Embed Size (px)

DESCRIPTION

jhgiuygfuygiugfiufiugfiugiuogfiugfiugfiuygffuyfuyfuyfuyfuyfuyuyfuyfuyfuyfuyfuyfuyfuyfuyfuyfuyfuyf

Citation preview

CHAPTER ONE ABOUT THE REPORT

1.1About Internship

The part ‘Internship’ indicates practical training in any area. Stated in other word internship is practically training in any real field where theoretical knowledge is practically applied. In academic teaching student become aware of common rules and principles that should be followed in the typical situations due to various reasonable causes. The participants of practical training become acquainted with practical rules that in follow in practical situation. They also become aware of how practical practice deviate from theoretical principles. Thus internship program expands the knowledge and it fulfills the theoretical knowledge of the participants.

Therefore in single word it would be called that internship is a process by which the acquired knowledge if the participant become expanded by application of academic knowledge in practical field.

1.2 Origin of the Report

The report is originated from the curriculum requirement of BBA program of American international university. The topic of my report is “Accounts Payable – Internal Control System, Compliance and Recording Process of Incepta Pharmaceuticals Ltd.”. The report has been prepared under direct supervision of Kazi Tanvir Mahmud Ph.D Assistant Professor, Department of Economics, Faculty of Arts & Social Sciences, AIUB and Md. Touhidun Nabi khan Accounts Officer, Finance & Accounts, Incepta Pharmaceuticals Ltd.

1.3 Background of the study

Accounts payable are unpaid obligations for goods and services received in the ordinary course of business. It is identified by the existence of vendor’s invoices for obligation. A large number of transactions are affected by accounts payable.

So it is important to maintain this account in such a way that possible misstatements, fraudulent activities or any other risks related to this account can be avoided. Incepta Pharmaceuticals Ltd. is one of the large local organizations in our country. It has plenty of vendors both local and foreign. Md. Touhidun Nabi khan, Accounts Officer, Finance & Accounts Department of Incepta Pharmaceutical Limited asked me for designing the existing methodology of recording process, compliance and internal control system of accounts payable of Incepta Pharmaceuticals Ltd.

1

1.4 Benefits to the organization through this report

The Institution will get an overall picture on internal control and recovery process of this report. It may take steps to overcome its shortages or weakness; at the same time it may explore the opportunities it does have.

1.5 Scope of the Report

The scope of my study is only about accounts payable- its recording process, compliance and internal control. The report describes about the existing procedure of recording process of accounts payable of Incepta Pharmaceuticals, the rules and regulations followed by it and the existing internal control system relating to this account. The report is prepared on the basis of interviews with personnel of accounts and finance department of IPL. My scope of work is limited to local transaction. For understanding the internal control system of accounts payable there is lots of audit related work. But as an intern I am not allowed to do that type of work.

1.6 Objective of the Report

The main objective of preparing this report is to fulfill the requirement of BBA program. This contains three credit hours for internship and to apply the theoretical knowledge gained from the coursework of the BBA program in a specific field. The other objectives are;

Broad Objective

The objective of this study is to determine the recording process, compliance and internal control.

Specific Objectives

The specific objectives of the study are to-

Know the ability of employees to perform promised service dependently and accurately.

To get an introduction about the organizational structure & how co-ordination among

different set of activities is made.

To know about the procedures of acquisition and payment.

To be familiar with internal control system of accounts payable payment procedure.

To get an idea about the related compliance of accounts payable

To relate the theoretical leanings with the real life situation.

2

1.7 Methodology of the Report

This report has been prepared on the basis of experience, which I was gathered during the period of internship. For preparing this report, I have also got information from various employees of IPL (Purchase Dept., Planning Dept., Accounts Dept., and Human Resources Dept. etc), different books and website of the Incepta Pharmaceutical Limited.

1.8 Data processing and Analysis

Data collected from primary and secondary sources have been processed and analyzed manually and qualitative approach has been used throughout the study. Data has been analyzed by using computer program with the help of Microsoft Word, and Microsoft Excel.

Primary sources

Practical deskwork

Face to face conversation with the officer

Direct observations

Face to face conversation with the client

Secondary sources

Annual report of IPL

Files & Folders

Various publications on IPL

Employee database prepared by HRD

Audit Report

Website

3

1.9 Limitation of the Report

Limitations may conflict the study, but among those some major limitations have been mentioned below: -

The duration that is for internship is not enough to learn about a big organization like Incepta Pharmaceuticals Limited.

For non-availability of secondary data and for time limitation it was not possible to work on the basis of board data.

Due to restriction of time, I could not get detailed information about every Departments of IPL.

Lack of confidential information about the organization makes many mistake and targeted aim.

It was very different to collect the information from various personnel for the job constrain.

Incepta policy was not disclosing some data and information for obvious reasons.

Lack of experiences has acted as constraints in the way of meticulous exploration on the topic.

Internet speed is very slow (outside) for collecting necessary data in time.

4

CHAPTER TWO AN OVERVIEW OF INCEPTA PHARMACEUTICAL LIMITED

2.1 History of Incepta Pharmaceutical Limited (IPL)

Incepta Pharmaceuticals Ltd. is a leading pharmaceutical company in Bangladesh established in the year 1999. The company has a very big manufacturing facility located at Savar, 35 kilometer away from the center of the capital city Dhaka. The company produces various types of dosage forms which include tablets, capsules, oral liquids, ampoules, dry powder vials; powder for suspension, nasal sprays etc. Since its inception, Incepta has been launching new and innovative products in order to fulfill unmet demand of the medical community. The focus was to bring more new technologically advanced molecules to this country.

The company specializes in value added high technology dosage form like sustained release tablets, quick mouth dissolving tablets, barrier coated delayed release tablets etc. It has established a modern research and development laboratory for the development of new advanced dosage forms for various drugs and devices like poorly soluble drugs, dry powder inhalers, coated pellets, modified release products, taste masked preparation etc.

Incepta quickly developed a very competent sales team, which promotes the specialties throughout the country. The company virtually covers every single corner of the rural as well as urban area of Bangladesh. It has its own large distribution network having 13 depots all over the country. The company has a clear vision to become a leading research based dosage form manufacturing company with global presence within a short period of time.

The Research and Development department for various dosage forms has been very well developed. Incepta intends to bring newer products of advanced technology through research hitherto unknown in this country. Such activities will not only benefit the company but also the total pharmaceutical sector of the country. In the post 2005 era, the company also intends to embark into the production of Active Pharmaceutical Ingredient (API). Plans are underway to get into reverse engineering and analogue research in order to produce new API.

The company is now expanding its activities beyond the geographical boundary of Bangladesh. The products are of high standard and therefore these will be exported to both developed and developing countries. The company is open to collaborate with interested parties in various countries. The future is wide open and the opportunities

Incepta will continue to strive to provide high quality medicine at affordable prices to the people here in Bangladesh and other parts of the globe.

5

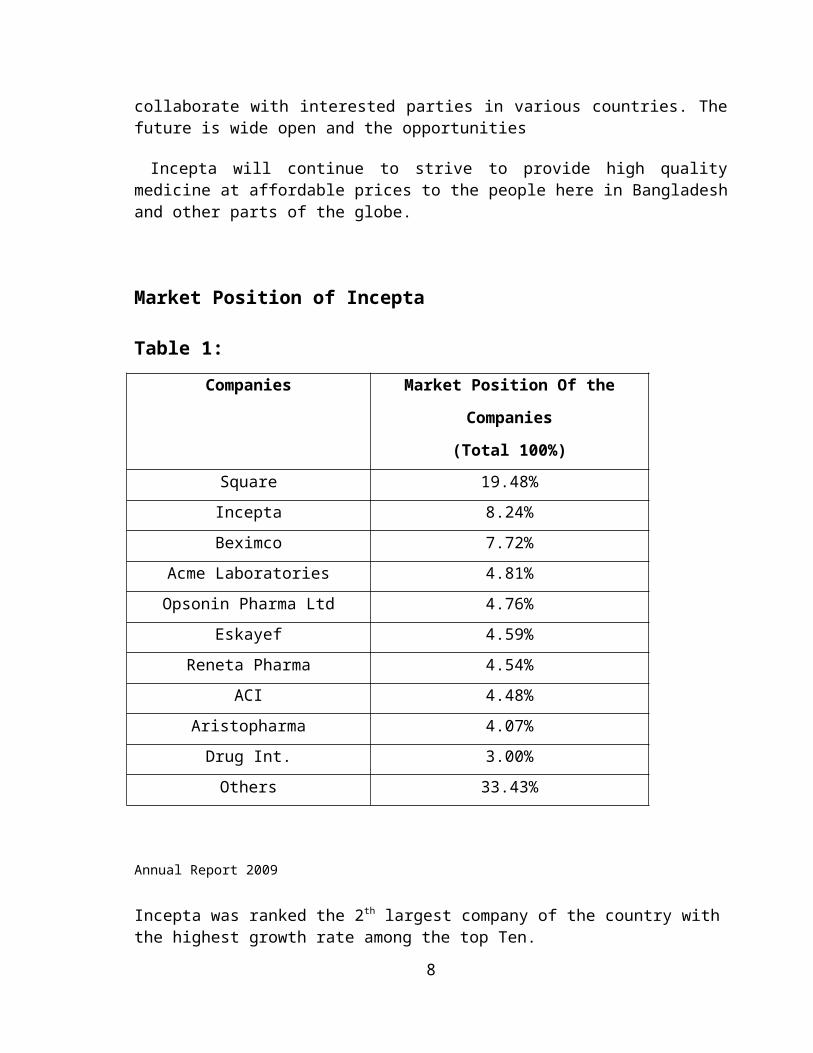

Market Position of Incepta

Table 1:

Companies Market Position Of the Companies

(Total 100%)

Square 19.48%

Incepta 8.24%

Beximco 7.72%

Acme Laboratories 4.81%

Opsonin Pharma Ltd 4.76%

Eskayef 4.59%

Reneta Pharma 4.54%

ACI 4.48%

Aristopharma 4.07%

Drug Int. 3.00%

Others 33.43%

Annual Report 2009

Incepta was ranked the 2th largest company of the country with the highest growth rate among the top Ten.

Highlight of the fastest growing Pharmaceuticals sectors in Bangladesh.

Total Market Size in 2009: US $ 715 M

Second highest contributor to national ex-checker

Largest white-collar labor intensive employment sector

97% Local Manufacturing

About 39,000 retail drug license holders in Bangladesh.

6

2.2 Vision and Mission

Vision

To become a research based global pharmaceutical company in addition to being a highly efficient generic manufacturer. To discover and develop innovative, value-added products those improves the quality of life of people around the world and significantly contribute towards the growth of Bangladesh.

Mission

Provide people globally with high quality health care products at affordable prices in order to improve access to medicine and to improve employees an enabling environment that facilities realization of their full potential.

2.3 Ownership Pattern

Incepta Pharmaceuticals Limited is the sister concern of the renowned Impress Group and the business is running as fully private limited company. Directors of Incepta Pharmaceuticals Limited own the majority shares. Incepta is not DSE listed in capital market yet, so it is controlled by the internal board of director’s .So any kind of significant decision taken by the management.

2.4 Scenario of Incepta

Exporting country

Afghanistan, Belize, Bhutan, Congo, Costa Rica, Cambodia, Dominican republic, EI Salvatore, Ethiopia, Guyana, Georgia, honk Kong, Honduras, Kenya, Myanmar, Mongolia, Mauritania, Srilanka, Somalia, Togo, Tajikistan, turkey, Ukraine, Vietnam.

7

2.5 Figures of Incepta

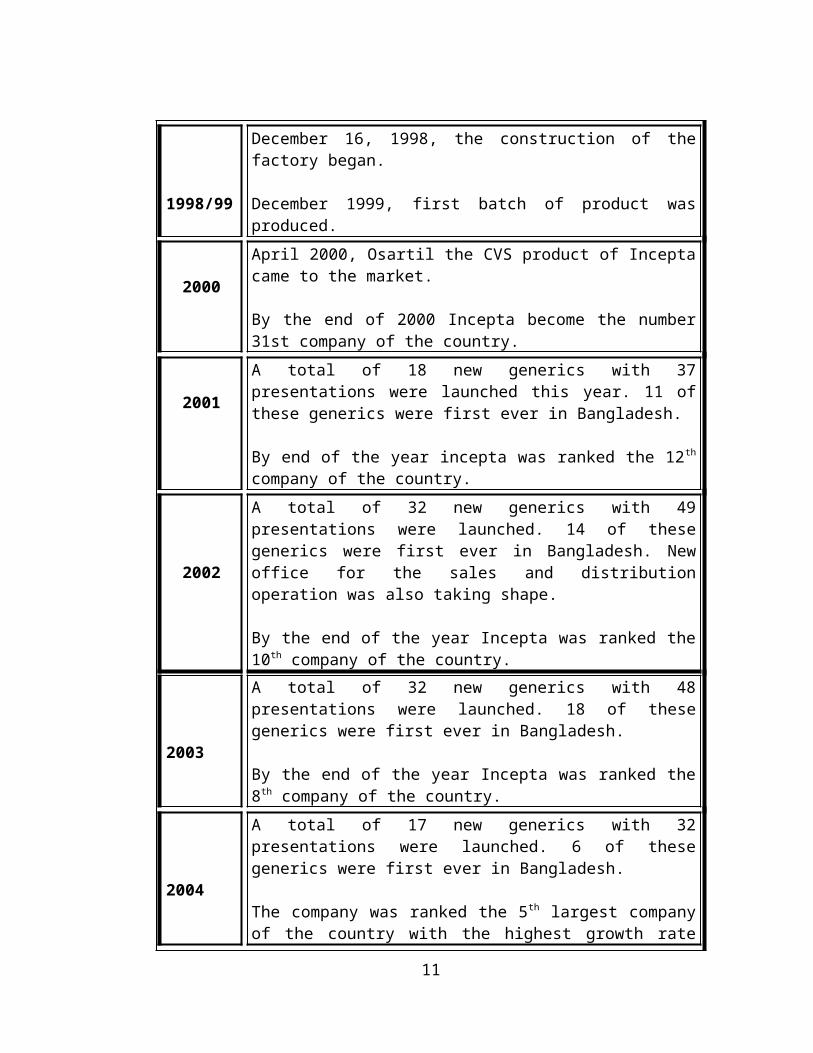

Incepta began its operation with a handful of highly skilled and dedicated professionals guided by an able leadership. Proper strategic planning, technical excellence, swift and timely decisions helped us achieve our objectives leading to much faster growth.

Table 2:

1998/99

December 16, 1998, the construction of the factory began.

December 1999, first batch of product was produced.

2000

April 2000, Osartil the CVS product of Incepta came to the market.

By the end of 2000 Incepta become the number 31st company of the country.

2001

A total of 18 new generics with 37 presentations were launched this year. 11 of these generics were first ever in Bangladesh.

By end of the year incepta was ranked the 12th company of the country.

2002

A total of 32 new generics with 49 presentations were launched. 14 of these generics were first ever in Bangladesh. New office for the sales and distribution operation was also taking shape.

By the end of the year Incepta was ranked the 10th company of the country.

2003

A total of 32 new generics with 48 presentations were launched. 18 of these generics were first ever in Bangladesh.

By the end of the year Incepta was ranked the 8th company of the country.

2004

A total of 17 new generics with 32 presentations were launched. 6 of these generics were first ever in Bangladesh.

The company was ranked the 5th largest company of the country with the highest growth rate among the top five.

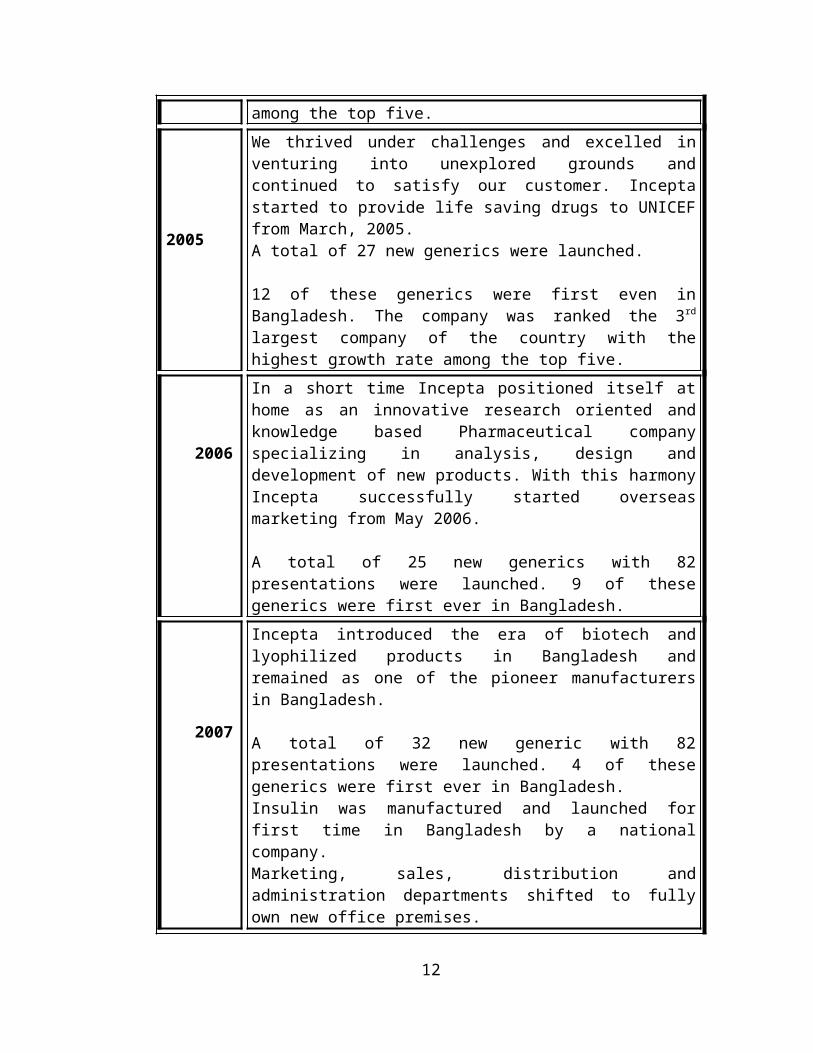

2005

We thrived under challenges and excelled in venturing into unexplored grounds and continued to satisfy our customer. Incepta started to provide life saving drugs to UNICEF from March, 2005. A total of 27 new generics were launched.

12 of these generics were first even in Bangladesh. The company was ranked the 3rd largest company of the country with the highest

8

growth rate among the top five.

2006

In a short time Incepta positioned itself at home as an innovative research oriented and knowledge based Pharmaceutical company specializing in analysis, design and development of new products. With this harmony Incepta successfully started overseas marketing from May 2006.

A total of 25 new generics with 82 presentations were launched. 9 of these generics were first ever in Bangladesh.

2007

Incepta introduced the era of biotech and lyophilized products in Bangladesh and remained as one of the pioneer manufacturers in Bangladesh.

A total of 32 new generic with 82 presentations were launched. 4 of these generics were first ever in Bangladesh.Insulin was manufactured and launched for first time in Bangladesh by a national company.Marketing, sales, distribution and administration departments shifted to fully own new office premises.

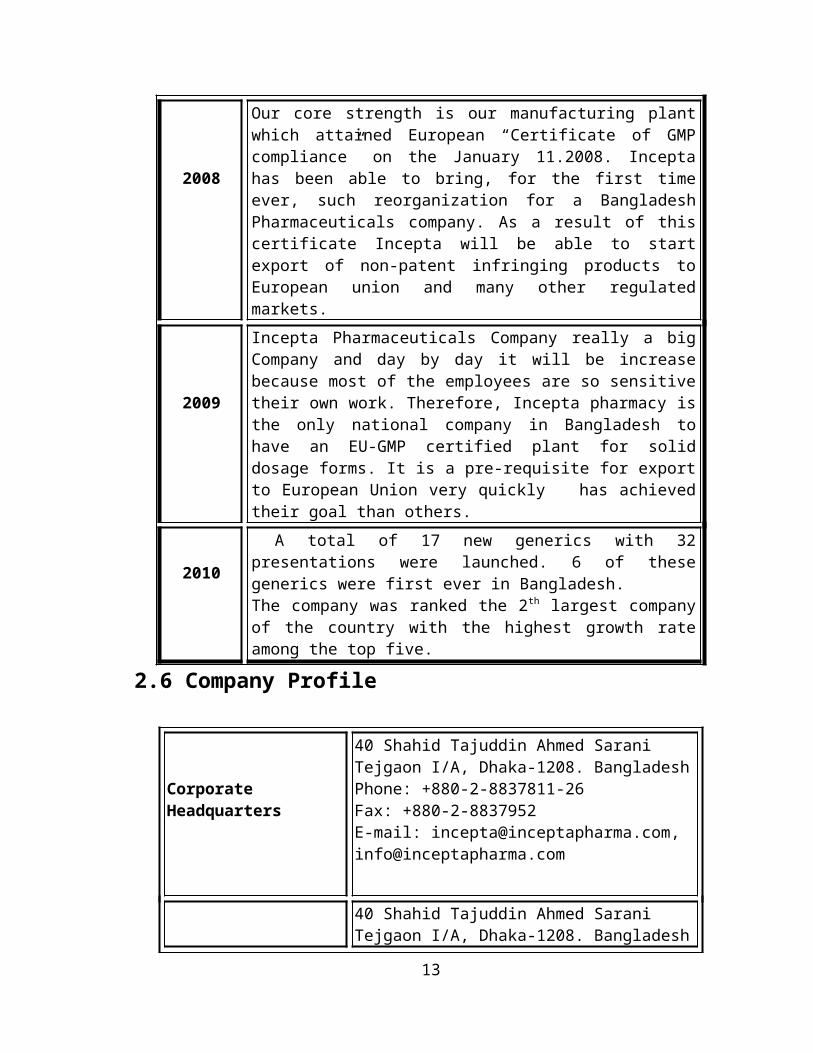

2008

Our core strength is our manufacturing plant which attained European “Certificate of GMP compliance” on the January 11.2008. Incepta has been able to bring, for the first time ever, such reorganization for a Bangladesh Pharmaceuticals company. As a result of this certificate Incepta will be able to start export of non-patent infringing products to European union and many other regulated markets.

2009

Incepta Pharmaceuticals Company really a big Company and day by day it will be increase because most of the employees are so sensitive their own work. Therefore, Incepta pharmacy is the only national company in Bangladesh to have an EU-GMP certified plant for solid dosage forms. It is a pre-requisite for export to European Union very quickly has achieved their goal than others.

2010

A total of 17 new generics with 32 presentations were launched. 6 of these generics were first ever in Bangladesh.The company was ranked the 2th largest company of the country with the highest growth rate among the top five.

2.6 Company Profile

Corporate Headquarters

40 Shahid Tajuddin Ahmed SaraniTejgaon I/A, Dhaka-1208. BangladeshPhone: +880-2-8837811-26Fax: +880-2-8837952E-mail: [email protected],

9

Director

General Manager

Deputy General Manager

Assistant General Manager

Senior Manager

Manager

Deputy Manager

Assistant Manager

Executive Officer

Officer

Senior Officer

Managing Director

Assistant Officer

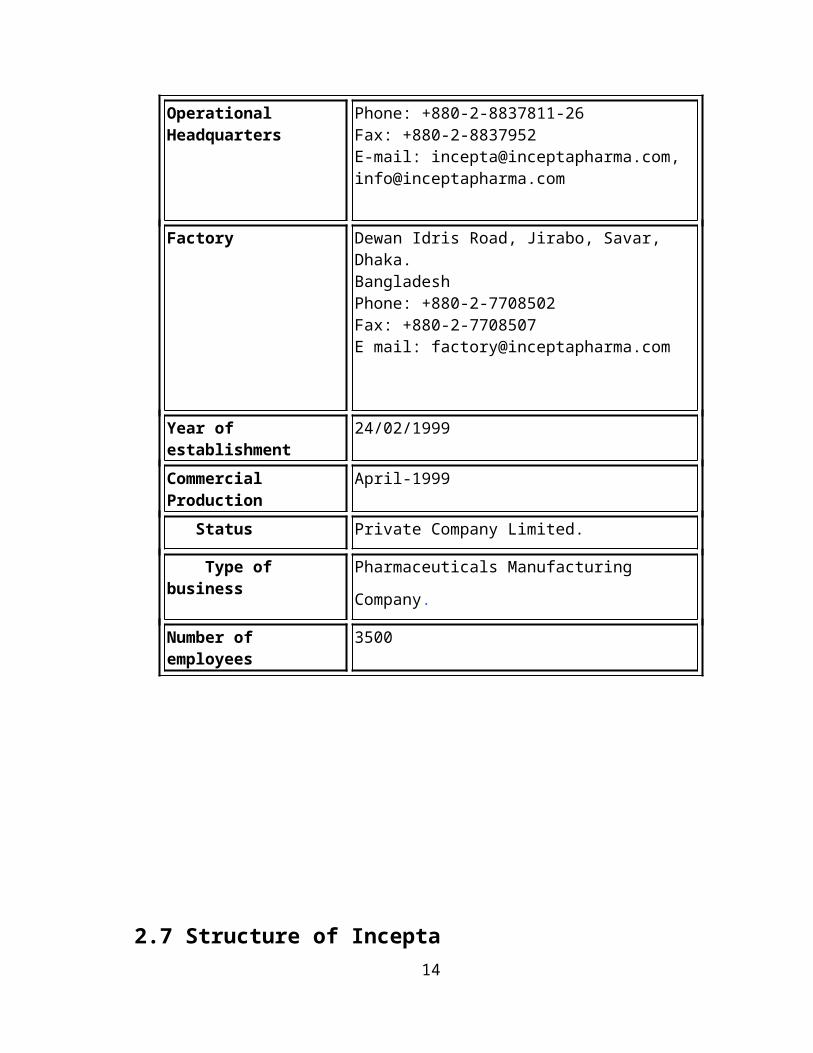

Operational Headquarters

40 Shahid Tajuddin Ahmed SaraniTejgaon I/A, Dhaka-1208. BangladeshPhone: +880-2-8837811-26Fax: +880-2-8837952E-mail: [email protected], [email protected]

Factory Dewan Idris Road, Jirabo, Savar, Dhaka. BangladeshPhone: +880-2-7708502Fax: +880-2-7708507E mail: [email protected]

Year of establishment 24/02/1999

Commercial Production April-1999

Status Private Company Limited.

Type of business Pharmaceuticals Manufacturing Company.

Number of employees 3500

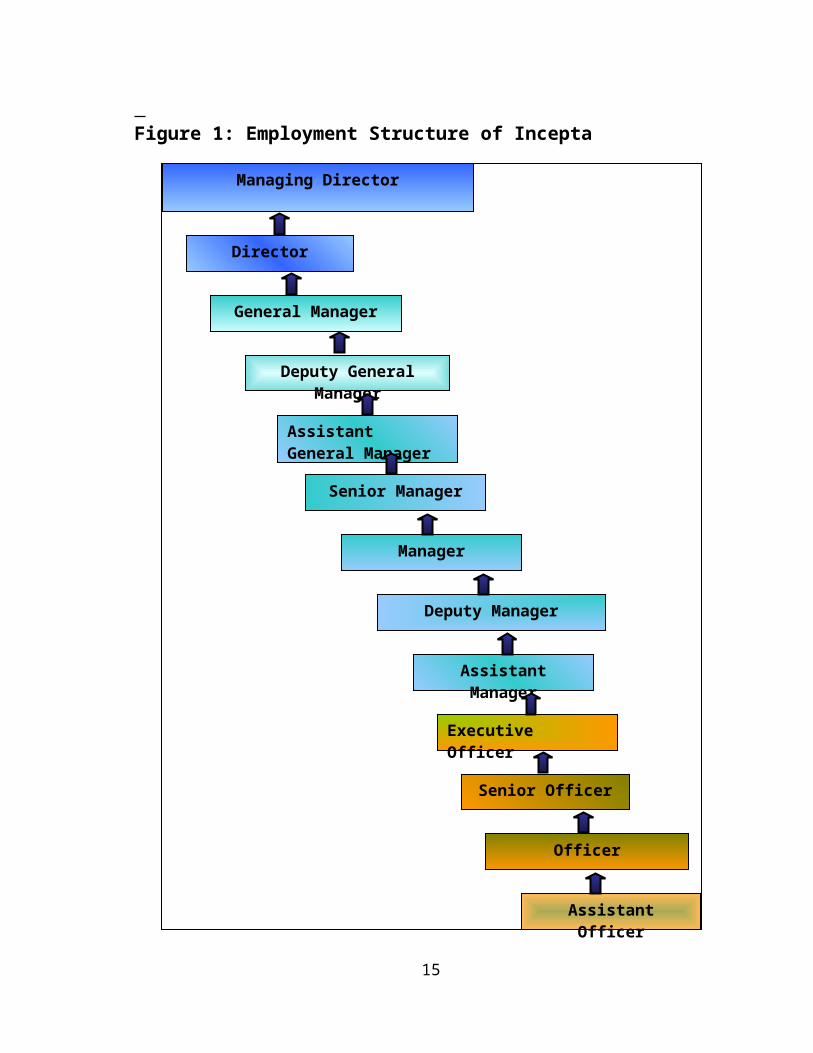

2.7 Structure of Incepta Figure 1: Employment Structure of Incepta

10

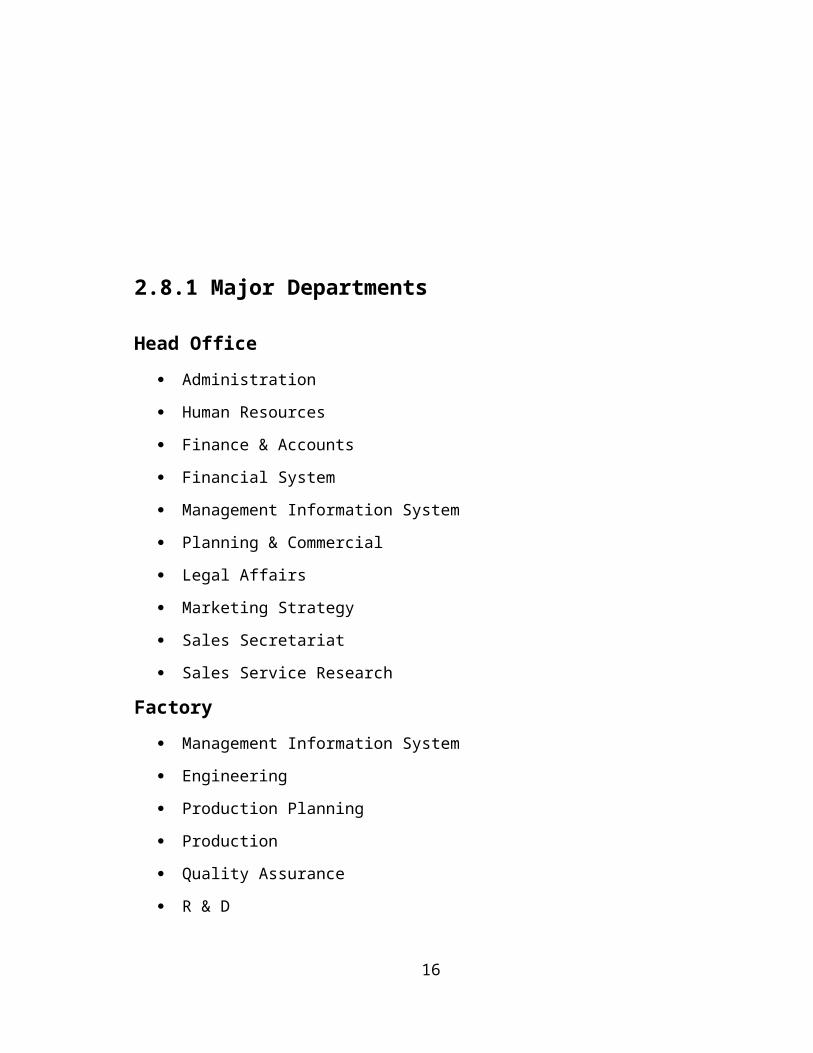

2.8.1 Major Departments

Head Office

Administration

Human Resources

11

Finance & Accounts

Financial System

Management Information System

Planning & Commercial

Legal Affairs

Marketing Strategy

Sales Secretariat

Sales Service Research

Factory

Management Information System

Engineering

Production Planning

Production

Quality Assurance

R & D

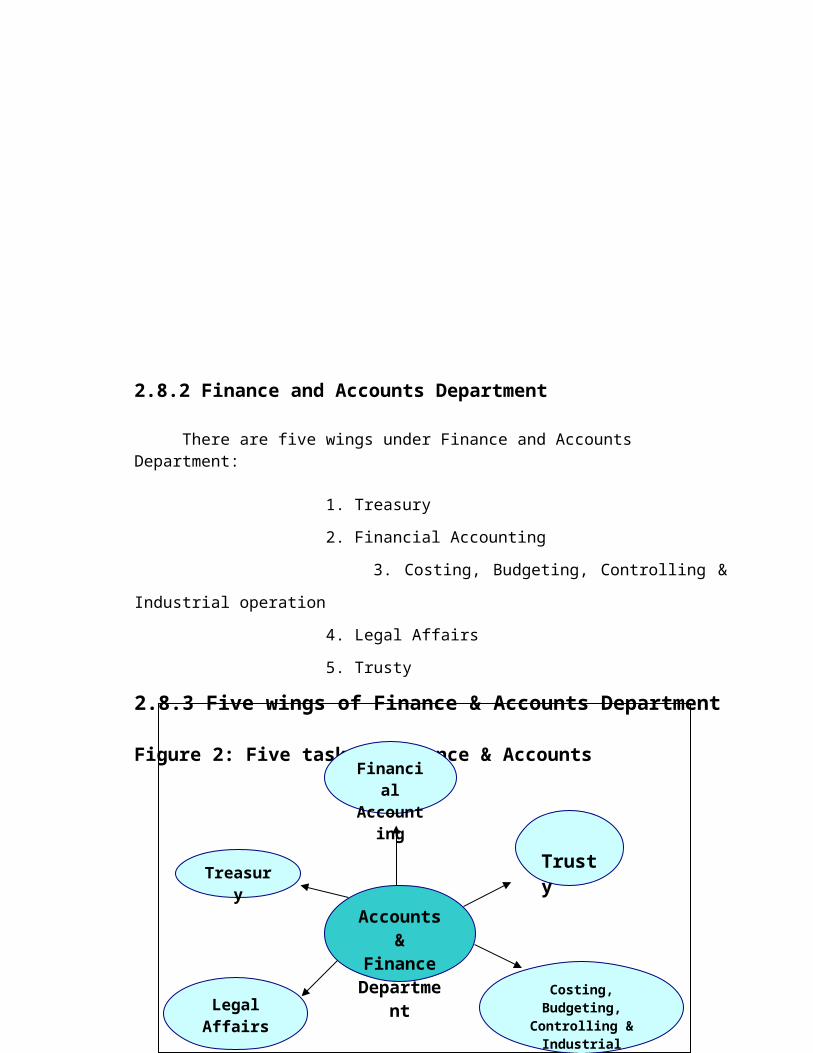

2.8.2 Finance and Accounts Department

There are five wings under Finance and Accounts Department:

1. Treasury

2. Financial Accounting

3. Costing, Budgeting, Controlling & Industrial operation

4. Legal Affairs

12

5. Trusty

2.8.3 Five wings of Finance & Accounts Department

Figure 2: Five task of Finance & Accounts

Annual Report 2009

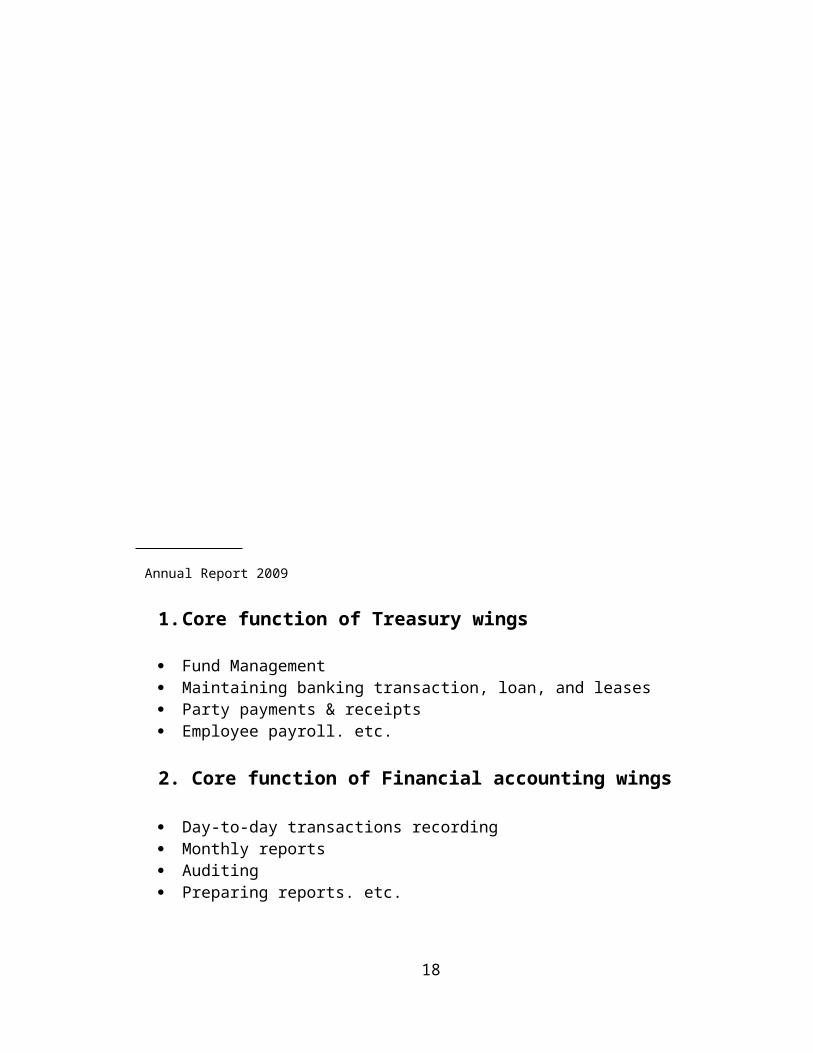

1. Core function of Treasury wings

Fund Management Maintaining banking transaction, loan, and leases Party payments & receipts Employee payroll. etc.

2. Core function of Financial accounting wings

Day-to-day transactions recording

13

Accounts & Finance

Department

Treasury

Financial Accountin

g

Legal Affairs

Trusty

Costing, Budgeting, Controlling &

Industrial operation

Monthly reports Auditing Preparing reports. etc.

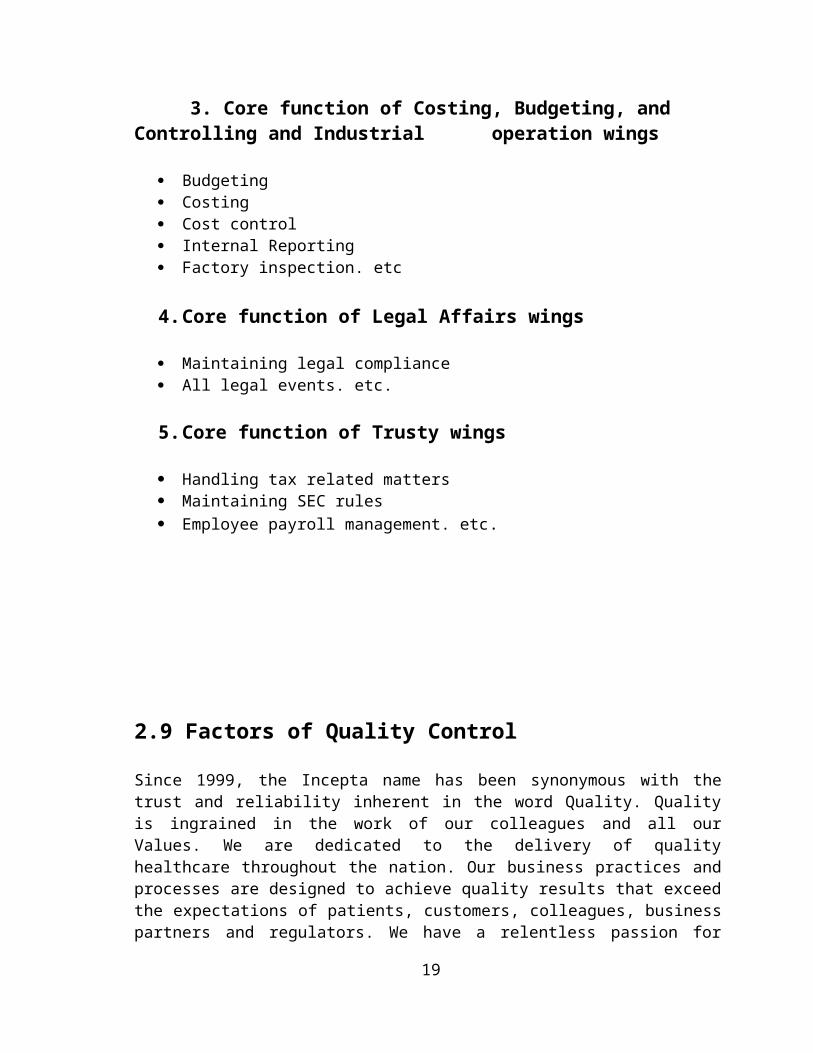

3. Core function of Costing, Budgeting, and Controlling and Industrial operation wings

Budgeting Costing Cost control Internal Reporting Factory inspection. etc

4. Core function of Legal Affairs wings

Maintaining legal compliance All legal events. etc.

5. Core function of Trusty wings

Handling tax related matters Maintaining SEC rules Employee payroll management. etc.

2.9 Factors of Quality Control

Since 1999, the Incepta name has been synonymous with the trust and reliability inherent in the word Quality. Quality is ingrained in the work of our colleagues and all our Values. We are dedicated to the delivery of quality healthcare throughout the nation. Our business practices and processes are designed to achieve quality results that exceed the expectations of patients, customers, colleagues, business partners and regulators. We have a relentless passion for Quality in everything we do.

2.9.1 Teamwork

We know that to be a successful company we must work together, frequently transcending organizational and geographical boundaries to meet the changing needs of our customers.

14

2.9.2 Performance

We strive for continuous improvement in our performance, measuring results carefully, and ensuring that respect for people are never compromised.

2.9.3 Community

We aim to become nation’s most admirable business enterprise through our honest and intelligent approach to everything that we do. We strive to support the community where we live and to also support our nation as far as possible at the time of its need. We truly believe that we can only survive and grow if our nation remains healthy.

2.10 Distribution channel of incepta

Incepta has highly disciplined and organized Sales and related information available to the customer. The company virtually covers every single corner of the rural as well as urban area of Bangladesh. The company has very large and competent sales team, which promotes the specialties throughout the country. Sales team operates its activity by dividing the whole country into 8 regions. Incepta have 600 members strong sales team promotes the products to the doctors. It has its own large distribution network having 13 depots all over the country. They make the products available in every single drug store of the country. The depots are located at Dhaka, Chittagong, Rajshahi, Bogra, Khulna, Sylhet, Barishal, Comilla.

2.11 Corporate Social Responsibility

Incepta achieved its tremendous commercial success through its honesty and sincerity in business polices. The company aims to become nation’s most admired company through their honest and intelligent approach to everything they do. Company management strives to support the community where they life and also to support this nation as far as possible in times of need. Incepta believes it can survive commercially and grow if the nation remains healthy. Incepta gives emphasis to its practice of corporate social responsibility and evidence of this commitment is found in its dealing with clients, employees, governments and the society at large.

Company CSR activity includes its finances because the company pays tax and VAT to the government and also settles bank and suppliers liabilities in a timely fashion and disburses benefits to employees on time. Incepta considers its employees to be valuable assets and

15

protects their rights and provides full range of staff facilities including life insurance and disbursement of 5% of the company profit to them. Incepta maximizes safety in work place for its employees and child labour is strictly prohibited.

As it commitment to society the company donates medicine to the government Relief Fund during natural disaster. Incepta also provides financial assistance for expensive treatment including heart and cancer and disburses its corporate zakat for relief of distressed people every year.

Incepta also products life saving ‘import-substitute medicines’ at affordable price for the people of Bangladesh as an expression of a true love and compassion for the people. All these activities are evidence of socially responsible and carrying company.

CHAPTER THREE PROJECT PART LITERATURE REVIEW

3.1Concepts of Accounts Payable

Accounts payable are unpaid obligations for goods and services received in the ordinary course of business. It is classified as a current liability account and as such normally has a credit balance. It is classified as a Current Liability because the obligation is generally due within 12 months from the initial transaction date.

This kind of liability usually arises from a purchase of merchandise, materials, or supplies. The accounts normally do not include accrued salaries payable, accrued interest payable, or

16

rent payable. This list is kept in the ordinary course of the debtor's business. Aside from materials and supplies from outside vendors, accounts payable might include such expenses as taxes, insurance, rent (or mortgage) payments, utilities, and loan payments and interest.

It is sometimes difficult to distinguish between accounts payable and accrued liabilities, but it is useful to define a liability as account payable if the total amount of the obligation is known and owed at the balance sheet date. Even as it is a debt owed by a business that arises in the normal course of its dealings, that has not been replaced by a note from another debtor, and that is not necessarily due or past due.

According to Britannica concise encyclopedia1, “Accounts payable is any amount owed as the result of a purchase of goods or services on a credit basis. Although a firm making a purchase issues no written promise of payment, it enters the amount owed as a current liability in its accounts. Companies often incur this type of short-term debt in order to finance their inventories, especially in industries where inventory turnover is rapid”.

Wikipedia2 describes accounts payable as one of a series of accounting transactions covering payments to suppliers’ owed money for goods and services. The average household performs this task by writing cheques each month to such suppliers as the electric company, telephone company, cable television or satellite dish service, newspaper subscription, and other such regular services.

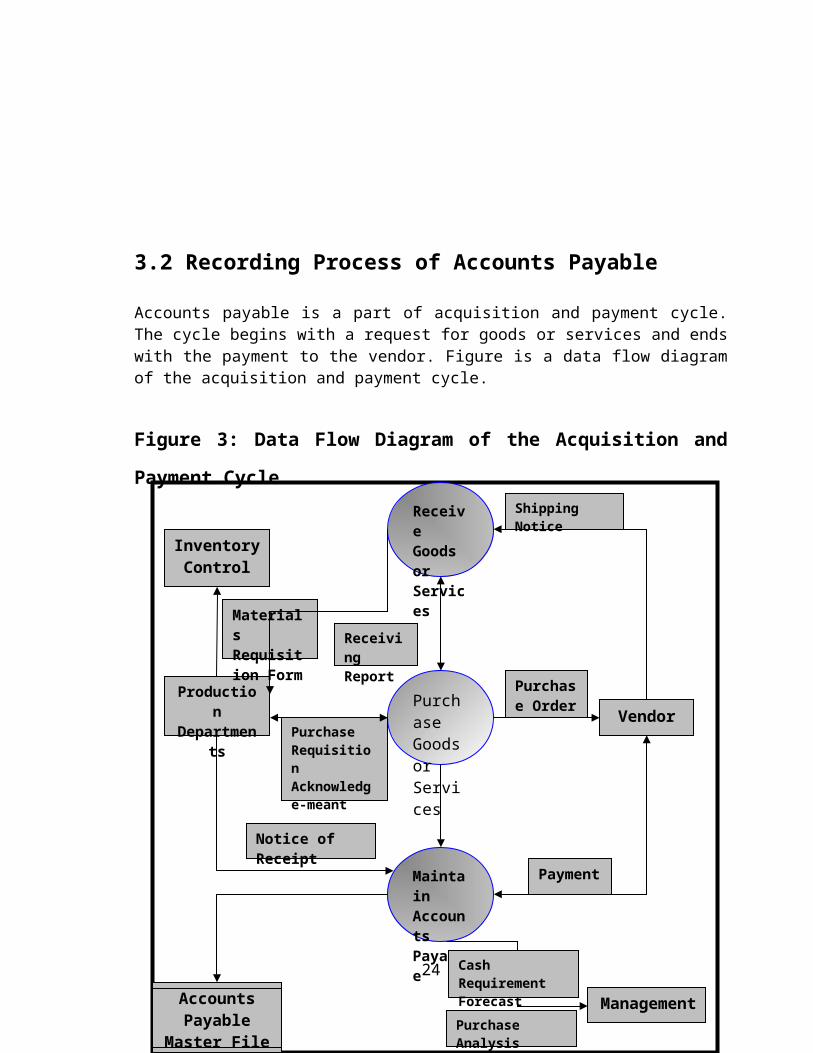

3.2 Recording Process of Accounts Payable

Accounts payable is a part of acquisition and payment cycle. The cycle begins with a request for goods or services and ends with the payment to the vendor. Figure is a data flow diagram of the acquisition and payment cycle.

Figure 3: Data Flow Diagram of the Acquisition and Payment Cycle

1 ? http://britannica.com

2 ? http://en.wikipedia.org/wiki/Accountspayable17

Inventory Control

Vendor

Management

Production Departments

Receive Goods or Services

Maintain Accounts Payable

Purchase Goods or Services

Materials Requisition Form

Shipping Notice

Purchase Order

Payment

Cash Requirement Forecast

Purchase Analysis

Purchase Requisition Acknowledge-meant

Receiving Report

Accounts Payable Master

File

Notice of Receipt

Casher, Jonathan D.; How to find and Eliminate Erroneous Payments; APA's Employer Practices;

winter 2000.

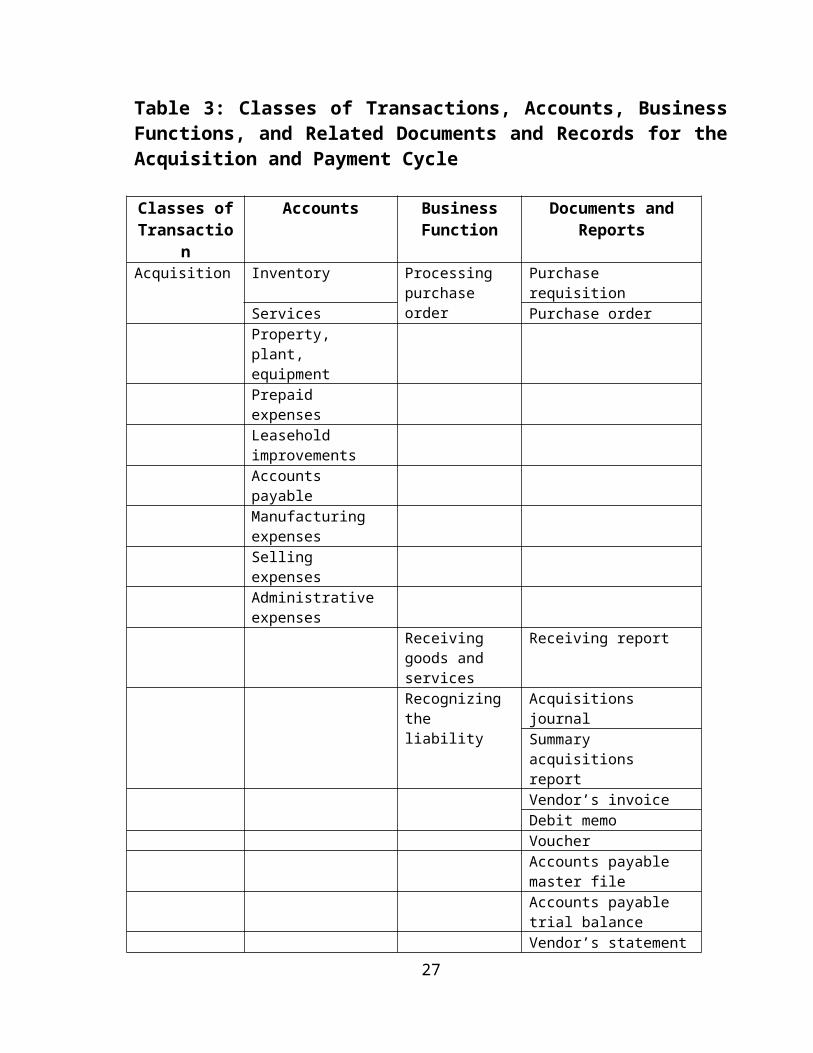

3.3 Classes of Transactions and Business Functions for the Acquisition and Payment Cycle

The cycle encompasses transactions related to credit purchase of goods and services, and to pay for the item purchased. According to Arens & Loebbecke3 there are three classes of transactions included in the cycle;

1. acquisition of goods and services2. cash disbursements3. purchase returns and allowances and purchase discounts

They have told that this cycle involves the decisions and processes necessary for obtaining the goods and services for operating a business. They have drawn a table showing the classes of transactions, accounts, business functions and related documents for the cycle. The table is shown in table 1. According to them there are four business functions shown in 3 Arens Alvin A and Loebbecke James K.;“Auditing- An Integrated Approach” ; Prentice Hall International; Eighth Edition; 2000.

18

the third column of table 1. But Romney and Steinbart has divided those functions into three categories;

1. Ordering goods, supplies and services2. Receiving and storing goods, supplies and services3. Paying for goods, supplies and services

He includes ‘the liability recognition’ in the paying for goods supplies and services function. As a whole we can say that acquisition and payment cycle includes four basic business activities;

1. Ordering for goods and services2. Receiving goods and services 3. Recognizing liability for receiving goods and services4. Paying for goods, supplies and services

1. Ordering For Goods and Service

The cycle begins with need reorganization. Respective department identifies its need, arise purchase requisition and then send it to purchase department. This department makes order for goods and services.

Table 3: Classes of Transactions, Accounts, Business Functions, and Related Documents and Records for the Acquisition and Payment Cycle

Classes of Transaction

Accounts Business Function

Documents and Reports

Acquisition Inventory Processing purchase order

Purchase requisitionServices Purchase orderProperty, plant, equipmentPrepaid expensesLeasehold improvementsAccounts payable

19

Manufacturing expensesSelling expensesAdministrative expenses

Receiving goods and services

Receiving report

Recognizing the liability

Acquisitions journalSummary acquisitions report Vendor’s invoiceDebit memoVoucher Accounts payable master fileAccounts payable trial balanceVendor’s statement

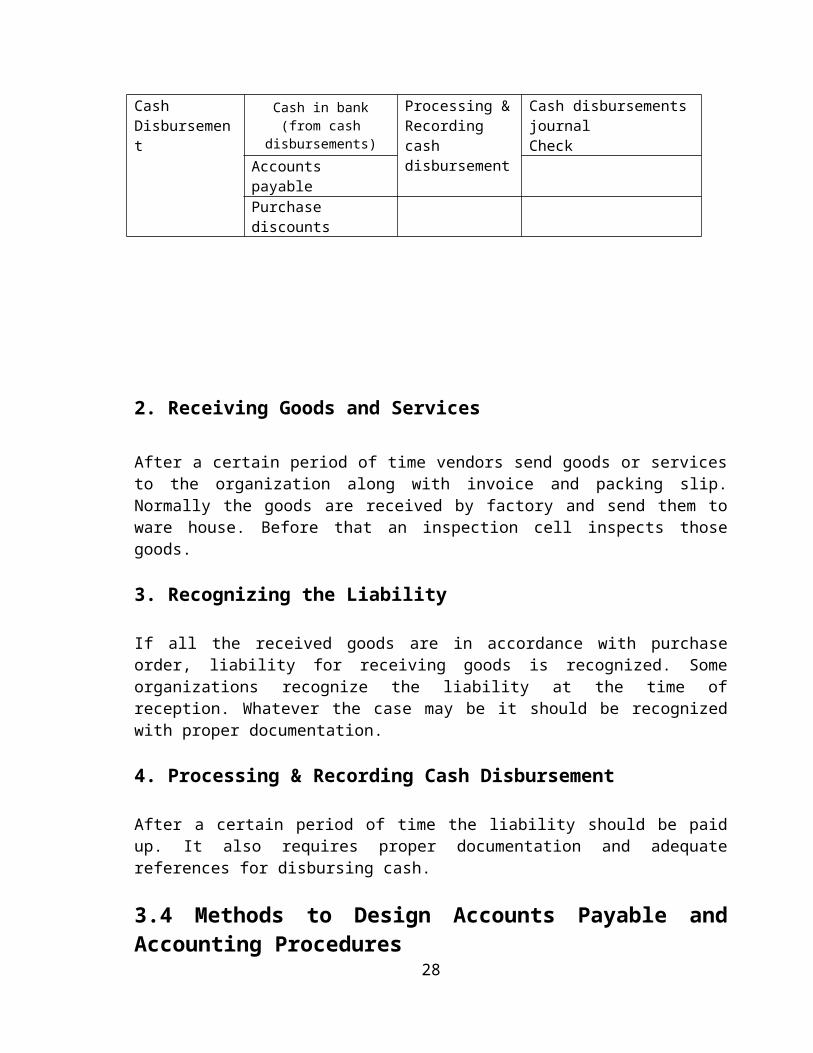

Cash Disbursement

Cash in bank (from cash disbursements)

Processing & Recording cash disbursement

Cash disbursements journalCheck

Accounts payablePurchase discounts

2. Receiving Goods and Services

After a certain period of time vendors send goods or services to the organization along with invoice and packing slip. Normally the goods are received by factory and send them to ware house. Before that an inspection cell inspects those goods.

3. Recognizing the Liability

If all the received goods are in accordance with purchase order, liability for receiving goods is recognized. Some organizations recognize the liability at the time of reception. Whatever the case may be it should be recognized with proper documentation.

4. Processing & Recording Cash Disbursement

After a certain period of time the liability should be paid up. It also requires proper documentation and adequate references for disbursing cash.

20

3.4 Methods to Design Accounts Payable and Accounting Procedures

If an organization follows some method it could improve its accounts payable procedure. According to Chris Anderson4 there are nine methods to design accounts payable and accounting procedures

1. Eliminate Paper

The single biggest cost for any purchasing and payables department is paper, including: purchase orders, purchase order follow-up, small-dollar purchases, delivery tracking & receipts, and vendor payments. Utilizing paperless invoices, Web-based supplier self-servicing, centralized vendor files, automated workflows for electronic or imaged invoices (see ERP below), and payment methods, such as business credit cards, Electronic Data Interchange (EDI) and Electronic Funds Transfer (EFT), can reduce by paper handling costs by as much as 90%.

2. Integrate ERP Systems

Enterprise Resource Planning (ERP) automates the purchasing and payables functions, which allows a company to get more work done with fewer personnel. Also, electronic invoice matching applications save time in retrieving paperwork. It is estimated that an ERP system can annually save an organization $300 per million in sales.

3. Increase Payment Terms

Negotiate payment terms based on receipt of goods or the invoice. This can add one week or more to your terms, which can be 25% of 30 day terms. Use EFT for just-in-time payments to maximize your payables terms and minimizing the impact to your credit.

4. Take Payment Discounts

If you are getting 2%/10 net 30 terms, then consider taking it. This means you are offered a 2% discount if you pay within 10 days, instead of the normal 30 day terms. This translates

4 http://www.bizmanualz.com?src=ART81

21

into an 18% return on your capital, and for many organizations this is a good return on your investment.

5. Review Purchases

Purchasing is a continuous process that requires continuous review. Consider: transportation charges, expedited fees, odd lot penalties, new pricing, new products, consolidating vendors, new vendors or buying groups, payment terms, and more. Communicate with your suppliers to improve the process. And review and monitor everything to account for changes in your environment.

6. Communicate with Suppliers

Communicate with your suppliers to improve the process. Ask suppliers to submit their invoices electronically. This will save you time, resources and losses due to waste.

7. Eliminate Disputes

Disputes with your suppliers are typically the result of a problem with your purchasing/receiving process. When disputes occur, review your purchasing procedures to ensure that they are producing the correct metrics and that you are not forced to pay for your mistakes.

3.5 Definition of Internal Control

An internal control system is the process that an administrator uses to provide reasonable assurance that the unit's goals and objectives will be achieved. It is the management of business risks and is a dynamic process that changes as personnel and

Circumstances change. The system includes organizational design, written policies and procedures, actual operating practices, physical barriers to protect assets and all personnel. The system should be designed to discourage occurrences of errors or irregularities and to identify, within a reasonable time frame, errors or irregularities that may occur. The internal control system encompasses a variety of internal controls such as background checks of prospective employees for sensitive positions to locking the door when the office is closed for the evening.

According to Arens & Loebbecke “a system of internal control consists of policies and procedure designed to provide management with reasonable assurance that the company achieves its objectives and goals. These policies and procedures are often called controls and

22

collectively they comprise the entity’s internal control.” Detailed definition of Internal Control per ISA 65 is given below

The term “Internal control system means all the policies and procedures (internal controls) adopted by the management of an entity to assist in achieving management’s objective of ensuring, as far as practicable, the orderly and efficient conduct of its business, including adherence to management policies, the safeguarding of assets, the prevention and detection of fraud and error, the accuracy and completeness of the accounting records, and the timely preparation of reliable financial information. The internal control system extends beyond those matters which relate directly to the functions of the accounting system and comprises

The control environment means the overall attitude, awareness and actions of directors and management regarding the internal control system and its importance in the entity. Factors reflected in the control environment include:

The function of the board of directors and its committees. Management’s philosophy and operating style. The entity’s organizational structure and methods of assigning authority and

responsibility. Management’s control system including the internal audit function, personnel

policies and procedures and segregation of duties.

3.6 Need of Internal Control

The internal control system provides for safeguarding of assets, proper recording of transactions and the efficient and effective accomplishment of the units and university's goals and objectives including compliance with federal, state, and university rules and regulations.

International Standards on Auditing relating to Risk Assessments and Internal Control, states (paragraph 2) about the importance of internal control that the auditor should obtain an understanding of the accounting and internal control systems sufficient to plan the audit and develop an effective audit approach. The auditor should use professional judgment to assess audit risk and to design audit procedure to ensure it is reduced to an acceptably low level.

There is no requirement that the auditor is to rely on any particular control. The requirement is that if the auditor wishes to rely upon controls as part of his audit evidence he must:

Gain an understanding of those controls. Study the operation of that control and evaluate the operation of those controls

5paragraph 6, international Standard on Auditing23

3.7 Responsibility for Internal Controls

The administrator who is responsible for the accomplishment of goals and objectives is also responsible for establishment, maintenance, and monitoring of the internal control system which helps ensure the accomplishment of those goals and objectives. He or she is responsible for the sound financial condition of the unit, protection of the university's assets including its human resources, and compliance with federal, state, and University rules, regulations, and procedures. He or she must ensure that the funds entrusted to the unit are used appropriately.

The administrator may delegate some of the related duties but cannot delegate accountability.

3.8 The Importance of Good Internal Controls

Good internal controls are essential to assuring the accomplishment of goals and objectives. They provide reliable financial reporting for management decisions. They ensure compliance with applicable laws and regulations to avoid the risk of public scandals. Poor or excessive internal controls reduce productivity, increase the complexity of processing transactions, increase the time required to process transactions and add no value to the activities.

Good internal controls help ensure efficient and effective operations that accomplish the goals of the unit and still protect employees and assets.

3.9 Components of Internal Controls

Environment Control

The control environment includes administrator's attitudes that are then reflected in the employees' attitudes. An administrator's attitudes should support ethical values and good business practices. An administrator should promote compliance with university policies and procedures through his or her actions as well as through unit policies and procedures. He or she should ensure that employees also support ethical values and have the technical competence for the position. Background checks should be performed prior to hiring for key positions. Policies and procedures should be written, provided to all staff, and expectations for compliance communicated to staff. There should be no tolerance for fraud or conflicts of interests. Disciplinary action should be consistently applied to all employees. Administrators must support compliance with university policies and procedures if they expect employees to have that attitude.

Risk Assessment

24

Administrators should identify and analyze the relevant risks to the achievement of unit goals and objectives. He or she should determine what can go wrong, what areas have the most risk, what assets are at risk, and who is in a position of risk. Risks may include:

Public scandal Revenues not received or if received, not recorded properly Assets (financial, personnel, space, personal property) not used efficiently Assets (financial, personnel, space, personal property) not used to accomplish unit

goals and objectives Assets (financial, personnel, space, personal property) may be diverted to personal

use Information used for decision making is not reliable, timely, or available Methods to control risks should be identified and the associated costs analyzed and

compared to the risk. For some risks, there may not be reasonable controls or the cost of controls may be prohibitive.

Uncontrolled risks may result in insufficient resources to achieve established goals through loss, misuse or mismanagement of resources.

Control Activities

Control activities are those activities that provide a "reasonable" level of assurance that the unit's goals and objectives will be accomplished. Absolute assurance is not possible due to costs, collusion, human error, and management's ability to override controls. Control activities include

Authorization to initiate or approve transactions should be limited to specific personnel. Authorizations can be limited by type of transactions or amount of transactions.

Separation of duties provides that one employee does not have the responsibility for all phases of a transaction. Generally, an employee with physical access to an asset should not also be responsible for accounting records relating to that asset.

Assets should be physically secured. Access to assets should be limited. Reconciliations of assets to accounting records should be prepared periodically and

reconciling items should be resolved timely. Physical assets should be counted periodically and the results of the counts compared

to accounting records. Discrepancies should be reported to appropriate administrators and investigated.

25

Transactions should be properly documented and the records retained in an

organized manner.

Information and Communication System

The purpose of the information and communication system is to help ensure that employees are aware of the unit's goals and objectives, how they are to be accomplished, and who is responsible for the specific tasks to accomplish them. The information and communication system must also provide administrators with reports containing operational, financial, and compliance information to monitor progress toward accomplishing established goals and objectives and to allow administrators to make appropriate decisions. Information and communication systems include:

The university's written policies and procedures The unit's goals and objectives The unit's documented policies and procedures Organization charts Position descriptions Performance evaluations Training programs

An essential part of the internal control system is an effective information and communication system that ensures that employees know what they are supposed to accomplish and how they are to do it.

Monitoring

Monitoring ensures that the internal control system is operating as expected. It should be performed by supervisory personnel and focused on high-risk areas Monitoring activities include:

Spot checks of transactions to ensure compliance with policies and procedure Reviews of outstanding encumbrances Reviews of high risk accounts or records including payroll pay lists and employee

leave records Evaluations of trends Review of supporting documentation

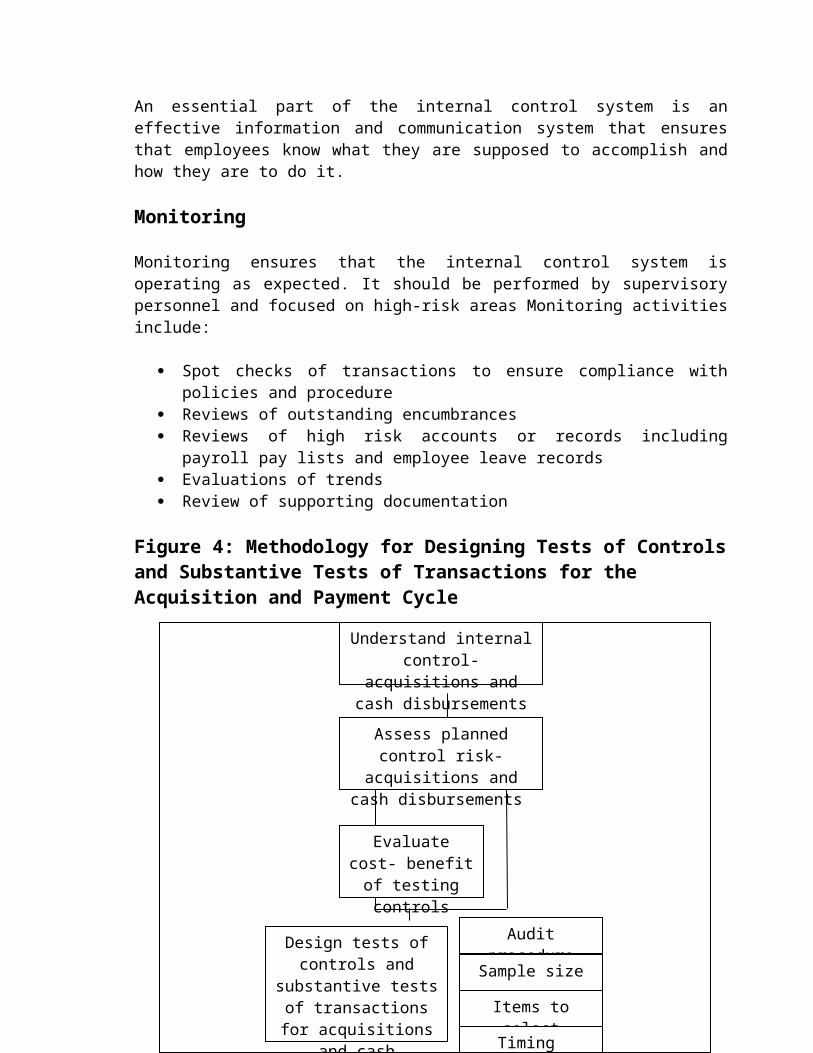

Figure 4: Methodology for Designing Tests of Controls and Substantive Tests of Transactions for the Acquisition and Payment Cycle

26

Understand internal control- acquisitions and cash

disbursements

Assess planned control risk- acquisitions and cash

disbursements

Evaluate cost- benefit of testing

controls

Design tests of controls and substantive tests of

transactions for acquisitions and cash disbursements to meet

transaction-related audit objective

Audit procedure

Sample size

Items to select

Timing

Internal control can be understood by studying the client’s flowcharts, preparing internal control questionnaires and performing walk through tests for acquisitions and cash disbursements. There are some key internal controls for all business functions mentioned earlier in this chapter. These key controls should be examined carefully. After identifying the weaknesses and assessed control risk, auditor will decide whether substantive tests will be reduced sufficiently

CHAPTER FOURE ACCOUNTS PAYABLE & RECORDING PROCESS OF IPL

As discussed earlier, accounts payable is a part of acquisition and payment cycle. The acquisition and payment cycle of Incepta Pharmaceuticals (IPL) begins with a request for goods or services from various departments and ends with the payment to the vendor by issuing checks. In some cases the procedure includes budgeting and prior approval of superior before requesting to the authority.

For the convenience of discussion I have divided this chapter in to four parts. The first part is about the accounts and classes of transactions in the acquisition and payment cycle of IPL. The second part is about related document and records kept by IPL. Third part talks about the procedure of acquisition and payment with related business functions. And in the last part I have talked about their accounting software in which they maintain a separate module for accounts payable.

27

4.1 Accounts and Classes of Transactions in the Acquisition and Payment Cycle

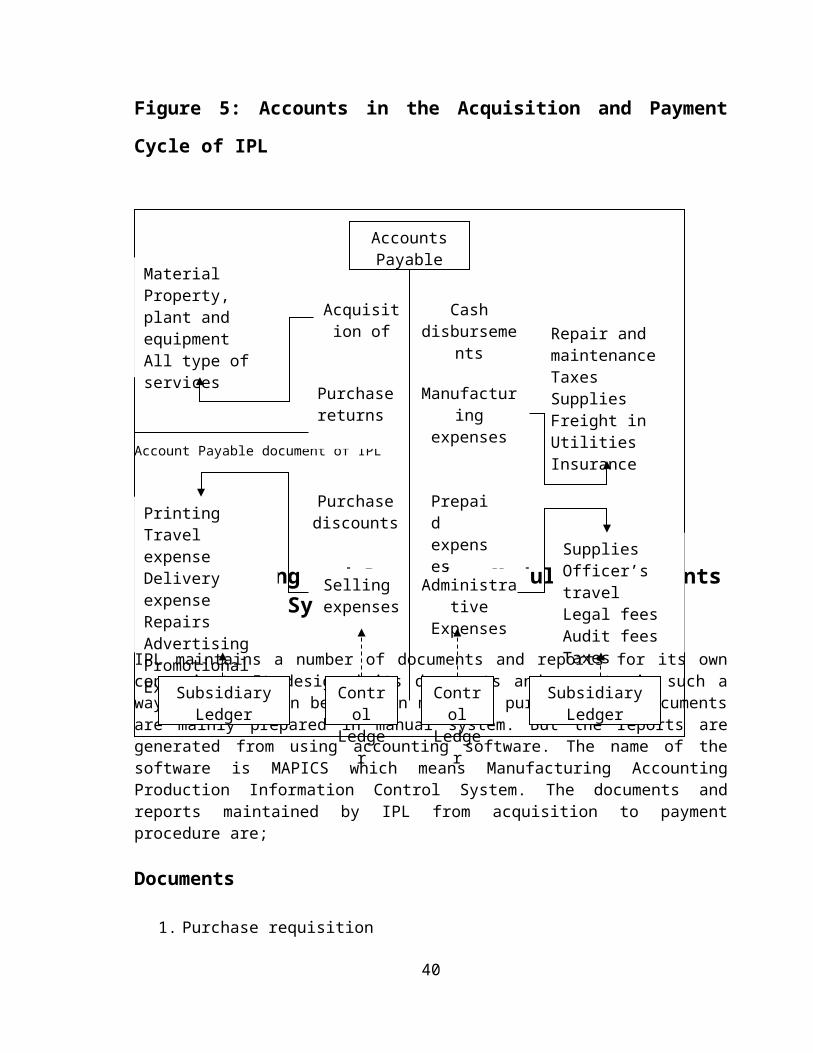

The acquisition and payment cycle of IPL consists of the procedure regarding procurement activities in order to continue the day to day business and production process. It helps them to minimize their cost of acquisition as well as control the quality. The cycle includes three classes of transactions;

Acquisition of goods6, property, plant & equipment7, and services8

Cash disbursement Purchase return

These transactions generate different types of accounts. Those accounts are shown in figure (below). If we note the figure carefully, we can see that each account is affected by accounts payable. All these accounts are either debited or credited against accounts payable. For example, acquisitions are debited against accounts payable and cash disbursement is credited against it.

Figure 5: Accounts in the Acquisition and Payment Cycle of IPL

Account Payable document of IPL

4.2 Recording and Reporting Module of Accounts Payable System

6 Here goods refers to inventoriable items like raw material and packing material.7 Refers to tangible fixed assets used by BPL.8 Service refers to all type of short term and long term services like cleaning, plantation, nursery, gardening, postal, software etc.

28

Accounts Payable

Acquisition of

Purchase returns

Manufacturing expenses

Cash disbursements

Administrative Expenses

Purchase discounts

Selling expenses

Prepaid expenses

MaterialProperty, plant and equipmentAll type of services

PrintingTravel expenseDelivery expenseRepairsAdvertisingPromotional Expenses

Repair and maintenanceTaxesSuppliesFreight inUtilitiesInsurance

SuppliesOfficer’s travelLegal feesAudit feesTaxes

Control Ledger

Control Ledger

Subsidiary Ledger

Subsidiary Ledger

IPL maintains a number of documents and reports for its own convenient. It designed its documents and reports in such a way that they can be used in multiple purposes. The documents are mainly prepared in manual system. But the reports are generated from using accounting software. The name of the software is MAPICS which means Manufacturing Accounting Production Information Control System. The documents and reports maintained by IPL from acquisition to payment procedure are;

Documents

1. Purchase requisition2. Purchase order3. Material receiving report (MRR) / Goods receiving report (GRR)4. Invoice / Bill5. Quality Assurance (QA) Report

Records and Reports under Accounting Software

6. Accounts payable payment voucher7. Vendor ledger8. Vendor account balance9. Journal register10. Cash requirement report11. Tax report 12. VAT (Musok 11) report13. Report on purchase14. Report on payment

1. Purchase Requisition

It’s a requisition generate by respective department. Data elements conveyed by a purchase requisition of IPL include unique number of purchase requisition, CEP and purchase order number with date name and description of material and service, unit number, required quantity, unit price and quantity ordered. It also includes signature and approval of authorized person, supplier’s name; mode of payment, advance payment (if any), terms and conditions, MRR number, invoice number etc.

If the requisition is for fixed asset then a CEP (Capital Expenditure Proposal) is raised by the user department. In this case, proposed suppliers name, estimated budget, justification for proposed expenditure and estimated life of proposed expenditure is also required. A sample of CEP is given in the Annexure –A (Figure 8)

2. Purchase Order

29

It’s a document through which an order is made. The heading contains the purchase order number, purchase requisition number and date. The body contains the description of required item, quantity required and ordered, amount with unit price, supplier’s name and address, terms and condition of order, due date, other relevant dates etc. Besides, it also describes the mode of purchase, advance payment (if any), purchase reference and other relevant information. A sample of purchase order is added with Annexure –A (Figure 9)

3. Material Receiving Report (MRR) / Goods Receiving Report(GRR)

It’s a report produced by the inspection department or receiving department. It is used to reflect the receipt of goods on consignment or goods returned to supplier. The report indicates item ordered, name of the material and supplier with the date of arrival of products, its quantity, quality and description of the received item. It also includes MRR number, order number, signature of the authorized person etc. The report is also used as inspection report. Because it mentioned information regarding to

Quantity ordered before quality test Quantity received after quality test Quality Whether as per specification or not Country of origin Deliver in time or not Pricing Legal requirements etc.

4. Accounts Payable Provision Voucher

Under this document provision i.e., entry is given against acquisition. Accounts payable is credited here. From the figure given is Annexure –A (Figure 10) we see that information relating to voucher no, vendor no, invoice no, and MRR no is required with their date for provision journal. Besides, information about due date for payment, item name, item number, unit, party name and the number of the account under which the item belongs to is also required. 5. Invoice / Bill

This document is generated by supplier/ service provider that mention the quantity and amount, bill number with date etc. The bill is attached with MUSOK 11, delivery challan etc.

6. Tax and VAT (Musok 11) Report

30

IPL prepares these reports for calculating the amount of Tax and VAT deducted at source of suppliers. Tax and VAT amount is deducted from the total amount due. Deduction and calculation is made according to section 51(A), 52 of ITO- 19849, rule 16 of ITR-198410, and the VAT Act-1991 (Musok 11). The reports contain vendor number, vendor name, and period, total amount due, tax amount, amount excluding tax amount, VAT amount and amount excluding VAT. A sample of tax and VAT report is added with Annexure (Figure 11) 7. Accounts Payable Payment Voucher

It’s the preliminary entry of a invoice in accounting software. The voucher contains the information of the payment date, mode of payment, item or batch no, voucher no with date, AP journal voucher number with date, amount, party name and other related information. A sample of this voucher is given in the Appendix-A (Figure 12)

8. Vendor account balance

It is nothing but a report about the due amount payable to an individual vendor 9r a number of vendors on a certain date. The report includes vendors’ name, code and the total due amount.

From this register management of IPL will get all related information of accounts payable transaction for a certain period of time. For example, if management wants to know about the amount of purchase of an individual vendor for a certain period of time with related deductions they can get it from journal register. Even the register also informs about whether any payment has been made or not and the due amount of that period.

9. Cash requirement report

It’s a managerial enquiry regarding vendors’ payable amount to forecast the current liabilities. From this report management of Finance and Accounts Department can be informed about the cash to be paid to individual vendor for a certain period of time.

10. Report on purchase

It’s a statement that informs manager about the amount of purchase that has been acquired from an individual vendor.

11. Report on payment

9 Income Tax Ordinance 1984.10 Income Tax Rules 1984.

31

It’s a statement of payment to vendor. Here vendor’s name, number, payment amount tax deducted amount etc. has been mentioned.

4.3 Acquisition and Payment Cycle of IPL

This cycle defines the buying process from initial need recognition through to cash disbursement. Here I am going to describe the whole procedure of acquisition and payment procedure of IPL.

1. The procedure includes following business functions;

2. Processing purchase order

3. Receiving goods, material and services

4. Recognizing the liability

5. Processing and recording cash disbursement

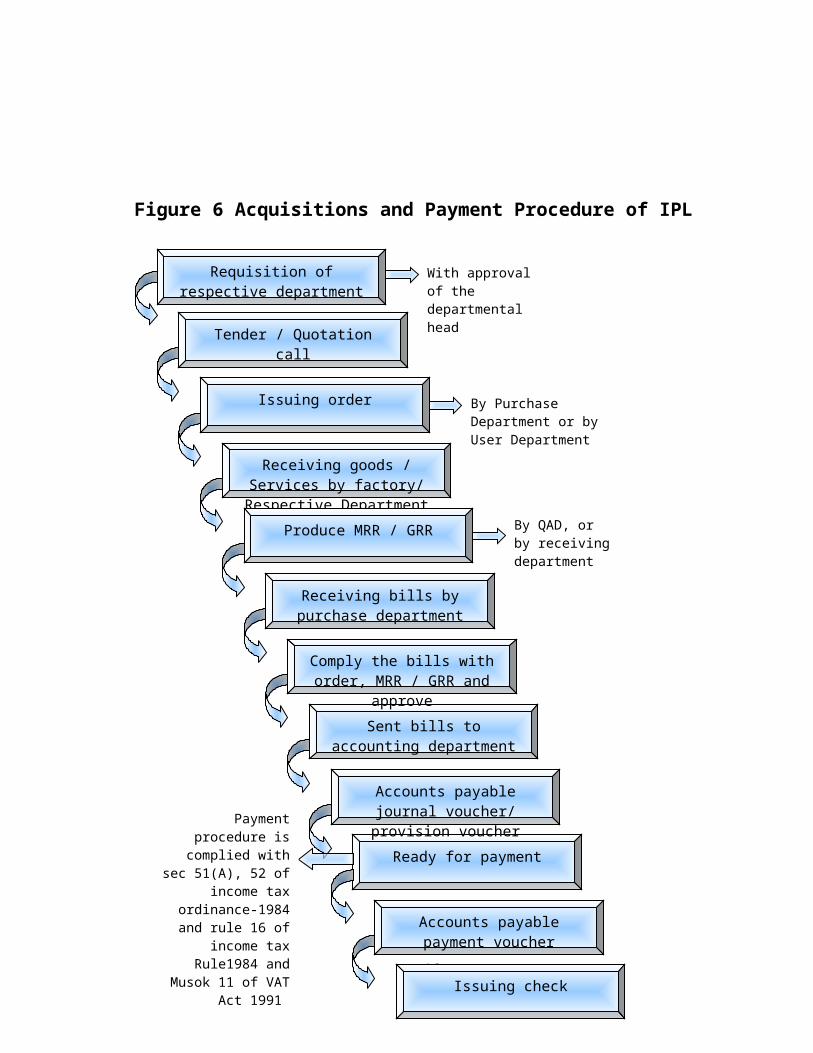

Figure 6 Acquisitions and Payment Procedure of IPL

32

Processing Purchase Order 33

With approval of the departmental head

Tender / Quotation call

Requisition of respective department

Issuing order

Receiving goods / Services by factory/ Respective Department

Produce MRR / GRR

Issuing check

Sent bills to accounting department

Comply the bills with order, MRR / GRR and approve

Receiving bills by purchase department

Accounts payable payment voucher

Ready for payment

Accounts payable journal voucher/ provision voucher

By Purchase Department or by User Department

By QAD, or by receiving department

Payment procedure is complied with sec

51(A), 52 of income tax ordinance-1984 and rule

16 of income tax Rule1984 and Musok 11

of VAT Act 1991

The procedure begins with need recognition. The respective department identifies its need, gets approval of the departmental head and with the approval an authorized person sends purchase requisition to purchase department to initiate purchase. In case of property, plant and equipment acquisition, before sending purchase requisition, a budget has to be prepared by the user department. If the departmental head or higher authorities, whichever is required, approve the proposed budget a purchase requisition is sent to purchase department. And in case of raw or packing materials, the planning department determines the quantity and timing of raw materials. This department informs the purchase department when to buy materials. When the purchase department got the requisition, it calls for quotation11 or tender12. After receiving the quotation or tender, supplier has been selected. The supplier may be local or international. If the terms and conditions are in favor of both IPL and the selected supplier, an order for the purchase is than issued by the purchase department. In case of raw or packing material, the purchase order is issued by the factory. A purchase register is maintained by the purchase department in which they maintain all the required information relating to a consignment.

Receiving Material, Goods and Services

Generally the goods and services are received by the user department who has issued the purchase requisition or in some cases by the authorized department. Materials are received by Quality Assurance Department (QAD) in the factory. After receiving materials, goods and services an MRR is issued for material and other than material a GRR is issued by receiving department to purchase department. In the mean time the invoice or bill is received by the purchase department. Before using the product by user department that is at the time of delivery, it has been inspected by the inspection or QAD, by user department or by authorized department. QAD examined the materials on a sample testing basis and provide a certificate. Normally,

1. QAD inspects standardized items like raw material, packing material etc.2. User department inspects non standardized items like services, stationeries etc.3. Inspection department inspects machineries, plants etc.

Again at IPL there are some authorized departments for inspection. For example, computer or IT related products are inspected by IT department, furniture are by HR department.

Refuse the order Reorder the item Received on condition

Figure 7: receiving function

11 Quotation is an indication of the price at which a seller might be willing to offer goods for sale. 12 Tender is a means of selecting supplier. The lowest bidder with required quality is selected.

34

Recognizing the Liability

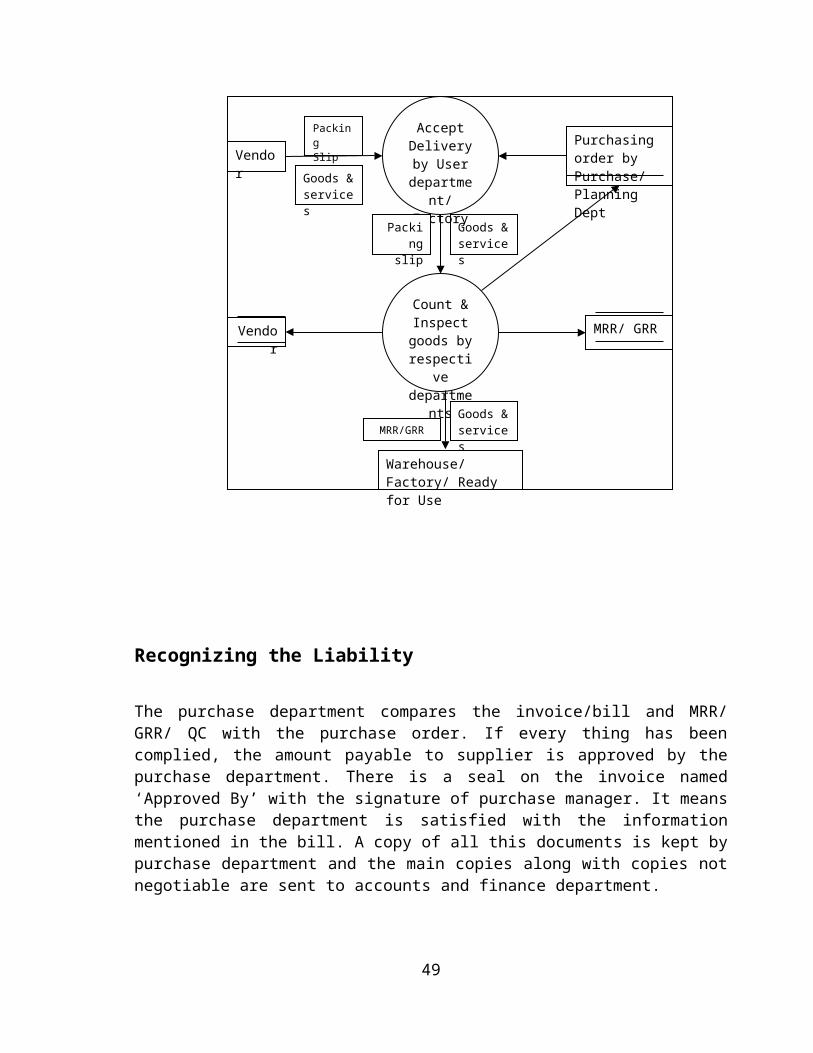

The purchase department compares the invoice/bill and MRR/ GRR/ QC with the purchase order. If every thing has been complied, the amount payable to supplier is approved by the purchase department. There is a seal on the invoice named ‘Approved By’ with the signature of purchase manager. It means the purchase department is satisfied with the information mentioned in the bill. A copy of all this documents is kept by purchase department and the main copies along with copies not negotiable are sent to accounts and finance department.

The accounts and finance department is then ready for giving provision voucher. An authorized person is liable for giving provision voucher. He examines the not negotiable copy of bill/ invoice at the time of giving provision voucher. Generally the liability is recognized when the vendor sends the invoice or bill. But in some cases it may be recognized at the time of goods received. The source documents for recognizing the amount of liability for acquisition are;

Report on purchase Vendor account balance

35

Vendor

Warehouse/ Factory/ Ready for Use

Accept Delivery by

User department/

Factory

Count & Inspect

goods by respective

departments

Purchasing order by Purchase/ Planning Dept

MRR/ GRRVendor

Packing slip

Goods & services

Packing Slip

Goods & services

Goods & servicesMRR/GRR

Vendor ledger Journal register Tax report VAT report

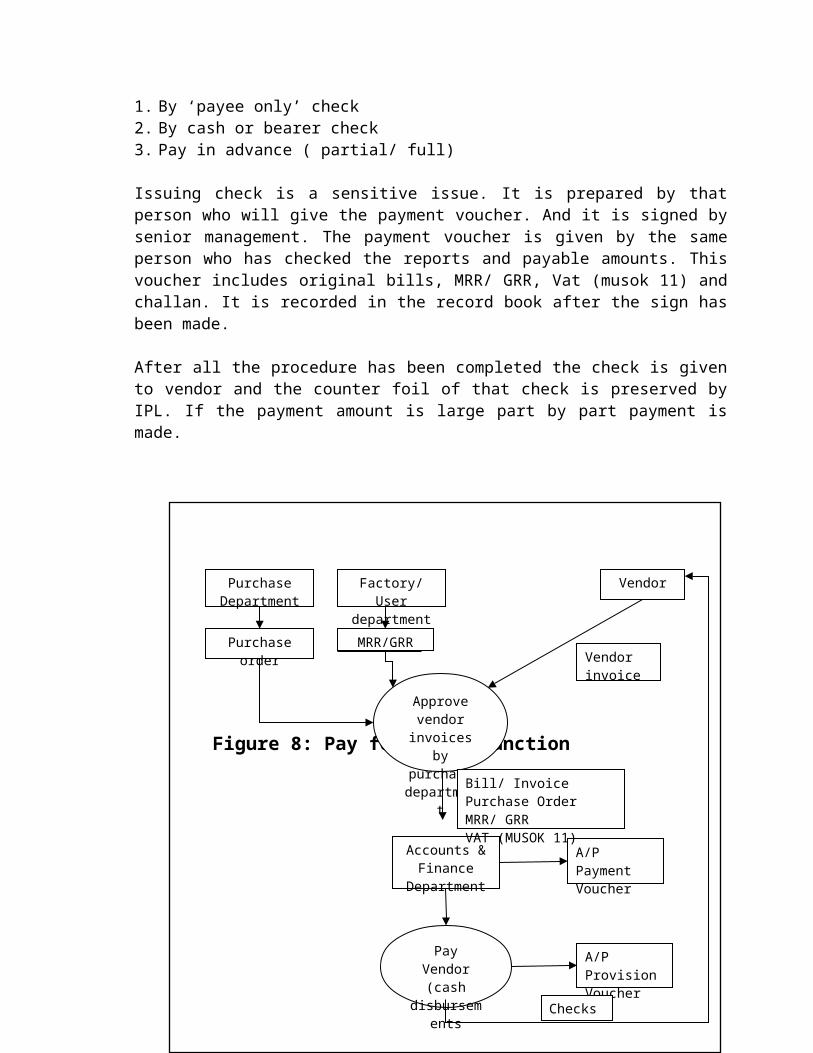

Processing and Recording Check/ Cash Disbursement

After a certain period of time when the date becomes matured for the liability the payment is made by IPL. The matured date has been calculated in the aged payable report for each vendor. The due amount for an individual vendor is identified from vendor business position report. In this stage another report is prepared for forecasting cash requirement. An individual person enters data in “MAPICS” for having this reports and forecasts. The same person checks the arithmetical accuracy, casts, cross casts, deductions and payable amounts. If the checking is matched with those reports checks are issued to pay vendor.

The mode of payment is usually pre numbered check. In most cases the payment is made by payee only check. In some cases the payment may be made by cash or by bearer check or paid in advance fully or partly. So we can say that IPL pays its supplier in three ways-

1. By ‘payee only’ check2. By cash or bearer check3. Pay in advance ( partial/ full)

Issuing check is a sensitive issue. It is prepared by that person who will give the payment voucher. And it is signed by senior management. The payment voucher is given by the same person who has checked the reports and payable amounts. This voucher includes original bills, MRR/ GRR, Vat (musok 11) and challan. It is recorded in the record book after the sign has been made.

After all the procedure has been completed the check is given to vendor and the counter foil of that check is preserved by IPL. If the payment amount is large part by part payment is made.

Figure 8: Pay for Goods Function

36

4.4 Accounting Software

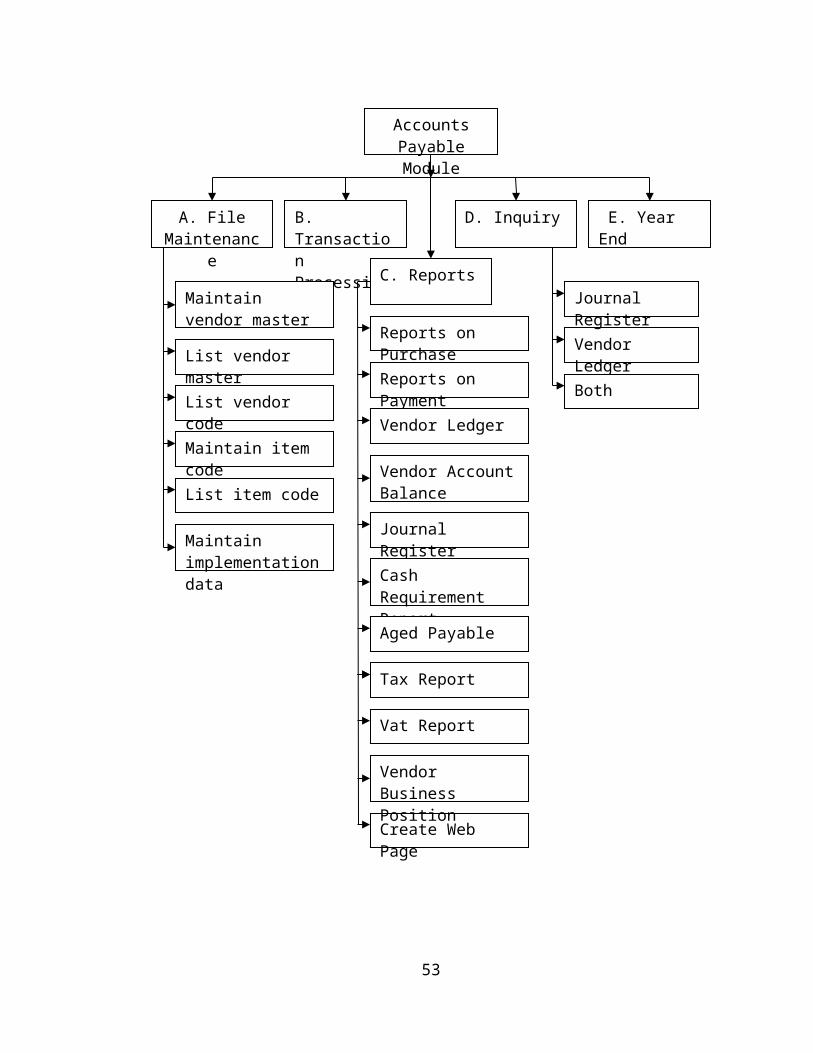

In MAPICS IPL maintains a separate accounts payable module for its own convenient. Through this module related transactions’ records and reports mentioned earlier are kept. Only the authorized personnel of IPL are allowed to use this module. The use of the module is controlled by user password.

Following items are the part of AP module;

Figure 9: Accounts Payable Module

37

Accounts Payable Module

Create Web Page

A. File Maintenance

B. Transaction Processing

D. Inquiry

C. Reports

E. Year End

Maintain vendor master

List vendor master

List vendor code

Maintain item code

List item code

Maintain implementation data

Reports on Purchase

Reports on Payment

Vendor Ledger

Vendor Account Balance

Journal Register

Cash Requirement Report

Aged Payable

Tax Report

Vat Report

Vendor Business Position

Vendor Ledger

Both

Journal Register

Purchase order

Factory/ User department

Vendor

Approve vendor

invoices by purchase

department

Pay Vendor (cash

disbursements

Purchase Department

Accounts & Finance

Department

Vendor invoice

A/P Payment Voucher

A/P Provision Voucher

MRR/GRR

Bill/ InvoicePurchase OrderMRR/ GRRVAT (MUSOK 11)

Checks

John Wiley and Sons; Accounting Payable System, 2000 Edition

CHAPTER FIVE38

ACCOUNTS PAYABLE INTERNAL CONTROL SYSTEMS OF IPL

In the literature review section, methodology for designing tests of controls and substantive tests of transactions has been described. In this section I am going to draw a picture of internal control system of Incepta Pharmaceuticals Ltd. relating to accounts payable. But before starting I want to confess that I have some inherent limitations. Internal control system is very sensitive issue for any organization and I was only an intern at BPL for three months. So it was not possible for me to do all the theoretical works. The picture that I have drawn in the following sections is prepared on basis of interviews with Incepta personnel, internal control questionnaires and my personal observations and assumptions.

5.1 Internal Control Committee

IPL has a specially assigned team to carry out internal financial audits of different segments of the business. The team is known as FSD (Financial System Department). The team is headed by a manager who reports to the CEO. After appropriate review of the report necessary corrective actions are undertaken. IPL claims that it employs a sound system of internal control including internal financial control to ensure compliance of its activities with the desired objectives. It also says that the FSD carries out internal audits of different segments of the business.

It reviews the system periodically Inspects what is done in the factory Inspect the inward and outward of materials and finished goods Review the cash receiving and disbursement process Monitor the activities to make sure that the standard and procedures set out for each

business function is being effectively complied with etc.

5.2 The Controlling System of Accounts Payable

39

A brief description of controlling system of accounts payable of IPL is given below. The description is designed on basis of internal control questionnaires attached in the annexure section.

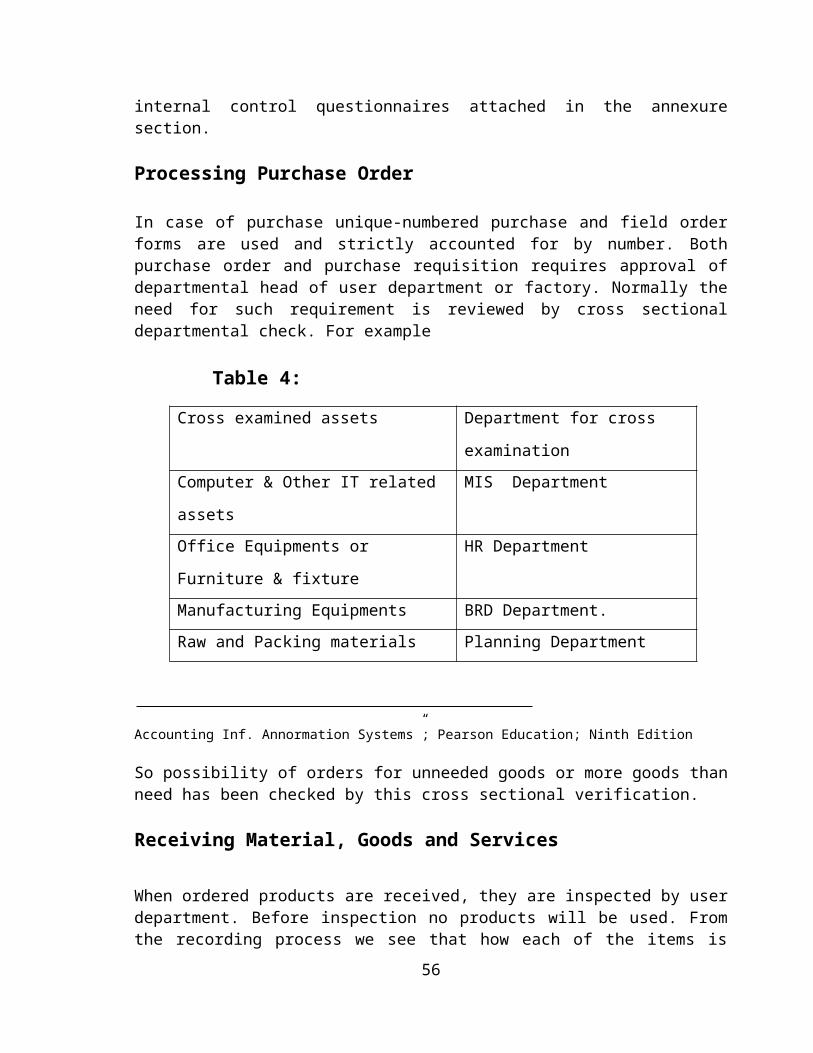

Processing Purchase Order

In case of purchase unique-numbered purchase and field order forms are used and strictly accounted for by number. Both purchase order and purchase requisition requires approval of departmental head of user department or factory. Normally the need for such requirement is reviewed by cross sectional departmental check. For example

Table 4:

Cross examined assets Department for cross examination

Computer & Other IT related assets MIS Department

Office Equipments or Furniture & fixture HR Department

Manufacturing Equipments BRD Department.

Raw and Packing materials Planning Department

Accounting Inf. Annormation Systems”; Pearson Education; Ninth Edition

So possibility of orders for unneeded goods or more goods than need has been checked by this cross sectional verification.

Receiving Material, Goods and Services

When ordered products are received, they are inspected by user department. Before inspection no products will be used. From the recording process we see that how each of the items is examined, who are responsible for inspection and what is inspected there. According to me the internal control system at this stage is satisfactory because the ordering department and the receiving department are different. Normally the user department receives items. In some cases items are received by another department, a third one. It inspects the items received and after inspection the product is sent to user department.

Recognizing the Liability and cash disbursement

40

Invoices are matched with purchase orders and receiving reports before approval for payment. Invoice computations and pricing are verified before approval for payment and are paid in a timely manner so that discounts may be taken. Monthly statements are compared with accounts payable balances. Payable Subsidiary Ledgers are reconciled to the control accounts monthly. Copies of the order forms are distributed to receiving and accounting departments. Claims are filed promptly for goods damaged in shipment.

The responsibility for disbursement procedures is clearly documented and assigned to specific personnel of IPL. Disbursements are handled in such a manner as to ensure that the proper funds and accounts are charged; that the disbursement is used only for authorized purposes; and that laws, rules, and regulations governing the disbursement are followed. Controls are established to assure that all payments are made on a timely basis and in accordance with all purchase orders and contracts and to ensure that duplicate payments are not made.

In IPL original invoices totaling the amount of the disbursement are to be attached to each voucher before payment. Employee duties in the handling of disbursements are separated to the extent possible with regard to:

The initiation of purchase requisitions and field orders. The approval of vouchers, invoices, and warrant registers. The preparation of checks. The recording of disbursements. Each cash disbursement is properly vouched and approved by the proper authorities

of the agency before the actual disbursement occurs. This will ensure the proper and regular review of all disbursements.

To the extent possible, employee duties in this area are to be complementary to or checked by another employee. Disbursements are to be made by and counter signatures provide an additional control. Blank checks are to be kept in locked storage under the control of a designated, responsible employee.

A separate record is maintained for each check series issued or voided. The record for voided warrants is to include the date voided, inclusive serial numbers, quantity voided, reason for voiding, and initials of individual taking action.

The bank checks of IPL are pre-numbered. They are completely filled out before being presented for signature. Someone maintains physical control of checks other than persons originating disbursement requests. Normally dual signatures are required on all checks.

Bills or vouchers are presented with checks for signature and are marked "Paid only” at the time checks are signed. The same person mails and prepares checks someone approves bills for payment other than the persons who sign checks. Bank statements are reconciled at least monthly by an employee not involved in cash receipt or disbursement procedures.

5.3 Internal Control Keys for Accounts Payable

41

In this section I am trying to compare my practical knowledge with theoretical. As described earlier key internal controls for accounts payable are;

1. Authorization of Purchases2. Separation of Asset Custody from Other Functions3. Timely Recording and Independent Review of Transactions4. Authorization of Payments

Major Internal Control Issue

This control is essential because it ensures that goods or services acquired are actually needed by the organization. It avoids the excessive or unnecessary items. There are some important controls regarding this area;

There should be an authorized person for acquisition of products

Different authorized personnel are required for acquiring different items

Approval of departmental head is required

There should be a specified limit. If the ordered amount cross that limit approval of Board of Directors is required

No purchase order would initiate without purchase requisition

Purchase order should be in written form because it’s a legal document to buy

The purchase department should not be responsible for authorizing the acquisition or receiving the goods.

All purchase order should be pre-numbered and have enough space to minimize unintentional omissions

Internal Control Procedure Followed by IPL

As described earlier in recording process section, at IPL the user department sent purchase requisition to purchase department with the approval of departmental head. An authorized person check that requisition and made the purchase order. Without purchase requisition no purchase order will be made. In case of materials, the planning department identifies the required quantities of materials and sent requisition to purchase department. And in case of fixed asset IPL required approval of CEO or deputy chairman. But before requisition a budget has been made for that asset. In each case there is a limit amount for ordering goods.

The purchase order document contains a unique number. This unique number is used as reference for further proceeds. It also contains the signature of the person raising requisition. The purchase department is responsible for making the order only. It is not responsible for authorizing or receiving goods. It maintains a purchase register where all given orders are recorded with ordered item, quantity, unit price and suppliers’ name. Separation of Asset Custody from Other Functions

Major Internal Control Issue

42

This control key says that

The receiving department should initiate the receiving report and the inspection report.

Both documents should be prepared in multiple set. Among them one set should be kept by the receiving department and others should be sent to accounts department and store room.

Goods should be physically controlled from the time of their receipt to disposal. This will help to prevent theft and misuse.

The personnel in the receiving department should be independent of the storeroom personnel and the accounting department.

The accounting records should transfer responsibility for the goods as they are transferred from receiving department to storage and from storage to manufacturing.

Internal Control Procedure Followed by IPL

Usually, the ordered items are received by user department. But in case of inventorial item, that is raw or packing material, it is received by factory. The receiving department produces the MRR/ GRR. The same report is also used as inspection report. In case of raw or packing material, Quality Assurance Department generates Quality Assurance report. One copy of MRR/ GRR/ QA is kept by the receiving department, one copy is sent to purchase department and another copy is sent to accounts department. So the personnel are separate from each other. Again there is a physical control over item from their acquisition to disbursement. A cross departmental monitoring activity is a common scene here.

Timely Recording and Independent Review of Transactions

Major Internal Control Issue

The accounts payable department recognizes the liability at the time of receiving goods or deferred until the vendors invoice is received. The department has the responsibility for verify the propriety of acquisitions.

The department should compare the details on the purchase order, receiving report and the vendor’s invoice

Extensions, footings, and account distributions should be verified. Personnel who record acquisitions do not have access to cash, marketable securities,

and other assets. Adequate documents and records should be kept

Internal Control Procedure Followed by IPL

IPL recognizes accounts payable as its liability at the time of vendors invoice is received. It recognizes the liability by analyzing the following documents;

43

Not negotiable copy of purchase order MRR/ GRR Not negotiable copy of invoice/ bill Vat report

If the person is satisfied with those documents he will then give the provision voucher. This person does not have the access to handle the cash, securities or other assets.

Authorization of Payments

Major Internal Control Issue

It’s a very important control. This control includes Checks should be signed by an individual with proper authority The personnel signs the check and performs accounts payable function should be

separate The check signer should carefully examine the supporting documents at the time of

signing the check The checks should be pre-numbered and printed on special paper Care should be taken on voided and signed checks.

Internal Control Procedure Followed by IPL

IPL pays its vendors after the date has been matured for payment. Normally the payment is made by pre-numbered check. A separate person gives the payment voucher. Before giving payment voucher he checks all the documents and reports relating to that transaction and also examined that the bills are approved by purchase department. The payment voucher includes original bills, MRR/ GRR, VAT (MUSHOK 11) and challan.

When the authorized person signs the checks, he just skims through the attached documents with the payment voucher. Normally these signs are made by managers or director of accounts and finance.

CHAPTER SIX FINDING &

44

RECOMMENDATION

6.1 Findings

Recording process of Accounts Payable in IPL is the most modern in Bangladesh Pharmaceuticals Business. The following Findings are made on the basis of the research for further improvement of the organization.

Source of documents (which are provide from Purchase Department) are not timely available to initiate the process of recording transaction and associated works.

Even when purchase department sends the documents timely. Some of these are missing due to indecent file maintenance. A separate file is maintained in a slapdash manner, especially without any sequence. Sometimes they are kept in other files. It requires extra time for searching the right one as and when needed.

Purchase department do not verify all relevant information sincerely. For that reason finance & accounts department respective person fall in many problem to complete party bills and record. Its time consuming.

The existing IPL accounts payable software is looking pretty difficult and not enough friendly for the user. Without trained person fall in difficult to operate it.

Some times documents are received in time but unrecorded and piled up for processing in the future when some other documents will come.

Incepta provide very good job environment for their personnel. That is very important for better business.

IPL need to provide priority (Job) for the BBA internees. Other wise may they can’t show their best performance in the work, and also IPL may loss someone they are looking for.

6.2 SWOT analysis of Incepta Pharmaceutical Ltd

Strengths

The company has successfully built up a good reputation.

45

The market share of the company is now around 4.67% with 42.47% annual

growth rate.

There is no financial liabilities of the company and the cash flow is steady and

stable

Over the last five years, the company has successfully launched numerous

products that provided the utmost demand of the customers as well as good

customer satisfaction.

Incepta pharmaceuticals ltd has the necessary technical experts in respective

fields-

(Chemists, Microbiologists, Doctors, Biochemists. Medical promotion officer

etc)

The product quality of the company is better than any other company

The service quality of the company is outstanding. The company regularly

provides doctors with the latest information regarding the development of the

medical science.

The distribution network of the company covers every corner of the country.

The product promotion effort of the company is outstanding and beat the

company in that industry with a big margin.

The sales force of the company is one of the youngest, largest and most dedicated

to lead in the country.

The company is capable is introducing the latest innovative products in the

country.

There is a well-developed formulation research and development laboratory.

The manufacturing facility of the company is one of the largest and most

advanced in the country.

The company management is proactive and the company practice a flexible

market oriented planning and execution.

Weaknesses

The company is entirely dependent on imported raw materials for production.

As the company is new and is heavily investing in capital machineries and

infrastructure import from other countries.

46

Although the company has plan for export but at the moment is too occupied in local

market development and recently started to explore market outside the country.

Rules and regulation are still in the process of development.

A dedicated human resource development is lacking now.

Employee’s benefits are not up to the mark in many cases.

Recruitment in many areas is lacking in systematic approaches and procedures.

The employees of the company are relatively young and lack of experience,

especially in sales and distribution.

There are very few experts on reverse engineering analogue research and chemical

synthesis available in this country so company is hiring employees from abroad

giving high remuneration.

Opportunities

From 2000 onwards Bangladesh being a member of LDC country will be allowed to

produce cheap copies of patented drugs and their raw materials.

Incepta having a CGMP(Current Good Manufacturing Practice ) compliant factory

and one of the best technological know Who in the industry can take the expert

opportunities that lie ahead.

The current level of penetration of allopathic medicine in Bangladesh is low and is

expected to increase significantly in the coming days. This is a great opportunity for

Incepta to penetrate the market at this growing stage.

If the government extends necessary support to the industry, it has the potential to

become, a very big export sectors both API and formulation products to all the LDC

countries and off patented formulation products to developing and developing

countries.

As Indian and Chinese companies will not be able to produce patented active

ingredients but they have the necessary technology and expertise in reserve

engineering and chemical synthesis they will be more interested in cooperation with

Bangladesh after 2004

As multinational companies will be allowed to come to Bangladesh for business.

Similarly, Bangladeshi companies will also have access to other countries for export

of both formulation products and raw materials under the open market system.47

Taking advantages Of TRIPS Agreement, Patented products for LDC.

Chief labor and cost advantage ,compare to world Generic Market

Threats

The present regulation does not allow local companies to advertise their OTC drugs

in the mass media whereas these are allowed in neighboring countries already

creating a market for those products. This situation is very likely to worsen in the

post 2010 scenario.

The drug act 1940 & the drug policy of 1982 need to be revised soon on order to

copy with the post 2004 scenario.

In the post 2010 scenario Bangladesh may end up not having the necessary raw

materials for its products .Incepta may also be forced to buy raw materials from the

innovator company at a much higher price leading to price hike and market

shrinkage.