Embed Size (px)

Citation preview

1/17/2018

1

1

Finance 101

2

Learning Outcomes• Define funds and review the fund structure of a government

• Identify the components of fund financial statements

• Know how fund balance is generated and what it should be used for

• Identify the laws affecting budget preparation and adoption

• Recognize the process of preparing, adopting and administering a budget

• Recall methods of budget communication

• Recite annual audit and financial reporting requirements

1/17/2018

2

33

Accounting

4

GASB AND GAAP• The Governmental Accounting Standards Board

(GASB) is the standard-setting body for state and local governments

• Generally Accepted Accounting Principles are conventions, rules, and procedures that serve as the norm for the fair presentation of financial statements

1/17/2018

3

5

What is a Fund?• Separate accounting entity• Separate set of self-balancing accounts• Separate set of financial statements• Three categories of funds

6

Minimum Number of FundsEstablish the minimum number of funds in order to

• Comply with laws• Exercise sound financial administration

1/17/2018

4

7

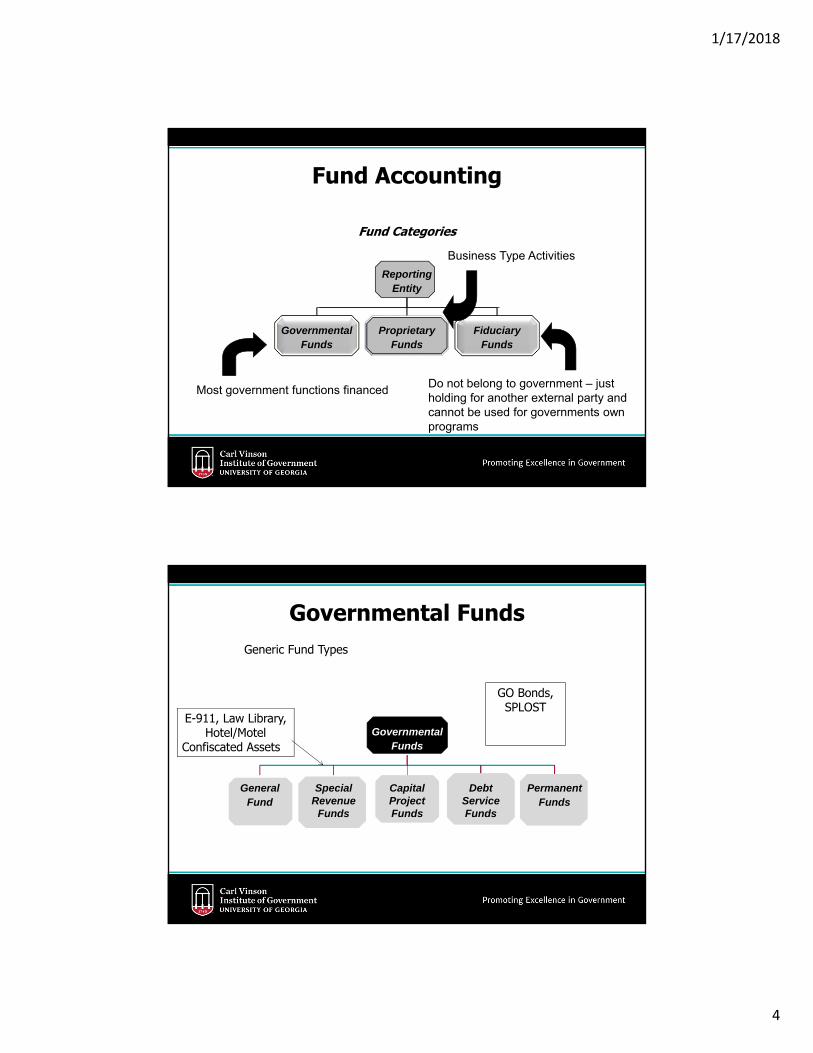

Fund Categories

FundsFiduciary

FundsProprietary

FundsGovernmental

EntityReporting

Most government functions financed

Business Type Activities

Do not belong to government – just holding for another external party and cannot be used for governments own programs

Fund Accounting

8

Governmental FundsGeneric Fund Types

FundsPermanent

Funds

DebtService

Funds

CapitalProject

Funds

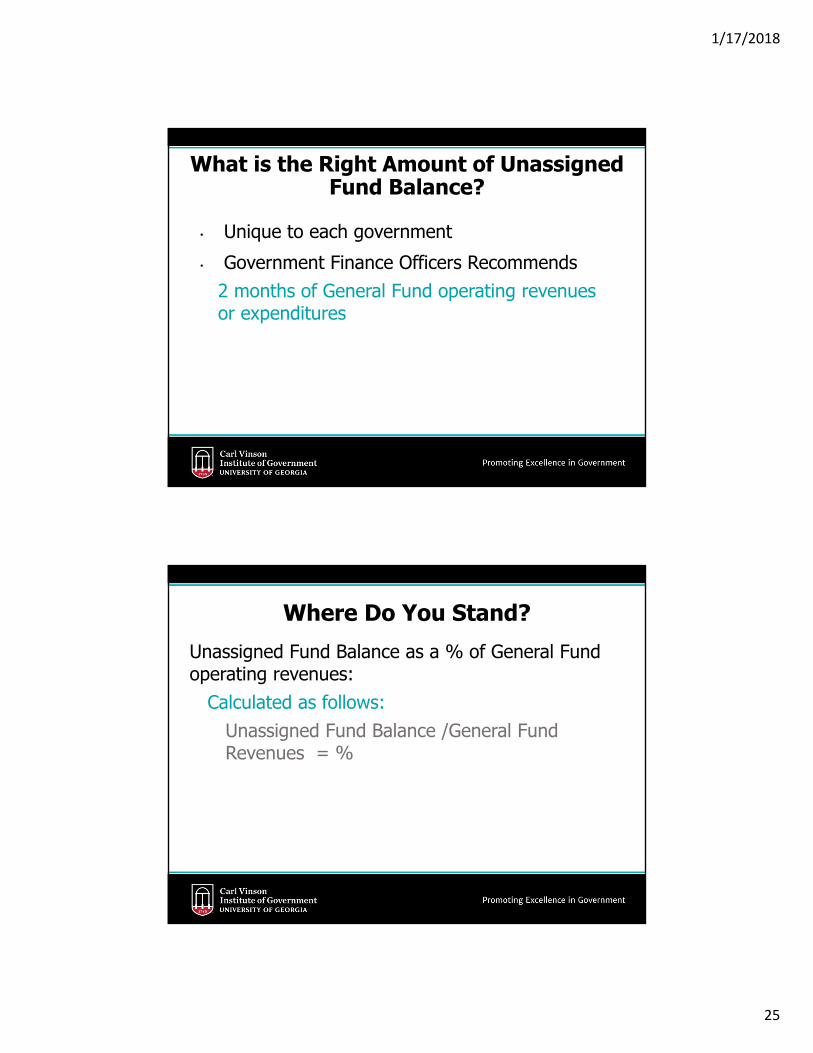

SpecialRevenueFund

General

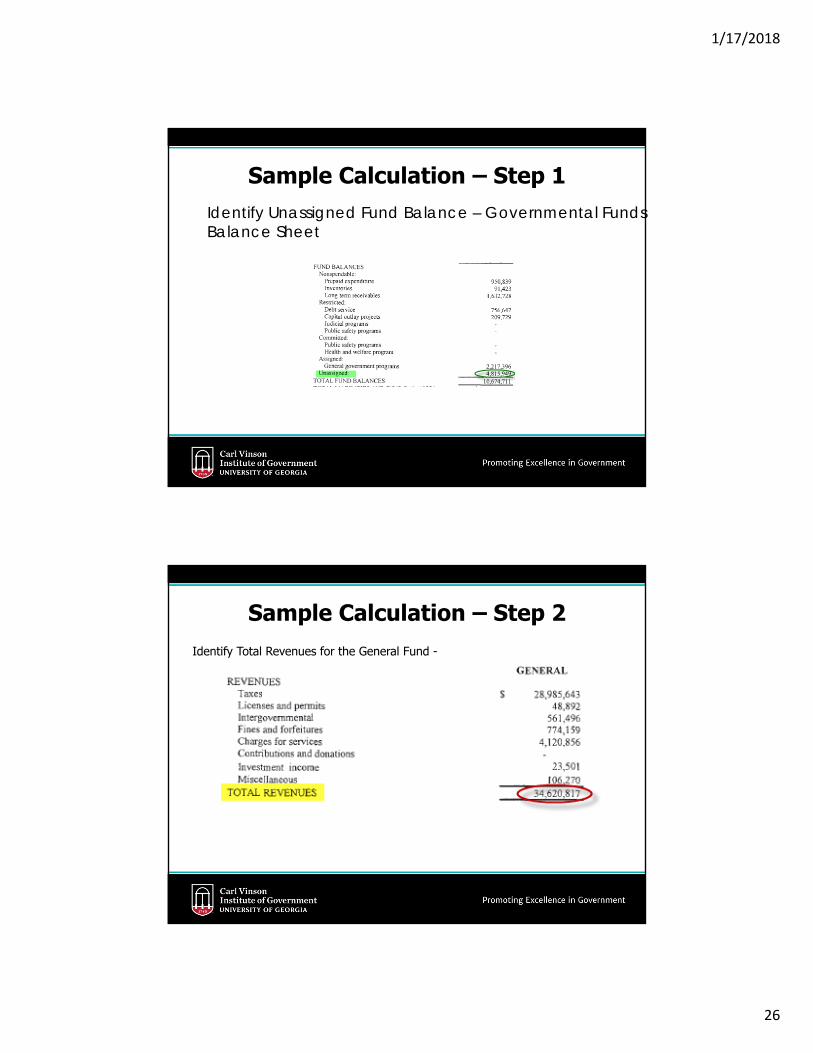

FundsGovernmental

E-911, Law Library, Hotel/Motel

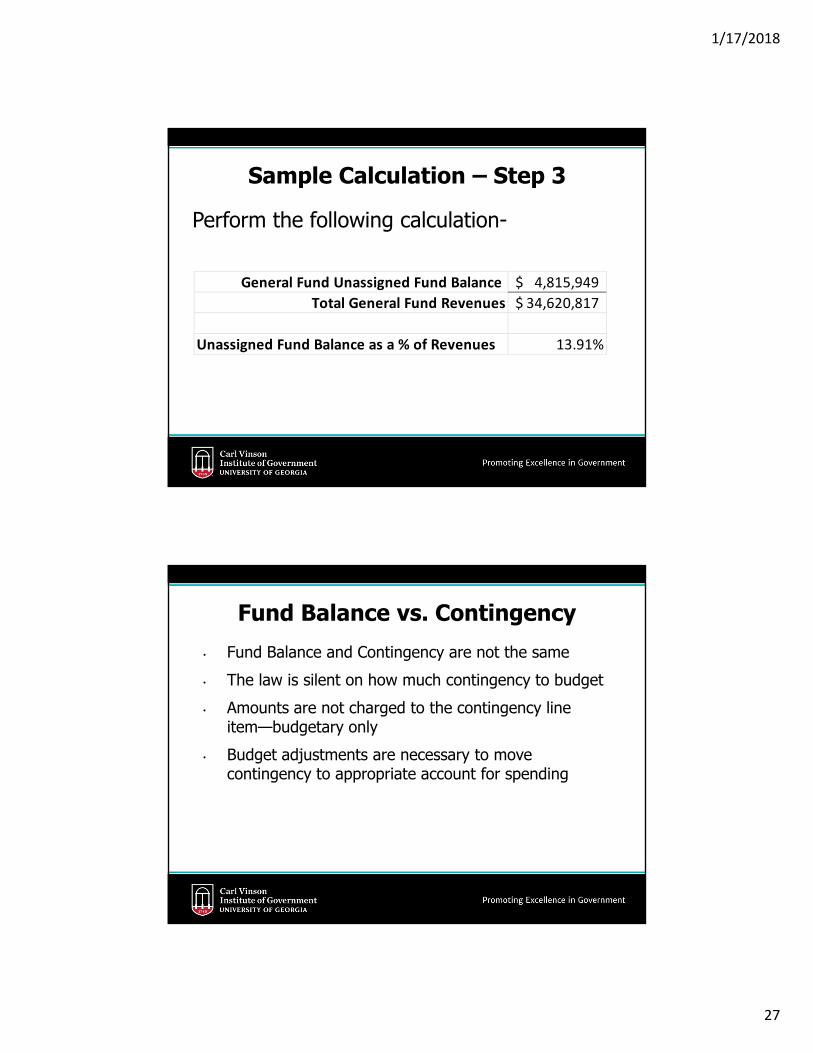

Confiscated Assets

GO Bonds, SPLOST

1/17/2018

5

9

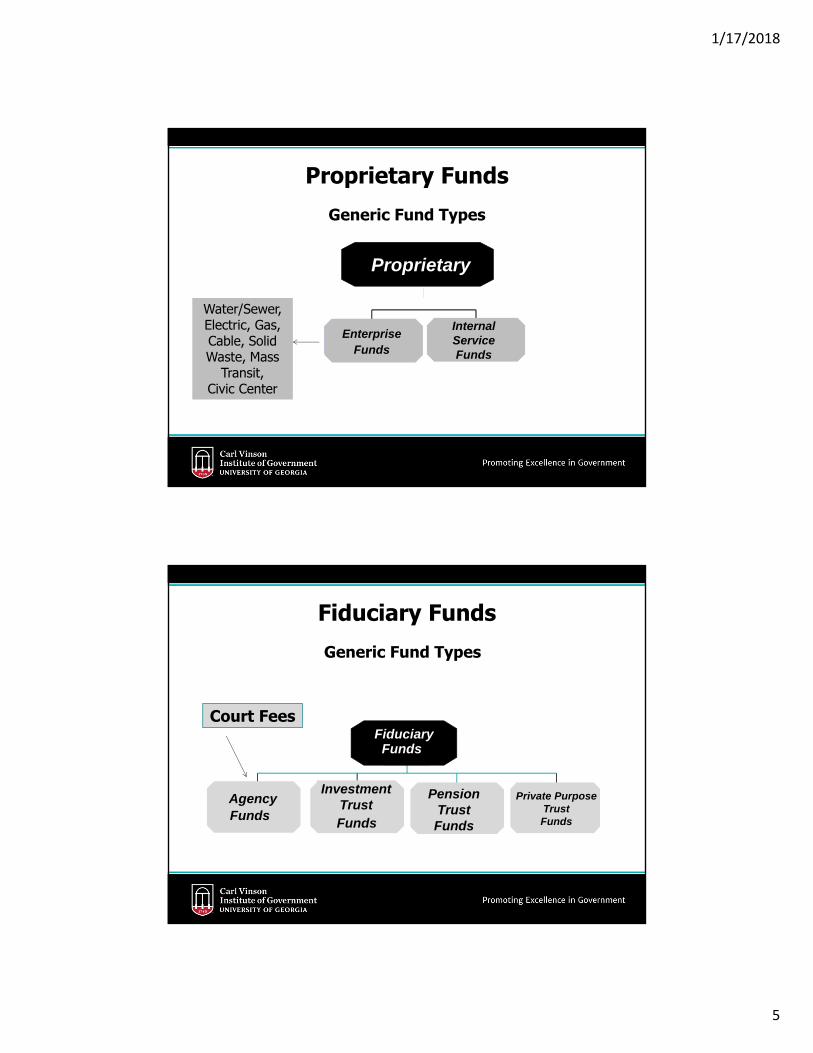

Proprietary FundsGeneric Fund Types

Internal ServiceFundsFunds

Enterprise

Proprietary

Water/Sewer, Electric, Gas, Cable, Solid Waste, Mass

Transit, Civic Center

10

Fiduciary FundsGeneric Fund Types

Funds

Private PurposeTrust

PensionTrustFundsFunds

InvestmentTrust

FundsAgency

FundsFiduciary

Court Fees

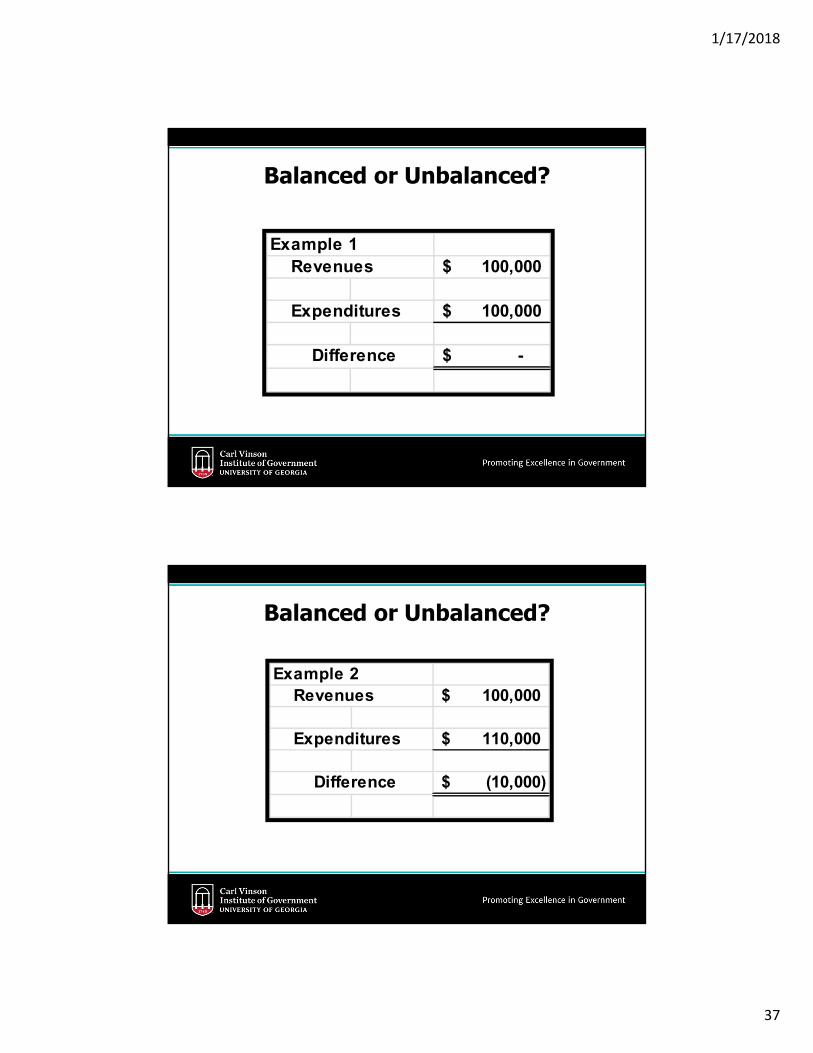

1/17/2018

6

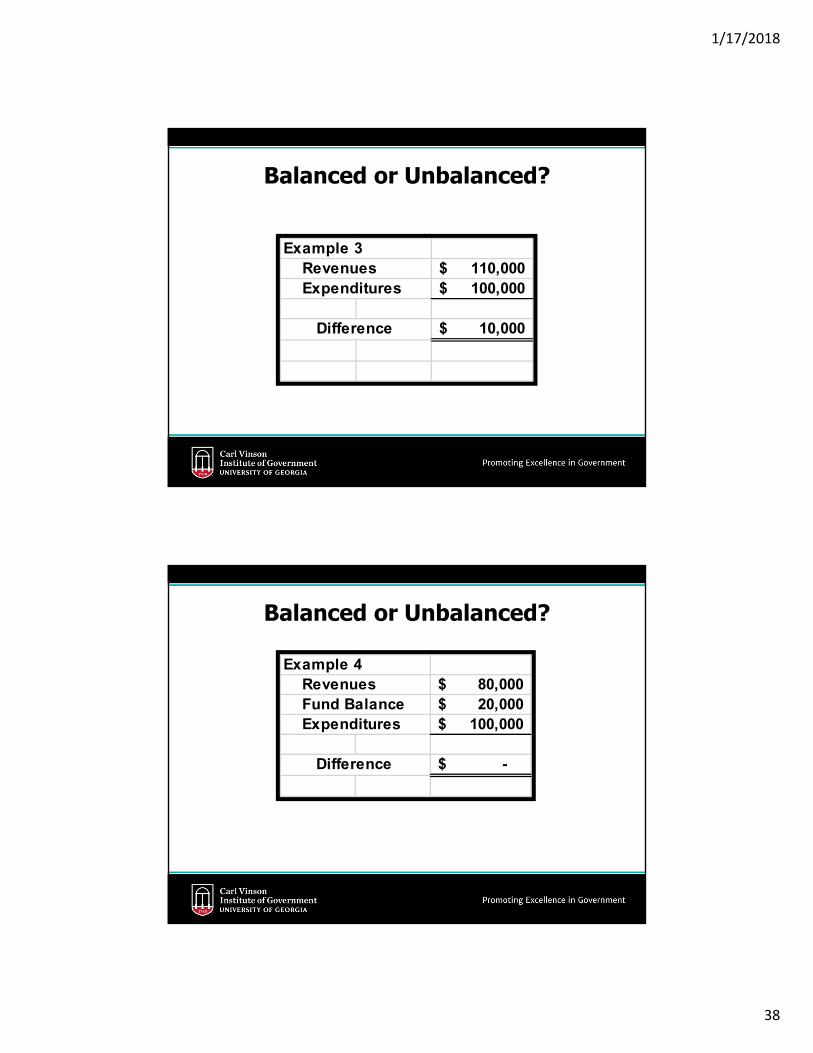

11

Uniform Chart of Accountshttp://www.dca.ga.gov/development/Research/programs/documents/UCOA_3rdEdition_DCA_Approved_12-4-13.pdf

12

TYPES of financial statements• Statements of Position• Operating Statements

1/17/2018

7

13

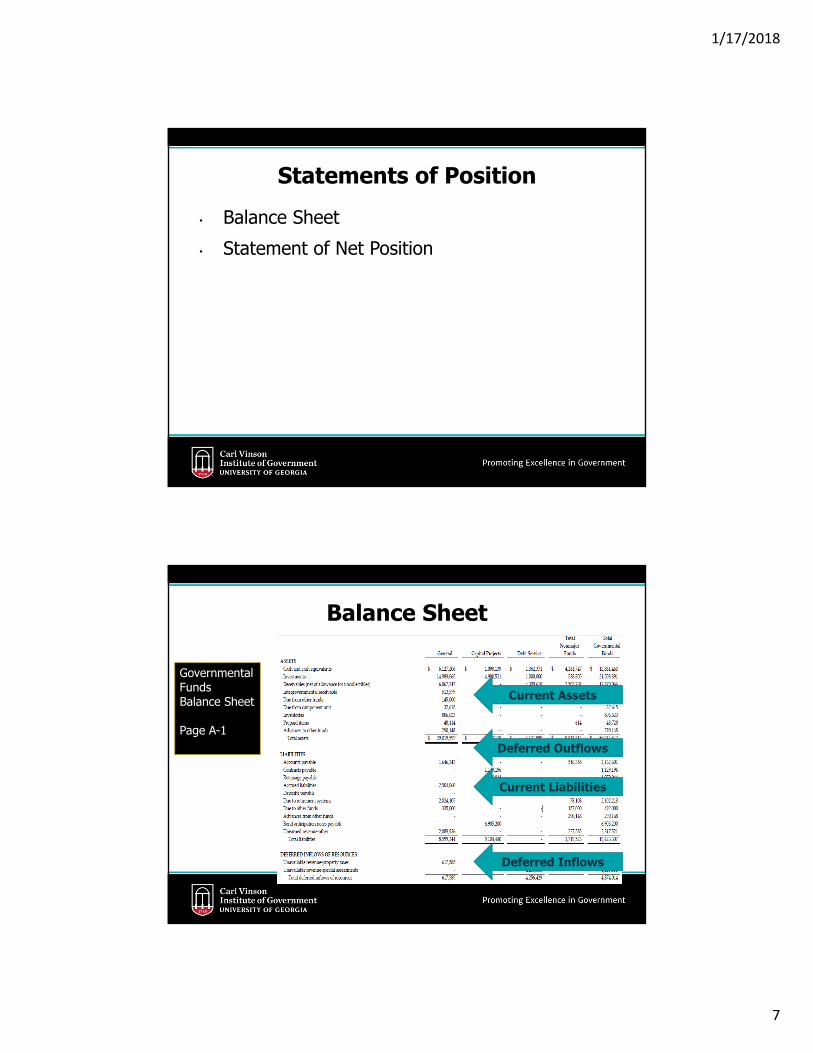

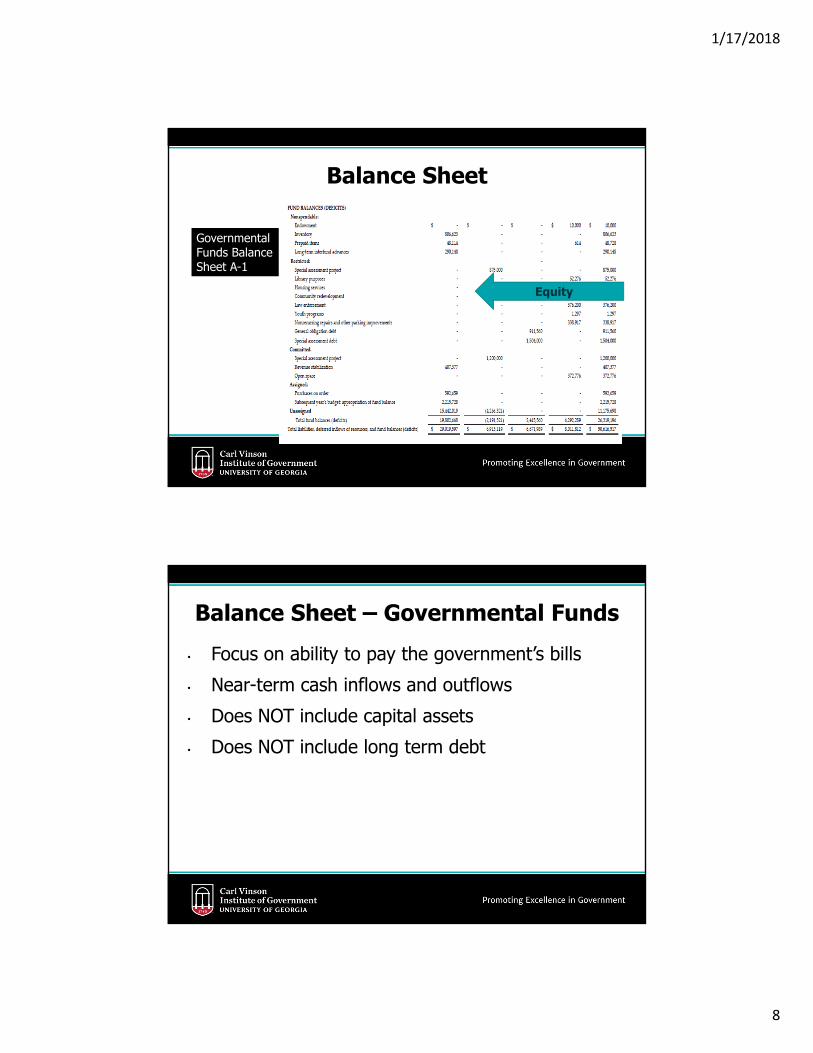

Statements of Position• Balance Sheet• Statement of Net Position

14

Current Assets

Deferred Outflows

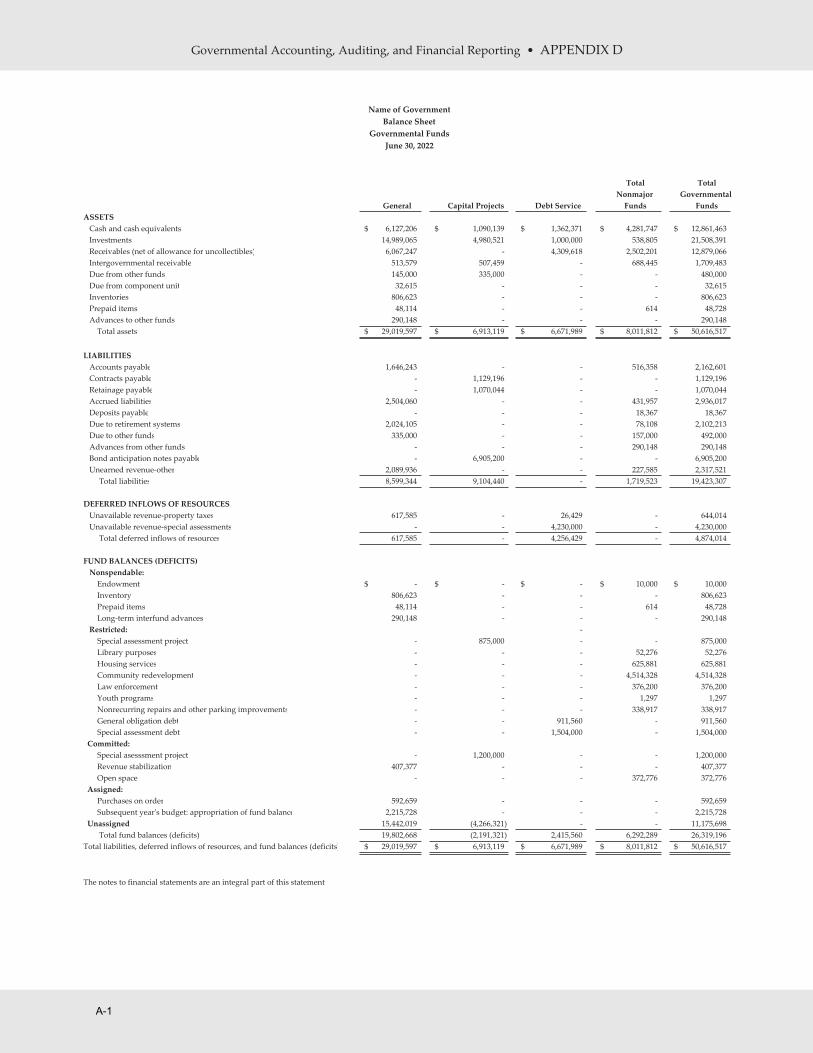

Governmental Funds Balance Sheet

Page A-1

Current Liabilities

Deferred Inflows

Balance Sheet

1/17/2018

8

15

Equity

Governmental Funds Balance Sheet A-1

Balance Sheet

16

Balance Sheet – Governmental Funds• Focus on ability to pay the government’s bills• Near-term cash inflows and outflows• Does NOT include capital assets• Does NOT include long term debt

1/17/2018

9

17

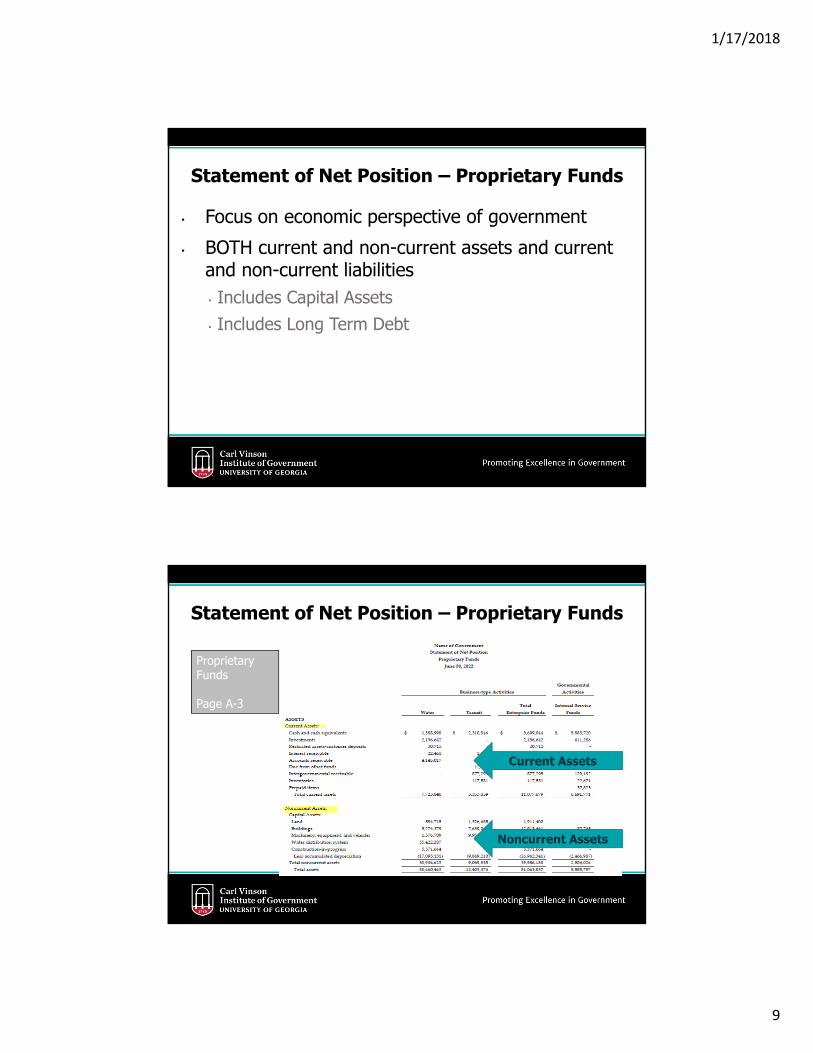

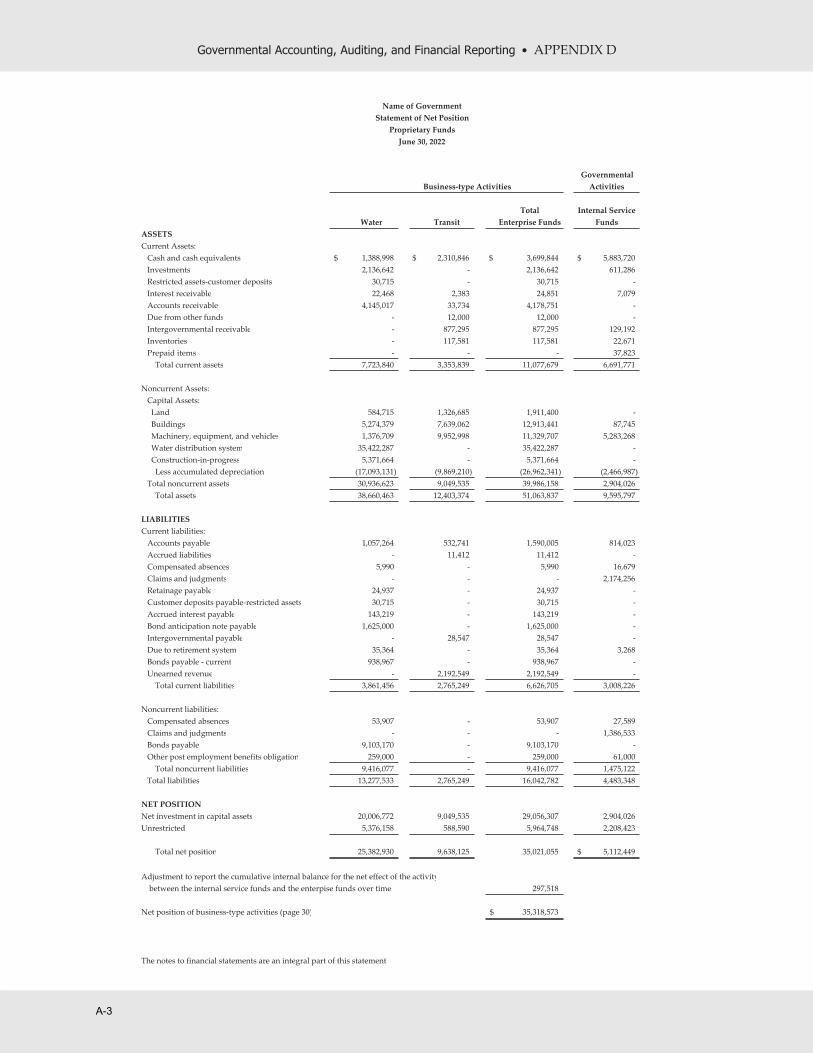

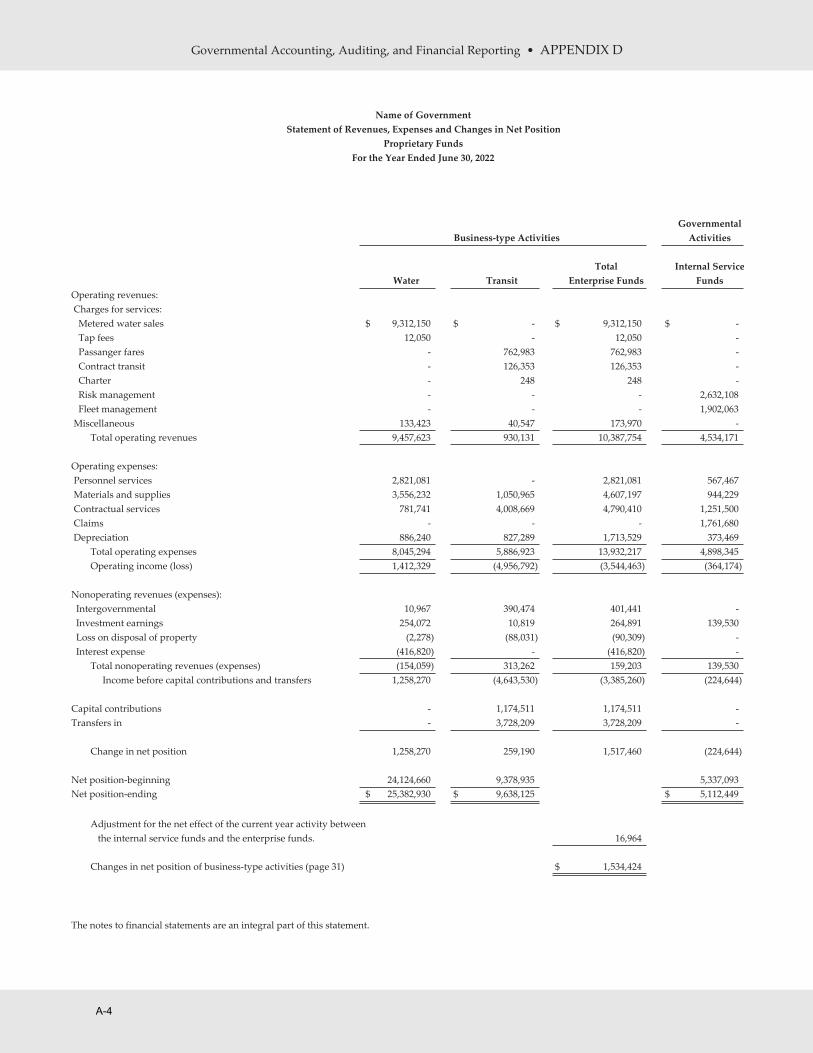

Statement of Net Position – Proprietary Funds

• Focus on economic perspective of government• BOTH current and non-current assets and current

and non-current liabilities • Includes Capital Assets• Includes Long Term Debt

18

Proprietary Funds

Page A-3

Current Assets

Noncurrent Assets

Statement of Net Position – Proprietary Funds

1/17/2018

10

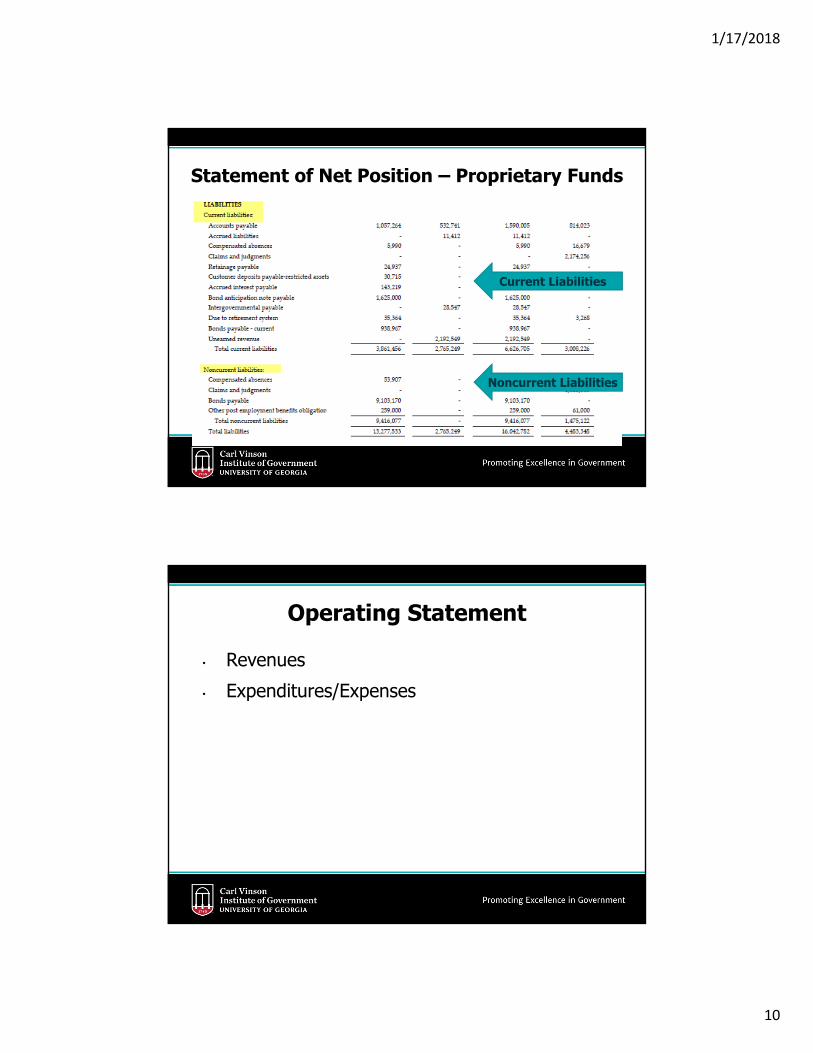

19

Current Liabilities

Noncurrent Liabilities

Statement of Net Position – Proprietary Funds

20

Operating Statement

• Revenues• Expenditures/Expenses

1/17/2018

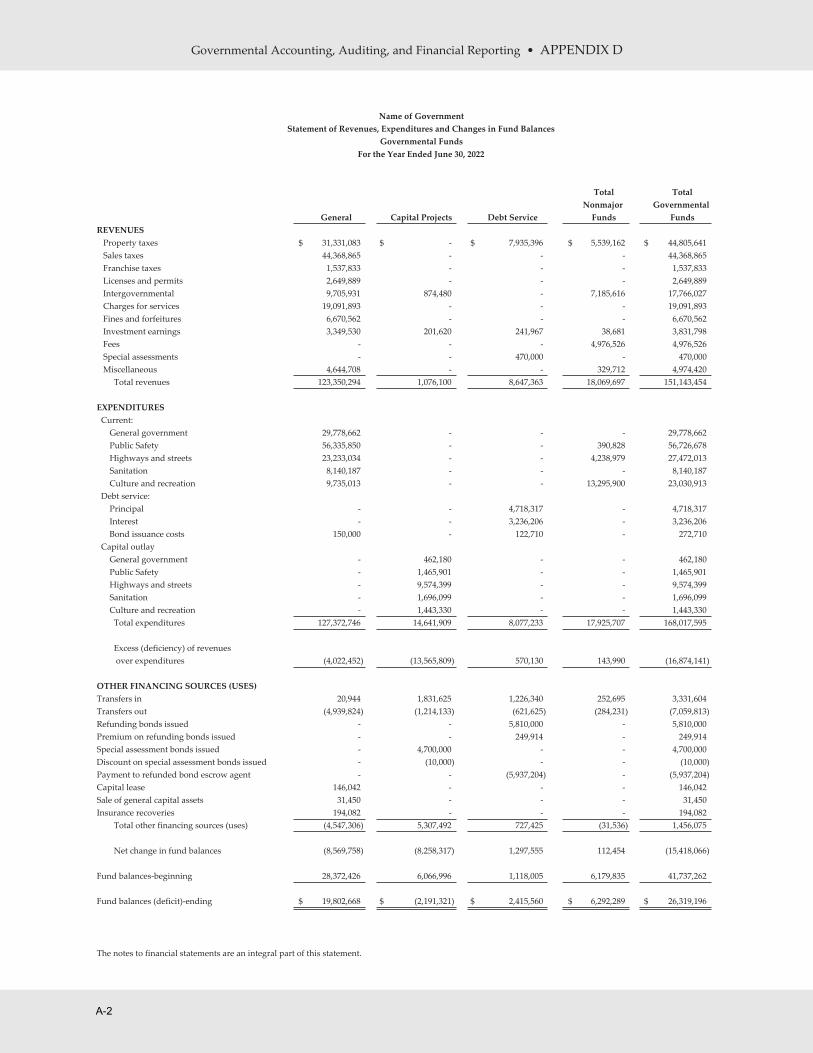

11

21

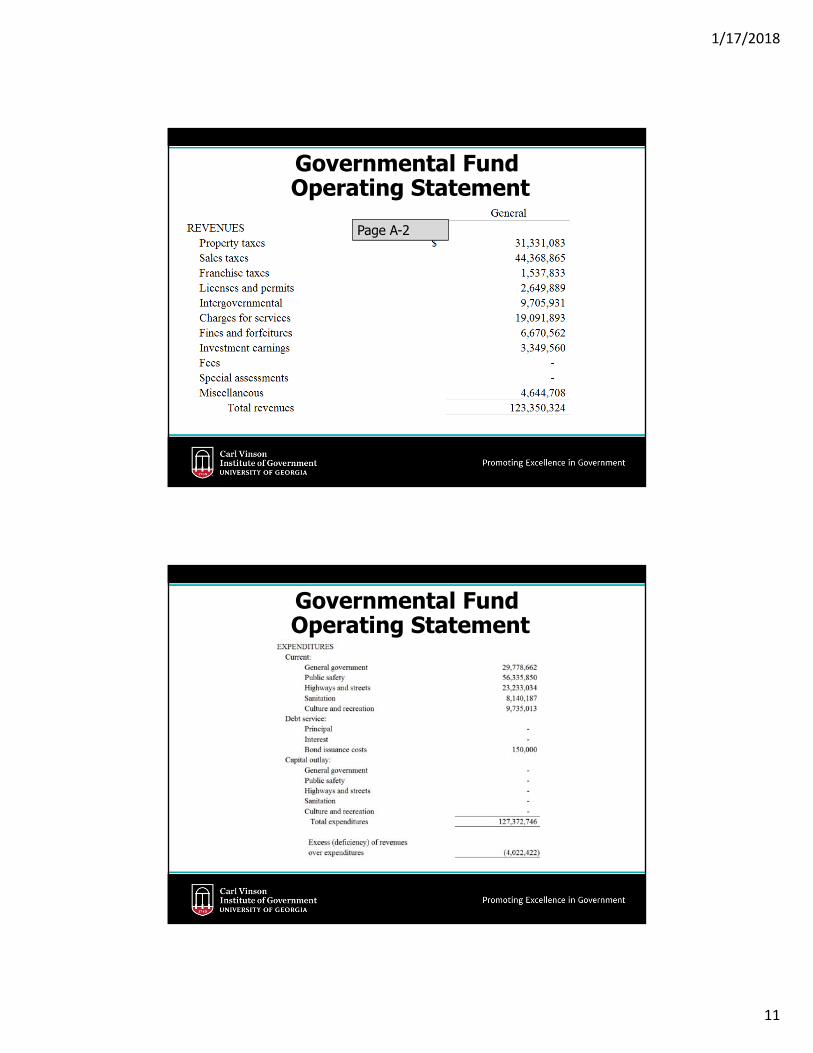

Governmental Fund Operating Statement

Page A-2

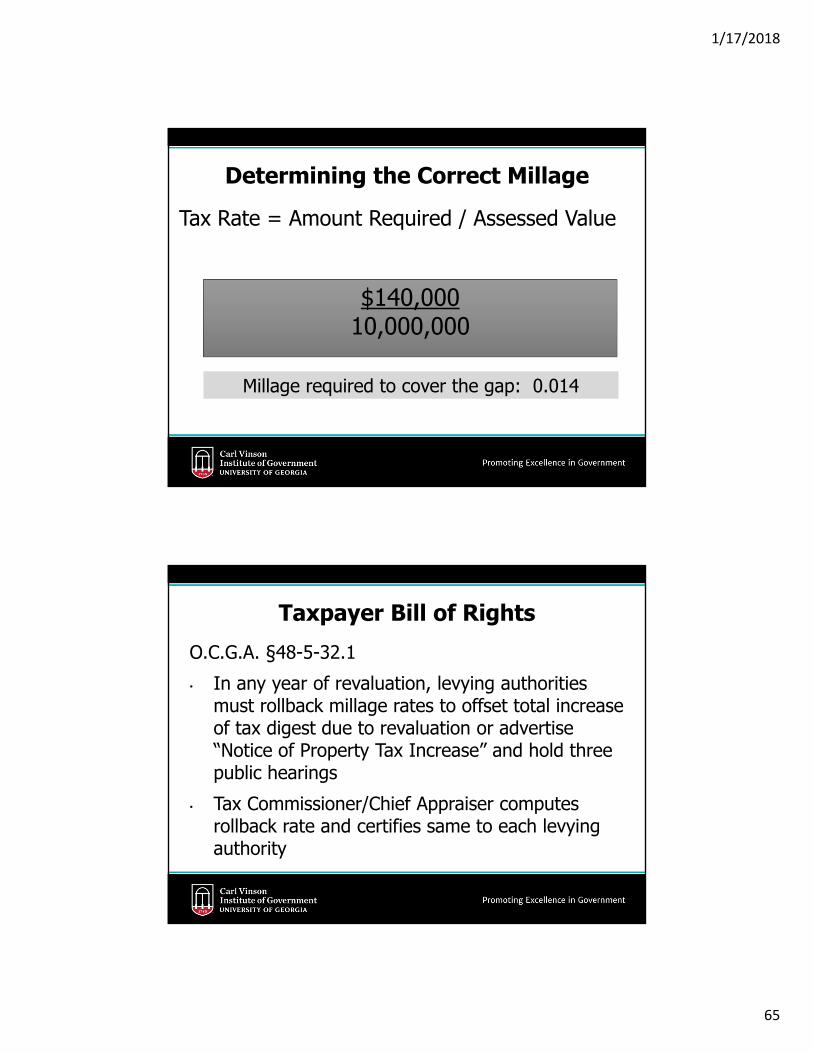

22

Governmental Fund Operating Statement

1/17/2018

12

23

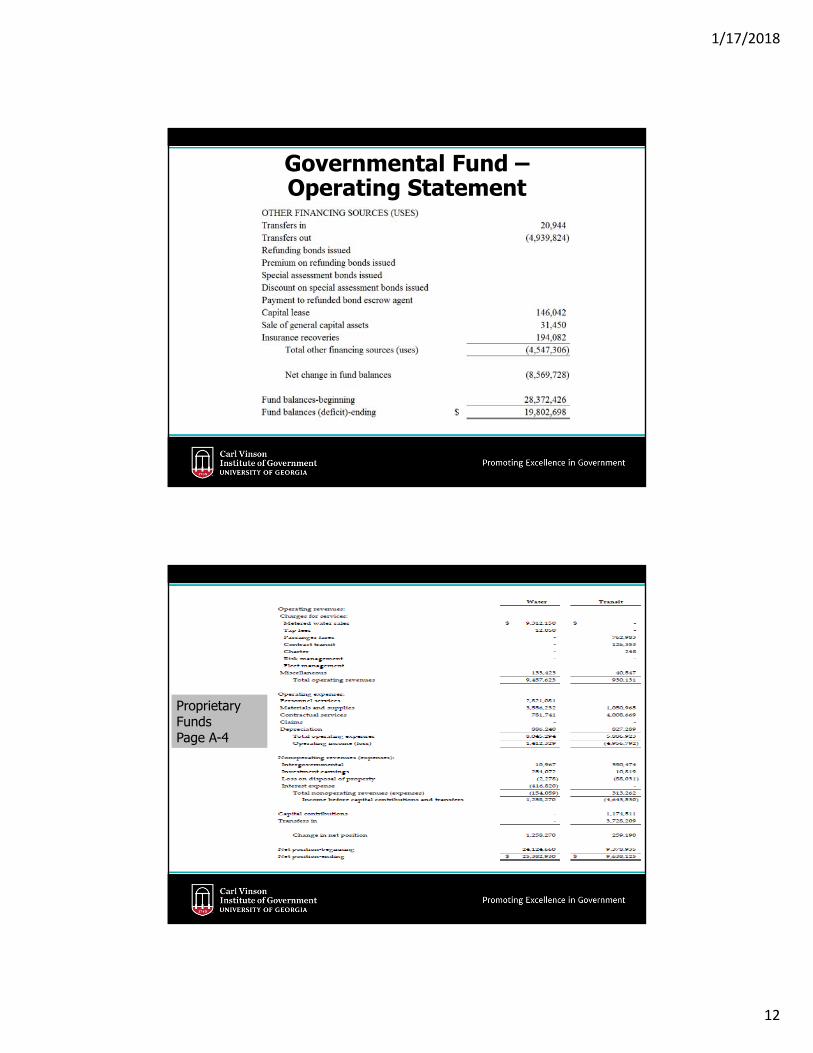

Governmental Fund –Operating Statement

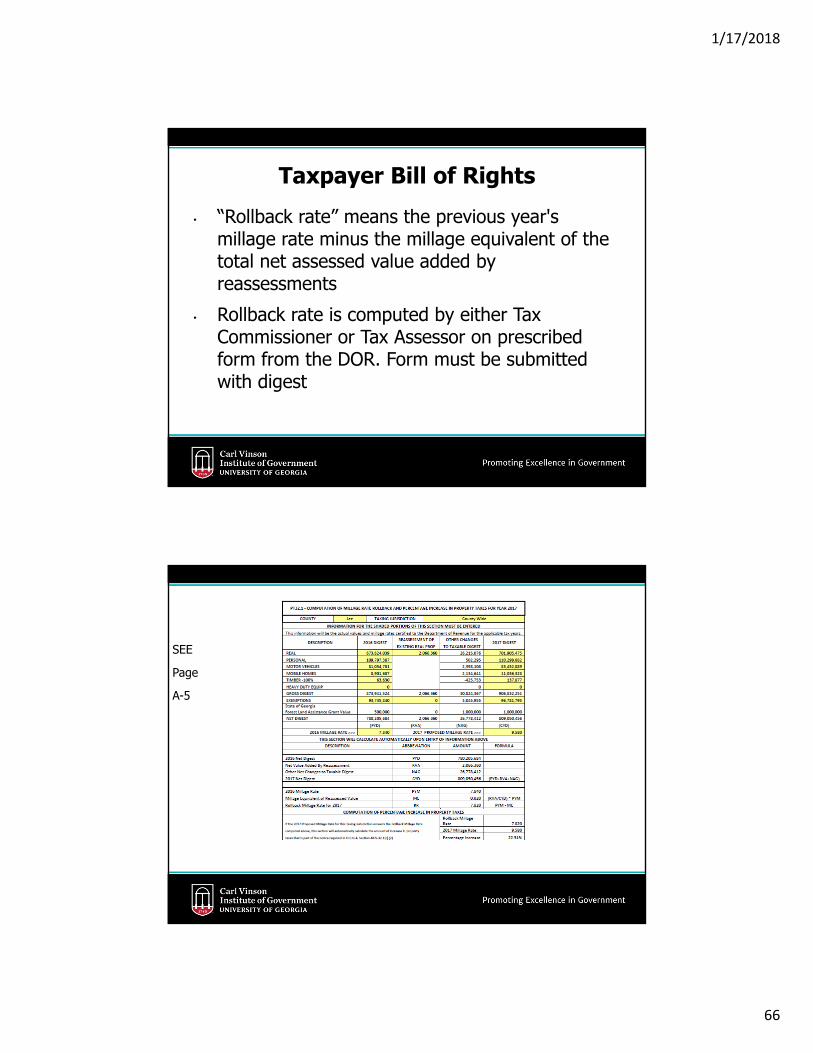

24

Proprietary FundsPage A-4

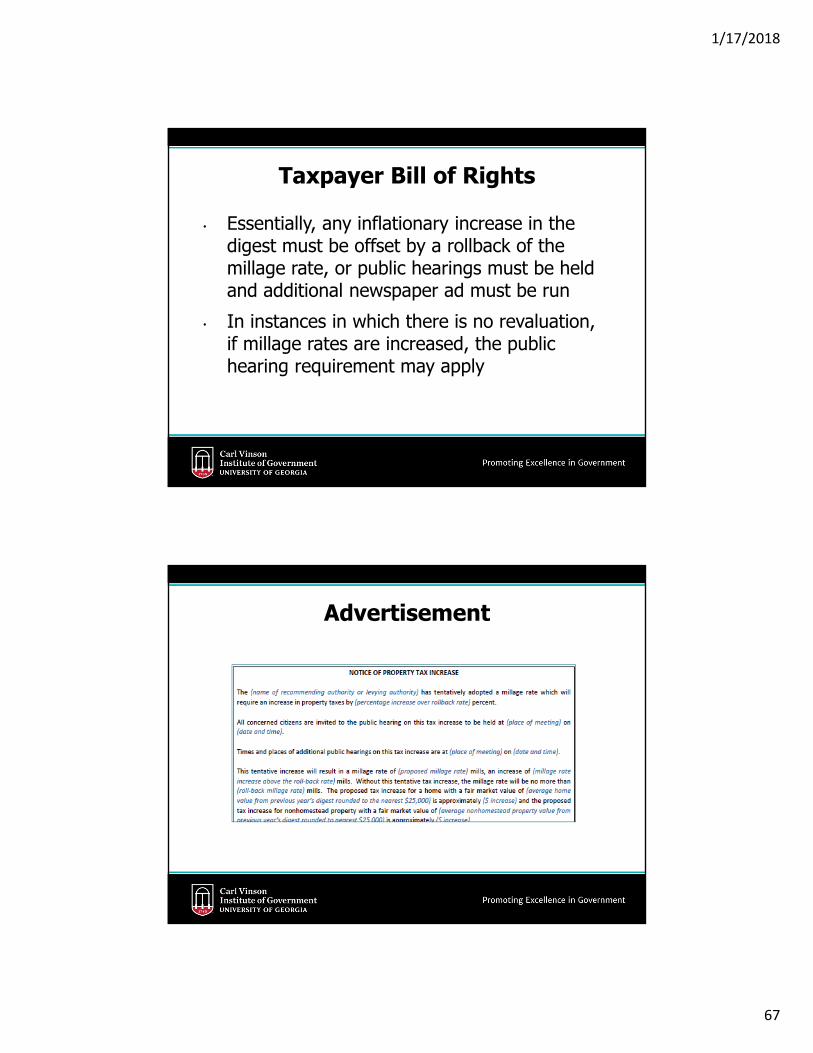

1/17/2018

13

25

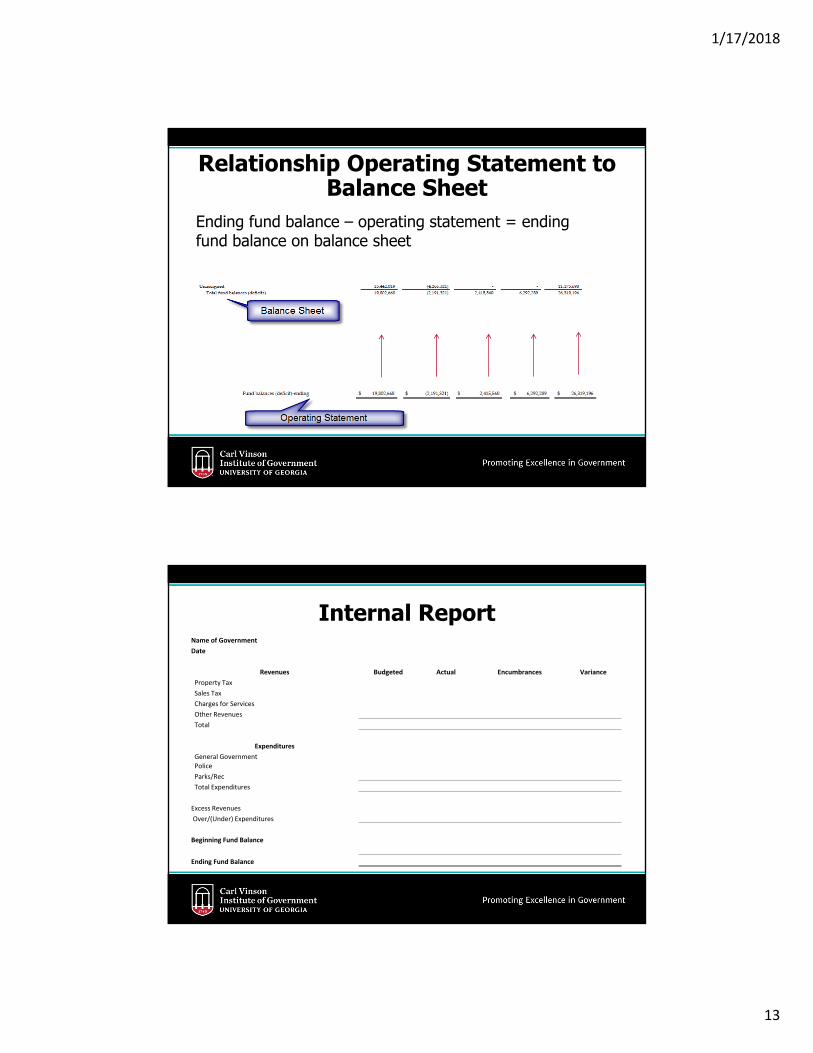

Relationship Operating Statement to Balance Sheet

Ending fund balance – operating statement = ending fund balance on balance sheet

26

Name of Government

Date

Revenues Budgeted Actual Encumbrances Variance

Property Tax

Sales Tax

Charges for Services

Other Revenues

Total

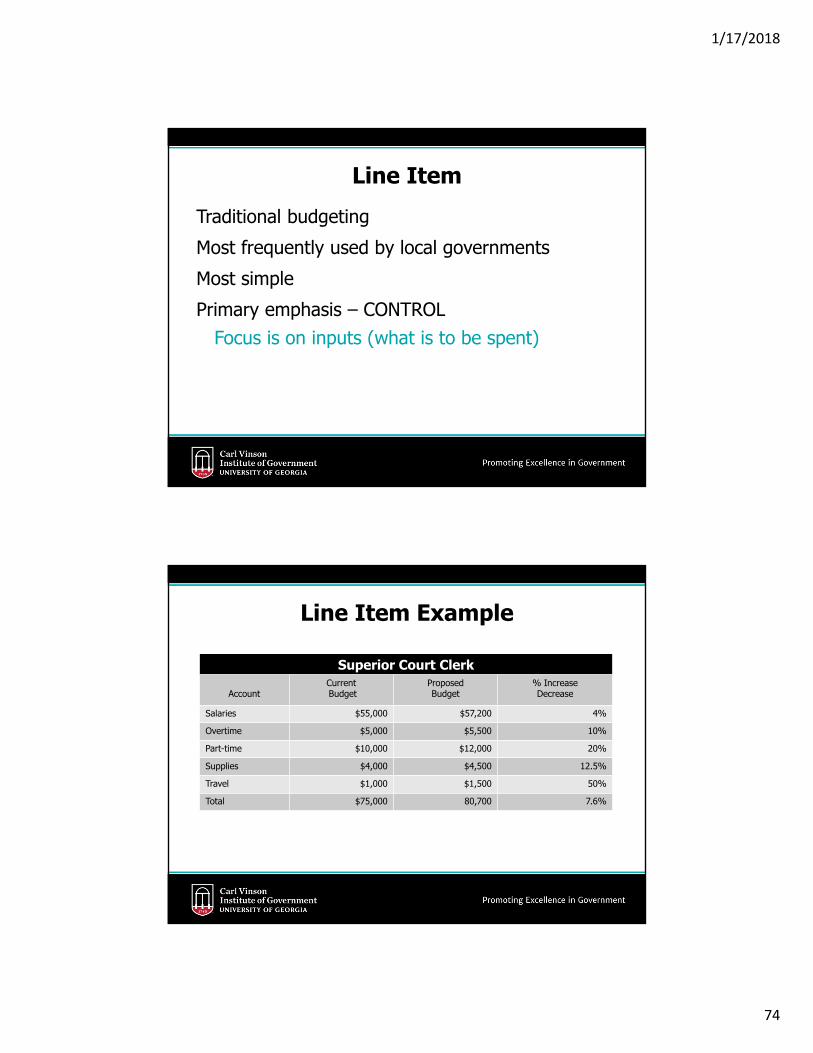

Expenditures

General Government

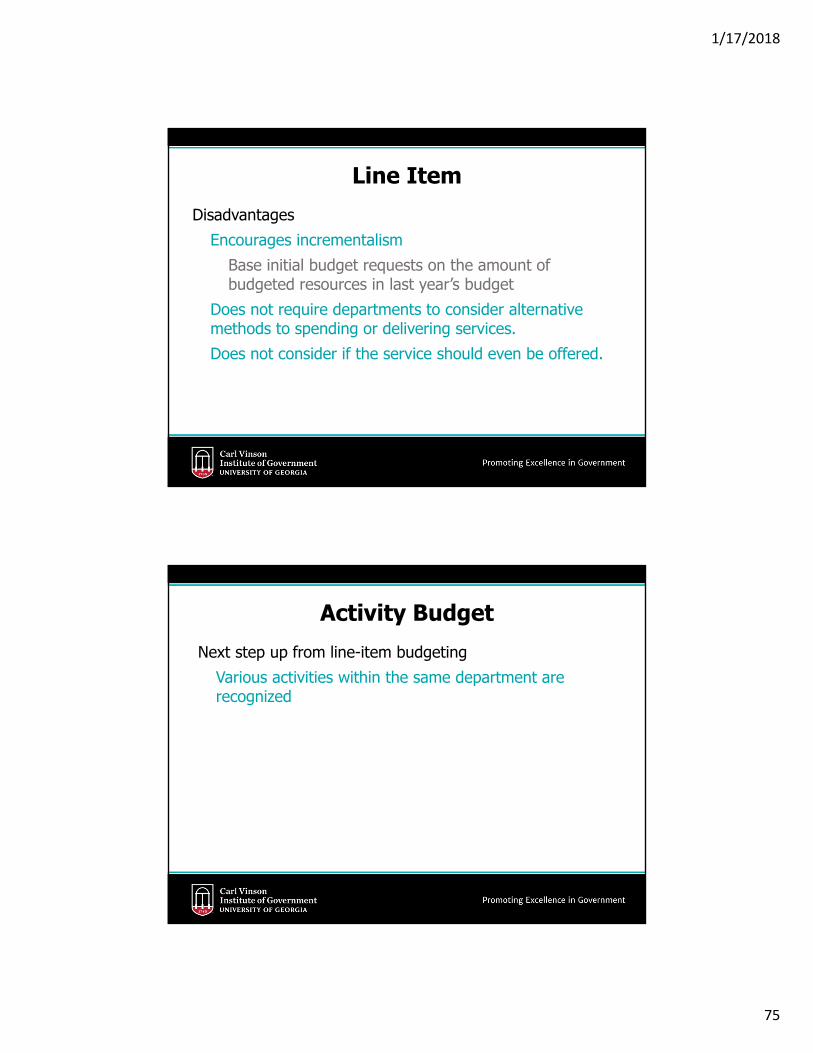

Police

Parks/Rec

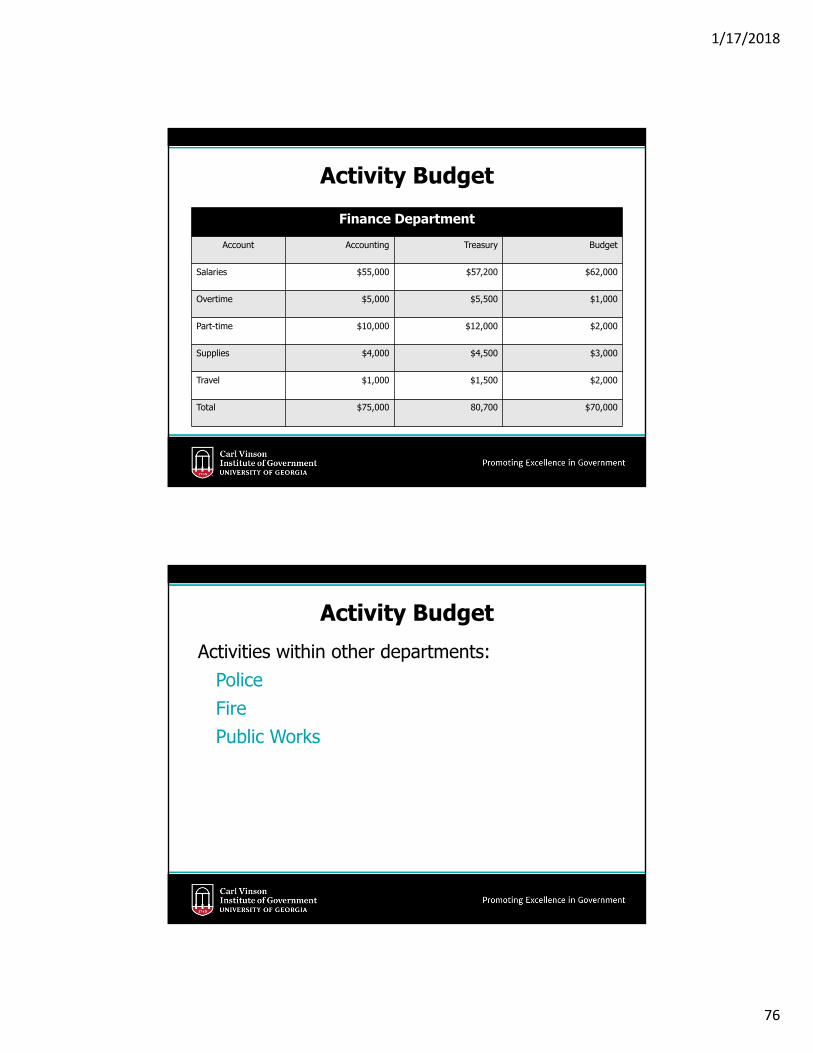

Total Expenditures

Excess Revenues

Over/(Under) Expenditures

Beginning Fund Balance

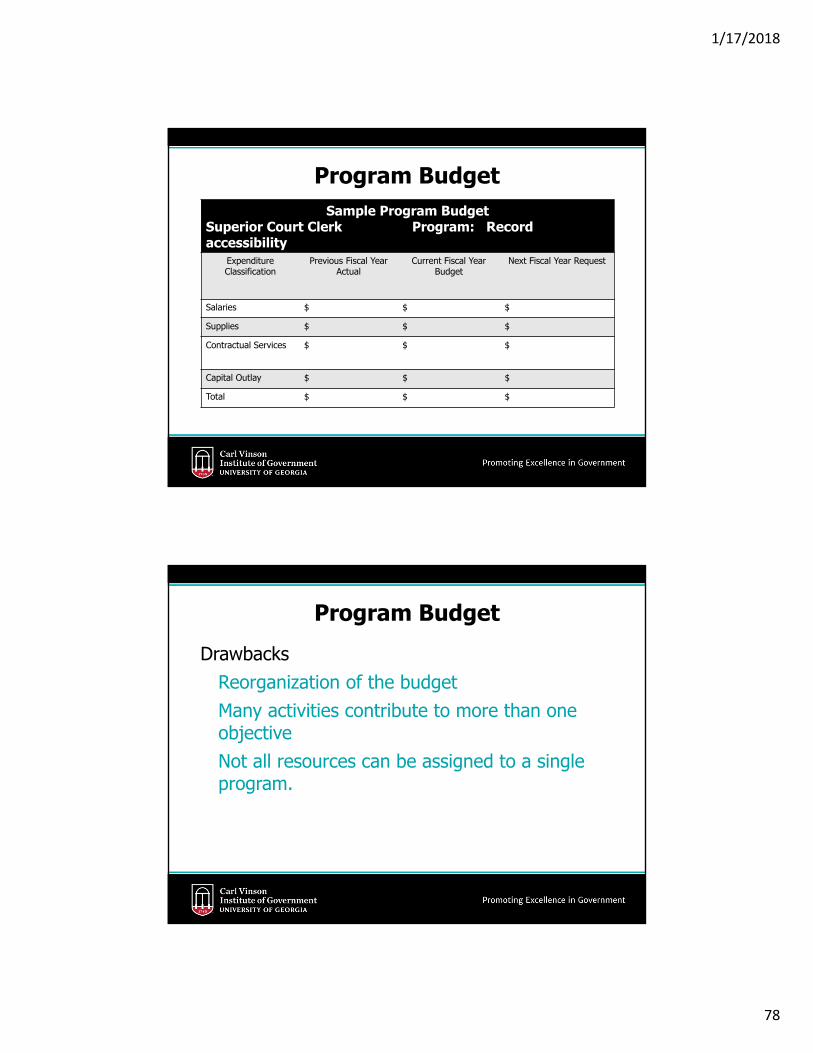

Ending Fund Balance

Internal Report

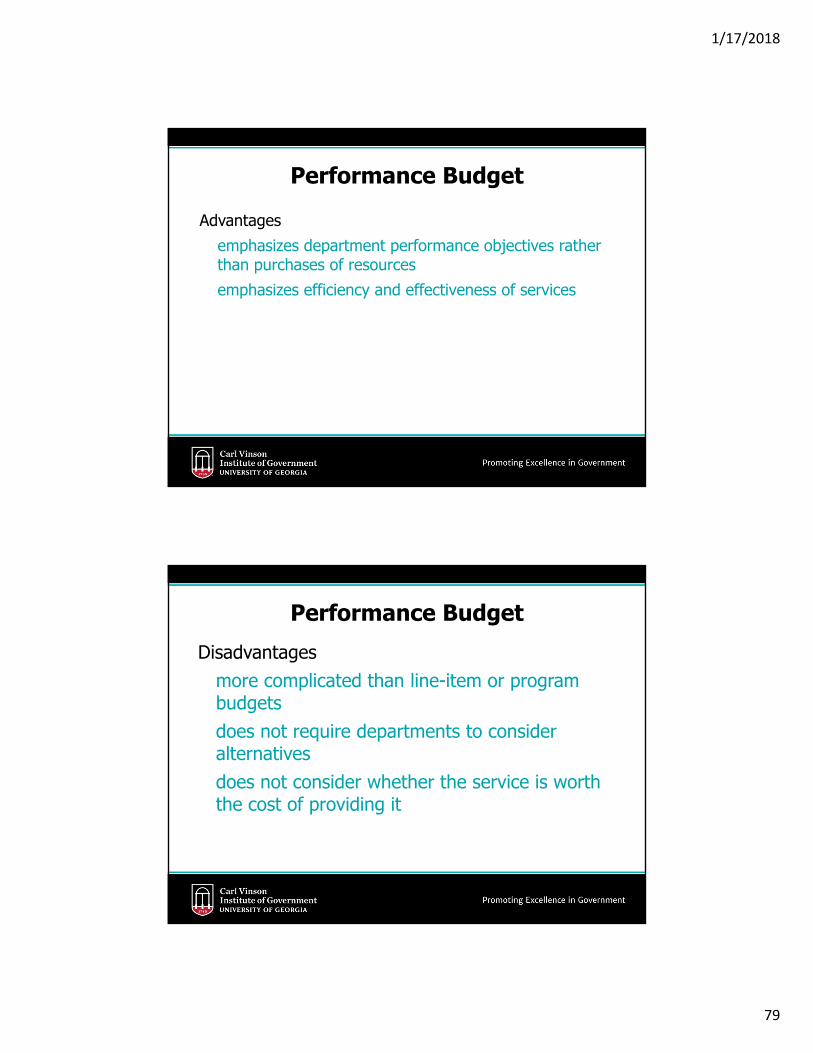

1/17/2018

14

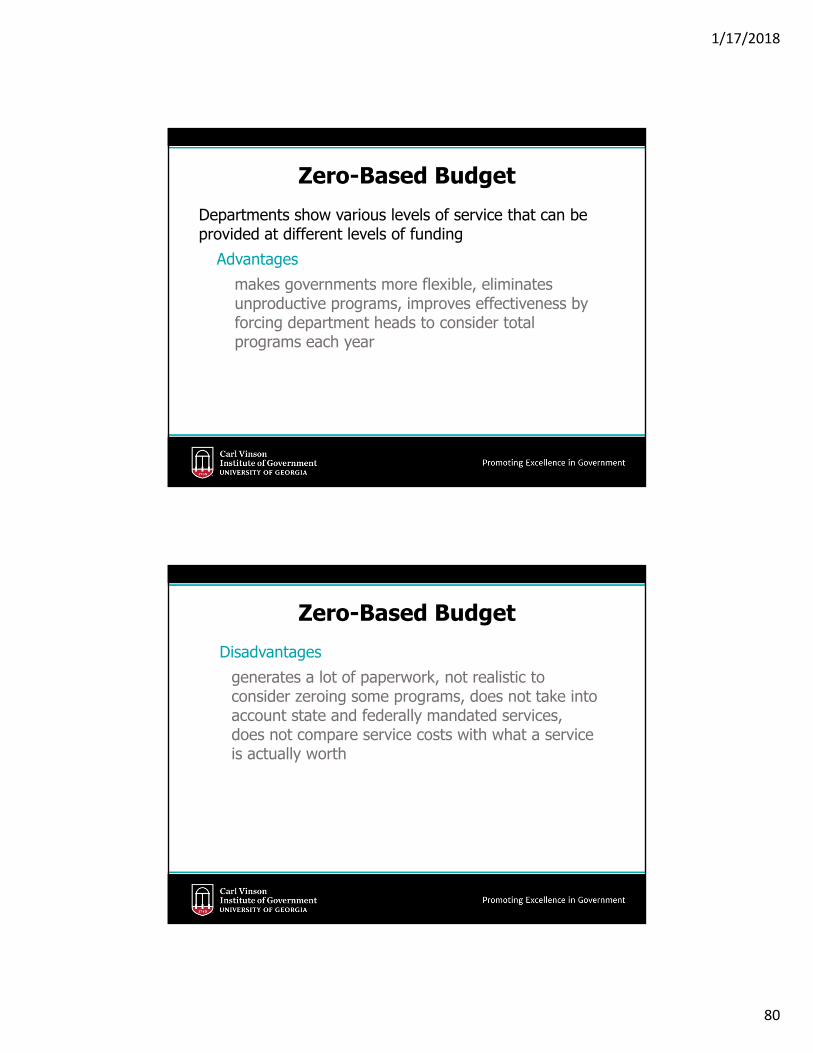

2727

Review

28

ReviewFor reporting purposes, governments classify their individual funds within three categories -A. Governmental, Proprietary, and Fiduciary B. General, Special, and Debt Service C. Governmental, Enterprise, and FiduciaryD. None of the above

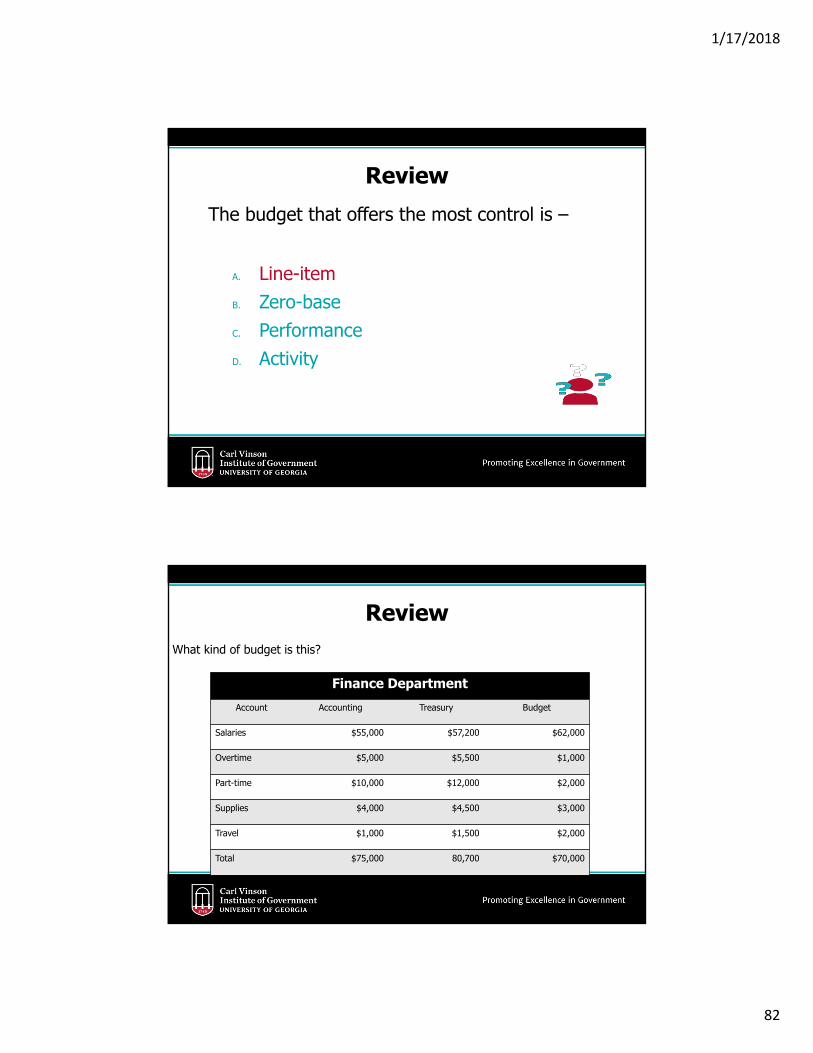

1/17/2018

15

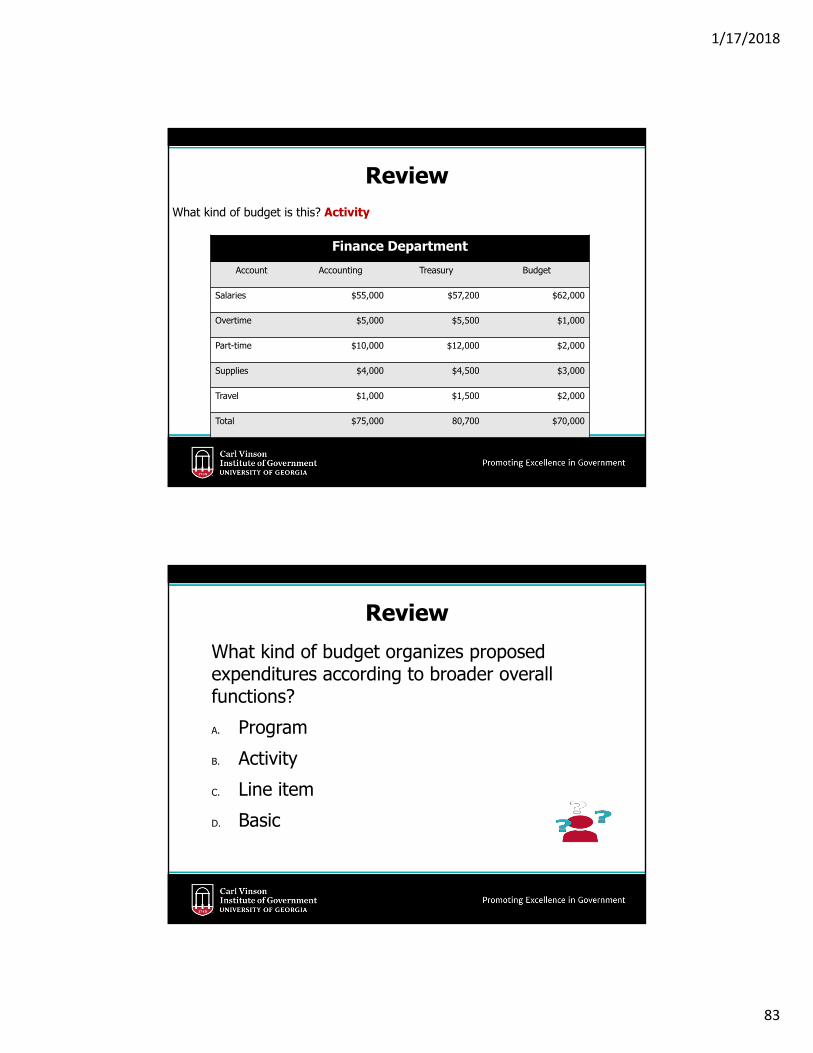

29

ReviewFor reporting purposes, governments classify their individual funds within three categories -A. Governmental, Proprietary, and Fiduciary B. General, Special, and Debt Service C. Governmental, Enterprise, and FiduciaryD. None of the above

30

ReviewThe five generic governmental funds are G___________S_______ R_________C_________ P________D________ S_________P__________

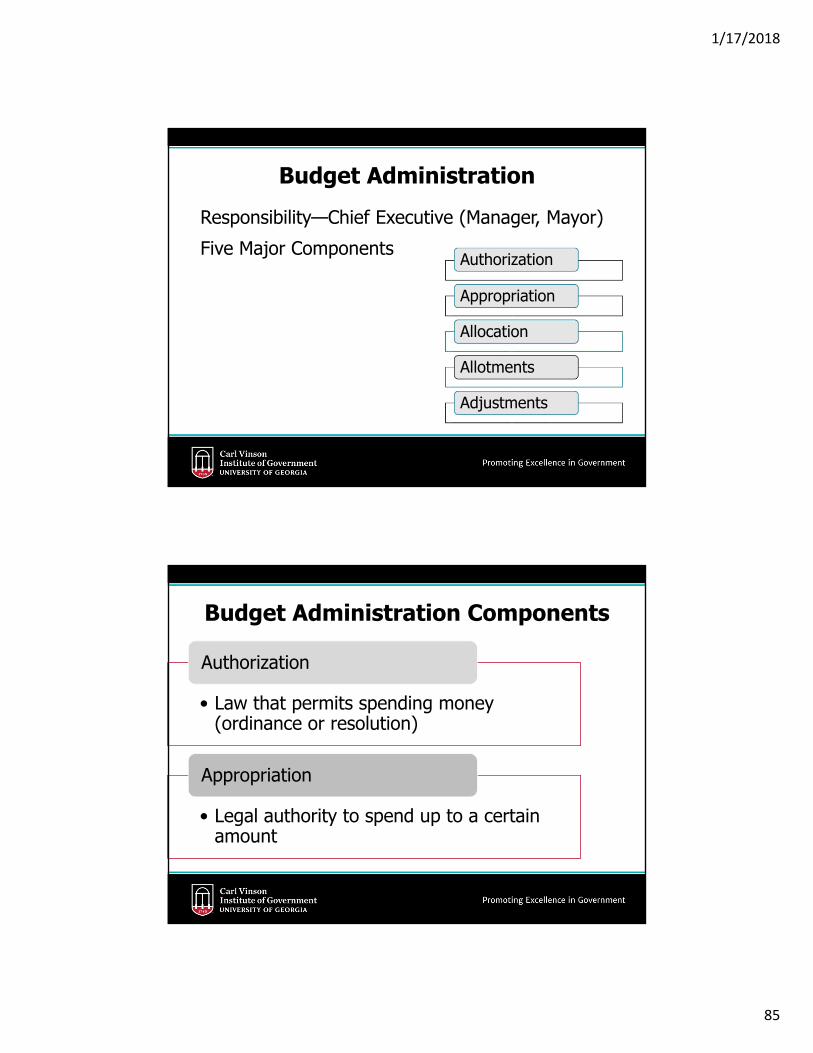

1/17/2018

16

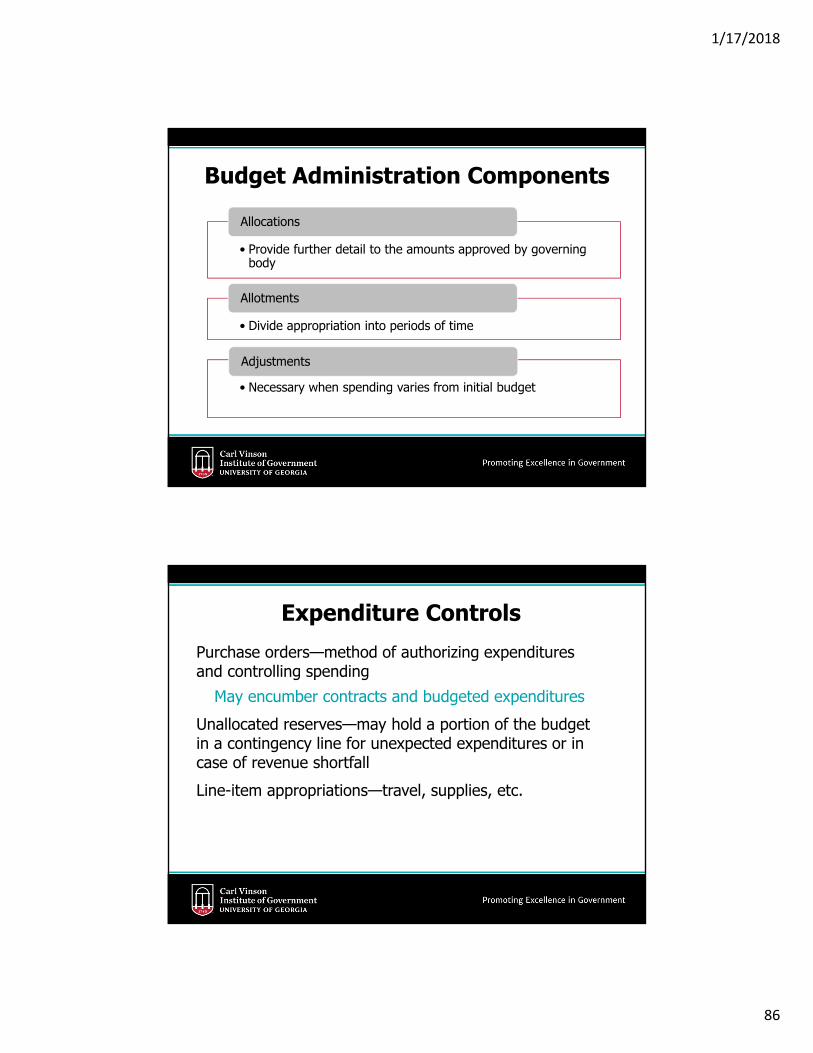

31

ReviewThe five generic governmental funds are GeneralSpecial RevenueCapital Projects Debt ServicePermanent

32

ReviewThe two generic proprietary funds are E_________I_________ S________

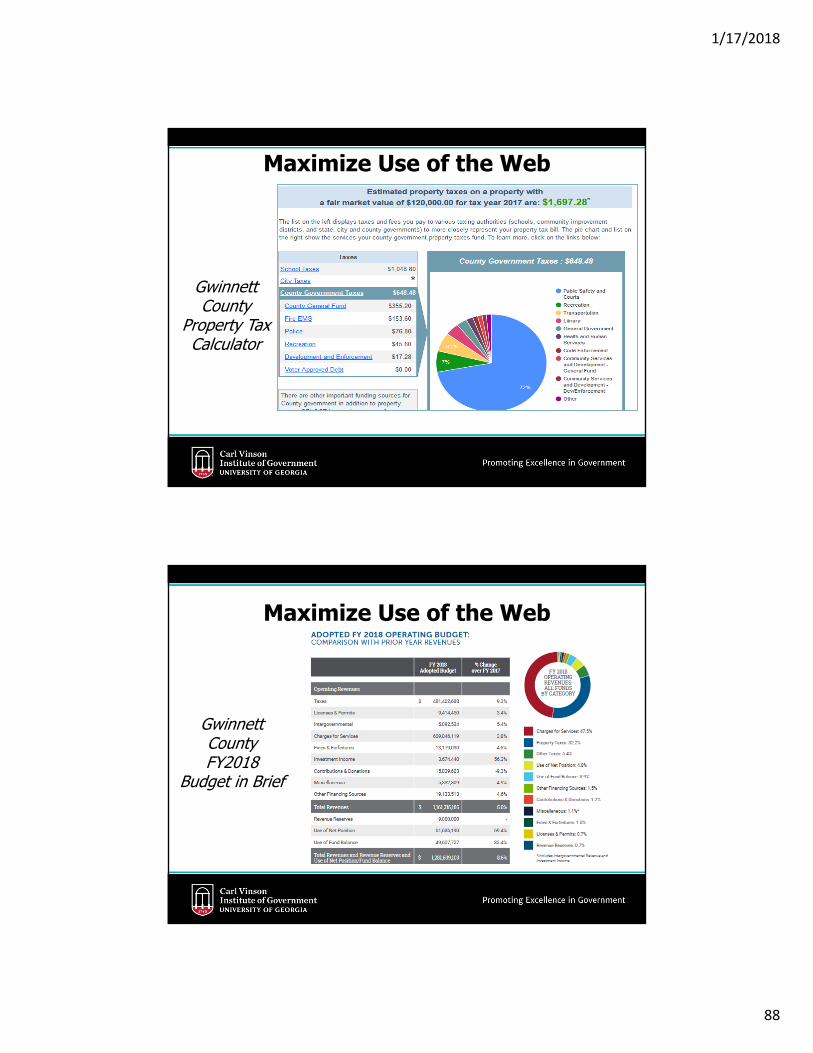

1/17/2018

17

33

ReviewThe two generic proprietary funds are EnterpriseInternal Service

34

ReviewThe four generic fiduciary funds are P_______ P_______ T_______P_______ T__________I___________ T______A_________

1/17/2018

18

35

ReviewThe four generic fiduciary funds are Private Purpose TrustPension TrustInvestment TrustAgency

3636

Fund Balance

1/17/2018

19

37

What is Fund Balance?• Equity in Governmental funds• Revenue increases fund balance and expenditures

decrease fund balance

38

Is Fund Balance Equal to Cash and Investments?

1/17/2018

20

39

Is Fund Balance Equal to Cash and Investments?

• Cash and investments are a part of fund balance• Other parts of fund balance include amounts

owed to your government, cash value of inventory and other assets

40

Governmental Fund EquityNet Current Assets or Fund BalanceCalculated as follows:

Current Assets & Deferred Outflows

Current Liabilities

& Deferred Inflows

Fund Balance

1/17/2018

21

41

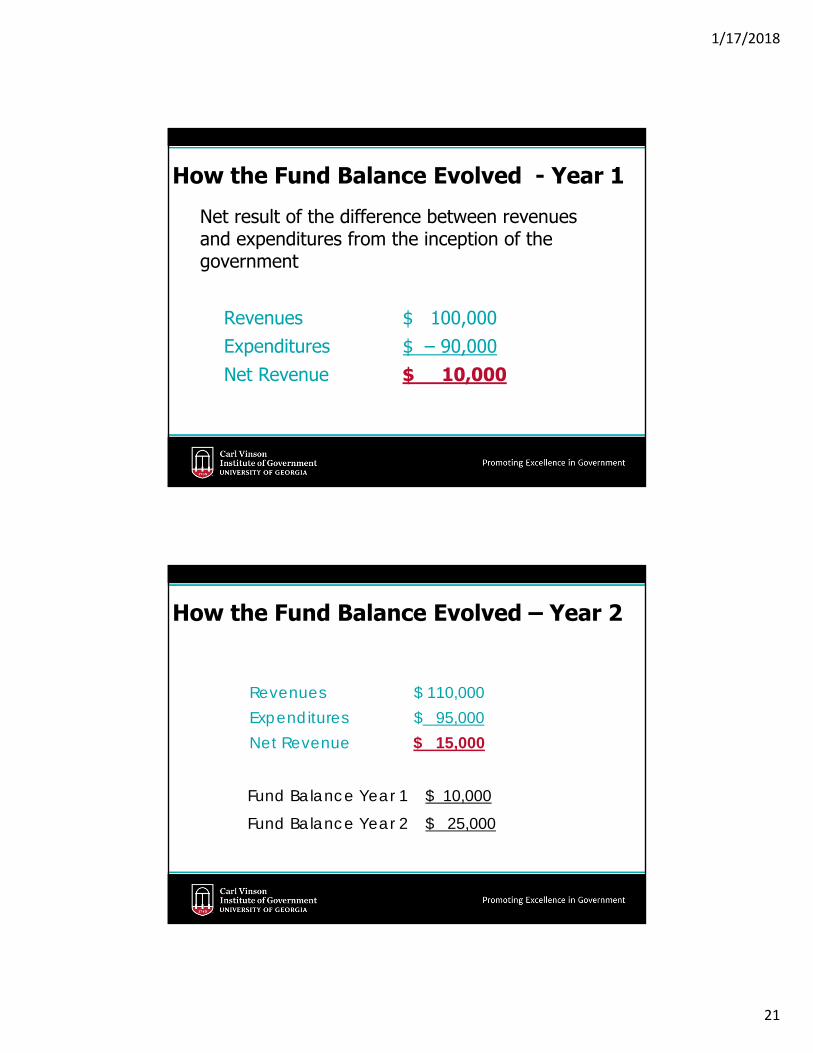

How the Fund Balance Evolved - Year 1Net result of the difference between revenues and expenditures from the inception of the government

Revenues $ 100,000Expenditures $ ‒ 90,000Net Revenue $ 10,000

42

How the Fund Balance Evolved – Year 2

Revenues $ 110,000Expenditures $ 95,000Net Revenue $ 15,000

Fund Balance Year 1 $ 10,000

Fund Balance Year 2 $ 25,000

1/17/2018

22

43

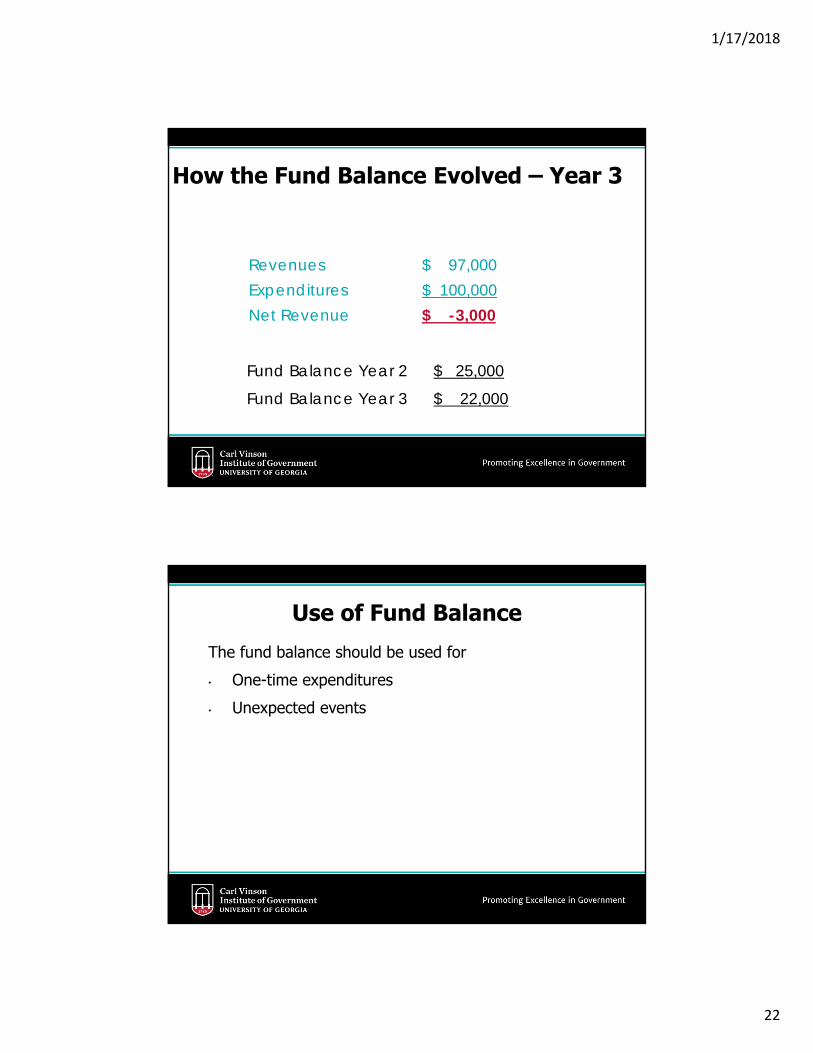

How the Fund Balance Evolved – Year 3

Revenues $ 97,000Expenditures $ 100,000Net Revenue $ -3,000

Fund Balance Year 2 $ 25,000

Fund Balance Year 3 $ 22,000

44

Use of Fund BalanceThe fund balance should be used for• One-time expenditures• Unexpected events

1/17/2018

23

45

Available Fund BalanceThe entire Fund Balance may not be available to fund deficiency of revenues and expenditures

46

Fund Balance—5 Categories

Nonspendable• Inventory• Advances to• Permanent fund

principal

Unassigned• What’s left

Restricted• Debt Covenant• Enabling

Legislation

Committed• Formal Board

Action to commit or de-commit

Assigned• Intent • Not

restricted or committed

1/17/2018

24

47

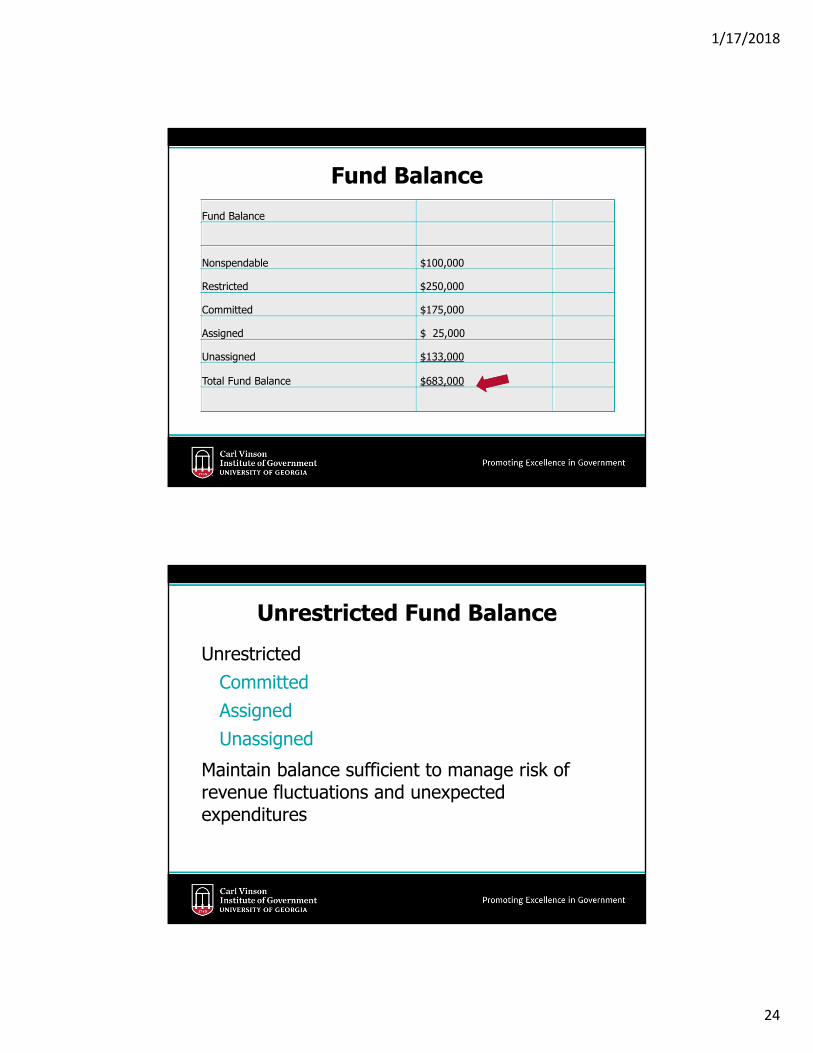

Fund BalanceFund Balance

Nonspendable $100,000

Restricted $250,000

Committed $175,000

Assigned $ 25,000

Unassigned $133,000

Total Fund Balance $683,000

48

Unrestricted Fund BalanceUnrestricted

Committed Assigned Unassigned

Maintain balance sufficient to manage risk of revenue fluctuations and unexpected expenditures

1/17/2018

25

49

What is the Right Amount of Unassigned Fund Balance?

• Unique to each government• Government Finance Officers Recommends

2 months of General Fund operating revenues or expenditures

50

Where Do You Stand?Unassigned Fund Balance as a % of General Fund operating revenues:

Calculated as follows: Unassigned Fund Balance /General Fund Revenues = %

1/17/2018

26

51

Sample Calculation – Step 1Identify Unassigned Fund Balance – Governmental FundsBalance Sheet

52

Sample Calculation – Step 2Identify Total Revenues for the General Fund -

1/17/2018

27

53

Sample Calculation – Step 3

General Fund Unassigned Fund Balance 4,815,949$

Total General Fund Revenues 34,620,817$

Unassigned Fund Balance as a % of Revenues 13.91%

Perform the following calculation-

54

Fund Balance vs. Contingency• Fund Balance and Contingency are not the same• The law is silent on how much contingency to budget• Amounts are not charged to the contingency line

item—budgetary only• Budget adjustments are necessary to move

contingency to appropriate account for spending

1/17/2018

28

55

Review

56

Review

Fund Balance is defined as the difference between current assets & deferred outflows of resources and current liabilities & deferred inflows of resources.

True or False

1/17/2018

29

57

Review

Fund Balance is defined as the difference between current assets & deferred outflows of resources and current liabilities & deferred inflows of resources.

True or False

58

Review

Georgia Law requires governments to budget a contingency in an amount no less than 3% and no greater than 5%.

True or False

1/17/2018

30

59

Review

Georgia Law requires governments to budget a contingency in an amount no less than 3% and no greater than 5%.

True or False

60

Review

Ending fund balance on the operating statement must equal ending fund balance on the balance sheet.

True or False

1/17/2018

31

61

Review

Ending fund balance on the operating statement must equal ending fund balance on the balance sheet.

True or False

62

ReviewGeneral Fund Balance categories include the following-A. NonspendableB. RestrictedC. Committed D. Assigned E. UnassignedF. All of the above

1/17/2018

32

63

ReviewGeneral Fund Balance categories include the following-A. NonspendableB. RestrictedC. Committed D. Assigned E. UnassignedF. All of the above

64

ReviewWhat is the minimum fund balance reserve recommended by the Government Finance Officers Association?A. 12 monthsB. 6 monthsC. 3 monthsD. 2 months

1/17/2018

33

65

Review

What is the minimum fund balance reserve recommended by the Government Finance Officers Association?A. 12 monthsB. 6 monthsC. 3 monthsD. 2 months

6666

Budget and Other Laws

1/17/2018

34

67

O. C. G. A.

Official Code of Georgia Annotated

http://www.lexisnexis.com/hottopics/gacode/Default.asp

68

Budget Law On-Line

1/17/2018

35

69

https://cviog.uga.edu/publications/compliance-auditing-publication.html

70

What Governs the Budget?

Georgia Budget Law and PolicyOfficial Code of Georgia Annotated (O.C.G.A) Sections 36-81-2 to 36-81-6Local ChartersFinancial Policies

1/17/2018

36

71

O.C.G.A. §36-81-3Balanced Budget

Estimated Revenue Sources + Fund Balances = Appropriations

General FundSpecial Revenue FundDebt Service Fund

Capital ProjectsProject-length balanced budget

72

O.C.G.A. §36-81-3

Option to adopt budgets for any remaining fundsAdopt by ordinance or resolution

1/17/2018

37

73

Balanced or Unbalanced?

Example 1 Revenues 100,000$

Expenditures 100,000$

Difference -$

74

Balanced or Unbalanced?

Example 2 Revenues 100,000$

Expenditures 110,000$

Difference (10,000)$

1/17/2018

38

75

Balanced or Unbalanced?

Example 3 Revenues 110,000$ Expenditures 100,000$

Difference 10,000$

76

Balanced or Unbalanced?

Example 4 Revenues 80,000$ Fund Balance 20,000$ Expenditures 100,000$

Difference -$

1/17/2018

39

77

Sample Budget Resolution

See

Sample

Resolution

Page A-7/A-8

78

Budget AmendmentsChanges to original budget—require ordinance or resolutionIncrease in appropriation—legal level of control

Change in revenuesTransfer of appropriations between departments

1/17/2018

40

79

Budget CommunicationO.C.G.A. §36-81-5

Citizens must have access to the budget document same day as it is made available to governing authorityAdvertise budget availability in newspaper during week budget is made available to governing authority as well as date of hearing for public comment. http://georgiapublicnotice.com/

Must be easily identified—CANNOT be placed with legal ads

80

Budget CommunicationO.C.G.A. §36-81-5

At least one week before budget resolution or ordinance is voted on, a public hearing must be held. Advertisement of the hearing date and time must occur one week prior to the hearing.See “Sample Public Hearing Advertisement (Page A-9).”

1/17/2018

41

81

Electronic Reports SubmissionO. C. G. A. §36-80-21Requirement to post documents to Carl Vinson Institute of Government website for governments with budget exceeding $1 million

PDF of approved budget must be posted within 30 calendar days of adoption by ordinance or resolutionPDF of completed audit must be posted as soon as practicable (also must submit to Department of Audits)

82

Electronic Reports SubmissionO. C. G. A. §36-80-21Report of Forfeited Assets required by O.C.G.A. §9-16-19 must be submitted to the Vinson Institute as soon as practicable

1/17/2018

42

83

https://ted.cviog.uga.edu/financial-documents/

84

O.C.G.A. §13-10-91

Requirement to post on the government’s website federally issued user ID # and date of authorization used to determine employment eligibility of workersIf government does not have a website, must post to Carl Vinson Institute of Government website

1/17/2018

43

85

E-Verify Posting

https://ted.cviog.uga.edu/financial-documents/node/add/e-verify-form

86

Property TaxesO.C.G.A. §48-5-32

Must publish in newspaper one week before establishment of millage rates

assessed taxable value of all property, by class and in totalproposed millage ratetotal ad valorem taxes to be levied

1/17/2018

44

87

Property TaxesO.C.G.A. §48-5-32

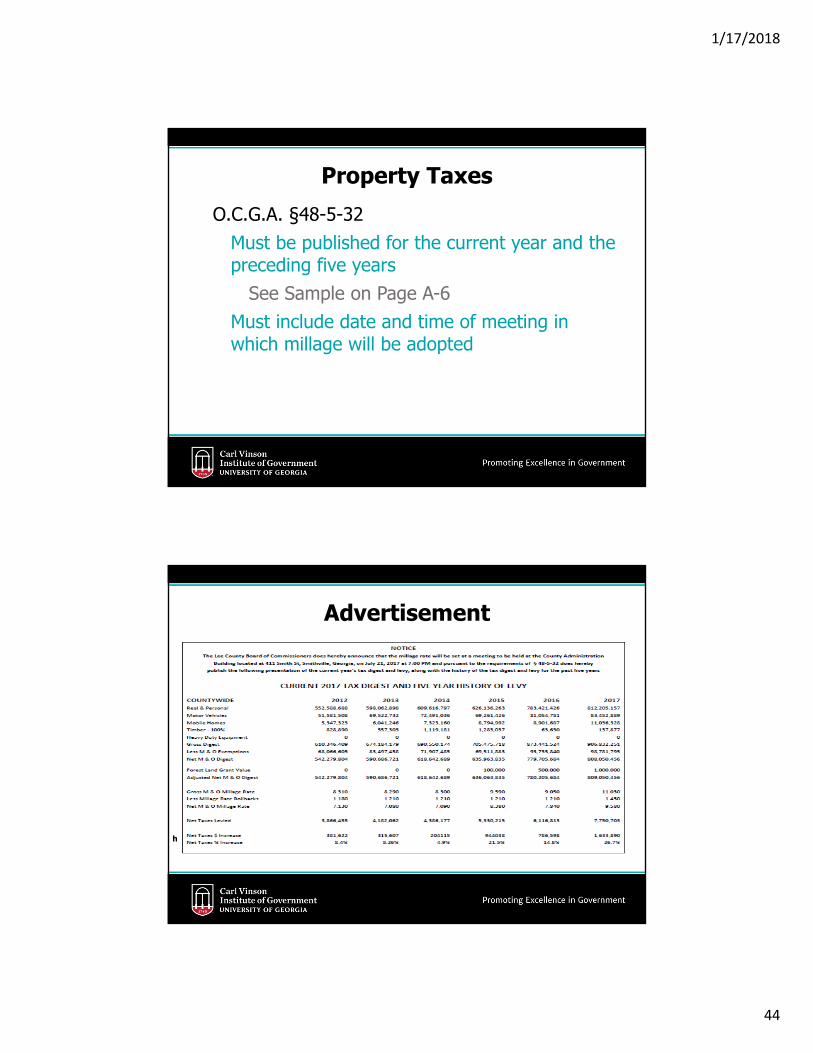

Must be published for the current year and the preceding five years

See Sample on Page A-6Must include date and time of meeting in which millage will be adopted

88

Advertisement

http://dor.georgia.gov/county-tax-digest-submission-package-2017

1/17/2018

45

89

Review

90

ReviewBy law, governments are required to adopt and operate under an annual balanced budget for the -

A. General fund, each special revenue fund and each debt service fund

B. All fundsC. Only the general fundD. None of the above

1/17/2018

46

91

ReviewBy law, governments are required to adopt and operate under an annual balanced budget for the -

A. General fund, each special revenue fund and each debt service fund

B. All fundsC. Only the general fundD. None of the above

92

ReviewGeorgia law states that governments are required to adopt and operate under a project-length balanced budget for -

A. All fundsB. The general fundC. Each capital project fundD. The general fund, special revenue fund and each

debt service fund

1/17/2018

47

93

ReviewGeorgia law states that governments are required to adopt and operate under a project-length balanced budget for -

A. All fundsB. The general fundC. Each capital project fundD. The general fund, special revenue fund and each

debt service fund

94

ReviewA budget ordinance or resolution is balanced when –

A. Assets minus liabilities equal fund balanceB. Credits equal debitsC. The sum of estimated revenues and appropriated

fund balances is equal to appropriationsD. Expenses/expenditures equal appropriations

1/17/2018

48

95

ReviewA budget ordinance or resolution is balanced when –

A. Assets minus liabilities equal fund balanceB. Credits equal debitsC. The sum of estimated revenues and appropriated

fund balances is equal to appropriationsD. Expenses/expenditures equal appropriations

9696

Budget Process Overview

1/17/2018

49

97

Purpose of a Budget

Tool for financial managementPlan for providing services Tool for communicating to the public

Fiscal and management policiesHow services are to be fundedPriorities for services delivered

98

Budget Process—OverviewThe budget process influences

Political goals and objectivesMaintain services without increasing taxes

Departmental revenue and staffing limitationsMandated programs and servicesChanges to service levels

Increase parks/recreation servicesIncrease fire and police

1/17/2018

50

99

Budget Process—OverviewProcess centers around start of fiscal year Budget calendar sets a timeline to ensure budget is adopted before beginning of fiscal year

Deadlines for departments to submit informationDates for advertising and hearingsGoverning Authority Review and Adoption

100

Budget Calendar

https://www.gwinnettcounty.com/static/departments/financialservices/2017_budget/2017_BudgetDocument_Final.pdf

1/17/2018

51

101

Budget Process—OverviewThe Budget Officer

• Develops and distributes budget forms and instructions to departments

• Compiles all information submitted into a single document

• Estimates revenues; combines with departmental expenditures

• Meets with government’s chief executive regarding changes

102

Budget Process—OverviewThe governing body

• Sets priorities for the upcoming year • Reviews proposed budget • Asks questions about increases and decreases and recommended allocation of resources

1/17/2018

52

103

Budget Process—RevenuesCommon Revenue Sources

Property taxesTitle ad valorem taxesInsurance premium taxesSales taxesFranchise fees Beer and wine license and excise taxes

104

Budget Process—Revenues

Common Revenue SourcesBusiness licensesBuilding permitsFines and forfeituresIntergovernmental revenues

1/17/2018

53

105

Revenue ProjectionRequires knowledge of

Present and past conditionsGovernment’s financial condition

Good judgment

106

Revenue ProjectionProperty taxes—estimated by using tax digest informationSales tax—current economic conditionBe conservative

Better to be too low than too high

1/17/2018

54

107

Budget Process—RevenueBasic ConsiderationsAcceptability—Will the tax fairly impact those affected?

Example—sales tax Stability—Will tax collections remain stable in times of economic fluctuations?

108

Budget Process—RevenueBasic Considerations

Self-sufficiency—avoid becoming dependent on state or federal grantsCost efficiency—providing the best quality of services in the most efficient manner

1/17/2018

55

109

Recommended PracticeRevenue Policy

Understanding the revenue stream is essential to prudent planning. Most of these policies seek stability to avoid potential service disruptions caused by revenue shortfalls. At a minimum, jurisdictions should have policies that address:

1. Revenue Diversification—A government should adopt a policy/policies that encourages a diversity of revenue sources in order to improve the ability to handle fluctuations in individual sources. (NACSLB Practice 4.6)

National Advisory Council on State and Local Budgeting (NACSLB)

Recommended Budget Practices—Revenue

110

Recommended PracticeRevenue Policy

2. Fees and Charges—A government should adopt policy(s) that identify the manner in which fees and charges are set and the extent to which they cover the cost of the service provided. (NACSLB Practice 4.2)

3. Use of One-Time Revenues—A government should adopt a policy(s) limiting the use of one-time revenues for ongoing expenditures. (NACSLB Practice 4.4)

4. Use of Unpredictable Revenues—A government should adopt a policy(s) on the use of major revenue sources it considers unpredictable. (NACSLB Practice 4.4a)

National Advisory Council on State and Local Budgeting (NACSLB)

Recommended Budget Practices—Revenue

1/17/2018

56

111

http://www.gfoa.org/framework-improved-state-and-local-government-budgeting

112

Review

1/17/2018

57

113

Review Revenues should be estimated on an objective and conservative basis.

True or False

114

Review Revenues should be estimated on an objective and conservative basis.

True or False

1/17/2018

58

115

Review The four basic considerations when budgeting revenueA__________S_________S________ S__________C_______ E___________

116

Review The four basic considerations when budgeting revenueAcceptabilityStabilitySelf Sufficiency Cost Efficiency

1/17/2018

59

117

Review The Budget is A. Tool for financial managementB. Plan for providing services C. Tool for communicating to the publicD. All of the above

118

Review The Budget is A. Tool for financial managementB. Plan for providing services C. Tool for communicating to the publicD. All of the above

1/17/2018

60

119

Property Tax Revenue

120

Property TaxesOldest form of taxes levied in U.S.Primary revenue source for countiesOnce considered a stable revenue source

1/17/2018

61

121

Property TaxesReal and personal property

Real – real estate, land and buildingsPersonal – inventory, equipment of businesses, boats and motors, airplanes and financial system assets.

Public utilitiesFor the majority of governments, Georgia law requires that property be valued at the fair market value then taxed at an assessed value of 40%

122

Millage RateMillage rate—applied to the appraised value of a parcel of property and determines the tax due

1/17/2018

62

123

Millage RateMill = $1 per $1,000 of assessed property value

Expressed in terms of the following; • 1/1000 of a dollar or• 0.001 x assessed value

124

Millage Rate

Appraisal value $100,000

Assessed at 40% (state law) $40,000

Less exemptions -$10,000

Taxable value $30,000

$30,000 x 12.5 mills (county) $375

18.2 (schools) $546

2.83 (cities) $85

Total $1,006

1/17/2018

63

125

Determining the Correct MillageProperty tax revenues cover the gap between the planned expenditures and forecasted revenues.

Tax Rate = Amount RequiredAssessed Value

126

Determining the Correct MillageEstimated expenditures = $1,560,000Estimated revenues = $1,420,000Total assessed value = $10,000,000

Calculate the millage necessary to balance the budget

1/17/2018

64

127

Determining the Correct Millage

Estimated expenditures = $1,560,000Estimated revenues = $1,420,000

Amount needed to balance the budget

$140,000

128

Determining the Correct Millage

Tax Rate = Amount Required / Assessed Value

$140,00010,000,000

1/17/2018

65

129

Determining the Correct Millage

Tax Rate = Amount Required / Assessed Value

$140,00010,000,000

Millage required to cover the gap: 0.014

130

Taxpayer Bill of RightsO.C.G.A. §48-5-32.1• In any year of revaluation, levying authorities

must rollback millage rates to offset total increase of tax digest due to revaluation or advertise “Notice of Property Tax Increase” and hold three public hearings

• Tax Commissioner/Chief Appraiser computes rollback rate and certifies same to each levying authority

1/17/2018

66

131

Taxpayer Bill of Rights• “Rollback rate” means the previous year's

millage rate minus the millage equivalent of the total net assessed value added by reassessments

• Rollback rate is computed by either Tax Commissioner or Tax Assessor on prescribed form from the DOR. Form must be submitted with digest

132

SEE

Page

A-5

1/17/2018

67

133

Taxpayer Bill of Rights

• Essentially, any inflationary increase in the digest must be offset by a rollback of the millage rate, or public hearings must be held and additional newspaper ad must be run

• In instances in which there is no revaluation, if millage rates are increased, the public hearing requirement may apply

134

Advertisement

1/17/2018

68

135

Review

136

ReviewFor the majority of governments, Georgia law requires that property be valued at the fair market value then taxed at an assessed value of -A. 30%B. 35%C. 40%D. 45%

1/17/2018

69

137

ReviewFor the majority of governments, Georgia law requires that property be valued at the fair market value then taxed at an assessed value of -A. 30%B. 35%C. 40%D. 45%

138

ReviewOne mill of tax is equivalent to $1 per thousand of taxable assessed value.

True or False

1/17/2018

70

139

ReviewOne mill of tax is equivalent to $1 per thousand of taxable assessed value.

True or False

140

ReviewFor a government that has a net taxable digest of $2,093,130,182, the value of one mill of tax would be equivalent to -A. $209,313,000B. $2,093,130C. $209,313D. None of the above are correct

1/17/2018

71

141

ReviewFor a government that has a net taxable digest of $2,093,130,182, the value of one mill of tax would be equivalent to -A. $209,313,000B. $2,093,130C. $209,313D. None of the above are correct

142

ReviewIf a governing authority levies a millage rate that is greater than the roll back rate they must hold _____ hearings to comply with the Tax Payer Bill of Rights.A. OneB. TwoC. ThreeD. Four

1/17/2018

72

143

ReviewIf a governing authority levies a millage rate that is greater than the roll back rate they must hold _____ hearings to comply with the Tax Payer Bill of Rights.A. OneB. TwoC. ThreeD. Four

144

Review______ weeks prior to setting the millage rate, Georgia governments are required to advertise, in the legal organ of their jurisdiction, the current year tax levy and five year history of the tax levy.A. OneB. TwoC. ThreeD. Four

1/17/2018

73

145

Review______ weeks prior to setting the millage rate, Georgia governments are required to advertise, in the legal organ of their jurisdiction, the current year tax levy and five year history of the tax levy.A. OneB. TwoC. ThreeD. Four

146

EXPENDITURES

1/17/2018

74

147

Line ItemTraditional budgetingMost frequently used by local governmentsMost simplePrimary emphasis – CONTROL

Focus is on inputs (what is to be spent)

148

Line Item Example

Superior Court Clerk

AccountCurrentBudget

ProposedBudget

% IncreaseDecrease

Salaries $55,000 $57,200 4%

Overtime $5,000 $5,500 10%

Part-time $10,000 $12,000 20%

Supplies $4,000 $4,500 12.5%

Travel $1,000 $1,500 50%

Total $75,000 80,700 7.6%

1/17/2018

75

149

Line ItemDisadvantages

Encourages incrementalismBase initial budget requests on the amount of budgeted resources in last year’s budget

Does not require departments to consider alternative methods to spending or delivering services.Does not consider if the service should even be offered.

150

Activity BudgetNext step up from line-item budgeting

Various activities within the same department are recognized

1/17/2018

76

151

Activity BudgetFinance Department

Account Accounting Treasury Budget

Salaries $55,000 $57,200 $62,000

Overtime $5,000 $5,500 $1,000

Part-time $10,000 $12,000 $2,000

Supplies $4,000 $4,500 $3,000

Travel $1,000 $1,500 $2,000

Total $75,000 80,700 $70,000

152

Activity BudgetActivities within other departments:

PoliceFirePublic Works

1/17/2018

77

153

Program Budget• Organizes proposed expenditures according

to broader overall functions• Focus is no longer on what is purchased• Focus is on what services are being provided• Goals are defined and expenses are allocated

based on the defined goal

154

Program BudgetExample: Enhance accessibility of official records for public use by expanding services available via the Internet

Provide on-line access of recorded court and real estate documents by September 2010

1/17/2018

78

155

Program BudgetSample Program Budget

Superior Court Clerk Program: Record accessibility

Expenditure Classification

Previous Fiscal Year Actual

Current Fiscal Year Budget

Next Fiscal Year Request

Salaries $ $ $

Supplies $ $ $

Contractual Services $ $ $

Capital Outlay $ $ $

Total $ $ $

156

Program BudgetDrawbacks

Reorganization of the budgetMany activities contribute to more than one objective Not all resources can be assigned to a single program.

1/17/2018

79

157

Performance Budget

Advantagesemphasizes department performance objectives rather than purchases of resources emphasizes efficiency and effectiveness of services

158

Performance BudgetDisadvantages

more complicated than line-item or program budgets does not require departments to consider alternatives does not consider whether the service is worth the cost of providing it

1/17/2018

80

159

Zero-Based BudgetDepartments show various levels of service that can be provided at different levels of funding

Advantages makes governments more flexible, eliminates unproductive programs, improves effectiveness by forcing department heads to consider total programs each year

160

Zero-Based BudgetDisadvantages

generates a lot of paperwork, not realistic to consider zeroing some programs, does not take into account state and federally mandated services, does not compare service costs with what a service is actually worth

1/17/2018

81

161

Review

162

ReviewThe budget that offers the most control is –

A. Line-itemB. Zero-baseC. PerformanceD. Activity

1/17/2018

82

163

ReviewThe budget that offers the most control is –

A. Line-itemB. Zero-baseC. PerformanceD. Activity

164

ReviewWhat kind of budget is this?

Finance DepartmentAccount Accounting Treasury Budget

Salaries $55,000 $57,200 $62,000

Overtime $5,000 $5,500 $1,000

Part-time $10,000 $12,000 $2,000

Supplies $4,000 $4,500 $3,000

Travel $1,000 $1,500 $2,000

Total $75,000 80,700 $70,000

1/17/2018

83

165

ReviewWhat kind of budget is this? Activity

Finance DepartmentAccount Accounting Treasury Budget

Salaries $55,000 $57,200 $62,000

Overtime $5,000 $5,500 $1,000

Part-time $10,000 $12,000 $2,000

Supplies $4,000 $4,500 $3,000

Travel $1,000 $1,500 $2,000

Total $75,000 80,700 $70,000

166

ReviewWhat kind of budget organizes proposed expenditures according to broader overall functions?A. ProgramB. ActivityC. Line itemD. Basic

1/17/2018

84

167

ReviewWhat kind of budget organizes proposed expenditures according to broader overall functions?A. ProgramB. ActivityC. Line itemD. Basic

168168

Administering the Budget

1/17/2018

85

169

Budget AdministrationResponsibility—Chief Executive (Manager, Mayor)Five Major Components Authorization

Appropriation

Allocation

Allotments

Adjustments

170

Budget Administration Components

• Law that permits spending money (ordinance or resolution)

Authorization

• Legal authority to spend up to a certain amount

Appropriation

1/17/2018

86

171

Budget Administration Components

• Provide further detail to the amounts approved by governing body

Allocations

• Divide appropriation into periods of time

Allotments

• Necessary when spending varies from initial budget

Adjustments

172

Expenditure ControlsPurchase orders—method of authorizing expenditures and controlling spending

May encumber contracts and budgeted expenditures Unallocated reserves—may hold a portion of the budget in a contingency line for unexpected expenditures or in case of revenue shortfallLine-item appropriations—travel, supplies, etc.

1/17/2018

87

173

Expenditure ControlsPosition control—ensures positions are limited to those funded in the budget processCeilings or freezes—used in financial crisis to freeze spending on some or all items or cap expenditures for some or all purposes

174174

Communicating the Budget

1/17/2018

88

175

Maximize Use of the Web

Gwinnett County

Property Tax Calculator

176

Maximize Use of the Web

Gwinnett County FY2018

Budget in Brief

1/17/2018

89

177

Gwinnett County FY2018

Budget in Brief

Maximize Use of the Web

178

Budget IncreasesUse an example that the public can relate to:

The millage rate increase of $.46 per $1,000 would result in a property tax increase for a homeowner with a $140,000 house and $10,000 homestead exemption of $23.92, about the cost of a hardback book.

1/17/2018

90

179179

Financial Reporting and Audits

180

Accounting

O.C.G.A. §36-81-3Requires use of a uniform chart of accounts

1/17/2018

91

181

Preparation of External Financial Statements

Required to be prepared in accordance with statements of the Governmental Accounting Standards Board as follows:

Management’s Discussion and AnalysisGovernment-wide financial statementsFund-level financial statementsNote disclosuresBudgetary comparison schedules on the General Fund and each fund that has a legally adopted budget

182

Audit Opinion

An opinion on the fair presentation in all material respects of financial statements

Unmodified opinionModified opinion

Qualified opinionAdverse opinion Disclaimer of opinion

1/17/2018

92

183

Report RequirementsAuditor compliance with GAGAS (Generally Accepted Government Auditing Standards)Reporting on internal control and compliance with provisions of laws, regulations, contracts, and grant agreementsDeficiencies in internal control, fraud, noncompliance with provisions of laws, regulations, contracts, grant agreements, and abuse

184

Report RequirementsViews of responsible officialsConfidential or sensitive informationDistribution requirements

1/17/2018

93

185

Georgia Law RequirementsO.C.G.A. §36-81-7

Each unit of local government with a population over 1,500 or expenditures of $300,000 must have an annual audit.Units of local government with a population of 1,500 or less or expenditures less than $300,000 are required to complete an audit every two years for both fiscal years.

186

Georgia Law RequirementsAudit is due 180 days after the year-end of your local government to the State of Georgia Local Government Division Department of Audits and Accounts.Corrective action plan is due 30 days after your audit is due to the state Department of Audits.

1/17/2018

94

187

Auditor SelectionIndependentQualified to perform government audits

CPE—required to complete every two years 24 hours of CPE pertaining to government audits or government environment as part of an 80-hour total requirement

RFP sample—Georgia Department of Audits

http://www.audits.ga.gov/NALGAD/Files/RFP_Revision_2015.doc

188

Other Types of AuditsPerformance Audits

Measure efficiency of performance of various activitiesProgram Audits

Evaluate the overall effectiveness of programs

Both Performance and Program Audits help governments make better decisions about whether services and programs are worth the investment of revenues.

1/17/2018

95

189

DCA—ReportingGeorgia law requires completion of Report of Local Government Finances.

Report form references uniform chart of account numbers to facilitate consistency in information reported.Data are used to publish the Local Government Fiscal Planning Guide, which can be accessed on the DCA website.www.dca.ga.gov/development/research/programs/fpg.asp

190

Financial Highlights Reporthttp://www.dca.ga.gov/development/research/programs/lgf.asp

Consolidation of information reported in Report of Local Government Finance

1/17/2018

96

191

192192

Governmental Accounting, Auditing, and Financial Reporting • APPENDIX D

Name of GovernmentBalance Sheet

Governmental FundsJune 30, 2022

Total TotalNonmajor Governmental

General Capital Projects Debt Service Funds FundsASSETS Cash and cash equivalents $ 6,127,206 $ 1,090,139 $ 1,362,371 $ 4,281,747 $ 12,861,463 Investments 14,989,065 4,980,521 1,000,000 538,805 21,508,391 Receivables (net of allowance for uncollectibles) 6,067,247 - 4,309,618 2,502,201 12,879,066 Intergovernmental receivable 513,579 507,459 - 688,445 1,709,483 Due from other funds 145,000 335,000 - - 480,000 Due from component unit 32,615 - - - 32,615 Inventories 806,623 - - - 806,623 Prepaid items 48,114 - - 614 48,728 Advances to other funds 290,148 - - - 290,148 Total assets $ 29,019,597 $ 6,913,119 $ 6,671,989 $ 8,011,812 $ 50,616,517

LIABILITIES Accounts payable 1,646,243 - - 516,358 2,162,601 Contracts payable - 1,129,196 - - 1,129,196 Retainage payable - 1,070,044 - - 1,070,044 Accrued liabilities 2,504,060 - - 431,957 2,936,017 Deposits payable - - - 18,367 18,367 Due to retirement systems 2,024,105 - - 78,108 2,102,213 Due to other funds 335,000 - - 157,000 492,000 Advances from other funds - - - 290,148 290,148 Bond anticipation notes payable - 6,905,200 - - 6,905,200 Unearned revenue-other 2,089,936 - - 227,585 2,317,521 Total liabilities 8,599,344 9,104,440 - 1,719,523 19,423,307

DEFERRED INFLOWS OF RESOURCES Unavailable revenue-property taxes 617,585 - 26,429 - 644,014 Unavailable revenue-special assessments - - 4,230,000 - 4,230,000 Total deferred inflows of resources 617,585 - 4,256,429 - 4,874,014

FUND BALANCES (DEFICITS) Nonspendable: Endowment $ - $ - $ - $ 10,000 $ 10,000 Inventory 806,623 - - - 806,623 Prepaid items 48,114 - - 614 48,728 Long-term interfund advances 290,148 - - - 290,148 Restricted: - Special assessment project - 875,000 - - 875,000 Library purposes - - - 52,276 52,276 Housing services - - - 625,881 625,881 Community redevelopment - - - 4,514,328 4,514,328 Law enforcement - - - 376,200 376,200 Youth programs - - - 1,297 1,297 Nonrecurring repairs and other parking improvements - - - 338,917 338,917 General obligation debt - - 911,560 - 911,560 Special assessment debt - - 1,504,000 - 1,504,000 Committed: Special asesssment project - 1,200,000 - - 1,200,000 Revenue stabilization 407,377 - - - 407,377 Open space - - - 372,776 372,776 Assigned: Purchases on order 592,659 - - - 592,659 Subsequent year's budget: appropriation of fund balance 2,215,728 - - - 2,215,728 Unassigned 15,442,019 (4,266,321) - - 11,175,698 Total fund balances (deficits) 19,802,668 (2,191,321) 2,415,560 6,292,289 26,319,196Total liabilities, deferred inflows of resources, and fund balances (deficits) $ 29,019,597 $ 6,913,119 $ 6,671,989 $ 8,011,812 $ 50,616,517

The notes to financial statements are an integral part of this statement.

Name of GovernmentBalance Sheet

Governmental FundsJune 30, 2022

A-1

Governmental Accounting, Auditing, and Financial Reporting • APPENDIX D

Name of GovernmentStatement of Revenues, Expenditures and Changes in Fund Balances

Governmental FundsFor the Year Ended June 30, 2022

Total TotalNonmajor Governmental

General Capital Projects Debt Service Funds FundsREVENUES Property taxes $ 31,331,083 $ - $ 7,935,396 $ 5,539,162 $ 44,805,641 Sales taxes 44,368,865 - - - 44,368,865 Franchise taxes 1,537,833 - - - 1,537,833 Licenses and permits 2,649,889 - - - 2,649,889 Intergovernmental 9,705,931 874,480 - 7,185,616 17,766,027 Charges for services 19,091,893 - - - 19,091,893 Fines and forfeitures 6,670,562 - - - 6,670,562 Investment earnings 3,349,530 201,620 241,967 38,681 3,831,798 Fees - - - 4,976,526 4,976,526 Special assessments - - 470,000 - 470,000 Miscellaneous 4,644,708 - - 329,712 4,974,420 Total revenues 123,350,294 1,076,100 8,647,363 18,069,697 151,143,454

EXPENDITURES Current: General government 29,778,662 - - - 29,778,662 Public Safety 56,335,850 - - 390,828 56,726,678 Highways and streets 23,233,034 - - 4,238,979 27,472,013 Sanitation 8,140,187 - - - 8,140,187 Culture and recreation 9,735,013 - - 13,295,900 23,030,913 Debt service: Principal - - 4,718,317 - 4,718,317 Interest - - 3,236,206 - 3,236,206 Bond issuance costs 150,000 - 122,710 - 272,710 Capital outlay General government - 462,180 - - 462,180 Public Safety - 1,465,901 - - 1,465,901 Highways and streets - 9,574,399 - - 9,574,399 Sanitation - 1,696,099 - - 1,696,099 Culture and recreation - 1,443,330 - - 1,443,330 Total expenditures 127,372,746 14,641,909 8,077,233 17,925,707 168,017,595

Excess (deficiency) of revenues over expenditures (4,022,452) (13,565,809) 570,130 143,990 (16,874,141)

OTHER FINANCING SOURCES (USES)Transfers in 20,944 1,831,625 1,226,340 252,695 3,331,604Transfers out (4,939,824) (1,214,133) (621,625) (284,231) (7,059,813) Refunding bonds issued - - 5,810,000 - 5,810,000Premium on refunding bonds issued - - 249,914 - 249,914Special assessment bonds issued - 4,700,000 - - 4,700,000Discount on special assessment bonds issued - (10,000) - - (10,000)Payment to refunded bond escrow agent - - (5,937,204) - (5,937,204) Capital lease 146,042 - - - 146,042Sale of general capital assets 31,450 - - - 31,450Insurance recoveries 194,082 - - - 194,082 Total other financing sources (uses) (4,547,306) 5,307,492 727,425 (31,536) 1,456,075

Net change in fund balances (8,569,758) (8,258,317) 1,297,555 112,454 (15,418,066)

Fund balances-beginning 28,372,426 6,066,996 1,118,005 6,179,835 41,737,262

Fund balances (deficit)-ending $ 19,802,668 $ (2,191,321) $ 2,415,560 $ 6,292,289 $ 26,319,196

The notes to financial statements are an integral part of this statement.

A-2

Governmental Accounting, Auditing, and Financial Reporting • APPENDIX D

Name of GovernmentStatement of Net Position

Proprietary FundsJune 30, 2022

GovernmentalBusiness-type Activities

TotalWater Transit Enterprise Funds

ASSETSCurrent Assets: Cash and cash equivalents $ 1,388,998 $ 2,310,846 $ 3,699,844 $ 5,883,720 Investments 2,136,642 - 2,136,642 611,286 Restricted assets-customer deposits 30,715 - 30,715 - Interest receivable 22,468 2,383 24,851 7,079 Accounts receivable 4,145,017 33,734 4,178,751 - Due from other funds - 12,000 12,000 - Intergovernmental receivable - 877,295 877,295 129,192 Inventories - 117,581 117,581 22,671 Prepaid items - - - 37,823 Total current assets 7,723,840 3,353,839 11,077,679 6,691,771

Noncurrent Assets: Capital Assets: Land 584,715 1,326,685 1,911,400 - Buildings 5,274,379 7,639,062 12,913,441 87,745 Machinery, equipment, and vehicles 1,376,709 9,952,998 11,329,707 5,283,268 Water distribution system 35,422,287 - 35,422,287 - Construction-in-progress 5,371,664 - 5,371,664 - Less accumulated depreciation (17,093,131) (9,869,210) (26,962,341) (2,466,987) Total noncurrent assets 30,936,623 9,049,535 39,986,158 2,904,026 Total assets 38,660,463 12,403,374 51,063,837 9,595,797

LIABILITIESCurrent liabilities: Accounts payable 1,057,264 532,741 1,590,005 814,023 Accrued liabilities - 11,412 11,412 - Compensated absences 5,990 - 5,990 16,679 Claims and judgments - - - 2,174,256 Retainage payable 24,937 - 24,937 - Customer deposits payable-restricted assets 30,715 - 30,715 - Accrued interest payable 143,219 - 143,219 - Bond anticipation note payable 1,625,000 - 1,625,000 - Intergovernmental payable - 28,547 28,547 - Due to retirement system 35,364 - 35,364 3,268 Bonds payable - current 938,967 - 938,967 - Unearned revenue - 2,192,549 2,192,549 - Total current liabilities 3,861,456 2,765,249 6,626,705 3,008,226

Noncurrent liabilities: Compensated absences 53,907 - 53,907 27,589 Claims and judgments - - - 1,386,533 Bonds payable 9,103,170 - 9,103,170 - Other post employment benefits obligation 259,000 - 259,000 61,000 Total noncurrent liabilities 9,416,077 - 9,416,077 1,475,122 Total liabilities 13,277,533 2,765,249 16,042,782 4,483,348

NET POSITIONNet investment in capital assets 20,006,772 9,049,535 29,056,307 2,904,026Unrestricted 5,376,158 588,590 5,964,748 2,208,423

Total net position 25,382,930 9,638,125 35,021,055 $ 5,112,449

Adjustment to report the cumulative internal balance for the net effect of the activity between the internal service funds and the enterpise funds over time 297,518

Net position of business-type activities (page 30) $ 35,318,573

The notes to financial statements are an integral part of this statement

Activities

Internal ServiceFunds

Name of GovernmentStatement of Net Position

Proprietary FundsJune 30, 2022

A-3

Governmental Accounting, Auditing, and Financial Reporting • APPENDIX D

Name of GovernmentStatement of Revenues, Expenses and Changes in Net Position

Proprietary FundsFor the Year Ended June 30, 2022

Governmental Business-type Activities Activities

Total Internal ServiceWater Transit Enterprise Funds Funds

Operating revenues: Charges for services: Metered water sales $ 9,312,150 $ - $ 9,312,150 $ - Tap fees 12,050 - 12,050 - Passanger fares - 762,983 762,983 - Contract transit - 126,353 126,353 - Charter - 248 248 - Risk management - - - 2,632,108 Fleet management - - - 1,902,063 Miscellaneous 133,423 40,547 173,970 - Total operating revenues 9,457,623 930,131 10,387,754 4,534,171

Operating expenses: Personnel services 2,821,081 - 2,821,081 567,467 Materials and supplies 3,556,232 1,050,965 4,607,197 944,229 Contractual services 781,741 4,008,669 4,790,410 1,251,500 Claims - - - 1,761,680 Depreciation 886,240 827,289 1,713,529 373,469 Total operating expenses 8,045,294 5,886,923 13,932,217 4,898,345 Operating income (loss) 1,412,329 (4,956,792) (3,544,463) (364,174)

Nonoperating revenues (expenses): Intergovernmental 10,967 390,474 401,441 - Investment earnings 254,072 10,819 264,891 139,530 Loss on disposal of property (2,278) (88,031) (90,309) - Interest expense (416,820) - (416,820) - Total nonoperating revenues (expenses) (154,059) 313,262 159,203 139,530 Income before capital contributions and transfers 1,258,270 (4,643,530) (3,385,260) (224,644)

Capital contributions - 1,174,511 1,174,511 -Transfers in - 3,728,209 3,728,209 -

Change in net position 1,258,270 259,190 1,517,460 (224,644)

Net position-beginning 24,124,660 9,378,935 5,337,093Net position-ending $ 25,382,930 $ 9,638,125 $ 5,112,449

Adjustment for the net effect of the current year activity between the internal service funds and the enterprise funds. 16,964

Changes in net position of business-type activities (page 31) $ 1,534,424

The notes to financial statements are an integral part of this statement.

Name of GovernmentStatement of Revenues, Expenses and Changes in Net Position

Proprietary FundsFor the Year Ended June 30, 2022

A-4

Department of Revenue / Local Government Services Division Revised March 2017

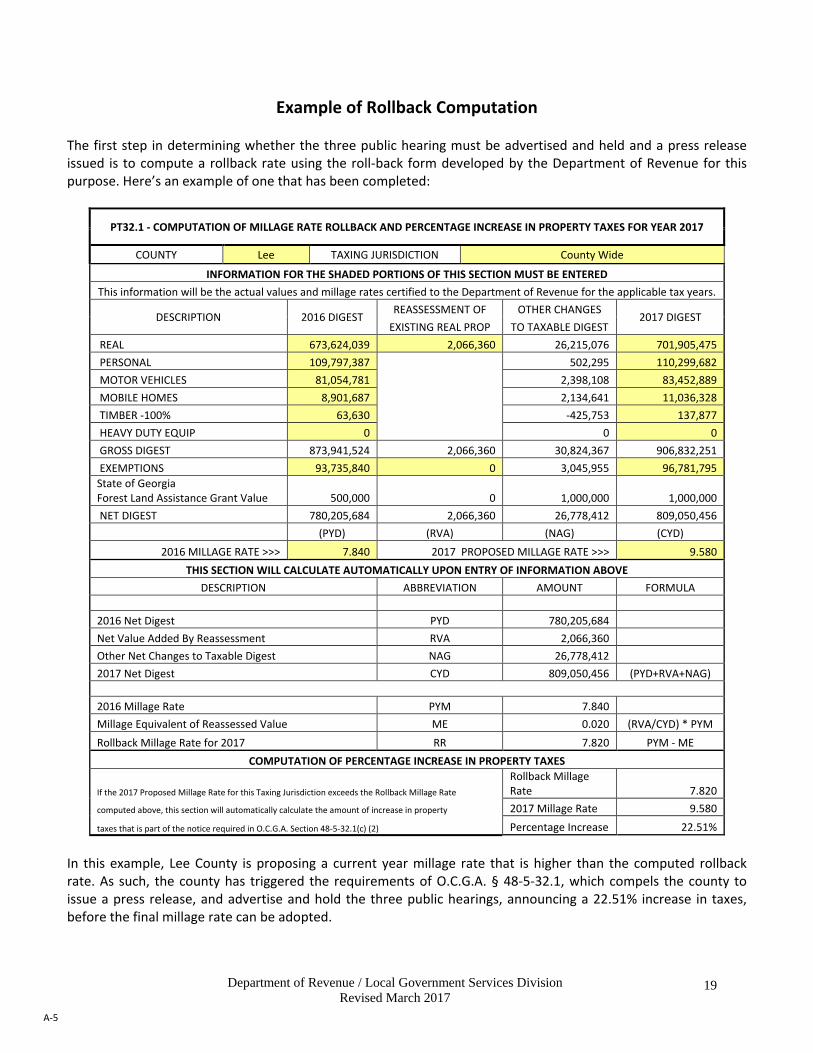

19

Example of Rollback Computation

The first step in determining whether the three public hearing must be advertised and held and a press release issued is to compute a rollback rate using the roll-back form developed by the Department of Revenue for this purpose. Here’s an example of one that has been completed:

PT32.1 - COMPUTATION OF MILLAGE RATE ROLLBACK AND PERCENTAGE INCREASE IN PROPERTY TAXES FOR YEAR 2017

COUNTY Lee TAXING JURISDICTION County Wide

INFORMATION FOR THE SHADED PORTIONS OF THIS SECTION MUST BE ENTERED This information will be the actual values and millage rates certified to the Department of Revenue for the applicable tax years.

DESCRIPTION 2016 DIGEST REASSESSMENT OF OTHER CHANGES

2017 DIGEST EXISTING REAL PROP TO TAXABLE DIGEST

REAL 673,624,039 2,066,360 26,215,076 701,905,475 PERSONAL 109,797,387 502,295 110,299,682 MOTOR VEHICLES 81,054,781 2,398,108 83,452,889 MOBILE HOMES 8,901,687 2,134,641 11,036,328 TIMBER -100% 63,630 -425,753 137,877 HEAVY DUTY EQUIP 0 0 0 GROSS DIGEST 873,941,524 2,066,360 30,824,367 906,832,251 EXEMPTIONS 93,735,840 0 3,045,955 96,781,795 State of Georgia Forest Land Assistance Grant Value 500,000 0 1,000,000 1,000,000 NET DIGEST 780,205,684 2,066,360 26,778,412 809,050,456

(PYD) (RVA) (NAG) (CYD) 2016 MILLAGE RATE >>> 7.840 2017 PROPOSED MILLAGE RATE >>> 9.580

THIS SECTION WILL CALCULATE AUTOMATICALLY UPON ENTRY OF INFORMATION ABOVE DESCRIPTION ABBREVIATION AMOUNT FORMULA

2016 Net Digest PYD 780,205,684 Net Value Added By Reassessment RVA 2,066,360 Other Net Changes to Taxable Digest NAG 26,778,412 2017 Net Digest CYD 809,050,456 (PYD+RVA+NAG)

2016 Millage Rate PYM 7.840 Millage Equivalent of Reassessed Value ME 0.020 (RVA/CYD) * PYM Rollback Millage Rate for 2017 RR 7.820 PYM - ME

COMPUTATION OF PERCENTAGE INCREASE IN PROPERTY TAXES

If the 2017 Proposed Millage Rate for this Taxing Jurisdiction exceeds the Rollback Millage Rate

Rollback Millage Rate 7.820

computed above, this section will automatically calculate the amount of increase in property 2017 Millage Rate 9.580

taxes that is part of the notice required in O.C.G.A. Section 48-5-32.1(c) (2) Percentage Increase 22.51%

In this example, Lee County is proposing a current year millage rate that is higher than the computed rollback rate. As such, the county has triggered the requirements of O.C.G.A. § 48-5-32.1, which compels the county to issue a press release, and advertise and hold the three public hearings, announcing a 22.51% increase in taxes, before the final millage rate can be adopted.

A-5

Department of Revenue / Local Government Services Division Revised March 2017

7

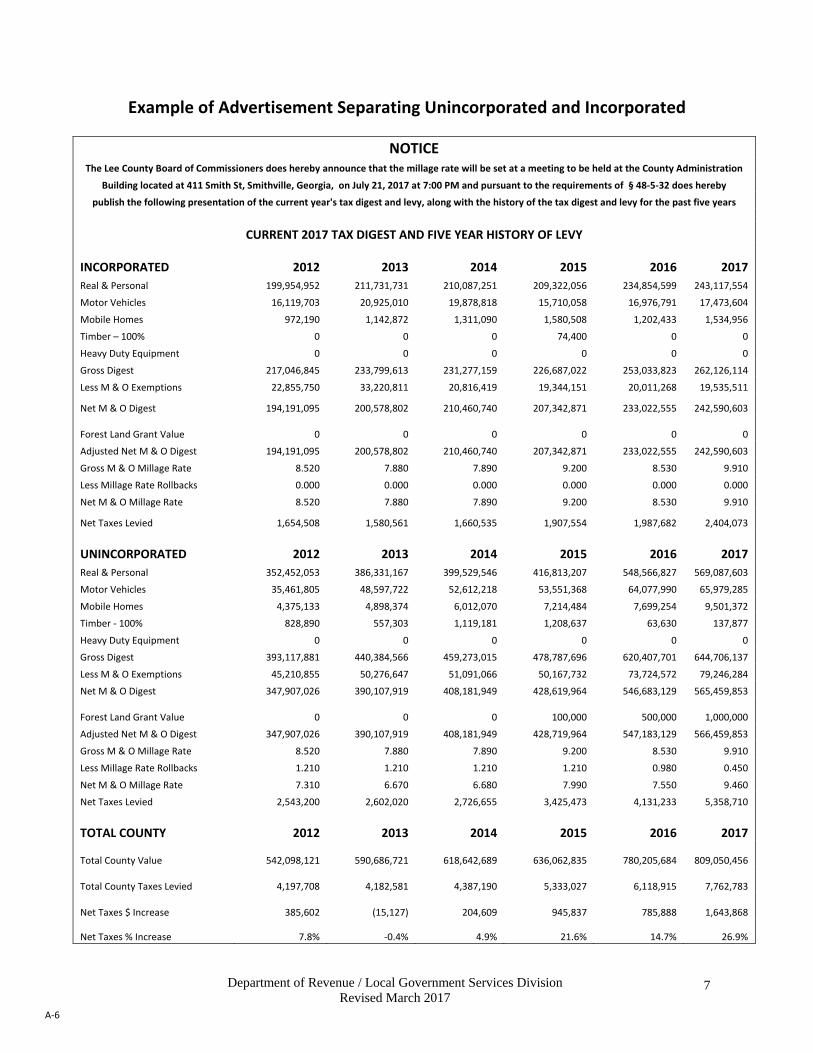

Example of Advertisement Separating Unincorporated and Incorporated

NOTICE The Lee County Board of Commissioners does hereby announce that the millage rate will be set at a meeting to be held at the County Administration

Building located at 411 Smith St, Smithville, Georgia, on July 21, 2017 at 7:00 PM and pursuant to the requirements of § 48-5-32 does hereby

publish the following presentation of the current year's tax digest and levy, along with the history of the tax digest and levy for the past five years

CURRENT 2017 TAX DIGEST AND FIVE YEAR HISTORY OF LEVY

INCORPORATED 2012 2013 2014 2015 2016 2017 Real & Personal 199,954,952 211,731,731 210,087,251 209,322,056 234,854,599 243,117,554

Motor Vehicles 16,119,703 20,925,010 19,878,818 15,710,058 16,976,791 17,473,604

Mobile Homes 972,190 1,142,872 1,311,090 1,580,508 1,202,433 1,534,956

Timber – 100% 0 0 0 74,400 0 0

Heavy Duty Equipment 0 0 0 0 0 0

Gross Digest 217,046,845 233,799,613 231,277,159 226,687,022 253,033,823 262,126,114

Less M & O Exemptions 22,855,750 33,220,811 20,816,419 19,344,151 20,011,268 19,535,511

Net M & O Digest 194,191,095 200,578,802 210,460,740 207,342,871 233,022,555 242,590,603

Forest Land Grant Value 0 0 0 0 0 0

Adjusted Net M & O Digest 194,191,095 200,578,802 210,460,740 207,342,871 233,022,555 242,590,603

Gross M & O Millage Rate 8.520 7.880 7.890 9.200 8.530 9.910

Less Millage Rate Rollbacks 0.000 0.000 0.000 0.000 0.000 0.000

Net M & O Millage Rate 8.520 7.880 7.890 9.200 8.530 9.910

Net Taxes Levied 1,654,508 1,580,561 1,660,535 1,907,554 1,987,682 2,404,073

UNINCORPORATED 2012 2013 2014 2015 2016 2017 Real & Personal 352,452,053 386,331,167 399,529,546 416,813,207 548,566,827 569,087,603

Motor Vehicles 35,461,805 48,597,722 52,612,218 53,551,368 64,077,990 65,979,285

Mobile Homes 4,375,133 4,898,374 6,012,070 7,214,484 7,699,254 9,501,372

Timber - 100% 828,890 557,303 1,119,181 1,208,637 63,630 137,877

Heavy Duty Equipment 0 0 0 0 0 0

Gross Digest 393,117,881 440,384,566 459,273,015 478,787,696 620,407,701 644,706,137

Less M & O Exemptions 45,210,855 50,276,647 51,091,066 50,167,732 73,724,572 79,246,284

Net M & O Digest 347,907,026 390,107,919 408,181,949 428,619,964 546,683,129 565,459,853

Forest Land Grant Value 0 0 0 100,000 500,000 1,000,000

Adjusted Net M & O Digest 347,907,026 390,107,919 408,181,949 428,719,964 547,183,129 566,459,853

Gross M & O Millage Rate 8.520 7.880 7.890 9.200 8.530 9.910

Less Millage Rate Rollbacks 1.210 1.210 1.210 1.210 0.980 0.450

Net M & O Millage Rate 7.310 6.670 6.680 7.990 7.550 9.460

Net Taxes Levied 2,543,200 2,602,020 2,726,655 3,425,473 4,131,233 5,358,710

TOTAL COUNTY 2012 2013 2014 2015 2016 2017

Total County Value 542,098,121 590,686,721 618,642,689 636,062,835 780,205,684 809,050,456

Total County Taxes Levied 4,197,708 4,182,581 4,387,190 5,333,027 6,118,915 7,762,783

Net Taxes $ Increase 385,602 (15,127) 204,609 945,837 785,888 1,643,868

Net Taxes % Increase 7.8% -0.4% 4.9% 21.6% 14.7% 26.9%

A-6

Department of Revenue / Local Government Services Division Revised March 2017

8

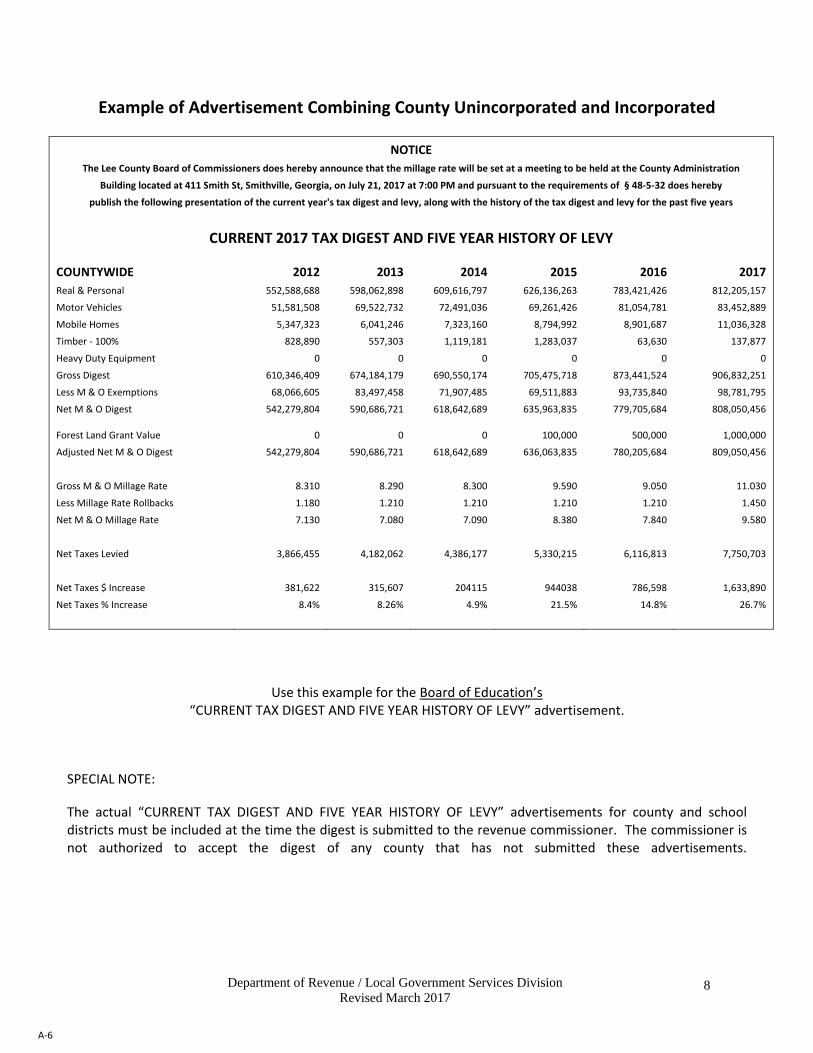

Example of Advertisement Combining County Unincorporated and Incorporated

NOTICE The Lee County Board of Commissioners does hereby announce that the millage rate will be set at a meeting to be held at the County Administration

Building located at 411 Smith St, Smithville, Georgia, on July 21, 2017 at 7:00 PM and pursuant to the requirements of § 48-5-32 does hereby

publish the following presentation of the current year's tax digest and levy, along with the history of the tax digest and levy for the past five years

CURRENT 2017 TAX DIGEST AND FIVE YEAR HISTORY OF LEVY

COUNTYWIDE 2012 2013 2014 2015 2016 2017 Real & Personal 552,588,688 598,062,898 609,616,797 626,136,263 783,421,426 812,205,157

Motor Vehicles 51,581,508 69,522,732 72,491,036 69,261,426 81,054,781 83,452,889

Mobile Homes 5,347,323 6,041,246 7,323,160 8,794,992 8,901,687 11,036,328

Timber - 100% 828,890 557,303 1,119,181 1,283,037 63,630 137,877

Heavy Duty Equipment 0 0 0 0 0 0

Gross Digest 610,346,409 674,184,179 690,550,174 705,475,718 873,441,524 906,832,251

Less M & O Exemptions 68,066,605 83,497,458 71,907,485 69,511,883 93,735,840 98,781,795

Net M & O Digest 542,279,804 590,686,721 618,642,689 635,963,835 779,705,684 808,050,456

Forest Land Grant Value 0 0 0 100,000 500,000 1,000,000

Adjusted Net M & O Digest 542,279,804 590,686,721 618,642,689 636,063,835 780,205,684 809,050,456

Gross M & O Millage Rate 8.310 8.290 8.300 9.590 9.050 11.030

Less Millage Rate Rollbacks 1.180 1.210 1.210 1.210 1.210 1.450

Net M & O Millage Rate 7.130 7.080 7.090 8.380 7.840 9.580

Net Taxes Levied 3,866,455 4,182,062 4,386,177 5,330,215 6,116,813 7,750,703

Net Taxes $ Increase 381,622 315,607 204115 944038 786,598 1,633,890

Net Taxes % Increase 8.4% 8.26% 4.9% 21.5% 14.8% 26.7%

Use this example for the Board of Education’s “CURRENT TAX DIGEST AND FIVE YEAR HISTORY OF LEVY” advertisement.

SPECIAL NOTE:

The actual “CURRENT TAX DIGEST AND FIVE YEAR HISTORY OF LEVY” advertisements for county and school districts must be included at the time the digest is submitted to the revenue commissioner. The commissioner is not authorized to accept the digest of any county that has not submitted these advertisements.

A-6

City of _______________ State of Georgia

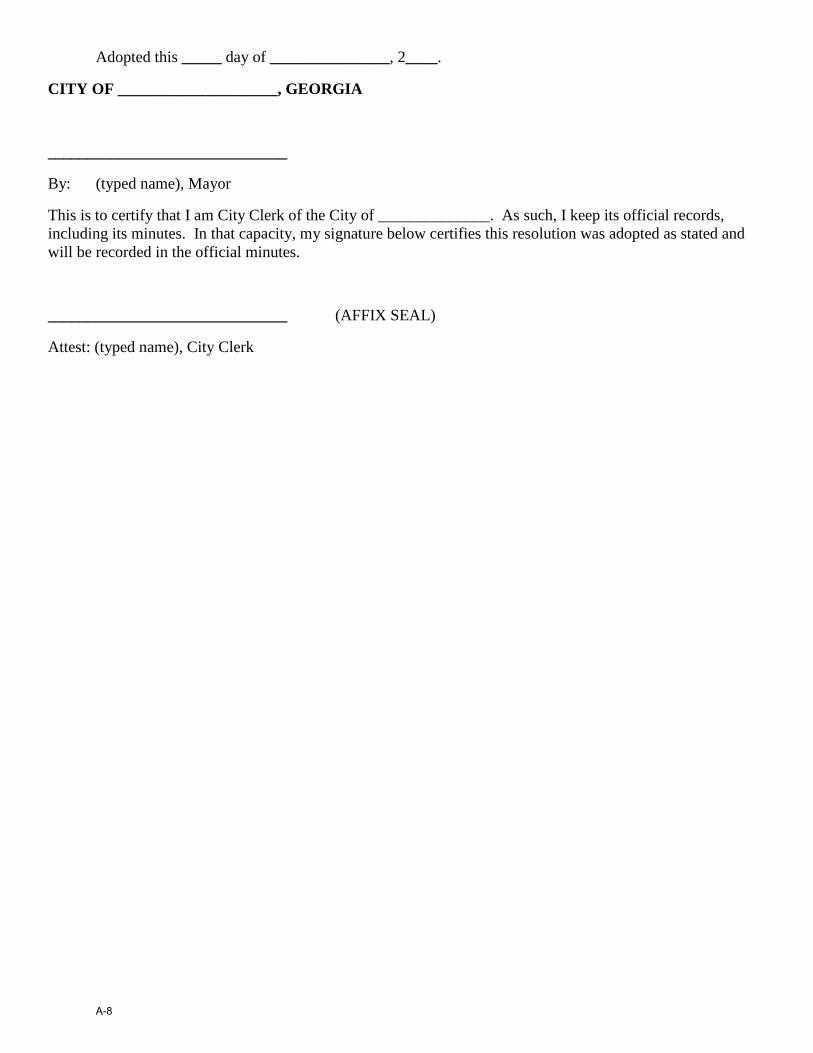

A RESOLUTION

TO ADOPT THE FISCAL YEAR 20___ BUDGET FOR EACH FUND OF THE CITY OF ________________, GEORGIA, APPROPRIATING THE AMOUNTS SHOWN IN EACH BUDGET AS

EXPENDITURES/EXPENSES, ADOPTING THE SEVERAL ITEMS OF REVENUE ANTICIPATIONS, AND PROHIBITING EXPENDITURES OR EXPENSES FROM EXCEEDING

THE ACTUAL FUNDING AVAILABLE

WHEREAS, sound governmental operations require a budget in order to plan the financing of services for the residents of the City of _________________; and

WHEREAS, Title 36, Chapter 81, Article 3 of the Official Code of Georgia Annotated (OCGA) requires a balanced budget for the City’s fiscal year, which runs from _______________ to _______________ of each year; and

WHEREAS, the Mayor and City Council of the City of _____________________ have reviewed the proposed FY ________ budget as presented by the City Manager; and

WHEREAS, advertised public hearing has been held on the _________ proposed budget, as required by State and Local Laws and regulations; and

WHEREAS, each of these funds has a balanced budget, such that anticipated funding sources equal proposed expenditures or expenses; and

WHEREAS, the Mayor and City Council wishes to adopt this proposal as the Fiscal Year ________ Annual Budget, effective from _______________ through _________________.

NOW THEREFORE BE IT RESOLVED by the Mayor and City Council of the City of ______________, Georgia, as follows:

Section 1. That the proposed Fiscal Year _____ Budget, attached hereto and incorporated herein as a part of this Resolution is hereby adopted as the Budget for the City of ______________________, Georgia for Fiscal Year _________, which begins ________ and ends on _________________.

Section 2. That the several items of revenues, other financial resources, and sources of cash shown in the budget for each fund in the amounts shown anticipated are hereby adopted, and that the several amounts shown in the budget for each fund as proposed expenditures or expenses, and uses of cash are hereby appropriated to the departments named in each fund.

Section 3. That the “legal level of control” as defined in OCGA §36-81-2 is set at the departmental level, meaning that the City Manager in his capacity as Budget Officer is authorized to move appropriations from one line item to another within a department, but under no circumstances may expenditures or expenses exceed the amount appropriated for a department without a further budget amendment approved by the Mayor and City Council.

Section 4. That all appropriations shall lapse at the end of the fiscal year.

Section 5. That this Resolution shall be and remain in full force and effect from and after its date of adoption.

A-7

Adopted this _____ day of _______________, 2____.

CITY OF ____________________, GEORGIA

______________________________

By: (typed name), Mayor

This is to certify that I am City Clerk of the City of ______________. As such, I keep its official records, including its minutes. In that capacity, my signature below certifies this resolution was adopted as stated and will be recorded in the official minutes.

______________________________ (AFFIX SEAL)

Attest: (typed name), City Clerk

A-8

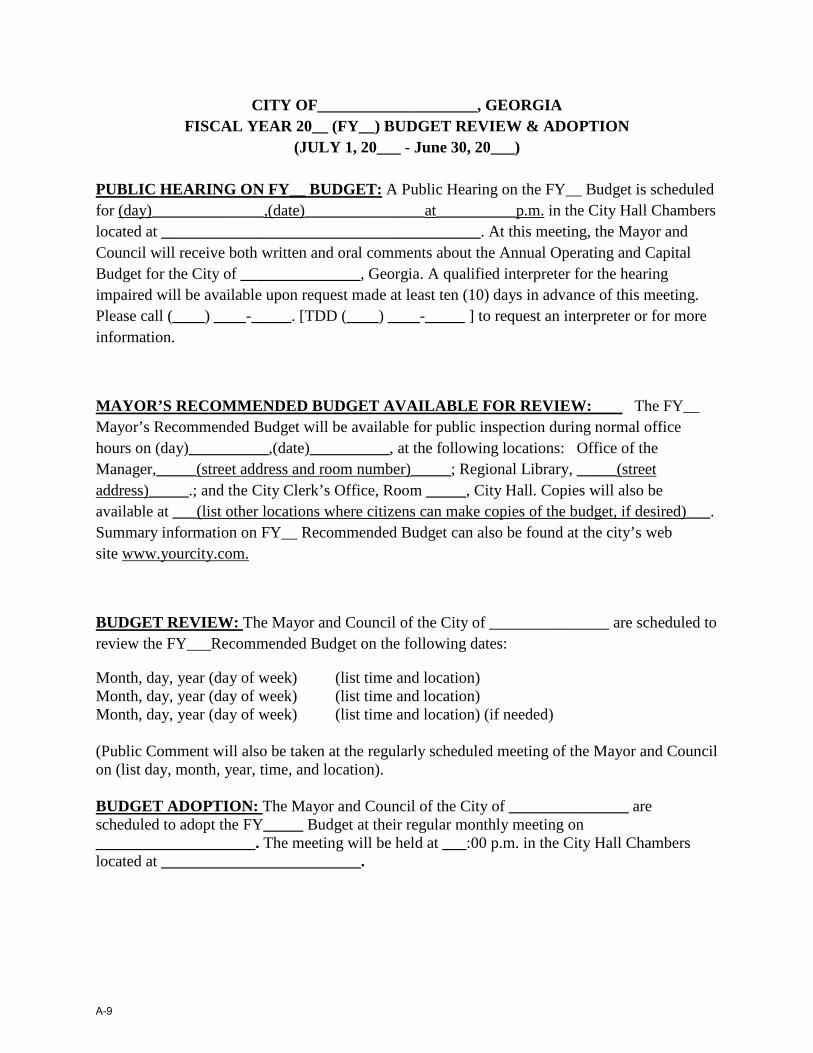

CITY OF____________________, GEORGIA FISCAL YEAR 20__ (FY__) BUDGET REVIEW & ADOPTION

(JULY 1, 20___ - June 30, 20___)

PUBLIC HEARING ON FY__ BUDGET: A Public Hearing on the FY__ Budget is scheduled for (day)______________,(date)_______________at__________p.m. in the City Hall Chambers located at ________________________________________. At this meeting, the Mayor and Council will receive both written and oral comments about the Annual Operating and Capital Budget for the City of _______________, Georgia. A qualified interpreter for the hearing impaired will be available upon request made at least ten (10) days in advance of this meeting. Please call (____) ____-_____. [TDD (____) ____-_____ ] to request an interpreter or for more information.

MAYOR’S RECOMMENDED BUDGET AVAILABLE FOR REVIEW: The FY__ Mayor’s Recommended Budget will be available for public inspection during normal office hours on (day)__________,(date)__________, at the following locations: Office of the Manager,_____(street address and room number)_____; Regional Library, _____(street address)_____.; and the City Clerk’s Office, Room _____, City Hall. Copies will also be available at ___(list other locations where citizens can make copies of the budget, if desired)___. Summary information on FY__ Recommended Budget can also be found at the city’s web site www.yourcity.com.

BUDGET REVIEW: The Mayor and Council of the City of _______________ are scheduled to review the FY___Recommended Budget on the following dates:

Month, day, year (day of week) (list time and location) Month, day, year (day of week) (list time and location) Month, day, year (day of week) (list time and location) (if needed)

(Public Comment will also be taken at the regularly scheduled meeting of the Mayor and Council on (list day, month, year, time, and location).

BUDGET ADOPTION: The Mayor and Council of the City of _______________ are scheduled to adopt the FY_____ Budget at their regular monthly meeting on ____________________. The meeting will be held at ___:00 p.m. in the City Hall Chambers located at _________________________.

A-9

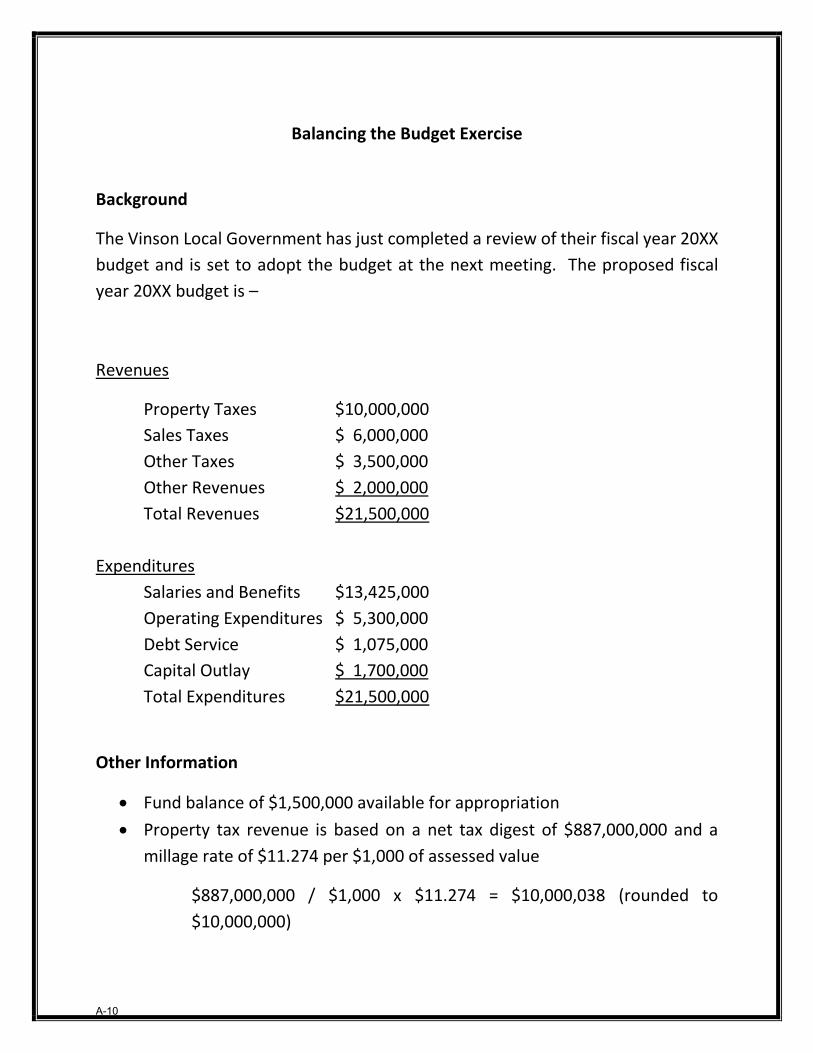

Balancing the Budget Exercise

Background

The Vinson Local Government has just completed a review of their fiscal year 20XX budget and is set to adopt the budget at the next meeting. The proposed fiscal year 20XX budget is –

Revenues

Property Taxes $10,000,000 Sales Taxes $ 6,000,000 Other Taxes $ 3,500,000 Other Revenues $ 2,000,000 Total Revenues $21,500,000

Expenditures Salaries and Benefits $13,425,000 Operating Expenditures $ 5,300,000 Debt Service $ 1,075,000 Capital Outlay $ 1,700,000 Total Expenditures $21,500,000

Other Information

• Fund balance of $1,500,000 available for appropriation• Property tax revenue is based on a net tax digest of $887,000,000 and a

millage rate of $11.274 per $1,000 of assessed value

$887,000,000 / $1,000 x $11.274 = $10,000,038 (rounded to $10,000,000)

A-10

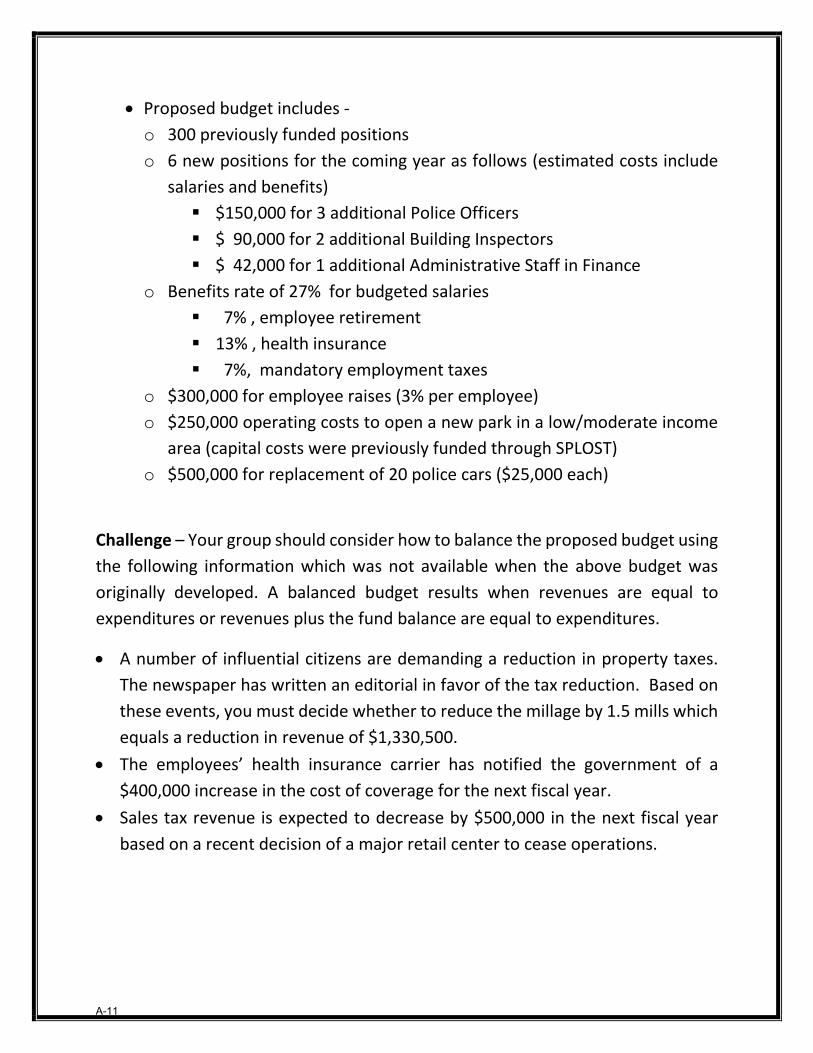

• Proposed budget includes -o 300 previously funded positionso 6 new positions for the coming year as follows (estimated costs include

salaries and benefits) $150,000 for 3 additional Police Officers $ 90,000 for 2 additional Building Inspectors $ 42,000 for 1 additional Administrative Staff in Finance

o Benefits rate of 27% for budgeted salaries 7% , employee retirement 13% , health insurance 7%, mandatory employment taxes

o $300,000 for employee raises (3% per employee)o $250,000 operating costs to open a new park in a low/moderate income

area (capital costs were previously funded through SPLOST)o $500,000 for replacement of 20 police cars ($25,000 each)

Challenge – Your group should consider how to balance the proposed budget using the following information which was not available when the above budget was originally developed. A balanced budget results when revenues are equal to expenditures or revenues plus the fund balance are equal to expenditures.

• A number of influential citizens are demanding a reduction in property taxes.The newspaper has written an editorial in favor of the tax reduction. Based onthese events, you must decide whether to reduce the millage by 1.5 mills whichequals a reduction in revenue of $1,330,500.

• The employees’ health insurance carrier has notified the government of a$400,000 increase in the cost of coverage for the next fiscal year.

• Sales tax revenue is expected to decrease by $500,000 in the next fiscal yearbased on a recent decision of a major retail center to cease operations.

A-11

Questions

1. What changes would you recommend implementing based on theinformation provided?

2. What are the advantages and disadvantages of each of your responses?

A-12

![WELCOME [cviog.uga.edu]](https://img.pdfslide.us/doc/110x75/626245ac7b1f1f7562200810/welcome-cviogugaedu.jpg)