Embed Size (px)

Citation preview

Fifth Street Finance Corp.

Investor Presentation

February 2010

www.fifthstreetfinance.com

2

Forward- Looking Statements

This presentation may contain certain forward-looking statements, including statements with regard to the future performance of Fifth Street Finance Corp. Words such as “believes,” “expects,” “projects,” “anticipates,” and “future” or similar expressions are intended to identify forward-looking statements. These forward-looking statements are subject to the inherent uncertainties in predicting future results and conditions. Certain factors could cause actual results to differ materially from those projected in these forward-looking statements, and these factors are identified from time to time in our filings with the Securities and Exchange Commission. Fifth Street Finance Corp. undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

3

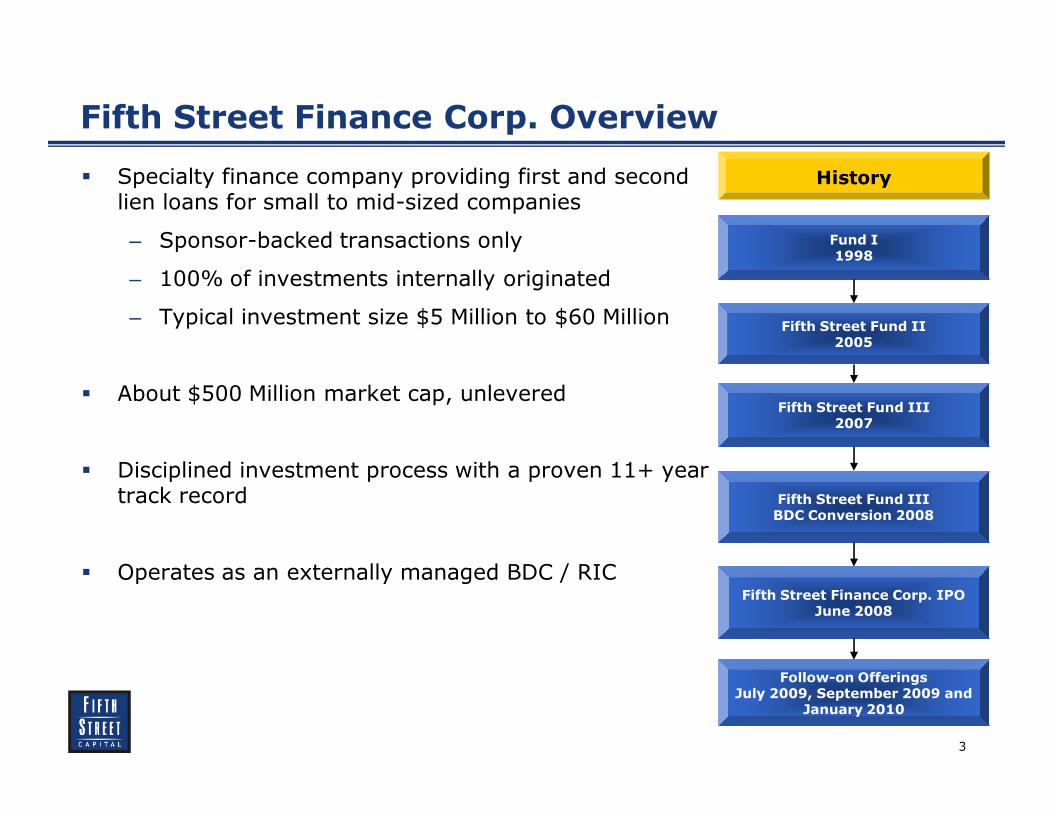

Fifth Street Finance Corp. Overview

History

Fund I1998

Fifth Street Fund II2005

Fifth Street Fund III2007

Fifth Street Fund III BDC Conversion 2008

Fifth Street Finance Corp. IPOJune 2008

Follow-on OfferingsJuly 2009, September 2009 and

January 2010

� Specialty finance company providing first and second lien loans for small to mid-sized companies

– Sponsor-backed transactions only

– 100% of investments internally originated

– Typical investment size $5 Million to $60 Million

� About $500 Million market cap, unlevered

� Disciplined investment process with a proven 11+ year track record

� Operates as an externally managed BDC / RIC

4

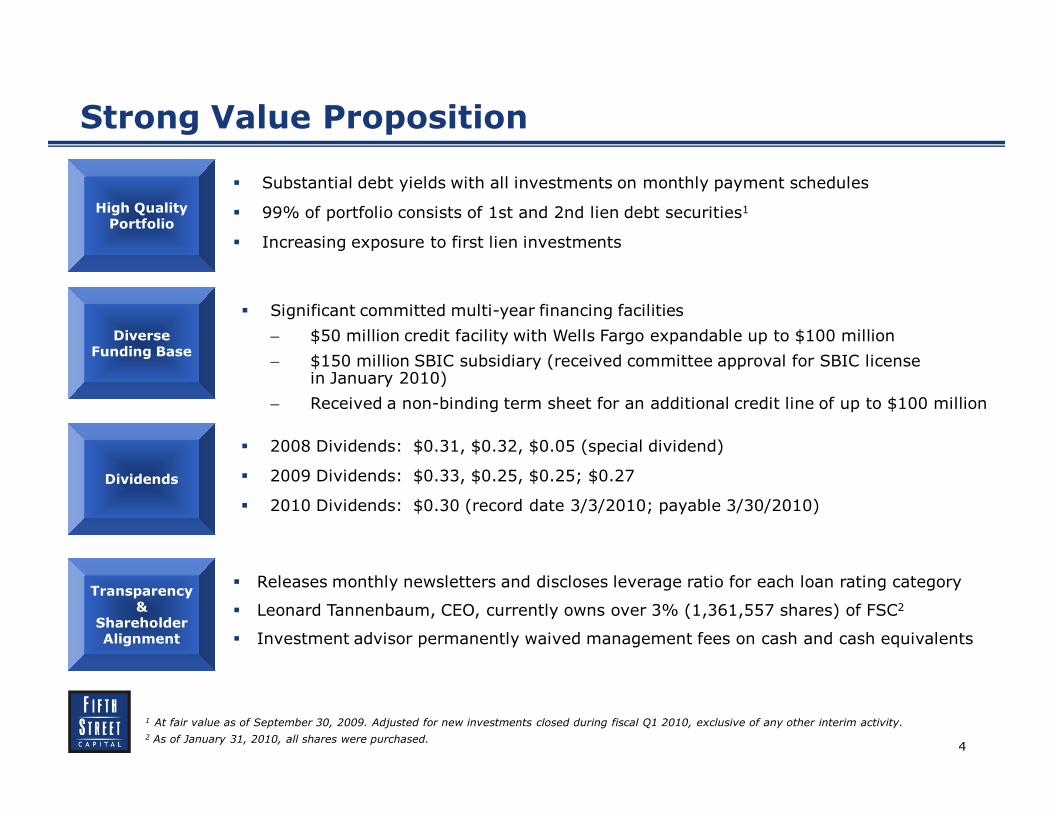

Strong Value Proposition

Transparency &

Shareholder Alignment

� Substantial debt yields with all investments on monthly payment schedules

� 99% of portfolio consists of 1st and 2nd lien debt securities1

� Increasing exposure to first lien investments

� Significant committed multi-year financing facilities

– $50 million credit facility with Wells Fargo expandable up to $100 million

– $150 million SBIC subsidiary (received committee approval for SBIC license in January 2010)

– Received a non-binding term sheet for an additional credit line of up to $100 million

� 2008 Dividends: $0.31, $0.32, $0.05 (special dividend)

� 2009 Dividends: $0.33, $0.25, $0.25; $0.27

� 2010 Dividends: $0.30 (record date 3/3/2010; payable 3/30/2010)

1 At fair value as of September 30, 2009. Adjusted for new investments closed during fiscal Q1 2010, exclusive of any other interim activity.

2 As of January 31, 2010, all shares were purchased.

� Releases monthly newsletters and discloses leverage ratio for each loan rating category

� Leonard Tannenbaum, CEO, currently owns over 3% (1,361,557 shares) of FSC2

� Investment advisor permanently waived management fees on cash and cash equivalents

High Quality Portfolio

Diverse Funding Base

Dividends

5

Why Fifth Street Today

� Strong unlevered asset yields will be enhanced by Fifth Street’s access to credit

� Fiscal 2010 second quarter dividend increased 11% to $0.30 per share

– Expect quarterly dividend to continue to increase during fiscal 2010

– Dividend policy is to distribute between 90–100% of distributable income

� Will NOT seek approval of shareholders at 2010 annual meeting to sell shares of its common stock below NAV

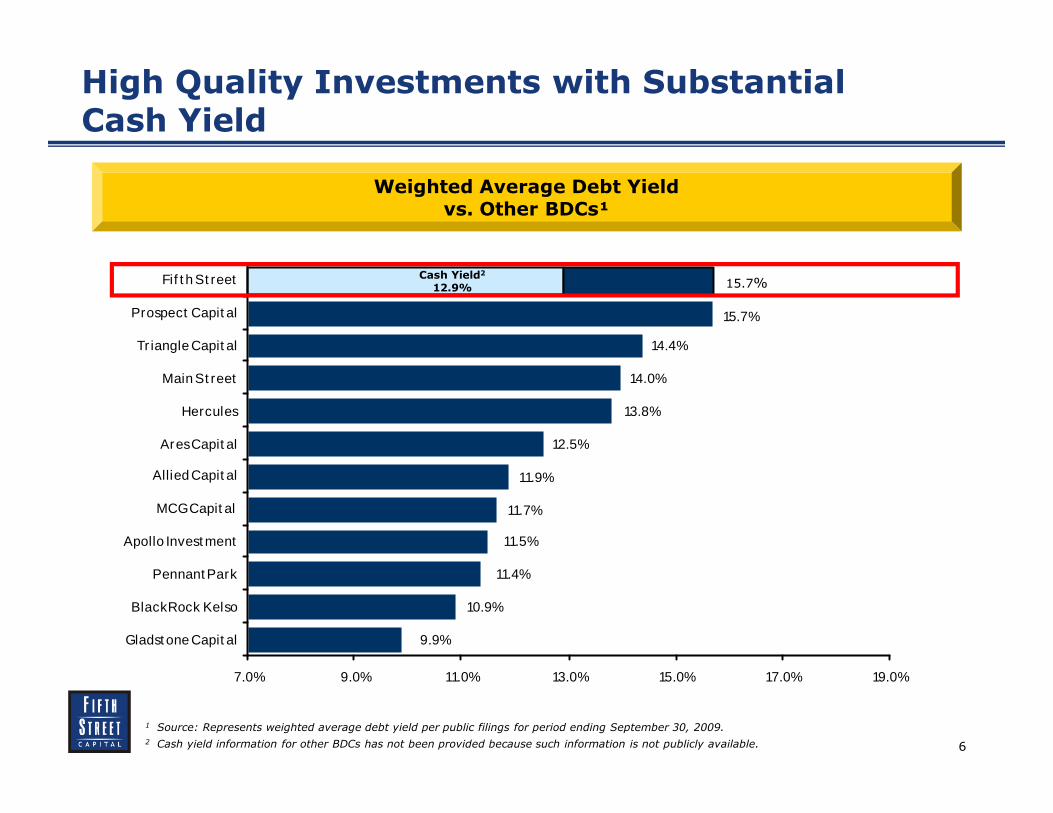

� Recurring revenue stream-weighted average portfolio debt yield is 15.7% vs. industry average of approximately 12.8%1

� 81% of debt portfolio consists of fixed rate debt securities; 100% of floating rate debt securities have interest rate floors of at least 9%2

� High quality pipeline comprised primarily of first lien investments provides attractive growth opportunities

1 As of September 30, 2009.

2 At fair value as of September 30, 2009. Adjusted for new investments closed during fiscal Q1 2010, exclusive of any other interim activity.

6

High Quality Investments with Substantial Cash Yield

1 Source: Represents weighted average debt yield per public filings for period ending September 30, 2009.

2 Cash yield information for other BDCs has not been provided because such information is not publicly available.

15.7%

14.4%

9.9%

10.9%

11.4%

11.5%

11.7%

11.9%

12.5%

13.8%

14.0%

7.0% 9.0% 11.0% 13.0% 15.0% 17.0% 19.0%

Gladst one Capit al

BlackRock Kelso

Pennant Park

Apollo Invest ment

MCG Capit al

Allied Capit al

Ares Capit al

Hercules

Main St reet

Tr iangle Capit al

Prospect Capit al

Fif t h St reet

Weighted Average Debt Yieldvs. Other BDCs¹

Cash Yield2

12.9% 15.7%

7

BDC Structure and Regulation

� Business Development Companies (“BDCs”) are uniquely positioned financing vehicles that provide debt and equity capital to private and small publicly-owned enterprises

� BDCs were created by Congress in 1980 with the stated mission of facilitating the flow of capital to companies lacking access to public capital markets

� BDC regulations allow a maximum debt-to-equity ratio of 1:1 which allow BDCs to modestly enhance their return

� BDCs are required to distribute at least 90% of their income to shareholders annually

� SEC regulations require BDCs to report the fair value of assets quarterly

8

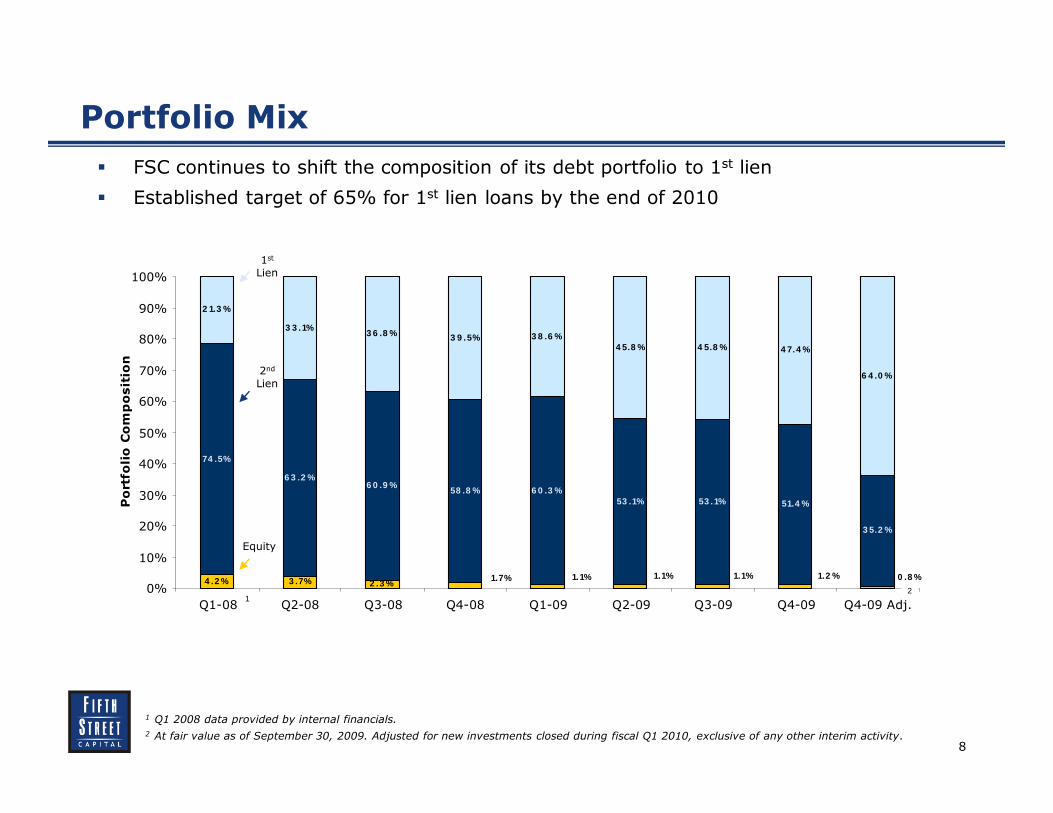

3 .7%

74 .5%

6 3 .2 %6 0 .9 %

58 .8 % 6 0 .3 %53 .1% 53 .1% 51.4 %

3 5.2 %

4 7.4 %

6 4 .0 %

2 .3 %4 .2 %1.2 %1.1%1.1%1.1%1.7% 0 .8 %

4 5.8 %4 5.8 %3 8 .6 %3 9 .5%3 6 .8 %

3 3 .1%

2 1.3 %

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1-08 Q2-08 Q3-08 Q4-08 Q1-09 Q2-09 Q3-09 Q4-09 Q4-09 Adj.

Portfolio Composition

Portfolio Mix

1 Q1 2008 data provided by internal financials.

2 At fair value as of September 30, 2009. Adjusted for new investments closed during fiscal Q1 2010, exclusive of any other interim activity.

� FSC continues to shift the composition of its debt portfolio to 1st lien

� Established target of 65% for 1st lien loans by the end of 2010

2

2nd

Lien

1st

Lien

Equity

1

9

Diversified Portfoilio1

Portfolio by Industry and Region

1 As of September 30, 2009 at fair value. Adjusted for new investments closed during fiscal Q1 2010, exclusive of any other interim activity.

2 Healthcare, education and childcare includes healthcare technology, healthcare services, healthcare facilities and education.

3 Household products & retail includes household products & specialty chemicals, home retail, home improvement, and housewares & specialty.

4 Advertising, media, entertainment & leisure includes media – advertising, merchandise display, leisure facilities and entertainment – theaters.

5 Infrastructure includes construction & engineering and emulsions manufacturing.

6 Food and restaurants includes food distributors and restaurants.

Healthcare services

20%

Healthcare technology

22%

Education19%

Healthcare facilities

11%

Healthcare equipment

28%

West21%

M idwest12%

Southeast16%

Southwest20%

Northeast31%

Footwear and apparel5%

Trailer leasing services2%

Air freight and logist ics3%

Infrastructure5

8%

Food and restaurants6

6%

Advertising, media,

entertainment & leisure4

9%

Healthcare, education and

childcare2

38%

Household products & retail3

19%

M anufacturing - mechanical products

3%

Data processing and outsourced services

3%

Capital goods2%

Building products1% Environmental & facilit ies

services1%

10

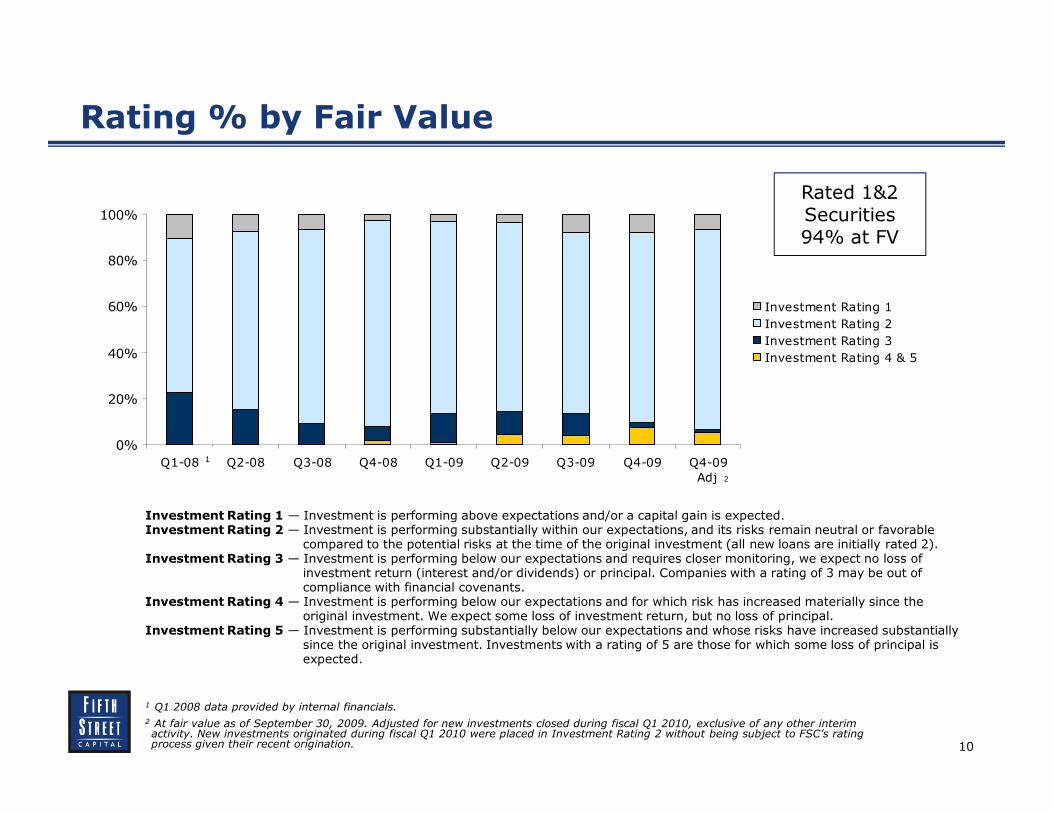

Rating % by Fair Value

0%

20%

40%

60%

80%

100%

Q1-08 Q2-08 Q3-08 Q4-08 Q1-09 Q2-09 Q3-09 Q4-09 Q4-09

Adj.

Investment Rating 1

Investment Rating 2

Investment Rating 3

Investment Rating 4 & 5

Investment Rating 1 — Investment is performing above expectations and/or a capital gain is expected.Investment Rating 2 — Investment is performing substantially within our expectations, and its risks remain neutral or favorable

compared to the potential risks at the time of the original investment (all new loans are initially rated 2).Investment Rating 3 — Investment is performing below our expectations and requires closer monitoring, we expect no loss of

investment return (interest and/or dividends) or principal. Companies with a rating of 3 may be out of compliance with financial covenants.

Investment Rating 4 — Investment is performing below our expectations and for which risk has increased materially since the original investment. We expect some loss of investment return, but no loss of principal.

Investment Rating 5 — Investment is performing substantially below our expectations and whose risks have increased substantially since the original investment. Investments with a rating of 5 are those for which some loss of principal is expected.

Rated 1&2Securities94% at FV

1 Q1 2008 data provided by internal financials.

2 At fair value as of September 30, 2009. Adjusted for new investments closed during fiscal Q1 2010, exclusive of any other interim activity. New investments originated during fiscal Q1 2010 were placed in Investment Rating 2 without being subject to FSC’s rating process given their recent origination.

1

2

11

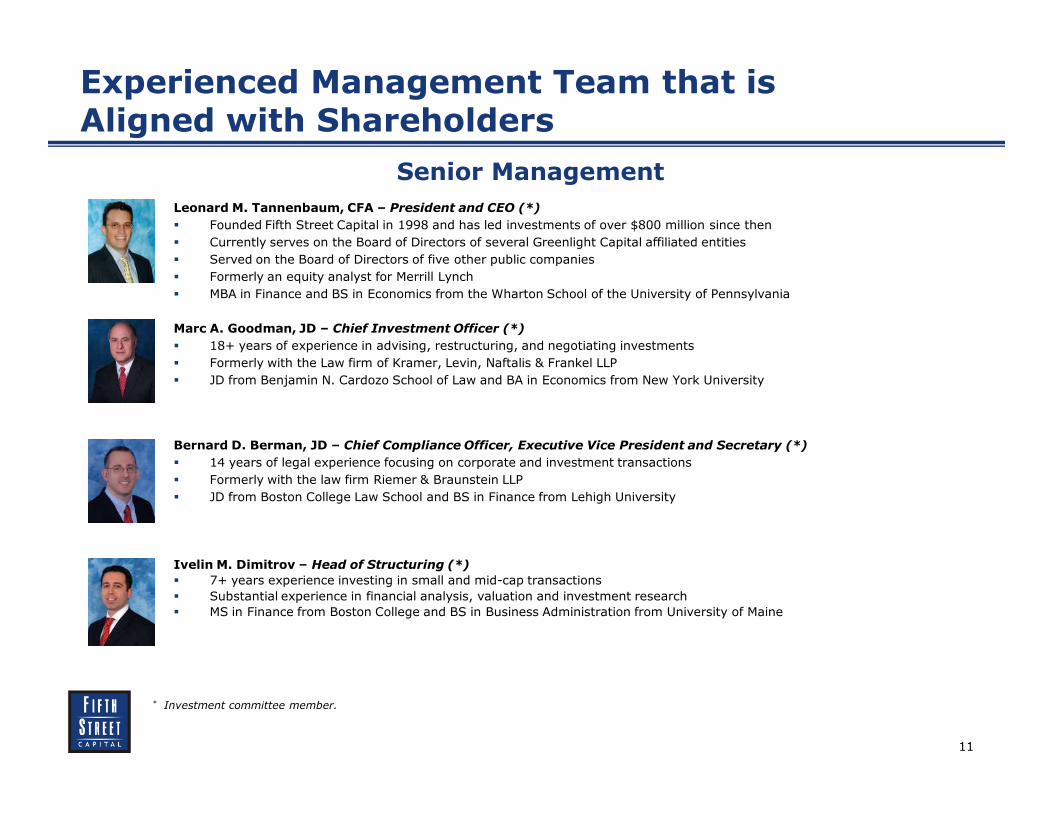

Experienced Management Team that is Aligned with Shareholders

Senior Management

Leonard M. Tannenbaum, CFA – President and CEO (*)

� Founded Fifth Street Capital in 1998 and has led investments of over $800 million since then

� Currently serves on the Board of Directors of several Greenlight Capital affiliated entities

� Served on the Board of Directors of five other public companies

� Formerly an equity analyst for Merrill Lynch

� MBA in Finance and BS in Economics from the Wharton School of the University of Pennsylvania

Marc A. Goodman, JD – Chief Investment Officer (*)

� 18+ years of experience in advising, restructuring, and negotiating investments

� Formerly with the Law firm of Kramer, Levin, Naftalis & Frankel LLP

� JD from Benjamin N. Cardozo School of Law and BA in Economics from New York University

Bernard D. Berman, JD – Chief Compliance Officer, Executive Vice President and Secretary (*)

� 14 years of legal experience focusing on corporate and investment transactions

� Formerly with the law firm Riemer & Braunstein LLP

� JD from Boston College Law School and BS in Finance from Lehigh University

Ivelin M. Dimitrov – Head of Structuring (*)

� 7+ years experience investing in small and mid-cap transactions

� Substantial experience in financial analysis, valuation and investment research

� MS in Finance from Boston College and BS in Business Administration from University of Maine

* Investment committee member.

12

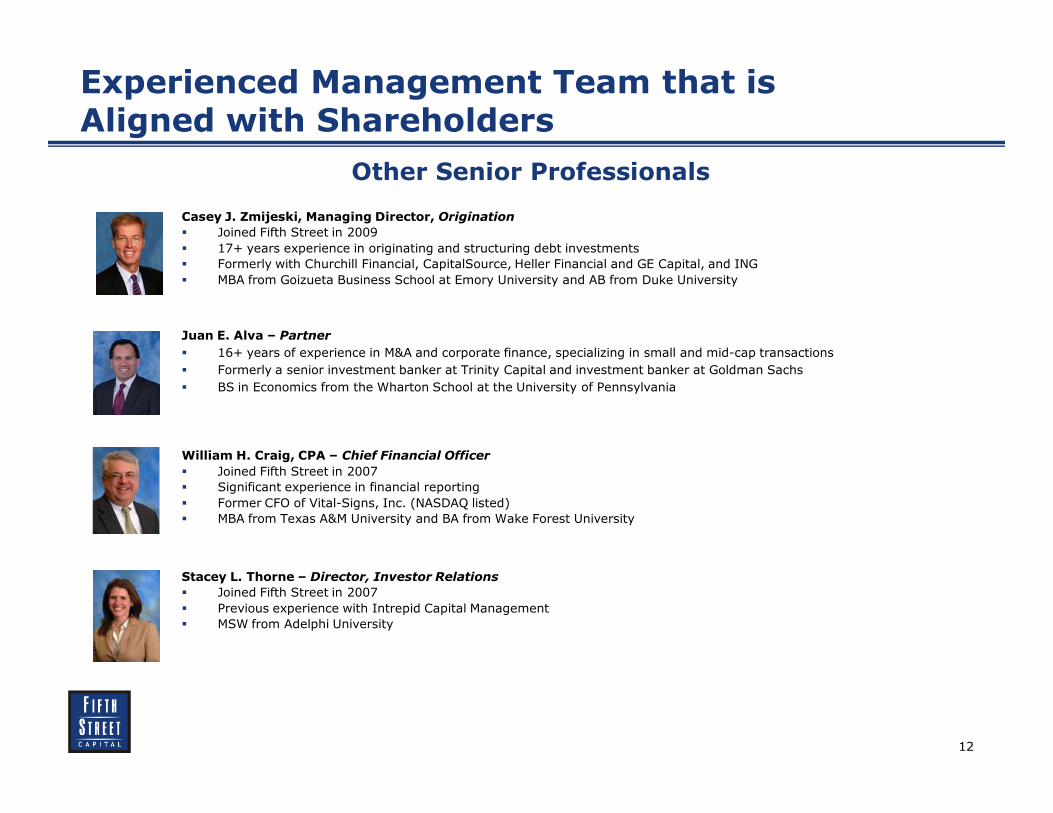

Experienced Management Team that is Aligned with Shareholders

Other Senior Professionals

Casey J. Zmijeski, Managing Director, Origination

� Joined Fifth Street in 2009

� 17+ years experience in originating and structuring debt investments

� Formerly with Churchill Financial, CapitalSource, Heller Financial and GE Capital, and ING

� MBA from Goizueta Business School at Emory University and AB from Duke University

Juan E. Alva – Partner

� 16+ years of experience in M&A and corporate finance, specializing in small and mid-cap transactions

� Formerly a senior investment banker at Trinity Capital and investment banker at Goldman Sachs

� BS in Economics from the Wharton School at the University of Pennsylvania

William H. Craig, CPA – Chief Financial Officer

� Joined Fifth Street in 2007

� Significant experience in financial reporting

� Former CFO of Vital-Signs, Inc. (NASDAQ listed)

� MBA from Texas A&M University and BA from Wake Forest University

Stacey L. Thorne – Director, Investor Relations

� Joined Fifth Street in 2007

� Previous experience with Intrepid Capital Management

� MSW from Adelphi University

13

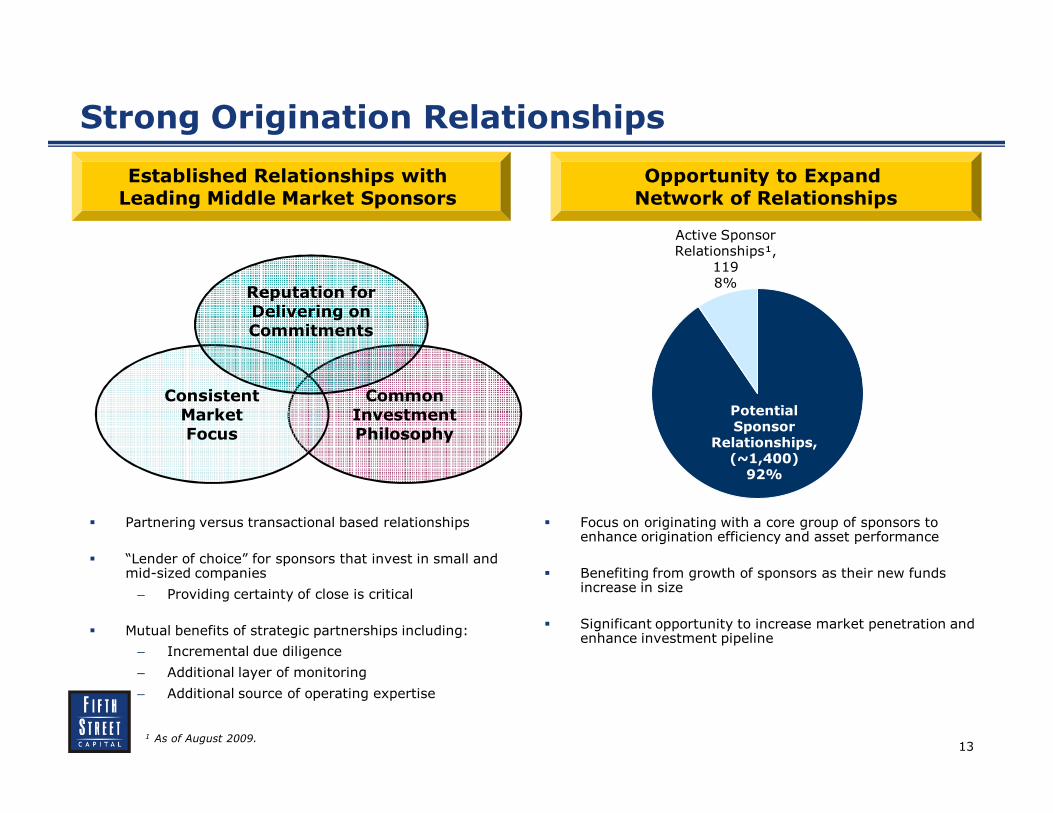

Strong Origination Relationships

� Partnering versus transactional based relationships

� “Lender of choice” for sponsors that invest in small and mid-sized companies

– Providing certainty of close is critical

� Mutual benefits of strategic partnerships including:

– Incremental due diligence

– Additional layer of monitoring

– Additional source of operating expertise

� Focus on originating with a core group of sponsors to enhance origination efficiency and asset performance

� Benefiting from growth of sponsors as their new funds increase in size

� Significant opportunity to increase market penetration and enhance investment pipeline

Opportunity to Expand Network of Relationships

Established Relationships with Leading Middle Market Sponsors

Common Investment Philosophy

Consistent Market Focus

Reputation for Delivering on Commitments

Potential Sponsor

Relationships, (~1,400) 92%

Active Sponsor Relationships¹,

1198%

1 As of August 2009.

14

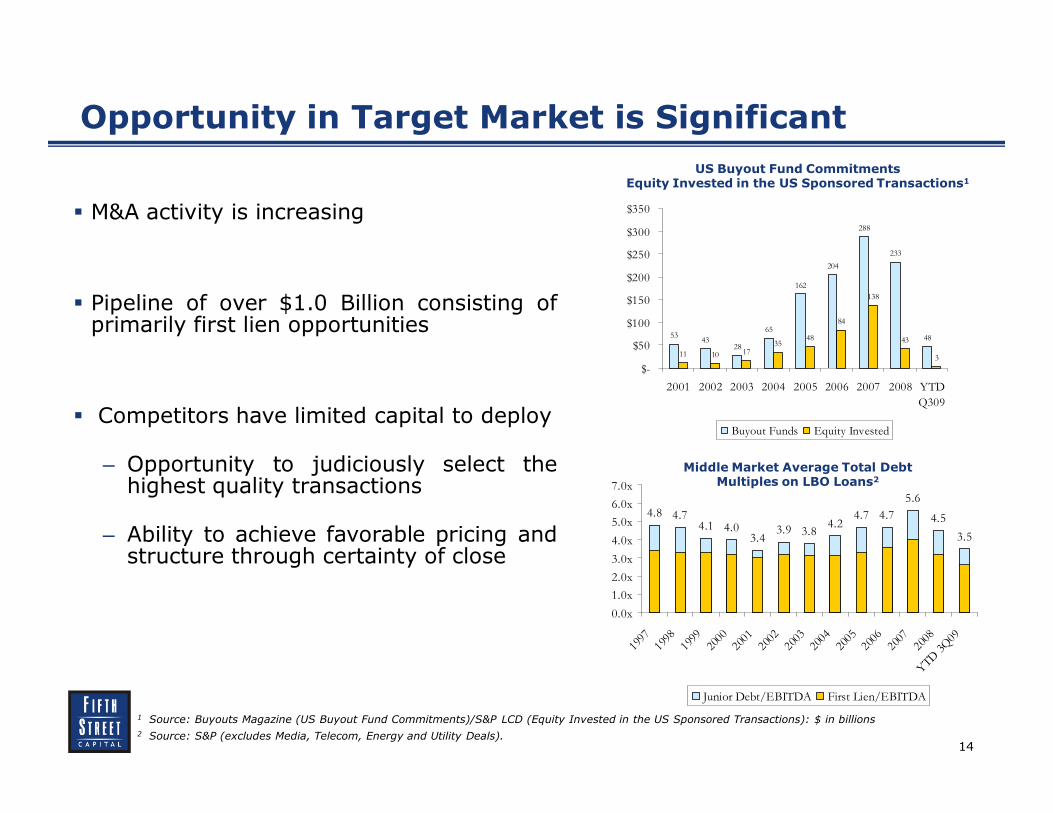

3.43.9 3.8

4.24.7 4.7

5.6

4.5

3.54.04.1

4.74.8

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

199719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

08YTD

3Q09

Junior Debt/EBITDA First Lien/EBITDA

5343

28

65

162

204

288

233

48

11 10 1735

48

84

138

43

3

$-

$50

$100

$150

$200

$250

$300

$350

2001 2002 2003 2004 2005 2006 2007 2008 YTD

Q309

Buyout Funds Equity Invested

Opportunity in Target Market is Significant

� M&A activity is increasing

� Pipeline of over $1.0 Billion consisting ofprimarily first lien opportunities

� Competitors have limited capital to deploy

– Opportunity to judiciously select thehighest quality transactions

– Ability to achieve favorable pricing andstructure through certainty of close

1 Source: Buyouts Magazine (US Buyout Fund Commitments)/S&P LCD (Equity Invested in the US Sponsored Transactions): $ in billions

2 Source: S&P (excludes Media, Telecom, Energy and Utility Deals).

US Buyout Fund CommitmentsEquity Invested in the US Sponsored Transactions1

Middle Market Average Total Debt Multiples on LBO Loans2

15

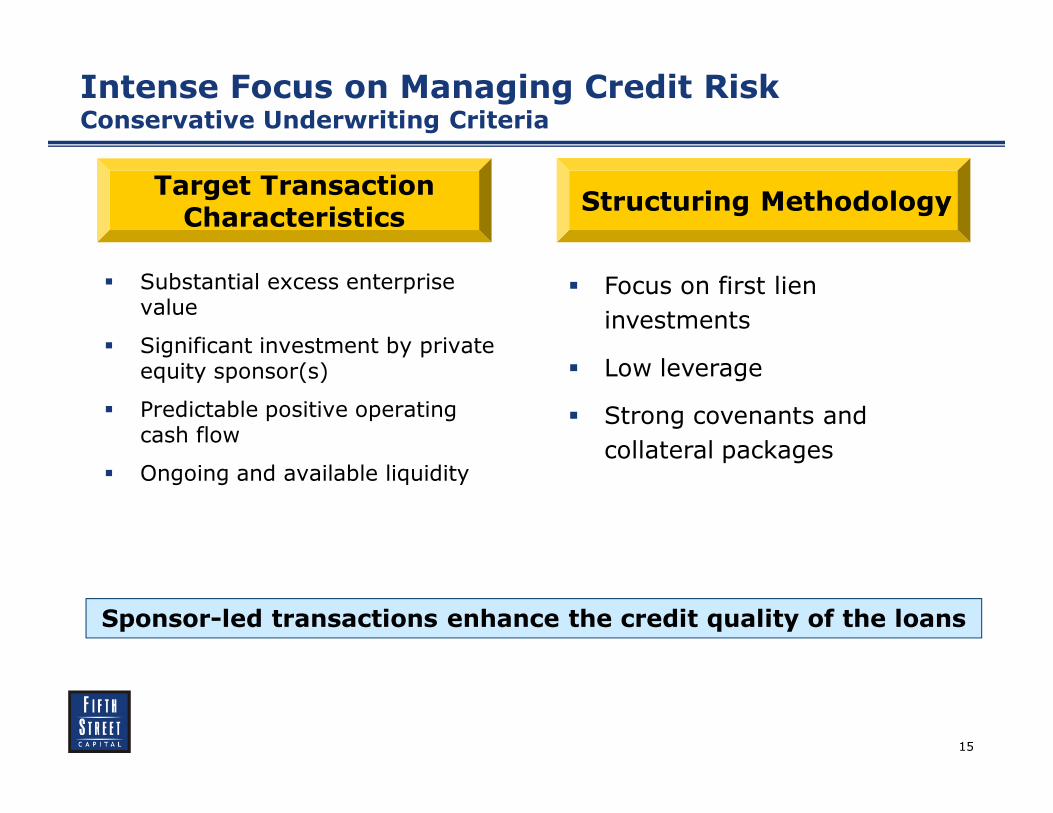

Intense Focus on Managing Credit Risk Conservative Underwriting Criteria

Structuring MethodologyTarget Transaction Characteristics

� Substantial excess enterprise value

� Significant investment by private equity sponsor(s)

� Predictable positive operating cash flow

� Ongoing and available liquidity

� Focus on first lien

investments

� Low leverage

� Strong covenants and

collateral packages

Sponsor-led transactions enhance the credit quality of the loans

16

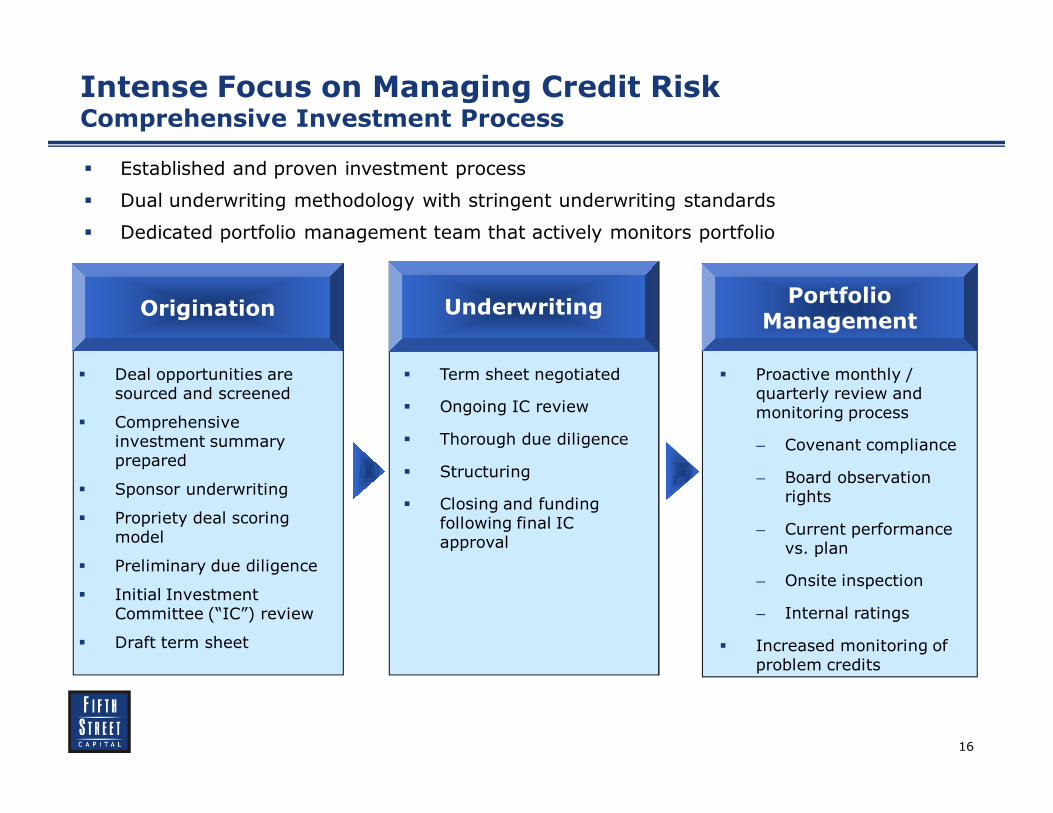

Intense Focus on Managing Credit Risk Comprehensive Investment Process

Portfolio Management

Origination Underwriting

� Deal opportunities are sourced and screened

� Comprehensive investment summary prepared

� Sponsor underwriting

� Propriety deal scoring model

� Preliminary due diligence

� Initial Investment Committee (“IC”) review

� Draft term sheet

� Term sheet negotiated

� Ongoing IC review

� Thorough due diligence

� Structuring

� Closing and funding following final IC approval

� Proactive monthly / quarterly review and monitoring process

– Covenant compliance

– Board observation rights

– Current performance vs. plan

– Onsite inspection

– Internal ratings

� Increased monitoring of problem credits

� Established and proven investment process

� Dual underwriting methodology with stringent underwriting standards

� Dedicated portfolio management team that actively monitors portfolio

17

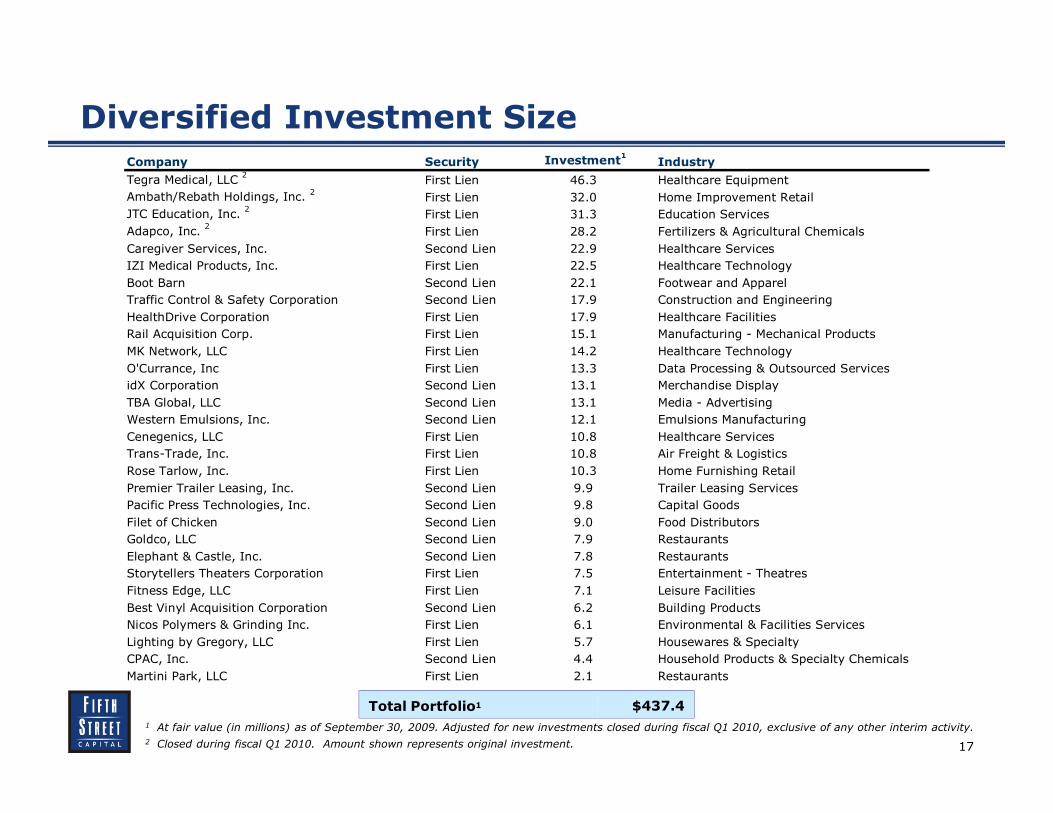

Diversified Investment Size

1 At fair value (in millions) as of September 30, 2009. Adjusted for new investments closed during fiscal Q1 2010, exclusive of any other interim activity.

2 Closed during fiscal Q1 2010. Amount shown represents original investment.

Total Portfolio1 $437.4

Company Security Investment1

Industry

Tegra Medical, LLC 2

First Lien 46.3 Healthcare Equipment

Ambath/Rebath Holdings, Inc. 2

First Lien 32.0 Home Improvement Retail

JTC Education, Inc. 2

First Lien 31.3 Education Services

Adapco, Inc. 2

First Lien 28.2 Fertilizers & Agricultural Chemicals

Caregiver Services, Inc. Second Lien 22.9 Healthcare Services

IZI Medical Products, Inc. First Lien 22.5 Healthcare Technology

Boot Barn Second Lien 22.1 Footwear and Apparel

Traffic Control & Safety Corporation Second Lien 17.9 Construction and Engineering

HealthDrive Corporation First Lien 17.9 Healthcare Facilities

Rail Acquisition Corp. First Lien 15.1 Manufacturing - Mechanical Products

MK Network, LLC First Lien 14.2 Healthcare Technology

O'Currance, Inc First Lien 13.3 Data Processing & Outsourced Services

idX Corporation Second Lien 13.1 Merchandise Display

TBA Global, LLC Second Lien 13.1 Media - Advertising

Western Emulsions, Inc. Second Lien 12.1 Emulsions Manufacturing

Cenegenics, LLC First Lien 10.8 Healthcare Services

Trans-Trade, Inc. First Lien 10.8 Air Freight & Logistics

Rose Tarlow, Inc. First Lien 10.3 Home Furnishing Retail

Premier Trailer Leasing, Inc. Second Lien 9.9 Trailer Leasing Services

Pacific Press Technologies, Inc. Second Lien 9.8 Capital Goods

Filet of Chicken Second Lien 9.0 Food Distributors

Goldco, LLC Second Lien 7.9 Restaurants

Elephant & Castle, Inc. Second Lien 7.8 Restaurants

Storytellers Theaters Corporation First Lien 7.5 Entertainment - Theatres

Fitness Edge, LLC First Lien 7.1 Leisure Facilities

Best Vinyl Acquisition Corporation Second Lien 6.2 Building Products

Nicos Polymers & Grinding Inc. First Lien 6.1 Environmental & Facilities Services

Lighting by Gregory, LLC First Lien 5.7 Housewares & Specialty

CPAC, Inc. Second Lien 4.4 Household Products & Specialty Chemicals

Martini Park, LLC First Lien 2.1 Restaurants

18

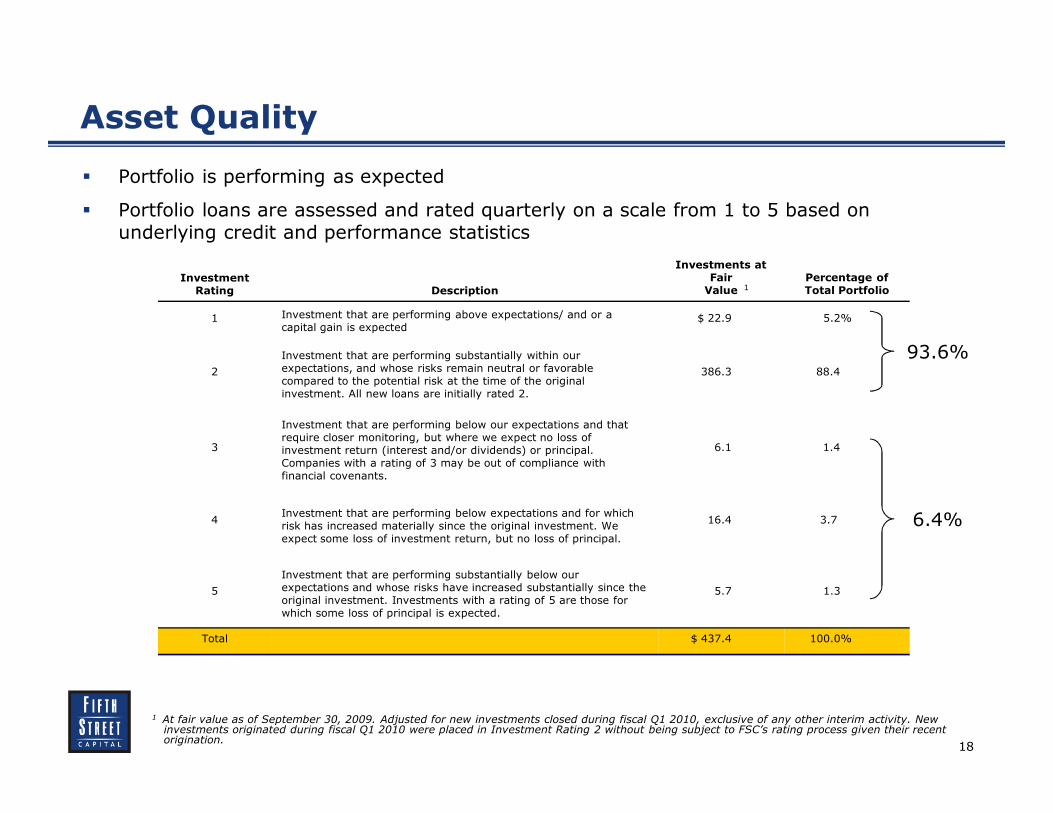

Asset Quality

� Portfolio is performing as expected

� Portfolio loans are assessed and rated quarterly on a scale from 1 to 5 based on underlying credit and performance statistics

Investment Rating Description

Investments at FairValue

Percentage of Total Portfolio

1 Investment that are performing above expectations/ and or a capital gain is expected

$ 22.9 5.2%

2

Investment that are performing substantially within our expectations, and whose risks remain neutral or favorable compared to the potential risk at the time of the original investment. All new loans are initially rated 2.

386.3 88.4

3

Investment that are performing below our expectations and that require closer monitoring, but where we expect no loss of investment return (interest and/or dividends) or principal. Companies with a rating of 3 may be out of compliance with financial covenants.

6.1 1.4%

4Investment that are performing below expectations and for which risk has increased materially since the original investment. We expect some loss of investment return, but no loss of principal.

16.4 3.7

5

Investment that are performing substantially below our expectations and whose risks have increased substantially since the original investment. Investments with a rating of 5 are those for which some loss of principal is expected.

5.7 1.3%

Total $ 437.4 100.0%

1 At fair value as of September 30, 2009. Adjusted for new investments closed during fiscal Q1 2010, exclusive of any other interim activity. New investments originated during fiscal Q1 2010 were placed in Investment Rating 2 without being subject to FSC’s rating process given their recent origination.

93.6%

6.4%

1

19

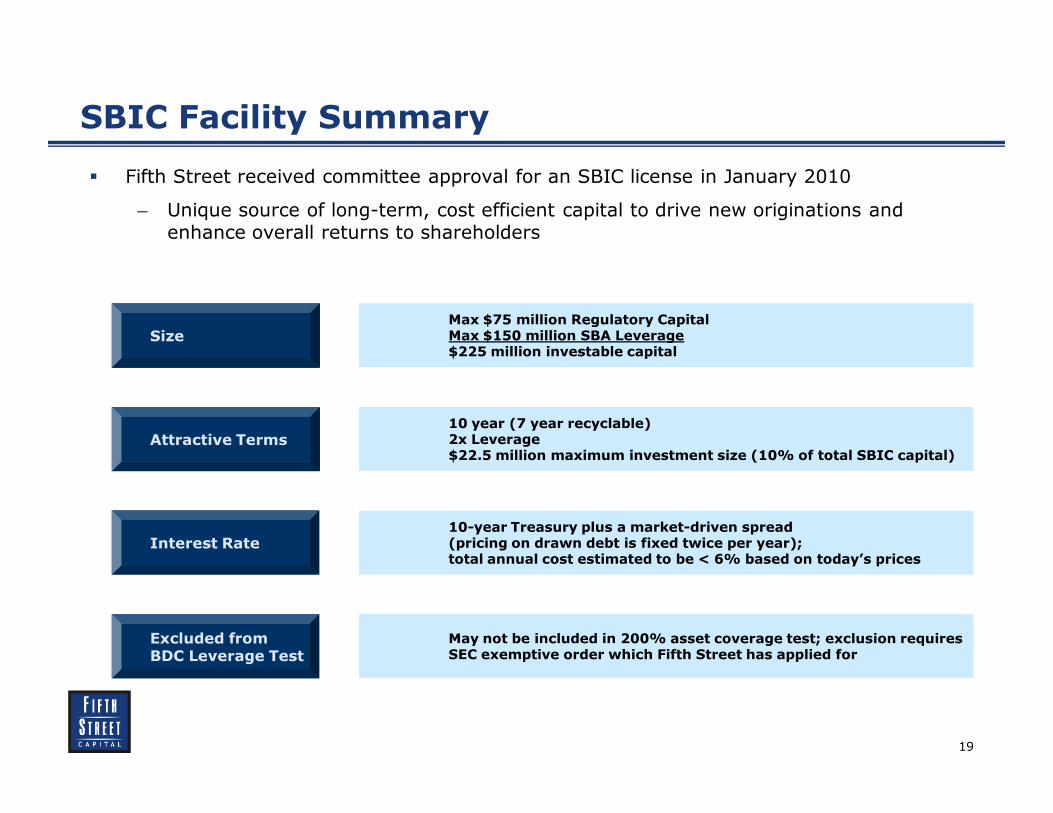

SBIC Facility Summary

Max $75 million Regulatory CapitalMax $150 million SBA Leverage$225 million investable capital

10 year (7 year recyclable)2x Leverage$22.5 million maximum investment size (10% of total SBIC capital)

10-year Treasury plus a market-driven spread(pricing on drawn debt is fixed twice per year);total annual cost estimated to be < 6% based on today’s prices

May not be included in 200% asset coverage test; exclusion requires SEC exemptive order which Fifth Street has applied for

� Fifth Street received committee approval for an SBIC license in January 2010

– Unique source of long-term, cost efficient capital to drive new originations and enhance overall returns to shareholders

Attractive Terms

Size

Interest Rate

Excluded from BDC Leverage Test

20

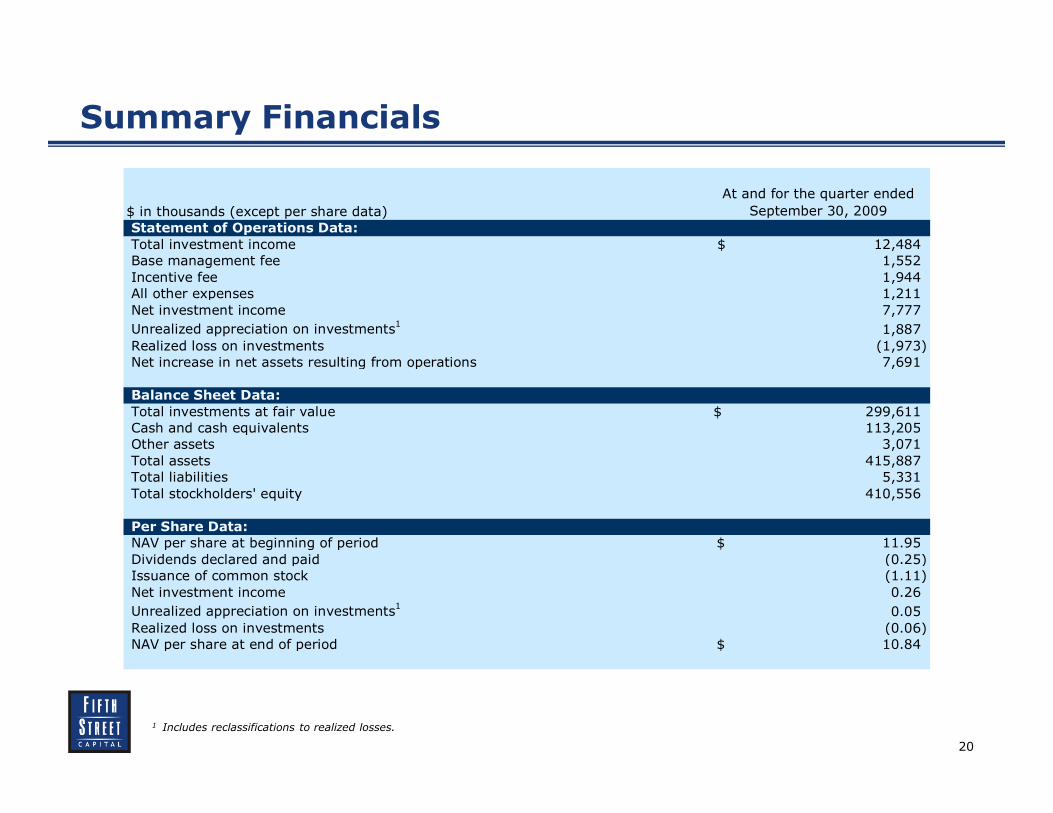

Summary Financials

1 Includes reclassifications to realized losses.

$ in thousands (except per share data)

At and for the quarter ended

September 30, 2009

Statement of Operations Data:

Total investment income 12,484$

Base management fee 1,552

Incentive fee 1,944

All other expenses 1,211

Net investment income 7,777

Unrealized appreciation on investments1

1,887

Realized loss on investments (1,973)

Net increase in net assets resulting from operations 7,691

Balance Sheet Data:

Total investments at fair value 299,611$

Cash and cash equivalents 113,205

Other assets 3,071

Total assets 415,887

Total liabilities 5,331

Total stockholders' equity 410,556

Per Share Data:

NAV per share at beginning of period 11.95$

Dividends declared and paid (0.25)

Issuance of common stock (1.11)

Net investment income 0.26

Unrealized appreciation on investments1

0.05

Realized loss on investments (0.06)

NAV per share at end of period 10.84$

21

Corporate Governance

Independent (5)

� Byron J. Haney (Chair of the Audit Committee) – 20+ years of business experience, including serving as chief financial officer of a private retail store chain and as an auditor with a predecessor of Deloitte & Touche LLP. Served on the Board of Directors of Sterling Chemicals, Inc. (public company) and Furniture.com

� Frank C. Meyer (Chair of the Valuation Committee) – Former Chairman of Glenwood Capital Investments, LLC (purchased by the Man Group). Previously served on the Board of Directors of several companies including Quality Systems, Inc. (public company)

� Adam C. Berkman, CPA (NYS inactive) – 20+ years of experience in strategy, operations, finance and business development in various industries

� Brian S. Dunn – 15+ years of marketing, logistical and entrepreneurial experience

� Douglas F. Ray – 14+ years experience acquiring, developing, financing and managing a diverse portfolio of real estate investments, including three healthcare properties funds

Interested (2)

� Leonard M. Tannenbaum, CFA – President and CEO of Fifth Street Finance Corp. – 12+ years of experience making investments in small to mid-sized companies. Mr. Tannenbaum has founded a number of private investment firms, including Fifth Street Capital LLC. Mr. Tannenbaum currently serves on the Board of Directors of several Greenlight Capital affiliated entities and has previously served on the Board of Directors of five other public companies

� Bernard D. Berman – Chief Compliance Officer, Executive Vice President and Secretary of Fifth Street Finance Corp. – 14 years oflegal experience focusing on corporate and investment transactions. Mr. Berman was formerly a corporate attorney with the lawfirm Riemer & Braunstein LLP

Board of Directors

22

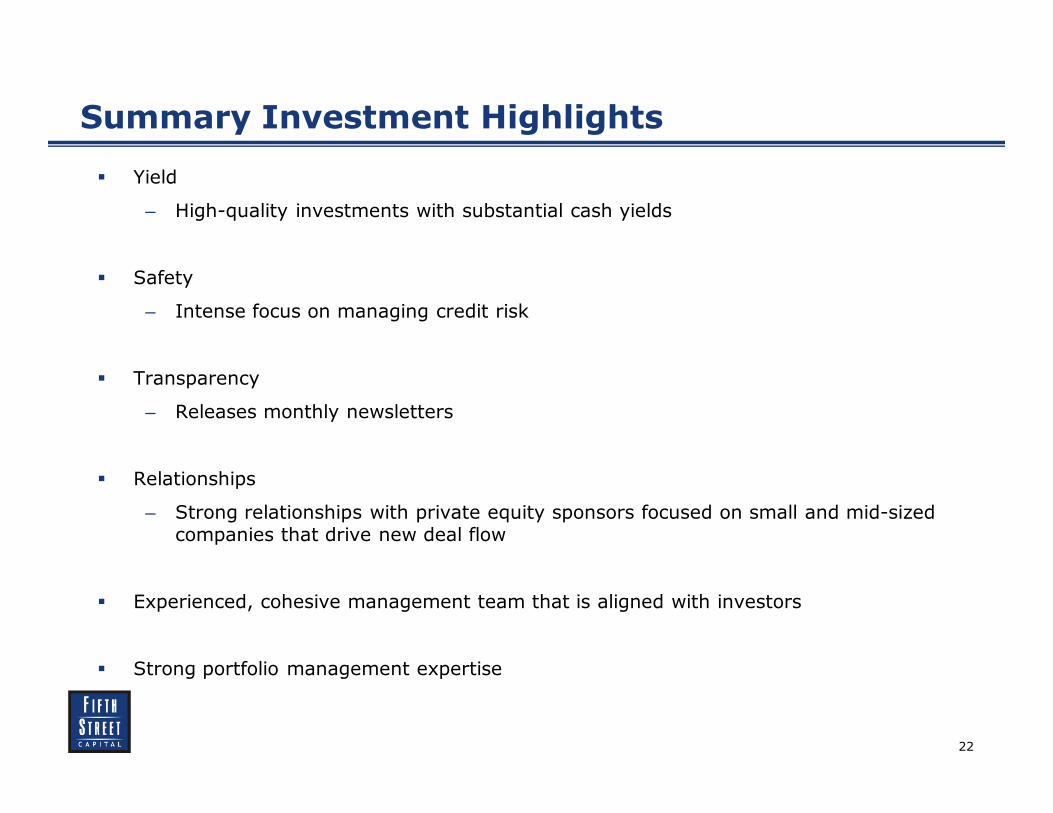

Summary Investment Highlights

� Yield

– High-quality investments with substantial cash yields

� Safety

– Intense focus on managing credit risk

� Transparency

– Releases monthly newsletters

� Relationships

– Strong relationships with private equity sponsors focused on small and mid-sized companies that drive new deal flow

� Experienced, cohesive management team that is aligned with investors

� Strong portfolio management expertise

23

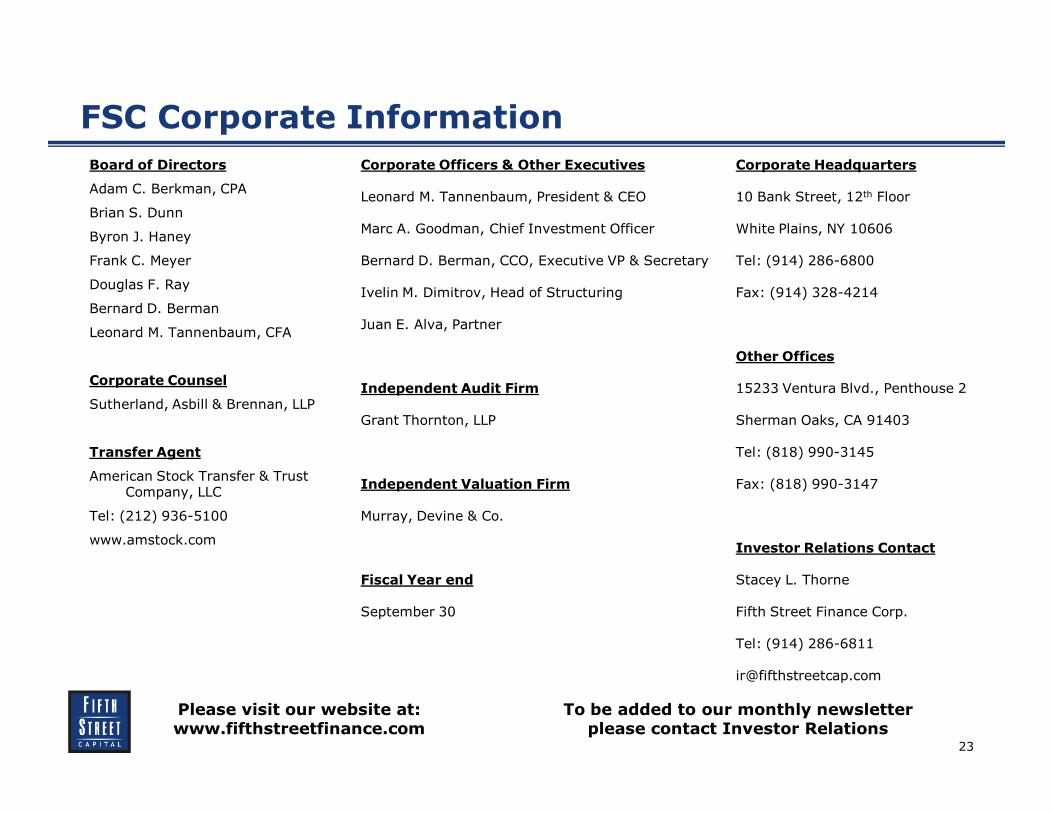

FSC Corporate Information

Board of Directors

Adam C. Berkman, CPA

Brian S. Dunn

Byron J. Haney

Frank C. Meyer

Douglas F. Ray

Bernard D. Berman

Leonard M. Tannenbaum, CFA

Corporate Counsel

Sutherland, Asbill & Brennan, LLP

Transfer Agent

American Stock Transfer & Trust Company, LLC

Tel: (212) 936-5100

www.amstock.com

Corporate Officers & Other Executives

Leonard M. Tannenbaum, President & CEO

Marc A. Goodman, Chief Investment Officer

Bernard D. Berman, CCO, Executive VP & Secretary

Ivelin M. Dimitrov, Head of Structuring

Juan E. Alva, Partner

Independent Audit Firm

Grant Thornton, LLP

Independent Valuation Firm

Murray, Devine & Co.

Fiscal Year end

September 30

Corporate Headquarters

10 Bank Street, 12th Floor

White Plains, NY 10606

Tel: (914) 286-6800

Fax: (914) 328-4214

Other Offices

15233 Ventura Blvd., Penthouse 2

Sherman Oaks, CA 91403

Tel: (818) 990-3145

Fax: (818) 990-3147

Investor Relations Contact

Stacey L. Thorne

Fifth Street Finance Corp.

Tel: (914) 286-6811

Please visit our website at: www.fifthstreetfinance.com

To be added to our monthly newsletter please contact Investor Relations

24

Research Coverage

James Shanahan (443) 263-6546 Christopher Harris (443) 263-6513

Troy Ward (314) 342-2714Greg Mason (314) 342-2194

David Chiaverini (212) 885-4115

Casey Alexander (212) 940-9276

John T.G. Rogers (202) 955-4316

James Ballan (212) 632-6762Tate Sullivan (212) 632-8246

John Arfstrom (612) 373-1785Andy Hedberg (612) 371-2709

BUY

BUY

OUTPERFORM

MARKET PERFORM

HOLD

BUY

OUTPERFORM

Robert Dodd (901) 579-4560 OUTPERFORM

25

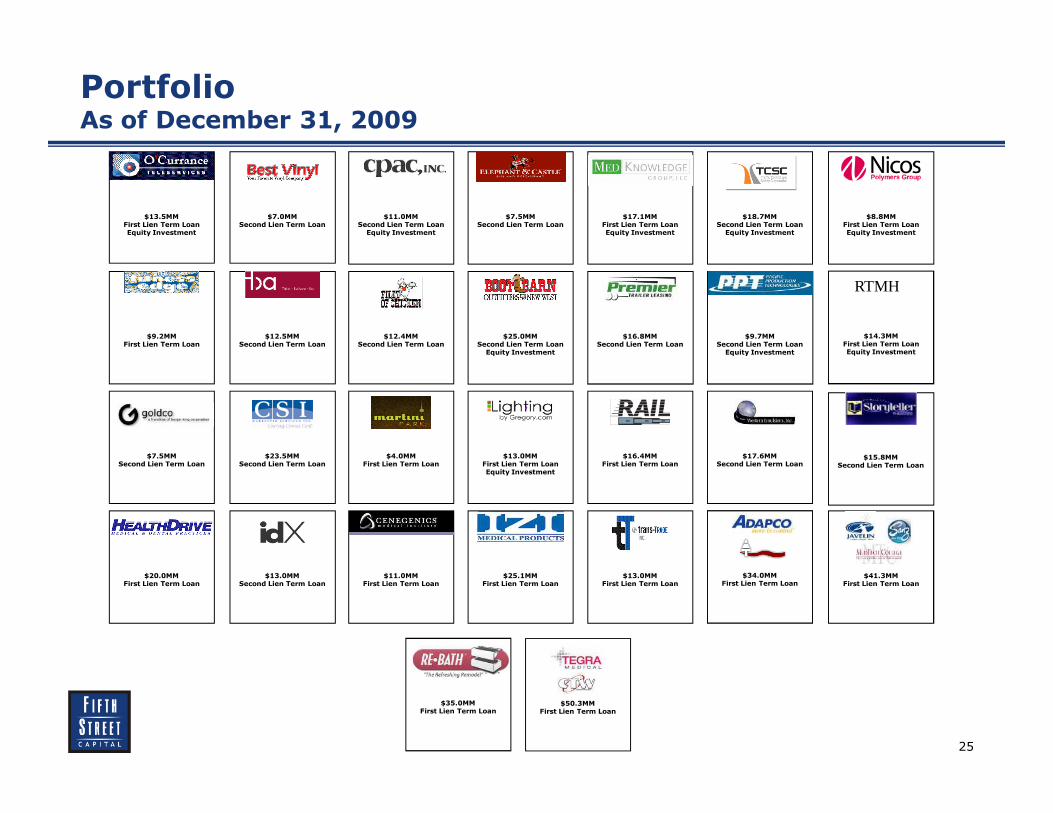

Portfolio As of December 31, 2009

$13.5MMFirst Lien Term LoanEquity Investment

$7.0MMSecond Lien Term Loan

$11.0MMSecond Lien Term LoanEquity Investment

$7.5MMSecond Lien Term Loan

$17.1MMFirst Lien Term LoanEquity Investment

$9.2MMFirst Lien Term Loan

$12.5MMSecond Lien Term Loan

$12.4MMSecond Lien Term Loan

$25.0MMSecond Lien Term LoanEquity Investment

$9.7MMSecond Lien Term LoanEquity Investment

$7.5MMSecond Lien Term Loan

$23.5MMSecond Lien Term Loan

$4.0MMFirst Lien Term Loan

$13.0MMFirst Lien Term LoanEquity Investment

$16.4MMFirst Lien Term Loan

$17.6MMSecond Lien Term Loan

$20.0MMFirst Lien Term Loan

$13.0MMSecond Lien Term Loan

$11.0MMFirst Lien Term Loan

$14.3MMFirst Lien Term LoanEquity Investment

RTMH

$15.8MMSecond Lien Term Loan

$18.7MMSecond Lien Term LoanEquity Investment

$16.8MMSecond Lien Term Loan

$8.8MMFirst Lien Term LoanEquity Investment

$25.1MMFirst Lien Term Loan

$13.0MMFirst Lien Term Loan

$34.0MMFirst Lien Term Loan

$41.3MMFirst Lien Term Loan

$35.0MMFirst Lien Term Loan

$50.3MMFirst Lien Term Loan