Embed Size (px)

Citation preview

First Data Corporation

Incentive Savings Plan

Summary Plan Description

January 2018

This document is being provided exclusively by your employer, which retains responsibility for the content.

2

This summary plan description (SPD) describes benefits provided to you by the First Data Corporation

Incentive Savings Plan and your rights under the plan. The SPD is based on official plan documents. It is not,

nor is it intended to be, the official plan document, or a contract between First Data and any employee or

contractor, or a guarantee of employment. Every effort has been made to ensure the accuracy of this

information. In the unlikely event that there is a discrepancy between the SPD and the official plan

documents, the official plan documents will control. First Data reserves the right to amend, suspend, or

terminate the plan at any time. First Data has delegated the discretionary authority to interpret the terms of the

plan summarized in this document and determine your eligibility for benefits under its terms to the Benefits

Committee.

This SPD is available through the ISP Website at www.benefits.ml.com. You may have access and the ability

to view and print selected pages from the SPD on the Website. You also have the right to request and receive,

free of charge, a printed copy of the SPD from the First Data Contact Center at Merrill Lynch by calling 1-

844-332-2200 any business day between 8:00 a.m. to 10:00 p.m. Eastern Time.

1

TABLE OF CONTENTS

OVERVIEW ............................................................................................................................. 3

ELIGIBILITY TO PARTICIPATE ............................................................................................... 4

ENROLLING IN THE PLAN ...................................................................................................... 4

YOUR CONTRIBUTIONS .......................................................................................................... 4

Changing Your Contributions ................................................................................................................................6

Eligible Plan Compensation ...................................................................................................................................6

Contribution Limits ................................................................................................................................................7

ROLLOVER CONTRIBUTIONS ................................................................................................. 7

Rollover Contributions from Eligible Employer Plans ..........................................................................................7

Rollover Contributions from an IRA .....................................................................................................................8

Types of Rollovers .................................................................................................................................................9

How to Complete a Rollover ..................................................................................................................................9

EMPLOYER CONTRIBUTIONS ................................................................................................. 9

Types of Contributions ...........................................................................................................................................9

Service Credit .......................................................................................................................................................10

VESTING ............................................................................................................................... 11

HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT (“HEART ACT”) ...................... 12

PLAN INVESTMENT OPTIONS ............................................................................................... 12

Making Investment Choices .................................................................................................................................14

Transferring Existing Balances ............................................................................................................................14

Self-Directed Brokerage Account ........................................................................................................................15

Investment Fund Information ...............................................................................................................................16

Monitoring Your Account ....................................................................................................................................16

PLAN LOANS ......................................................................................................................... 17

Interest on Your Loan ..........................................................................................................................................18

Amount You Can Borrow ....................................................................................................................................18

Loan Repayments .................................................................................................................................................19

Loan Defaults and Deemed Distributions ............................................................................................................20

PLAN WITHDRAWALS .......................................................................................................... 21

After-tax Withdrawal ...........................................................................................................................................21

Age 59 ½ Withdrawal ..........................................................................................................................................21

Rollover Withdrawal ............................................................................................................................................22

2

Disability Withdrawal ..........................................................................................................................................22

Hardship Withdrawal ...........................................................................................................................................22

TOTAL DISTRIBUTIONS ........................................................................................................ 25

Distribution Options .............................................................................................................................................25

Rollover to Eligible Employer Plans and Individual Retirement Accounts .........................................................27

If You Defer Payment of Your Account ..............................................................................................................27

PAYMENTS TO YOUR DESIGNATED BENEFICIARY .............................................................. 28

QUALIFIED DOMESTIC RELATIONS ORDER (QDRO) ........................................................ 28

TAXES ON PAYMENTS .......................................................................................................... 28

SPECIAL TAX TREATMENT .................................................................................................. 29

SPECIAL TAX NOTICE .......................................................................................................... 30

TYPES OF LEAVE AND DISABILITY ...................................................................................... 30

IMPORTANT PLAN INFORMATION ....................................................................................... 31

Plan Identification ................................................................................................................................................31

Plan Sponsor and Administrator ..........................................................................................................................32

Benefit Review Process........................................................................................................................................33

Situations Affecting Your Benefits ......................................................................................................................34

Changes to the Plan ..............................................................................................................................................35

Your Legal Rights Under the Plan .......................................................................................................................35

3

Overview

The First Data Corporation Incentive Savings Plan is a 401(k) plan that gives you an easy and effective way to

save for retirement. There are many advantages to participating in the plan. You may:

Defer taxes on your before-tax contributions to the plan

Make Roth after-tax contributions to the plan and, if certain conditions are met, withdraw your

contributions and earnings tax-free

Be eligible to receive plan contributions from First Data

Defer taxes on the investment earnings on all plan contributions

Because the plan’s purpose is to help you save for retirement, you might not be allowed to withdraw money out

of the plan until you leave First Data, unless you meet special requirements.

Qualified Plans

In order to provide tax-deferred savings the plan must be qualified. That means it must meet certain requirements

of the Internal Revenue Service (IRS). For example, the plan must:

Be maintained for the exclusive benefit of plan participants and beneficiaries

Not discriminate in favor of highly compensated employees

Meet minimum standards for participation and vesting

Provide that neither you nor the plan can assign your benefits to someone else, except in limited

circumstances, such as a Qualified Domestic Relations Order (QDRO) if you get a divorce or have to pay

child support

Putting Money into Your Account

If you’re eligible to participate in the plan, you can contribute through payroll deductions. You choose how much

to contribute on a before-tax basis and/or on a Roth after-tax basis. You may also be able to roll over balances

from another eligible employer plan or Individual Retirement Account (IRA).

First Data may also make contributions to the plan.

Investing Your Contributions

You can invest the contributions to your account in one or more of the plan’s investment options. The investment

options offer different levels of risk, which affect the potential return on your investment.

The plan is intended to meet the requirements under Section 404(c) of the Employee Retirement Income Security

Act of 1974 (ERISA). This means that the plan offers a range of investment options and the opportunity to make

your own investment decisions. The plan also provides information about your investment options and the

risk/return characteristics of each option. As a result, plan fiduciaries generally are not liable for any losses, or by

reason of any breach, resulting from your investment instructions and decisions.

Taking Money Out of Your Account

While you work for First Data, you may be able to take money out of the plan through a loan or withdrawal.

When you take a loan, you borrow money from your account and pay it back to your account, with

interest, over a specified period.

When you take a withdrawal, your account balance is permanently reduced. Taxes may apply.

When you leave First Data, you can also elect a total distribution from the plan. Your account balance

will be permanently reduced.

4

Eligibility to Participate

Employees who are Eligible

You are immediately eligible to participate in the Incentive Savings Plan if you are employed by First Data

Corporation or one of its affiliates that has adopted the plan as a participating employer, and treated as an

employee for the purpose of First Data’s U.S. payroll. Before you can begin contributing, you must be enrolled in

the plan. You are immediately eligible to receive First Data contributions, if any, that may be made. First Data

currently makes no contributions to the plan.

You are not eligible to participate in the plan if you are:

Covered by a collective bargaining agreement (unless the agreement expressly provides for participation)

Paid in a currency other than the U.S. dollar

An independent contractor, regardless of any reclassification as an employee by a court or government

agency

A leased employee

An employee whose contract states that you are not eligible

An employee who is a resident of Puerto Rico

An intern who is hired after December 31, 2015

Enrolling in the Plan You choose whether to contribute to the Incentive Savings Plan.

As of January 1, 2016, you will be automatically enrolled in the plan with a before-tax contribution rate of 4% of

your eligible pay and your contributions will be invested in the Vanguard Target Date Trust I Fund that most

closely matches your target retirement year (based on an assumed retirement age of 65) approximately 30 days

following your date of hire (if you were automatically enrolled in the plan before January 1, 2016, you were

enrolled at a rate of 3% of your eligible pay). You may opt out of automatic enrollment, remain eligible, and wait

to enroll at a later date.

If you are automatically enrolled, you will also be enrolled in the contribution escalation program. Your before-

tax contribution rate will increase by 1% each year to a maximum of 10% of your eligible pay.

If you wish to enroll before the automatic enrollment takes effect or choose different enrollment elections, you

may enroll on the ISP Website at www.benefits.ml.com or by calling the First Data Contact Center at Merrill

Lynch at 1-844-332-2200 any business day between 8:00 a.m. to 10:00 p.m. Eastern Time.

Once you are enrolled, your contributions start as soon as administratively possible.

Even if you decide not to contribute money to the Incentive Savings Plan, as a participant, you may be eligible to

receive certain contributions made by First Data to the Incentive Savings Plan.

Your Contributions You can contribute to the Incentive Savings Plan on a before-tax or Roth after-tax basis. Once you choose which

type of contribution to make and how much to contribute, your contributions are deducted automatically from

your pay.

You can also roll over money from an eligible employer plan or an IRA.

Generally, if you are a Non-Highly Compensated Employee (those whose base and bonus was less than $120,000

in 2017) you may contribute up to 50% of your eligible pay on a before-tax and/or Roth basis. If you are a new

hire, you will be considered a Non-Highly Compensated Employee for the remainder of the calendar year in

which you were hired, regardless of your current compensation. If you are a Highly Compensated Employee

(those who made $120,000 or more in 2017) you may contribute up to 6% of your eligible pay on a before-tax

and/or Roth basis. This percentage is deducted from your paycheck each payroll period until you change your

5

contribution rate, stop your contributions entirely, or reach statutory or plan-imposed limits on combined before-

tax and Roth contributions, or your eligible compensation for the plan year has reached the IRS-imposed annual

compensation limit ($275,000 in 2018).

In addition, if you’ll be age 50 or older in the current plan year, you’re eligible to make additional before-tax

and/or Roth catch-up contributions.

Your contributions are subject to IRS limits. There could be additional limits on how much you can contribute to

the plan if certain tax law limits apply.

Before-Tax Contributions

If you choose to contribute to the plan on a before-tax basis, First Data deducts contributions from your pay

before most federal and state taxes are withheld. This reduces your taxable income for the year.

You do not pay taxes on your before-tax contributions until you withdraw those contributions from your account.

The IRS places limits on contributions.

Unless you elect how your contributions should be invested, your before-tax contributions will be automatically

invested in the Vanguard Target Date Trust I Fund that most closely matches your target retirement year (based

on an assumed retirement age of 65).

Roth Contributions

If you choose to contribute to the plan on a Roth after-tax basis, First Data deducts contributions from your pay

after federal and state taxes are withheld. This does not reduce your taxable income now, but your Roth

contributions and any earnings on them can grow tax-free if they are withdrawn or distributed in a “qualified

distribution.” The same IRS-imposed limits that apply to before-tax contributions also apply to Roth

contributions.

Withdrawals and distributions of your Roth contributions and earnings will be tax-free if they are part of a

“qualified distribution.” A qualified distribution is one that is taken at least five tax years from the year of your

first Roth contribution and after you have reached age 59½, become totally and permanently disabled or are

deceased. If you do not follow these rules, your Roth contributions may be subject to taxes and penalties upon

withdrawal or distribution. Note that as with your before-tax contributions, your Roth contributions cannot be

withdrawn while you are still employed with First Data unless you are at least age 59½ or have a hardship. Your

Roth rollover contributions can be withdrawn at any time. Thus if you take a hardship withdrawal of your Roth

contributions, or withdraw your Roth rollover contributions, while you are still employed, the withdrawal amount

will be subject to the 10% penalty tax and the earnings will be taxed unless you are at least age 59½ or are totally

and permanently disabled.

Roth contributions allow tax-diversification within the plan. You should talk with your own financial or tax

adviser before you decide whether to make Roth contributions.

After-Tax Non-Roth Contributions

You may have money in an after-tax source if you previously contributed to the plan on an after-tax basis. The

plan does not allow any new after-tax contributions.

Because you’ve already been taxed on your after-tax contributions, you won’t be taxed again when you withdraw

those contributions from the plan. However, you’ll be taxed on the investment earnings when you take a

withdrawal.

Catch-Up Contributions

If you will be age 50 or older in the current plan year, you’re eligible to make additional before-tax and/or Roth

after-tax catch-up contributions to the Incentive Savings Plan.

Catch-up contributions are before-tax and/or Roth contributions that are made in excess of either of the following

limits:

6

Annual IRS employee contribution limit (i.e. 402(g) limit, which is $18,500 in 2018)

The plan’s maximum employee contribution limit (50% of eligible pay or, for Highly Compensated

Employees, 6% of eligible pay)

Changing Your Contributions

Your contribution rate is the percentage of your income you elect to contribute to the plan. Contribution

percentage changes take effect in the plan as soon as administratively possible after your request is received. If

you stop contributing, you can start again at any time. You may change your contribution rate on the ISP

Website or by calling the First Data Contact Center at Merrill Lynch.

Annual Contribution Rate Increase

You can choose to have your before-tax contribution rate increased automatically each year by entering an annual

rate increase percentage on the ISP Website or by calling the First Data Contact Center at Merrill Lynch.

Your before-tax contribution rate will continue to increase each year by the percentage you enter until you reach

your target contribution rate. Your contributions are subject to IRS limits and plan limits.

If you are automatically enrolled in the Incentive Savings Plan, you will also be enrolled in the contribution

escalation program. Your before-tax contribution rate will increase by 1% each subsequent year up to a maximum

of 10% or for Highly Compensated Employees, up to a maximum of 6%. You may opt out of the escalation

program at any time.

Example

If your initial before-tax contribution rate is 4% and you choose a 1% annual rate increase up to 8%, your before-

tax contribution the next year will be 5%. The rate will continue to increase each subsequent year by 1% up to the

8% maximum you elected.

Eligible Plan Compensation

The IRS limits the amount of your eligible pay that’s used to determine your contributions for a plan year. The

limit amount is indexed and may change each year. The limit for 2018 is $275,000. Once you have received

eligible pay in a plan year equal to the annual limit, no more contributions will be taken from your pay or

otherwise made on your behalf for the rest of the plan year.

For the purposes of calculating the amount you can contribute to the Incentive Savings Plan, your eligible pay

includes:

Base pay or regular salary

Commission

Overtime

Bonuses

Elective deferrals made under Internal Revenue Code Section 401(k) or 125

The IRS limits the amount of eligible pay used to determine your contributions.

Eligible pay does not include:

Non-cash compensation (including any equity plan awards)

Severance payments

Gross-up payments

Reimbursements and expense allowances

Special awards

Fringe benefits

BRAVO! Awards

7

Payments made under the Long Term Cash Award Plan

Any other amounts that receive special tax benefits under the IRS but are not specifically included in

eligible pay

Contribution Limits

The IRS sets limits on the contributions to your account. Whether you reach these limits depends on your pay,

your contributions, and First Data contributions you receive for the year.

These limits may be indexed by the IRS from year to year.

Before-Tax and Roth Contribution Limit

The IRS limits your combined before-tax and Roth contributions for 2018 to $18,500. Before-tax and Roth

contributions made by those who are Highly Compensated Employees will be further limited to 6% of eligible

compensation. If you are a new hire, you will be considered a Non-Highly Compensated Employee for the

remainder of the calendar year in which you were hired, regardless of your current compensation.

However, if you’ll be age 50 or older in 2018, you’re also eligible to make additional catch-up contributions of up

to $6,000 for 2018, and additional amounts in future plan years.

These limits apply not only to the Incentive Savings Plan, but also to all 401(k) plans you participate in during the

calendar year. Contact the First Data Contact Center at Merrill Lynch if you have questions about how your

participation in other plans affects your Incentive Savings Plan contributions.

Total Annual Contribution Limits

The total of all employee before-tax and employer contributions to your account for a calendar year are limited to

the lesser of:

$55,000 for 2018 (This amount is indexed and may change each year.)

100% of your pay

These limits apply to all defined contribution plans sponsored by the same employer (as defined by the IRS) in a

calendar year.

Rollover Contributions

Before joining First Data, you may have participated in another eligible employer plan or IRA. You can defer

paying taxes on your retirement savings if you roll over an eligible distribution from another eligible employer

plan or IRA into the Incentive Savings Plan.

A rollover contribution must be deposited into the Incentive Savings Plan within 60 days of the date it is made to

you. If the rollover contribution is not deposited within 60 days, the plan will not be able to accept it under IRS

guidelines and the payment may become taxable to you.

The 60-day requirement does not apply to direct rollovers, which are made payable directly to the Incentive

Savings Plan from the distributing employer plan or IRA.

Rollover Contributions from Eligible Employer Plans

You can roll over an eligible distribution from another eligible employer plan to the Incentive Savings Plan.

The following are not considered eligible rollover distributions:

Substantially equal periodic payments made at least annually over:

o Your life expectancy

o The joint life expectancy of you and your beneficiary

o A specified period of 10 or more years

Required minimum distribution amounts

8

Payments made to you as a nonspouse beneficiary

Payments made to you as an alternate payee under a QDRO

Hardship withdrawals

Loans treated as deemed distributions due to default

Pass-through dividends from an Employee Stock Ownership Plan (ESOP)

Payments made to correct contributions in excess of the plan’s contribution limits

Eligible Employer Plans

You can roll money into the Incentive Savings Plan if it’s an eligible distribution from an eligible employer plan

or an IRA.

These types of plans may be considered eligible employer plans:

Any plan qualified under Internal Revenue Code Section 401(a), including:

o 401(k) plan

o Defined benefit plan

o Profit sharing or thrift plan

o Money purchase pension plan

o Stock bonus plan

o ESOPs

Section 403(b) tax-sheltered annuity plan

Certain governmental Section 457 plans

SIMPLE 401(k) plan

Section 403(a) annuity plan

These types of plans are not eligible employer plans for rollover contribution purposes:

Excess plan

Nonqualified plan

Stock option plan

Rollover Contributions from an IRA

You can roll money into the Incentive Savings Plan from:

A traditional IRA to which you’ve been making tax-deductible contributions, Roth contributions, or

personal after-tax contributions

An IRA you set up to accept a rollover of before-tax, Roth, and/or after-tax balances from an eligible

employer plan

Eligible IRAs

You can roll over taxable distributions from these types of IRAs:

Traditional IRA

Roth IRA

An IRA set up to receive a distribution from an eligible employer plan

SIMPLE IRA in which you participated for two or more years

You can’t roll over a distribution from these types of IRAs:

SIMPLE IRA in which you participated for less than two years

SEP IRA

SARSEP IRA

Education IRA

9

Types of Rollovers

Direct Rollover

A direct rollover occurs when the distributing eligible employer plan or an IRA makes the eligible distribution

payable to the Incentive Savings Plan.

The portion of the eligible distribution that’s directly rolled over isn’t subject to the mandatory 20% federal tax

withholding and the 10% penalty tax on early distributions.

60-Day Rollover

When an eligible distribution is made payable to you, you can roll over all or part of it to the Incentive Savings

Plan. You must deposit the rollover into the plan within 60 days after it is distributed to you.

The money that is not directly rolled over may be subject to tax withholding and penalties if distributed directly

to you. If you want to roll over the entire eligible distribution amount, you must use your own money to replace

the money that was withheld for taxes. You’ll receive a credit for the taxes withheld when you file your personal

tax return.

How to Complete a Rollover

Requesting a Rollover into the Plan

To roll money into the plan, request a Rollover Contribution Form on the ISP Website or by calling the First Data

Contact Center at Merrill Lynch. Your rollover money will be invested according to the elections you stated on

your Rollover Form. If you do not have an election on your Rollover Form, your rollover contribution will be

invested in your current investment elections. Your rollover contribution is credited to a separate rollover source

in the Incentive Savings Plan.

The Plan does not accept stock certificates or any “in-kind” transfers for a rollover contribution.

Rollover Check

Send the rollover contribution to the First Data Contact Center at Merrill Lynch along with the Rollover

Contribution Form. The check must be made payable to Trustee for First Data Corporation Incentive Savings

Plan, FBO (your name). The address for Merrill Lynch is listed under the Plan Information section of this

Summary Plan Description.

If the distributing employer plan or IRA makes the check payable to you, endorse the check and, under your

signature, make it payable to Trustee for First Data Corporation Incentive Savings Plan, FBO (your name).

If you are not completing a direct rollover, then the rollover must be deposited with the Incentive Savings Plan no

later than 60 days after the date of distribution.

Employer Contributions

How Employer Contributions Work

If you’re eligible, First Data may add to your account through employer contributions. When you leave First

Data, you receive only the vested portion of your employer contributions.

Types of Contributions

Employer Matching Contributions

You may have a balance in the Employer Matching Contribution source if you were eligible to receive the

contributions before January 1, 2014. Effective January 1, 2014, Employer Matching Contributions are no longer

made.

10

Employer Special Contributions

You don’t have to contribute to the Incentive Savings Plan to be eligible for Employer Special Contributions. For

any year, First Data may elect to contribute an additional percentage of your eligible pay so long as you are

employed on the last day of the year.

Employer Service Related Contributions

You may have a balance in the Service Related Contribution (SRC) source if you were eligible to receive the

contributions before January 1, 2008. Effective January 1, 2008, Service Related Contributions are no longer

made.

Employer ISP Plus Contributions

You may have money in the ISP Plus Contribution source if you were eligible to receive the contributions before

January 1, 2008. Effective January 1, 2008, ISP Plus contributions are no longer made.

Prior Plan Employer Match Contributions

You may have money in a Prior Plan Employer Match source if you’re a participant of a plan that merged into the

Incentive Savings Plan.

Qualified Nonelective Contributions

You may receive a Qualified Nonelective Contribution (QNEC) if you’re a non-highly compensated employee

and meet certain other requirements, and a contribution is required to comply with certain IRS limits. If the plan

fails certain nondiscrimination tests imposed by the IRS, First Data, in its discretion, may make additional

contributions to the plan that would cause the plan to pass the nondiscrimination tests.

You’re 100% vested in this money. However, you’re prohibited from withdrawing these contributions and

earnings associated with these contributions until age 59 ½, or upon separation from service, whichever occurs

first.

Service Credit

What Service Means

Service means the length of time you work for First Data. Your years of service determine when your employer

contributions and earnings are vested. You earn service from the date you first perform an hour of service until

you leave First Data. An hour of service is time for which you’re paid or entitled to be paid.

Period of Leave or Separation from Service

Except for a maternity or paternity leave, you are considered to have a one-year leave or separation from service if

you return to work one year following the earlier of these events:

The date you resign, are terminated, or retire

The first anniversary of the date you began a paid or unpaid absence for any other reason, such as

vacation, holiday, illness, disability, leave of absence, layoff, etc.

When You Return Before Having a One-Year Period of Leave

If you return to work with First Data within 12 months of your leave period, you receive service credit (for

eligibility and vesting purposes) for the time you were gone.

If you resign, are terminated, or retire during your leave period and return to work on or before the first

anniversary of the date your leave began, you receive service credit (for eligibility and vesting purposes). This

credit is for the period between the start of your leave period and the first anniversary of your initial leave date.

11

When You Return After Having a One-Year Period of Leave

You will receive credit for your service prior to your leave period when you return to work, but will not be

credited for service for the time you were on your leave period.

Vesting Vesting refers to the percentage of employer contributions and related investment earnings you own based on

your years of service, that is, the length of time you work for First Data. Your years of service determine when

your employer contributions and earnings are vested. You earn service credit from the date you first perform an

hour of service until the date you leave First Data.

You’re always 100% vested in any of the following sources that you might hold in your account:

Your Before-Tax Contributions

Your Roth Contributions

Your Pre-87 After-Tax Contributions

Your Post-86 After-Tax Contributions

Your Rollover Contributions

Your Roth Rollover Contributions

Your After-Tax Rollover Contributions

Your Employer Service Related Contributions

Your Employer Special Contributions

Your Prior Plan Employer Match Contributions

Your Qualified Voluntary Elective Contributions (QVEC)

Your Qualified Nonelective Contributions (QNEC)

The investment earnings on these contribution sources

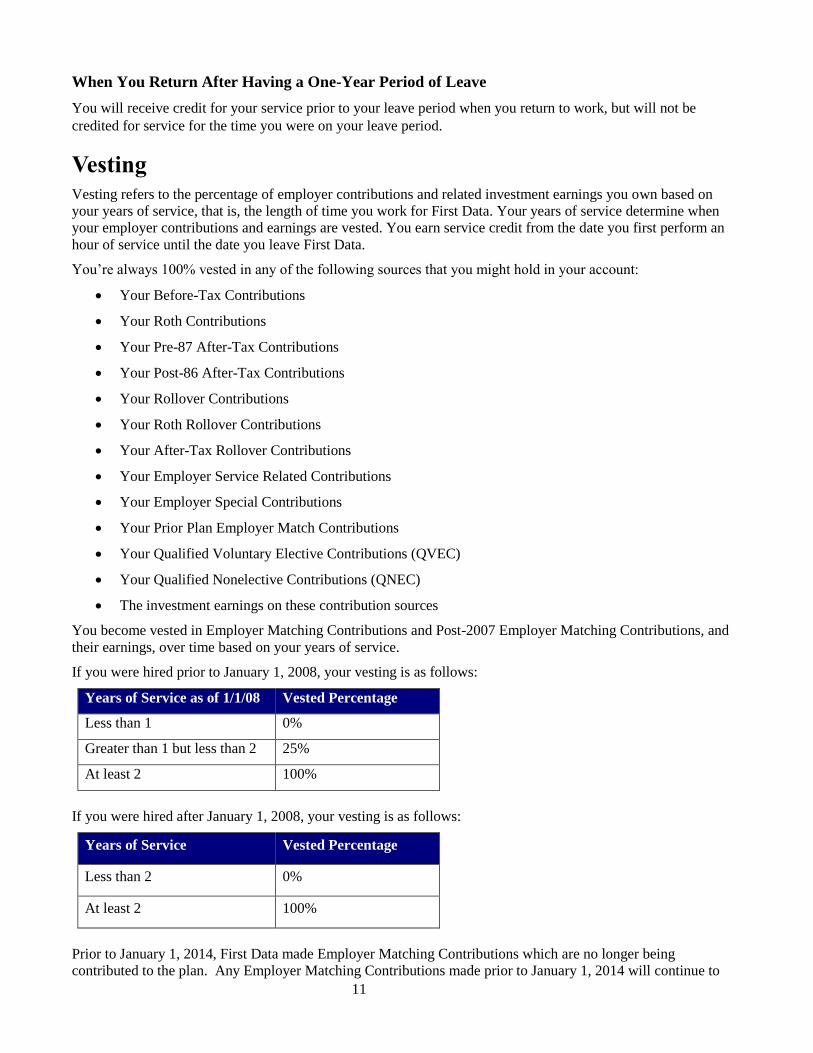

You become vested in Employer Matching Contributions and Post-2007 Employer Matching Contributions, and

their earnings, over time based on your years of service.

If you were hired prior to January 1, 2008, your vesting is as follows:

Years of Service as of 1/1/08 Vested Percentage

Less than 1 0%

Greater than 1 but less than 2 25%

At least 2 100%

If you were hired after January 1, 2008, your vesting is as follows:

Years of Service Vested Percentage

Less than 2 0%

At least 2 100%

Prior to January 1, 2014, First Data made Employer Matching Contributions which are no longer being

contributed to the plan. Any Employer Matching Contributions made prior to January 1, 2014 will continue to

12

vest based on the above schedule. Prior to January 1, 2008, First Data made SRC and ISP Plus contributions,

which are no longer being contributed to the plan. If you leave First Data:

You receive the vested portion of your employer contributions

Any nonvested portion of your employer contributions are forfeited

You become 100% vested in employer contributions and their earnings when:

You reach normal retirement age of 65 while employed with First Data

You become totally and permanently disabled while employed with First Data

First Data Corporation terminates the plan

You die while employed with First Data

You die while on active military leave

Forfeitures and Restoring Forfeited Nonvested Amounts

If you leave First Data before you become fully vested, you forfeit the portion of your employer contributions that

is not vested.

This forfeiture occurs at the earlier of:

The date you take a total distribution from the plan

The quarter following 90 days from the date you leave First Data

First Data may use forfeitures to reduce future plan contributions or to pay plan expenses.

Restoring Forfeited Amounts

If you forfeit a nonvested amount, but return to work before you have five consecutive one-year periods of leave,

you can restore your account by “buying back” the forfeited amount. In other words, you can repay the amount

you received as a distribution. Employer contributions that were forfeited will be deposited back into your

account.

If you received a total distribution because you left First Data, in order to have the forfeited amount reinstated,

you must repay the amount to the Incentive Savings Plan by the earlier of:

Five years after the date you are rehired

The end of the first period of 5 consecutive one-year periods of leave beginning after the distribution

Heroes Earnings Assistance and Relief Tax Act (“HEART Act”) If you take a leave from First Data’s employment for active military duty and die while on such leave your

account will become fully vested.

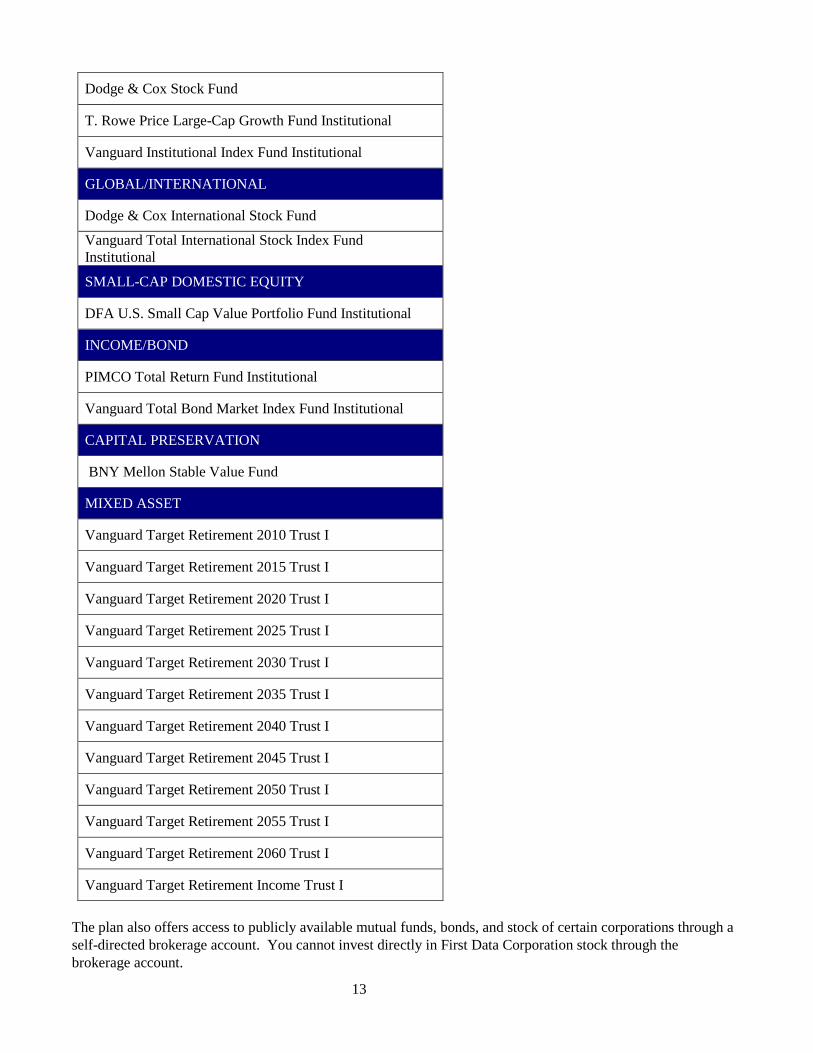

Plan Investment Options

The Incentive Savings Plan offers a range of investment funds for your contributions. Each fund and its manager

are listed below:

MID-CAP DOMESTIC EQUITY

Wells Fargo Discovery Fund Institutional

Vanguard Extended Markets Index Fund Institutional

LARGE/MULTI-CAP DOMESTIC EQUITY

13

Dodge & Cox Stock Fund

T. Rowe Price Large-Cap Growth Fund Institutional

Vanguard Institutional Index Fund Institutional

GLOBAL/INTERNATIONAL

Dodge & Cox International Stock Fund

Vanguard Total International Stock Index Fund

Institutional

SMALL-CAP DOMESTIC EQUITY

DFA U.S. Small Cap Value Portfolio Fund Institutional

INCOME/BOND

PIMCO Total Return Fund Institutional

Vanguard Total Bond Market Index Fund Institutional

CAPITAL PRESERVATION

BNY Mellon Stable Value Fund

MIXED ASSET

Vanguard Target Retirement 2010 Trust I

Vanguard Target Retirement 2015 Trust I

Vanguard Target Retirement 2020 Trust I

Vanguard Target Retirement 2025 Trust I

Vanguard Target Retirement 2030 Trust I

Vanguard Target Retirement 2035 Trust I

Vanguard Target Retirement 2040 Trust I

Vanguard Target Retirement 2045 Trust I

Vanguard Target Retirement 2050 Trust I

Vanguard Target Retirement 2055 Trust I

Vanguard Target Retirement 2060 Trust I

Vanguard Target Retirement Income Trust I

The plan also offers access to publicly available mutual funds, bonds, and stock of certain corporations through a

self-directed brokerage account. You cannot invest directly in First Data Corporation stock through the

brokerage account.

14

Information about the funds and their past performance is available on the ISP Website. The site also provides a

variety of resources to help you monitor your investments.

Default Investment Fund

If you don’t provide an investment election for your contributions they will be automatically invested in the

Vanguard Target Retirement Trust I Fund that most closely matches your target retirement year (based on an

assumed retirement age of 65).

Risk versus Return

The different investment options provide a wide range of risk and potential return.

You may want to consider your financial situation and how long you intend to have the money invested when

making your investment choices.

Information about the funds and their past performance is available on the ISP Website and by request. The site

also provides a variety of resources to help you monitor your investments.

By providing you with a range of investment alternatives with different risk and reward characteristics and by

allowing you to control how your account balances are invested, the plan is intended to satisfy section 404(c) of

ERISA, as amended. Neither First Data Corporation, the Investment or Benefits Committees, the trustee, any

investment manager, nor any plan fiduciary is responsible for any losses in your plan accounts, or by reason of

any breach, that result from your investment decisions—or your failure to make sound investment decisions.

Therefore, it’s very important you understand the investment choices available to you, to monitor your plan

investments, and to ensure that your choices and decisions are appropriate in light of your individual situation.

Making Investment Choices

When you enroll in the plan, you may elect the percentage of your contributions to invest in each investment

option. You may choose that all of your contributions be invested in one investment or among two or more

investments. Investments must be in 1% increments.

For Future Contributions

You can change your investment choices at any time. Any change you make prior to 4pm ET will be reflected on

the ISP website the next business day and affects future contributions only beginning with the next payroll cycle.

Changing your investment choices does not affect the investment of your existing account balance.

Transferring Existing Balances

Fund Transfers

You can transfer current balances among the investment options at any time. When you make a fund transfer, you

take a percentage or dollar amount out of one investment option and move it into another.

A fund transfer affects your existing account balance only. It does not affect how your future contributions are

invested.

Fund Reallocations

You can reallocate (redistribute) your total account balance among the investment options. When you make a

fund reallocation, you specify the percentage of your total account balance that you want invested in each option.

A fund reallocation affects your existing account balance only. It does not affect how your future contributions

are invested.

If you request a fund transfer or fund allocation before the close of the New York Stock Exchange (NYSE)

(generally 3:00 p.m. Central Time) on any day that the NYSE is open, the change will normally take place at that

day’s closing price. If you request to transfer account balances among investment options after the close of the

15

NYSE, or on a day that the NYSE is not open, the change will occur at the closing price on the next day that the

NYSE is open.

Investment Fees and Expenses

The investment managers charge an annual fee in connection with the management of the investment options.

These fees, along with any brokerage commissions, are charged against the fund’s assets. Therefore, these

investment manager fees are reflected in each fund’s net asset value (NAV), or unit value, and are not directly

debited from your account. The monthly management fees are currently computed at an annual percentage rate of

the fund’s net assets. Please review the fund prospectus on the ISP Website for the most up-to-date management

expense and fee information.

Self-Directed Brokerage Account

The self-directed brokerage account gives you the opportunity to create a personal investment mix by allowing

you to invest a portion of your Incentive Savings Plan account in any publicly available stocks (other than First

Data stock), bonds, or mutual funds. Two self-directed brokerage accounts are available to you: a Direct

Advantage account, in which you alone direct the investments, and an Advisor Advantage account, in which you

direct the investments with the assistance from a Merrill Lynch advisor.

A $50 administrative fee is charged to the cash component of the self-directed brokerage account on an annual

basis. Commissions and transaction fees on trades within the self-directed brokerage account are paid from your

balance in the self-directed brokerage account.

The self-directed brokerage account is an alternative within the plan that is intended to provide experienced,

knowledgeable investors with investment choices beyond those in the plan’s core investment funds. The core

funds are the mutual funds in the Incentive Savings Plan listed under the Investment Options.

You should not use this investment alternative unless you have significant experience managing your

investments, extensive knowledge regarding the risks of investing in individual stocks and bonds and similar

investment instruments, and the time and ability to closely monitor your investments in this fund.

Transferring Existing Balances to the Self-Directed Brokerage Account

To invest in one of the investments available through the self-directed brokerage account, you must first transfer

money to the self-directed brokerage account from any of the core investment options in the Incentive Savings

Plan. The initial transfer and each subsequent transfer must be at least $1,000.

Remember, fund transfers affect your existing account balance only. They don’t affect how your future

contributions are invested. You may not have your contributions invested directly into the self-directed brokerage

account.

The balance you transfer to the self-directed brokerage account is held in the money market account within the

self-directed brokerage account until you invest in other funds or securities in the self-directed brokerage account.

Buying or Selling Investments in the Self-Directed Brokerage Account

Once you transfer money to the self-directed brokerage account, you can buy or sell other investments within the

self-directed brokerage account. You can buy or sell those investments at any time.

Transferring Balances from the Self-Directed Brokerage Account

To transfer money out of the self-directed brokerage account, you must first transfer money from any or all of

your investment options within the self-directed brokerage account to the money market account in the self-

directed brokerage account.

Once the transfer is processed, you can transfer balances out of the self-directed brokerage account to any other

core investment option within the Incentive Savings Plan.

16

Investment Fund Information

All the information below is available on the ISP Website or by calling the First Data Contact Center at Merrill

Lynch. You can also request the following information about any of the investment options from the Plan

Administrator:

A description of the annual operating expenses of each investment option and the total amount of such

expenses as a percentage of the investment option’s NAV (examples of these expenses include

investment management fees, administrative fees, and transaction costs)

Copies of any prospectuses, financial statements and reports, and any other materials relating to the

investment options available under the plan, to the extent such information is provided to the plan

Information concerning the value of shares in the available investment options, as well as the past and

current investment performance (net of expenses)

Information concerning the value of shares in the investment options held in your account

Transfer Restrictions and Redemption Fees

In some circumstances, you may be subject to restrictions on moving money in and out of certain investment

options. These rules apply to the frequency and timing of transferring money among funds.

For the most up to date information regarding transfer restrictions and redemption fees, you may access the

information on the ISP Website.

If you transfer out of a fund, some investment options may block you from transferring money back into the fund

for a specified period of time. Some funds apply this restriction to a minimum dollar amount, while others block

any amount from being transferred back in before the required waiting time.

Monitoring Your Account

How Your Contributions Are Organized

Contributions to your account are divided into these sources:

1. Before-Tax Matched Contributions

2. Before-Tax Unmatched Contributions

3. Roth Contributions

4. Pre-87 After-Tax Contributions

5. Post-86 After-Tax Contributions

6. Rollover Contributions

7. After-Tax Rollover Contributions

8. Roth Rollover Contributions

9. Employer Matching Contributions

10. Post-2007 Employer Matching Contributions

11. Employer Service Related Contributions

12. Employer ISP Plus Contributions

13. Employer Special Contributions

14. Prior Plan Employer Match Contributions

15. Qualified Voluntary Elective Contributions (QVEC)

16. eOne Contributions

17. Qualified Nonelective Contributions (QNEC)

Each source holds the contributions and attributable investment earnings.

17

How Your Account Value Is Determined

Your account value is updated at the end of each business day to reflect these transactions:

Your contributions

Your withdrawals

Your loans

Your loan repayments

Your transfers and reallocations

Gains or losses related to each investment option

Plan Loans

You can borrow money from the Incentive Savings Plan for any reason. You’ll be charged a $50 processing fee

in addition to the amount of your requested loan. Unlike a withdrawal, a loan isn’t taxable and doesn’t

permanently reduce your account balance as long as you repay the loan.

There are two types of loans available:

General purpose

Primary residence

You can request either type of loan on the ISP Website.

You are limited to one of each type of loan (general purpose or primary residence) at any one time. You must pay

off your outstanding loan within either category before requesting a new one.

General Purpose Loan

You can take a general purpose loan for any reason. You must repay the loan within 5 years (60 months).

If you request a general purpose loan, you’ll receive a promissory note and certain disclosures about the loan,

which show:

Loan amount

Loan duration

Interest rate

Repayment amount

You don’t need to return the note. Retain it for your records. Based on your request, the loan proceeds will be

mailed to you within seven days. Payroll will begin deducting loan repayments from your paycheck as soon as

administratively possible. You are responsible for ensuring that loan payments are being properly deducted from

your paycheck. In the event the payment is not reflected on your paystub, or the amount appears to be incorrect,

you should contact the First Data Contact Center at Merrill Lynch immediately at 1-844-332-2200 any business

day between 8:00 a.m. to 10:00 p.m. Eastern Time.

Primary Residence Loan

You can take a primary residence loan to purchase a primary residence for yourself. Your primary residence can

be a house, condominium, co-op, mobile home, or new home constructed by a builder or yourself, or the land for

new construction or a mobile home.

Your Purchase and Sales Agreement must be provided to the Plan Recordkeeper to obtain a primary residence

loan. You will be charged an additional $45 primary residence loan qualification fee.

First Data reserves the right to audit all primary residence loans, which may require providing supporting

documentation such as a signed sales contract, home purchase agreement, or builder’s construction contract.

You must repay the loan within 15 years (180 months).

18

If you request a primary residence loan, you’ll receive a promissory note and certain disclosures about the loan,

which show:

Loan amount

Loan duration

Interest rate

Repayment amount

You don’t need to return the note. Retain it for your records. Based on your request, the loan proceeds will be

mailed to you within seven days. Payroll will begin deducting loan repayments from your paycheck as soon as

administratively possible. You are responsible for ensuring that loan payments are being properly deducted from

your paycheck. In the event the payment is not reflected on your paystub, or the amount appears to be incorrect,

you should contact the First Data Contact Center at Merrill Lynch immediately at 1-844-332-2200 any business

day between 8:00 a.m. to 10:00 p.m. Eastern Time.

Please note that First Data reserves the right to audit your primary residence loan to ensure that the loan is used

for the specific purpose of purchasing a primary residence.

Interest on Your Loan

At the beginning of each quarter, the Incentive Savings Plan determines the interest rate that applies to loans

requested from the plan during that quarter. The rate is based on the prime interest rate on the first business day of

the month plus one, which is published in the Wall Street Journal.

This interest rate won’t change during the term of your loan, even though the interest rate for loans requested in

later months may be different.

Amount You Can Borrow

The minimum amount you can borrow is $1,000.

The maximum amount you can borrow is the lesser of:

50% of your vested account balance (including any outstanding loans) minus your current outstanding

loan balance

$50,000 minus your highest outstanding loan balance(s) across any other of the employer’s qualified

plans during the past 12 months

Note: Balances in your Qualified Voluntary Elective Contribution account (QVEC) and eOne Contributions

account are not included in the account balance when determining the amount available.

Loan Sources

The loan is secured by a portion of your vested account balance as required by the Plan Administrator.

When you borrow from your Incentive Savings Plan account, the money is taken from your sources in this order:

1. Prior Plan Employer Match Contributions

2. Employer ISP Plus Contributions (You can borrow vested employer contributions and earnings only.)

3. Employer Matching Contributions (You can borrow vested employer contributions and earnings only.)

4. Post-2007 Employer Matching Contributions

5. Employer Special Contributions

6. Employer Service Related Contributions

7. Qualified Nonelective Contributions

8. Before-Tax Matched Contributions

9. Before-Tax Unmatched Contributions

10. Roth Contributions

11. Rollover Contributions

12. After-Tax Rollover Contributions

19

13. Roth Rollover Contributions

14. Post-86 After-Tax Contributions

15. Pre-87 After-Tax Contributions

All of the available money in the first source must be depleted before money is taken from the next source. For

example, the amount available in your Prior Plan Employer Match Contributions must be fully depleted before

money is taken from your Employer ISP Plus Contributions to fund the loan amount requested.

How Loans Affect Your Investment Fund Balances

The amount taken from each investment fund reflects how your balance in each source is invested. For example,

if all of the money for your loan is taken from your vested Employer Matching Contributions and 10% of that

source is invested in the Vanguard Target Retirement Trust I Fund then 10% of your loan amount comes from

that fund.

The percentage taken from each fund is based on the source balance invested in that fund, not your investment

choices for future contributions.

Loan Repayments

Payroll Repayments

Loan repayments are deducted automatically from your paychecks after federal and state taxes are calculated.

You pay principal and interest with each loan repayment. You are responsible for ensuring that loan payments

are being properly deducted from your paycheck. In the event the payment is not reflected on your paystub, or

the amount appears to be incorrect, you should contact the First Data Contact Center at Merrill Lynch

immediately at 1-844-332-2200 any business day between 8:00 a.m. to 10:00 p.m. Eastern Time.

Your loan repayments are credited to your contribution sources from which the loan was taken from your

account.

The money you repay is invested according to your investment elections for new contributions as of the date of

repayment.

Making Repayments While on an Unpaid Leave

You must send loan repayments to the First Data Contact Center at Merrill Lynch if you’re not receiving a

paycheck (for example, during an unpaid leave of absence).

To make loan repayments while on an unpaid leave, you can either set up recurring ACH payments from your

bank account on the ISP website, send a certified check or bank check made payable to Merrill Lynch. If you pay

by check, please reference your name and SSN on the check and mail it to the following address:

Merrill Lynch Retirement & Benefit Plan Services

1400 Merrill Lynch Drive

Mail-Stop NJ2-140-03-50

Pennington, NJ 08534

When you don’t make a loan repayment as scheduled, you will be required to make up the missed loan payments

or have your loan re-amortized to keep your loan from going into default and becoming a taxable distribution.

You may contact the First Data Contact Center at Merrill Lynch for more information on making loan repayments

while you’re on an unpaid leave.

Making Repayments While on Military Leave

Loan repayments will be suspended for the time that you’re on military leave. When you return from your leave,

your loan term will be extended by the time you were on leave.

20

Interest on any loans will continue to accrue while you’re on a military leave. For a loan taken prior to your leave,

interest will continue to accrue at the lower of the following:

6% interest rate

Your original loan interest rate

If you took a loan after the start of your leave, interest will accrue at your original interest rate. As a result of the

accruing interest, your loan repayment will increase when you return.

Your loan repayment payroll deductions will start again as soon as administratively possible when you return.

Paying Off Your Loan Early

You can repay your loan in full at any time with no prepayment penalties. To do this, you can request an early

loan payoff on the ISP Website or by calling the First Data Contact Center at Merrill Lynch.

If You Leave First Data

If you leave First Data, your outstanding loan or loans are considered to be in default. To repay your outstanding

loan(s), you have until the earlier of:

90 days from the day you leave First Data

The date you request a total distribution from the plan

You can go to the ISP website or call the First Data Contact Center at Merrill Lynch to receive your loan payoff

amount. To pay off your loan(s), send a certified check or bank check made payable to Merrill Lynch or an ACH

payment to Merrill Lynch. Please reference your name and SSN on the check and mail it to the following

address:

Merrill Lynch Retirement & Benefit Plan Services

1400 Merrill Lynch Drive

Mail-Stop NJ2-140-03-50

Pennington, NJ 08534

Loan Defaults and Deemed Distributions

When a Loan Goes Into Default

Your loan is considered to be in default 90 days after:

You miss a scheduled loan repayment

You leave First Data

If you miss a loan repayment while you’re a First Data employee, you have until the end of the quarter following

the quarter in which you missed the payment to make up the missed repayment. At the end of the quarter, your

outstanding loan is considered a “deemed distribution” and subject to taxes like a withdrawal. However, unlike a

withdrawal, a deemed distribution is not an eligible rollover distribution. Besides the income taxes that may be

due, the deemed distribution may be subject to an additional 10% penalty tax on early distributions.

The amount of the deemed distribution is your outstanding principal balance plus any interest on the loan

repayments that would have been made through the date of taxation had the loan not been in default.

When a loan is considered a deemed distribution, it remains an outstanding obligation and continues to accrue

interest until you leave First Data or repay the loan in full, including interest, whichever is earlier. Because it

remains outstanding, the loan counts toward:

The maximum number of loans you can have outstanding

The maximum amount available for a new loan

21

If you want to repay the taxed loan, you can do so at any time by making one lump-sum repayment.

The amount you pay on a previously taxed loan won’t be taxed again when you take a payment from the plan.

Plan Withdrawals

The plan’s primary purpose is to provide benefits when you retire. However, under certain circumstances, you

may be able to withdraw money from your account while you’re still working by taking:

After-tax withdrawals

Age 59 ½ withdrawals

Rollover withdrawals

Disability withdrawals

Hardship withdrawals

The amount available to you and the way the withdrawal affects your account depends on the type of withdrawal

you request.

When you take a withdrawal, you take money out of your account permanently. You may need to pay taxes on

the amount you withdraw. You may also need to pay a penalty tax if the withdrawal is considered an early

distribution from the plan.

You may take up to two hardship withdrawals each year. If you take a hardship withdrawal, you’ll be suspended

from contributing to the plan for six months. Your contributions will not automatically resume. You will need to

elect a new contribution rate. To process your new contribution rate request, you may do so on the ISP Website or

you may contact the First Data Contact Center at Merrill Lynch.

Requesting a Withdrawal

To request a withdrawal, follow the rules and procedures described below for each type of withdrawal.

Special tax rules apply when you take a withdrawal. Depending on the type of withdrawal you take, you may be

able to defer taxes by rolling over the withdrawal to another eligible retirement plan or an IRA.

Balances in your self-directed brokerage account are not included in the amount available for withdrawal.

You can request most types of withdrawals on the ISP Website or by calling the First Data Contact Center at

Merrill Lynch. The amount available for withdrawal is based on your account value at the close of each business

day (4:00 p.m. Eastern Time or when the NYSE closes).

After-tax Withdrawal

You can take a withdrawal from your After-Tax Account (as distinguished from your Roth Account) for any

reason, but only from the sources listed below.

The amount that’s available for withdrawal depends on:

Whether you’ve taken an after-tax withdrawal in the last six months

You can roll over the withdrawal to another eligible retirement plan or IRA.

Age 59 ½ Withdrawal

Once you reach age 59 ½, you can take a withdrawal for any reason. The amount that’s available for withdrawal

depends on:

Whether you’re vested

You can roll over the withdrawal to another eligible retirement plan or IRA.

22

After-tax and Age 59 ½ Withdrawal Sources

When you withdraw money from your Incentive Savings Plan account, the funds are withdrawn from sources in

the following order:

1. Pre-87 After-Tax Contributions

2. Post-86 After-Tax Contributions

3. After-Tax Rollover Contributions

4. Rollover Contributions

5. Roth Rollover Contributions

6. Before-Tax Unmatched Contributions

7. Before-Tax Matched Contributions

8. Roth Contributions

9. eOne Contributions (if applicable)

10. Qualified Voluntary Elective Contributions

11. Employer Service Related Contributions

12. Employer Special Contributions

13. Employer Matching Contributions (You can borrow vested employer contributions and earnings only.)

14. Post-2007 Employer Matching Contributions

15. Employer ISP Plus Contributions (You can borrow vested employer contributions and earnings only.)

16. Qualified Nonelective Contributions

17. Prior Plan Employer Match Contributions

The amount taken from each investment fund reflects how your sources are invested. For example, if all of the

money for your withdrawal is taken from your Pre-87 After-Tax Contributions and 10% of that source is invested

in the Vanguard Target Retirement Income Trust I Fund then 10% of your withdrawal amount comes from that

fund.

Similarly, all of the available funds in the first source must be depleted before money is taken from the next

source. For example, the amount available in your Pre-87 After-Tax Contributions must be fully depleted before

money is taken from your Post-86 After-Tax Contributions.

Rollover Withdrawal

While you remain employed, you may withdraw any portion of your Rollover Contributions and Roth Rollover

Contributions sources after you have withdrawn the entire available balance from your After-tax Rollover source,

if any.

You can roll over the withdrawal to another eligible retirement plan or IRA.

Disability Withdrawal

If, while you are employed by First Data, you become Disabled (as defined in the plan and described on page 31),

you may withdraw any or all of your vested Incentive Savings Plan account balance. Funds shall be withdrawn

from contribution sources in the same order as described above for After-Tax and Age 59 ½ withdrawals.

Hardship Withdrawal

In certain situations, you can take a hardship withdrawal from your before-tax and Roth contributions. You are

limited to two hardship withdrawals each year.

To take a hardship withdrawal:

You or your primary beneficiary must have an immediate and heavy financial need.

23

The withdrawal must be necessary to satisfy that need.

You must provide documentation to prove your financial hardship.

In most cases, you must incur the expense before requesting the withdrawal (except for tuition). However, you

cannot pay the expense and then request a hardship withdrawal for reimbursement. The money you withdraw for

hardship must be used to pay for that expense.

Events that Qualify as a Hardship

You can apply for a hardship withdrawal only if your financial need is for one of these reasons:

Costs directly related to buying your primary residence (excluding mortgage payments)

Payments necessary to prevent your eviction from your primary residence or foreclosure on the mortgage

on that residence

Medical care expenses that you could deduct on your income tax return that either:

o You, your spouse, primary beneficiary, or any of your dependents (as defined by the IRS)

previously incurred

o Were necessary for you, your spouse, primary beneficiary, or any of your dependents to receive

medical care

Payment of tuition, related educational fees, or room and board expenses for:

o The next 12 months of postsecondary education

o You, your spouse, primary beneficiary, or your dependents (as defined by the IRS)

Funeral and/or burial expenses for your parent, your spouse, your children, or any of your dependents (as

defined by the IRS)

Repair of unforeseen damage to your principal residence not compensated for by insurance that would

qualify as a casualty deduction as defined by the IRS

Meeting the Financial Need Requirement

A hardship withdrawal request is deemed necessary if all of these requirements are met:

The withdrawal does not exceed the amount of the immediate and heavy financial need.

You’ve obtained all other withdrawals and nontaxable loans available to you from the plan and all other

plans maintained by First Data.

You stop contributing to the Incentive Savings Plan and to all other plans maintained by the employer for

at least six months after the hardship withdrawal.

Amount You May Withdraw

You can withdraw up to the amount of your immediate financial need or the maximum amount available,

whichever is less.

However, you can request that the amount of your hardship withdrawal be increased to cover any federal, state, or

local income taxes or penalties reasonably anticipated to result from the withdrawal.

Federal law prohibits the withdrawal of earnings related to any before-tax or Roth contributions credited to your

account after December 31, 1988.

You cannot roll over the withdrawal to another eligible employer plan or IRA.

Hardship Withdrawal Sources

When you withdraw money from your Incentive Savings Plan account, it’s taken from your sources in this order:

1. Before-Tax Unmatched Contributions

2. Before-Tax Matched Contributions

3. Roth Contributions

4. Employer Matching Contributions (You can only withdraw vested Employer Matching

Contributions made prior to 1/1/08 and the associated earnings.)

5. Employer ISP Plus Contributions (vested contributions and associated earnings.)

24

6. Employer Special Contributions

7. eOne Contributions (if applicable)

8. Employer Service Related Contributions

All of the money in the first source must be depleted before money is taken from the next source. For example,

the amount available in your Before-Tax Unmatched Contributions must be fully depleted before money is taken

from your Before-Tax Matched Contributions.

Required Documentation

To be approved for a hardship withdrawal, you must send supporting documents to the First Data Contact Center

at Merrill Lynch. First Data may require documentation to approve a hardship in addition to the items listed

below. First Data also reserves the right to deny hardship requests at its discretion. Submission of false

documentation may result in your termination of employment.

Purchase of Your Primary Residence

For costs directly related to buying your primary residence, submit one of the following:

Signed purchase contract

Intent-to-purchase agreement

Copy of the builder’s contract

The contract or agreement must be dated within the last 30 days and reflect:

o Purchase price

o Down payment amount

o Closing date

Past-Due Mortgage or Rent Payments

To prevent your eviction from your primary residence or foreclosure on your mortgage, submit either:

A letter from your landlord summarizing past-due rent payments and threatening eviction

A bank/mortgage statement indicating that payments are overdue and threatening foreclosure

Also, attach an eviction notice or a letter from the landlord or financial institution, threatening eviction or

foreclosure. Both items of documentation should be dated within the last four months and indicate that the

obligation is still pending with a future due date and a dollar amount.

Unreimbursed Medical Expenses

For expenses that haven’t been reimbursed by your medical insurance, submit an Explanation of Benefits (EOB)

from your medical insurer. The EOB should be dated within the last two years.

Postsecondary Education Expenses

For postsecondary education tuition, related educational fees, or room and board expenses, submit an itemized

tuition statement or room and board expense statement from the school. The statement must be dated within four

months of the beginning of the quarter or semester.

Funeral and/or Burial Expenses

For funeral/burial expenses for your parent, spouse, children, other dependents, or primary beneficiary, submit a

copy of the funeral/burial billing statement, including all of the following:

Name of deceased

Dates of services provided within the past 90 days

Itemized funeral/burial expenses

25

Primary Residence Repairs Due to Disaster

For repair expenses due to unforeseen damage to your primary residence not paid for by insurance, submit one of

the following:

Insurance report that includes:

o Address of the property damaged

o Date of damage within the past 90 days

o Cause of damage, if available

o Amount paid or to be paid by the insurance company

o Amount owed by you

A letter from you stating you have no insurance, which includes:

o Address of the property damage

o Cause of damage

o Date of damage within the past 90 days

o Statement from you that the property isn’t insured

In addition, you must submit all of the following:

An estimate or bill of itemized repairs that includes:

o Your name

o Address of the damaged property

o Date when the estimate or bill was calculated

o Document explaining the cause of the damage, if your insurance report doesn’t include it (police or

fire report, newspaper story, or a letter from you, for example)

Proof that you own or rent the residence (property tax bill, mortgage statement, property deed, or lease

agreement, for example), which reflects:

o Address of property damaged

o Your status as either owner or renter of the property

o Your liability—if you rent—to the owner for damages

Total Distributions You should receive payment within 10 business days of the date you request a total distribution.

You forfeit any employer contributions that are not vested when you leave First Data. To receive a final total

distribution from your account, follow the distribution procedures.

Distribution Options

If Your Vested Account Value Is $5,000 or Less

If upon separation from service, your vested account balance is $5,000 or less, excluding your rollover

contributions, and greater than $1,000, including your rollover contributions, and you don’t request a distribution

by the last business day of the quarter following the quarter in which you leave First Data, First Data Corporation

reserves the right to transfer your account to an IRA held in your name. This transfer will preserve the tax-

deferred status of your account balance.

If your vested balance, including your rollover contributions, is $1,000 or less, and you don’t request a

distribution by the last business day of the quarter following the quarter in which you leave First Data, the

distribution check will be made payable directly to you. However, 20% of the taxable portion of the distribution

is withheld for payment of federal taxes, unless you choose to directly roll over any or the entire taxable portions

to another eligible employer plan or IRA.

26

You can request a distribution at any point after your term, prior to the last business day of the quarter following

the quarter you leave First Data, and you can specify if you want to roll over the distribution directly to another

eligible employer plan or IRA.

If Your Vested Account Value Is More Than $5,000

If upon separation from service, your vested account balance, excluding your rollover contributions, is more than

$5,000, you can:

Receive a lump-sum payment in cash

Defer payment until age 70 ½

Depending on the payment option you choose, you may be able to roll over the payment to another eligible

employer plan or IRA.

If You Die Before Receiving Payment

If you die before receiving the full value of your account, your beneficiary receives your remaining vested

balance.

Your beneficiary must begin receiving payments according to the required minimum distribution rules.

If You Have an Outstanding Loan

If you have a loan outstanding when you leave First Data, the unpaid balance is considered in default and will be

deemed distributed and will be taxable to you. To avoid having the unpaid balance of the loan deemed

distributable, you have the option to pay the loan in full prior to the last business day of the quarter following the

quarter you leave First Data.

Rollover Distributions

You can roll over an eligible distribution from the Incentive Savings Plan to another eligible employer plan or

IRA. Your beneficiaries, including your spouse, may roll over your account balance to another qualifying

account. The primary advantage of rolling over an eligible distribution is that you continue to defer paying taxes

on the money.

An eligible rollover distribution is any distribution except:

Substantially equal periodic payments made at least annually over:

o Your life expectancy

o The joint life expectancy of you and your designated beneficiary

o A specified period of 10 or more years

Required minimum distribution amounts

Payments made to you as a nonspouse beneficiary or alternate payee under a QDRO

Any hardship withdrawal amounts

Loans treated as deemed distributions due to default