Embed Size (px)

Citation preview

FINANCIAL RESULTS & GROUP UPDATE

FOR SIX MONTHS ENDED 30 JUNE 2017

17 AUGUST 2017

Central, 797,

39%

Southern,

237, 11%

Northern, 42,

2%

Australia,

799, 39%

UK, 131, 6%

Singapore, 48, 2%Vietnam, 19, 1%

SALES PERFORMANCE - PICKING UP MOMENTUM

2

• Sales > halfway mark of RM4.00 billion target

• Sales at 88% more than first half of FY2016

RM2.07 billion

6 months sales for the period ended 30 June 2016

6 months sales for the period ended 30 June 2017

RM1.11 billion

Central, 856,

77%

Southern,

108, 10%

Northern,

26, 2%

Eastern, 6, 1%

UK, 51, 5%

Singapore,

56, 5%Vietnam, 2,

<1%

Malaysia,

1,076, 52%

Internatioanal,

997, 48%Malaysia,

996, 90%

International,

109, 10%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Q1 Q2 Q3 Q4 Q1 Q2 Q3&Q4

2016 2017

Central Southern Northern Eastern International Pipeline

843

1,042

2,208

587

1,946

2,939

MORE LAUNCHES- TO MEET MARKET DEMAND

3

129

RM972 million of launches in

1H FY2016

RM2.53 billion of launches in

1H FY2017

• Sales skewed to second half • Trend of increase launches year-on-year (161%)

Q3 & Q4

FINANCIAL HIGHLIGHTS

4

Profit & Loss (RM million) Q2FY2017 Q2FY20166M YTD

30 June 20176M YTD

30 June 2016

Revenue 795 1,013 1,735 1,922

Gross Profit 214 294 474 555

Profit Before Tax 184 203 358 397

Profit After Tax 155 143 274 283

Profit Attributable to Shareholders 136 126 242 249

Basic Earnings per Share (RM sen) 4.78 4.79 8.46 9.48

Balance Sheet (RM million)As At

30 June 2017As At

31 December 2016

Shareholders’ Funds 9,500 9,201

Total Equity 10,551 10,243

Total Assets 18,504 18,690

Total Cash 3,469 4,170

Total Borrowings 5,736 5,826

Net Gearing Ratio (times) 0.21x 0.16x

Net Assets per share (RM sen) 2.93 2.83

KEY LAUNCHES

DIVERSIFIED PRODUCTS…

6

TOTAL LAUNCHES AS AT 30 JUNE 2017- 4,204 UNITS WITH GDV OF RM2.53 BILLION

459

RM

20m

NORTHGDV

Units

SOUTH

305

RM

167m

GDV

Units

Australia

RM

1.24b

(AUD376m)

GDV

Units

345

VIETNAM

RM

68m

(US19m)

GDV

Units

252

PangsapuriRimbun

Central

2,843

RM

1.03b

GDV

Units

7

KEY LAUNCHES IN SETIA ALAM- OSIRIS & EPLITICA

Osiris : 18 x 65

GDV RM47m

Units 75

Price RM598k onwards

Build up size From 1,735 sq ft

Launch date 18 March 2017

85% Take-Up Rate

Eplitica : 20 x 65

GDV RM49m

Units 72

Price RM659k onwards

Build up size From 1,970 sq ft

Launch date 18 March 2017

100% Take-Up Rate

COMMERCIAL LAUNCHES IN SETIA ECO TEMPLER- THE GROVE : 2 & 3-Storey Shop Office

8

The Grove

GDV RM77m

Units 40

Price RM1.4m onwards

Build up size From 2,996 sq ft

Launch date 9 February 2017

60% Take-Up Rate

TRANSIT ORIENTED DEVELOPMENT- TRIO BY SETIA

9

TRIO by Setia – Block A

GDV RM214m

Units 426

Price RM412k onwards

Build up size From 656 sq ft

Launch date 8 April 2017

71% take-up rate

within 4 weeks of launch

60% Take-Up Rate

Better accessibility and added convenience via the proposed LRT 3.

10

KEY LAUNCHES IN JOHOR- ELONIA AT BUKIT INDAH & ELATA VITA AT SETIA TROPIKA

Elonia : 20 x 70

GDV RM69m

Units 100

Price RM693k onwards

Build up size From 1,770 sq ft

Launch date 21 April 2017

80% Take-Up Rate

Elata Vita : 20 x 65

GDV RM93m

Units 138

Price RM588k onwards

Build up size From 1,880 sq ft

Launch date 3 June 2017

90% Take-Up Rate

11

SAPPHIRE BY THE GARDENS, MELBOURNE- ANCHORED BY SHANGRI-LA HOTEL

• Launched simultaneously inKuala Lumpur, Jakarta, Sydneyand Melbourne on 17th June 2017

• 70% sold within 1 week

• Latest take-up at 74%• Anchored by Shangri-La Hotel

Sapphire By The Gardens

GDV AUD376m

Units 345

Price AUD510k onwards

Build up size From 549 sq ft

Launch date 17 June 2017

12

OVERWHELMING RESPONSE- SAPPHIRE BY THE GARDENS

FOCUS FOR THE REMAINING MONTHS OF

FY2017

MEETING THE MARKET DEMAND AND EXPECTATIONS…

14

PLANNED NEW LAUNCHES IN 2H FY2017- TARGET TO LAUNCH 3,550 UNITS WITH GDV OF RM2.94 BILLION

459

RM

20m

GDV

Units

EASTERN

395

RM

177m

GDV

Units

Australia

RM

111m

(AUD34m)

GDV

Units

47

RM

12m

(US3m)

GDV

Units

28

Central

2,545

RM

2.47b

GDV

Units

SOUTH

535

RM

165m

GDV

Units

Vietnam

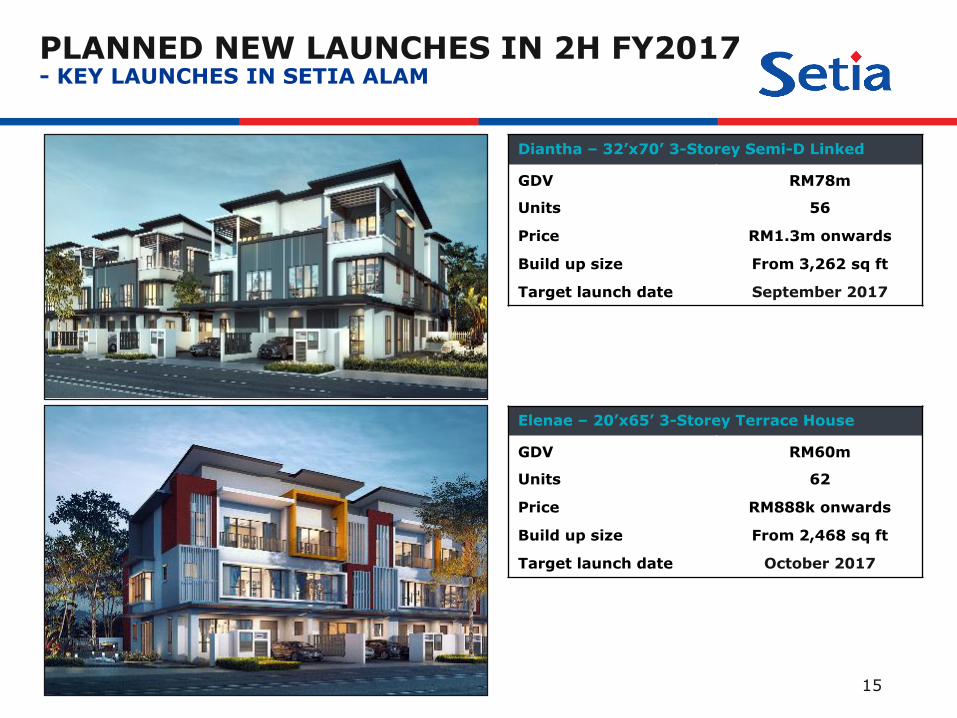

PLANNED NEW LAUNCHES IN 2H FY2017- KEY LAUNCHES IN SETIA ALAM

Diantha – 32’x70’ 3-Storey Semi-D Linked

GDV RM78m

Units 56

Price RM1.3m onwards

Build up size From 3,262 sq ft

Target launch date September 2017

Elenae – 20’x65’ 3-Storey Terrace House

GDV RM60m

Units 62

Price RM888k onwards

Build up size From 2,468 sq ft

Target launch date October 2017

15

PLANNED NEW LAUNCHES IN 2H FY2017- KEY LAUNCHES IN SETIA ALAM

Rimba Villa Phase 132’ x 75’ 2-Storey Semi-D Linked

GDV RM259m

Units 174

Price RM1.45m onwards

Build up size From 2,653 sq ft

Targeted launch date September 2017

16

PLANNED NEW LAUNCHES IN 2H FY2017- KEY LAUNCHES IN SETIA ECOHILL

GLORIS 24x76

GDV RM65m

Units 77

Price RM848k onwards

Build up size From 2,645 sq ft

Target launch date September 2017

KINGSVILLE 52x90/105

GDV RM104m

Units 75

Price RM1.28m onwards

Build up size From 2,373sq ft

Target launch date October 2017

17

PLANNED NEW LAUNCHES IN 2H FY2017- KEY LAUNCHES IN SETIA ECOHILL 2

ELMERA 32x60

GDV RM64m

Units 92

Price RM693k onwards

Build up size From 2,052 sq ft

Target launch date October 2017

BARRAS 20x70

GDV RM55m

Units 114

Price RM488k onwards

Build up size From 1,600 sq ft

Target launch date November 2017

18

PLANNED NEW LAUNCHES IN 2H FY2017- KEY LAUNCHES IN SETIA ECO PARK

Phase 16B - Elizabeth Falls Signature

GDV RM37m

Units 12

Price RM2.6 Mil onwards

Build up size 2,864sf - 3,413 sq ft

Target launch date August 2017

59 x 115

66 x 85

Bungalow

Zero Lot Bungalow 19

PLANNED NEW LAUNCHES IN 2H FY2017- KEY LAUNCHES IN SETIA ECO TEMPLER

Phase 2A – Ophelia : 24 x 80

GDV RM38m

Units 40

Price RM970k onwards

Build up size From 2,477 sq ft

Target launch date October 2017

Phase 2A – Azula : 22 x 75

GDV RM45m

Units 54

Price RM850k onwards

Build up size From 2,292 sq ft

Target launch date October 2017

20

PLANNED NEW LAUNCHES IN 2H FY2017- KEY LAUNCHES IN SETIA ECO GLADES

Jewels of Grasmere (Type A)

GDV RM43m

Units 33

Price RM1.09 Mil onwards

Build up size 2,301 & 2,471 sq ft

Target launch date September 2017

Jewels of Grasmere (Type B)

GDV RM91m

Units 84

Price RM990k onwards

Build up size 2,117 & 2,306 sq ft

Target launch date September 2017

24 x 80

22 x 80

21

PLANNED NEW LAUNCHES IN 2H FY2017- KEY LAUNCHES IN SETIA TROPIKA & SETIA INDAH, JOHOR

22

Setia Tropika – Bungalow

GDVRM57m

Units 18

Price RM3.6m onwards

Build up size From 6,098 sq ft

Target launch date October 2017

Setia Indah – Shoplot

GDV RM34m

Units 27

Price RM1.3m onwards

Build up size From 3,080 sq ft

Target launch date October 2017

60 x 120/14070 x 120/14090 x 120/140

22 x 70

UPDATE ON ACQUISITION OF I&P GROUP

SYNERGISTIC ACQUISITION…

EQUITY POSITIONING- ENLARGED SETIA

24

A good deal

The purchase consideration of

RM3.65b is at 39.3% discount to the Net

Asset of I&P

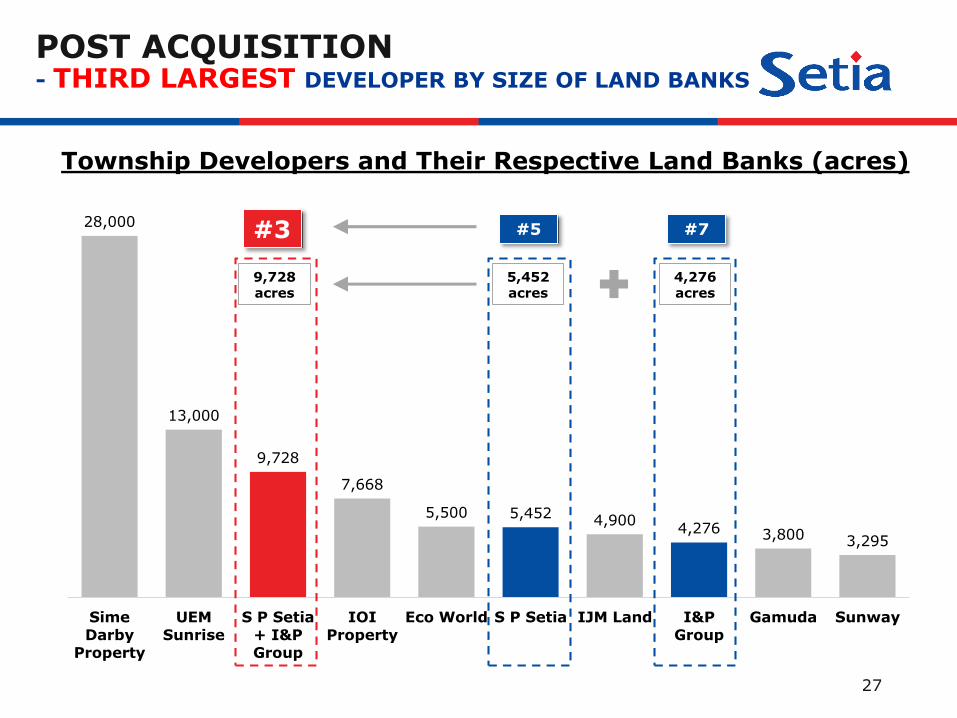

9,728 acres of prime land banks

3rd largest developer by size of land banks

Accelerates plan to double market capitalization

18 X 21

To improve the share liquidity

Pole position to gain access to KLCI/MSCI

SYNERGISTIC ACQUISITIONGood locations

I&P’s land banks are mainly in growth

areas where Setiabrand had established

a stronghold

25

Land Banks Location in Klang Valley

KL Eco City, Setia Sky Seputeh,

Setia Federal Hill

Kenny Hill Grande

Setia Eco Templer (outside map)

Seri Beringin

Sungai Sedu (outside map)

S P Setia I&P Group

Central Region 1

Setia Alam

Setia Eco Park

Temasya Putra

Setia Ecohill

Setia Ecohill2

Brogaville

Glengowrie land

Central Region 2

Central Region 3

Temasya Glenmarie

Setia Eco Glades

Salak Tinggi

Central Region 4

Bandar Kinrara

Alam Damai

Bandar Baru Seri Petaling

Petaling Heights

Alam Sutera

Alam Impian

Bayuemas

Kota Bayuemas

Central Region 5

Dwiputra Residences

Alam Sari

Bangi Estate (signed SPA)

AMALGAMATION OF PRIME LAND BANKS OF SETIA AND I&P GROUP IN KLANG VALLEY

26

AMALGAMATION OF PRIME LAND BANKS OF SETIA AND I&P GROUP IN JOHOR

Land Banks Location in Johor Bahru

Taman Setia Indah

Setia Eco Cascadia

Setia Tropika

Setia Business Park II

Taman Pelangi

Taman Pelangi Indah

Taman RintingTaman Pelangi Indah II

Bukit Indah

Setia Eco Garden

Setia Business Park

Taman Perling

Taman Industri Jaya

Tanjung Kupang

Southern Region 1

Southern Region 2

S P Setia I&P Group

27

28,000

13,000

9,728

7,668

5,500 5,452 4,9004,276 3,800 3,295

SimeDarby

Property

UEMSunrise

S P Setia+ I&PGroup

IOIProperty

Eco World S P Setia IJM Land I&PGroup

Gamuda Sunway

Township Developers and Their Respective Land Banks (acres)

#3 #5 #7

5,452 acres

4,276 acres

9,728 acres

POST ACQUISITION- THIRD LARGEST DEVELOPER BY SIZE OF LAND BANKS

UNBILLED SALES, LAND BANKS & GDV

STRONG PIPELINE…

29

Central,

2,572 , 47%

Northern,

1,809 , 33%

Southern,

719 , 13%

Eastern,

44 , 1%

International,

307 , 6%

RemainingLand Banks

5,452acres

Central,

38.57 , 48%

Northern,

13.77 , 17%

Southern,

6.02 , 8%

Eastern,

1.95 , 2%

International,

19.73 , 25%

Remaining GDV

RM80.03 billion

STRONG PIPELINE5,452 acres of remaining land bank and RM80.03 billion of remaining

GDV supported by RM8.00 billion of unbilled sales as at 30 June 2017

Remaining Land Banks & Remaining GDV = Effective Stake

Total Unbilled Sales = RM8.00 billion– Local = RM3.65 billion– International = RM4.35 billion

30

I&P’S LAND BANKS- MAINLY IN KLANG VALLEY AND JOHOR: AREAS WHERE SETIA BRAND HAD ESTABLISHED A STRONGHOLD

Johor, 1,704 ,

40%

Klang Valley,

2,556 , 60%

Others, 16 ,

<1%

Johor, 12.05 ,

31%

Klang Valley,

27.07 , 69%

Others, 0.05 ,

<1%

RemainingLand Banks

4,276acres

Remaining GDV

RM39.16 billion

Remaining Land Banks & Remaining GDV = Effective Stake

Total Unbilled Sales = RM277 million

RM39.16 billion is based on I&P’s Masterplan. Focus is to

enhance the GDV once the acquisition is completed.

FOCUS- PRIORITIES FOR THE REMAINING MONTHS OF FY2017

31

To ensure smooth and

successful integration of

I&P Group

2

Optimizing I&P land banks and

emphasis on value creation

3

To achieve the RM4.0 billion sales target for FY2017

1

Preparing beyond FY2017 with

higher sales and profit

4

Thank You

![RESORT LIFESTYLE | SMART LIVING · 2020. 6. 18. · pemaju: gamuda land (t12) sdn bhd [199401024746(310424-m)] • gamuda cove experience gallery, persiaran cove sentral, bandar gamuda](https://img.pdfslide.us/doc/110x75/60c53faa48bd340d8b3381a2/resort-lifestyle-smart-living-2020-6-18-pemaju-gamuda-land-t12-sdn-bhd.jpg)