Embed Size (px)

Citation preview

4th Quarter 2016

Financial Report

Island Offshore Shipholding LP

10th of March 2017

The businessIsland Offshore Shipholding, L.P. (the “Company” or “Island Offshore”) is the parent company in the Island Offshore

group (the “Group”). At present the Group has 25 vessels in operation within the vessel segments PSV, AHTS, Well

Stimulation (WS), Subsea Construction (SCV) and Light Well Intervention (LWI). Three vessels were sold in January/

February 2017 as part of the ongoing restructuring of the Group.

In 2016 the fleet has operated in Norway, Denmark, UK, Holland, India, Ghana, Angola and Gulf of Mexico.

The fleet is modern and versatile and Island Offshore has taken a leading position in attractive market segments. The

Group is privately owned.

Recent contract awards Island Contender, Lundin Norway, extension one well

Island Crusader, Wintershall, 500 days firm

Ocean Intervention III, Oceaneering Inc, 3 month extension

Island Crown, Bluestream, project term

Island Empress, SNS Peterson, one year extension

Island Endeavour, SNS Peterson, one year extension

Island Constructor, Shell Norway, Shell UK, NCA

Island Valiant, KD Marine

Fleet changes

Sale of Island Earl, February 2017

Sale of Island Express, January 2017

Sale of Island Performer, January 2017

Sale of Island Patriot, May 2016

Fleet The fleet comprises 25 vessels including the Island Champion which is leased back on bareboat. In addition the Island

Patriot which was sold in May 2016 but is still operated by Island Offshore. Three vessels were divested in January/

February 2017 as part of the ongoing restructuring of the Group. All three vessels have been delivered to the new

owner.

10 vessels were in lay-up at year end 2016, whereof 5 of the vessels will be activated in March 2017 following recent

contract awards and commencement of seasonal term work. Overall both spot and term day rates for PSVs and AHTS

remain low and unsustainable; however the recent awards indicate a marginal increase in the overall activity level.

We expect the other vessels in lay up to remain cold stacked until sustainable term work can be secured. The Group

currently has 2 AHTS vessels in the spot market. Vessels are tendered for term work globally.

1

4th Quarter Financial Report 2016

Main events:

Type Vessels in operation*

Vessels under construction

TOTAL

PSV 15 0 15

AHTS 2 1 3

SCV 4 0 4

RLWI 4 0 4

STIM 3 0 3

THD 0 1 1

TOTAL 28 2 30

Oilman of the Year ONS Innovation Award 2016

Due to the continued market state, the Company declared a standstill with the secured lenders of the Group on 22nd November 2016. Negotiations for a long-term and sustainable financing platform have been initiated and are progressing.

*Prior to completed sales in 2017

Income Statement

Revenue totals NOK 363 mill in Q4-16, down from NOK 560 million in Q3-16, and lower than the same quarter last year.

Fleet utilization in Q4-16 was 57% including vessels in lay-up. Full year revenue is NOK 1,908 mill and down from NOK

2,457 mill in 2015. YTD vessel utilization was 65%.

Revenue from the LWI segment was NOK 138 mill in Q4-16 down from NOK 286 mill in Q3-16, however, in line with Q4-

15. Vessels Island Frontier and Island Wellserver completed seasonal campaigns mid-October as planned, and will be

re-activated in March 2017. The AHTS vessels had low utilization and revenue amounted to NOK 9 mill in Q4-16 versus

NOK 49 mill in Q3-16. One of the two vessels was dry-docked for 10-year class renewal in December 2016, and the second

one was dry-docked in January 2017. The SCV revenue and EBITDA was in line with previous quarters with satisfactory

utilization for both term and project vessels. High spot exposure and unsustainable day rates, leaves PSV revenue and

EBTIDA low also this quarter.

EBITDA in Q4-16 totals NOK 116 mill versus NOK 231 mill in Q3-16. The reduction is mainly due to completion of seasonal

work for the LWI units and disappointing results for spot AHTS and PSV vessels. The EBITDA margin was 35% in Q4-16,

which is down from 47% in Q3-16. Full year EBITDA is NOK 687 mill and down from NOK 984 mill in 2015. All segments

report positive EBITDA despite challenging market conditions.

Cost improvements implemented provide important contributions to earnings, especially vessel lay-ups and associated crew

reductions, but also continued salary reductions onshore and offshore. The measures will be continued in 2017.

A revised impairment analysis of fleet value has been performed based on estimates of expected future earnings for each

vessel and broker value estimates. The analysis takes into account the present market conditions for each segment and

vessel. The future cash flow for the Group is expected to be negatively impacted by lower average utilization and reduced

charter hire rates in coming years. The analysis includes an assumed gradual improvement of both charter hire rates

and utilization through the rest of the expected vessel usage time. Key assumptions in the analysis include the Weighted

Average Cost of Capital (WACC), which is set to 8 %. The usage period of the vessel is assumed to be 30 years after

delivery. The analysis implies a significant increase of the provision for impairment at 31.12.2016. The write down recorded

in Q4-16 totals NOK 896 mill resulting in a negative EBIT of NOK -872 mill in Q4-16 and NOK -573 mill for the full year. The

adjustment includes a provision of NOK 145 mill for net loss realized in connection with the sale of two vessels in 2017.

Q4-16 profit before tax is a loss of NOK -1 048 mill including the above write down of vessel book values and an unrealized

FX loss of NOK -83 mill related to conversion of ship mortgages in USD. Full year profit before tax is NOK -917 mill

compared to NOK -371 mill in 2015, explained by reduced operating result for the fleet and increased impairment provision.

Quarterly Financial Report

2

- Comments

Oilman of the Year ONS Innovation Award 2016

Vessel Type/Design Yard

Island Victory DWIV, UT 797 CX Vard Brevik

Island Navigator THDV, UT 777 Kawasaki Heavy Industries

*Please see table on the next page

Vessels under construction:

3

Photo: Sondre Solvang

Oilman of the Year ONS Innovation Award 2016

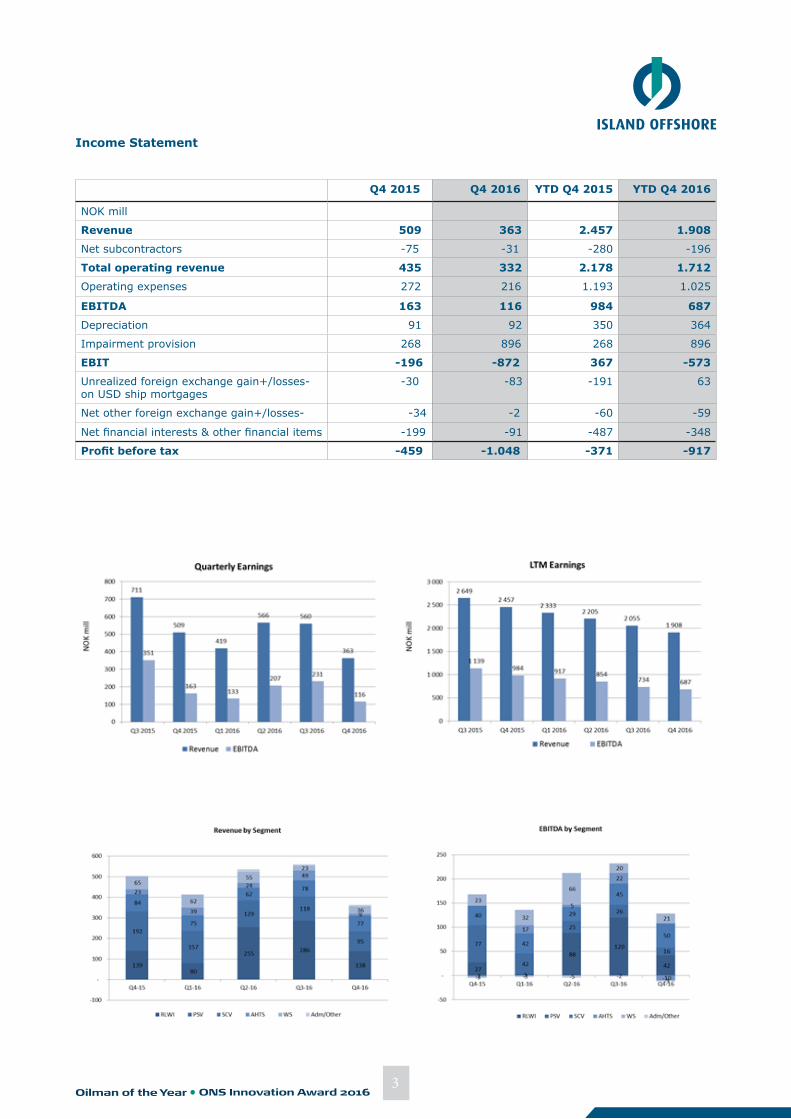

Q4 2015 Q4 2016 YTD Q4 2015 YTD Q4 2016

NOK mill

Revenue 509 363 2.457 1.908

Net subcontractors -75 -31 -280 -196

Total operating revenue 435 332 2.178 1.712

Operating expenses 272 216 1.193 1.025

EBITDA 163 116 984 687

Depreciation 91 92 350 364

Impairment provision 268 896 268 896

EBIT -196 -872 367 -573

Unrealized foreign exchange gain+/losses- on USD ship mortgages

-30 -83 -191 63

Net other foreign exchange gain+/losses- -34 -2 -60 -59

Net financial interests & other financial items -199 -91 -487 -348

Profit before tax -459 -1.048 -371 -917

Income Statement

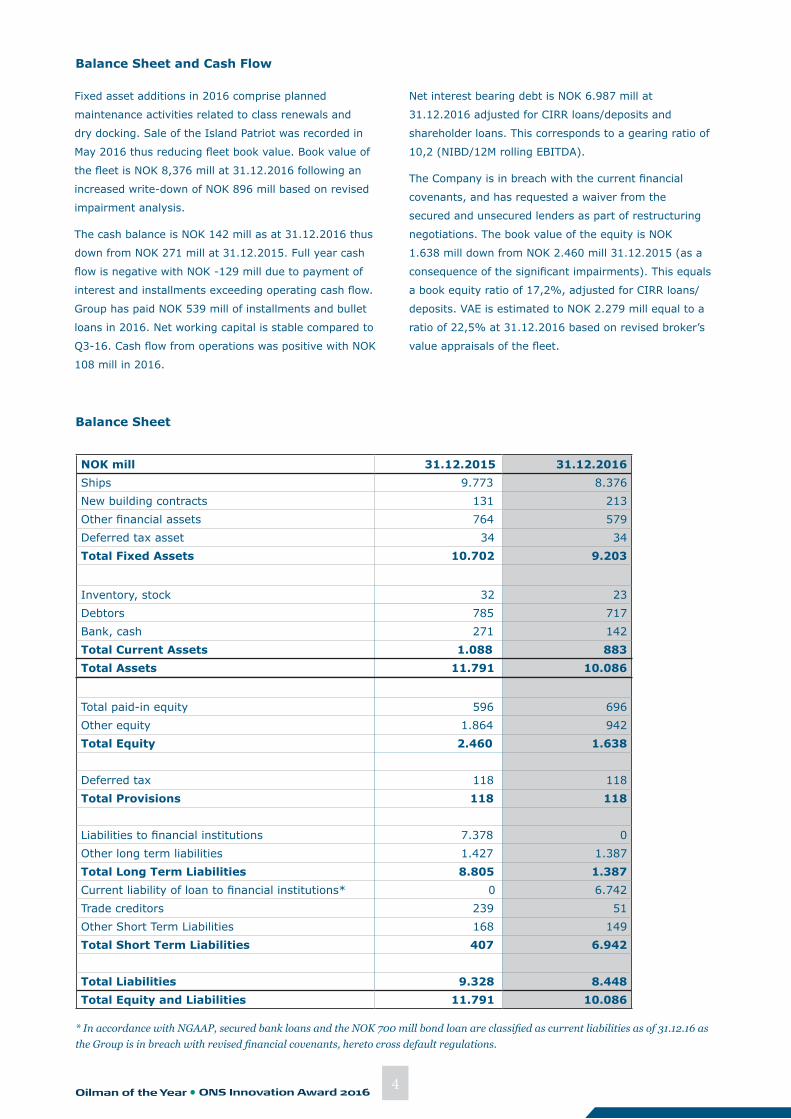

NOK mill 31.12.2015 31.12.2016Ships 9.773 8.376New building contracts 131 213Other financial assets 764 579Deferred tax asset 34 34Total Fixed Assets 10.702 9.203

Inventory, stock 32 23Debtors 785 717Bank, cash 271 142Total Current Assets 1.088 883Total Assets 11.791 10.086

Total paid-in equity 596 696Other equity 1.864 942Total Equity 2.460 1.638

Deferred tax 118 118Total Provisions 118 118

Liabilities to financial institutions 7.378 0Other long term liabilities 1.427 1.387Total Long Term Liabilities 8.805 1.387Current liability of loan to financial institutions* 0 6.742Trade creditors 239 51Other Short Term Liabilities 168 149Total Short Term Liabilities 407 6.942

Total Liabilities 9.328 8.448Total Equity and Liabilities 11.791 10.086

Balance Sheet

4

Fixed asset additions in 2016 comprise planned

maintenance activities related to class renewals and

dry docking. Sale of the Island Patriot was recorded in

May 2016 thus reducing fleet book value. Book value of

the fleet is NOK 8,376 mill at 31.12.2016 following an

increased write-down of NOK 896 mill based on revised

impairment analysis.

The cash balance is NOK 142 mill as at 31.12.2016 thus

down from NOK 271 mill at 31.12.2015. Full year cash

flow is negative with NOK -129 mill due to payment of

interest and installments exceeding operating cash flow.

Group has paid NOK 539 mill of installments and bullet

loans in 2016. Net working capital is stable compared to

Q3-16. Cash flow from operations was positive with NOK

108 mill in 2016.

Net interest bearing debt is NOK 6.987 mill at

31.12.2016 adjusted for CIRR loans/deposits and

shareholder loans. This corresponds to a gearing ratio of

10,2 (NIBD/12M rolling EBITDA).

The Company is in breach with the current financial

covenants, and has requested a waiver from the

secured and unsecured lenders as part of restructuring

negotiations. The book value of the equity is NOK

1.638 mill down from NOK 2.460 mill 31.12.2015 (as a

consequence of the significant impairments). This equals

a book equity ratio of 17,2%, adjusted for CIRR loans/

deposits. VAE is estimated to NOK 2.279 mill equal to a

ratio of 22,5% at 31.12.2016 based on revised broker’s

value appraisals of the fleet.

Balance Sheet and Cash Flow

Oilman of the Year ONS Innovation Award 2016

* In accordance with NGAAP, secured bank loans and the NOK 700 mill bond loan are classified as current liabilities as of 31.12.16 as the Group is in breach with revised financial covenants, hereto cross default regulations.

5

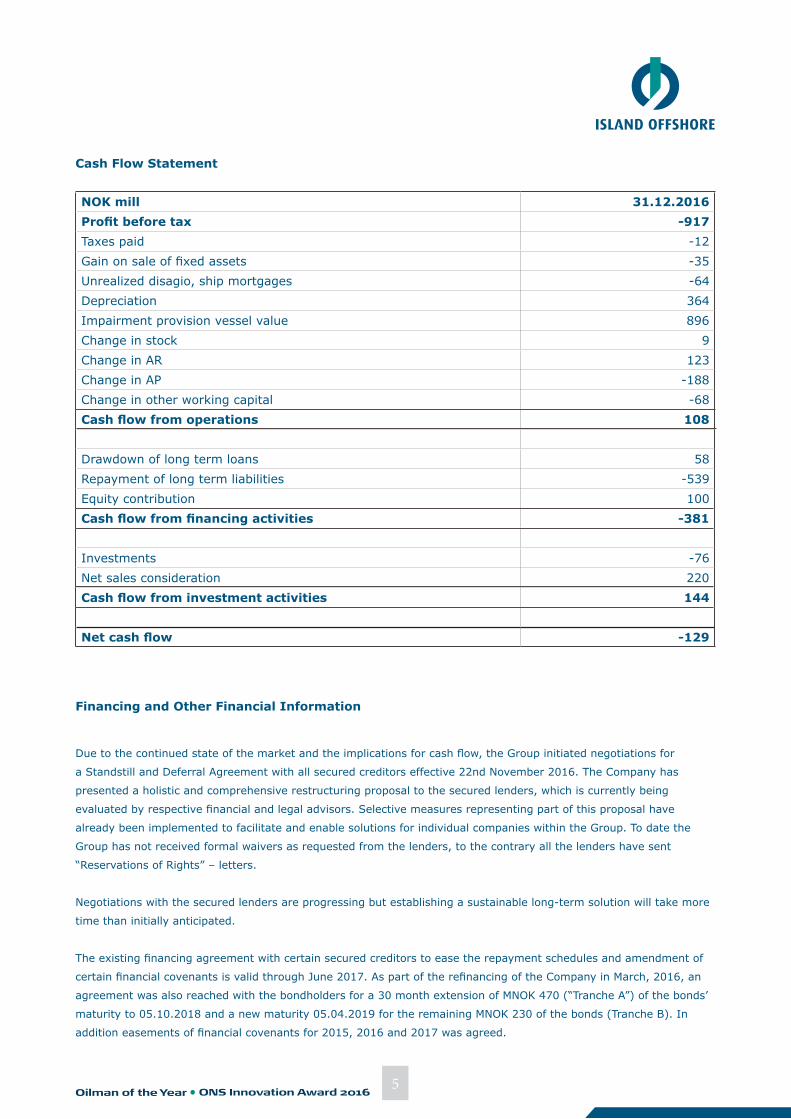

Cash Flow Statement

Due to the continued state of the market and the implications for cash flow, the Group initiated negotiations for

a Standstill and Deferral Agreement with all secured creditors effective 22nd November 2016. The Company has

presented a holistic and comprehensive restructuring proposal to the secured lenders, which is currently being

evaluated by respective financial and legal advisors. Selective measures representing part of this proposal have

already been implemented to facilitate and enable solutions for individual companies within the Group. To date the

Group has not received formal waivers as requested from the lenders, to the contrary all the lenders have sent

“Reservations of Rights” – letters.

Negotiations with the secured lenders are progressing but establishing a sustainable long-term solution will take more

time than initially anticipated.

The existing financing agreement with certain secured creditors to ease the repayment schedules and amendment of

certain financial covenants is valid through June 2017. As part of the refinancing of the Company in March, 2016, an

agreement was also reached with the bondholders for a 30 month extension of MNOK 470 (“Tranche A”) of the bonds’

maturity to 05.10.2018 and a new maturity 05.04.2019 for the remaining MNOK 230 of the bonds (Tranche B). In

addition easements of financial covenants for 2015, 2016 and 2017 was agreed.

Financing and Other Financial Information

NOK mill 31.12.2016Profit before tax -917Taxes paid -12Gain on sale of fixed assets -35Unrealized disagio, ship mortgages -64Depreciation 364Impairment provision vessel value 896Change in stock 9Change in AR 123Change in AP -188Change in other working capital -68Cash flow from operations 108

Drawdown of long term loans 58Repayment of long term liabilities -539Equity contribution 100 Cash flow from financing activities -381

Investments -76Net sales consideration 220Cash flow from investment activities 144

Net cash flow -129

Oilman of the Year ONS Innovation Award 2016

6

Photo: Sondre Solvang

Oilman of the Year ONS Innovation Award 2016

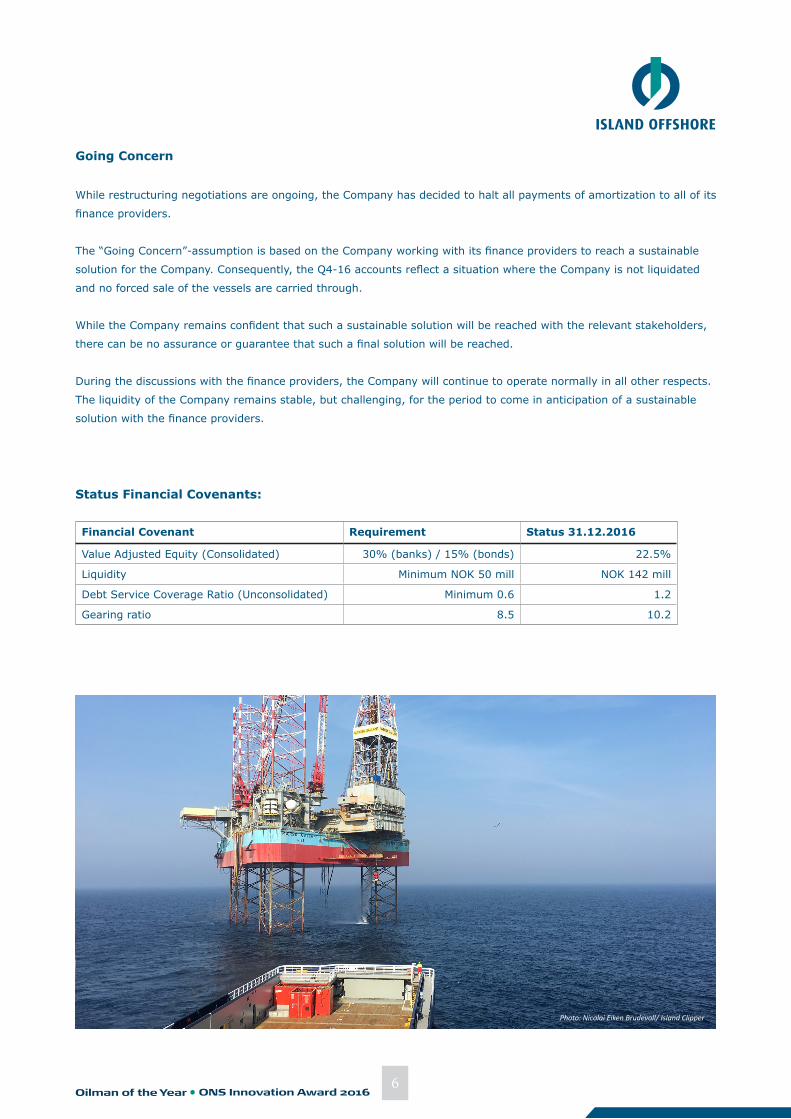

While restructuring negotiations are ongoing, the Company has decided to halt all payments of amortization to all of its

finance providers.

The “Going Concern”-assumption is based on the Company working with its finance providers to reach a sustainable

solution for the Company. Consequently, the Q4-16 accounts reflect a situation where the Company is not liquidated

and no forced sale of the vessels are carried through.

While the Company remains confident that such a sustainable solution will be reached with the relevant stakeholders,

there can be no assurance or guarantee that such a final solution will be reached.

During the discussions with the finance providers, the Company will continue to operate normally in all other respects.

The liquidity of the Company remains stable, but challenging, for the period to come in anticipation of a sustainable

solution with the finance providers.

Going Concern

Financial Covenant Requirement Status 31.12.2016

Value Adjusted Equity (Consolidated) 30% (banks) / 15% (bonds) 22.5%

Liquidity Minimum NOK 50 mill NOK 142 mill

Debt Service Coverage Ratio (Unconsolidated) Minimum 0.6 1.2

Gearing ratio 8.5 10.2

Status Financial Covenants:

Photo: Nicolai Eiken Brudevoll/ Island Clipper

7

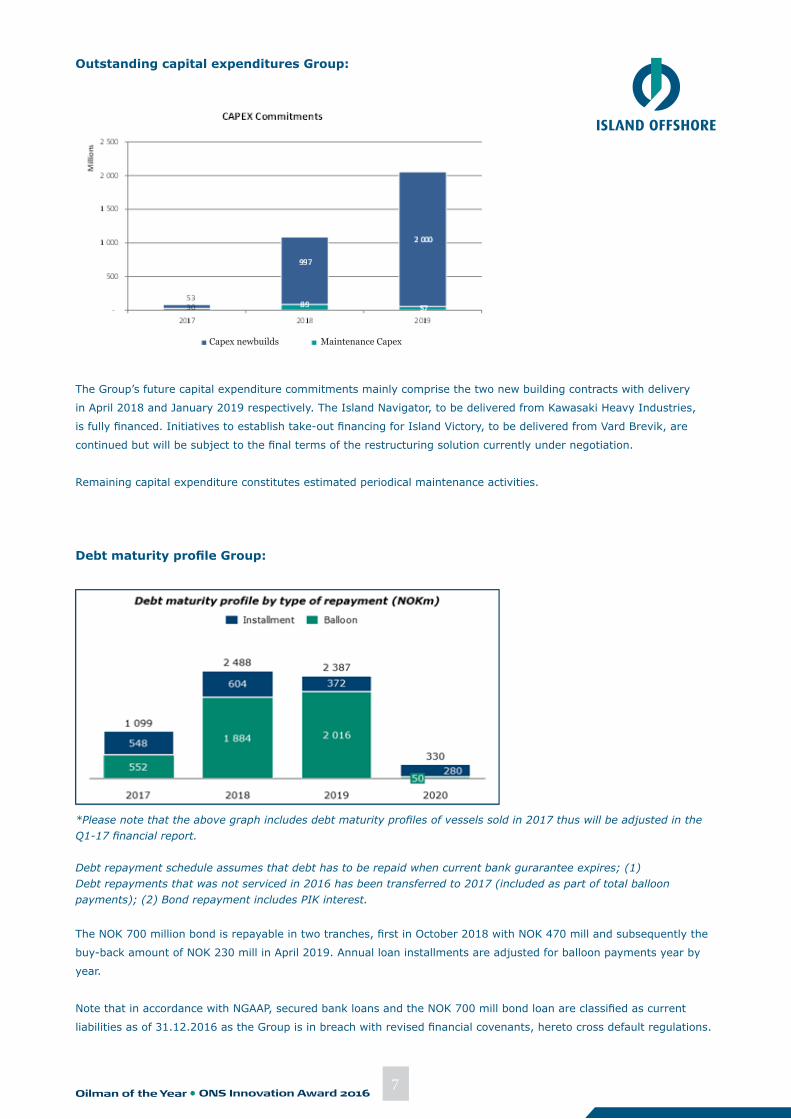

Debt maturity profile Group:

The NOK 700 million bond is repayable in two tranches, first in October 2018 with NOK 470 mill and subsequently the

buy-back amount of NOK 230 mill in April 2019. Annual loan installments are adjusted for balloon payments year by

year.

Note that in accordance with NGAAP, secured bank loans and the NOK 700 mill bond loan are classified as current

liabilities as of 31.12.2016 as the Group is in breach with revised financial covenants, hereto cross default regulations.

Outstanding capital expenditures Group:

The Group’s future capital expenditure commitments mainly comprise the two new building contracts with delivery

in April 2018 and January 2019 respectively. The Island Navigator, to be delivered from Kawasaki Heavy Industries,

is fully financed. Initiatives to establish take-out financing for Island Victory, to be delivered from Vard Brevik, are

continued but will be subject to the final terms of the restructuring solution currently under negotiation.

Remaining capital expenditure constitutes estimated periodical maintenance activities.

Oilman of the Year ONS Innovation Award 2016

*Please note that the above graph includes debt maturity profiles of vessels sold in 2017 thus will be adjusted in the Q1-17 financial report.

Debt repayment schedule assumes that debt has to be repaid when current bank gurarantee expires; (1) Debt repayments that was not serviced in 2016 has been transferred to 2017 (included as part of total balloon payments); (2) Bond repayment includes PIK interest.

Capex newbuilds Maintenance Capex

Island Offshore has secured important contract awards in recent months, allowing 6 vessels to be taken out of lay-up and

into operation in Q1-17. Day rates are low but acceptable considering the alternative of continued lay-up. The awards have

been secured with strategically important and recurring customers.

Overall spot and term rates in the conventional PSV and AHTS markets continue to be depressed by reduced activity

and vessel oversupply. However, there are signs of increased activity enabling opportunities to activate selective vessels

currently cold stacked. We do however, not expect to see a more extensive market recovery until a more sustainable oil

price is established, inducing increased E&P investment thus market activity. Short and long-term work across markets is

still extremely competitive. Our view on the subsea and LWI market is maintained and we anticipate an earlier recovery

for this market.

Our chartering strategy remains firm with focus on securing long-term commitment with strategically preferred clients, in

addition to exploring new business opportunities.

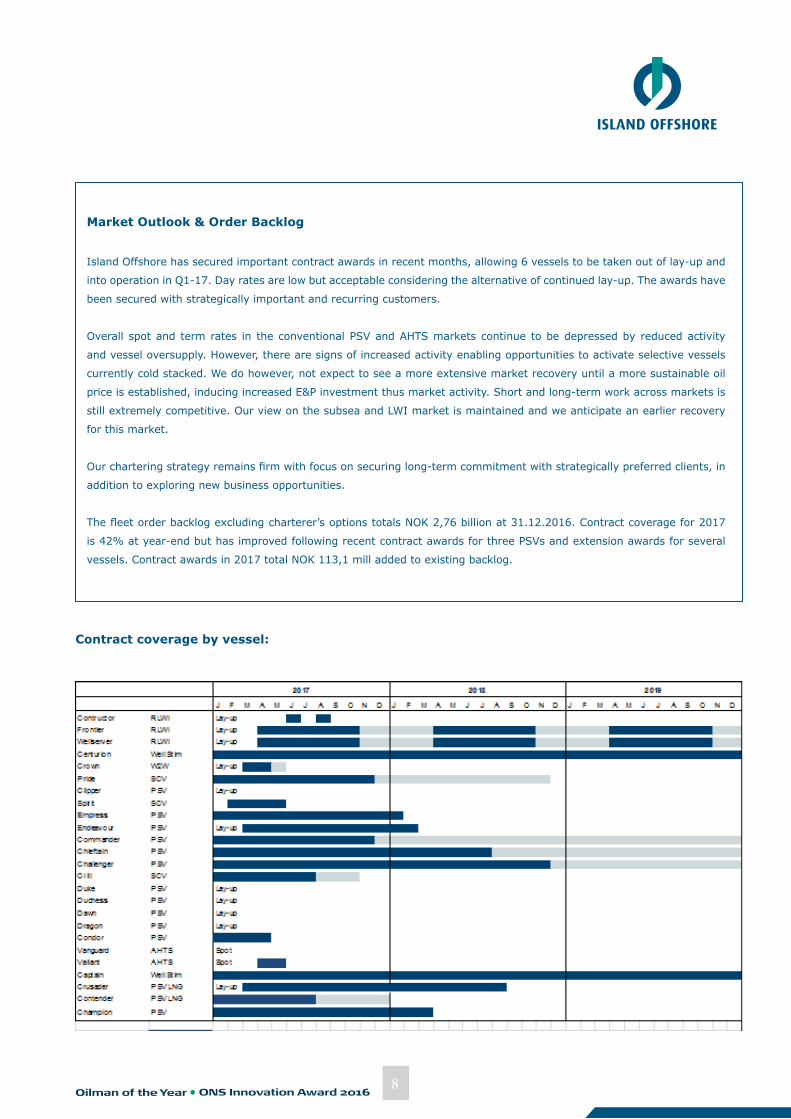

The fleet order backlog excluding charterer’s options totals NOK 2,76 billion at 31.12.2016. Contract coverage for 2017

is 42% at year-end but has improved following recent contract awards for three PSVs and extension awards for several

vessels. Contract awards in 2017 total NOK 113,1 mill added to existing backlog.

Market Outlook & Order Backlog

8

Contract coverage by vessel:

Oilman of the Year ONS Innovation Award 2016

9

Health, Safety and the Environment

Island Offshore endeavor to promote and maintain a safe and healthy working environment offshore and onshore.

This includes considering health and safety factors in the design, construction and operation of all vessels and

equipment. We are committed to increasing the level of safety involvement and awareness among all employees.

Key performance targets are set, validated and monitored in a QHSE plan. The personnel injury frequency remains

low and has improved further in recent months. Sick leave for offshore personnel has stabilized but the objective is

still to reduce sick leave beyond current levels. CO2 emission from the fleet has been reduced by 14% in 2016, partly

explained by lower vessel activity and lay-up.

We continue with the main focus areas:

- Reductions in emissions by use of alternative fuels, reduction in fuel consumption and cleaning of exhaust

- Selection and handling of chemicals

- Waste management

- Handling of environmentally harmful substances from marine and subsea operations

Photo: Sondre Solvang/ Island Challenger

Investor relations:

Mr. Henning Sundet, Chief Financial Officer: [email protected], +47 913 65 735

*This financial report represents the consolidated financial statements for the Island Offshore Shipholding LP Group. The report is prepared on the basis of Generally Accepted Accounting Principles in Norway and has not been audited.

Oilman of the Year ONS Innovation Award 2016

![FY2019 FULL YEAR RESULTS MACRO CONDITIONS There is broad consensus that the market is recovering 5 “Demand trending higher –we see recovery towards c. 80% [AHTS and PSV] utilization](https://img.pdfslide.us/doc/110x75/5e8c65b6ba3d737ddc667762/fy2019-full-year-macro-conditions-there-is-broad-consensus-that-the-market-is-recovering.jpg)