Embed Size (px)

DESCRIPTION

Finance

Citation preview

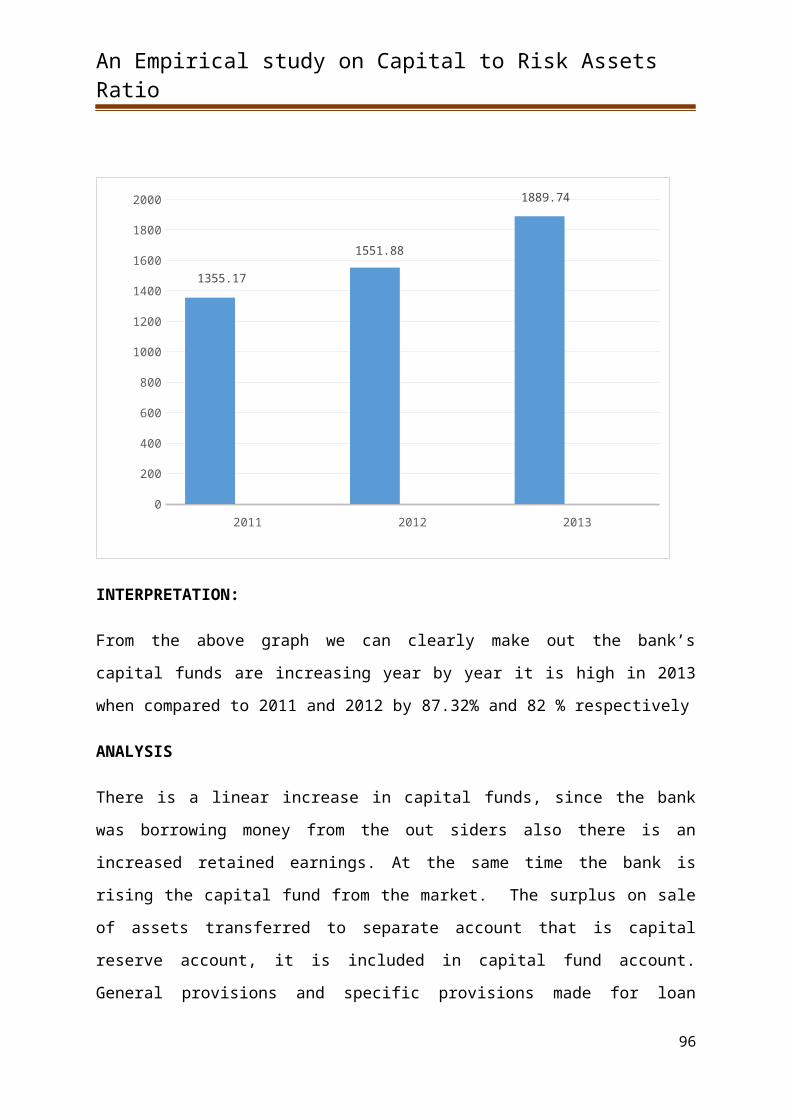

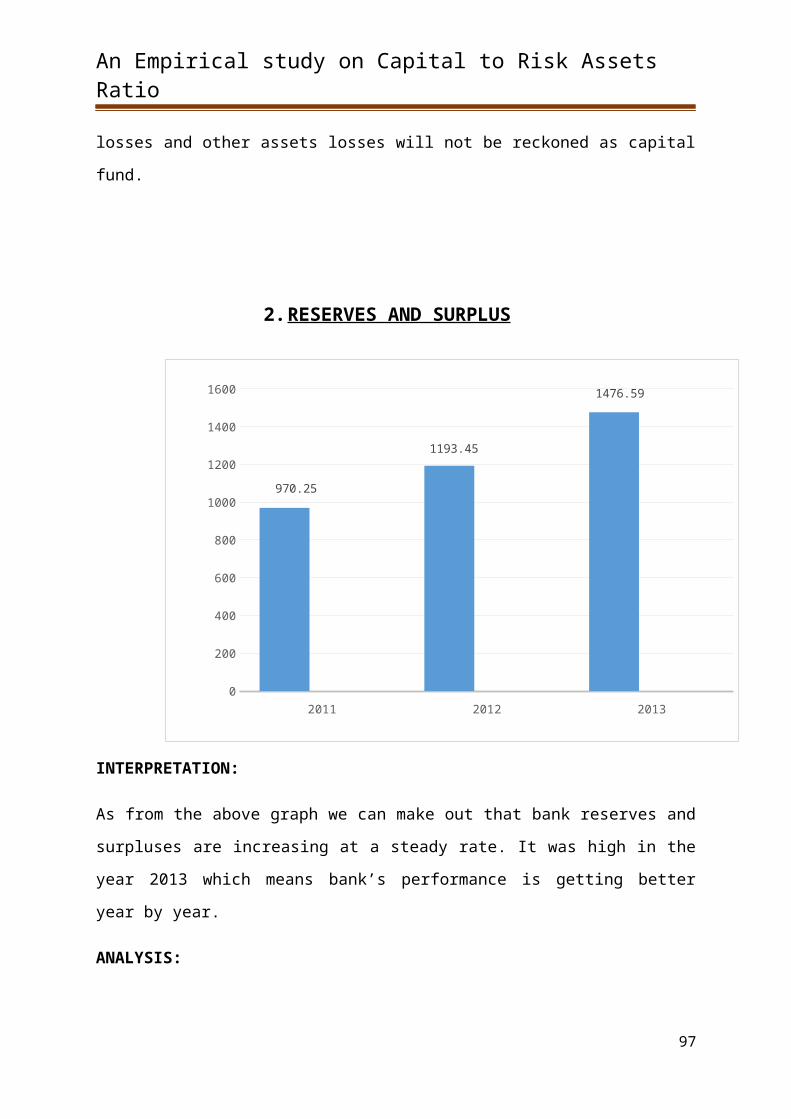

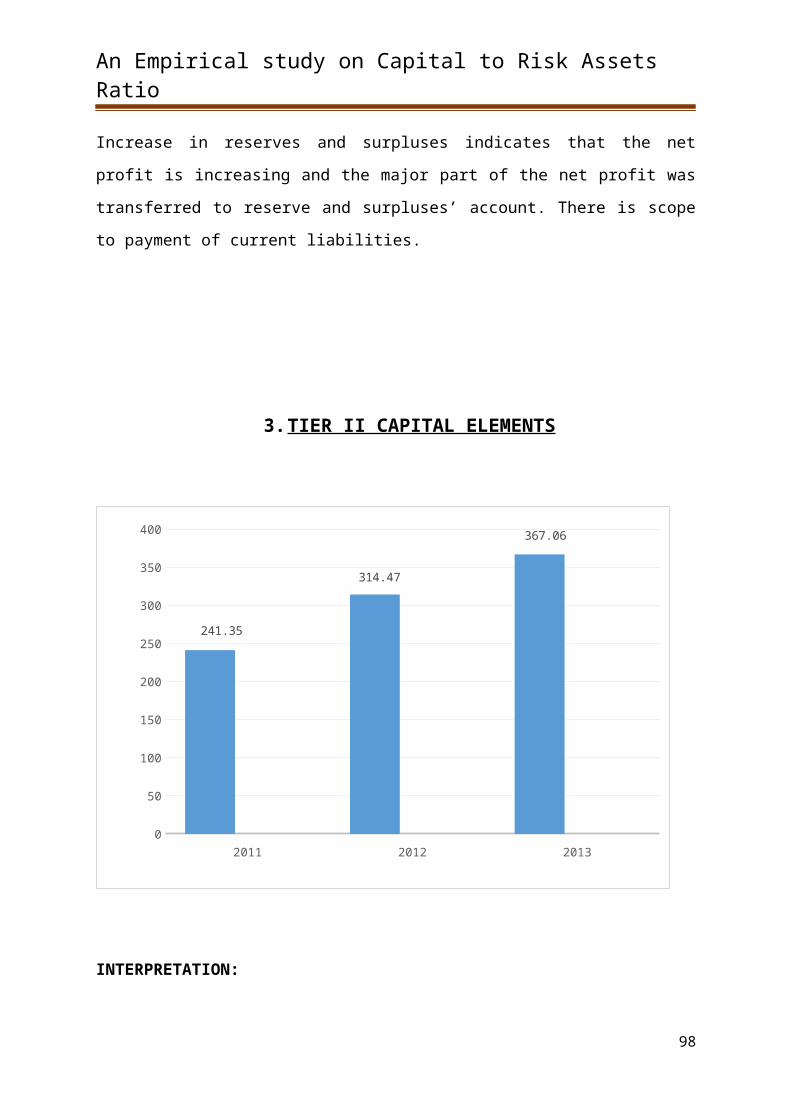

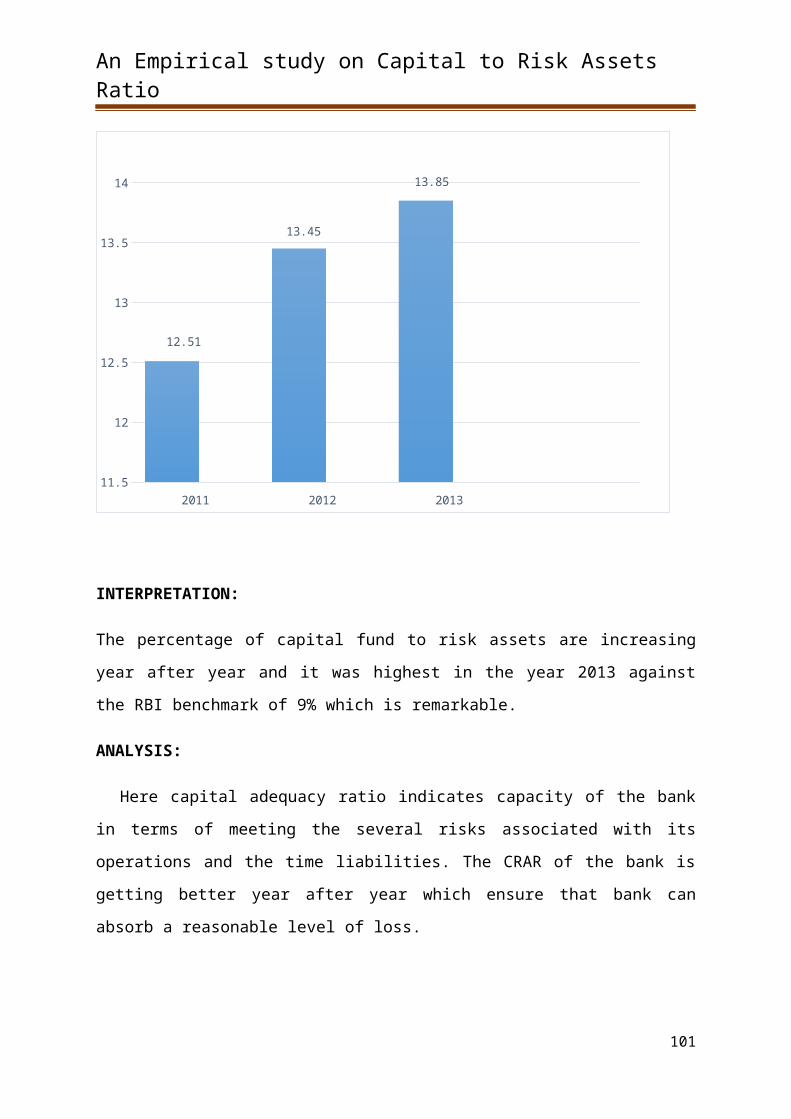

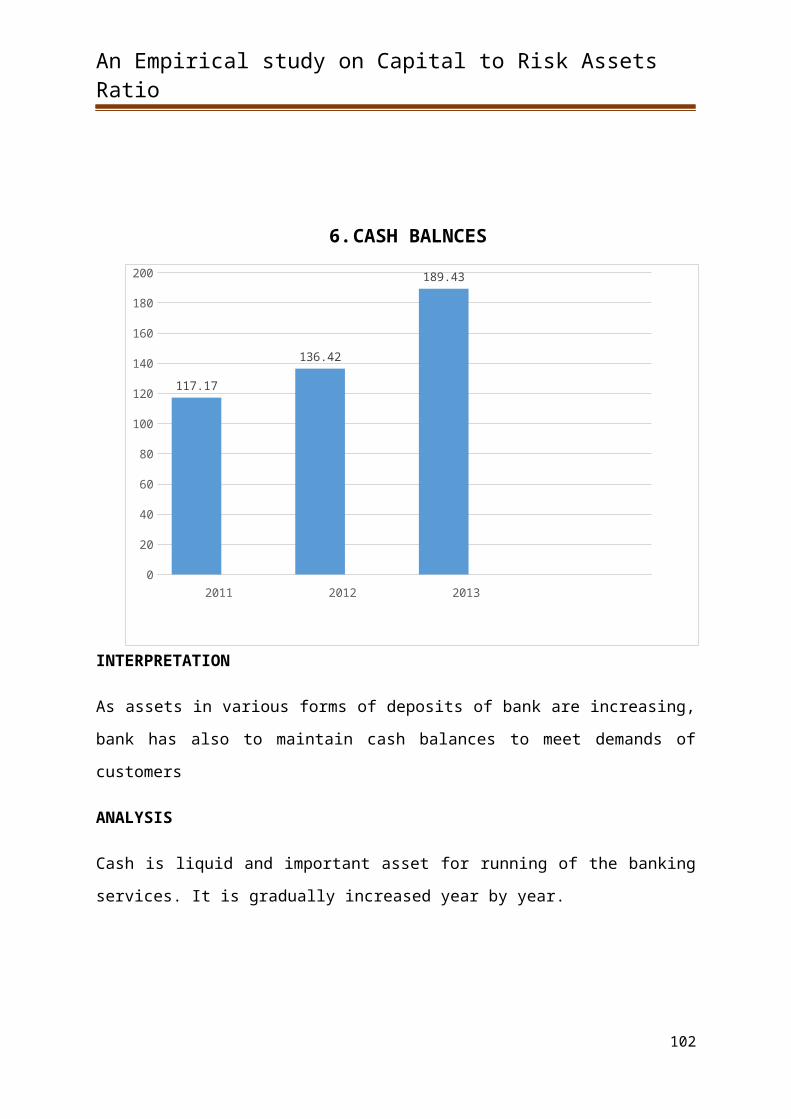

An Empirical study on Capital to Risk Assets Ratio

CHAPTER-1

INTRODUCTION1.1 Introduction about the internship:“Internships give students their first exposure to working in an organization and also a flavor

of the functional area they are interested in pursuing later in their careers. Internships present

a great way for companies to evaluate potential permanent hires. Interns can boost company

productivity and provide much needed support on special projects. In addition, when interns

are pleased with their internship experience, they add to a company's campus presence and

act as company emissaries. Internship program helps in experiential learning for a student in

an organizational environment which serves his academic requirements and also provides

valuable hands-on experience in a chosen area of interest. Internships are focused on what a

student learns, not what the student does. Faculty and Company supervised Internships for a

specified period of time with a focus on learning executive skills attempt to bridge the gap

between theoretical learning in the classroom and company practices. Value addition through

internships includes the following:

1. A good performance in internship fetches higher academic credentials,

particularly for those who are practice oriented

2. A good platform to reflect on theories and concepts learnt in the classroom to

observe and apply in real life situations. It reinforces the classroom learning

through practice.

3. . Provides first-hand experience into company environment, business

processes and markets.

4. Successful internships build self-confidence of students and enhance their self-

esteem. It helps in behavioural modifications and emotional balance. Students

learn to be independent and responsible.

5. Students gain new skills – cognitive, emotional and social. Learn corporate

etiquettes, understand corporate culture – all through own experiences and

observations.

6. Leads to self-discovery of strengths and weaknesses while facing the

challenges on-the-job. This coupled with coaching and mentoring by faculty

members and company executives would shape up the future manager

1

An Empirical study on Capital to Risk Assets Ratio

7. Intern gets a chance to network with executives in a company who can help in

paving the way for future opportunities

Internships give a feel of career opportunities and lay the foundation for

career planning.

8. The power of internships is that they mould the business school students into

an effective manager.

1.2 Topic chosen for study The title of the study is “An EMPIRICAL STUDY ON CAPITAL TO RISK ASSETS

RATIO” of urban co-operative bank ltd Perinthalmanna”

A bank’s real capital worth is evaluated after taking into account

the riskiness of its assets. It was earlier hoped that the capital would provide banks with a

comfortable cushion against insolvency, thereby ensuring market stability. In the wake of the

introduction of prudential regulation as an integral part of financial sector reforms in India,

there has been a growing debate as to whether capital adequacy requirements are the best

means to regulate the banking system.

1.3 Need of the study:Banks face high risks primarily because banking is one of the most highly

leveraged sectors of any economy. To tackle risk and function efficiently, there is a need to

manage all kinds of risk associated with banking. Thus, risk management is core to any banks

face high risks primarily because banking is one of the most highly leveraged sectors of any

economy. To tackle risk and function efficiently, there is a need to manage all kinds of risk

associated with banking. Thus, risk management is core to any bank. The study of CRAR

analysis of UCBP ltd will enable as to know the financial position, of UCBP ltd. The study

also reveals the performance of the UCBP ltd and also its prospects.

2

An Empirical study on Capital to Risk Assets Ratio

1.4 Objectives of the study:The main objectives of the research are as following:

To explain the importance of risk assets ratio to analyze the performance of the firm.

To analyze the current financial condition of the firm.

To compare the present ratios with past ratios of the firm.

To interpret the ratios to identify the strengths and weakness of the organization.

To measure the adequacy of an entities capital resources in relation to its current

liabilities and also in relation to the risk associated with its assets.

To strengthen the soundness and stability of the banking system.

1.5 SCOPE OF THE STUDY The scope is limited to published information received from annual reports.

The study covers P&L a/c and balance sheet items only.

The study covers a period of three financial years ranging from 2010-11 to 2012-13.

This is so because CRAR prescribes practical standards, for each element of the

study.

1.6 METHODOLOGY ADOPTED There are two types of data collection method which are being used in this research:

PRIMARY DATA

SECONDARY DATA

1. Collection of Primary data:

Primary data is that type of data which includes the first hand information which is

being collected during the course of training through observations and discussion with

departmental heads, accountants, assistants and office.

Direct interaction

Observations

2. Collection of Secondary Data:

Secondary data means data that are already available i.e., they refer to the data which

have already been collected and analyzed by someone else. When the researcher utilizes the

secondary data, then he has to look into various sources from where he can obtain them. In

this case he is certainly not confronted with the problems are usually associated with the

3

An Empirical study on Capital to Risk Assets Ratio

collection of the original data secondary data may either be published data or unpublished

data.

Here in this research, I collected the secondary data from the following

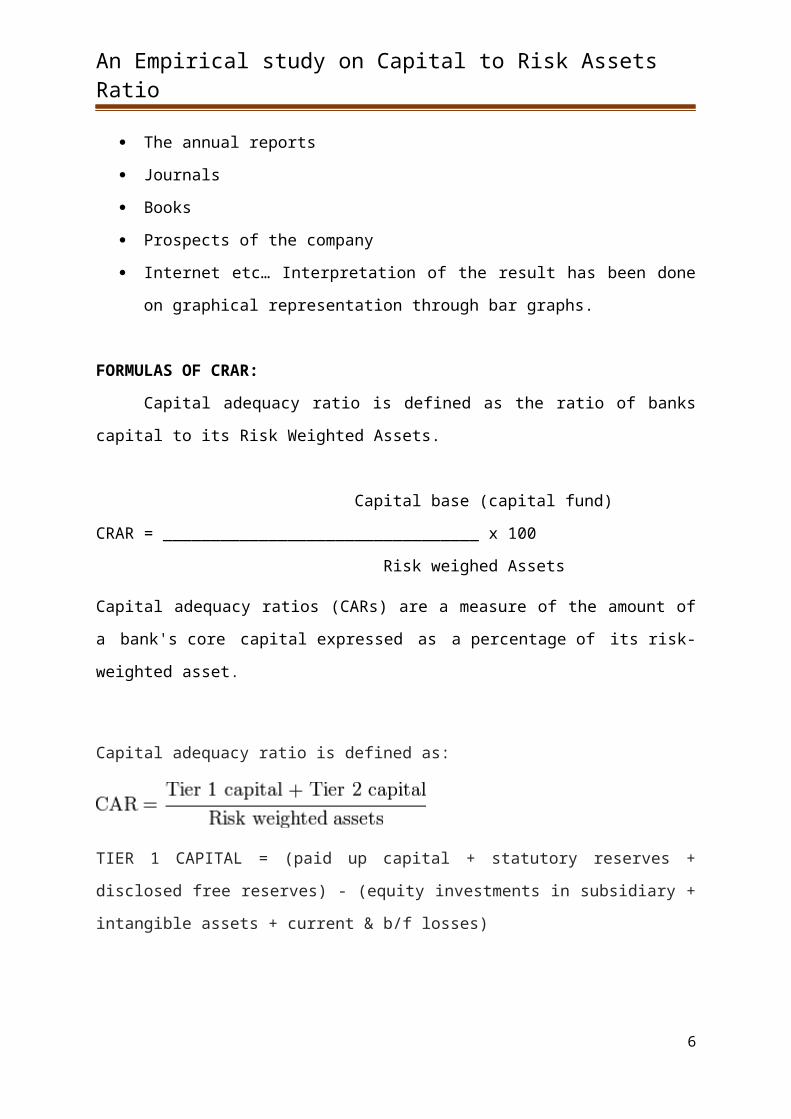

The annual reports

Journals

Books

Prospects of the company

Internet etc… Interpretation of the result has been done on graphical representation

through bar graphs.

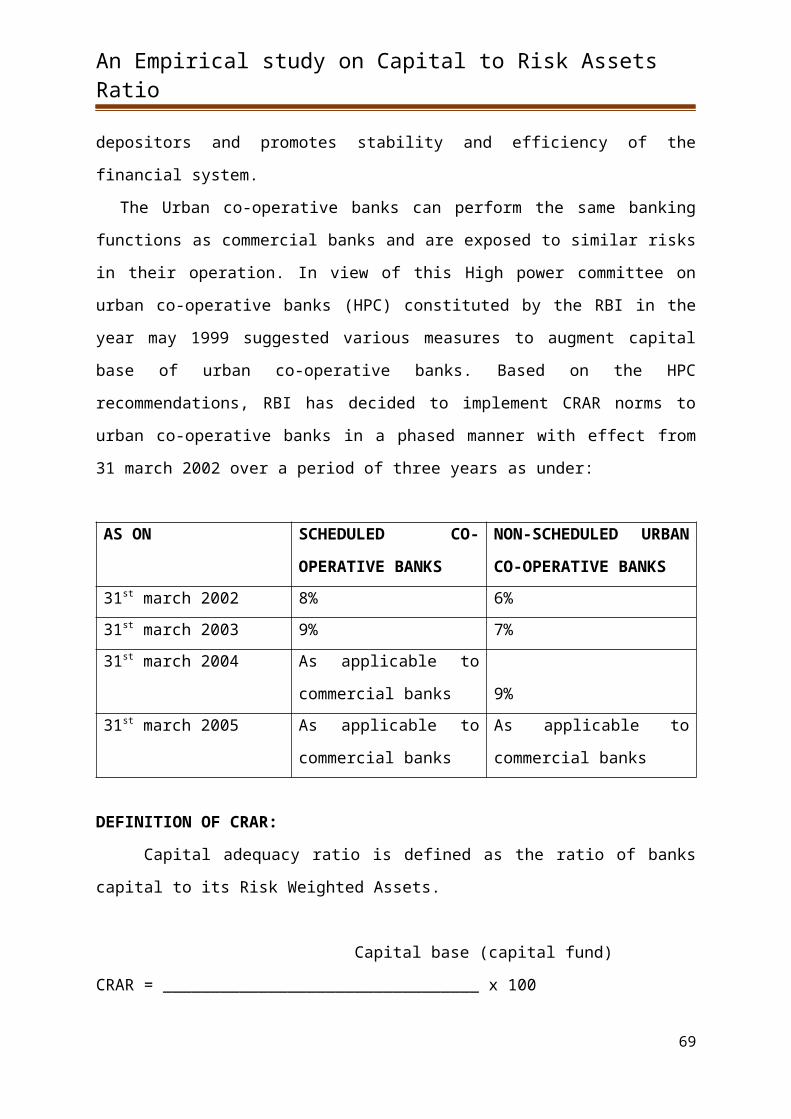

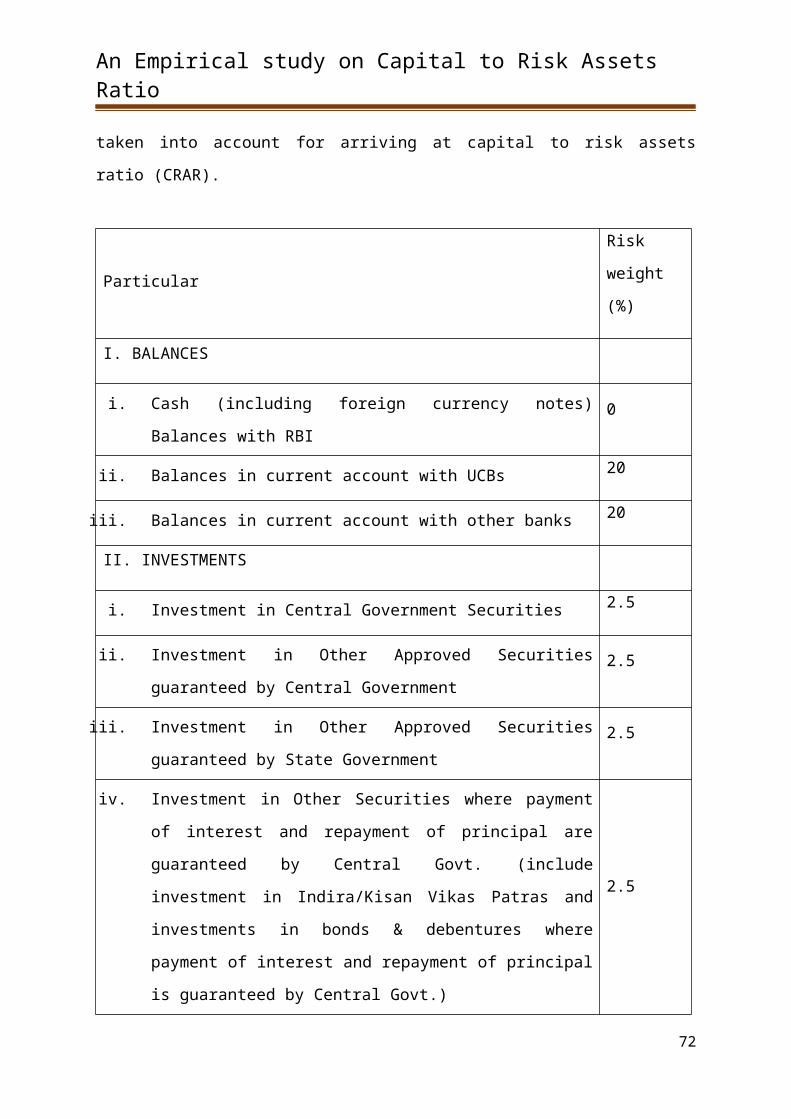

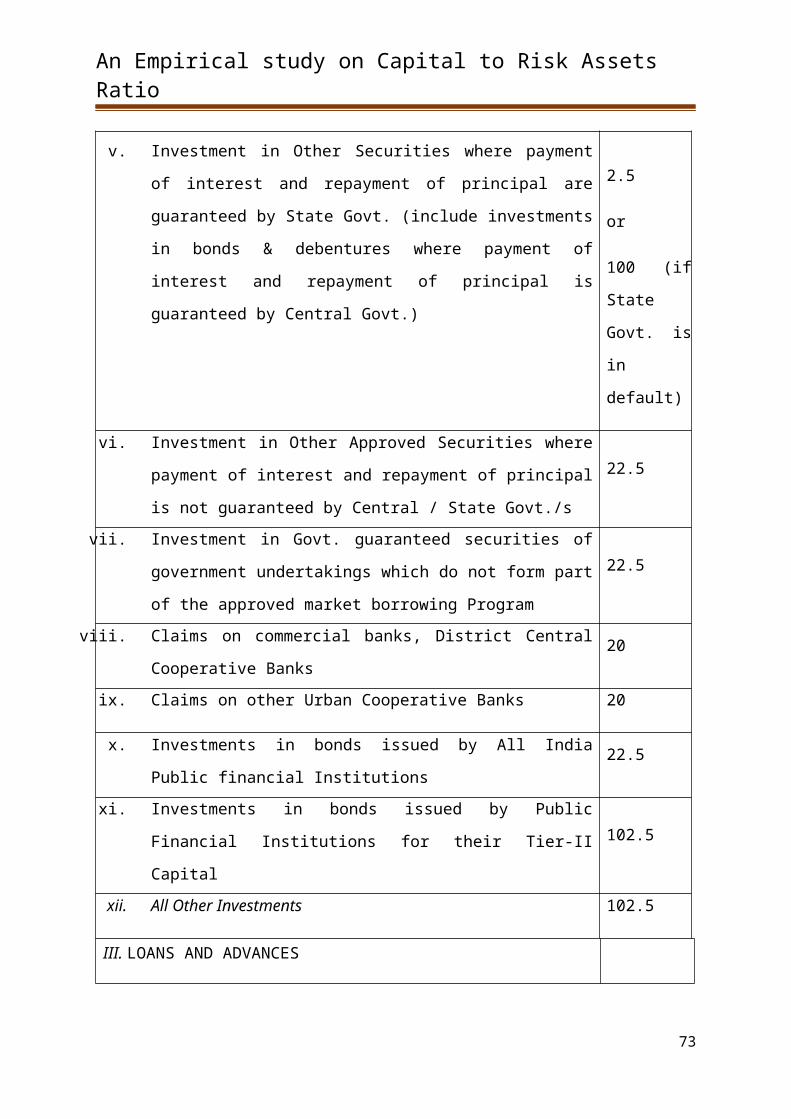

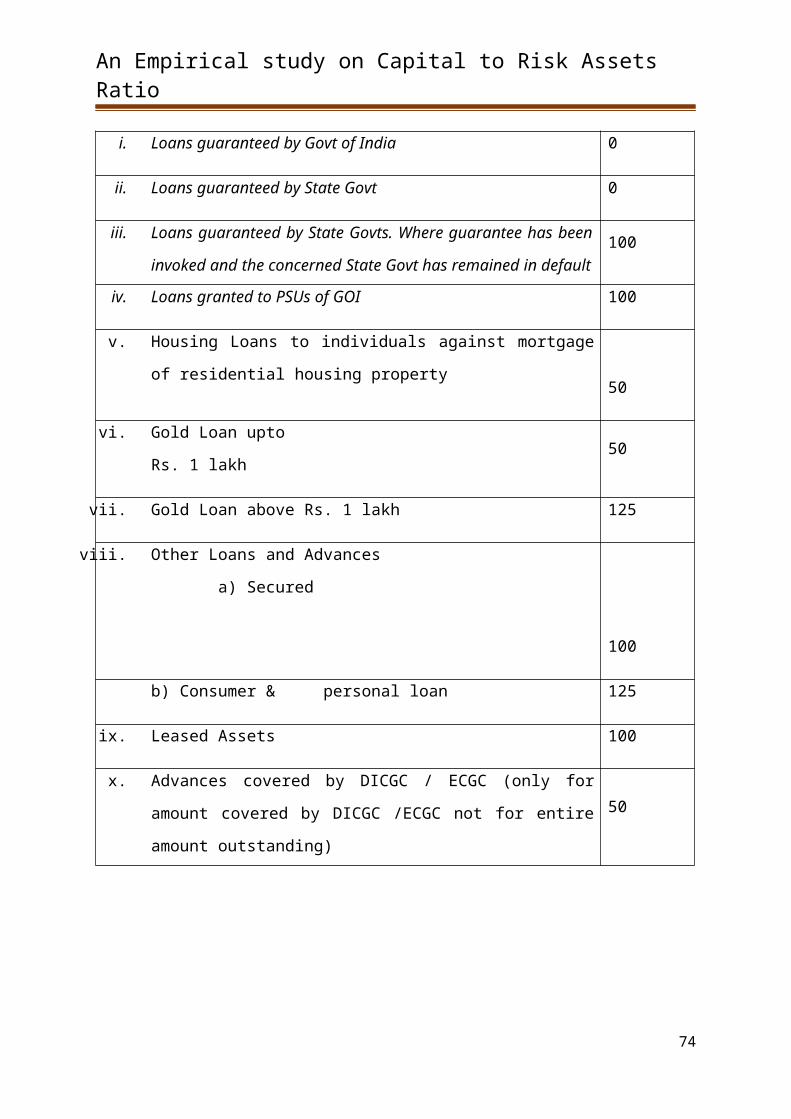

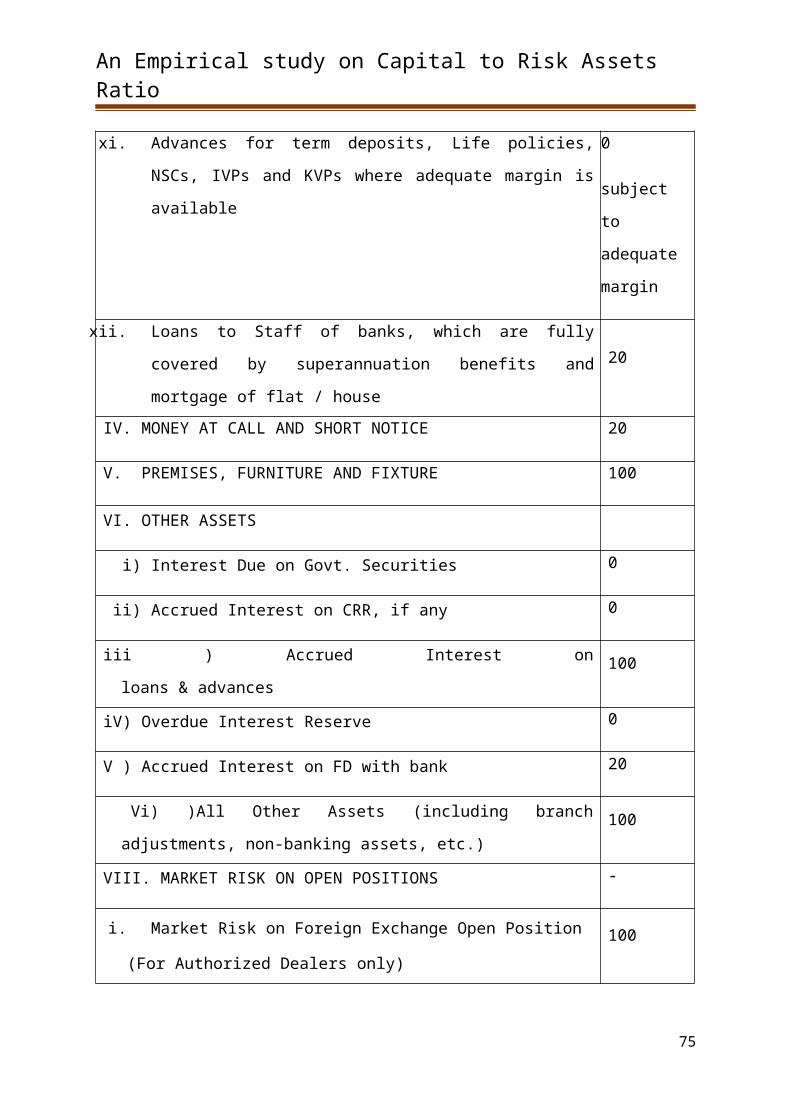

FORMULAS OF CRAR:

Capital adequacy ratio is defined as the ratio of banks capital to its Risk Weighted

Assets.

Capital base (capital fund)

CRAR = _________________________________ x 100

Risk weighed Assets

Capital adequacy ratios (CARs) are a measure of the amount of a bank's core

capital expressed as a percentage of its risk-weighted asset.

Capital adequacy ratio is defined as:

TIER 1 CAPITAL = (paid up capital + statutory reserves + disclosed free reserves) - (equity

investments in subsidiary + intangible assets + current & b/f losses)

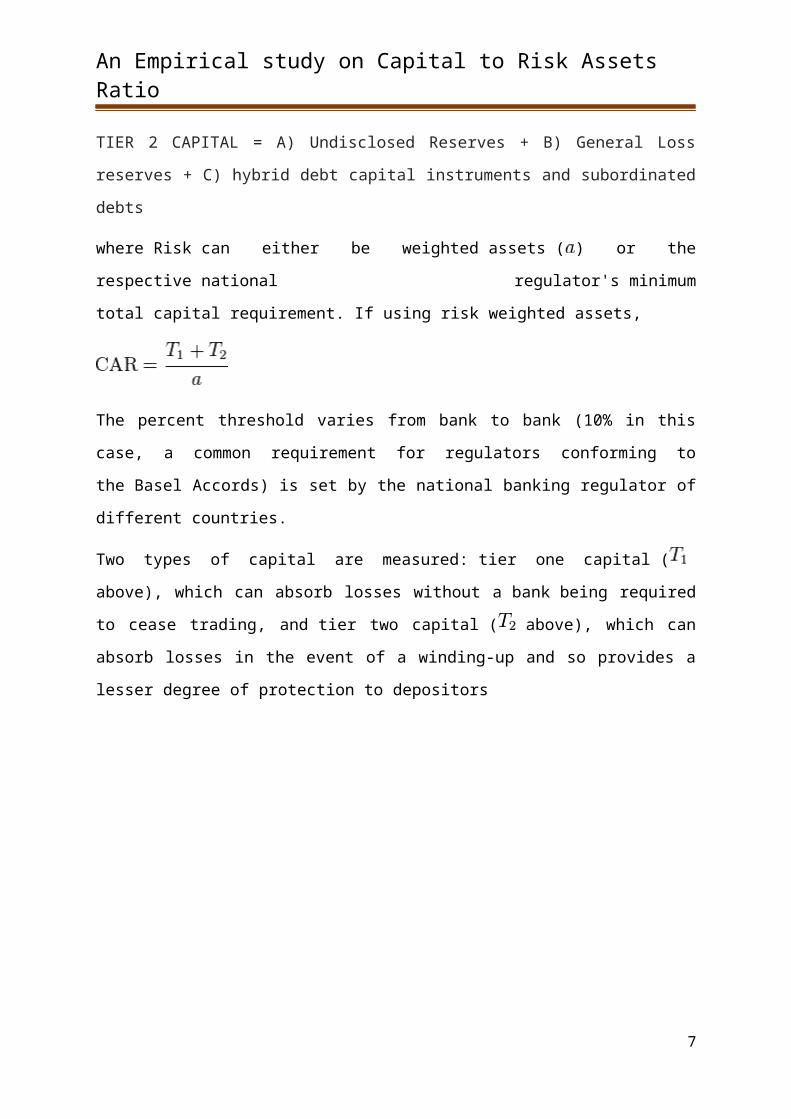

TIER 2 CAPITAL = A) Undisclosed Reserves + B) General Loss reserves + C) hybrid debt

capital instruments and subordinated debts

where Risk can either be weighted assets ( ) or the respective national regulator's minimum

total capital requirement. If using risk weighted assets,

4

An Empirical study on Capital to Risk Assets Ratio

The percent threshold varies from bank to bank (10% in this case, a common requirement for

regulators conforming to the Basel Accords) is set by the national banking regulator of

different countries.

Two types of capital are measured: tier one capital ( above), which can absorb losses

without a bank being required to cease trading, and tier two capital ( above), which can

absorb losses in the event of a winding-up and so provides a lesser degree of protection to

depositors

5

An Empirical study on Capital to Risk Assets Ratio

1.7 LITERATURE REVIEW

Alfriend (1988) pointed out that a weakness of the minimum capital standards was

that they failed to acknowledge the heterogeneity of bank assets and, as a result, banks had an

incentive to shift their portfolios from low-risk to high-risk assets. Jackson (1999) points out

that one of the reasons why the Basel Committee adopted a single standard for internationally

active banks is that the framework would strengthen the soundness and stability of the

international banking system by encouraging organizations to boost their capital positions.

Moreover, the framework established a structure that was intended to: (1) make regulatory

capital more sensitive to differences in risk profiles among banking organization 2) Take off

balacesheet explosure expicity in to account in assessing capital adequacy (3) lower the

disincentives to holding liquid, low risk assets. Nachane et al (2000) examined the impact of

capital adequacy norms on public sector banks in India for the period 1997 to 1999 and

concluded that capital remains a useful tool in the hands of policy makers for influencing the

banks’ behaviour and there is no conclusive evidence

to support a shift from high risk to low risk assets by banksNag and Das (2002) studied the

impact of capital requirement norms on flow of credit to the business sector by public sector

banks in India and found that in the post reform period, public sector banks did shift their

portfolio in a way that reduced their capital requirements. Rowe (2004) notes that the first

pillar defines the minimum regulatory capital for three different risk categories. Apart from

credit risk and market risk, it prescribes a capital requirement for operational risk as well.

Hall (2004) states that disclosure of risk-based capital ratios calculated are in accordance with

the prescribed methodology and qualitative disclosure about the internal processes are used to

evaluate capital adequacy. Mishra (2004)Opines that the new framework seeks to ensure that

a bank's capital position is consistent with its overall risk profile and strategy. Since the new

norms stress the need for the bank management to evolve an internal capital assessment

process and earmark capital commensurate with the bank's specific risk profile and control

environment, a supervisory review to validate such assessment is recommended as a

corollary. Rao (2004) views that Basel I norms aim at ensuring capital adequacy of banks as a

proportion of the risk-weighted assets. Vyas et al (2007) studied the impact of capital

regulation norms like Basel II on the credit growth of Indian banks and concluded that capital

regulations

6

An Empirical study on Capital to Risk Assets Ratio

do not seem to affect credit growth in spite of the growing concerns about banks’ stability.

Murali and Subbakrishna (2008) are of the view that the twin objectives of the accord were to

ensure an adequate level of capital in the international banking system and create a “more

level playing field” in competitive terms so that banks could no longer build business

volumes without adequate capital backing. Radhakrishnan and Ravi (2009) state that capital

requirements not only protect investors but also safeguard them against the possibility of

failure of big banks. They also improve market discipline. Gupta and Meera (2011) feel that

Basel II regulations have led to a significant improvement in the risk structure of banks

because their capital adequacy has improved. Also, there exists an inverse relation between

CAR and Non-Performing Assets (NPAs), which clearly indicates that due to capital

regulation, banks have to increase their CAR which leads to decrease in NPAs.

1.8 Limitations of the study:

The study was limited to finding the selected ratios only.

The study depends on the published data and documents such as balance sheet and

income statements.

It was difficult to obtain confidential data from the concern department with a view

point of confidentiality.

The time period of the project is restricted for short period.

7

An Empirical study on Capital to Risk Assets Ratio

Chapter- 2 INDUSTRY PROFILE

Urban co-operative banks have in the product category of banks. The term urban co-

operative banks (UCBs) though not formally defined, refers to primary co-operative banks

located in urban and semi urban areas. These banks till 1996, were allowed to lend money

only for non-agricultural purposes. This distinction does not hold today. These banks were

traditionally centered on communities, localities work place groups. They essentially sent to

small borrowers and businesses. Today their scope of operations has widened considerably.

The urban co-operative banks using the authorized capital of rupees thousand three

hundred and ninety five cores a class shares of rupees twenty five each. They received the

incomes of interest on deposits, borrowings, salaries, allowances and provident funds……etc.

The origins of the urban co-operative banking movement in India can be traced to the close of

nineteenth century. When inspired by the success of the experiments related to the co-

operation movement in Britain and co-operative credit movement in Germany. Such societies

were set up in India. These are based on the principles of co-operation, mutual help,

democratic decision making and open membership. Urban co-operative banks has to mobilize

savings from the middle and low income urban groups and purvey credit to their members

many of which belonged to weaker sections.

Urban co-operative banks have a role to play in economic construction. The features

of urban co-operative movements has been its heterogeneous character and its uneven

geographical spread.

Cooperative Movement in India

The Indian cooperative movement, like its counterparts in other countries of the world

has been essentially a child of distress. Based on the recommendations of Sir Frederick

Nicholson (1899) and Sir Edward Law (1901), the Cooperative Credit Societies Act was

passed in 1904, paving the way for the establishment of cooperative credit societies in rural

and urban areas on the patterns of Raiffeisen and Schulze Delitzch respectively. The

Cooperative Societies Act of 1912 recognized the formation of non-credit societies and the

central cooperative organizations /federations. The state patronage to the cooperative

8

An Empirical study on Capital to Risk Assets Ratio

movement continued even after 1947, the year in which India attained freedom. The

independent India accepted the concept of planned economy and cooperative organizations

were assigned an important role.

The policy of the Government towards the cooperative movement was guided by the

recommendations of the Saraiya Committee, which stated that .the cooperative society has an

important role to play as the most suitable medium for the democratization of economic

planning.. Various expert committees, which examined the problem of rural Credit

subsequently, have come to the same conclusion, without exception, that in the Indian

context, there is no alternative from the point of view of structural appropriateness, to

cooperatives at the village level. The Rural Credit Survey Committee (1954), the first

comprehensive enquiry into problems of rural credit, after a detailed examination of the entire

gamut of issues including the social ethos of rural society, summed up its findings in the

celebrated dictum that .cooperation has failed, but cooperation must succeed.. Since 1950s,

the cooperatives in India have made remarkable progress in the various segments of Indian

economy. During the last century, the cooperative movement has entered several sectors like

credit, banking, production, processing, distribution/marketing, housing, warehousing,

irrigation, transport, textiles and even industries. In fact, dairy and sugar cooperatives have

made India a major nation in the world with regard to milk and sugar production. Today,

India can claim to have the largest network of cooperatives in the world numbering more than

half a million, with a membership of more than 200 million. Of the primary (village) level

cooperatives, around 28 percent with 137 million memberships are agricultural cooperatives,

dealing directly or indirectly with agricultural sector. The cooperative network in the country

is rather strong covering all the villages in the country and more than 67 percent of the

households have been brought under the cooperative hold. Cooperatives supply about 46

percent of the total rural credit (including agricultural credit), account for 36 percent of the

total distribution of fertilizers, produce about 55 percent of the total sugar and constitute for

28 percent of the rural fair shops (distributing consumer articles). Though cooperative

movement has made remarkable progress in several areas, certain glaring defects have also

developed in the movement, which have been, in a way, defeating the very objectives of these

institutions. The following are the unique features of Indian cooperative movement.

9

An Empirical study on Capital to Risk Assets Ratio

COOPERATIVE BANKING IN INDIA:

Historically, Governments and policy makers have paid more attention to agricultural

cooperatives and thus, the growth and development of the Indian cooperative movement is

heavily tilted in favor agricultural cooperatives in general and in particular, credit

cooperatives. In some areas like dairy, urban banking and sugar, the cooperatives have

achieved success to an extent but there are larger areas where they have not been so

successful. The cooperative credit movement in modern India, curiously, is a state initiated

movement. The state partnership is, perhaps, the unique feature of the Indian cooperative

movement. As of today, Government contribution to the share capital of primary agricultural

cooperatives accounts for about 7.5 percent of the total. Paradoxically, the state partnership

which was conceived as a measure for strengthening the cooperative institutions had paved

the way for ever-increasing state control over cooperatives, their increasing officialization

and politicization culminating.

As against three-tier structure of short-term credit cooperatives, the long-term in virtually

depriving the cooperatives of their vitality as well as their democratic and autonomous

character. Dormant membership, lack of active participation of the members in the

management, lack of professionalism (and absence of corporate governance), undue political

and bureaucratic intervention, have made majority of the cooperatives at the primary level

almost moribund. Understandably, this has resulted in weakening of the cooperative edifice.

The upwardly transmission of the weaknesses of the primary societies have affected the

capabilities of the higher level cooperative federations in so far as their usefulness to the

former is concerned. With regard to agricultural cooperative credit structure, although the

quantitative expansion has been somewhat satisfactory, the movement continues to suffer

from structural defects and operational deficiencies. The acknowledged operational

deficiencies of the cooperative credit structure have been

(I) weak recycling of credit,

(II) poor resource mobilization,

(III) Ineffective lending and

(IV) Poor recovery.

10

An Empirical study on Capital to Risk Assets Ratio

The agricultural credit cooperative system in general has become rather over dependent on

external support in terms of participation in share capital by Government and refinance from

Government owned Financial Institutions .Credit cooperatives are the oldest and most

numerous of all the types of cooperatives in India. The cooperative credit institutions in the

country may be broadly classified into urban credit cooperatives and rural credit

cooperatives. There are about 2090 urban credit cooperatives and these societies together

constitute for about 10 percent of the aggregate banking business and therefore regarded as an

important segment of the banking system. The urban credit cooperatives are also popularly

known as Urban Cooperative Banks.

The rural credit cooperatives may be further divided into short-term credit

cooperatives and long-term credit cooperatives. With regard to short term credit cooperatives,

at the grass-root level there are around 92,000 Primary Agricultural Credit Societies (PACS)

dealing directly with the individual borrowers. At the central level (district level) District

Central Cooperative Banks (DCCB) function as a link between primary societies and State

Cooperative Apex Banks (SCB). It may be mentioned that DCCB and SCB are the federal

cooperatives and thus the objective is to serve the member cooperatives cooperative credit

structure has two tiers in many states with Primary Cooperative Agriculture and Rural

Development Banks (PCARDB) at the primary level and State Cooperative Agriculture and

Rural Development Bank at the state level. However, some states in the country have unitary

structure with state level cooperative operating with through their own branches and in one

state an integrated structure prevails. The organizational structure of the credit cooperatives

in India is illustrated in chart I.Interestingly, under the Banking Regulation Act 1949, only

State Cooperative Apex Banks, District Central Cooperative Banks and select Urban Credit

Cooperatives are qualified to be called as banks in the cooperative sector. In other words,

only these banks are licensed to conduct full-fledged banking business.

Urban Cooperative Banks in India

The term Urban Co-operative Banks (UCBs), though not formally defined, refers to

primary cooperative banks located in urban and semi urban areas. These banks, till 1996,

were allowed to lend money only for non-agricultural purposes. This distinction does not

hold today. These banks were traditionally centered around communities, localities work

11

An Empirical study on Capital to Risk Assets Ratio

place groups. They essentially lent to small borrowers and businesses. Today, their scope of

operations has widened considerably.

The origins of the urban cooperative banking movement in India can be traced to the

close of nineteenth century when, inspired by the success of the experiments related to the

cooperative movement in Britain and the cooperative credit movement in Germany such

societies were set up in India. Cooperative societies are based on the principles of

cooperation, mutual help, democratic decision making and open membership. Cooperatives

represented a new and alternative approach to organization as against proprietary firms,

partnership firms and joint stock companies which represent the dominant form of

commercial organization.

Characteristics of urban cooperative banking in India

Cooperatives may still have an edge in identifying and serving consumer needs.

In theory, cooperatives are better able to maximize consumer surplus. Hansmann, for

example, notes that inefficiencies may arise from firms seeking to satisfy the preferences of

the marginal patron (to maximize sales/profits) rather than those of the average patron (which

would maximize consumer surplus). In a cooperative, the one-member one-vote system will

lead the firm to seek to satisfy the preferences of the median patron, who is closer to the

average patron than the marginal patron is. However, in part because the median voter does

not necessarily reflect average preferences, Hart and Moore (1998) find that, for consumers,

cooperative ownership becomes less advantageous the more competitive a market is and

more so the more uniform the membership base is However, these theoretical considerations

are predicated on the assumption that all relevant decisions are made by the full membership

base, or at least by a representative sample of members. The reality is very different (see

section on corporate governance). Nevertheless, the fact that a cooperative‘s clients are also

its members and are involved in its decision-making, should provide it with an informational

advantage over commercial banks. While size and increasing distance between members and

management are likely to reduce this advantage, the remarkably high market shares some

cooperative banks have in the market segments they target (e.g., farmers in France) seem to

indicate that it remains in place to a significant extent.

12

An Empirical study on Capital to Risk Assets Ratio

Challenges for urban cooperative banks cooperatives and financial

stability:Prudential authorities need to be conscious of the specific risks cooperative banks

face, as well as of the potential impact they may have on the banking system as a whole. The

most important of these specific risks are related to the combination of the governance

challenges and the constraints cooperatives face in managing their capital.

The Experience Thus Far

Cooperative banks generally have lower incentives to take on risks, and this seems to be

confirmed by experience. The lack of a need to maximize profits and the absence of many of

the factors that lead rational managers in commercial banks to adopt short-term horizons

means that cooperative banks have lower incentives to take on risk. Much of the available

evidence is consistent with this prior. During the US savings and loans crisis, investor-owned

S&Ls fared much worse than mutual S&Ls, because they had tended to pursue more

speculative investment policies (Hansmann, 1996). It is also found that Cooperative banks in

France and Switzerland fared generally better than commercial banks during the banking

problems of the early 1990s. It‘s noted that cooperatives typically have more risk averse

clients, who may prefer member shares in a cooperative over more risky assets such as stocks

in Capital Market. Cooperative banks may be more vulnerable to certain shocks, including

credit quality and interest rate developments, but possibilities to manage these vulnerabilities

are increasing. Old-fashioned intermediation is cooperatives ‘core business. Hence, while

they may still have a bit of an edge in managing credit risk, cooperative banks typically have

a lot of such risk. Moreover, the credit risks they face tend to be correlated with each other

due to cooperatives ‘focus on a usually in at least some ways homogenous member base. As

noted above, cooperatives ‘business model also relies more on one particular source of

revenues (the interest margin), which is likely to imply higher vulnerability to interest rate.

Developments Overall, while cooperative banks may generally be stable, they do tend to be

vulnerable to certain types of instability. Just few years bank many cooperative banks in India

have had problems with nonperforming assets. However, developments in financial markets,

in particular the increased opportunities to hedge against interest rate risk and securitize loan

portfolios, should allow cooperatives to reduce and better manage the risks they face In our

country India also, because of very problem two large cooperative banks such as,

13

An Empirical study on Capital to Risk Assets Ratio

Madhavpura Mercantile Bank in Gujarat and Charminar Bank in Andhra Pradesh failed. Both

of these banks carry with them several other small and medium cooperative banks towards

failure. Cooperative banks may have more difficulties adjusting to adverse circumstances and

changing risks. The Swedish cooperative banking sector did not survive the crisis of the early

1990s in a cooperative form, and the need to restore capital was a major factor in the decision

to demutualize. A cooperative‘s typical business model comes with a relatively high fixed

cost base. With employees involved in decision making, it may be hard to cut these costs

quickly when needed. Strong

Union affiliation makes the mater worst. In many such cooperative banks cost

of employees is more than 80% of the total administrative cost. On the positive side,

employees-members may be more loyal and motivated, and therefore more determined to

pull the firm through times of hardship rather than abandon it. Cooperatives ‘business and

depositors are also more stable, allowing them to thrive with a higher (fixed) cost base.

Beyond conjuncture developments, the risk of technological change rendering the

cooperatives ‘branch-based strategies obsolete needs to be taken seriously. Risks have also

materialized when Cooperatives ventured onto unfamiliar terrain (e.g., derivatives markets).

Democratic decision-making may come at the expense of the speed and quality of decision-

making needed to thrive under rapidly changing circumstances. In cooperatives in which

members are routinely involved in strategic and managerial decisions, the outcome may be

indecisiveness, conflict, slow adaptability, and an inability to jump on business opportunities

or take tough decisions in a timely way.

Building Empires?

Capital and growth dynamics. Most cooperatives are designed to perpetually

accumulate capital, thus building an ever-larger intergenerational endowment. At the time

they were set up, a shortage of funds was typically one of the most important challenges

cooperatives faced. To remedy this, mechanisms were put in place to ensure capital

accumulation. As discussed above, this led to the creation of an intergenerational endowment

that in most cases constitutes the bulk of a cooperative‘s equity and that keeps on growing as

long as the cooperative remains profitable. Now, a century and a half after the cooperative

banking movement started, in many cases the shortage of capital problem is no longer

present, but the mechanisms that ensure capital accumulation remain in place. This section

argues that cooperatives are caught between their capital-accumulating set-up, pressures to

14

An Empirical study on Capital to Risk Assets Ratio

achieve similar profitability as commercial banks, and the already sizable equity they have

built up throughout their history.

Cooperative banks face specific challenges in managing their capital:• They have limited control over their cooperative capital, although over many decades this

has typically been rather stable.

Since in most cooperatives members can withdraw their membership and ask to have

their shares reimbursed, cooperative capital (the part of capital to which members ‘shares

represent a claim) is variable and cooperatives could theoretically face a ―run on capital‖. In

practice this has not been an issue, given the buffer provided by the intergenerational

endowment and considering lengthy withdrawal mechanisms and the unconditional rights

that some cooperatives have to refuse redemption. In many cooperatives, there is a minimum

level of capital below which redemption is refused.

• They often face binding restrictions on their pay-out policies.

At many cooperatives, there are statutory or legal restrictions that put limits on

shareholder remuneration. For example, Swiss Raiffeisen banks are legally not allowed to pay

more than 6 percent dividend on the notional value of member shares; some French

cooperative banks cannot pay more than the government bond yield; Rabobanks do not pay

dividends to members because membership is free of charge and the Italian banking law

requires that credit cooperatives add 70 percent of their annual profits to their reserves and

three percent to a solidarity fund. As far as India is concerned, The Reserve Bank of India do

not permit to Pay more than 15% Dividend to their Shareholders.

• They can face severe difficulties raising capital in times of need.

Provided there is a prospect of future profits, commercial banks (Private) can always issue

new shares and sell those at market price when the need to shore up equity arises.

Cooperatives, by contrast, can only raise new cooperative capital by increasing their

membership or by asking existing members to buy more shares. They can also issue certain

kinds of securities and, in many cases, mobilize capital from their network in times of need.

However, both raising new capital and tapping alternative sources of funding come with

potential problems. First, members may not be well placed to provide capital when needed.

They typically pay very little for their shares and buy them to gain access to the benefits the

15

An Empirical study on Capital to Risk Assets Ratio

cooperative offers rather than as a financial investment (with low dividends and no potential

of appreciation). As a result, they may not have any incentive to buy more than the minimum

number of shares needed (a sort of ―membership fee‖).

The lack of diversification at small cooperatives and the high degree of overlap between their

member and clients also means that in times of difficulties many members may not be in a

position to provide significant amounts of fresh capital. Furthermore, in many cases there are

legal and/or statutory restrictions on the total value of shares a member may hold. Second,

issuing other securities is from various perspectives not as attractive as raising cooperative

capital. Among other things, such securities often require a relatively high remuneration. In

both approaches, decision-making procedures to raise new capital may be cumbersome and

time-consuming.

• Even in the absence of restrictions, there may be few incentives to pay out a significant

share of profits.

Cooperatives are not at risk of seeing their share price traded at a discount because of

dissatisfaction with their pay-out policies. And since shareholder ship in a cooperative is not

usually driven by investment considerations, members are unlikely to care enough about the

level of dividends they receive to organize a ―member revolt,‖ which may be difficult to

begin with.

Competition between Cooperative and Commercial Banks

Cooperatives can follow market share-based or Deposit -based growth strategies, both

of which may lead to overcapacity that may need to be resolved through retrenchment of

commercial banks. Competition between cooperative and commercial banks is likely to be

beneficial to consumers. In the long run, however, it may affect the structure and stability of

the financial system, the impact of which is a subject of debate. Market share-based growth

strategies focus on selling at lower prices than the competition (adjusted for quality, location

and everything else) and therefore accepting lower profitability. Deposit -based growth

strategies are based on relatively high organic growth rates of the capital base. Such a

strategy requires significant profits because for cooperatives profits constitute the main

source of fresh Deposits. As a result of these expansion strategies, competing commercial

banks may face reduced profitability and transition costs and risks (e.g., costs of restructuring

and closing branches). May lead to macroeconomic inefficiency, waste and overcapacity in

16

An Empirical study on Capital to Risk Assets Ratio

the banking system that may take a long time to work out. However, given the higher

inherent stability of cooperative banks, they find a positive overall impact of cooperative

presence on overall banking system stability.

Other Prudential Challenges and Concerns

The third pillar of Basel II is less effective in the case of cooperative banks. The third

pillar relies on extensive disclosure to ensure that banks are subject to market discipline.

However, as noted above, disclosure practices (and requirements) at cooperatives are often

below standards at commercial banks, especially listed ones. Also, even when disclosure is

adequate, there are rarely markets that can exert effective disciplining pressure in response.

As discussed above, shareholder pressure cannot be relied upon, loyal – to some degree

perhaps even captive—and insured retail depositors may not exert any effective market

disciplining effect either at an early enough stage .Contagion from cooperative to commercial

banks is more likely to take the form of liquidity shocks than solvency problems. Given their

typically high levels of liquidity, cooperative banks tend to be net lenders in the interbank

market. In times of stress, they are likely to cut their exposures in the interbank market,

which may cause liquidity problems for other banks. Prudential authorities may face calls to

apply different standards to cooperative banks, Cooperatives ‘not-for-profit statute, large

membership, close involvement in local communities, retail orientation, and links to broader

movements imply that they can often count on a higher level of public sympathy and political

support than commercial banks.

This is only reinforced by cooperatives ‘disproportionate market shares in terms of

deposits and branch networks, and in rural areas where competition between banks is low to

begin with. All of this may lead for pressure to ―go soft‖ on cooperative banks, in terms or

regulation as well as supervisory enforcement, and may create particular problems in case a

cooperative runs into financial difficulties. In Ireland, for example, the Irish League of Credit

Unions has lobbied for, and obtained, a specific regulatory and supervisory framework for

credit unions that takes into account their not-for profit orientation and the volunteer nature of

much its human resources .Though in India since last few years such soft views are not taken

by Reserve Bank of India but measures introduced after MMCD are much tougher. In some

cases, risks may arise as a result of not differentiating between commercial and cooperative

banks. The main area where this risk appears to exist is corporate governance. Corporate

governance regulations that are tailor-made for commercial banks and fail to take into

account the different nature of cooperatives may fail to address the specific risks that exist at

17

An Empirical study on Capital to Risk Assets Ratio

the latter. Given the large number of small cooperative banks, supervisory authorities

sometimes rely on the apex organization for supervision. In many European countries, there

are hundreds of small cooperatives, many of which have their headquarters far away from the

big cities where supervisory authorities typically have most of their staff. Individually

supervising all of these small cooperatives may require a level of resources that most

supervisory agencies lack. Also, full-fledged supervision might not even be necessary, given

that many of the cooperative banks are not dissimilar in terms of size from branches of large

commercial banks, especially in the presence of strong solidarity mechanisms. In India many

States have Apex Bank, however the entire structure needs to be changed. Present structure

do not permit any direct supervision at all on member cooperative banks. Neither any

reporting systems is designed for APEX BANK to guide or to come to rescue in case of need.

A well designed structure of Apex Bank can be extremely useful to small, medium and weak

cooperative banks. The table will describe such possible structure.

Current Policy Framework

Current policy frameworks appear characterized by a lack of attention for the specific

risks faced by, and related to, cooperative banks. Governance issues discussed in the

document relate mainly to internal control procedures within financial institutions, rather than

to external control over management. Similarly, the Basel Committee‘s most recent

publication on corporate governance for banking organizations (Basel Committee on Banking

Supervision, 2005a) does not contain any cooperative-specific discussion. Recent initiatives

to improve corporate governance have focused on corporation and large companies. Given

cooperative banks ‘economic importance and large member and depositor bases, this lack of

attention appears mainly the result of the absence, of corporate Governance for cooperative

Banks. However since last few years the need has been recognized and now many

discussions are taking place all over India.

Following Weaknesses are generally found in the working of Urban Co-operative

Banks.

• Absence of systematic approach to profit planning, risk and resources management.

• Miss match in cost, yield and maturity profile of asset and liability.

• Shoddy accounting practices (income and expenses recognition, investment valuation,

depreciation, NPA provisioning etc.)

• Misleading Management control systems, performance measurement and compensation

system.

18

An Empirical study on Capital to Risk Assets Ratio

• Increase in level of NPA‘s due to inadequate asset portfolio management.

• High deposit and lending rates.

• Unprofessional approach on credit and loan appraisal, product pricing and management of

asset portfolio.

• Shrinking spreads, thinning margins, poor credits off take due to general industrial

recession.

• Confidence crisis.

• Dual Regulations.

• High burden / cost of operations.

• Conflicting objectives Business V/s Societal

• Miss conceptions about cost of owned funds, deposits and borrowings.

• Inadequate technological usage and harnessing.

• Miniscule share of Para-banking, fee based banking.

• Limited area of operation and Regional presence.

• Inadequate treasury operations and management.

Role of the UCBs in the Indian Banking System:-

The performance of the co-operative banking sector as a whole has attracted attention

in recent year. Today they have become an important constituent of the Indian financial

system and cover a large segment of society because of their prompt and personalized

service. They take the responsibility of covering the unmonitored sector neglected by

commercial banks and most priority is given by UCBS to small and medium enterprise UCBs

provide service with no bars of caste religion etc. and thus spread the feeling of ―Unity of

diversity‖. Some UCBs operate beyond their state of registration and are governed by the

Multi state Co-operative Act 1984. They are not responsible only to employees and societies.

The UCBs bears some responsibility in the following ways.

A. Service on Behalf of Customers:-

1. Provide facility regarding opening current, saving and fixed deposit accounts and collect

deposits.

2. Issue draft, letter of credit and discount bill on a low rate of commission.

3. Provide services of automatic teller machine mobile banking and depository participants

and do immediate transfer of money.

4. Computerized bank passbook issued to customers.

5. Received complaint of customers and solve it as early as possible

19

An Empirical study on Capital to Risk Assets Ratio

6. Provide self-deposit vault facilities

7. Advances are given to small scale and medium enterprise and cottage industries.

8. Advances against properties, jewelry, govt. securities, life policy and new or old vehicles.

B. Service on Behalf of Employees:-

1. Provide medical facilities and educational facilities.

2. Provide various types of allowances.

3. Maintain various types of funds like staff provident fund bonus fund etc.

4. Conduct training programs for new employees and refresher programs for old employees

and organize a seminar and the conferences to update their knowledge.

5. Special education reward is given to employees children for highest percentage.

C. On Behalf of Society:-

1. Provide donation to educational institutions charitable institutions and hospitals etc.

2. Advances to the weaker sections of the societies to be self -sufficient.

3. Helping to the people at the time of natural calamity like earthquake, flood, drought.

4. Sustain and generate gainful employment.

5. Equal distribution of credit structure by branch expansion particularly in areas which are

not covered by the banking system.

Problems & Prospects of UCBs:-

UCBs were setup with the objective of promoting saving habits amongst the middle-

income group of the urban population 2004 is golden jubilee of urban co-operative banks

celebrated by govt. of Gujarat. During the 100 years of their inception they have attracted

considerable attention and large 78 number of them has shown creditable performance but

fair number of them have simultaneously shown discernible signs of weakness too because of

the problems they could not overcame some important factors, Which are barriers to the

progress of the UCBs are as given below.

1. Dual Control: -A major problem faced by UCBs is the duality of control by the State

Government and the RBI. The UCBs are supervised by RBI and also issued for license while

regarding administrations like, registration, administration constitution and administration

and selection etc. This had negative impact on the functioning of the UCBs. Duality in

command hampers effective supervision. The Narsimhan committee suggests removing dual

control system which is affected to UCBs. High power Committee also.

20

An Empirical study on Capital to Risk Assets Ratio

2. Limited Area of Operations:-

The UCBs have to function within restricted framework in the context of

mobilization of deposits. The need for heavy industrial advances and trade finance for

industrial units as well as for commercial enterprises is here but the UCBs are not able to

meet with it is they have to serve as per the RBI directives. But to survive in the competitive

world the UCBs should enhance their area of operation and start providing loans as per local

needs.

3. Violation of Prudential Financial Norms: -It is found that many UCBs Violate norms

governing advances. Top officials of the banks receive loans without documents. The failure

of Visangar Co-operative Bank (Mehsana) and Madhavpura Mercantile Co-operative Bank

(A ‘bad) are the example of violation of prudential norms. The UCBs must adopt a system of

internal audit and inspection of branches and department, the RBI should follow strict

supervision and to stop such malpractices.

4. Poor Management: - The necessity of the financial institution has a good corporate

financial management and articles. The Madhavrav committee insisted to appoint two

directors who are professional or experience persons. But in UCBs directors are politician or

illiterate. Due to this reasons management of the UCBs are poor. The RBI advice to directors

about it by letter dated 05-04-2002

5. Poor Quality Services: -The services of the UCBs are not significant enough in terms of

quality and have failed to attract deposits from individuals and institutions other than the co-

operative sectors. Hence they should try to improve the quality of services by providing

required facilities like waiting space; customer information counter, complain box, banking

information chart, easy accessibility to higher officials at the banking promises etc. At the

same time they should maintain good customer relations and keep positive attitude towards

customer. Besides this; they should start providing door to door services.

6. Lack of Modernization:- In today‘s world of technological advancement, still manual

form of work followed in some of the UCBs which cause delay and increase operational cost.

Most of the UCBs failed to provide service through use of modern technology except some

UCBs. It has become inevitable now on part of the UCBs to have computerized system of

banking and adopt latest banking technique like ATM, Credit Card, Internet Banking, Branch

Banking, Tele Banking etc.

7. Increasing Overdoes: - The UCBs suffer from dangerously. Low or weak quality of loans

assets and highly unsatisfactory recovery of loans, which enhance the proportion of overdue.

21

An Empirical study on Capital to Risk Assets Ratio

Due to this situation, UCBs must have to develop a separate recovery department for quick

recoveries.

8. Political Interference: -Political interference in affairs of the UCBs leads to faulty lending

and poor recovery. It compels, to pressure on the banks to provide loan to parties whose

repaying capacity is doubtful. Visanagar co-operative bank is a example of this situation.

Though banks take to legal action against the defaulter it often interferes by putting an end or

postponing such an action. Hence political interferes is damage to UCBs administration.

9. Staff Problems and prospects:-The UCBs have not trained and professional staff. The

UCBs do not select staff on professional basis. External pressures are a cause of untrained

and low standard staff which directly affect on quality work. At least appointment of chief

executive officer ( like Manager or Managing director) should be made on professional lines

and provide training to untrained or fresh staff members or employees.

10. Some Other Problems of UCBs are as under: -

I. Low capital adequacy ratio etc.

II. Lack of transparency in financial statement.

III. The Balance sheet of most of UCBs are not finalized in time due to

Non-completion of audit purpose.

IV. Lack of planning and co-ordination.

V. Lack of standardization in data reported by ratio etc.

Future of the UCBSS:-

Looking at the progress of the UCBs it can be said that they have expended by leaps

and Bounds and increased their business over the last few decades. A walk down the streets

of Mumbai, Ahmedabad, Hyderabad, Surat etc. reveals how widely they have spread their

tentacle across the nation. Every nook and corner displays the hoarding of the office of one or

the other UCB. But an increasing number of failures of the UCBs have spoiled the image of

the UCBs and shaken the faith of their depositors and investors. The scam of Madhapura

Mercantile Co-operative Bank (MMCB) of Ahmedabad, Krushi Co-operative Bank of

Hyderbad and Visanagar Nagrik Sahkari Bank (Mehsana Dist.) have brought into the fact that

loopholes exist within the banking system itself and the RBI failed to perform its duties as a

banking regulators. In the case of Krushi bank, it was found that the Chairman and the Vice

Chairman got loans from the bank without any collateral and the funds were siphoned off for

other purposes. Similarly in MMCB lending norms were violated and crores of rupees were

given to Mr. Ketan Parekh violating norms of the bank. In case of Visangar Sahakari Bank, it

22

An Empirical study on Capital to Risk Assets Ratio

was found that the chairman and his relatives got loans from bank without any proper

documents and guarantors. Free entry of private financial institutions has

also led to a threat to their existence. In spite of these problems, with regard to the future of

these banks it can be said that the UCBs will continue to be promoters of mass banking as

distinguished from class banking usually practiced by commercial banks. The future of UCBs

is much better due to their numerous distinctive such as85

(a) Close familiarity with the members

(b) Local feel

(c) Democratic management

(d) Personalized service

(e) Compactness in the area of operation

(f) Close supervision over the end use of credit

(g) Prompt recovery of dues from member borrowers.

But both the RBI and the UCBs should try to maintain this distinctive identity of the UCBs

and take care to waive scandals or scams. In order to achieve this goal, the RBI should take

measures to strengthen the regulatory frame work for the co-operative sector, lay down clear

cut guidelines for their management structure and should enforce further prudential standards

in respect of access to uncollateralized funds and lending against volatile assets.

Simultaneously, the UCBs should try to complete with private financial institutions and

commercial banks within their limits. Their main inclination should be towards customer‘s

satisfaction. They should introduce a ―Customer Day‖ on which customers can meet and

discuss with the Board of Directors their problems. They should also try to reach to the

customers by providing door-to-door services. They should open a separate wing for

publicity and advertisement of existing well as new schemes of deposits loans and other

services provided by them. Simultaneously they should try to enhance their deposits and

advances by providing quality services. For enhancing deposits, they should introduce

children savings and youth savings centers in schools and colleges respectively and provide

knowledgeabout the benefit of savings. All UCBs should introduce mobile vans for

handicapped and illiterate people. Similarly for enhancing advances, they should do market

research and start loaning according to the local needs ;keep less margin of profit on

advances; provide a guideline about the procedure of advances to the general public so that

they would not procedure of advancing loans; etc.. Such comprehensive attempts will help

the UCBs in enhancing the banking business in limited areas only. In short, the UCBs must

come into their own to take the future head on. It‘s time for them to think strategically and

23

An Empirical study on Capital to Risk Assets Ratio

focus on the opportunities in terms of market, products and customers. It requires a vision

about which their future customers are going to be what they will need; who their competitors

will be and what their disadvantages mean for the UCBs; etc. They should be ready to make

changes in their policy as per the demands and competition. They should consider

diversification of business product and must upgrade their skills and technology to provide

efficient and affordable services. At evolve a systematic approach towards human resource

development in many areas like manpower planning, recruitment, placement and leadership

development for motivating staff and increasing productivity. In short UCBs should pay

attention to human resources development and evolve a systematic approach toward human

resource development in many areas. They should focus on the opportunities in terms of

market, products and customers. They also focus on need of customers should be removed

disadvantages of management and administration

24

An Empirical study on Capital to Risk Assets Ratio

COMPANY PROFILEHistorical Background:

The urban co-operative bank ltd Perinthalmanna was commenced on 1916 April 5 and

affiliated to an urban bank branch in 1940 July. It has come under Banking Regulation Act

in1966 and it has provided insurance to the money under deposit insurance and credit

Guarantee Corporation. Today the members are numbering up to 47000. In 1966it has

covered only 6 villages but in 1972 it is covering all the Perinthalmanna taluk. In 1979 its

first branch opened at karinkallathani. In 1980-91 the bank has entered a depression stage. In

1994 got license according to the Banking Regulation Act of Reserve bank. Now bank has

fully computerized 15 branches at Perinthalmanna today the bank has 110 permanent

employees, 9 part time employees and 13 daily deposit collectors based on commission and

also 6 other workers and 5 securities. The chairman of urban co-operative bank, Board of

directors and employees, workers are foreseeing future actions and policies accordingly, has

achieved the required CRAR AND decreased NPA very effectively. Today net NPA is zero

percentage from the net profit of bank, 1% is used for the social welfare activities .And

benefit allowed 2500 for cancer, kidney and heart patients admitting EMS cooperative

hospital and to provide bed rent. This year 311800 has giving in this aspect. The urban co-

operative bank has clear vision and mission. Bank provides RTGS, NEFT lacer facilities in

all branches. Core banking facility is now providing soon. If the core banking is started ATM,

malty banking, net banking, tale banking ………..etc., can be started high interest rate are

given for depositories up to 12.5%. This bank provides loans up to 5000000 former chants

and also provides loan for retailers in with simple condition and they provides loans for

employees to meet their needs and wants. And they provide vehicle loan, gold loan and

housing loan………etc., the urban co-operative bank Perinthalmanna is act as the head office

of urban co-operative banks. It is situated pattambi road Perinthalmanna. Cooperative society

is the nature of ownership. The urban co-operative bank using 18.89 crore amount of capital.

And they using share capital and reserves as their source of capital. In the bank total 91

employees are working. These including male and female workers. It worked as two different

branches morning branch and evening branch. Morning started at 9.30 am to 4.30 pm. And

evening branch starting 3 to 8 pm. The urban co-operative bank ltd is offered loans, advances

and deposits as to its products and services. The Registration number of the bank is 1758 Dt

07.03.1916 and the RBI License No is UBD.KR.1070P.Dt.23.04.1994. The email address of

Perinthalmanna urban co-operative bank is ucbpmna@ yahoo.com

25

An Empirical study on Capital to Risk Assets Ratio

PROMOTERSThe bank is completely controlled by the President, Vice president, and the Directors.

Only RBI can interfere in the rules and regulations of the bank.

The bank consists of a President, a Vice president and 13 Directors

CHAIRMAN - Mr.DIVAKARAN

GENERAL MANAGER - V. MOHAN

DIRECTORS - M.K BALAKRISHNAN

- M. CHATHAN

- PALOLI KUNJIMOHAMMED

- K.R. BEENA

- E.V. SANKARANARAYANAN

- P.C. SHAMSUDHEEN

- V. SREEKUMARAN

- UMMER

- K.VASUDEVAN

26

An Empirical study on Capital to Risk Assets Ratio

VISION AND QUALITY POLICY1. Accepting deposits for the purpose of promoting saving habits in the minds of the

public and members.

2. Providing various types of loan facilities to members and associates members

3. QUALITY POLICY: to render good customer service

VISIONFor the growth of the bank with stability, the vision 2015 document targeted to become the

first scheduled Urban Co-Operative Bank in Kerala by mobilizing a deposit of Rs.750 crores

and to provide the specialized service to customer

To make "The urban Co-Operative Bank, Perinthalmanna" synonymous to trust and

reliability, to be a leader amongst the co-operative banks in Kerala, to render excellent and

personalized services and to contribute to co-operative movement making credit available to

the customers, more particularly to individuals, SHGS, JLGS, there by contributing to their

growth and striving to maintain net NPA at 0% level.

MISSION

1. To meet the growing aspirations of the customers of the bank in the changing

environment

2. To bring total customer satisfaction by providing quality service

3. To meet the career aspirations of the employees.

4. To promote the effectiveness of credit and to reduce the risk in granting a credit

through careful and continuous supervision.

5. The mission of this bank is to provide society with superior products and

6. Services. Satisfy customer needs and provide employees with meaningful work and

Advancement.

27

An Empirical study on Capital to Risk Assets Ratio

MISSION-2020

Inspired by the sparking performance of the bank between the years 2005-2012, the mission

of the bank has been given an upward push as -"The Urban Co-Operative Bank Ltd,

Perinthalmanna is set to scale new heights by the year 2020 the Banks ambitions is to

achieves Rs. 2000 crores business, Rs. 10 crore Profit, net NPAs to be maintained at 0%

level, net worth of Rs.100 crores and network of 20 branches and ATMs and also to become

the 1st scheduled co-operative Urban bank in kerala.

28

An Empirical study on Capital to Risk Assets Ratio

PRODUCT / SERVICE PROFILE CORE BANKING

Since all branches under core banking, the customers can make their transactions

irrespective of their home bank.

RTGS / NEFT

RTGS/NEFT facility is available in all our branches.

DD / PAY ORDER

The bank provide Demand Draft all over in India. We are members in MASK and

AIMAS. Moreover we have arrangement with HDFC Bank for issuing and collecting

demand drafts.

NRE SERVICES

The customer can open the NRE account in all of our branches.

CLEARING

We are a permanent member in Perinthalmanna and Malappuram clearing house. It

helps our customer for collection without any delay.

LOCKER

We provide locker facility for customers in our selected branches. Customers can

avail this facility on a nominal security and rent.

ATM

Now Bank is in the process of implementation of this facility.

NETBANKING

Now Bank is in the process of implementation of this facility.

29

An Empirical study on Capital to Risk Assets Ratio

The various products and services offered by the bank are ;-

1. CASH CREDITS

2. OVERDRAFTS

3. DISCOUNTING OF BILLS

4. LOAN

5. DEPOSITS

CASH CREDITS: This is a very popular type of Advance made by commercial

banks. This is sanctioned against the Hypothecation or Pledge of the goods like agriculture

and industrial product or against the guarantee of the individual or co-obligate. As per these

financial arrangements, some amount of loan is sanctioned to the borrower and he cannot

utilize it whenever he wants.

It is not obligatory to draw the entire amount in lump. The cheque are issued against

the accounts as and when required by the loans can be credited to the accounts. Thus, cash

credit account is a running account which can be operated according to the will of the

borrower. However the debt balances in the account should not exceed the sanctioned limit.

The interest will be charged quarterly or half yearly on the amount actually used at an agreed

rate. When the cash credit is sanctioned, the banker should keep the amount at the credit of

the borrower, irrespective of the fact that he utilizes the amount or not. Thus, the banker will

lose interest earnings on unpaid balance. To compensate this loss, he incorporates

(MINIMUM INTEREST CLAUSE) according to which the interests to be paid on the

amount utilized at an agreed rate or on the portion of cash credit sanctioned, whichever is

higher. Therefore, cash credit is a popular loan account sanctioned by the commercial banks.

They are also called (revolving goods loan) account as the arrangements are made against the

stock and it is for a longer period and a current account need not be opened in this case.

OVER DRAFT: This is a type of loan sanctioned up to a certain limit against a

current account. Over draft means over drawing the current account account up to a

sanctioned limit. The amount so drawn carries an agreed rate of interest. This is a temporary

financial agreement made for a short period. By the end of the financial year, the borrower

should bring back the current account to credit balance. The interest is paid only on the

utilized portion of the sanctioned limit. Hence, the charges are one percent on the (minimum

interest clause) which is explained under cash credit. Overdraft is sanctioned against the

collateral securities or against the personal security of the borrower.

30

An Empirical study on Capital to Risk Assets Ratio

DISCOUNTING OF BILLS: This is a type of financial accommodation made

between the banker and the customer. According to this, the banker discounts the trade bills

and the accommodation bills of exchange for a shorter period, say 60 days to 90 days and

credits the customer account with the proceeds (i,e., face value of the bills minus the discount

charges). The bill of exchange may be discounted or purchased by the banker or it is given as

a security against an advance.

If they are discounted or purchased by the banker, he will become the (holder for

value), and can freely act as it will be his absolute property. But in case of bills given as

security, the banker cannot freely handle such bills as they are not absolute property. Another

point to be noted here is that the banker gets discount in advance in case of bills are given as

a security against an advance.

LOAN: According to this type of advance, the banker makes advances to the

customer against his personal security of one person. The amount is credited to the

customer’s account immediately in a lump sum or in installments. The period of loan ranges

from one year to ten-twelve years. Accordingly, it has been classified as;

Short-term loan : for one year

Medium –term loan : from one to six years

Long-term loan : for more than six years

REGISTERED OFFICE

The registered office of the bank shall be situated at Perinthalmanna,

Malappuram District.

AREA OF OPERATION

31

An Empirical study on Capital to Risk Assets Ratio

The Urban Co-operative Bank Perinthalmanna has well established branches in

various major areas of Malappuram. This is done to establish a well networked customer

relation.

Bank has 15 branches. They are operating in following areas:-

PERINTHALMANNA MAIN BRANCH

KARINKALLATHANI

MALAPPURAM

PANANGANGARA

CHATTIPARAMBA

MELATTUR

PULAMANTHOLE

MAKKARAPARAMBA

KOLATHUR

PERINTHALMANNA EVENING BRANCH

PATTIKAD

THOOTHA

ANGADIPPURAM

MANKADA

MALAPPURAM EVENING BRANCH

INFRASTRUCTURAL FACILITIESThe bank has 160 X 134 sq feet site. The building is built in 100 X 100 sq feet of site.

A ground floor and first floor is built to carry out the banking activities. It is built for own

use. In top floor, there is a head office branch of the bank and in the first floor, there is an

administrative office.

The head office of the bank is located in Perinthalmanna. It has 15 other branches. All

the branches have computer facilities. Each branch has its own department which is fully

furnished and well equipped for smooth functioning of the banking activities.

The infra of the bank is not only providing facilities to employees like canteen

facilities, drinking water, snacks, proper lighting, ventilation facilities etc. with all these

facilities the employees are more motivated to work in this environment.

32

An Empirical study on Capital to Risk Assets Ratio

COMPETITOR’S INFORMATIONCo-operative bank is facing competition from the commercial banks and foreign

banks. They are not providing core banking facilities, which make the customer to make

banking transactions easy, the bank is yet to adopt this facility. So core banking providers are

the main competitor to the co-operative bank.

Apex co-operative bank

Canara bank

ICICI bank

HDFC

Axis bank

Visveswarayya bank,

33

An Empirical study on Capital to Risk Assets Ratio

SWOT ANALYSIS STRENGTH

1. Social Principles

2. Wide Network

3. Democratic Control

4. Mutuality

5. People's Support

6. Rural Accessibility

7. State's Support

8. Integration

9. Leadership

10. Cooperative Ideology & Principles

11. Apex Bank with Good Network

12. Vast Human Resources

13. Refinance on Concessional Rates

14. Support from Government

15. Support from NABARD

16. Most Modern Banking Technology Support

WEAKNESSES

1. Absence of systematic approach to profit planning, risk and resources

management.

2. Miss match in cost, yield and maturity profile of asset and liability.

3. Shoddy accounting practices (income and expenses recognition,

4. Investment valuation, depreciation, NPA provisioning etc.)

5. Misleading Management control systems, performance measurement

and compensation system.

6. Increase in level of NPA‘s due to inadequate asset portfoliomanagement.

7. High deposit and lending rates.

8. Unprofessional approach on credit and loan appraisal, product pricing

34

An Empirical study on Capital to Risk Assets Ratio

and management of asset portfolio.

9. Shrinking spreads, thinning margins, poor credits off take due to

general industrial recession.

10. Confidence crisis.

11. High burden / cost of operations.

12. Lack Of Autonomy

13. Dependency On Government:

14. Political Interference

15. Absence Of Professionalism

16. Duality Of Control

17. High Establishment Costs:

OPPORTUNITES

1. Professional Management:

2. Diversification Of Activities

3. Expansion Of Business:

THREATS

1. Competition

2. Disloyalty Of Members

3. Increasing Trend Of Corruptive Practices

FUTURE GROWTH AND PERSPECTIVE

In the near future,

The bank wants to increase its operations by setting up its branches all over the

district

They are planning to enter core banking.

Improve customer service.

To increase deposits

Expansion of credit for medium scale industries

35

An Empirical study on Capital to Risk Assets Ratio

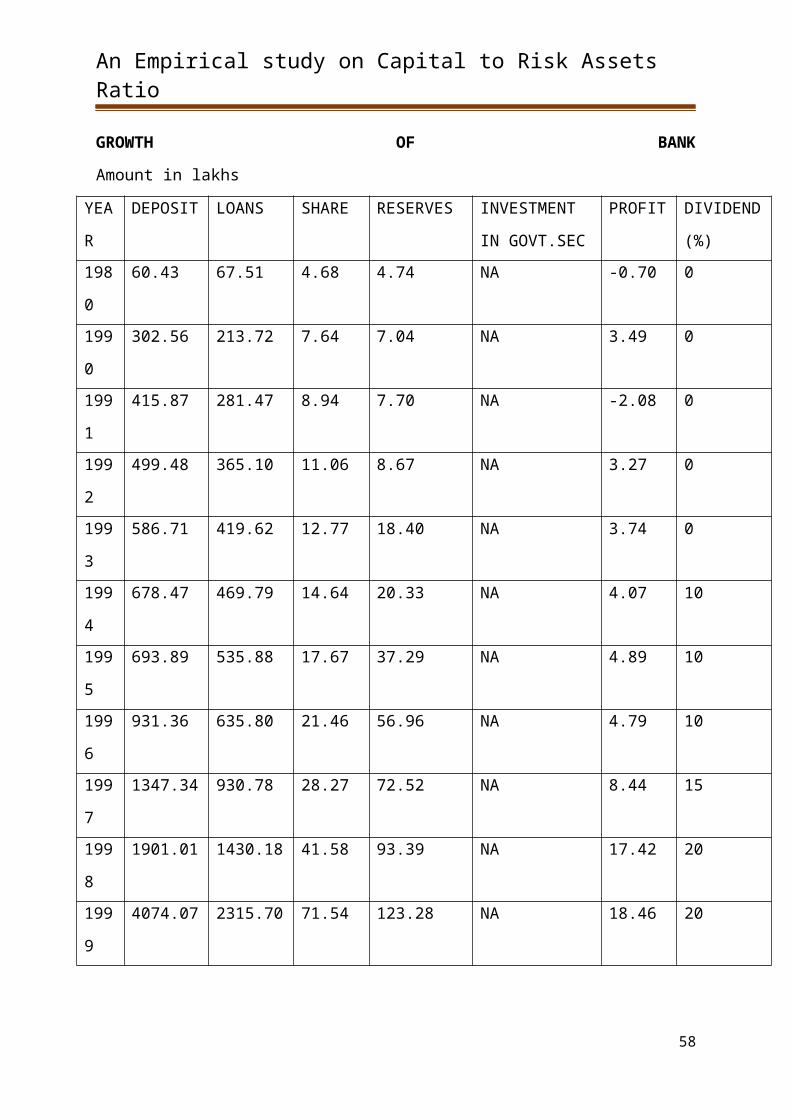

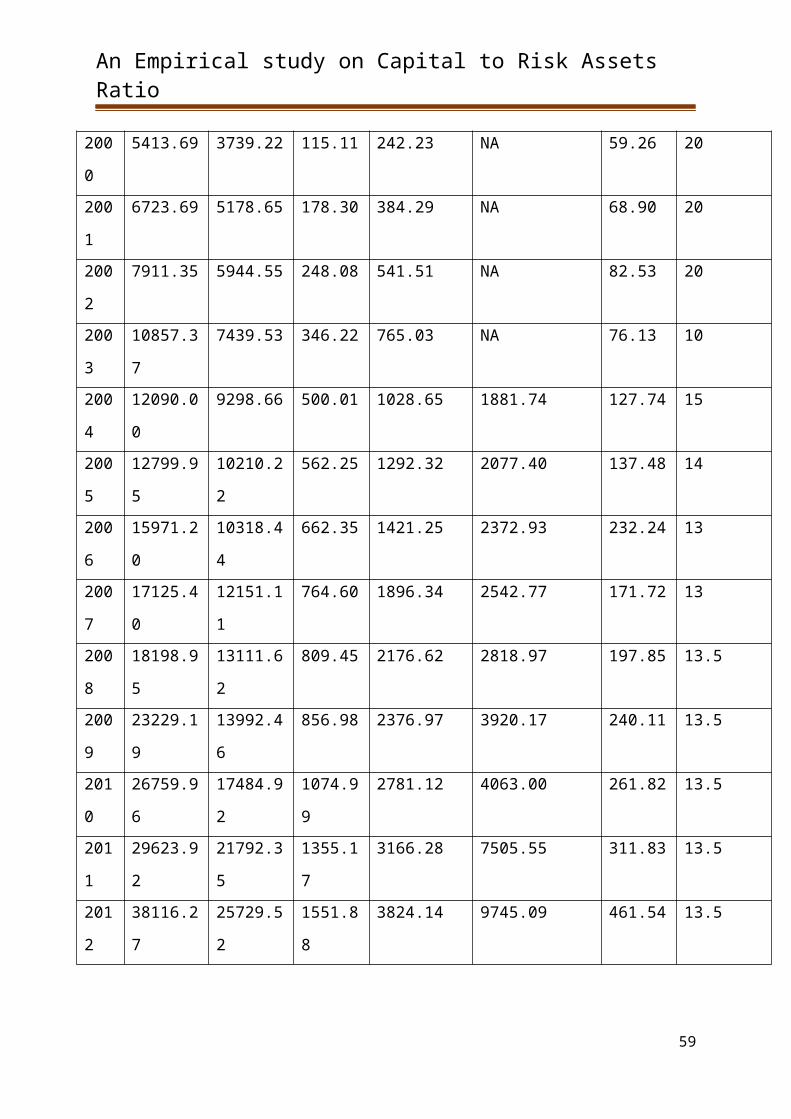

GROWTH OF BANK Amount in lakhs

YE

AR

DEPOSIT LOANS SHARE RESERVES INVESTMENT

IN GOVT.SEC

PROFIT DIVIDEND

(%)

1980 60.43 67.51 4.68 4.74 NA -0.70 0

1990 302.56 213.72 7.64 7.04 NA 3.49 0

1991 415.87 281.47 8.94 7.70 NA -2.08 0

1992 499.48 365.10 11.06 8.67 NA 3.27 0

1993 586.71 419.62 12.77 18.40 NA 3.74 0

1994 678.47 469.79 14.64 20.33 NA 4.07 10

1995 693.89 535.88 17.67 37.29 NA 4.89 10

1996 931.36 635.80 21.46 56.96 NA 4.79 10

1997 1347.34 930.78 28.27 72.52 NA 8.44 15

1998 1901.01 1430.18 41.58 93.39 NA 17.42 20

1999 4074.07 2315.70 71.54 123.28 NA 18.46 20

2000 5413.69 3739.22 115.11 242.23 NA 59.26 20

2001 6723.69 5178.65 178.30 384.29 NA 68.90 20

2002 7911.35 5944.55 248.08 541.51 NA 82.53 20

2003 10857.37 7439.53 346.22 765.03 NA 76.13 10

2004 12090.00 9298.66 500.01 1028.65 1881.74 127.74 15

2005 12799.95 10210.22 562.25 1292.32 2077.40 137.48 14

2006 15971.20 10318.44 662.35 1421.25 2372.93 232.24 13

2007 17125.40 12151.11 764.60 1896.34 2542.77 171.72 13

2008 18198.95 13111.62 809.45 2176.62 2818.97 197.85 13.5

2009 23229.19 13992.46 856.98 2376.97 3920.17 240.11 13.5

2010 26759.96 17484.92 1074.99 2781.12 4063.00 261.82 13.5

2011 29623.92 21792.35 1355.17 3166.28 7505.55 311.83 13.5

2012 38116.27 25729.52 1551.88 3824.14 9745.09 461.54 13.5

2013 43354.55 31707.68 1889.74 4597.29 11525.00 542.99 13.5

Organization structure

36

An Empirical study on Capital to Risk Assets Ratio

The institution is coming under the administrative control of the

Registrar of Co-operative Societies. The Management and administration of the Welfare

Board is vested with a Managing Committee constituted by the Government of Kerala. The

Managing Committee consists of 13 members headed by the Humble Minister for Co-

operation as Chairman (Ex-officio). There is a Vice-Chairman nominated by Government

from among the members of the Managing Committee. Secretary- Treasurer of the Board

shall be an officer in the cadre of an Additional Registrar of Co-operative Societies appointed

by Government. The Secretary- Treasurer shall be the person to sue and be sued on behalf of

the Board. In addition to that the managing committee consisting of;

Secretary (Co-operation) to Government of Kerala

Registrar of Co-operative Societies, Trivandrum

Chairman, Kerala State Co-operative Union, Trivandrum.

Joint or Deputy Secretary to Government, Finance Department (to be

nominated by the Government of Kerala).

Two representatives of Associations of Co-operative Employees (to be

nominated by the Government of Kerala)

Five persons who are associated with the Co-operative movement to be

nominated by the Government of Kerala.

ORGANISATION STRUCTURE OF THE URBAN CO-OPERATIVE BANK LTD

PERINTHALMANNA

37

An Empirical study on Capital to Risk Assets Ratio

NATURE OF BUSINESS

38

BOARD OF DIRECTORS

GENERAL MANAGER

CHAIRMAN

ASSISTANT GENERAL MANAGER

PEON

ATTENTER

JUNIOR CLERK

ACCOUNTANTS

BRANCH MANAGERS

GENERAL BOADY

An Empirical study on Capital to Risk Assets Ratio

The operation of the bank is throughout Urban Co-operative bank limited

Perinthalmanna. They offer all types of banking services to the customers like deposits, loans,

DD pay order, bank guarantees, cheque collection facility, insurance products in

collaboration with ICICI LOMBARD, etc.

OBJECTIVES OF THE BANK

1. To encourage thrift, self – help and co-operation among members.

2. To accept deposits of money from the public repayable on demanded or other wise

and withdrawal by cheque, draft, order or otherwise for the purpose of

lending on investment.

3. To borrow or raise money.

4. To lend or to advance money either upon or without security to members and others

as permitted by Registrar.

5. To draw , make a dept. , discount , buy , sell , collect and deal in bills of exchanges ,

bundies , promissory notes , coupons , drafts , warrants, certificate, scripts , and

other instruments and other securities whether transferable or negotiable or not .

6. To grant and to issue letters of credit, travelers cheque and circular notes.

7. To buy and sell foreign exchange including foreign bank notes.

8. To purchase and to sell bonds, scripts or other forms of securities on behalf of

constituents.

9. To provide safe vaults

10. To collect and transmit money and securities.

11. To negotiate loans and advances.

39

An Empirical study on Capital to Risk Assets Ratio

SHARES

The authorized capital of the bank for the present shall Rs.18.89 crores made up of the

following type of shares, 7442730 A class shares of Rs.25 each by person which should be

paid in full on application. 1 B class shares of Rs. 1000- each by state Government ,

Panchayath , Municipalities, and other body or persons approved by the Govt. 29050 C class

shares of Rs. 100-each persons residing outside the area of operation but within Malappuram

district which should be paid in full on applications .

MEMBERSHIP

Membership is open to all persons residing within the area of operation of the bank or

should be in the location of the land within the area of operation of the bank. The person who

seeks membership must have attained the age of 18 and should be of sound mind.

SHARE CAPITAL

Share capital of this bank is subscribed by the shares from the individuals and the

Government.

‘A’ class shares of Rs. 25- each by persons which should be paid in full on

application.

‘B’ class shares of Rs. 1000 –each by state Government and other body or persons

approved by the Government.

‘C’ class shares of Rs. 100- each persons residing outside the area of operation but

within the Malappuram district.

RESERVE FUND

Reserve funds are created out of net profit. It is created to meet

unforeseen losses and eventualities. So that the bank can bear the resultant shocks. It helped

in attracting deposits and creating confidence among the members, and outsiders and also

serves as a security in borrowing. reserve funds are usually invested in outside of the bank.

Withdrawal of the reserve funds are allowed only with the special permission of the Registrar

of co-operative bank.

40

An Empirical study on Capital to Risk Assets Ratio

CHAPTER- 3