Embed Size (px)

Citation preview

FINANCIAL MANAGEMENT

Presentation to Members by The Head of Finance, Donna Laws

20 July 2007

Content

• General Introduction to Finance• Financial Regulations & Financial Grant

Memorandum• The Budget & MTFP • Financial Planning, Management & Control• 2008/09 Budget and Service Plan Process• Future Pressures

The Finance Team

Cornelia Angell-ReimersSenior Finance Officer

Rob ButlerFinance Officer

Steve KentFinance Officer

Financial Services Objectives

To provide effective and efficient financial services to meet the legislative and operational demands of the National Park Authority, its Committees and Management

To support the Authority’s Members, Committees and Service Directorates in achieving the optimum utilisation of resources.

To contribute to strategies, policies and other activities to support the achievement of the Authority’s strategic objectives and priorities

What does Finance do?(one)

• Strategic financial advice, financial planning & evaluation• Preparation of the Revenue & Capital Budget and Medium

Term Financial Plan• Financial management, monitoring and control• Preparation & submission of year end accounts• Managing working capital / Treasury Management • Preparation & submission of all statutory returns to Defra &

Central Government• Preparation & submission of bids for external funding, claims

& returns and provide accounts for audit.

• VAT and taxation compliance

What does Finance do? (two)

• Internal Audit & External Audit• Local Government Pension Scheme• Managing relationships with financial institutions • Maintain/operate the fixed asset register & other inventories• Establish & maintain the Authority’s Financial Regulations,

ensuring that everyone complies with them• Issue purchase orders, pay creditors, raise debtor invoices• Receive & account for all income, plus monthly bank rec.• Process travel claims & make travel/accommodation

bookings• Procurement

Services bought in / external relationships

Economy of scale means that the Authority buys-in a number of its support services to varying degrees:

Devon County Council Section 151 Officer, Internal Audit, VAT,

Payroll, Pensions & ICT

Audit Commission Statutory Audit, Value for Money Studies,

Best Value, Corporate Governance

Other Devon Procurement Partnership

Statutory Accounting Framework & Legislation

• Local Government and Housing Act 1989 • Audit Commission Act 1998• Local Government Act 1999• The SORP – the Chartered Institute of Public Finance &

Accountancy Statement of Recommended Practice• National Parks In England Grant Memorandum 2000

(currently being revised)• Accounts and Audit Regulations 2003• Financial Regulations, Standing Orders and Scheme of

Delegation approved by the Authority. • Best Value Accounting Code of Practice (BVACOP)• And many more including the Prudential Code, Risk

Management, Corporate Governance and Pensions

Financial Regulations

Financial Regulations & Financial Grant

Memorandum

Financial Regulations

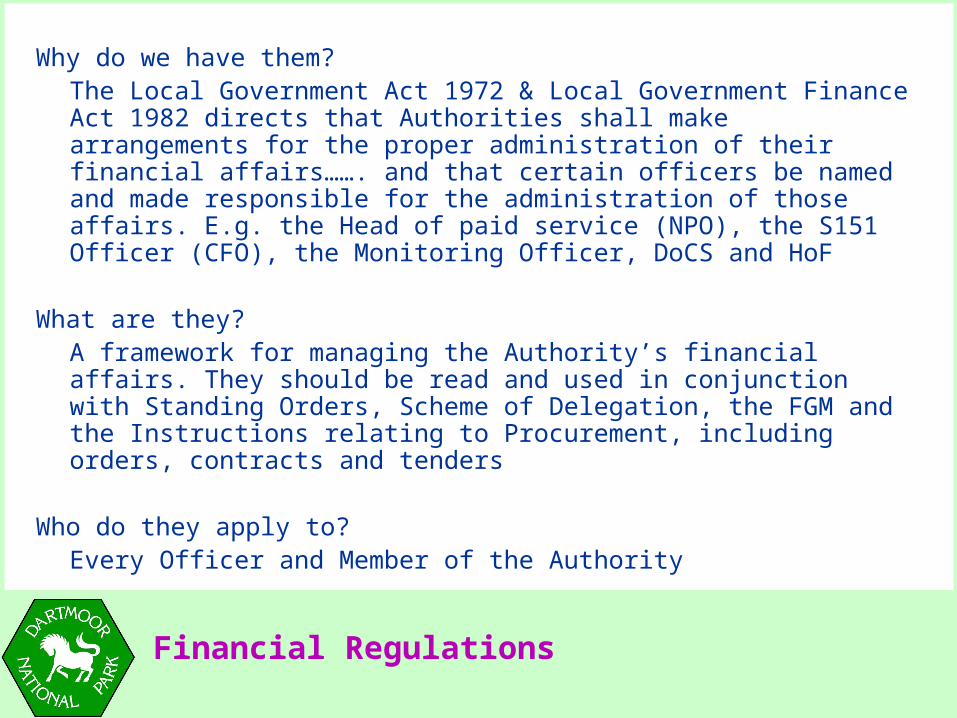

Why do we have them?The Local Government Act 1972 & Local Government Finance Act 1982 directs that Authorities shall make arrangements for the proper administration of their financial affairs……. and that certain officers be named and made responsible for the administration of those affairs. E.g. the Head of paid service (NPO), the S151 Officer (CFO), the Monitoring Officer, DoCS and HoF

What are they?A framework for managing the Authority’s financial affairs. They should be read and used in conjunction with Standing Orders, Scheme of Delegation, the FGM and the Instructions relating to Procurement, including orders, contracts and tenders

Who do they apply to?Every Officer and Member of the Authority

Financial Regulations

What do Financial Regulations tell us?

• The principles• Section A – Financial Management• Section B – Financial Planning & Control of Expenditure• Section C – Risk Management & Control of Resources• Section D – Systems & Procedures• Section E – External Arrangements

You need to know where to find them, you must comply with them and are ultimately responsible for ensuring that the Authority and its staff also complies with them

Financial Grant Memorandum

• Explains who we are, how we were formed, how we are funded and how we should operate financially

• Source of funds• Levying (VAT implications)• How our financial cycle fits with that of Defra• Directs how we submit bids and budgets and how to claim

the grant• Lays down prescribed reporting formats (financial, BVPP,

Corporate Plans, NPMP etc)• Is currently being reviewed in conjunction with the creation

of a NPA specific BVACOP SEA format

The Budget & MTFP

The Budget and MTFP

The 2007/08 Revenue Budget

2007/08 Revenue Budget

The Authority has a statutory duty to set a balanced budget £

Gross expenditure 5,466,664

Income from fees & charges (810,002)Net Budget 4,656,662

Financed from:National Park Grant (Defra) (4,321,078)Planning Delivery Grant (DCLG) (28,452)Slippage B/fwd (105,600)Authority Reserve Balances (201,532)Total (4,656,662)

2007/08 Revenue Budget & MTFP

Breakdown of Net Budget:2007/08 2008/09 2009/10 £ £ £

Salaries & Travel 3,523,091 3,586,228 3,730,267Other core running costs:Premises/Estab/Transport 702,212 721,144 742,778Discretionary spend 1,241,361 1,033,977 1,042,232Income from fees, charges& partners & PDG (810,002) (652,443) (623,469)Net Budget 4,656,662 4,688,906

4,891,808PDG (28,452) 0 0NPG (4,321,078) (4,429,105)

(4,539,833)Shortfall 307,132 259,801 351,975The shortfall is currently being met from reserves & slippage b/fwd

Financial Management & Monitoring

Outturn position2006/07 2005/06 2004/05 2003/04 £ £ £ £

Outturn (215,497) (95,631) (40,460) (552,987)Slippage b/fwd (158,707) (140,101) (123,991) (129,530)Slippage c/fwd 156,423 158,707 140,101 123,991Appropriations (9,269)*** (70,000)** 0 541,000*Net underspend (227,050) (147,024) (24,350) (17,526)% of net budget -5.14% -2.26% -1.03% -14.63%

Plus:BMF not used (145,423) (48,074) (196,260) 0

*Created the budget management fund **NPAPA, Ancient Woodlands, Day visitor Survey

***Capital - Haytor

Reserves

Reserve Balances at 1 April 2007

£

General Reserve (statutory) 270,000

(Represents 5.8% net budget)

Unapplied capital receipt 11,500

Provision for legal costs 12,000

Pension fund provision 41,903

Provision for external (match) funding 85,370

Reserves

£Buildings Reserve:

Haytor 229,231 Accommodation 100,000

Newbridge 150,000 Unallocated 97,574

576,805

Budget Management Fund 834,015 Less commitments to the MTFP (813,308) 20,707

2008/09 Budget

The 2008/09 Budget, MTFP&

Service Planning Process

What drives the budget?

The budget is driven by the:

• National Park Purposes• The National Park Management Plan• The Corporate Plan & Corporate Priorities• Defra expectations for National Parks

Three year zero based budgets are submitted by Heads of Service for work programmes that demonstrate the achievement of all of the above.

The budget and service planning process

The process starts in July / August

• Determine level of NPG and how much of our reserves we can afford to utilise

• Review fees and charges

• Heads of Service submit service plans containing a proposed prioritised work programme, detailing the staff resources & budgets required for each service / area of activity, demonstrating compliance with objectives and setting performance targets

• Directors examine service plans with their teams and start to cut or refine anything that is not a priority or will not help us achieve our objectives

The hard part – how do you get a balanced budget?

• 1st draft budget produced by the HoF and any shortfall identified (budget gap)

• The SMT reviews the draft budget & service plans, gives strategic direction to HoS and makes the first amendments / cuts if required

• Members scrutinise & challenge the draft budget and service plans & give further strategic direction to the SMT and HoS

• 2nd draft budget produced and any shortfall identified

• Further scrutiny and cuts have to be made if the budget and MTFP is still proving unaffordable and unsustainable

• The budget is finally approved in Feb/March

The even harder part

We must do the same for 2 more years, which then gives us a three year Medium Term Financial Plan. Which must be:

• Affordable• Sustainable• Prudent

The whole process is difficult and hard decisions have to be made, especially when the indication from Defra is that NPG will continue to be very tight.

However, now the Authority has a much clearer strategic direction as laid down in its Corporate Plan and with the imminent delivery of the New Management Plan, this process should become easier, even in the face of poor funding settlements.

Future Pressures

• The outcome of the CSR07 – will we still be facing a standstill grant settlement or below inflation increase?

• The S33 VAT issue surrounding the levying powers• The financial impact of Job Evaluation, both in terms of

back pay and future years costs• Maintaining Parke to the standards required by the NT, or

out-growing it and having to find new premises• Staff capacity issues - still many projects and corporate

governance issues to address whilst doing the ‘day-job’• Continuing small annual increases in employer

superannuation contribution rates