Embed Size (px)

Citation preview

Financial Support for Offshore Projects in BrazilBNDES: Current Status and Future Plans

November/2014

BNDESBrazilian Development Bank

BNDES Highlights

Fully state-owned company under private law.

Key instrument for implementation of Federal Government’s industrial and infrastructure policies - broad presence on brazilian economy.

Provides long-term financing (the main provider) directly or by accredited financial agents.

Provides equity investment directly or by funds.

Emphasis on financing investment projects, but also supports exports, environmental and social projects.

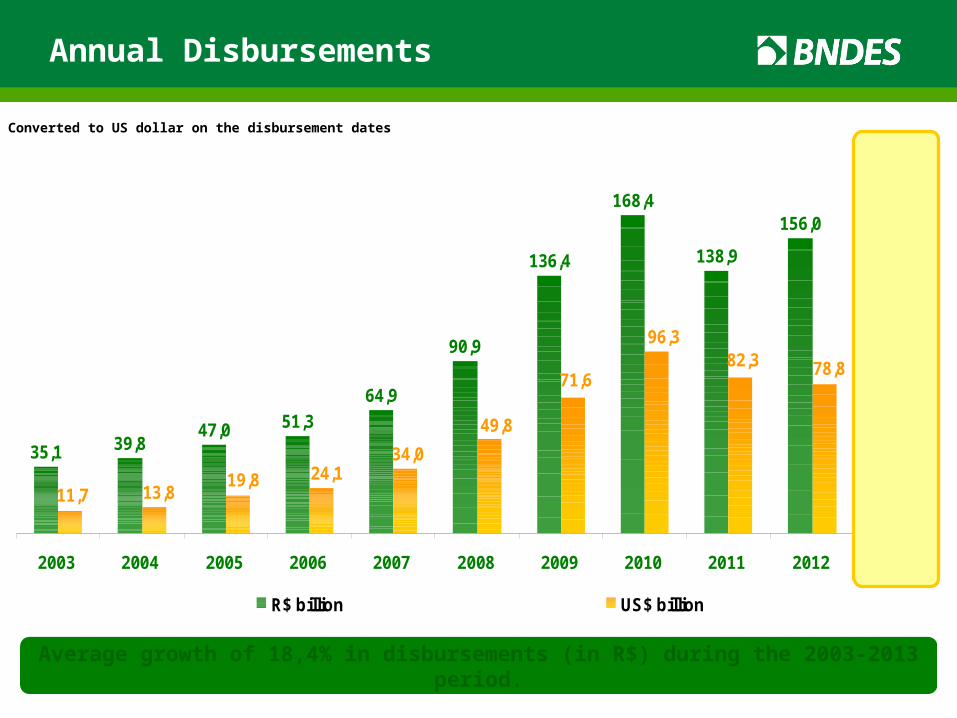

Annual Disbursements

Converted to US dollar on the disbursement dates

35,1 39,847,0 51,3

64,9

90,9

136,4

168,4

138,9

156,0

190,4

88,178,882,3

96,3

71,6

49,8

34,024,119,8

13,811,7

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

R$ billion US$ billion

Average growth of 18,4% in disbursements (in R$) during the 2003-2013 period.

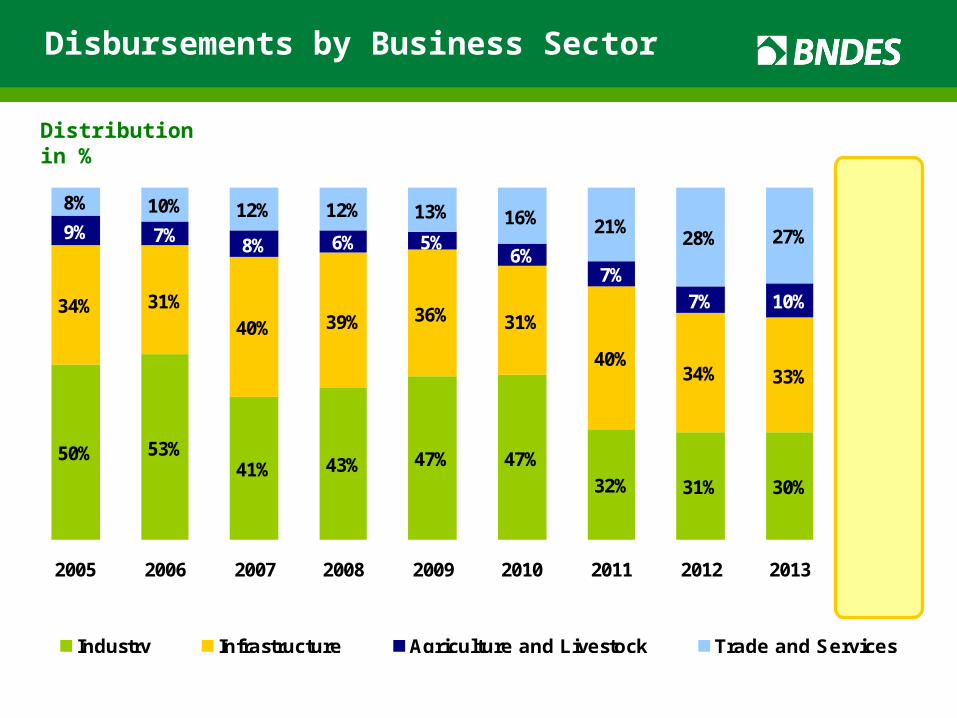

Disbursements by Business Sector

50% 53%41% 43% 47% 47%

32% 31% 30% 26%

34% 31%40% 39% 36% 31%

40%34% 33% 37%

9% 7% 8% 6% 5%6%

7%7% 10% 9%

8% 10% 12% 12% 13% 16% 21%28% 27% 28%

2005 2006 2007 2008 2009 2010 2011 2012 2013 jan-apr2014

Industry Infrastructure Agriculture and Livestock Trade and Services

Distribution in %

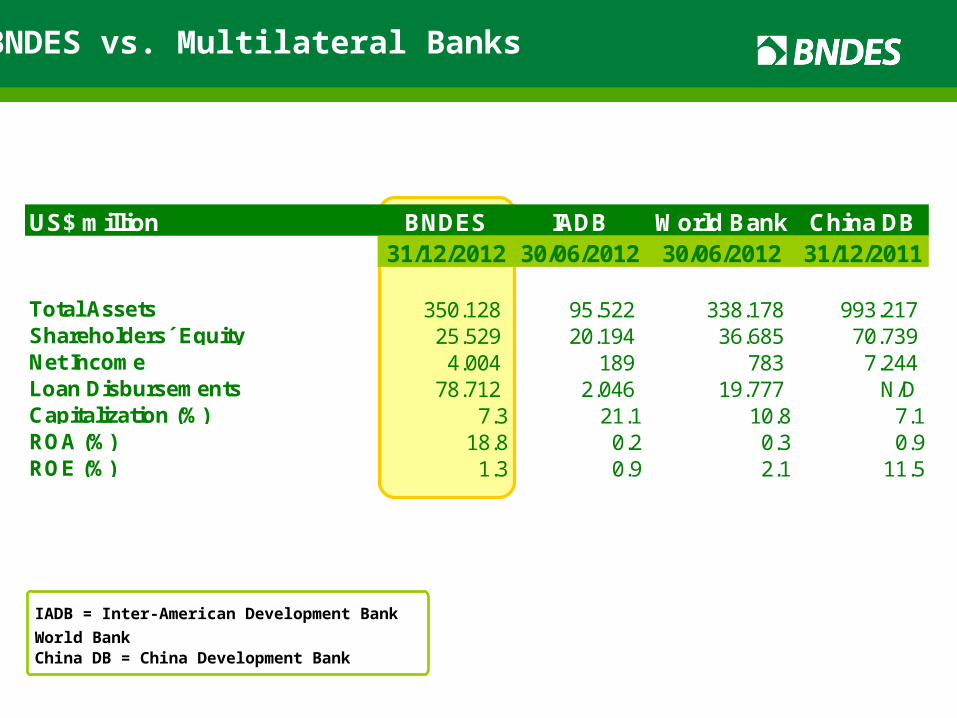

BNDES vs. Multilateral Banks

US$ million BNDES IADB World Bank China DB31/12/2012 30/06/2012 30/06/2012 31/12/2011

Total Assets 350.128 95.522 338.178 993.217 Shareholders´ Equity 25.529 20.194 36.685 70.739 Net Income 4.004 189 783 7.244 Loan Disbursements 78.712 2.046 19.777 N/DCapitalization (%) 7.3 21.1 10.8 7.1ROA (%) 18.8 0.2 0.3 0.9ROE (%) 1.3 0.9 2.1 11.5

IADB = Inter-American Development Bank World Bank China DB = China Development Bank

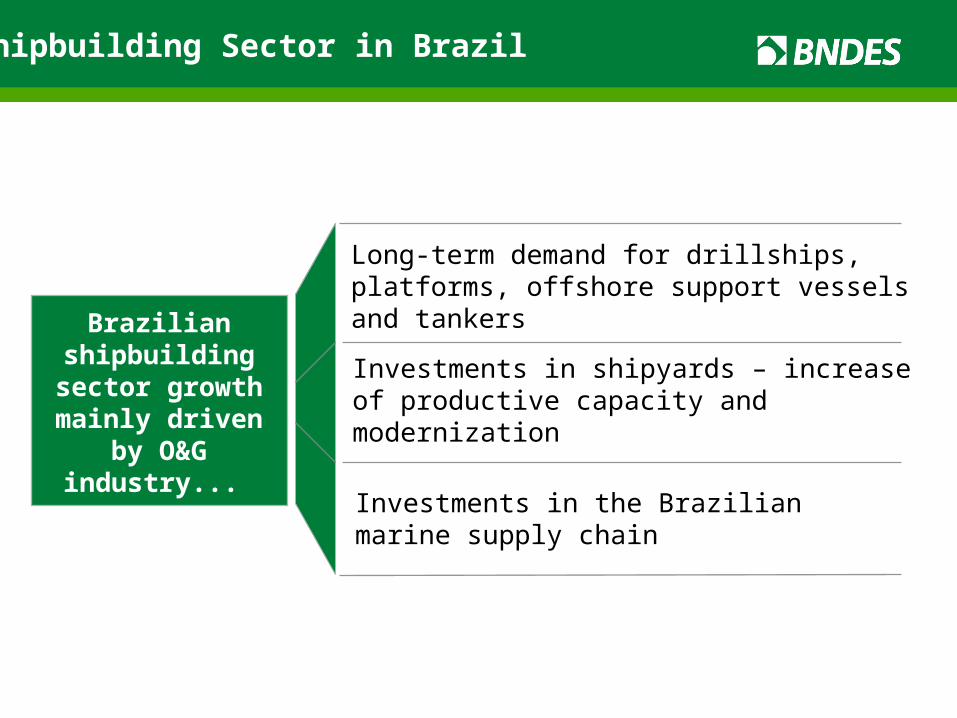

BNDES and the Shipbuilding Sector

Brazilian shipbuilding

sector growth mainly driven

by O&G industry...

Long-term demand for drillships, platforms, offshore support vessels and tankers

Investments in the Brazilian marine supply chain

Investments in shipyards – increase of productive capacity and modernization

Shipbuilding Sector in Brazil

• The 2000s: ressurge of shipbuilding sector based on offshore support vessels and tankers.

• Outlook: Sustainable demand of OSVs in the long term.

• BNDES acts with FMM funding.

Shipbuilding Sector in Brazil

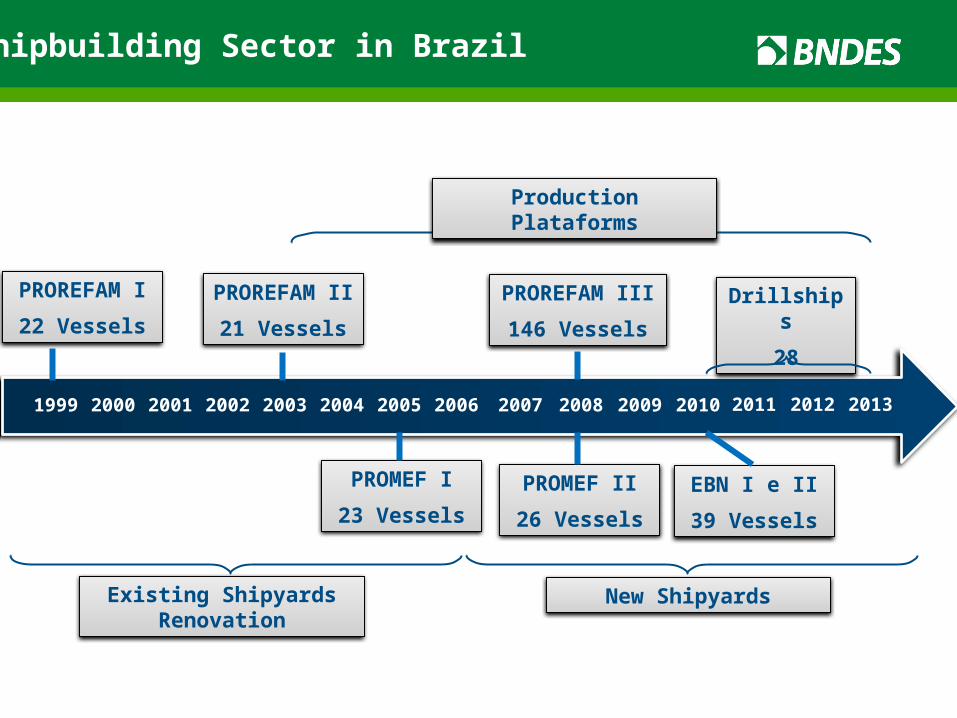

201320122011201020092008200720062005200420032002200120001999

PROREFAM I

22 Vessels

PROREFAM II

21 Vessels

PROREFAM III

146 Vessels

PROMEF I

23 Vessels

PROMEF II

26 Vessels

EBN I e II

39 Vessels

Drillships

28

Production Plataforms

Existing Shipyards Renovation New Shipyards

Shipbuilding Sector in Brazil

NewnsalNew Shipyard InvestmentsInternational Partnerships

Shipbuilding Sector in Brazil

MAUÁ (4 tankers)BRASFELS (6 DS, 2 PU)INHAÚMA (4 PU)

ESTALEIRO ATLÂNTICO SUL (7 DS, 19 tankers)VARD PROMAR (8 tankers)

ENSEADA PARAGUAÇU (6 DS)

JURONG ARACRUZ (7 DS)

ESTALEIRO RIO GRANDE (3 DS, 8 PU)HONÓRIO BICALHO (QUIP) (2 PU)ESTALEIRO DO BRASIL (EBR) (1 PU)

Up to:

• 32 PUs

• 28 DSs

2003-2013:

• 16 PUs

• 06 Vessels

Shipbuilding Sector in Brazil

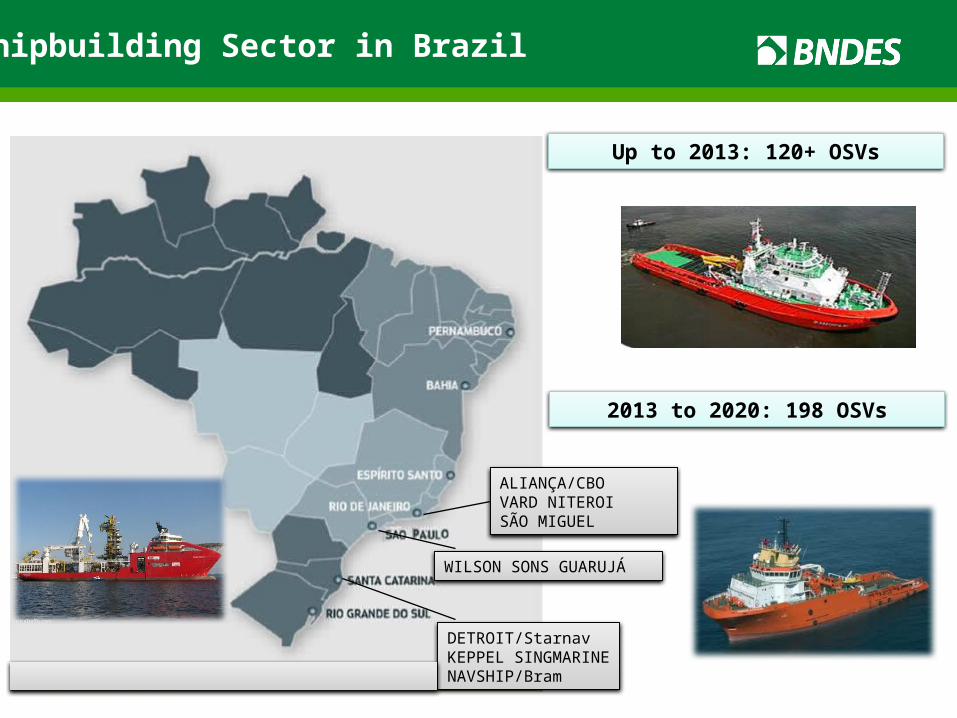

Shipbuilding Sector in Brazil

Up to 2013: 120+ OSVs

2013 to 2020: 198 OSVs

DETROIT/StarnavKEPPEL SINGMARINENAVSHIP/Bram

ALIANÇA/CBOVARD NITEROISÃO MIGUEL

WILSON SONS GUARUJÁ

Shipbuilding Sector in Brazil

0

10000

20000

30000

40000

50000

60000

70000

80000

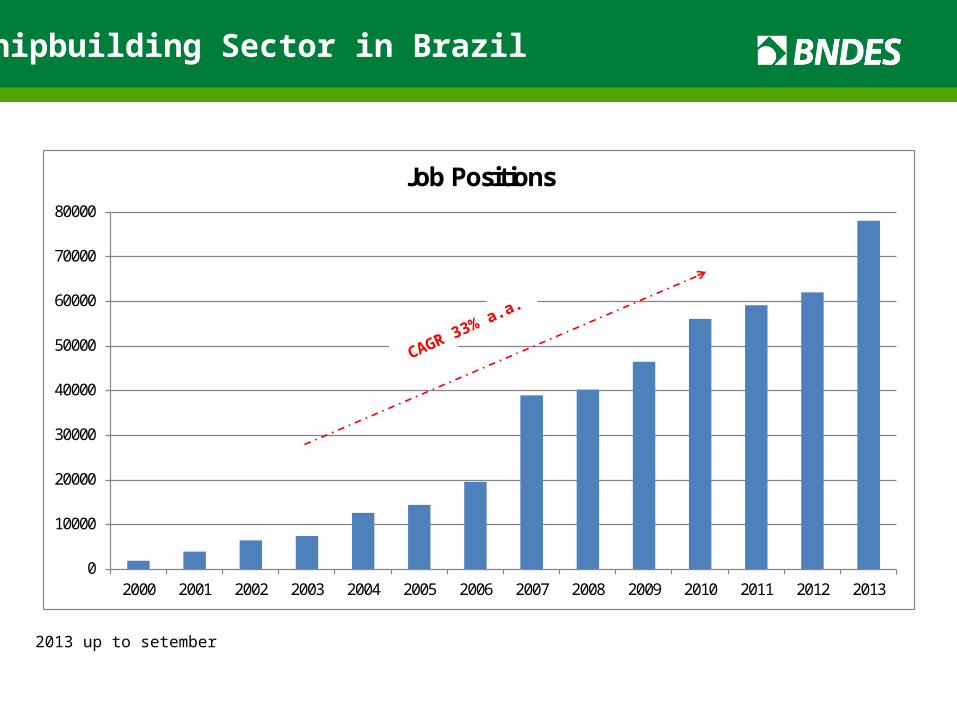

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Job Positions

CAGR 33% a.a.

2013 up to setember

Fonte: IPEA. Valores reais de 2010, corrigidos pelo IGPM.

Shipbuilding Sector in Brazil

Merchant Marine Fund – FMM

Treasury fund, managed by the Ministry of Transportation, and operated by Federal State-owned banks.

Projects must be eligible by the FMM Committee (CDFMM) before being analyzed by the accredited bank.

Supports vessels construction, jumborization and modernization, made in Brazilian shipyards (Buyer’s and Supplier’s Credit).

Supports Brazilian shipyards construction, expansion and modernization.

Holds for all eligible items, with better conditions for local content.

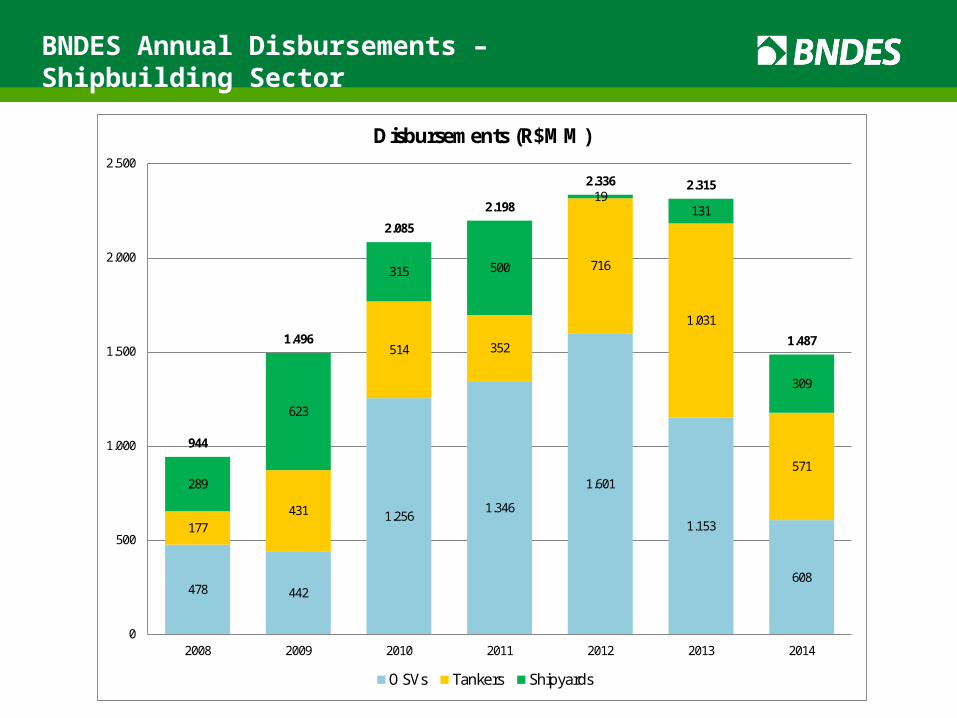

BNDES Annual Disbursements – Shipbuilding Sector

478 442

1.2561.346

1.601

1.153

608

177431

514 352

716

1.031

571289

623

315 500

19131

309

944

1.496

2.085

2.198

2.336 2.315

1.487

0

500

1.000

1.500

2.000

2.500

2008 2009 2010 2011 2012 2013 2014

Disbursements (R$MM)

OSVs Tankers Shipyards

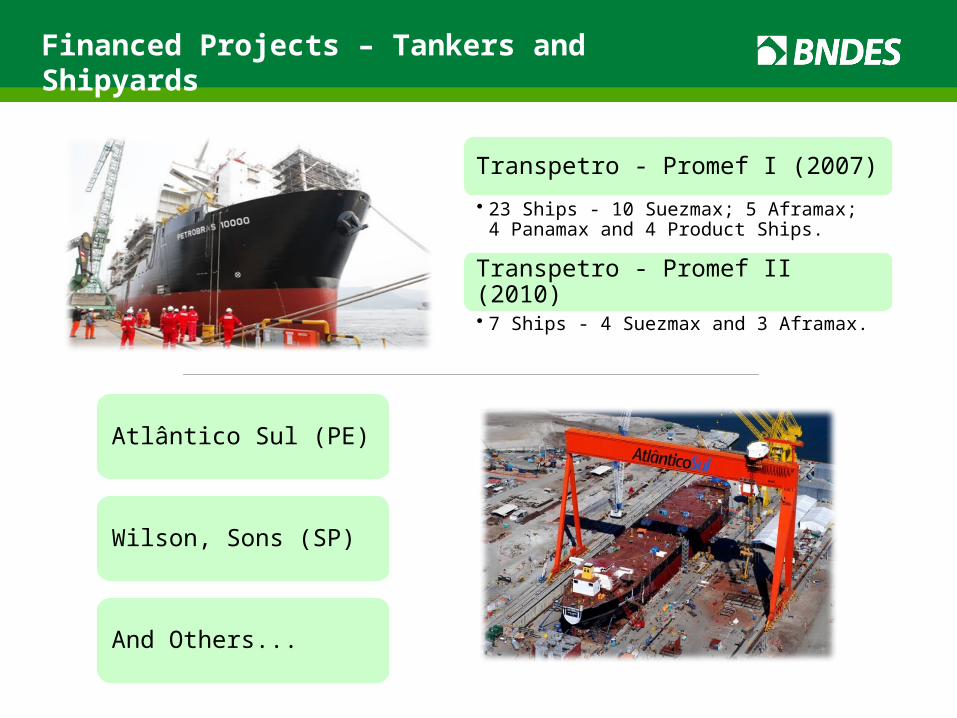

Transpetro - Promef I (2007)

• 23 Ships - 10 Suezmax; 5 Aframax; 4 Panamax and 4 Product Ships.

Transpetro - Promef II (2010)

• 7 Ships - 4 Suezmax and 3 Aframax.

Atlântico Sul (PE)

Wilson, Sons (SP)

And Others...

Financed Projects – Tankers and Shipyards

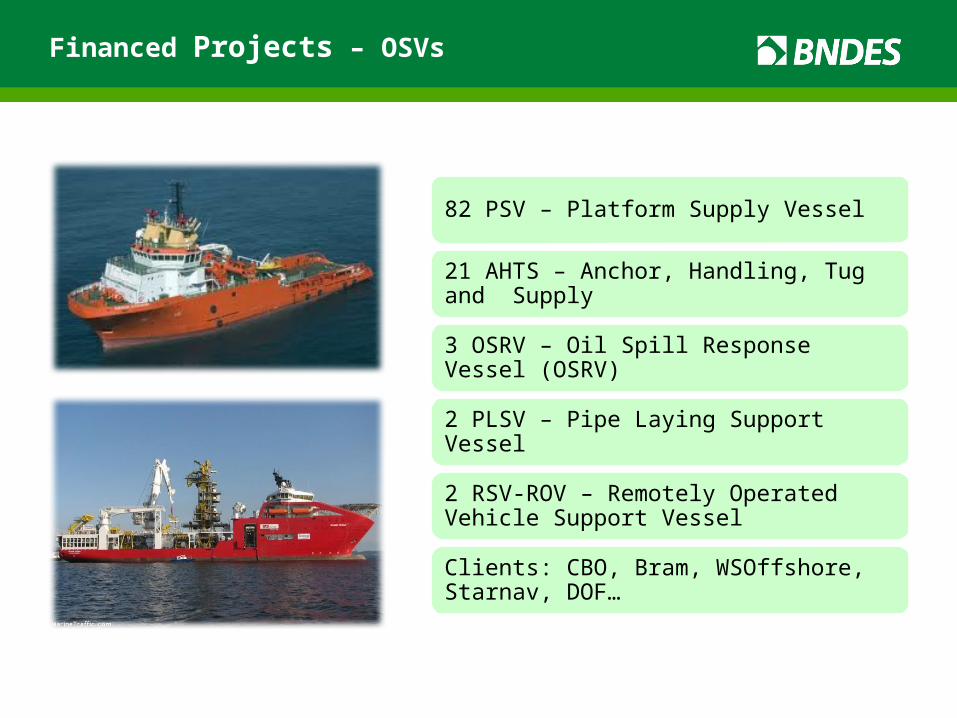

82 PSV – Platform Supply Vessel

21 AHTS – Anchor, Handling, Tug and Supply

3 OSRV – Oil Spill Response Vessel (OSRV)

2 PLSV – Pipe Laying Support Vessel

2 RSV-ROV – Remotely Operated Vehicle Support Vessel

Clients: CBO, Bram, WSOffshore, Starnav, DOF…

Financed Projects – OSVs

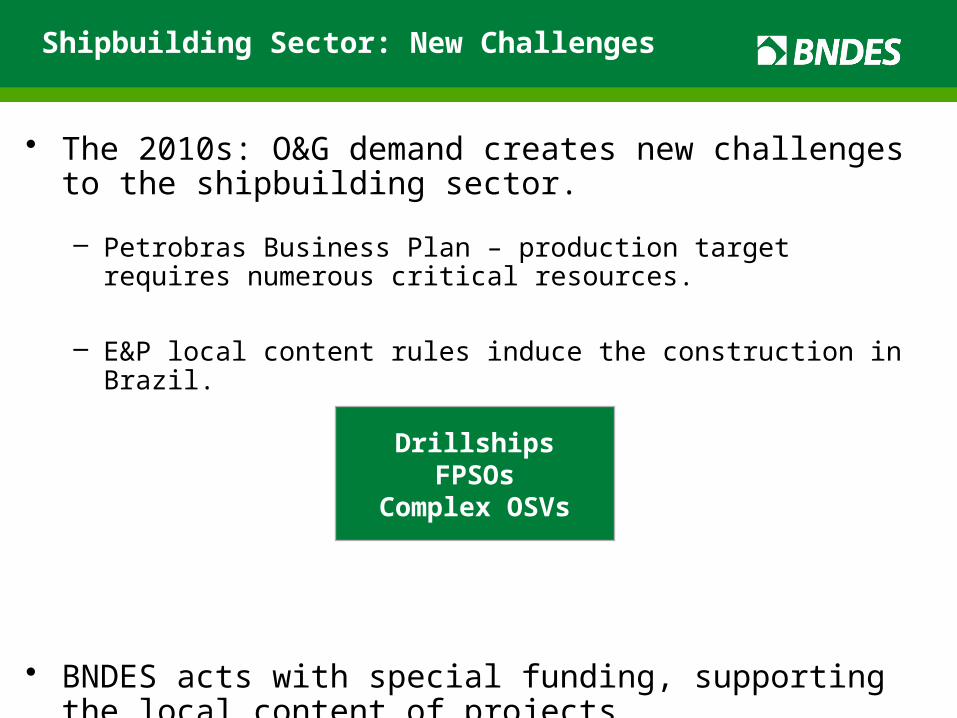

• The 2010s: O&G demand creates new challenges to the shipbuilding sector.

– Petrobras Business Plan – production target requires numerous critical resources.

– E&P local content rules induce the construction in Brazil.

• BNDES acts with special funding, supporting the local content of projects.

DrillshipsFPSOs

Complex OSVs

Shipbuilding Sector: New Challenges

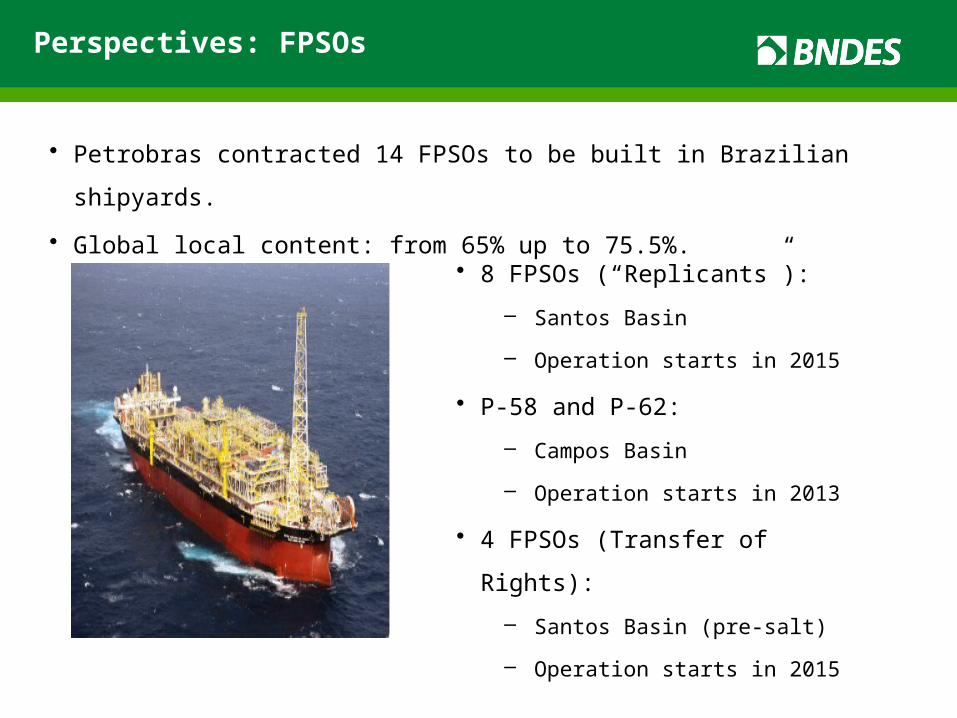

• 8 FPSOs (“Replicants”):

– Santos Basin

– Operation starts in 2015

• P-58 and P-62:

– Campos Basin

– Operation starts in 2013

• 4 FPSOs (Transfer of Rights):

– Santos Basin (pre-salt)

– Operation starts in 2015

Perspectives: FPSOs

• Petrobras contracted 14 FPSOs to be built in Brazilian shipyards.

• Global local content: from 65% up to 75.5%.

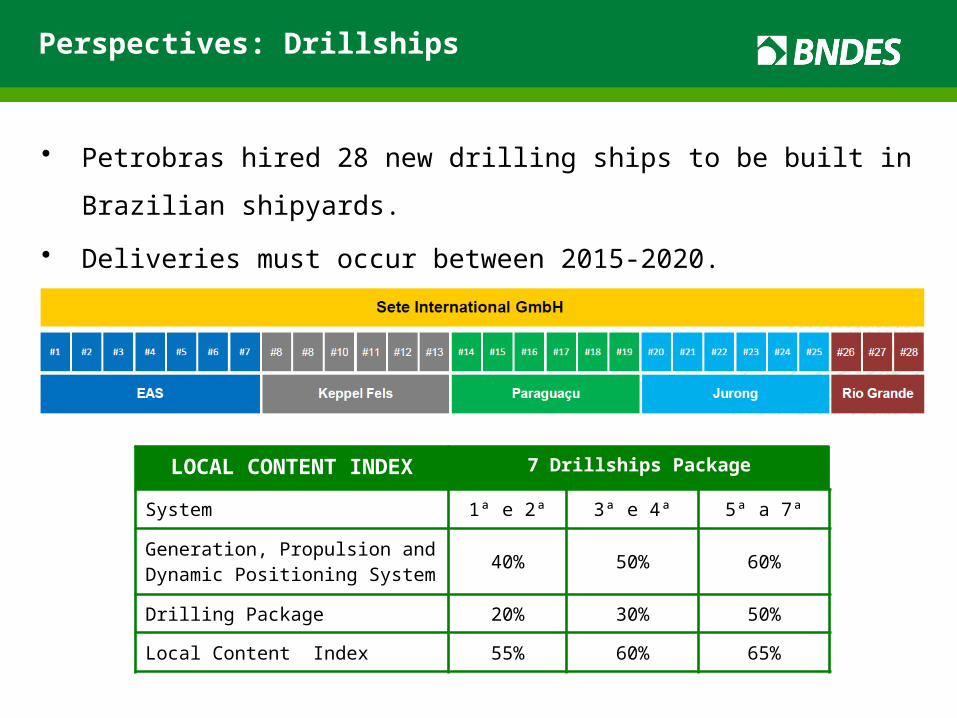

• Petrobras hired 28 new drilling ships to be built in Brazilian

shipyards.

• Deliveries must occur between 2015-2020.

LOCAL CONTENT INDEX 7 Drillships Package

System 1ª e 2ª 3ª e 4ª 5ª a 7ª

Generation, Propulsion and Dynamic Positioning System

40% 50% 60%

Drilling Package 20% 30% 50%

Local Content Index 55% 60% 65%

Perspectives: Drillships

25

Texto

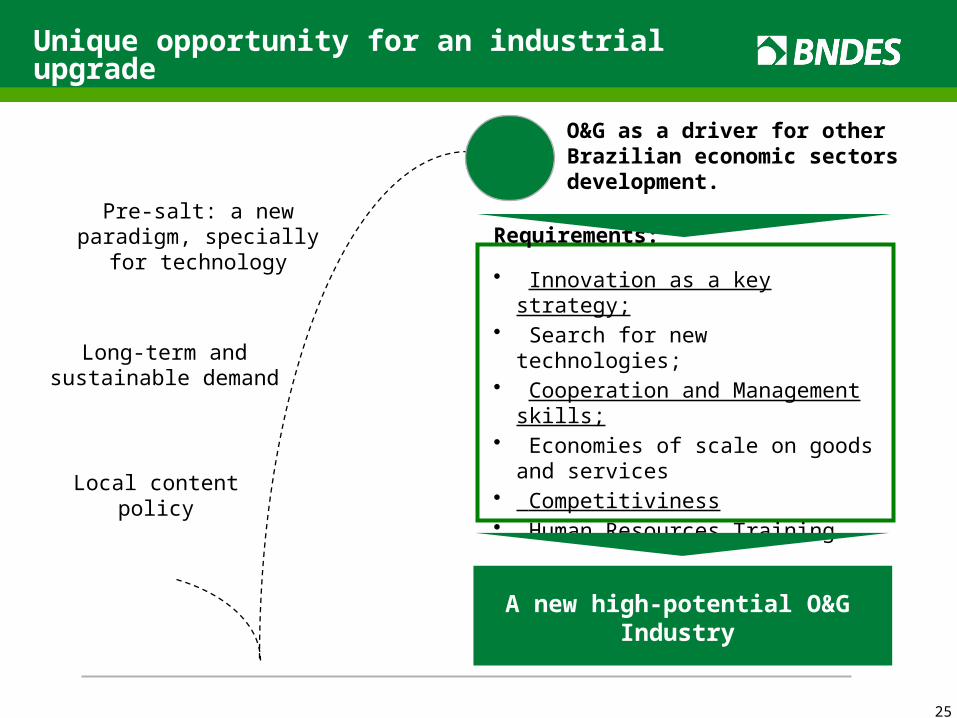

Local content policy

Unique opportunity for an industrial upgrade

Long-term and sustainable demand

Pre-salt: a new paradigm, specially for technology Requirements:

• Innovation as a key strategy;• Search for new technologies; • Cooperation and Management

skills;• Economies of scale on goods and

services• Competitiviness• Human Resources Training

A new high-potential O&G Industry

O&G as a driver for other Brazilian economic sectors development.

THANK YOU

Luiz Marcelo Martins Almeida

www.bndes.gov.br/english