Embed Size (px)

Citation preview

STANDARD TWINNING PROJECT FICHE

1. Basic Information

1.1 Programme: ENPI 2013 Annual Action Plan1.2 Twinning Number: GE/13/ENP/FI/181.3 Title: Capacity Building of the Investigation Service of the Ministry of

Finance of Georgia 1.4 Sector: Finance1.5 Beneficiary country: Georgia

2. Objectives2.1 Overall Objective(s):

Combating economical-financial crime in fiscal sphere and fostering healthy business environment in Georgia

2.2 Project purpose:

The purpose of this project is to strengthen the administrative capacity of the Investigation Service of the Ministry of Finance of Georgia in line with the European Union and international standards in the following fields:

Improvement of the legal framework connected to Tax Crime, in particular subordinate Articles and regulations of tax evasion, such as VAT fraud;

Capacity development in human resource management, modern methodology of investigation, statistical and analytical work, training of trainers;

Development of different guidelines (rules and procedures) to improve the efficiency of the general management and operation of the IS;

Improvement of information processing, risk identification and management system (precise identification of companies, enterprises including risk factors or criminal points such as tax evasion, money laundering and fictitious financial transactions in order to initiate the right investigation);

Reinforcement of Intellectual Property Rights investigation, technologies and operation mechanisms.

2.3 Contribution to Cooperation Agreement/Association Agreement/Action Plan

In the last few years the Georgian Government has introduced several reforms with the aim of supporting the overall macro-economic stability, fiscal consolidation and continuous growth. The reform efforts, particularly those related to the liberalisation of the economy and the fight against corruption, have received international recognition.

The present Twinning project is in line with the EU-Georgian Agenda:

The EU-Georgia European Neighbourhood Policy (ENP) Action Plan came into force in November 2006, and it defines areas of cooperation relevant to the reform and development of state institutions such as the Ministry of Finance.

1

Priority area 2 of ENP Action Plan: Improve the business and investment climate, including a transparent privatization process, and continue the fight against corruption

Priority area 2 of the ENP Action Plan concerns reforms in the area of tax administration, audit and investigation, and also refers to cooperation with taxpayers.

Specific actions: Continue the modernisation, simplification and computerisation of the tax

administration. Ensure the smooth enforcement of the new Tax Code also by defining all necessary administrative structures and procedures, including a fiscal control strategy, audit and investigation methods, co-operation with the tax payers and tax compliance;

Priority area 3 covers economic development and refers to specific reforms in public finance management, such as education and life-long learning opportunities to promote sustainable human resources development.

In the General Objectives and Actions of ENP are listed specific priorities, such as. the cooperation in the fight against money laundering and Information and Communication Technology related crimes (4.3.3).

The National Indicative Programme (NIP) 2011-2013, which is an ENP Instrument, has as Priority Area 2 the “Trade and investment, regulatory alignment and reform”. The sub-priority 2.1 is defined as “Export and investment promotion, in particular through market and regulatory reform” with the expected result defined as “market and reform measures particularly in the areas of protection of intellectual property rights, customs and taxation”.

The EU-Georgia Partnership and Cooperation Agreement (PCA) entered into force in July 2009. It covers the following articles which are relevant to the development strategy of the Ministry of Finance of Georgia:

Intellectual, industrial and commercial property protection (Art. 42)Legislative Cooperation (Art. 43 ff)Cooperation on prevention of illegal activities (Art. 72 ff), e.g. money laundering

Georgia is in the final stages of the negotiations with the EU to sign the Association Agreement (AA). The expectation is that the AA will be initialled by the end of 2013. Once this has been achieved the AA will constitute the main regulatory document in the relations between Georgia and the EU.

Under the Association Agreement Georgia will be required to carry out the approximation process with the EU Convention of 26 July 1995 on the protection of the European Communities’ financial interests in the field of prevention of fraud, corruption and other illegal activities. In accordance with Title 7 of the AA on Financial Cooperation Georgia has

2

to take effective measures to prevent and fight fraud, corruption and any other illegal activities in connection with the use of EU funds:

The competent Georgian and EU authorities shall regularly exchange information and, at the request of one of the Parties, shall conduct consultations.

The European Anti-Fraud Office (OLAF) may agree with competent Georgian counterparts in accordance with Georgian legislation on further cooperation in the field of anti-fraud, including operational arrangements with the Georgian authorities.

The Georgian and EU authorities shall check regularly that the operations financed with EU funds have been properly implemented. They shall take any appropriate measure to prevent and remedy irregularities and fraud.

The Georgian and EU authorities shall take any appropriate measure to prevent and remedy any active or passive corruption practices and exclude conflict of interest at any stage of the procedures related to the use of EU funds.

The Georgian authorities shall inform the European Commission of any preventive measure taken.

The Georgian authorities shall initiate legal proceedings including, if appropriate, investigation and prosecution of suspected and actual cases of fraud, corruption or any other irregularity such as conflict of interest, following national or EU controls.

The Georgian authorities shall transmit to the European Commission without delay any information which has come to their attention involving existing cases of fraud or corruption and shall inform the Commission without delay of any other irregularity, including conflict of interest, in connection with the use of EU funds. The Georgian authorities shall also report on all measures taken in connection with the facts communicated.

In the Annex of the AA is stated that several investigation related provisions will apply inter alia to “Money Laundering”.

3

3. Description3.1 Background and justification:

3.1.1 Background

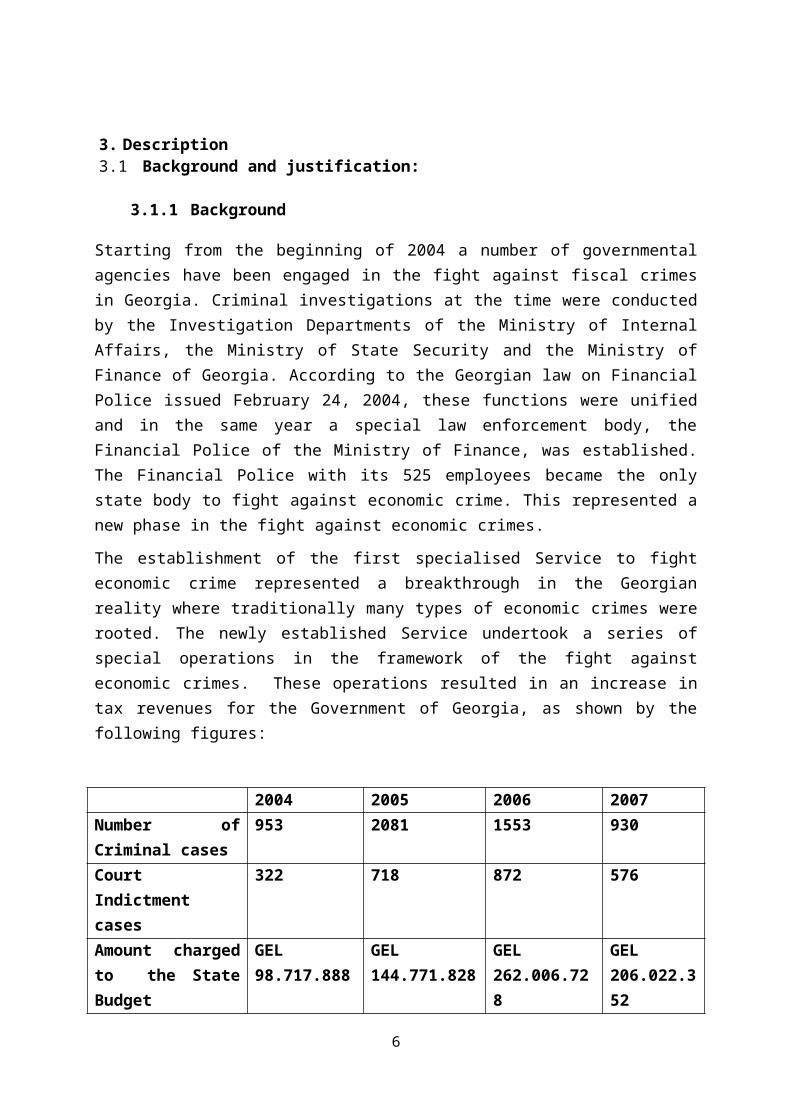

Starting from the beginning of 2004 a number of governmental agencies have been engaged in the fight against fiscal crimes in Georgia. Criminal investigations at the time were conducted by the Investigation Departments of the Ministry of Internal Affairs, the Ministry of State Security and the Ministry of Finance of Georgia. According to the Georgian law on Financial Police issued February 24, 2004, these functions were unified and in the same year a special law enforcement body, the Financial Police of the Ministry of Finance, was established. The Financial Police with its 525 employees became the only state body to fight against economic crime. This represented a new phase in the fight against economic crimes.

The establishment of the first specialised Service to fight economic crime represented a breakthrough in the Georgian reality where traditionally many types of economic crimes were rooted. The newly established Service undertook a series of special operations in the framework of the fight against economic crimes. These operations resulted in an increase in tax revenues for the Government of Georgia, as shown by the following figures:

2004 2005 2006 2007Number of Criminal cases

953 2081 1553 930

Court Indictment cases

322 718 872 576

Amount charged to the State Budget

GEL98.717.888

GEL144.771.828

GEL262.006.728

GEL206.022.352

Amount mobilized in favour of the State Budget

GEL14.470.853

GEL34.364.575

GEL82.144.310

GEL165.501.423

In 2007 the Financial Police, Tax and Customs Departments under the Ministry of Finance (MoF) were united into one Service which was named the Revenue Service of the MoF. As a result of this reorganisation, the cooperation between the different departments became more active, as reflected in the joint definition of priorities and the simplification of coordination between different institutions. An authoritative tax service was set up, and as a consequence the business environment improved. Important steps were taken in the direction of a more effective tax administration.

Starting from 2007 a new phase in the fight against corruption began. The control over the budget became stricter, the level and quality of crime concealment required a strengthening of the operative and investigation activities. The fight against corruption, smuggling and tax evasion demanded a more active and independent contribution from the investigation

4

department of RS. On December 1, 2009 the Law on the Investigation Service was officially adopted and resulted in the establishment of the Investigation Service (IS) of the Ministry of Finance of Georgia as a sub-division of the latter. Officials of the Department of Financial Expertise of the Revenue Service, the Investigation Department and the Special Mission Unit were recruited for the new Investigation Service.

The scope of activities of the IS is based on the following legal acts: Georgian Law on Investigation Service of Ministry of Finance Georgian Law on Operative-Investigation Activity Criminal Code of Georgia Criminal Procedures Code of Georgia Tax Code of Georgia Georgian Law on Public Service Law of Georgia on Interests Conflict and Corruption in Public Service Law of Georgia on Arms and Order №790 of the Minister of Finance of Georgia (November 30, 2009) confirming

the Regulations of the Investigation Service of the Ministry of Finance of Georgia

In accordance with Article 12 of the Law on the Investigation Service of the MoF the IS a sub-division of the MoF and it reports to the President of Georgia and the Minister of Finance.

The Investigation Service is the only entity in Georgia responsible for combating economic-financial crimes. The service carries out its functions on behalf of the state and is accountable to the President of Georgia and to the Minister of Finance of Georgia. The latter is responsible for the supervision and coordination of the activities of the IS

The day-to-day management and administration of the IS comes under the responsibility of the Head of the Investigation Service, who is appointed by the President of Georgia on the basis of a nomination by the Minister of Finance and in agreement with the Prime Minister of Georgia.

There are several stakeholders in the field of investigation of financial and economical crimes in Georgia. These institutions are as following: Investigation Service of the Ministry of Finance, the Chief Prosecutor’s Office of Georgia, and the Ministry of Internal Affairs. According to the Georgian Law on Operative Investigation Activities, the Prosecutor’s office is involved in operational investigation through the classification and justification of activities of IS in the field of fighting Economical-Financial crimes. The Chief Prosecutor’s Office of Georgia comes under the Ministry of Justice (MoJ) of Georgia, and is responsible for the coordination of the fight against economic-financial crimes carried out by the IS. The main function of the Chief Prosecutor’s Office is to conduct criminal prosecution and to supervise the work of the IS.

The cooperation between the Prosecutor’s Office and the IS is smooth and data are exchanged electronically between the two organisations.

The cooperation of the IS with the Ministry of Internal Affairs is based on identical tasks in accordance with the Criminal Code (CC) (for example Article 338 on Accepting Bribes). The Anti-Corruption Department which fights against corruption comes under the Ministry of

5

Internal Affairs. The IS also handled more than 150 cases of corruption in the period of 2004-2012 (on which preliminary investigations were started).

In accordance with the Order #178 issued In September 29, 2010 of the Minister of Justice the investigation of Intellectual Property Right (IPR) crimes come under the competence of the IS. The main stakeholder is the National Intellectual Property Centre of Georgia ,,Sakpatenti”. The activities of the IS in this area are governed by the following national legislation:

Article 1891 Encroachment upon Right of Intellectual Property: a total of 7 cases, out of which 2 cases in 2012 and 1 case in 2013;

Article 196 Illegal Application of Trade (Service) Mark: a total of 24 cases, out of which 1 case in 2012 and 6 cases in 2013;

These Articles were included in the CC of Georgia in 1999. However, due to the social and economic challenges in the country there were difficulties in relation to the enforcement of these laws. Moreover, the relevant authorities lacked the knowledge and capacity required to tackle IPR crimes. With the signing of the AA by the Georgian Government the fight against IPR crimes will become a priority.

The functions of the Investigation Service in this field are as follows:

To detect and prevent crimes committed in the financial-economic field that are within the competence of the Service;

To perform complete pre-trial investigations and, if required, organize and conduct the appropriate examination;

To perform operational and investigation activities for the purpose of crime detection and elimination;

To obtain information and analyse it for further use within the competence of the Service;

To detect and prevent administrative offences in the financial-economic field; To prevent, detect and eliminate crime and corruption bargaining in the financial-

economic field; To perform written tasks and instructions given by the judge and the prosecutor as

well as to assist them within the competence of the Service;

To protect the employees of the system of the Ministry of Finance of Georgia from malpractice in the process of supporting the financial security of Georgia and in the performance of services in accordance with specific rules;

1 Article 189. Encroachment upon Right of Intellectual Property 1. Misappropriation of copyright or any other allied right similar thereof on other person’s scientific, literary or arts piece, invention, useful model, industrial pattern or other result of intellectual-creative, as well as illegal multiplication for distribution purposes, distribution, disposal, public performance, import, export or otherwise use of such piece without a prior consent of the author, other person possessing copyright, or the right allied thereof, - shall be punishable by fine or by corrective labour for up to two years in length. 2. Illegal use or other illegal application of the result of other person’s intellectual-creative activity that is an object of copyright or the right allied thereof, or disclosure of information on invention, useful model or industrial pattern without a prior consent of the author or other person possessing copyright, - shall be punishable by fine or by restriction of freedom for up to two years in length. 3. The action referred to in Paragraph 1 or 2 of this article, perpetrated repeatedly or that has substantially prejudiced the interest of the author, other person possessing copyright or the right allied thereof, as well as coercion into co-authorship, - shall be punishable by restriction of freedom for up to three years in length or by imprisonment similar in length.

6

To support the implementation of the State Tax Policy, develop recommendations to improve cooperation with other stakeholders in the field and mobilize taxes into the State Budget fully and timely within the competence of the Service;

To detect the factors which contribute to the breach of law in a financial-budgetary and cash-credit context and to examine and analyze the specific conditions surrounding these breaches and develop relevant recommendations.

To fight against Customs violations and to render assistance to the tax administration and the customs authorities.

To fight against IPR crimes and violations

The IS has introduced information technology (IT) methods in the fight against IPR-related crimes. All necessary forms and templates for the daily investigation work are available electronically.

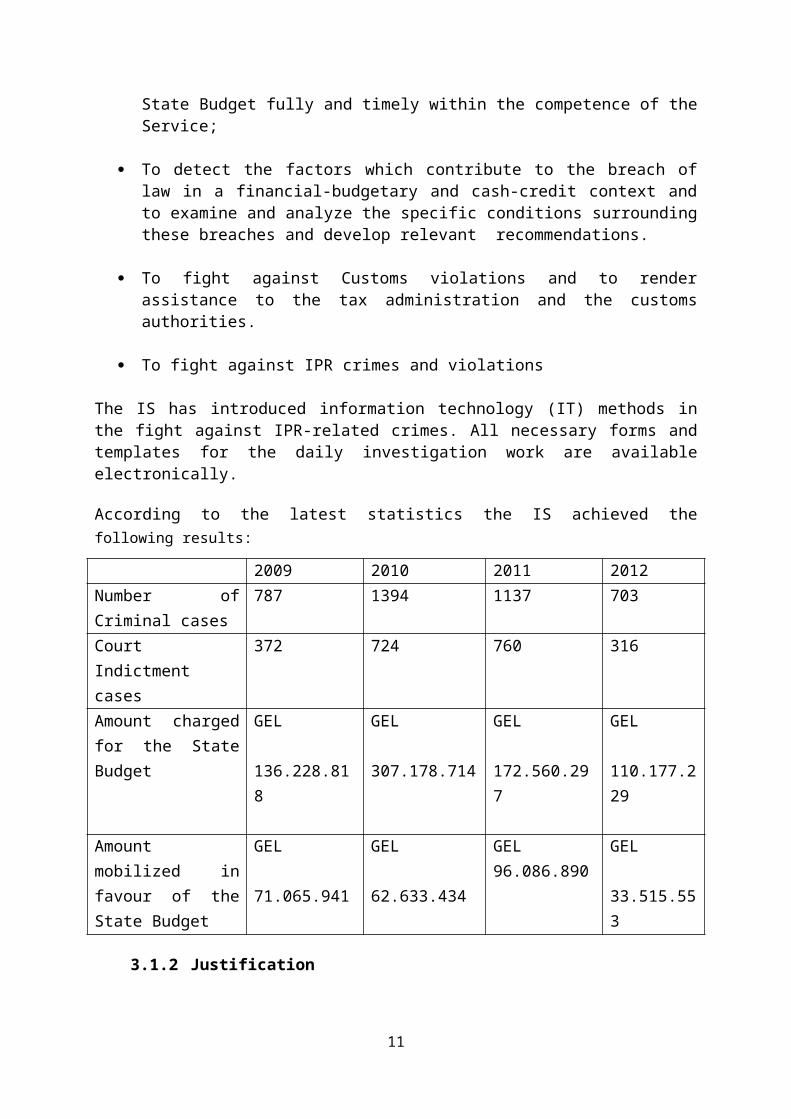

According to the latest statistics the IS achieved the following results:

2009 2010 2011 2012Number of Criminal cases

787 1394 1137 703

Court Indictment cases

372 724 760 316

Amount charged for the State Budget

GEL

136.228.818

GEL

307.178.714

GEL

172.560.297

GEL

110.177.229

Amount mobilized in favour of the State Budget

GEL

71.065.941

GEL

62.633.434

GEL96.086.890

GEL

33.515.553

3.1.2 Justification

In spite of the fact that the IS has come a long way in modernizing its services and controls, there are still areas that require further development and where international assistance and cooperation is of key importance. The work force lacks experience and in-depth knowledge in areas such as human resources development. The introduction and implementation of best EU practices in the field of human resources management (HRM) will contribute to strengthening the sustainability of human resources development inside the IS.

The IS, as a relatively new organisation, needs to train its staff members in legal procedures and rules as well as how to deal with different kinds of economic crimes. The IS equally needs to further develop its IT methods in order to strengthen the analytical capacities of the staff.

The IT Division as well as the Statistics and Analytical Divisions are an important part of the IS. Well trained Information Technology (IT) specialists will be required to enable the IS to

7

cope with future technical challenges, such as the investigation of different kinds of IT crime, the preparation of digital evidence, and the set-up of the IS’ own databases.

The Tax Policy Department of the Ministry of Finance of Georgia is responsible for the legislation related to taxation measures. The IS also has important legal requirements to fulfil in the areas of legislation covered by the Association Agreement which is expected to be initialled toward the end of 2013. Due to the differences in terminology and structure between the Criminal Code of Georgia and corresponding EU standards, it is important for the IS to be able to access EU expertise in the field at an early stage in order to ensure a smooth and successful approximation process.

Georgian legislation contains no (legal) definition of tax evasion, only a description of the punishment. Tax evasion, however, is a priority activity of the IS, as shown in the following figures:

Art. 210 CC False Tax documentation 1325 cases of preliminary investigation Art. 218 CC Tax evasion 1348 cases of preliminary investigation

The definition of money laundering needs revision (Article 194 of the CC)2 in order to comply with EU legislation. European legislation in this field was adopted in order to protect the financial system including vulnerable professions and activities from being misused for money laundering and financing of terrorism purposes.3

The above provided figures regarding IPR crime cases show that there is a need to develop the methodology and expertise linked to the fight against IPR-related crimes. This should include raising the awareness and building the capacity of the investigators fighting IPR crimes. Currently the IS has very limited experience and knowledge in this field and is therefore not able to carry out its responsibilities in the sector in an effective manner.

The successful implementation of the project will contribute to strengthening the administrative capacity of the Investigation Service by increasing the efficiency and effectiveness of its investigation functions.

The project will equally contribute to the implementation of the PCA, ENP AP and the AA. Georgia wishes to improve its legislation and its internal procedures, and to fulfil the commitment taken under the Association Agreement between the Government of Georgia and the EU on the implementation of measures to prevent and fight fraud, corruption and other illegal activities. The exchange of information and further cooperation at operational level will be enhanced.

2 Article 194. Legalization of Illicit Income 1. Legalization of illicit income, i.e. giving a legal form to money or other property, as well as concealing the source, location, allotment, circulation of illicit income, the actual owner or possessor of property or property right, - shall be punishable by fine or by imprisonment for up to five years in length.

3 Directive 2005/60/EC of the European Parliament and of the Council of 26 October 20058

3.2 Linked activities (other international and national initiatives):

There have been relatively few activities by other donors directly targeting investigation policy. These have mainly consisted in workshops (see Annex 2 for a list of the activities undertaken by other donors in this field).

3.3 Results

Result 1: Draft of the revised legal framework and new instructions for the Investigation Service are in place.

Result 2: Human Resources Division has implemented new methods of effective management of the staff of Investigation Service.

Result 3: New rules and procedures are introduced to combat tax fraud and tax fraud related crimes in accordance with the EU standards.

Result 4: The Investigation Service has developed and improved rules and procedures in the area of risk analysis and management.

Result 5: Rules and procedures of fighting against IPR related crimes are established based on the EU best practice.

3.4 Activities:

The activities set out in this section and the proposed method of implementation, are indicative and should, where appropriate, be revised during the preparation of the work plan and contract between the IS and the MS administration. In developing their proposals, potential Twinning Partners are invited to propose their own solutions, based on their own experience.

3.4.1 General Activities

3.4.1.1 Kick-off Conference

Method: The first month of the project will see the arrival of the Resident Twinning Advisor (RTA) in Georgia and her/his familiarisation with the local surroundings. The RTA will be located at the Investigation Service. During this time, she/he will be introduced to the Beneficiary

9

Country stakeholders4, the RTA counterpart, and key officials within the IS. The RTA will hire two assistants (RTA Assistant and Translator) through an appropriate selection procedure (as foreseen in the Common Twinning Manual).

A one day ‘kick-off’ conference will be held in the first month aimed at launching and presenting the project to the stakeholders, the media, and the public at large. In order to inform the public about the start of the project and to conform to the EU visibility requirements, the meeting will be concluded with a press conference and a press release.

Also in the first month, the RTA will establish working relations with the leaders of other bilateral co-operations and form a formal co-ordinating committee, including IS senior management, which will be tasked with ensuring that the different projects run smoothly and that there is no overlap with activities. The group will meet periodically as required.

Benchmark: Stakeholders, media and public informed about the start and content of the project.

Resources: RTA + PL + Interpretation + Translation.

3.4.1.2 Final Conference

Method: During the last month of the project, a final ‘closing’ conference will be organised at which the results of the project will be presented. The conference should include presentations on the project’s achievements and the challenges still facing the IS.

Benchmark: Stakeholders, media and the public informed about the project’s achievements and the remaining challenges for the IS, in particular, and public accountability more generally.

Resources: RTA + PL + STE days + Interpretation + Translation

3.4.2 Activities for Result 1. Draft of the revised legal framework and new instructions for the Investigation Service are in place.

Activity 1.1 Assessment and analysis of the existing Criminal Code and Criminal Procedure Code of Georgia based on the international standards in the field of criminal law

4 Stakeholders are: Investigation Service of the Ministry of Finance, the Chief Prosecutor’s Office of Georgia, the Ministry of Internal Affairs and the National Intellectual Property Centre of Georgia ,,Sakpatenti”.

10

Method: STE assesses structural and procedural differences between CC and CPC of Georgia and international criminal legislation. Prepares report on findings and recommendations for improvement.

Benchmarks: Assessment carried out, report on proposals delivered, STE mission report delivered

Resources: STE, interpretation

Activity 1.2 Drafted amendments to the Criminal Code of Georgia according EU standards to define special kind of crimes for performing procedures and regulations on modern standards according to Activity 1.1; translation completed.

Method: STE together with the BA will analyses the findings of activity 1.1. Legislative changes are proposed based on these findings. STE holds workshop with IS staff from the Investigation Department and the Legal Division to review the proposed changes and amendments together with stakeholders. Report on results of the workshop to be prepared. Draft amendments to the Criminal Code of Georgia to be prepared by STE in cooperation with IS staff

Benchmarks: Workshops conducted. Drafted amendments to the Criminal Code of Georgia according EU standards delivered, STE mission report delivered

Resources: STE, interpretation

Activity 1.3 Drafted changes and amendments to the relevant laws to achieve further alignment with EU Directives referring to tax fraud legislation; translation completed.

Method: Working group will be created and together with the STE the WG will elaborate the relevant amendments to the laws. STE analyses the existing laws. Legislative changes are proposed based on these findings. STE holds workshop with BA to review the proposed changes and amendments together stakeholders. Report on results of the workshop to be prepared. Draft amendments to the relevant laws to be prepared by STE in cooperation with IS staff

Benchmarks: Working group created. Workshops conducted. Draft changes and amendments delivered.

Resources: STE, interpretation

11

Activity 1.4 Draft operational instructions for investigators based on outcomes of the activities 1.2, and 1.3.

Method: STE will draft operational instructions for the IS concerning the relevant amendments in accordance with EU best practices. Draft operational instructions are discussed and agreed with the BA

Benchmarks: Operational instructions drafted

Resources: STE, interpretation

Activity 1.5 Training based on new instruction for the relevant IS staff, Prosecutor’s office and the Revenue Service

Method: STE together with the BA will identify 25 trainees; STE will elaborate the training materials. STE will conduct the training in accordance with findings of activity 1.4

Benchmarks: Training programme and training materials produced. Training sessions carried out.

Resources: STE, interpretation

3.4.3 Activities for Result 2. Human Resources Division has implemented new methods of effective management of the staff of the Investigation Service

Activity 2.1 Review of the present system and the structure of the IS

Method: STE carries out analysis of the existing system and the structure of the IS; In coordination with the BA and relevant stakeholders, STE will draft the recommendations for the improvement of the IS structure for better operation.

Benchmarks: Analytical report prepared, recommendations elaborated

Resources: STE, interpretation

Activity 2.2 Draft action plan/roadmap of changes according to the findings of the activity 2.1

Method: STE and BA jointly draft action plan/road map of the procedures to be implemented for the improvement of the IS structure and system based on the recommendations elaborated in activity 2.1

Benchmarks: Action plan/road map delivered.

12

Resources: STE, interpretation

Activity 2.3 Perform gap and needs analysis of the Human Resource Management system of the IS

Method: STE performs a Gap and Needs Analysis of current system and prepares report with proposals for possible improvement of the HRM system. Proposals to be reviewed by the relevant staff of the IS.

Benchmarks: Analysis performed, and GNA report delivered, recommendations elaborated

Resources: STE, interpretation

Activity 2.4 Elaborate operational handbook for the IS inspectors and investigators

Method: STE together with BA will prepare a handbook for IS inspectors and investigators. The handbook will be presented to the relevant IS staff.

Benchmarks: handbook is elaborated

Resources: STE, interpretation

Activity 2.5 Development of the methodology of the conducting the training needs analysis for the inspectors and investigators of the fiscal and criminal crimes

Method: STE develops methods and tools in Training need analysis specifically for the professionals working in the field of the economical and fiscal crimes. STE together with the BA conducts a workshop to present the elaborated methodology for the relevant staff of the IS.

Benchmarks: methodology is elaborated, workshop conducted.

Resources: STE, interpretation

Activity 2.6 Training of management staff of the IS in the effective Human Resources Management tools

Method: STE develops the training program and materials. STE conducts the training for the heads and deputy heads of the departments and divisions (20 persons) in HRM tools and effective motivate tools for the IS employees

13

Benchmarks: Training programme and training materials produced. Training sessions carried out.

Resources: STE, interpretation

3.4.4 Activities for Result 3. New rules and procedures are introduced to combat tax fraud and tax fraud related crimes in accordance with the EU standards

Activity 3.1 Conduct a Gap and Needs analysis to establish divergences between Georgian Tax Code, Criminal Code and EU Directive, and to establish articles where assistance with interpretation is needed

Method: STE performs a Gap and Needs Analysis (GNA) of exiting Georgian Tax Code, Criminal Code to establish divergences between Georgia Tax Code (articles related to the criminal cases) and other legislation and the EU directives. Establish articles which need further interpretation and clarification assistance by STE. The result of the GNA is presented in a report.

Benchmarks: Analysis prepared, GNA report delivered

Resources: STE, interpretation

Activity 3.2 Develop guideline on combating VAT fraud

Method: STE analyses the existing regulations and situation in the country in the field of combating VAT fraud, based on the findings develops a guideline on combating VAT fraud in line with EU experience.

Benchmarks: Guideline on combating VAT fraud developed

Resources: STE, interpretation

Activity 3.3 Conduct training courses with specialized staff of the IS regarding modern methodology of combating the VAT fraud

Method: STE elaborates the training materials and conducts train for 60 persons in combating the VAT fraud with regards to the new guidelines

Benchmarks: Training programme and training materials produced. Training sessions carried out.

Resources: STE, interpretation

14

Activity 3.4 Develop effective methodology of fighting against money laundering

Method: STE will analyze and asses the current money laundering legislation, drafts the recommendations for improvement and together with the BA develops methods of fighting against money laundering. Findings, recommendations and methodology is presented to the relevant authorities and BA staff

Benchmarks: Assessment performed, recommendations drafted. Methodology elaborated

Resources: STE, interpretation

Activity 3.5 Training of the IS staff in combating money laundering

Method: STE elaborates training methods on money laundering and conducts training course for 60 persons.

Benchmarks: Training programme and training materials produced. Training sessions carried out.

Resources: STE, interpretation

Activity 3.6 Improve knowledge of IS staff through training course regarding combating cyber crime (or computer crime)

Method: STE elaborates training materials and conducts trains for 30 persons in effective countermeasures to combat cyber crime.

Benchmarks: Training programme and training materials produced. Training sessions carried out.

Resources: STE, interpretation

Activity 3.7 Developed instructions for internal training of trainers for IS staff (training for trainers scheme) to ensure that current investigation knowledge of VAT fraud including money laundering and cyber crime is available.

Method: STE prepares training materials to hold interactive trainings with 20persons of the BA in investigation of VAT fraud including money

15

laundering and cyber crime. Trainings to be given using ToT methodology.

Benchmarks: Training material prepared. Trainings carried out

Resources: STE, interpretation

Activity 3.8 Conduct study visit to MS to improve experience and practical use of investigating tax evasion and cyber crime

Method: MSA arranges study visit to a MS partner of the Twinning project, where 7 IS staff will have the possibility to gain operational experience in the investigating tax evasion and cyber crime during 5 working days. Study visit report to be prepared with experiences and conclusions made.

Benchmarks: Study visit conducted, report delivered

Resources: MSA, study visit costs (flight tickets, per-diems).

Activity 3.9 Conduct study visit to MS to improve experience and practical use of money laundering

Method: MSA arranges study visit to a MS partner of the Twinning project, where 7 IS staff will have the possibility to gain operational experience in the investigating money laundering during 5 working days. Study visit report to be prepared with experiences and conclusions made.

Benchmarks: Study visit conducted, report delivered

Resources: MSA, study visit costs (flight tickets, per-diems).

3.4.5 Activities for Result 4. The Investigation Service has developed and improved rules and procedures in the area of risk analysis and management.

Activity 4.1 Analyze and assess the current risk analysis system, available information and criteria of risk assessment (Intelligence Standards).

Method: STE will analyse and assess the current risk analysis system, available information and criteria. Need for further information from different sources such as third parties, will be assessed. Proposals for amendments to be implemented and development of criteria according

16

to assessment prepared in report. If possible implement new criteria in risk analysis system to best EU practice.

Benchmarks: Analysis and assessment carried out, report delivered.

Resources: STE, interpretation

Activity 4.2 Prepare required manual of risk assessment (Intelligence Standards)

Method: STE produces manual for Intelligence Standards together with IS staff based on the findings of the activity 4.1 and use of Law Enforcement Programme Standards documents. STE conducts a workshop of the BA to present and discuss the manual.

Benchmarks: Manual prepared. Workshop conducted

Resources: STE, interpretation

Activity 4.3 Draft the recommendations regarding the improvement of methods for further information, cooperation and communication.

Method: STE will assess the exiting information, cooperation and communication system of the IS. STE will draft the recommendations to support the IS to develop an efficient system of collecting and exchanging intelligence data in the IS with relevant international organization including open sources

Benchmarks: Assessment conducted. Recommendations drafted. Report prepared

Resources: STE, interpretation

Activity 4.4 Training of the relevant IS staff members in new criteria of risk assessment and methods in risk analysis system according to Activity 4.1, 4.2 and 4.3

Method: STE prepares training materials to hold interactive trainings with 20 persons of the BA in risk management and risk analysis.

Benchmarks: Training programme and training materials produced. Training sessions carried out.

Resources: STE, interpretation

17

Activity 4.5 Conduct Study visit to MS to experience practical use of risk management

Method: MSA arranges study visit to a MS partner of the Twinning project, where 8 IS staff will have the possibility to gain practical experience in risk management during 12 working days. Study visit report to be prepared with experiences and conclusions made.

Benchmarks: Study visit conducted, report delivered

Resources: MSA, study visit costs (flight tickets, per-diems).

Activity 4.6 Conduct Study visit to MS to experience practical use of IT system related to investigation of financial and economic crimes

Method: MSA arranges study visit to a MS partner of the Twinning project, where 7 IS staff will have the possibility to gain practical experience in IT system 5 working days. Study visit report to be prepared with experiences and conclusions made.

Benchmarks: Study visit conducted, report delivered

Resources: MSA, study visit costs (flight tickets, per-diems).

3.4.6 Activities for Result 5. Rules and procedures of fighting against IPR related crimes are established based on the EU best practice

Activity 5.1 Assess the current situation concerning the IPR crimes in Georgia

Method: STE will conduct analysis and assessment of the Georgian situation in IRP crimes

Benchmarks: Assessment performed, report drafted

Resources: STE, interpretation

Activity 5.2 Develop Action Plan for the investigators to effective combating IPR crimes in Georgia

Method: MSA and BA create a working group (WG), the WG will consist with STE of the MSA, relevant IS staff and other stakeholders. The WG together with the STE will develop an Action Plan aiming combating IPR crimes in Georgia, Conduct workshop in order to present the developed Action Plan with participation of IS staff, National Intellectual Property Center of Georgia (Sakpatenti) and Prosecutor’s office

Benchmarks: Working group established, Action Plan drafted

18

Resources: STE, interpretation

Activity 5.3 Train officers in the field of Investigation of Intellectual Property Rights crimes

Method: STE will elaborate training materials and conducts 10 days train course for 15 IS officers specialized in identification and investigation of the IPR crimes in Georgia

Benchmarks: Training material elaborated. Training conducted

Resources: STE, interpretation.

Activity 5.4 Conduct Study visit to MS to experience practical use of investigating IPR crimes

Method: MSA arranges study visit to a MS partner of the Twinning project, where 7 IS staff will have the possibility to gain practical experience in combating IPR crimes 5 working days. Study visit report to be prepared with experiences and conclusions made.

Benchmarks: Study visit conducted, report delivered

Resources: MSA, study visit costs (flight tickets, per-diems).

3.5 Means/ Input from the MS Partner Administration:

3.5.1 Profile and tasks of the Project Leader

Role and tasks

The Project Leader will direct, co-ordinate, and control the overall thrust of the project. He/she will lead the activities of the project, ensure the achievement of the results, be responsible for the implementation of the activities and, with the support of the RTA, produce progress reports.

The Project Leader is expected to devote a minimum of three days per month to the project in his home administration, not in Georgia. In addition, as Co-Chairman, he/she should co-ordinate, from the Member State side, the Project Steering Committee (PSC), which will meet in Georgia at least every three months.

Profile

Qualification and skills:

Good English language skills, both spoken and written; Good inter-personal skills;

19

Command of the Georgian language would be a strong asset.

General professional experience:

Long term civil servant from the MS administration; Minimum 8 years of professional experience; Experienced project manager, demonstrating good record in organisational leadership,

staff motivation, and communication.

Specific professional experience:

Knowledge and experience of investigation of fiscal and economical crimes and EU legislation.

Currently belonging to a Member State finance administration.

3.5.2 Profile and tasks of the RTA

Role and tasks

The RTA will be responsible for the day-to-day management and implementation of the project. He/she will be responsible for co-ordinating all the different activities and inputs and for liaising with the RTA Counterpart in the Investigation Service of the Ministry of Finance of Georgia. Specifically, the RTA will be responsible for:

Overall supervision of the project implementation and co-ordination of all activities, as well as managing the project administration;

Co-ordinating the activities of team members in line with agreed work programs to enable timely completion of project outputs;

Providing technical input to the project whenever needed and providing advice in their field of expertise;

Liaising with MS and BC Project Leaders and ensuring on-going regular contact with the RTA Counterpart;

Liaising with the EU Project Manager; Liaising with key stakeholders (e.g. other relevant projects and Georgian institutions).

The RTA will provide 21 months input on site (including leave) and will be based in an office in the IS.

Profile

Qualification and skills:

University level education, or professional qualification, preferably in accounting, business studies, or related discipline;

Excellent English language skills, both spoken and written, and command of the Georgian language would be a strong asset;

PC Computer literacy; Good inter-personal skills.

20

General professional experience:

Civil Servant from an EU MS Administration; Minimum 7 years of professional experience; Experienced project manager, demonstrating good record in organisational leadership,

staff motivation and communication; Excellent team-working skills; Strong analytical skills;

Specific professional experience:

At least 5 years’ experience in investigation of economic and fiscal crime, preferably in a management role;

Relevant working experience in Eastern European and/or transition economies of the ENP countries would be an asset.

3.5.3 Profile and tasks of the short-term experts

Tasks of short term expertise

Terms of Reference for short-term experts will be elaborated by Project Leader/RTA at the work plan preparation stage.

Profile of short term expertise

To cover all the 31 activities described in 3.4 there must be different short term experts with a set of different skills and qualifications. The actual duration of the assignments of each of the short-term experts will be defined during the drafting of the twinning agreement. The short term experts will work in close co-operation with the Project Leader/ RTA and the Beneficiary in order to meet the specific objectives as set out above.

The exact number of short term experts and their required qualifications should be identified by the Project Leader/RTA in the course of designing the delivery of the project. But in order to cover the activities to be performed in the project the short term experts are expected to have following qualifications and skills:

General:

University degree or relevant professional background in tax administration of minimum 7 years.

At least 5 years working experience in their respective field of expertise Sound knowledge of relevant EU legislative and institutional requirements related to the

various components of this project Very good command of English (oral and written) Good writing and presentation skills Good training and facilitation skills Excellent computer skills (Word, Excel, Power Point);

21

Specific:

STE on Legislation and Human Resources Management

Expertise in Criminal laws legislation and instructions Expertise in motivation and promotion Expertise in Job Tasks Analysis Expertise in Training Needs Analysis

STE on Fiscal and Economic Crimes

Expertise in VAT legislation and in implementation of EU VAT Directives in national legislation

Expertise in tax evasion, especially VAT fraud Expertise in money laundering Expertise in cyber crime Expertise in IPR crime

STE on Risk Management

Expertise in development of risk analysis system and risk criteria Experience in developing and managing IT systems for the Investigation Service

Terms of Reference for short-term experts will be elaborated by Project Leader/RTA at the work plan preparation stage.

4 Institutional Framework

The main Beneficiary Institution (BI) of the project is the Investigation Service (IS) of the Ministry of Finance (MoF) of Georgia. For the criminal investigation activities the Prosecutor’s office will also be Beneficiary Institution together with the IS and regarding legal amendments of the project the Tax Policy Department of the MoF.

Overview of the structure of the IS

22

Head of Service

Deputy Head of Service

Deputy Head of Service

Special Mission Unit

Investigation Department

Operational –Technical Support

Department

Economic Department

Division for Fighting Against Customs Rules

Violations

Tbilisi Main Division

Kakheti Regional Division

Internal Inspection

Division

Administration

Statistics and Analytical Division

Main Division for Especially

Important Cases

Operative Registration

Division

Human Resources Division

Chancellery

Legal Issues and International

Relations Division

Information Technology Division

Logistics Division

Accounting and Reporting Division

Shida KartliRegional Division

Kvemo KartliRegional Division

Samtskhe-Javakheti

Regional Division

Samegrelo-ZemoSvaneti Regional

Division

Imereti-RachaLechkhumi

Regional Division

Adjara and GuriaRegional Division

Mtskheta-Mtianeti

Regional Division

Public Relations Division

Special Research and Expertise Department

As this overview of the structure of the IS shows there are two deputies responsible for the Administration, Economic, and Investigation Departments.

Directly subordinated to the Head of Service is the Internal Inspection Division (7 staff members), the Special Mission Unit (85 staff members) and the Operational Technical Support Department (110 staff members).

The number of employees in each Division/Department is divided as follows: Economic Department (1) – Logistics Division (3) – Accounting Division (3); Administration (5) – HR Division (5) – Chancellery (6) – Legal Issues and international

Relations Div. (3) – IT Division (7) – Public Relations Div. (3); Special Research and Expertise Department (19); Investigation Department (6) – Statistics and Analytical Div. (10) – Operative

Registration Div. (4) – Main Division for Important Cases (43) – Division for Fighting Against Customs Rules Violation (33);

and 9 Regional Divisions (Tbilisi Main Division 123 and the other 8 in total 190 staff members);

The IS has a total of 670 employees, including 60 interns.

23

Required contributions of BC:

Office space: Sufficient office space shall be allocated by the IS to the MS Twinning Partner for the Project Leader, the RTA and for the short-term experts on mission. Meeting space will be provided when necessary.

Logistical support: The project office at the IS will be furnished with necessary number of telephones and PC’s. The IS shall also make available vehicle(s) for the purposes of the project.

5. Budget

Euro 1, 230,000 million.

6. Implementation Arrangements6.1 Implementing Agency responsible for tendering, contracting and accounting (AO/CFCU/PAO/Commission), including contact person and full contact details.

The European Union Delegation in Tbilisi, Georgia, will be responsible for the tendering, contracting, payments and financial reporting, and will work in close co-operation with the Beneficiary. The person in charge of this project at the Delegation of the European Union to Georgia is:

Mr.Irakli KhmaladzeProject Manager, Economics and Public FinanceDelegation of the European Union to Georgia38 Nino Chkheidze St, 0102 Tbilisi, Georgia Tel: +995 32 2943 763E-mail: [email protected]

The Project Administration Office (PAO) of the Office of the State Minister of Georgia on European and Euro-Atlantic Integration will support the Twinning Project implementation process together with the EU Delegation. The person in charge of this project is:

Mr Roman Kakulia

Head of Project Administration Office (PAO) in Georgia,Office of the State Minister of Georgia on European and Euro-Atlantic Integration7, Ingorokva Street, Tbilisi 0134, GeorgiaTel: +995 32 299 89 14e-mail: [email protected]

6.2 Main counterpart in the BC

Project Leader:Mrs Tamar MachavarianiDeputy Head of the Investigation Service of Ministry of Finance of GeorgiaUniversity st. 2a; Tbilisi 0177, GeorgiaTel:+995 32 2261970

24

e-mail: [email protected]

RTA counterpartMr Giorgi GogadzeHead of Legal Issues and International Relations Division of the Investigation Service of Ministry of Finance of GeorgiaUniversity st. 2a; Tbilisi 0177, GeorgiaTel: +995 32 2262013e-mail: [email protected]

6.3 Contracts

The Project will be implemented in the form of a twinning contract between Georgia and an EU Member State.

7 Implementation Schedule (indicative)7.1 Launching of the call for proposals (Date) May 20147.2 Start of project activities (Date) October 20147.3 Project completion (Date) June 20167.4 Duration of the execution period (number of months)

The implementation period will be 21 months. Legal duration of the Twinning contract, including periods for start-up and completion of activities, is 23 months in accordance with the Twinning Manual 2012 (update 2013-2014).

8 Sustainability

The achievements of a Twinning project (mandatory results) should be maintained as a permanent asset to the Beneficiary administration even after the end of the Twinning project implementation. This presupposes inter alia that effective mechanisms are put in place by the Beneficiary administration to disseminate and consolidate the results of the project.

The Beneficiary Institution is fully committed to ensure the long term impact of the Twinning project. During the project implementation, the twinning partners should develop documents/handouts, guidelines that will be easily accessible for later use by the beneficiary administration. Staff benefiting from trainings/study visits shall transfer knowledge through subsequent training to their colleagues at all levels. The BA participants in project activities should be asked to provide feedback, in the form of short evaluation sheets (or questionnaires), to establish how they consider the value of the activity

9 Crosscutting issues (equal opportunity, environment, etc…)

Equal Opportunities and non-discrimination

25

The principles and practice of equal opportunity will be guaranteed so as to ensure equitable gender participation in the project. The principle of equal opportunity shall apply both to the IS staff involved in the project and project members participating from contracting authority/ies. Every effort will be made to ensure broad gender representation among all participants.

Environment and climate change

Not applicable

Minorities and vulnerable groups

Minority and vulnerable groups' concerns will be reflected in all activities of the project. Participation in the project activities will be guaranteed on the basis of equal access regardless of racial or ethnic origin, religion or belief, disability, sex or sexual orientation.

10 Conditionality and sequencing

This Twinning Project Fiche has been drafted in close cooperation with the Georgian counterpart, which commits itself to provide the contributions stated in the Fiche. They include such as:

Strong commitment and support of IS management to the Project implementation Strong involvement and commitment of IS staff at all levels Assigning dedicated staff to activities connected with the Project Ensuring coordination between departments and institutions connected with the

Project Ensuring access to indispensable information and documents Supply of office room for the RTA for the entire duration of the Project, including

access to computer, telephone, internet, printer, photocopier Adequate conditions for the STEs to perform their work while on mission to the BI Providing suitable venues and equipment for the training sessions and meetings that

will be held under the Project Designating a IS counterpart for each MS expert

26

The list of Acronyms:

Glossary: Abbreviation MeaningAA EU-Georgia Association AgreementBI Beneficiary InstitutionCC Criminal CodeCPC Criminal Procedure CodeCLDP Commercial Law Development ProgrammDG TAXUD Directorate General Taxation and Customs UnionEC European CommissionEEC European Economic CommunityENP (AP) European Neighbourhood Plan (Action Plan)ENPI European Neighbourhood Plan InstrumentEU European UnionEUR The European Union Currency ‘Euro’GEL Currency of Georgia ‘Lari’GEPLAC Georgian European Policy and Legal Advice CentreGRS Georgia Revenue ServiceIFC International Finance CorporationIMF International Monetary FundIPR Intellectual Property RightsIS Investigation Service MOF Ministry of FinanceMOU Memorandum of UnderstandingMS Member StateMSA Member State AdministrationNIP National Indicative ProgrammePAO Programme Administration OfficePCA Partnership and Cooperation AgreementPL Project LeaderPSC Project Steering CommitteeRS Revenue ServiceRTA Resident Twinning AdviserSTE Short Term ExpertTA Technical AssistanceToT Training of TrainersTAIEX Technical Assistance Information Exchange UnitUSAID United States Agency for International DevelopmentVAT Value Added TaxWIPO World Intellectual Property Organisation

27

ANNEXES TO PROJECT FICHE

1. Logical framework matrix in standard format (compulsory)2. Detailed implementation chart (optional)3. The list of the activities undertaken by other donors

28