Embed Size (px)

Citation preview

Heading Futures

Fáilte Ireland Futures

Key Tourism & Travel Trends

Orla Canavan

for Dublin Breakfast Briefing

Flat Screen TVs

Video Conference

Technology

Biometric

Identification

3D

Holographic

Displays

Drones

Agenda

Context – Why are trends important

Contextual Trends

Global Growth in Tourism

Ageing & Ageless Society

Generations – Millennials and Gen Z

Globalisation

Behavioural Trends

Experience society

Mobile living

Networked Society & Culture of recognition

No one wants to be these guys……

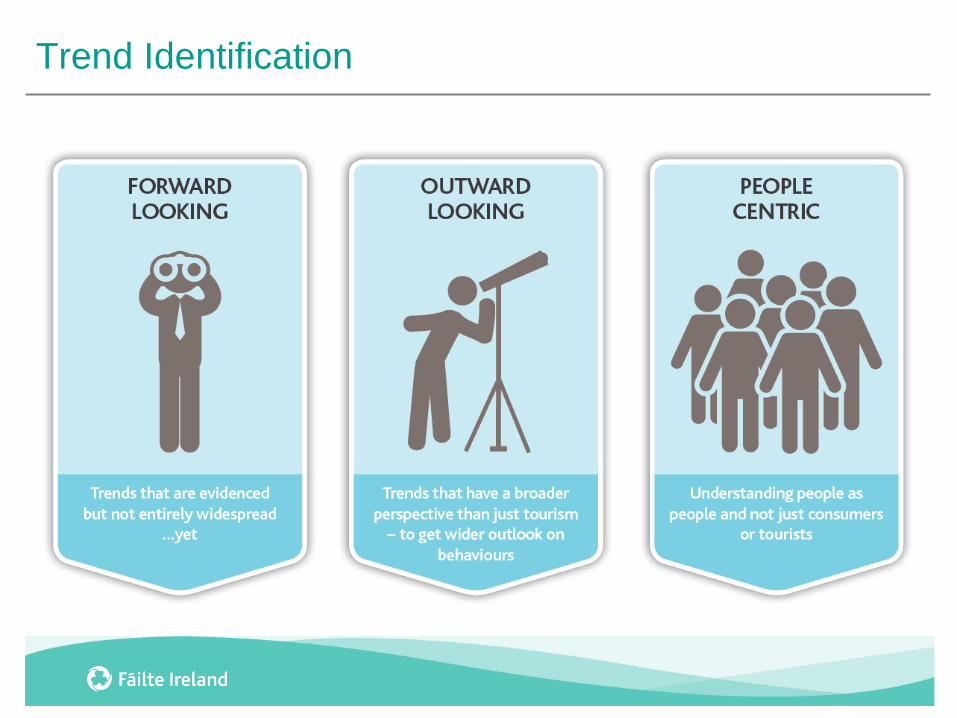

Context – More Consumer Focus

Consumer Research highlighted Ireland as a

destination was not best in class in terms of

iconic experiences

Perceived as one region’ by many visitors

Wild Atlantic Way

2,500 km route along the

Atlantic coast, from Malin Head

to Kinsale.

Dublin

Deliver on Dublin's potential –

from party perception to dialling

up the coast, mountains and

outdoor opportunities

Ireland’s Ancient East

Discovery of 5,000 years of

Europe’s diverse & ancient

history, older than the Pyramids

and set in a natural lush green

landscape

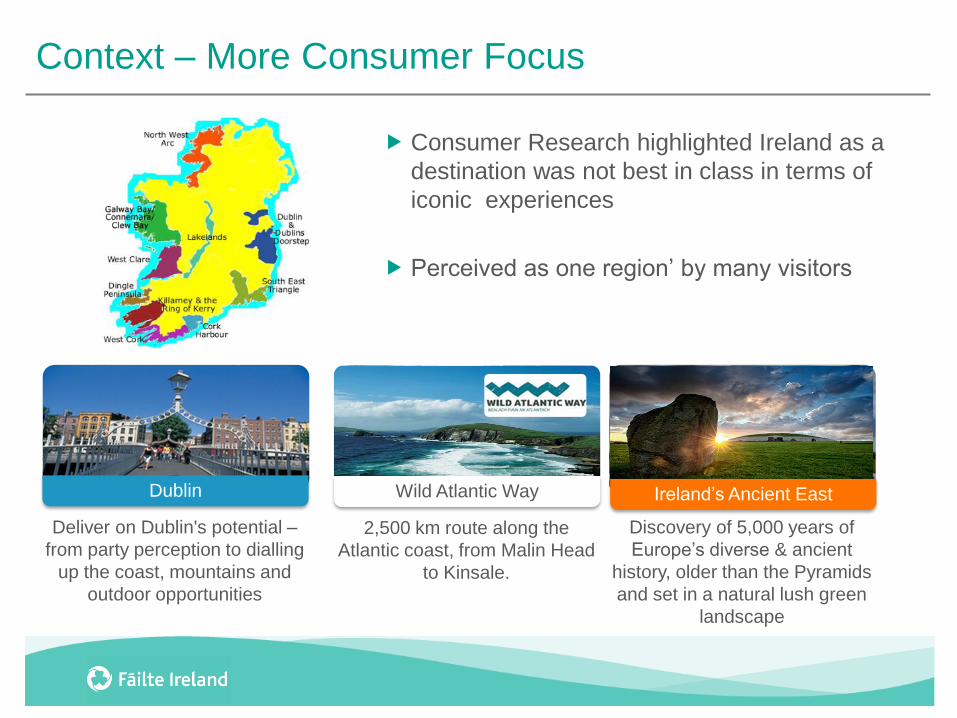

Global Segmentation Model

Priority Segments

Social Energiser Busy

Looking for excitement

New experiences and fun

Social holiday somewhere different

At the ‘in’ places to shop, cool places to eat, best sightseeing opportunities

Stay close to the action

Culturally Curious Culture

Independent 'active sightseers'

Broaden their mind

Explore landscapes, history and culture

Immerse in local experiences

Stay somewhere there’s lot to see

Great Escapers Together

Take ‘time out’

Spend quality time with loved ones

Enjoy experiences / activities off the beaten track

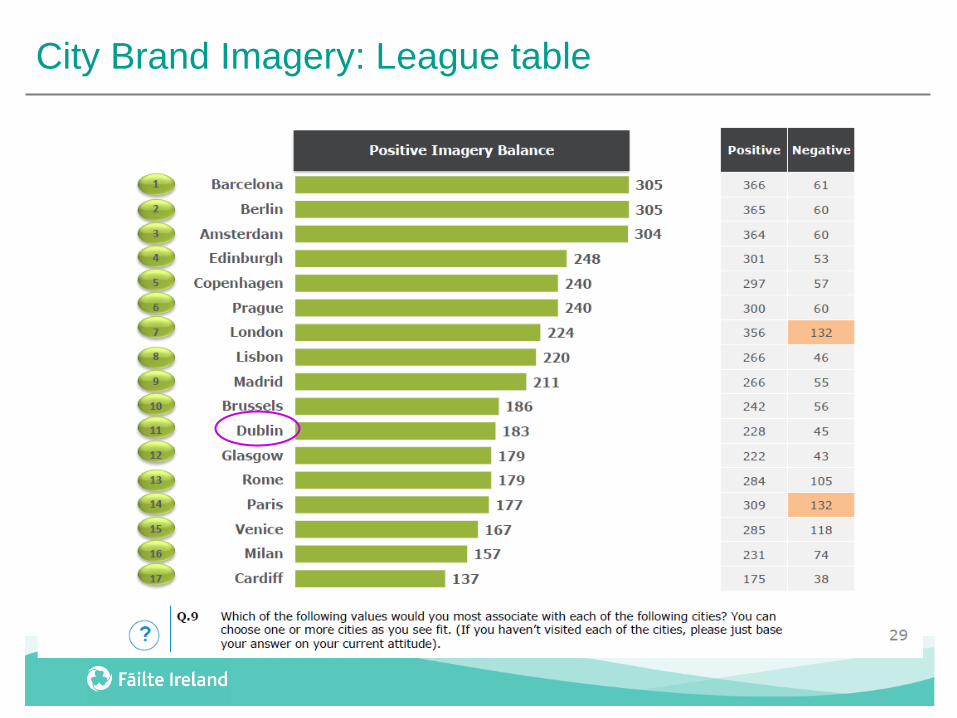

City Brand Imagery: League table

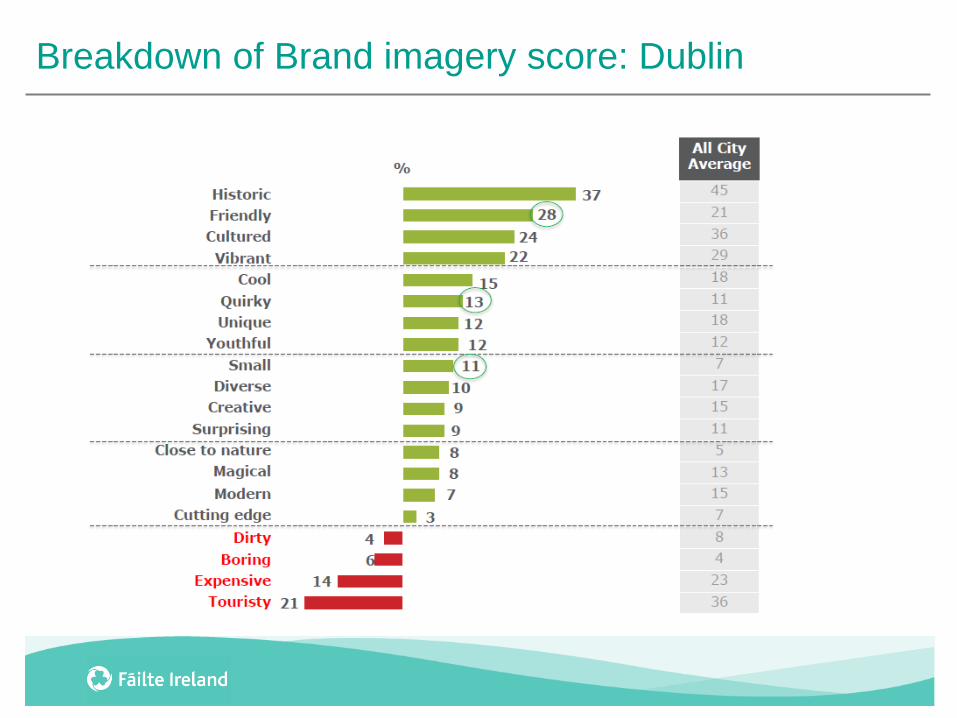

Breakdown of Brand imagery score: Dublin

Rationale for Future Looking

Capture market opportunities

Basis for innovation process

Better decision making for strategic management

Everett Rogers 1962

By focusing on Innovators and Early

Adopters, it’s possible to anticipate Early

Majority and Late Majority tastes

Consider………

Trend content is everywhere - How can we apply the trend to travel, tourism and hospitality industry?

What competitive advantage is to be gained

Local context is important, but aspiration is global

Consumer don’t live inside industry silos. Neither should we

TRENDS

What is a Trend?

A trend is an empirically observable movement

or tendency within prevailing socio-economic

conditions which results in a (potentially

sustainable) alteration of expectation, decision

or behaviour on the part of a significant number

of citizens and/or institutions

“

”

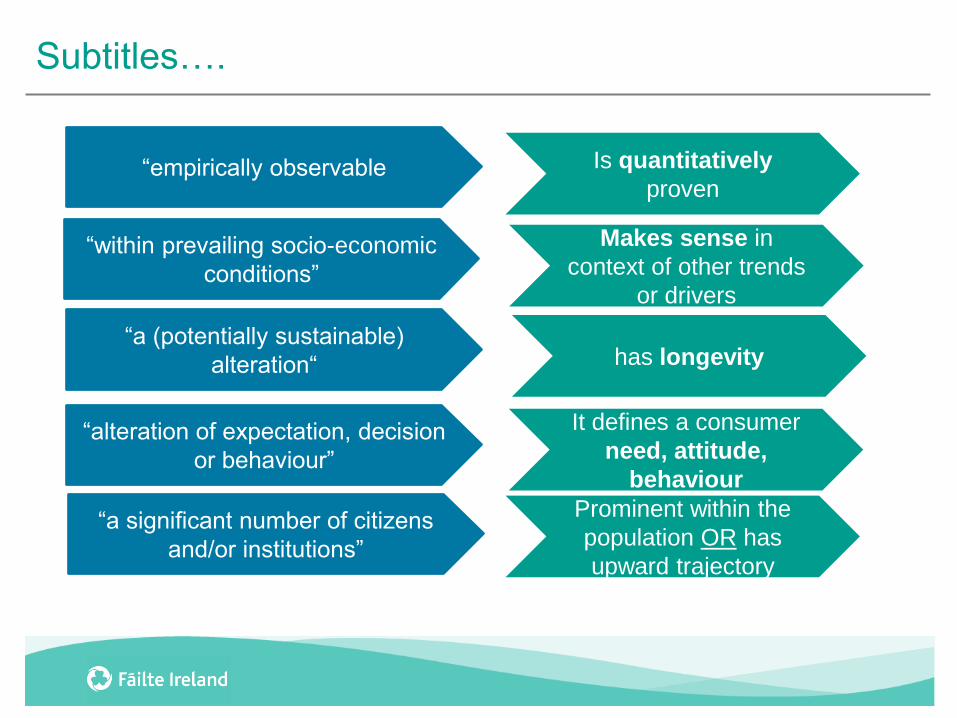

Subtitles….

“empirically observable

“within prevailing socio-economic

conditions”

“a (potentially sustainable)

alteration“

“alteration of expectation, decision

or behaviour”

“a significant number of citizens

and/or institutions”

Is quantitatively

proven

Makes sense in

context of other trends

or drivers

has longevity

It defines a consumer

need, attitude,

behaviour

Prominent within the

population OR has

upward trajectory

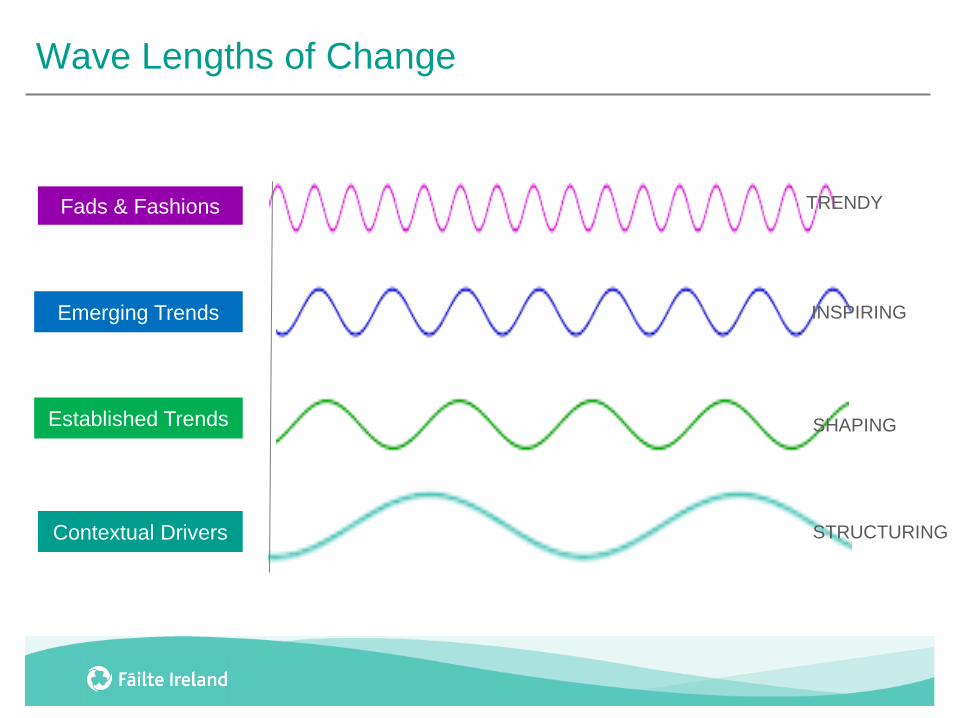

Wave Lengths of Change

Contextual Drivers

Established Trends

Emerging Trends

Fads & Fashions TRENDY

INSPIRING

SHAPING

STRUCTURING

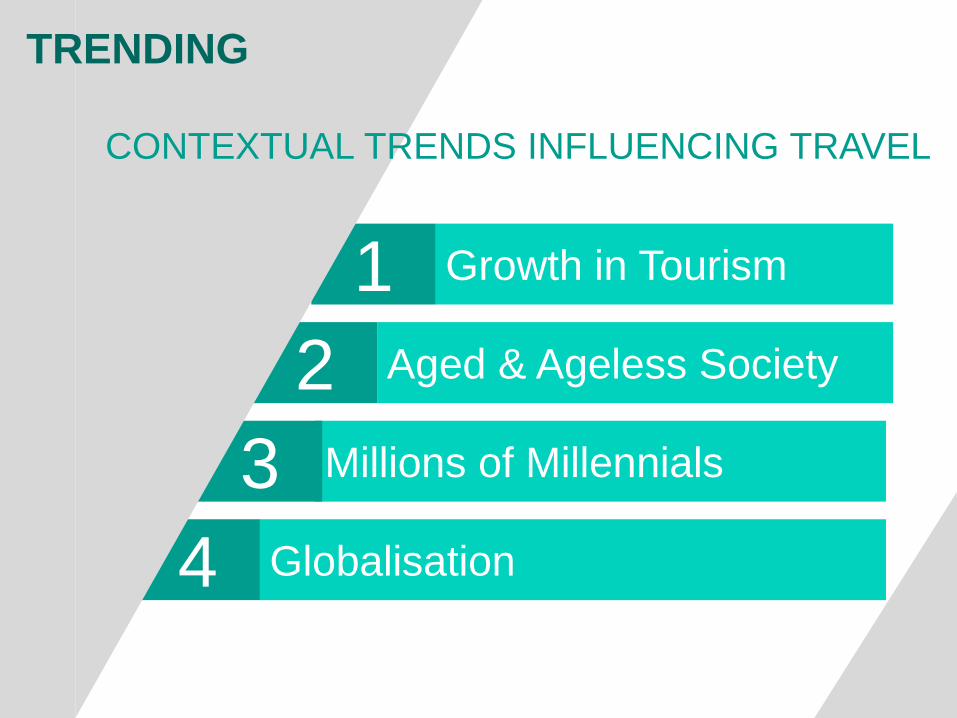

Growth in Tourism 1

Aged & Ageless Society 2

Millions of Millennials 3

Globalisation 4

TRENDING

CONTEXTUAL TRENDS INFLUENCING TRAVEL

19

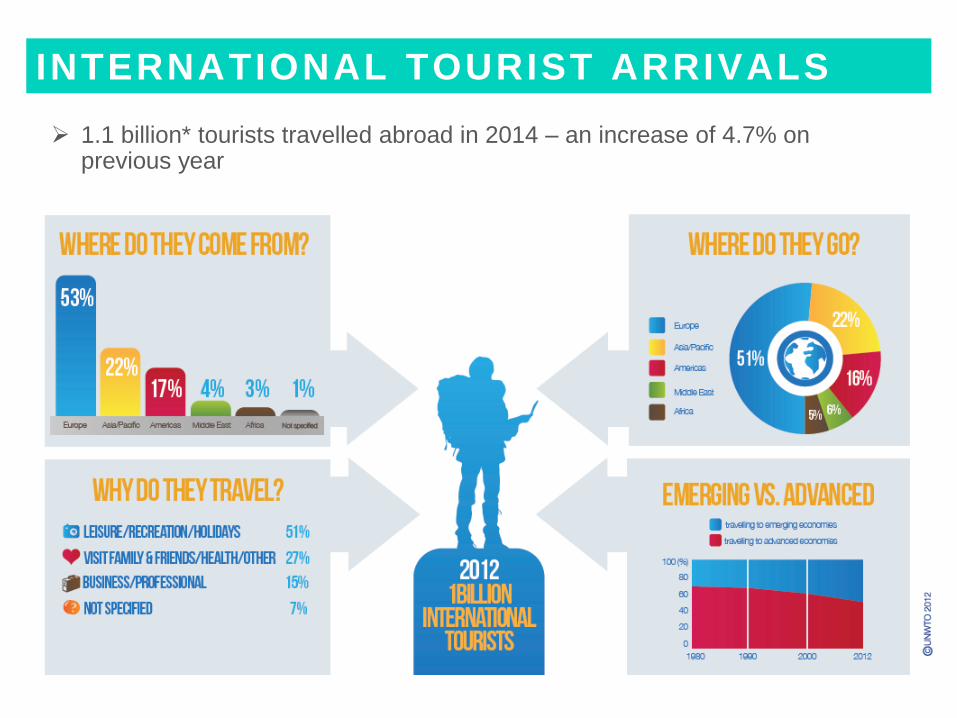

GLOBAL GROWTH IN TOURISM

1.1 billion* tourists travelled abroad in 2014 – an increase of 4.7% on previous year

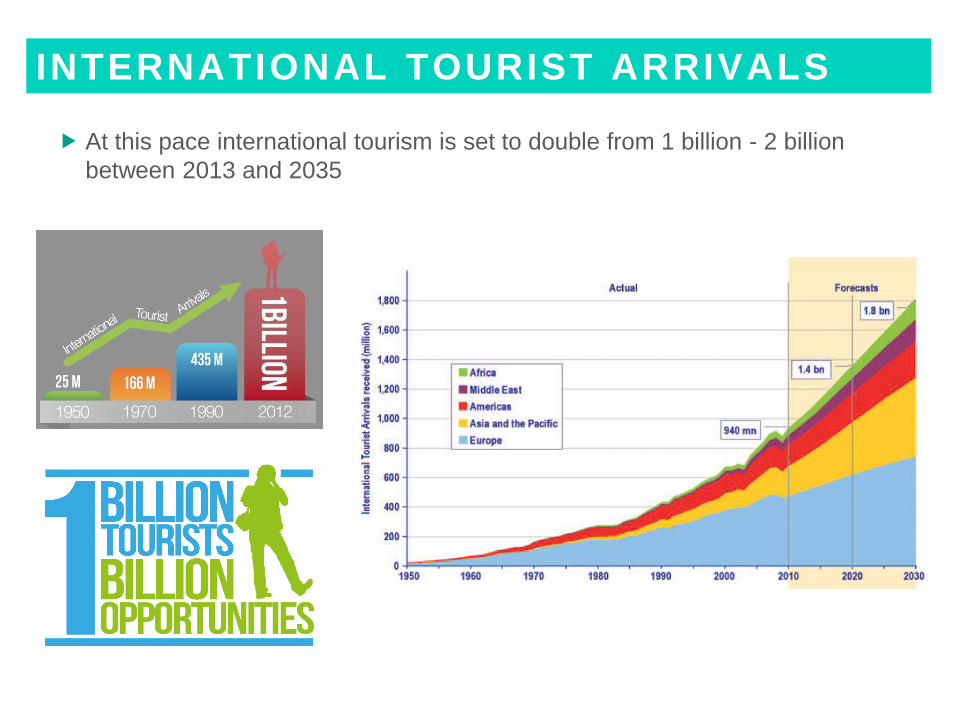

INTERNATIONAL TOURIST ARRIVALS

At this pace international tourism is set to double from 1 billion - 2 billion

between 2013 and 2035

* UNWTO World Tourism Barometer

INTERNATIONAL TOURIST ARRIVALS

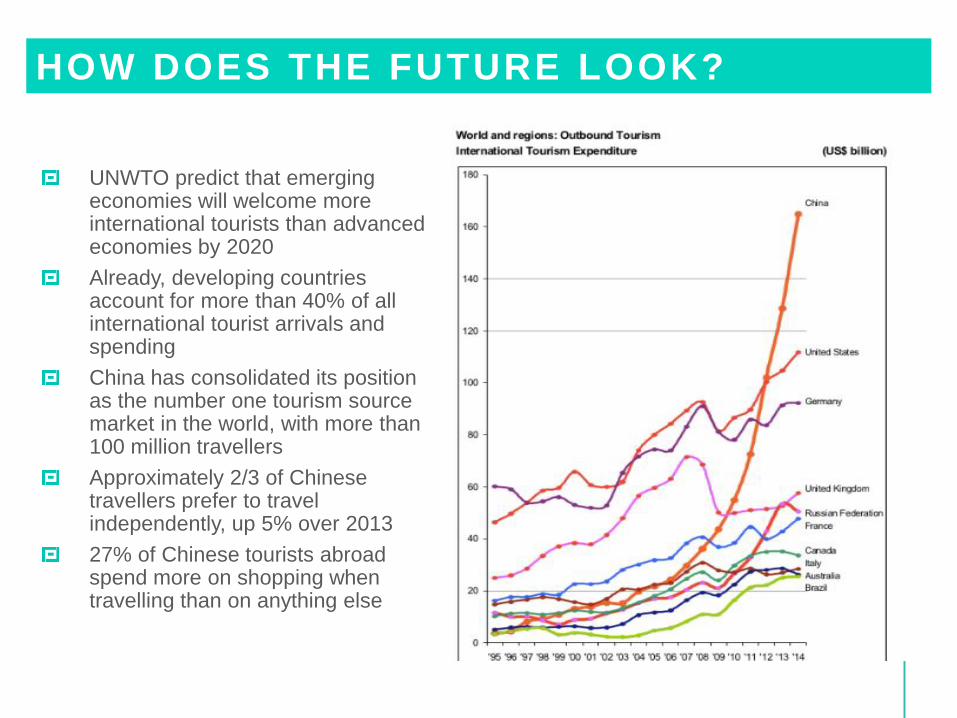

HOW DOES THE FUTURE LOOK?

UNWTO predict that emerging economies will welcome more international tourists than advanced economies by 2020

Already, developing countries account for more than 40% of all international tourist arrivals and spending

China has consolidated its position as the number one tourism source market in the world, with more than 100 million travellers

Approximately 2/3 of Chinese travellers prefer to travel independently, up 5% over 2013

27% of Chinese tourists abroad spend more on shopping when travelling than on anything else

Source: World Bank, OECD; Główny Urząd Statystyczny

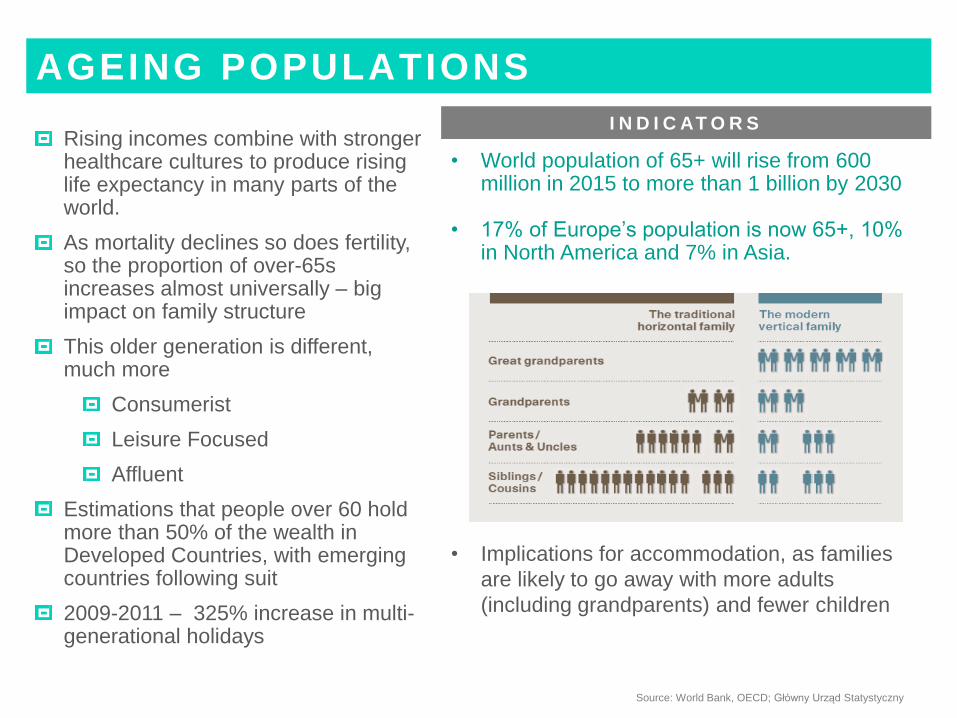

AGEING POPULATIONS

Rising incomes combine with stronger healthcare cultures to produce rising life expectancy in many parts of the world.

As mortality declines so does fertility, so the proportion of over-65s increases almost universally – big impact on family structure

This older generation is different, much more

Consumerist

Leisure Focused

Affluent

Estimations that people over 60 hold more than 50% of the wealth in Developed Countries, with emerging countries following suit

2009-2011 – 325% increase in multi-generational holidays

• World population of 65+ will rise from 600 million in 2015 to more than 1 billion by 2030

• 17% of Europe’s population is now 65+, 10% in North America and 7% in Asia.

• Implications for accommodation, as families

are likely to go away with more adults

(including grandparents) and fewer children

I N D I C AT O R S

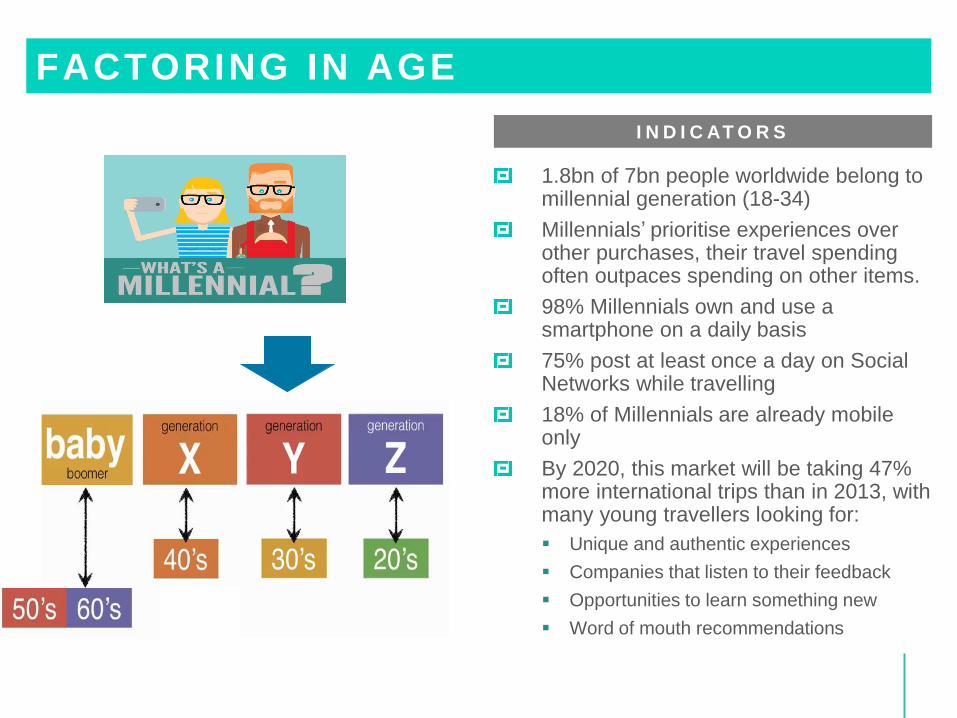

1.8bn of 7bn people worldwide belong to millennial generation (18-34)

Millennials’ prioritise experiences over other purchases, their travel spending often outpaces spending on other items.

98% Millennials own and use a smartphone on a daily basis

75% post at least once a day on Social Networks while travelling

18% of Millennials are already mobile only

By 2020, this market will be taking 47% more international trips than in 2013, with many young travellers looking for:

Unique and authentic experiences

Companies that listen to their feedback

Opportunities to learn something new

Word of mouth recommendations

FACTORING IN AGE

I N D I C AT O R S

Children Connect Everything – Gen Z

Source: 10 Hot Consumer Trends 2015 – Ericsson ConsumerLab

Post Demographic Imperatives

Source: IMF, UN DESA, US Dept of Commerce

Source: Greg Richards, 2014

Source: Resonance Portrait of US International Traveler Report 2015

GLOBALISATION

National borders are progressively erased

World is a giant bazaar & consumers can enjoy massively expanded choice and are constantly invited to be adventurous (in what they eat, how they dress, where they travel, how they entertain themselves...)

Big brands try to standardise consumer behaviour in their favour

While behaviour may align, requirements for new, authentic and non-homogenous experiences increases

I N D I C AT O R S

• Traditional cultural tourism is centred on

built heritage, but there is a growing

interest in ‘intangible heritage’ – popular

culture, traditions and storytelling

• Cities with ‘creative class’ population and

culture attract traveller from developed

markets, where built heritage continues

to resonate with emerging markets

• 27% of US international travellers are

‘Sophisticated Explorers’ for whom

‘Exploring new culture & their traditions

while on vacation’ is the #1 vacation

motivation

• Higher level of interest in active/creative

cultural participation rather than passive

observation

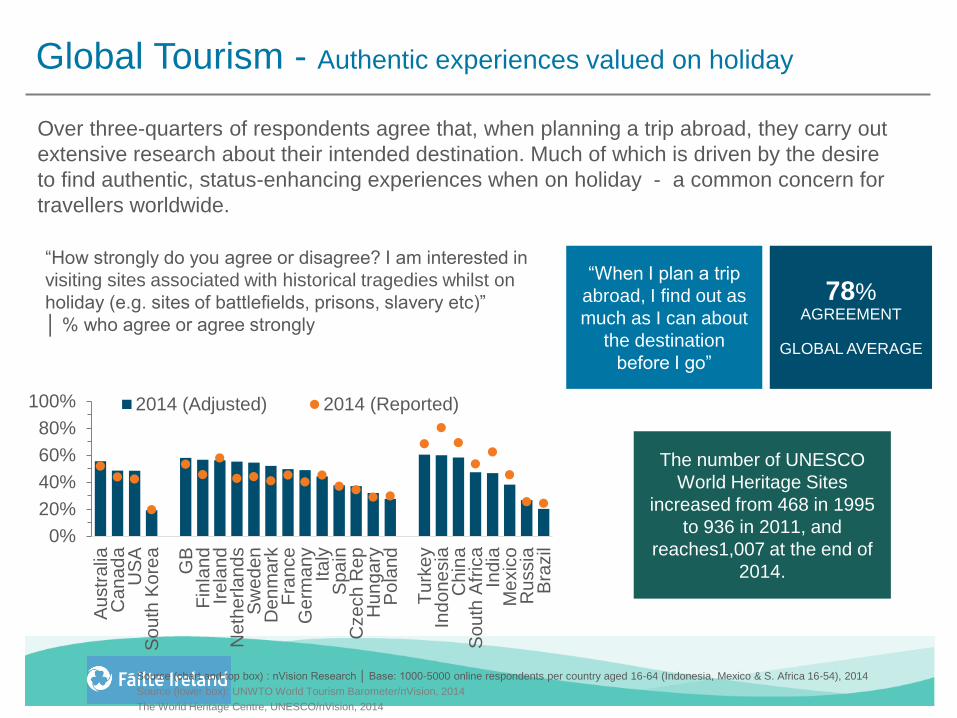

Global Tourism - Authentic experiences valued on holiday

0%

20%

40%

60%

80%

100%

Au

str

alia

Ca

na

da

US

AS

ou

th K

ore

a

GB

Fin

lan

dIr

ela

nd

Ne

the

rla

nd

sS

we

de

nD

enm

ark

Fra

nce

Ge

rma

ny

Ita

lyS

pa

inC

zech

Re

pH

ungary

Po

land

Tu

rke

yIn

do

ne

sia

Ch

ina

South

Afr

ica

Ind

iaM

exic

oR

ussia

Bra

zil

2014 (Adjusted) 2014 (Reported)

Source (chart and top box) : nVision Research │ Base: 1000-5000 online respondents per country aged 16-64 (Indonesia, Mexico & S. Africa 16-54), 2014

Source (lower box): UNWTO World Tourism Barometer/nVision, 2014

The World Heritage Centre, UNESCO/nVision, 2014

Over three-quarters of respondents agree that, when planning a trip abroad, they carry out

extensive research about their intended destination. Much of which is driven by the desire

to find authentic, status-enhancing experiences when on holiday - a common concern for

travellers worldwide.

“How strongly do you agree or disagree? I am interested in

visiting sites associated with historical tragedies whilst on

holiday (e.g. sites of battlefields, prisons, slavery etc)”

│ % who agree or agree strongly

“When I plan a trip

abroad, I find out as

much as I can about

the destination

before I go”

78% AGREEMENT

GLOBAL AVERAGE

The number of UNESCO

World Heritage Sites

increased from 468 in 1995

to 936 in 2011, and

reaches1,007 at the end of

2014.

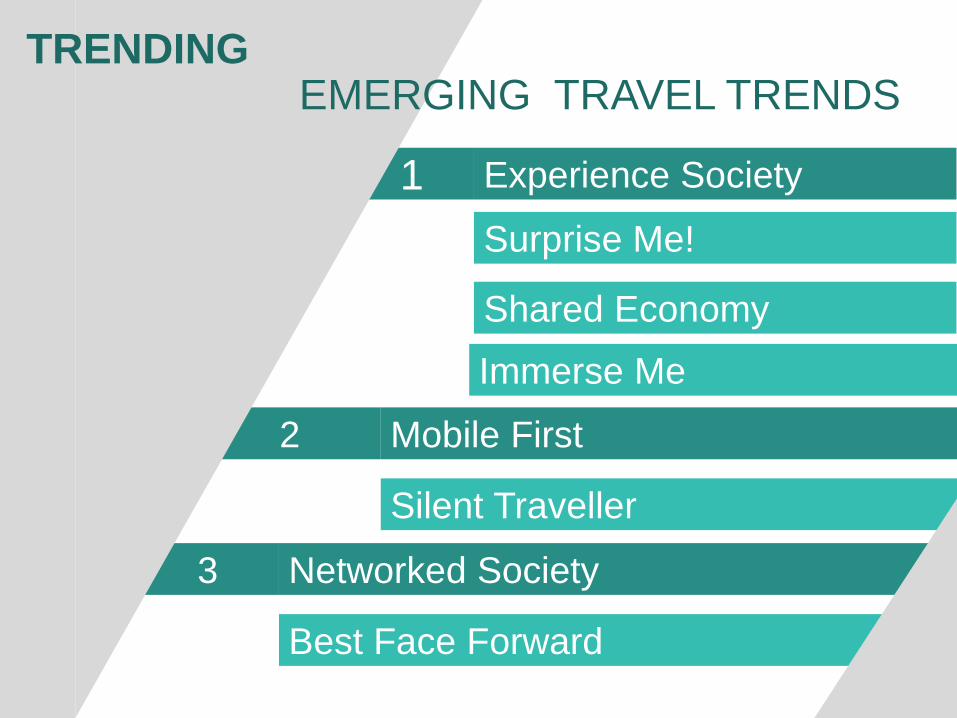

Networked Society

Best Face Forward

3

Experience Society 1

Surprise Me!

Shared Economy

Mobile First 2

Silent Traveller

TRENDING EMERGING TRAVEL TRENDS

Immerse Me

33

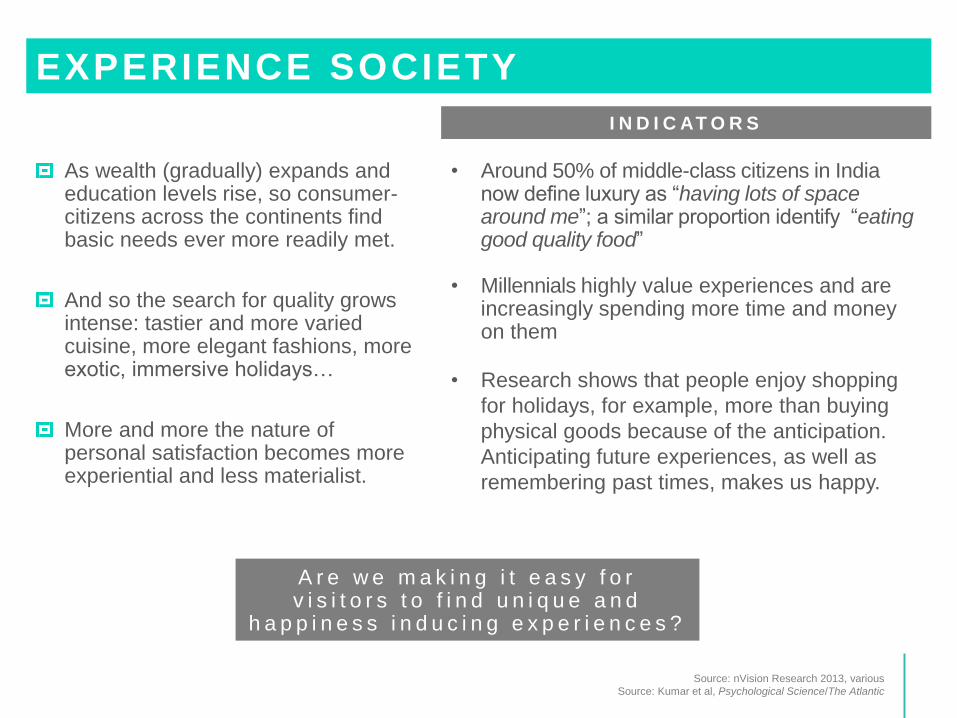

EXPERIENCE SOCIETY

Source: nVision Research 2013, various

Source: Kumar et al, Psychological Science/The Atlantic

EXPERIENCE SOCIETY

As wealth (gradually) expands and education levels rise, so consumer-citizens across the continents find basic needs ever more readily met.

And so the search for quality grows intense: tastier and more varied cuisine, more elegant fashions, more exotic, immersive holidays…

More and more the nature of personal satisfaction becomes more experiential and less materialist.

• Around 50% of middle-class citizens in India now define luxury as “having lots of space around me”; a similar proportion identify “eating good quality food”

• Millennials highly value experiences and are increasingly spending more time and money on them

• Research shows that people enjoy shopping

for holidays, for example, more than buying

physical goods because of the anticipation.

Anticipating future experiences, as well as

remembering past times, makes us happy.

I N D I C AT O R S

A r e w e m a k i n g i t e a s y f o r v i s i t o r s t o f i n d u n i q u e a n d

h a p p i n e s s i n d u c i n g e x p e r i e n c e s ?

Experiences must be Authentic

Millennials & Experiences

When it comes to money, ‘experiences’

trump ‘things’:

More than 3 in 4 millennials (78%) would

choose to spend money on a desirable

experience or event over buying

something desirable

78%

28%

Millennials

Spend money onexperiences overmaterial goods

Spend money onmaterial goods overexperiences

FOMO drives millennials’

experiential appetite: Nearly

7 in 10 (69%) millennials

experience FOMO.

In a world where life

experiences are broadcasted

across social media, the fear

of missing out drives

millennials to show up, share

and engage.

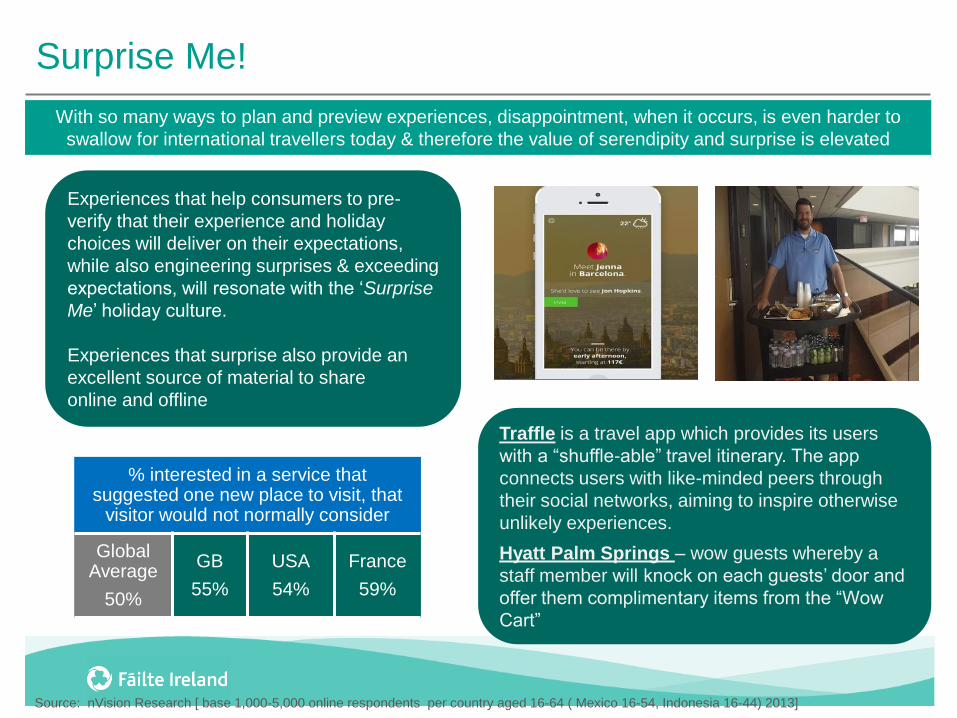

Surprise Me!

Experiences that help consumers to pre-

verify that their experience and holiday

choices will deliver on their expectations,

while also engineering surprises & exceeding

expectations, will resonate with the ‘Surprise

Me’ holiday culture.

Experiences that surprise also provide an

excellent source of material to share

online and offline

With so many ways to plan and preview experiences, disappointment, when it occurs, is even harder to

swallow for international travellers today & therefore the value of serendipity and surprise is elevated

Traffle is a travel app which provides its users

with a “shuffle-able” travel itinerary. The app

connects users with like-minded peers through

their social networks, aiming to inspire otherwise

unlikely experiences.

Hyatt Palm Springs – wow guests whereby a

staff member will knock on each guests’ door and

offer them complimentary items from the “Wow

Cart”

Source: nVision Research [ base 1,000-5,000 online respondents per country aged 16-64 ( Mexico 16-54, Indonesia 16-44) 2013]

% interested in a service that suggested one new place to visit, that

visitor would not normally consider

Global Average

50%

GB

55%

USA

54%

France

59%

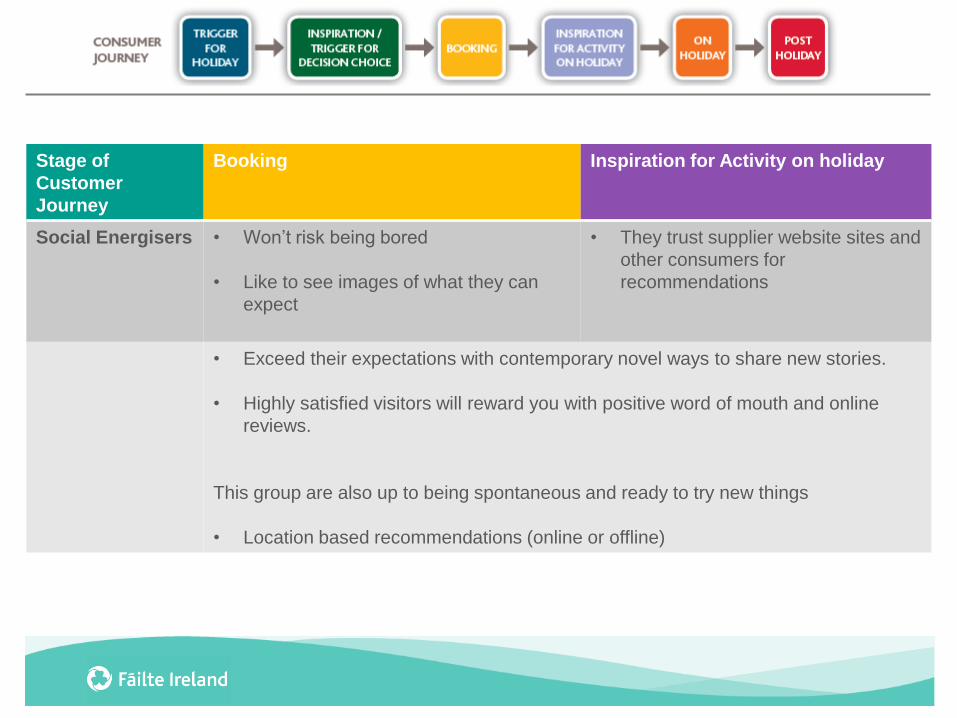

Stage of

Customer

Journey

Booking Inspiration for Activity on holiday

Social Energisers • Won’t risk being bored

• Like to see images of what they can

expect

• They trust supplier website sites and

other consumers for

recommendations

• Exceed their expectations with contemporary novel ways to share new stories.

• Highly satisfied visitors will reward you with positive word of mouth and online

reviews.

This group are also up to being spontaneous and ready to try new things

• Location based recommendations (online or offline)

Stage of

Customer

Journey

Booking Inspiration for Activity on holiday

Culturally

Curious

• Gather lots of information before the trip

& enjoy the process of doing so

• More likely to book in-destination and

with the provider.

• They don’t like to follow the herd and

like to keep their options open.

• Enjoy discovering places when they

arrive

For the Culturally Curious who will research things to do but don’t necessarily book

until they are on holiday, recommendations from people they interact with (locals,

trade and other visitors) is key.

40

It’s Good to Share (Sharing Economy)

9%

9%

11%

13%

0% 2% 4% 6% 8% 10% 12% 14%

US

UK

France

Germany

Column1

Trust in strangers and a desire to travel like a local makes collaborate

consumption more appealing.

Interaction with locals and the unique experience it provides, along

with a greater trust in online interactions is winning many

tourists over to the shared economy

The traditional notions of private ownership are being challenged as shared production and consumption of goods and services is growing

Is there room for the Shared Economy alongside traditional

models? Is the need to eat with a stranger a niche trend, or will

it become main-stream?

Source: Phocuswright 2015 [4,000 online travellers]

Percentage of Travellers who have rented space in a Private home/Apartment in the past year

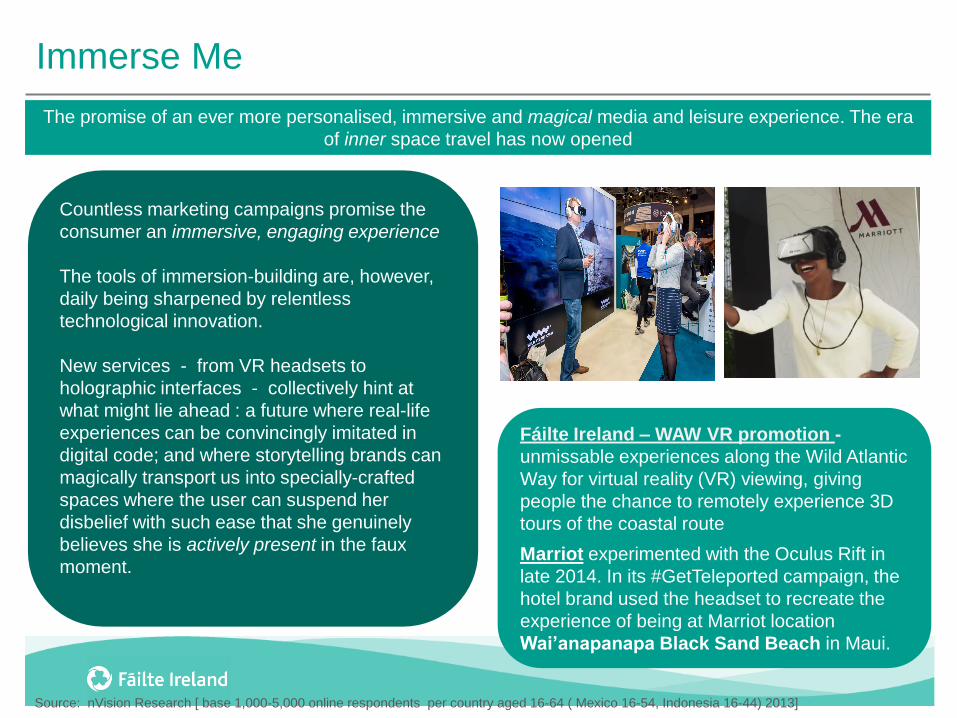

Immerse Me

Countless marketing campaigns promise the

consumer an immersive, engaging experience

The tools of immersion-building are, however,

daily being sharpened by relentless

technological innovation.

New services - from VR headsets to

holographic interfaces - collectively hint at

what might lie ahead : a future where real-life

experiences can be convincingly imitated in

digital code; and where storytelling brands can

magically transport us into specially-crafted

spaces where the user can suspend her

disbelief with such ease that she genuinely

believes she is actively present in the faux

moment.

The promise of an ever more personalised, immersive and magical media and leisure experience. The era

of inner space travel has now opened

Fáilte Ireland – WAW VR promotion -

unmissable experiences along the Wild Atlantic

Way for virtual reality (VR) viewing, giving

people the chance to remotely experience 3D

tours of the coastal route

Marriot experimented with the Oculus Rift in

late 2014. In its #GetTeleported campaign, the

hotel brand used the headset to recreate the

experience of being at Marriot location

Wai’anapanapa Black Sand Beach in Maui.

Source: nVision Research [ base 1,000-5,000 online respondents per country aged 16-64 ( Mexico 16-54, Indonesia 16-44) 2013]

43

https://www.youtube.com/watch?v=xVigoyrmcC0

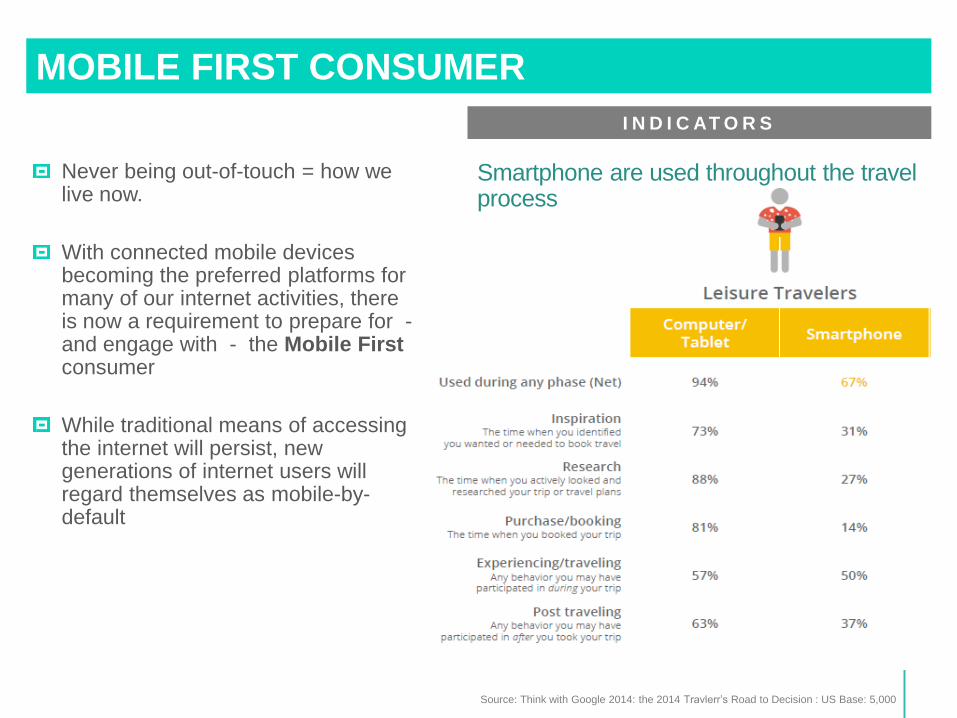

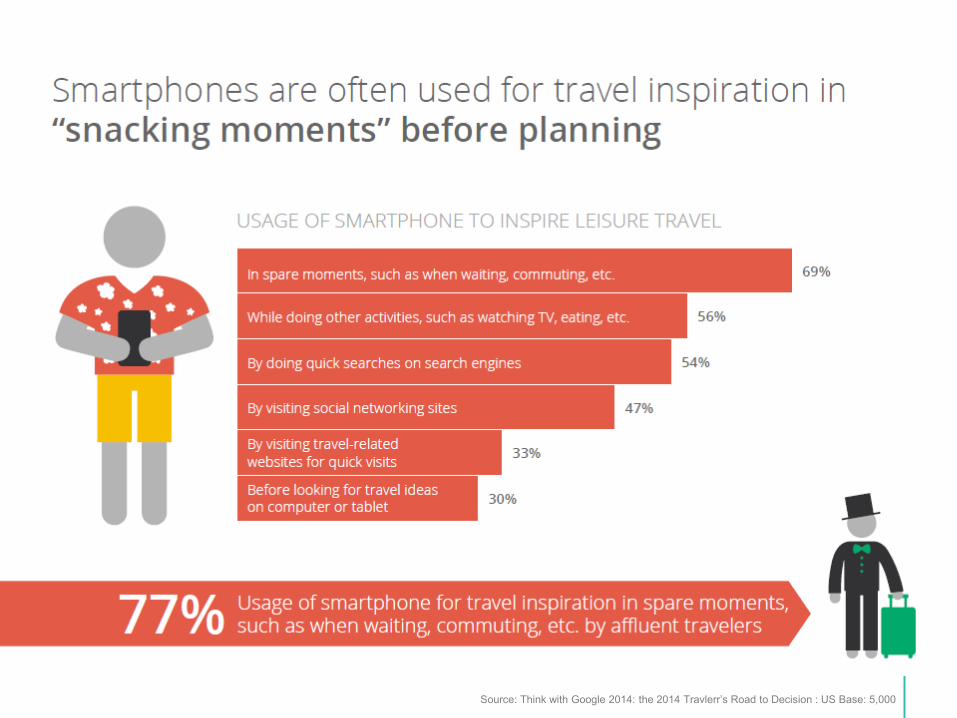

MOBILE FIRST CONSUMER

Source: Think with Google 2014: the 2014 Travlerr’s Road to Decision : US Base: 5,000

MOBILE FIRST CONSUMER

Never being out-of-touch = how we live now.

With connected mobile devices becoming the preferred platforms for many of our internet activities, there is now a requirement to prepare for - and engage with - the Mobile First consumer

While traditional means of accessing the internet will persist, new generations of internet users will regard themselves as mobile-by-default

I N D I C AT O R S

Smartphone are used throughout the travel process

Source: Think with Google 2014: the 2014 Travlerr’s Road to Decision : US Base: 5,000

Overwhelmingly leisure travellers rely on search engines via their smartphone at both the planning stages of the holiday and when on holiday to find local information

Are we catering for the mobile first consumer adequately?

Are we mobile optimised and ranking high on the search engine lists?

Are we catering for both practical information while on holiday and also the inspirational content to motivate visitors to visit our area?

Source: Think with Google 2014: the 2014 Travlerr’s Road to Decision : US Base: 5,000

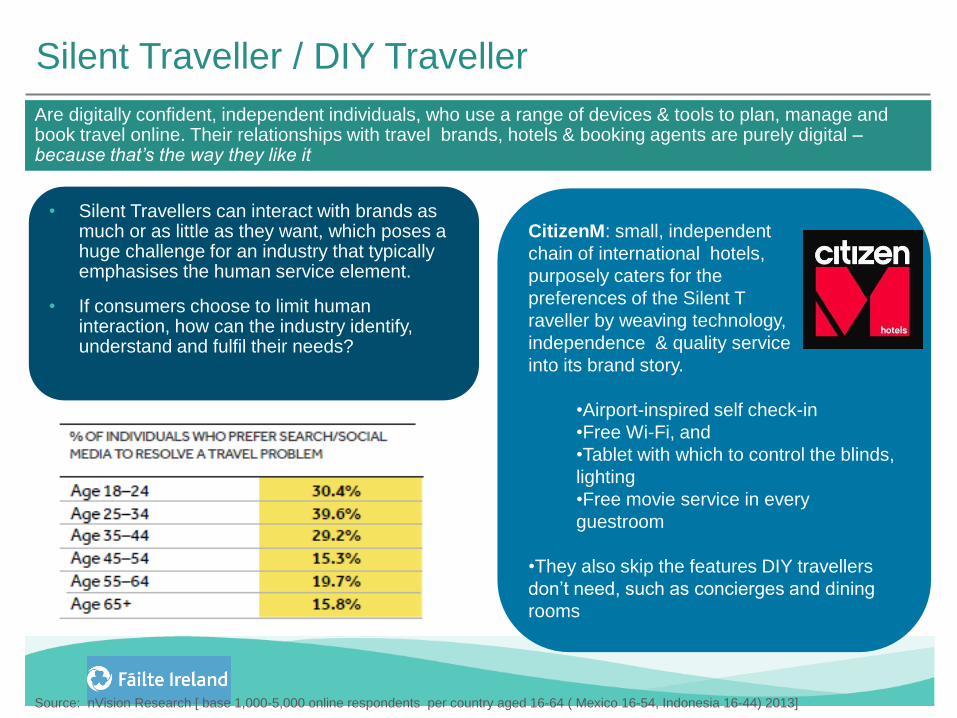

Silent Traveller / DIY Traveller

• Silent Travellers can interact with brands as much or as little as they want, which poses a huge challenge for an industry that typically emphasises the human service element.

• If consumers choose to limit human interaction, how can the industry identify, understand and fulfil their needs?

Are digitally confident, independent individuals, who use a range of devices & tools to plan, manage and book travel online. Their relationships with travel brands, hotels & booking agents are purely digital – because that’s the way they like it

CitizenM: small, independent

chain of international hotels,

purposely caters for the

preferences of the Silent T

raveller by weaving technology,

independence & quality service

into its brand story.

•Airport-inspired self check-in

•Free Wi-Fi, and

•Tablet with which to control the blinds,

lighting

•Free movie service in every

guestroom

•They also skip the features DIY travellers

don’t need, such as concierges and dining

rooms

Source: nVision Research [ base 1,000-5,000 online respondents per country aged 16-64 ( Mexico 16-54, Indonesia 16-44) 2013]

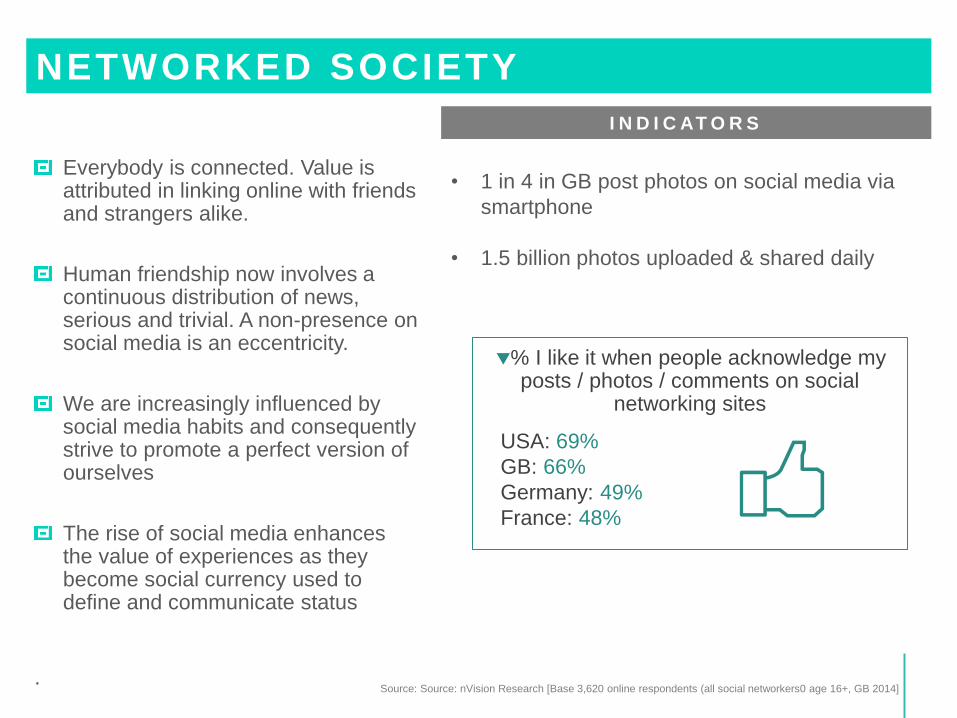

NETWORKED SOCIETY

Source: Source: nVision Research [Base 3,620 online respondents (all social networkers0 age 16+, GB 2014]

NETWORKED SOCIETY

Everybody is connected. Value is attributed in linking online with friends and strangers alike.

Human friendship now involves a continuous distribution of news, serious and trivial. A non-presence on social media is an eccentricity.

We are increasingly influenced by social media habits and consequently strive to promote a perfect version of ourselves

The rise of social media enhances the value of experiences as they become social currency used to define and communicate status

.

• 1 in 4 in GB post photos on social media via

smartphone

• 1.5 billion photos uploaded & shared daily

I N D I C AT O R S

% I like it when people acknowledge my posts / photos / comments on social

networking sites

USA: 69%

GB: 66%

Germany: 49%

France: 48%

5% Baby Boomers

17% Gen X

29% Gen Y

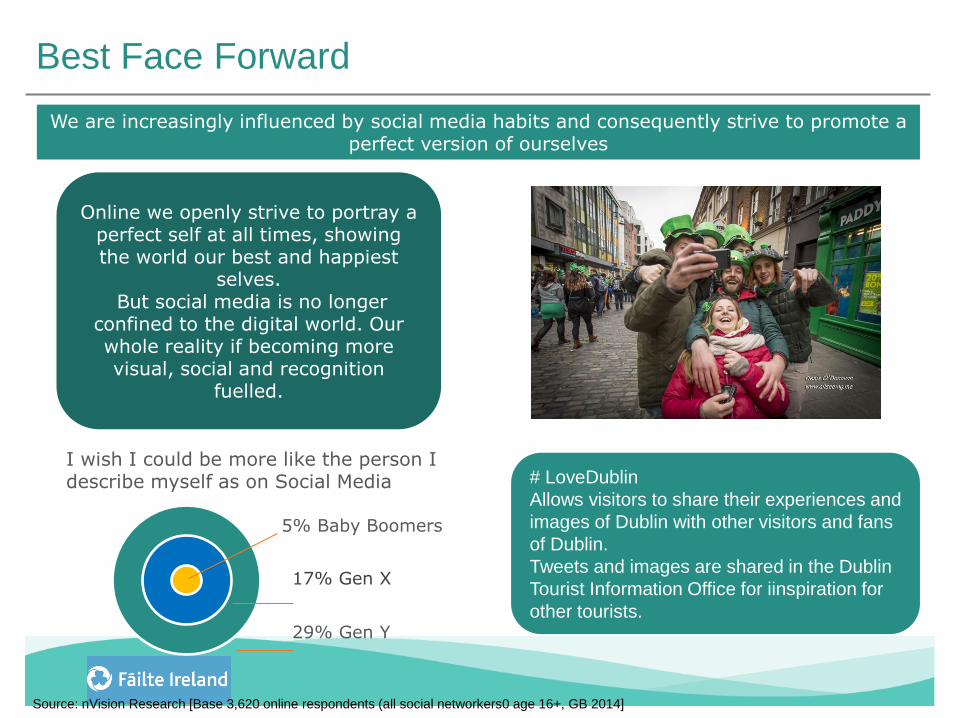

Best Face Forward

Online we openly strive to portray a perfect self at all times, showing the world our best and happiest

selves. But social media is no longer

confined to the digital world. Our whole reality if becoming more visual, social and recognition

fuelled.

We are increasingly influenced by social media habits and consequently strive to promote a perfect version of ourselves

# LoveDublin

Allows visitors to share their experiences and

images of Dublin with other visitors and fans

of Dublin.

Tweets and images are shared in the Dublin

Tourist Information Office for iinspiration for

other tourists.

I wish I could be more like the person I describe myself as on Social Media

Source: nVision Research [Base 3,620 online respondents (all social networkers0 age 16+, GB 2014]

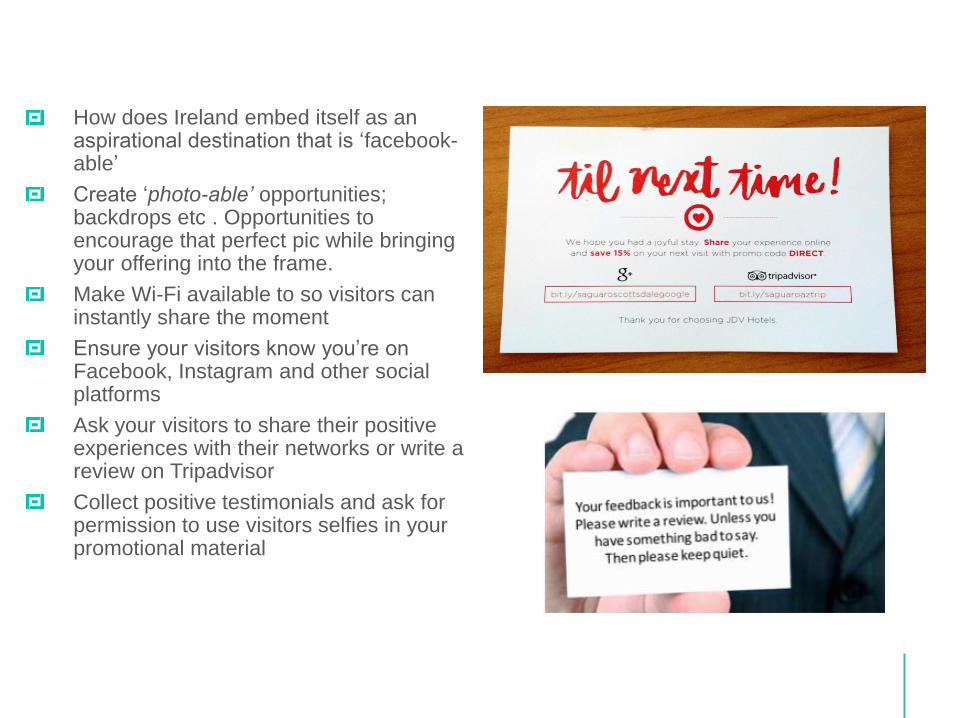

How does Ireland embed itself as an aspirational destination that is ‘facebook-able’

Create ‘photo-able’ opportunities; backdrops etc . Opportunities to encourage that perfect pic while bringing your offering into the frame.

Make Wi-Fi available to so visitors can instantly share the moment

Ensure your visitors know you’re on Facebook, Instagram and other social platforms

Ask your visitors to share their positive experiences with their networks or write a review on Tripadvisor

Collect positive testimonials and ask for permission to use visitors selfies in your promotional material

Heading Futures

Thank You

For more visit

www.failteireland.ie/trends