Embed Size (px)

Citation preview

Financial Provisions for Rehabilitation and Closure in South African Mining:Discussion Document on Challenges and Recommended Improvements

page 2 | WWF-SA Mining Financial Provisions

ACKNOWLEDGEMENTSThis report was made possible with funding from the World Wide Fund for Nature (WWF) and with appreciated guidance from its staff including Malango Mughogho and Dr Deon Nel.

We would also like to thank the numerous people interviewed as part of the research process who gave freely of their time and options (see Appendix 1 for a list of interviewees).

The views expressed in the report are those of the authors and do not necessarily reflect of those of WWF or any other organisation.

Published in August 2012 by WWF-World Wide FundFor Nature (Formerly World Wildlife Fund), Cape Town,South Africa. Any reproduction in full or in part must mentionthe title and credit the above-mentioned publisher as thecopyright owner.

© Text 2012 WWF-SA

All rights reserved

WWF is one of the world’s largest and most experiencedindependent conservation organizations, with overfive million supporters and a global Network active inmore than 100 countries.

WWF’s mission is to stop the degradation of the planet’snatural environment and to build a future in which humans livein harmony with nature, by: conserving the world’s biologicaldiversity, ensuring that the use of renewable natural resourcesis sustainable, and promoting the reduction of pollution andwasteful consumption.

www.wwf.org.za

WWF-SA Mining Financial Provisions | page 3

Financial Provisions for Rehabilitation and Closure in South African Mining: Discussion Document on Challenges and Recommended Improvements

Prepared with funding from the World Wide Fund for Nature (WWF)

Prepared by:Hugo van Zyl,1 Marguerite Bond-Smith,2 Tessa Minter,3 Mark Botha,4

and Anthony Leiman5

1 – Independent Economic Researchers

2 – Independent Consultant and Trustee on the SA Water Stewardship Council Trust

3 – University of Cape Town, Department of Accounting

4 – Independent Consultant

5 – University of Cape Town, School of Economics

page 4 | WWF-SA Mining Financial Provisions

WWF-SA Mining Financial Provisions | page 5

EXECUTIVE SUMMARYOngoing concerns regarding environmental degradation in mining areas, the high number of ownerless and abandoned mines, and the incidence of acid mine drainage (AMD) have highlighted the need for improved environmental maintenance and rehabilitation in the mining sector. These concerns give rise to questions about the availability of funds to manage the impacts of mining and the adequacy of financial provisions made by mining companies for rehabilitation. With this in mind, this discussion document provides a critical review of the processes surrounding financial provisions for mine rehabilitation and closure and recommends potential improvements. It emphasises the need to deepen the debate on key issues in order to arrive at collective improvements and a more sustainable mining industry.

The estimation and adequacy of financial provisionsHaving established a general understanding of the process through which financial provision estimations are generated, a broad review was conducted focused on the practice of financial provision estimation. The result of the review indicated the following areas of concern:

High levels of variation with regard to the quality of Environmental Management Plans • or Programmes (EMPs) and inadequate consideration of longer term water quality issues in particular.EMPs with inadequate or no rehabilitation plans at all, making it difficult to trace the links • that should be clearly present between these plans and calculations of financial provisions.Master rates contained in the 2005 Department of Mineral Resources (DMR) • guidelines (2005 DMR Guidelines) are not adjusted for inflation, resulting in significant underestimations of adequate financial provisions.Lack of concurrent rehabilitation and clear incentives to rehabilitate, resulting in higher • longer term and more significant risks, particularly with regard to water quality impacts.There are indications that a number of mines are not making adequate financial provision • for closure (uncertainty with regard to the adequacy of financial provisions appears to be greatest in relation to providing for adequate post closure water treatment and management). This is supported by targets set in the two most recent strategic plans of the DMR, which explicitly recognise that more needs to be done to ensure greater compliance with financial provision requirements.1Confidence in financial provision estimates is undermined by the lack of publicly available • independent reviews of financial provision calculations.

This discussion document makes the following recommendations:

The addition of more stringent provisions accompanied by regular updating of the DMR • guidelines for the evaluation of the quantum of closure-related financial provisions including:

Augmentation of the guideline to ensure that it remains clear, responsive to changes and • actively draws on industry/stakeholder experience and advances on an ongoing basis.Incorporation of other relevant resources such as the 2008 Department of Water • Affairs (DWA) best practice guideline series and the 2007 CoM & Coaltech guidelines2 on rehabilitation.

1. Department of Mineral Resources 2010. Department of Mineral Resources Strategic Plan: 2010/2011-2012/2013. DMR, Pretoria, at 41.2. Chamber of Mines of South Africa and Coaltech Research Association. 2007. Guidelines for the rehabilitation of mined lands. CoM and Coaltech, Johannesburg (hereafter referred to as “CoM & Coaltech Guidelines”)

page 6 | WWF-SA Mining Financial Provisions

Clarification of links between the EMP guidelines and the DMR financial provision • calculation guidelines to ensure comprehensive, easily referenced and quantified rehabilitation plans in EMPs.Incorporation of measures to incentivise concurrent rehabilitation.•

Augmented and structured use of the independent review mechanism as a standard, default • approach when assessing the adequacy of financial provisions.Improved public access to data and information on financial provisions.• Enhancement of the South African Code for Reporting of Exploration Results, Mineral • Resources and Mineral Reserves (SAMREC code) to allow for greater clarity on how environmental liability costs need to be taken into account, including potential links to the DMR guidelines for the evaluation of the quantum of closure-related financial provisions.Integrated authorisation/sign-off of EMPs from environmental and water authorities.•

Securing financial provisions using financial instrumentsThe financial rehabilitation provision required in terms of section 41 of the Mineral and Petroleum Resources Development Act3 can be provided in one of four methods: cash deposit, guarantee, insurance or approved trust fund. Each of these methods has certain advantages, but also contains certain risks. In the instance of insurance and bank guarantees, the creditworthiness of the counterparties involved plays a key role, as does the ability of the counterparty to on-sell a portion or all of the risks it has assumed by means of credit derivatives. In the instance of a trust fund, the ability of the DMR to access the funds as contemplated in section 41(2) of the MPRDA may be problematic. In addition, it seemed that the standard trust documentation prescribed by the DMR purports to impose obligations on the mining entity in its capacity as beneficiary, which is problematic in law. The wording of the trust deed and the MPRDA must be aligned with the provisions of the Income Tax Act4 due to the former making reference to repealed sections of the Income Tax Act. Furthermore, while section 37A of the ITA places welcome and needed limitations on the type of investments that these trusts may make, further recommendations are made to ensure that funds invested by the trust are capital protected and enjoy the appropriate degree of diversification and spreading to limit risk.

The impact of the Insolvency Act5 and the business rescue provisions of the Companies Act on the financial provision and whether it is adequately protected is uncertain and legislative amendment is required in this regard.

It is noted that the provisions of the standard trust deed are not completely aligned with the National Environmental Management Act,6 the MPRDA, the Trust Property Control Act7 or the Companies Act8 insofar as the limitation of liability of trustees/directors is concerned. Consequently recommendations are made with regard to the inadequate cross referencing of the MPRDA with other legislation to adequately deal with liability of directors/trustees. While the liability of trustees should not be too onerous, at a minimum trustees should assume liability should the trust be administered in a manner that would result in the obligations imposed in terms of section 41 of the MPRDA not being discharged.

In addition, the ability to deregister companies in terms of the Companies Act can occur independently of whether a closure certificate has been issued in terms of section 41 of the MPRDA. Furthermore, distributions made by mining entities to shareholders where unfunded environmental obligations exist may not always be subject to the protection afforded by section 4 of the Companies Act imposing a solvency and liquidity test before the making of distributions as defined.

3. Act 28 of 2002 (“MPRDA”)4. Act 58 of 1962 (“the ITA”)5. Act 24 of 19366. Act 107 of 1998 (“NEMA”)7. Act 57 of 19888. Act 71 of 2008

WWF-SA Mining Financial Provisions | page 7

Financial reporting of environmental risks and closure liabilitiesA review of the financial reporting framework relating specifically to environmental risks and closure liabilities revealed:

There exists a lack of compatibility between environmental considerations and the standard • accounting framework. This is particularly apparent in the context of the quantification of liabilities or provisions where uncertainties exist (which is typically the case with environmental obligations). Secondly, the fact that the primary users of the financial statements typically do not include regulators raises concerns as to the efficacy of the financial reporting framework as a primary means of verifying environmental compliance. Thirdly, materiality both qualitative and quantitative is an important factor in the context of the presentation of financial statements. It is hoped that the concept of qualitative materiality would play an important role in ensuring that environmental risks are appropriately disclosed in the financial statements. Fourthly, we express reservations about the safe haven provisions with limited liability for inaccuracies that apply to “forward looking statements” as defined and how this interacts with the duty of care provisions of NEMA.The lack of standardisation and industry benchmarking in the context of the integrated • reports of various entities were also found to be problematic as they rendered meaningful comparison difficult.Much of the integrated report is not customised for the South African context, and allows • too much scope for “ticking the boxes” in the absence of substantial compliance, for instance with regard to the disclosure of water and energy consumption without simultaneous or comparative disclosure as to the extent of available resources. Recommendations were made with regard to standardizing disclosure practices to be adopted by all mining entities.The role that shareholder involvement can play needs to be stressed with specific reference • to Code for Responsible Investing in South Africa,9 King lll, Regulation 2810 to the Pension Funds Act11 and the role of the Equator Principles12 in respect of funded projects. The efficacy of these measures in improving environmental compliance is limited by the absence of clear guidelines until now and lack of applicability to all mining entities.The possibility of requiring all mining entities, whether legally incorporated as companies or • not, to conduct an annual audit in terms of section 30 of the Companies Act was explored on the basis that mining per se falls within the public interest as contemplated in that section. Cost constraints, inter alia, mitigate against the need for a “full audit” and may be in excess of what is required in terms of an environmental assurance report. The latter, which would be adequate from an environmental perspective, would simply entail the assurance that there has been substantial compliance with environmental laws and regulations and that the provision required by section 41 is adequate and the assumptions used in its calculation are reasonable, consistent with prior years and comprehensive. It is recommended that the format and content of the assurance report be researched further.The concerns raised regarding financial reporting in general seem to suggest the need • for a customised accounting standard or other form of guidance applicable to accounting disclosures to be made by mining entities. In this regard, guidance can be obtained from “Exposure Draft of Australian Water Accounting Standard” issued by the Australian Government Department of Meteorology in 201013 or the principles of a Carbon Disclosure Project, customised for the mining and South African context.14

9. Issued by Institute of Directors in July 2011 (CRISA).10. Published in Government Gazette 34070 dated 4 March 2011.11. Act 24 of 1956.12. Equator Principles June 2006 accessed via http://www.equator-principles.com.13. Australian Government Bureau of Meteorology: Exposure Draft of Australian Water Accounting Standard 1 accessed via http://www.bom.gov.au/water/standards/documents/ed_awas1_v1.0.pdf.14. On Carbon Disclosure Project, refer https://www.cdproject.net/CDPResults/CDP-2010-South-Africa-JSE100-Summary.pdf inter alia.

page 8 | WWF-SA Mining Financial Provisions

ABBREVIATIONSAMD Acid Mine DrainageCGS Council for GeoscienceCMMI Council of Mining and Metallurgical InstitutionsCoM Chamber of Mines (of South Africa)CPIX Consumer Price Index excluding mortgage costsCRISA Code for Responsible Investment in South AfricaDE Department of EnergyDEA Department of Environmental AffairsDME Department of Minerals and Energy DMR Department of Mineral ResourcesDWA Department of Water AffairsDWAF Department of Water Affairs and ForestryEIA Environmental Impact AssessmentEMP Environmental Management PlanGRI Global Reporting InitiativeICMM International Council on Mining and MetalsITA Income Tax Act 58 of 1962Minerals Act Minerals Act 50 of 1991MPRDA Minerals and Petroleum Resources Development Act 28 of 2002NEMA National Environmental Management Act 107 of 1998SAMREC South African Mineral Resource CommitteeToR Terms of ReferenceWaste Act National Environmental Management: Waste Act 59 of 2008WWF World Wide Fund for Nature

WWF-SA Mining Financial Provisions | page 9

GLOSSARY15

Competent person – A person whois qualified by virtue of his or her knowledge, training, skills and experience to organise the • work and its performance, andis familiar with the provision of the Act and other related legislation which apply to the work • to be performed, andhas been trained to recognise any potential or actual problem in the performance of the work.• 16

Concurrent rehabilitation – Rehabilitation that occurs during the process of mining as the ore body is mined out in parts of a mine.

Environment – The surroundings within which humans exist and that are made up of land, water and atmosphere of the earth, micro-organisms, plant and animal life, any part or combination of the foregoing as well as the physical, chemical, aesthetic and cultural properties and conditions of the foregoing that influence human health and well-being.17

Environmental Management Plan – A plan to manage and rehabilitate the environmental impact as a result of prospecting, reconnaissance, exploration or mining operations.18

Financial provision – The insurance, bank guarantee, trust fund or cash that applicants for or holders of a right or permit must provide in terms of sections 41 and 89 of the MPRDA guaranteeing the availability of sufficient funds to undertake the agreed work programmes and to rehabilitate the prospecting, mining, reconnaissance, exploration or production areas as the case may be.19

Master rate – Standardised cost associated with a given rehabilitation action as outlined in the 2005 DMR guidelines for the evaluation of the quantum of closure-related financial provisions.20

Mine Closure – This entails the process of rehabilitation at the end of a mine’s life leading to the issue of a closure certificate in terms of section 12 of the Minerals Act21 or in terms of section 43 of the MPRDA.

Mine closure certificate – The holder of a prospecting right, mining right, retention permit or mining permit must apply to the Regional Manager for a closure certificate within 180 days of the occurrence of closure, as defined above. No closure certificate will be issued unless the Chief Inspector and the Department of Water Affairs and Forestry have confirmed in writing that the provisions relating to health and safety and management of potential pollution to water resources have been addressed.22

Mine closure cost estimation models – Cost model used to estimate the funds that would be required to achieve mine closure and receive a closure certificate.

15. Sources: Golder Associates (2004), SAMREC (2007) or as specifically indicated otherwise.16. Golder Associates (2004) at A16, SAMREC code at 5-7, Regulations in Government Gazette 26275 dated 23 April 2004 at 7.17. Section 1 of NEMA.18. Section 1 of MPRDA.19. Section 1 of MPRDA.20. In particular refer Golder Associates (2004) at C3 1 et seq.21. 50 of 1991(“Minerals Act”).22. Term not defined in section 1, but process described in section 43 of MPRDA.

page 10 | WWF-SA Mining Financial Provisions

Mineral reserve – The economically mineable material derived from a Measured or Indicated Mineral Resource or both. It includes diluting and contaminating materials and allows for losses that are expected to occur when the material is mined. Appropriate assessments with a minimum of a Pre-Feasibility Study for a project, or a Life of Mine Plan for an operation, must have been completed, including consideration of, and modification by, realistically assumed mining, metallurgical, economic, marketing, legal, environmental, social and governmental factors. Where the term “Ore Reserve” is used, this is synonymous with the term “Mineral Reserve.”23

Planned mine closure – Form of mine closure that occurs when closure is undertaken in a planned way as outlined in a long-term mine plan.

Polluter Pays Principle – Principle according to which the person responsible for harming the environment (i.e. the polluter) should bear the costs of remedying pollution or environmental degradation and consequent adverse health effects to the extent of either the damage done to society or exceeding an acceptable level (standard) of pollution.24

Post-closure management – The ongoing management of residual environmental impacts for a specified period as determined after closure in terms of section 43(1) of the MPRDA has been obtained.25

Premature mine closure – Form of mine closure that occurs when closure is unexpectedly necessitated before the anticipated time of closure as outlined in a long-term mine plan. Reasons for this form of closure can include unforeseen technical difficulties in mining, sharp decreases in ore prices, etc.

Rehabilitation – The process of reshaping and re-vegetating land to restore it to a stable condition with a land-use that is appropriate for the particular location and is not associated with any pollution issues such as water pollution.26

Rehabilitation plan – Plan describing and detailing the concrete actions that are required to adequately mitigate environmental impacts and achieve rehabilitation outcomes.

SAMREC Code – Means the South African Code for Reporting of Exploration Results, Mineral Resources and Mineral Reserves.

Sustainable development – The integration of social, economic and environmental factors into planning, implementation and decision-making so as to ensure that development serves present and future generations.27

23. SAMREC code 2007 edition at 17.24. Section 2(4)(p) of NEMA.25. Golders 2004 at A18.26. Also refer Golders 2004 at A18, CoM & Coaltech Guidelines at 4.27. Section 1 of NEMA and section 1 of MPRDA.

WWF-SA Mining Financial Provisions | page 11

CONTENTSExecutive Summary ............................................................................................................................................ i

Acknowledgements ............................................................................................................................................ ii

Abbreviations .................................................................................................................................................... iv

Glossary ............................................................................................................................................................. v

1. Introduction ....................................................................................................................................................11.1 Background ...................................................................................................................................................11.2 Objectives and terms of reference ...............................................................................................................1

2. Approach ....................................................................................................................................................... 5

3. Legal review ................................................................................................................................................... 7

4. The financial provisions process and key challenges................................................................................... 11

5. The estimation and adequacy of financial provisions ..................................................................................155.1 The process for determining financial provisions for closure ....................................................................155.2 Implementation capacity and strategic targets .........................................................................................195.3 Review of financial provision estimation practice ....................................................................................215.3.1 Inadequate EMPs and associated rehabilitation plans ..........................................................................215.3.2 Non-inflation of master rates ................................................................................................................ 225.3.3 Lack of concurrent rehabilitation .......................................................................................................... 225.3.4 Reservations regarding adequate financial provisions for closure ....................................................... 225.4 Recommendations for improvements ...................................................................................................... 235.4.1 Elevation, enhancement and regular updating of the DMR guidelines ............................................... 245.4.2 Greater and more structured use of the independent review mechanism ........................................... 275.4.3 Greater public access to data and information on financial provisions ............................................... 275.4.4 Augmentation of the SAMREC code ..................................................................................................... 27

6. Securing financial provisions using financial intruments ..........................................................................316.1 Recap of the legislative framework ............................................................................................................316.2 Risks and benefits associated with financial instruments ........................................................................316.2.1 Cash deposit ...........................................................................................................................................326.2.2 Bank guarantee ......................................................................................................................................326.2.3 Insurance ...............................................................................................................................................326.2.4 Trust funds ............................................................................................................................................ 336.3 Investment of financial provisions held in trust ...................................................................................... 346.4 Ring-fencing of financial provisions on insolvency ................................................................................. 356.5 Cross referencing between the MPRDA and other legislation ................................................................ 35

7. Financial reporting of environmental risks and closure liabilities ............................................................ 397.1 Compatibility of the environmental regulations with the current accounting framework ..................... 397.2 Role of the International Council on Mining and Metals (ICMM) ..........................................................407.3 Role of Global Reporting Initiative (GRI) sustainability reports .............................................................417.3.1 Identification of risks, stakeholders ........................................................................................................417.3.2 Non-standardised information...............................................................................................................417.3.3 Definition of environmental performance indicators ........................................................................... 427.4 Value of shareholder/stakeholder involvement ....................................................................................... 427.5 Audit requirements for mining entities .................................................................................................... 43

8. Conclusions and key recommendations .................................................................................................... 45

9. References ...................................................................................................................................................49

10. Annexures ..................................................................................................................................................57

page 12 | WWF-SA Mining Financial Provisions

1. INTRODUCTION

WWF-SA Mining Financial Provisions | page 1

1. INTRODUCTION

1.1 BackgroundOngoing concerns regarding environmental degradation in mining areas, high numbers of ownerless and abandoned mines, and the incidence of acid mine drainage (AMD) have all highlighted the need for improved environmental maintenance and rehabilitation in the mining sector. These concerns give rise to questions about the availability of funds to manage the impacts of mining and the adequacy of financial provisions made by mining companies for rehabilitation. Recent research summarising impacts of coal mining in the Olifants catchment indicates that impacts are severe in many cases and have significant measurable external costs (WWF, 2011). In addition, the report to the inter-ministerial committee on AMD makes for sober reading with regard to impacts and challenges. Although it focuses primarily on abandoned mines in the Witwatersrand gold fields, it also warns about other areas such as the upper reaches of the Vaal and Olifants River systems where the impact of mining on the freshwater sources is noted as a serious concern (CGS et al., 2010). While there is relatively broad consensus that a significant portion of current environmental impacts relate to abandoned mines, there is a clear need to also ensure that current and future mining activities do not add to unacceptable environmental impacts and impose costs on society. The harsh lessons of the past need to be applied lest history be allowed to repeat itself.

Key to the achievement of improved environmental management and rehabilitation are the provisions of the MPRDA and particularly the provisions of section 41 of the MPRDA that incorporate the ‘polluter pays principle’ into South Africa’s mining legislation. Among other things, section 41 requires applicants for prospecting or mining rights to make a financial provision “for the rehabilitation or management of negative environmental impacts”. These financial provisions and particularly those relating to mine closure are key tools aimed at ensuring that the taxpayer is not burdened with the costs of rehabilitation. The accurate estimation of the financial provision, the types of financial instruments that may be used, the protection of the provision against claims of other creditors and the reporting of the provision are all important issues for consideration and debate. With this in mind, this discussion document was commissioned by WWF to contribute to improved environmental management in the mining sector by focusing on the process and outcomes of the financial provisions system for mines.

page 2 | WWF-SA Mining Financial Provisions

1.2 Objectives and terms of referenceThe main objective of the research was to provide a critical review of the processes surrounding the making of financial provisions for mine rehabilitation and closure in particular. This is appropriate given the important role financial provisions play in ensuring that mines do not leave a negative environmental legacy after closure.

With this mind, the terms of reference (ToR) were as follows:

Use published sources, stakeholder interviews and other data in order to clearly formulate • the challenges and issues with regard to financial provisions for rehabilitation and closure. It is anticipated that these could take the form of:

Inadequate clarity in legislation;• Constraints associated with the financial instrument choices open to mines with regard • to making financial provisions;.Inadequate funding levels for rehabilitation and closure being maintained and secured;• Limited auditing of the adequacy of financial provisions by the mines and the state;• Inadequate protection of financial provisions in the event of insolvency, sale, etc.• Unclear and potentially misleading financial reporting with regard to financial provisions.•

Based on the review, establish whether the financial provisions system and/or the provisions • themselves that exist at present are insufficient or inadequate to adequately address current and future environmental rehabilitation.Elaborate on the relative importance of key areas of weakness in the system in order to • inform the focus of further research.Make recommendations for potential improvements to the financial provisions system.•

WWF-SA Mining Financial Provisions | page 3

2. APPROACH

page 4 | WWF-SA Mining Financial Provisions

WWF-SA Mining Financial Provisions | page 5

2. APPROACHA phased approach was used with regular team meetings in order to discuss progress and adapt the research process as necessary. The first phase of research was devoted to a lengthy scoping exercise in order to understand the workings of the financial provisions system and identify key areas to focus research in further phases. The areas chosen were those where it was thought recommendations for improvement could be made.

Key information sources included written sources, requested data and interviews with key mining stakeholders, including those involved in environmental as well as financial/accounting matters (see Appendix 1 for a list of people interviewed). We found that most stakeholders interviewed were willing to express their views freely and were eager to contribute to discussions on this important topic.

Throughout the research process the focus was on critical review and analysis in order to provide constructive recommendations on improvements for further discussion. The emphasis was therefore on deepening the debate on these issues in order to arrive at collective improvements and a more sustainable mining industry. In certain instances, issues were simplified to ensure that key issues were not submerged by complexity but were in fact addressed.

Findings and recommendations were broadly grouped in the following areas, which have been used to structure the report:

The overall legislative environment governing mining and financial provisions in particular;• The processes and technicalities associated with determining or estimating the appropriate • funds needed to meet rehabilitation and closure requirements;Financial instruments used to secure financial provisions needed to meet closure • requirements including prudent investment of trust monies;Financial reporting of closure and rehabilitation liabilities in company accounts.•

The study focuses on the systems and mechanisms that govern financial provisions and not on potential human resources capacity constraints within the DMR, although these would appear to be highly relevant.

page 6 | WWF-SA Mining Financial Provisions

3. LEGAL REVIEW

WWF-SA Mining Financial Provisions | page 7

3. LEGAL REVIEW28

The detailed report setting out the legal position on financing mine decommissioning is set out in Appendix 8 to this document. By way of summary we wish to mention the following aspects in the main body of this report:

MPRDA

Section 37 of the MPRDA provides that the principles set out in section 2 of NEMA apply to all prospecting and mining operations.Section 38 of the MPRDA provides that holders of permits or rights in terms of the MPRDA must give effect to the objectives of integrated environmental management laid down in Chapter 5 of NEMA, imposes an obligation to rehabilitate areas affected by mining to its natural or predetermined state and makes the holder of such permits or licences liable for environmental damage, pollution or ecological degradation as a result of their mining activities.

Section 41 of the MPRDA requires an applicant for a prospecting right, mining right or mining permit to make a prescribed financial provision for the rehabilitation or management of negative environmental impacts before the Minister approves the EMP.

Section 1 of the MPRDA defines a “financial provision” to mean “the insurance, bank guarantee, trust fund or cash that applicants … must provide in terms of section 89 guaranteeing the availability of sufficient funds to undertake the agreed work programmes and to rehabilitate the prospecting, mining, reconnaissance, exploration or production areas, as the case may be”.

Section 89 provides that no exploration or production operations may commence unless financial provision has been made that is “acceptable to the designated agency guaranteeing the availability of sufficient funds for the due fulfilment of all exploration and production work programmes by the holder”.

Government Gazette 26275 dated 23 April 2004, item 53-54, sets out the format that such financial provisions may take: a contribution to a trust fund as contemplated in section 10(1)(cH) of the Income Tax Act, a financial guarantee from a bank or financial institution approved by the Director-General, a deposit into an account specified by the Director-General, or such other method as the Director-General may approve.

The inclusion of costs relating to “agreed work programmes” in the definition of “financial provision” appears to relate to “mining work programmes”, which is defined in section 1 of the MPRDA as relating to a work programme to be followed in order to mine a mineral optimally. This appears to be inconsistent with Regulation 54(1) of the MPRDA regulations as the regulations itemise costs making up the financial provision, but make no reference to costs related to the implementation of “mining work programmes”.

Secondly, the definition of “mining area” in Regulation 54 appears to include the underground portion of land for which mining rights were granted, but limits the concept of mining area to surface areas only in respect of adjacent land.

It is uncertain whether the practice of allowing the capital set aside for financial provision to be phased in is legally sanctioned, based on the wording of section 41 of the MPRDA.

28. The authors wish to thank the Centre for Environmental Rights for extensive input and assistance with the drafting of this section of the discussion document.

page 8 | WWF-SA Mining Financial Provisions

National Water Act 36 of 1998

This act finds application to the present context in that section 40 et seq. provides for certain categories of water users to apply for a water use licence, section 19 imposes obligations on certain categories of persons (owners of land or person occupying land) to undertake reasonable measures to prevent pollution of a water resource from occurring, recurring or continuing. In addition, section 30 of the act allows the responsible authority (DWA) to require an applicant or holder of a water use licence to furnish security in respect of any obligation or potential obligations arising from a licence to be issued under the act if deemed necessary for the protection of the water resource or property. This obligation to provide security is insufficiently cross referenced to the financial rehabilitation provisions in section 41 of the MPRDA.

NEMA

The amendments to NEMA intending to incorporate all environmental provisions relating to mining, including the financial provision into Chapter 5 of NEMA, which provisions take effect 18 months after the date of commencement of the Mineral and Resource Development Amendment Act 2008 that to date has not been enacted.Section 28 of NEMA places a retrospective duty of care on persons who cause, have caused or may cause significant pollution or degradation of the environment.

Section 24(5)(d) of NEMA empowers the Minister to make regulations requiring the provision of “financial or other security to cover the risks to the State and the environment of non-compliance with conditions attached to environmental authorisations”. It would be desirable if this obligation in terms of NEMA is explicitly cross referenced to the financial provision in section 41 of the MPRDA to determine the extent of overlap or the extent to which they complement each other.

National Environmental Management Waste Act 59 of 2008

Waste generated by mining is specifically included in the definition of waste, yet the act specifically excludes “residue stockpiles” and “residue deposits”. Accordingly, waste management activities that do not relate to the latter will result in the mining entity requiring a waste licence. It is also uncertain whether and to what extent the contaminated land provisions of the act, once operative, would apply in the mining context.

Promotion of Access to Information Act 2 of 2000

The provisions of this Act are relevant to the present discussion insofar as various environmental groups have attempted to obtain information from the DMR and licence holders relating inter alia to the financial provisions made by mining entities.

Insolvency Act 24 of 1936 and Companies Act 71 of 2008

The impact of the financial provision upon insolvency and whether it is ring-fenced would appear to depend on the format in which the financial provision has been made, i.e. cash, guarantee, insurance or trust fund. The DMR insofar as its claim in respect of the financial provision is concerned, would not be a secured or preferred creditor upon insolvency and as such this has implications for the DMR in the event of insolvency of a mine.

Furthermore, the impact of the business rescue provision of the Companies Act has relevance in that its effect would be to result in a general moratorium on civil legal proceedings and the enforcement of debts may only be carried out with the consent of the business rescue practitioner or the court; accordingly the impact hereof on the ability of the DMR to call up or access the financial provision in terms of section 41(2) of the MPRDA is uncertain.

WWF-SA Mining Financial Provisions | page 9

4. THE FINANCIAL PROVISIONS PROCESS AND KEY CHALLENGES

page 10 | WWF-SA Mining Financial Provisions

WWF-SA Mining Financial Provisions | page 11

4. THE FINANCIAL PROVISIONS PROCESS ANDKEY CHALLENGESThe preceding legal review provides a basic outline of the processes and systems associated with making financial provision for closure. In order to build on this understanding, Figure 1 shows the key elements or steps in the financial provisions process including those falling outside of state mandates associated with financial reporting by companies and related processes. As can be seen from the figure, the financial provisions process requires mining entities to re-assess and adjust their provisions on an ongoing basis to the satisfaction of the authorities (DMR). Parallel to this, mining companies manage their financial provisions and the financial instruments that they use (i.e. trust funds, bank guarantees, etc.) and report on these provisions as part of their financial reporting processes, which is of particularly interest to shareholders.

Figure 1: Key elements in the legislated financial provisions process and reporting

Appropriate amount of financial provisions for closure (planned and pre-mature) determinded by mine as part of EMP.

Mine specifies which financial instrments/methods (trust fund, deposit, bank guarantee insurance) will be used to ensure amount is set aside.

EMP, financial provisions amount and financial instrument checked and approved by DMR using DMR guidelines.

Mining starts once financial provisions agreements signed and financial instruments put in place (e.g. Trust fund is established or bank

guarantees is signed)

Annual revision of EMP and financial provision done by mine and checked by DMR. Adjustments made if needed.

Concurrent rehabilitation is hopefully carried out where possible thereby minimising risks and limiting need for rehabilitation at closure.

Mining stops and closure rehabilitation specified in EMP is undertaken by mine.

DMR checks final rehabilitation and issues closure certificate if satisfied in consultation with other relevant authorities (e.g. DWA)

If mine fails to rehabilitate for whatever reason. DMR can use financial provision to conduct rehabilitation.

Financial instruments maintained (e.g. Trust fund investment portfolio managed)

Ongoing financial reporting of rehabilitation and closure liabilities by mine.

page 12 | WWF-SA Mining Financial Provisions

Based on the scoping stage of the research, the following key aspects were identified as the focus of the remainder of this report:

The potential refinement of the DMR guidelines for the evaluation of the quantum of • closure-related financial provisions;Measures to incentivise concurrent rehabilitation as opposed to rehabilitation conducted • post closure of the mine which in turn impacts on the financial viability of a mine;Amendment of the SAMREC code to allow for greater clarity on how environmental costs • need to be taken into account;Ways of ensuring that the value of trust fund assets is protected by means of prescribed • asset categories;Ways of ensuring that financial provisions enjoy greater protection in the event of • unexpected events such as mining company insolvency;Improvements to financial reporting including “conventional” accounting and auditing • standards as well as newer generation integrated reporting;Greater public accessibility of data and information on financial provisions.•

WWF-SA Mining Financial Provisions | page 13

5. THE ESTIMATION AND ADEQUACY OF FINANCIAL PROVISIONS

page 14 | WWF-SA Mining Financial Provisions

WWF-SA Mining Financial Provisions | page 15

5. THE ESTIMATION AND ADEQUACY OF FINANCIAL PROVISIONSThe first step in the process (through which financial provision is made for mine closure) is the estimation of the amount of money necessary to undertake the required environmental rehabilitation prior to mine closure. The manner in which the amount is determined is therefore critical to the overall success of the financial provisions system. With this mind, this section reviews issues and challenges associated with quantum estimation and makes recommendations for improvement. As such it focuses on how the financial provisions estimation process works, what the outcomes of the practical application of the process teach us, and, how it should improve.

5.1 The process for determining financial provisions for closureBefore commencing with mining, mining companies are required to draw up an EMP in accordance with section 39 of the MPRDA for approval by the DMR and without which mining cannot commence. This EMP must detail how environmental impacts will be dealt with and environmental costs internalised and must include the presentation of a rehabilitation and closure plan (see DMR, 2006 for more detailed guidance on the compilation and format of EMPs). The EMP must (DMR, 2006):

Include a rehabilitation plan showing the areas and aerial extent of the main mining • activities, including the anticipated mined-out area at the time of closure, from which the quantum of financial provision can be calculated in accordance with the DMR guideline.Ensure that the rehabilitation plan is compatible with the closure objectives.• Ensure that the quantum calculation distinguishes between those areas that can be • rehabilitated concurrently and those that can only be rehabilitated at closure.

Once an EMP is approved, the financial provisions and associated rehabilitation and closure plans need to be reviewed annually by the mining company and adjusted if necessary. As with initial estimates, DMR verification and approval are required in keeping with the ongoing monitoring mandate of the DMR.

The process of actually calculating adequate financial provisions for closure is challenging, as the calculations must provide clarity on what actions must be taken together with the cost estimations in respect of such actions, which estimations are based primarily on experience built up over time. As a result, some of the larger mining companies and their environmental consultants have developed rehabilitation and closure cost estimation models that can be applied in this regard. The DMR also has a “Guideline document for the evaluation of the quantum of closure-related financial provision provided by a mine” released in 2005, which is based on work commissioned by Golder Associates (2004) and includes specific guidance with regard to cost estimation (see DME, 2005). The guideline document is not only used by DMR officials when reviewing the financial provisions of mines but also by miners and consultants that don’t have their own closure cost estimation models. It is thus central to the estimation and ongoing monitoring of adequate financial provisions both from a mining company and state authority perspective.

The principles that have been adopted in the Guidelines are as follows (DME, 2005):

Legal standing: The guideline document is to be used by the Regional Office personnel as • a tool to assess the appropriateness of the quantum of financial provision submitted to the DMR by the mining industry. The guideline document does not, therefore, obviate in

page 16 | WWF-SA Mining Financial Provisions

any way the holder of a prospecting right, mining right or mining permit from the legal requirement to annually assess his or her environmental liability and adjust his or her financial provision to the satisfaction of the Minister.Generic nature: The guideline document is generic in nature and cannot answer all possible • questions or deal with all situations relating to financial provision, rehabilitation and mine closure. Further advice and/or experience may be required, based on circumstances that prevail at specific mine sites, to fully assess the quantum for financial provision.Standardized approach: The guideline document’s generic approach aims to avoid a • situation of applying non-aligned empirical approaches and interpretations between DMR Regional Offices.29

Complete picture: The guideline document covers the most essential closure components • that are generally required for the closure of a mine site. Site specific conditions must also be considered and under these circumstances, specialist studies (and related closure costs) on aspects such as surface and groundwater pollution and remediation may be required. The outcome of these studies must be considered in the determination of the quantum to arrive at a complete picture of the quantum for financial provision. The guideline does not adequately address the ongoing post-closure impacts and the financial liability that such impacts impose.The methodology for computing the quantum is based on the assumption that a third party • will be employed by the DMR to undertake the necessary rehabilitation and remedial work should the mining operation close prematurely.

Limitations: The document has certain specific limitations or instances where some sectors of the very diverse spectrum of the mining industry in South Africa are not catered for. The subsistence mining sector (so-called “pick and shovel operations”) is a case in point. These sectors could be the subject of a future guideline. Currently there exists a standard practice to impose a flat rate cash deposit in the case of subsistence mining, which will remain in use for the foreseeable future.

Figure 2 indicates the process and possible routes to be followed in the assessment of the quantum for financial provision for closure according to the DMR guidelines. It shows that the following inputs are required to enable determining of the quantum of financial provision:

Risk ranking for mine type and mineral by-product• Environmental sensitivity of the mining area• Level of information available to the DMR Regional Office personnel• Type of mining operation• Geographic location of the mine• Areas of disturbance: Class A and B mines• Closure costs from specialist studies• Overall size of mine: Class C mines•

29. The Guideline document in fact refers to DME, which it is submitted should read DMR.

WWF-SA Mining Financial Provisions | page 17

Figure 2: The process to be followed in determining the quantum for financial provisions

Source: DME (2005)

The guideline divides closure into the following 14 components in order to facilitate quantum estimation (Step 4.2 in Figure 2):

Dismantling of processing plant and related structures1. (a) Demolition of steel buildings and structures2.

(b) Demolition of reinforced concrete buildings and structures

page 18 | WWF-SA Mining Financial Provisions

Rehabilitation of access roads3. (a) Demolition and rehabilitation of electrified railway lines4.

(b) Demolition and rehabilitation of non-electrified railway linesDemolition of housing and facilities5. Opencast rehabilitation (including final voids and ramps)6. Sealing of shafts, adits and inclines7. (a) Rehabilitation of overburden and spoils8.

(b) Rehabilitation of processing waste deposits and evaporation ponds (basic, salt- producing waste) (c) Rehabilitation of processing waste deposits and evaporation ponds (acidic, metal-rich waste)

Rehabilitation of subsided areas9. General surface rehabilitation including grassing of all denuded areas10. River diversions11. Fencing12. Water management (Separating clean and dirty water, managing polluted water and 13. managing the impact on groundwater, including water treatment)Two to three years of maintenance and aftercare14.

Standard cost factors or so-called “master rates” are then supplied for application in the case of each component along with adjustment/multiplication factors that take into account the risk class of the mine (A, B or C in descending order of risk depending on the material being mined) and the environmental sensitivity of the mining site (see Steps 4.3 and 4.4 in Figure 2). Table 1 provides an example of the master rates and adjustment factors to be used for Component 6 of mine closure: opencast rehabilitation (including final voids and ramps). The guidelines make it clear that these master rates require annual updating for inflation based on CPIX or a similar approved method as one would expect.

Table 1: Master rate and adjustment factors for open cast rehabilitation costs

COMPONENT 6 OPENCAST REHABILITATION (including final voids and ramps)

Unit Master rate

ha 96,700.00

Multiplication factor

Risk Class (A, B or C)

A 0.04 0.52 1.00

B 0.04 0.52 1.00

C 0.04 0.52 1.00

Low Medium High

Environmental Sensitivity

Source: DME (2005)

For planned closure annual contributions are most commonly made to a trust fund where they build up over time and are eventually adequate to cover closure costs. These contributions are calculated annually as (A-B)/C, where (Golder Associates, 2004):

“A” represents the amount determined by a suitably qualified person of the estimated costs to be • incurred at the time that operations of the mine or part of the mine are discontinued in order to discharge the obligations imposed in terms of any law that relates to mining operations.“B” means the market value of the assets held by the company, society, association or trust in • respect of that mine on the date of the determination of the estimated costs in symbol “A”.“C” represents the estimated remaining life of that mine in number of years.•

Figure 3 shows how funds for planned closure build up over time and makes the distinction between providing for planned closure (generally using a trust fund, but also with the option of a bank guarantee or deposit with the DMR) and for premature closure (using non-trust fund methods such as bank guarantees). The guideline specifies that the holder of a prospecting right, mining right or mining permit is required to annually assess the total quantum of environmental liability for the mining operation (points D and A on the graph) and ensure that the financial provision is sufficient to cover the current liability (in the event of premature closure) as well

WWF-SA Mining Financial Provisions | page 19

as the end-of-mine liability. This is referred to as the “window approach” as each assessment provides an indication of the environmental liability at that time only (Point D). The holder will also provide, on an annual basis, an indication of the end-of-life environmental liability (Point A).

Figure 3: Schematic indication of the environmental liability of a mining operation

Source: Golder Associates (2004)

In essence, the system is geared towards guaranteeing that adequate funds are available for planned or premature closure at all times and in all possible circumstances. Mining companies need to re-assess their provisions annually and report on these to the DMR who are then required to examine these provisions critically and ensure that they are adequate. The MPRDA allows the Minister to commission an independent review particularly if there is a dispute between the financial provision estimate submitted by the mining company and those thought appropriate by the DMR. This can be a powerful compliance and enforcement tool if used properly and with sufficient frequency. Previous requests addressed to the DMR for details of the frequency and extent to which the provisions relating to the independent review of the quantum of financial provision have been invoked have not been met with a response as yet.

5.2 Implementation capacity and strategic targetsIt is clear that the current financial provision system requires significant human resource capacity within the DMR for success. Samson30 argues that the MPRDA’s sustainability framework for the development of EMPs is laudable, if somewhat overwhelming from an implementation and compliance perspective. With regard to capacity, the most recently available published figures indicate that in 2009 the DMR employed 78 officials dedicated to environmental protection and monitoring with a further 13 vacant posts.31 The question of whether these staff numbers (and their capacity) are adequate in order to deal with significant monitoring and compliance burdens imposed on the DMR is an important one, although not dealt with as part of this research.

30. McLean, J.K. & Carrick, P.J. Environmental Management and Rehabilitation under the Minerals and Petroleum Resources Development Act: A Biodiversity Outlook. 2007 (14) SAJELP 187-215.31. Source: Reply of the Minister of Mineral Resources to parliamentary question number 1797 on 16 October 2009.

page 20 | WWF-SA Mining Financial Provisions

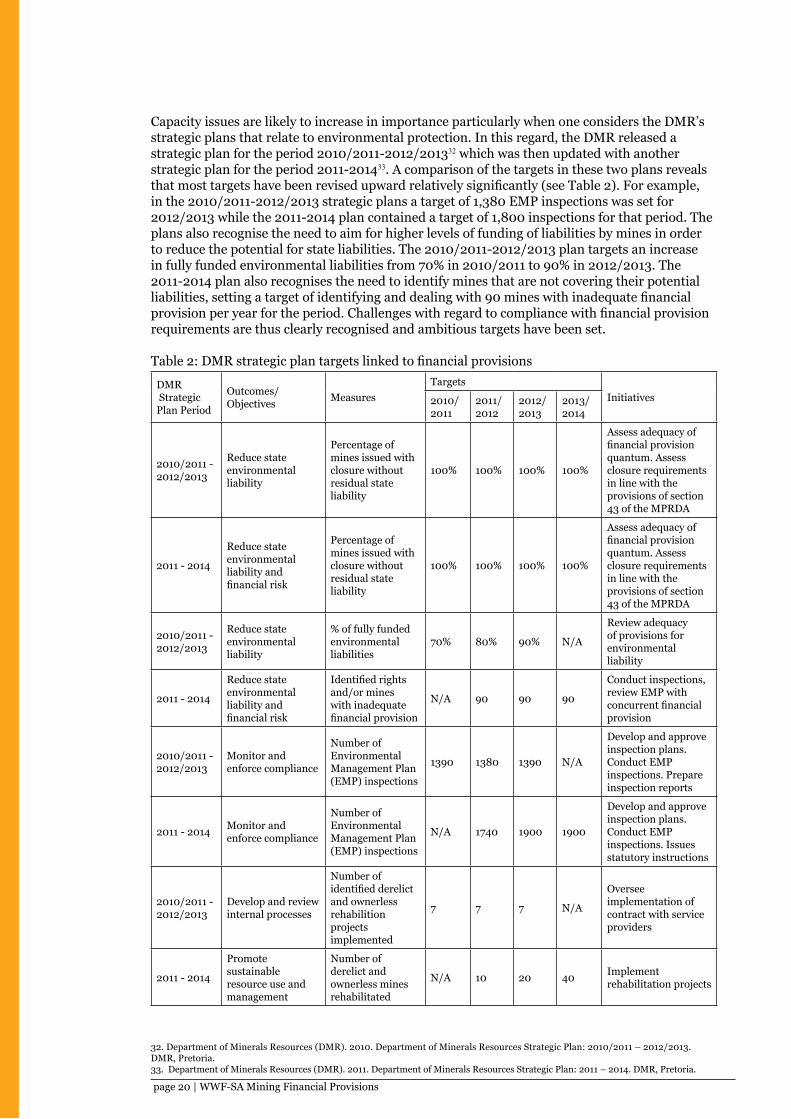

Capacity issues are likely to increase in importance particularly when one considers the DMR’s strategic plans that relate to environmental protection. In this regard, the DMR released a strategic plan for the period 2010/2011-2012/201332 which was then updated with another strategic plan for the period 2011-201433. A comparison of the targets in these two plans reveals that most targets have been revised upward relatively significantly (see Table 2). For example, in the 2010/2011-2012/2013 strategic plans a target of 1,380 EMP inspections was set for 2012/2013 while the 2011-2014 plan contained a target of 1,800 inspections for that period. The plans also recognise the need to aim for higher levels of funding of liabilities by mines in order to reduce the potential for state liabilities. The 2010/2011-2012/2013 plan targets an increase in fully funded environmental liabilities from 70% in 2010/2011 to 90% in 2012/2013. The 2011-2014 plan also recognises the need to identify mines that are not covering their potential liabilities, setting a target of identifying and dealing with 90 mines with inadequate financial provision per year for the period. Challenges with regard to compliance with financial provision requirements are thus clearly recognised and ambitious targets have been set.

Table 2: DMR strategic plan targets linked to financial provisions

DMR Strategic Plan Period

Outcomes/Objectives Measures

TargetsInitiatives2010/

20112011/2012

2012/2013

2013/2014

2010/2011 - 2012/2013

Reduce state environmental liability

Percentage of mines issued with closure without residual state liability

100% 100% 100% 100%

Assess adequacy of financial provision quantum. Assess closure requirements in line with the provisions of section 43 of the MPRDA

2011 - 2014

Reduce state environmental liability and financial risk

Percentage of mines issued with closure without residual state liability

100% 100% 100% 100%

Assess adequacy of financial provision quantum. Assess closure requirements in line with the provisions of section 43 of the MPRDA

2010/2011 - 2012/2013

Reduce state environmental liability

% of fully funded environmental liabilities

70% 80% 90% N/A

Review adequacy of provisions for environmental liability

2011 - 2014

Reduce state environmental liability and financial risk

Identified rights and/or mines with inadequate financial provision

N/A 90 90 90

Conduct inspections, review EMP with concurrent financial provision

2010/2011 - 2012/2013

Monitor and enforce compliance

Number of Environmental Management Plan (EMP) inspections

1390 1380 1390 N/A

Develop and approve inspection plans. Conduct EMP inspections. Prepare inspection reports

2011 - 2014 Monitor and enforce compliance

Number of Environmental Management Plan (EMP) inspections

N/A 1740 1900 1900

Develop and approve inspection plans. Conduct EMP inspections. Issues statutory instructions

2010/2011 - 2012/2013

Develop and review internal processes

Number of identified derelict and ownerless rehabilition projects implemented

7 7 7 N/A

Oversee implementation of contract with service providers

2011 - 2014

Promote sustainable resource use and management

Number of derelict and ownerless mines rehabilitated

N/A 10 20 40 Implement rehabilitation projects

32. Department of Minerals Resources (DMR). 2010. Department of Minerals Resources Strategic Plan: 2010/2011 – 2012/2013. DMR, Pretoria.33. Department of Minerals Resources (DMR). 2011. Department of Minerals Resources Strategic Plan: 2011 – 2014. DMR, Pretoria.

WWF-SA Mining Financial Provisions | page 21

5.3 Review of financial provision estimation practiceHaving established a general understanding of the legislated process through which financial provision estimations are generated, a broad review was conducted focused on the practice of financial provision estimation. Given its central role, the review included a consideration of the efficacy and application of the DMR guideline document released in 2005 for the evaluation of the quantum of closure-related financial provision provided by a mine released in 2005.34 The review relied relatively heavily on interviews and discussions with a broad range of mining stakeholders given the need to draw on direct experience along with the relative lack of written sources.35 With regard to the latter, EMP (and associated financial provisions) case studies were accessed and reviewed where possible bearing in mind that these documents are often difficult to find and interpret. As outlined previously, the review is not intended to be extensive or definitive. Its aim is rather to raise important concerns and encourage discussion on key issues in keeping with the overall focus of the research.

In the sections that follow, the results of the review are discussed with specific reference to the following areas of concern:

Inadequate EMPs and rehabilitation plans including no or tenuous links between the plans • and financial provisions;Non-inflation of master rates contained in the 2005 DMR guidelines;• Reservations that a number of mines are still not making adequate financial provision for • closure;Lack of concurrent rehabilitation.•

5.3.1 Inadequate EMPs and associated rehabilitation plans

The EMPs and associated rehabilitation and closure plans that need to be prepared and regularly updated for mines are central to the accurate estimation of appropriate financial provisions. These plans must describe the concrete actions that are required to adequately mitigate environmental impacts and achieve an acceptable closure. Once these actions have been described in detail, they need to be individually and clearly costed allowing for proper calculation of the overall financial provisions.

Research has indicated that the content and quality of EMPs varies significantly in practice. Cases have been identified where the information contained in the EMP is insufficient both for the DMR to fully evaluate the reported impact of the proposed mining activity, and for the applicant’s subsequent actions to be measured against the EMP’s contents (Brownlee in McLean & Carrick, 2007). The review and interviews with stakeholders revealed that this variability is largely still applicable. The following specific practices can be highlighted as particularly problematic in this regard:

EMPs that do not contain rehabilitation plans at all, making it impossible to trace the links • that should be clearly present between these plans and calculations of financial provisions. The financial provision calculations in these EMPs can be best described as “black box” given their highly significant lack of information and transparency.EMPs that contain insufficient rehabilitation plans with tenuous links to the calculation • of financial provisions. These often contain limited or unclear distinctions between areas that can be rehabilitated concurrent to mining and those that can only be rehabilitated at closure. These can be best described as “grey box” EMPs given their only barely adequate information and low levels of transparency.EMPs that contain inadequate consideration of longer term water quality issues in particular.•

EMPs containing these deficiencies have nevertheless been approved by the DMR. This indicates that the lack of a standard or benchmark EMP, with a further concomitant variability in the qualification and experience of practitioners preparing these EMPs, is a major problem.

34. Hereafter referred to as the “2005 DMR guidelines”.35. See Appendix 1 for a list of people interviewed for the project.

page 22 | WWF-SA Mining Financial Provisions

A standard needs to be established and enforced with appropriately qualified practitioners responsible for the drafting of EMPs.

5.3.2 Non-inflation of master rates

As mentioned above, the 2005 DMR guidelines make it clear that master rates require annual updating in order to take inflation into account (DME, 2005). However, a number of EMPs were found still to be using the master rates contained in the 2005 DMR guidelines.36 This introduces almost certain underestimation of the necessary financial provisions, yet financial provision calculations that do not inflation-adjust their numbers have been accepted by the DMR. For example, a 2010 estimate incorrectly using 2005 master rates could represent an underestimate of roughly 35% relative to appropriately inflated costs.37 It is highly likely that the annual updating of the master rates in the DMR guidelines would put a stop to this practice (see section 5.4.1 for more discussion on this). In the interim, however, for some mining companies and/or their consultants to claim that inflation of costs can be ignored is either extremely naive or disingenuous. The impact that the use of appropriately inflation adjusted master rates may have on the financial viability of certain mines is cause for concern.

5.3.3 Lack of concurrent rehabilitation

The link between the application of concurrent rehabilitation and the need for closure rehabilitation is clear – thorough application of concurrent rehabilitation where possible is one of the best ways to ensure that closure rehabilitation needs and costs are minimised. Environmental managers pointed out that if one applies the principle of “the earlier the better” to rehabilitation it can have a significant impact on reducing future risks. This approach can be particularly effective in ensuring that long term water quality problems do not become difficult to manage. It also allows for greater chances of success with regard to re-establishing the productive potential of land and holds significant aesthetic benefits with potential implications for sectors such as tourism. In most cases, concurrent rehabilitation results in long term cost saving but, importantly, not necessarily in short to medium term cost saving. This has implications for the incentive to apply concurrent rehabilitation. It was also noted in interviews that the incentive structures faced by mine managers (and mining companies) often do not encourage concurrent rehabilitation, focusing instead on conventional and more easily quantified measures such as production, profit, number of accidents, etc.

The application of concurrent rehabilitation has increased over the years in keeping with a growing realisation regarding its benefits. The CoM & Coaltech guidelines devote significant effort to detailing the “how to” of concurrent rehabilitation. However, the mining stakeholders interviewed made it clear that there is still significant underperformance with regard to concurrent rehabilitation generally. Given the links between concurrent and closure rehabilitation, this lack of concurrent rehabilitation can be interpreted as something that does not bode well for the achievement of adequate rehabilitation at closure. In essence, if best practice concurrent rehabilitation was the norm there would be less reason for concern. There is therefore an argument that lack of concurrent rehabilitation can be treated as a leading negative indicator for adequate rehabilitation being achieved at closure.

5.3.4 Reservations regarding adequate financial provisions for closure

There are significant obstacles to generating conclusive, empirically substantiated, independent proof that a particular mine has not made adequate financial provision for closure. This relates not least to the difficulty associated with accessing the required information, conducting a site inspection and securing the cooperation of mine management particularly in the absence of formal authority, legislative mandate or sanction.

36. One of the more prominent cases of this practice is the Environmental Management Plan released in 2009 for Coal of Africa Limited’s proposed Vele Colliery in Limpopo (Jacana Environmental, 2009).37. Note that the master rates in the 2005 DMR guideline were taken unadjusted from the Golder Associates report completed in 2004 (Golder Associates, 2004). It is therefore probably more accurate to consider them as 2004 costs and not 2005 costs.

WWF-SA Mining Financial Provisions | page 23

Notwithstanding these obstacles it was instructive to canvass opinions among mining stakeholders regarding the adequacy of financial provisions on the whole in order to inform further discussions and recommendations. This exercise pointed to the following tentative findings:

As in the case of EMPs, relatively high levels of variability with regard to the perceived • adequacy of financial provisions were reported. Views were that some mines and mining companies appear to be applying the precautionary principle with regard to financial provisions while others clearly are not.Uncertainty with regard to the adequacy of financial provisions appears to be highest in • relation to providing for adequate post-closure water treatment. The costs associated with treatment can be particularly high and combined with uncertainty about what is strictly required can lead to mines effectively trying to downplay or even ignore unacceptable risks.38 These high costs and uncertainties also tend to make it difficult for DMR officials to demand that significant financial provisions be made for water treatment. In addition, the lack of mine closure certificates issued may be interpreted partially as an indication that DWA is not satisfied entirely that water quality impacts have been adequately dealt with (which in turn may imply that financial provisions for these impacts may not be adequate). Formal requests by environmental action groups for information with regard to closure certificates issued by DMR have not been responded to at date of publication of this document.Certain mining companies are thought to be in the process of building up their trust funds • to an adequate level to cover planned closures. They are therefore temporarily inadequate, but one would hope that this is known to DMR and a process is ongoing in which DMR gives these mining companies a certain agreed time frame during which they need to ensure adequate levels are reached for trust funds. The risk of insufficient funds to undertake rehabilitation can be exacerbated where pricing fluctuations in the underlying commodity have a significant impact on the estimated useful life of a mine, which was used as a guideline in calculating the period over which funds were to be built up. It is not clear to what extent these factors are taken into account.Confidence in financial provision estimates is not helped by the lack of publicly available • independent reviews of financial provision calculations.Mining companies in particular, along with industry bodies and investors, are concerned • that aside from their impacts on the environment and the reputation of mining, inadequate financial provisions can give non-compliant mines an unfair cost advantage over their competitors. In addition, the cost implications of having to deal with environmental and pollution risks of so-called “toxic non-compliant” neighbours is an issue, especially to larger mining entities that are subject to increased regulatory and stakeholder controls. This creates an uneven playing field and distorts investment decisions.

These findings with regard to general compliance correlate well with the targets in the DMR’s two most recent departmental strategic plans, which explicitly recognise that more needs to be done to ensure greater compliance with financial provision requirements (see Section 5.2 for an outline of these).

5.4 Recommendations for improvementsThe review in the previous section indicates that despite significant progress as a result of the publication of the 2005 DMR guidelines, challenges remain in the process through which financial provisions are estimated. In keeping with the overall aims of the study, this section makes broad recommendations that should lead to improvements in the financial provisions calculation process. They are focused on the following:

Elevation, enhancement and regular updating of the DMR guidelines for the evaluation of • the quantum of closure-related financial provisions.

38. For example, a 7 Ml/day water treatment plant can cost R200 million to build and have a lifetime running cost of R700 million to R1 billion, albeit that some costs can generally be recovered through the sale of treated water.

page 24 | WWF-SA Mining Financial Provisions

Greater and more structured use of the independent review mechanism when assessing the • adequacy of financial provisions.Greater public access to data and information on financial provisions.• Amendment of the SAMREC code to allow for greater clarity on how environmental costs • need to be taken into account, including potential links to the DMR guidelines for the evaluation of the quantum of closure-related financial provisions.Integrated authorisation/sign-off of EMPs required from the relevant environmental • authorities (DWA and DEA).

5.4.1 Elevation, enhancement and regular updating of the DMR guidelines

The 2005 DMR guidelines for the evaluation of the quantum of closure-related financial provisions have laid a foundation for the estimation of and evaluation of financial provisions. However, as one would expect from the first edition of any guideline, they necessitate review for the following reasons:

Rehabilitation is a dynamic field in which useful research is conducted, techniques evolve • and usable information on what constitutes effective rehabilitation and the associated costs is constantly generated and can be used to refine financial provision estimates. This includes information from mines themselves, environmental experts, contractors, researchers and the state (particularly through the rehabilitation of abandoned mines). For example, one of the top priorities for Coaltech sponsored research is preventing and mitigating the impacts of land compaction, about which not enough is understood at present.The need to reflect changes in environmental legislation that determines the nature and • extent rehabilitation required (e.g. if legislation on water quality standard becomes stricter then rehabilitation and closure requirements must adjust accordingly).The guidelines may require modification to take into account changes in the environmental • landscape (e.g. water scarcity may result in stricter guidelines as to how water pollution prevention should be dealt with in rehabilitation and closure requirements).The need to avoid ambiguity or uncertainties or lacunae with regard to issues such as the • appropriate use of inflation adjustment and any other areas where greater clarity is needed, as one would expect with the first edition of a guideline.39

In order to draw the full potential out of the guidelines (and associated updating processes) it is recommended that serious consideration be given to:

Augmentation of the guidelines to ensure that they remain clear, comprehensive and • responsive to changes and actively draw on industry/stakeholder experience and advances on an ongoing basis;Drawing on and incorporating other relevant resources such as the 2008 DWA best practice • guideline series and the CoM & Coaltech guidelines on rehabilitation;Clarifying links between the EMP guidelines and the DMR financial provision calculation • guidelines to ensure comprehensive, easily referenced and quantified rehabilitation plans in EMPs;Incorporation of measures to incentivise concurrent rehabilitation.•

These actions should ensure that the status of the guideline is elevated allowing it to become more effective in its primary aim of allowing for more accurate closure cost estimation. It should also improve the probability that it (or at least key elements of it) becomes more widely used by mining companies in their financial provision calculation processes. As was noted in the input document to the DMR guidelines (i.e. Golder Associates, 2004), there would be “… significant benefits if the guideline document were to be used by both the DMR and the mining industry, in order to align the assessment of the environmental liability for a mine.”

39. E.g. the master rate for Component 6 (Opencast rehabilitation) in the 2005 DMR guidelines is the only master rate that differs from the master rates in the Golder Associates input document to the guideline (i.e. R96,700/ha in the DMR guideline and R99,600/ha in Golder Associates). This may be a small difference in percentage terms (i.e. 3%); it is, however, significant in absolute terms and should be rectified if needed. Most financial provision calculations reviewed use the DMR master rate although two were found that used the Golder Associates master rate.

WWF-SA Mining Financial Provisions | page 25

5.4.1.1 Augmentation process and creation of a living document

In order to ensure that the guideline remains up to date, it would be worth considering the process surrounding its updating. This could include: