Embed Size (px)

DESCRIPTION

t

Citation preview

Foodservice Equipment Reports ©2014 1

How Big U.S Chains And

Institutions Purchase Equipment

And Select Suppliers

By Robin Ashton, Publisher,

Beth Lorenzini, Editor-In-Chief

Foodservice Equipment Reports

Hotelex, Shanghai, P.R. of China

31 March, 2014

Foodservice Equipment Reports ©2014

Researching How Multiunit Operators

Buy E&S And Choose Suppliers • Big chain, institutional and other multiunit foodservice

operators rule the U.S. and global markets.

• They continue to grow and gain market share everywhere.

• In the U.S. market, they clearly purchase a majority of all

new equipment and supplies.

• As multiunit operators, they have unique needs and much

more complex specification and purchasing processes.

• To better understand these needs, processes and the

criteria they use to evaluate and choose E&S suppliers,

FER undertook exclusive new research.

Foodservice Equipment Reports ©2014

Researching How Multiunit Operators

Buy E&S And Choose Suppliers • During the past year, FER surveyed first chain and other

commercial operators, then large institutional operators;

FER’s exclusively multiunit operator circ. lists were used.

• The 16-question surveys, specific to commercial and

noncommercial segments, were e-mailed using Survey

Monkey research software.

• The questionnaires probed which functions are involved in

spec and purchase decisions, outside influences with input,

and criteria used in supplier and brand selection.

• We received 99 complete commercial surveys and 124

complete noncommercial surveys.

Foodservice Equipment Reports ©2014

Researching How Multiunit Operators

Buy E&S And Choose Suppliers • The research is not designed to be statistically accurate, but to

serve as a guide to how these large organizations evaluate and

select E&S products and specific suppliers.

• We, of course, found that there is a great deal of diversity in

criteria and procedures in these complex organizations.

• Few operators organize their E&S spec and purchasing

operations exactly the same.

• But there are commonalities that the research reveals.

• Some of it may surprise you; it did us.

• But before we dig into the research, let’s do an overview of the

structure and typical spec processes in the U.S.

Foodservice Equipment Reports ©2014

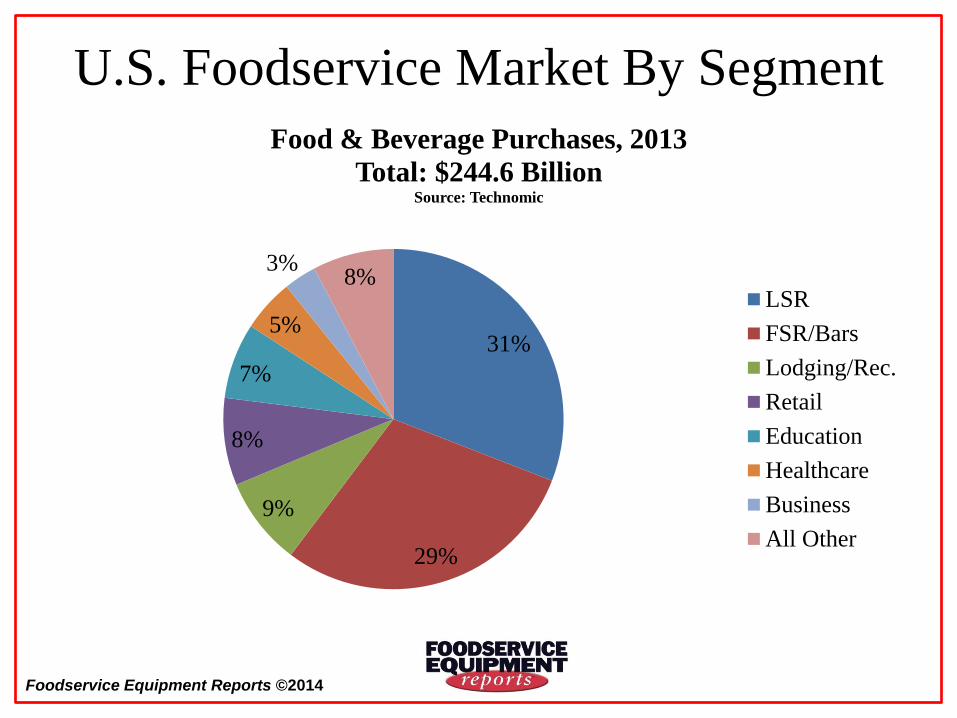

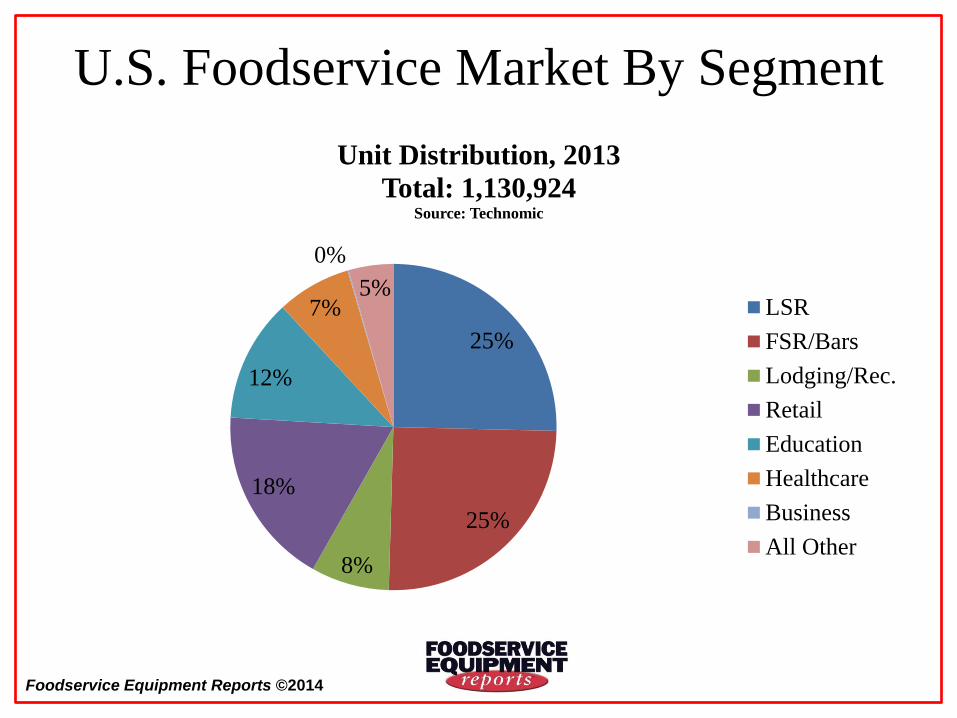

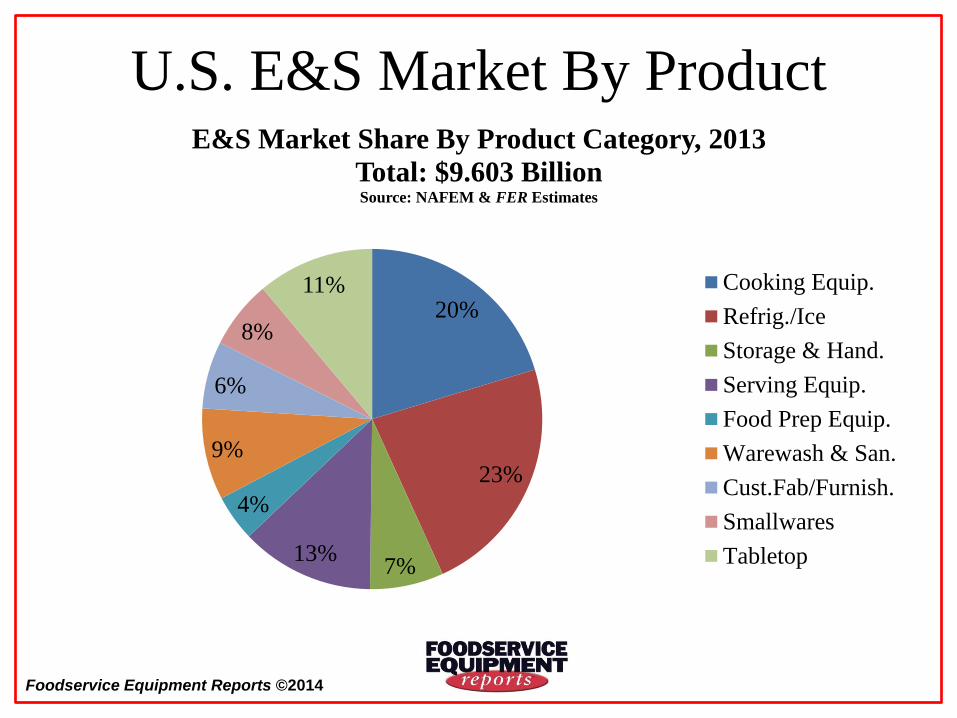

U.S. Foodservice & Equipment Markets

• The foodservice market in the United States is huge,

complex, diverse and relatively mature.

• Chicago-based research firm Technomic Inc. estimates

U.S. market at end-user level at US$682 billion in 2013.

• Technomic details 20 foodservice “segments,” purchasing

$245 billion of food, beverages and non-foods in ’13.

• NAFEM/FER estimates equipment and supplies market at

$9.6 billion in’13 at manufacturer level.

• Equipment accounts for 82% of total U.S./Canada E&S

market, durable supplies and tabletop 18%.

Foodservice Equipment Reports ©2014

U.S. Foodservice Market By Segment

31%

29%

9%

8%

7%

5%

3% 8%

Food & Beverage Purchases, 2013

Total: $244.6 Billion Source: Technomic

LSR

FSR/Bars

Lodging/Rec.

Retail

Education

Healthcare

Business

All Other

Foodservice Equipment Reports ©2014

U.S. Foodservice Market By Segment

25%

25%

8%

18%

12%

7%

0%

5%

Unit Distribution, 2013

Total: 1,130,924 Source: Technomic

LSR

FSR/Bars

Lodging/Rec.

Retail

Education

Healthcare

Business

All Other

Foodservice Equipment Reports ©2014

U.S. E&S Market By Product

20%

23%

7% 13%

4%

9%

6%

8%

11%

E&S Market Share By Product Category, 2013

Total: $9.603 Billion Source: NAFEM & FER Estimates

Cooking Equip.

Refrig./Ice

Storage & Hand.

Serving Equip.

Food Prep Equip.

Warewash & San.

Cust.Fab/Furnish.

Smallwares

Tabletop

Foodservice Equipment Reports ©2014

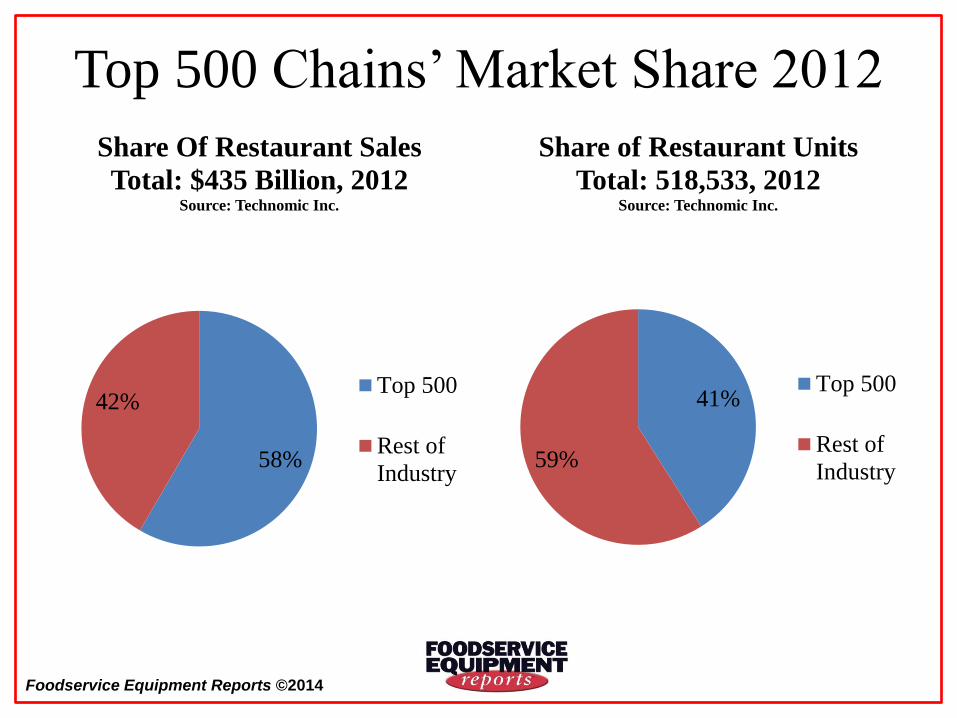

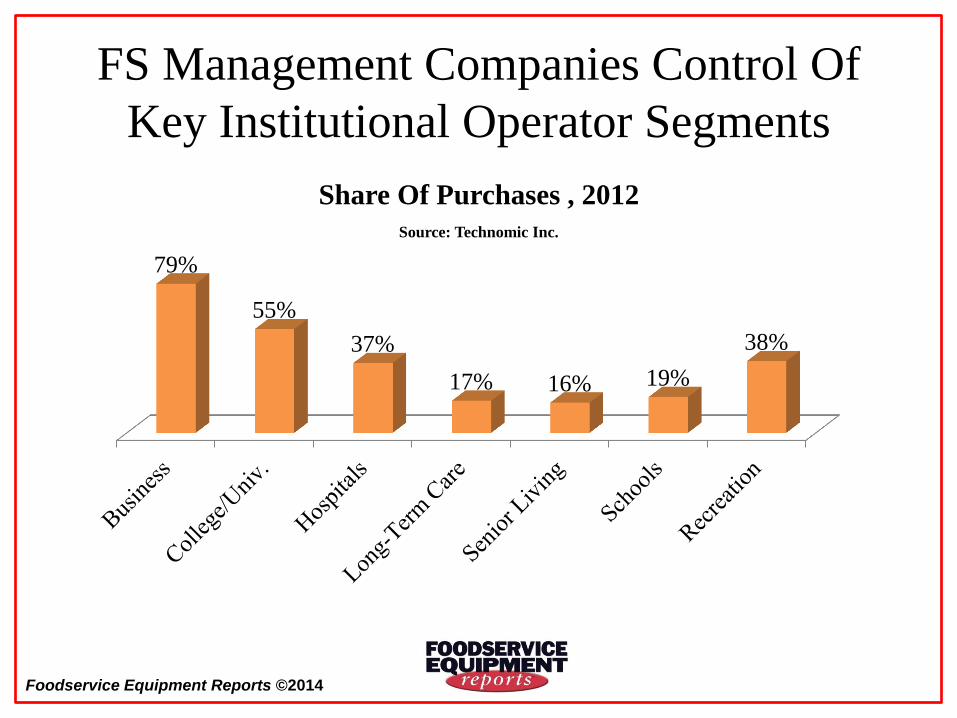

Operator Market Structure

• There are 1.3 million foodservice kitchens in the U.S., but

“it’s a multiunit world.”

• U.S. foodservice is dominated by chain and other

“multiunit” operators including foodservice management

companies and big institutional operators.

• Top 500 chain concepts control nearly 60% of restaurant

sales and 40% of all units.

• On the institutional side of foodservice, management

companies operate 20% to 80% of key segments.

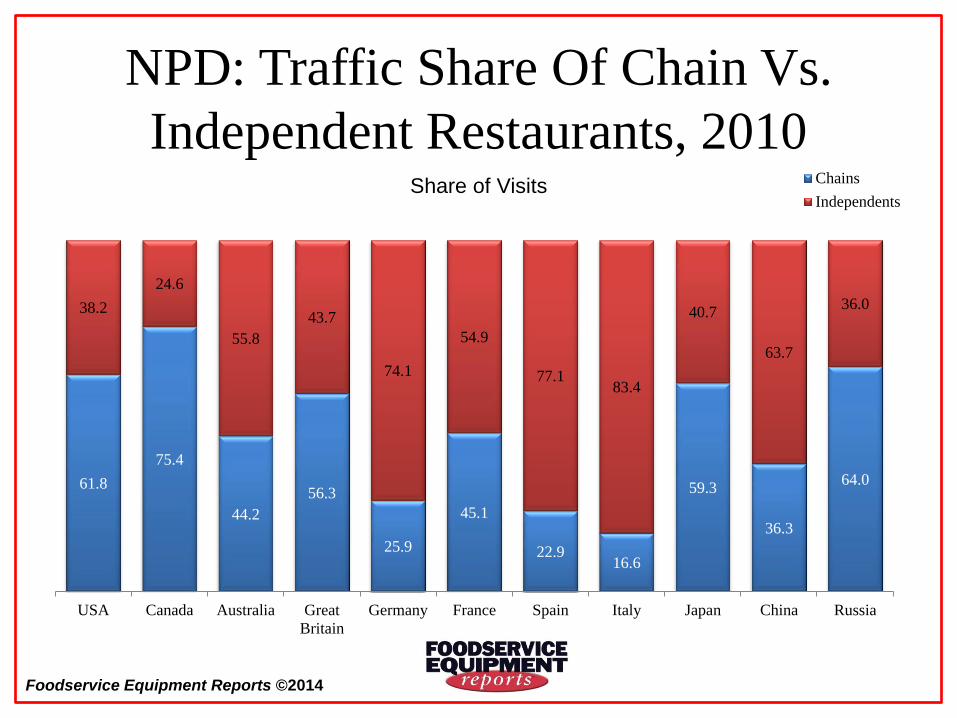

• U.S. more “chain” dominant than most other developed

and developing foodservice markets.

Foodservice Equipment Reports ©2014

Top 500 Chains’ Market Share 2012

58%

42%

Share Of Restaurant Sales

Total: $435 Billion, 2012 Source: Technomic Inc.

Top 500

Rest of

Industry

41%

59%

Share of Restaurant Units

Total: 518,533, 2012 Source: Technomic Inc.

Top 500

Rest of

Industry

Foodservice Equipment Reports ©2014

FS Management Companies Control Of

Key Institutional Operator Segments

79%

55%

37%

17% 16% 19%

38%

Share Of Purchases , 2012

Source: Technomic Inc.

Foodservice Equipment Reports ©2014

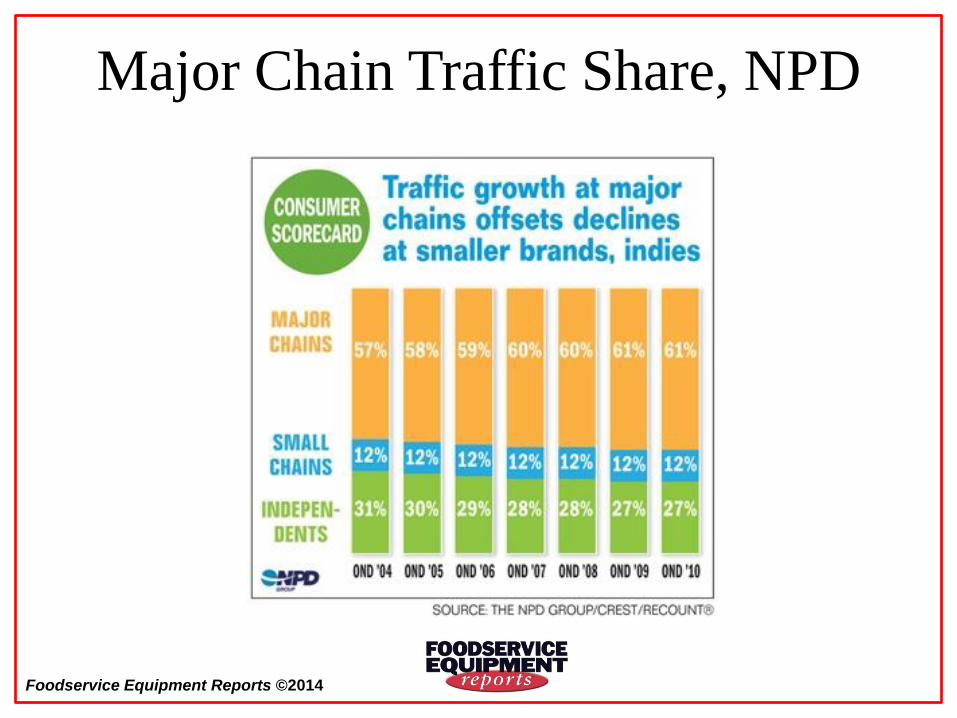

NPD: Traffic Share Of Chain Vs.

Independent Restaurants, 2010

61.8

75.4

44.2

56.3

25.9

45.1

22.9 16.6

59.3

36.3

64.0

38.2

24.6

55.8

43.7

74.1

54.9

77.1 83.4

40.7

63.7

36.0

USA Canada Australia Great

Britain

Germany France Spain Italy Japan China Russia

Chains

IndependentsShare of Visits

Foodservice Equipment Reports ©2014

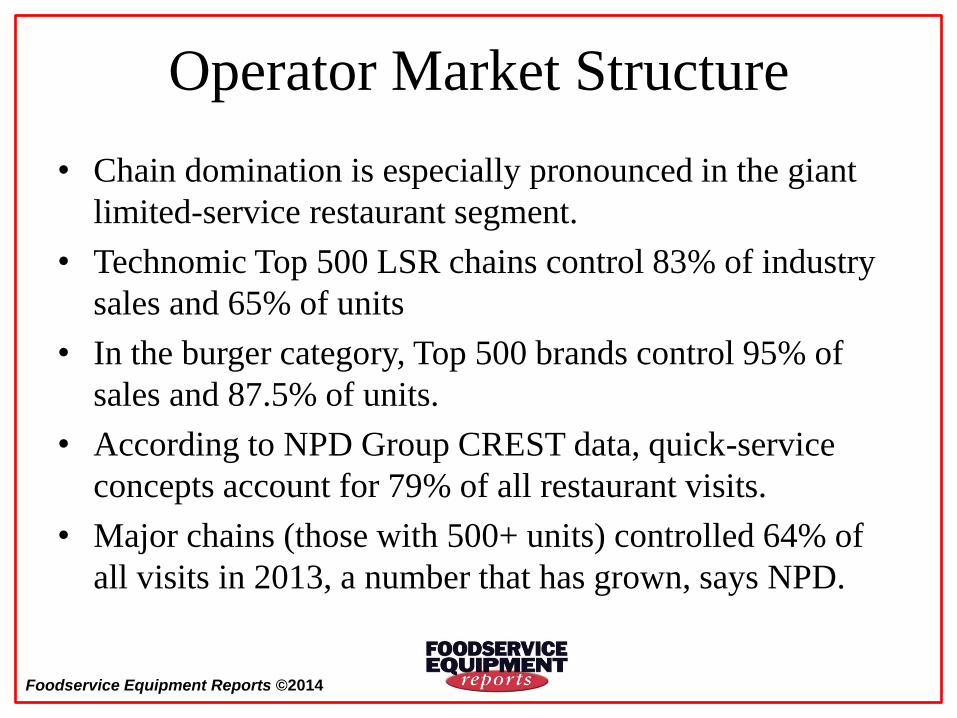

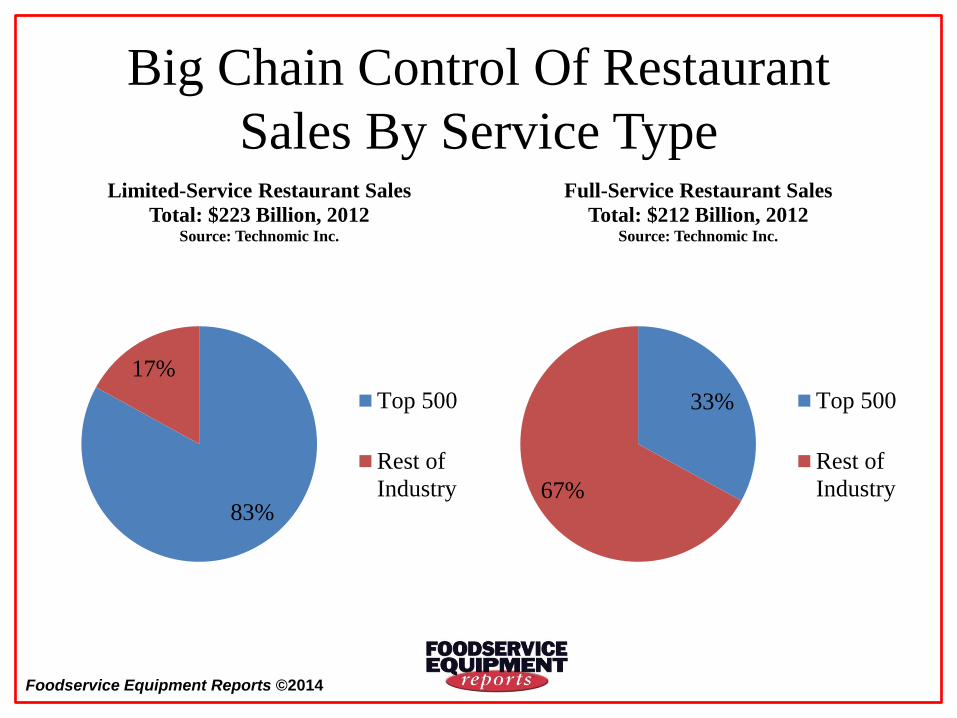

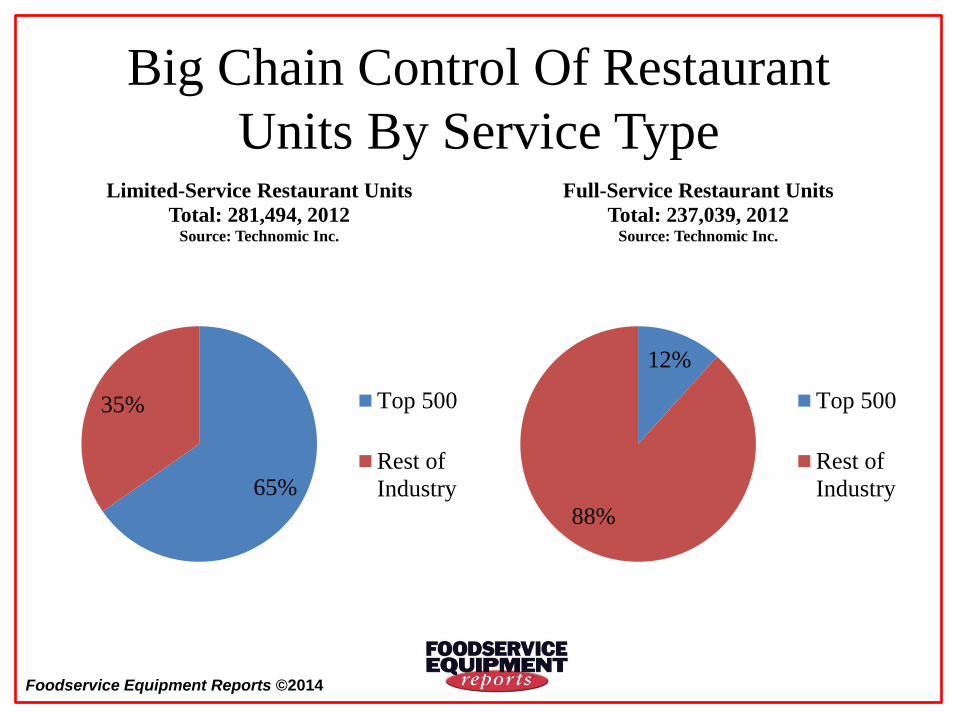

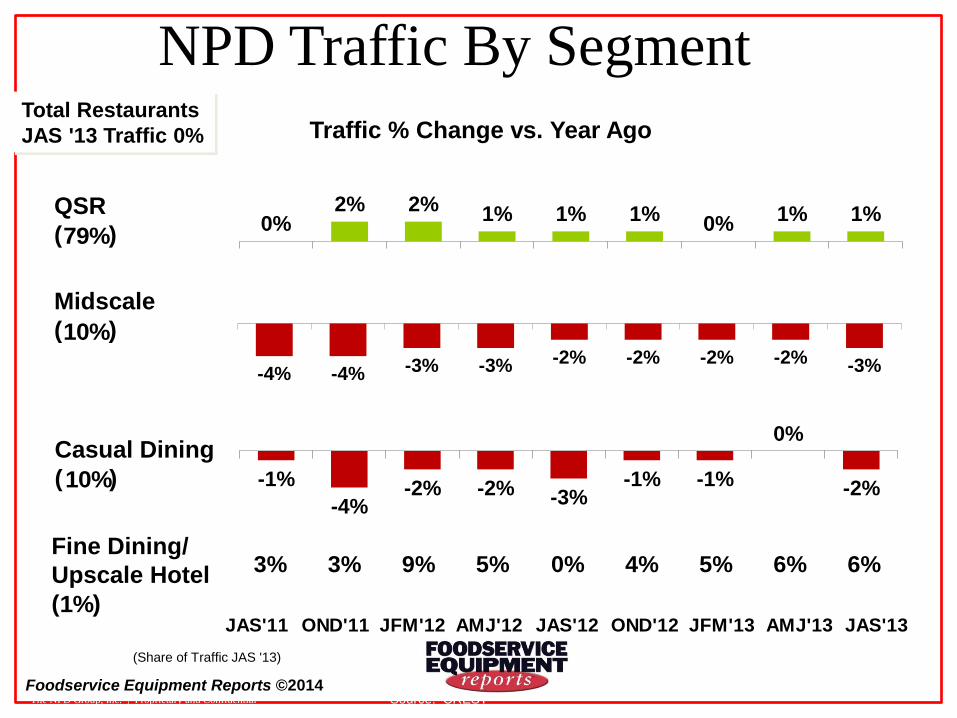

Operator Market Structure

• Chain domination is especially pronounced in the giant

limited-service restaurant segment.

• Technomic Top 500 LSR chains control 83% of industry

sales and 65% of units

• In the burger category, Top 500 brands control 95% of

sales and 87.5% of units.

• According to NPD Group CREST data, quick-service

concepts account for 79% of all restaurant visits.

• Major chains (those with 500+ units) controlled 64% of

all visits in 2013, a number that has grown, says NPD.

Foodservice Equipment Reports ©2014

Big Chain Control Of Restaurant

Sales By Service Type

83%

17%

Limited-Service Restaurant Sales

Total: $223 Billion, 2012 Source: Technomic Inc.

Top 500

Rest of

Industry

33%

67%

Full-Service Restaurant Sales

Total: $212 Billion, 2012 Source: Technomic Inc.

Top 500

Rest of

Industry

Foodservice Equipment Reports ©2014

Big Chain Control Of Restaurant

Units By Service Type

65%

35%

Limited-Service Restaurant Units

Total: 281,494, 2012 Source: Technomic Inc.

Top 500

Rest of

Industry

12%

88%

Full-Service Restaurant Units

Total: 237,039, 2012 Source: Technomic Inc.

Top 500

Rest of

Industry

Foodservice Equipment Reports ©2014

NPD Traffic By Segment

-4% -4% -3% -3% -2% -2% -2% -2% -3%

0% 2% 2% 1% 1% 1% 0% 1% 1%

-1%

-4% -2% -2% -3%

-1% -1%

0%

-2%

Traffic % Change vs. Year Ago

QSR

( )

Midscale

( )

Casual Dining

( )

Fine Dining/

Upscale Hotel

( )

(Share of Traffic JAS '13)

79%

10%

10%

1%

3% 3% 9% 5% 0% 4% 5% 6% 6%

JAS'11 OND'11 JFM'12 AMJ'12 JAS'12 OND'12 JFM'13 AMJ'13 JAS'13

Total Restaurants

JAS '13 Traffic 0%

The NPD Group, Inc. | Proprietary and Confidential Source: CREST

Foodservice Equipment Reports ©2014

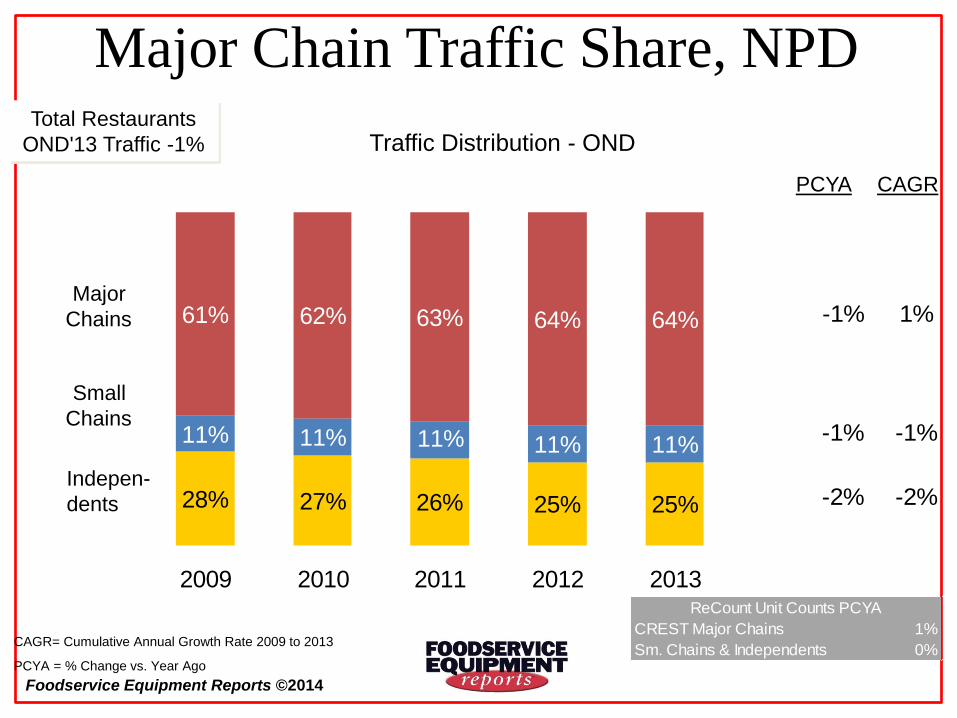

Major Chain Traffic Share, NPD

Foodservice Equipment Reports ©2014

62% 63% 64% 64%

11% 11% 11%

28% 27% 26% 25% 25%

61%

11%11%

2009 2010 2011 2012 2013

Major Chain Traffic Share, NPD

PCYA = % Change vs. Year Ago

Traffic Distribution - OND

Major

Chains

Small

Chains

Indepen-

dents

PCYA CAGR

1%-1%

-1%-1%

-2%-2%

CAGR= Cumulative Annual Growth Rate 2009 to 2013

Total Restaurants

OND'13 Traffic -1%

CREST Major Chains 1%

Sm. Chains & Independents 0%

ReCount Unit Counts PCYA

18 Source: CREST / ReCount

Foodservice Equipment Reports ©2014

U.S. Foodservice & E&S Market Realities

• A few thousand organizations—chains, FS mgmt.

companies, big institutions—are keys to U.S. market.

• They not only control a majority of operator sales, but

account for an estimated 70-75% of new E&S purchases.

• They don’t purchase E&S like independent operators.

• They are the most brand sensitive and have complex

specification, evaluation and distribution processes.

• This is particularly true of the big QSR brands, but is also

true of other chains and big institutions.

• Which is why FER researched those processes.

Foodservice Equipment Reports ©2014

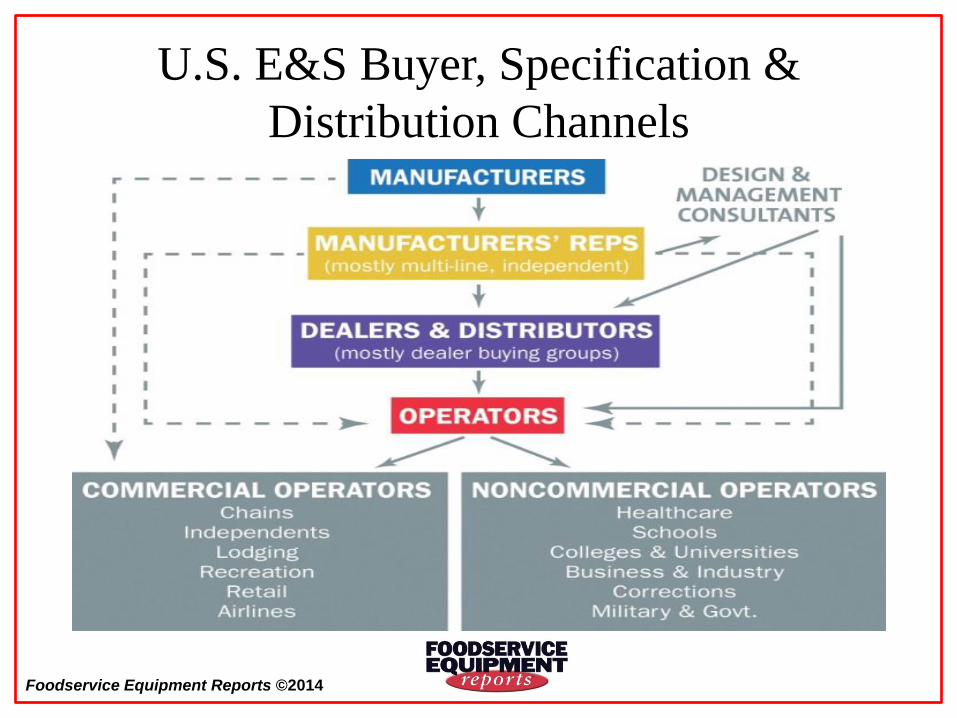

U.S. E&S Buyer, Specification &

Distribution Channels

• The paths and influences in big operator E&S buying,

specifying and logistics decisions are multi-faceted.

• The “normal” path is OEM manufacturer to independent

multi-line sales rep to dealer to operator.

• Big institutional operators usually also employ an

independent design or concept consultant

• Many chain and big institutional operators generally

follow these “normal” paths and channels.

• But there are also many side paths, “direct” relationships

and other outside influences.

Foodservice Equipment Reports ©2014

U.S. E&S Buyer, Specification &

Distribution Channels

Foodservice Equipment Reports ©2014

How Chains Purchase Equipment:

Overview • U.S. restaurants chains come in all sizes, service and

menu types and ownership structures.

• These differences influence, if not dictate, how they

evaluate equipment, select suppliers and purchase E&S.

• As we’ve seen, specification and distribution are very

complex, with multiple influences and channels.

• Generally, larger chains deal more directly with the OEM

manufacturers and their sales reps; a semi-custom world.

• The larger the chain, the more “specialists” influence

equipment selection and purchase procedures.

Foodservice Equipment Reports ©2014

How Chains Purchase Equipment:

Overview

• Quick-service giants are usually franchised, while

full-service chains often own all or most of their units.

• Franchised systems have another layer of buyers, the

franchisees themselves.

• Many franchised systems have purchasing co-operatives

that are jointly owned by the company and franchisees.

• Quick-service equipment packages are more custom,

often designed by company R&D engineers and OEMs.

• Full-service chains generally have larger kitchens and use

more “standard” equipment items.

Foodservice Equipment Reports ©2014

How Chains Purchase Equipment:

Overview • Smaller chains, both quick- and full-service, generally rely

more on manufacturers’ reps, dealers and distributors.

• These entities help specify and provide a kitchen package, as

well as provide the services for opening stores.

• In smaller chains, there are fewer “specialists,” and senior

execs, operations execs, and chefs are key specifiers.

• Even the largest chains use some form of dealer or KES

(kitchen equipment supplier, usually also a manufacturer),

even, in a few cases, in-house distribution.

• The FER Commercial Multiunit Purchasing Practices Survey

reflects this diversity.

Foodservice Equipment Reports ©2014

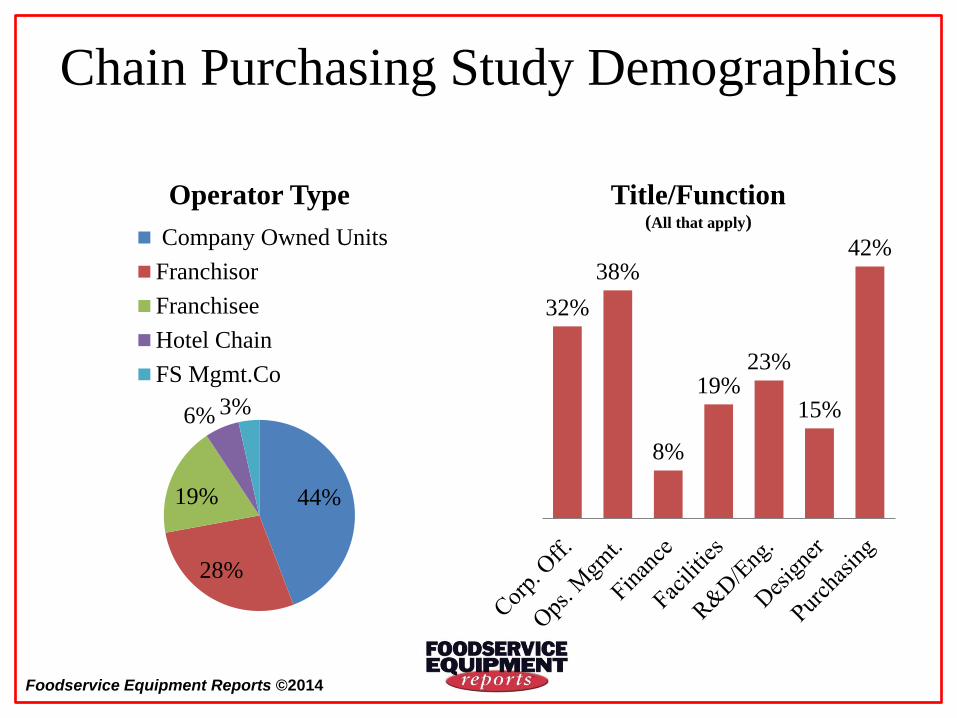

Chain Purchasing Study Demographics

44%

28%

19%

6% 3%

Operator Type

Company Owned Units

Franchisor

Franchisee

Hotel Chain

FS Mgmt.Co

32%

38%

8%

19% 23%

15%

42%

Title/Function (All that apply)

Foodservice Equipment Reports ©2014

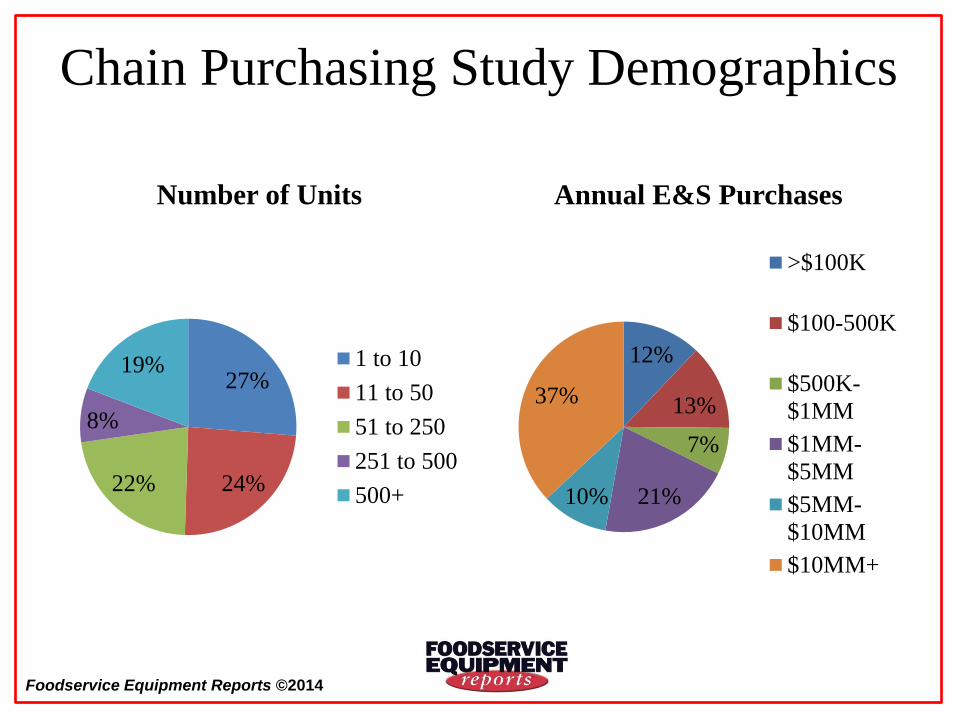

Chain Purchasing Study Demographics

27%

24% 22%

8%

19%

Number of Units

1 to 10

11 to 50

51 to 250

251 to 500

500+

12%

13%

7%

21% 10%

37%

Annual E&S Purchases

>$100K

$100-500K

$500K-

$1MM

$1MM-

$5MM

$5MM-

$10MM

$10MM+

Foodservice Equipment Reports ©2014 27

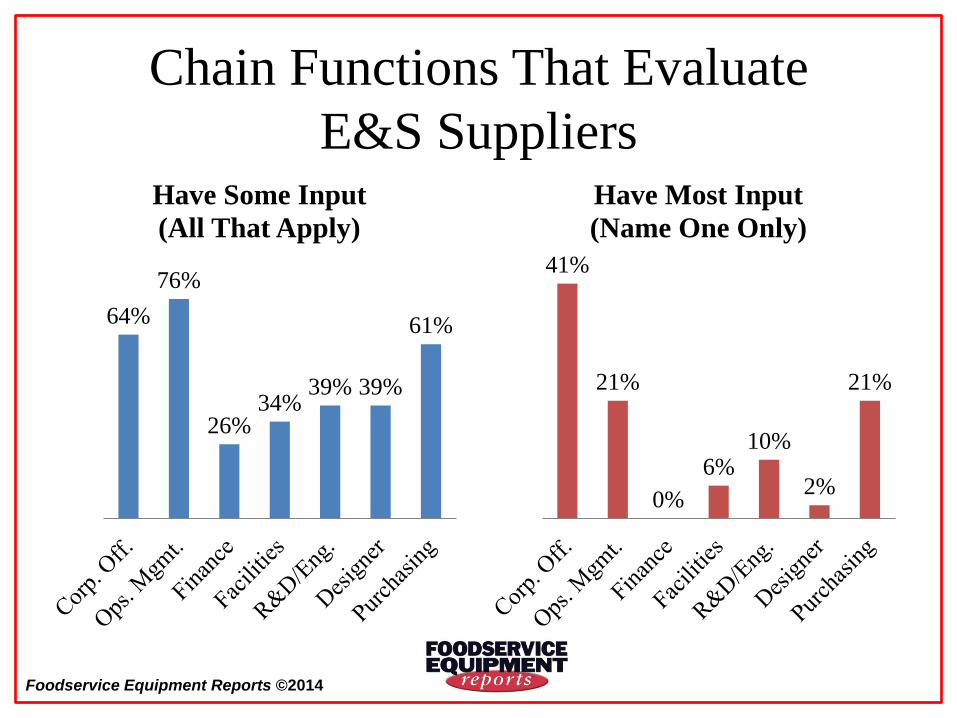

Chain Functions That Evaluate

E&S Suppliers • No matter the size or structure of a chain, multiple

functions have some input into selecting suppliers.

• Almost always, operations management have significant input as do senior execs and culinary.

• But when it comes to the most say in supplier choice, senior execs are key, especially in smaller chains.

• About one in five respondents name purchasing or operation management as the key “chooser.”

• In larger chains, R&D personnel, both equipment engineers and culinary are named more often, along with other specialist titles.

Foodservice Equipment Reports ©2014

Chain Functions That Evaluate

E&S Suppliers

64%

76%

26% 34%

39% 39%

61%

Have Some Input

(All That Apply)

41%

21%

0%

6% 10%

2%

21%

Have Most Input

(Name One Only)

Foodservice Equipment Reports ©2014

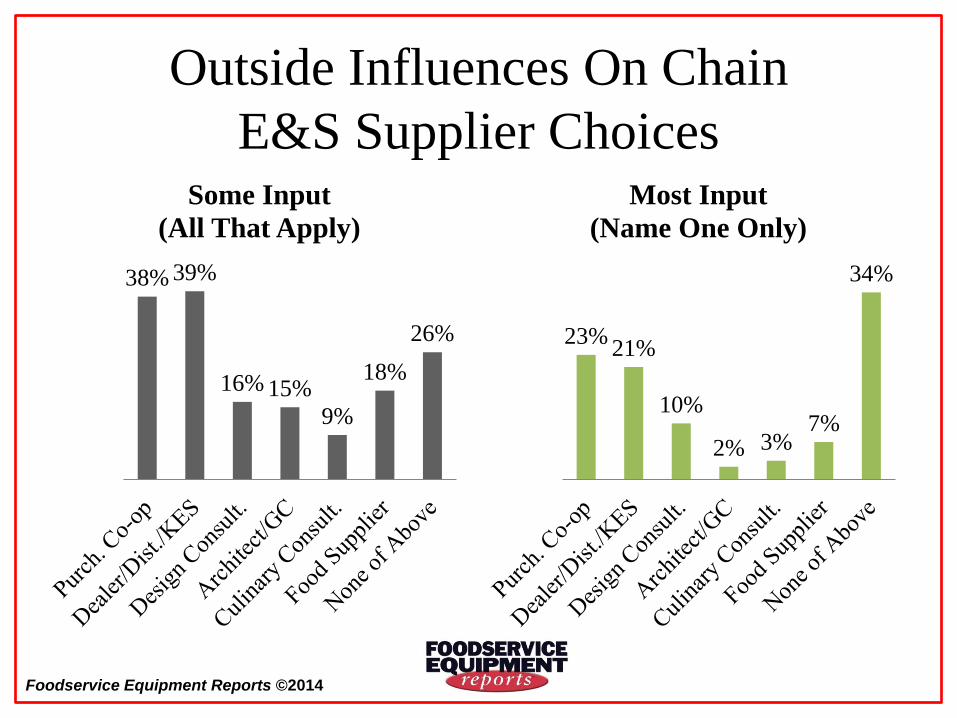

Outside Influences On Chain

E&S Supplier Choices • Outside distribution and purchasing partners, designers,

architects and food suppliers can also have spec inputs.

• Affiliated purchasing co-ops or distributors, and

dealer/KES partners are mentioned the most often.

• Food suppliers have more input than one might expect,

perhaps because of their role in new menu items.

• Architects and general contractors and culinary

consultants have the least role.

• Most surprising are percent of respondent who say none

of these functions have a role in choosing E&S suppliers.

Foodservice Equipment Reports ©2014

Outside Influences On Chain

E&S Supplier Choices

38% 39%

16% 15%

9%

18%

26%

Some Input

(All That Apply)

23% 21%

10%

2% 3% 7%

34%

Most Input

(Name One Only)

Foodservice Equipment Reports ©2014

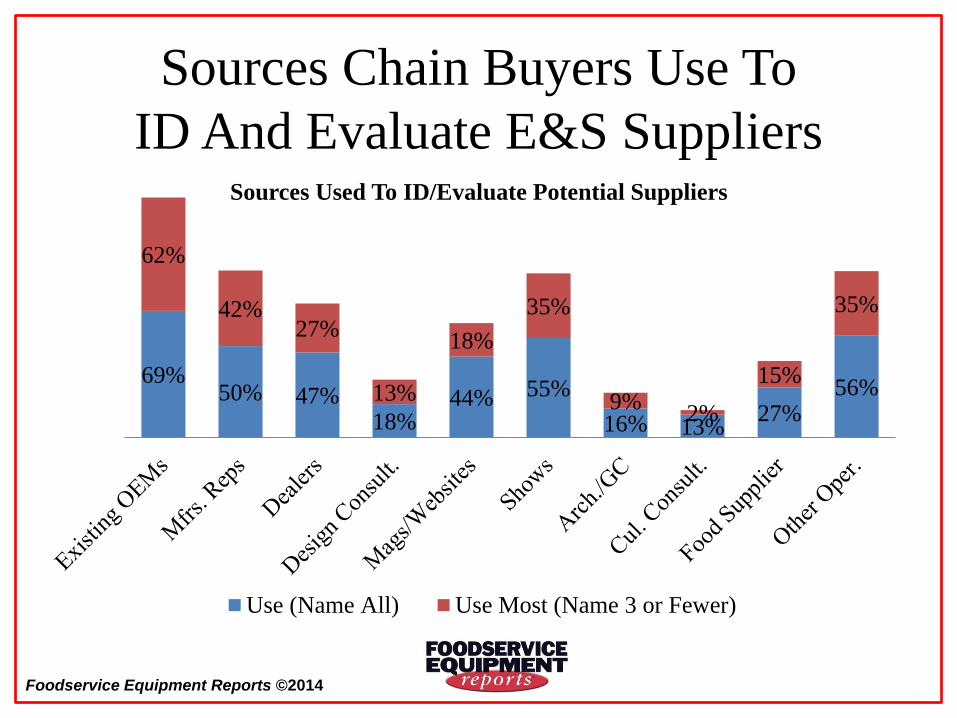

Sources Chain Buyers Use To

ID And Evaluate E&S Suppliers • Chain spec/buyers tap into many sources when looking

for and evaluating E&S products and suppliers.

• Dealers, consultants, trade magazines and shows, even

food suppliers enter into the mix.

• But when asked to name the sources they depend on

most, existing suppliers and mfrs. reps are dominant.

• Recommendations from other operators, “word of mouth”

is also a very significant and important influence.

• Dealers, trade magazines and consultants are still factors.

• It’s significant how much chains rely on existing OEMs.

Foodservice Equipment Reports ©2014

Sources Chain Buyers Use To

ID And Evaluate E&S Suppliers

69% 50% 47%

18% 44% 55%

16% 13% 27%

56%

62%

42% 27%

13%

18%

35%

9% 2%

15%

35%

Sources Used To ID/Evaluate Potential Suppliers

Use (Name All) Use Most (Name 3 or Fewer)

Foodservice Equipment Reports ©2014

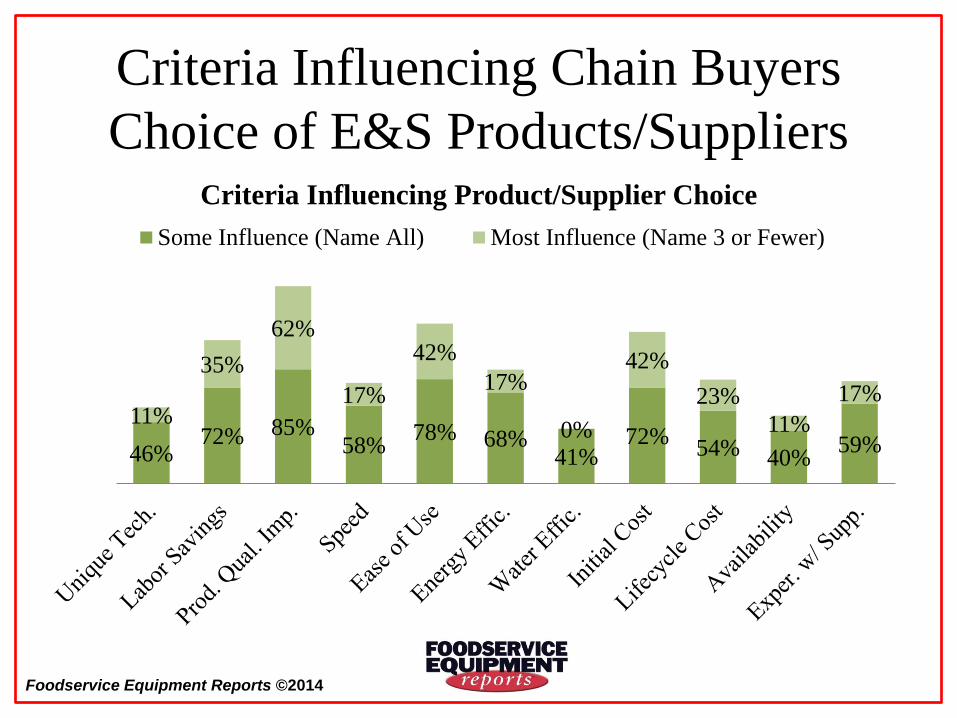

Criteria Influencing Chain Buyers

Choice of E&S Products/Suppliers • Many different criteria are involved in chain buyers E&S

product and supplier choices.

• Labor savings, ease of use, energy efficiency, both initial and

lifecycle cost, speed and previous experience with the supplier

are all named by more than 50% of buyers.

• But the most critical criteria is clearly the product’s and

supplier’s impact on food and menu product quality.

• Ease of use, initial cost and labor savings are the next most

commonly mentioned criteria.

• Unique technology, water savings and availability are cited by

the fewest respondents as important.

Foodservice Equipment Reports ©2014

Criteria Influencing Chain Buyers

Choice of E&S Products/Suppliers

46% 72% 85%

58% 78% 68%

41% 72%

54% 40% 59%

11%

35%

62%

17%

42%

17%

0%

42%

23%

11%

17%

Criteria Influencing Product/Supplier Choice

Some Influence (Name All) Most Influence (Name 3 or Fewer)

Foodservice Equipment Reports ©2014

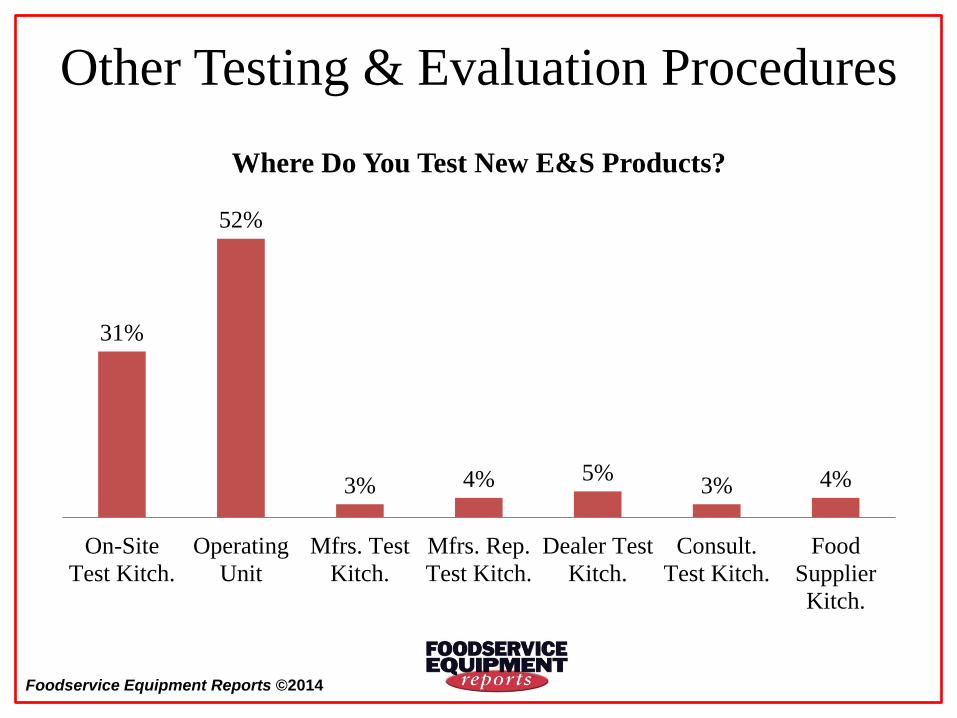

Other Testing & Evaluation Procedures

31%

52%

3% 4% 5% 3% 4%

On-Site

Test Kitch.

Operating

Unit

Mfrs. Test

Kitch.

Mfrs. Rep.

Test Kitch.

Dealer Test

Kitch.

Consult.

Test Kitch.

Food

Supplier

Kitch.

Where Do You Test New E&S Products?

Foodservice Equipment Reports ©2014

Other Testing & Evaluation Procedures

• Chain buyers most often test and evaluate new E&S

products in existing operating units.

• But a significant number have on-site test facilities.

• The testing is the key determinate of the E&S product’s

impact on food product quality.

• But chains also test to help them determine operational

impacts, speed of service impacts, etc.

• Big chains have very rigorous supplier testing and vetting

processes including factory visits, financial vetting,

service network reach and warranty history analysis.

Foodservice Equipment Reports ©2014

U.S. Chain E&S

Purchasing Take-Aways • U.S. chain spec/buyers purchase billions of dollars of

E&S products every year.

• They employ complex criteria and procedures to evaluate

products and suppliers.

• They listen to nearly everyone they can in identifying and

evaluating potential products and suppliers.

• They also have complex testing and evaluation processes.

• But while they are open to new products, suppliers and

technologies, their complex multiunit needs and scale

requires suppliers of equal experience and scale.

Foodservice Equipment Reports ©2014

How Big Institutions Purchase

Equipment: Overview • Big institutional foodservice operators are usually true

“multiunit” operators, just like chain restaurants & hotels.

• But their kitchens, from huge production facilities to

commercial style a la carte serveries are more individual.

• They purchase more “stock” equipment and supplies.

• But they also buy a great deal of custom fabrication for

serveries, tray-make up systems and the like.

• They usually purchase equipment less often, partly

because their volumes are lower, their staff better trained

and because they maintain equipment much better.

Foodservice Equipment Reports ©2014

How Big Institutions Purchase

Equipment: Overview • This is how the process works for most big projects,

whether new construction or major renovations:

– Project is conceived and announced.

– Architects and general contractor are chosen by institution execs.

– Foodservice director works with internal teams to outline scope.

– FS director usually (but not always) hires design and/or concept

consultants to help create menus, concepts and kitchen design.

– Design consultants specify E&S, including brands.

– After approvals, including budgetary OKs, project is put out to

equipment dealers for bid.

– Consultant helps FS director chose winning bid.

– Facility and kitchen are built and the kitchen equipment installed.

Foodservice Equipment Reports ©2014

How Big Institutions Purchase

Equipment: Overview • But in fact there is a lot more complication and back and

forth than the “normal” process entails.

• The architect/GCs sometimes select the foodservice

consultant without the foodservice director’s input.

• Lots of “prime specs” are broken for monetary reasons,

both budgetary and to help the dealers make some money.

• Since most dealers belong to buying groups, back-end

rebates help offset traditionally low bid-work margins

• Normal replacement is more dealer-based, but beyond an

item or two still usually requires a bid process.

Foodservice Equipment Reports ©2014

How Big Institutions Purchase

Equipment: Overview • Because of the size of the projects—equipment packages run

into the millions—OEMs and their reps “sit” on the

foodservice directors, consultants, dealers and others involved.

• In the noncommercial world, the foodservice director is clearly

the key specifier.

• They often have a great deal of E&S brand knowledge and

opinions, based on experience.

• The opinions of culinary staff are listened to very closely.

• And because many institutions have dedicated facilities

personnel, they have good data on maintenance and reliability.

Foodservice Equipment Reports ©2014

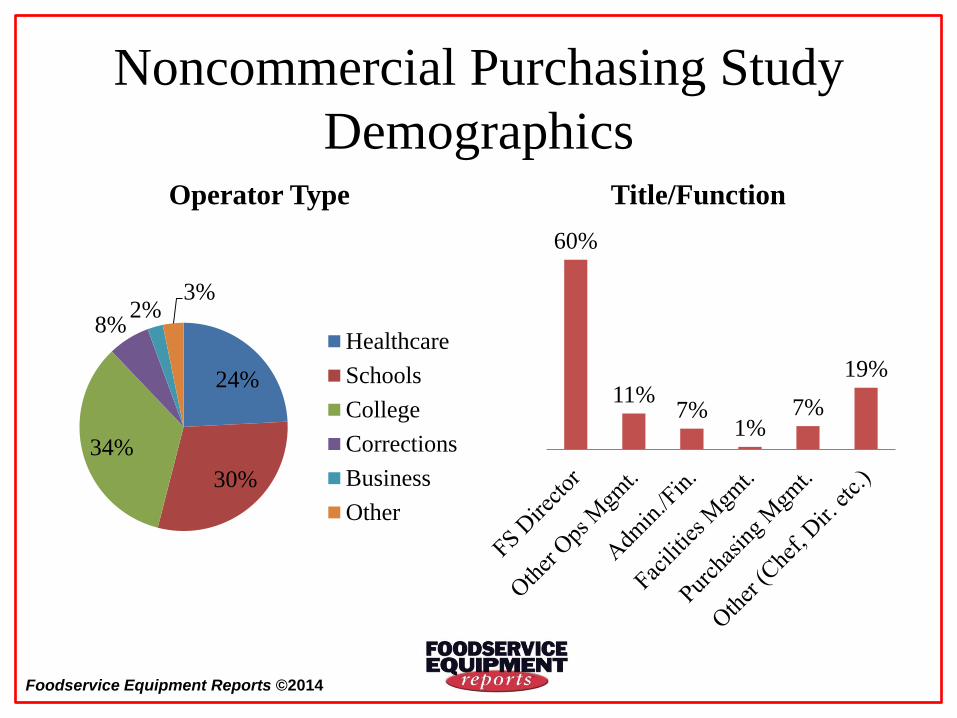

Noncommercial Purchasing Study

Demographics

24%

30%

34%

8% 2%

3%

Operator Type

Healthcare

Schools

College

Corrections

Business

Other

60%

11% 7%

1% 7%

19%

Title/Function

Foodservice Equipment Reports ©2014

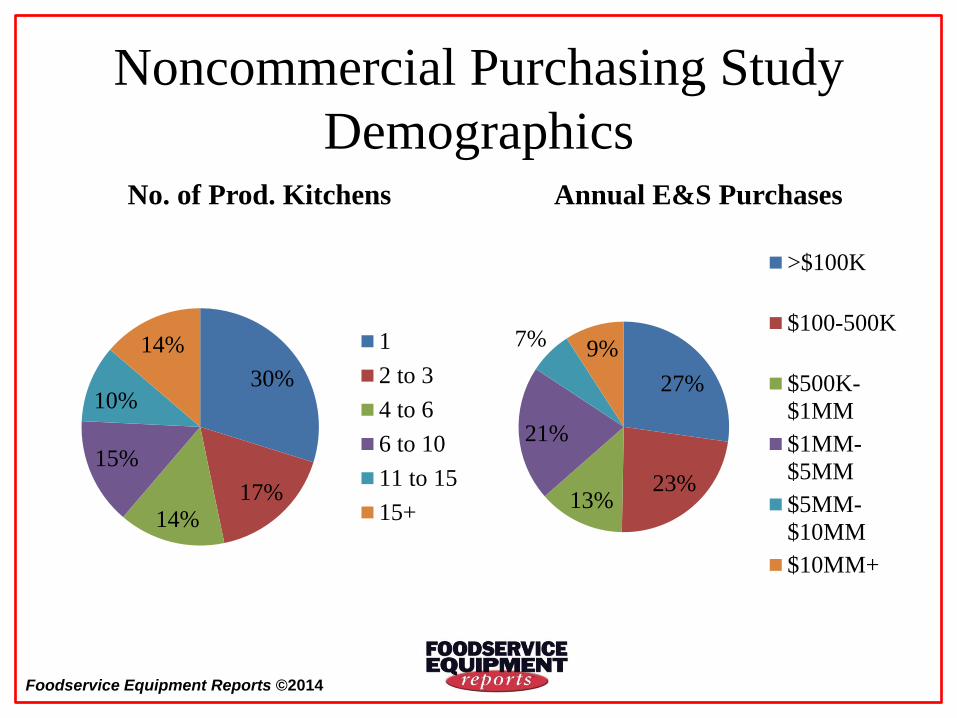

Noncommercial Purchasing Study

Demographics

30%

17% 14%

15%

10%

14%

No. of Prod. Kitchens

1

2 to 3

4 to 6

6 to 10

11 to 15

15+

27%

23% 13%

21%

7% 9%

Annual E&S Purchases

>$100K

$100-500K

$500K-

$1MM

$1MM-

$5MM

$5MM-

$10MM

$10MM+

Foodservice Equipment Reports ©2014

Noncommercial Functions That

Evaluate E&S Suppliers • In most larger noncommercial foodservice operations,

foodservice directors are the key equipment specifier.

• Other functions, including administrative execs and

purchasing personnel have some input.

• Input from facilities personnel is often sought in

institutions; they usually keep detailed equipment records.

• The influence of culinary personnel such as executive

chefs is larger than the survey shows.

• But while others have input or sign-off authority, the

foodservice director is by far the dominant specifier.

Foodservice Equipment Reports ©2014

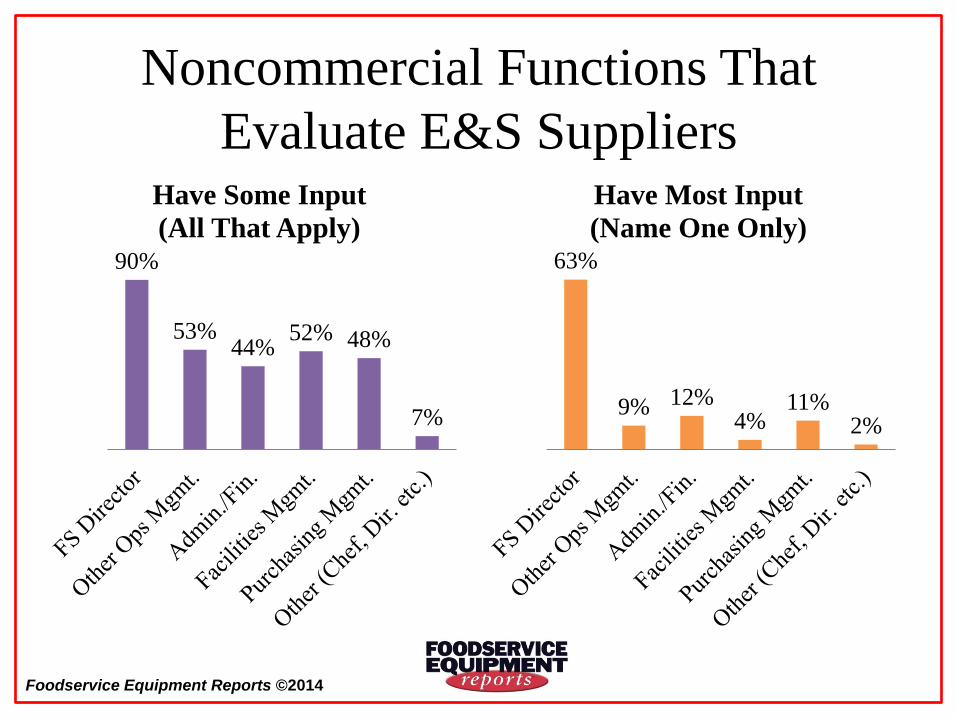

Noncommercial Functions That

Evaluate E&S Suppliers

90%

53% 44%

52% 48%

7%

Have Some Input

(All That Apply) 63%

9% 12% 4%

11% 2%

Have Most Input

(Name One Only)

Foodservice Equipment Reports ©2014

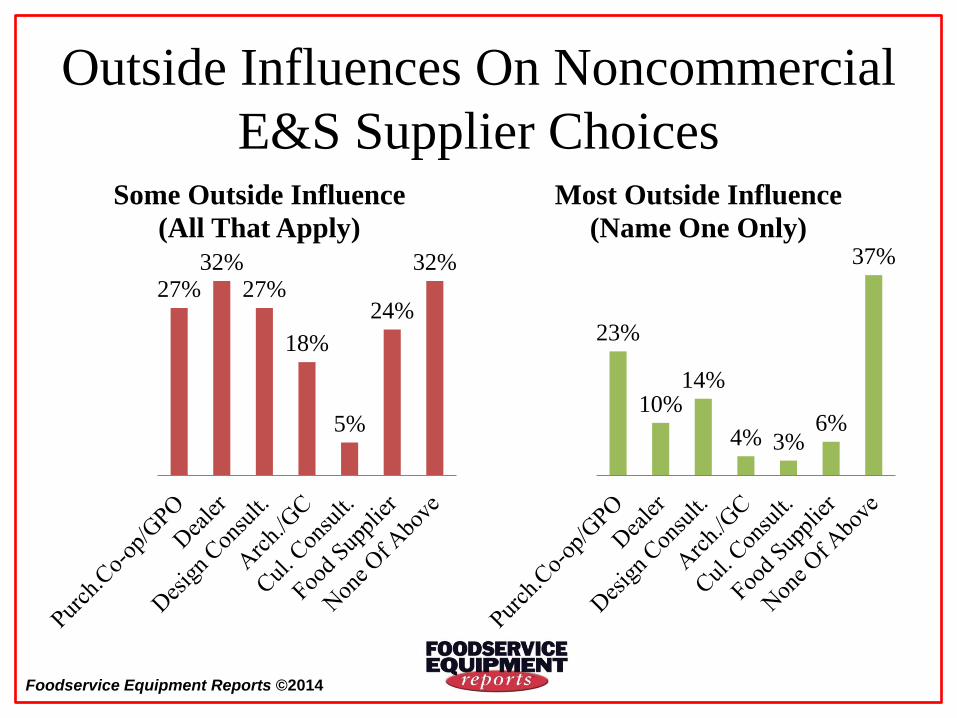

Outside Influences On Noncommercial

E&S Supplier Choices • Noncommercial operators also rely on a variety of outside

sources for help in evaluating products and suppliers.

• Design consultants are a significant influence, especially for

new facilities and big renovation projects.

• Dealers also still matter, especially for replacement items, and

when projects need to be “value engineered.”

• Purchasing co-ops and gross purchasing organizations (GPOs)

are prevalent in some segments, especially healthcare.

• The need for bids for many buys beyond $5,000-$10,000

likely constrains outside influence on brand choice.

• “None of the above” answers are even higher than in chains.

Foodservice Equipment Reports ©2014

Outside Influences On Noncommercial

E&S Supplier Choices

27% 32%

27%

18%

5%

24%

32%

Some Outside Influence

(All That Apply)

23%

10% 14%

4% 3% 6%

37%

Most Outside Influence

(Name One Only)

Foodservice Equipment Reports ©2014

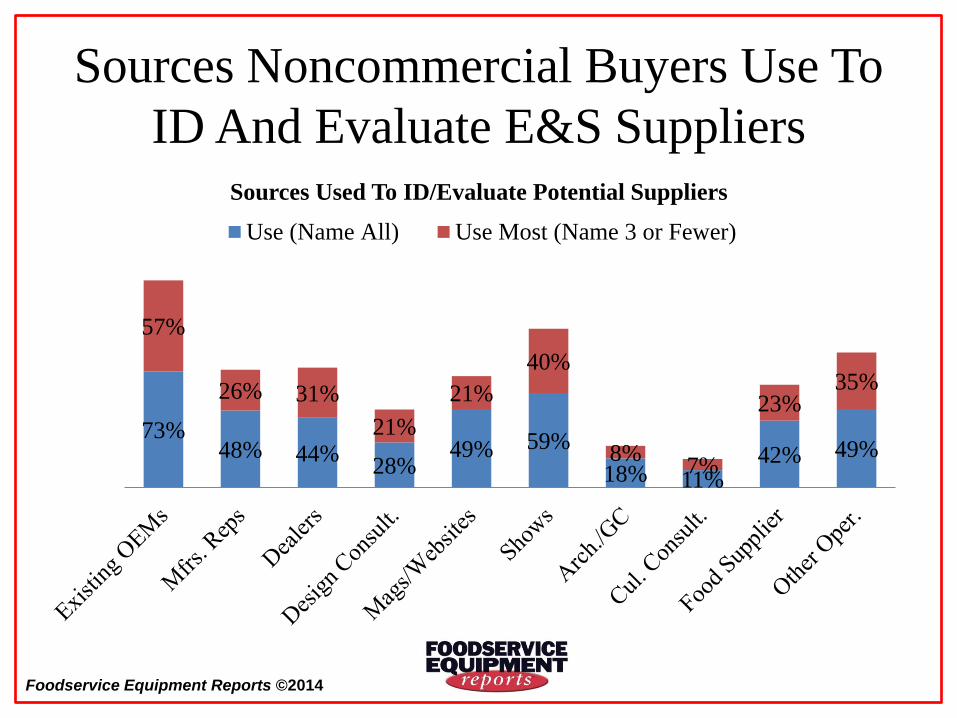

Sources Noncommercial Buyers Use To

ID And Evaluate E&S Suppliers

• Noncommercial operators also use a wide variety of

sources to identify E&S products and suppliers.

• Dealers, trade media, consultants and food suppliers are a

source for nearly half of all survey respondents at times.

• And their mentions when the choices are limited to three

or fewer remain quite high.

• But as we saw on the chain side, OEM suppliers and their

reps are the most commonly noted sources of info.

• Trade shows are very important to this audience, as are

recommendations from other operators.

Foodservice Equipment Reports ©2014

Sources Noncommercial Buyers Use To

ID And Evaluate E&S Suppliers

73% 48% 44%

28% 49% 59%

18% 11% 42% 49%

57%

26% 31%

21%

21%

40%

8% 7%

23% 35%

Sources Used To ID/Evaluate Potential Suppliers

Use (Name All) Use Most (Name 3 or Fewer)

Foodservice Equipment Reports ©2014

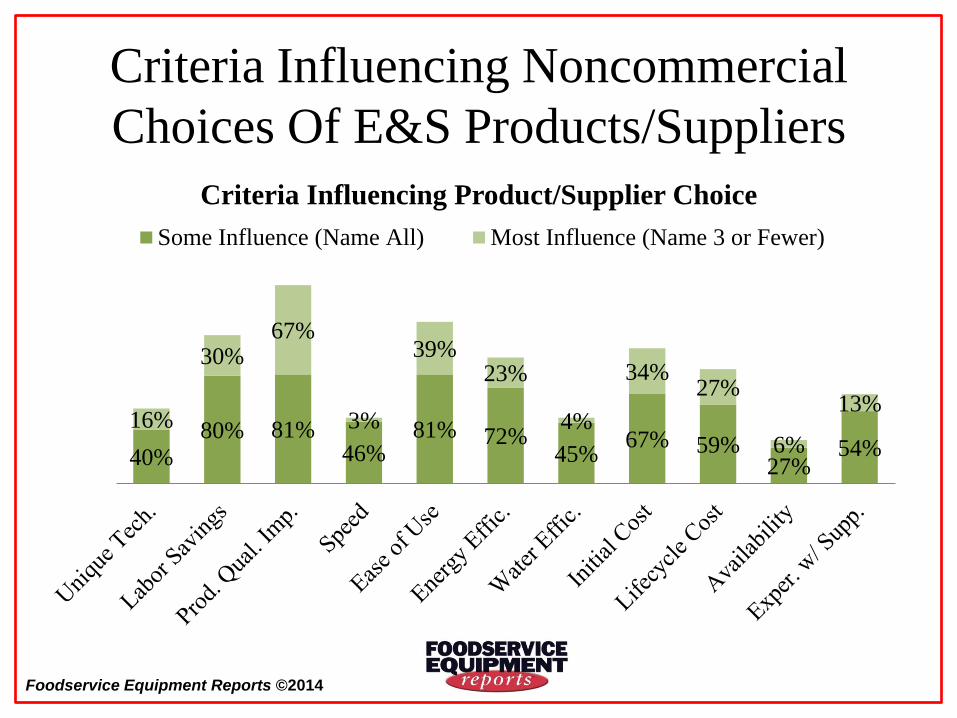

Criteria Influencing Noncommercial

Choices Of E&S Products/Suppliers

• The impact on product quality and labor savings and ease

of use issues are again the critical criteria in E&S choices.

• Initial cost is still a very important criteria, but somewhat

less so than with chain buyers.

• Lifecycle cost, on the other hand, is more important.

• Both energy efficiency and water efficiency rank higher

as criteria among noncommercial buyers.

• Energy efficiency is the fourth highest ranked criteria

having some influence.

• Speed and availability are cited least often.

Foodservice Equipment Reports ©2014

Criteria Influencing Noncommercial

Choices Of E&S Products/Suppliers

40% 80% 81%

46% 81% 72%

45% 67% 59%

27% 54%

16%

30% 67%

3%

39% 23%

4%

34% 27%

6%

13%

Criteria Influencing Product/Supplier Choice

Some Influence (Name All) Most Influence (Name 3 or Fewer)

Foodservice Equipment Reports ©2014

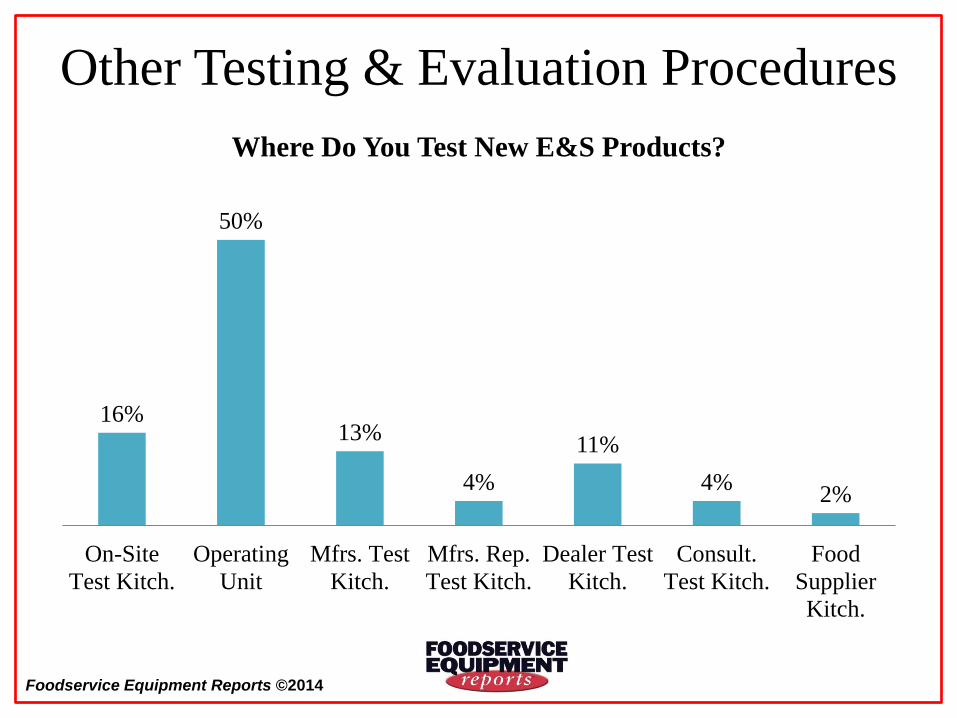

Other Testing & Evaluation Procedures

16%

50%

13%

4%

11%

4% 2%

On-Site

Test Kitch.

Operating

Unit

Mfrs. Test

Kitch.

Mfrs. Rep.

Test Kitch.

Dealer Test

Kitch.

Consult.

Test Kitch.

Food

Supplier

Kitch.

Where Do You Test New E&S Products?

Foodservice Equipment Reports ©2014

Other Testing & Evaluation Procedures

• Equipment testing and evaluation in noncommercial

operation most often takes place in an operating kitchen.

• But nearly one out of six operators has a test facility.

• And noncomm operators are more like to use a dealer or

manufacturers’ rep test kitchen than chain buyers.

• As in chains, the key criteria are checking impact on food

quality and labor and ease of use issues.

• Since institutional kitchens generally use more stock

equipment items with fewer pre-programed controls,

control interface issues loom large in testing.

Foodservice Equipment Reports ©2014

Noncommercial Operator E&S

Purchasing Take-Aways • “Beyond restaurants” segments account for as much a 40% of

the E&S market in the U.S.

• Big institutions are very big buyers of E&S, not just when they

build new facilities or renovate, but for replacement.

• They employ many of the same criteria and use many of the

same outside sources as big chain players.

• As with chains, while dealers, consultants and others are

important influences, the OEMs are again prime sources.

• Word of mouth recommendations from fellow operators is also

a very big influence on supplier and product choice.

• The foodservice director is queen (or king) of specifications.

Foodservice Equipment Reports ©2014

Closing Thoughts

• Breaking in to these large multiunit organizations as an

E&S supplier is difficult and complex. It can take years.

• But the value of such customers is so great, world-class

suppliers always find it worth the effort.

• Knowing the complexities and criteria makes it possible

to develop a plan of engagement.

• Remember each organization is unique.

• When we asked what one thing suppliers could do to

make the task of selecting then easier, they answered,

“Work harder to understand my operation.”

Foodservice Equipment Reports ©2014

Thank You

And

Good Luck!

Foodservice Equipment Reports ©2014

Acknowledgements & Sources

• This complete presentation is can be downloaded at

fermag.com/medialibrary/research.

• We thank Technomic Inc. for the generous sharing of their research.

More information on their extensive products and capabilities is at

technomic.com.

• We thank The NPD Group for allowing us use of their multi-faceted

research. More info is at npd.com.

• We want to thank Hotelex and UBM SinoExpo for their ongoing

support of the Foodservice Forum. Special thanks to Zoi Fan, Alex

Ni and Alvina Kwok.

• Not least, we thank our Forum sponsors: Greenfield World Trade,

Alto-Shaam, Scotsman/Ali Group, T&S Brass and Halton.

![Il-fer] ta’ grazzja [dida Il-fer] ta’ ]a[a [dida](https://img.pdfslide.us/doc/110x75/5697c0241a28abf838cd4ad1/il-fer-ta-grazzja-dida-il-fer-ta-aa-dida.jpg)

![FER, B. 3. Surrealismo, Mito e Psicanálise in FER, B Et Alli [1993]](https://img.pdfslide.us/doc/110x75/563dbb96550346aa9aae78df/fer-b-3-surrealismo-mito-e-psicanalise-in-fer-b-et-alli-1993.jpg)