Embed Size (px)

Citation preview

Closed Joint Stock Company “SUKHOI CIVIL AIRCRAFT” Financial Statements for the year ended 31 December 2012

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT”

2

Contents

AUDITORS’ REPORT ............................................................................................................. 3

STATEMENT OF FINANCIAL POSITION ......................................................................... 5

STATEMENT OF COMPREHENSIVE INCOME ............................................................... 6

STATEMENT OF CASH FLOWS ........................................................................................... 7

STATEMENT OF CHANGES IN EQUITY .......................................................................... 8

NOTES TO THE FINANCIAL STATEMENTS ................................................................... 9

Audited entity: Closed Join-Stock Company “Sukhoi Civil Aircraft”

Registered by the Moscow Registration Chamber on 25 May 2000, Registration No. 002.003.097

Registered in the Unified State Register of Legal Entities on 5 September 2002 by the Moscow Inter-Regional Tax Inspectorate No.39 of the Ministry for Taxes and Duties of the Russian Federation, Registration No. 1027739155180, Certificate series 77 No. 007809294.

2 build. 23 B, Polykarpov Street, Moscow, 125284.

Independent auditor: ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

Registered by the Moscow Registration Chamber on 25 May 1992, Registration No. 011.585.

Entered in the Unified State Register of Legal Entities on 13 August 2002 by the Moscow Inter-Regional Tax Inspectorate No.39 of the Ministry for Taxes and Duties of the Russian Federation, Registration No. 1027700125628, Certificate series 77 No. 005721432.

Member of the Non-commercial Partnership “Chamber of Auditors of Russia”. The Principal Registration Number of the Entry in the State Register of Auditors and Audit Organisations: No.10301000804.

ZAO KPMG 10 Presnenskaya Naberezhnaya Moscow, Russia 123317

Telephone +7 (495) 937 4477 Fax +7 (495) 937 4400/99 Internet www.kpmg.ru

Auditors’ Report

To the Shareholders and Board of Directors

Closed Joint-Stock Company “Sukhoi Civil Aircraft”

We have audited the accompanying financial statements of Closed Joint-Stock Company “Sukhoi Civil Aircraft” (the “Company”), which comprise the statement of financial position as at 31 December 2012 and the statements of comprehensive income, changes in equity and cash flows for 2012, and notes, comprising a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on the fair presentation of these financial statements based on our audit. We conducted our audit in accordance with Russian Federal Auditing Standards and International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to express an opinion on the fair presentation of these financial statements.

Auditors’ Report

Page 2

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as at 31 December 2012, and its financial performance and its cash flows for 2012 in accordance with International Financial Reporting Standards.

Ilya O. Belyatski, Director, power of attorney dated 3 October 2011 No. 35/11

ZAO KPMG

24 April 2013

Moscow, Russian Federation

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT”

The accompanying notes are an integral part of these financial statements

5

STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 2012

Notes 2012

000'USD 2011

000'USD

ASSETS

Non-current assets Intangible assets 6 868,181 728,393

Property, plant and equipment 7 357,294 299,395

Value added tax receivable 17,327 21,714

Other receivables 9 50,611 48,738

Net investment in financial leases 8 25,815 26,179

Deferred tax assets 10 116,548 89,533

Total non-current assets 1,435,776 1,213,952

Current assets Inventories 11 428,936 223,012

Trade and other receivables 12 218,307 52,595

Net investment in financial leases 8 1,017 500

Value added tax receivable 119,692 101,727

Cash and cash equivalents 13 182,458 17,691

Total current assets 950,410 395,525

TOTAL ASSETS 2,386,186 1,609,477

EQUITY AND LIABILITIES

Equity Share capital 14 100,856 100,856

Share premium 171,751 171,751

Additional paid-in-capital 55,362 55,362

Foreign currency translation reserve 31,380 43,180

Accumulated losses (635,007) (523,760)

Total equity (275,658) (152,611)

Non-current liabilities Loans and borrowings 15 1,126,694 872,965

Onerous contract provision 16 16,503 15,428

Advances from customers 77,647 77,088

Trade and other payables 9,610 12,610

Total non-current liabilities 1,230,454 978,091

Current liabilities Loans and borrowings 15 991,269 593,923

Trade and other payables 17 219,697 137,405

Advances from customers 217,920 50,754

Taxes payable 2,504 1,915

Total current liabilities 1,431,390 783,997

Total liabilities 2,661,844 1,762,088

Total equity and liabilities 2,386,186 1,609,477

The financial statements were authorised for issuance on 24 April 2013 by management and signed on its behalf. ____________ ____________ Kalinovsky A.V. Stolina M.A. President Chief accountant

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT”

The accompanying notes are an integral part of these financial statements

6

STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 2012

Notes2012

000'USD 2011

000'USD

Revenues 18 197,902 77,661

Cost of sales (217,338) (66,570)

GROSS(LOSS)/PROFIT (19,436) 11,091

Government grants related to income 19 1,255 653

Selling expenses (5,402) (2,867)

Administrative expenses 20 (55,330) (52,284)

Other operating income /(expenses) (775) (1,905)

Change in onerous contract provision 16 (145) 17,669

Accrual for insurance recovery 7 17,220 -

Cost of disposed aircraft 7 (17,220) -

Write down of work-in progress to net realisable value 11 (11,302) -

Impairment of non-current assets 7 (795) (41,977)

OPERATING LOSS (91,930) (69,620)

Interest income 7,334 5,875

Interest expense (107,923) (102,623)

Foreign exchange gains /(losses) 60,133 (38,123)

LOSS BEFORE TAX (132,386) (204,491)

Income tax benefit 21 21,139 32,994

LOSS FOR THE YEAR (111,247) (171,497)

Effect of translation to the presentation currency (11,800) 11,546

Total comprehensive income for the year (123,047) (159,951)

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT”

The accompanying notes are an integral part of these financial statements

7

STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 DECEMBER 2012

2012 000'USD

2011 000'USD

OPERATING ACTIVITIES: Loss before tax (132,386) (204,491)

Depreciation and amortisation recognised in income 37,666 7,928

Interest income (7,334) (5,875)

Unrealised foreign exchange differences (65,644) 37,060

Loss/(gain) on assets disposal 106 (7,297)

Write-down of value added tax receivable 1,096 354

Write-down of work-in-progress to net realisable value 11,302 -

Change in onerous contract provision 145 (17,669)

Impairment of non-current assets 795 41,977

Interest expense and commission amortisation 107,923 105,003

Other 1,964 1,682

Cash flow from operating activities before changes in working capital and income tax

(44,367) (41,328)

Increase in inventories (220,918) (113,403)

Increase in trade and other receivables (111,250) (17,793) Increase in other current assets (3,738) (27,915)

Increase in advances from customers 156,342 98,968 Increase in trade and other payables 78,516 67,298

Increase in taxes payable 732 22

Interest paid (104,704) (99,002)

Cash flow used in operating activities (249,387) (133,153)

INVESTING ACTIVITIES:

Acquisition of property, plant and equipment (86,275) (166,603)

Acquisition of intangible assets (81,628) (112,319)

Increase of non-current value added tax receivable (5,558) (13,561)

Interest received 2,022 2,531

Government grant related to assets - 708

Cash flows used in investing activities (171,439) (289,244)

FINANCING ACTIVITIES:

Proceeds from borrowings, net 1,240,437 773,218

Repayment of borrowings (657,694) (427,574)

Finance lease payments (2,003) (4,862)

Cash flows from financing activities 580,740 340,782

Effect of translation to foreign currency 4,853 1,919

Increase / (decrease) in cash and cash equivalents 164,767 (79,696)

Cash and cash equivalents at the beginning of period (Note 13) 17,691 97,387

Cash and cash equivalents at the end of period (Note 13) 182,458 17,691

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT”

The accompanying notes are an integral part of these financial statements

8

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 2012

000'USD Share

capital Share

premium Additional

paid-in-capital Foreign currency translation reserve

Accumulated losses Total

Balance as at 01 January 2011 100,856 171,751 3,568 31,634 (355,414) (47,605)

Loss for the year - - - - (171,497) (171,497)

Other comprehensive income

Effect of translation to the presentation currency - - - 11,546 - 11,546

Total comprehensive income for the year (159,951)

Transactions with owners, recorded directly in equity

Transactions with entities under common control, net of related income tax effect of income of USD 788 thousand (Note 9) - - - - 3,151 3,151

Contribution, net of related income tax of USD 12,949 thousand (Note 14) 51,794 51,794

Balance as at 31 December 2011 100,856 171,751 55,362 43,180 (523,760) (152,611)

Loss for the year - - - - (111,247) (111,247)

Other comprehensive income

Effect of translation to the presentation currency - - - (11,800) - (11,800)

Total comprehensive income for the year (123,047)

Balance as at 31 December 2012 100,856 171,751 55,362 31,380 (635,007) (275,658)

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

9

Note 1. The Company

Closed Joint-Stock Company “Sukhoi Civil Aircraft” (hereafter “the Company”) was established on 25 May 2000 with the purpose of development, testing, production and operation of new types of civil aircraft. In 28 January 2011 the Company received ARMAK Type Certificate for “Sukhoi Super Jet – 100” aircraft (formerly “Russian Regional Jet” or “RRJ”) - a civil aircraft with a capacity of 95 seats in basic configuration. In February 2012, the Company received EASA Type Certificate for “Sukhoi Super Jet – 100” aircraft.

The Company’s registered address is at: 2 build, 23B, Polykarpov Str., 125284, Moscow, Russia.

The Company has the following branches:

Komsomolsk-on-Amur branch located at address: 1 Sovetskaya Str., Komsomolsk-on-Amur 681018, Khabarobvsk Region, Russia.

Novosibirsk branch located at address: 15, Polzunova Str., Novosibirsk, Russia.

Voronezh branch located at address: 27, Tsiolkovskogo Str., Voronezh, Russia.

Ulyanovsk branch located at address: 1, Antonova avenue, Uljyanovsk, Russia

The Company has no subsidiaries.

The Company’s shareholders are:

JSC “Sukhoi Design Bureau”, which owns 3.01% of ordinary shares;

JSC “Aviation Holding Company Sukhoi”, which owns 71.99% of ordinary shares (the “Parent Company”).

World Wings S.A. (96% subsidiary of Alenia Aermacchi, formerly Alenia Aeronautica, ultimately controlled by Finmeccanica), which owns 25% plus one share.

Russian business environment

The Company’s operations are located in the Russian Federation. Consequently, the Company is exposed to the economic and financial markets of the Russian Federation which display characteristics of an emerging market. The legal, tax and regulatory frameworks continue development, but are subject to varying interpretations and frequent changes which together with other legal and fiscal impediments contribute to the challenges faced by entities operating in the Russian Federation. These financial statements reflect management’s assessment of the impact of the Russian business environment on the operations and the financial position of the Company. The future business environment may differ from management’s assessment.

Note 2. Basis of presentation

Statement of compliance

These financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRSs”) and related interpretations adopted by the International Accounting Standards Board (“IASB”).

Basis of measurement

The financial statements are prepared on the historical cost basis except that the carrying amounts of assets, liabilities and equity items in existence at 31 December 2002 include adjustments for the effects of hyperinflation, which were calculated using conversion factors derived from the Russian Federation

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

10

Consumer Price Index published by the Russian Statistics Agency, GosKomStat. Russia ceased to be hyperinflationary for IFRSs purposes as at 1 January 2003.

Functional and presentation currency

The national currency of the Russian Federation is the Russian Rouble (“RUB”), which is the Company’s functional currency taking into account the economic environment in which the Company operates.

These financial statements are presented in US dollars (USD), since management believes that this currency is more meaningful for the users of the financial statements. The assets and liabilities of the Company are translated from RUB into USD at the exchange rate at the end of the year. Revenues and expenses are translated into USD using rates approximating exchange rates at the dates of the transactions. The resulting exchange difference is recorded directly in equity in the foreign currency translation reserve. For translation purposes the following exchange rates were used:

As at 01 January 2011 - RUB 30.4769 for USD 1;

As at 31 December 2011 - RUB 32.1961 for USD 1;

As at 31 December 2012 - RUB 30.3727 for USD 1;

Average exchange rate for 2011 - RUB 29.3874 for USD 1;

Average exchange rate for 2012 - RUB 31.0929 for USD 1.

The RUB is not a readily convertible currency outside the Russian Federation and, accordingly, any conversion of RUB to USD should not be construed as a representation that the RUB amounts have been, could be, or will be in the future, convertible into USD at the exchange rate disclosed, or at any other exchange rate.

Going concern

These financial statements were prepared on the basis of accounting principles applicable to a going concern, which assumes that the Company will continue operations in the foreseeable future and will be able to realize its assets and discharge its liabilities in the normal course of operations.

As at 31 December 2012 year the Company’s current liabilities exceeded its current assets by USD 480,980 thousand (2011: USD 388,472 thousand) and its net assets were negative both at the reporting date and as at 31 December 2011 (USD 275,658 thousand and USD 152,611 thousand, respectively).

The Company’s net assets determined with reference to the statutory financial statements of the Company prepared in accordance with the legislation of the Russian Federation as at 31 December 2012 and at 31 December 2011 were below the Company’s share capital. Under these circumstances, according to the Federal Law of Russian Federation “On joint-stock companies”, the Company shareholders are required to decide either to reduce the share capital to the net assets amount or to liquidate the Company before 30 June 2013. Management does not believe that this issue would impact Company’s ability to continue as a going concern and developed an action plan addressing this risk. This plan, inter alia, includes future share issues and sale of assets. In particular, in January 2013 the Board of Directors approved additional shares issue (Note 27).

Management assesses that the Company will continue to operate in the foreseeable future and will be able to realize its assets and discharge its liabilities in the normal course of business. The factors that contributed most to this assessment are as follows.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

11

The ultimate realization of the Company’s assets and its long-term liquidity will be impacted by its success in completion of the “Sukhoi Super Jet – 100” development program (refer to Note 6). The “Sukhoi Super Jet – 100” program is included in the Federal Target Program “Development of the civil aircraft for 2002-2011 and for the period until 2015” approved by the Decision of the Federal Government of the Russian Federation No. 728 dated 15 October 2001.

Management believes that financial support from the Federal Government, together with the Company’s other capital resources, is sufficient to meet its obligations, as they become due.

In 2013 the management plans to increase its sales to 27 aircraft which is expected to improve Company’s financial result and reputation. Management has available borrowing facilities that are sufficient to manage liquidity, including USD 1,000,000 thousand facility provided by VEB, a Russian government owned bank, of which approximately USD 600,000 thousand was undrawn as at the reporting date (refer also to Note 15).

Therefore, management does not believe that there is a material uncertainty regarding Company’s ability to continue as a going concern in the foreseeable future.

Use of estimates and judgments

The preparation of these financial statements in conformity with IFRSs requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results could differ from those estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimates are revised and in any future periods affected.

In particular, information about significant areas of estimation uncertainty and critical judgments in applying accounting policies are described in the following notes:

Note 2 – Going concern;

Note 6 – Intangible assets;

Note 11 – Inventories;

Note 16 – Onerous contract provision;

Note 10 – Recoverability of deferred tax assets

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

12

Note 3. Summary of significant accounting principles

The following are the main principles of the Company’s accounting policies that are applied consistently during all reporting periods.

(a) Foreign currencies

Transactions in foreign currencies are translated to RUB at the foreign exchange rate ruling at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies at the reporting date are translated to RUB at the foreign exchange rate ruling at that date. Non-monetary assets and liabilities denominated in foreign currencies that are stated at historical cost are translated to RUB at the foreign exchange rate ruling at the date of the transaction. Non-monetary assets and liabilities denominated in foreign currencies that are stated at fair value are translated to RUB at the foreign exchange rate ruling at the dates the fair values were determined. Foreign exchange differences arising on translation are recognised in the statement of comprehensive income.

(b) Intangible assets

Research and development

Expenditure on research activities, undertaken with the prospect of gaining new scientific or technical knowledge and understanding, is recognised in profit or loss as incurred.

Expenditure on development activities, whereby research findings are applied to a plan or design for the production of new or substantially improved products and processes, is capitalised if the product or process is technically and commercially feasible and the Company has sufficient resources to complete development. The expenditure capitalised includes the cost of materials, direct labour and an appropriate proportion of overheads. Furthermore, borrowing costs that are directly attributable to the acquisition, construction or production of qualifying assets are included in the cost. Any related government grants are deducted from the cost. Other development expenditure is recognised in the statement of comprehensive income as an expense as incurred. Upon completion of the development phase capitalised development expenditure is stated at cost less accumulated amortisation and impairment losses.

Other intangible assets Other intangible assets, which are acquired by the Company, are stated at cost less accumulated amortisation and impairment losses and less any related government grants. Expenditure on internally generated goodwill and brands is recognised in profit or loss as incurred.

Amortisation

Intangible assets with a definite lifetime are amortised on a straight-line basis over their estimated useful lives from the date the asset is available for use.

Capitalised development costs are amortised on the unit-of-production method.

(c) Impairment

Financial assets

A financial asset is considered to be impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of the asset.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

13

An impairment loss in respect of a financial asset measured at amortised cost is calculated as the difference between its carrying amount, and the present value of the estimated future cash flows discounted at the original effective interest rate.

Individually significant financial assets are tested for impairment on an individual basis. The remaining financial assets are assessed collectively in groups that share similar credit risk characteristics.

All impairment losses are recognised in profit or loss. Any cumulative loss in respect of an available-for-sale financial asset recognised previously in equity is transferred to profit or loss.

An impairment loss is reversed if the reversal can be related objectively to an event occurring after the impairment loss was recognised, and is recognised in profit or loss.

Non-financial assets

The carrying amounts of the Company’s non-financial assets, other than inventories and deferred tax assets, are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. For intangible assets that are not yet available for use, recoverable amount is estimated at each reporting date.

The recoverable amount of an asset or cash-generating unit is the greater of its value in use and its fair value less costs to sell.

In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. For the purpose of impairment testing, assets are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other assets or groups of assets (the “cash-generating unit”).

An impairment loss is recognised if the carrying amount of an asset or its cash-generating unit exceeds its recoverable amount. Impairment losses are recognised in profit or loss.

Impairment losses recognised in prior periods are assessed at each reporting date for any indications that the loss has decreased or no longer exists. An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

(d) Property, plant and equipment

Owned assets

Property, plant and equipment is stated at historical cost less depreciation and impairment loss. The cost of self-constructed assets includes the cost of materials, direct labour and an appropriate proportion of overheads. Furthermore, borrowing costs that are directly attributable to the acquisition, construction or production of qualifying assets are included in the cost. Related government grants are deducted from cost of acquired or constructed property, plant and equipment.

Where an item of property, plant and equipment comprises major components having different useful lives, they are accounted for as separate items of property, plant and equipment.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

14

Leased assets

Leases under which the Company assumes substantially all the risks and rewards of ownership are classified as finance leases. Plant and equipment acquired by way of finance lease is stated at an amount equal to the lower of its fair value and the present value of the minimum lease payments at inception of the lease, less accumulated depreciation and impairment losses.

Subsequent expenditure

Expenditure incurred to replace a component of an item of property, plant and equipment that is accounted for separately, is capitalised with the carrying amount of the component being written off. Other subsequent expenditure is capitalised if future economic benefits will arise from the expenditure. All other expenditure, including repairs and maintenance expenditure, is recognised in profit or loss as incurred.

Depreciation

Depreciation is recognised in profit or loss on a straight-line basis over the estimated useful lives of the individual assets. Depreciation commences on the date of acquisition or, in respect of internally constructed assets, from the time an asset is completed and ready for use. Land is not depreciated.

The estimated useful lives are as follows:

Buildings and Constructions 10 - 20 years Machinery and Equipment 5 - 15 years Vehicles 5 - 10 years Other 3 - 10 years

Depreciation methods, estimated useful lives and residual values are re-assessed annually.

(e) Inventories

Inventories are stated at the lower of cost and net realisable value. Net realisable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and selling expenses.

The cost of inventories is based on the average cost principle and includes expenditure incurred in acquiring the inventories and bringing them to their existing location and condition.

In the case of manufactured inventories and work-in-progress cost includes all direct costs such as labour, material and direct overheads, and an allocation of fixed and variable production overheads. Labour costs include taxes and employee benefit costs associated with labour that is involved directly in the production process.

(f) Non-derivative financial instruments

Non-derivative financial instruments comprise trade and other receivables, cash and cash equivalents, loans and borrowings, and trade and other payables.

Non-derivative financial instruments are recognised initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition non-derivative financial instruments are measured as described below.

Cash and cash equivalents comprise cash balances and call deposits with maturities of three months or less from acquisition date that are subject to an insignificant risk if changes in their fair value and are used by the Company in the management of its short-term commitment.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

15

Trade and other receivables are stated at amortised cost less impairment losses.

Loans and borrowings are stated at amortised cost using the effective interest method, less impairment losses.

Trade and other payables are stated at amortised cost.

Accounting for finance income and costs is discussed in note 3(l).

(g) Provisions

A provision is recognised in the statement of financial position when the Company has a legal or constructive obligation as a result of a past event, and it is probable that an outflow of economic benefits will be required to settle the obligation. If the effect is material, provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability.

Onerous contract provision

A provision for onerous contracts is recognised when the expected benefits to be derived by the Company from a contract are lower than the unavoidable cost of meeting its obligations under the contract. The provision is measured at the present value of the lower of the expected cost of terminating the contract and the expected net cost of fulfilling the contract. The estimate of net cost of fulfilling the contract includes expected late delivery penalties, if applicable. Before a provision is established, the Company recognises any impairment loss on the assets associated with that contract.

Provision for warranty costs

A provision for estimated standard warranty costs is recognised in the period in which the related product sales occur. An accrual for warranty costs is recognised based on the Company’s historical experience on previous deliveries of aircraft. Estimates are adjusted as necessary based on subsequent experience.

(h) Employee benefits

The Company makes contributions for the benefit of employees to Russia’s State pension fund. The contributions are expensed as incurred.

(i) Income tax

Income tax expense comprises current and deferred tax. Current tax and deferred is recognised in profit or loss except for items recognised directly in equity or in other comprehensive income.

Current tax expense is the expected tax payable on the taxable income for the year, using tax rates enacted or substantively enacted at the reporting date, and any adjustment to tax payable in respect of previous years.

Deferred tax is recognised using the balance sheet method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. Deferred tax is not recognised for the following temporary differences: the initial recognition of goodwill, the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit, and differences relating to investments in subsidiaries to the extent that it is probable that they will not reverse in the foreseeable future. Deferred tax is measured at the tax rates that are expected to be applied to the temporary differences when they reverse, based on the laws that have been enacted or substantively enacted by the reporting date.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

16

A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will be available against which temporary difference can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realised.

(j) Government grants

Government grants (including non-monetary grants at fair value), are not recognised until there is reasonable assurance that the Company will comply with the conditions attaching to them; and the grants will be received. Government grants are recognised in profit or loss on a systematic basis over the periods necessary to match them with the related costs which they are intended to compensate.

A government grant, to compensate for expenses or losses already incurred is recognised as income of the period in which it becomes receivable.

(k) Revenues

Sale of aircraft

Revenue from the sale of goods is recognised in profit or loss when the significant risks and rewards of ownership have been transferred to the buyer, the amount of revenue can be measured reliably, it is probable that the economic benefits associated with the transaction will flow to the entity, and the costs incurred or to be incurred in respect of the transaction can be measured reliably. Any cash outflows related to customer penalties for late delivery of aircraft are deducted from gross amount of revenue.

Services

Revenue from services rendered is recognised in profit or loss in proportion to the stage of completion of the transaction at the date of the statement of financial position. The stage of completion is assessed by reference to surveys of work performed.

Operating lease

A lease is classified as an operating lease if it does not transfer substantially all risks and rewards incidental to ownership.

Where the Company is the lessor in an operating lease agreement the leased asset is recognised in the Company’s financial statements, and depreciation and lease income are recognised in profit or loss on a straight-line basis over the period.

(l) Finance income and costs

Finance income comprises interest income on funds invested and foreign currency gains. Interest income is recognised as it accrues in profit or loss, using the effective interest method, except for the interest income on the funds, which were borrowed specifically for the purposes of obtaining a qualifying asset which reduces the amount of capitalised borrowing costs.

Finance costs comprise interest expense on borrowings, foreign currency losses and impairment losses recognised on financial assets. All borrowing costs are recognised in profit or loss using the effective interest method, except for costs directly attributable to the acquisition, construction or production of qualifying assets which are included in the cost of qualifying assets.

Foreign currency gains and losses are reported on a net basis.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

17

(m) Operating leases

Payments made under operating leases are recognised in profit or loss on a straight-line basis over the term of the lease. Lease incentives received are recognised in profit or loss as an integral part of the total lease payments made.

(n) Determination and presentation of operating segments

An operating segment is a component of the Company that engages in business activities from which it may earn revenues and incur expenses, including revenues and expenses that relate to transactions with any of the Company’s other components, and for which discrete financial information is available. All operating segment’s operating results are reviewed regularly by the Board of Directors to make decisions about resources to be allocated to the segment and assess its performance.

As disclosed in Note 1, the Company’s current principal activity is the development of SSJ-100 program which is a start-up operation that earned the first revenues in 2011. Nearly all of the Company’s assets are associated with this program and are located in one geographical region – Russian Federation. The Company expects to receive the majority of its revenues from sales of SSJ-100. Giving regard to these factors, management believes that as of 31 December 2011 and 31 December 2012 all assets and liabilities related to operating activities of the Company are associated with a single operating segment, SSJ-100 program. The reconciliation of segment revenue and segment measure of profit or loss with reported amounts required by IFRS 8 Operating Segments is disclosed in Note 5.

(o) New standards and Interpretations not yet adopted

A number of new Standards, amendment to Standards and Interpretations are not yet effective as at 31 December 2012, and have not been applied in preparing these financial statements. Management of the Company does not expect these pronouncements to have a significant impact of the Company’s operations. The company plans to adopt these pronouncements when they become effective.

Note 4. Reclassification and changes in presentation

In 2011 several loans totalling USD 733,918 thousand were disclosed as unsecured loans, including long-term and short-term part totalling USD 284,337 thousand and USD 449,581 thousand, respectively, however certain terms of the relevant loan agreements indicate that there is security pledged against them. The Company has changed the presentation of comparative information in these financial statements and the relevant loans have been presented as secured (see Note 15).

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

18

Note 5. Operating segments

The Company has one reportable segment “Sukhoi Super Jet-100” that includes development and production of civil aircraft, primarily (Note 3 (n)).

The Board of Directors reviews internal management reports on a quarterly basis based on the statutory accounting records.

The major reconciling differences between the information provided to the Board of Director and the related IFRS-based amounts relate to:

Timing differences related when revenue and costs are recognised;

Adjustments of net realisable value of inventories, provision for property, plant and equipment and change in onerous contracts;

Administrative and selling expenses.

Information regarding the results of reportable segment is included below. Segment performance is measured based on segment profit before income tax. Segment profit is used to measure performance as management believes that such information is the most relevant in evaluating the results of certain segments relative to other entities that operate within these industries.

Reconciliation of reportable segments' profit

2012 000’USD

2011 000’USD

Reportable segment loss before income tax

(183,839)

(149,891)

Adjustments for:

Difference in timing of recognition of revenue and cost of sales 43,993 84,775

Presentation of certain types of administrative and other expenses (13,312) (35,629)

Net realisable value of inventories and fixed assets (6,462) (62,713)

Reclassification of commissions 5,961 6,670

Leasing 3,937 3,690

Onerous contract provision (284) (46,764)Interest capitalised - (3,844)Zero-rate debt interest expense (5,429) (4,383)Difference in timing of recognition of other income and expenses 23,049 3,598 Loss before income tax (132,386) (204,491)

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

19

Note 6. Intangible assets

In thousands USD Software Development of SSJ-

100 program Advances given for development costs Total

COST

At 01 January 2011 16,483 649,201 31,301 696,985

Additions 3,036 151,761 8,727 163,524

Disposal (1,893) (3,685) (1,682) (7,260)

Reclassification to property, plant and equipment - - (9,416) (9,416)

Transfers 1,219 11,085 (12,304) -

Government grant related to development cost - (708) - (708)

Effect of translation to the presentation currency (1,086) (48,489) (496) (50,071)

At 31 December 2011 17,759 759,165 16,130 793,054

Additions 1,282 99,773 8,555 109,610

Disposal (2,000) - (390) (2,390)

Transfers - 4,793 (4,793) -

Effect of translation to the presentation currency 1,049 48,056 1,048 50,153

At 31 December 2012 18,090 911,787 20,550 950,427

ACCUMULATED AMORTISATION

At 01 January 2011 2,884 61,521 - 64,405

Charge for the period 2,145 3,796 - 5,941

Disposal (1,893) - - (1,893)Effect of translation to the presentation currency (176) (3,616) - (3,792)

At 31 December 2011 2,960 61,701 - 64,661

Charge for the period 1,311 11,071 - 12,382

Disposal (2,000) - - (2,000)Effect of translation to the presentation currency 161 7,042 - 7,203

At 31 December 2012 2,432 79,814 - 82,246

NET BOOK VALUE At 01 January 2011 13,599 587,680 31,301 632 580

At 01 January 2012 14,799 697,464 16,130 728,393

At 31 December 2012 15,658 831,973 20,550 868,181

Capitalisation of development costs

On 28 January 2011 the Company obtained the Type Certificate for serial aircraft production and subsequently commenced deliveries to the first customers.

Management concluded that development costs capitalised up to the date of the Type Certificate met the requirement of IAS 38 Intangible assets as ‘available for use’ which triggered commencement of amortisation of these costs based on the unit-of-production method. Management expects that certain development activities are still required to complete the development of the aircraft to ensure its operating capabilities and required aviation standards in the target markets.

Management will monitor whether future development activities will result in meeting capitalisation requirements of IAS 38 and, if met, related costs will adjust the carrying amount of related intangible asset. The amortisation schedule will be adjusted prospectively as necessary.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

20

As a consequence of substantial completion of development of the SSJ-100 program management ceased capitalisation of borrowing costs from 28 January 2011. Additions to development costs for the year ended 31 December 2012 do not include capitalised borrowing costs (2011: USD 3,456 thousand).

Impairment of intangible assets

Management constantly monitors the SSJ-100 program for signs of impairment. As at 31 December 2012, management performed an impairment test taking into account the current financial position of the Company as an indicator for potential impairment.

Following the requirements of IAS 36 Impairment of assets and taking into account that the related development costs were considered particularly ‘available for use’, in measuring value in use management calculated the cash flow projections for a period of 10 years as the program is expected to mature in 2022. The terminal value, representing the cash flows beyond the ten-year period, was calculated based on the 10th forecasted year with zero growth rate.

Forecasted cash flow projections used for impairment test were based on the latest business plan which was revised in December 2012. The cash flow model is substantially sensitive to changes in key assumptions. Below is the analysis of the sensitivity of the cash flow model to changes in the production capacity, sales price per aircraft and discount rate.

Revised sales volume for 2013 is 27 aircraft with expected increase to maximum production capacity of 70 aircraft in 2016 (under previous year business plan maximum production capacity of 70 aircraft was also expected to be achieved in 2016, however expected sales volume for 2013 was 41 aircraft). This expectation is based on the result of recent review of achievable production capacity which will be fully utilised in 2016. An even decrease of annual production volumes by 10% after full utilisation of production capacity (i.e. annual sales volumes would be less than expected by 10% in each forecasted year starting from 2016, assuming that actual sales volumes in 2013-2015 will be as expected) would result in an impairment loss of USD 144,867 thousand. If, in addition to lower utilisation of production capacity after 2016, an annual sales volume in 2013-2015 would be lower than expected by 5 aircraft in each of these years, an additional impairment loss of USD 211,173 thousand would be required.

The overall market demand for SSJ-100 aircraft is expected to remain the same. An annual increase in future real sales prices by 3% starting from 2013 would result in additional excess of discounted cash flows over the carrying amount of the asset by USD 875,171 thousand. An annual decrease in future real sales prices by 3% starting from 2013 would result in an impairment loss of USD 122,633 thousand.

As a key assumption, the Company expects to be able to increase real sales prices by 10% starting from 2018 after introduction of the enhanced versions of basic and long-range modification of the aircraft to achieve an average real sales price of USD 28,400 thousand for SSJ-100 “B” and USD 29,100 thousand for SSJ-100 “LR”. By this time the Company would be able to demonstrate an operating usage history of SSJ-100 fleet by airline customers which should further support expected demand for existing and newer modifications of SSJ-100 family. Failure to enjoy advantage of increase in future real sales prices in 2018 and beyond would result in an impairment loss of USD 668,457 thousand.

Due to adverse change in macroeconomic indicators, the pre-tax nominal rate applied for discounting of expected cash flows increased to 15.6% as compared to last year (2011: 15.39%). An application of 14.6% pre-tax nominal discount rate would result in additional excess of discounted cash flows over the carrying amount of the asset by USD 613,188 thousand. An application of 16.6% pre-tax nominal discount rate would result in additional excess of discounted cash flows over the

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

21

carrying amount of the asset by USD 174,097 thousand.

Note 7. Property, plant and equipment

In thousands USD Buildings and Constructions

Machinery and

equipment

Aircraft in operating

leases Vehicles Other

Advances paid for acquisition of equipment & Building &

Construction Total

COST At 01 January 2011 54,093 241,503 - 3,562 12,566 14,842 326,566

Additions and transfers 17,131 31,308 129,584 23 167 (446) 177,767

Disposal - (557) - (91) (50) - (698)

Transfer to financial lease - (27,677) - - - - (27,677)Transfer from Inventories into operating leases - - 37,743 - - - 37,743

Effect of translation into presentation currency (4,383) (13,164) (14,597) (184) (681) (754) (33,763)

At 31 December 2011 66,841 231,413 152,730 3,310 12,002 13,642 479,938

Additions and transfers 12,293 21,738 59,311 117 1,002 (1,625) 92,836 Transfer from /(to) Inventories - - 23,702 - - (3,949) 19,753

Disposal (8) (37,715) - (140) (281) - (38,144)

Effect of translation into the presentation currency 4,304 13,514 11,137 198 738 687 30,578

At 31 December 2012 83,430 228,950 246,880 13,485 13,461 8,755 584,961

ACCUMULATED DEPRECIATION

At 01 January 2011 13,046 75,852 - 1,726 9,075 - 99,699 Depreciation for the period 5,717 43,169 1,388 684 1,842 - 52,800

Disposal - (233) - (91) (50) - (374)

Impairment losses - - 41,977 - - - 41,977

Effect of translation into presentation currency (1,195) (7,796) (3,783) (144) (641) - (13,559)

At 31 December 2011 17,568 110,992 39,582 2,175 10,226 - 180,543 Depreciation for the period 7,434 36,676 9,976 573 1,059 - 55,718

Disposal - (20,649) - (140) (280) - (21,069)Impairment losses - - 795 - - - 795

Effect of translation into presentation currency 1,231 7,043 2,633 141 632 - 11,680

At 31 December 2012 26,233 134,062 52,986 2,749 11,637 - 227,667

NET BOOK VALUE At 01 January 2011 41,047 165,651 - 1,836 3,491 14,842 226,867

At 31 December 2011 49,273 120,421 113,148 1,135 1,776 13,642 299,395

At 31 December 2012 57,197 94,888 193,894 736 1,824 8,755 357,294

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

22

Disposal of machinery and equipment

In May 2012, during a demonstration flight, a test aircraft with 45 people on board crashed in Indonesia in bad weather conditions. Management of the Company does not believe that the catastrophe will have a significant impact on the future of the SSJ-100 program.

The aircraft was insured against all risks and third party legal liability in respect of aircraft in favour of Closed Joint-Stock Company “Sukhoi Civil Aircraft”. The insurance covers the aircraft carrying amount and is expected to be received within 2013 annual reporting period.

Aircraft in operating lease

In 2011 the Company revised the sales contract with Aeroflot to supply aircraft. According to the revised terms the Company has a firm obligation to repurchase at later dates ten first aircraft out of 40 to be delivered. Accordingly, the first ten deliveries are accounted for as operating lease and the carrying amounts of these aircraft were transferred from inventory to property, plant and equipment. As at 31 December 2012, ten completed aircraft with a book value of USD 193,384 thousand were delivered to Aeroflot (31 December 2011: four completed aircraft with book value of USD 76,163 thousand were delivered to Aeroflot and six aircraft with carrying value of USD 36,985 thousand were under construction).

As at 31 December 2012 the aircraft in operating leases were tested for impairment. As a result, the book value of the aircraft was reduced to its net selling price which was determined based on management’s best estimate of the market sales price of the aircraft upon repurchase from Aeroflot. An additional impairment loss was recognised in the amount of USD 795 thousand (2011: USD 41,977 thousand).

Finance lease

The Company leases equipment and vehicles under a number of finance lease agreements. At the end of each of the leases the Company has the option to purchase the equipment at a beneficial price. At 31 December 2012 the net book value of leased assets was USD 4,542 thousand (31 December 2011: USD 6,199 thousand). The leased equipment secures lease obligations (refer Note 15).

Security

At 31 December 2012 equipment with a carrying value of USD 11,209 thousand (31 December 2011: 2,500) is pledged as collateral for secured loans (see note 15).

Note 8. Net investment in finance leases

2012

000'USD 2011

000'USD

Net investment in finance leases 26,832 26,679

of that: Current portion 1,017 500

Non-current portion 25,815 26,179

26,832 26,679

The carrying amount of net investment in finance lease is represented by a number of simulators which were transferred under finance lease arrangements to Superjet International S.A.(SJI), an entity which is a related party to the Company, in 2011 and 2012. The gross investment in finance lease does not include any material unguaranteed residual values.

The simulators leased out under finance lease arrangements secure lease receivables and are pledged as collateral for secured bank loans.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

23

000'USD

Future minimum lease payments 2012

Interest 2012

Present value of minimum lease payments 2012

Future minimum

lease payments

2011 Interest

2011

Present value of minimum

lease payments

2011

Less than one year 3,608 2,591 1,017 3,426 2,926 500

Between one and five years 14,032 8,070 5,962 13,706 8,536 5,170

More than five years 28,227 8,374 19,853 30,838 9,829 21,009

Total 45,867 19,035 26,832 47,970 21,291 26,679

Note 9. Other receivables

In 2010-2011 the Company disposed of certain items of machinery and equipment previously acquired under finance lease agreements. All rights and liabilities under lease agreement were transferred to JSC KnAAPO and JSC NAPO, entities under common control with the Company, which are the manufacturing and assembling sites for Sukhoi SuperJet-100 aircraft. Before this equipment was transferred, the related items of property, plant and equipment and finance lease liabilities were classified as assets held for sale. In accordance with the lease transfer agreements all payments, which include mainly finance lease payments and lease advances made by the Company in the past, shall be compensated by JSC KnAAPO and JSC NAPO by 2029.

As at 31 December 2012 the related amounts of future cash inflows, adjusted for the time value of money, consisted of other non-current receivables in the amount of USD 50,611 thousand (31 December 2011: USD 48,738 thousand) and other current receivables in the amount of USD 14,409 thousand (31 December 2011: USD 6,832 thousand).

Note 10. Deferred tax assets

Deferred tax assets and liabilities attributed to the following items:

000'USD 31 December

2012 Recognised in profit or loss

Recognised in equity

Foreign currency

translation 01 January

2012

Intangible assets (50,721) 32 - (2,874) (47,879)Property, plant and equipment (68,857) (47,080) - (2,281) (19,496)Inventories (25,279) (32,906) - (309) 7,936 Trade and other accounts receivable 9,041 538 - 492 8,011 Trade and other accounts payable 35,363 20,859 - 1,288 13,216 Loans and borrowings (14,376) (178) - (808) (13,390)Provision 3,330 57 - 187 3,086 Tax loss carry-forwards 228,047 79,817 - 10,181 138,049 Net deferred tax assets 116,548 21,139 - 5,876 89,533

000'USD 31 December

2011 Recognised in profit or loss

Recognised in equity

Foreign currency

translation 01 January

2011

Intangible assets (47,879) (52,202) - 4,568 (245)Property, plant and equipment (19,496) (20,474) - 1,832 (854)Inventories 7,936 (7,640) - (175) 15,751 Trade and other accounts receivable 8,011 (1,838) (788) (381) 11,018 Trade and other accounts payable 13,216 15,929 - (1,315) (1,398)Loans and borrowings (13,390) 388 (12,949) 1,204 (2,033)Provision 3,086 (3,534) - (47) 6,667 Tax loss carry-forwards 138,049 102,365 - (11,117) 46,801 Net deferred tax assets 89,533 32,994 (13,737) (5,431) 75,707

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

24

Management estimates that the Company will have sufficient future taxable profits to utilise the deferred tax asset after completion of “Sukhoi Super Jet – 100” development program and commencement of production and sales of the aircraft. Management expects that the Company would generate sufficient profits to utilise deferred tax assets recognised for tax losses carry forward prior to their expiry.

Note 11. Inventories

2012 000'USD

2011 000'USD

Raw materials for aircraft serial production 183,412 116,305 Advances given for aircraft serial production 116,923 70,170 Work-in-progress 149,451 40,395 Finished goods 242 5,158 Other inventories and suppliers 4,129 3,862 Subtotal 454,157 235,890 Net realisable value allowance (25,221) (12,878)Total 428,936 223,012

Work-in-progress is stated at the lower of cost and net realisable value. Net realisable value is the estimated selling price in the ordinary course of business, less the estimated incremental costs of completion and selling expenses.

At 31 December 2012 work in progress with a carrying value of USD 12,167 thousand (31 December 2011: USD 3,751 thousand) was pledged as collateral for secured loans (see Note 15).

Note 12. Trade and other receivables

2012

000'USD 2011

000'USD Trade accounts receivable 138,931 32,429 Advances to suppliers 3,789 4,182 Prepaid expenses 3,007 3,394 Prepaid bank commissions related to undrawn borrowing facilities 1,497 3,467 Other receivables 71,083 9,123 Total 218,307 52,595

As at 31 December 2012 trade accounts receivable included USD 17,802 thousand due from Armenian airline Armavia airways for the aircraft delivered in 2011.

The terms of sales agreement provide that the aircraft is pledged as collateral in favour of the Company until its full payment by Armavia. Due to its financial difficulties Armavia was unable to pay for the aircraft delivered and returned the aircraft back on the territory of the Russian Federation after both parties have signed an amendment to the sales agreement for termination of the deal. The termination of the deal assumed that Armavia returns the aircraft to the Company free from any encumbrance while the Company had to return advance cash payments received for aircraft. The Company fully discharged its obligations under this amendment. At the same time Armavia failed to release the aircraft being pledged for its liabilities to other third parties. Therefore, although the aircraft is located on the territory of the Russian Federation the Company is restricted from its disposal until the encumbrance imposed by Armavia is removed. At the date when these financial statements were authorised for issue the encumbrance is still present, therefore the termination agreement has not yet been exercised in full. In 2013 the Company filed a claim to International Arbitration Court (Note 27) and expects a favourable ruling enforcing Armavia to release encumbrance.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

25

After the reporting date, in March 2013, Armavia management announced that Armavia will probably declare itself bankrupt in the near future. In such case, the local court may arrests the assets of Armavia, including the aircraft in question, until completion of bankruptcy procedures or undertake other actions not in favour of the Company’s interests. The Company management intends to undertake further steps that might be necessary to speed up releasing the aircraft from external encumbrances.

Taking into account the above circumstances, a significant uncertainty arises as to whether the Company will be able to receive the economic benefits in the full amount of receivable due from Armavia. Management performed analysis of the likelihood and impact of potential scenarios under which the situation may develop, including consultation with external legal counsel. Based on this analysis, management does not believe that the Company will suffer significant losses with regard to the matter. Therefore no adjustment to the carrying amount of receivable from Armavia was made in these financial statements.

As at 31 December 2012 other receivables include:

USD 35,325 thousand (at 31 December 2011: nill) receivable for own bonds transferred with secondary issue (Note 15);

USD 17,351 thousand (at 31 December 2011: nill) accrual for insurance recovery for the crashed test aircraft (Note 7).

Note 13. Cash and cash equivalents

2012

000'USD 2011

000'USD

Bank accounts 181,967 16,991

Bank deposits 413 680

Other cash and cash equivalents 78 20

Total 182,458 17,691

Note 14. Equity

Share capital and Share premium

As at 1 January 2012, the share capital of the Company comprised of 3,065,725 authorised and fully paid ordinary shares all with par value of RUB 1,000 each. The structure of shareholding is as follows: JSC “Sukhoi Design Bureau”: 3.01%, JSC “Aviation Holding Company “Sukhoi”: 71.99% and World Wings S.A.: 25% plus one share.

Additional paid-in capital

Additional paid-in capital in the amount of USD 55,362 thousand represents a fair value adjustment relating to zero-interest loans received from JSC “United Aircraft Corporation” and JSC “Sukhoi OKB” (of which USD 3,568 thousand was received from JSC “United Aircraft Corporation” in 2010 and USD 51,794 thousand received from JSC “United Aircraft Corporation” and JSC “Sukhoi OKB” in 2011).

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

26

Distributable profit

In accordance with Russian legislation the Company’s distributable reserves are limited to the balance of accumulated retained earnings as recorded in the Company’s statutory financial statements prepared in accordance with Russian Accounting Principles.

As at 31 December 2012 the Company had cumulative losses and, therefore, no profits available for distribution (2011: nil).

Dividends

No dividends were declared for the year ended 31 December 2012 and 2011.

Note 15. Loans and borrowings

This note provides information about the contractual terms of the Company’s loans and borrowings, which are measured at amortised cost. For more information about the Company’s exposure to interest rate, foreign currency and liquidity risk, see note 22.

Non-current

2012 000'USD

2011 000'USD

(restated)*

Secured bank loans 797,149 301,535

Unsecured bank loans 109,111 125,520

Secured loans from companies - 2,355

Unsecured loans from related parties 219,564 347,522

Unsecured bond issues - 93,943

Finance lease liabilities 870 2,090

Total 1,126,694 872,965

Current

2012 000'USD

2011 000'USD

(restated)*

Secured bank loans 526,901 440,761

Unsecured bank loans 40,123 33,620

Secured loans from companies 3,202 1,180

Unsecured loans from related parties 198,605 -

Secured bond issues 54,497 8,414

Unsecured bond issues 166,711 107,442

Finance lease liabilities 1,230 2,506

Total 991,269 593,923

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

27

Terms and debt repayment schedule

Effective

interest rate,%Year of

maturity

2012 000'USD

2011 000'USD

(restated)*

Secured bank loans

GBP 11.20%-11.83% 2013-2020 16,254 12,174

US dollars Libor+4% 2013-2018 85,642 99,846

US dollars 6.21% 2014 191,668 -

US dollars Libor+5.5% 2013 50,509 50,261

US dollars Libor+5.0% 2012 - 70,787

US dollars** Libor+3%-6% 2013-2014 66,501 92,587

US dollars 5.85%-8.62% 2013 204,297 -

US dollars 8.33% 2015-2024 422,304 -

US dollars 7.34% 2013-2027 67,409 -

EUR 8.37%-8.53% 2013 5,101 9,846

EUR 6.35%-8.34% 2013-2018 38,081 48,907

EUR Euribor+6.5% 2013-2017 100,611 119,004

RUB 7.16%-9.5% 2012 - 238,884

RUB 9.36% 2013 55,888 -

RUB 9.93% 2017 19,785 -

Unsecured bank loans:

US dollars 5.49% 2012 - 6,590

GBP 11.27% 2013-2020 7,467 8,154

EUR** Euribor+0.9%-

7% 2013-2016 104,437 123,374

US dollars** Libor+8.5 2013-2016 37,330 21,022

Secured bond issues

Note A RUB 7.23%-8.50% 2013 54,497 8,414

Unsecured bonds issues

Note B RUB 8.42%-9.28% 2013 166,711 201,385

Finance lease liabilities:

RUB 18.66%-19.68% 2012 - 429

US dollars 17.15% 2013-2015 1,679 2,534

EUR 9.08% 2013 421 1,633

Loans from related parties

RUB 4.78%-10% 2013-2020 317,984 292,474

US dollars Libor+5.2 2013-2014 100,185 55,048

Other loans

US dollars 2.67%-3.06% 2013 3,202 3,535

Total 2,117,963 1,466,888

* See Note 4 ** See Note C

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

28

Finance leases repayment schedule:

At 31 December 2012 000'USD Minimum

lease payments Interest Principal

During the first year 1,443 213 1,230

During the second year 879 76 803

During the third year 68 1 67

Total 2,390 290 2,100

At 31 December 2011 000'USD Minimum

lease payments Interest Principal

During the first year 2,962 456 2,506

During the second year 1,434 213 1,221

During the third year 945 76 869

Total 5,341 745 4,596

The finance lease liabilities are secured by the leased assets (refer Note 7).

Pledges

Loans are secured with property, plant and equipment with a carrying amount of USD 11,209 thousand (31 December 2011: USD 2,500 thousand), and inventory with a carrying amount of USD 12,167 thousand (31 December 2011: USD 3,751 thousand). The assets related to the net investment in financial leases with a carrying amount of USD 19,032 thousand are also pledged (31 December 2011: USD 17,604 thousand).

Bonds (Note A)

In March 2007, the Company issued 5,000,000 non-convertible rouble-denominated bonds with the face value of 1,000 roubles maturing in March 2017 with twenty coupons payable semi-annually.

In accordance with the terms of the issue starting from September 2009 the Company must annually offer to redeem the bonds upon determination of the new coupon rate.

In September 2012 the Board of Directors approved the new coupon rate of 8.00% p.a. for the twelfth and thirteenth coupon period. In September 2012 the Company redeemed 780,091 bonds.

The next offer in respect of non-convertible rouble-denominated bonds shall be made in September 2013.

As at 31 December 2012 2,264,814 bonds were sold under REPO and buy-sell agreements with the face value of 1,000 roubles per 1 bond.

Stock bonds (Note B)

In December 2010 the Company announced an issue of 9,000,000 non-convertible rouble-denominated stock bonds (series BO-01, BO-02 and BO-03: 3,000,000 bonds each), with the face value of 1,000 roubles. The issue was planned to be exercised in three stages.

In December 2010 the Company issued 3,000,000 series BO-01 bonds maturing in December 2013. In accordance with the terms of issue the Company must annually offer to redeem the bonds upon determination of the new coupon rate. In December 2012 the Company redeemed 403,384 bonds with coupon rate of 8.25% p.a. approved by the Board of Directors for the fifth and sixth coupon periods. The bond of series BO-01 shall be fully paid off in December 2013. As at 31 December 2012 1,105,000 bonds of series BO-01 were sold under REPO with the face value of 1,000 roubles per 1 bond.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

29

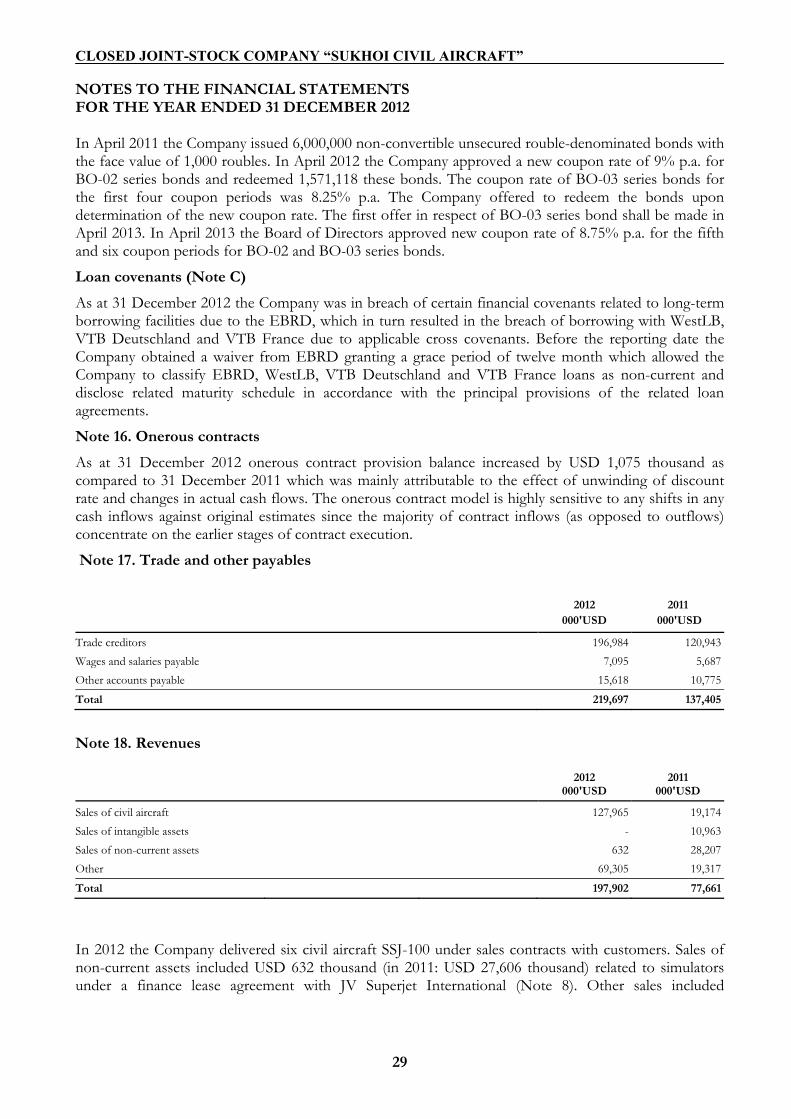

In April 2011 the Company issued 6,000,000 non-convertible unsecured rouble-denominated bonds with the face value of 1,000 roubles. In April 2012 the Company approved a new coupon rate of 9% p.a. for BO-02 series bonds and redeemed 1,571,118 these bonds. The coupon rate of BO-03 series bonds for the first four coupon periods was 8.25% p.a. The Company offered to redeem the bonds upon determination of the new coupon rate. The first offer in respect of BO-03 series bond shall be made in April 2013. In April 2013 the Board of Directors approved new coupon rate of 8.75% p.a. for the fifth and six coupon periods for BO-02 and BO-03 series bonds.

Loan covenants (Note C)

As at 31 December 2012 the Company was in breach of certain financial covenants related to long-term borrowing facilities due to the EBRD, which in turn resulted in the breach of borrowing with WestLB, VTB Deutschland and VTB France due to applicable cross covenants. Before the reporting date the Company obtained a waiver from EBRD granting a grace period of twelve month which allowed the Company to classify EBRD, WestLB, VTB Deutschland and VTB France loans as non-current and disclose related maturity schedule in accordance with the principal provisions of the related loan agreements.

Note 16. Onerous contracts

As at 31 December 2012 onerous contract provision balance increased by USD 1,075 thousand as compared to 31 December 2011 which was mainly attributable to the effect of unwinding of discount rate and changes in actual cash flows. The onerous contract model is highly sensitive to any shifts in any cash inflows against original estimates since the majority of contract inflows (as opposed to outflows) concentrate on the earlier stages of contract execution.

Note 17. Trade and other payables

2012

000'USD 2011

000'USD

Trade creditors 196,984 120,943

Wages and salaries payable 7,095 5,687

Other accounts payable 15,618 10,775

Total 219,697 137,405

Note 18. Revenues

2012

000'USD 2011

000'USD

Sales of civil aircraft 127,965 19,174

Sales of intangible assets - 10,963

Sales of non-current assets 632 28,207

Other 69,305 19,317

Total 197,902 77,661

In 2012 the Company delivered six civil aircraft SSJ-100 under sales contracts with customers. Sales of non-current assets included USD 632 thousand (in 2011: USD 27,606 thousand) related to simulators under a finance lease agreement with JV Superjet International (Note 8). Other sales included

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

30

USD 47,546 thousand (in 2011: 15,347 thousand) related to engineering services rendered to the entities under common control (UAC Group).

Note 19. Government grants

The Company’s activity on development of the “Sukhoi Super Jet – 100” aircraft is included in the Federal Target Program “Development of the civil aircraft for 2002-2012 and for the period until 2015” approved by the Decision of the Federal Government of the Russian Federation No. 728 dated 15 October 2001. In accordance with this program, the Company receives financing from the Federal Government. Funds were received under the contract with Ministry of Industry and Trade (Minpromtorg) and Joint Stock Company “United Aircraft Corporation”(JSC “UAC”) which is structured as a contract for the development services, and as contract to cover certain types of expenses. In 2012 the Company received government grant for interest expense compensation. The summary of government grants received by the Company is presented below.

2012 000'USD

2011 000'USD

Grants related to development costs - 708

Total government grants related to assets - 708

Total grants related to income 1,255 653

Total grants related to income received during the year 1,255 653

Total 1,255 1,361

Note 20. Administrative expenses

2012

000'USD 2011

000'USD

Wages and unified social tax 28,975 26,690

Rent 5,813 7,317

Other expenses 20,542 18,277

Total 55,330 52,284

Note 21. Income taxes

The Company’s applicable tax rate is the Russian Federation corporate income tax rate of 20%.

Reconciliation of effective tax rate:

2012

000'USD 2011

000'USD Deferred tax - origination and reversal of temporary differences 21,139 32,994 Deferred income tax benefit 21,139 32,994

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

31

Income tax (expense)/benefit

2012

000'USD %2011

000'USD %

Loss before tax (132,386) 100 (204,491) 100

Theoretical income tax (expense)/benefit at the statutory tax rate 26,477 20 40,898 20

Tax effect of non-deductible expenses (5,338) (4) (7,904) (4)

Total income tax (expense)/benefit 21,139 16 32,994 16

Note 22. Financial instruments

Exposure to credit, interest rate and currency risk arises in the normal course of the Company’s business. The Company does not hedge its exposure to such risk.

Credit risk

Credit risk is the risk of financial loss to the Company if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from related parties receivables from customers and investment securities.

The maximum exposure to credit risk is represented by the carrying amount of financial assets. Maximum exposure to credit risk at the reporting date was as follows:

Note 2012

'000USD 2011

'000USD

Trade receivables 12 138,931 32,429

Other receivables 9,12 121,694 57,861

Net investment in finance lease 8 26,832 26,679

Cash and cash equivalents 13 182,458 17,691

Total 469,915 134,660

Liquidity risk

The Company’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Company’s reputation.

The table below analyses the Company’s financial liabilities into relevant maturity Company’s based on the remaining period from the reporting date to the contractual maturity date, based on the contractual undiscounted cash flows including estimated interest payments.

2012 000'USD

Carrying amount

Contractual cash flows

6 months or less

6 – 12 months

1 – 2 years

2 – 5 years

More than

5 years

Bank and other loans 1,894,655 2,281,002 341,819 492,348 369,119 482,256 595,460

Bond issue 54,497 59,983 19,800 40,183 - - -

Unsecured bond issue 166,711 170,802 170,321 481 - - -

Finance lease 2,100 2,390 879 564 879 68 - Trade and other payables 229,307 237,405 113,124 115,981 4,245 4,055 -

Total 2,347,270 2,751,582 645,943 649,557 374,243 486,379 595,460

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

32

2011 000'USD

Carrying amount

Contractual cash flows

6 months or less 6 – 12 months

1 – 2 years

2 – 5 years

More than

5 years

Bank and other loans 1,252,493 1,458,843 208,070 334,053 357,952 376,550 182,218

Bond issue 8,414 8,840 288 8,552 - - -

Unsecured bond issue 201,385 215,415 101,072 17,331 97,012 - -

Finance lease 4,596 5,341 1,612 1,350 1,434 945 - Trade and other payables 142,405 152,328 71,396 69,000 5,030 6,901 -

Total 1,609,293 1,840,767 382,438 430,286 461,428 384,396 182,218

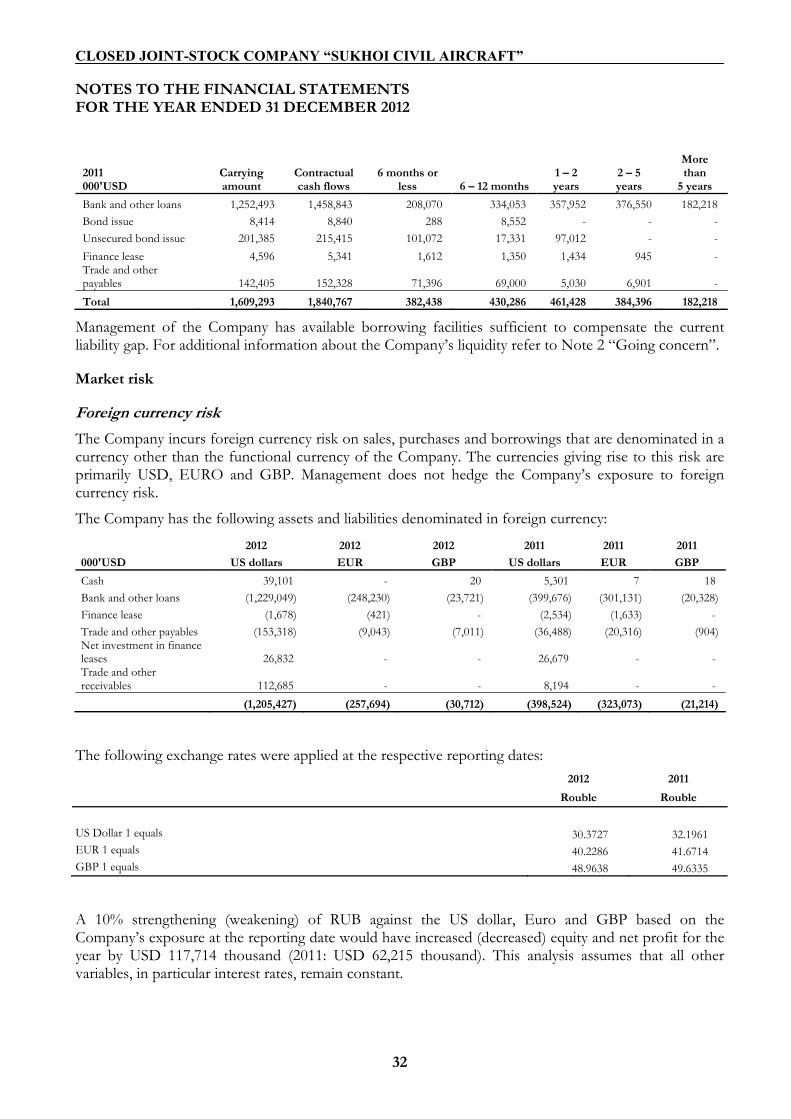

Management of the Company has available borrowing facilities sufficient to compensate the current liability gap. For additional information about the Company’s liquidity refer to Note 2 “Going concern”.

Market risk

Foreign currency risk

The Company incurs foreign currency risk on sales, purchases and borrowings that are denominated in a currency other than the functional currency of the Company. The currencies giving rise to this risk are primarily USD, EURO and GBP. Management does not hedge the Company’s exposure to foreign currency risk.

The Company has the following assets and liabilities denominated in foreign currency:

2012 2012 2012 2011 2011 2011

000'USD US dollars EUR GBP US dollars EUR GBP

Cash 39,101 - 20 5,301 7 18

Bank and other loans (1,229,049) (248,230) (23,721) (399,676) (301,131) (20,328)

Finance lease (1,678) (421) - (2,534) (1,633) -

Trade and other payables (153,318) (9,043) (7,011) (36,488) (20,316) (904)Net investment in finance leases 26,832 - - 26,679 - - Trade and other receivables 112,685 - - 8,194 - -

(1,205,427) (257,694) (30,712) (398,524) (323,073) (21,214)

The following exchange rates were applied at the respective reporting dates:

2012 2011

Rouble Rouble

US Dollar 1 equals 30.3727 32.1961 EUR 1 equals 40.2286 41.6714 GBP 1 equals 48.9638 49.6335

A 10% strengthening (weakening) of RUB against the US dollar, Euro and GBP based on the Company’s exposure at the reporting date would have increased (decreased) equity and net profit for the year by USD 117,714 thousand (2011: USD 62,215 thousand). This analysis assumes that all other variables, in particular interest rates, remain constant.

CLOSED JOINT-STOCK COMPANY “SUKHOI CIVIL AIRCRAFT” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2012

33

Interest rate risk

At the reporting date the interest rate profile of the Company’s interest bearing financial instruments was:

2012

000'USD 2011

000'USD

Fixed rate instruments

Cash equivalents 182,458 17,691

Bank and other loans (1,570,648) (830,365)