Embed Size (px)

Citation preview

FINANCIAL MANAGEMENT: A COURSE FOR

SCHOOL NUTRITION DIRECTORS

Gilbert Requena, FNP Specialist

National Food Service Management Institute February 06, 2014

Acknowledgement Statement 2

You understand and acknowledge that:

The training you are about to receive does not

cover the entire scope of the program; and that

You are responsible for knowing and understanding

all handbooks, manuals, alerts, notices and

guidance, as well as any other forms of

communication that provide further guidance,

clarification or instruction on operating the program

Learning Objectives

3

Identify basic financial statements used in the school nutrition program

Describe the process used in a school financial management information system

Identify conditions that impact the financial status of school nutrition programs

Determine appropriate adjustments required to improve the financial position in a school nutrition operation

Chapter 1 Importance of Financial

Management 4

Objective: Know the importance of financial

management to nutritional integrity and fiscally sound

operations in the school nutrition program

Can you answer these financial management questions

about the school nutrition program in your district?

5

Main sources of revenue?

Percentage of total revenue attributed to

each source?

Expenditure categories?

More questions?

6

Cost to produce a meal?

Percent of revenue spent for labor or food?

Labor productivity index (meals per labor

hour)?

More questions?

7

Net gain or loss over the past 3 years?

How many employees understand the

importance of cost controls to the success of the

program?

Defining Financial Management

8

Financial Management can be defined as

The process of defining the financial goals and

program objectives for the school nutrition

program, and

Implementing activities to attain those goals

through the effective use of resources

Activities for More Effective Financial Management

9

School nutrition programs should

plan through the budget process,

apply more efficient cost control measures,

increase productivity, and

identify ways to increase resources.

Role of the School Nutrition Director in Managing

Finances 10

Management of financial resources

Maintain financial accountability

Involve administrators, board members, cafeteria managers, and nutrition staff to identify goals

Promote team approach

Assess, monitor, and evaluate program funds

Maintain on-going training

Chapter 2 Development of a Financial Management

System 11

Objective: Know the basic financial recording

and reporting processes and procedures for

directing the operation of a school nutrition

program

Financial Management Information System

12

Provides a uniform and consistent financial

reporting structure

Provides meaningful and timely financial

management information

Supports federal reporting requirements

Financial Management Information System (cont.)

13

Adheres to Generally Accepted Accounting

Principles (known as GAAP)

Provides a basis for determining accountability

Generally Accepted Accounting Principles (GAAP)

14

uniform standard of guidelines for financial

accounting established by the Governmental

Accounting Standards Board (GASB)

used in school districts for compliance with the

Federal Department of Education requirements

NFSMI Financial Management Information System

Available at

www.nfsmi.org

15

Classification of Expenditures

Labor

Employee Benefits

Professional and

Technical Services

Property Services

Food and USDA

Foods

Supplies

Capital Equipment

Miscellaneous

Indirect Costs

Fund Transfer-Out

16

Chapter 3 Financial Reporting of Revenue and

Expenditure Transactions 17

Objective: Know how to use financial reports

that are consistent with federal and state

guidelines to achieve a financial management

system that supports a cost effective program

with high integrity

Types of Financial Reports

18

Statement of Revenue and Expenditures (Net

Gain/Loss Statement)

Statement of Net Assets (Balance Sheet)

Budget

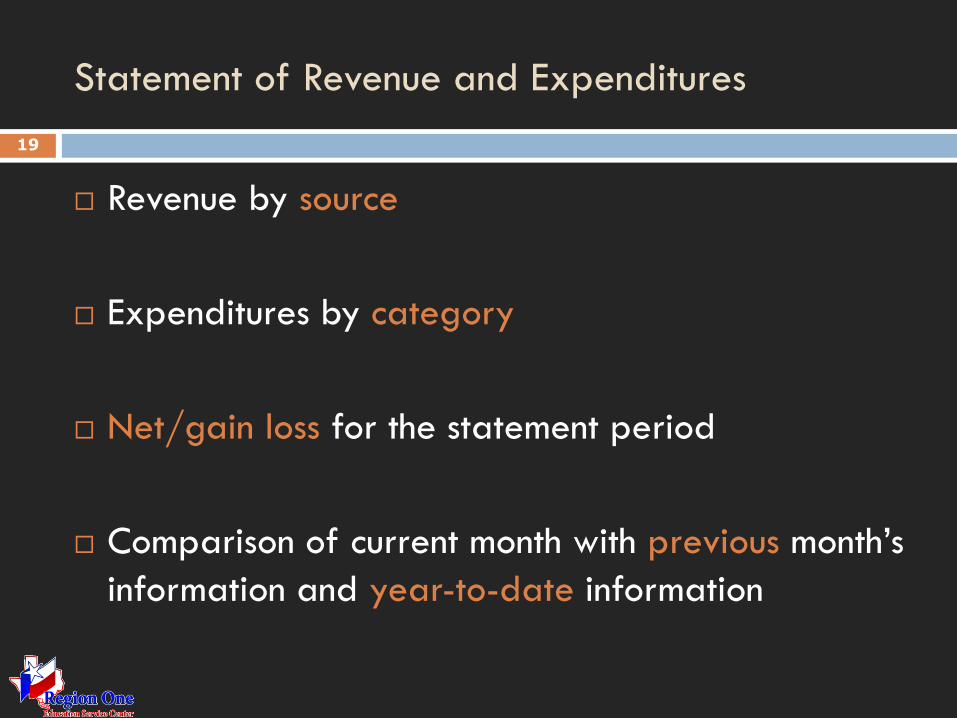

Statement of Revenue and Expenditures

19

Revenue by source

Expenditures by category

Net/gain loss for the statement period

Comparison of current month with previous month’s

information and year-to-date information

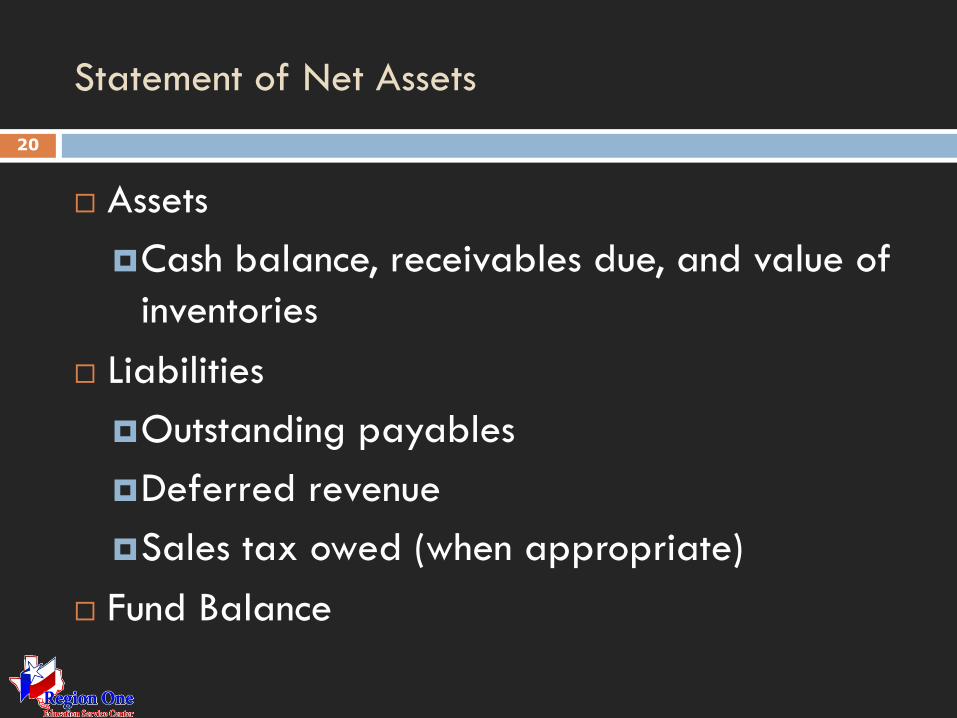

Statement of Net Assets

20

Assets

Cash balance, receivables due, and value of

inventories

Liabilities

Outstanding payables

Deferred revenue

Sales tax owed (when appropriate)

Fund Balance

The Budget as a Management Tool

21

The budget assists in managing the school nutrition program by forecasting revenue,

identifying how revenue will be allocated for

expenditures, and

predicting how much money will be in the fund balance at year’s end.

Methods of Budgeting

22

1. Incremental (baseline) – Previous year’s

budget is starting point. Adjustments made

to each line item to reflect expected changes

2. Zero – Start with zero for each line item and

build according to expectations

3. Combination – Uses zero for some items and

incremental for other items

School Budgets

23

Public Documents

The school nutrition program is a nonprofit operation conducted for the benefit of children.

The program is tax supported.

Public has a right to expect the nutritional needs of children are met in the most cost effective way.

Chapter 4 Setting a Meal Standard for Financial

Management and Analysis 24

Objective: Know how to use financial

management tools and standards to operate a

financially and nutritionally accountable school

nutrition program consistent with federal and

state guidelines

Using Meal Equivalents in Program Analysis to Measure

Performance

25

By converting food sales to meal equivalents,

the school nutrition director can determine

meal cost,

labor productivity ratios, and

the average revenue earned per meal/meal

equivalent.

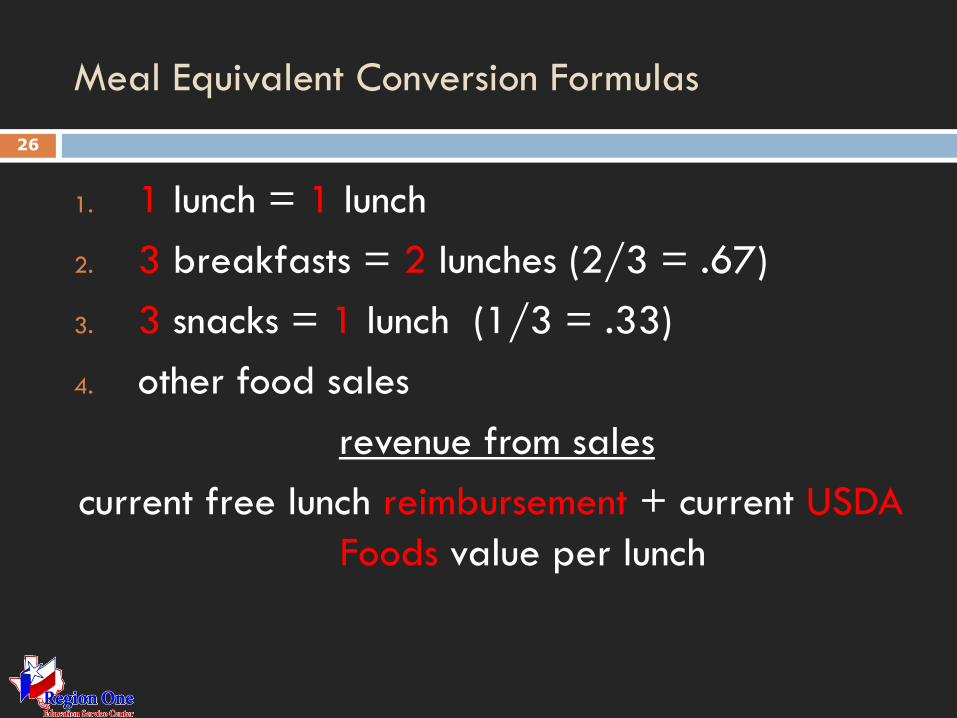

Meal Equivalent Conversion Formulas

26

1. 1 lunch = 1 lunch

2. 3 breakfasts = 2 lunches (2/3 = .67)

3. 3 snacks = 1 lunch (1/3 = .33)

4. other food sales

revenue from sales

current free lunch reimbursement + current USDA

Foods value per lunch

Chapter 5 Managing Revenue in School Nutrition

Programs 27

Objective: Know how to analyze, interpret, and

use revenue data for program evaluation and

improvement

Revenue Accountability

28

USDA mandates accountability

for all revenue received,

how that revenue is dispersed, and

that the revenue generated is sufficient to

sustain a nutrition program that serves food

high in quality and nutritional value.

Revenue Analysis

29

Calculate average revenue per meal or meal

equivalent

Establish consistent guidelines for pricing

meals and other food items for sale

Compare revenue generated per meal with

costs per meal

Why it’s important to compare revenue earned with

meal cost

30

This comparison is useful because

it helps determine if and where revenue

needs to be increased,

it allows you to analyze revenue by source,

and

it identifies areas in which revenue should be

monitored for revenue loss.

Paid Lunch Equity and Non Program Food Revenue

31

Sections 205 and 206 of the Healthy, Hunger Free Kids Act (HHFKA) established requirements for

Revenue from paid reimbursable lunches [7 CFR 210.14 (e)]; and

Revenue from foods sold outside of reimbursable meals when those foods are purchased with school food service account funds [7 CFR 210.14 (f)].

Paid Lunch Equity

32

The Act directs SFAs to:

Compare the average price charged for lunches served to students not eligeble for free or reduced price lunches (1.3., “paid lunches”) to the difference between the higher Federal reimbursement provided for free lunches and the lower Federal reimbursement provided for paid lunches.

If the average paid lunch price is less than the difference, an SFA must either gradually adjust average prices or provide non-Federal funding to cover the difference (For SY 13-14 the price is $2.59)

Calculating the Price

33

The amount of he per meal increase is

calculated using 2 percent plus current SY

inflation rate.

2013-2014 Calcualtion: 2% + 2.93% (SY

2012-2013 inflation rate), or 4.93 percent

SY 2013-2014 non-Federal source

34

For SY 2013-2014: non-federal source

1. Per-Meal non-federal reimbursement for any

paid meal (breakfast, lunch, etc.)

2. Any funds provided by organization for any

paid meal

3. Any proportion attributable to paid meals

from direct payments made from school

district funds to support lunch service.

Three-month operating balance 35

For SY 2013-2014 State agencies, upon request by

an SFA, should exempt an SFA from the paid lunch

Revenue requirements if the SFA: has been certified

as meeting the meal pattern requirements, and; can

demonstrate that the required increase to paid

lunch prices or revenue contributions would cause

the SFA to exceed the three-month operating

balance limit.

Paid Lunch Equity: 2013-2014 36

While flexibilities are available for SY 2013-2014,

FNS will carefully evaluate the information and

data gathered from State agencies regarding how

these policies are being implemented in order to

better understand their impact on school food

service revenue and whether they further the goals

of the HHFKA.

SY 2013-14 PLE tool 37

A PLE tool is available on the FNS website to help

SFAs calculate the price of lunch

The tool can be retrieved at

http://www.fns.usda.gov/cnd/governance/policy.htm

Revenue from Nonprogram Food 38

Section 206 of the Healthy, Hunger-Free Kids Act of

2010 requires that the proportion of total school

food service revenue provided by the sale of

nonprogram foods to the total revenue of the school

food service account must be equal to or greater

than the proportion of total food cost associated

with obtaining nonprogram foods to the total costs

associated with obtaining program and nonprogram

foods from the account.

Revenue From Nonprogram Foods 39

Intent: To ensure that revenues from the sale of

nonprogram foods generate at least the same

proportion as they contribute to SFA foods costs

Revenue From Nonprogram Food 40

To implement this requirement SFAs will nee to:

Identify the proportion of total food costs attributable

to nonprogram food in order to establish its revenue

target

Price nonprogram food items to ensure that revenues

will meet the requirement

Track nonprogram food revenues separately from all

other revenue items

What are nonprogram foods 41

Examples of nonprogram foods that require tracking to ensure revenue generated is in the same proportion as costs are:

1. Single Item Sales: A la carte an individual meal components

2. School Meals: School meals served to adults and second meals served to students

3. Special School Functions: Refreshments, banquets, and special meals such as athletic meals, etc.

4. Contract Meals: Catered, organization contracts such as YMCA, community events.

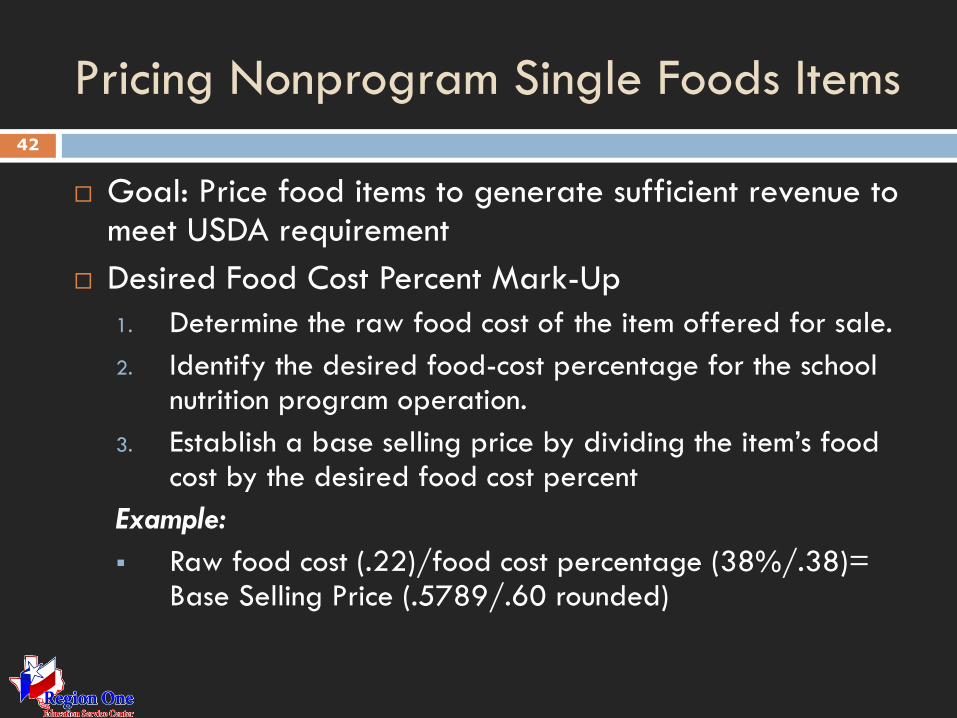

Pricing Nonprogram Single Foods Items 42

Goal: Price food items to generate sufficient revenue to meet USDA requirement

Desired Food Cost Percent Mark-Up

1. Determine the raw food cost of the item offered for sale.

2. Identify the desired food-cost percentage for the school nutrition program operation.

3. Establish a base selling price by dividing the item’s food cost by the desired food cost percent

Example:

Raw food cost (.22)/food cost percentage (38%/.38)= Base Selling Price (.5789/.60 rounded)

Pricing Nonprogram Single Food Items 43

Handout 1

Example: Calculating A la carte and Individual Menu

Components

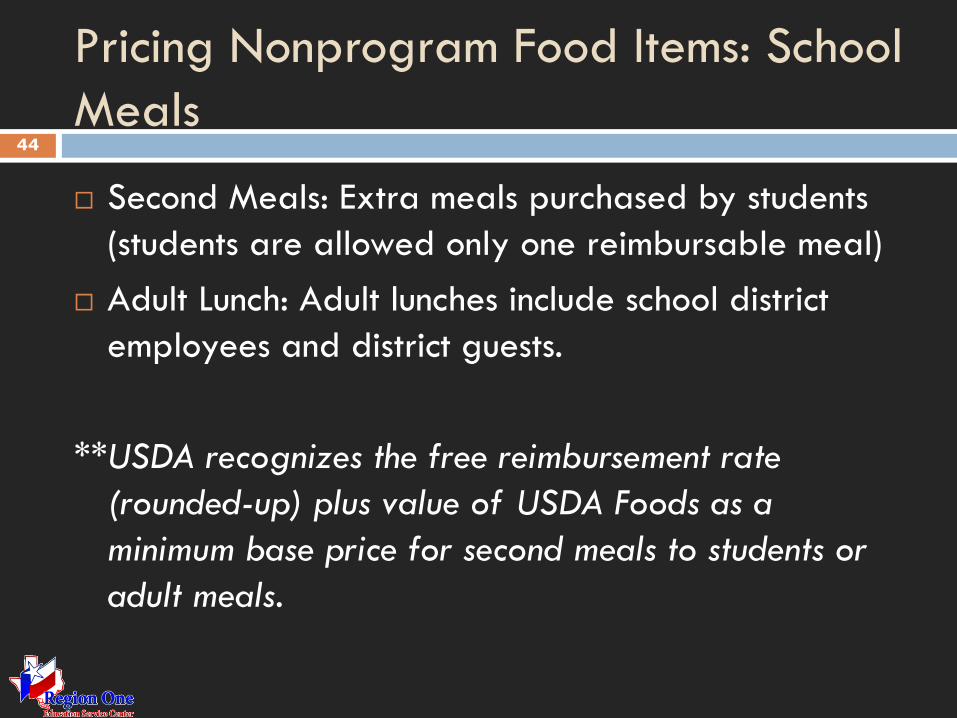

Pricing Nonprogram Food Items: School

Meals 44

Second Meals: Extra meals purchased by students

(students are allowed only one reimbursable meal)

Adult Lunch: Adult lunches include school district

employees and district guests.

**USDA recognizes the free reimbursement rate

(rounded-up) plus value of USDA Foods as a

minimum base price for second meals to students or

adult meals.

Pricing Non-Program Food Items:

School Meals 45

Handout 2

Example: Calculating Nonoprogram School Meals

Pricing Nonprogram Food Items:

Contract Meals/Special Occasions 46

Specialty nonprogram meals served outside the school day include

Catered meals,

Contract meals, and

School function meals such as banquets.

Special Occasions could include

Refreshments for a faculty event (cookies/fruit punch), or

Sandwiches for administrative functions or guest meetings.

Pricing NonProgram Food Items:

Contract Meals/Special Occasions 47

Handout 3

Example: Calculating Special School

Functions/Contract Meals

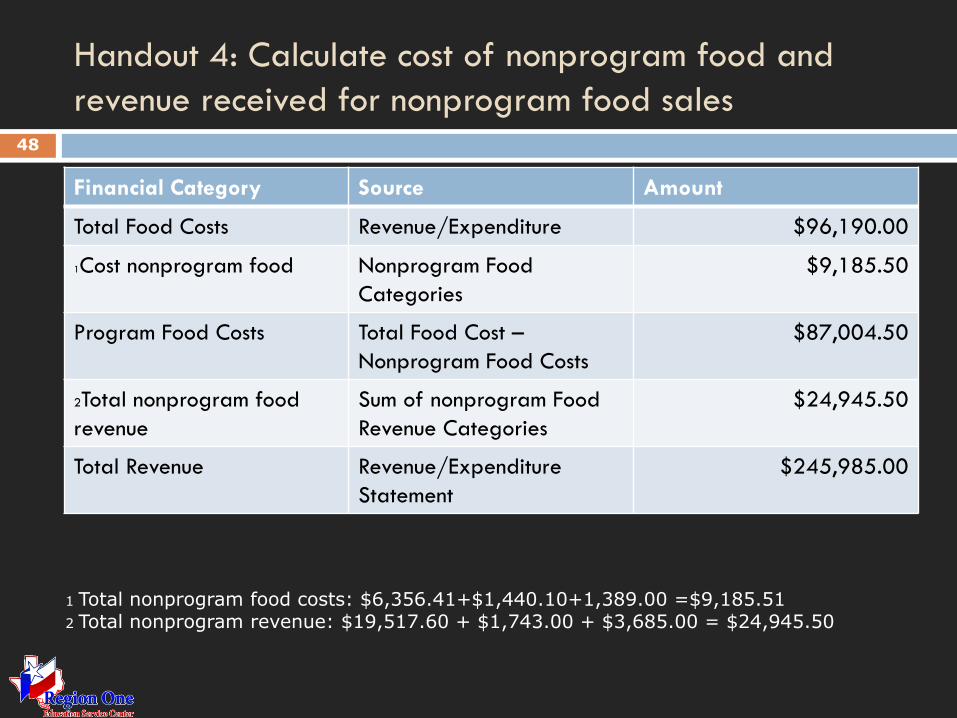

Handout 4: Calculate cost of nonprogram food and

revenue received for nonprogram food sales 48

Financial Category Source Amount

Total Food Costs Revenue/Expenditure $96,190.00

1Cost nonprogram food Nonprogram Food

Categories

$9,185.50

Program Food Costs Total Food Cost –

Nonprogram Food Costs

$87,004.50

2Total nonprogram food

revenue

Sum of nonprogram Food

Revenue Categories

$24,945.50

Total Revenue Revenue/Expenditure

Statement

$245,985.00

1 Total nonprogram food costs: $6,356.41+$1,440.10+1,389.00 =$9,185.51 2 Total nonprogram revenue: $19,517.60 + $1,743.00 + $3,685.00 = $24,945.50

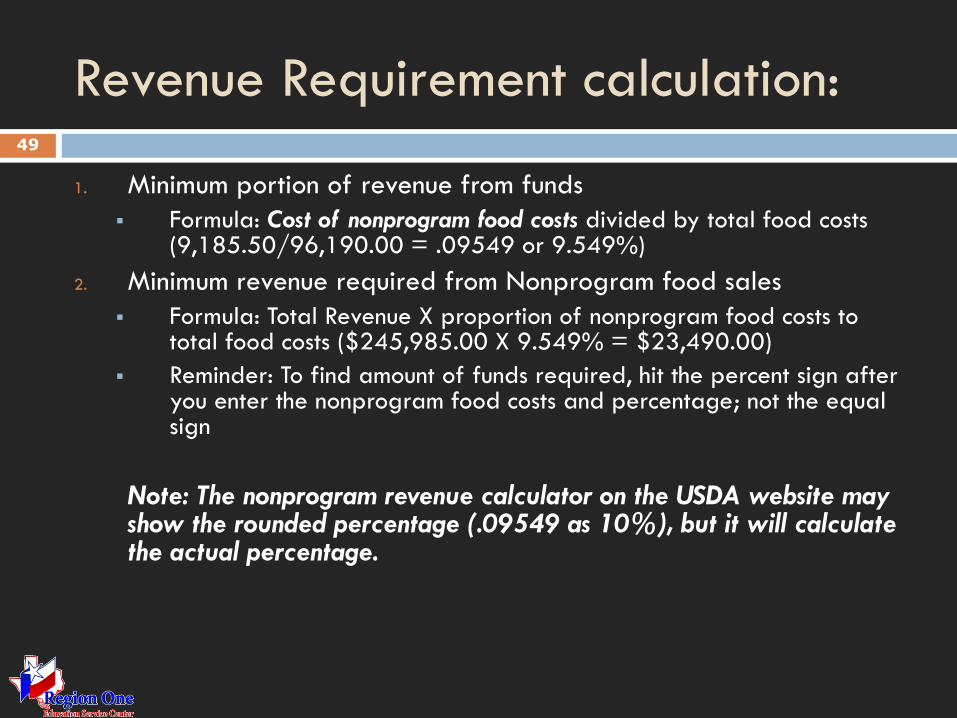

Revenue Requirement calculation: 49

1. Minimum portion of revenue from funds

Formula: Cost of nonprogram food costs divided by total food costs (9,185.50/96,190.00 = .09549 or 9.549%)

2. Minimum revenue required from Nonprogram food sales

Formula: Total Revenue X proportion of nonprogram food costs to total food costs ($245,985.00 X 9.549% = $23,490.00)

Reminder: To find amount of funds required, hit the percent sign after you enter the nonprogram food costs and percentage; not the equal sign

Note: The nonprogram revenue calculator on the USDA website may show the rounded percentage (.09549 as 10%), but it will calculate the actual percentage.

Checking Compliance 50

http://www.fns.usda.gov/cnd/governance/legislation/

CNR_2010.hmt

Focus of School Nutrition Programs 51

The main focus of the school nutrition program is to

provide good nutrition that promotes the health and

wellness of students so they can be more productive

in the classroom.

Chapter 6 Managing Expenditures in the School

Nutrition Program

52

Objective: Know how to analyze, interpret, and

use expenditure data for program evaluation

and improvement

Expenditure Analysis

53

Analyzing financial reports can provide

information about

patterns or trends,

significant changes in costs categories,

deviations from financial goals,

possible abuse or theft, and

transaction errors.

Types of Expenditure Analysis

54

Total costs to produce a meal

Meal costs per expenditure category

Percentages of operational costs to total

revenue

Costs to produce a meal compared with the

average revenue generated per meal

Meal Costs Deviations

55

Higher food costs at the beginning of the year

due to larger than normal food purchases

Purchase of a large ticket item

Unplanned large repair bills

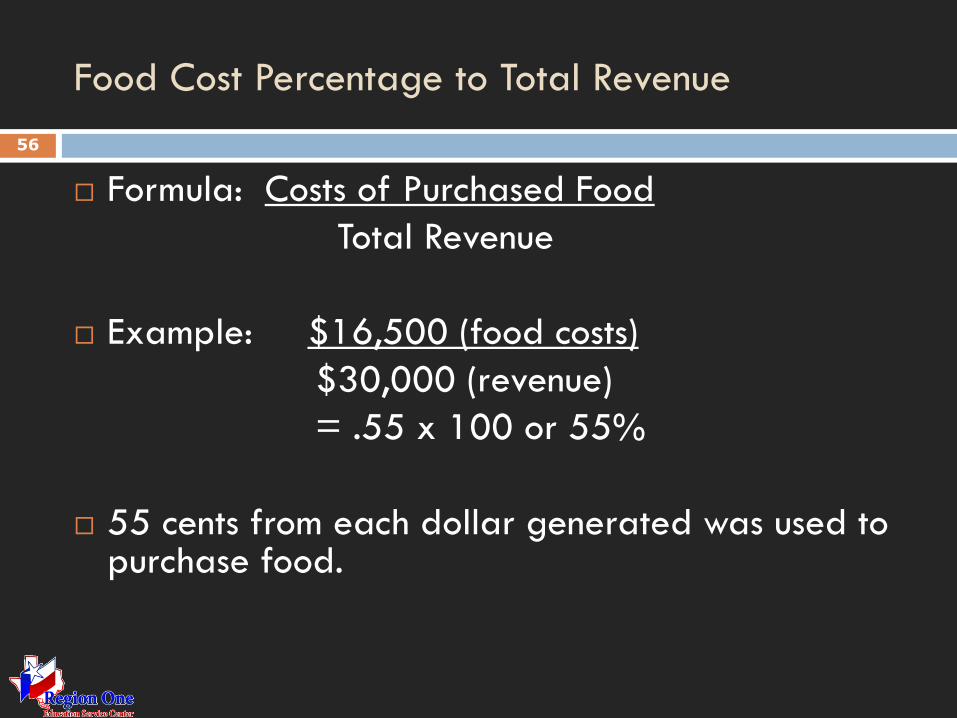

Food Cost Percentage to Total Revenue

56

Formula: Costs of Purchased Food

Total Revenue

Example: $16,500 (food costs)

$30,000 (revenue)

= .55 x 100 or 55%

55 cents from each dollar generated was used to purchase food.

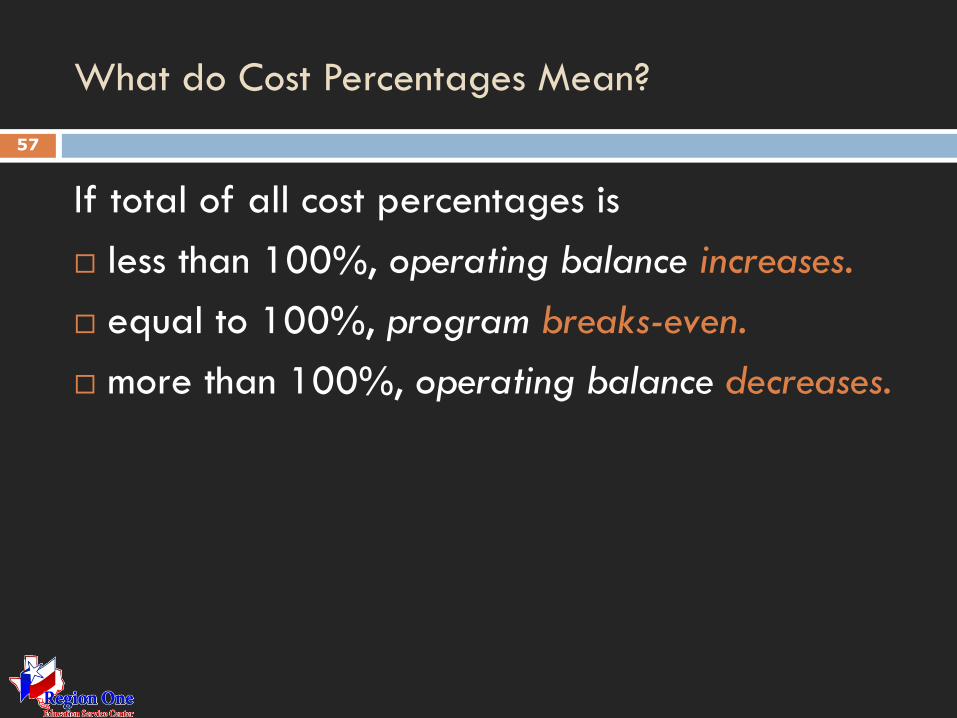

What do Cost Percentages Mean?

57

If total of all cost percentages is

less than 100%, operating balance increases.

equal to 100%, program breaks-even.

more than 100%, operating balance decreases.

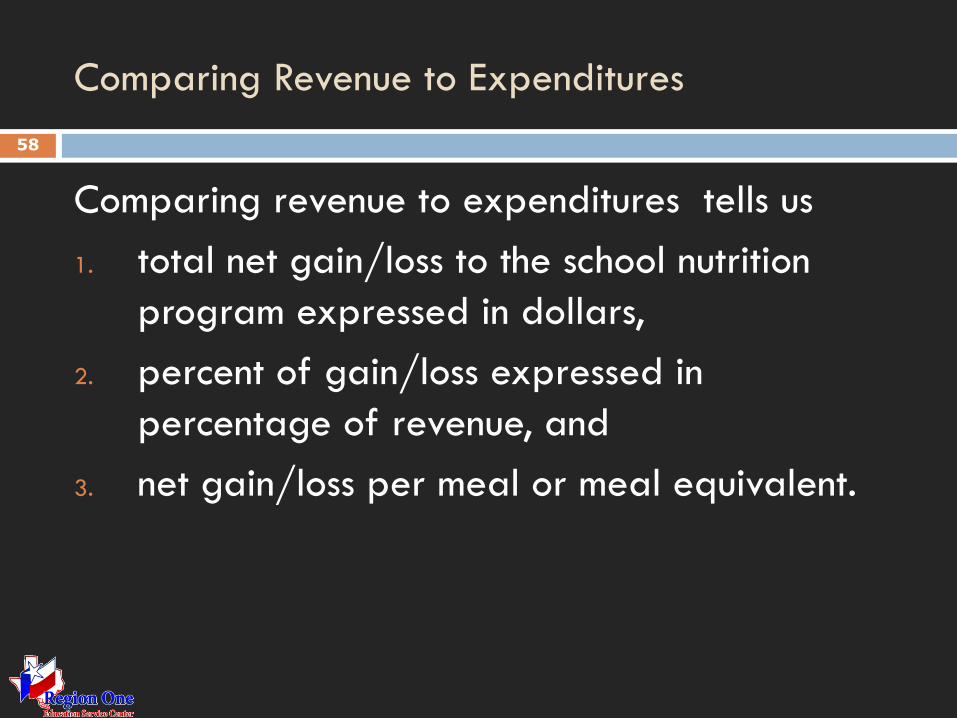

Comparing Revenue to Expenditures

58

Comparing revenue to expenditures tells us

1. total net gain/loss to the school nutrition

program expressed in dollars,

2. percent of gain/loss expressed in

percentage of revenue, and

3. net gain/loss per meal or meal equivalent.

Chapter 7 Controlling Food and Labor Costs in School

Nutrition Programs 59

Objective: Know how to apply cost control

measures to operate a financially sound

program with nutritional integrity

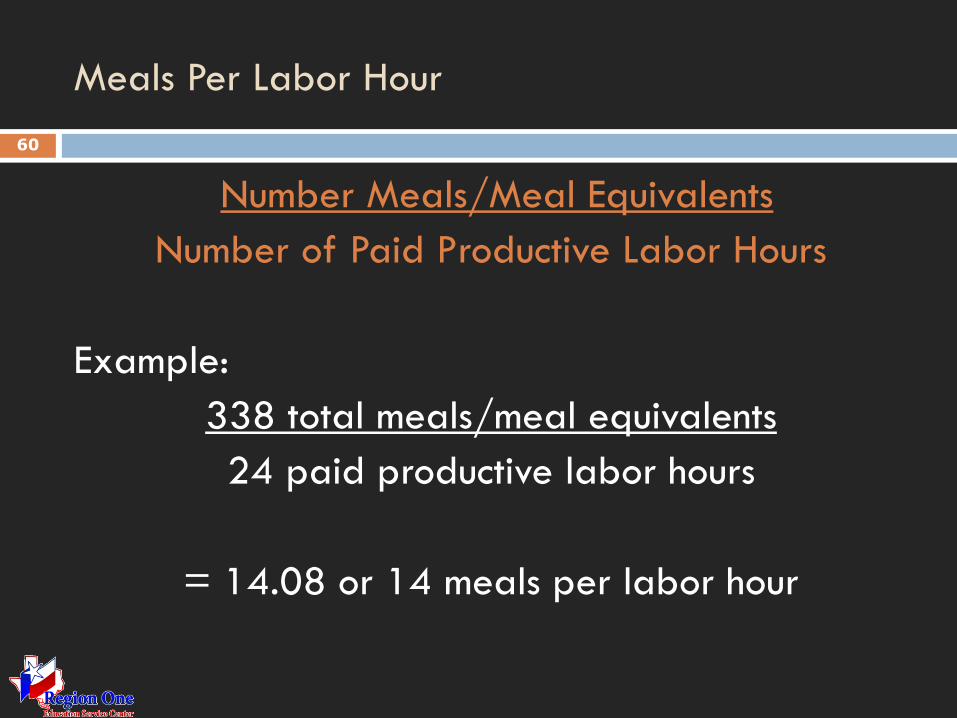

Meals Per Labor Hour

60

Number Meals/Meal Equivalents

Number of Paid Productive Labor Hours

Example:

338 total meals/meal equivalents

24 paid productive labor hours

= 14.08 or 14 meals per labor hour

Using Participation as a Financial Management Tool

61

Used as a forecasting tool to

prevent waste in excess labor hours and

overproduction of food.

reduce customer dissatisfaction because of

inadequate staff and too little food prepared

for the number served.

Calculating the cost of food used helps to

62

determine if costs are within guidelines,

ascertain if there are sufficient funds to pay

expenditures,

establish the cost for each meal equivalent

served, and

prevent waste and food theft through

monitoring food use.

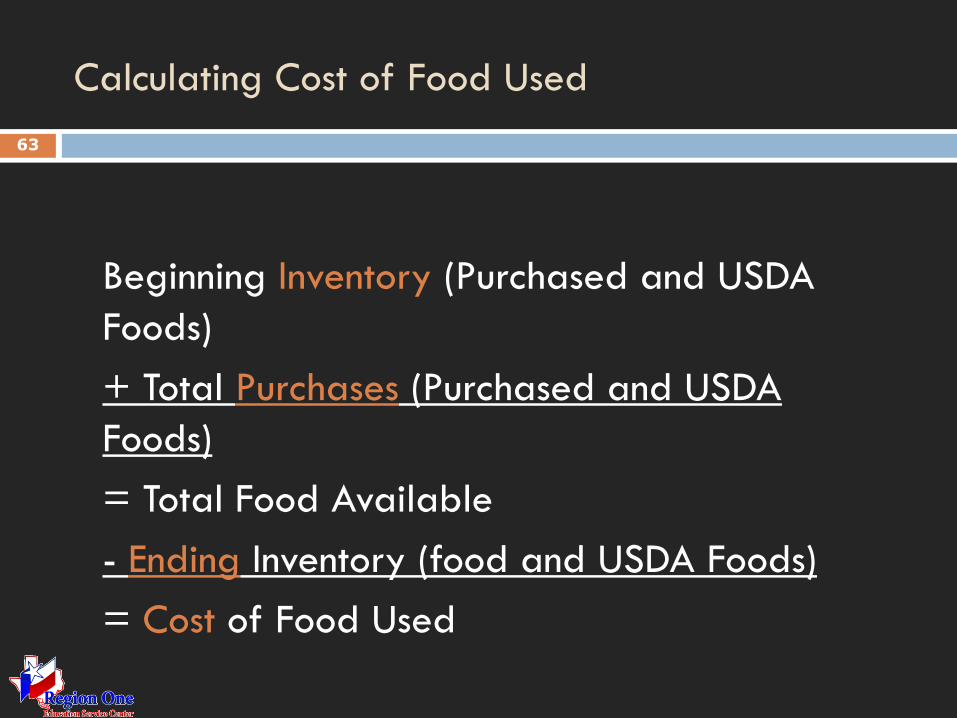

Calculating Cost of Food Used

63

Beginning Inventory (Purchased and USDA

Foods)

+ Total Purchases (Purchased and USDA

Foods)

= Total Food Available

- Ending Inventory (food and USDA Foods)

= Cost of Food Used

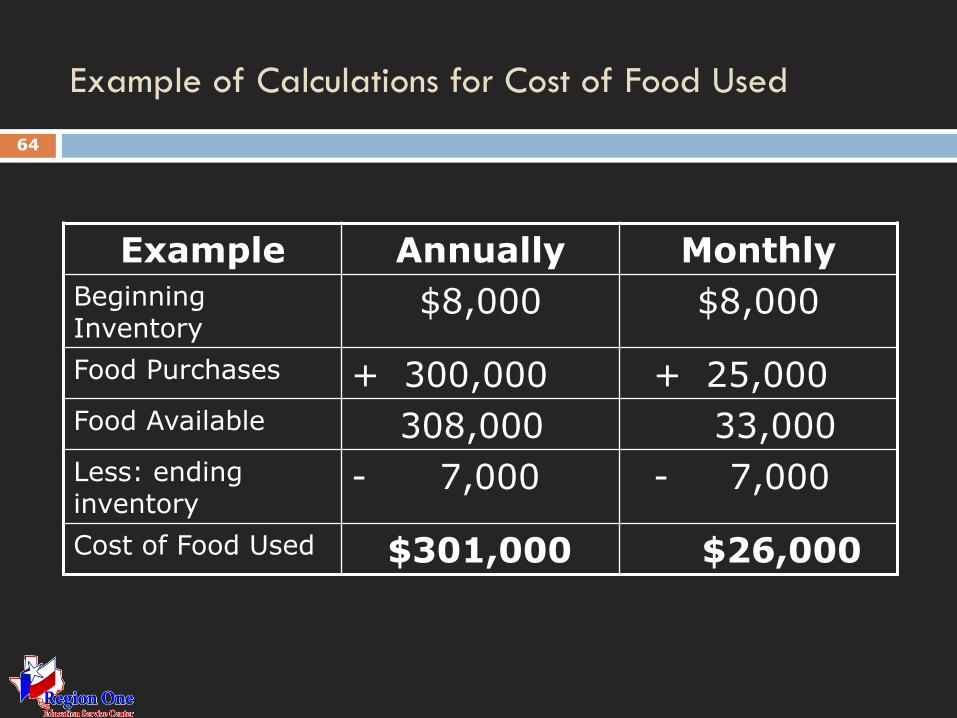

Example of Calculations for Cost of Food Used

Example Annually Monthly

Beginning Inventory

$8,000 $8,000

Food Purchases + 300,000 + 25,000

Food Available 308,000 33,000

Less: ending inventory

- 7,000 - 7,000

Cost of Food Used $301,000 $26,000

64

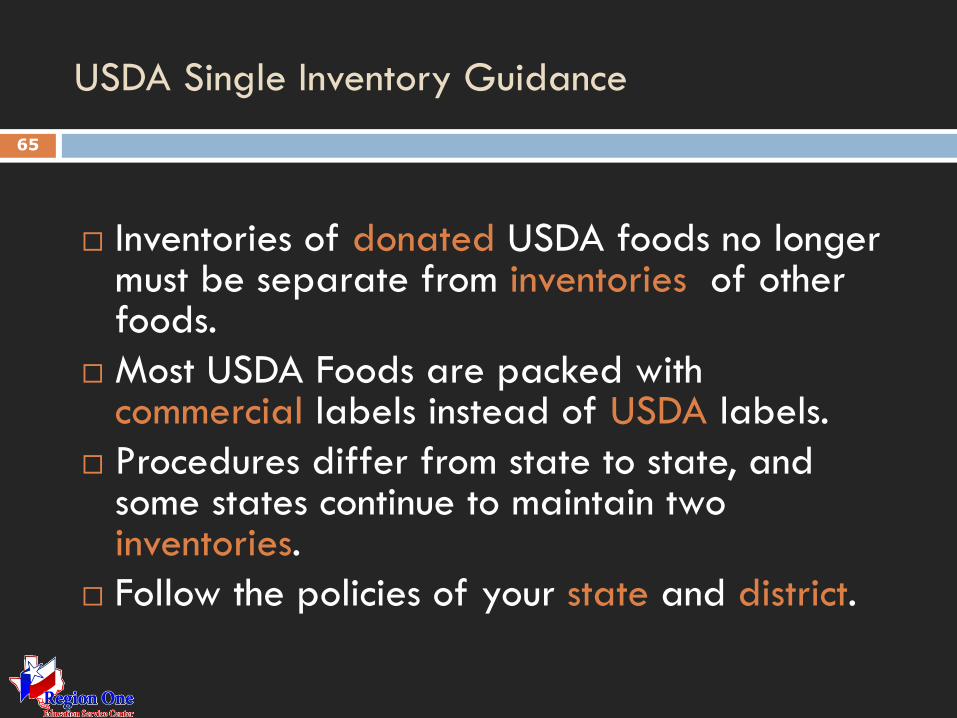

USDA Single Inventory Guidance

65

Inventories of donated USDA foods no longer must be separate from inventories of other foods.

Most USDA Foods are packed with commercial labels instead of USDA labels.

Procedures differ from state to state, and some states continue to maintain two inventories.

Follow the policies of your state and district.

Chapter 8 Developing and Analyzing a School Nutrition

Budget

66

Objective: Understand the importance of using

the budget as an analysis tool and control

document

Resources 67

United States Department of Agriculture Food and

Nutrition Service www.fns.usda.gov

Texas Department of Agriculture Food and Nutrition

Program www.squaremeals.org

National Food Service Management Institute – The

University of Mississippi www.nfsmi.org

Texas Education Agency www.tea.state.tx.us

Technical Assistance 68

Carmen Ocanas-Lerma, Food & Nutrition Program Director (956) 984-6124

Kimberly Keller Food & Nutrition

Specialist (956) 984-6121 [email protected]

Iris Perez Food & Nutrition

Specialist (956) 984-6102 [email protected]

Gilberto Requena Food & Nutrition

Specialist (956) 984-6108

Erika Leal Food & Nutrition

Program Technician (956) 984-6126 [email protected]

Sandra Bazan Food & Nutrition

Program Technician (956) 984-6120 [email protected]

Acknowledgement Statement

You understand and acknowledge that:

The training you are about to receive does not

cover the entire scope of the program; and that

You are responsible for knowing and understanding

all handbooks, manuals, alerts, notices and

guidance, as well as any other forms of

communication that provide further guidance,

clarification or instruction on operating the program.

Thank You

“This service (or product) is provided through the Texas Department of

Agriculture's school nutrition education, and outreach program funded

by the U. S. Department of Agriculture, Food and Nutrition Service. In

accordance with Federal Law and U.S. Department of Agriculture

policy, this institution is prohibited from discriminating on the basis of

race, color, national origin, sex, age, or disability. To file a complaint of

discrimination, write USDA, Director, Office of Adjudication, 1400

Independence Avenue, SW, Washington, D.C. 20250-9410 or call toll

free (866) 632-9992 (Voice). Individuals who are hearing impaired or

have speech disabilities may contact USDA through the Federal Relay

Service at (800) 877-8339; or (800) 845-6136 (Spanish). USDA is an

equal opportunity provider and employer” (USDA, 2011).

![GENC'{ ],GIn; [x]NUTRITION DIRECTORS (X ]HFAP · [x]NUTRITION DIRECTORS [ ] ... Wild Blueberry Assn. of North America. BROCCOLI; ... California Raisin Advisory Board Califomia Redi](https://img.pdfslide.us/doc/110x75/5b3c22b07f8b9a5e1f8d31d9/genc-gin-xnutrition-directors-x-hfap-xnutrition-directors-.jpg)