Embed Size (px)

Citation preview

Corporate Finance

Final project: The Air transportation industry

Submitted by: Andrea Trozzi Braulio Serna

David Calvo Platero Dimitar Petrov

New York University New York

May2, 2005

1

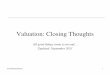

Company Risk Characteristics Investment Performance Capital

Structure Dividend Policy Valuations

Approach Beta Jensen's Alpha

R squared

ROE - COE

ROC - WACC EVA

Current Debt ratio

Optimal Debt Ratio

Change in

WACC

Duration Dividends FCFE Value/share Price/Share American Airlines B 6.26 -5.92% 35.00% n.m.

-8.15% (1,129.50) 86.65% 20.00%

-7.06% 0 0 765.3

10.06

10.20

Ryanair B 1.24 27.35% 27.00% 5.24% 2.01% 53.30 23.87% 10.00% -

0.04% 5.3 0 23.5205 6.76

5.55

BAA B 1.42 4.43% 7.00% -

2.80% -

2.27% (191.00) 44.86% 45.00% 0.00% 3.3 145 257.1 3.22

5.80

Asur B 0.82 28.42% 15.00% -

3.23% -

3.53% (37.30) 0.00% 20.00% -

0.54% 0 14.3 41.2 31.69

30.45

1

EXECUTIVE SUMMARY................................................................................................... 3

INTRODUCTION AND THE COMPANIES........................................................................ 4

1. Introduction ......................................................................................................................................................................... 4

2. Brief description of the companies .................................................................................................................................. 6

CORPORATE GOVERNANCE ANALYSIS ...................................................................... 8

1. Balance of power between management and shareholders .......................................................................................... 8

2. Management compensation.............................................................................................................................................. 9

3. Market coverage................................................................................................................................................................ 11

4. Social responsibility.......................................................................................................................................................... 12

STOCKHOLDER ANALYSIS.......................................................................................... 14

RISK PROFILE ............................................................................................................... 16

1. Market risk and return...................................................................................................................................................... 16

2. Bottom up betas................................................................................................................................................................ 20

3. Cost of equity .................................................................................................................................................................... 22

4. Cost of debt........................................................................................................................................................................ 23

5. Cost of capital.................................................................................................................................................................... 25

INVESTMENT RETURN ANALYSIS............................................................................... 27

1. Typical project ................................................................................................................................................................... 27

2. Measuring Returns ........................................................................................................................................................... 28

3. Future outlook................................................................................................................................................................... 30

CAPITAL STRUCTURE CHOICES................................................................................. 33

1. Current financing mix ...................................................................................................................................................... 33

2. Trade off on Debt and Equity......................................................................................................................................... 35

2

OPTIMAL CAPITAL STRUCTURE................................................................................. 37

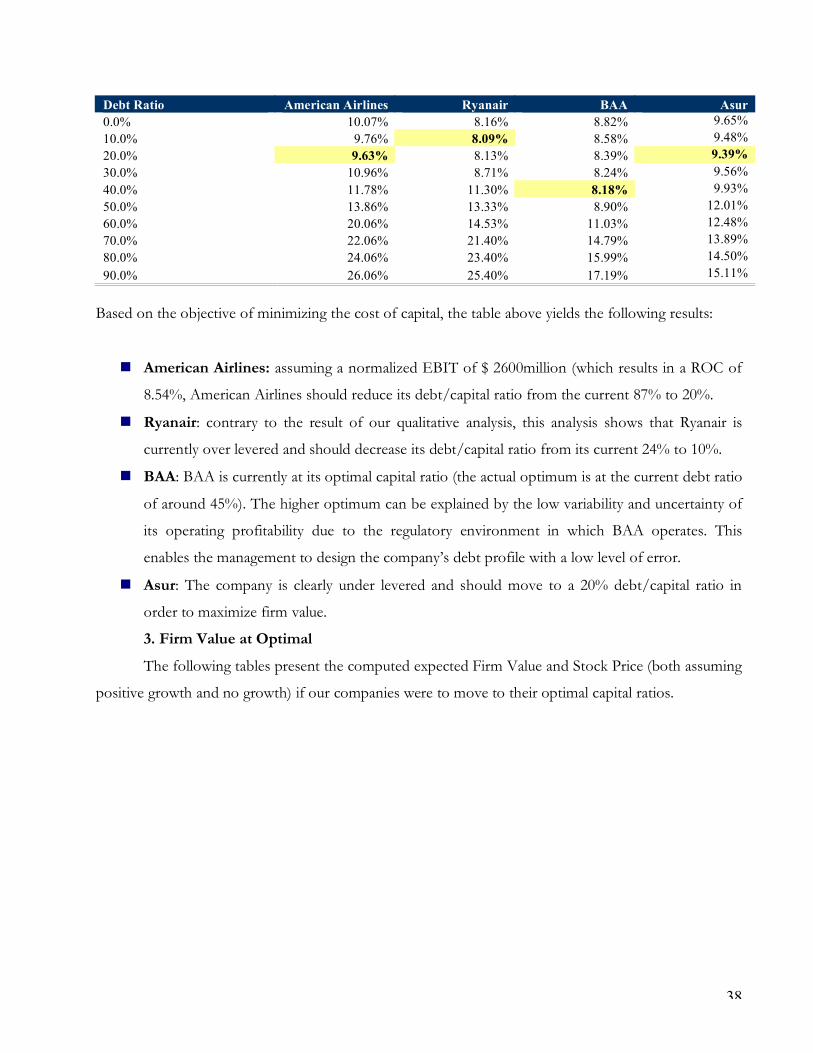

1. Current Cost of Capital / Financing Mix ...................................................................................................................... 37

2. Cost of Capital at Different Financing Mixes............................................................................................................... 37

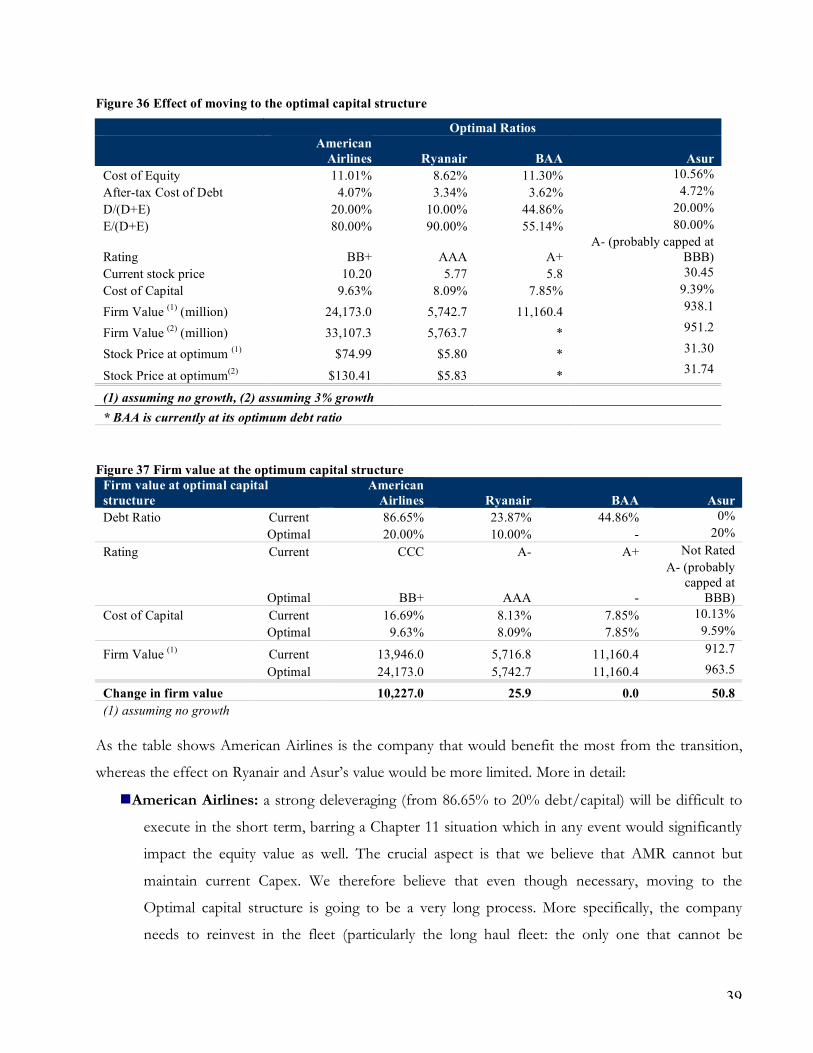

3. Firm Value at Optimal ..................................................................................................................................................... 38

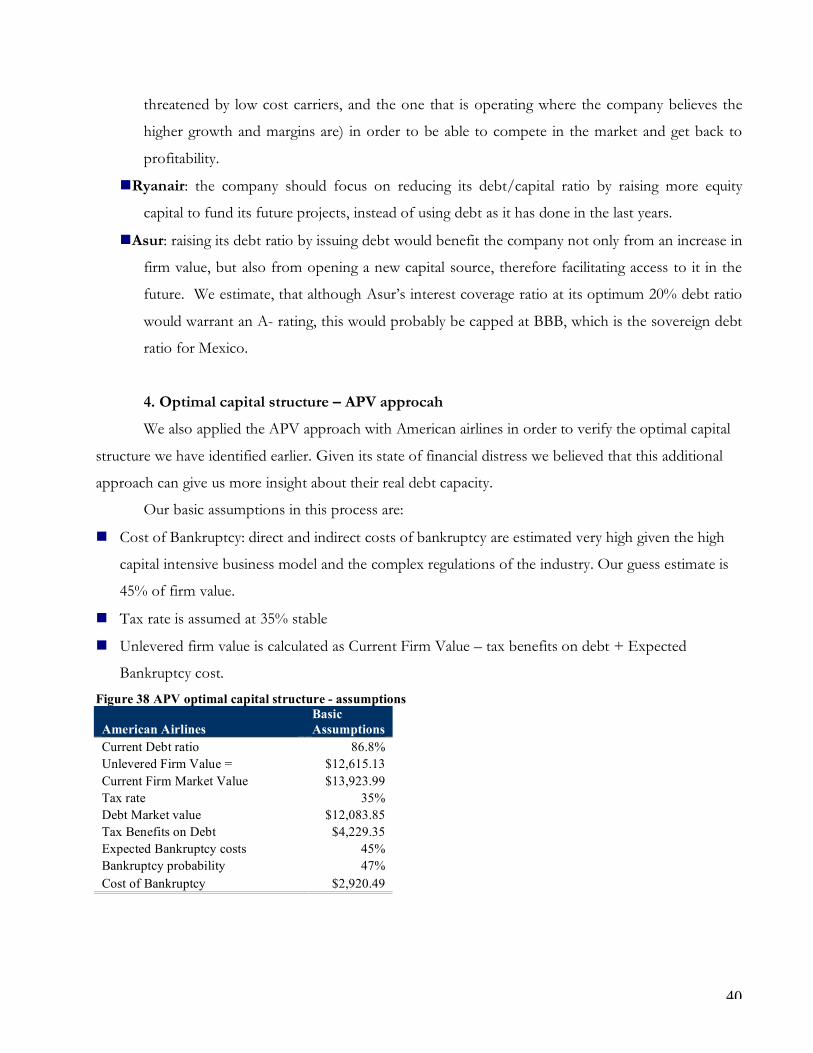

4. Optimal capital structure – APV approcah ................................................................................................................... 40

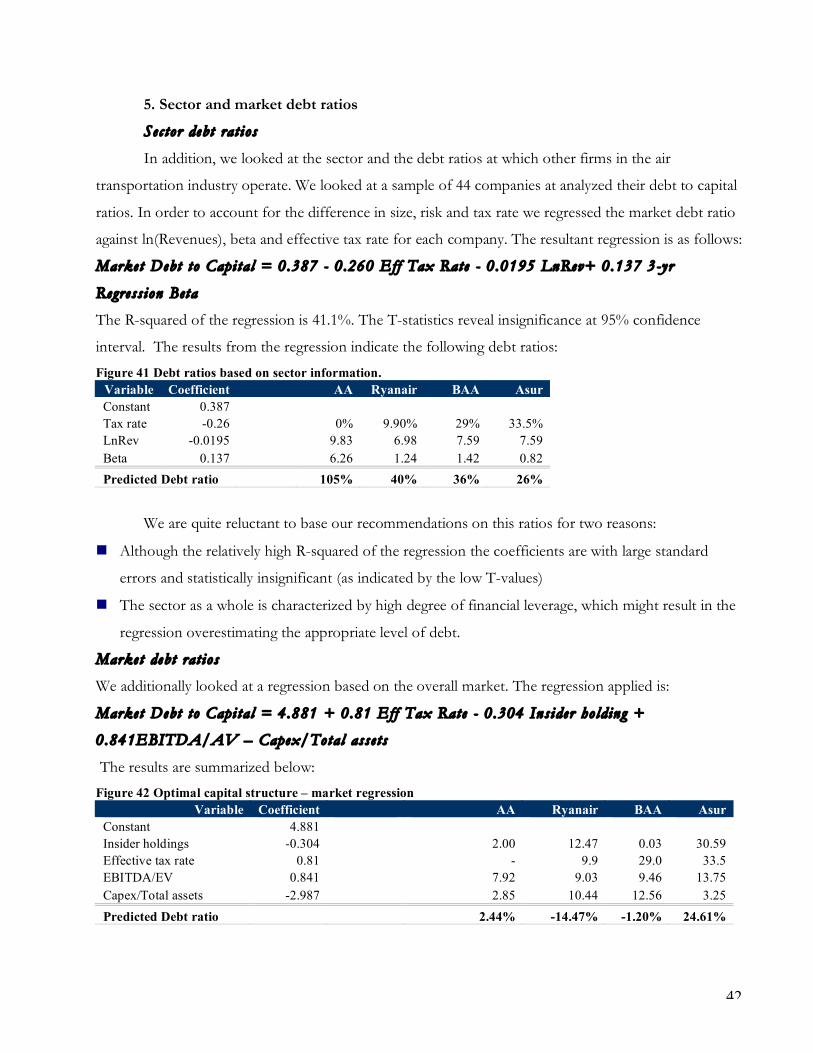

5. Sector and market debt ratios ......................................................................................................................................... 42

MECHANICS OF MOVING TOWARDS THE OPTIMAL................................................. 43

1. A Path to the Optimal...................................................................................................................................................... 43

2. Quantitative Analysis and Overall Recommendation on Financing Mix................................................................. 43

3. Summary of desirable debt charachteristics ................................................................................................................. 47

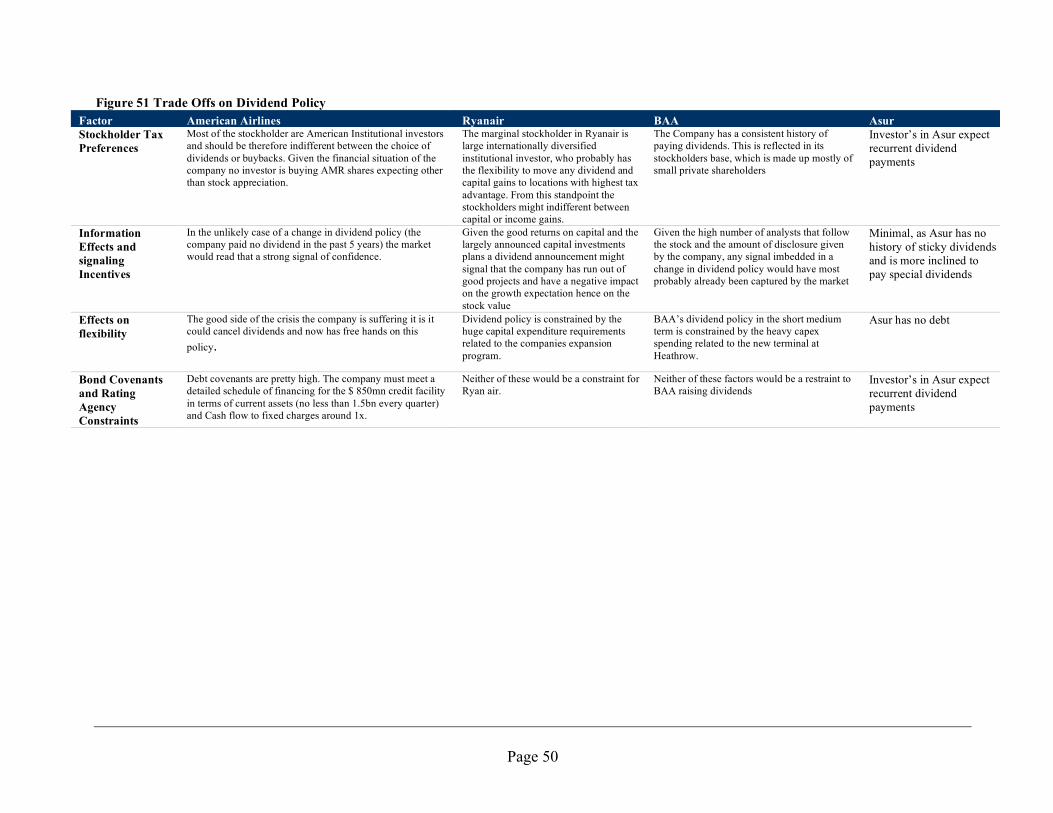

DIVIDEND POLICY ......................................................................................................... 48

1. Current Dividend Policy .................................................................................................................................................. 48

DIVIDEND POLICY: A FRAMEWORK ........................................................................... 51

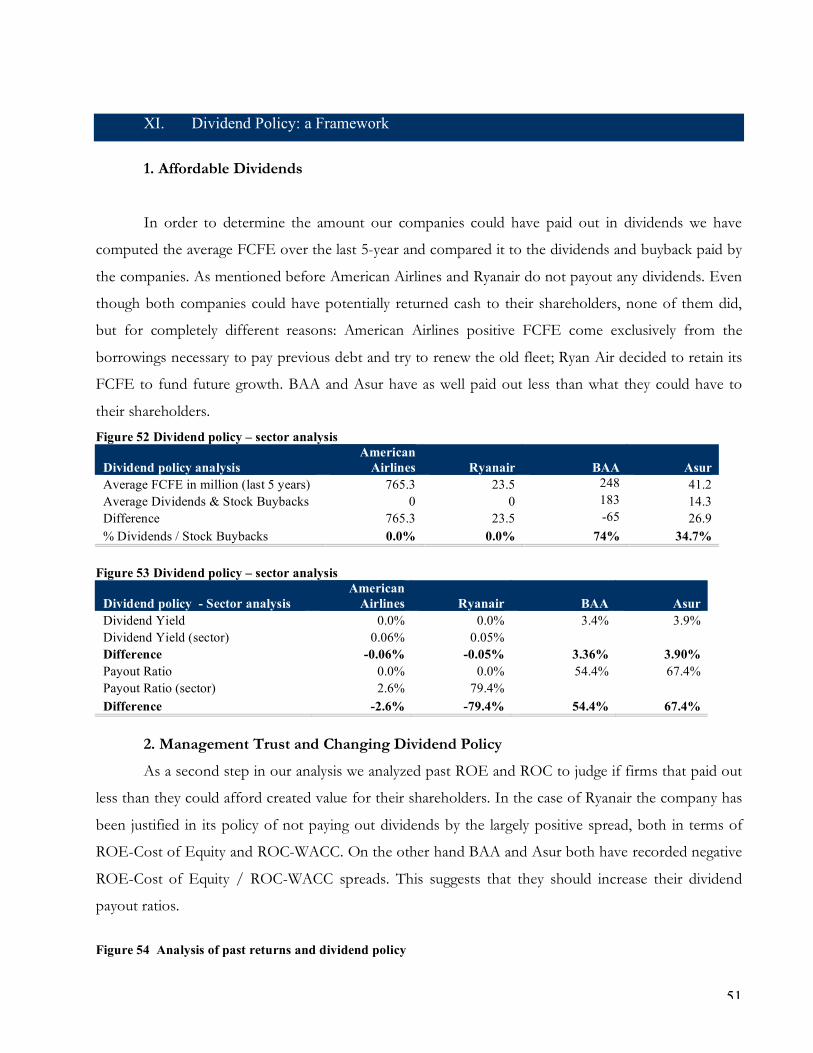

1. Affordable Dividends........................................................................................................................................................ 51

2. Management Trust and Changing Dividend Policy ................................................................................................... 51

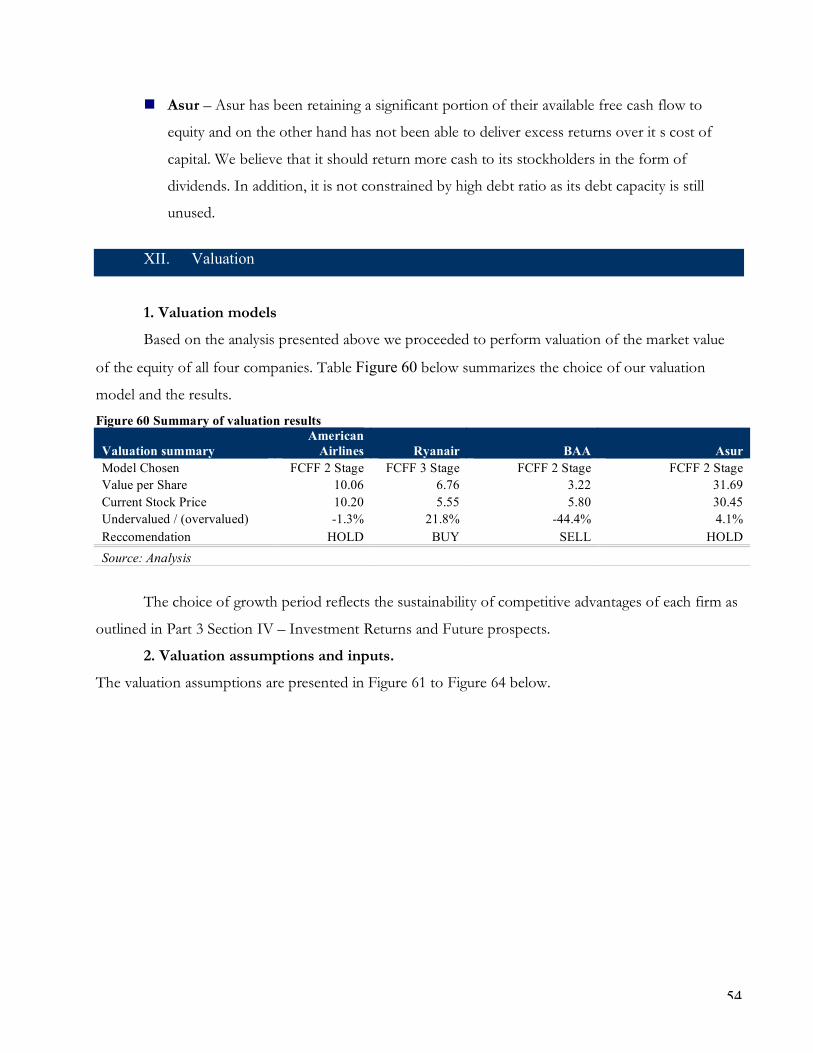

VALUATION.................................................................................................................... 54

1. Valuation models .............................................................................................................................................................. 54

2. Valuation assumptions and inputs................................................................................................................................. 54

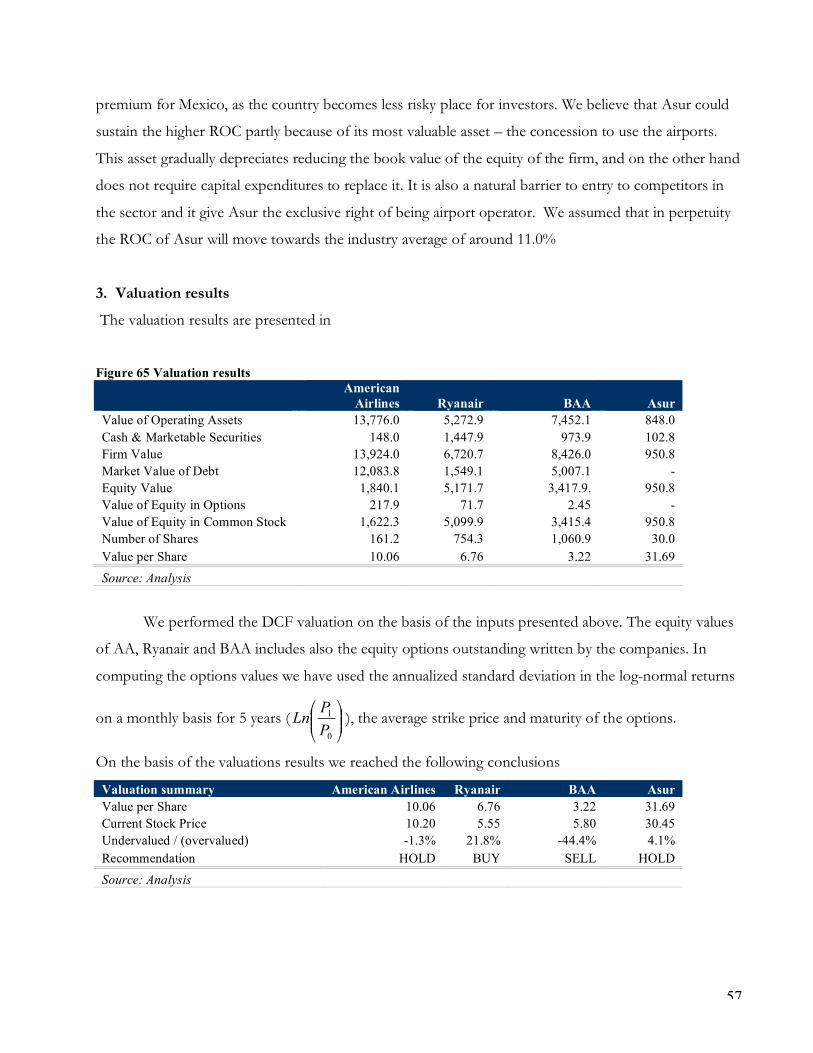

3. Valuation results .............................................................................................................................................................. 57

3

I. Executive Summary

Corporate Governance and Stockholder analys i s

We believe that the stockholders’ interests are generally well protected in the companies

subject to our review with the exception of American Airlines, which has some controversial

corporate governance practices in place. The marginal investor in all companies is well diversified,

often internationally, investors. In three out the four companies there were significantly large

institutional holdings.

Risk Prof i l e

We used two measures of bete to estimate the exposure of each company to market risk. Not

surprisingly, the results reflect the fundamental characteristics of each company and in particular

variance of earnings and leverage. The riskiest company as measured by historical regression beta is

American Airlines and the least risky – BAA. Because of the historical character of the regressions

beta and high standard errors of the estimates we used bottom-up betas in our further analysis.

In addition, we used two methods to compute returns of each company with relation to its risk

– Jensen’s Alpha and Treynor ratio. Under both methods the top performing companies were Ryanair

and Asur.

Inves tment analys i s

In analyzing the returns of the investment projects at which companies we looked at a typical

project in each line of business and computed accounting measures of returns, such as ROC and

ROE. Ryanair proved to be the company with highest returns and it was the only company that

generated positive EVA. In addition we assessed the future prospects of each company, analyzing the

sustainability of its competitive advantages. This analysis was used as a basis for the valuation of the

firms.

Capi tal s t ruc ture

The four companies adopt very different policies with regards to their capital structure,

ranging from the highly overlevered American Airlines (debt ratio of 87%) to the all equity financed

Asur. Taking into account the potential benefits and disadvantages from the use of debt we computed

optimal capital structures for each firm and assessed the impact on the share price from moving from

the current capital structure to the optimal. The result was an average of 8.12% increase in the firm

4

value of the firms, although most of this increase comes from American Airlines. It was interesting to

find that BAA’s current debt ratio is equal to its optimum – roughly 45%.

Dividend pol i cy

Both Amrican Airlines and Ryanair are non-dividend paying companies, although for very

different reason. While focus of AA’s policies is to return to profitability before being able to afford

any dividends, Ryanair exhibits a great potential to invest in projects with positive excess returns

(ROC exceeds Cost of capital). BAA and Asur are companies with more steady and predictable cash

flows and reinvestment needs and this is reflected in their dividend policies. Our analysis is presented

in Sections X and XI.

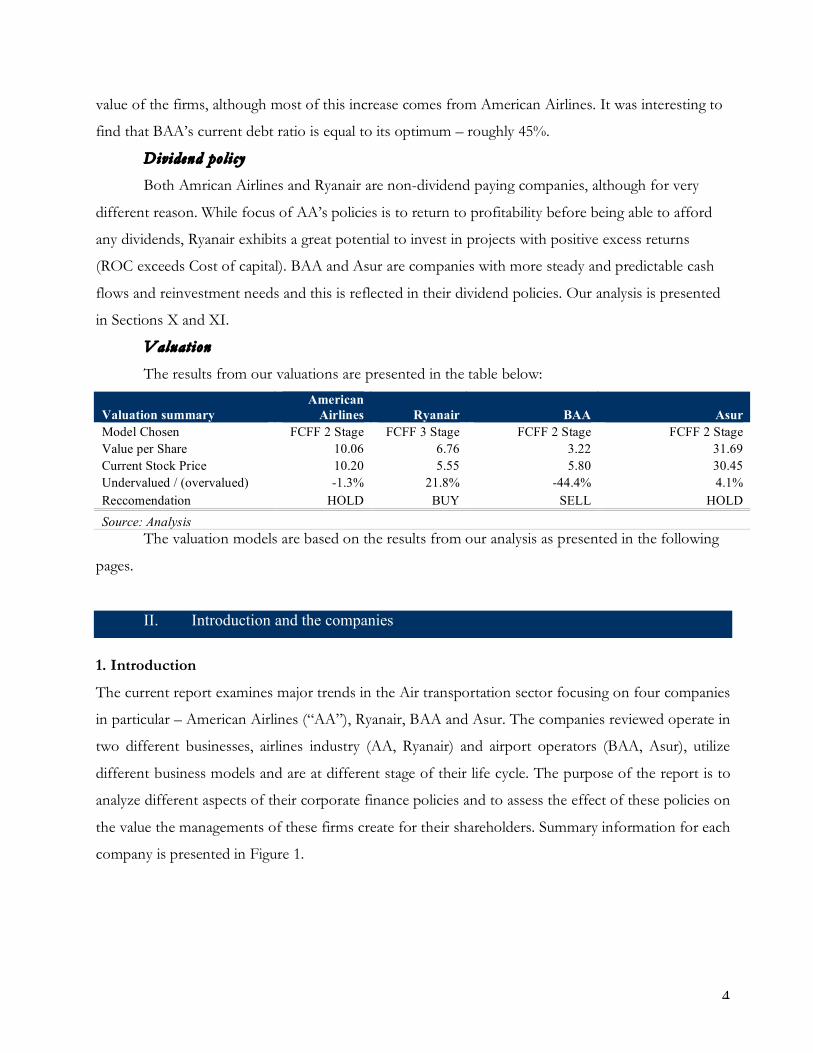

Valuat ion

The results from our valuations are presented in the table below:

Valuation summary American

Airlines Ryanair BAA Asur Model Chosen FCFF 2 Stage FCFF 3 Stage FCFF 2 Stage FCFF 2 Stage Value per Share 10.06 6.76 3.22 31.69 Current Stock Price 10.20 5.55 5.80 30.45 Undervalued / (overvalued) -1.3% 21.8% -44.4% 4.1% Reccomendation HOLD BUY SELL HOLD Source: Analysis

The valuation models are based on the results from our analysis as presented in the following

pages.

II. Introduction and the companies

1. Introduction

The current report examines major trends in the Air transportation sector focusing on four companies

in particular – American Airlines (“AA”), Ryanair, BAA and Asur. The companies reviewed operate in

two different businesses, airlines industry (AA, Ryanair) and airport operators (BAA, Asur), utilize

different business models and are at different stage of their life cycle. The purpose of the report is to

analyze different aspects of their corporate finance policies and to assess the effect of these policies on

the value the managements of these firms create for their shareholders. Summary information for each

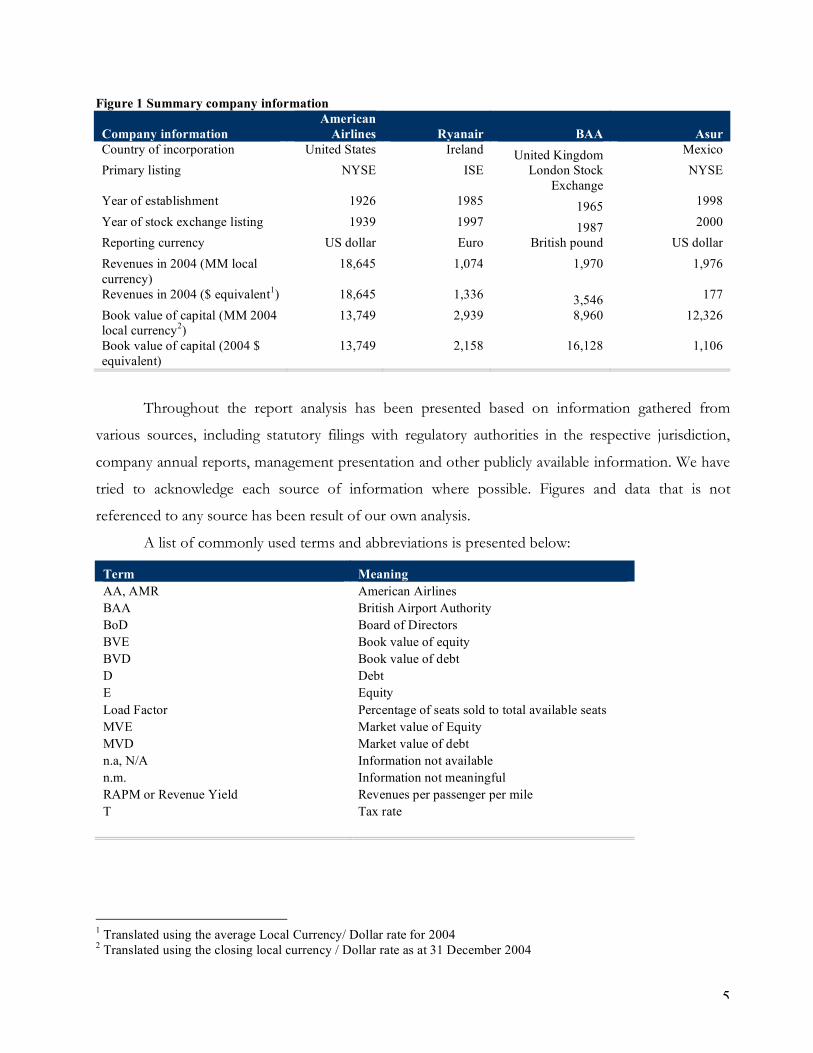

company is presented in Figure 1.

5

Figure 1 Summary company information

Company information American

Airlines Ryanair BAA Asur Country of incorporation United States Ireland United Kingdom Mexico Primary listing NYSE ISE London Stock

Exchange NYSE

Year of establishment 1926 1985 1965 1998 Year of stock exchange listing 1939 1997 1987 2000 Reporting currency US dollar Euro British pound US dollar Revenues in 2004 (MM local currency)

18,645 1,074 1,970 1,976

Revenues in 2004 ($ equivalent1) 18,645 1,336 3,546 177 Book value of capital (MM 2004 local currency2)

13,749 2,939 8,960 12,326

Book value of capital (2004 $ equivalent)

13,749 2,158 16,128 1,106

Throughout the report analysis has been presented based on information gathered from

various sources, including statutory filings with regulatory authorities in the respective jurisdiction,

company annual reports, management presentation and other publicly available information. We have

tried to acknowledge each source of information where possible. Figures and data that is not

referenced to any source has been result of our own analysis.

A list of commonly used terms and abbreviations is presented below:

Term Meaning AA, AMR American Airlines BAA British Airport Authority BoD Board of Directors BVE Book value of equity BVD Book value of debt D Debt E Equity Load Factor Percentage of seats sold to total available seats MVE Market value of Equity MVD Market value of debt n.a, N/A Information not available n.m. Information not meaningful RAPM or Revenue Yield Revenues per passenger per mile T Tax rate

1 Translated using the average Local Currency/ Dollar rate for 2004 2 Translated using the closing local currency / Dollar rate as at 31 December 2004

6

For computational ease the analysis for each company has been undertaken in the reporting

currency under which the company reports annual results – US dollars (for AA and Asur), Euro

(Ryanair), British pounds (BAA). All figures are in million local currency unless otherwise indicated.

2. Brief description of the companies

Ameri can Airl ines

AMR was established in 1926 and had Charles Lindberg as chief pilot of its fleet of 3 DH 4 bi-

planes. The company was listed in 1939 and throughout the years grew on acquisitions and survived

several crisis (included World War II that forced them to turn half of the fleet to the military airline).

The company grew internationally and domestically especially after the deregulation act of 1978. In

2001, before September 11 acquired all the assets of TWA, but then was hit by an economic recession,

increased competition from low cost carriers and the terrorist attack.

Nowadays AMR Corporation is a holding company that provides scheduled passenger and

airfreight services to approximately 150 destinations in North America, the Caribbean, Latin America,

Europe and the Pacific through its American Airlines subsidiary. The Company in 2004 employed

roughly 92,000 people and its headquarter is at Dallas Forth Worth Airport, Texas. For the FY ended

12/31/04, revenues rose 7% to $18.65B. Net loss fell 38% to $761M. Results reflect higher affiliate

passenger revenues a decline in wage costs but also an increase in fuel costs.

Ryanair

Ryanair was founded in 1985 by the Ryan family in Ireland. It started with one scheduled flight

between south-eastern Ireland and London Gatwick. First crew members were required to be less

than 5 foot 2 inches tall in order to fit in the tiny cabin of the only 15-seater aircraft. Soon after its

launch, the company acquires permission to challenge British Airways and Aer Lingus on the Dublin –

London route. The number of passengers grew from 5,000 to 82,000 in the first 2 year of operations.

The next few years are marked by growth in the number of routes and passengers between Ireland and

the United Kingdom. However, by 1990 the company had accumulated over � 20 million in losses.

The Ryan family invested additional 20 million in capital in the business which went through

substantial financial and operational restructuring – copying the South West Airlines model, Ryanair

was re-launched as Europe’s first low cost airline. This was a revolutionary new model for the

European air transportation market and some publications note that “people queued up for three days

7

to get the Easter sale fares”. The new model incorporated move towards same aircraft fleet, direct

sales, scrapping of drinks and food served on board and cutting turnaround time and costs. In 1995

the company launches the first low cost airfares on UK routes and in 1997 – in Europe. In the same

year the company gets listed on the Irish Stock Exchange. Promotional fares of � 1 on domestic and

European routes attracted the attention of passengers. Today, Ryanair is the largest European low cost

airline carrying over 7 million passengers annually on 220 routes across 19 countries. Operations are

concentrated in 12 European bases and the company employees over 2,600 employees.

BAA

BAA is engaged in the management and operation of airport facilities in the UK and overseas.

The company is headquartered in London, UK and has a workforce of about 12,500 employees. The

company owns seven UK airports: Heathrow, Gatwick, Stansted, Glasgow, Edinburgh, Aberdeen and

Southampton. BAA also has interests in 13 airports located in Italy, Australia, US and Oman. BAA’s

airports in the UK and overseas serve 230 million passengers a year. The company’s operations are

divided into the following segments: airports, retail, BAA Property, rail and other. The airport segment

primarily oversees terminal and airfield management. In the terminal management area, the company

looks after buildings, passenger services and cargo. In the airfield management division, the company

maintains and operates runways and taxiways. BAA also develops, manages and markets commercial

activities at its UK airports. BAA’s UK airport retail activity is made up of two complementary

businesses: Retail management at UK airports and World Duty Free. Retail management at UK

airports involves the development, management and marketing of commercial activities at BAA’s

seven UK airports. These include shopping, catering, financial services, travel, services, parking,

telecommunications and media management. The business specializes in luxury brands and operates

64 stores across the UK airports.

Asur

Grupo Aeroportuario del Sureste (“Asur”) holds a concession from the Mexican government

to operate, maintain and develop nine airports in the, primarily touristic, Southeastern region of

Mexico. The company’s main airport is the Cancun International Airport, which generates over 70%

of Asur’s revenues and is the second busiest airport in Mexico. Cancun and the surrounding Mayan

Riviera, are Mexico’s top tourist destination and among the fastest growing tourist developments in

the country. Asur’s nine airports served more than 13.8 million passengers in 2004, of which around

8

60% were international passengers and 40% were domestic passengers. Approximately 70% of the

international passengers traveled on flights originating from the United States. As of 2003, 17

Mexican and 45 international airlines operated directly or through code-sharing agreements from

Asur’s airports.

Asur was established in 1998 as part of the Mexican government’s airport privatization program,

which included three regional airport groups and the Mexico City International Airport. A private

consortium, ITA, led by Copenhagen Airports won the 50-year concession to operate the nine airports

in the Southeastern group. The consortium acquired a 15% stake in Asur, while the remaining shares

were floated in the NYSE and the Mexican Stock Exchange on October 3, 2000. The Mexican

government, through one of its development banks, Nafin, retained an 11.1% stake in Asur to be

floated on a future date. As the long-term operator of the airports, Asur generates revenues from two

main sources: aeronautical services and non-aeronautical services. The former account for 75% of

total revenues and are derived primarily from passenger and landing charges, aircraft parking charges,

and general airport services. Non-aeronautical services are divided into retail operations and access

fees charged to third-party providers of complementary services. While the aeronautical revenues are

heavily regulated by the Mexican government, the retail operations and access fees provide an

important growth opportunity for Asur. These have grown at a compounded annual growth rate of

22.9% since 1999, when they accounted for only 14% of total revenues.

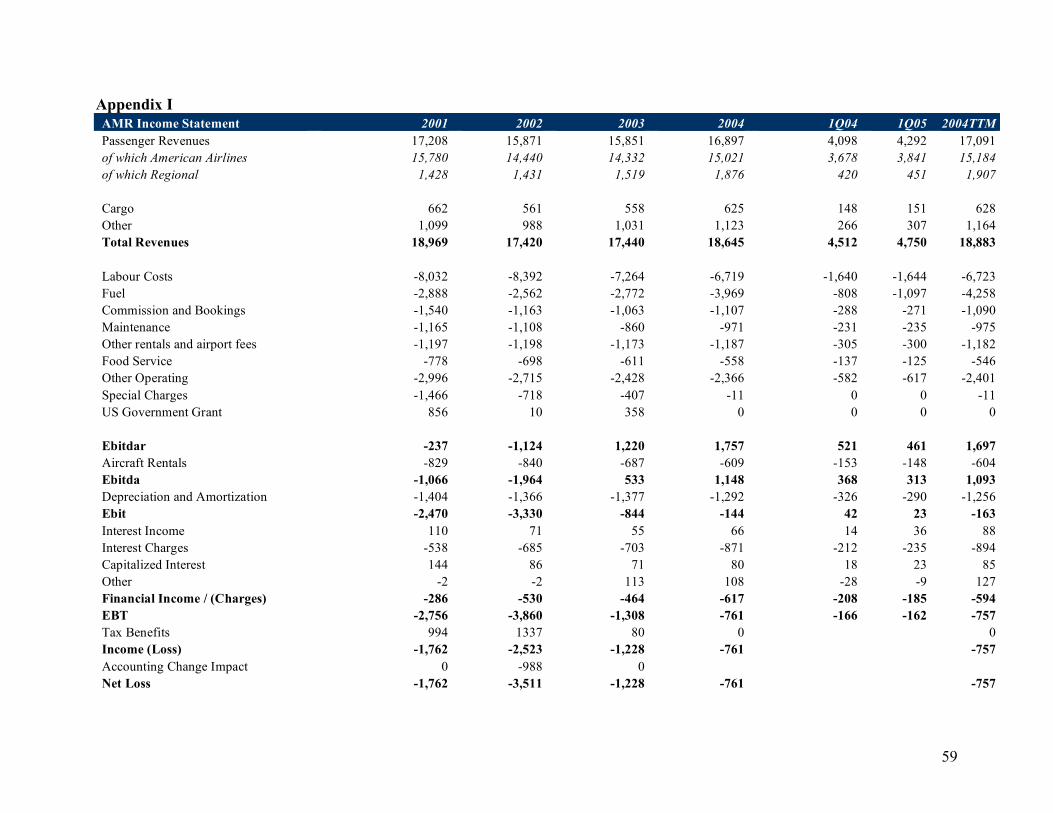

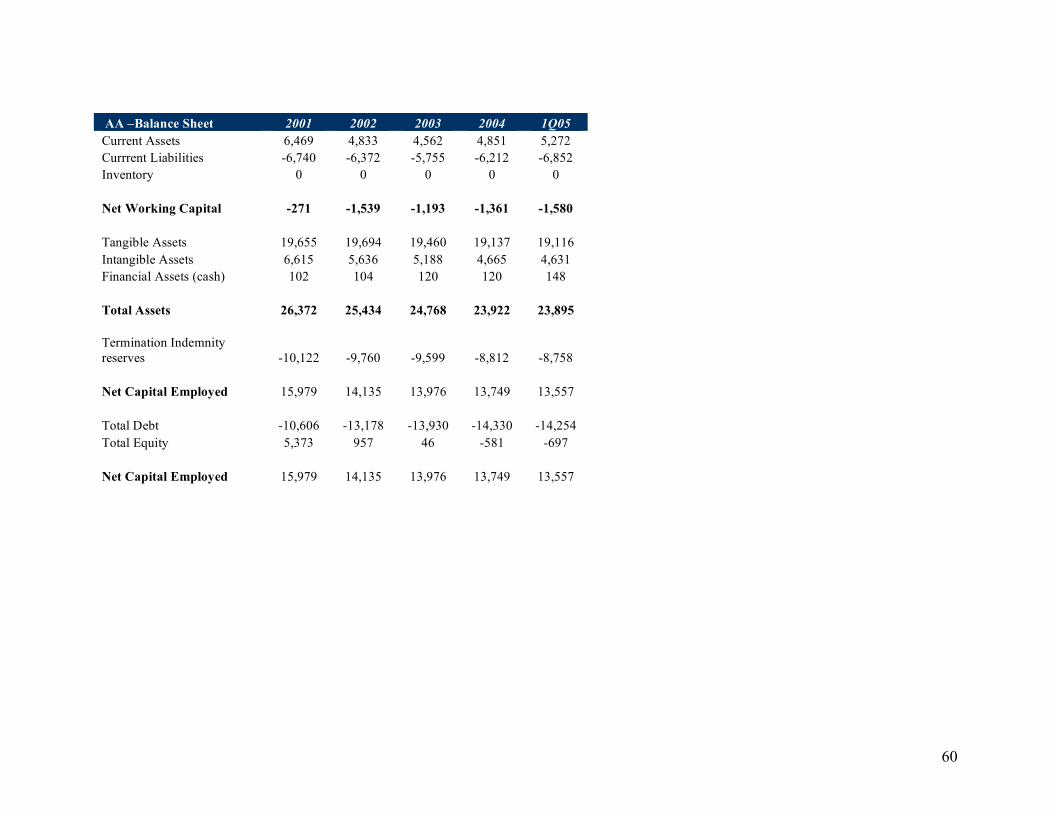

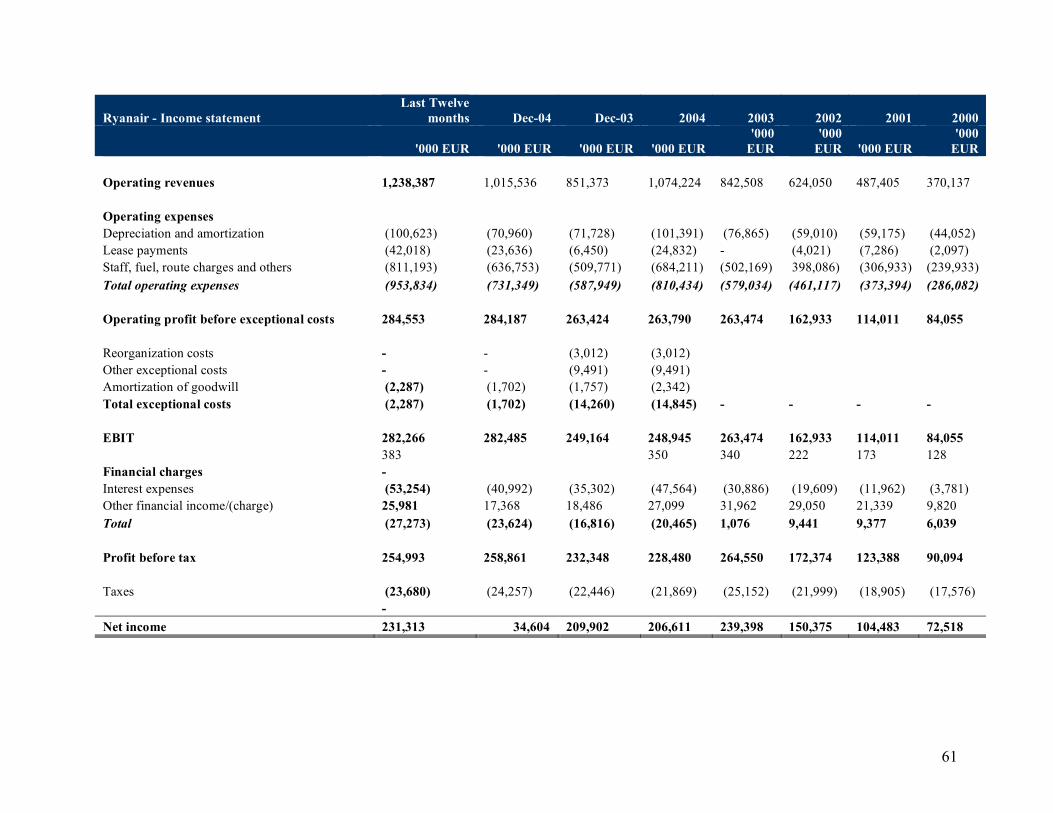

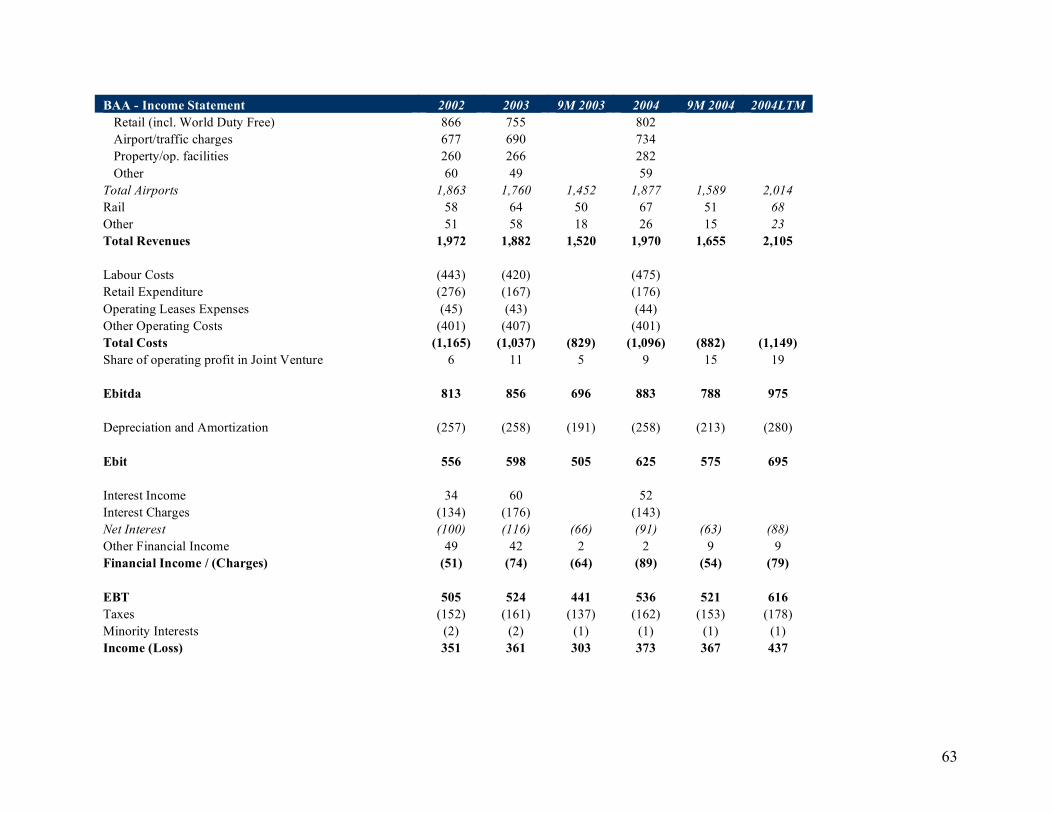

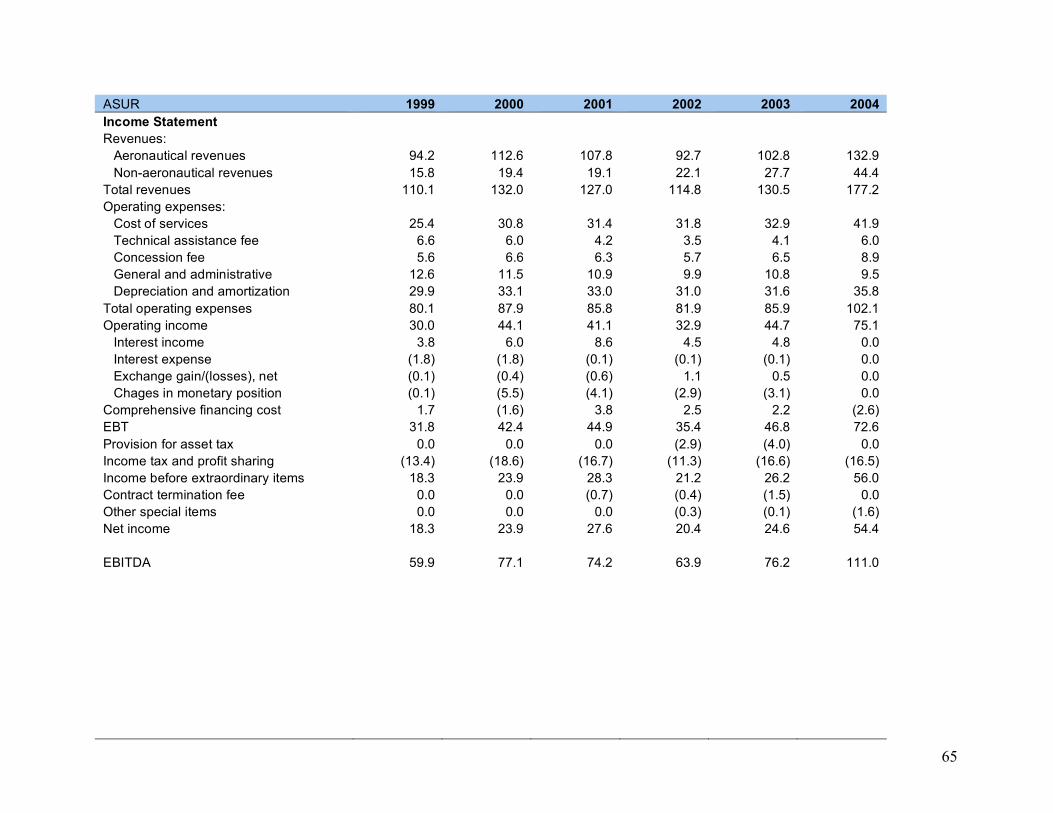

Summary financial data for each company is presented in Appendix I.

III. Corporate Governance Analysis

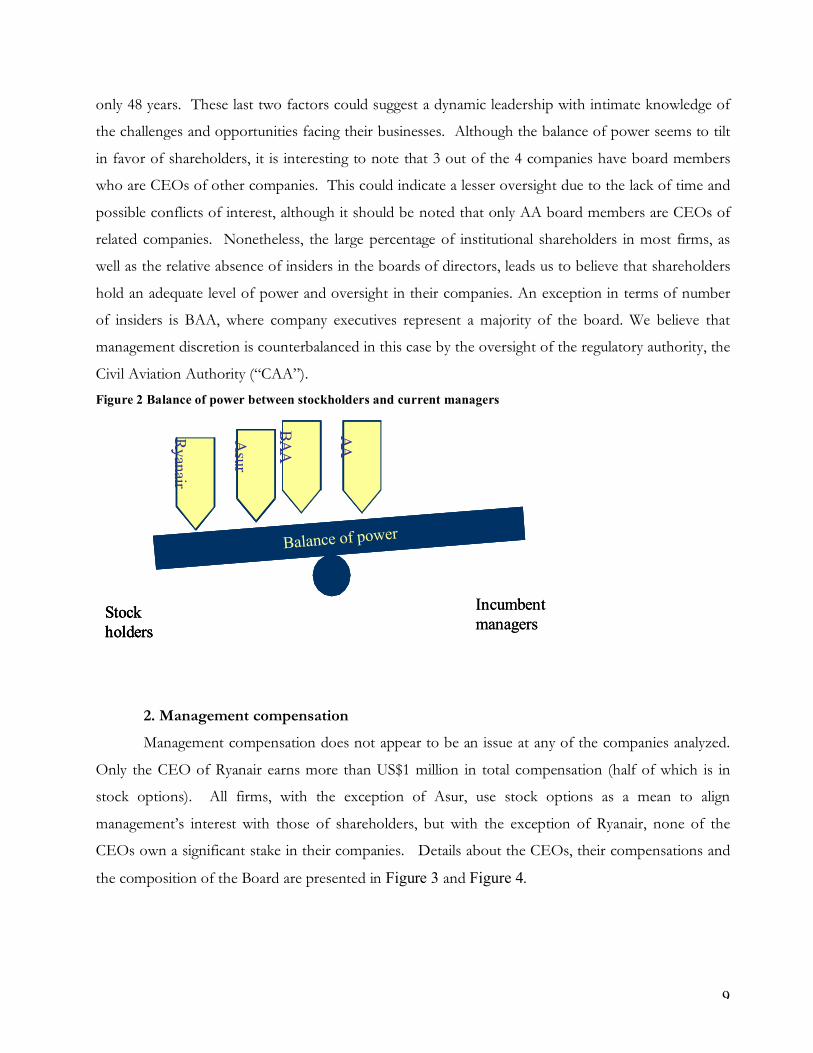

1. Balance of power between management and shareholders

We believe that the interests of shareholders are relatively well protected by the corporate

governance policies of the four companies analyzed, with the possible exception of American Airlines.

As an example at AA, directors are nominated for life and more than half are CEOs of other

companies, two of them in related businesses. A shareholder is challenging the lifetime rule at the

next general shareholders’ meeting in May. Recently, some board members and the CEO have raised

their own salaries.

Insiders are generally not overrepresented in the companies’ boards, while the CEOs tend to

have a long history with their companies, once again with the notable exception of American Airlines.

One interesting common feature is that all of the CEOs are relatively young with an average age of

9

only 48 years. These last two factors could suggest a dynamic leadership with intimate knowledge of

the challenges and opportunities facing their businesses. Although the balance of power seems to tilt

in favor of shareholders, it is interesting to note that 3 out of the 4 companies have board members

who are CEOs of other companies. This could indicate a lesser oversight due to the lack of time and

possible conflicts of interest, although it should be noted that only AA board members are CEOs of

related companies. Nonetheless, the large percentage of institutional shareholders in most firms, as

well as the relative absence of insiders in the boards of directors, leads us to believe that shareholders

hold an adequate level of power and oversight in their companies. An exception in terms of number

of insiders is BAA, where company executives represent a majority of the board. We believe that

management discretion is counterbalanced in this case by the oversight of the regulatory authority, the

Civil Aviation Authority (“CAA”).

Figure 2 Balance of power between stockholders and current managers

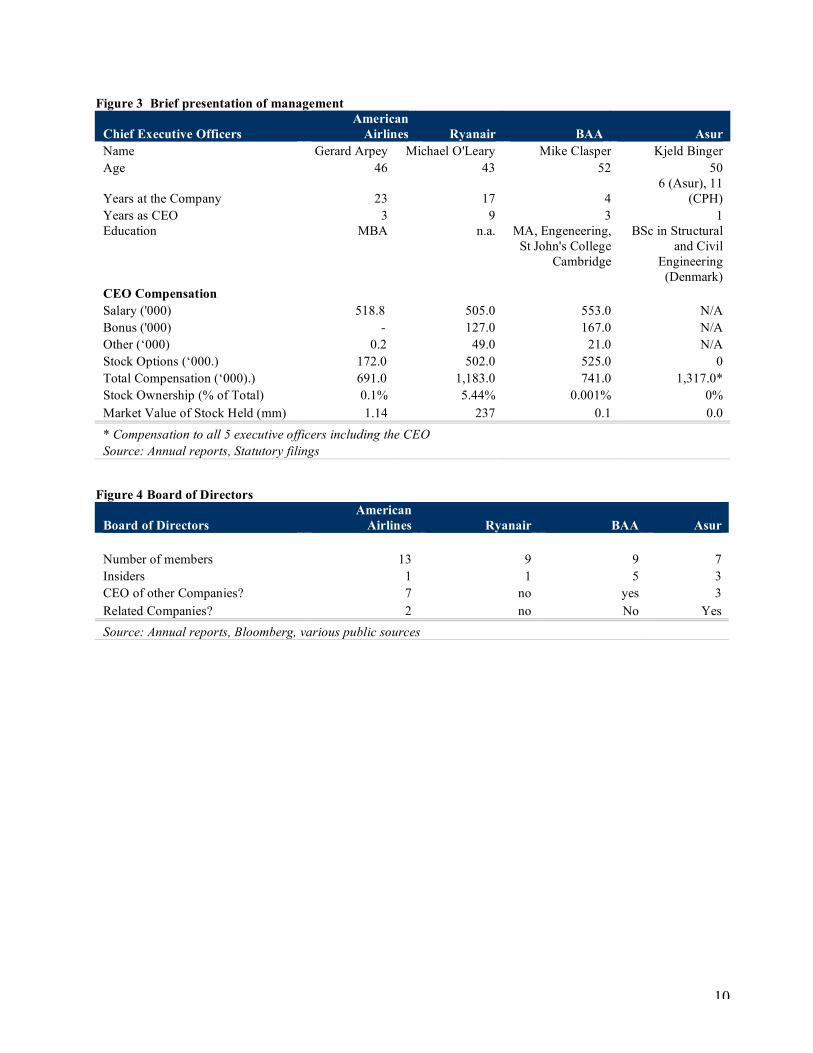

2. Management compensation

Management compensation does not appear to be an issue at any of the companies analyzed.

Only the CEO of Ryanair earns more than US$1 million in total compensation (half of which is in

stock options). All firms, with the exception of Asur, use stock options as a mean to align

management’s interest with those of shareholders, but with the exception of Ryanair, none of the

CEOs own a significant stake in their companies. Details about the CEOs, their compensations and

the composition of the Board are presented in Figure 3 and Figure 4.

Incumbent

managers

Balance of power

Stock

holdersR

yan

air

Asu

r

BA

A

AA

Incumbent

managers

Balance of power

Stock

holdersR

yan

air

Asu

r

BA

A

AA

Balance of power

Stock

holdersR

yan

air

Asu

r

BA

A

AA

10

Figure 3 Brief presentation of management

Chief Executive Officers American

Airlines Ryanair BAA Asur Name Gerard Arpey Michael O'Leary Mike Clasper Kjeld Binger Age 46 43 52 50

Years at the Company 23 17 4 6 (Asur), 11

(CPH) Years as CEO 3 9 3 1 Education MBA n.a. MA, Engeneering,

St John's College Cambridge

BSc in Structural and Civil

Engineering (Denmark)

CEO Compensation Salary ('000) 518.8 505.0 553.0 N/A Bonus ('000) - 127.0 167.0 N/A Other (‘000) 0.2 49.0 21.0 N/A Stock Options (‘000.) 172.0 502.0 525.0 0 Total Compensation (‘000).) 691.0 1,183.0 741.0 1,317.0* Stock Ownership (% of Total) 0.1% 5.44% 0.001% 0% Market Value of Stock Held (mm) 1.14 237 0.1 0.0 * Compensation to all 5 executive officers including the CEO Source: Annual reports, Statutory filings

Figure 4 Board of Directors

Board of Directors American

Airlines Ryanair BAA Asur Number of members 13 9 9 7 Insiders 1 1 5 3 CEO of other Companies? 7 no yes 3 Related Companies? 2 no No Yes Source: Annual reports, Bloomberg, various public sources

11

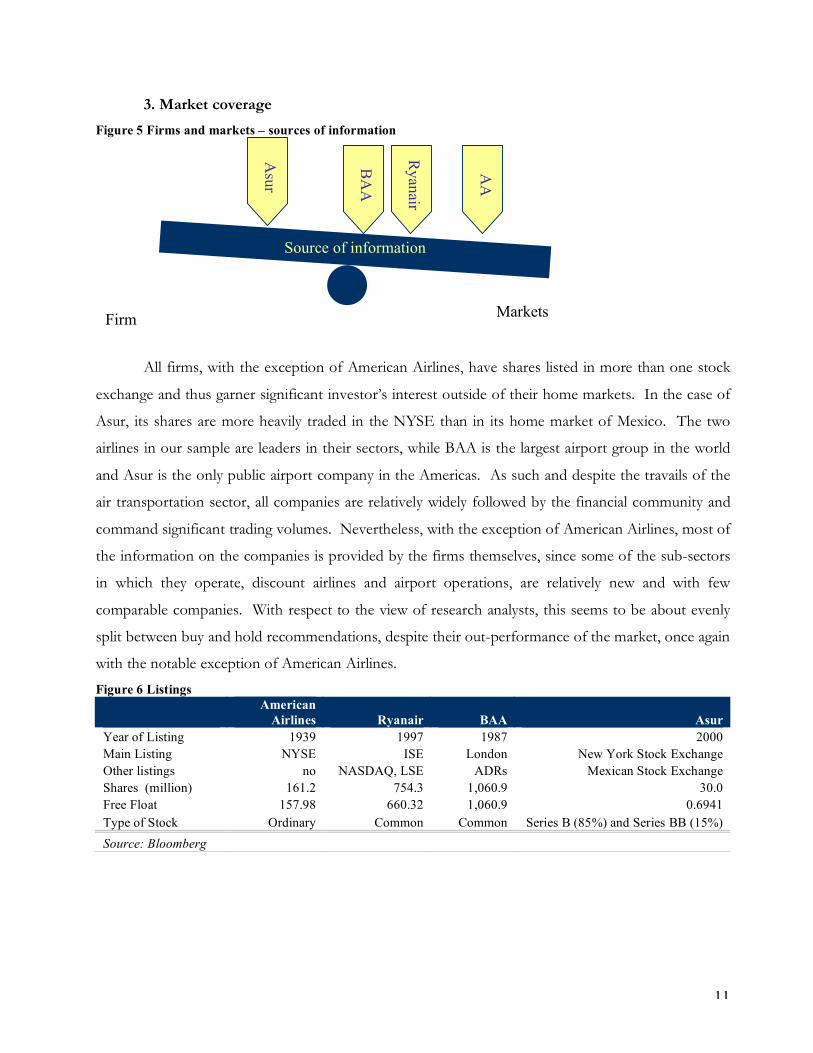

3. Market coverage

Figure 5 Firms and markets – sources of information

All firms, with the exception of American Airlines, have shares listed in more than one stock

exchange and thus garner significant investor’s interest outside of their home markets. In the case of

Asur, its shares are more heavily traded in the NYSE than in its home market of Mexico. The two

airlines in our sample are leaders in their sectors, while BAA is the largest airport group in the world

and Asur is the only public airport company in the Americas. As such and despite the travails of the

air transportation sector, all companies are relatively widely followed by the financial community and

command significant trading volumes. Nevertheless, with the exception of American Airlines, most of

the information on the companies is provided by the firms themselves, since some of the sub-sectors

in which they operate, discount airlines and airport operations, are relatively new and with few

comparable companies. With respect to the view of research analysts, this seems to be about evenly

split between buy and hold recommendations, despite their out-performance of the market, once again

with the notable exception of American Airlines.

Figure 6 Listings

American

Airlines Ryanair BAA Asur Year of Listing 1939 1997 1987 2000 Main Listing NYSE ISE London New York Stock Exchange Other listings no NASDAQ, LSE ADRs Mexican Stock Exchange Shares (million) 161.2 754.3 1,060.9 30.0 Free Float 157.98 660.32 1,060.9 0.6941 Type of Stock Ordinary Common Common Series B (85%) and Series BB (15%) Source: Bloomberg

Markets

Source of information

Firm

Ryanair

Asur

BA

A

AA

12

Figure 7 Market coverage Analyst coverage American Airlines Ryanair BAA Asur Number of Analysts 10 19 12 5+ Analysts Recommendations (%) Buy 50% 63.16% 50% 60.0% Hold 40% 26.32% 50% 40.0% Sell 10% 10.53% 0% 0.0% Daily Average Trading Volume (mm) 2002 2.14 1.54 4.98 1.01 2003 8.06 2.64 7.01 0.83 2004 5.13 2.26 6.43 1.37 2005YTD 4.06 3.41 6.93 3.27 Source: Annual reports, Statutory filings, Bloomberg, Zacks, Yahoo Finance and various public sources

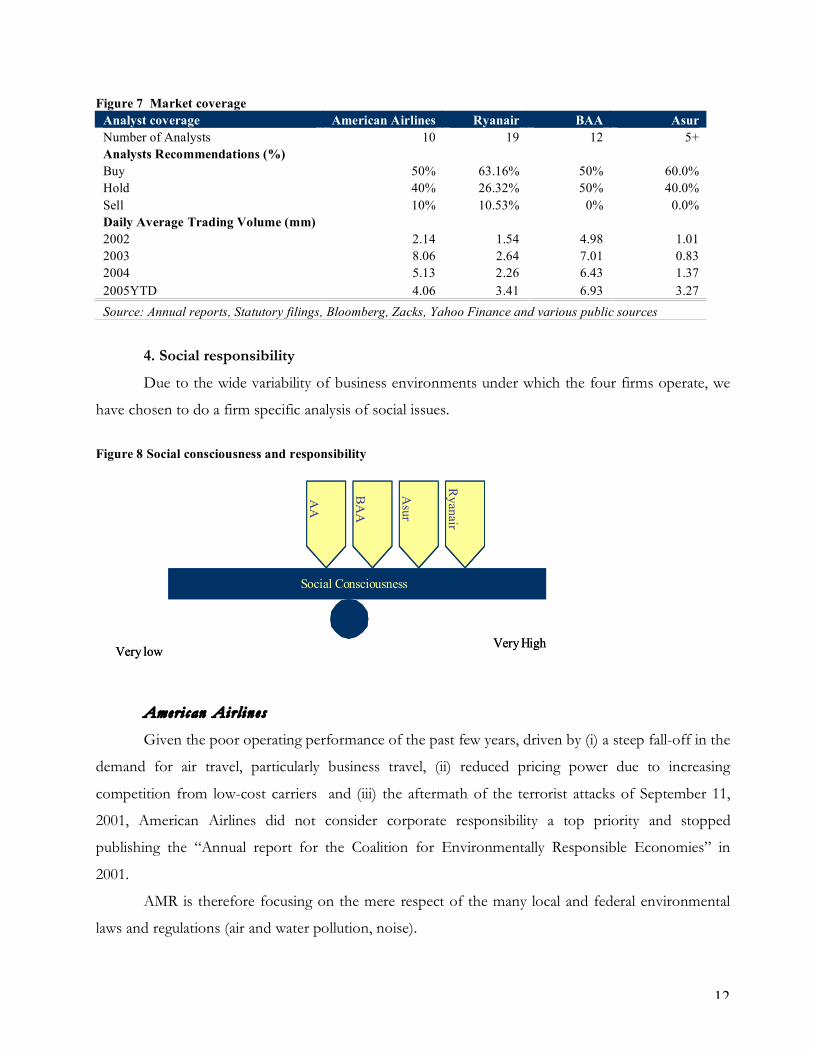

4. Social responsibility

Due to the wide variability of business environments under which the four firms operate, we

have chosen to do a firm specific analysis of social issues.

Figure 8 Social consciousness and responsibility

Ameri can Airl ines

Given the poor operating performance of the past few years, driven by (i) a steep fall-off in the

demand for air travel, particularly business travel, (ii) reduced pricing power due to increasing

competition from low-cost carriers and (iii) the aftermath of the terrorist attacks of September 11,

2001, American Airlines did not consider corporate responsibility a top priority and stopped

publishing the “Annual report for the Coalition for Environmentally Responsible Economies” in

2001.

AMR is therefore focusing on the mere respect of the many local and federal environmental

laws and regulations (air and water pollution, noise).

Social Consciousness

Very lowVery High

Ryan

air

Asu

r

BA

A

AA

Social Consciousness

Very lowVery High

Ryan

air

Asu

r

BA

A

AA

13

The company has been named as a potentially responsible party for land or water

contaminations in California, Oklahoma and Florida. AMR has already accrued $ 6 millionn for

settlement expected, but the actual amount that AMR will have to pay is still unknown.

Ryanair

The perceived image of Ryanair as a low cost air carrier and provider of value of its passengers

is extremely important for the company. This image is aligned with the operational model of the

company, using modern fleet of aircrafts with lower fuel consumption reducing the emissions and

environmental damage. In addition, its policy to operate from remote airports resulted in numerous

benefits for the communities in these regions, increasing economic activity. However, major focus of

the company is to be perceived as a value provider for its passengers.

BAA

Given its handling of all the major airports in the UK BAA as well undergoes substantial

public scrutiny. Recently the debate over the environmental impact of the new Terminal at Heathrow

and the new runaway at Stansted has further heightened attention. BAA has always been receptive to

issues coming from airport communities and currently pledges 0.15% of its pre-tax profits (equiv. to

slightly under £1 mm in 2004). to 21st Century Communities Trust, a charity it created.

Asur

As the monopoly provider of the main airport facilities in nine southeastern Mexican cities,

Asur faces significant public oversight and societal constraints. The Mexican Airport Law of 1995

established the general framework regulating the construction, operation, maintenance and

development of Mexican airport facilities in the benefit of the public good. Moreover, Asur is also

subject to Mexican federal and state laws and regulations relating to the protection of the

environment. The level of environmental regulation in Mexico has increased in recent years, and the

enforcement of the law is becoming more stringent.

Asur generally has a positive image with the Mexican public and a strong reputation as a good

corporate citizen, since it has greatly improved the quality and scope of the facilities and services

offered by its nine airports. However, in the near future the company could face criticism by local

14

government officials that want to build new airport facilities in their regions, such as in Veracruz and

Quintana Roo (Cancun and Cozumel airports).

IV. Stockholder Analysis

All firms in our sample, with the exception of BAA which has a more widespread investor

base made up of small private investors, have a strong institutional shareholder base which commands

over 2/3 of the total outstanding shares of their companies. This contrasts sharply with an industry

average of only 33%, and gives credibility to our argument that corporate governance is relatively

strong and minority shareholder rights are well protected. Moreover, the top 5 institutional

shareholders in all companies are among the largest and most diversified asset management companies

in the world. On the other hand and with the exception of Asur, insider holdings are relatively small

and in line with the industry average of 6%. All these facts suggest that the marginal investor for all

firms is a well diversified global institutional investor and we can thus proceed to carry out CAPM

based risk and return analyses for the companies. In the case of BAA, even though the majority of the

shares are held by private individuals, these tend to be buy-and-hold investors with the majority of the

trading is done by institutional funds, which are therefore the marginal investor.

Most firms in our sample have only one type of share, common or ordinary. We take a look at

the exceptions below:

Ameri can Airl ines AMR Corporation has only common stock outstanding, but the board of directors has already

authorized the CEO to issue 20million shares of preferred stock, probably to ease the deep financial

stress of the company. Book value of equity has been negative for the last 3 quarters and debt ratio is

around 90%.

Asur Asur has two types of shares: B shares and BB shares. Series B shares currently represent 85%

of the company’s capital, while series BB shares represent the remaining 15%. Each series B share

and series BB share entitles the holder to one vote at the general shareholders’ meeting. However,

holders of series BB shares are entitled to elect only two members of the board of directors, while

holders of series B shares are entitled to name the remaining directors. Under the company’s bylaws,

each shareholder or group of shareholders owning at least 10% of Asur’s capital stock in the form of

15

series B shares is entitled to elect one member to the board of directors for each 10% interest that it

owns. Directors and senior management do not own any shares of Asur. Pursuant to the company’s

bylaws, the holders of series BB shares are entitled to appoint and remove Asur’s CEO and one half

of the executive officers reporting directly to the CEO. Currently, four executive officers report

directly to the CEO, one of whom was appointed by ITA as holder of the BB shares.

The shareholders distribution as well as details about institutional and insiders holdings in the

companies are presented in Figure 9, Figure 10 and Figure 11.

Figure 9 Distribution of stockholders

Institutional 12%

Institutional 69%

Insider 12%

Other 88%

Institutional 87%

Institutional 98%

Insider 2%

Insider 0.03%

Insider 31%

Other 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AA Ryan BAA Asur

Figure 10 Institutional Holdings Institutional holdings American Airlines Ryanair BAA Asur Number of shares held (million)

158.0 n/a 124.2 20.8

% of Shares Outstanding

98.0% 70% + 11.6% 69.41%

Top 5 Holders Fidelity Management Fidelity Investment Legal & General First State Investment Management UK

Primecap Management Capital Group Company Scottish Widows Columbia Wagner Asset

Management

Wellington

Management Guilder Gagnon

Holding Newton Inv.

Mgmt Oakmark International

Small Cap Fund

Allianz Global Wellington

Management Threadneedle Inv. Schroder Investment

Management Group

Hall Phoenix Janus Causeway Capital American Express

Financial Corp Number of shares held by Top 5 (million)

69.5 392.2 93.1 6.5

% of Shares Outstanding 43.1% 52.0% 8.7% 21.57%

Source: Bloomberg, Statutory filings

16

Figure 11 Insiders holdings

Insiders ownership American Airlines Ryanair BAA Asur

Number of shares held (million) 3.22 88.3 0.3 9.2 % of Shares Outstanding 2% 12.47% 0.03% 30.59% Major Holders Daniel Garton

(CEO) Michael O'Leary Sir Mike Hodgkinson

(Exec. Director) ITA (15.01%)

Jeffrey Campbell Anthony Ryan Joel Hoerner

(Non-exec. Dir) Nafin (11.10%)

Charles Marlett (Executive VP)

Ryan Family members

Tony Ward (Exec. Director)

Copenhagen Airports (2.50%)

Gary Kennedy

JanisKong (Exec. Dir.) Fernando Chico Pardo

(1.98%) Source: Bloomberg, Statutory filings, various public sources

V. Risk Profile

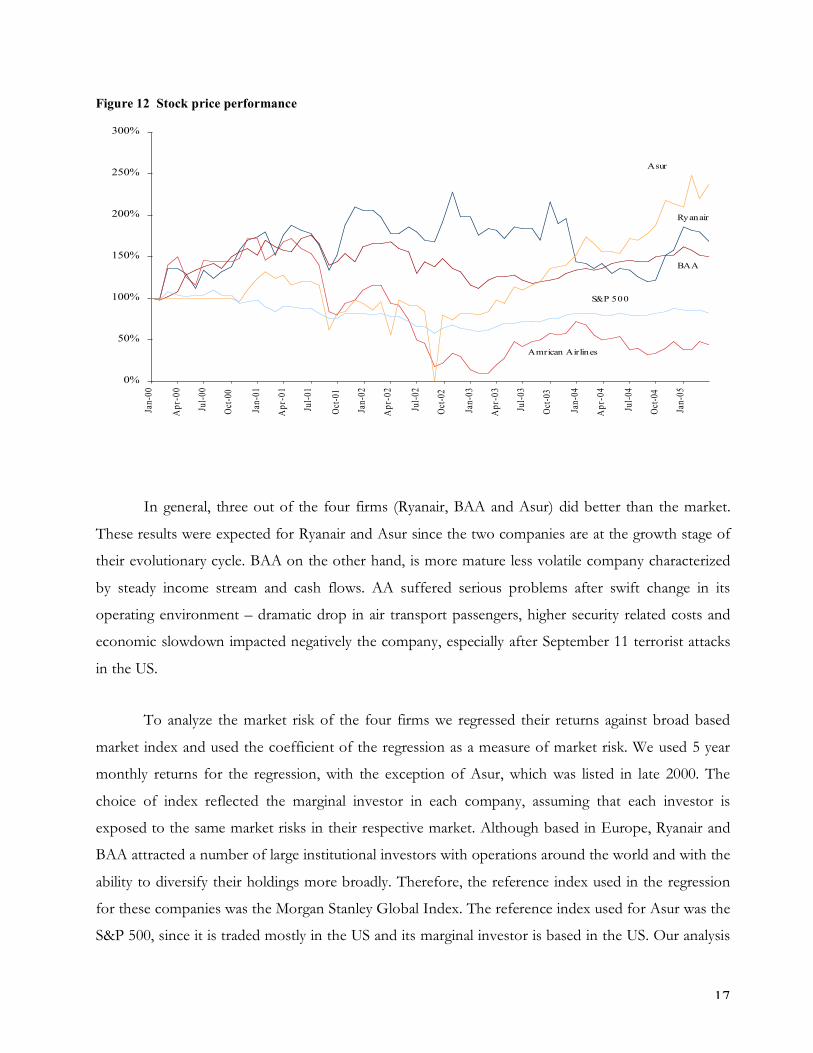

1. Market risk and return In analyzing the risk characteristics of the four companies we first looked at their returns over

a five year period compared them to the returns of a broad based market index such as the S&P 500.

Figure 12 below presents the rebased share prices of all four companies and the level of the S&P 500

(Jan 2000 = 100).

17

Figure 12 Stock price performance

0%

50%

100%

150%

200%

250%

300%

Jan

-00

Ap

r-0

0

Jul-

00

Oct

-00

Jan

-01

Ap

r-0

1

Jul-

01

Oct

-01

Jan

-02

Ap

r-0

2

Jul-

02

Oct

-02

Jan

-03

Ap

r-0

3

Jul-

03

Oct

-03

Jan

-04

Ap

r-0

4

Jul-

04

Oct

-04

Jan

-05

Amrican Airlines

S&P 500

Asur

BAA

Ryanair

In general, three out of the four firms (Ryanair, BAA and Asur) did better than the market.

These results were expected for Ryanair and Asur since the two companies are at the growth stage of

their evolutionary cycle. BAA on the other hand, is more mature less volatile company characterized

by steady income stream and cash flows. AA suffered serious problems after swift change in its

operating environment – dramatic drop in air transport passengers, higher security related costs and

economic slowdown impacted negatively the company, especially after September 11 terrorist attacks

in the US.

To analyze the market risk of the four firms we regressed their returns against broad based

market index and used the coefficient of the regression as a measure of market risk. We used 5 year

monthly returns for the regression, with the exception of Asur, which was listed in late 2000. The

choice of index reflected the marginal investor in each company, assuming that each investor is

exposed to the same market risks in their respective market. Although based in Europe, Ryanair and

BAA attracted a number of large institutional investors with operations around the world and with the

ability to diversify their holdings more broadly. Therefore, the reference index used in the regression

for these companies was the Morgan Stanley Global Index. The reference index used for Asur was the

S&P 500, since it is traded mostly in the US and its marginal investor is based in the US. Our analysis

18

focuses on the regression coefficient (beta), the regression constant (used for computation of Jensen’s

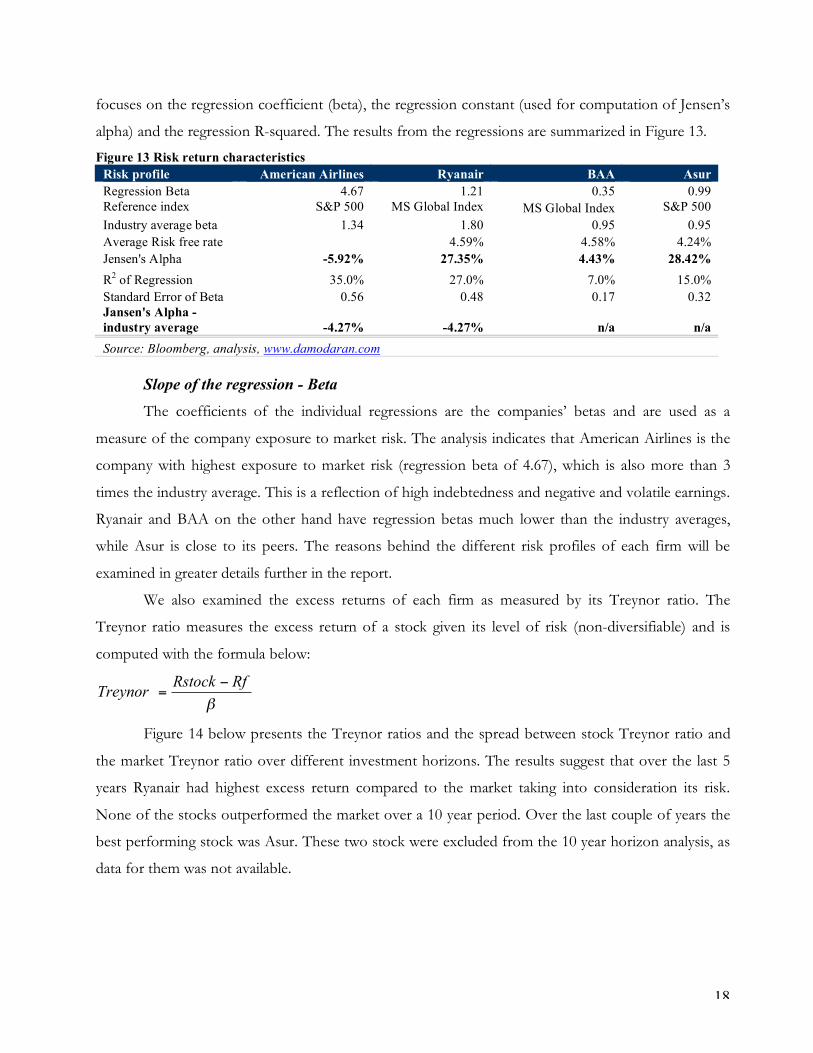

alpha) and the regression R-squared. The results from the regressions are summarized in Figure 13.

Figure 13 Risk return characteristics Risk profile American Airlines Ryanair BAA Asur Regression Beta 4.67 1.21 0.35 0.99 Reference index S&P 500 MS Global Index MS Global Index S&P 500 Industry average beta 1.34 1.80 0.95 0.95 Average Risk free rate 4.59% 4.58% 4.24% Jensen's Alpha -5.92% 27.35% 4.43% 28.42% R2 of Regression 35.0% 27.0% 7.0% 15.0% Standard Error of Beta 0.56 0.48 0.17 0.32 Jansen's Alpha - industry average -4.27% -4.27% n/a n/a Source: Bloomberg, analysis, www.damodaran.com

Slope of the regression - Beta The coefficients of the individual regressions are the companies’ betas and are used as a

measure of the company exposure to market risk. The analysis indicates that American Airlines is the

company with highest exposure to market risk (regression beta of 4.67), which is also more than 3

times the industry average. This is a reflection of high indebtedness and negative and volatile earnings.

Ryanair and BAA on the other hand have regression betas much lower than the industry averages,

while Asur is close to its peers. The reasons behind the different risk profiles of each firm will be

examined in greater details further in the report.

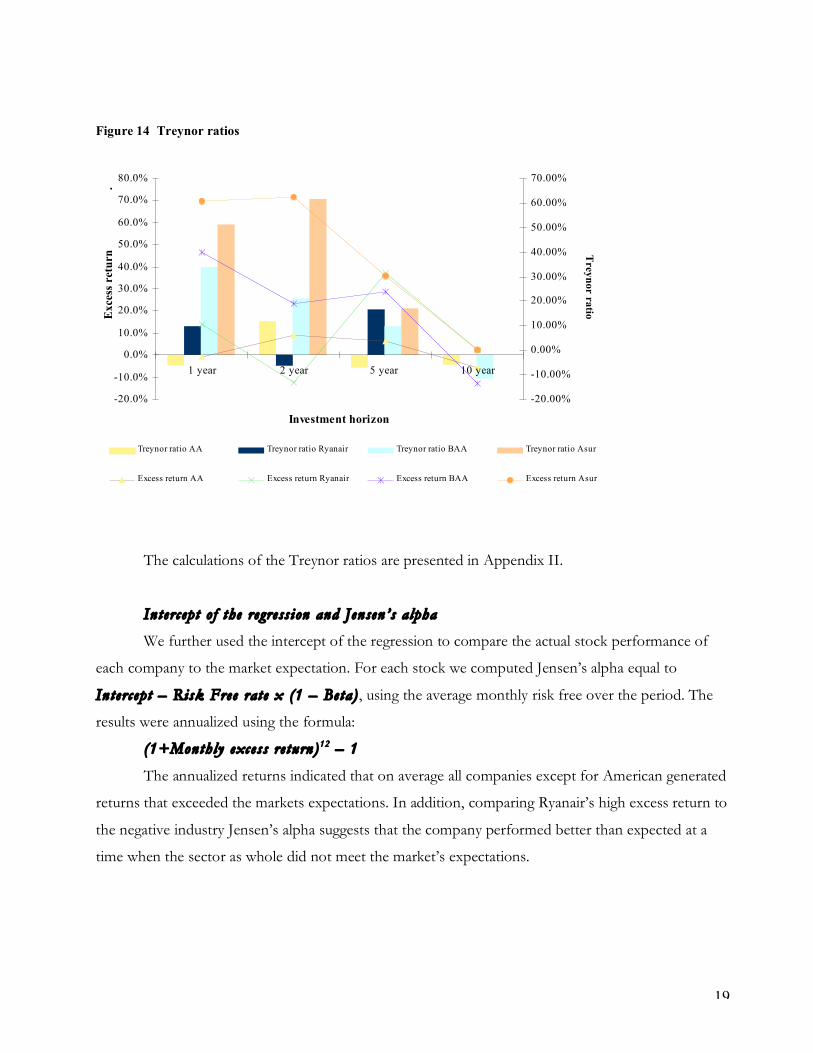

We also examined the excess returns of each firm as measured by its Treynor ratio. The

Treynor ratio measures the excess return of a stock given its level of risk (non-diversifiable) and is

computed with the formula below:

!

RfRstockTreynor

"=

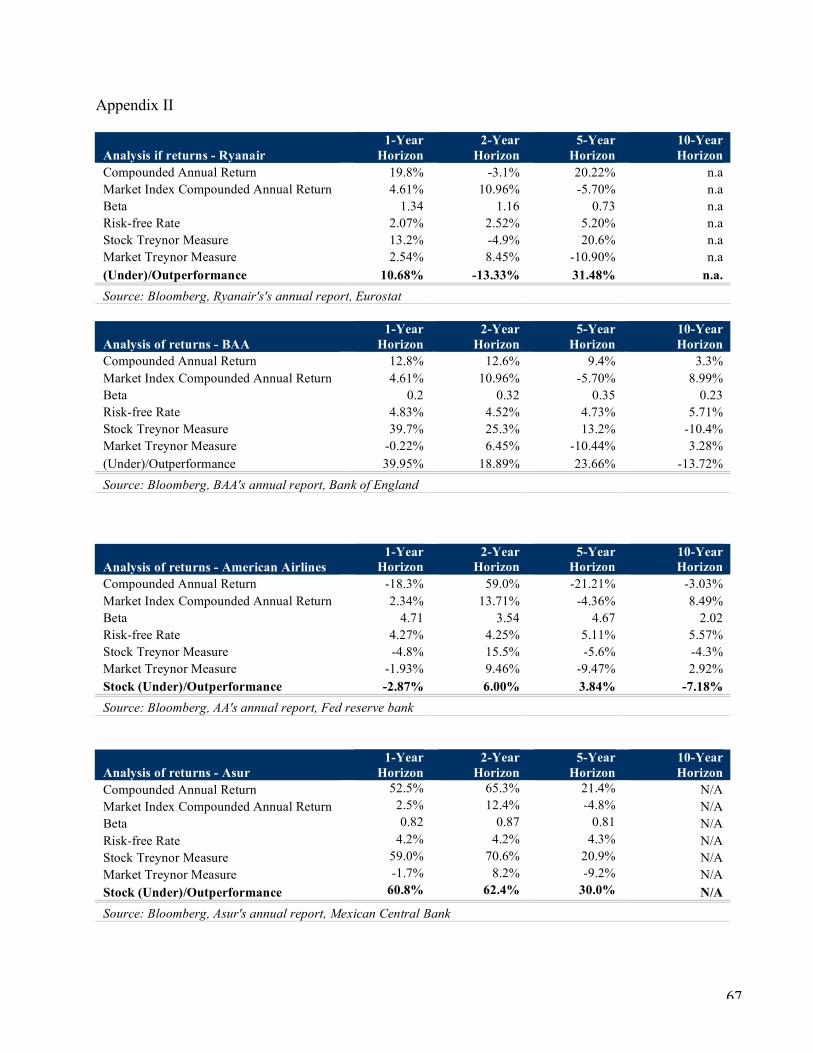

Figure 14 below presents the Treynor ratios and the spread between stock Treynor ratio and

the market Treynor ratio over different investment horizons. The results suggest that over the last 5

years Ryanair had highest excess return compared to the market taking into consideration its risk.

None of the stocks outperformed the market over a 10 year period. Over the last couple of years the

best performing stock was Asur. These two stock were excluded from the 10 year horizon analysis, as

data for them was not available.

19

Figure 14 Treynor ratios

The calculations of the Treynor ratios are presented in Appendix II.

In t erc ept o f the regress ion and Jensen ’s alpha

We further used the intercept of the regression to compare the actual stock performance of

each company to the market expectation. For each stock we computed Jensen’s alpha equal to

Interc ept – Risk Free rat e x (1 – Beta) , using the average monthly risk free over the period. The

results were annualized using the formula:

(1+Monthly excess re turn)12 – 1

The annualized returns indicated that on average all companies except for American generated

returns that exceeded the markets expectations. In addition, comparing Ryanair’s high excess return to

the negative industry Jensen’s alpha suggests that the company performed better than expected at a

time when the sector as whole did not meet the market’s expectations.

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

1 year 2 year 5 year 10 year

Investment horizon

Exce

ss r

etu

rn

.

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

T

reyn

or ra

tio

Treynor ratio AA Treynor ratio Ryanair Treynor ratio BAA Treynor ratio Asur

Excess return AA Excess return Ryanair Excess return BAA Excess return Asur

20

R-squared

R-squared of the regression provides information as to what proportion of the variability in

returns could be explained by the regression, or in other words what part of the variability in the

returns (total risk) can be attributed to beta (market risk). The market non-diversifiable risk represents

35%, 27%, 7% and 15% for AA, Ryanair, BAA and Asur respectively. The remainder is company

specific, non-diversifiable risk. While the relatively low R-squared for Ryanair and Asur could be

explained by the fact that they were small, fast growing companies during the observed period and

were facing numerous company specific challenges in establishing their business models, we were

surprised to estimate that BAA was characterized by a large proportion of (93%) of company specific,

diversifiable risk. One possible explanation could be the fact that airport operators’ revenues are

generally much more stable stream and have a fixed nature – they are based on long term contracts

under which airport slots are sold to airline companies. Even in the event of drop in passenger

numbers the charge payable to airports is generally steady.

Standard errors

The standard errors of the regression betas appear to be significant, suggesting a wide interval

for the possible values of the beta. This is one of the reasons why we considered an alternative

approach to measuring the companies exposure to market risk, which is described bellow.

2. Bottom up betas As an alternative approach to regressions betas we considered using bottom-up betas for our

analysis. This is mainly due to the following factors:

As growing companies Ryanair and Asur are likely to change over time, hence alter

their risk profile. In addition, their capital structure is likely to change;

BAA is mature, steady company which risk profile is likely to remain similar.

However, the standard error of the regression beta indicates that it might nor be a

reliable measure of risk;

American Airline as a company facing financial difficulties is likely to change in the

long term if it is to return to profitability. Making a going concern assumption

about the business requires change in the company and hence, its risk profile.

Therefore we believed that historical indicators might not be a reliable measure for

the future.

21

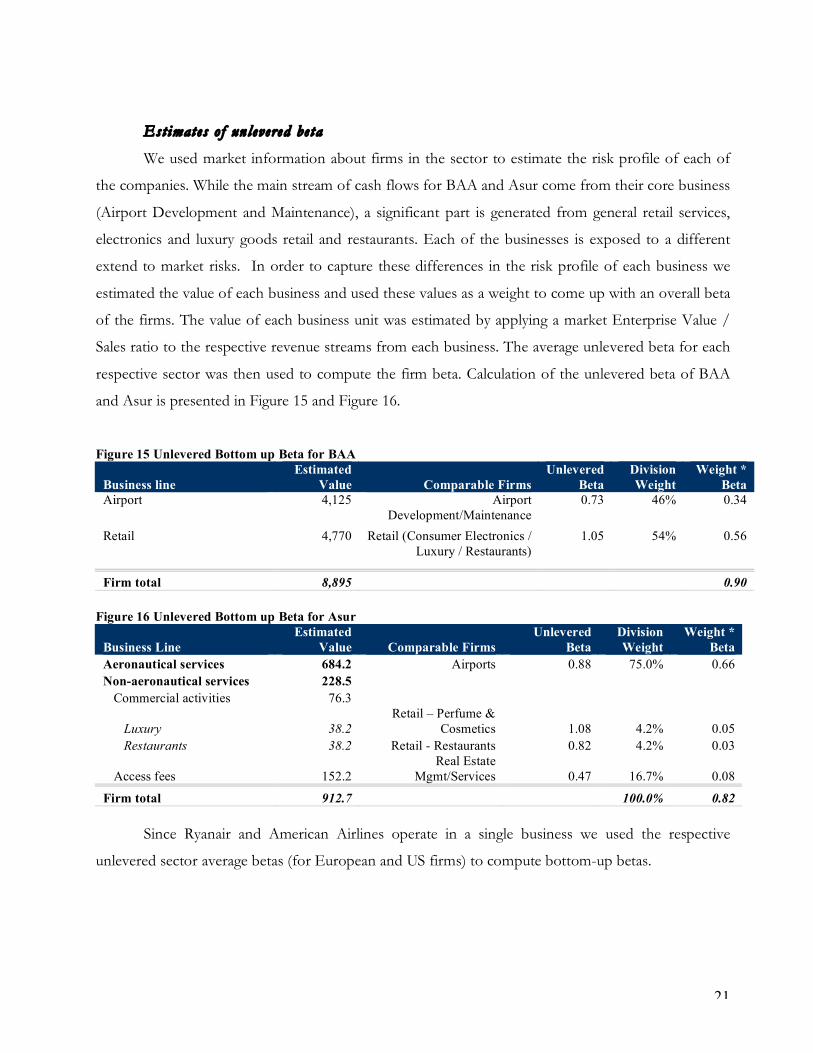

Est imates o f un levered be ta

We used market information about firms in the sector to estimate the risk profile of each of

the companies. While the main stream of cash flows for BAA and Asur come from their core business

(Airport Development and Maintenance), a significant part is generated from general retail services,

electronics and luxury goods retail and restaurants. Each of the businesses is exposed to a different

extend to market risks. In order to capture these differences in the risk profile of each business we

estimated the value of each business and used these values as a weight to come up with an overall beta

of the firms. The value of each business unit was estimated by applying a market Enterprise Value /

Sales ratio to the respective revenue streams from each business. The average unlevered beta for each

respective sector was then used to compute the firm beta. Calculation of the unlevered beta of BAA

and Asur is presented in Figure 15 and Figure 16.

Figure 15 Unlevered Bottom up Beta for BAA

Business line Estimated

Value Comparable Firms Unlevered

Beta Division Weight

Weight * Beta

Airport 4,125 Airport Development/Maintenance

0.73 46% 0.34

Retail 4,770 Retail (Consumer Electronics / Luxury / Restaurants)

1.05 54% 0.56

Firm total 8,895 0.90

Figure 16 Unlevered Bottom up Beta for Asur

Business Line Estimated

Value Comparable Firms Unlevered

Beta Division Weight

Weight * Beta

Aeronautical services 684.2 Airports 0.88 75.0% 0.66 Non-aeronautical services 228.5

Commercial activities 76.3

Luxury 38.2 Retail – Perfume &

Cosmetics 1.08 4.2% 0.05 Restaurants 38.2 Retail - Restaurants 0.82 4.2% 0.03

Access fees 152.2 Real Estate

Mgmt/Services 0.47 16.7% 0.08

Firm total 912.7 100.0% 0.82 Since Ryanair and American Airlines operate in a single business we used the respective

unlevered sector average betas (for European and US firms) to compute bottom-up betas.

22

Bottom-up be tas After estimating unlevered beta for each firm we levered back the beta to estimate a firm beta

that reflects the additional risk associated with financial leverage. The sector betas were unlevered and

re-levered using the formulae bellow:

)/)(1(1( EDT

market

unlevered

!+=

"" ))/()1(1( EDxTx

unleveredlevered!+= ""

Where:

T applicable tax rate;

D/E market value of debt / market value of equity

The market value of equity has been computed as current share price multiplied by the number of

shares outstanding. Details of the computation of the market value of debt are presented in Figure 21.

Figure 17 Beta estimation - summary

Beta measure American

Airlines Ryanair BAA Asur

Top down Beta

4.67

1.21 0.35 0.99

Bottom up Beta (levered)

6.26

1.24 1.42 0.82

Industry avg. Beta (levered)

1.34

1.80 0.95 0.88 3. Cost of equity

The computed bottom up beta has been use to compute the cost of equity for the firms. This is the

return expected return by equity investors in the observed companies and an important input for the

calculation of the overall cost of capital. The cost of equity has been calculate using the Capital Asset

Pricing Model and includes the following inputs:

Risk free rate of return (Rf) – in estimating the cost of equity we have used long term government

bond denominated in the respective currency to come up with the risk free. The current 10 year

US, German and UK bond yields were used in the analysis for AA, Ryanair and BAA respectively.

The 10 year maturity of the bond used reflects the long term investment horizon of the likely

projects. Other periods should be considered for shorter term projects. The analysis for Asur is

done in US dollars and the relevant risk free rate used in the analysis is the 10 years US treasure

bond.

Market risk premium (Rp)– this measure reflects the excess return to which an investor is entitled

as a compensation for the higher risk he/she undertakes by investing in risky security rather than a

23

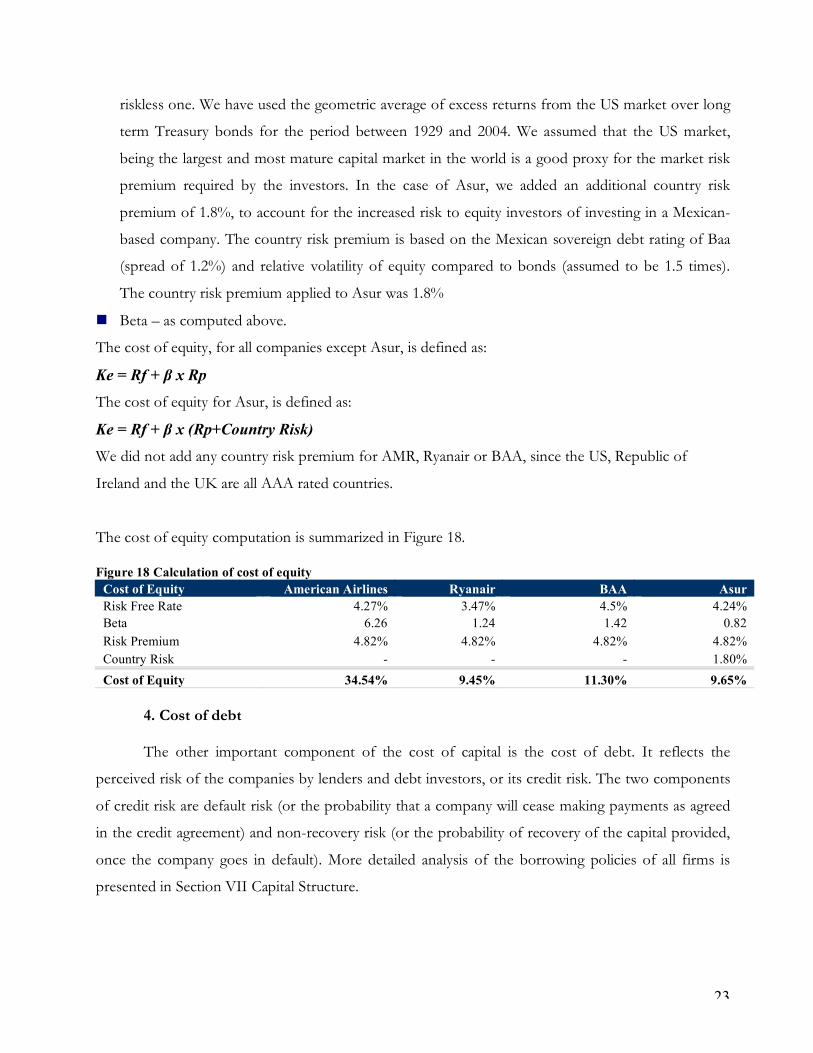

riskless one. We have used the geometric average of excess returns from the US market over long

term Treasury bonds for the period between 1929 and 2004. We assumed that the US market,

being the largest and most mature capital market in the world is a good proxy for the market risk

premium required by the investors. In the case of Asur, we added an additional country risk

premium of 1.8%, to account for the increased risk to equity investors of investing in a Mexican-

based company. The country risk premium is based on the Mexican sovereign debt rating of Baa

(spread of 1.2%) and relative volatility of equity compared to bonds (assumed to be 1.5 times).

The country risk premium applied to Asur was 1.8%

Beta – as computed above.

The cost of equity, for all companies except Asur, is defined as:

Ke = Rf + β x Rp The cost of equity for Asur, is defined as:

Ke = Rf + β x (Rp+Country Risk) We did not add any country risk premium for AMR, Ryanair or BAA, since the US, Republic of

Ireland and the UK are all AAA rated countries.

The cost of equity computation is summarized in Figure 18.

Figure 18 Calculation of cost of equity Cost of Equity American Airlines Ryanair BAA Asur Risk Free Rate 4.27% 3.47% 4.5% 4.24% Beta 6.26 1.24 1.42 0.82 Risk Premium 4.82% 4.82% 4.82% 4.82% Country Risk - - - 1.80% Cost of Equity 34.54% 9.45% 11.30% 9.65%

4. Cost of debt

The other important component of the cost of capital is the cost of debt. It reflects the

perceived risk of the companies by lenders and debt investors, or its credit risk. The two components

of credit risk are default risk (or the probability that a company will cease making payments as agreed

in the credit agreement) and non-recovery risk (or the probability of recovery of the capital provided,

once the company goes in default). More detailed analysis of the borrowing policies of all firms is

presented in Section VII Capital Structure.

24

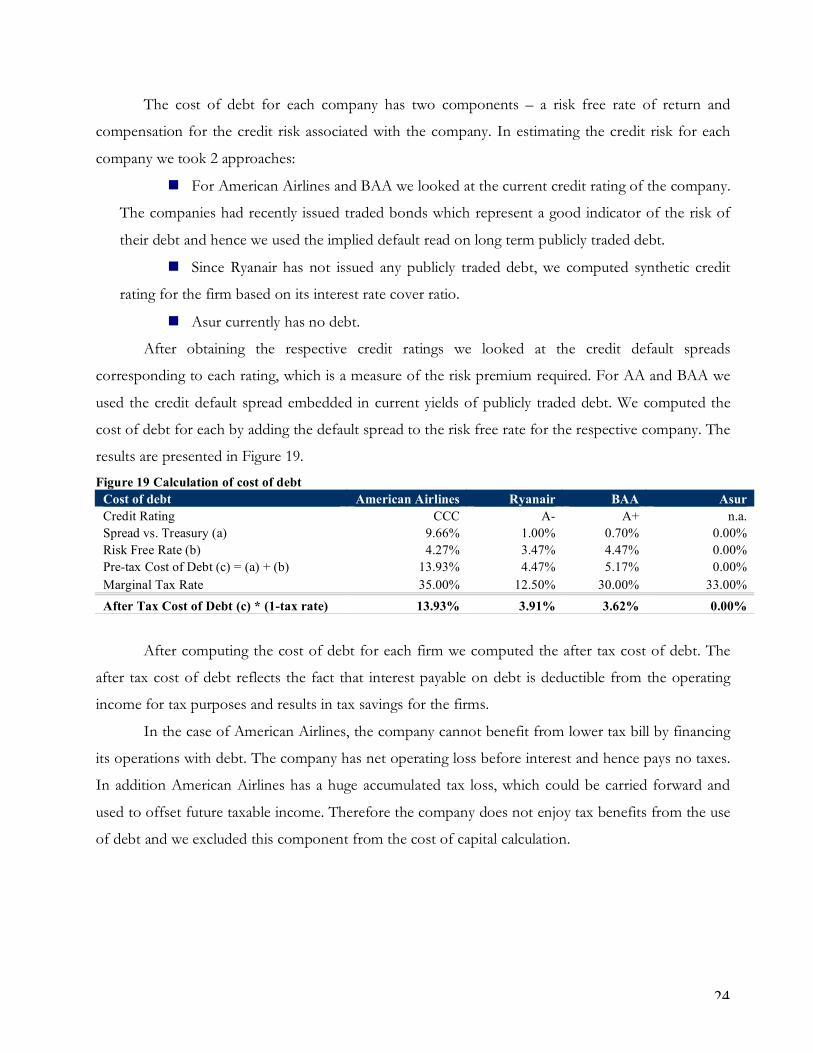

The cost of debt for each company has two components – a risk free rate of return and

compensation for the credit risk associated with the company. In estimating the credit risk for each

company we took 2 approaches:

For American Airlines and BAA we looked at the current credit rating of the company.

The companies had recently issued traded bonds which represent a good indicator of the risk of

their debt and hence we used the implied default read on long term publicly traded debt.

Since Ryanair has not issued any publicly traded debt, we computed synthetic credit

rating for the firm based on its interest rate cover ratio.

Asur currently has no debt.

After obtaining the respective credit ratings we looked at the credit default spreads

corresponding to each rating, which is a measure of the risk premium required. For AA and BAA we

used the credit default spread embedded in current yields of publicly traded debt. We computed the

cost of debt for each by adding the default spread to the risk free rate for the respective company. The

results are presented in Figure 19.

Figure 19 Calculation of cost of debt Cost of debt American Airlines Ryanair BAA Asur Credit Rating CCC A- A+ n.a. Spread vs. Treasury (a) 9.66% 1.00% 0.70% 0.00% Risk Free Rate (b) 4.27% 3.47% 4.47% 0.00% Pre-tax Cost of Debt (c) = (a) + (b) 13.93% 4.47% 5.17% 0.00% Marginal Tax Rate 35.00% 12.50% 30.00% 33.00% After Tax Cost of Debt (c) * (1-tax rate) 13.93% 3.91% 3.62% 0.00%

After computing the cost of debt for each firm we computed the after tax cost of debt. The

after tax cost of debt reflects the fact that interest payable on debt is deductible from the operating

income for tax purposes and results in tax savings for the firms.

In the case of American Airlines, the company cannot benefit from lower tax bill by financing

its operations with debt. The company has net operating loss before interest and hence pays no taxes.

In addition American Airlines has a huge accumulated tax loss, which could be carried forward and

used to offset future taxable income. Therefore the company does not enjoy tax benefits from the use

of debt and we excluded this component from the cost of capital calculation.

25

5. Cost of capital

Market value o f equi ty

The market value of equity for each firm has been estimated by multiplying the number of

shares outstanding for each company by the current share price. The market values of equity are

presented in Figure 20.

Figure 20 Market values of equity Market Value of Equity (million) American Airlines Ryanair BAA Asur

Market Value of Equity (million) 1,862.2 4,352.4 6,153.3 912.7

Source: Bloomberg

Market value o f debt

In estimating the market value of debt we again took two approaches:

Use the current value for debt that is publicly traded and information is obtainable;

Project interest and principal payments and discount them back at the current cost of

debt as estimated above.

In projecting the interest payments we have used the current interest payments to book value

of debt ratio as a proxy for the average interest rate payable on the debt; and the average maturity of

the outstanding debt.

In addition, AA, Ryanair and BAA have significant operating lease commitments, which are

not recorded in their books. Such commitments require that the firms make regular payments to the

lessors in exchange for the use of assets (aircrafts, real estate). Such transactions are treated as rent for

accounting purposes and lease payments are recorded as operating expense. The essence of the

transaction, however, is financing the use of the assets and lease payments could be viewed as interest

and principal repayment of a loan provided for the acquisition of the assets. Moreover, the companies

are committed to making these payments for a long period of time.

We treated lease commitment as another form of debt and discounted the future lease

payments at the current cost of debt to estimate their current market value. The present value of all

future lease payments have been included in the market value of the companies’ debt and the

operating income has been adjusted by adding back the operating lease payment and subtracting the

estimated depreciation charge associated with recording the leased assets in the companies’ books.

Summary of the market value of debt calculation is presented in Figure 21.

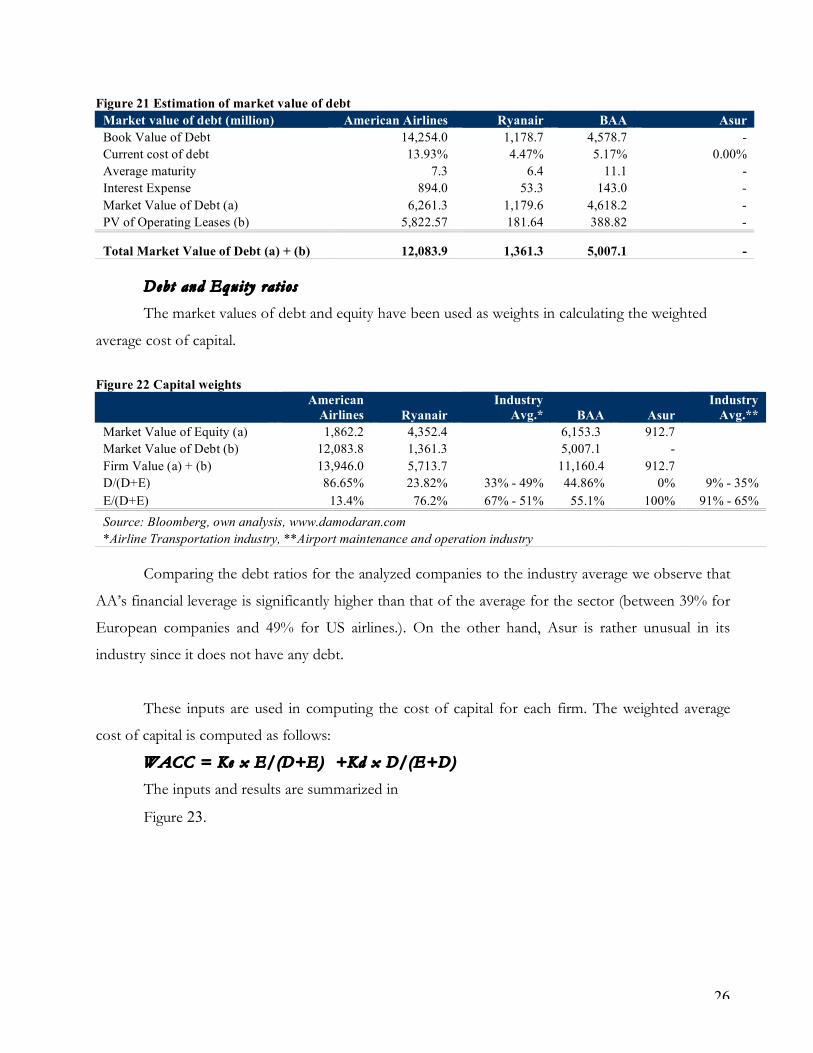

26

Figure 21 Estimation of market value of debt Market value of debt (million) American Airlines Ryanair BAA Asur Book Value of Debt 14,254.0 1,178.7 4,578.7 - Current cost of debt 13.93% 4.47% 5.17% 0.00% Average maturity 7.3 6.4 11.1 - Interest Expense 894.0 53.3 143.0 - Market Value of Debt (a) 6,261.3 1,179.6 4,618.2 - PV of Operating Leases (b) 5,822.57 181.64 388.82 -

Total Market Value of Debt (a) + (b) 12,083.9 1,361.3 5,007.1 -

Debt and Equity rat ios

The market values of debt and equity have been used as weights in calculating the weighted

average cost of capital.

Figure 22 Capital weights

American

Airlines Ryanair Industry

Avg.* BAA Asur Industry

Avg.** Market Value of Equity (a) 1,862.2 4,352.4 6,153.3 912.7 Market Value of Debt (b) 12,083.8 1,361.3 5,007.1 - Firm Value (a) + (b) 13,946.0 5,713.7 11,160.4 912.7 D/(D+E) 86.65% 23.82% 33% - 49% 44.86% 0% 9% - 35% E/(D+E) 13.4% 76.2% 67% - 51% 55.1% 100% 91% - 65% Source: Bloomberg, own analysis, www.damodaran.com *Airline Transportation industry, **Airport maintenance and operation industry

Comparing the debt ratios for the analyzed companies to the industry average we observe that

AA’s financial leverage is significantly higher than that of the average for the sector (between 39% for

European companies and 49% for US airlines.). On the other hand, Asur is rather unusual in its

industry since it does not have any debt.

These inputs are used in computing the cost of capital for each firm. The weighted average

cost of capital is computed as follows:

WACC = Ke x E/(D+E) +Kd x D/(E+D)

The inputs and results are summarized in

Figure 23.

27

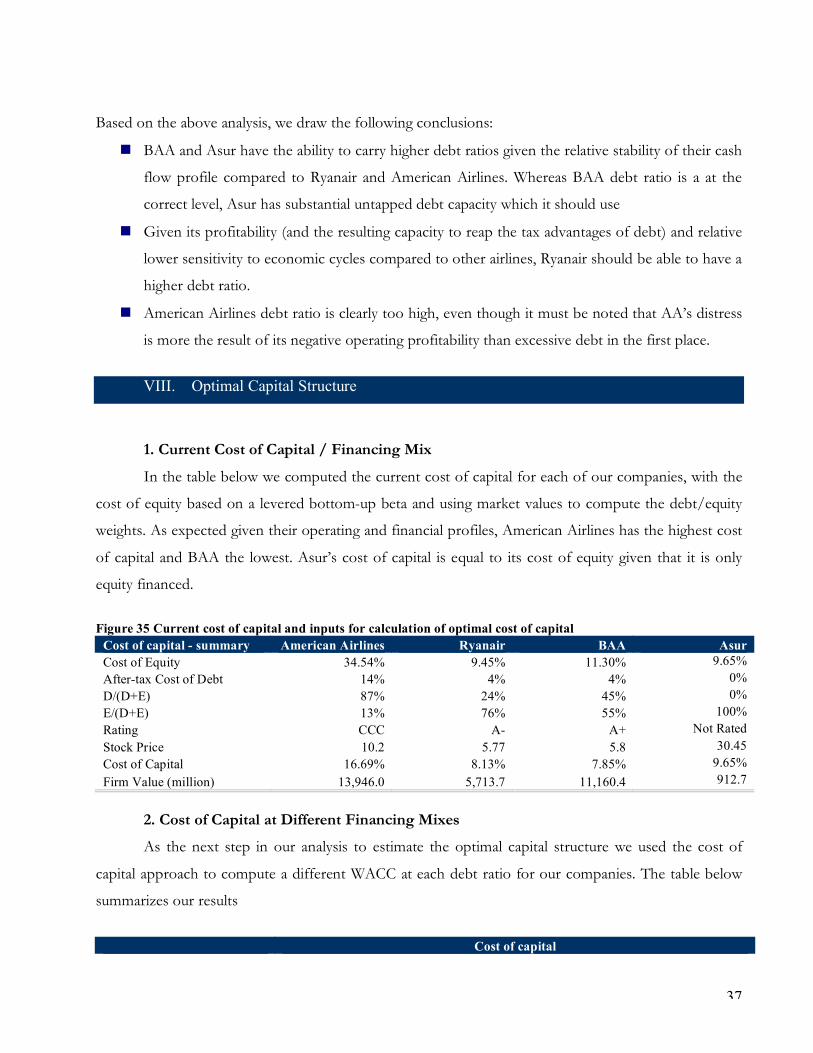

Figure 23 Calculation of cost of capital Cost of capital American Airlines Ryanair BAA Asur Beta 6.26 1.24 1.42 0.82 Cost of Equity 34.54% 9.45% 11.30% 9.65% E/(D+E) 13.35% 76.18% 55.14% 100.00% After-tax Cost of Debt 13.93% 3.91% 3.62% 0.00% D/(D+E) 86.65% 23.82% 44.86% 0.00% WACC 16.69% 8.13% 7.85% 9.65%

Not surprisingly the company with highest cost of capital is American Airlines, reflecting its

high risk. The high cost of capital is driven by two factors – high beta (volatile earnings and high debt

to equity ratio) and high cost of debt (low credit rating because of high debt and huge interest

payments). The lowest cost of capital, that of BAA, reflects the fact that the company is relatively

mature and stable, with predictable earnings and cash flows and is less subjective to market

fluctuations.

The estimated cost of capital of and cost equity are the hurdle rates that should be used in

capital allocation decisions in each company. These are the minimum acceptable rates against

performance of each new project considered should be measured – return on equity against the cost

of equity and return on capital against cost of capital. In addition, the cost of equity and cost of capital

rates are the rates at which projects’ cash flows should be discounted to estimate their net present

value.

VI. Investment Return Analysis

The ability of each firm to grow and create value for its stockholders ultimately depends on its

management capability to identify and undertake projects that generate returns exceeding the cost of

capital employed. In this section we will analyze the quality of the projects that the four companies

undertake ad review the past performance of the companies as measured by indicators such as Return

on Capital (ROC) and Return on Equity (ROE).

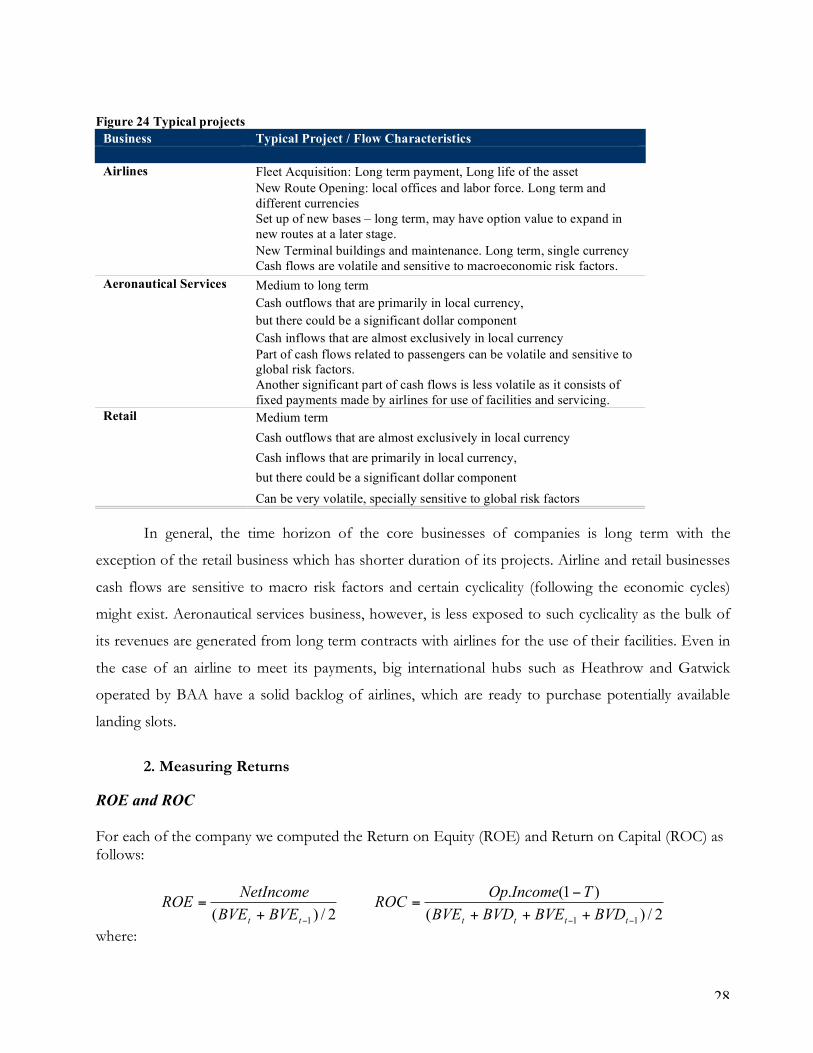

1. Typical project

The companies, subject to our analysis are involved primarily in 3 types of businesses – air

transportation, aeronautical services and retail services. Aeronautical services include operation and

maintenance of airport and all related facilities that are used by passengers and airlines. Some of the

characteristics of a typical project for each business are presented in Figure 24.

28

Figure 24 Typical projects

Business Typical Project / Flow Characteristics

Fleet Acquisition: Long term payment, Long life of the asset New Route Opening: local offices and labor force. Long term and different currencies Set up of new bases – long term, may have option value to expand in new routes at a later stage.

Airlines

New Terminal buildings and maintenance. Long term, single currency Cash flows are volatile and sensitive to macroeconomic risk factors. Medium to long term Cash outflows that are primarily in local currency, but there could be a significant dollar component Cash inflows that are almost exclusively in local currency

Aeronautical Services

Part of cash flows related to passengers can be volatile and sensitive to global risk factors. Another significant part of cash flows is less volatile as it consists of fixed payments made by airlines for use of facilities and servicing. Medium term Cash outflows that are almost exclusively in local currency Cash inflows that are primarily in local currency, but there could be a significant dollar component

Retail

Can be very volatile, specially sensitive to global risk factors

In general, the time horizon of the core businesses of companies is long term with the

exception of the retail business which has shorter duration of its projects. Airline and retail businesses

cash flows are sensitive to macro risk factors and certain cyclicality (following the economic cycles)

might exist. Aeronautical services business, however, is less exposed to such cyclicality as the bulk of

its revenues are generated from long term contracts with airlines for the use of their facilities. Even in

the case of an airline to meet its payments, big international hubs such as Heathrow and Gatwick

operated by BAA have a solid backlog of airlines, which are ready to purchase potentially available

landing slots.

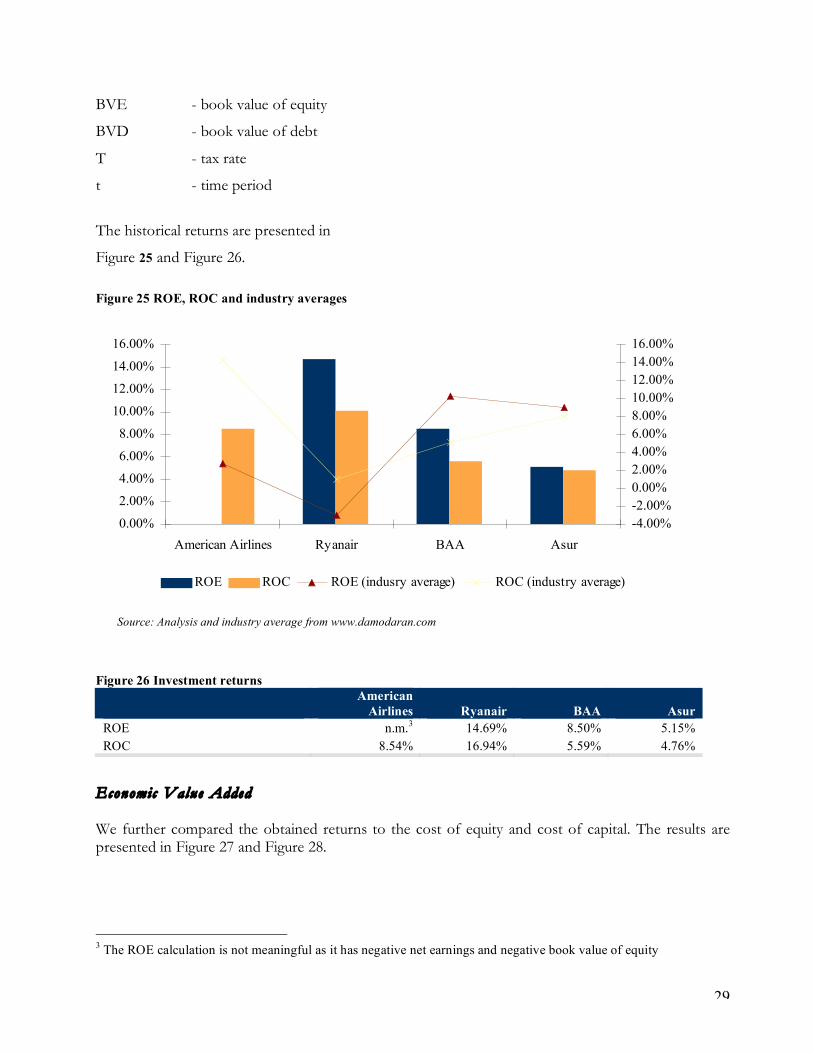

2. Measuring Returns

ROE and ROC For each of the company we computed the Return on Equity (ROE) and Return on Capital (ROC) as follows:

2/)( 1!+=

ttBVEBVE

NetIncomeROE

2/)(

)1(.

11 !! +++

!=

tttt BVDBVEBVDBVE

TIncomeOpROC

where:

29

BVE - book value of equity

BVD - book value of debt

T - tax rate

t - time period

The historical returns are presented in

Figure 25 and Figure 26.

Figure 25 ROE, ROC and industry averages Figure 26 Investment returns

American

Airlines Ryanair BAA Asur ROE n.m.3 14.69% 8.50% 5.15% ROC 8.54% 16.94% 5.59% 4.76%

Economic Value Added We further compared the obtained returns to the cost of equity and cost of capital. The results are presented in Figure 27 and Figure 28.

3 The ROE calculation is not meaningful as it has negative net earnings and negative book value of equity

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

American Airlines Ryanair BAA Asur

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

ROE ROC ROE (indusry average) ROC (industry average)

Source: Analysis and industry average from www.damodaran.com

30

Figure 27 Equity Economic Value Added

American

Airlines Ryanair BAA Asur ROE (a)4 nm 14.69% 8.50% 5.15% Cost of Equity (b) 34.54% 9.45% 11.30% 9.65% Equity Return Spread (a)-(b) nm 5.24% -2.80% -3.23% Average book value of equity (268.0) 1,574.7 4,797.0 1,057.7

Equity EVA n.a

82.5

(134.5)

(47.6)

From the companies included in the analysis only Ryanair created excess returns on equity

(Return in Equity – Cost of Equity). It created a positive equity economic value added (EVA) of €

82.5 million based on the last 12 months results. At the same time the airline industry destroyed on

average value of $ 4,95765.7 in 20045. Both BAA and Asur had return on equity lower than their cost

of equity. Comparing these results with the positive Jensen’s alpha values calculated in Section IV, we

can conclude that although both firms performed better that the market expected, they still have not

generated equity returns in excess of their equity costs.

Multiplying the spread between the return on capital and cost of capital for each company by

the average book value of total capital (equity + debt) we estimated the economic value added for each

firm.

Figure 28 Economic Value Added

American

Airlines Ryanair BAA Asur ROC 8.54% 10.14% 5.59% 4.76% Cost of Capital (b) 16.69% 8.13% 7.85% 9.65% Capital Return Spread (a)-(b) -8.15% 2.01% -2.27% -4.89% Average book value of capital 13,862.5 2,652.8 8,427.0 1,057.7 EVA (million) (1,129.5) 53.3 (191.0) (51.7)

Again the only company that created value during the observed period was Ryanair. The

average EVA for the sector in 2004 was $9,551.76

3. Future outlook

The ability of any of the companies to generate positive excess returns depends on its competitive

advantages and their sustainability in the medium and long term. In this section we look at some key

4 The ROE calculation is not meaningful as it has negative net earnings and negative book value of equity 5 Equity EVA for US market used as a comparison. Source: www.damodaran.com 6 EVA for US air transportation sector used as comparable. Source: www.damodaran.com

31

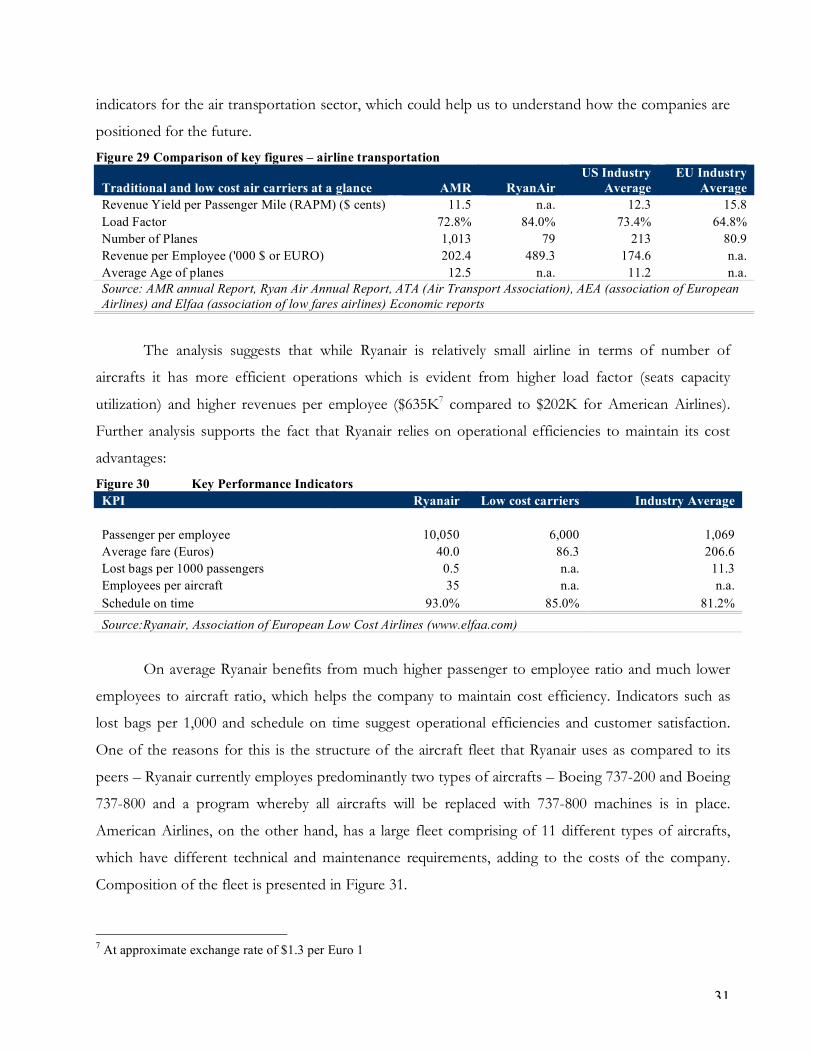

indicators for the air transportation sector, which could help us to understand how the companies are

positioned for the future.

Figure 29 Comparison of key figures – airline transportation

Traditional and low cost air carriers at a glance AMR RyanAir US Industry

Average EU Industry

Average Revenue Yield per Passenger Mile (RAPM) ($ cents) 11.5 n.a. 12.3 15.8 Load Factor 72.8% 84.0% 73.4% 64.8% Number of Planes 1,013 79 213 80.9 Revenue per Employee ('000 $ or EURO) 202.4 489.3 174.6 n.a. Average Age of planes 12.5 n.a. 11.2 n.a. Source: AMR annual Report, Ryan Air Annual Report, ATA (Air Transport Association), AEA (association of European Airlines) and Elfaa (association of low fares airlines) Economic reports

The analysis suggests that while Ryanair is relatively small airline in terms of number of

aircrafts it has more efficient operations which is evident from higher load factor (seats capacity

utilization) and higher revenues per employee ($635K7 compared to $202K for American Airlines).

Further analysis supports the fact that Ryanair relies on operational efficiencies to maintain its cost

advantages:

Figure 30 Key Performance Indicators KPI Ryanair Low cost carriers Industry Average Passenger per employee 10,050 6,000 1,069 Average fare (Euros) 40.0 86.3 206.6 Lost bags per 1000 passengers 0.5 n.a. 11.3 Employees per aircraft 35 n.a. n.a. Schedule on time 93.0% 85.0% 81.2% Source:Ryanair, Association of European Low Cost Airlines (www.elfaa.com)

On average Ryanair benefits from much higher passenger to employee ratio and much lower

employees to aircraft ratio, which helps the company to maintain cost efficiency. Indicators such as

lost bags per 1,000 and schedule on time suggest operational efficiencies and customer satisfaction.

One of the reasons for this is the structure of the aircraft fleet that Ryanair uses as compared to its

peers – Ryanair currently employes predominantly two types of aircrafts – Boeing 737-200 and Boeing

737-800 and a program whereby all aircrafts will be replaced with 737-800 machines is in place.

American Airlines, on the other hand, has a large fleet comprising of 11 different types of aircrafts,

which have different technical and maintenance requirements, adding to the costs of the company.

Composition of the fleet is presented in Figure 31.

7 At approximate exchange rate of $1.3 per Euro 1

32

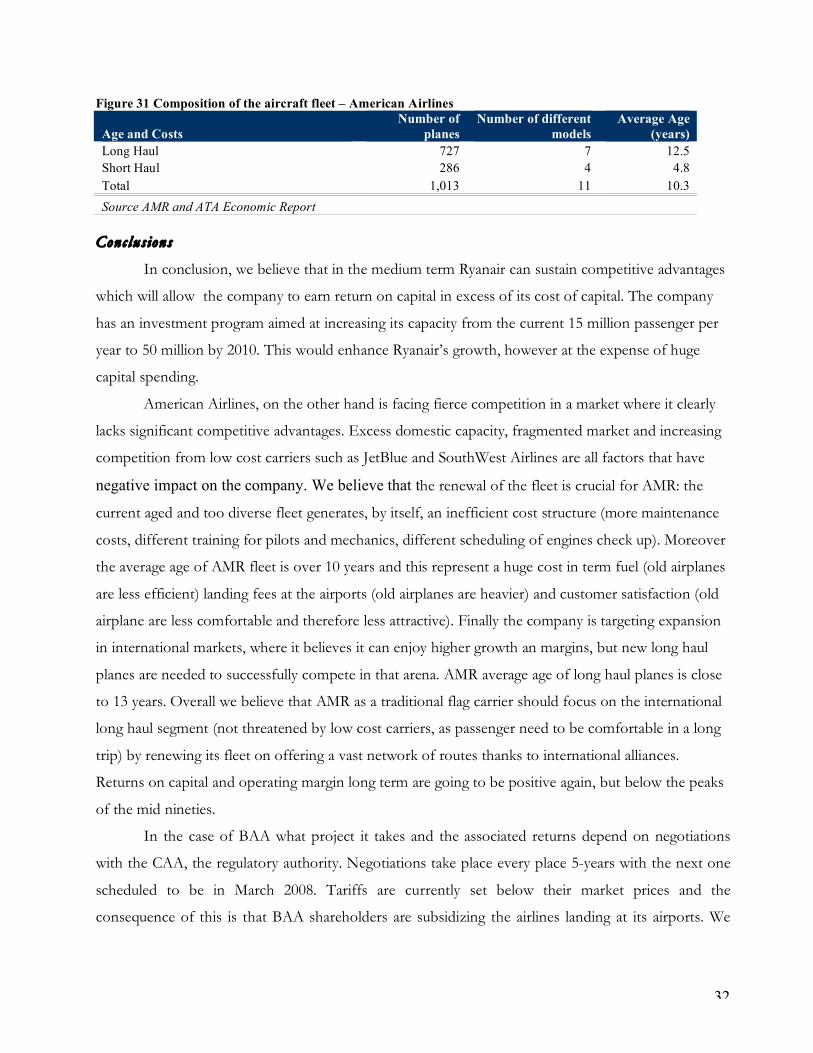

Figure 31 Composition of the aircraft fleet – American Airlines

Age and Costs Number of

planes Number of different

models Average Age

(years) Long Haul 727 7 12.5 Short Haul 286 4 4.8 Total 1,013 11 10.3 Source AMR and ATA Economic Report

Conc lus ions

In conclusion, we believe that in the medium term Ryanair can sustain competitive advantages

which will allow the company to earn return on capital in excess of its cost of capital. The company

has an investment program aimed at increasing its capacity from the current 15 million passenger per

year to 50 million by 2010. This would enhance Ryanair’s growth, however at the expense of huge

capital spending.

American Airlines, on the other hand is facing fierce competition in a market where it clearly

lacks significant competitive advantages. Excess domestic capacity, fragmented market and increasing

competition from low cost carriers such as JetBlue and SouthWest Airlines are all factors that have

negative impact on the company. We believe that the renewal of the fleet is crucial for AMR: the

current aged and too diverse fleet generates, by itself, an inefficient cost structure (more maintenance

costs, different training for pilots and mechanics, different scheduling of engines check up). Moreover

the average age of AMR fleet is over 10 years and this represent a huge cost in term fuel (old airplanes

are less efficient) landing fees at the airports (old airplanes are heavier) and customer satisfaction (old

airplane are less comfortable and therefore less attractive). Finally the company is targeting expansion

in international markets, where it believes it can enjoy higher growth an margins, but new long haul

planes are needed to successfully compete in that arena. AMR average age of long haul planes is close

to 13 years. Overall we believe that AMR as a traditional flag carrier should focus on the international

long haul segment (not threatened by low cost carriers, as passenger need to be comfortable in a long

trip) by renewing its fleet on offering a vast network of routes thanks to international alliances.

Returns on capital and operating margin long term are going to be positive again, but below the peaks

of the mid nineties.

In the case of BAA what project it takes and the associated returns depend on negotiations

with the CAA, the regulatory authority. Negotiations take place every place 5-years with the next one

scheduled to be in March 2008. Tariffs are currently set below their market prices and the

consequence of this is that BAA shareholders are subsidizing the airlines landing at its airports. We

33

think that this situation is very unlikely to change in the short term, at least until the new review in

March 2008.

Similarly for Asur, the company faces mandatory capital investments which are negotiated with

the Mexican Ministry of Communications and Transportation every five years. In the coming years,

Asur’s main investment project will be the construction of a second runway at the Cancun airport, to

handle the higher than expected growth in passenger volumes. This project has already been moved

forward five years from its original start date, signaling the company’s strong confidence in its growth

prospects for the coming years.

VII. Capital Structure Choices

1. Current financing mix

Figure 32 below summarizes the current debt structure of American Airlines, BAA and Ryanir (Asur

has no debt). As can be observed, the three companies employ very different kinds of debt:

Ameri can Airl ines

AA has outstanding a wide variety of notes, from bank debt, plain vanilla bonds to more structured

debt instruments. On one hand this is driven by the necessity to tailor the debt to match the

company’s cash flow profile and risk, which is very specific. On the other hand this is a symptom of

the financial difficulties the company has been going through and the need to raise capital in any form

it was available. With this respect, it is worth noticing that the BoD has even authorized (but not yet

issued) the emission of 20million preferred shares.

Ryanair

Ryanair has only bank debt outstanding and this is a reflection of both the early stage of the life cycle

is in and its ability to generate cash flows, thus funding growth largely with internal funds. We expect

the financing mix to change as the company continues to expand and it will need to access the public

bond markets to fund its future projects.

34

BAA

BAA’s debt is almost all made up by straight bonds (82% of the total), with the rest coming from bank

debt and two outstanding convertible bonds issues. This is due to the high stability and predictability

of its cash flows, which has given BAA easy access to the public the bond markets. The company has

issued substantial debt over the last years (Gross Debt went from approx. £1.0 bn in 1995 to over £4

bn today with D/E climbing from 20% to 81%) as a result of the expected capex expenditures

connected with the fifth terminal at Heathrow and other projects.

Asur

Asur has no debt outstanding as it has been able to fund all its capex requirements through internal

cash-flows.

Figure 32 Current debt characteristics

Company Type of Financing Amount (mm) Interest Rate on

Books Maturity Secured Variable and Fixed rate indebtness 6,340.0 2.03% - 9.16% 2021 Enhanced Equipment trust certificates 3,707.0 2.14% - 9.09% 2011 Special facility revenue bond 946.0 6.00% - 8.50% 2036 Credit Facility Agreement 850.0 9.150% 2010 Senior Convertibles Notes 619.0 4.25% - 4.50% 2023-2024 Debentures 330.0 9.00% - 10.20% 2021 Notes 303.0 7.88% - 10.55% 2039

Americal Airlines

Other 1,159.0 Straight Bond 200.0 7.875% 2007 Straight Bond 400.0 5.750% 2013 Straight Bond 300.0 11.750% 2016 Straight Bond 250.0 8.500% 2021 Straight Bond 200.0 6.375% 2028 Straight Bond 900.0 5.750% 2031 Straight Bond 750.0 4.500% 2014 Convertible Bond 424.0 2.940% 2008

BAA

Convertible Bond 425.0 2.625% 2009 Secured bank debt 80.3 n.a. 2005 Secured bank debt 84.2 n.a. 2006 Secured bank debt 88.1 n.a. 2007 Secured bank debt 92.1 n.a. 2008

Ryanair

Secured bank debt 608.2 n.a. 2009 - 2016

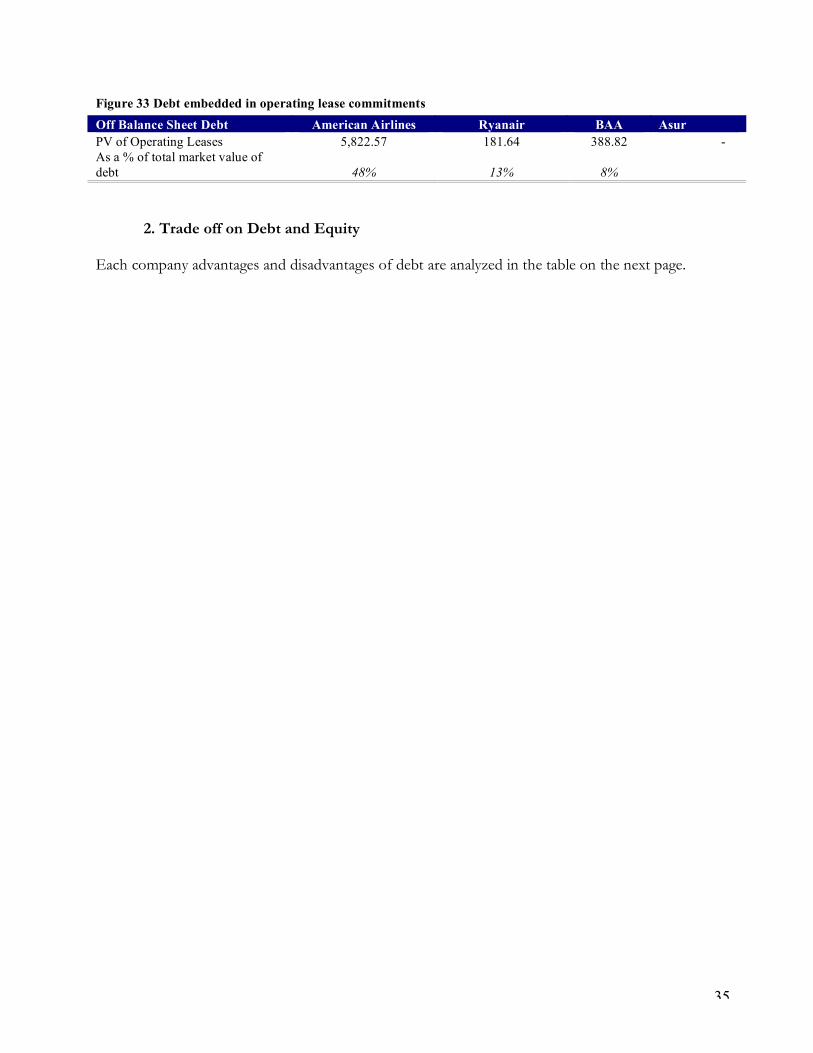

In addition to the balance sheet debt 3 of the 4 companies analyzed have relevant off-balance

sheet items related to operating leases that we summarize below.

35

Figure 33 Debt embedded in operating lease commitments

2. Trade off on Debt and Equity

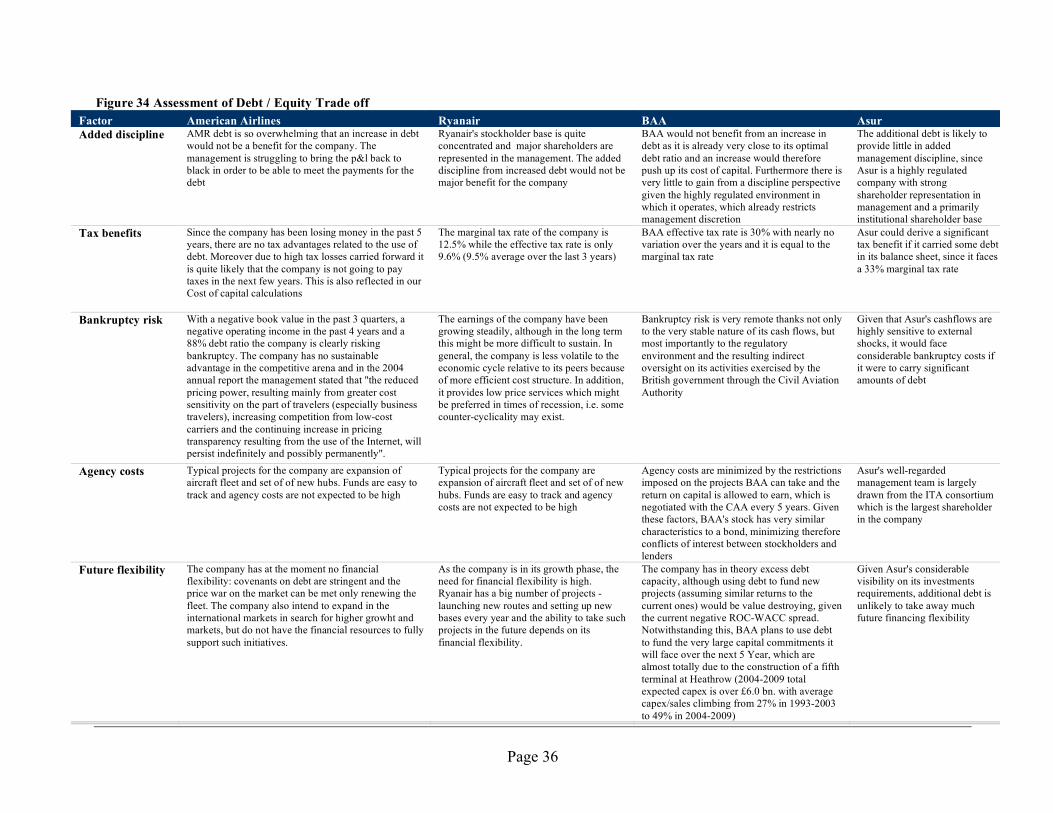

Each company advantages and disadvantages of debt are analyzed in the table on the next page.

Off Balance Sheet Debt American Airlines Ryanair BAA Asur PV of Operating Leases 5,822.57 181.64 388.82 - As a % of total market value of debt 48% 13% 8%

Page 36

Figure 34 Assessment of Debt / Equity Trade off Factor American Airlines Ryanair BAA Asur Added discipline AMR debt is so overwhelming that an increase in debt

would not be a benefit for the company. The management is struggling to bring the p&l back to black in order to be able to meet the payments for the debt

Ryanair's stockholder base is quite concentrated and major shareholders are represented in the management. The added discipline from increased debt would not be major benefit for the company

BAA would not benefit from an increase in debt as it is already very close to its optimal debt ratio and an increase would therefore push up its cost of capital. Furthermore there is very little to gain from a discipline perspective given the highly regulated environment in which it operates, which already restricts management discretion

The additional debt is likely to provide little in added management discipline, since Asur is a highly regulated company with strong shareholder representation in management and a primarily institutional shareholder base

Tax benefits Since the company has been losing money in the past 5 years, there are no tax advantages related to the use of debt. Moreover due to high tax losses carried forward it is quite likely that the company is not going to pay taxes in the next few years. This is also reflected in our Cost of capital calculations

The marginal tax rate of the company is 12.5% while the effective tax rate is only 9.6% (9.5% average over the last 3 years)

BAA effective tax rate is 30% with nearly no variation over the years and it is equal to the marginal tax rate

Asur could derive a significant tax benefit if it carried some debt in its balance sheet, since it faces a 33% marginal tax rate

Bankruptcy risk With a negative book value in the past 3 quarters, a negative operating income in the past 4 years and a 88% debt ratio the company is clearly risking bankruptcy. The company has no sustainable advantage in the competitive arena and in the 2004 annual report the management stated that "the reduced pricing power, resulting mainly from greater cost sensitivity on the part of travelers (especially business travelers), increasing competition from low-cost carriers and the continuing increase in pricing transparency resulting from the use of the Internet, will persist indefinitely and possibly permanently".

The earnings of the company have been growing steadily, although in the long term this might be more difficult to sustain. In general, the company is less volatile to the economic cycle relative to its peers because of more efficient cost structure. In addition, it provides low price services which might be preferred in times of recession, i.e. some counter-cyclicality may exist.

Bankruptcy risk is very remote thanks not only to the very stable nature of its cash flows, but most importantly to the regulatory environment and the resulting indirect oversight on its activities exercised by the British government through the Civil Aviation Authority

Given that Asur's cashflows are highly sensitive to external shocks, it would face considerable bankruptcy costs if it were to carry significant amounts of debt

Agency costs Typical projects for the company are expansion of aircraft fleet and set of of new hubs. Funds are easy to track and agency costs are not expected to be high

Typical projects for the company are expansion of aircraft fleet and set of of new hubs. Funds are easy to track and agency costs are not expected to be high