Embed Size (px)

Citation preview

Domingo Alvarez, CPA, Managing Partner Alvarez & Mendoza, PA Certified Public Accountants 9830 SW 77 Avenue, Suite 115 Miami, FL 33156 Email. [email protected] (o) 305.275.3011

FINANCIAL SOUNDNESS

Presentation

Ratio Exercises

Q&A (Any time during presentation)

Presentation Format

Stability is the ability to withstand a temporary problem, such as a decrease in sales

Financial soundness can keep your school from progressing (i.e. adding a new program, branches, etc).

Why Is Financial Soundness So Important

Many schools are started by technicians with a desire to teach other people their trade

When you start a business you also become the entrepreneur and the manager of your company. The company depends on your ability to manage results

Why Is Financial Soundness So Important

Florida Commission for Independent Education Rules

How to financially survive a CIE application

Financial improvement plan

Important terms defined

Understanding your financial statements

Important ratios

Objectives

www.fldoe.org/cie [Chapter 6E FL Administrative Code]

Standard 6 - Finances

CIE Rules

All institutions must demonstrate that the financial structure of the institution is sound, with resources sufficient for the proposed operations of the institution and the discharge of its obligations to the students.

Commission for Independent Education Rules

CIE utilizes different forms to determine financial soundness:

A business plan (Form 605)

A budget (Form 606)

A proforma balance sheet

Financial statement compiled, reviewed or audited of the parent corporation and/or personal for new schools

All of these must tie together!

Commission for Independent Education Rules

How CIE quantifies financial stability:

1. Current assets exceed current liabilities (Greater than 1 to 1 current ratio)

2. Positive net working capital (current assets – current liabilities > 0)

3. Profit or surplus for the prior year

Commission for Independent Education Rules

Ensure that you submit financials at the level CIE, your accrediting body and the U.S. Department of Education needs

Commission for Independent Education Rules

Business Plan -

To be successful you must have a real strategic plan

Documentation of your thought process and how you came to the conclusion that is was a good idea to open a school.

This document is a living breathing plan

CIE Forms

This document must agree with your budget, proforma statement and reason

Take time to perform a market study of the schools in your area, the programs they offer, and the prices they charge.

Business plan - > 605_Business_Plan.docx

CIE Forms

Budget –

A budget is a financial summary of what you expect the next 12 months will look like

It includes revenues, expenses and capital improvements

The end result must take into consideration your business plan

CIE Forms

When developing a budget take care in considering your inputs

Start with a zero based budget approach. Develop each entry from scratch

Don’t just take a number and divide it by 12. Expenses usually do not work that way

Budget - > 606_Budget.xlsx

CIE Forms

Don’t throw away your work. Utilizing your budget you can create a forecast by simply changing the budgeted amounts to actual as the months go by

Questions

CIE Forms

Attend the meeting (#1)

Be on point about projections and other budget assumptions – Be realistic

Be ready to discuss and defend your plan

Tie it all together

Ensure you have sufficient resources (cash) to substantiate your plan including your programs and any projected losses

(Questions)

How to Financially Survive a CIE Application

If required to provide or discuss a financial improvement plan be prepared to provide a detailed and thoughtful financial improvement plan that takes into consideration the causes and remedies of your financial situation

How to Financially Survive a CIE Application

A financial improvement plan sets out to tell your regulator how you plan to address a short fall in your financial performance

Shortfall could be a net loss from operations or less than 1 to 1 current ratio (clue to insolvency)

Preparing a Financial Improvement Plan

Defines the problem and address it with a robust plan to improve financial performance and ensure future profitability

There is currently no CIE template

Must be in your words, include a clear understanding of your financial status, improvements and elements of form 605 and 606

Financial Improvement Plan

A plan may include: Cost saving ideas

Admissions improvement (new relationships)

Better licensing passing scores

Keep in mind that the issue may not be getting students, but keeping students

Look at your largest expenses (Salaries, rent, advertising)

Financial Improvement Plan

Important Terms Defined

Accrual vs. Cash Basis

Accrual = Generally Accepted Accounting Principals (GAAP)

Record items when earned or when incurred.

This creates A/R and A/P

• Generally accepted auditing standards

• Generally accepted government auditing standards (GAGAS) – Yellow book audit

• Required for certain accrediting bodies

• Required for the U.S Department of Education

• Standards under which auditors must audit

Important Terms Defined

BASIC TRUTH IN ACCOUNTING

ASSETS = LIABILITIES + EQUITY

This means anything the school owns (assets) is either owed (liabilities) to someone else or provided for by the owner (equity) or operations (retained earnings).

Your financial position at a moment in time

Example December 31, 2015

(Handouts)

Balance Sheet

Presenting a classified balance sheet is crucial to CIE

Assets - Resources with future benefits

Cash, Accounts receivable, and Inventory

Short term – Anything you will use within a year.

Cash, A/R, and Inventory

Long Term – Anything you will use after a year

Equipment, Deposits on lease, Goodwill

Balance Sheet

Liabilities – Amounts owed

A/P, payroll accruals, deferred tuition, notes payable

Short term – Anything due within a year

A/P and Payroll Accruals

Long Term – Anything due after a year

Notes Payable

Balance Sheet

Equity - belongs to the owners

Investment you make into the company Distributions to you Retained earnings (Profit/loss)

Balance Sheet

Accounts receivable is simply the amount of money a student owes the school. Different industry accepted ways to present on financial statements (Gross versus net method)

Deferred tuition is the amount of money the school has received in excess of what has been earned by the school

Schools recognize revenue ratably over the length of the program or over a term (Not to be confused with refund policy)

Important Terms

Revenues are amounts earned by the institution for tuition, fees, books and supplies, etc.

Expenses are amounts due or expended for rent, salaries, etc.

Income Statement

Cash Flows – Summary cash flows in and out for the year. Three major sections. (Least attended to, but most important)

Operations – Is exactly what that means. It is money generated by the operations of the school.

Investing – Money you invest or equipment you buy.

Financing – Money you repay to a loan or a shareholder or money you borrow.

(Questions)

Statement of Cash Flows

Ratios are required by all of your regulatory bodies.

Ratio Analysis

Ratios

1. *Current ratio (current assets/current liabilities)

2. *Acid Ratio (Cash + A/R)/(current liabilities)

3. Profitability (Net income/gross tuition sales) 4. *Composite score ratio 5. Assets to Unearned Tuition (cash + accounts

receivable/unearned tuition) 6. Burn rate (Cash/Cash operating expenses per

month)

You can avoid pitfalls by knowing these ratios

Current Ratio (current assets/current liabilities)

Current Assets $76,230

Current Liabilities $31,762

Current Ratio: 2.4 to 1

Agencies require greater than 1 to 1

To increase this pay bills – Example $20,000

New ratio: 4.71 to 1

Ratio Analysis - Example

A quick and dirty way to know if you are profitable via a rule of thumb.

For example in the many financial statements I have looked at personnel costs typically approximate 40% of tuition revenue

Example: Assume you pay teacher 20/hr. To keep personnel costs at 40% you would have to make $50/hr during that class. If your tuition charge is $10/hr you would need 5 students in that class

Ratio Analysis – Profitable?

RATIO EXERCISE

Responses

2015 2014

Profit Margin on Total Revenue (net income/total revenue)

21% 21%

Current Ratio (current assets/current liabilities)

2.4 1.7

Acid Ratio (Current assets - inventory)/(current liabilities)

2.2 1.5

Assets to Unearned Tuition (cash + accounts receivable/unearned tuition)

5.5 7.1

Liquidity (working capital/total assets)

45% 25%

Responses

With a burn rate of just .69 is this company financially stable?

2015 2014

Burn rate (Cash/Cash operating expenses per month)

.69 .80

Establish trends

Ask your in-house accountant to calculate over several periods and explain differences from period to period

Questions

Ratio Analysis

1. Audit under GAAP performed under GAGAS. Not all accrediting bodies require GAGAS, but the DOE does!

2. Current ratio greater than 1 to 1

3. Total assets to total liabilities greater than 1 to 1

4. Net income

5. No contingencies that will materially affect operations (i.e. lawsuits)

6. Positive cash flows from operations

7. Agencies are all a little different. You have to make sure you are aware of the requirements for your agency.

8. Run your school as if you were already accredited

Accreditation Ratio Requirements

Composite Score

U.S. Department of Education

1. Must be prepared under GAAP and audited under GAGAS

2. Does not care about current ratio, etc.

3. Must meet a financial composite score of 1.5 or could require a letter of credit which is a large burden on school

U.S. Department of Education

Applies to both for profit and not for profit. Calculations are different for each.

34 CFR 668.171-175 and Appendix A to Subpart L.

Score combines 3 different measurements

Primary reserve ratio – measures viability and liquidity

Equity ratio – measures capital resources and ability to borrow

Net income ratio – measures profitability

Composite Score

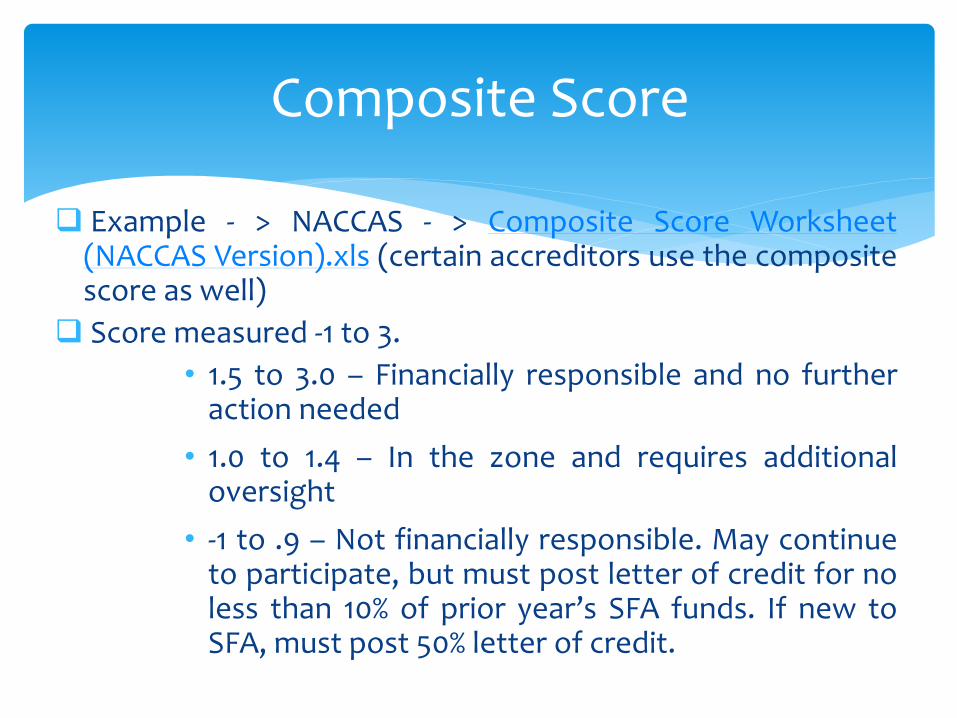

Example - > NACCAS - > Composite Score Worksheet (NACCAS Version).xls (certain accreditors use the composite score as well)

Score measured -1 to 3.

• 1.5 to 3.0 – Financially responsible and no further action needed

• 1.0 to 1.4 – In the zone and requires additional oversight

• -1 to .9 – Not financially responsible. May continue to participate, but must post letter of credit for no less than 10% of prior year’s SFA funds. If new to SFA, must post 50% letter of credit.

Composite Score

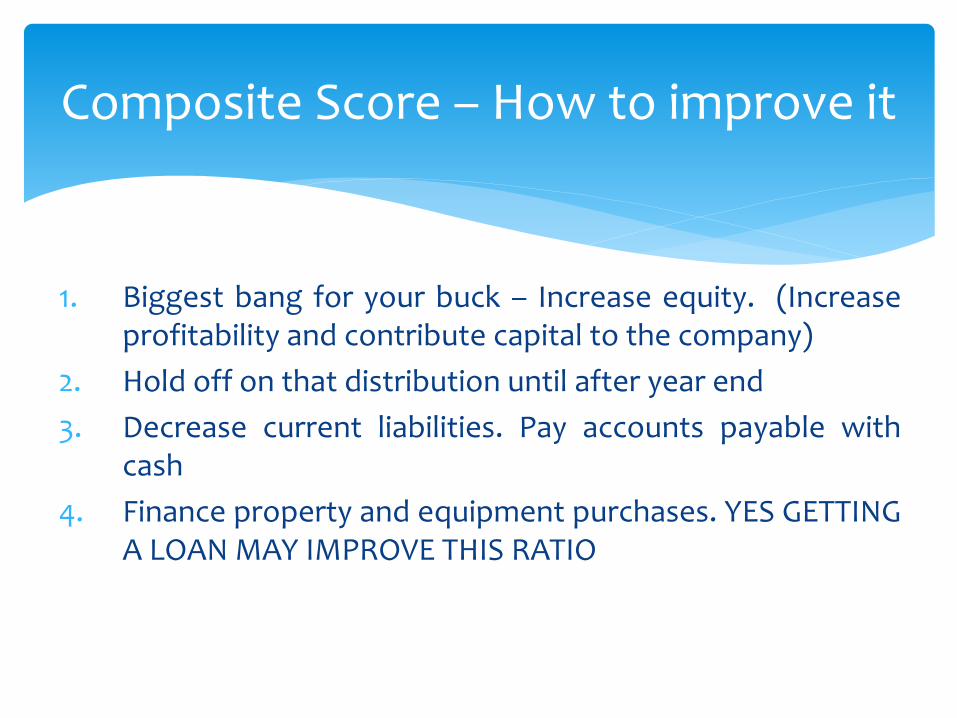

1. Biggest bang for your buck – Increase equity. (Increase profitability and contribute capital to the company)

2. Hold off on that distribution until after year end

3. Decrease current liabilities. Pay accounts payable with cash

4. Finance property and equipment purchases. YES GETTING A LOAN MAY IMPROVE THIS RATIO

Composite Score – How to improve it

You should perform a soft closing as of Nov 30.

Review ratios quarterly and once as of Nov 30.

Communicate with your CPA and perhaps:

Postpone orders of major items to the following year

Review A/R for bad debt or collection of bad debt

Review depreciation calculations

Review intangibles (goodwill) for impairment, if any.

Cash capital contributions

Monitor/Improve Ratios

Don’t let these surprise you:

Accounts Receivable

Deferred Student Deposits

Payroll Accrual/Vacation

Accounts Payable

Capital Leases

Personal Credit Cards with Business Exp

Prepaid Assets (Rent and Insurance)

Most Common Audit Adjustments

1. Hidden inside your financial statements is a wealth of information

2. Knowing how the regulatory bodies will look at your financial statements is extremely important

3. Establishing trends is important 4. Think ahead… Using your financial statements as a tool

for growth and management 5. By managing your financials you can avoid costly surprises

(i.e. letter of credit) 6. Work closely and throughout the year with your CPA

Recap

Questions

State web site: www.fldoe.org/cie

FAPSC: www.fapsc.org

Your accreditation’s web site:

www.acics.org, www.accsc.org, www.council.org, www.naccas.org, www.abhes.org

DOE: http://ifap.ed.gov/

Where to Get More Information

Thank you for your

Time