Embed Size (px)

Citation preview

INFORMING TODAY’S INVESTORS

Financial Capability in the United StatesReport on the National Survey Component of the National

Financial Capability Study – December 2009

Presenters

John Gannon

President, FINRA

Investor Education Foundation

Annamaria Lusardi

Dartmouth College, Financial Literacy Center, and U.S. Treasury

Copyright 2007, FINRA Investor Education Foundation

Objective

Annamaria Lusardi (Dartmouth College)

Applied Research & Consulting LLC (ARC)

FINRA Investor Education Foundation

Office of Financial Education, U.S. Treasury Department

Additional input from:

– Craig Copeland, Employee Benefit Research Institute (EBRI)

– American Institute of Certified Public Accountants (AICPA)

– Bob Willis, Univ. of Michigan, past PI of U.S. Health and Retirement Study

Establish a baseline measure of the ability of

Americans to manage their money.

Multi-Disciplinary Team:

Copyright 2007, FINRA Investor Education Foundation

Study Methodology

National Financial Capability Study includes three

linked surveys:

1. National Survey: Nationally-projectable telephone

survey of 1,488 American adults

2. State-by-State Survey: Online survey of

approximately 25,000 respondents (roughly 500 per

state + DC)

3. Military Survey: Online survey of 800 military

personnel and spouses

Copyright 2007, FINRA Investor Education Foundation

Four Key Financial Capability Components

1. Making Ends Meet

2. Planning Ahead

3. Managing Financial Products

4. Financial Knowledge and

Decision-Making

Copyright 2007, FINRA Investor Education Foundation

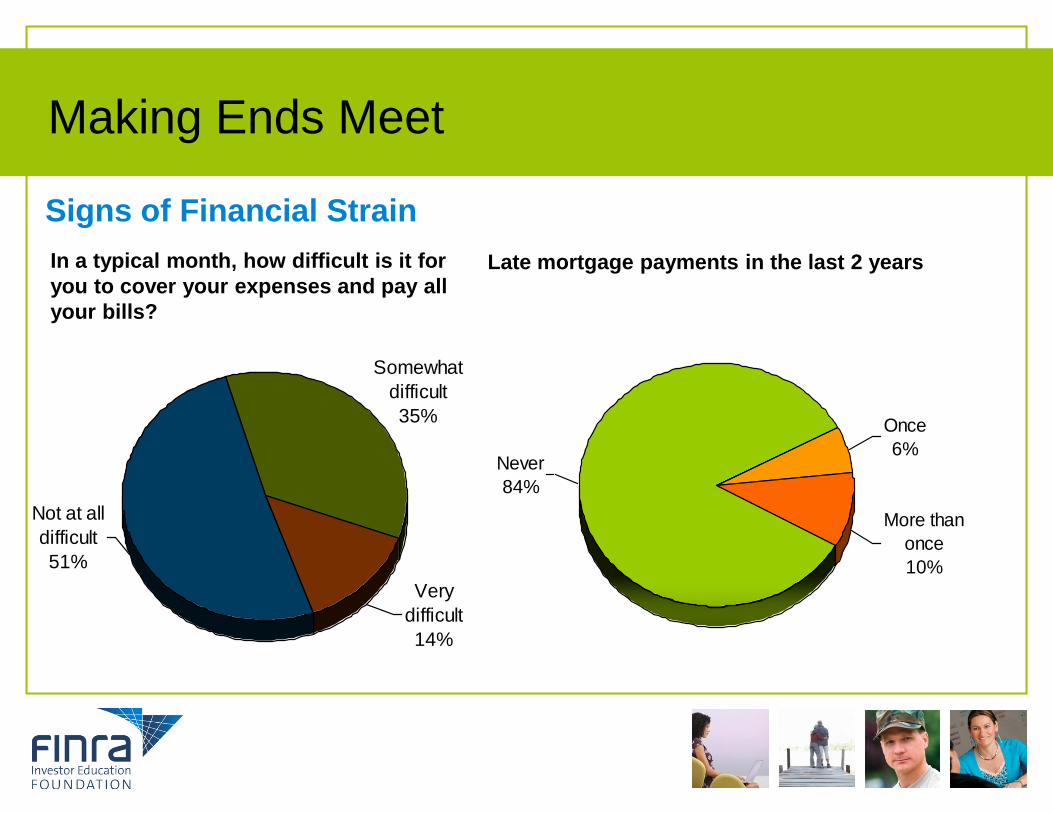

Making Ends Meet

Very

difficult

14%

Not at all

difficult

51%

Somewhat

difficult

35%

In a typical month, how difficult is it for

you to cover your expenses and pay all

your bills?

Signs of Financial Strain

More than

once

10%

Never

84%

Once

6%

Late mortgage payments in the last 2 years

Making Ends Meet

28%

53%

79%

27%

9%

18%

38%

45%

3%

0%

25%

50%

75%

100%

<$25K $25-75K $75K+

% R

espondents

Very

difficult

Somewhat

difficult

Not at all

difficult

In a typical month, how difficult is it for

you to cover your expenses and pay all

your bills?

41%

33%

23%

0%

10%

20%

30%

40%

50%

<$25K $25-75K $75K+

% R

espondents

Respondents with unexpected large drop

in income in past 12 months

Copyright 2007, FINRA Investor Education Foundation

Low Income Households Under Greatest Strain

Second Component of Financial Capability

Making Ends Meet

2. Planning Ahead

Copyright 2007, FINRA Investor Education Foundation

Many Americans Don’t Plan Ahead

Yes: Other

Savings

26%

Yes: Tax-

Advantaged

Account

14%

No

58%

Don't

know

2%

Are you setting aside any money for

your children's college education?

No

51%

Yes

49%

Have you set aside an emergency or

rainy day fund??

Yes

42%No

58%

Have you ever tried to figure out how much

you need to save for retirement?

Copyright 2007, FINRA Investor Education Foundation

Those Most at Risk Are Least Prepared for Emergencies...

49%45%

31%26%

31% 31%23%

44%

0%

20%

40%

60%

80%

100%

Total Female 18-29 <$25K Black Hispanic Less

than HS

HS grad

% R

espo

nden

ts

Respondents with emergency or rainy day funds that would cover

expenses for 3 months

Copyright 2007, FINRA Investor Education Foundation

...And Least Likely to Plan for Retirement

42% 39%

23%17%

38%

20%

41%

22%28%

0%

20%

40%

60%

80%

100%

Total Female 18-29 <$25K Black Hispanic Asian Less

than HS

HS grad

% R

espondents

Respondents who have tried to figure out how much to save for retirement

Copyright 2007, FINRA Investor Education Foundation

Third Component of Financial Capability

Making Ends Meet

Planning Ahead

3. Managing Financial Products

Copyright 2007, FINRA Investor Education Foundation

Lack of Assets

Respondent has… Total African-

Americans

Hispanics

No bank accounts (neither checking nor saving) 12% 28% 30%

No credit cards 31% 49% 42%

No retirement accounts 38% 53% 55%

No home that they own 39% 59% 58%

No stocks, bonds or mutual funds outside of

retirement accounts

53% 72% 73%

Copyright 2007, FINRA Investor Education Foundation

No Bank Accounts

Unbanked respondents (no checking or savings accounts)

12% 14%22%

31% 28% 30%36%

15%

0%

20%

40%

60%

80%

100%

Total Female 18-29 <$25K Black Hispanic Less

than HS

HS grad

% R

espo

nden

ts

Copyright 2007, FINRA Investor Education Foundation

Profile of the Unbanked

Reasons for Not Having a Bank Account

Which of the following are reasons why you do not have a checking or

savings account?

72%

35%

35%

34%

0% 20% 40% 60% 80% 100%

Do not have

enough money to

make it worthwhile

Do not want to

share my personal

information

Bank fees are too

high

Do not like dealing

with banks

% Yes

Copyright 2007, FINRA Investor Education Foundation

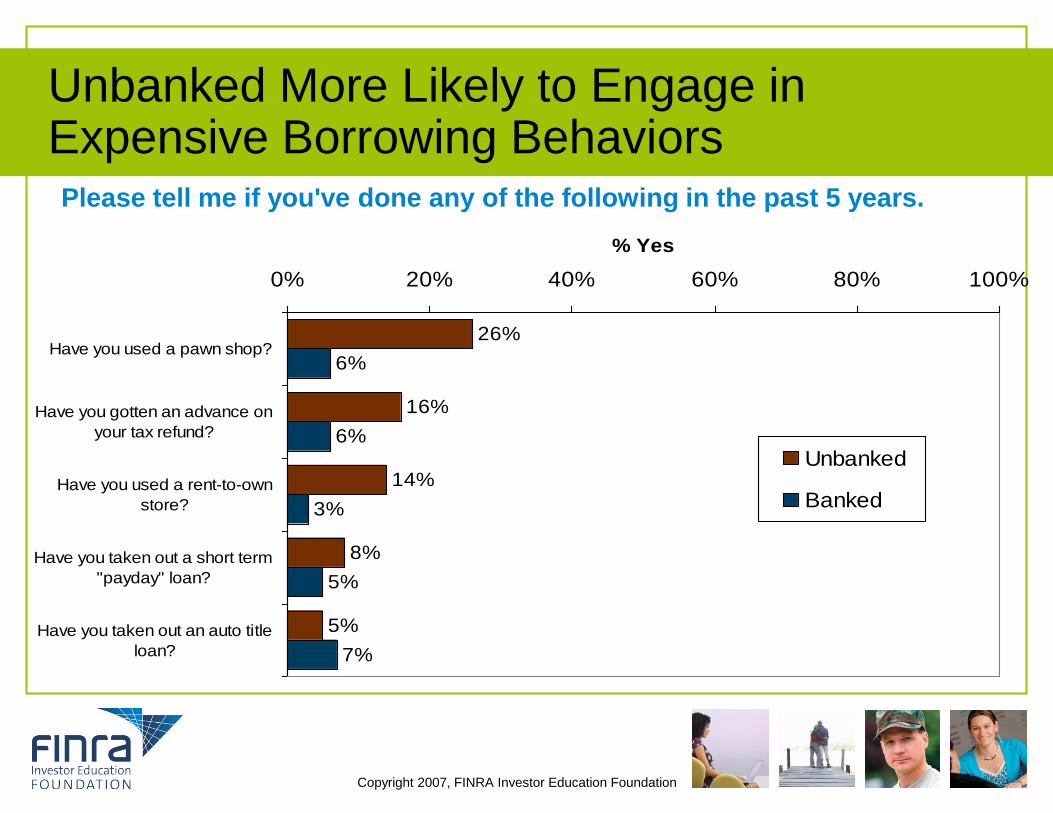

Unbanked More Likely to Engage inExpensive Borrowing BehaviorsPlease tell me if you've done any of the following in the past 5 years.

26%

16%

14%

8%

5%

6%

6%

3%

5%

7%

0% 20% 40% 60% 80% 100%

Have you used a pawn shop?

Have you gotten an advance on

your tax refund?

Have you used a rent-to-own

store?

Have you taken out a short term

"payday" loan?

Have you taken out an auto title

loan?

% Yes

Unbanked

Banked

Copyright 2007, FINRA Investor Education Foundation

Credit Cards

In the past 12 months… Total 18-29 30-44 45-59 60+

I always paid credit cards in full 54% 51% 45% 44% 75%

In some months, I carried over a balance

and was charged interest

51% 46% 62% 58% 33%

In some months, I paid the minimum

payment only

29% 41% 35% 31% 11%

In some months, I was charged a fee for

late payment

23% 24% 27% 29% 11%

In some months, I was charged a fee for

exceeding my credit line

8% 14% 8% 9% 2%

In some months, I used the cards for a

cash advance

8% 11% 10% 8% 5%

Copyright 2007, FINRA Investor Education Foundation

12% of respondents who do not pay in full each month do not know the interest

rate on their credit card.

Home Ownership and Mortgages

Homeowners that

stated

Total <$25K $25-$75K >$75K

Have a mortgage 61% 31% 61% 77%

Have line of credit 21% 11% 20% 27%

Copyright 2007, FINRA Investor Education Foundation

When asked whether they have a mortgage that is either an interest-only mortgage

or has an interest-only option, 20% responded they did not know the answer to this

question.

Moreover, 10% of mortgage borrowers did not know the interest rate they are

paying on their mortgage.

Retirement Accounts and Investments

Respondents

who…

Total <$25K $25-

$75K

>$75K Less

than

HS

HS Some

College

College

Have a retirement

plan via employer

51% 13% 61% 83% 22% 39% 54% 76%

Have other

retirement accounts

28% 4% 27% 57% 7% 14% 26% 55%

Have stocks, bonds

or mutual funds

outside of retirement

accounts

46% 17% 47% 72% N/A 34% 46% 66%

Copyright 2007, FINRA Investor Education Foundation

Note that about 9% of those with self directed retirement accounts have taken a loan from their

retirement accounts and 5% have taken a hardship withdrawal.

Moreover, 17% of those with self-directed accounts do not know how their wealth was allocated in

their accounts and 37% did not know whether they invested primarily in life-cycle funds,

Fourth Component of Financial Capability

Making Ends Meet

Planning Ahead

Managing Financial Products

4. Financial Knowledge and

Decision-Making

Copyright 2007, FINRA Investor Education Foundation

Highly Positive Self-Perceptions

6% 2% 4%12% 12%

17%

46%

0%

25%

50%

75%

100%

1 -

Strongly

Disagree

2 3 4 -

Neither

5 6 7 -

Strongly

Agree

% R

espondents

I am good at dealing with day-to-day

financial matters.

5% 3% 4%11% 13% 18%

46%

0%

25%

50%

75%

100%

1 -

Strongly

Disagree

2 3 4 -

Neither

5 6 7 -

Strongly

Agree

% R

espondents

I am pretty good at math.

5% 3% 6%

16%

32%

20% 17%

0%

25%

50%

75%

100%

1 - Very

Low

2 3 4 5 6 7 - Very

High

% R

espondents

How would you assess your overall financial knowledge?

Top 3 = 75% Top 3 = 77%

Top 3 = 70%

Copyright 2007, FINRA Investor Education Foundation

Financial Literacy

Count of correct and incorrect quiz answers (total 5 questions)

Number of correct answers Number of incorrect answers

2.722.46

2.16

2.69

2.022.28

2.07 2.032.29

1.14 1.14 1.451.02 1.38 1.61 1.52 1.28 1.32

00.5

11.5

22.5

33.5

4

4.55

Total Female 18-29 60+ <$25K Black Hispanic Less

than HS

HS grad

Mean

Copyright 2007, FINRA Investor Education Foundation

Self-Perception versus Financial Behavior

However, 24% who

strongly agreed and 40%

who agreed engaged in

behaviors that generated

fees or high costs.

Copyright 2007, FINRA Investor Education Foundation

“I am good at dealing with day-to-day financial matters”Respondents with credit cards and checking accounts

50%

Strongly

agreed

20%

13%

9%

Disagreed

9%

71-3

4

56

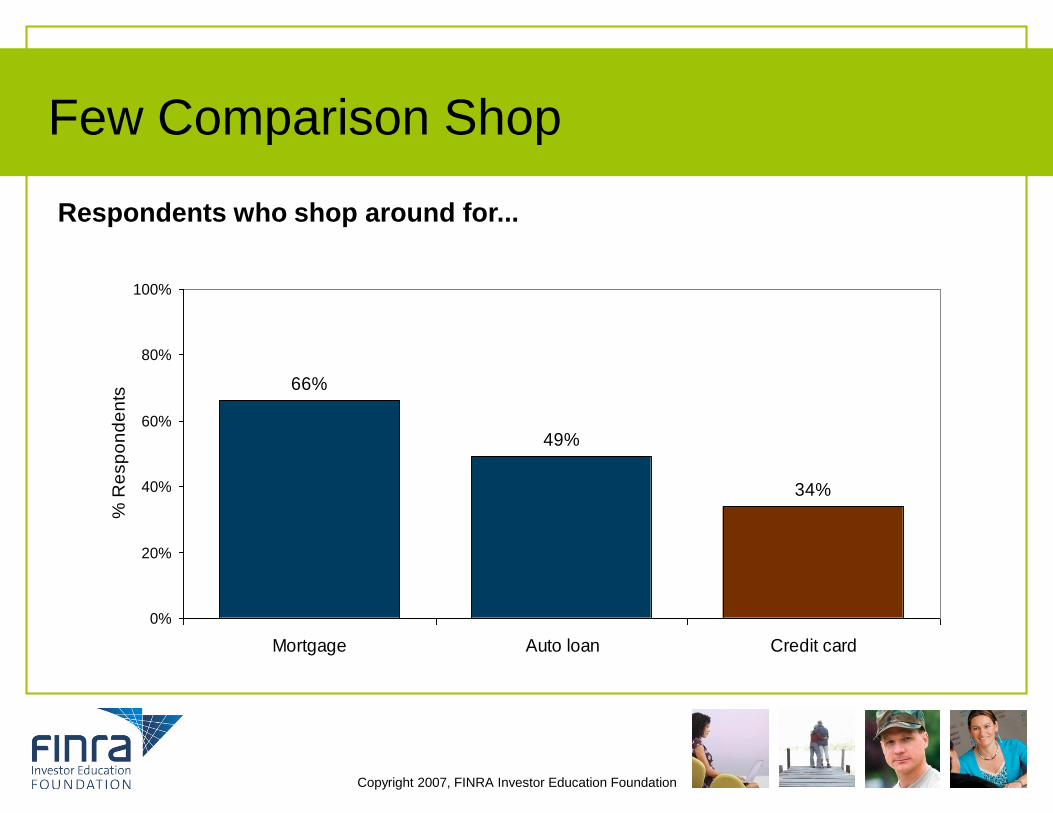

Few Comparison Shop

Respondents who shop around for...

66%

49%

34%

0%

20%

40%

60%

80%

100%

Mortgage Auto loan Credit card

% R

esp

on

de

nts

Copyright 2007, FINRA Investor Education Foundation

Few Obtain Credit Scores and Reports

Respondents

who, in the past

12 months,…

Total <$25K $25-

$75K

>$75K Less

than HS

HS Some

College

College

Obtained copy of

credit report

38% 18% 43% 56% 25% 30% 39% 53%

Checked credit

score

36% 15% 42% 55% 22% 29% 35% 53%

Copyright 2007, FINRA Investor Education Foundation

Summary

The survey provides evidence that:

People are not well equipped to make financial decision

People are not well informed about the terms of their financial

contracts and they do not shop around

The majority of Americans do not plan ahead for life-cycle

events and do not insure against unexpected ones

Many incur in behaviors that generate fees, interest payments,

and other costs

There are signs of financial distress

The groups displaying lower financial capability are those with

low income, low education, and minorities

Copyright 2007, FINRA Investor Education Foundation

Next Steps

National Survey

Analysis of open-ended numeric responses

Data will be made available to the public for independent analysis

State-By-State Survey

Preparation of report for public release (2010)

Large data set will enable much more detailed analysis of specific

demographic groups and opportunity for state-by-state comparison

Data will be made available to the public for independent analysis

Military Survey

Preparation of report for public release (2010)

Data will be made available to the public for independent analysis

Copyright 2007, FINRA Investor Education Foundation