Embed Size (px)

Citation preview

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

Journal of Policy Modeling xxx (2014) xxx–xxx

Available online at www.sciencedirect.com

ScienceDirect

Financial development and economic growth:New evidence from Tunisia

Khoutem Ben Jedidia a,b,1, Thouraya Boujelbène c,∗,Kamel Helali d,2

a Higher Institute of Accountancy and Business Administration (ISCAE), Manouba Campus, 2010, University ofManouba, Tunisia

b URED, Faculty of Economics and Management of Sfax, Tunisiac Faculty of Economics and Management of Sfax, UREA, University of Sfax, Route de l’Aérodrome km 4.5, B.P.

1088-3018, Sfax, Tunisiad Faculty of Economics and Management of Sfax, University of Sfax, Route de l’Aérodrome km 4.5, B.P. 1088-3018,

Sfax, Tunisia

Received 3 November 2013; received in revised form 28 May 2014; accepted 26 July 2014

Abstract

This paper examined an empirical investigation of whether financial development can boost economicgrowth in Tunisia. We used an Autoregressive Distributed Lag method to assess the finance-growth rela-tion taking private credit, value traded and issuing bank’s securities on the financial market as financialdevelopment indicators.

The empirical results showed that the domestic credit to private sector has a positive effect on the economicgrowth suggesting that the financial development is a driver of a long term economic growth, but subject toa financial fragility at the short run. Moreover, this study confirmed the view of bidirectional relationshipbetween credit and economic growth. However, we found that neither the stock market development northe intervention of banks in the stock market had robust and positive effects on the economic growth. Thus,Tunisia is recommended to accelerate in priority the financial reforms of the Tunisian stock market in orderto contribute to mobilize savings and promote long run economic growth.© 2014 Society for Policy Modeling. Published by Elsevier Inc. All rights reserved.

∗ Corresponding author. Tel.: +216 98 974 240.E-mail addresses: [email protected] (K. Ben Jedidia), [email protected] (T. Boujelbène),

[email protected] (K. Helali).1 Tel.: +216 98 945 309.2 Tel.: +216 98 667 705.

http://dx.doi.org/10.1016/j.jpolmod.2014.08.0020161-8938/© 2014 Society for Policy Modeling. Published by Elsevier Inc. All rights reserved.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

2 K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx

JEL classification: E44; O11; O43; O55

Keywords: Financial development; Economic growth; Intermediation-stock market; Autoregressive Distributed Lagmethod; Tunisia

1. Introduction

The debate on optimal financial structure that promotes long-run economic growth culminatesin four distinct views: the bank-based, the market-based, the financial services, and the law andfinance (Dolar & Meh, 2002; Levine, 2005). This debate was initiated by Goldsmith (1969) whocompared Germany to the UK, conducting empirical studies to see whether a financial structurematters for an economic growth.3

The bank-based view emphasizes the important role of intermediaries to stimulate economicgrowth. Since Schumpeter (1911), the banking sector has been an engine of the economicgrowth thanks to its funding of productive investment. Therefore, the economic growth is seenas connected to the indirect finance spread (Gurley & Shaw, 1960). Later, and considering themicroeconomic foundations of intermediation, the bank was regarded as the best tool to overcomemarket frictions; it reduced information cost (Greenwood & Jovanovic, 1990), mobilized savingsand provided liquidity (Gorton & Pennacchi, 1990).

In contrast, the market-based proponents insist on the merits of market financing. In fact,markets facilitate the diversification of risk and provide risk management tools. They enhancecorporate governance and make it easy to tie managerial compensation to firm performance.They, also, provide managers with valuable information through the feedback effect of prices(Subrahmanyam & Titman, 1999). Then, they are better at funding projects of new technologiessubject to diversity of opinions (Boot & Thakor, 1997).

On the other hand, the financial services view, developed by Merton and Bodie (1995),overcame this distinction and minimized the importance of bank-based/market-based debate.According to Levine (1997), the emphasis is put on the stability of financial functions carriedout by both banks and markets. We must focus on the capacity of the overall system to offersignificant financial services, regardless of the relative importance of its various components, theinstitutional structure or its evolution. Similarly, according to the legal view developed by LaPorta, Lopez-de-Silanes, Shleifer, and Vishny (1997), bank based/market based classification isnot a useful way to distinguish financial systems. In fact, the financial development componentsare determined by the legal codes that impose the respect of the property rights and the efficiencyof contracts.

Furthermore, because of recent financial innovations, deregulation and financial globalizationoccurring since the 80s, the noticed convergence of the different financial systems would occurin terms of complementarity between the banks and the financial market rather than in terms

3 Several recent empirical works on financial structure and economic growth using the panel and/or pure cross-sectionframeworks concluded that the financial structure is irrelevant (Luintel, Khan, Arestis, & Theodoridis, 2008). However,Deidda and Fattouh (2008) showed that a change from a bank-dominated system to another in which market-finance andbank-finance coexist might harm economic growth.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx 3

of opposition (Allen & Santomero, 2001). Actually, the financial intermediation evolved towarda growing interpenetration of intermediaries and markets. Since then, the new approaches onfinancial intermediation have been founded on the management of risk and participation costs(Allen & Santomero, 1998, 2001; Matthews & Thompson, 2008).

Yet, from Song and Thakor (2010) point of view, banks and markets are considered as com-petitors, implying that each develops at the expense of the other without even studying theirco-evolution as they are regarded as two separate entities. However, growth promotion is theresult of the development of banks as well as that of markets. In the same trend, Allen and Gale(2000) affirm that we can no longer examine the role of financial markets and that of financialinstitutions separately.

Consequently, the aim of this paper was to study empirically the relationship between finan-cial development and economic growth in Tunisia during the 1973–2008 period just as the recentfinancial crisis has brought renewed attention to the impact of finance. This study, achieved in thecase of a specific country, is justified by time series studies of a selection of countries by Abu-Bader and Abu-Qarn (2008), concluding that the pattern of causality differs significantly amongcountries, which strengthens the lead of country-specific studies. Otherwise, cross countries com-parisons have shown that the financial sector development has a stronger impact on growth in lowand middle incomes than in a high one (Beck, Demirguc-Kunt, & Levine, 2009).

The previous models dealing with the relation between financial development and economicgrowth in Tunisia (Ghali, 1999; Inoubli, 2004), or in the south Mediterranean region (BenM’rad, 2000), the MENA region (Abu-Bader & Abu-Qarn, 2008; Ben Naceur, Ghouzoani, &Omran, 2008; Boulila & Trabelsi, 2004) concentrated on variables that reflect either the banks’role, that of markets or that of both separately without considering their complementarity. Sofar, no attempt has been made to consider banks-markets relations in the study of financegrowth.

Hence, the present study was pursued in this direction to fill this gap. The originality of this studyis that it focuses on a simultaneous exploration of the role of financial intermediaries notably banksby offering credits (domestic credit to private sector), the role of the activity of stock market (valuetraded) and also the role of bank-stock market relations (issuing of bank’s securities on financialmarket) – all expressed in percentages of GDP – and assess them in an integrated framework ofeconomic growth. Considering the emission of bank securities on the financial market allows usto adapt a larger view of the banks’ financial intermediation.4 This topic permits a larger and morecareful consideration of the contribution of banks to the economic financing in order to test indepth the hypothesis that the banks-markets relation promotes financial development or vice versa.In this wide spectrum, we tested whether the movement of the Tunisian financial system from arepressed to a more liberalized one starting in 1986 has boosted the economic growth. Anothermerit of this paper is that it employs a recent econometric technique which is the AutoregressiveDistributed Lag (ARDL) suggested by Pesaran, Shin, and Smith (2001) to assess finance-growthrelationship in Tunisia.

The remainder of this paper is organized as follows: In Section 2 the financial depth in Tunisiais analyzed. Section 3 presents the empirical analysis. In Section 4, however, the relationshipbetween financial development and economic growth is fully discussed. Eventually, Section 5offers conclusions and some policy implications.

4 But, our purpose is different from Deidda and Fattouh’s (2008). They introduce “an interaction term” in their modelin order to measure the effect of banking development on growth at different levels of stock market development.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

4 K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx

2. Financial depth in Tunisia

Since the independence in 1956, the Tunisian policy has been characterized by a pervasivepublic control over the different economic sectors in order to protect the economy. So, the Tunisianbanks were considered as guarantees of the economic growth thanks to the credits they allocatedand their compulsory compliance to equipment bonds issued by the State (the ratio of the GlobalFinancial Development to total financing of banks is fixed at 25%). In this context, the financialmarket, created only in 1969, was exempted from a leading role in the economic growth. However,the Tunisian economy plunged into a “financial repression” until 1986. The policy of massiveintervention was more apparent in the fact that Tunisian banks were subject to strict control. Theadministration of fixed interest rates at artificially low levels resulted in negative unstable outcomesof savings. In fact, the intermediate financing oriented to specific sectors5 at favorable rates couldnot engender a mobilization via a sufficient banking of savings to feed the distributed credits.The most fortunate savers favored to invest in the estate sector and gave priority to consumptionin a second place. The banking finance, strongly based on money creation, caused an averageinflation rate of about 10% during the 1980–1986 period. Consequently, the financial sector wascharacterized by rigidities, controls and inefficiencies.

2.1. PAS and financial liberalization

In order to optimize a financing process that favors an economic growth, the authorities optedfor more flexibility to the economy and a more active role to the private sector in the growthprocess. This option was made concrete through the adoption of a Structural Adjustment Plan(Plan d’Ajustement Structurel (PAS)) in 1986 established in collaboration with the InternationalMonetary Fund. The economic liberalization became a major choice of the Tunisian economicpolicy. Since 1986, the financial liberalization has been accompanied with an introduction offinancial innovations. Among the gradual liberalization and modernization key reforms of themonetary and financial policies we can cite:

- The abolition of previous Central Bank authorization for loans in 1988 as well as the financingof certain public enterprises at preferential conditions; the liberalization of the banking marginin 1994; the rediscount financing was totally abolished in 1996. Then, the monetary policyshifted from direct to indirect control; the adoption of the universal bank principal in 2001; theadoption of prudential and supervision regulations in line with international standards.

- The partial liberalization of the monetary market interest rate in 1986; the establishment of anew management of the monetary market in 1987 and the creation of new short-term finan-cial instruments on the monetary market in December 1989 (deposit certificates, commercialpapers, treasury bills), and the introduction of new instruments of liquidity management (suchas permanent facility of loaning and depositing within 24 h since February 2009).

- The financial market reform series: a new status for intermediaries; a reduction of the benefittaxes for listed enterprises (from 35% to 20%), a new regulation of bond loans in 1988; thecreation of new companies in order to promote placements on the financial market, the diversi-fication of securities (e.g. Prioritary dividend shares, participating securities), the introductionof a public appeal for saving, the law on financial security in 2005, and the establishment of

5 These were called priority sectors such as tourism, agriculture and crafts.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx 5

35

40

45

50

55

60

65

70

75

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

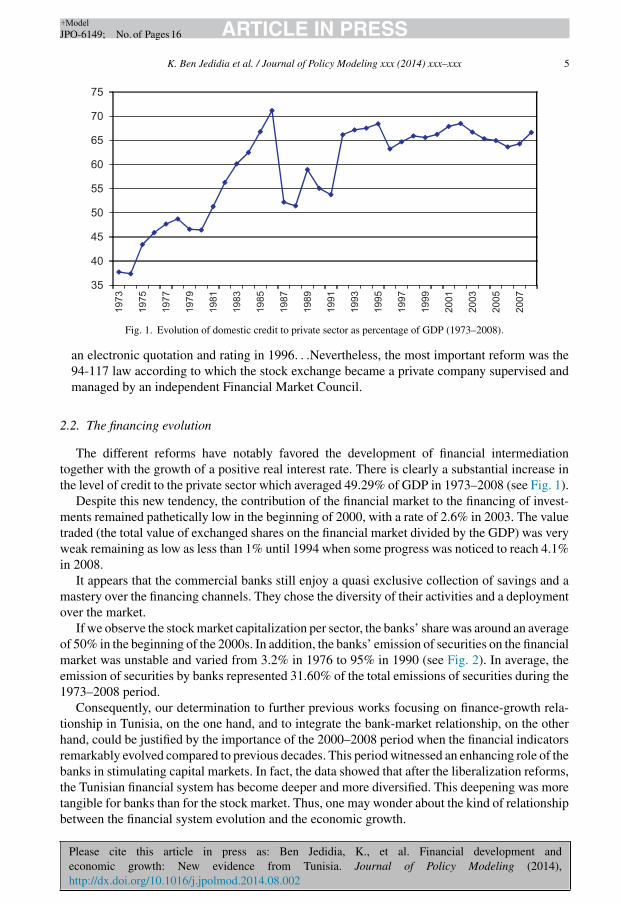

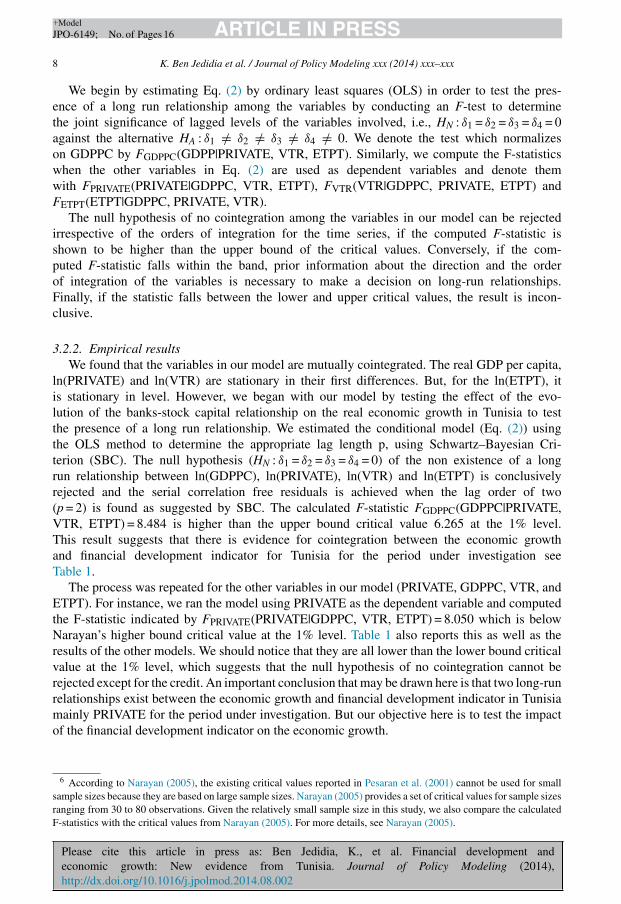

Fig. 1. Evolution of domestic credit to private sector as percentage of GDP (1973–2008).

an electronic quotation and rating in 1996. . .Nevertheless, the most important reform was the94-117 law according to which the stock exchange became a private company supervised andmanaged by an independent Financial Market Council.

2.2. The financing evolution

The different reforms have notably favored the development of financial intermediationtogether with the growth of a positive real interest rate. There is clearly a substantial increase inthe level of credit to the private sector which averaged 49.29% of GDP in 1973–2008 (see Fig. 1).

Despite this new tendency, the contribution of the financial market to the financing of invest-ments remained pathetically low in the beginning of 2000, with a rate of 2.6% in 2003. The valuetraded (the total value of exchanged shares on the financial market divided by the GDP) was veryweak remaining as low as less than 1% until 1994 when some progress was noticed to reach 4.1%in 2008.

It appears that the commercial banks still enjoy a quasi exclusive collection of savings and amastery over the financing channels. They chose the diversity of their activities and a deploymentover the market.

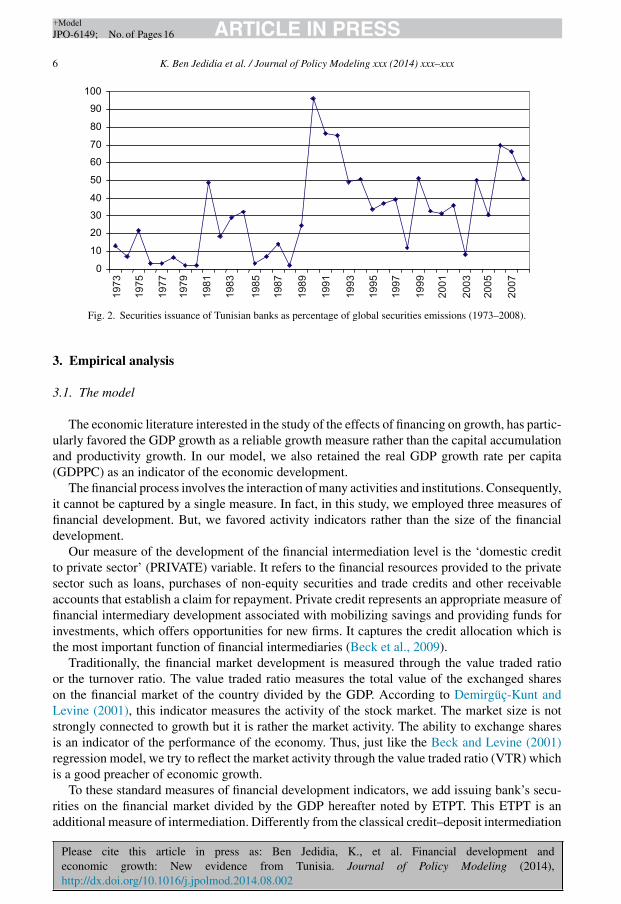

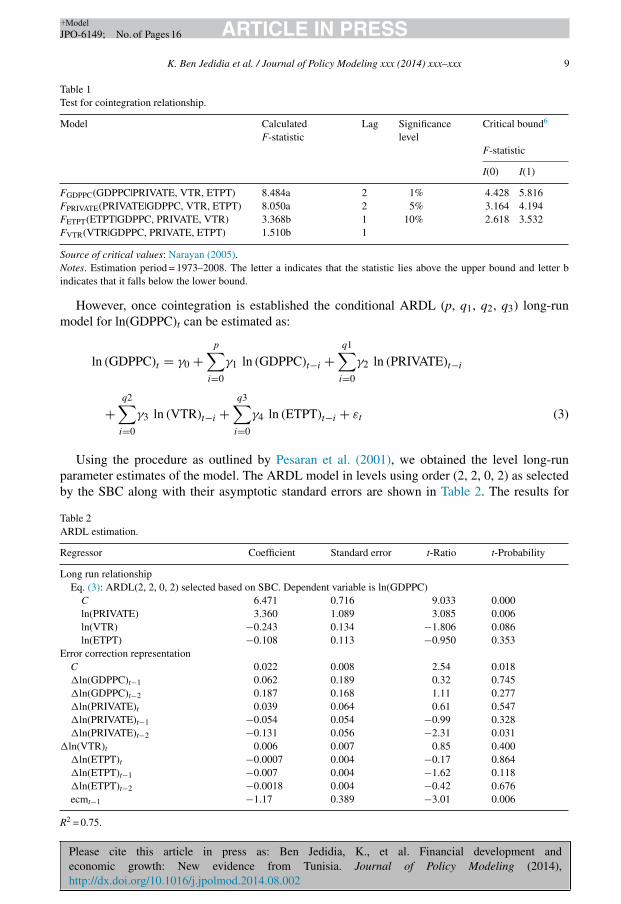

If we observe the stock market capitalization per sector, the banks’ share was around an averageof 50% in the beginning of the 2000s. In addition, the banks’ emission of securities on the financialmarket was unstable and varied from 3.2% in 1976 to 95% in 1990 (see Fig. 2). In average, theemission of securities by banks represented 31.60% of the total emissions of securities during the1973–2008 period.

Consequently, our determination to further previous works focusing on finance-growth rela-tionship in Tunisia, on the one hand, and to integrate the bank-market relationship, on the otherhand, could be justified by the importance of the 2000–2008 period when the financial indicatorsremarkably evolved compared to previous decades. This period witnessed an enhancing role of thebanks in stimulating capital markets. In fact, the data showed that after the liberalization reforms,the Tunisian financial system has become deeper and more diversified. This deepening was moretangible for banks than for the stock market. Thus, one may wonder about the kind of relationshipbetween the financial system evolution and the economic growth.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

6 K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx

0

10

20

30

40

50

60

70

80

90

100

2005

2007

2003

2001

1999

1997

1995

1993

1991

1989

1987

1985

1983

1981

1979

1977

1975

1973

Fig. 2. Securities issuance of Tunisian banks as percentage of global securities emissions (1973–2008).

3. Empirical analysis

3.1. The model

The economic literature interested in the study of the effects of financing on growth, has partic-ularly favored the GDP growth as a reliable growth measure rather than the capital accumulationand productivity growth. In our model, we also retained the real GDP growth rate per capita(GDPPC) as an indicator of the economic development.

The financial process involves the interaction of many activities and institutions. Consequently,it cannot be captured by a single measure. In fact, in this study, we employed three measures offinancial development. But, we favored activity indicators rather than the size of the financialdevelopment.

Our measure of the development of the financial intermediation level is the ‘domestic creditto private sector’ (PRIVATE) variable. It refers to the financial resources provided to the privatesector such as loans, purchases of non-equity securities and trade credits and other receivableaccounts that establish a claim for repayment. Private credit represents an appropriate measure offinancial intermediary development associated with mobilizing savings and providing funds forinvestments, which offers opportunities for new firms. It captures the credit allocation which isthe most important function of financial intermediaries (Beck et al., 2009).

Traditionally, the financial market development is measured through the value traded ratioor the turnover ratio. The value traded ratio measures the total value of the exchanged shareson the financial market of the country divided by the GDP. According to Demirgüc-Kunt andLevine (2001), this indicator measures the activity of the stock market. The market size is notstrongly connected to growth but it is rather the market activity. The ability to exchange sharesis an indicator of the performance of the economy. Thus, just like the Beck and Levine (2001)regression model, we try to reflect the market activity through the value traded ratio (VTR) whichis a good preacher of economic growth.

To these standard measures of financial development indicators, we add issuing bank’s secu-rities on the financial market divided by the GDP hereafter noted by ETPT. This ETPT is anadditional measure of intermediation. Differently from the classical credit–deposit intermediation

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx 7

reflected by PRIVATE, this variable represents a “marketized intermediation” where the emissionof financial assets on the market allows banks to collect funds and use them at the service of theirintermediation. Implementing this variable in our regressions allows us to consider the comple-mentarity between banks and the stock market. That is to say, it permits a better identificationof the channels through which the relationship banks-stock market does cause economic growthor not. The expected impact may be either positive or negative: Positive if the commercial bankssupport the financial market and hence promote economic growth. Nevertheless, such a domi-nance of the banks can be predicted as a handicap to economic growth due to the eviction effectbanks may cause to the promotion of the financial market.

Therefore, our model can be written as follows:

ln (GDPPC)t = α + β ln (PRIVATE)t + λ ln (VTR)t + δ ln (ETPT)t + εt (1)

where GDPPC represents the real GDP per capita and VTR expresses the value traded ratio.Whereas, PRIVATE is domestic credit to private sector divided by the GDP and ETPT is the sumof issuing bank’s securities on the financial market, also, divided by the GDP. εt is a randomvariable assumed as in the usual fashion to be serially uncorrelated with zero mean and constantvariance.

The parameters of the model measure the sensitivity of the variables to the economic growth.Typically, the equation of our model will have β (elasticity of domestic credit to private sector

to the economic growth) > 0, λ (elasticity of value traded ratio of economic growth) > 0, and, asmentioned earlier δ can be either positive or negative depending on the impact of the presence ofbanks on the stock market. All the variables are obtained in Logarithm.

3.2. The econometric methodology

We estimated our model using the Autoregressive Distributed Lag (ARDL) cointegration pro-cedure proposed by Pesaran et al. (2001) to overcome the limits related to the method suggested byEngle and Granger (1987) and Johansen (1991). The most important advantage of this techniqueis that the bounds test approach is applicable irrespective of whether the underlying regressorsare purely I(0), purely I(1) or mixed cointegrated. Thus, this avoids the potential bias associatedwith unit roots and cointegration tests.

3.2.1. Estimation model using Autoregressive Distributed Lag (ARDL)The ARDL procedure classifies variables as either dependent or explanatory. So, in this case,

the error correction representation of the ARDL specification model for Eq. (1) is given by:

� ln (GDPPC)t = a0 +p∑

i=1

bi� ln (GDPPC)t−i +p∑

i=0

ci� ln (PRIVATE)t−i

+p∑

i=0

di� ln(VTR)t−i +p∑

i=0

ei� ln(ETPT)t−i + δ1 ln (GDPPC)t−1

+ δ2 ln (PRIVATE)t−1 + δ3 ln (VTR)t−1 + δ4 ln (ETPT)t−1 + εt (2)

where � denotes the first difference operator, a0 is the drift component, εt is the usual white noiseresiduals, and the variables ln(GDPPC), ln(PRIVATE), ln(VTR) and ln(ETPT) are as definedearlier.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

8 K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx

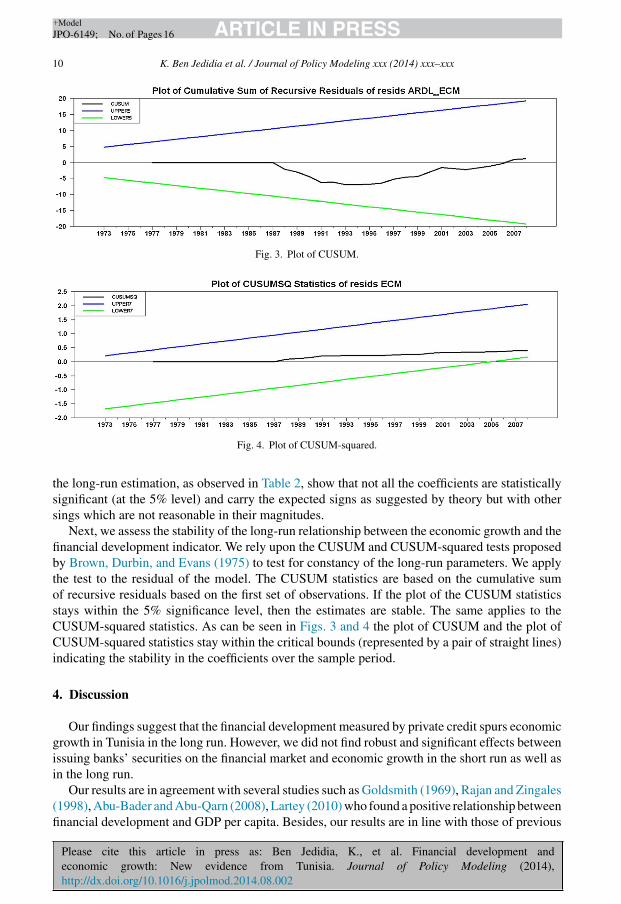

We begin by estimating Eq. (2) by ordinary least squares (OLS) in order to test the pres-ence of a long run relationship among the variables by conducting an F-test to determinethe joint significance of lagged levels of the variables involved, i.e., HN : δ1 = δ2 = δ3 = δ4 = 0against the alternative HA : δ1 /= δ2 /= δ3 /= δ4 /= 0. We denote the test which normalizeson GDPPC by FGDPPC(GDPP|PRIVATE, VTR, ETPT). Similarly, we compute the F-statisticswhen the other variables in Eq. (2) are used as dependent variables and denote themwith FPRIVATE(PRIVATE|GDPPC, VTR, ETPT), FVTR(VTR|GDPPC, PRIVATE, ETPT) andFETPT(ETPT|GDPPC, PRIVATE, VTR).

The null hypothesis of no cointegration among the variables in our model can be rejectedirrespective of the orders of integration for the time series, if the computed F-statistic isshown to be higher than the upper bound of the critical values. Conversely, if the com-puted F-statistic falls within the band, prior information about the direction and the orderof integration of the variables is necessary to make a decision on long-run relationships.Finally, if the statistic falls between the lower and upper critical values, the result is incon-clusive.

3.2.2. Empirical resultsWe found that the variables in our model are mutually cointegrated. The real GDP per capita,

ln(PRIVATE) and ln(VTR) are stationary in their first differences. But, for the ln(ETPT), itis stationary in level. However, we began with our model by testing the effect of the evo-lution of the banks-stock capital relationship on the real economic growth in Tunisia to testthe presence of a long run relationship. We estimated the conditional model (Eq. (2)) usingthe OLS method to determine the appropriate lag length p, using Schwartz–Bayesian Cri-terion (SBC). The null hypothesis (HN : δ1 = δ2 = δ3 = δ4 = 0) of the non existence of a longrun relationship between ln(GDPPC), ln(PRIVATE), ln(VTR) and ln(ETPT) is conclusivelyrejected and the serial correlation free residuals is achieved when the lag order of two(p = 2) is found as suggested by SBC. The calculated F-statistic FGDPPC(GDPPC|PRIVATE,VTR, ETPT) = 8.484 is higher than the upper bound critical value 6.265 at the 1% level.This result suggests that there is evidence for cointegration between the economic growthand financial development indicator for Tunisia for the period under investigation seeTable 1.

The process was repeated for the other variables in our model (PRIVATE, GDPPC, VTR, andETPT). For instance, we ran the model using PRIVATE as the dependent variable and computedthe F-statistic indicated by FPRIVATE(PRIVATE|GDPPC, VTR, ETPT) = 8.050 which is belowNarayan’s higher bound critical value at the 1% level. Table 1 also reports this as well as theresults of the other models. We should notice that they are all lower than the lower bound criticalvalue at the 1% level, which suggests that the null hypothesis of no cointegration cannot berejected except for the credit. An important conclusion that may be drawn here is that two long-runrelationships exist between the economic growth and financial development indicator in Tunisiamainly PRIVATE for the period under investigation. But our objective here is to test the impactof the financial development indicator on the economic growth.

6 According to Narayan (2005), the existing critical values reported in Pesaran et al. (2001) cannot be used for smallsample sizes because they are based on large sample sizes. Narayan (2005) provides a set of critical values for sample sizesranging from 30 to 80 observations. Given the relatively small sample size in this study, we also compare the calculatedF-statistics with the critical values from Narayan (2005). For more details, see Narayan (2005).

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx 9

Table 1Test for cointegration relationship.

Model CalculatedF-statistic

Lag Significancelevel

Critical bound6

F-statistic

I(0) I(1)

FGDPPC(GDPPC|PRIVATE, VTR, ETPT) 8.484a 2 1% 4.428 5.816FPRIVATE(PRIVATE|GDPPC, VTR, ETPT) 8.050a 2 5% 3.164 4.194FETPT(ETPT|GDPPC, PRIVATE, VTR) 3.368b 1 10% 2.618 3.532FVTR(VTR|GDPPC, PRIVATE, ETPT) 1.510b 1

Source of critical values: Narayan (2005).Notes. Estimation period = 1973–2008. The letter a indicates that the statistic lies above the upper bound and letter bindicates that it falls below the lower bound.

However, once cointegration is established the conditional ARDL (p, q1, q2, q3) long-runmodel for ln(GDPPC)t can be estimated as:

ln (GDPPC)t = γ0 +p∑

i=0

γ1 ln (GDPPC)t−i +q1∑

i=0

γ2 ln (PRIVATE)t−i

+q2∑

i=0

γ3 ln (VTR)t−i +q3∑

i=0

γ4 ln (ETPT)t−i + εt (3)

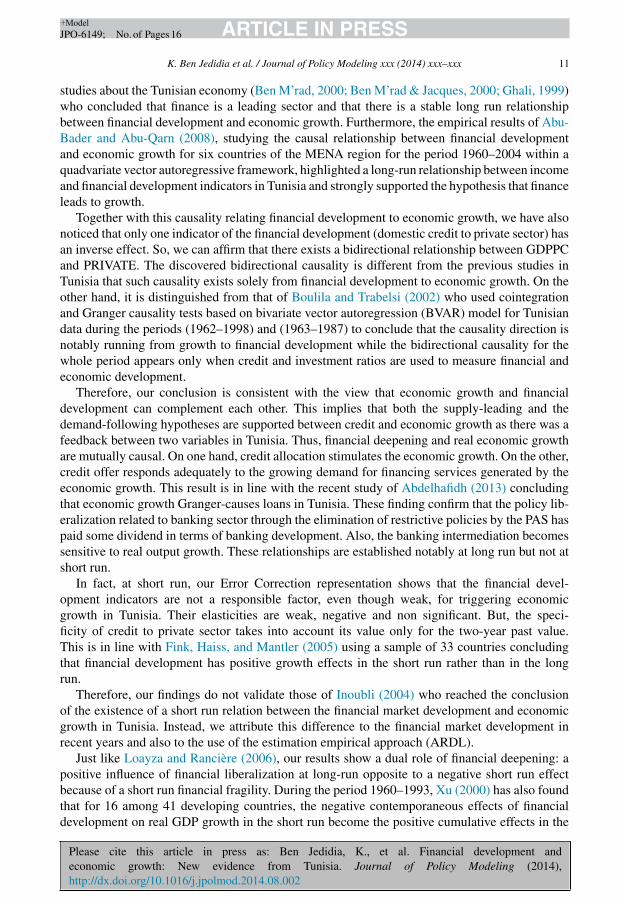

Using the procedure as outlined by Pesaran et al. (2001), we obtained the level long-runparameter estimates of the model. The ARDL model in levels using order (2, 2, 0, 2) as selectedby the SBC along with their asymptotic standard errors are shown in Table 2. The results for

Table 2ARDL estimation.

Regressor Coefficient Standard error t-Ratio t-Probability

Long run relationshipEq. (3): ARDL(2, 2, 0, 2) selected based on SBC. Dependent variable is ln(GDPPC)

C 6.471 0.716 9.033 0.000ln(PRIVATE) 3.360 1.089 3.085 0.006ln(VTR) −0.243 0.134 −1.806 0.086ln(ETPT) −0.108 0.113 −0.950 0.353

Error correction representationC 0.022 0.008 2.54 0.018�ln(GDPPC)t−1 0.062 0.189 0.32 0.745�ln(GDPPC)t−2 0.187 0.168 1.11 0.277�ln(PRIVATE)t 0.039 0.064 0.61 0.547�ln(PRIVATE)t−1 −0.054 0.054 −0.99 0.328�ln(PRIVATE)t−2 −0.131 0.056 −2.31 0.031

�ln(VTR)t 0.006 0.007 0.85 0.400�ln(ETPT)t −0.0007 0.004 −0.17 0.864�ln(ETPT)t−1 −0.007 0.004 −1.62 0.118�ln(ETPT)t−2 −0.0018 0.004 −0.42 0.676ecmt−1 −1.17 0.389 −3.01 0.006

R2 = 0.75.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

10 K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx

Fig. 3. Plot of CUSUM.

Fig. 4. Plot of CUSUM-squared.

the long-run estimation, as observed in Table 2, show that not all the coefficients are statisticallysignificant (at the 5% level) and carry the expected signs as suggested by theory but with othersings which are not reasonable in their magnitudes.

Next, we assess the stability of the long-run relationship between the economic growth and thefinancial development indicator. We rely upon the CUSUM and CUSUM-squared tests proposedby Brown, Durbin, and Evans (1975) to test for constancy of the long-run parameters. We applythe test to the residual of the model. The CUSUM statistics are based on the cumulative sumof recursive residuals based on the first set of observations. If the plot of the CUSUM statisticsstays within the 5% significance level, then the estimates are stable. The same applies to theCUSUM-squared statistics. As can be seen in Figs. 3 and 4 the plot of CUSUM and the plot ofCUSUM-squared statistics stay within the critical bounds (represented by a pair of straight lines)indicating the stability in the coefficients over the sample period.

4. Discussion

Our findings suggest that the financial development measured by private credit spurs economicgrowth in Tunisia in the long run. However, we did not find robust and significant effects betweenissuing banks’ securities on the financial market and economic growth in the short run as well asin the long run.

Our results are in agreement with several studies such as Goldsmith (1969), Rajan and Zingales(1998), Abu-Bader and Abu-Qarn (2008), Lartey (2010) who found a positive relationship betweenfinancial development and GDP per capita. Besides, our results are in line with those of previous

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx 11

studies about the Tunisian economy (Ben M’rad, 2000; Ben M’rad & Jacques, 2000; Ghali, 1999)who concluded that finance is a leading sector and that there is a stable long run relationshipbetween financial development and economic growth. Furthermore, the empirical results of Abu-Bader and Abu-Qarn (2008), studying the causal relationship between financial developmentand economic growth for six countries of the MENA region for the period 1960–2004 within aquadvariate vector autoregressive framework, highlighted a long-run relationship between incomeand financial development indicators in Tunisia and strongly supported the hypothesis that financeleads to growth.

Together with this causality relating financial development to economic growth, we have alsonoticed that only one indicator of the financial development (domestic credit to private sector) hasan inverse effect. So, we can affirm that there exists a bidirectional relationship between GDPPCand PRIVATE. The discovered bidirectional causality is different from the previous studies inTunisia that such causality exists solely from financial development to economic growth. On theother hand, it is distinguished from that of Boulila and Trabelsi (2002) who used cointegrationand Granger causality tests based on bivariate vector autoregression (BVAR) model for Tunisiandata during the periods (1962–1998) and (1963–1987) to conclude that the causality direction isnotably running from growth to financial development while the bidirectional causality for thewhole period appears only when credit and investment ratios are used to measure financial andeconomic development.

Therefore, our conclusion is consistent with the view that economic growth and financialdevelopment can complement each other. This implies that both the supply-leading and thedemand-following hypotheses are supported between credit and economic growth as there was afeedback between two variables in Tunisia. Thus, financial deepening and real economic growthare mutually causal. On one hand, credit allocation stimulates the economic growth. On the other,credit offer responds adequately to the growing demand for financing services generated by theeconomic growth. This result is in line with the recent study of Abdelhafidh (2013) concludingthat economic growth Granger-causes loans in Tunisia. These finding confirm that the policy lib-eralization related to banking sector through the elimination of restrictive policies by the PAS haspaid some dividend in terms of banking development. Also, the banking intermediation becomessensitive to real output growth. These relationships are established notably at long run but not atshort run.

In fact, at short run, our Error Correction representation shows that the financial devel-opment indicators are not a responsible factor, even though weak, for triggering economicgrowth in Tunisia. Their elasticities are weak, negative and non significant. But, the speci-ficity of credit to private sector takes into account its value only for the two-year past value.This is in line with Fink, Haiss, and Mantler (2005) using a sample of 33 countries concludingthat financial development has positive growth effects in the short run rather than in the longrun.

Therefore, our findings do not validate those of Inoubli (2004) who reached the conclusionof the existence of a short run relation between the financial market development and economicgrowth in Tunisia. Instead, we attribute this difference to the financial market development inrecent years and also to the use of the estimation empirical approach (ARDL).

Just like Loayza and Rancière (2006), our results show a dual role of financial deepening: apositive influence of financial liberalization at long-run opposite to a negative short run effectbecause of a short run financial fragility. During the period 1960–1993, Xu (2000) has also foundthat for 16 among 41 developing countries, the negative contemporaneous effects of financialdevelopment on real GDP growth in the short run become the positive cumulative effects in the

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

12 K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx

long-term. Thus, we can conclude that the effect of finance on growth is established over timemainly in the context of weaknesses in the Tunisian productive system as well as in the economicinstability. Consequently, the undertaken reforms aiming to enhance development should havetargeted not only the long run but the short run, as well.

We should underline, however, the important impact of credits on growth of GDP per capitaat long run. In fact, any increase of credits of 1% results in an increase of 3.360 of the real GDPper capita. The private credit is economically meaningful thanks to deposit mobilization and theinvestment of financial resources in the private sector. This result clearly conforms that of thecross country study of King and Levine (1993) who found that countries initially enjoying alarger credit sector experienced faster growth in the following thirty years.

The Tunisian financing system has clearly been dominated by the classical intermediation(credits–deposits) since the commercial banks are the greatest collectors of savings and privilegeddistributors of credits. The Tunisian economy has, in fact, moved from an “overdraft economy” toa “liberalized overdraft economy” despite liberalization and promotion measures of the markets.

Our results also show that the growth in the real side of the economy has stimulated the increaseof credits in response to a higher demand for financial services. The inefficiency of the Tunisianbanks declined due to the privatization of many State-Owned Banks and the integration of foreigncapitals in the banks. The NPL (Non Productive Loans) ratio has decreased from 19% in 2001 to13.2% in 2009 (IMF, 2010), which reduces the exposure of the vulnerable sectors.

At long run, the value traded ratio is negatively related to growth in Tunisia. Nevertheless, itselasticity is around 24.3% and is significant only at 10%. Its impact is weak, indicating that thestock market is not a component of the national growth in Tunisia (see Table 2). The findingsabout the absence of causality imply that the evolution of the value traded was not affected directlyby the monetary and financial policy applied in Tunisia over the period of study. Similarly, theempirical results of Ben Naceur et al. (2008) indicate that the stock market liberalization has noeffect on economic and investment growth.

But, Rioja and Valev (2004) proved that the financial markets have an uncertain effect ongrowth for countries with a very low level of financial development. In our study, the weaknessand negative link between economic growth and development of financial market reflect pervasiveinefficiencies in the allocation mechanism in the underdeveloped and emergent stock market.7 Infact, since 2000 the dynamic evolution of the Tunisian financial market has strongly been tiedto the introduction of public securities to the stock market (Negotiable Treasury Bills). In thatyear, the public securities represented 90% of the emissions through the public appeal to saving.Since 2003, public securities are no longer issued on the monetary market but rather on the bondmarket. This importance of the public securities to the financial market has caused an “evictioneffect” of the private sector financed by the public investments allowing the financing of publicdeficits. As a result, the reform toward a market-oriented economy failed to establish a financialmarket which contributes to economic development. On the opposite, this financial market doesnot react to the economic growth.

Furthermore, we did not really find a causality relationship running from economic growthto the activity of financial market. This might be explained by the fact that the level of theeconomic growth in Tunisia is not high enough to stimulate the stock market development as wellas the dominance of banks that provided the necessary support to economic growth. In fact, stock

7 On 30 June 2011, the Tunisian financial market remained limited as the number of companies which capital sharesare admitted to the stock market is of 57 among which 21 are financial companies (11 banks, 6 leasing companies, and 4insurance companies).

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx 13

markets tend to be more active and efficient relative to banks in developed and richer countries(Demirgüc-Kunt & Levine, 2001).

The elasticity of issuing bank stock-exchange securities on the financial market noted by(ETPT) is in fact negative, weak and non significant at short as well as long runs (see Table 2).Besides, there is no causality relationship between ETPT and economic growth. Therefore, wecan deduce that the banks’ role in the intermediation-market process is so inconsistent that itcannot promote economic growth. This can be explained by: first the insufficient amount ofsecurities issued by banks in comparison with the approved credits; then the insufficiencies of thefinancial market itself. Finally, the bankers-intermediaries monopole in the stock market was atthe origin of an anti-market practice responsible for the marginalization of the saving placements.Before 1994, banks were asked to play the roles of intermediaries at the stock exchange and thatof a financial intermediary simultaneously. To guarantee their functioning and survival, bankswere rather motivated to direct their customers toward bank placements aiming at increasing theirdeposits rather than urging them to carry out placements in the stock market. Since then, the 94-117law forbade banks from practicing this intermediation role starting from 15th, November 1995.This reform made banks shift toward a new policy. The rehabilitation of the banks’ interventionswas expected to stimulate the market development since they can prepare their customers (mainlyenterprises) to familiarize with the markets. They can support the functioning of the market thanksto the liquidity they can provide, as well. Such a reinforcement of these relations is also beneficialto the development of the banks as the financial market is a means of recycling, an outlet ofgathering of financial assets for these banks.

5. Conclusions and policy implications

This paper re-investigates the empirical relationship between financial development and eco-nomic growth in Tunisia during the period 1973–2008. It might be viewed as an additionalcontribution to the anterior studies yet considering the period of the 2000s. We employ an econo-metric technique which is Autoregressive Distributed Lag (ARDL). Our objective is to test thelong run relationship between economic growth reflected by the real GDP per capita and financialdevelopment indicators. The results seem to give an important support to the hypothesis that thefinancial development reflected by total credit to private sector is a leading sector in the long rungrowth process but not at the short run. This result is in line with many above mentioned previousstudies relative to the Tunisian economy.

At short run, only the specificity of credit to private sector takes into account its value for thetwo year past is an impact on economic growth. This shows that the banking sector is an importantcomponent of the national growth. Moreover, we found that economic growth promotes bankingdevelopment. Then, there is a bi-directional causality between banking development and economicgrowth.

The banks’ emission of securities on the financial market has no significant role, neither at theshort run nor at the long one. This could be explained by the weaknesses of the emerging financialmarket. The other possible explanation is the “eviction effect” between the classical intermediation(credit–deposit) and the intermediation-market. Banks tend to gather funds on the market butuse them to increase their credit activities and not at the service of developing the financialmarket. Furthermore, the role of the financial market in economic growth has unfortunately beenmarginalized i.e. it suffers from narrowness, lack of information transparency, domination ofpublic issuing of bond market etc. despite all the measures taken to revitalize it and provide longrun available saving resources.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

14 K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx

In the light of our findings, the banking development in Tunisia is considered as a policyvariable to boost the economic growth. This same economic growth is considered as a pol-icy variable to generate the banking development. It is recommended that Tunisia continue onthe way of financial liberalization to deepen the financial sector to reach sustainable growth atlong run. To enhance the long run relationship between the financial sector and the real eco-nomic sector, it is desirable to further improve the efficiency of the financial system throughappropriate regulatory policy reforms such as applying more efficient legal and fiscal systems.As suggested by Bittencourt (2012), more financial development needs more macroeconomicperformance.

The main policy debate is whether it is more appropriate to reinforce the bank based systemor to concentrate the efforts to develop the stock market via the development the intervention ofBanks in the stock market.

For the first alternative, the most appropriate policy would be to privilege the improvement ofthe banking sector performance thanks to a total privatization of this sector and the establishmentof a fully independent Central Bank.

As for the second alternative, the policy implication is that Tunisia should give policy priorityto stock market adequate reforms because this market allows a greater diversification of risks andbetter allocation of resources as an alternative source to finance and boost the real economy. In thiscontext the development of the intermediation-market can stimulate the growth of the financialmarket since countries with well-developed banking sectors also tend to have well-developed stockmarkets. It is important that a variety of institutional investors, such as insurance companies, haveto be integrated in this intermediation-market relationship to make it healthier.

Finally, it is highly desirable to expand the scope of our study to encompass a wide comparisonbetween the Maghreb countries which have experienced diverse growth experiences and financialreforms.

Acknowledgements

We are extremely grateful to Hammami Soufiane (Tunisian Stock Market Council) for his helpin the collection of data related to Tunisian Stock Market. We would like to thank the TunisianMinistry of Higher Education for providing facilities to make this research possible. We wouldalso like to thank Mr. Abdelmajid Dammak for his help with the English and the proofreading ofthis paper.

Appendix.

The data of this study are from the following sources: World Development Indicators (2010),Tunisian Stock Market Council, International Financial Statistics of the IMF (2010) Tunisia:Selected Issues, IMF Country Report No. 10/109 and Global Innovation Index Report 2009-2010.INSEAD, 30-Mar-2010.

References

Abdelhafidh, S. (2013). Potential financing sources of investment and economic growth in North African countries: Acausality analysis. Journal of Policy Modeling, 35, 150–169.

Abu-Bader, S., & Abu-Qarn, A. M. (2008). Financial development and economic growth: Empirical evidence from MENAcountries. Review of Development Economics, 12, 803–817.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx 15

Allen, F., & Gale, D. (2000). Comparing financial systems. Cambridge, MA: MIT Press.Allen, F., & Santomero, A. M. (1998). The theory of financial intermediation. Journal of Banking and Finance, 21,

1461–1485.Allen, F., & Santomero, A. M. (2001). What do financial intermediaries do? Journal of Banking and Finance, 25, 271–294.Beck, T., Demirguc-Kunt, A., & Levine, R. (2009). Financial institutions and markets across countries and over time –

Data and analysis. Policy Research Working Paper Series (No. 4943) The World Bank.Beck, T., & Levine, R. (2001). . Stock markets, banks, and growth: correlation or causality? World Bank Policy, Research

Working Paper (No. 2670).Ben M’rad, F. W. (2000). Financial development and economic growth: Time-series evidence from south Mediterranean

countries. Working Paper. Université Paris IX Dauphine.Ben M’rad, F. W., & Jacques, J. F. (2000). La relation finance - développement: un éclairage par le modèle de vecteur

à correction d’erreurs pour cas du système financier tunisien. In XVIIème Journées Internationales d’EconomieMonétaire et Bancaire Lisbonne, Portugal, 06-2000.

Ben Naceur, S., Ghouzoani, S., & Omran, M. (2008). Does stock market liberalization spur financial and economicdevelopment in the MENA region? Journal of Comparative Economics, 36, 673–693.

Bittencourt, M. (2012). Financial development and economic growth in Latin America: Is Schumpeter right? Journal ofPolicy Modeling, 34, 341–355.

Boot, A. W. A., & Thakor, A. V. (1997). Banking scope and financial innovation. Review of Financial Studies, 10,1099–1131.

Boulila, G., & Trabelsi, M. (2002, September). Financial development and long-run growth: granger causality in abivariate VAR structure, evidence from Tunisia: 1962–1997. FSEGT Working Paper.

Boulila, G., & Trabelsi, M. (2004). The causality issue in the finance and growth nexus: Empirical evidence from MiddleEast and North African countries. Review of Middle East Economics and Finance, 2, 123–138.

Brown, R. L., Durbin, J., & Evans, J. M. (1975). Techniques for testing the constancy of regression relationships overtime (with Discussion). Journal of the Royal Statistical Society, 37, 149–192.

Deidda, L., & Fattouh, B. (2008). Banks, financial markets and growth. Journal of Financial Intermediation, 17, 6–36.Demirgüc-Kunt, A., & Levine, R. (2001). Financial structure and economic growth. Cambridge: MIT Press.Dolar, V., & Meh, C. (2002). Financial structure and economic growth: A non-technical Survey. Working Paper 2002-24.

Bank of Canada.Engle, R. F., & Granger, C. W. J. (1987). Co-integration and error correction: Representation, estimation and testing.

Econometrica, 55, 251–276.Fink, G., Haiss, P., & Mantler, H. C. (2005). The finance-growth-nexus: Market economies vs transition countries. Europa

institut Working Paper No. 64.Ghali, K. H. (1999). Financial development and economic growth: The Tunisian experience. Review of Development

Economics, 3, 310–322.Goldsmith, R. (1969). Financial structure and development. New Haven: Yale University Press.Gorton, G., & Pennacchi, G. (1990). Financial intermediaries and liquidity creation. Journal of Finance, 45, 49–71.Greenwood, J., & Jovanovic, B. (1990). Financial development, growth, and the distribution of income. Journal of Political

Economy, 98, 1076–1107.Gurley, J. G., & Shaw, E. S. (1960). Money in a theory of finance. Washington: Brooking Institution.Inoubli, C. (2004). Le Développement financier et la croissance économique: le cas de la Tunisie. Paper presented at 8ème

Rencontres Euro-méditerranéennes Conférence. Réformes financières et performances économiques dans le contextedes intégrations régionales, 8-10 décembre 2004. Tunis.

Johansen, S. (1991). Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models.Econometrica, 59, 1551–1580.

King, R. G., & Levine, R. (1993). Finance, entrepreneurship and growth: Theory and evidence. Journal of MonetaryEconomics, 32, 513–542.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (1997). Legal determinants of external finance. Journal ofFinance, 52, 1131–1150.

Lartey, E. (2010). A note on the effect of financial development on economic growth. Applied Economics Letters, 17,685–687.

Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic literature, 35,688–726.

Levine, R. (2005). Finance and growth: Theory, mechanism and evidence. In P. Aghion, & S. N. Durlauf (Eds.), Handbookof economic growth (pp. 865–934). North-Holland: Elsevier.

Please cite this article in press as: Ben Jedidia, K., et al. Financial development andeconomic growth: New evidence from Tunisia. Journal of Policy Modeling (2014),http://dx.doi.org/10.1016/j.jpolmod.2014.08.002

ARTICLE IN PRESS+ModelJPO-6149; No. of Pages 16

16 K. Ben Jedidia et al. / Journal of Policy Modeling xxx (2014) xxx–xxx

Loayza, N. V., & Rancière, R. (2006). Financial development, financial fragility, and growth. Journal of Money, Credit,and Banking, 38, 1051–1076.

Luintel, K. B., Khan, M., Arestis, P., & Theodoridis, K. (2008). Financial structure and economic growth. Journal ofDevelopment Economics, 86, 181–200.

Matthews, K., & Thompson, J. (2008). The economics of banking. Chichester: Wiley.Merton, R. C., & Bodie, Z. (1995). A conceptual framework for analyzing the financial environment. In Crane, Crane,

et al. (Eds.), The global financial system: A functional perspective (pp. 3–31). Boston: Harvard Business School Press.Narayan, P. K. (2005). The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics,

37, 1979–1990.Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal

of Applied Economics, 16, 289–326.Rajan, R. G., & Zingales, L. (1998). Financial dependence and growth. American Economic Review, 88, 559–586.Rioja, F., & Valev, N. (2004). Finance and the sources of growth at various stages of economic development. Economic

Inquiry, 42, 127–140.Schumpeter, J. (1911). The theory of economic development. , 1934, 1964. New York.Song, F., & Thakor, A. V. (2010). Financial system architecture and the co-evolution of banks and capital markets. The

Economic Journal, 120, 1021–1055.Subrahmanyam, A., & Titman, S. (1999). The going-public decision and the development of financial markets. Journal

of Finance, 54, 1045–1082.Xu, Z. (2000). Financial development, investment, and economic growth. Economic Inquiry, 38, 331–344.