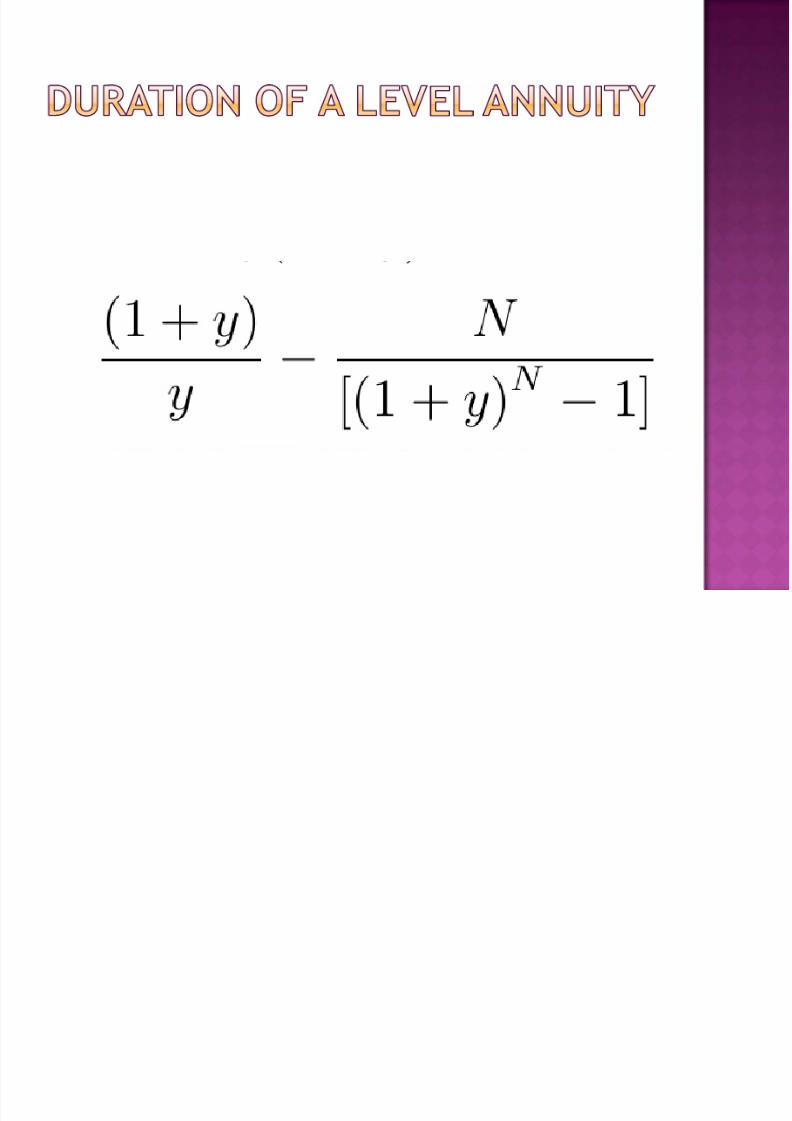

Both y and c are in periodic terms (usuallysemi-annual)

N is the number of coupons remaining

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 16/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 17/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 18/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 19/105

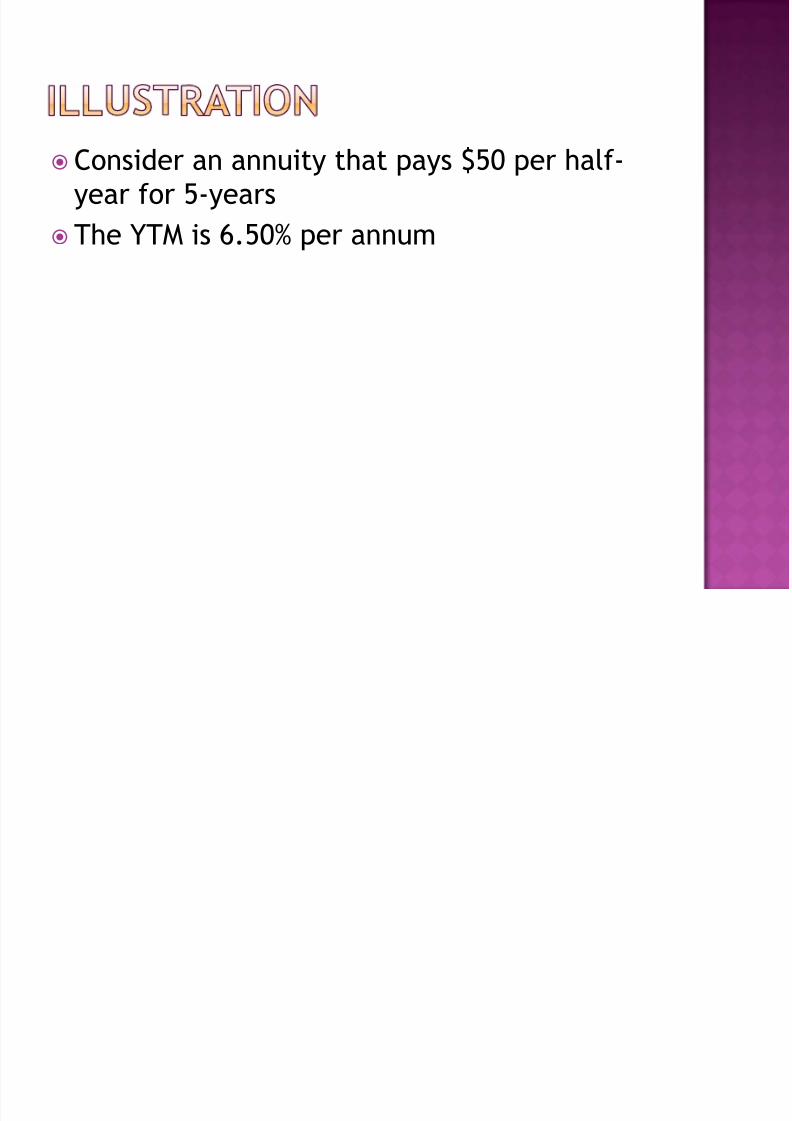

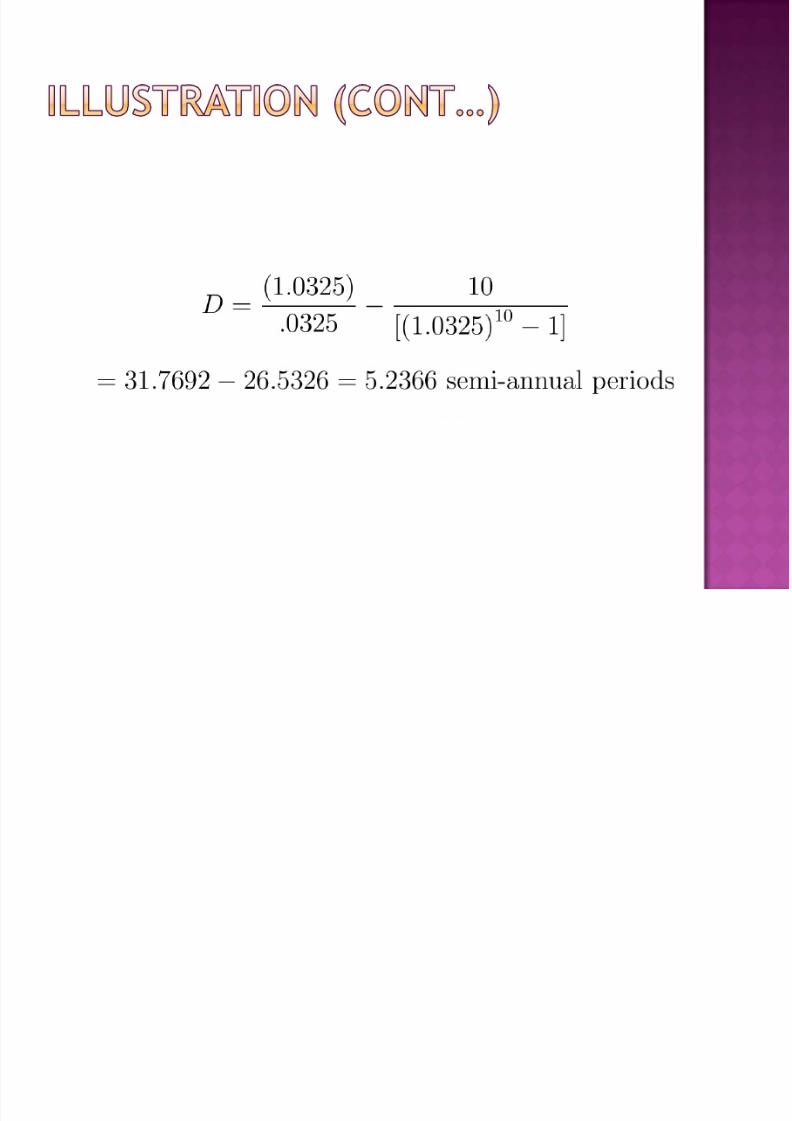

Consider an annuity that pays $50 per half-year for 5-years

The YTM is 6.50% per annum

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 20/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 21/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 22/105

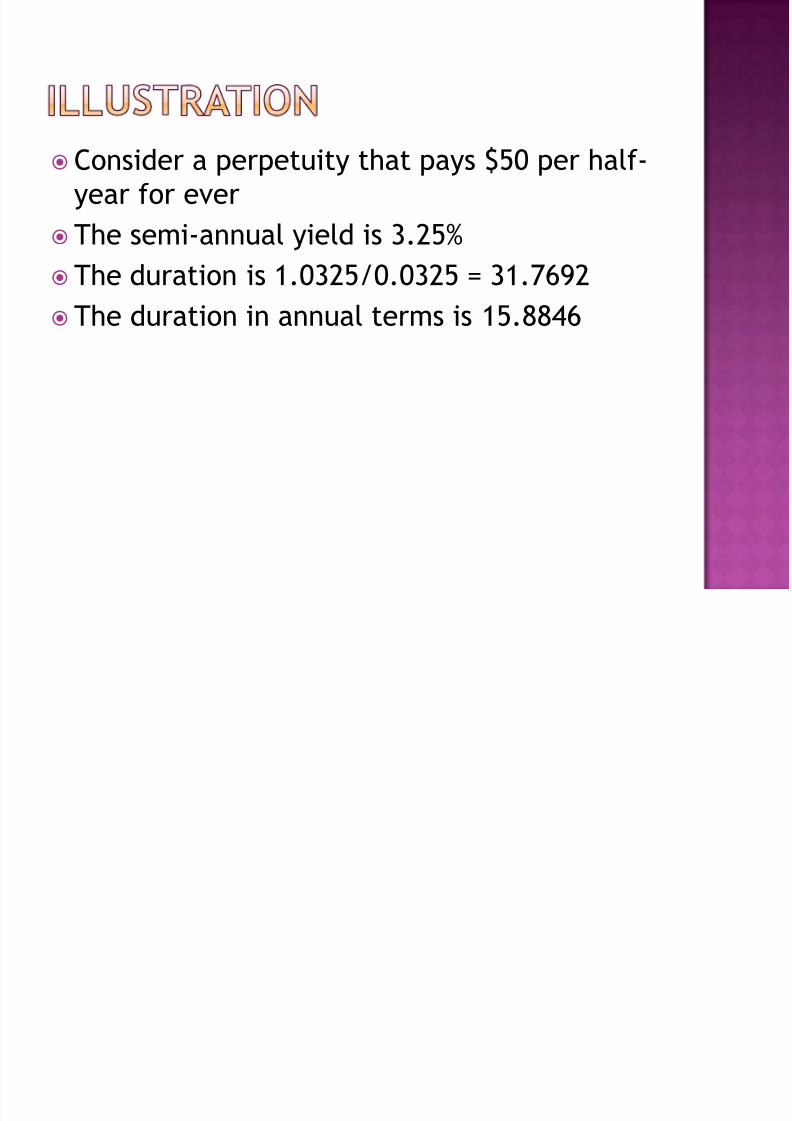

Consider a perpetuity that pays $50 per half-year for ever

The semi-annual yield is 3.25%

The duration is 1.0325/0.0325 = 31.7692 The duration in annual terms is 15.8846

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 23/105

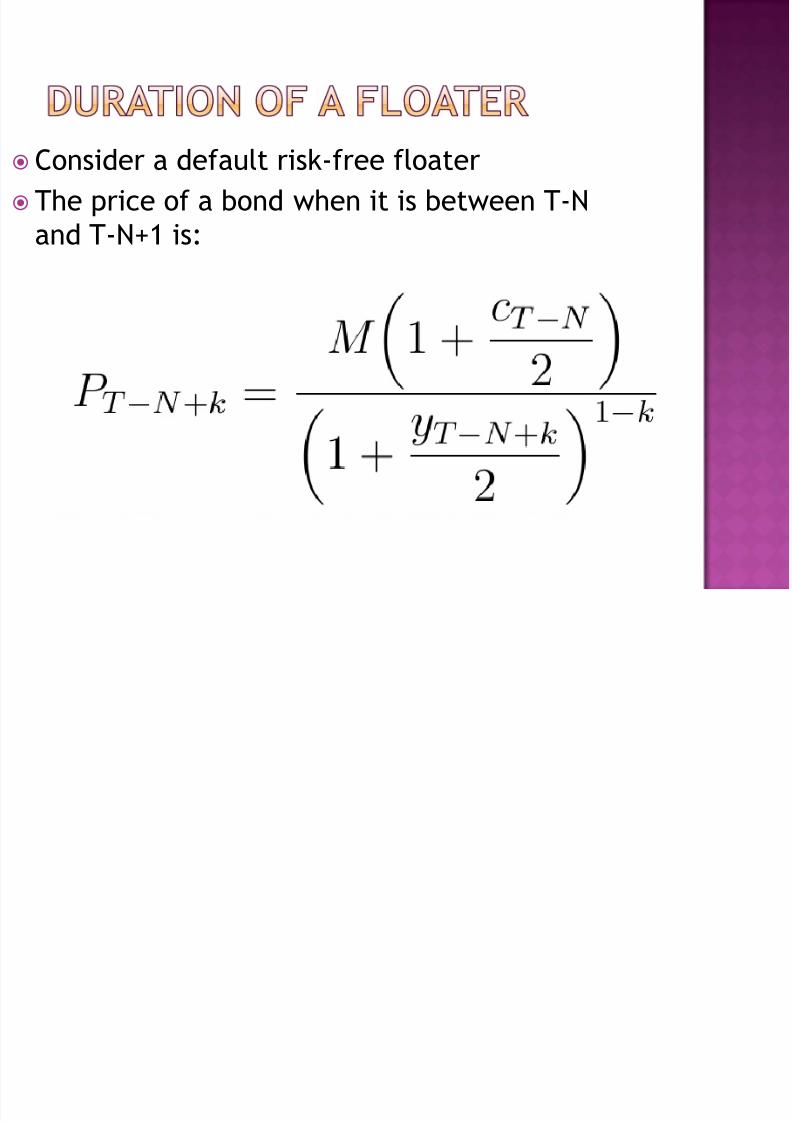

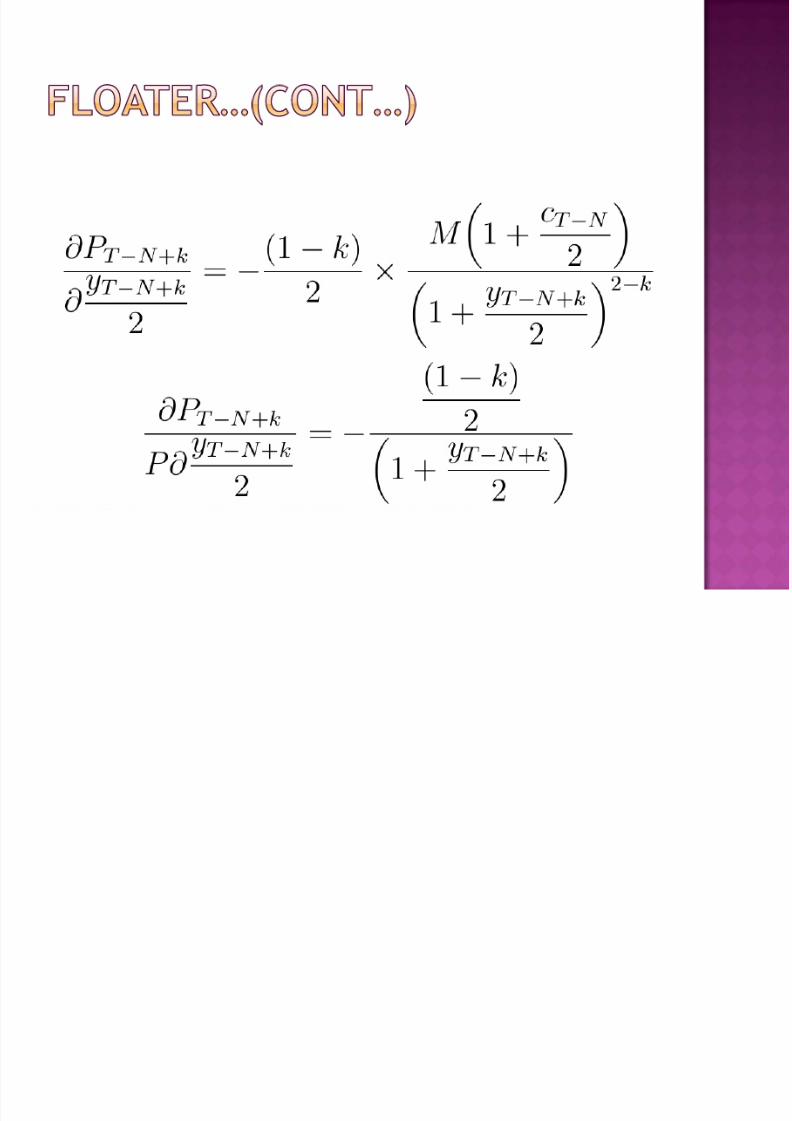

Consider a default risk-free floater

The price of a bond when it is between T-Nand T-N+1 is:

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 24/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 25/105

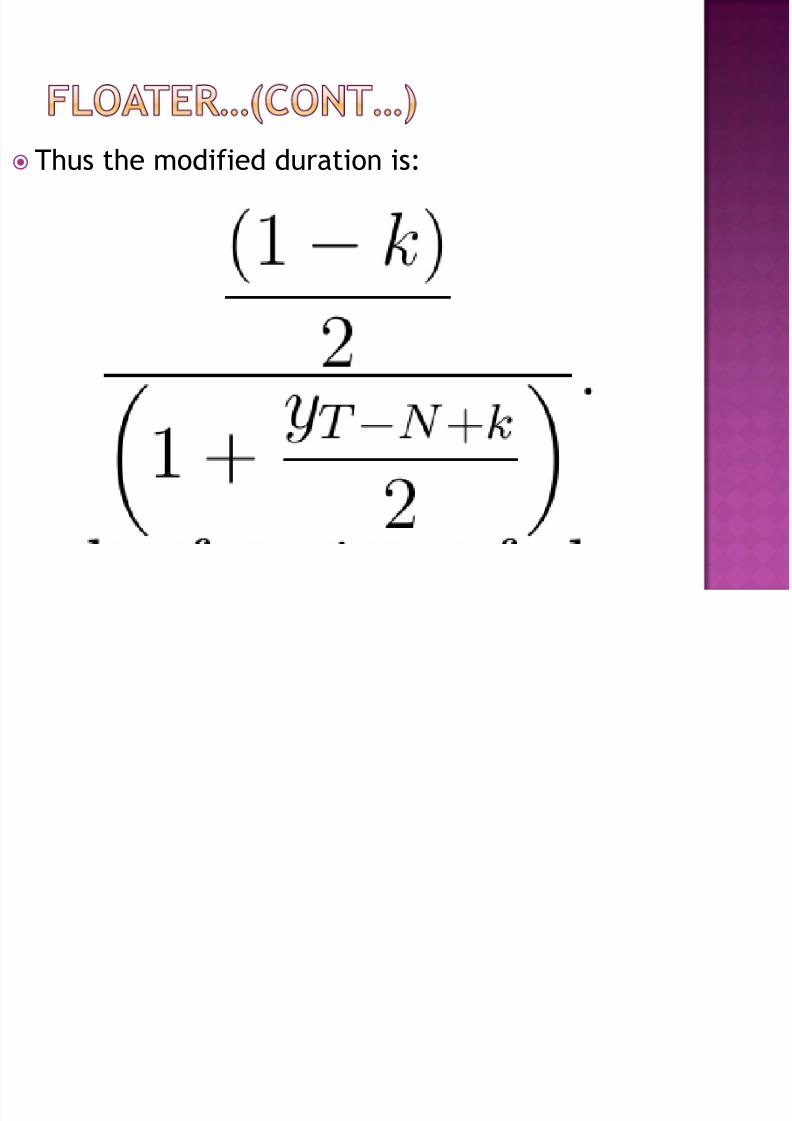

Thus the modified duration is:

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 26/105

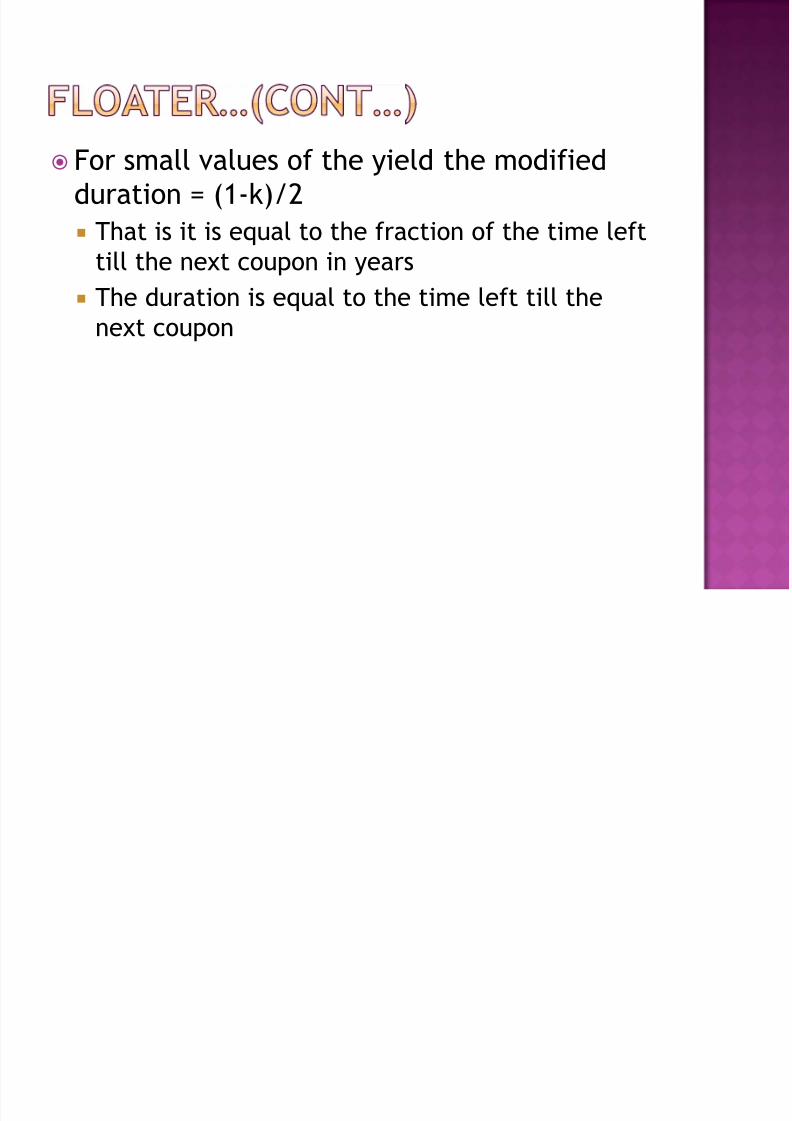

For small values of the yield the modifiedduration = (1-k)/2

That is it is equal to the fraction of the time lefttill the next coupon in years

The duration is equal to the time left till thenext coupon

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 27/105

Duration of a ZCB is equal to its stated timeto maturity

Keeping maturity and yield constant, the

higher the coupon rate, the lower is theduration

The greater the relative weights of the earliercash flows the lower will be the duration

In the case of bonds paying high coupons theweights associated with the earlier cash flowsare higher This brings down the duration

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 28/105

Holding coupon and yield constant, theduration of a bond generally increases withthe time to maturity For par and premium bonds, duration always

increases with the time to maturity For discount bonds duration generally increases

with the time to maturity

But there could be bonds trading at a substantialdiscount for which duration could decrease withthe time to maturity

Holding coupon and maturity constant, thehigher the YTM of the bond the lower is theduration

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 29/105

There are four primary influences on a plainvanilla bond’s duration

Term to maturity

Coupon Accrued Interest

Coupon Frequency

Market Yield Level

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 30/105

Duration is positively related to a bond’sremaining term to maturity

Duration increases as maturity is extended

but it does so at a decreasing rate For a ZCB duration increases at a constant

rate as the maturity lengthens

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 31/105

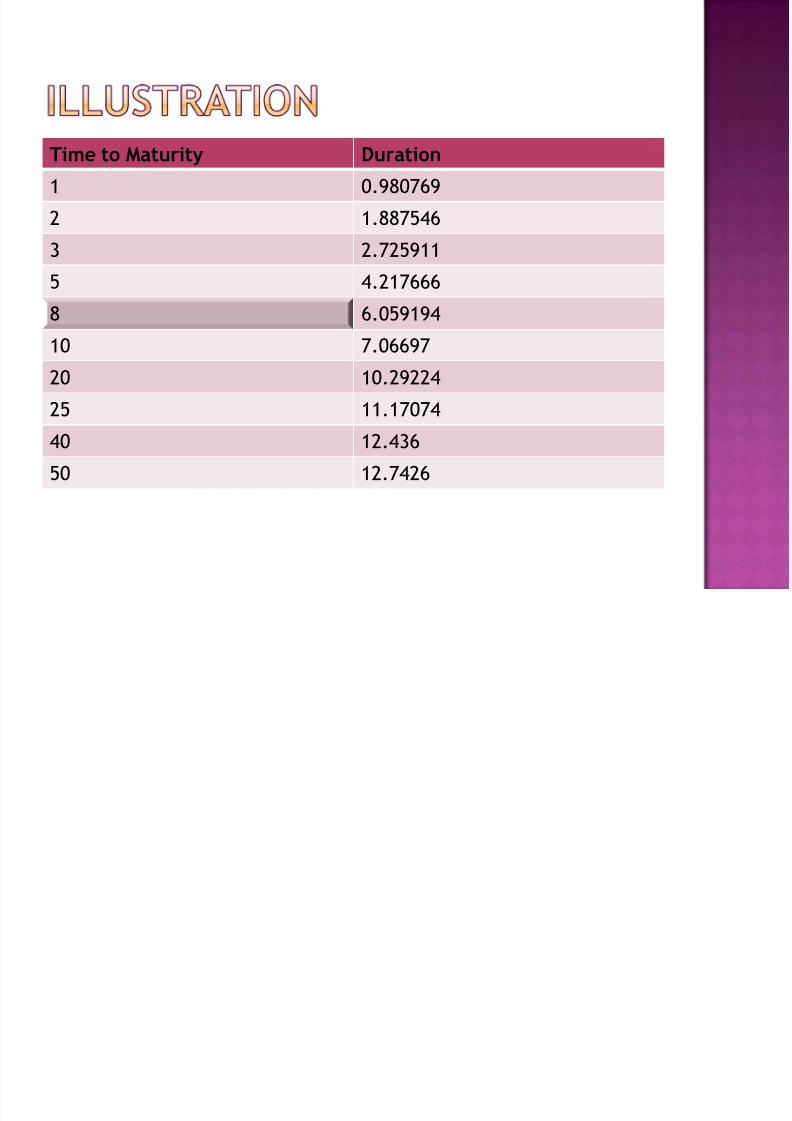

Time to Maturity Duration

1 0.980769

2 1.887546

3 2.725911

5 4.2176668 6.059194

10 7.06697

20 10.29224

25 11.1707440 12.436

50 12.7426

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 32/105

Duration and time to maturity are positivelyrelated for two key reasons

One is that the principal repayment is a large

contributor to the bond price and is a majorinfluence on its duration

If this cash flow is postponed it pulls the durationwith it

In addition the long-term coupon payments assistthis process

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 33/105

Second long maturity bonds have cash flowsthat occur after a shorter-term securitymatures

Consider three bonds with a coupon and YTM

= 10% We have a 5-year; a 10-year; and a 30-year bond

A 10 year bond receives 75% of its cash flowsafter a five year bond matures

A 30 year bond receives 87.50% of its cash flowsafter a 5 year bond matures

And 75% of its cash flows after a 10 year bondmatures

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 34/105

A 10 year bond has a total cash flow of 20x50+ 1000 = 2000

Of this $ 1500 comes after 5 years

This is 75% of $ 2000 A 30 year bond has a total cash flow of 60 x

50 + 1000 = 4,000

Of this $ 3,500 comes after 5 years

This is 87.50% of $4,000 $3,000 comes after 10 years

This is 75% of 4,000

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 35/105

These longer cash flows create a higherduration for the long maturity bond

However duration increases at a decreasing

rate Because long-term cash flows (of a fixed nominal

amount) are assigned progressively lower presentvalues

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 36/105

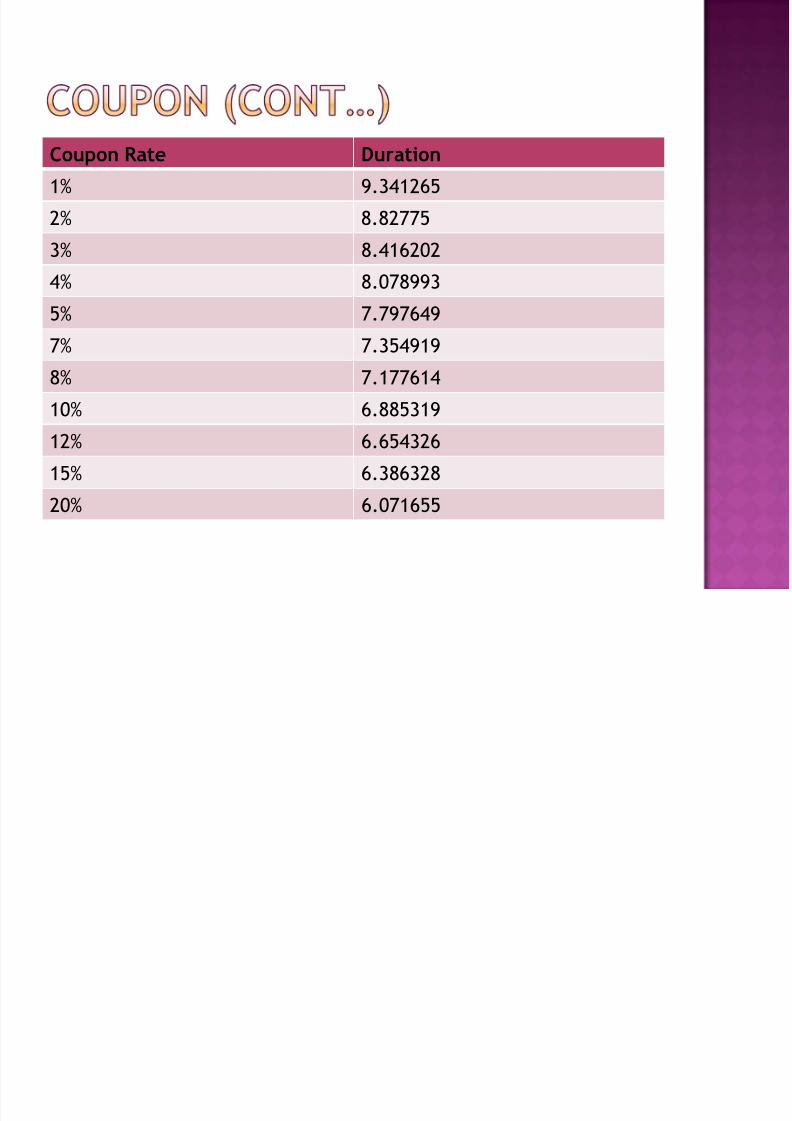

Duration is inversely related to a bond’scoupon rate of interest

Keeping all other factors constant a high

coupon rate corresponds to a lower duration.Consider a bond with a face value of $1,000;

10 years to maturity; and a YTM 0f 7%

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 37/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 38/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 39/105

Duration and coupon are inversely related fortwo primary reasons

First higher coupon bonds have greateramounts of cash flows occurring before the

final maturity This reduces the influence of the principal

repayment at maturity

Take the 10% 10-year bond

It has 50% of its cash flows coming in the form ofcoupons

A 30 year bond has 75% of its cash flows comingin the form of coupons

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 40/105

The discounting process has less effect onthe early cash flows (coupon payments) thanon later cash flows (coupons as well asprincipal)

Thus larger coupon cash flows are assignedgreater weights in present value terms

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 41/105

A bond’s duration is inversely related to theamount of accrued interest attached to thebond The duration computation is based on the Dirty

Price and not on the Clean Price Thus AI has an impact on duration

Accrued Interest is an investment with a zeroduration

The upcoming coupon payment reimbursesthe bond holder for the AI paid upfront Thus a bond with a higher AI will have a lower

duration than a similar bond with less AI

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 42/105

Thus the AI component of a bond’s dirty pricedrags down the bond’s overall duration

When the bond’s coupon payment is made

the AI component disappears and theduration will lengthen because the bond isrelieved of its zero duration component

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 43/105

Consider a $1000 face value T-bond with acoupon = YTM = 7% and 30 years to maturity.

The bond has been issued on 15 July 2014

and we are on 14 January 2015 The Duration is 12.4116 years

On the next day the Duration is 12.8432years because the Dirty Price on that day no

longer includes the accrued interest

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 44/105

The Accrued Interest induced effect is morepronounced in the case of bonds which paycoupons on an annual basis

Because the buildup of accrued interest isgreater in the case of bonds that paycoupons on an annual basis

A full year’s coupon has to be accrued

Whereas in the case of bonds paying coupons ona semi-annual basis only a maximum of C/2 isaccrued

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 45/105

Consider the T-bond with a coupon and yieldof 7% and 30 years to maturity

Assume that the bond was issued on 15 July2014 and that we are on 14 July 2015 If we assume semi-annual coupons the duration is

12.3460 years

If we assume annual coupons it is 12.2804 years

On the next day, 15 July 2015

The bond with semi-annual coupons has aduration of 12.7752 years

The bond paying annual coupons has a durationof 13.1371 years

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 46/105

The jump in duration is significantly higherfor the bond paying annual coupons

Notice that the bond paying annual coupons

has a higher duration on the coupon datethan the bond paying semi-annual coupons

This is because the entire coupon is received atyear-end

Whereas in the case of semi-annual bond half thecoupon is received after six months

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 47/105

Duration is inversely related to the YTM of abond

High yield environments lead to low duration

Low yield environments create high durations

Consider a bond with 30 years to maturity

The face value is $ 1,000

The coupon is 7% per annum paid semi-annually

As can be seen the duration is inversely relatedto the YTM

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 48/105

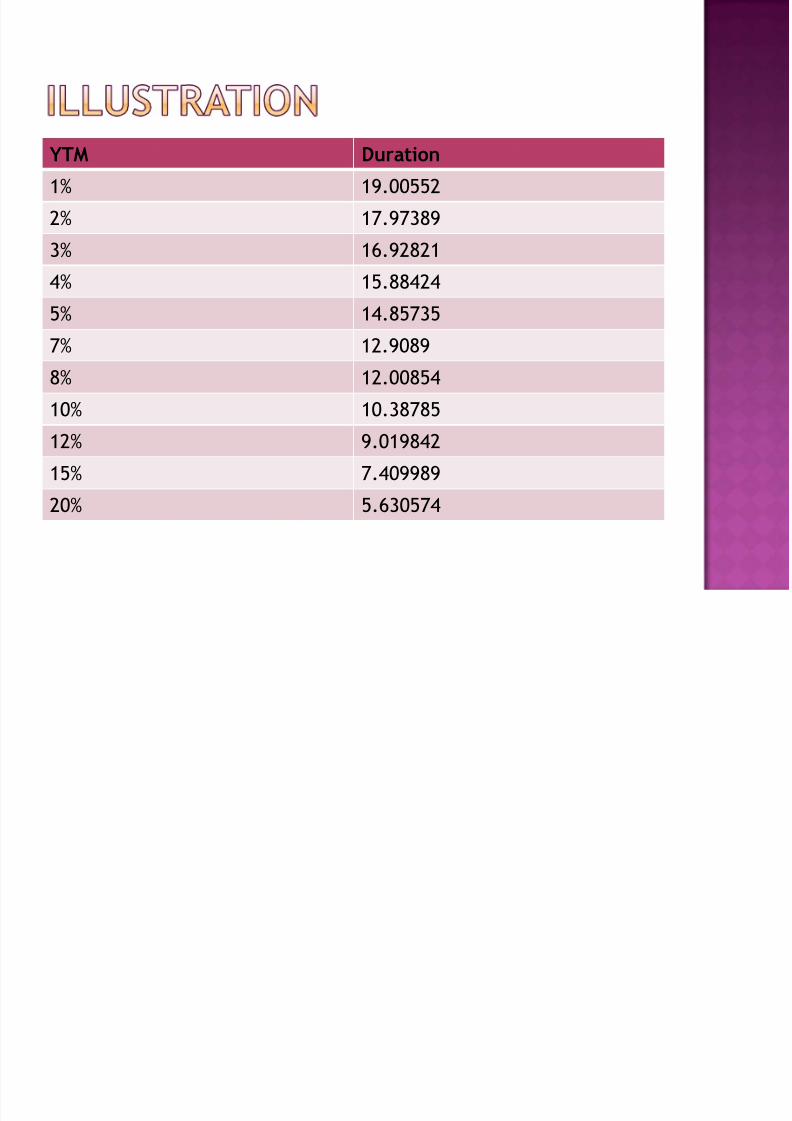

YTM Duration

1% 19.00552

2% 17.97389

3% 16.92821

4% 15.884245% 14.85735

7% 12.9089

8% 12.00854

10% 10.38785

12% 9.019842

15% 7.409989

20% 5.630574

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 49/105

There are two reasons why duration and YTMare inversely related

First duration is based on the present value

weights of a bond’s cash flows As rates rise we assign relatively lower

weights to long-term cash flows and higherweights to short term cash flows

This brings down the duration Besides the present value of the principal

amount falls disproportionately driving down itsrelative contribution to the bond price

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 50/105

Second newly issued bonds have a couponthat is close to the prevailing YTM

Higher yield environments lead to higher couponbonds

Lower yield environments lead to lower couponbonds

In a high yield environment the couponcomponent of a newly issued bond’s marketvalue is even higher Thus it is very sensitive to changes in yield

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 51/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 52/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 53/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 54/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 55/105

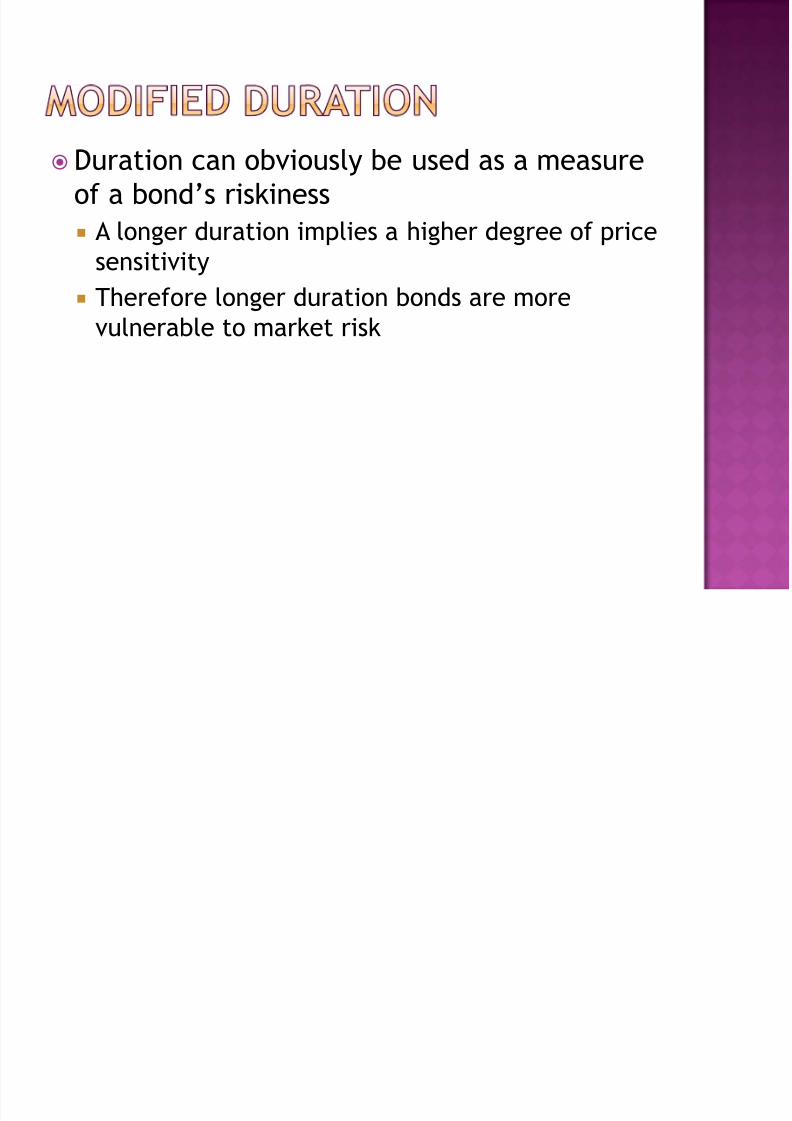

Duration can obviously be used as a measureof a bond’s riskiness

A longer duration implies a higher degree of pricesensitivity

Therefore longer duration bonds are morevulnerable to market risk

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 56/105

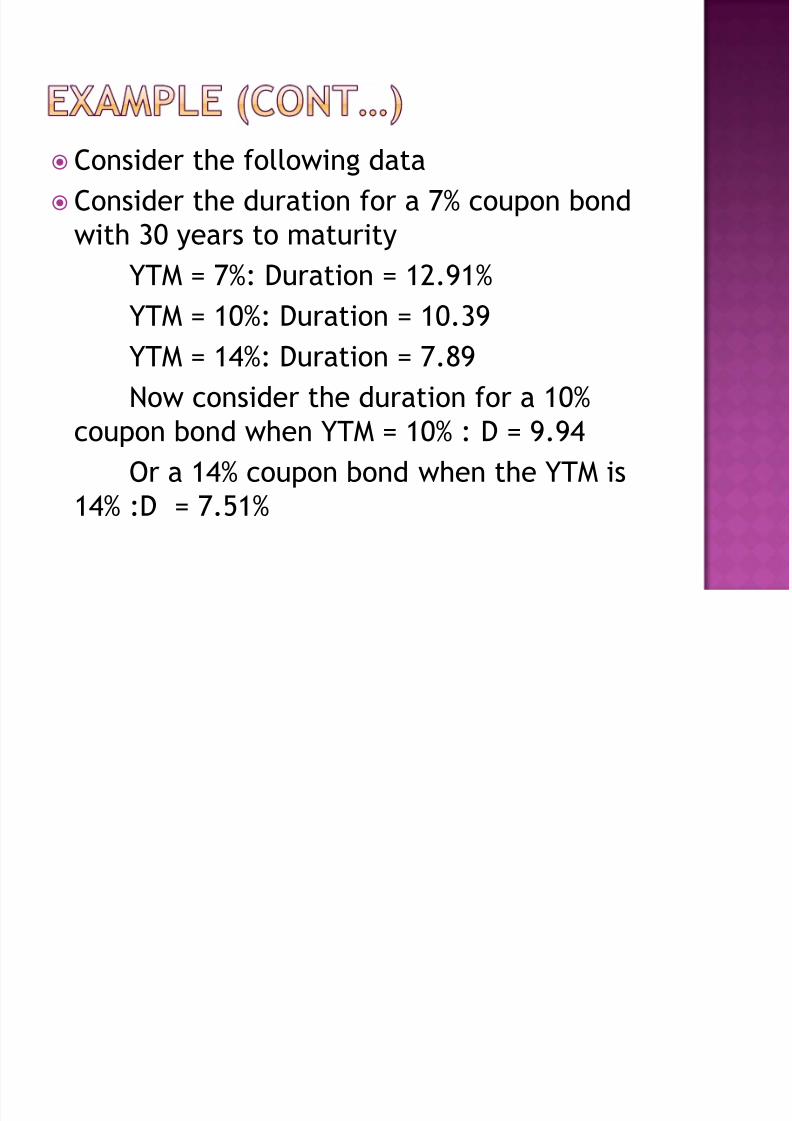

Consider a 3-year bond with a face value of$1,000

The coupon = YTM = 10%

The duration is 2.6647 years The modified duration is 2.6647/1.05 = 2.54

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 57/105

Consider a 30 year bond with a face value of$1,000

Coupon = YTM = 10%

The duration is 9.94 years The modified duration is 9.94/1.05 = 9.47

The larger the duration the greater thedifference between the duration and the

corresponding modified duration The greater the YTM the larger is the

difference between the duration and thecorresponding modified duration

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 58/105

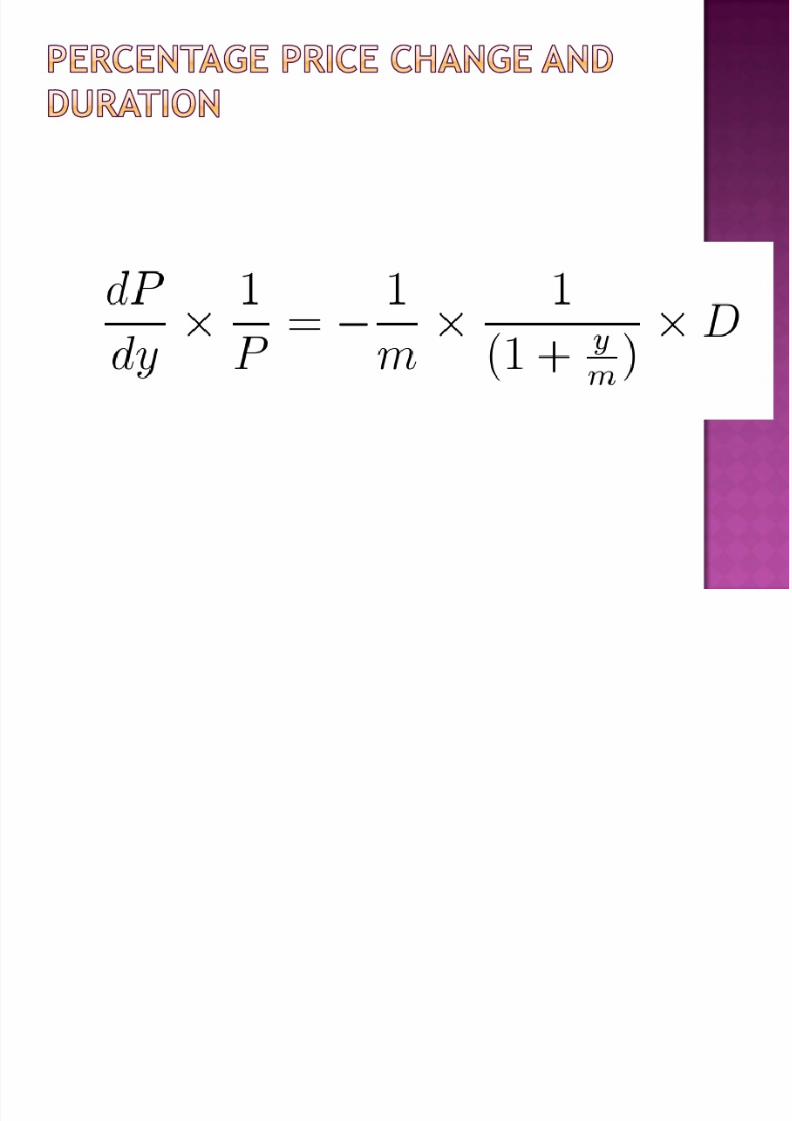

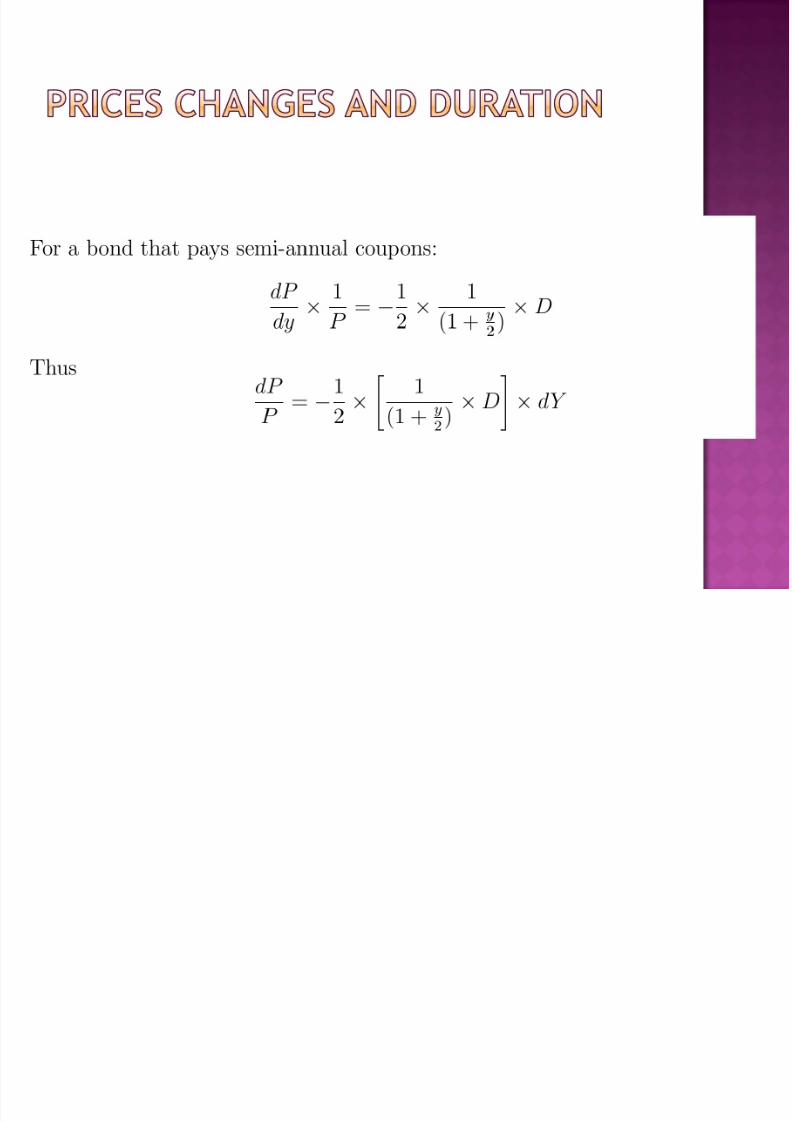

Modified duration is a measure of thesensitivity of a bond’s price to changes in theYTM

%age change in bond price = - ModifiedDuration x Change in Yield (in bp)/100

Consider a bond with a modified duration of5 years

If the yield falls by 100 basis points the pricerises by approximately 5%

If the yield falls by 200 bp, the price rises byapproximately 10%

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 59/105

We know that prices and yields are inverselyrelated

The negative sign attached to the modifiedduration captures this

Modified Duration acts as a multiplier

The larger the modified duration the greater isthe price impact for a given change in interestrates

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 60/105

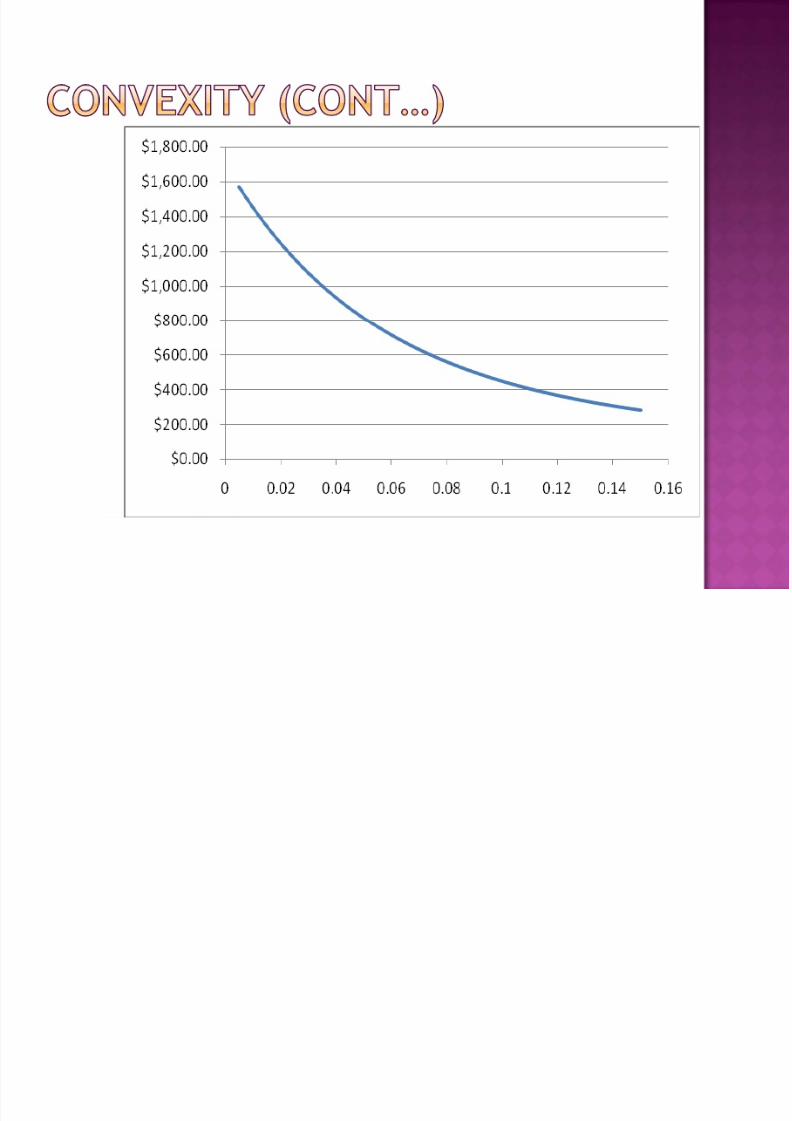

If we plot price versus yield we get a Convexrelationship

The slope of the tangent to this curve at anypoint is the modified duration at that point. Strictly speaking the slope of the tangent is

-Modified Duration x Market Price

Thus modified duration captures the Price-Yieldrelationship on a straight line basis

Thus it is only an estimate of the true price-yieldrelationship

The larger the change in yield the greater will be theerror due to the approximation

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 61/105

The product of the modified duration and theprice of the bond is referred to as the DollarDuration of the bond

In our case

Modified duration = 4.3853 years

Price was 978.9440

Dollar duration = 4,292.9631

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 62/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 63/105

The price-yield relationship for a plainvanilla bond is convex in nature.

Duration is a measure of the first derivative, andvaries along with yield.

To factor in the convex nature, or the curvature,of the bond we need to compute the secondderivative.

Convexity is the rate of change of the

modified duration with respect to yield

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 64/105

Modified duration is the slope of the price-yield curve at a point

Convexity measures the gap between themodified duration tangent line and the price-yield curve

Thus convexity may be defined as thedifference between the actual bond price

and the price predicted by the tangent line It enhances a bond’s performance in both

bull and bear markets but not uniformly

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 65/105

For plain vanilla bonds the convexity isalways positive

Thus the price-yield curve will always lieabove the modified duration tangent line

The convexity effect becomes greater withlarger changes in yield

Modified duration is a good estimate for

small yield changes But loses its predictive power for large yield

changes

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 66/105

If a bond’s duration were to be constant forall values of yield then convexity would notexist

The change in duration with yield movementscreates the convexity effect

Duration increases in a bull market as yieldsfall

This enhances the price gainDuration decreases in a bear market as yield

rise

This mitigates the price decline

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 67/105

We will illustrate the price-yield relationshipfor a plain vanilla bond.

The bond is assumed to have 10 years tomaturity, a face value of $ 1,000, and a coupon

of 7% per annum payable semi-annually.

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 68/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 69/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 70/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 71/105

y is the semi-annual YTM

c is the semi-annual coupon

N is the number of remaining coupons

The convexity of a bond is defined as:

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 72/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 73/105

Take the 5-year T-note

Price is 978.9440

Coupon is 6% per annum

YTM is 6.50% per annum

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 74/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 75/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 76/105

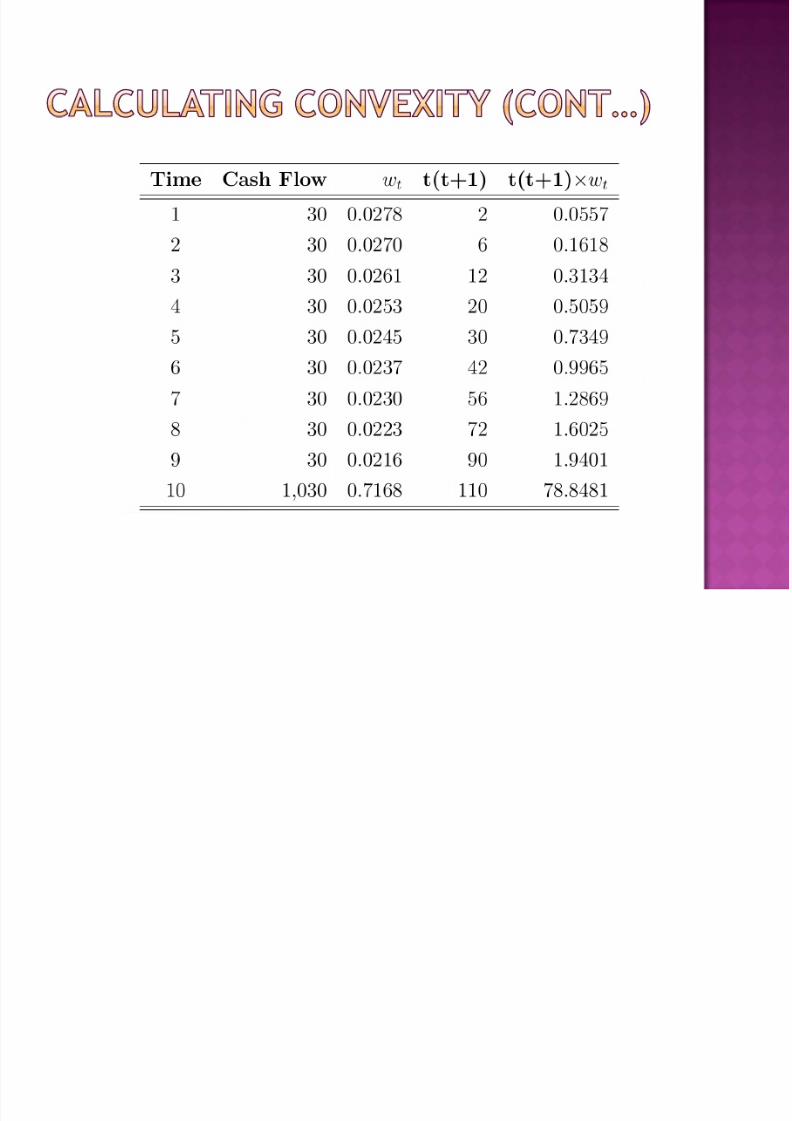

The convexity in semi-annual terms is86.4458

The convexity in annual terms is 21.6115

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 77/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 78/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 79/105

Consider a 50b.p increase in the YTM of a 5-yearT-note

The new price will be 958.4170

The exact price change is:

958.4170 – 978.9440 = -20.5270

The price change due to duration is:

-4.3853 x 978.9440 x0.005 = -21.4648

The price change due to convexity is:0.5X21.6115X978.9440X(0.005)2 = 0.2645

The approximate change due to both factors is:

-21.4648 + 0.2645 = -21.2003

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 80/105

The primary factors which influence a bond’sconvexity are the following

Duration

Cash flow distribution

Market yield volatility

Direction of yield change

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 81/105

Convexity is positively related to theduration of a bond

Long duration bonds have higher convexity thanbonds with a shorter duration

The convexity factor captures the relationbetween duration and convexity

Convexity factor =[Convexity in % x 100] ÷absolute yield change in basis points

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 82/105

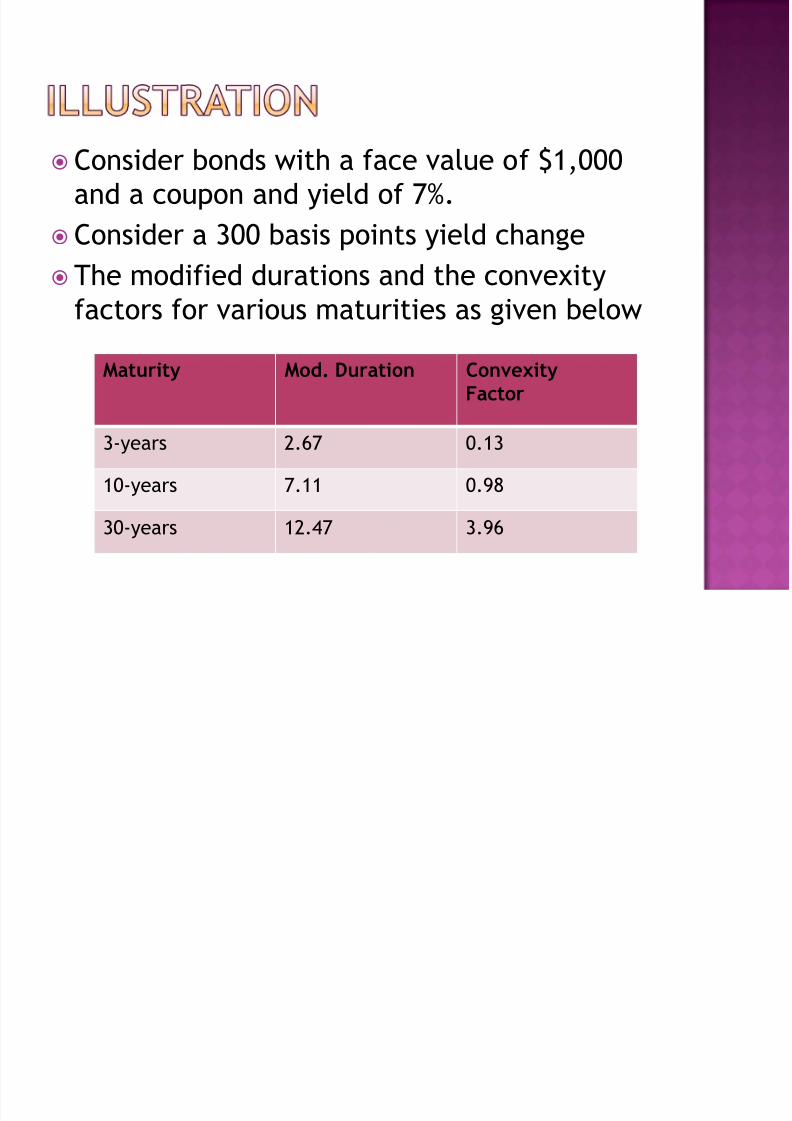

Consider bonds with a face value of $1,000and a coupon and yield of 7%.

Consider a 300 basis points yield change

The modified durations and the convexityfactors for various maturities as given below

Maturity Mod. Duration Convexity

Factor

3-years 2.67 0.13

10-years 7.11 0.98

30-years 12.47 3.96

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 83/105

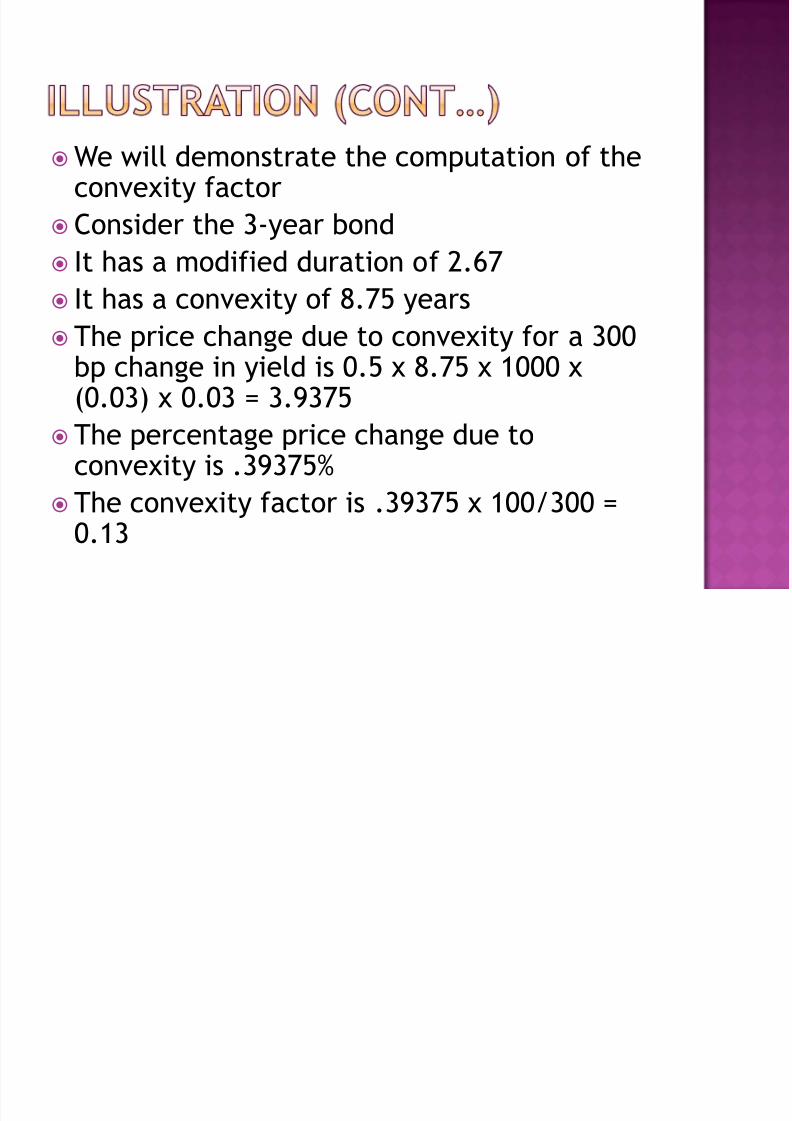

We will demonstrate the computation of theconvexity factor

Consider the 3-year bond

It has a modified duration of 2.67

It has a convexity of 8.75 years The price change due to convexity for a 300

bp change in yield is 0.5 x 8.75 x 1000 x(0.03) x 0.03 = 3.9375

The percentage price change due toconvexity is .39375%

The convexity factor is .39375 x 100/300 =0.13

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 84/105

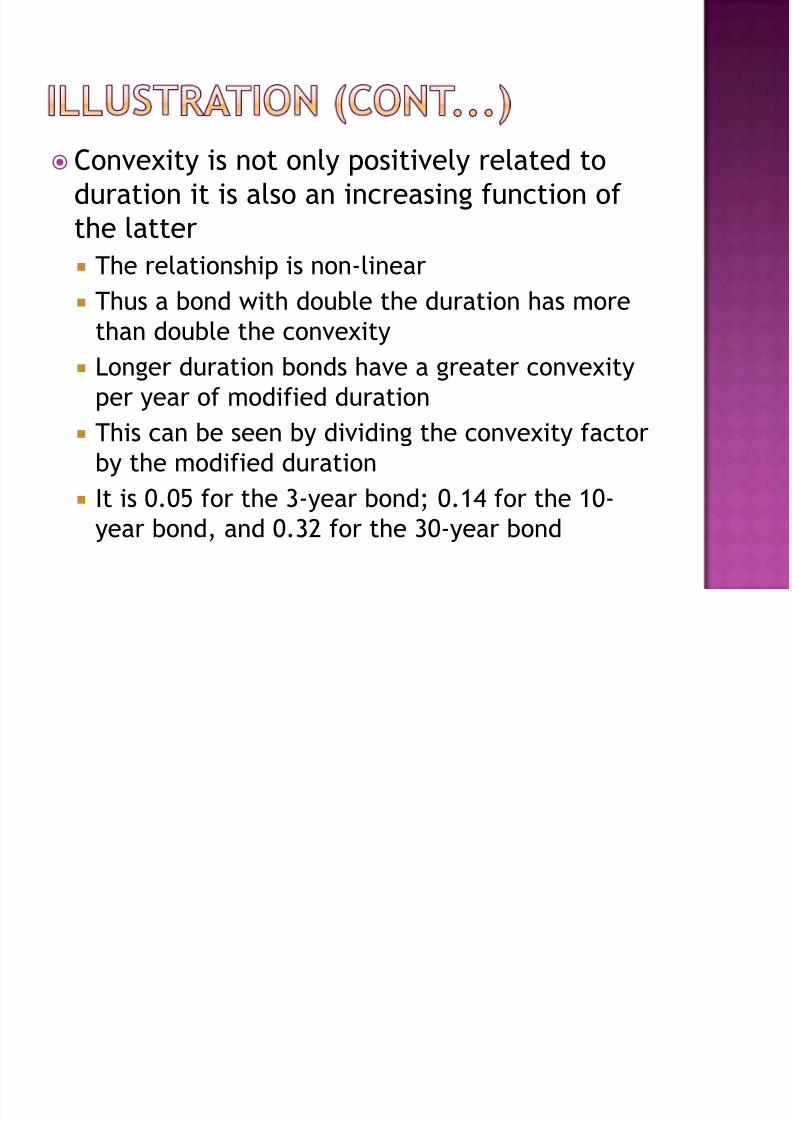

Convexity is not only positively related toduration it is also an increasing function ofthe latter

The relationship is non-linear

Thus a bond with double the duration has morethan double the convexity

Longer duration bonds have a greater convexityper year of modified duration

This can be seen by dividing the convexity factorby the modified duration

It is 0.05 for the 3-year bond; 0.14 for the 10-year bond, and 0.32 for the 30-year bond

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 85/105

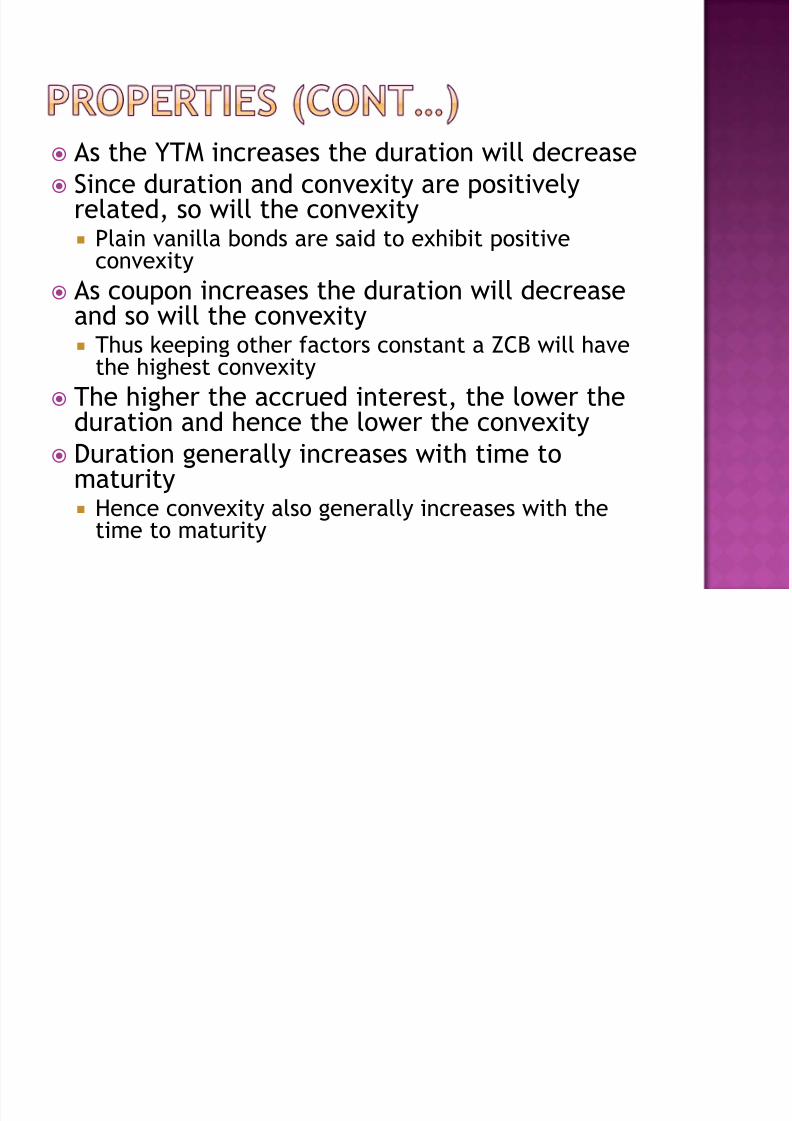

As the YTM increases the duration will decrease Since duration and convexity are positively

related, so will the convexity Plain vanilla bonds are said to exhibit positive

convexity

As coupon increases the duration will decreaseand so will the convexity Thus keeping other factors constant a ZCB will have

the highest convexity

The higher the accrued interest, the lower the

duration and hence the lower the convexity Duration generally increases with time to

maturity Hence convexity also generally increases with the

time to maturity

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 86/105

Convexity is positively related to the degreeof dispersion in cash flows

If we consider two bonds with the sameduration the bond with more dispersed cashflows will have a higher convexity

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 87/105

Consider a 30-year bond with a face value of$1,000 and coupon and yield of 7%

The duration is 12.91 years and the modifiedduration is 12.47

The convexity factor for a 300 bp yield change is3.96

Now consider a zero coupon bond with thesame duration

For a similar yield change the convexity factor isonly 2.46

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 88/105

Long-term cash flows carry progressively higheramounts of convexity Thus they provide higher convexities per year of

modified duration If the convexity per year of modified duration

were to be constant Then cash flow distribution would have no impact on

convexity

A bond’s convexity reflects the convexities ofcomponent cash flows

The wider the dispersion the greater is the convexityeffect And it is the long-term cash flows which are

responsible

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 89/105

Convexity is positively related to marketyield volatility

Higher volatility in interest rates createslarger convexity effects

The curvature of the price-yield curve ismore pronounced for larger shifts in the YTM

And greater yield volatility increases the

probability of major yield changes

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 90/105

Convexity is more positively influenced by adownward yield change of a given magnitude

Than by an upward movement of the samemagnitude

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 91/105

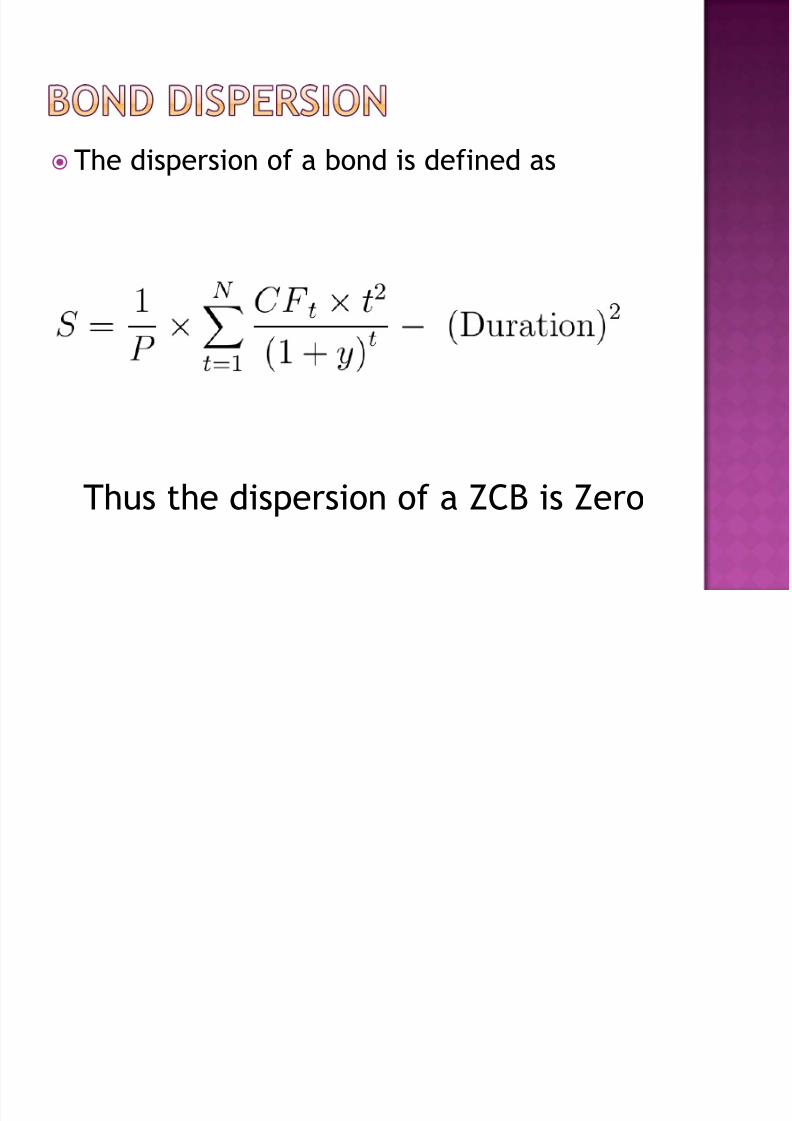

The dispersion of a bond is defined as

Thus the dispersion of a ZCB is Zero

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 92/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 93/105

Thus for a given level of duration, the lowerthe dispersion the lower the convexity

Thus for a given duration zero coupon bondshave the lowest convexity

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 94/105

A bonds dispersion is the variance of the timeto receipt of all cash flows from it

While its duration is the mean of the time toreceipt of all the cash flows

Dispersion measures how spread out in timethe payments are relative to duration

The more spread out the cash flows relative

to the mean (duration) the greater thedispersion

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 95/105

For a given duration the higher thedispersion the greater is the convexity

For plain vanilla bonds both duration anddispersion are non-negative

Thus the convexity is positive

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 96/105

There is a closed-form expression forcomputing the convexity of a plain vanillabond. It may be stated as

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 97/105

c and y are semi-annual ratesN is the number of coupons left

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 98/105

A pension fund has promised a return of 8.40% perannum compounded annually after 8 years on aninvestment of 5MM If it were to invest the corpus in a bond, it is exposed to

two types of risks. The first is re-investment risk

The risk that the cash flows received atintermediate stages may have to be invested atlower rates of interest.

The second is price or market risk The risk that interest rates could increase, causing

the price of the bond to fall at the end of the

investment horizon.

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 99/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 100/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 101/105

Consider a bond with a face value of $ 1,000and 12 years to maturity.

Assume that the coupon rate is equal to theYTM is equal to 8.40% per annum.

It can be shown that the duration is eight years.

Since the liability is 5 MM and the price ofthe bond is 1,000, we need 5,000 bonds

Now consider a one-time change in interestrates right at the outset.

Consider increments and decrements in multiplesof 20 bp from the prevailing rate

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 102/105

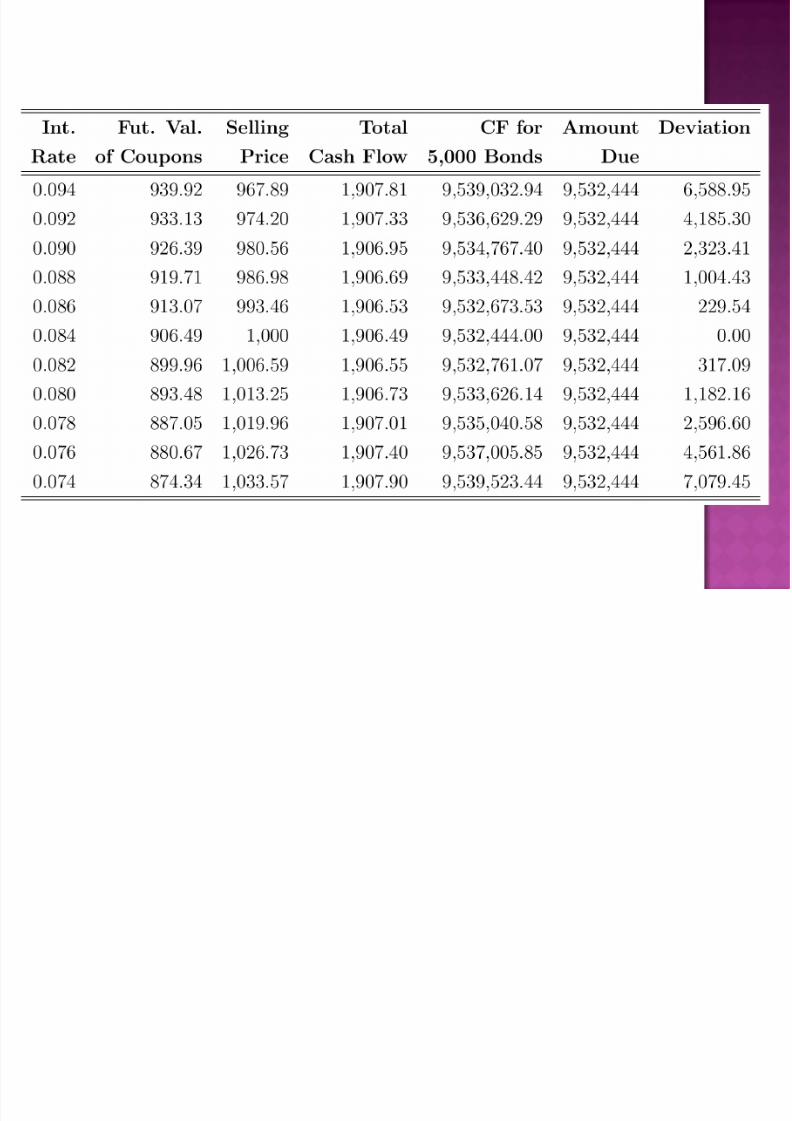

The following table gives the terminal cashflow for various values of the interest rate.

The income from reinvested coupons steadilyincreases with the interest rate

The sale price steadily declines with the interestrate

When the rate does not change the terminal cashflow is exactly adequate to satisfy the liability

In all the other cases there is a surplus Thus the pension fund will always be able to

satisfy the liability no matter what happens

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 103/105

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 104/105

Thus if the pension fund were to invest in anasset, whose duration is equal to the time tomaturity of its liability Then the funds received will always be adequate to

meet the contractual outflow.

To meet this requirement, certain conditionsmust be satisfied.

First the amount invested in the bonds must beequal to the present value of the liability.

In this case since the bond is assumed to beselling at par, we need to invest in 5000 bonds.

8/11/2019 FISD-05

http://slidepdf.com/reader/full/fisd-05 105/105

Second, the duration of the asset must equal thematurity horizon of the liability.

In this case the bond has a duration of 8 yearswhich is the investment horizon

Third, there must be a one time change in theinterest rate, right at the very outset.

Fourth, there must be a parallel shift in the yieldcurve.

That is all spot rates must change in an identicalfashion