Embed Size (px)

Citation preview

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

Maximizing Tax Savings for Closely Held Companies with the IC-DISC Federal Export Tax Incentive Don Reiser (CBIZ) Amit Mathur and David Reid (Quantitax) Oct. 28 & Nov. 10, 2015

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest* and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent accounting firms

#cbizmhmwebinar 3

Before We Get Started…

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

#cbizmhmwebinar 6

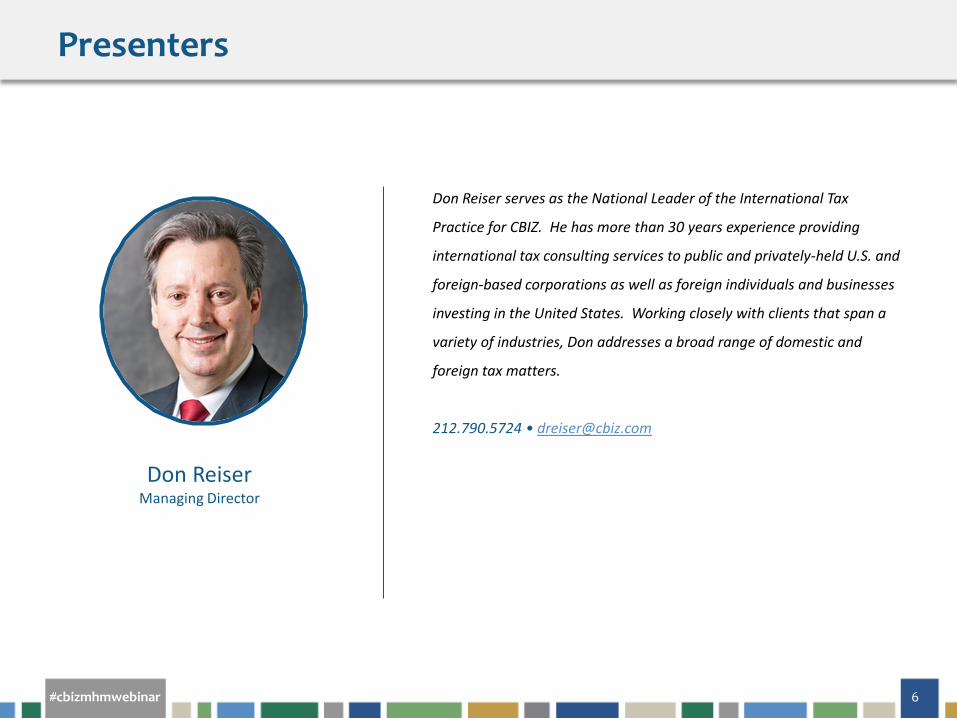

Presenters

Don Reiser serves as the National Leader of the International Tax

Practice for CBIZ. He has more than 30 years experience providing

international tax consulting services to public and privately-held U.S. and

foreign-based corporations as well as foreign individuals and businesses

investing in the United States. Working closely with clients that span a

variety of industries, Don addresses a broad range of domestic and

foreign tax matters.

212.790.5724 • [email protected]

Don Reiser Managing Director

#cbizmhmwebinar 7

Amit Mathur is a partner with Quantitax, an alliance partner firm that

assists business units with the IC-DISC Export Incentive. Amit is a

licensed C.P.A. with over 17 years of experience assisting companies with

optimizing export incentive calculations.

216.292.6732 • [email protected]

Amit Mathur Partner - Quantitax

#cbizmhmwebinar 8

David Reid is a partner with Quantitax, an alliance partner firm that

assists business units with the IC-DISC Export Incentive. David is a

licensed C.P.A. with over 18 years of experience providing international

tax services and export incentive calculations.

206.854.8351 • [email protected]

David Reid Partner - Quantitax

#cbizmhmwebinar 9

Agenda

Often Overlooked Industries/Scenarios & Misconceptions 02

01

03

04 Benefits of a Detailed IC-DISC Analysis

“Hot Topics”

Questions?

Overview & Qualification for the IC-DISC (US content, manufacture, etc.)

03

04 05

#cbizmhmwebinar 10

MAXIMIZING TAX SAVINGS FOR CLOSELY HELD COMPANIES WITH THE IC-DISC

FEDERAL TAX INCENTIVE

#cbizmhmwebinar 11

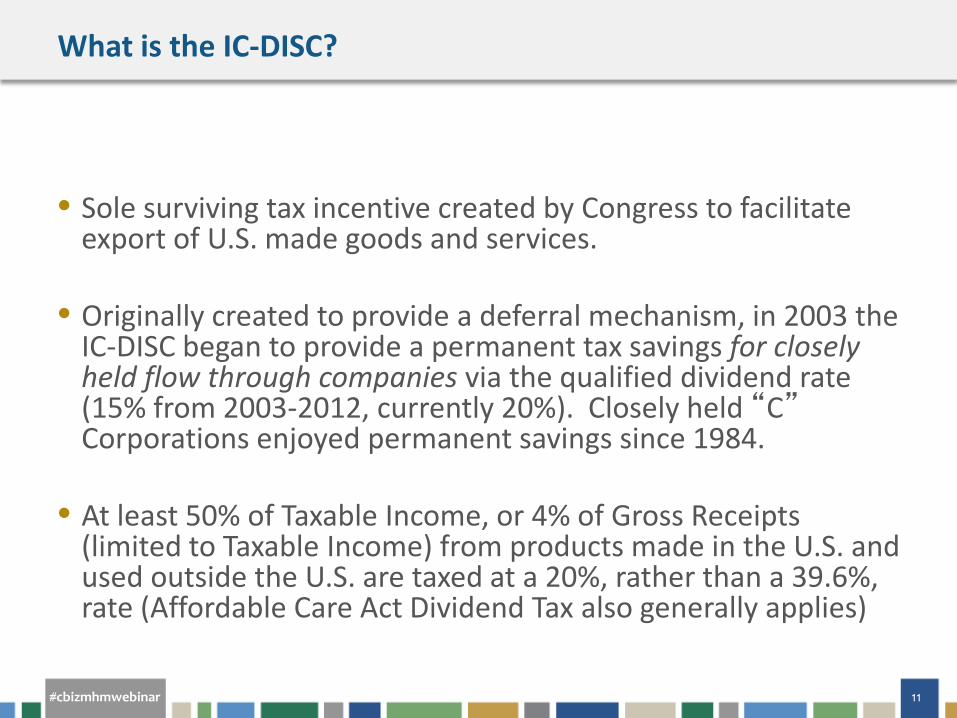

What is the IC-DISC?

• Sole surviving tax incentive created by Congress to facilitate

export of U.S. made goods and services. • Originally created to provide a deferral mechanism, in 2003 the

IC-DISC began to provide a permanent tax savings for closely held flow through companies via the qualified dividend rate (15% from 2003-2012, currently 20%). Closely held “C” Corporations enjoyed permanent savings since 1984.

• At least 50% of Taxable Income, or 4% of Gross Receipts

(limited to Taxable Income) from products made in the U.S. and used outside the U.S. are taxed at a 20%, rather than a 39.6%, rate (Affordable Care Act Dividend Tax also generally applies)

#cbizmhmwebinar 12

What is the IC-DISC? (continued)

• Requires setup of a corporation which elects treatment as

an IC-DISC and can be paid a deductible commission based on export sales or income. Dividends paid back to the parent are taxed at a 20% rate. The entity files an 1120-IC DISC federal return.

• No change in business operations is needed.

• Typical structures on following slides.

#cbizmhmwebinar 13

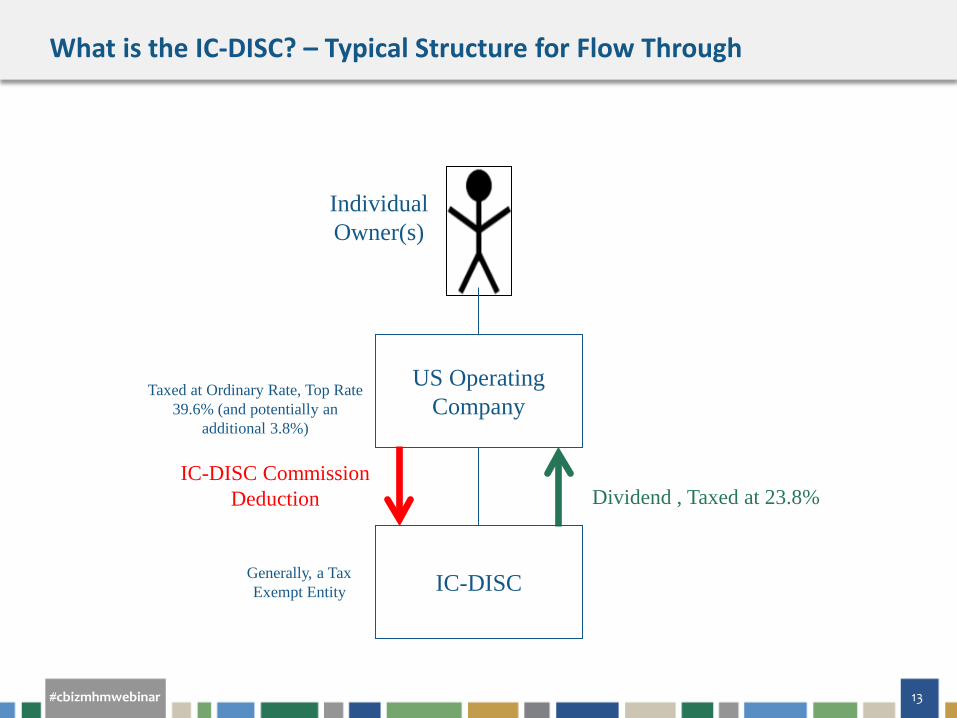

What is the IC-DISC? – Typical Structure for Flow Through

Taxed at Ordinary Rate, Top Rate 39.6% (and potentially an

additional 3.8%)

IC-DISC Commission Deduction

US Operating Company

Generally, a Tax Exempt Entity

Dividend , Taxed at 23.8%

Individual Owner(s)

IC-DISC

#cbizmhmwebinar 14

What is the IC-DISC? – Typical Structure for Closely Held C-Corp

Taxed at Ordinary Rates

IC-DISC Commission

US Operating Company

Generally, a Tax Exempt Entity

Dividend, Taxed at 23.8%

Individual Owner(s)

IC-DISC

#cbizmhmwebinar 15

What Products or Services Qualify for the IC-DISC?

• “Exported” Goods (direct or indirectly exported, includes Canada/Mexico!). • U.S. Content (no more than 50% of sales price can be foreign content) • U.S. Manufactured Goods (20% of COGS U.S. labor/burden safe harbor). • Products must not be further manufactured within the U.S. by another

party (further manufacture outside the U.S generally qualifies) after the sale.

• Certain services (Related and Subsidiary and Architectural and Engineering)

and leases.

#cbizmhmwebinar 16

Frequently Missed Opportunities

• “Ultimate Use” Sales • Sales to Related Party (and by Related Party in Some

Cases) • Detailed Calculations

• Distributor Sales

• Services

#cbizmhmwebinar 17

Misconceptions

• $10 Million Maximum Export Sales • Taxpayer Must Manufacture Products • Aggressive/Tax Shelter

• Business Operations Disrupted/Administrative Burden

• 4% of Export Sales or 50% of Export Profit is Maximum Commission

• IC-DISC Benefits for Foreign Owners Endorsed by Tax Code

#cbizmhmwebinar 18

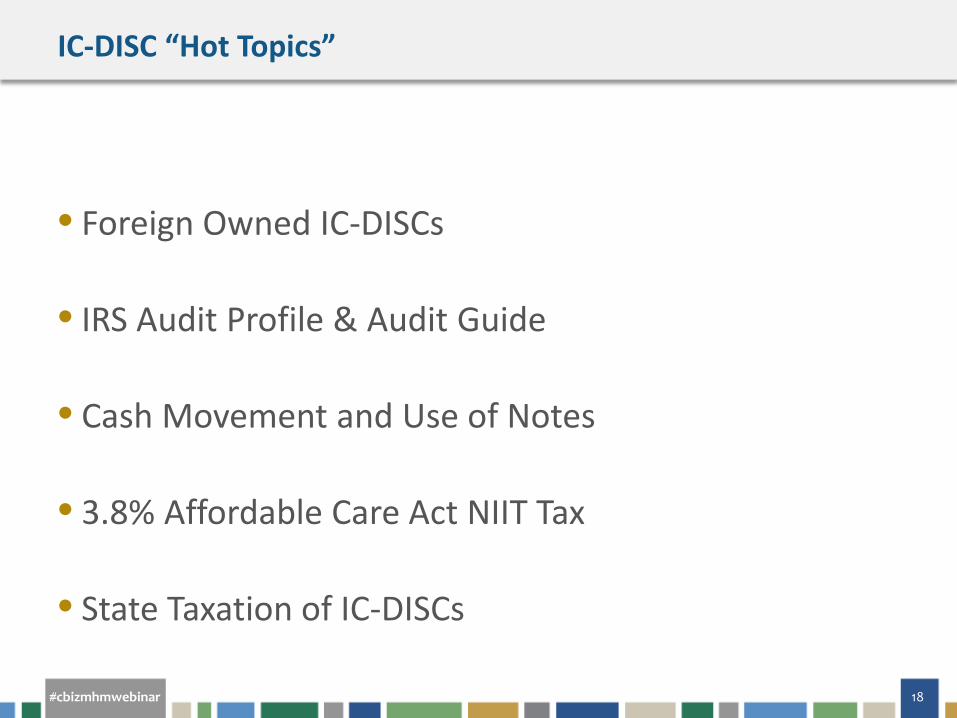

IC-DISC “Hot Topics”

• Foreign Owned IC-DISCs • IRS Audit Profile & Audit Guide

• Cash Movement and Use of Notes • 3.8% Affordable Care Act NIIT Tax

• State Taxation of IC-DISCs

#cbizmhmwebinar 19

Benefits of a Detailed IC-DISC Analysis

• Identification of Additional Eligible Sales

• Allocation and Apportionment of Expenses

• Transactional Calculation with Marginal Costing

• Re-Determination of Prior Year Calculations

#cbizmhmwebinar 20

Benefits of a Detailed IC-DISC Analysis

Identification of Eligible Sales – Overlooked Industries • Software Companies • Distributors/Brokers • Food Growers • Food Processors • Equipment Leasing • Recyclers • Architectural/Engineering

#cbizmhmwebinar 21

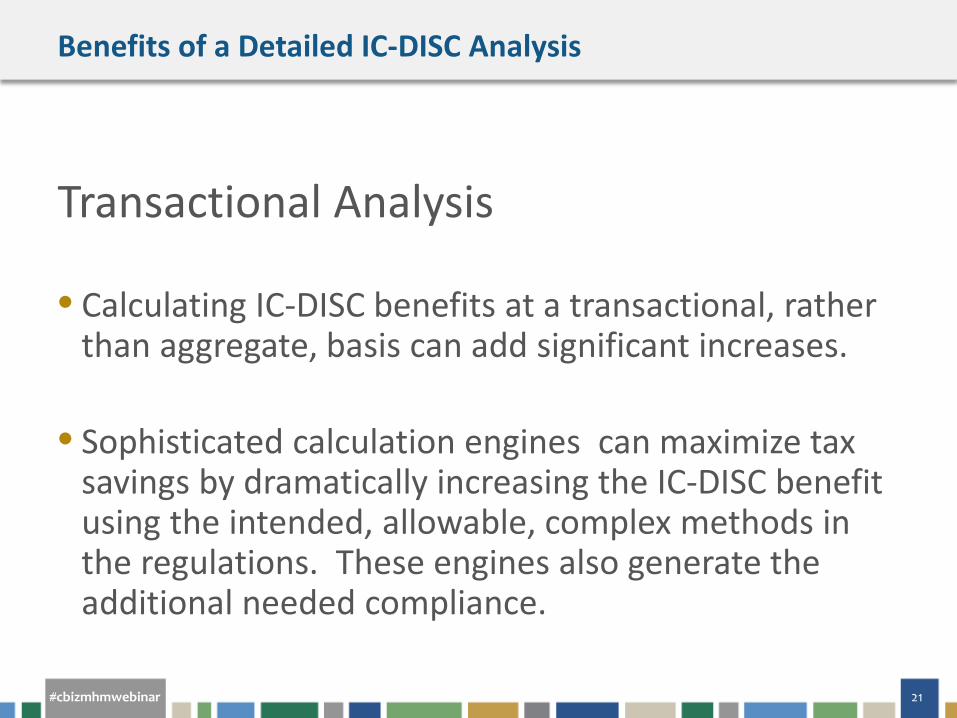

Benefits of a Detailed IC-DISC Analysis

Transactional Analysis • Calculating IC-DISC benefits at a transactional, rather

than aggregate, basis can add significant increases.

• Sophisticated calculation engines can maximize tax savings by dramatically increasing the IC-DISC benefit using the intended, allowable, complex methods in the regulations. These engines also generate the additional needed compliance.

#cbizmhmwebinar 22

Benefits of a Detailed IC-DISC Analysis

Transactional Analysis

• Needed data usually exists, and for many companies is easily obtainable, from Sales and Cost systems. Re-Determinations are allowed for prior years from the date of the DISC’s inception.

• Until 2006, large public companies routinely enjoyed significant increases in their export incentive calculations from detailed analyses using calculation engines. Now, such increased benefits are available to closely held companies through the IC-DISC.

#cbizmhmwebinar 23

Benefits of a Detailed IC-DISC Analysis

Transactional Analysis – Marginal Costing • In conjunction with transactional analysis, marginal

costing is an element of the IC-DISC regulations which allows less profitable transactions to derive IC-DISC benefit largely as if they were as profitable as an average transaction.

• Marginal costing can be applied at transactional, product, product line, etc. levels. Highly sophisticated software is needed to optimize marginal costing benefits in conjunction with loss optimization.

#cbizmhmwebinar 24

Benefits of a Detailed IC-DISC Analysis

Transactional Analysis – Marginal Costing Example

#cbizmhmwebinar 25

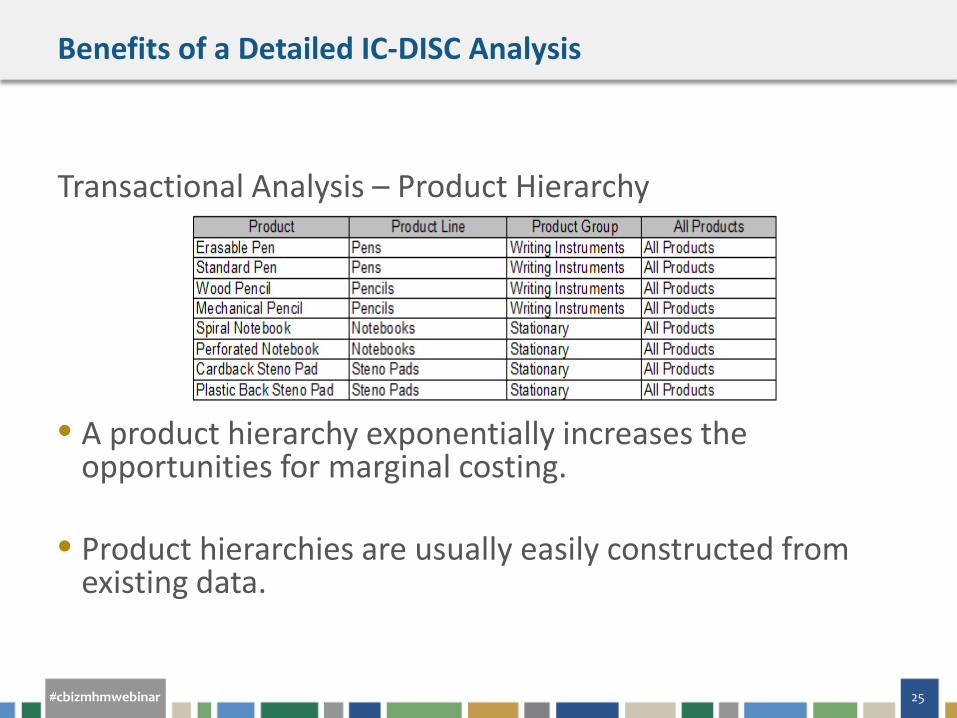

Benefits of a Detailed IC-DISC Analysis

Transactional Analysis – Product Hierarchy • A product hierarchy exponentially increases the

opportunities for marginal costing.

• Product hierarchies are usually easily constructed from existing data.

#cbizmhmwebinar 26

? QUESTIONS

#cbizmhmwebinar 27

If You Enjoyed This Webinar…

Upcoming Courses: • 10/29, 11/3 & 11/4: Eye on Washington: Quarterly Business Tax Update, Q3 2015

• 11/5 & 12/2: Individual Year-End Tax Planning Tips for 2015 and Beyond

• 11/10: Maximizing Tax Savings for Closely Held Companies with the IC-DISC Federal Export Tax Incentive

• 11/11: Revenue Recognition Updates for Manufacturers

• 12/1 & 12/15: Recent Tax Developments Impacting the Construction Industry

Recent Thought Leadership: • The Top Five Risks Facing Manufacturers

• Local Deductibility of Management Services Charges

• A Chance of Clouds: Sales Tax Considerations of Cloud Computing

#cbizmhmwebinar 28

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ