Embed Size (px)

Citation preview

IASA 86TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW

Financial Instruments

Insurance Accounting, Risk Management and Finance

Session 705

Learning Objectives

Review current FASB proposals on Financial Instruments

• Classification & Measurement

• Impairments

Highlight recent changes/updates from FASB & IASB

Highlight specific changes that will need to be made in

reporting/accounting processes

Compare and contrast proposed guidance with the current

Statutory & International guidance

Panel Members

Don Dilmore

Vice President – Investment

Accounting

BLACKROCK

8+ years insurance accounting

experience

Works with clients on regulatory

& financial statement filings

Member - Pennsylvania

Institute of Certified Public

Accountants

Maria Bifulco

Director – Project

Management

Prudential

25+ years insurance accounting

experience

Lead Business Analyst/Project

Manager for Investment

Related Systems, Reporting,

and Workflow projects

LOMA Investment Accounting

Working Group member

Michael Herling

Vice President – Consulting

Services

Princeton Financial Services

30+ years insurance accounting

experience

23 years at PFS

Consults with clients on best

practices, accounting issues,

optimizing workflow

CLASSIFICATION & MEASUREMENT

FINANCIAL INSTRUMENTS

Classification and Measurement Project

Part of FASB and IASB’s joint Financial Instruments project

• Original proposal would’ve moved US GAAP closer to IASB, but

recent revisions have moved them further apart

Similar classifications would remain, but would be renamed

to be more consistent with IFRS

• “Fair Value through Net Income” instead of “Trading”

• “Fair Value through OCI” instead of “Available for Sale”

• “Amortized Cost” replaces “Held to Maturity”

FV-OCI would remain the ‘residual’ category

• Amortized Cost and FV-NI will be defined, while FV-OCI is not

• Original proposal would have FV-NI as the residual

FASB Timeline

Q3 2009: IASB issues

Exposure Draft

Q4 2009: IASB

issues IFRS 9

Q1 2013: FASB issues

new Exposure Draft

Q2 2010: FASB issues

Exposure Draft requiring

all instruments to be

reported at Fair Value

Q1 2011: FASB moves

away from full fair value

to mixed measurement

Q4 2011: IASB delays

IFRS 9 effective date,

considers amendments

Q1 2012: FASB and IASB

begin joint discussions

Q2 2012: FASB and IASB

agree on three-category

approach for debt investments

Q4 2012: IASB exposes

amendments to IFRS 9

Q1 2014: FASB abandons

Converged Business Model

Assessment / FASB removes

Cash Flow Characteristics Test

Q4 2013: FASB

abandons SPPI Test

Late 2014: FASB expected

to issue final ASU

2015 – 2017: Expected

Implementation for

FASB updates

Q3 2013: FASB & IASB plan

redeliberations. IASB

indefinitely defers mandatory

effective date of IFRS 9

FASB Process

Q2 2010: FASB issues

Exposure Draft requiring

all instruments to be

reported at Fair Value

Q1 2011: FASB moves

away from full fair value

to mixed measurement Q2 2012: FASB and

IASB agree on three-

category approach for

debt investments

Q1 2013: FASB issues

new Exposure Draft

Q4 2013: FASB

abandons SPPI Test Q1 2014: FASB abandons

Converged Business Model

Assessment / FASB removes

Cash Flow Characteristics Test

Late 2014: FASB expected

to issue final ASU

And…we’re essentially

right back where we

started.

Start: FAS 115

Trading, AFS, HTM

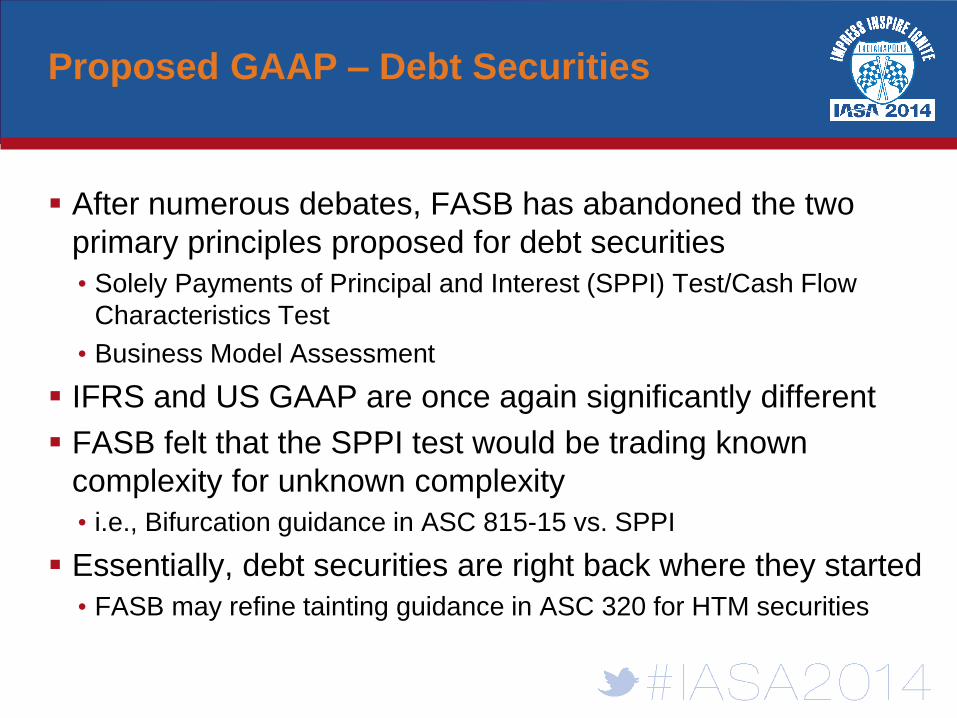

Proposed GAAP – Debt Securities

After numerous debates, FASB has abandoned the two

primary principles proposed for debt securities

• Solely Payments of Principal and Interest (SPPI) Test/Cash Flow

Characteristics Test

• Business Model Assessment

IFRS and US GAAP are once again significantly different

FASB felt that the SPPI test would be trading known

complexity for unknown complexity

• i.e., Bifurcation guidance in ASC 815-15 vs. SPPI

Essentially, debt securities are right back where they started

• FASB may refine tainting guidance in ASC 320 for HTM securities

Proposed GAAP – Equity Securities

FASB reaffirmed their proposal to require equity securities

to be measured at FV-NI

• Change from current GAAP

Equities would not have an option for FV-OCI

• Differs from proposed IFRS, where a one-time irrevocable election to

report equities at FV-OCI exists

Exception would exist for

• Certain securities reported under the equity method

• Certain securities that qualify for the practicability exception

• i.e., no readily determinable fair value

Current GAAP Measurement

Neither intend to

sell in near term, nor

have intent/ability to

hold until maturity

Intend and are able

to hold security until

maturity

Debt Security

Held to Maturity

Carry at

Amortized Cost

Available for Sale

Carry at Fair

Value; FV

changes through

OCI

Trading

Carry at Fair

Value; FV

changes through

Net Income

Intend to sell

security in near term

Investment Type

Equity Security

Hybrid Security with

Embedded Feature

(i.e., Bifurcation)

Non-Hybrid

Carry at:

Fair Value; FV

changes through

Net Income

Embedded Feature Debt Piece

Proposed GAAP Measurement

Neither intend to

sell in near term, nor

have intent/ability to

hold until maturity

Intend and are able

to hold security until

maturity

Debt Security

Amortized Cost

Carry at

Amortized Cost

Fair Value - OCI

Carry at Fair

Value; FV

changes through

OCI

Fair Value - NI

Carry at Fair

Value; FV

changes through

Net Income

Intend to sell

security in near term

Investment Type

Equity Security

Hybrid Security with

Embedded Feature

(i.e., Bifurcation)

Non-Hybrid

Embedded Feature Debt Piece

Carry at:

Fair Value; FV

changes through

Net Income

Current STAT – Debt and Equity

While intent is the principal classification driver in GAAP,

STAT is primarily based on certain risk characteristics of

the security

• Type of asset

• NAIC Designation

• Insurance Company type

Intended use of the security is irrelevant in STAT

Measurement is determined cusip-by-cusip

• May create inconsistencies in carrying value with similar assets

In general, more debt securities are reported at Amortized

Cost than Fair Value

• STAT also does not have an equivalent concept of Fair Value – NI

GAAP / STAT Differences

TOPIC PROPOSED FASB MODEL CURRENT STAT MODEL

Categories of

Classification

• Trading (FV – NI)

• Available for Sale (FV – OCI)

• Held to Maturity (Amort. Cost)

• Based on security type and

other risk characteristics

Classification

Decision

• Solely based on business

model/intent

• (Save equities in HTM)

• Type of asset

• NAIC Designation

• Insurance Company type

Debt Securities • All three categories allowed

• Reported at B/ACV

• Other options not allowed

• No equivalent idea of FV-NI

Equities • Only Fair value – Net Income

• Fair value – OCI eliminated

• Fair value – with changes

through Capital & Surplus

• No equivalent idea of FV-NI

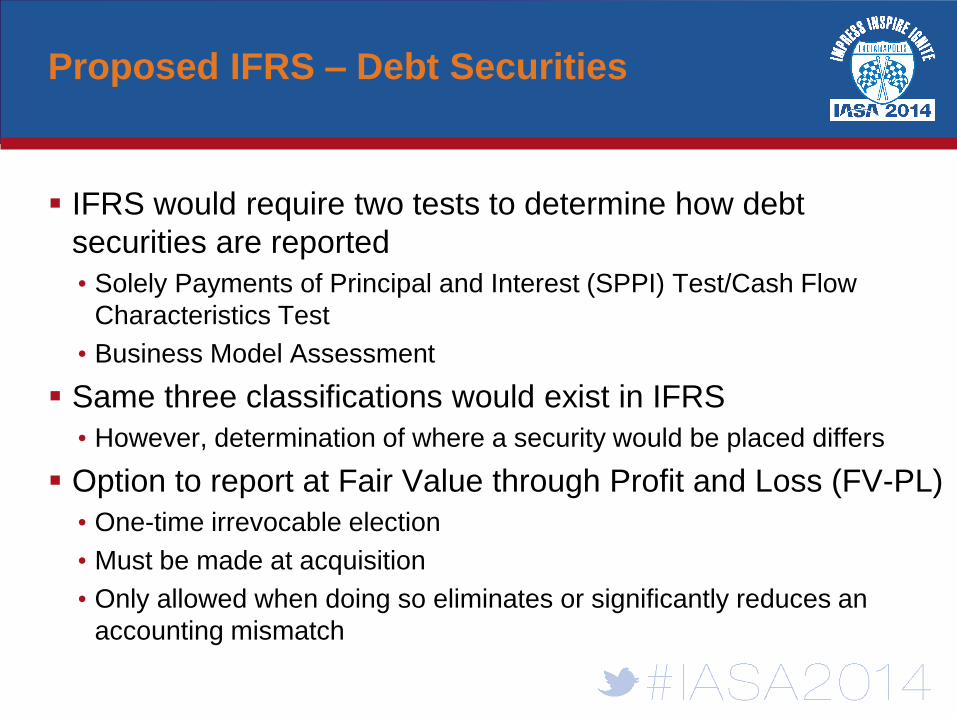

Proposed IFRS – Debt Securities

IFRS would require two tests to determine how debt

securities are reported

• Solely Payments of Principal and Interest (SPPI) Test/Cash Flow

Characteristics Test

• Business Model Assessment

Same three classifications would exist in IFRS

• However, determination of where a security would be placed differs

Option to report at Fair Value through Profit and Loss (FV-PL)

• One-time irrevocable election

• Must be made at acquisition

• Only allowed when doing so eliminates or significantly reduces an

accounting mismatch

Proposed IFRS – Equity Securities

IFRS 9 requires equity securities to be measured at Fair

Value through Profit and Loss (FV-PL)

• Matches current proposed GAAP

However, equities would have an option for FV-OCI under

IFRS

• One-time irrevocable election

• Must be made at acquisition

• Requires all unrealized and realized gains and losses to flow through

Other Comprehensive Income

• Never recycled into Realized Gain/Loss

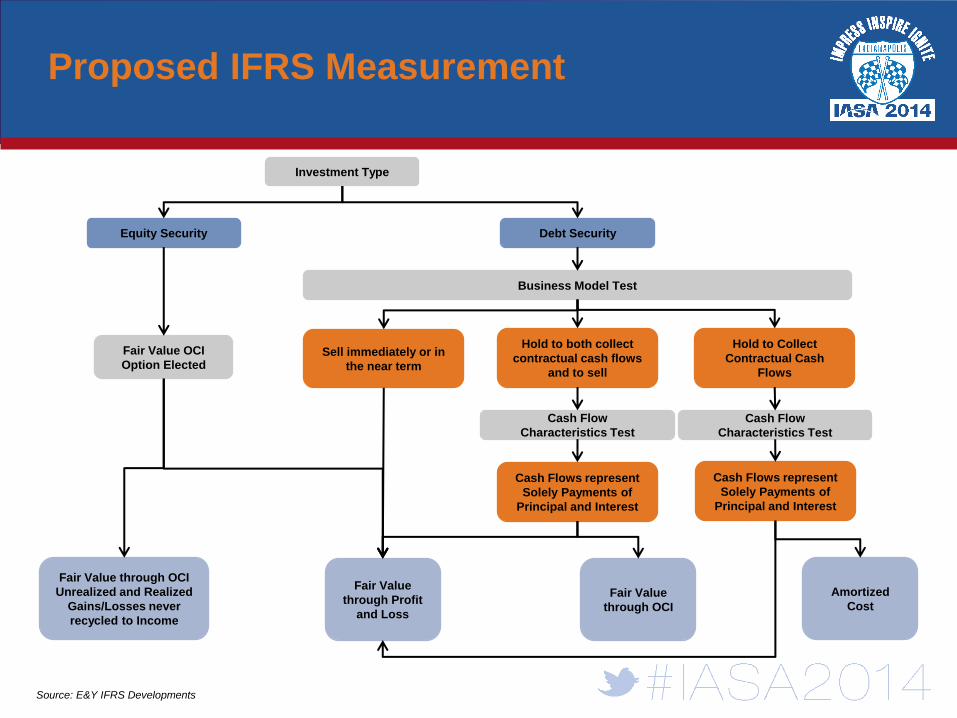

Proposed IFRS Measurement

Source: E&Y IFRS Developments

Cash Flow

Characteristics Test

Hold to both collect

contractual cash flows

and to sell

Hold to Collect

Contractual Cash

Flows

Fair Value OCI

Option Elected

Debt Security

Amortized

Cost Fair Value

through OCI

Fair Value

through Profit

and Loss

Sell immediately or in

the near term

Business Model Test

Equity Security

Fair Value through OCI

Unrealized and Realized

Gains/Losses never

recycled to Income

Investment Type

Cash Flows represent

Solely Payments of

Principal and Interest

Cash Flow

Characteristics Test

Cash Flows represent

Solely Payments of

Principal and Interest

GAAP / IFRS Differences

TOPIC PROPOSED FASB MODEL PROPOSED IASB MODEL

Categories of

Classification

• Trading (FV – NI)

• Available for Sale (FV – OCI)

• Held to Maturity (Amort. Cost)

• Fair value through Profit/Loss

• Fair value through OCI

• Amortized cost

Classification

Decision

• Solely based on business

model/intent

• (Save equities in HTM)

• Business model/intent

• Cash flow characteristics

(SPPI)

Debt Securities • All three categories allowed • All three categories allowed

Equities • Only Fair value – Net Income

• Fair value – OCI eliminated • Fair value – Net Income

Fair Value OCI

Option: Equities • Not allowed

• Allowed if elected at purchase

• Irrevocable

• Cannot recycle Unrealized G/L

into Realized when sold

IMPAIRMENT

FINANCIAL INSTRUMENTS

Impairment Project Background

Joint project with the FASB and IASB

FASB Accounting Standard Update, Financial

Instruments—Credit Losses (Subtopic 825-15)

IASB Exposure Draft ED/2013/3 Financial Instruments:

Expected Credit Losses

Q4 2012: FASB issues

revised Exposure Draft

Q4 2009: IASB issues

Exposure Draft

Q2 2010: FASB issues

Exposure Draft

Q1 2011: FASB & IASB

issue supplementary

document

Q4 2014: Final GAAP

Standard expected to

be issued

Q2 2014: Final IFRS

Standard expected

to be issued

Q1 2018: Anticipated

Effective Date for IFRS

guidance

Q1 2013: IASB issues revised

Exposure Draft

GAAP guidance Effective

Date To Be Determined…

Overview – FASB Credit Losses Exposure Draft

Current Expected Credit Loss (CECL) Model

Generally applies to instruments that are measured at

amortized cost

• Removes the probability threshold for recognizing credit losses

• Credit losses include estimates of future events

• An allowance account (contra asset) is established to track losses

For Fair Value through OCI, expected credit losses is

determined

• When an asset’s fair value is less than its amortized cost

• Credit losses would be recognized in net income under the CECL

model

Comparison Current GAAP to Proposed Model

TOPIC CURRENT FASB MODEL PROPOSED FASB MODEL

Timing of

Recognition

• Loss is probable/likely to have

occurred • Estimated Losses recorded Day 1

Measurement

Calculation

• Incurred Loss Model

Current conditions & experience

• Expected Loss Model

• Includes multiple forecast of future

events

Recognition • Adjust Cost Basis • Record an Allowance

Overview - IASB Exposure Draft on Credit Losses

Expected credit losses

• 12 month expected credit losses for good assets

• Lifetime expected credit loss when there is significant deterioration

Calculation

• Not a best or worst case scenario

• Probability that a loss will occur and a probability a loss will not occur

Assessment

• Includes estimates about future events

• No loss calculations for investment grade securities

Exposure Drafts on Credit Losses

Comparison of FASB and IASB Models

• Notion of good versus bad assets

• Length of time when estimating into the future

PREPARING FOR CHANGES

FINANCIAL INSTRUMENTS

What Should Companies Do?

Wait for the new FASB and IASB pronouncements?

What Should Companies Do?

No, Let’s keep on eye on the FASB and IASB happenings

Suggestions to Help Monitor Progress

Collect Information:

Check with your external auditors

• Can they give you regular updates or sign up to get regular updates from

their website?

Check with your accounting system vendor

Listen to or read the minutes from FASB discussions

Work with industry groups to see what information they may have

• LOMA, ACLI, etc.

Discuss with peer insurance companies

When exposure drafts are released, try to send a comment letter and

read other company comment letters

Suggestions to Help Monitor Progress

Use the Information:

In 2013, Balance sheet compare current GAAP classification to

proposed GAAP classification

In 2014, adjusted the compare as receive new information

Quarterly Accounting update meetings internally

• Help make sure we have consistency between pronouncements

• Insurance Contracts

For impairments, taking a look at our asset manager models

Implementation Preparation

Develop an outline for implementation:

Identify where processes and systems will need to change

If you need to follow STAT, GAAP and IFRS, can your company handle

multiple accounting bases?

What resources would you need?

Additional Information

FASB Financial Instruments Projects

• Classification and Measurement • http://www.fasb.org/jsp/FASB/FASBContent_C/ProjectUpdatePage&cid=1176159267718

• Impairment • http://www.fasb.org/jsp/FASB/FASBContent_C/ProjectUpdatePage&cid=1176159268094

IASB

• Classification and Measurement • http://www.ifrs.org/current-projects/iasb-projects/financial-instruments-a-replacement-of-ias-39-

financial-instruments-recognitio/phase-i-classification-and-measurement/Pages/Phase-I-

Classification-and-measurement.aspx

• Amortized Cost and Impairment of Financial Assets • http://www.ifrs.org/current-projects/iasb-projects/financial-instruments-a-replacement-of-ias-39-

financial-instruments-recognitio/impairment/Pages/Financial-Instruments-Impairment-of-Financial-

Assets.aspx

Questions?

Maria Bifulco

Director | Prudential

Project Management – Investment Operations

[email protected] | 973.802.6720

Don Dilmore

Vice President | BLACKROCK

Investment Accounting Group

[email protected] | 302.797.2498

Mike Herling

Vice President | Princeton Financial Systems

Consulting Services

[email protected] | 609.514.4631

IASA 86TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW

Please Complete the Session Evaluation Form on the Conference App and Include Your Conference Registration ID# to be Included in a Drawing for a Free Conference Registration for the 2014 Annual Conference! NOTE: Your Conference Registration ID# is Located at the

Bottom Left Hand Corner of Your Badge.

![INTERMEDIATE - preview.kingborn.netpreview.kingborn.net/920000/4344e7e68c624fa98fe9d9d76dffe1c1.pdf · FASB CODIFICATION FASB Codification References [1] FASB ASC 350-10-05. [Predecessor](https://img.pdfslide.us/doc/110x75/5b892df67f8b9a770a8cf6c0/intermediate-fasb-codification-fasb-codification-references-1-fasb-asc-350-10-05.jpg)