Embed Size (px)

Citation preview

Financial statements and ratiosFinancial statements and ratios

PreamblePreamble

The overview of Financial Statements reveals information about past and current performance of the firm.

When combining this information with other sources, we might be able to form expectations about the firm’s future cash flows.

OutlineOutline

• The Balance Sheet

• The Income Statement

• The Statement of Cash Flows

• On ratio analysis

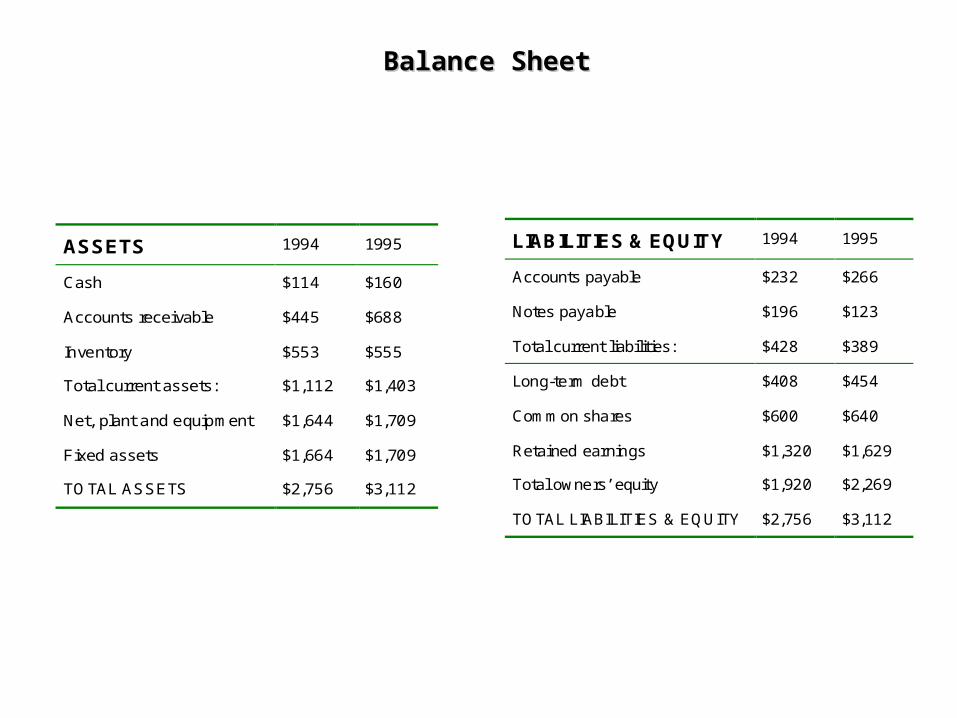

Balance SheetBalance Sheet

Financial Statement showing a firm’s accounting value on a particular date.

Balance SheetBalance Sheet

ASSETS 1994 1995

Cash

Accounts receivable

Inventory

Total current assets:

$114

$445

$553

$1,112

$160

$688

$555

$1,403

Net, plant and equipment

Fixed assets

$1,644

$1,664

$1,709

$1,709

TOTAL ASSETS $2,756 $3,112

LIABILITIES & EQUITY 1994 1995

Accounts payable

Notes payable

Total current liabilities:

$232

$196

$428

$266

$123

$389

Long-term debt $408 $454

Common shares

Retained earnings

Total owners’ equity

$600

$1,320

$1,920

$640

$1,629

$2,269

TOTAL LIABILITIES & EQUITY $2,756 $3,112

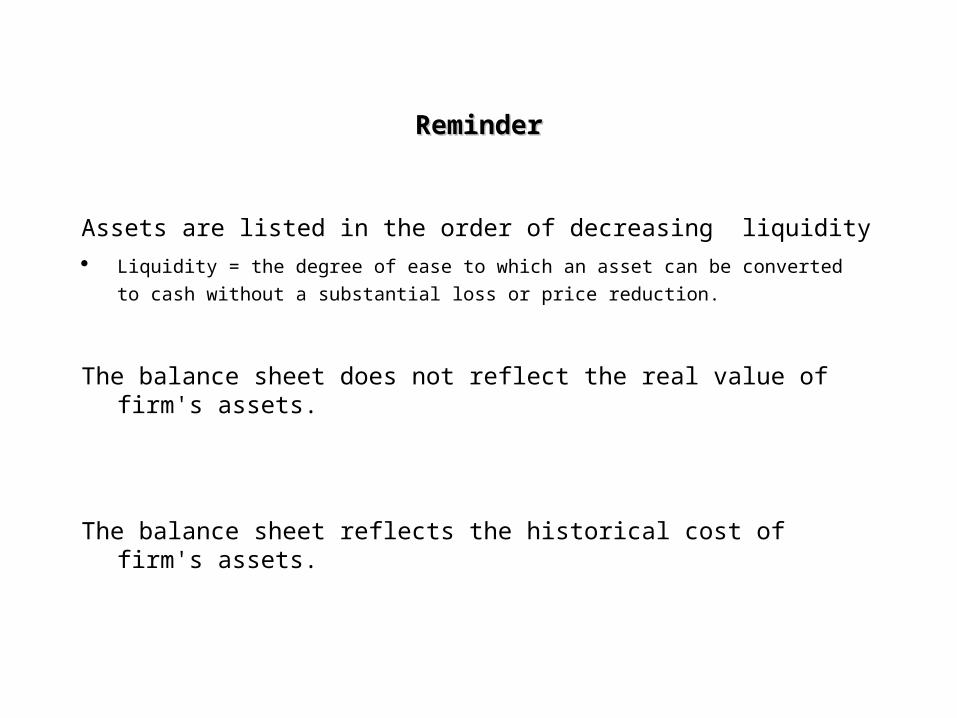

ReminderReminder

Assets are listed in the order of decreasing liquidity

Liquidity = the degree of ease to which an asset can be converted to cash without a

substantial loss or price reduction.

The balance sheet does not reflect the real value of firm's assets.

The balance sheet reflects the historical cost of firm's assets.

The Income StatementThe Income Statement

Reveals how profitable the firm is over a certain period of time.

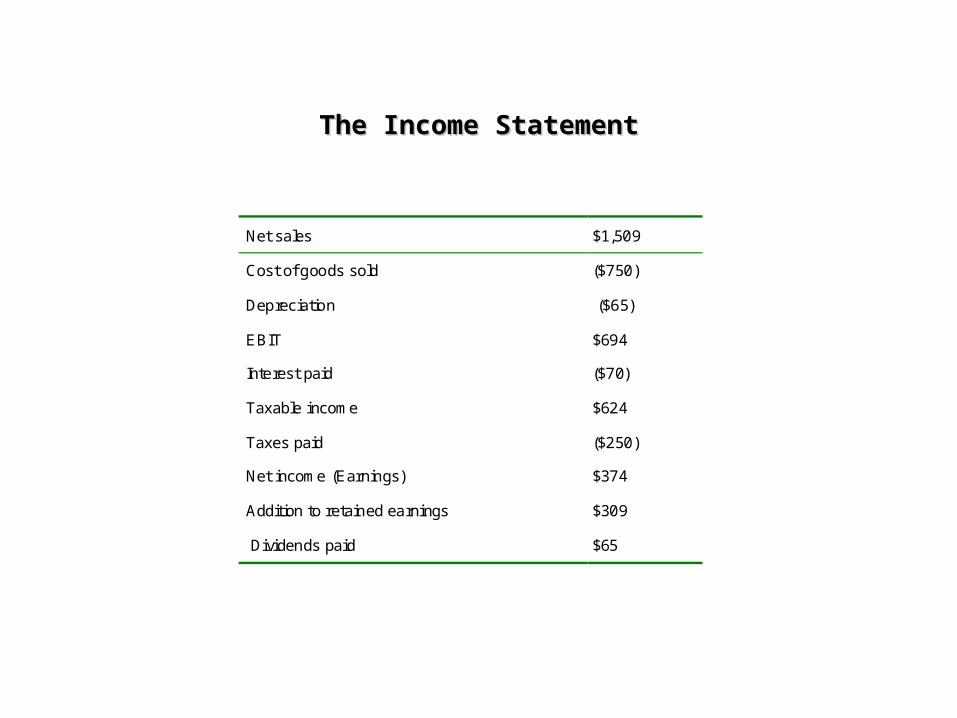

The Income StatementThe Income Statement

Net sales $1,509

Cost of goods sold ($750)

Depreciation ($65)

EBIT $694

Interest paid ($70)

Taxable income $624

Taxes paid ($250)

Net income (Earnings) $374

Addition to retained earnings $309

Dividends paid $65

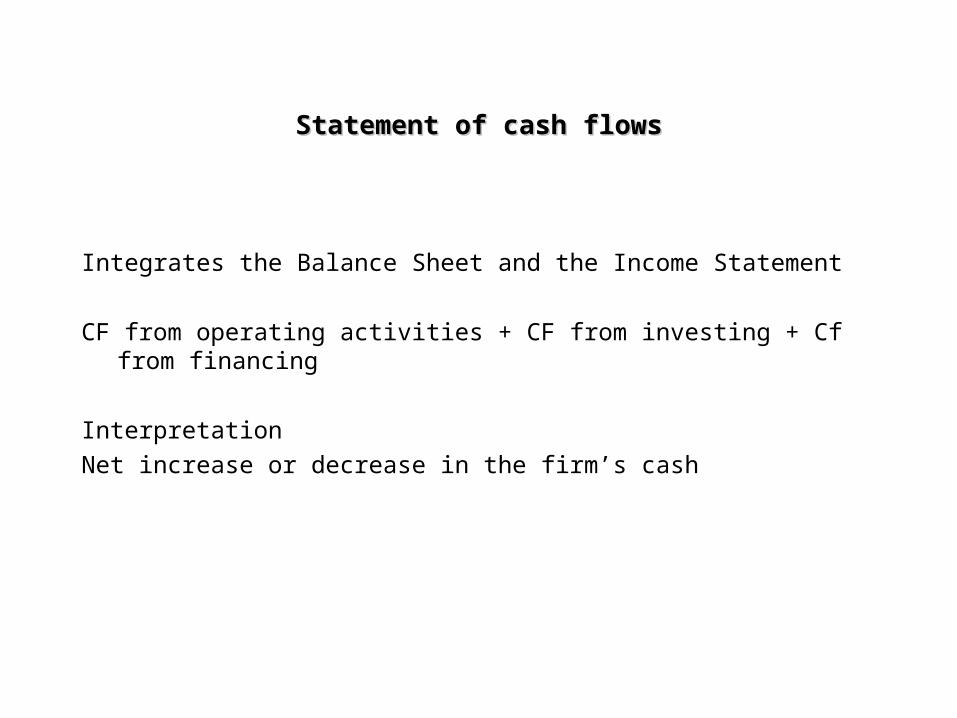

Statement of cash flowsStatement of cash flows

Integrates the Balance Sheet and the Income Statement

CF from operating activities + CF from investing + Cf from financing

Interpretation

Net increase or decrease in the firm’s cash

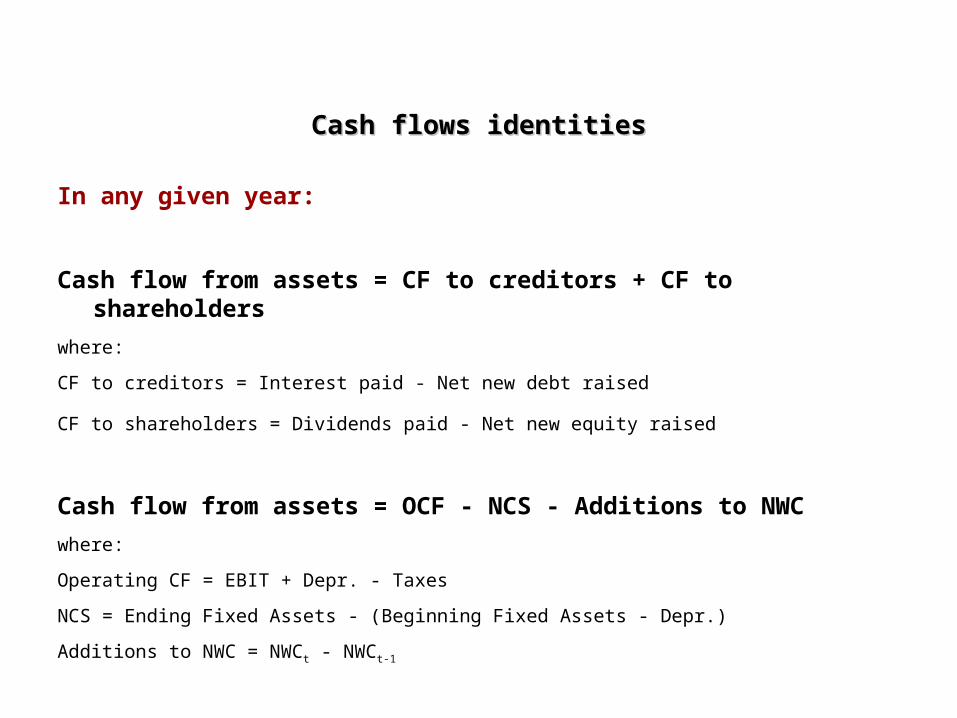

Cash flows identitiesCash flows identities

In any given year:

Cash flow from assets = CF to creditors + CF to shareholders

where:

CF to creditors = Interest paid - Net new debt raised

CF to shareholders = Dividends paid - Net new equity raised

Cash flow from assets = OCF - NCS - Additions to NWC

where:

Operating CF = EBIT + Depr. - Taxes

NCS = Ending Fixed Assets - (Beginning Fixed Assets - Depr.)

Additions to NWC = NWCt - NWCt-1

Cash flows identitiesCash flows identities

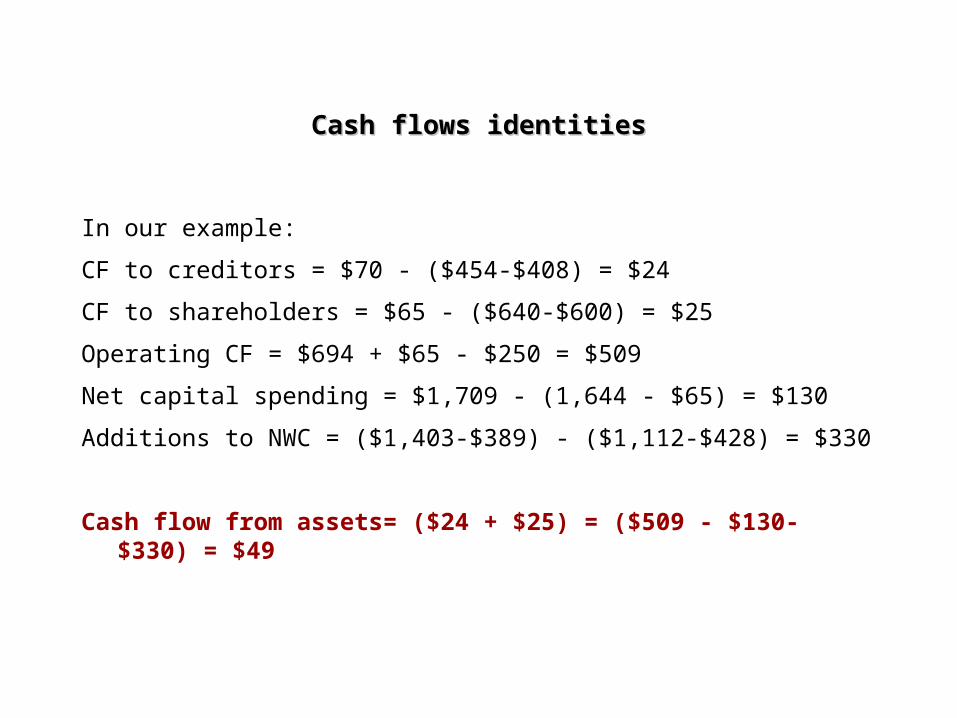

In our example:

CF to creditors = $70 - ($454-$408) = $24

CF to shareholders = $65 - ($640-$600) = $25

Operating CF = $694 + $65 - $250 = $509

Net capital spending = $1,709 - (1,644 - $65) = $130

Additions to NWC = ($1,403-$389) - ($1,112-$428) = $330

Cash flow from assets= ($24 + $25) = ($509 - $130- $330) = $49

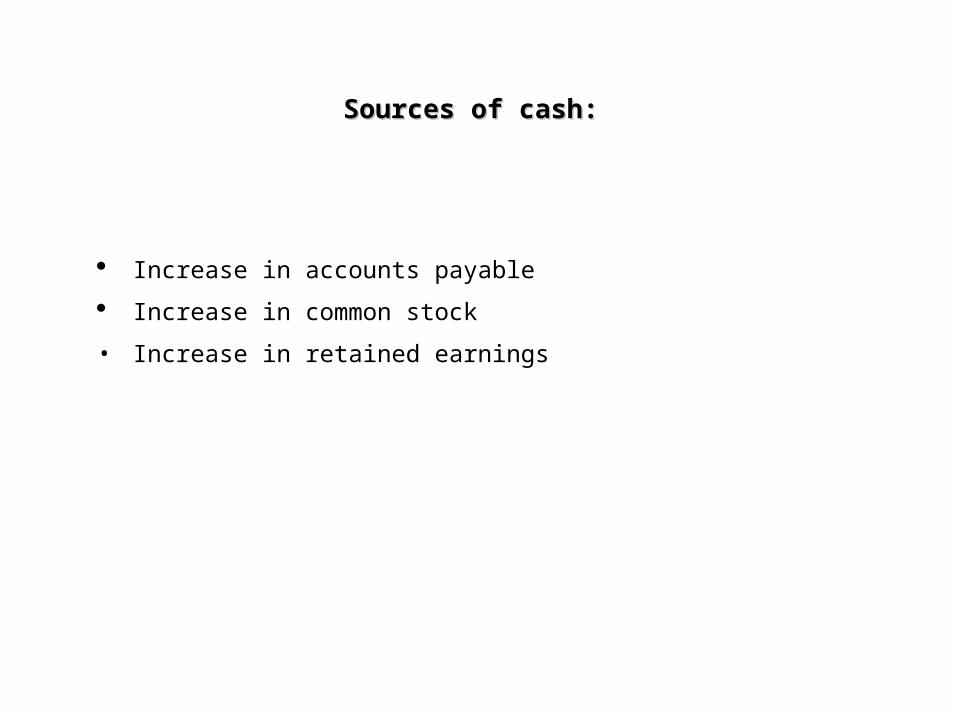

Sources of cash: Sources of cash:

Increase in accounts payable

Increase in common stock

• Increase in retained earnings

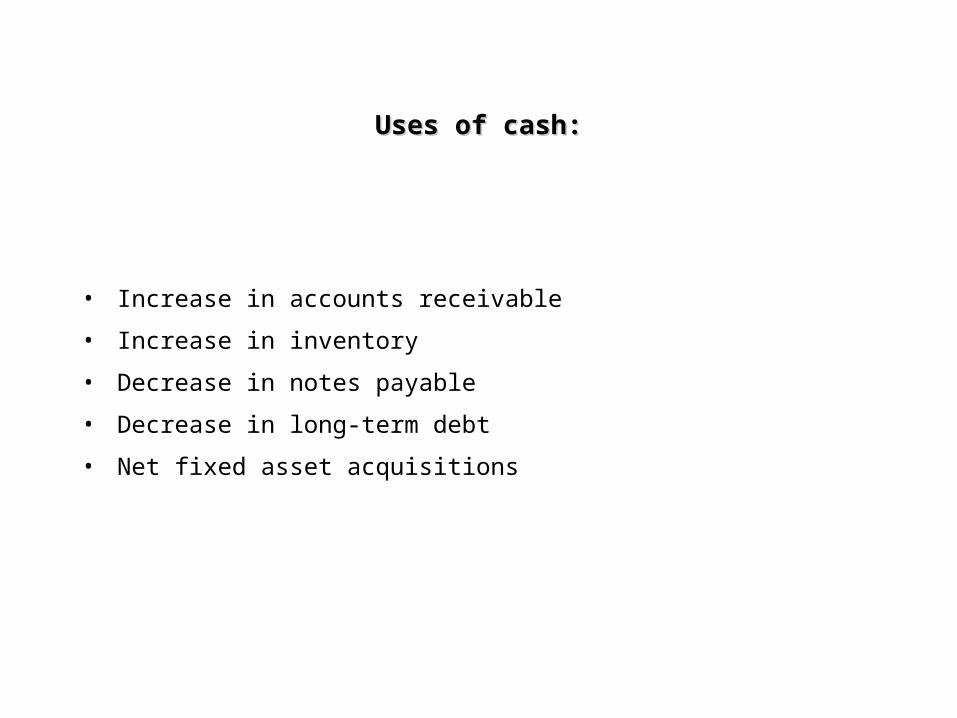

Uses of cash:Uses of cash:

• Increase in accounts receivable

• Increase in inventory

• Decrease in notes payable

• Decrease in long-term debt

• Net fixed asset acquisitions

Ratio analysisRatio analysis

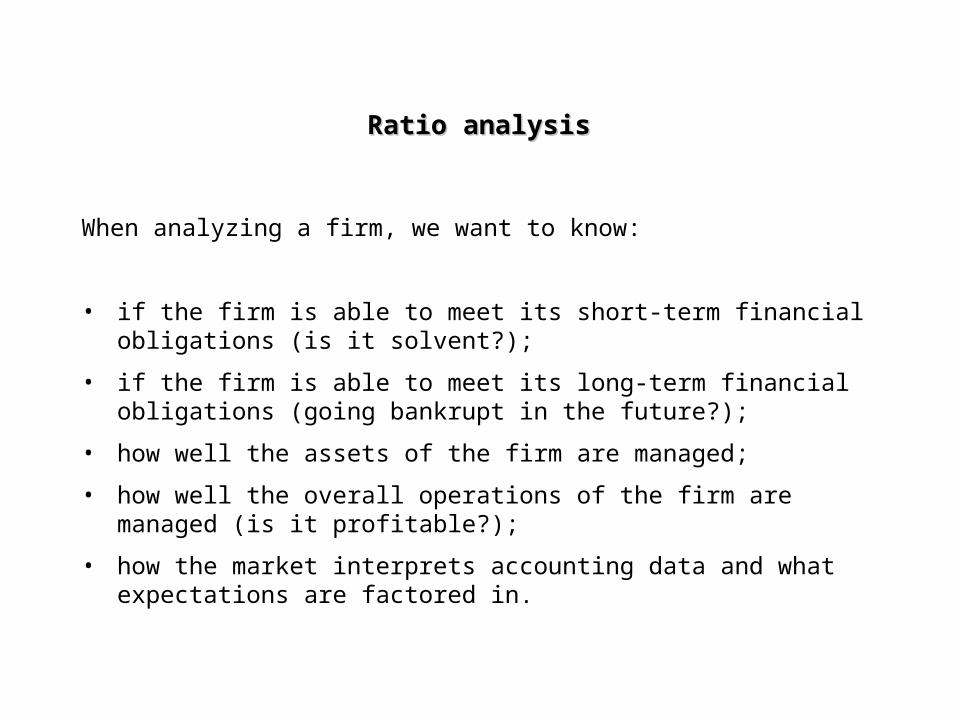

When analyzing a firm, we want to know:

• if the firm is able to meet its short-term financial obligations (is it solvent?);

• if the firm is able to meet its long-term financial obligations (going bankrupt in the future?);

• how well the assets of the firm are managed;

• how well the overall operations of the firm are managed (is it profitable?);

• how the market interprets accounting data and what expectations are factored in.

Ratio analysisRatio analysis

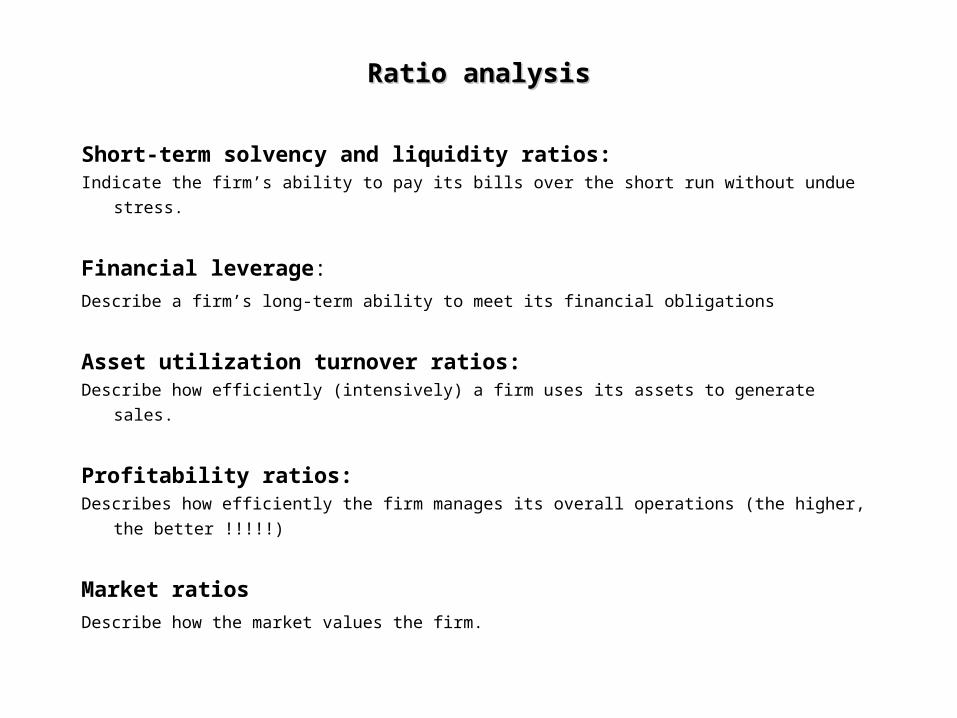

Short-term solvency and liquidity ratios:

Indicate the firm’s ability to pay its bills over the short run without undue stress.

Financial leverage:

Describe a firm’s long-term ability to meet its financial obligations

Asset utilization turnover ratios:

Describe how efficiently (intensively) a firm uses its assets to generate sales.

Profitability ratios:

Describes how efficiently the firm manages its overall operations (the higher, the better !!!!!)

Market ratios

Describe how the market values the firm.

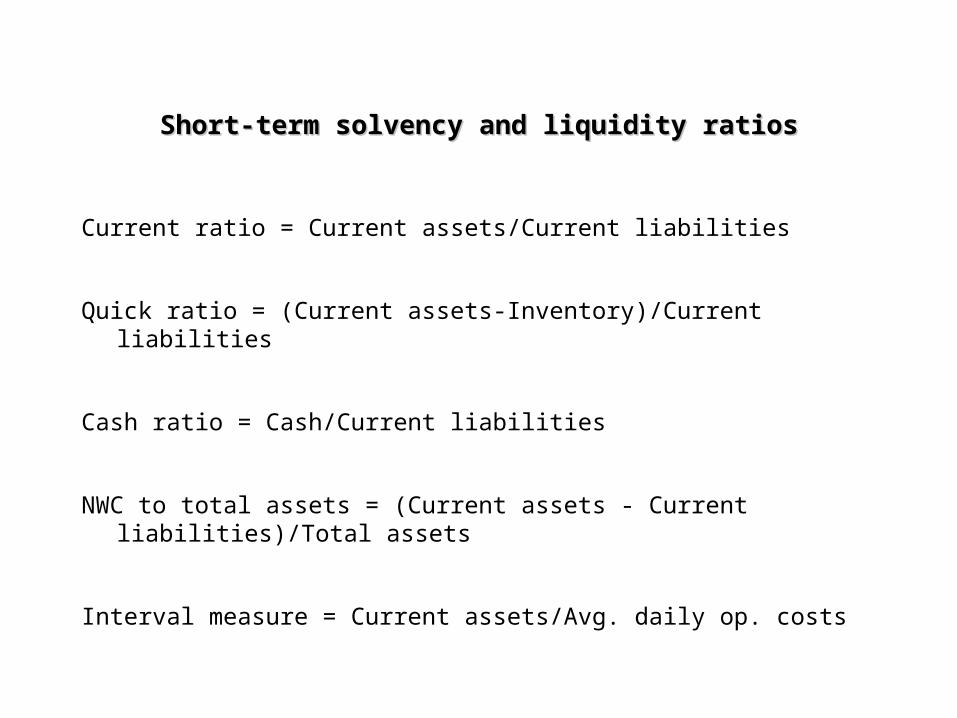

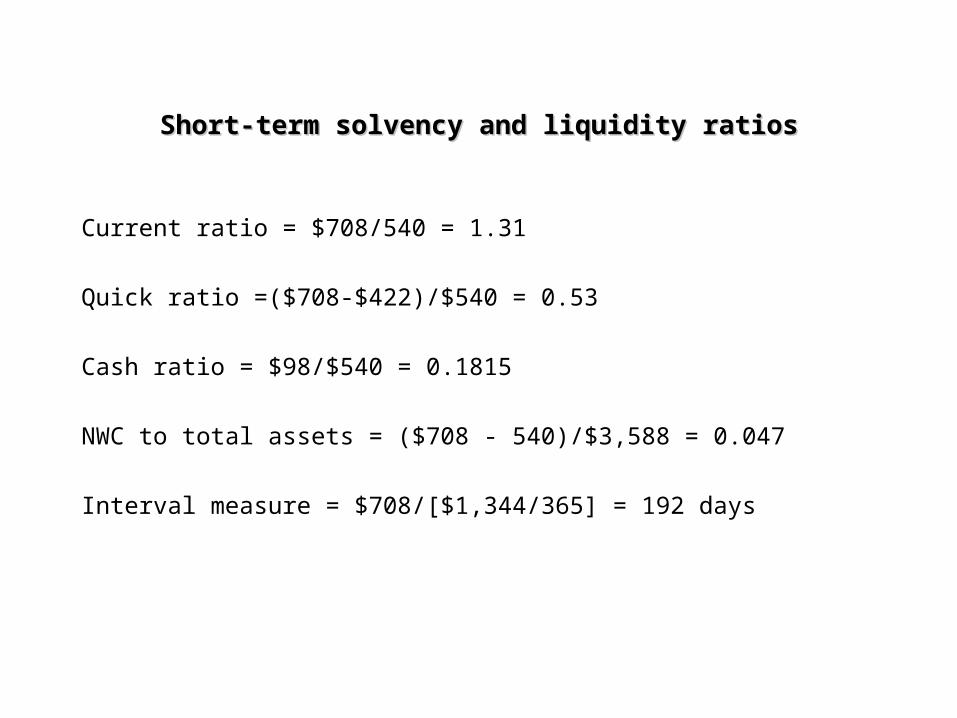

Short-term solvency and liquidity ratiosShort-term solvency and liquidity ratios

Current ratio = Current assets/Current liabilities

Quick ratio = (Current assets-Inventory)/Current liabilities

Cash ratio = Cash/Current liabilities

NWC to total assets = (Current assets - Current liabilities)/Total assets

Interval measure = Current assets/Avg. daily op. costs

Short-term solvency and liquidity ratiosShort-term solvency and liquidity ratios

Current ratio = $708/540 = 1.31

Quick ratio =($708-$422)/$540 = 0.53

Cash ratio = $98/$540 = 0.1815

NWC to total assets = ($708 - 540)/$3,588 = 0.047

Interval measure = $708/[$1,344/365] = 192 days

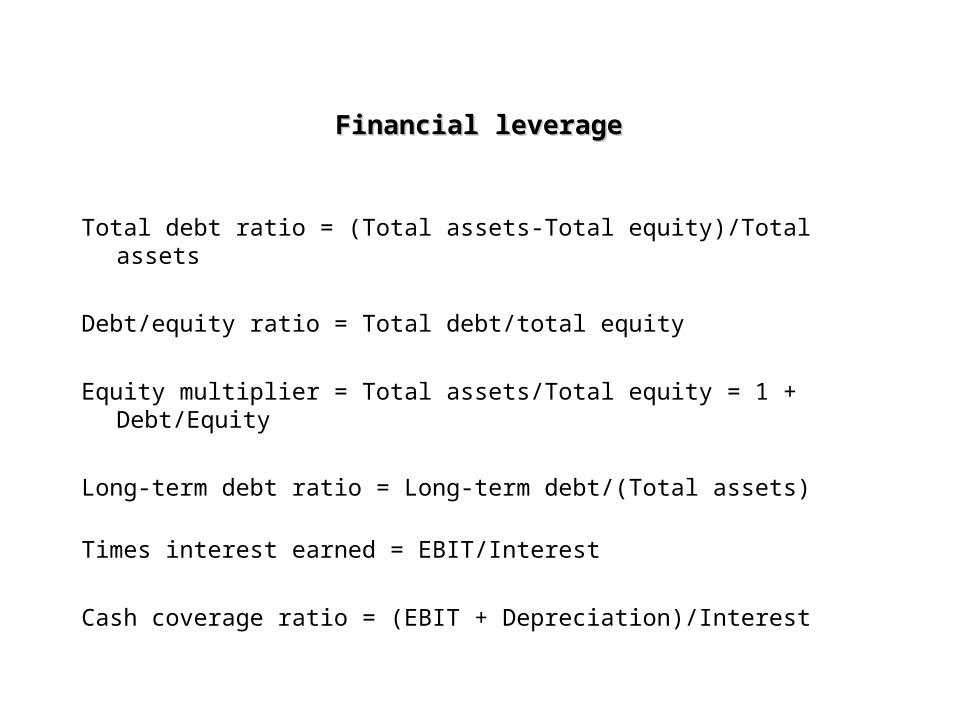

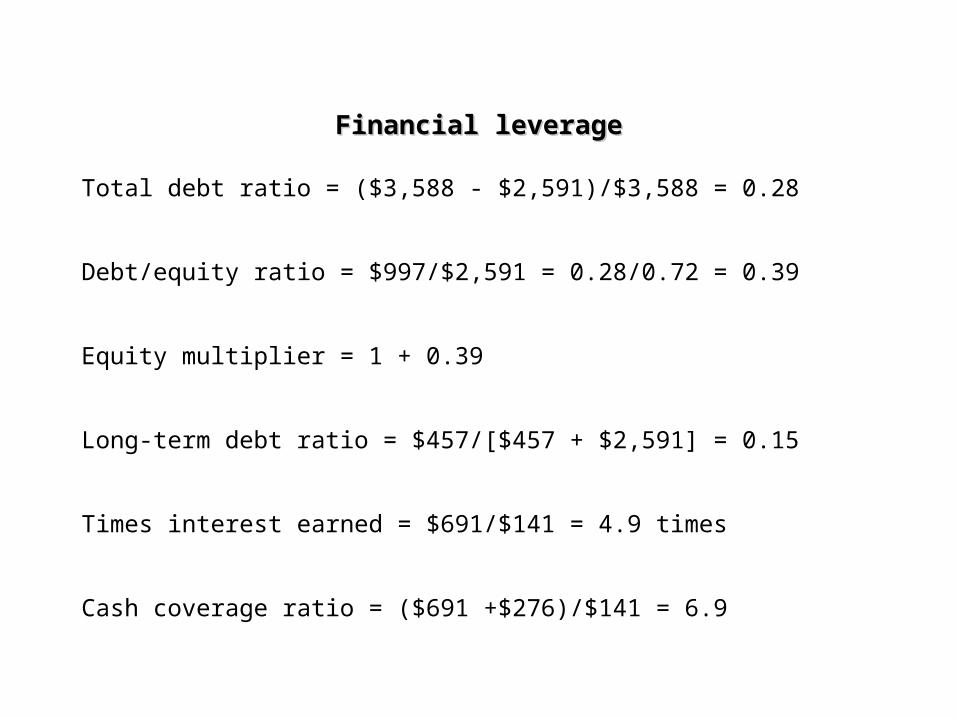

Financial leverageFinancial leverage

Total debt ratio = (Total assets-Total equity)/Total assets

Debt/equity ratio = Total debt/total equity

Equity multiplier = Total assets/Total equity = 1 + Debt/Equity

Long-term debt ratio = Long-term debt/(Total assets)

Times interest earned = EBIT/Interest

Cash coverage ratio = (EBIT + Depreciation)/Interest

Financial leverageFinancial leverage

Total debt ratio = ($3,588 - $2,591)/$3,588 = 0.28

Debt/equity ratio = $997/$2,591 = 0.28/0.72 = 0.39

Equity multiplier = 1 + 0.39

Long-term debt ratio = $457/[$457 + $2,591] = 0.15

Times interest earned = $691/$141 = 4.9 times

Cash coverage ratio = ($691 +$276)/$141 = 6.9

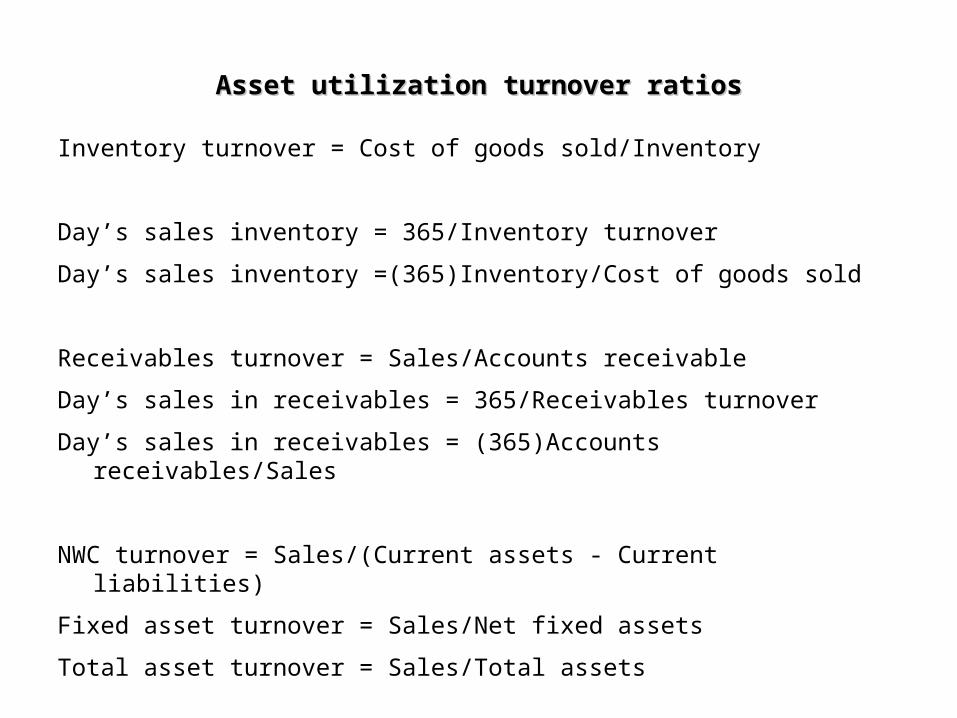

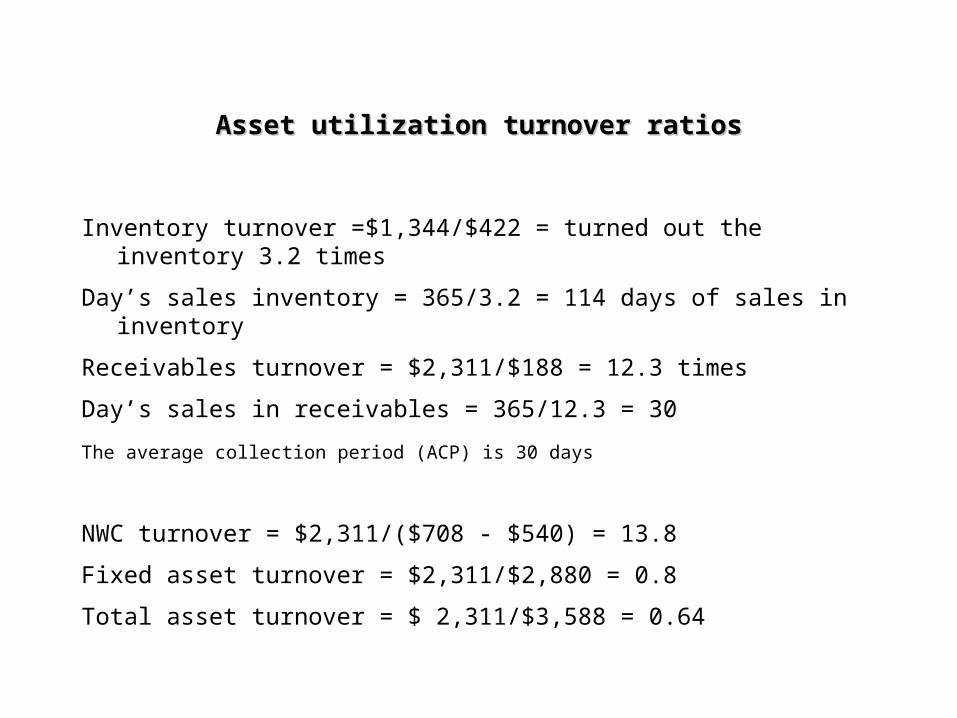

Asset utilization turnover ratiosAsset utilization turnover ratios

Inventory turnover = Cost of goods sold/Inventory

Day’s sales inventory = 365/Inventory turnover

Day’s sales inventory =(365)Inventory/Cost of goods sold

Receivables turnover = Sales/Accounts receivable

Day’s sales in receivables = 365/Receivables turnover

Day’s sales in receivables = (365)Accounts receivables/Sales

NWC turnover = Sales/(Current assets - Current liabilities)

Fixed asset turnover = Sales/Net fixed assets

Total asset turnover = Sales/Total assets

Asset utilization turnover ratiosAsset utilization turnover ratios

Inventory turnover =$1,344/$422 = turned out the inventory 3.2 times

Day’s sales inventory = 365/3.2 = 114 days of sales in inventory

Receivables turnover = $2,311/$188 = 12.3 times

Day’s sales in receivables = 365/12.3 = 30

The average collection period (ACP) is 30 days

NWC turnover = $2,311/($708 - $540) = 13.8

Fixed asset turnover = $2,311/$2,880 = 0.8

Total asset turnover = $ 2,311/$3,588 = 0.64

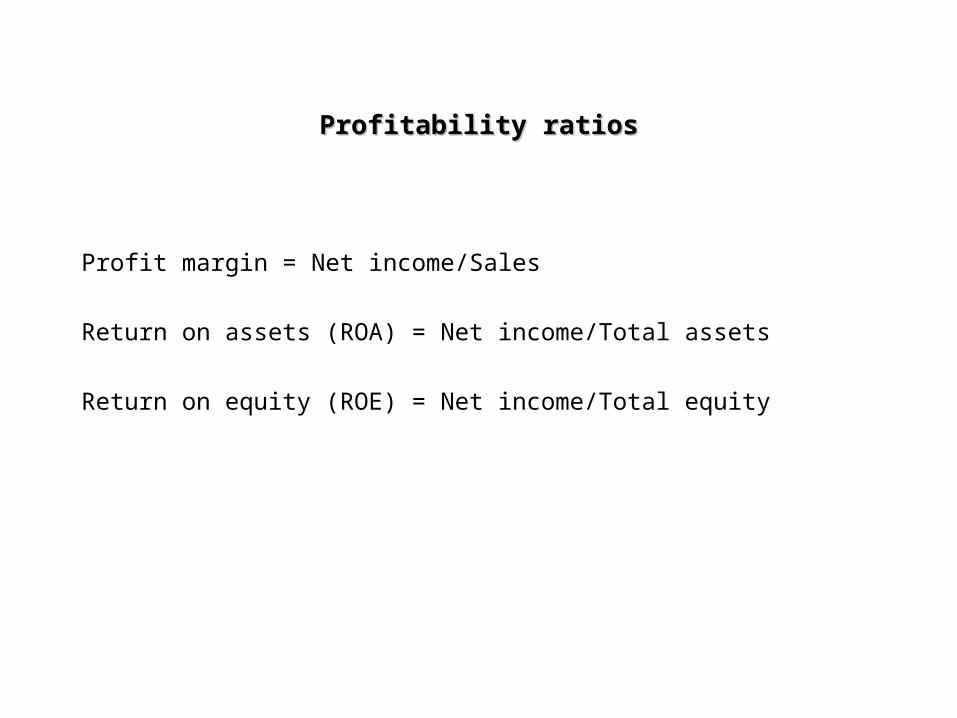

Profitability ratiosProfitability ratios

Profit margin = Net income/Sales

Return on assets (ROA) = Net income/Total assets

Return on equity (ROE) = Net income/Total equity

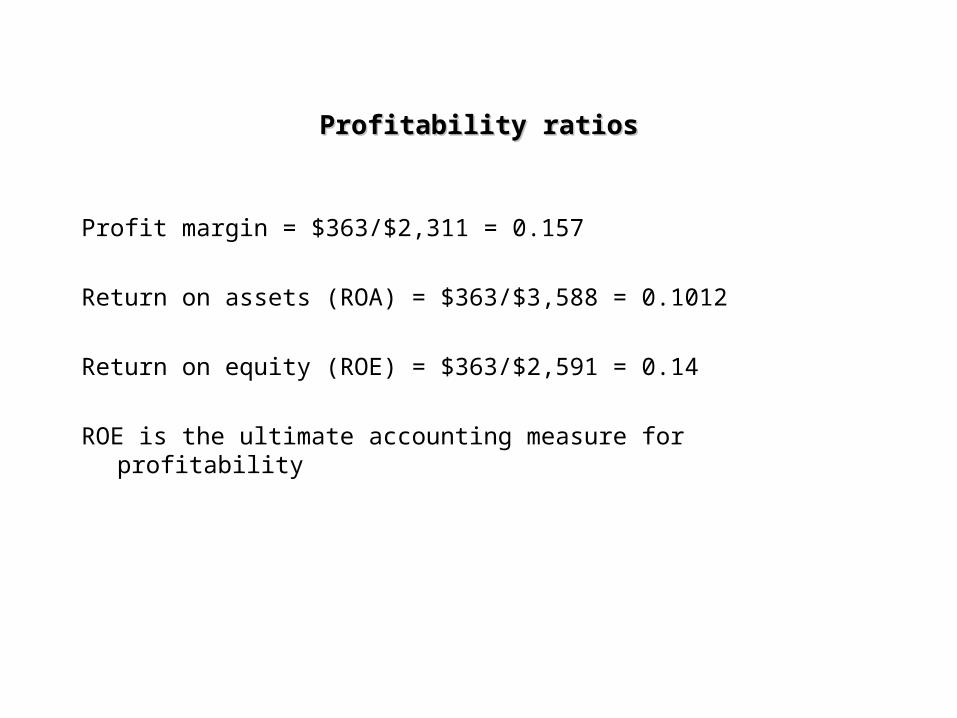

Profitability ratiosProfitability ratios

Profit margin = $363/$2,311 = 0.157

Return on assets (ROA) = $363/$3,588 = 0.1012

Return on equity (ROE) = $363/$2,591 = 0.14

ROE is the ultimate accounting measure for profitability

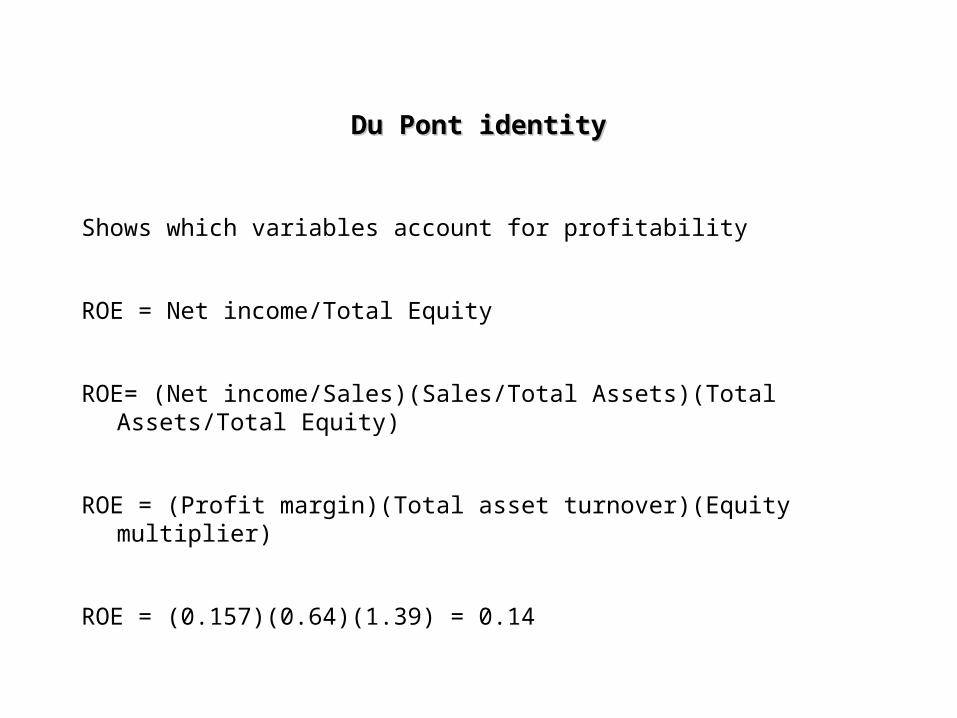

Du Pont identityDu Pont identity

Shows which variables account for profitability

ROE = Net income/Total Equity

ROE= (Net income/Sales)(Sales/Total Assets)(Total Assets/Total Equity)

ROE = (Profit margin)(Total asset turnover)(Equity multiplier)

ROE = (0.157)(0.64)(1.39) = 0.14

Extended DuPont Equality

ROE = NI/E = (EBT/TA)(TA/E)(NI/EBT)

ROE = [EBIT/TA – I/TA](TA/E)(EBT/EBT – Tax/EBT)

ROE = [(EBIT/S)(S/TA) – I/TA](TA/E)(1- Tax/EBT)

ROE = [(Operating margin) (TAT) – Interest expense rate]

(Equity multiplier)

(Tax retention rate)

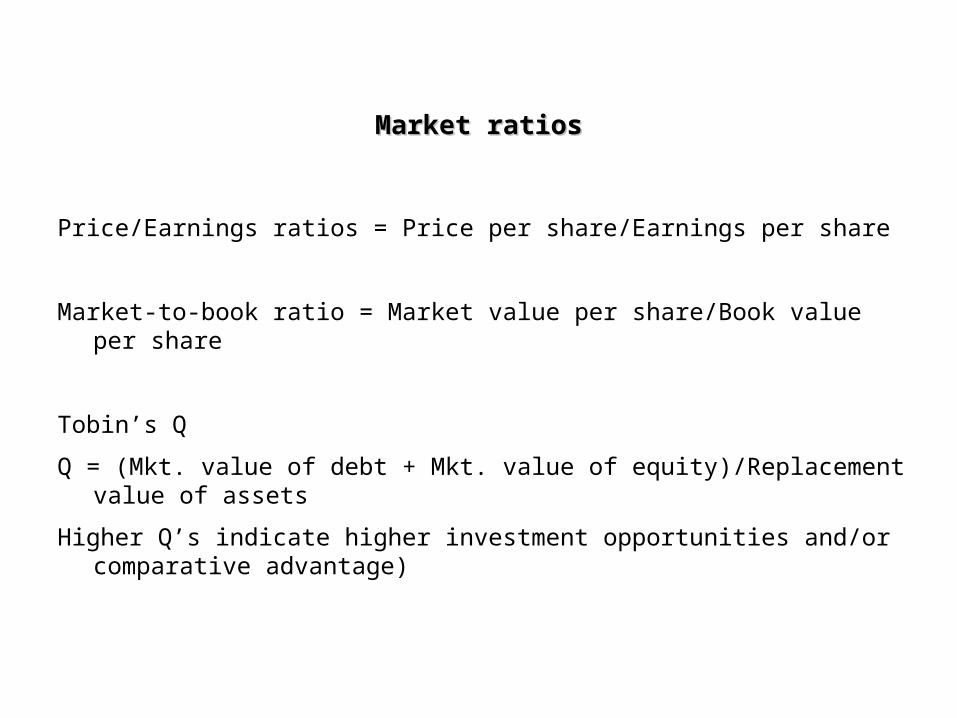

Market ratiosMarket ratios

Price/Earnings ratios = Price per share/Earnings per share

Market-to-book ratio = Market value per share/Book value per share

Tobin’s Q

Q = (Mkt. value of debt + Mkt. value of equity)/Replacement value of assets

Higher Q’s indicate higher investment opportunities and/or comparative advantage)

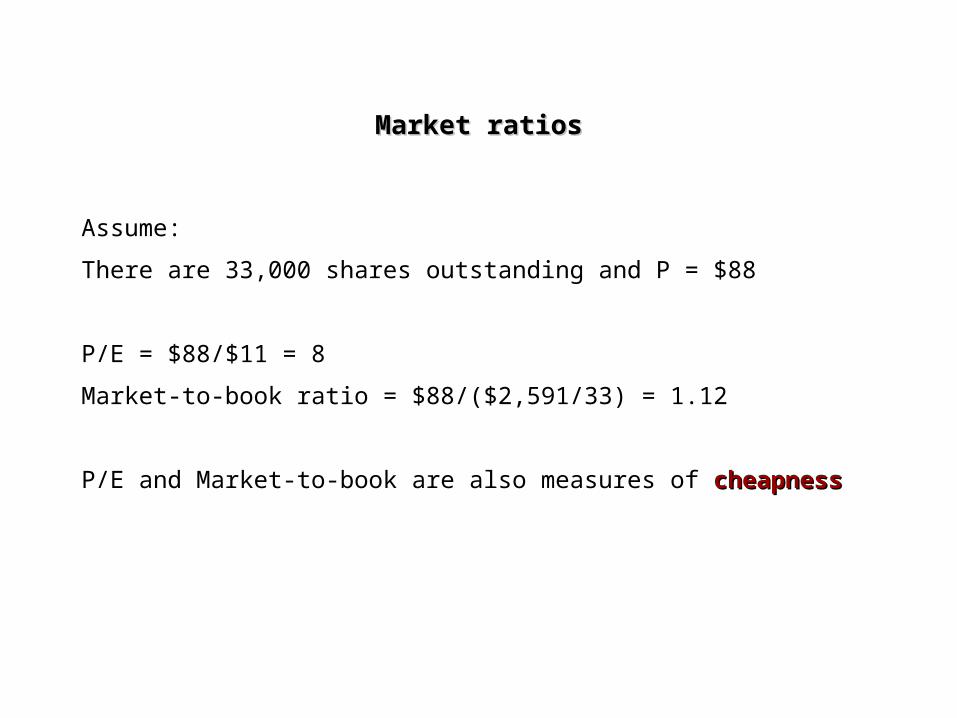

Market ratiosMarket ratios

Assume:

There are 33,000 shares outstanding and P = $88

P/E = $88/$11 = 8

Market-to-book ratio = $88/($2,591/33) = 1.12

P/E and Market-to-book are also measures of cheapnesscheapness