Embed Size (px)

Citation preview

1

“Version 14_05_15”

REVISED SYLLABUS

REPORT 191 (NATED)

FINANCIAL ACCOUNTING N6

REPUBLIC OF SOUTH AFRICA

CODE NUMBER: 04010216

IMPLEMENTATION DATE: JANUARY 2015

2

“Version 14_05_15”

CONTENTS

1. Aims

2. Duration of instruction

3. Evaluation

4. Semester mark

5. Examination

6. Pass requirements

7. General information

8. Learning content

9. Literature reference

10. Detailed syllabus

3

“Version 14_05_15”

FINANCIAL ACCOUNTING N6

1. GENERAL AIM 1.1 GENERAL OBJECTIVES

* To develop the logical thought process and analytical abilities of students

to enable them to apply the fundamental principles of accounting to new and unfamiliar situations.

* To encourage a sound and systematic approach to the solution of

problems. * To contribute to the formative education of students by developing

characteristic demands associated with accounting, such as neatness, orderliness, thoroughness, accuracy, sound judgement and a sense of responsibility.

* To develop the understanding students have of and their integration with

their social environment through the meaningful interpretation of accounting information which they will come across in future.

* To enable students to deal with the basic demands of an accounting

occupation with confidence. 1.2 SPECIFIC AIMS

* To develop the accounting and numeracy skills of students who enter an accounting occupation directly, to enable them to deal with all procedures followed in the field of accounting.

* To increase students’ understanding of accounting and management

principles.

* To enable students to acquire knowledge and skills of accounting systems generally used by business enterprises.

* To give students the opportunity to apply in practice the theoretical

knowledge of accounting principles and procedures acquired during the learning process by giving them the necessary exposure to practice-related application of exercises directly from source and supporting documents, and by simulating feasible situations related to the accounting practice.

4

“Version 14_05_15”

* To enable students to acquire knowledge and skills of all administrative accounting tasks and related matters; for example completing of and handling business documents, filing, cost accounting, prospects of investment and financing.

* To equip students with knowledge of the required principles, concepts and

procedures of accounting that are in line with generally accepted accounting practice.

2. ENTRANCE REQUIREMENT Financial Accounting N5 3. DURATION OF INSTRUCTION Full-time: A minimum of five (5) contact hours per week for one semester Part-time: A minimum of three hours per week for one semester 4. EVALUATION/ASSESSMENT

Evaluation is conducted on a continual basis by means of short class and revision tests, formal tests, internal assessment and practice-orientated assignments, exercises as well as an external examination.

4.1 Internal evaluation/assessment 4.1.1 Class and revision tests/assessments

Short class and revision tests are given on a regular basis and are aimed at rectifying problems before proceeding with new modules. Class and revision tests can be short daily tests that take up a short time during each period, and are compiled and marked in accordance with the amount of work done in the module. Exercises done by students, as well as short assignments can also be marked and can count towards the semester mark for class and revision tests.

4.1.2 Formal tests/assessments

Formal tests are conducted to cover all modules or work units. These tests are aimed at evaluating students’ knowledge on completion of modules or work units.

4.1.3 Practice-orientated assignments

Students are given a practice-orientated assignment and projects to evaluate whether they have mastered the practical component of Accounting. Student performance with regard to zeal, punctuality in completing tasks or assignments conscientiousness, interest, dedication, adaptability, etc. which should be gradually developed to facilitate entrance to the world of work, is also included.

5

“Version 14_05_15”

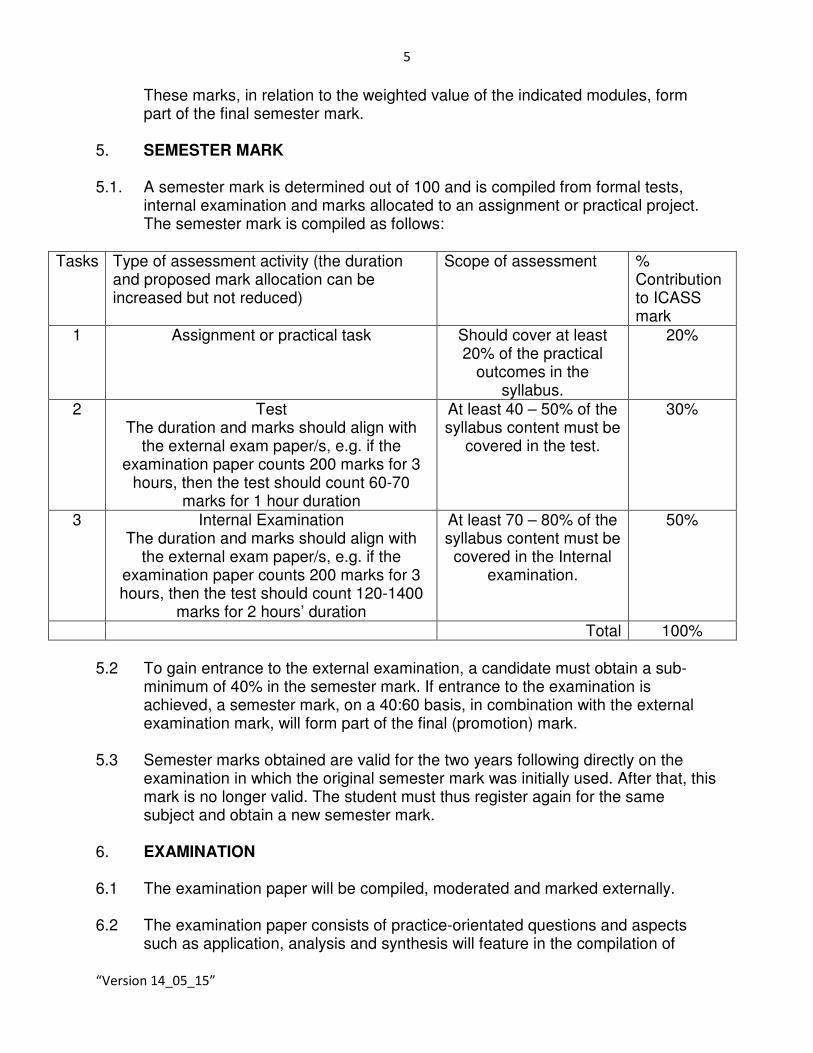

These marks, in relation to the weighted value of the indicated modules, form part of the final semester mark.

5. SEMESTER MARK 5.1. A semester mark is determined out of 100 and is compiled from formal tests,

internal examination and marks allocated to an assignment or practical project. The semester mark is compiled as follows:

Tasks Type of assessment activity (the duration

and proposed mark allocation can be increased but not reduced)

Scope of assessment % Contribution to ICASS mark

1 Assignment or practical task Should cover at least 20% of the practical

outcomes in the syllabus.

20%

2 Test The duration and marks should align with

the external exam paper/s, e.g. if the examination paper counts 200 marks for 3

hours, then the test should count 60-70 marks for 1 hour duration

At least 40 – 50% of the syllabus content must be

covered in the test.

30%

3 Internal Examination The duration and marks should align with

the external exam paper/s, e.g. if the examination paper counts 200 marks for 3 hours, then the test should count 120-1400

marks for 2 hours’ duration

At least 70 – 80% of the syllabus content must be covered in the Internal

examination.

50%

Total 100% 5.2 To gain entrance to the external examination, a candidate must obtain a sub-

minimum of 40% in the semester mark. If entrance to the examination is achieved, a semester mark, on a 40:60 basis, in combination with the external examination mark, will form part of the final (promotion) mark.

5.3 Semester marks obtained are valid for the two years following directly on the

examination in which the original semester mark was initially used. After that, this mark is no longer valid. The student must thus register again for the same subject and obtain a new semester mark.

6. EXAMINATION 6.1 The examination paper will be compiled, moderated and marked externally. 6.2 The examination paper consists of practice-orientated questions and aspects

such as application, analysis and synthesis will feature in the compilation of

6

“Version 14_05_15”

accounts, statements and accounting-related calculations. Although comprehension questions could also be used, these will be limited as far as possible seeing that the examination papers are directly aimed at accounting-related tasks as carried out in practice.

6.3 A three-hour paper totalling 200 marks will be set at the end of the semester. 7. PASS REQUIREMENTS 7.1 To pass Financial Accounting N6, a candidate must obtain a final mark of 40% by

addition of the semester mark and the examination mark in a 40:60 ratio, provided that a sub- minimum of 40% is obtained as a semester mark as well as an examination mark.

8. GENERAL INFORMATION 8.1 The practical components (assignments and projects) are aimed at preparing the

student for the world of work in general and at the execution of accounting functions in particular.

8.2 The practical components are also aimed at increasing the student’s competence

level in such a way that he/she can be productive in a job for which an accounting background is required.

8.3 It is thus necessary that the student acquires practical experience in the field of

accounting by doing assignments on the execution of accounting functions as dealt with in organisations to establish direct contact between the student and the accounting practice. Visits by experts in accounting can guide the students and help to train them.

8.4 The practical components are further directed at learning an accounting package

on a microcomputer so as to keep pace with modern computer-directed trends in accounting areas as applied in practice. It is therefore recommended that students enrol for Computerised Financial Systems N6 together with Financial Accounting N6.

9. LEARNING CONTENT WEIGHTED VALUE MODULE 1: CONCEPTUAL FRAMEWORK 5 (1 WEEK) MODULE 2: VALUE-ADDED TAX 10 (1 WEEK)

MODULE 3: COMPANIES 40 (7 WEEKS) MODULE 4: CLOSE CORPORATIONS 15

7

“Version 14_05_15”

(3 WEEKS) MODULE 5: CASH FLOW STATEMENTS: COMPANIES AND CLOSE CORPORATIONS 15 (2 WEEKS) MODULE 6: AUDITING 15 (2 WEEKS) Total: 100

8

“Version 14_05_15”

FINANCIAL ACCOUNTING N6 MODULE 1: CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING

Content Learning objectives

1.1 Introduction

1.2 Qualitative characteristics

• Comparability

• Verifiability

• Timeliness

• Understandability

1.3 Underlying assumption

• Going concern

1.4 Elements of financial statements

• Assets

• Liabilities

• Equity

• Income

• Expenses

1.5 Recognition criteria

Students should be able to 1.1 Give a short description of the

conceptual framework and the objectives of general financial reporting

1.2 Name and explain what each of the characteristics is and what it means.

1.3 Explain what is meant by the term

“going concern”

1.4 Name and briefly describe each of the elements of financial statements and apply them to an example.

1.5 Describe the recognition criteria and

apply them to an example. Didactic guidelines With reference to learning objectives 1.1 to 1.5:

1. The aim of these themes is to provide the student with background knowledge on the conceptual framework, the characteristics of financial statements, what is meant by the underlying assumption, going concern, and what the different elements of financial statements are and how to recognize them.

Evaluation/Assessment With reference to learning objectives 1.1 to 1.5:

1. Short theory questions are asked.

With reference to learning objectives 1.4 and 1.5:

9

“Version 14_05_15”

2. Apply it to a practical example in a short question. Determine what type of element the example is according to the definition and decide if and when the element must be recognized.

10

“Version 14_05_15”

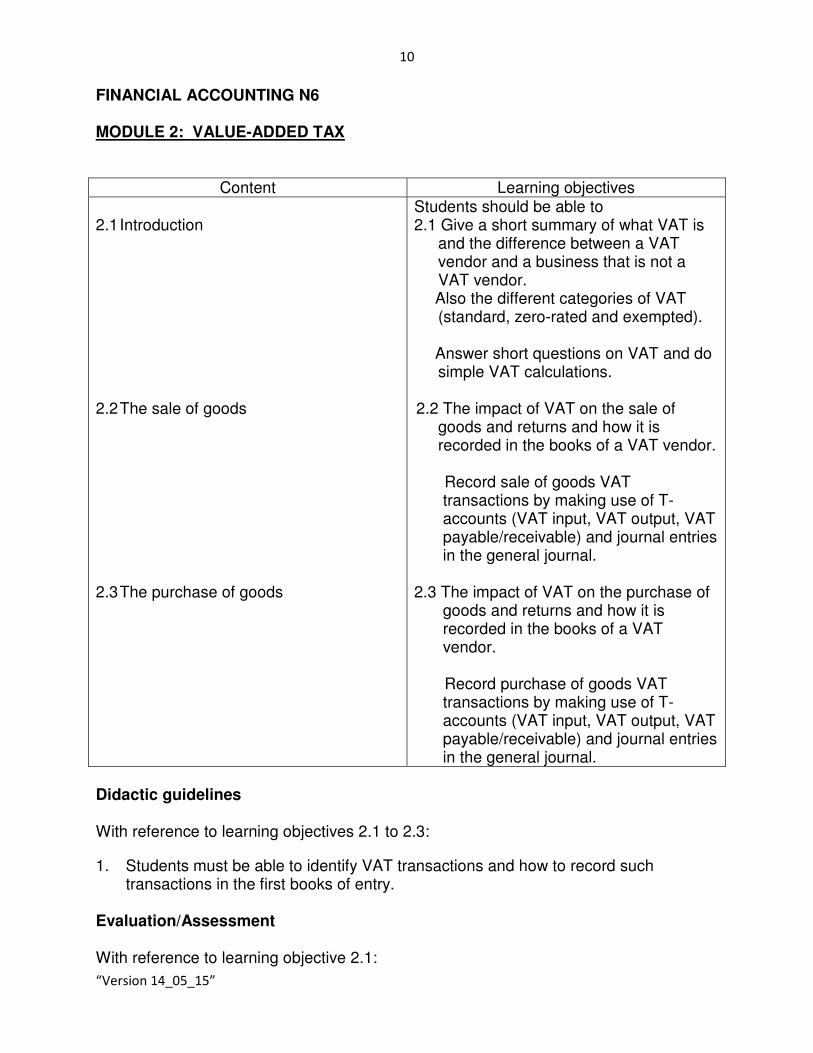

FINANCIAL ACCOUNTING N6 MODULE 2: VALUE-ADDED TAX

Content Learning objectives

2.1 Introduction

2.2 The sale of goods

2.3 The purchase of goods

Students should be able to 2.1 Give a short summary of what VAT is

and the difference between a VAT vendor and a business that is not a VAT vendor. Also the different categories of VAT (standard, zero-rated and exempted).

Answer short questions on VAT and do simple VAT calculations.

2.2 The impact of VAT on the sale of

goods and returns and how it is recorded in the books of a VAT vendor.

Record sale of goods VAT transactions by making use of T-accounts (VAT input, VAT output, VAT payable/receivable) and journal entries in the general journal.

2.3 The impact of VAT on the purchase of

goods and returns and how it is recorded in the books of a VAT vendor.

Record purchase of goods VAT transactions by making use of T-accounts (VAT input, VAT output, VAT payable/receivable) and journal entries in the general journal.

Didactic guidelines With reference to learning objectives 2.1 to 2.3:

1. Students must be able to identify VAT transactions and how to record such transactions in the first books of entry.

Evaluation/Assessment With reference to learning objective 2.1:

11

“Version 14_05_15”

1. Short questions to recognize VAT and

2. Short calculations how to calculate VAT

With reference to learning objectives 2.2 and 2.3:

3. Record simple VAT transactions in T-accounts as well as journal entries.

12

“Version 14_05_15”

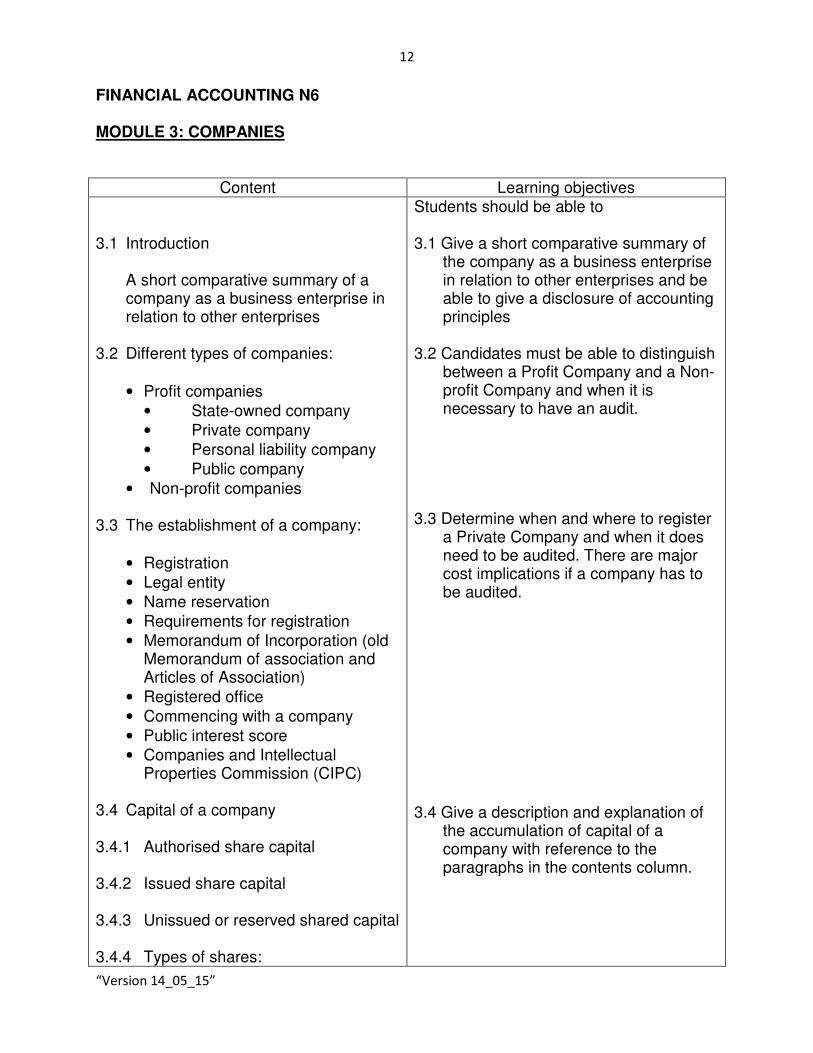

FINANCIAL ACCOUNTING N6 MODULE 3: COMPANIES

Content Learning objectives

3.1 Introduction

A short comparative summary of a company as a business enterprise in relation to other enterprises

3.2 Different types of companies:

• Profit companies

• State-owned company

• Private company

• Personal liability company

• Public company

• Non-profit companies

3.3 The establishment of a company:

• Registration

• Legal entity

• Name reservation

• Requirements for registration

• Memorandum of Incorporation (old Memorandum of association and Articles of Association)

• Registered office

• Commencing with a company

• Public interest score

• Companies and Intellectual Properties Commission (CIPC)

3.4 Capital of a company

3.4.1 Authorised share capital

3.4.2 Issued share capital

3.4.3 Unissued or reserved shared capital 3.4.4 Types of shares:

Students should be able to 3.1 Give a short comparative summary of

the company as a business enterprise in relation to other enterprises and be able to give a disclosure of accounting principles

3.2 Candidates must be able to distinguish

between a Profit Company and a Non-profit Company and when it is necessary to have an audit.

3.3 Determine when and where to register

a Private Company and when it does need to be audited. There are major cost implications if a company has to be audited.

3.4 Give a description and explanation of

the accumulation of capital of a company with reference to the paragraphs in the contents column.

13

“Version 14_05_15”

• Preference shares

• Ordinary share capital

3.4.5 Issuing of share capital 3.4.6 Reserves

3.4.7 Dividends 3.5 Taxation:

• Different from other enterprises e.g. sole trader and partnership

• Current tax rate

3.6 Financial statements according to the requirements of International Financial Reporting Standards

3.6.1 General information

• Reasonable edition

• Internal Financial Statements according to the Memorandum (old Articles) of Association

• Minimum requirements for financial statements compiled for publication or circulation

3.6.2 STATEMENT OF FINANCIAL

POSITION: Framework and Notes 3.6.3 STATEMENT OF COMPREHENSIVE INCOME:

Framework and Notes 3.6.4 STATEMENT OF CHANGES IN

EQUITY: Framework and Notes

3.5 Give a short explanation of the tax

implications for companies, compared to other business enterprises, and name the prescribed tax rate for companies

3.6.1 Give the requirements of

International Financial Reporting Standards (IFRS) external financial statements

3.6.2 Write short explanatory notes on the

different sections of the STATEMENT OF FINANCIAL POSITION and describe the aims and importance of each section or note

3.6.3 Write short explanatory notes on the

different sections of the STATEMENT OF COMPREHENSIVE INCOME and describe the aims and importance of each section or note

3.6.4 Write short explanatory notes on the

different sections of the

14

“Version 14_05_15”

STATEMENT OF CHANGES IN EQUITY

Didactic guidelines With reference to learning objectives 3.1 to 3.3: 1. The aim of these themes is to provide the student with background knowledge on

the company as business enterprise. It is therefore necessary continuously to make comparisons between the different enterprises. Students must be able to identify when it is necessary to register a Private company and know what the requirements are to be audited.

With reference to learning objective 3.4: 2. The aim of these themes is to provide the student with background knowledge on

the acquisition of share capital and the statutory requirements of issuing shares and dividends.

With reference to learning objective 3.6: 3. The aim of these themes is to clarify for students the requirements according to the

Companies Act (2008 amended) in respect of format and minimum disclosure of the financial statements of a company. Students should therefore be able to explain the aim of each note in the context of the framework of the Statement of Financial Position and Statement of Comprehensive Income.

4. The most recent requirements of the Companies Act (2008 amended) appear in the Government Gazette. It is the responsibility of lecturers to know all the most recent changes and terminology.

EVALUATION/ASSESSMENT With reference to learning objectives 3.1 to 3.5: 1. Short theory questions could be asked.

With reference to 3.6: 2. A fully or partially completed set of financial statements could be given to students.

Theory questions as well as calculations could be asked to evaluate the students’ insight into the Companies Act (2008 amended).

3. Short theory questions could be asked on this theme. FINANCIAL ACCOUNTING N6

15

“Version 14_05_15”

MODULE 4: CLOSE CORPORATIONS

Content Learning objectives Accommodate terminology changes according to IFRS for SMEs based on the latest Company Amendments Act 4.1 Close Corporations as an enterprise 4.2 Members’ contribution and members’

interest as per new Companies Act. 4.3 Financial statements of Close

Corporations

4.4 Disclosure items

Accommodate terminology changes according to IFRS for SMEs based on the latest Company Amendments Act 4.1 Distinguish a Close Corporation as an enterprise from other enterprises according to the new Companies Act as follows:

• Characteristics

• Advantages

• Disadvantages

4.2.1 Explain what membership contributions are and how these are made 4.2.2 Explain the compilation of members’ interest 4.3.1 Compile the following Statements of

a Close Corporation according to the latest Company Law Amendment Act based on IFRS for SMEs

• Statement of Comprehensive income

• Statement of financial position

• Statement of changes in equity 4.4 Separate the following disclosure items from the Financial statements of Close Corporations to indicate the total amounts at the beginning and the end of the financial year, as well as the movements during the financial year: comparative figures are not required.

• Contributions by members

• Retained income (profits)

• Revaluation of fixed assets

16

“Version 14_05_15”

Didactic guidelines With reference to learning objectives 4.1 to 4.3:

1. The content of Close Corporations is explained with a view to application in

practice.

2. Students are expected to compile the financial statements and disclosures of a Close Corporation in accordance with the latest Company Law Amendment Act, based on IFRS for SMEs, and in line with the latest terminology changes in the financial field. (See enclosed appendix).

Evaluation/Assessment With reference to learning objectives 4.1:

1. Theoretical information for embedded knowledge is not examinable in the

external examination

With reference to learning objectives 4.2 to 4.4:

2. Application questions are asked.

3. Questions are asked to determine whether students can correctly interpret the financial statements and identify and record the items which must be disclosed.

17

“Version 14_05_15”

FINANCIAL ACCOUNTING N6 MODULE 5: STATEMENT OF CASH FLOWS: CLOSE CORPORATIONS AND COMPANIES

Content Learning objectives 5.1 The objectives of a statement of cash

flows 5.2.1 Users of a cash flow statement:

• Entrepreneur/Owner

• Credit suppliers

• Cash flow planning

5.2.2 Useful definitions:

• Cash

• Cash equivalents

• Cash flows

• Operating activities

• Investing activities

• Financing activities

5.2.3 Advantages and disadvantages of Statement of Cash Flows

5.3 Descriptions and concepts

Students should be able to 5.1.1 Students must be able to

understand and explain the objectives of a cash flow statement

5.1.2 Students must understand how the

statement of cash flows will:

• Provide quality information to the user of the financial statements

• Identify the degree of risk

• Identify the company’s ability to generate profits and favourable cash flows in the future.

5.2.1 Mention the users of a statement of

cash flows and explain why they are interested in the statement of cash flows of an enterprise. The provision of cash flow information is primarily aimed at more effectively informing users about the liquidity and solvency of the entity.

5.2.2 Mention and explain the meaning of

each term to understand the content of the cash flow better.

5.2.3 Students must be able to mention

the advantages and disadvantages of the statement of cash flows

5.3 Describe the different cash flow items

and explain the most important

18

“Version 14_05_15”

The following concepts which will be used must be thoroughly explained:

• Operating activities

• Investing activities

• Financing activities

• Cash 5.4 Non-cash flow items 5.5 Procedures to be followed when

compiling a statement of cash flows (direct method)IAS 7 (AC118)

5.5.1 Cash flow from operating activities 5.5.2 Cash flow from investing activities 5.5.3 Cash flow from financing activities 5.6 Special items 5.6.1 Depreciation 5.6.2 Profit/loss on sale of assets/scrap-

ping of fixed assets

principles when compiling a statement of cash flows

5.4 Mention and explain in detail the

different non-cash flow items 5.5 Follow the correct procedure when

compiling a statement of cash flows and the note in respect of non-cash transactions pertaining to investing and financing activities of a company and close corporation according to the requirements of Standard IAS 7 (AC118) by utilising information which is mainly obtained from the other financial statements and any relevant notes thereto.

5.6 Explain special items with reference to

cash flow and record them in the statement of cash flows

Didactic guidelines 1. The themes of this module must be explained with a view to application in practice.

2. Students must be able to draw up a cash flow statement of a Close Corporation or

a Company. (See the enclosed appendix). Evaluation/Assessment 1. Application questions are asked.

2. Questions are asked to determine whether the students’ interpretation of the

statement of cash flows and items to be disclosed is correct.

19

“Version 14_05_15”

FINANCIAL ACCOUNTING N6 MODULE 6: AUDITING

Content Learning objectives Introduction 6.1 Internal Auditing 6.1.1 Define internal auditing 6.1.2 Objectives of internal auditing 6.1.3 The internal audit process 6.1.3.1 Internal Control 6.1.3.2 Risks 6.2 External Auditing 6.2.1 Define external auditing 6.2.2 Objectives of external auditing 6.3 Difference between internal and external auditing 6.4 Audit evidence 6.4.1 Compliance procedures 6.4.2 Substantive procedures 6.5 Audit reports 6.5.1 Internal audit reports

Students should be able to 6.1.1 Give a definition of the term internal

auditing 6.1.2 Describe the objectives of internal

auditing 6.1.3 Describe what is meant by the

internal audit process, internal control and name the risks involved in this

6.2.1 Give a definition of the term external

auditing 6.2.2 Describe the objectives of external

auditing 6.3 Give five points of difference between

internal and external auditing 6.4.1 Describe what is meant by

compliance procedures and how to gather this evidence

6.4.2 Describe what is meant by

substantive procedures and how to gather this evidence

6.5.1& 6.5.2 Describe the difference

20

“Version 14_05_15”

6.5.2 External audit reports 6.5.2.1 Qualified opinion 6.5.2.2 Unqualified opinion 6.5.2.3 Withholding of an opinion

between the internal audit and external audit reports

6.5.2.1 Describe what is meant by a

qualified opinion 6.5.2.2 Describe what is meant by an

unqualified opinion 6.5.2.3 Describe what is meant by the

withholding of an opinion

Didactic guidelines

1. The contents of this module should be discussed with a view to application in practice.

2. Students should be introduced to internal auditing procedures as applied in practice. Further knowledge in this regard can be obtained by inviting experts to talk to students as well as arranging visits to or from auditing firms.

Evaluation/Assessment 1. Theoretical and simple application questions could be asked – only short questions.

Not more than 10 marks per question.

21

“Version 14_05_15”

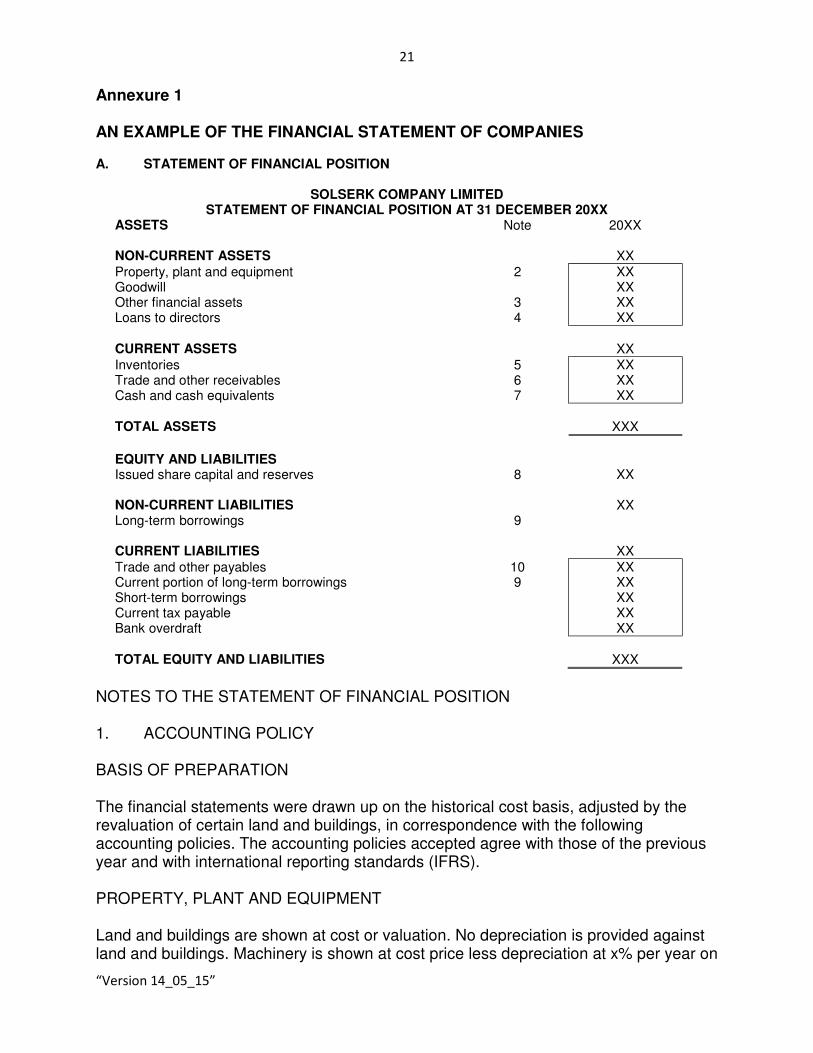

Annexure 1 AN EXAMPLE OF THE FINANCIAL STATEMENT OF COMPANIES A. STATEMENT OF FINANCIAL POSITION

SOLSERK COMPANY LIMITED STATEMENT OF FINANCIAL POSITION AT 31 DECEMBER 20XX

ASSETS NON-CURRENT ASSETS

Note 20XX

XX

Property, plant and equipment Goodwill Other financial assets Loans to directors

2 3 4

XX XX XX XX

CURRENT ASSETS

XX

Inventories Trade and other receivables Cash and cash equivalents

5 6 7

XX XX XX

TOTAL ASSETS

XXX

EQUITY AND LIABILITIES Issued share capital and reserves

8

XX NON-CURRENT LIABILITIES Long-term borrowings

9

XX

CURRENT LIABILITIES

XX

Trade and other payables Current portion of long-term borrowings Short-term borrowings Current tax payable Bank overdraft

10 9

XX XX XX XX XX

TOTAL EQUITY AND LIABILITIES

XXX

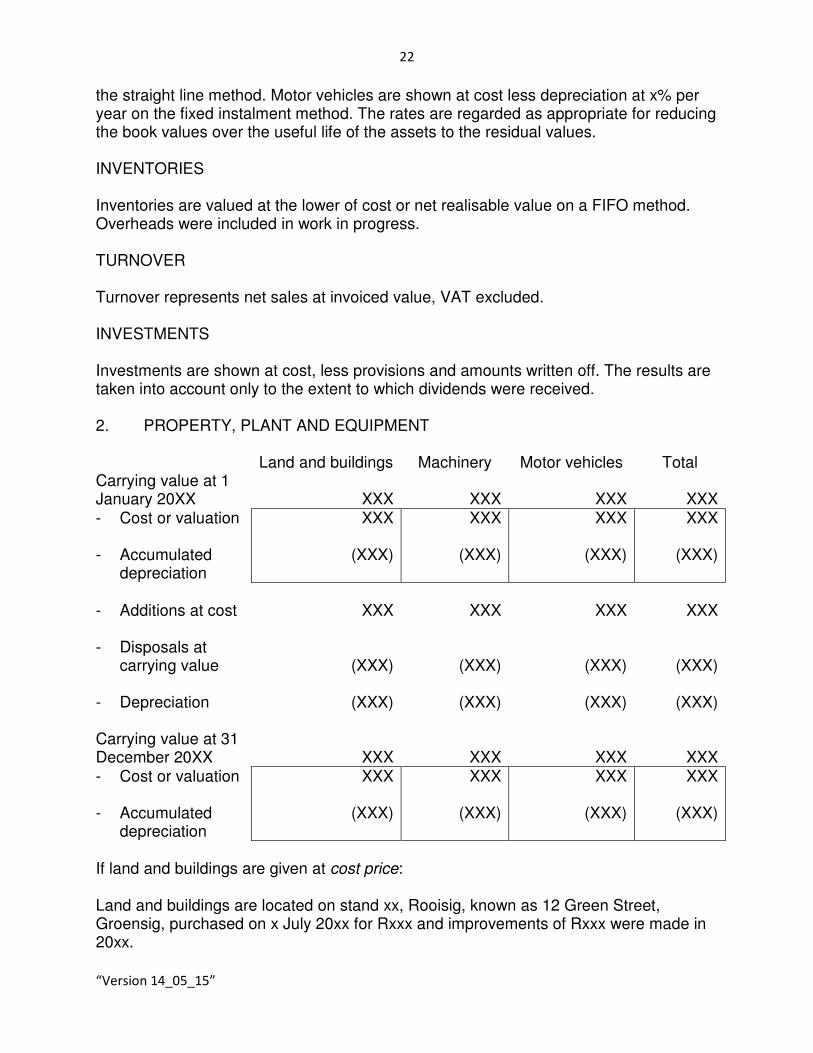

NOTES TO THE STATEMENT OF FINANCIAL POSITION 1. ACCOUNTING POLICY BASIS OF PREPARATION The financial statements were drawn up on the historical cost basis, adjusted by the revaluation of certain land and buildings, in correspondence with the following accounting policies. The accounting policies accepted agree with those of the previous year and with international reporting standards (IFRS). PROPERTY, PLANT AND EQUIPMENT Land and buildings are shown at cost or valuation. No depreciation is provided against land and buildings. Machinery is shown at cost price less depreciation at x% per year on

22

“Version 14_05_15”

the straight line method. Motor vehicles are shown at cost less depreciation at x% per year on the fixed instalment method. The rates are regarded as appropriate for reducing the book values over the useful life of the assets to the residual values. INVENTORIES Inventories are valued at the lower of cost or net realisable value on a FIFO method. Overheads were included in work in progress. TURNOVER Turnover represents net sales at invoiced value, VAT excluded. INVESTMENTS Investments are shown at cost, less provisions and amounts written off. The results are taken into account only to the extent to which dividends were received. 2. PROPERTY, PLANT AND EQUIPMENT Land and buildings Machinery Motor vehicles Total Carrying value at 1 January 20XX

XXX

XXX

XXX

XXX

- Cost or valuation

- Accumulated depreciation

XXX

(XXX)

XXX

(XXX)

XXX

(XXX)

XXX

(XXX)

- Additions at cost

- Disposals at

carrying value

- Depreciation

XXX

(XXX)

(XXX)

XXX

(XXX)

(XXX)

XXX

(XXX)

(XXX)

XXX

(XXX)

(XXX)

Carrying value at 31 December 20XX

XXX

XXX

XXX

XXX

- Cost or valuation

- Accumulated depreciation

XXX

(XXX)

XXX

(XXX)

XXX

(XXX)

XXX

(XXX)

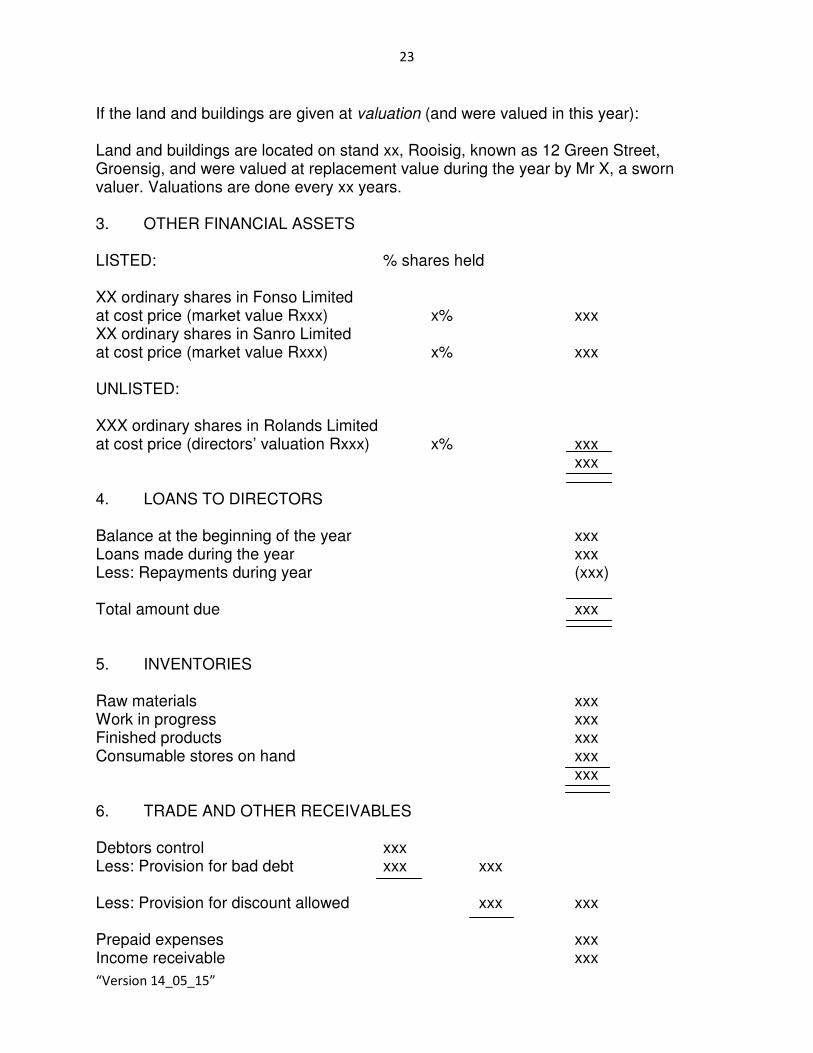

If land and buildings are given at cost price: Land and buildings are located on stand xx, Rooisig, known as 12 Green Street, Groensig, purchased on x July 20xx for Rxxx and improvements of Rxxx were made in 20xx.

23

“Version 14_05_15”

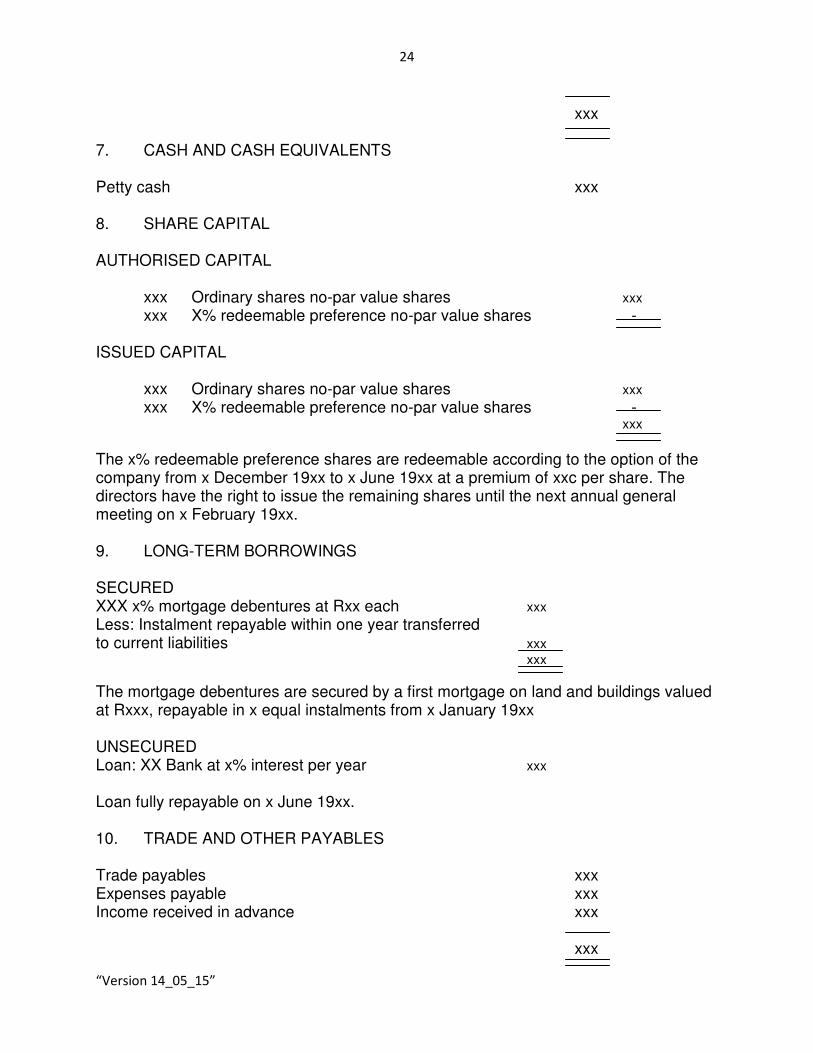

If the land and buildings are given at valuation (and were valued in this year): Land and buildings are located on stand xx, Rooisig, known as 12 Green Street, Groensig, and were valued at replacement value during the year by Mr X, a sworn valuer. Valuations are done every xx years. 3. OTHER FINANCIAL ASSETS LISTED: % shares held XX ordinary shares in Fonso Limited at cost price (market value Rxxx) x% xxx XX ordinary shares in Sanro Limited at cost price (market value Rxxx) x% xxx UNLISTED: XXX ordinary shares in Rolands Limited at cost price (directors’ valuation Rxxx) x% xxx xxx 4. LOANS TO DIRECTORS Balance at the beginning of the year xxx Loans made during the year xxx Less: Repayments during year (xxx) Total amount due xxx 5. INVENTORIES Raw materials xxx Work in progress xxx Finished products xxx Consumable stores on hand xxx xxx 6. TRADE AND OTHER RECEIVABLES Debtors control xxx Less: Provision for bad debt xxx xxx Less: Provision for discount allowed xxx xxx Prepaid expenses xxx Income receivable xxx

24

“Version 14_05_15”

xxx 7. CASH AND CASH EQUIVALENTS Petty cash xxx 8. SHARE CAPITAL AUTHORISED CAPITAL xxx Ordinary shares no-par value shares xxx

xxx X% redeemable preference no-par value shares - ISSUED CAPITAL xxx Ordinary shares no-par value shares xxx

xxx X% redeemable preference no-par value shares - xxx

The x% redeemable preference shares are redeemable according to the option of the company from x December 19xx to x June 19xx at a premium of xxc per share. The directors have the right to issue the remaining shares until the next annual general meeting on x February 19xx. 9. LONG-TERM BORROWINGS SECURED XXX x% mortgage debentures at Rxx each xxx Less: Instalment repayable within one year transferred to current liabilities xxx

xxx

The mortgage debentures are secured by a first mortgage on land and buildings valued at Rxxx, repayable in x equal instalments from x January 19xx UNSECURED Loan: XX Bank at x% interest per year xxx

Loan fully repayable on x June 19xx. 10. TRADE AND OTHER PAYABLES Trade payables xxx Expenses payable xxx Income received in advance xxx xxx

25

“Version 14_05_15”

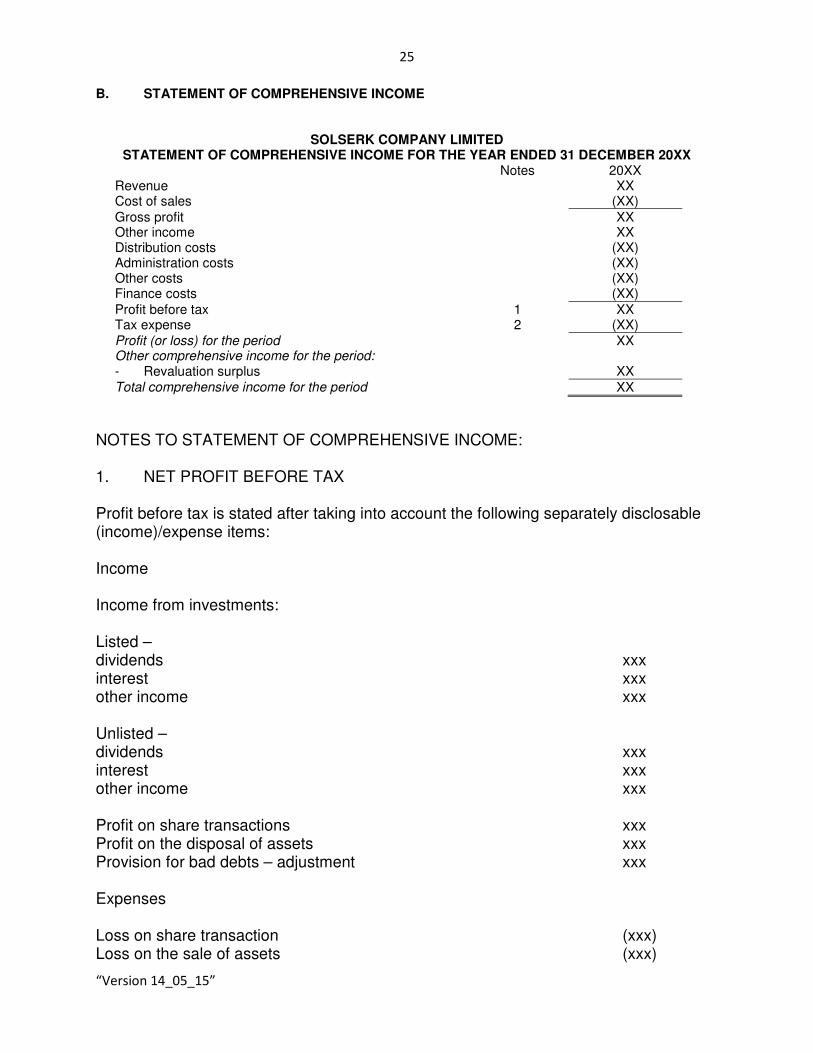

B. STATEMENT OF COMPREHENSIVE INCOME

SOLSERK COMPANY LIMITED

STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 20XX Revenue Cost of sales

Notes 20XX XX

(XX)

Gross profit Other income Distribution costs Administration costs Other costs Finance costs

XX XX

(XX) (XX) (XX) (XX)

Profit before tax Tax expense

1 2

XX (XX)

Profit (or loss) for the period Other comprehensive income for the period: - Revaluation surplus

XX

XX Total comprehensive income for the period XX

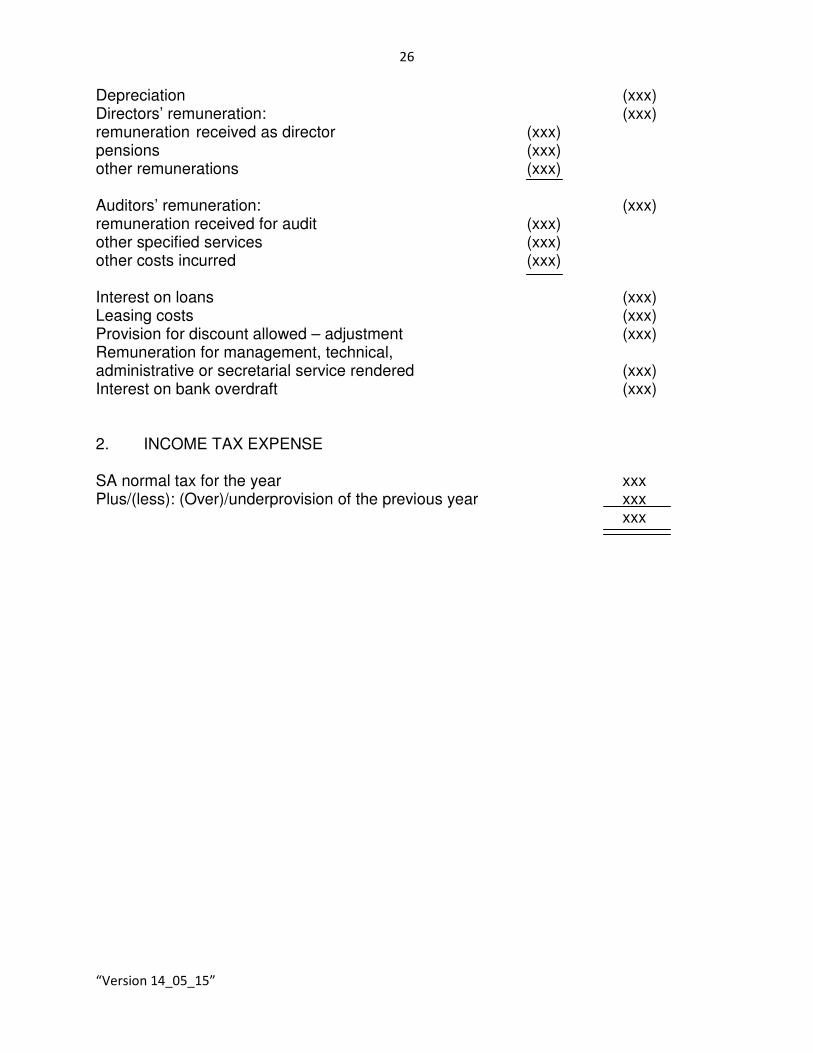

NOTES TO STATEMENT OF COMPREHENSIVE INCOME: 1. NET PROFIT BEFORE TAX Profit before tax is stated after taking into account the following separately disclosable (income)/expense items: Income Income from investments: Listed – dividends xxx interest xxx other income xxx Unlisted – dividends xxx interest xxx other income xxx Profit on share transactions xxx Profit on the disposal of assets xxx Provision for bad debts – adjustment xxx Expenses Loss on share transaction (xxx) Loss on the sale of assets (xxx)

26

“Version 14_05_15”

Depreciation (xxx) Directors’ remuneration: (xxx) remuneration received as director (xxx) pensions (xxx) other remunerations (xxx) Auditors’ remuneration: (xxx) remuneration received for audit (xxx) other specified services (xxx) other costs incurred (xxx) Interest on loans (xxx) Leasing costs (xxx) Provision for discount allowed – adjustment (xxx) Remuneration for management, technical, administrative or secretarial service rendered (xxx) Interest on bank overdraft (xxx) 2. INCOME TAX EXPENSE SA normal tax for the year xxx Plus/(less): (Over)/underprovision of the previous year xxx xxx

27

“Version 14_05_15”

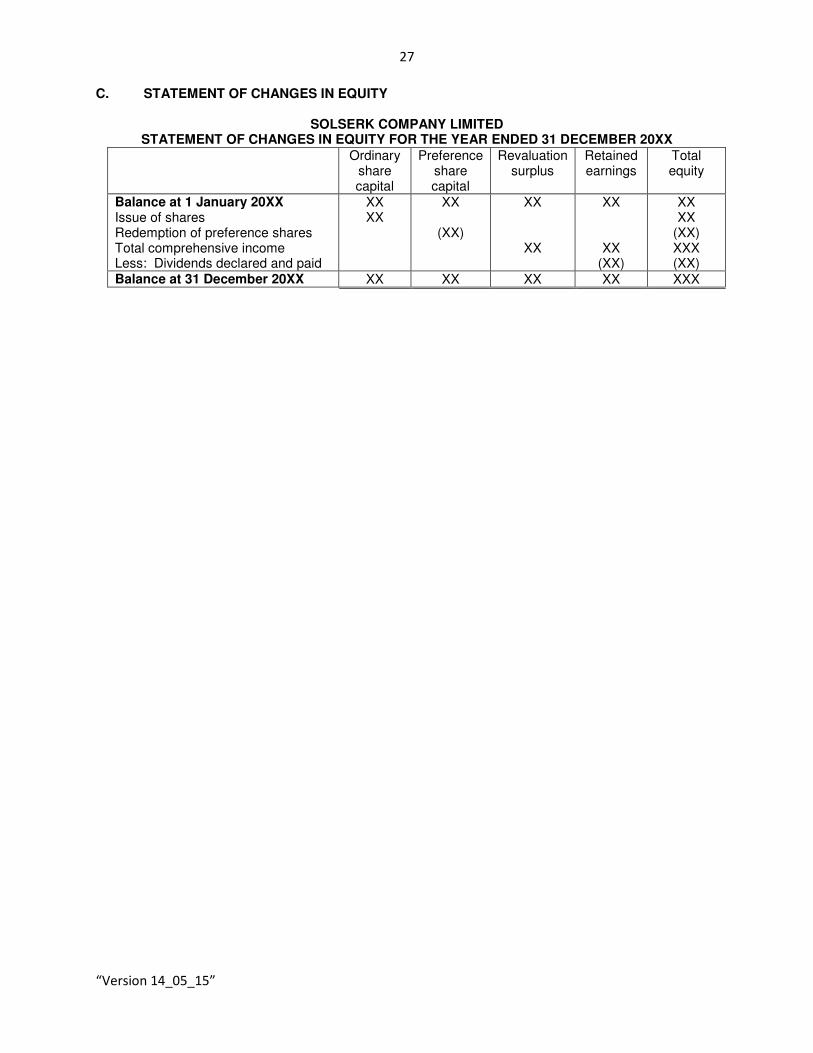

C. STATEMENT OF CHANGES IN EQUITY

SOLSERK COMPANY LIMITED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 20XX

Ordinary share capital

Preference share capital

Revaluation surplus

Retained earnings

Total equity

Balance at 1 January 20XX Issue of shares Redemption of preference shares Total comprehensive income Less: Dividends declared and paid

XX XX

XX

(XX)

XX

XX

XX

XX (XX)

XX XX

(XX) XXX (XX)

Balance at 31 December 20XX XX XX XX XX XXX

28

“Version 14_05_15”

ANNEXURE 2

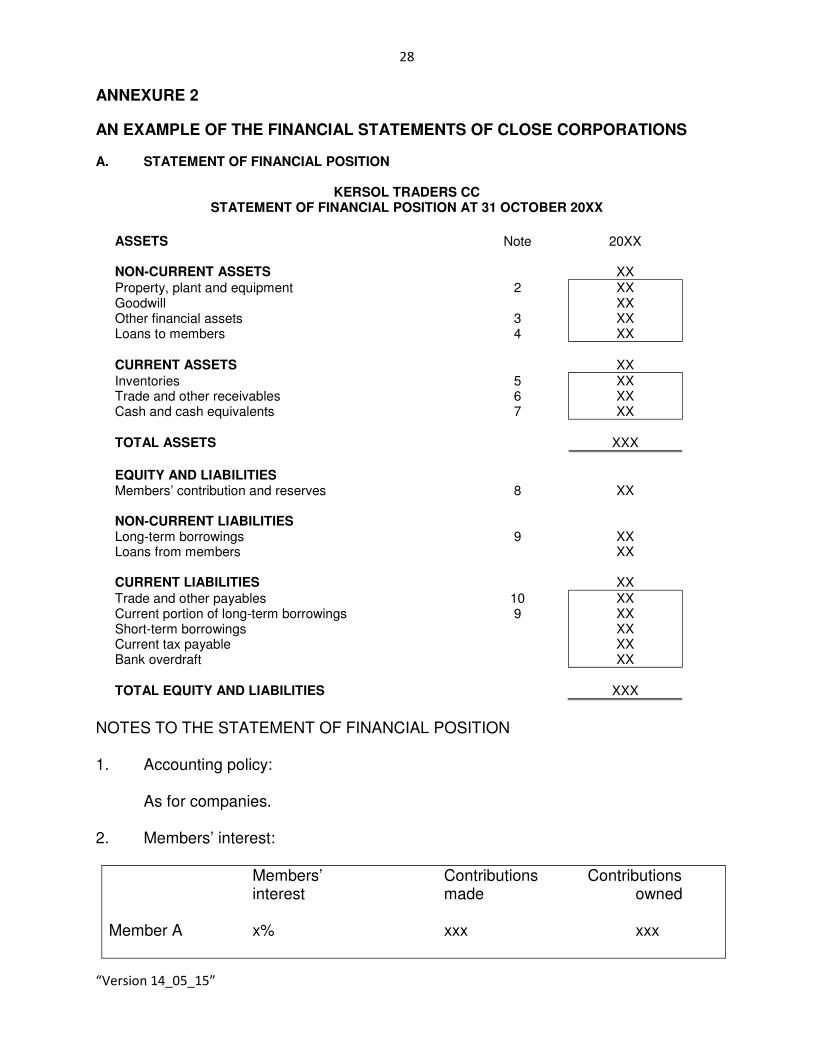

AN EXAMPLE OF THE FINANCIAL STATEMENTS OF CLOSE CORPORATIONS A. STATEMENT OF FINANCIAL POSITION

KERSOL TRADERS CC STATEMENT OF FINANCIAL POSITION AT 31 OCTOBER 20XX

ASSETS NON-CURRENT ASSETS

Note 20XX

XX

Property, plant and equipment Goodwill Other financial assets Loans to members

2 3 4

XX XX XX XX

CURRENT ASSETS

XX

Inventories Trade and other receivables Cash and cash equivalents

5 6 7

XX XX XX

TOTAL ASSETS

XXX

EQUITY AND LIABILITIES Members’ contribution and reserves

8

XX NON-CURRENT LIABILITIES Long-term borrowings Loans from members

9

XX XX

CURRENT LIABILITIES

XX

Trade and other payables Current portion of long-term borrowings Short-term borrowings Current tax payable Bank overdraft

10 9

XX XX XX XX XX

TOTAL EQUITY AND LIABILITIES

XXX

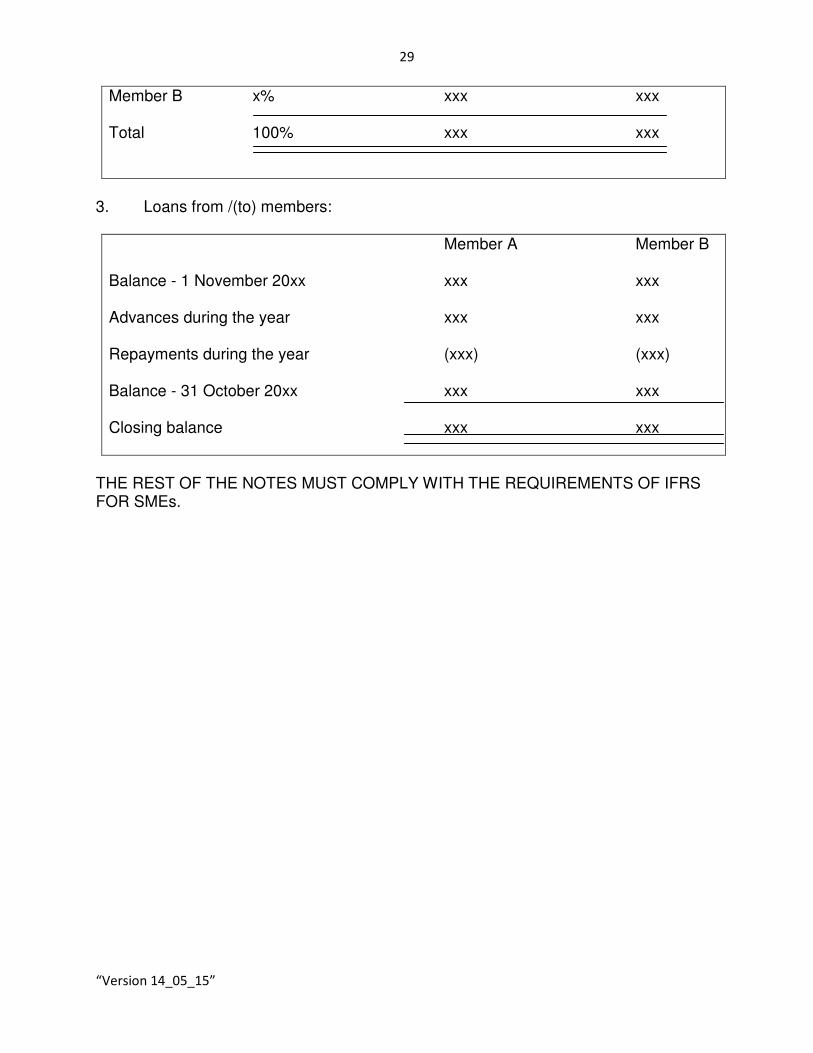

NOTES TO THE STATEMENT OF FINANCIAL POSITION 1. Accounting policy: As for companies. 2. Members’ interest:

Members’ Contributions Contributions interest made owned Member A x% xxx xxx

29

“Version 14_05_15”

Member B x% xxx xxx Total 100% xxx xxx

3. Loans from /(to) members:

Member A Member B Balance - 1 November 20xx xxx xxx Advances during the year xxx xxx Repayments during the year (xxx) (xxx) Balance - 31 October 20xx xxx xxx Closing balance xxx xxx

THE REST OF THE NOTES MUST COMPLY WITH THE REQUIREMENTS OF IFRS FOR SMEs.

30

“Version 14_05_15”

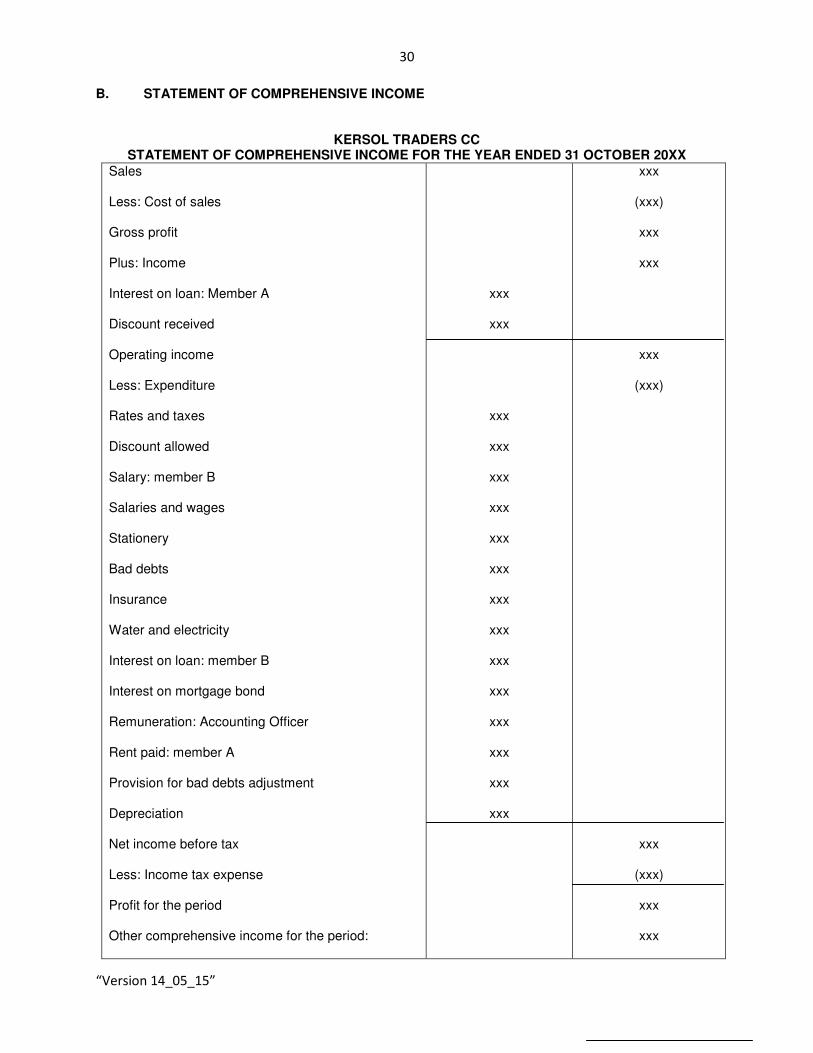

B. STATEMENT OF COMPREHENSIVE INCOME

KERSOL TRADERS CC

STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 OCTOBER 20XX

Sales Less: Cost of sales Gross profit Plus: Income Interest on loan: Member A Discount received Operating income Less: Expenditure Rates and taxes Discount allowed Salary: member B Salaries and wages Stationery Bad debts Insurance Water and electricity Interest on loan: member B Interest on mortgage bond Remuneration: Accounting Officer Rent paid: member A Provision for bad debts adjustment Depreciation Net income before tax Less: Income tax expense Profit for the period Other comprehensive income for the period:

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

(xxx)

xxx

xxx

xxx

(xxx)

xxx

(xxx)

xxx

xxx

31

“Version 14_05_15”

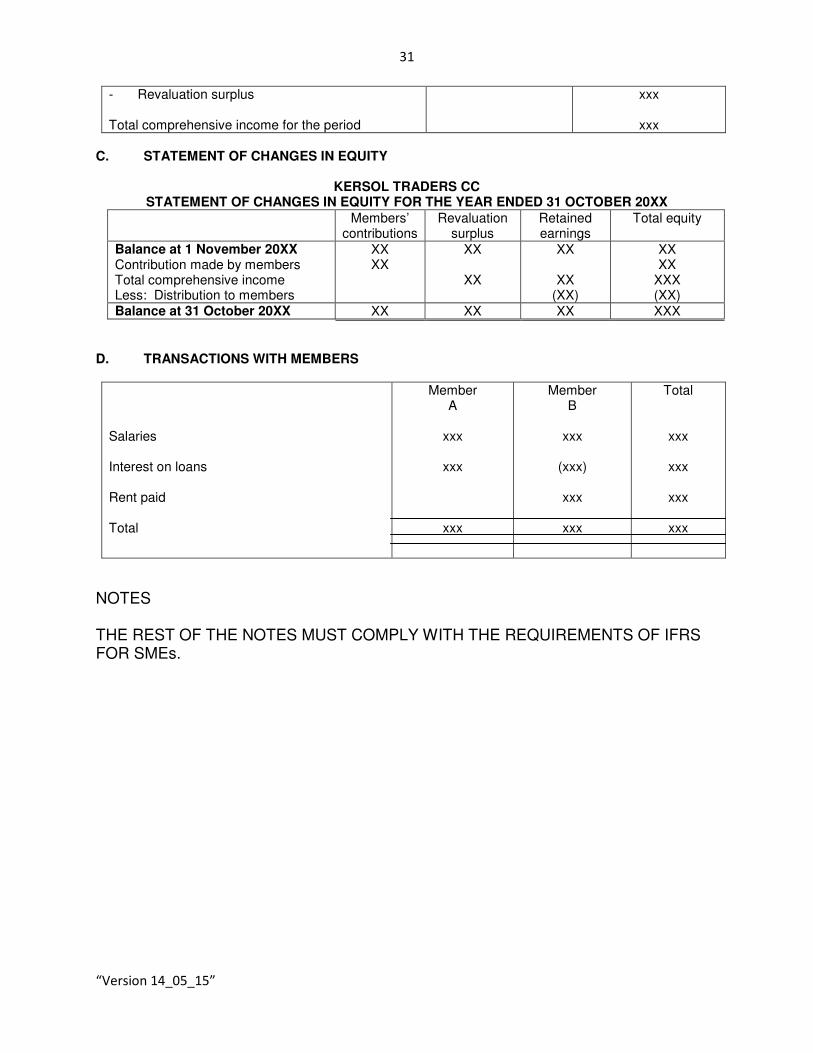

- Revaluation surplus Total comprehensive income for the period

xxx

xxx C. STATEMENT OF CHANGES IN EQUITY

KERSOL TRADERS CC STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 OCTOBER 20XX

Members’ contributions

Revaluation surplus

Retained earnings

Total equity

Balance at 1 November 20XX Contribution made by members Total comprehensive income Less: Distribution to members

XX XX

XX

XX

XX

XX (XX)

XX XX

XXX (XX)

Balance at 31 October 20XX XX XX XX XXX

D. TRANSACTIONS WITH MEMBERS

Salaries Interest on loans Rent paid Total

Member A

xxx

xxx

xxx

Member B

xxx

(xxx)

xxx

xxx

Total

xxx

xxx

xxx

xxx

NOTES THE REST OF THE NOTES MUST COMPLY WITH THE REQUIREMENTS OF IFRS FOR SMEs.

32

“Version 14_05_15”

ANNEXURE 3

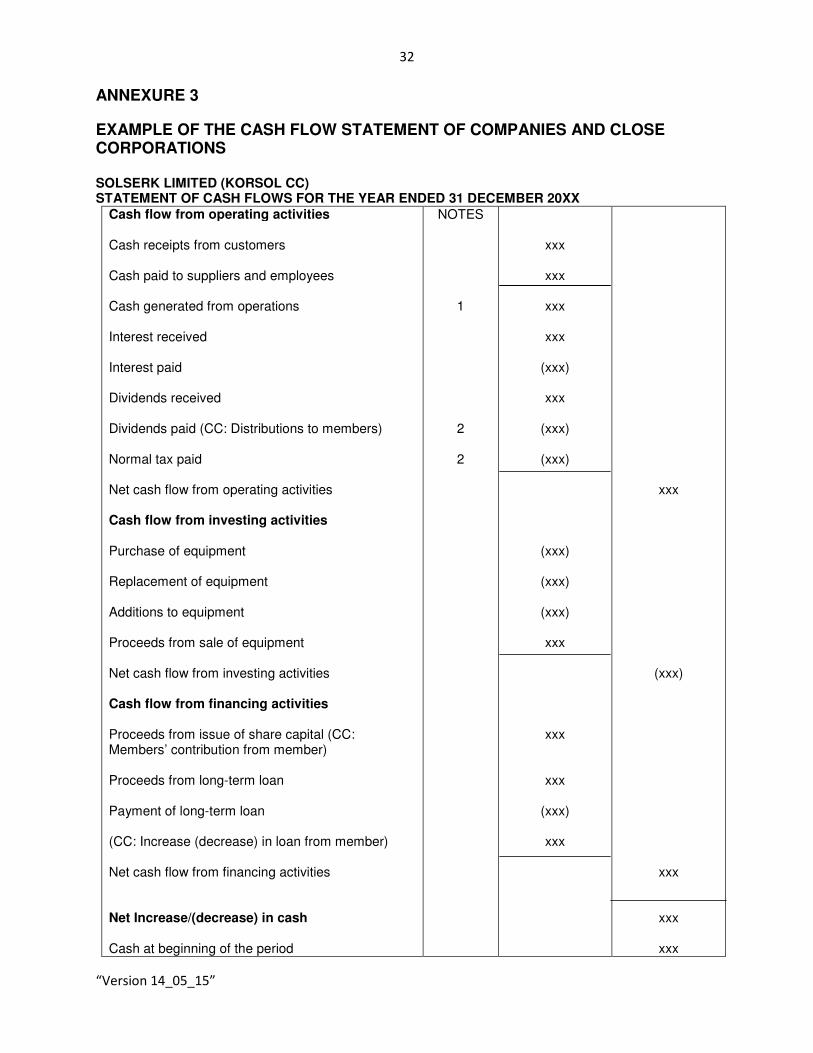

EXAMPLE OF THE CASH FLOW STATEMENT OF COMPANIES AND CLOSE CORPORATIONS SOLSERK LIMITED (KORSOL CC) STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 DECEMBER 20XX

Cash flow from operating activities Cash receipts from customers Cash paid to suppliers and employees Cash generated from operations Interest received Interest paid Dividends received Dividends paid (CC: Distributions to members) Normal tax paid Net cash flow from operating activities Cash flow from investing activities Purchase of equipment Replacement of equipment Additions to equipment Proceeds from sale of equipment Net cash flow from investing activities Cash flow from financing activities Proceeds from issue of share capital (CC: Members’ contribution from member) Proceeds from long-term loan Payment of long-term loan (CC: Increase (decrease) in loan from member) Net cash flow from financing activities Net Increase/(decrease) in cash Cash at beginning of the period

NOTES 1 2 2

xxx

xxx

xxx

xxx

(xxx)

xxx

(xxx)

(xxx)

(xxx)

(xxx)

(xxx)

xxx

xxx

xxx

(xxx)

xxx

xxx

(xxx)

xxx

xxx

xxx

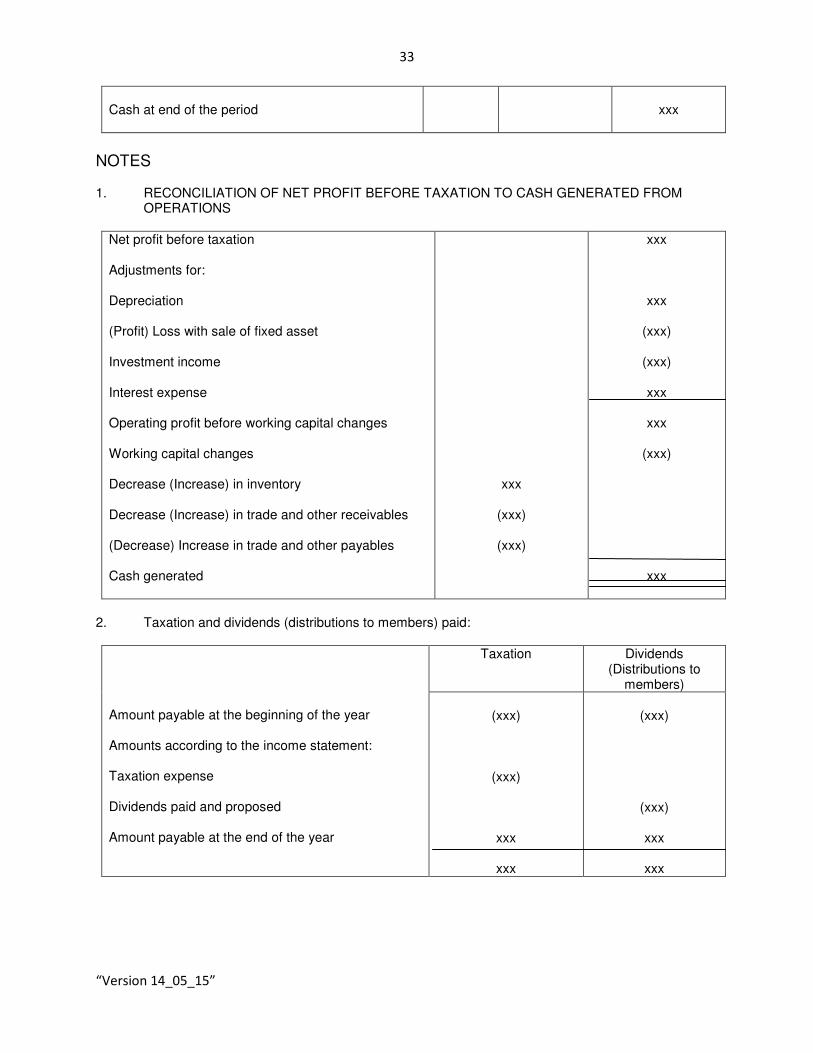

33

“Version 14_05_15”

Cash at end of the period

xxx

NOTES 1. RECONCILIATION OF NET PROFIT BEFORE TAXATION TO CASH GENERATED FROM

OPERATIONS

Net profit before taxation Adjustments for: Depreciation (Profit) Loss with sale of fixed asset Investment income Interest expense Operating profit before working capital changes Working capital changes Decrease (Increase) in inventory Decrease (Increase) in trade and other receivables (Decrease) Increase in trade and other payables Cash generated

xxx

(xxx)

(xxx)

xxx

xxx

(xxx)

(xxx)

xxx

xxx

(xxx)

xxx

2. Taxation and dividends (distributions to members) paid:

Amount payable at the beginning of the year Amounts according to the income statement: Taxation expense Dividends paid and proposed Amount payable at the end of the year

Taxation Dividends (Distributions to

members)

(xxx)

(xxx)

xxx

xxx

(xxx)

(xxx)

xxx

xxx