Embed Size (px)

Citation preview

FFY2012 FFY2012 EAP Annual EAP Annual TrainingTrainingSection 3Section 3

Includes Chapter 4 Application & Processing, Chapter 5 Program Eligibility, Chapter 6 Primary Heat, Chapter 7 Crisis and Chapter 8 ERR

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

2

Chapter 4 Chapter 4

Applications & Application ProcessingApplications & Application Processing

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

3

2011-2012 Minnesota Energy Assistance 2011-2012 Minnesota Energy Assistance Programs ApplicationPrograms Application

2011-2012 Energy Asst Prgms App - 144,527

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

4

2011-2012 Minnesota Energy Assistance 2011-2012 Minnesota Energy Assistance Programs Application - RecertificationPrograms Application - Recertification

Recertification Applications – 26,245

Differences between the Recert App and PreApp:

IF THERE IS NO CHANGE OF INCOME SINCE LAST YEAR YOU DO NOT NEED TO SEND PROOF OF INCOME

If your household income has changed, contact the agency listed on the front of this application for instructions.

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

5

Energy Programs Application Energy Programs Application Instructions and Privacy NoticeInstructions and Privacy Notice

2011-2012 App Instructions

2011-2012 Recert App Instructions

2011-2012 Privacy Notice

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

6

Completed by EAP staff from: Heartland Prairie Five Three Rivers

Request for volunteers for this year’s application, instructions and rights and responsibility

Spanish Version of ApplicationSpanish Version of Application

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

7

(Page 1, second paragraph)

“The last date to apply for EAP is May 31. Applications must be received or postmarked by May 31 to be processed for EAP eligibility and benefit payment.

Requests for applications may be logged as telephone or incomplete applications. As May 31 approaches, this practice can give households extra time to complete their applications. Households have until June 30 to provide any missing information…” July 2 – Actual last day to return any missing info

due to June 30, 2012 falling on a Saturday.

Chapter 4 – Apps and App ProcessingChapter 4 – Apps and App Processing

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

8

Information to Have Available When Information to Have Available When Entering ApplicationsEntering ApplicationsIncome: Income: (page 8-9)(page 8-9)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

9

Service Providers are required to use address standards to reduce the entry of duplicate addresses into eHEAT and prevent potential errors and fraud. Service Providers must follow the standards shown in Appendix 4G – Address Standards. If a standard is not listed in Appendix 4G, additional guidance can be found at the U.S. Postal Service website http://pe.usps.gov/cpim/ftp/pubs/Pub28/pub28.pdf

Address Standards (New) Address Standards (New) (page 9)(page 9)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

10

Address Standards Address Standards (cont.)(cont.)

Address Standards - 4G

The purpose of these standards is to assist EAP Service Providers to avoid entry of duplicate addresses into eHEAT, to reduce errors and fraud.Service Providers must correct current addresses in eHEAT

Use all UPPERCASE letters Enter directionals (N, S, E, W, NE, NW, SE, SW) last Only one space between words eHEAT Enhancement – ‘Personal Information’ screen says is if address is a duplicate when saved

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

11

Applicants sign the EAP application to authorize use of their private data to provide EAP services (see Chapter 14 - Data Practices and Records, page 9.) The signer must be an adult and can be any member

of the household named on the application. The signer is not required to be the Primary Applicant. Service Providers must confirm the signer is named on

the application and is an adult.

Signature RequirementsSignature Requirements (page 9)(page 9)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

12

Common Errors: App and eHEAT are not reviewed before mailing Not mailing the application to John Harvanko (p. 10-11) Not checking the “board member or employee” box before

determining eligibility. Not indicating how many HH members had income UI calculated incorrectly and/or first week of UI missing Addition errors

Excel spreadsheet for eligibility income is most accurate Year-to-date calculations are most accurate

Faxing crisis app without talking to staff (p. 11)

Employee ApplicationsEmployee Applications

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

13

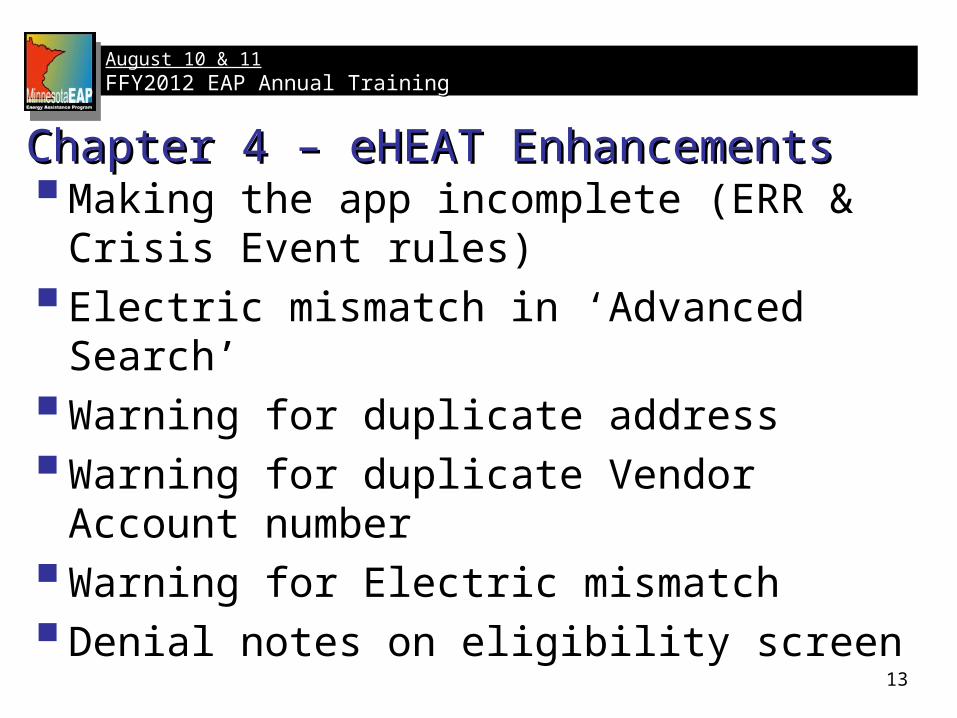

Making the app incomplete (ERR & Crisis Event rules)Electric mismatch in ‘Advanced Search’Warning for duplicate addressWarning for duplicate Vendor Account number Warning for Electric mismatchDenial notes on eligibility screen

Chapter 4 – eHEAT EnhancementsChapter 4 – eHEAT Enhancements

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

14

Making the application incomplete (ERR and Crisis Event rules) Any Crisis or ERR with $ attached results in:

Chapter 4Chapter 4

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

15

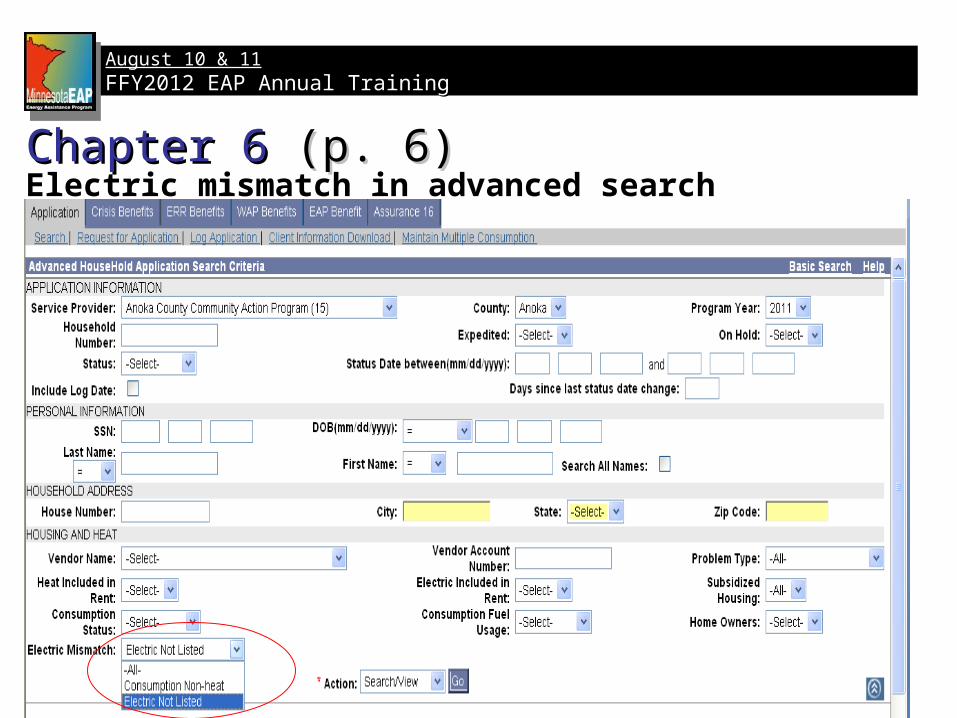

Electric mismatch in advanced searchChapter 6 Chapter 6 (p. 6)(p. 6)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

16

Warning for Electric mismatchChapter 6Chapter 6

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

17

Warning for duplicate addressChapter 4Chapter 4

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

18

Warning for duplicate Vendor Account number Chapter 4Chapter 4

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

19

Denial notes on eligibility screenChapter 4Chapter 4

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

20

Coordinator’s RoleQ & A: SSN Project & ApplicationQ & A: SSN Project & Application

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

21

Chapter 5 Program EligibilityChapter 5 Program Eligibility

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

22

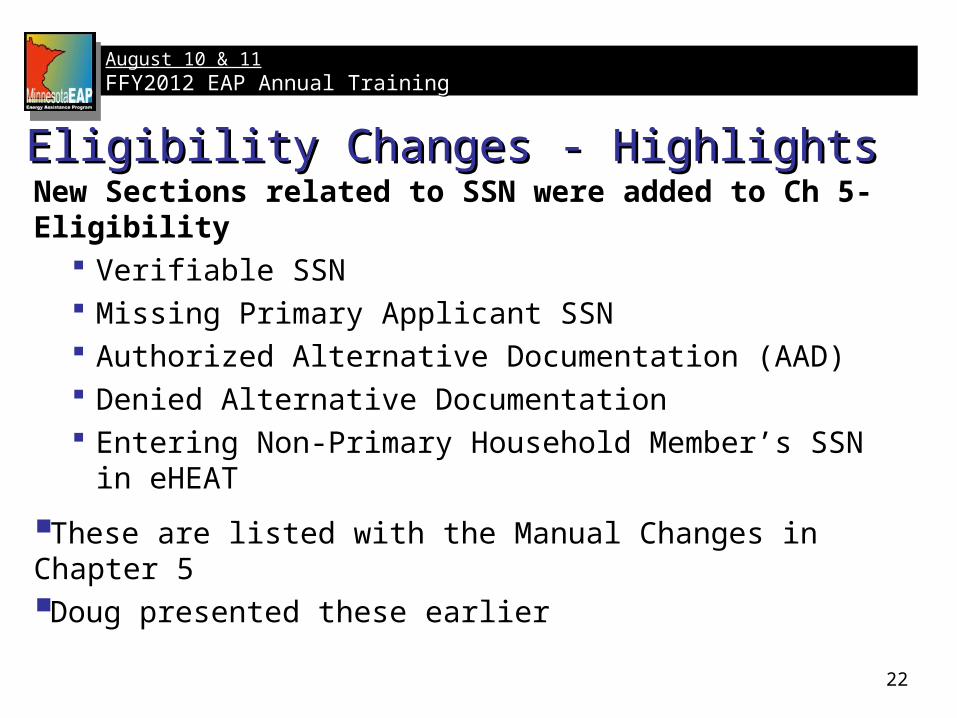

New Sections related to SSN were added to Ch 5- Eligibility Verifiable SSN Missing Primary Applicant SSN Authorized Alternative Documentation (AAD) Denied Alternative Documentation Entering Non-Primary Household Member’s SSN in eHEAT

These are listed with the Manual Changes in Chapter 5 Doug presented these earlier

Eligibility Changes - HighlightsEligibility Changes - Highlights

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

23

Household Changes Households Defined Households in Institutions Households with Shared Meters When the household situation changes New Appendix11F – eHEAT To-Dos when a HH moves

Income Documentation Differences in EAP versus WAP incomes and documentations Income Types now Excluded from EAP Countable Income

Combat Pay Child Support

Retirement Accounts (Medical Expenses withdrawals) Self Employment

Eligibility Changes - HighlightsEligibility Changes - Highlights

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

24

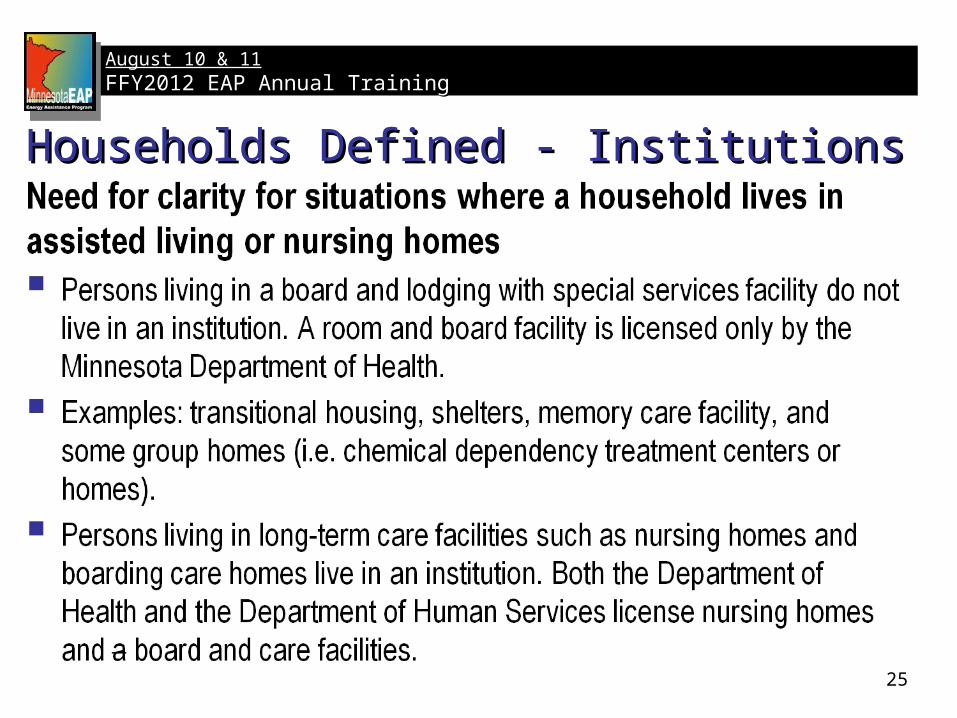

Household Definition A household includes all individuals who:

Live together as one economic unit. One economic unit is individuals who:

Occupy a residence, which has not been subdivided. Share a living area (bathroom, kitchen, living room).

and Are customarily provided residential energy in common or who make

undesignated energy payments in rent.

and Do not live in an institution.

EAP Households DefinedEAP Households Defined

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

25

Households Defined - InstitutionsHouseholds Defined - Institutions

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

26

Service Providers are responsible for knowing the nursing homes and board and care facilities in their service area.

Easiest solution is to call the home and ask; they will know what they are and who licenses them

Document what you learn in the household file.Can also use this information for future outreach

opportunities for those not in institutions.

Households Defined - InstitutionsHouseholds Defined - Institutions

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

27

A person who rents a room, does not share living area and does not share other dwelling or household costs is not a member of the landlord household.

Examples of other dwelling or household costs are food, shelter, heat and utilities.

This renter may apply as a separate household. An applicant who rents out a room to a renter must count the

rental income and may deduct rental expenses. These applicants must supply an IRS Form 1040 or should be

given a Self-Employed Income Worksheet to complete.

Households DefinedHouseholds DefinedLandlords & RentersLandlords & Renters

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

28

We are seeing more situations of households in creative housing situations. What are the state's preferences and intentions for handling these situations?Examples Include :

Owner of a house rents a room to help pay the mortgage Boarders, Roommates, Doubling Up, House Splitting and Sharing. Landlords that have the meter in their name and get the bill paid by

the tenants – either with some sort of flat rate, or monthly amount based on the bill

Not a surprise considering the current housing and economic situations that low to moderate income households are exploring creative housing

Guidance For HouseholdsGuidance For HouseholdsWith Shared MetersWith Shared Meters

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

29

What are the state's preferences and intentions for handling these situations? Intention is to provide households meeting the household definition with appropriate benefits paidDo the best we can with what we know.Review the Household definition first to determine what you’re dealing with –

Household sharing living space? Household sharing living expenses?

Flat rates or percentages

Guidance For Households With Shared MetersGuidance For Households With Shared Meters

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

30

Relevant bullets from Focus and Intentions for Eligibility

Use information provided on and supplied with the (complete) application to determine eligibility

Household size Determine eligibility based on program policies and available information (Corollary) Do the best we can with what we have Intentions: What we want to accomplish; our outcomes Summary: Simple and Fair

EAP Policy Manual FFY2012 Chapter 4 Applications & Application Processing Page 3 The EAP Application for new applicants provides the information necessary to determine

eligibility, and the applicant’s signature verifies that it is true.

Guidance For Households With Shared MetersGuidance For Households With Shared Meters

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

31

Documentation of Eligibility – At times more of an art than a scienceFirst and foremost is the documentation the application providesLease and other formal or written agreements Informal agreementsIf you have concerns, call the landlord and/or householdDocument the information in the household’s file with date and name/initials

Guidance For Households With Shared MetersGuidance For Households With Shared Meters

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

32

Prefer Payments in this order: pay the vendor account the landlord as a vendor Household directly (should be the exception)Backup Matrix The Eligibility Guidelines Table for the Backup Benefit Matrix

is used when… for households paying heat costs indirectly with their rent payment, for households with shared meters….

EAP Policy Manual FFY2012 Chapter 6 Primary Heat Page 3

Guidance For Households With Shared MetersGuidance For Households With Shared Meters

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

33

EAP Policy Manual FFY2012 Chapter 11 Benefit Payments and Refunds Page 4 Payments to Applicants Households may receive direct payments under circumstances that make payment to vendors difficult or

impossible. Direct payments will be distributed in one payment and not scheduled. Make direct payments to: Households with all energy utilities, electric and heat included in the rent. Households with heat included in rent, and only the amount that exceeds their electric costs for the previous year. Households whose vendors refused to sign the vendor agreement. Households unable to secure a vendor. Payments to Households with Account in Landlord’s Name If the household’s energy account is in the landlord’s name, it can be addressed as follows: Payments are made to the account on behalf of the household to the energy vendor. The landlord can become an EAP vendor. All agreement, registration and participation requirements are the

same for landlords as energy vendors (see Chapter 3 - Energy Vendors). Households may receive direct payments under circumstances that make payment to vendors difficult or

impossible.

HH with shared Meters –Payments – CH11HH with shared Meters –Payments – CH11

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

34

Know and understand that our guidelines including our definition of household are different than other economic assistance programs;

Food Support, for example, does not necessarily count every member living in the house as a member of the household.

The households that participate with both our program and economic assistance programs are often confused by this.

The major difference; we heat households; not individuals.

Households Sharing – Final ThoughtsHouseholds Sharing – Final Thoughts

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

35

Vendor account Name doesn’t match name listed on payment & vendor doesn’t know who payment is for. A few vendors don’t accept these payments. Response:Not an unusual situation, SP are familiar & resolve these issues all the time.When payments are made to a landlord’s vendor account for exampleSP staff should work with the vendor to manage the assignment of EAP payments to the appropriate accountPut account name in the vendor record & eHEAT Vendors can see the name on the account in the vendor screenVendors can export the search screen data to list the actual names on account and household number

Vendor Account Name v. EAP Primary ApplicantVendor Account Name v. EAP Primary Applicant

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

36

Refer to Chapter 11: Benefit Payments & Refunds for assistance with handling changes to the household’s situation during the program year. Examples of household situation changes include the household moving, adding or losing members, or combining with another household. Relevant after eligibility has been determined and/or payments have been made; that’s why this information is in Chapter 11Prior to determining eligibility; changes can be made to application; may require new application or new signature page.

Changes to Household’s SituationChanges to Household’s Situation

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

37

Household Member Moves

If any, but not all members move to a new dwelling: The EAP grant stays with the remaining household members Household members that leave the household must be

changed to “inactive” The members that moved may apply for an EAP grant at their

new residence; unless they join a current EAP household.

When Household’s Situation ChangesWhen Household’s Situation Changes

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

38

EAP Household Adds One Or More New EAP Or Non-EAP Member(s)

If household is joined during the EAP program year by EAP or non-EAP members:

The benefit amount is not reassessed Record the new household members information into

household file This change does not change the household’s eligibility for

EAP services for the current program year

When Household’s Situation ChangesWhen Household’s Situation Changes

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

39

EAP Households Combine If two or more EAP households combine into a new dwelling: Disburse any remaining PH benefits from both EAP households to

current address’ accounts Choosing which household to close: Close the household with the least remaining crisis benefit If neither household has received a crisis benefit, either can be closed

Work with the household to resolve EBA questions, because the newly combined household is only eligible for one EBA

When Household’s Situation ChangesWhen Household’s Situation Changes

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

40

If EAP Households Combine Into One Of The Households’ Current DwellingsChoosing which HH to close

Close the household application(s) with the least remaining crisis benefit (this may be the occupied dwelling.)

If neither HH received a crisis benefit; close the application from the vacated dwelling

Disburse any remaining PH benefits from the vacated address to the current address Work with the household to resolve EBA questions, because the newly combined household is only eligible for one EBA

When Household’s Situation ChangesWhen Household’s Situation Changes

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

41

For the application that remains open update the information as appropriate: Household member information (add new member information and deactivate those

who are no longer in the household.) Address Housing type Fuel type Vendors information including

Vendor name Account number Consumption – all consumption should be invalidated except the one for the

current dwelling Document in the notes section in eHEAT, including previous household number,

date of change and staff person who made the change.

When Household’s Situation ChangesWhen Household’s Situation Changes

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

42

Appendix 11F –

Handling Payments

and Refunds in

eHEAT When a

Household

Moves

Ch 11 Ch 11 Benefit Payments and RefundsBenefit Payments and Refunds

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

43

When a household moves within the Service Provider’s service areaThe vendor refunds any remaining EAP benefit in eHEAT so the Service Provider can re-

direct the payment to the household’s new vendor. Go into manage payment to remove schedule and then cancel any remaining

payments. Go to “Client Services” to update address, member, housing type, fuel type and

vendor information. Make notes in eHEAT regarding the change. Include previous household number, date of change, staff person who made the change and other information as appropriate.

Next go to “EAP Benefit”, select the household and click “Make Primary Heat payment.”

Finally, go to “Payment Services”, search for the household, manage the payment, choose new vendor and save.

Handling Payments and Refunds in eHEAT when a Household Handling Payments and Refunds in eHEAT when a Household MovesMoves

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

44

When a household moves to an unknown location Remove schedule Void payments (which will de-obligate the money)

When a household moves from another Service Provider Go to “Client Services” to update household and vendor information as

appropriate. If they have an EAP balance remaining, make payment to their new vendor(s)

by: Go to “EAP Benefit”, select the household and click “Make Primary Heat

payment.” Finally, go to “Payment Services”, search for the household, manage the

payment, choose new vendor and save.

Handling Payments and Refunds in eHEAT when a Household Handling Payments and Refunds in eHEAT when a Household MovesMoves

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

45

When a household moves from another Service Provider Go to “Client Services” to update household and vendor

information as appropriate. If they have an EAP balance remaining, make payment to

their new vendor(s) by: Go to “EAP Benefit”, select the household and click “Make

Primary Heat payment.” Finally, go to “Payment Services”, search for the household,

manage the payment, choose new vendor and save.

Handling Payments and Refunds in Handling Payments and Refunds in eHEAT when a Household MoveseHEAT when a Household Moves

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

46

For the application that remains open update the information as appropriate: Household member information (add new member information and deactivate those

who are no longer in the household) Address Housing type Fuel type Vendors information including

Vendor name Account number Consumption – all consumption should be invalidated except the one for the

current dwelling Document in the notes section in eHEAT, including previous household number, date of

change and staff person who made the change.

Handling Payments and Refunds in eHEAT when a Household Handling Payments and Refunds in eHEAT when a Household MovesMoves

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

47

DOE Excludes The Following From Income So To Increase Consistency Between Programs:Child Support payments received will no longer be counted as income when determining EAP eligibilityCombat Pay is not EAP countable incomeTribal Judgment Funds above $2,000; Only annual payments above $2,000. (This income is rare in Minnesota and is related to land acquisitions.)

Changes to the Household Employment Income Documentation section: The Green Thumb program is now called Experience WorksAdded that the use of pay dates is preferred to pay period end dates; when availableRemoved public records from the documentation list

Added to the List of Income Excluded From EAPAdded to the List of Income Excluded From EAP

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

48

Child Support Received By A Household Is Not Counted As Income For EAPDetermined to no longer count child support as income.When child support is the only household income, the household is not required to fill out a No Income Form; because they have income. Documentation of Spousal SupportStill considered EAP incomeDivorce Decree is appropriate documentation only if relevantWant to document what they are actually receiving; not what they were awarded, if they are not the same.Other documentation may be more appropriate if payments are not regularly being made.

Child Support Is No Longer EAP IncomeChild Support Is No Longer EAP Income

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

49

One change we did not make to match DOE is the documentation required from no income households. Do not be confused!

Although DOE is requiring households to provide a notarized statement if they have no income.

EAP has made no changes to the No Income Household documentation requirements; EAP will not be requiring a notarized statement from no income households.

Because DOE WAP accepts EAP eligibility for weatherization, the only households that should be affected by this change will be the ones that are “WAP Only Households”; that EAP does not determine eligibility for.

No Income Documentation; EAP vs. WAPNo Income Documentation; EAP vs. WAP

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

50

Request to Not Count Withdrawals from Retirement Accounts if Used for Medical expenses.Major Medical situations; HH can withdraw from retirement funds (in some cases) without penalty; if withdrawal is due to a major medical situation & they’re using money to pay medical bills.For example, the person is 60 and withdraws from a retirement account to pay medical bills related to a major medical situation. If they are older than 59 and ½; continue to count as income.

Withdrawal from Retirement Account for Medical ExpensesWithdrawal from Retirement Account for Medical Expenses

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

51

Retirement Income is complex and varies dramatically Many of the laws and rules that impact retirement income are often age

based; so this is where we started. We have determined that our approach to retirement income is primarily

to be determined by the age of the applicant. When an applicant is under 59 1/2 and withdrawing large amounts of

retirement income, this is a drawdown of assets. If the applicant is over 59½ and withdraws from a retirement account,

this is their income. These type of lump sums should be divided by four

Withdrawal from Retirement Account for Medical ExpensesWithdrawal from Retirement Account for Medical Expenses

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

52

Income is difficult to determine and documentSE income as income subset & even more complex EAP always tries to balance “simple and fair” for income determination; these values are often in conflict with each other. Begin with the desire to have as accurate of information as is possible regarding the household’s income that represents the household’s condition as closely as possible. For self employment income, this means collecting as many months of information as are available, up to one full year’s worth of self employment income and expenses.

Self Employment Income Self Employment Income

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

53

New Section added to manual: Self-Employment Income including Business, Farm and Rental IncomeProvides specific instructions for documenting and figuring self employment income.Changed how we figure Self Employment income by eliminating line 13 from the income included from the1040.Address and accommodate when self employment begins and ends.

Changes to Self Employment IncomeChanges to Self Employment Income

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

54

New Section added: Self-Employment Income including Business, Farm and Rental IncomeReceived a request for more specific instructionsLast year field reps found self employment income figured incorrectly; some consistency in the confusionProvided specific instructions for documenting and figuring self employment incomeNo changes to how it’s done, except for the following:

Changes to Self Employment IncomeChanges to Self Employment Income

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

55

Eliminating the use of Line 13 for SE Income Line 13 of 1040 not a business gain – It only includes personal

income from personal assets what we characterize as a "draw down of assets".

The instructions for line 13 and schedule D (which is where line 13 is actually figured) are very clear:

Line 13 should only include what they call "capital assets" which is "... property you own and use for personal purposes, pleasure or investment..." and NOT business income or assets.

Business gains and losses are to be reported on Line 14. So, discontinue the use of line 13 when figuring SE income.

Eliminate use of Line 13Eliminate use of Line 13

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

56

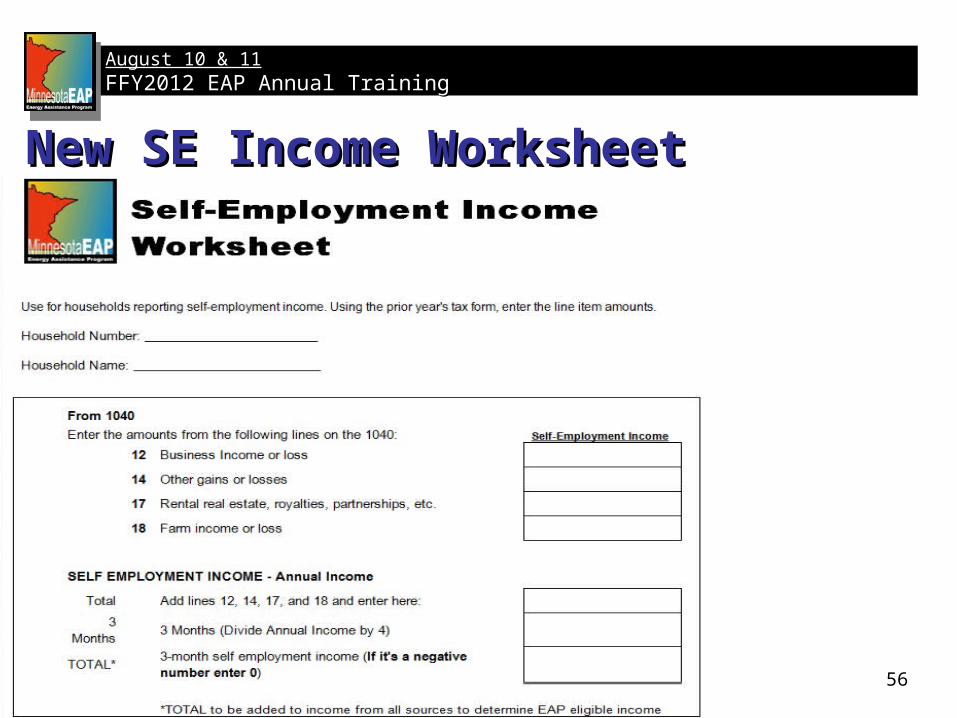

New SE Income WorksheetNew SE Income Worksheet

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

57

Appendix 5B Self-Employment Income WorksheetUse for households reporting self-employment income. Using the prior year's tax form, enter the line item amounts.

Household Number: ________________________

Household Name: __________________________

From 1040 Enter the amounts from the following lines on the 1040:

Line 12 Business Income or loss

Line 14 Other gains or losses

Line 17 Rental real estate, royalties, partnerships, etc.

Line 18 Farm income or loss

The way you figure self employment income remains the same; except for the exclusion of line 13 from the formula.

Self-Employment Income WorksheetSelf-Employment Income Worksheet

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

58

SE Income; Beginnings & EndingsSE Income; Beginnings & Endings Documentation of self employment income for EAP is the

most recent year’s Federal Tax Form 1040, provided it includes 12 months of self employment income.

If the household’s taxes do not include 12 months of self employment income, the household needs to complete and sign the Self-Employed Worksheet Cash Accounting Method (Appendix 5C) or if their business is a farm, the Self-Employment Worksheet: Farm Cash Accounting Method for Farms (Appendix 5D).

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

59

If the household was self employed for the entire previous tax (calendar) year and filed a 1040: Use Federal Tax Form 1040 and the Self-Employment Worksheet (Appendix 5B) to figure the household’s self employment income.

If the household was self employed for the entire previous tax (calendar) year but did not file a 1040:The household must complete and sign the Self-Employed Worksheet Cash Accounting Method (Appendix 5C) or the Self-Employment Worksheet: Farm Cash Accounting Method for Farms (Appendix 5D) if their business is a farm.

Self Employment Income DocumentationSelf Employment Income Documentation

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

60

If the household was not self employed for the entire previous tax (calendar) year (due to the opening or closing of the business) the household’s most recent tax form will not include 12 full months of self employment income, so their 1040 should not be used. Instead the household must complete and sign the Self-Employed Worksheet Cash Accounting Method (Appendix 5C) or if their business is a farm, the Self-Employment Worksheet: Farm Cash Accounting Method for Farms (Appendix 5D) to verify their income for EAP eligibility. In this instance, EAP can get the most accurate information regarding the household’s income by having the household use the cash accounting method worksheet.

SE Income – Partial YearSE Income – Partial Year

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

61

Business opening example: A household applies for EAP in March. They started their business in July of last year. The Federal Tax Form 1040 reports their business income or loss, but it is only

for the six month period from July until December of the previous year. In this instance the household should be completing a Self-Employed

Worksheet Cash Accounting Method (Appendix 5C) or the Self-Employment Worksheet: Farm Cash Accounting Method for Farms (Appendix 5D) if their business is a farm, for as many months as the business has been operating (up to twelve).

In this example, using the worksheet the household will provide eight months (July through February) of income information rather than the six months reported on the tax form.

SE Income – Business OpensSE Income – Business Opens

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

62

Business closing example: A household applies for EAP in March. They closed their business in January, during the EAP eligibility period. The Federal Tax Form 1040 reports their business income or loss, but it

does not include the no income period from January and February. In this instance the household should be completing a Self-Employed

Worksheet Cash Accounting Method (Appendix 5C) or the Self-Employment Worksheet: Farm Cash Accounting Method for Farms (Appendix 5D) if their business is a farm.

In this example, using the worksheet the household will provide twelve months of information and include the two months of no income; January and February.

SE Income – Business ClosesSE Income – Business Closes

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

63

In this example: The household should start with the first month prior to

application as the last month on the Self Employment Cash Accounting Worksheet and document all income and expenses for each month for the previous twelve months.

The income reported on the worksheet should be figured as instructed below.

Filling Out the Filling Out the

SE Cash Accounting WorksheetSE Cash Accounting Worksheet

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

64

Calculate and record self-employment income as follows: Regardless of documentation self employment income is

always calculated the same way; annualized and divided by four.

To calculate self-employment income: Business expenses are subtracted from the business income

for the entire previous year and then divided by 4 to get a three month income average that is used to determine EAP eligibility.

Self Employment Income - CalculationSelf Employment Income - Calculation

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

65

Coordinator’s RoleQ & A: EligibilityQ & A: Eligibility

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

66

Chapter 6 Primary HeatChapter 6 Primary Heat

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

67

Training will cover: New policy/procedure added to primary heat benefit

determination when electricity is not the primary heating fuel Primary heat benefit requirement clarifications Collecting consumption data clarifications eHEAT enhancement - Recalculating Primary Heat Can

Reduce an Existing Benefit

Chapter 6 Primary HeatChapter 6 Primary Heat

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

68

EAP policy/procedure regarding electric heat changed a couple years ago due to more households heating with electricity

Procedure to include all electric cost if electricity is used to heat one or more rooms

Since then there have concerns about the EAP primary heat benefits being to high when electricity is not the primary heating fuel Not the fuel with the highest heating cost)

Policy and procedures reviewed for FFY2012

Electric Heat - JADedElectric Heat - JADed

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

69

What we know about heating fuelsWhat we know about heating fuelsPercent of Heat by Fuel Type – One Heating Fuel Oil/Biofuel 100.0% Propane 91.7% Natural Gas 79.3% Electricity 51.7%Approximately 1/2 of the electric cost is for heating use

if electricity is the only heating fuel

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

70

100% electric heat is 52% of electric cost As a household uses other heating fuels, the percent

of electricity used for heating goes down Electric heat in only one bedroom on average would

to be a small percent of the total electric cost when most of the dwelling’s heat comes from another fuel type

What about electricity is not the primary heating fuel? (Electricity is not the fuel with the highest heating cost)

Electricity as a heating fuelElectricity as a heating fuel

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

71

Examples from FFY2011 policies and procedures when electricity is a heating fuel:If oil cost was $900 and electricity was $1,100, the total cost of $2,000 is calculated at the percent for ElectricityIf oil cost was $1,100 and electricity was $900, the total cost of $2,000 is calculated at Oil’s percentage

Primary Heating Fuel Is Based on Primary Heating Fuel Is Based on Highest CostHighest Cost

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

72

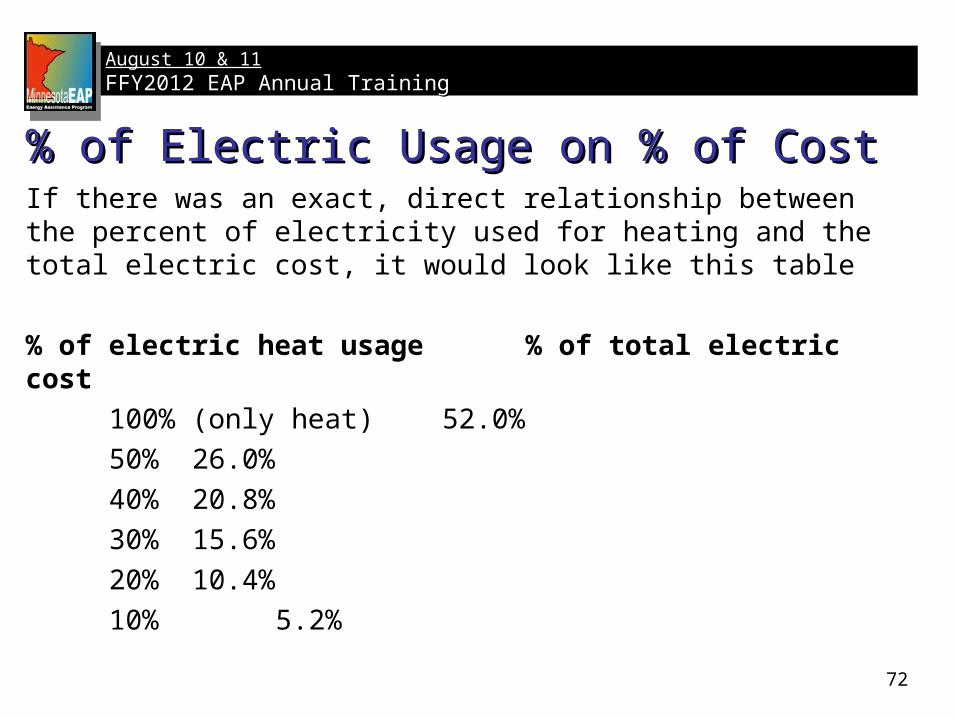

% of Electric Usage on % of Cost% of Electric Usage on % of CostIf there was an exact, direct relationship between the percent of electricity used for heating and the total electric cost, it would look like this table

% of electric heat usage % of total electric cost

100% (only heat) 52.0% 50% 26.0% 40% 20.8%30% 15.6%20% 10.4%10% 5.2%

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

73

JAD SMEs and DOC staff agree there is a problem regarding secondary electric & including & calculating all electric cost as if it were a fuel with a higher percent used for heating. (From previous example: oil cost was $1,100 and electricity was $900, the total cost of $2,000 is calculated at oil’s percentage)

Resolution: Use one half of the total electric cost. In the example above, $1,550 is calculated at the oil percentage. (eHEAT does the calculation. Consumption record will not change)

Decision Regarding Electric HeatDecision Regarding Electric Heat

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

74

Benefit Determination Benefit Determination (Chap. 6, p. 2.)(Chap. 6, p. 2.)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

75

Clarifications (Chapter 6, p 1): For current winter’s heat costs to degree possibleApply only to the HH account designated by EAPCannot be used to pay for other items such as service

contracts, water, sewer, garbage or other merchandise

PH benefits can be applied to no heat situations when Crisis funds are inadequate

Primary Heat Benefit RequirementsPrimary Heat Benefit Requirements

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

76

Clarification (cont.)When Crisis funds are inadequate, Primary Heat can be used for: Payments due & past due amounts for electricity & heating fuels. Continuation or reconnection of connected utilities. Payments for service deposits, minimum delivery requirements

and costs, pressure tests, leak seek, line bleeding, tank setting, tank rental, membership fee, emergency fuel and after hours delivery costs if applicable.

Removal from load limiters.

Primary Heat Benefit RequirementsPrimary Heat Benefit Requirements

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

77

Any 12 consecutive months between June 1, 2010 and September 30, 2011Include the entire previous heating season (Oct – May)Never combine portions of two heating seasonsAllowable periods are (only 5):

1. June 1 – May 312. July 1 – June 303. August 1 – July 314. September 1 – August 315. October 1 – September 30

Collecting Consumption DataCollecting Consumption Data (Chap 6, p 4) (Chap 6, p 4)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

78

If less than 12 months of consumption data exists for the residence, report the available cost and the actual beginning and ending dates of the available consumption data.This is for instances when a household has not been a vendor’s customer for a full 12-month consumption periodA new customer that started in August will have 10 months (August – May) of reported consumption, if a vendor uploads consumption from June 1 to May 30 for all households. A consumption request for the household on October 1 or after will include a full 12 months.If no consumption exists for the residence, report as “unavailable.”

Collecting Consumption Data Collecting Consumption Data (cont.)(cont.)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

79

If no consumption exists for the residence, report as “unavailable.” Vendors may have a policy to not report a monthly list of

consumption data for a dwelling for a previous customer Vendors should report summary data in these instances

Collecting Consumption Data Collecting Consumption Data (cont.)(cont.)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

80

When there is a break in the service for connected utilities, then consumption must be entered for each length of service. If energy service was disconnected for 30 days or more during the 12 month consumption period, multiple consumption reports are needed to exclude the months with no service. For example: A household has been a long term customer and between June 1 and May 30 they were disconnected for the months of December and January. Two entries are needed to accurately report consumption. The first report is from June 1 to November 30 and the second report is from February 1 to May 30.

Collecting Consumption Data Collecting Consumption Data (cont.)(cont.)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

81

For delivered fuels: If a household has a customer account for 12 consecutive months, report the entire 12-month period. Do not just show the first and last delivery dates. For example: A household has been a long term customer and received three LP deliveries (9-1, 12-1 and 3-1) between June 1 and May 30. The correct date range is June to May … not September to March.

Collecting Consumption Data Collecting Consumption Data (cont.)(cont.)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

82

The Recalculate Primary Heat Benefit (RPHB) function can now reduce an existing benefit when it is discovered that application or consumption information does not accurately reflect a household’s situation. Reducing a benefit works the same way as increasing a benefit, but with one additional step.

eHEAT – Recalculating Primary Heat Can eHEAT – Recalculating Primary Heat Can Reduce an Existing BenefitReduce an Existing Benefit

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

83

First, changes are made in the application or consumption information that would result in a benefit reduction

Then a portion of the existing benefit must be de-obligated. The amount of the de-obligation must equal or exceed the amount

the benefit is to be reduced

After changes to the application/consumption information and the de-obligation occur then a reduction of benefit is possible using the RPHB function

eHEAT – Reduce Benefit eHEAT – Reduce Benefit (cont.)(cont.)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

84

Primary Heat Benefit Needs ReducingPrimary Heat Benefit Needs ReducingChanges to application or consumption information result in a benefit reduction

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

85

Enter the Correct ConsumptionEnter the Correct ConsumptionIf consumption update the information

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

86

Next Void Payment(s)Next Void Payment(s)On ‘Payment’ tab select payment and void

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

87

This makes $700 De-obligatedThis makes $700 De-obligated

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

88

Choose HH from Search Select Recalculate Primary Heat Benefit from Manage Application pull-down. Then click ‘Go’.

Go to Benefit Adjustment ScreenGo to Benefit Adjustment Screen

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

89

Add Note and Click ‘Recalculate’Add Note and Click ‘Recalculate’

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

90

Check the Status MessageCheck the Status MessageA payment without a vendor attached will be created if the amount de-obligated exceeded the amount of the benefit reduction. ■If the de-obligation equals the benefit reduction, no payment is created. ■If the de-obligated amount is less than the amount of the reduction, the recalculation will fail and be indicated in the status message.

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

91

Certifiable or Payable payments can be voided as shown in slide above or when processing a refund. De-obligation occurs when the ‘De-obligation’ button is clicked. If you are reducing a benefit where payments are paid you may request the exact amount of the reduction as a refund from the vendor. This would produce no payment when the benefit is recalculated.If a household is no longer eligible after the changes made to the application then all payments must be de-obligated before RPHB function is used.

Note: Two Ways to De-obligate PaymentsNote: Two Ways to De-obligate Payments

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

92

Coordinator’s RoleQ & A: Primary HeatQ & A: Primary Heat

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

93

Chapter 7 CrisisChapter 7 Crisis

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

94

Chapter StructureCrisis Policies and ProceduresEmergency Benefit Adjustment (EBA)Crisis Categories and TimelinesCrisis Assistance - Accessible 24/7Using eHEAT for Crisis

Chapter 7 CrisisChapter 7 Crisis

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

95

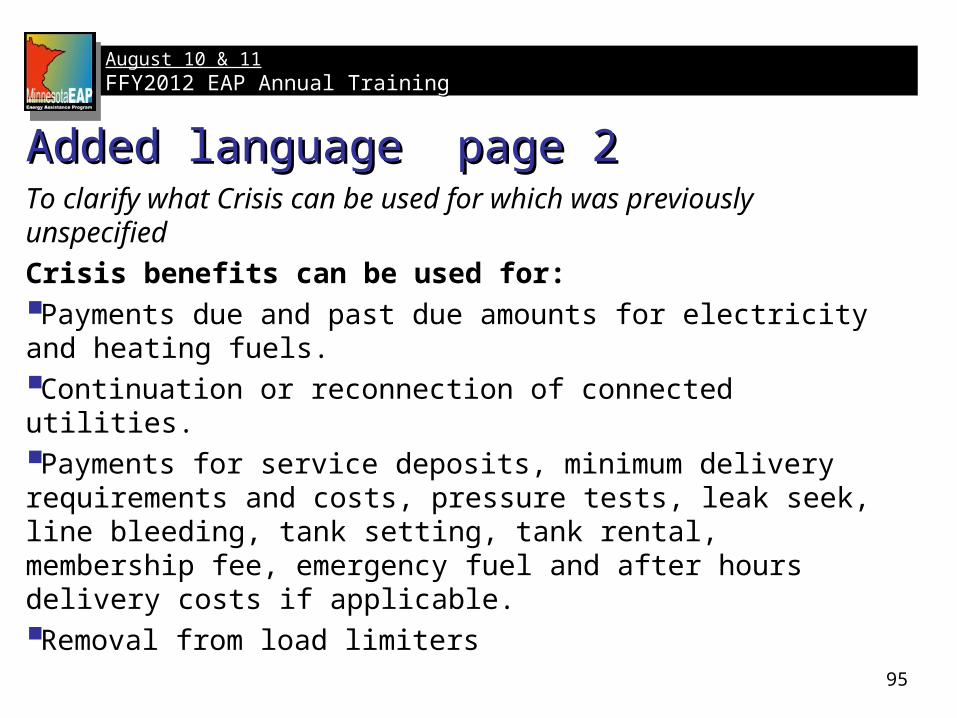

To clarify what Crisis can be used for which was previously unspecified

Crisis benefits can be used for:Payments due and past due amounts for electricity and heating fuels. Continuation or reconnection of connected utilities.Payments for service deposits, minimum delivery requirements and costs, pressure tests, leak seek, line bleeding, tank setting, tank rental, membership fee, emergency fuel and after hours delivery costs if applicable.Removal from load limiters

Added language page 2Added language page 2

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

96

eHEAT Improvement eHEAT Improvement A16 Access Button

From the Crisis screen an A16 activity can be entered using this button

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

97

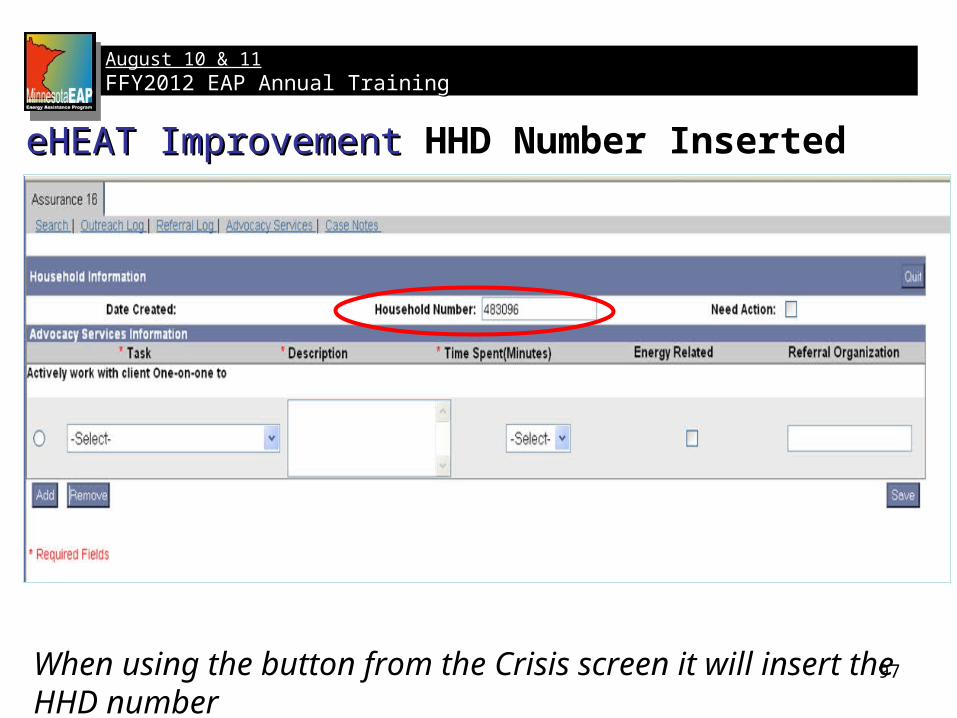

eHEAT Improvement eHEAT Improvement HHD Number Inserted

When using the button from the Crisis screen it will insert the HHD number

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

98

eHEAT enhancementeHEAT enhancementManage ERR From Eligibility Screen

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

99

Allowable activity in vendor agreement Tank setting with primary heat and crisis fundsERR section has limitations The Manual Implementations Include:

Chapter 6 – PH page 1 Chapter 7 – Crisis page 3 Chapter 8 – ERR page 3 and 6

FFY12 Tank Setting ClarificationFFY12 Tank Setting Clarification

SP asked to get clarification on tank setting. This effort included looking at what was said about all benefit categories and clarifying fund usage. The effort expanded beyond tank setting

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

100

Can be costly: price differ from vendor to vendorExamples:

Tank Setting - continuedTank Setting - continued

No charge if within normal prox. of house & if they become a regular customer of theirs

$50 hr. + mileage $350 (includes 2 regulators,

15 ft. copper, mileage $100 + pipe and fittings

$250 - $500 $65 $201 variable They charge $80/hr. Approx. 1 to

½ hrs. plus: $68 regulator $27.50 line (min.) $20.00 misc.

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

101

Primary Heat, Chapter 6, page 1Payments for service deposits, minimum delivery

requirements and costs, pressure tests, leak seek, line bleeding, tank setting, tank rental, membership fee, emergency fuel and after hours delivery costs if applicable.

Tank Setting (continued)Tank Setting (continued)

None of this language previously appear in chapter 5 but came from other EAP information including Vendor agreement and chapters.

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

102

Crisis - Chapter 7, page 3

Continuation or reconnection of connected utilities.Payments for service deposits, minimum delivery

requirements and costs, pressure tests, leak seek, line bleeding, tank setting, tank rental, membership fee, emergency fuel and after hours delivery costs if applicable.

Tank Setting (continued)Tank Setting (continued)

None of this language previously appear in chapter 7 but came from other EAP information including Vendor agreement and chapters.

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

103

Chapter 8 reference: page 3ERR cannot be use for tank setting for changing fuel

types or vendors when the household elects to change fuel or vendor and does not meet the requirement for medical or fuel change allowable under ERR. (See “Elective Fuel Type Changes”)

Setting fuel tanks (“Medically Necessary Fuel Type Changes” sections for exception)

Tank Setting (continued)Tank Setting (continued)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

104

Coordinator’s RoleQ & A: CrisisQ & A: Crisis

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

105

Chapter 8 Energy Related RepairChapter 8 Energy Related Repair

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

106

Time Frames for ERR ServiceAssistance Limit ProcurementMechanical Equipment and Work StandardsVerification/Completion Certificates/PaymentsPaymentsERR File DocumentationWalk Away Policy

Chapter 8 Energy Related RepairChapter 8 Energy Related Repair

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

107

ERR TimelinesERR form update and refresher Furnace in harms wayClarification of ERR policiesAdded a question to ERR TTT

ERR TopicsERR Topics

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

Section 2604 (C) (1) and (2) The program rules state ERR event must be

addressed within 48 hours from the date initiated (Or 18 hours in life threatening situations)

Always remember: Safety First!

LIHEAP Federal LawLIHEAP Federal LawERR Timelines ERR Timelines (From Manual & Law)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

109

Local deliverers (Program – State, SP, energy vendors & mechanical contractors) must implement a process to assure the safety of the client.

Secure vendors that know the program timelines and can reliably meet them

Secure vendors that have the capacity and commitment to supply the client with adequate temporary heat if the work will take longer than 18 hours.

As an alternative, Service Providers may supply temporary heat sources. Check with your Service Provider attorney regarding liability.

ERR Timelines ERR Timelines (From Manual & Law)

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

110

Largest single benefit to households - responsible management of resourcesUse your SP’s Fiscal Internal ControlsDocumentation: InvoicesMost important is to get all contractors on the same page when doing businessContractor meetings

building relationships All policies as well as timelines

A16 to conduct the meetings

ERR DocumentationERR Documentation

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

111

New ERR Form Combines ERR Forms into one Excel Workbook– ERR Troubleshooting– ERR Tracking– ERR Completion Certificate– ERR Inspection Forms

ERR Completion Certificate

Household Name: Household #

Address: 2010 ERR Place, Any City, MN 54321

Telephone: (218) 555-1234 Emergency Phone:

Contractor:I certify that the work authorized by is complete. All work conforms

Name of Firm Contractor License Number

Date Work Started

Number to call us, if problems (_____) _______ - ______________ Date Work Completed

FOR REPLACEMENTS ONLY:

Manufacturer Model Number Serial Number

Date of required pressure test (LP or Natural Gas) Pressure test results(after Gas or Manifold valve)

Test Comment(s):

Homeowner:I certify that the contractor has delivered the materials and completed the work listed on the work order. The EAP ServiceProvider may pay the contractor on my behalf.

Signature of Homeowner Date

Inspector: (WHEN REPLACEMENT IS SELECTED FOR INSPECTION)

I certify that the contractor has delivered the materials and completed the work listed on the work order. The EAP ServiceProvider may pay the contractor.

Signature of Inspector Date

Fixet, Anita 123456

Authorized Signature of Firm Date

to all standards and codes that apply. All work meets the agreements between this firm and the Energy Assistance Program Service Provider. All the work performed by this firm is subject to and follows manufacturer and contractor warranties.

ERRERR

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

112

New ERR Form Download information functionality– In eHEAT, Go to ‘Client Services’ Menu/’Application Application’ pull

down/’Reasonable Payment Export’ Not real data

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

113

New ERR Form Open ERR Download Template– Copy data from download file– Paste data into ‘Download’ worksheet from the export– Information is on all forms

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

114

New ERR FormPaste from Download file to ERR Form

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

115

Description of need: Explain the existing conditions that make the request necessary

Explain how the problem (existing condition) will be fixed so that the household has a safe and reliable source of heat.

Must have all information completed and updated ERR Service Information Section– Activity Dates Make notes on timelines if it looks like you are not

going to make the timeline (when in doubt, write it out)

ERR Tracking Form is MandatoryERR Tracking Form is Mandatory

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

ERR Form WalkthroughERR Form Walkthrough

116

ERR Form

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

117

Chapter 8, page 6 – Assistance LimitsWhen a household’s furnace needs replacing due to

an event (i.e., flooding, sump pump failure, sewer backup, etc.) evaluate the probability of the event reoccurring.

Service Providers must assess the situation to determine if conditions warrant additional measures to prevent similar event damage to the new furnace.

Furnace in Harms WayFurnace in Harms Way

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

118

Contractor recommendations may include raising the furnace off the floor or relocating the furnace to an event-free location.

If the household refuses to allow ERR measures recommended by the heating contractor and authorized by the Service Provider to safeguard the new furnace from potential event damage, implement the Walk Away Policy if there is no viable alternative.

ERR Furnace in Harms WayERR Furnace in Harms Way

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

119

Relocating the new furnace to area where it will not get harmed

Floods: consider alternatives in repeated disasters Becomes a contractor recommendation

Furnace in Harms wayFurnace in Harms way

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

120

Chapter 8 page 3 – Delete list from Pg 1 & Combine on Pg 3 ERR may not be used for:

Non emergency repairs or replacements Repairs or a replacement not initiated by the EAP Service Provider Unoccupied dwellings A dwelling that currently does not have an installed furnace Rental units Structures not meeting the definition of a “Dwelling Unit” (See “Dwelling Unit Definition”

section below) Setting fuel tanks (See “Elective Fuel Type Changes” and “Medically Necessary Fuel

Type Changes” sections below for exception) Secondary and redundant heating systems Portable heaters being used as a furnace

ERR re-write sectionERR re-write section

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

121

ERR funds can be used to repair or replace a furnace if the furnace was not working or needed replacing at the time the household purchased the dwelling. A policy was implemented several years ago, but was removed after a couple of years because proving the household knew the furnace was inoperative at the time of sale was difficult or impossible. It was argued that often the furnace failed after the purchase when the household needed to start using the furnace in the fall. Additionally age, stress or metal fatigue finally took its toll on the furnace or the household was unaware of the problem and should not be denied service for these reasons.

Clarification of ERR PolicyClarification of ERR Policy

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

122

Contractor List & Pull down Alpha OrderContractor List & Pull down Alpha Order

August 10 & 11August 10 & 11FFY2012 EAP Annual TrainingFFY2012 EAP Annual Training

123

Coordinator’s RoleQ & A: ERRQ & A: ERR