Embed Size (px)

Citation preview

FEDERAL TAX LAW AND ISSUES RELATED TO THE UNITED STATES TERRITORIES

Scheduled for a Public Hearing Before the

SENATE COMMITTEE ON FINANCE on May 15, 2012

Prepared by the Staff of the

JOINT COMMITTEE ON TAXATION

May 14, 2012 JCX-41-12

i

CONTENTS

Page

INTRODUCTION AND SUMMARY ........................................................................................... 1

I. ECONOMIC CONDITIONS OF U.S. TERRITORIES ......................................................... 3

II. PRESENT LAW U.S. TAX PROVISIONS RELATED TO U.S. TERRITORIES ............... 7

A. Overview of the U.S. Tax Provisions Related to U.S. Territories ................................... 7 1. In general ................................................................................................................... 7 2. Income taxation of individuals................................................................................... 8 3. Income taxation of corporations .............................................................................. 11 4. Estate and gift taxation ............................................................................................. 12 5. Payroll taxes ............................................................................................................. 13 6. Excise tax ................................................................................................................. 14 7. Tax incentives .......................................................................................................... 15 8. Tax treaties ............................................................................................................... 15

B. Overview of U.S. Tax Provisions Related to American Samoa .................................... 17 1. In general ................................................................................................................. 17 2. Taxation of individuals ............................................................................................ 17 3. Taxation of corporations .......................................................................................... 18 4. Excise tax ................................................................................................................. 18 5. Tax incentives .......................................................................................................... 18

C. Overview of U.S. Tax Provisions Related to Guam ...................................................... 20 1. In general ................................................................................................................. 20 2. Taxation of individuals ............................................................................................ 20 3. Taxation of corporations .......................................................................................... 20 4. Payroll taxes ............................................................................................................. 21 5. Excise taxes .............................................................................................................. 21

D. Overview of U.S. Tax Provisions Related to Commonwealth of the Northern Mariana Islands .............................................................................................. 22 1. In general ................................................................................................................. 22 2. Taxation of individuals ............................................................................................ 22 3. Taxation of corporations .......................................................................................... 23 4. Payroll taxes ............................................................................................................. 23

E. Overview of U.S. Tax Provisions Related to Puerto Rico ............................................. 24 1. In general ................................................................................................................. 24 2. Income taxation of individuals................................................................................. 24 3. Income taxation of corporations .............................................................................. 25 4. Payroll taxes ............................................................................................................. 25 5. Excise taxes .............................................................................................................. 26 6. Tax incentives .......................................................................................................... 27

F. Overview of U.S. Tax Provisions Related to U.S. Virgin Islands ................................. 28 1. In general ................................................................................................................. 28 2. Taxation of individuals ............................................................................................ 28

ii

3. Taxation of corporations .......................................................................................... 29 4. Payroll taxes ............................................................................................................. 29 5. Excise taxes .............................................................................................................. 29

III. LEGAL ANALYSIS ............................................................................................................. 31

A. Uniform or Varied Treatment ........................................................................................ 32 B. Principles for Territories-Related Tax Rules ................................................................. 34 C. Income Tax Treaties ...................................................................................................... 36

1

INTRODUCTION AND SUMMARY

The Senate Committee on Finance has scheduled a public hearing for May 15, 2012, entitled, “Tax Reform: What It Could Mean for Tribes and Territories.” This document,1 prepared by the staff of the Joint Committee on Taxation, provides an overview and analysis of Federal tax laws relating to five U.S. territories and describes the economies of these territories, in part by comparison to economic measures for the United States as a whole.

The United States has 13 territories under the jurisdiction of the Department of the Interior.2 Three of the territories, Navassa Island, Puerto Rico, and the U.S. Virgin Islands, are in the Caribbean Sea. Ten territories – American Samoa, Baker Island, Guam, Howland Island, Jarvis Island, Johnston Atoll, Kingman Reef, Midway Atoll, the Northern Mariana Islands, and Wake Atoll – are in the Pacific Ocean. Two territories, the Northern Mariana Islands (also referred to as “Northern Marianas”) and Puerto Rico, are commonwealths. Commonwealth status typically involves a legal relationship with the United States that is embodied in a written mutual agreement. Territories that do not have commonwealth status generally have less developed legal relationships with the United States. Their governments are generally constituted by U.S. Federal statutes referred to as organic acts.

This pamphlet describes U.S. Federal tax rules and issues related to the five territories that have significant populations: American Samoa, Guam, the Northern Mariana Islands, Puerto Rico, and the U.S. Virgin Islands. American Samoa became a U.S. territory by deed of cession from the local chiefs of the largest island in 1900. It has no organic act for the establishment of its government, but it adopted its own constitution in 1967. Guam became a territory in 1898, and its organic act was enacted in 1950. For the Northern Mariana Islands a covenant to establish political union with the United States signed in 1975 and came into full effect in 1986. Puerto Rico became a territory in 1898 and a commonwealth 1952. The United States purchased the U.S. Virgin Islands from Denmark in 1917, and the Virgin Islands’ current organic act was enacted in 1954. The five territories are represented in the U.S. Congress by non-voting delegates (in the case of Puerto Rico, a non-voting resident commissioner) in the House of Representatives. Residents of Guam, the Northern Mariana Islands, Puerto Rico, and the U.S. Virgin Islands are generally U.S. citizens. American Samoa residents, by contrast, are generally nationals but not citizens.

Following common current and historical usage, this document uses the term “possessions” interchangeably with “territories.”

1 This document may be cited as follows: Joint Committee on Taxation, Federal Tax Law and Issues

Related to the United States Territories (JCX-41-12), May 14, 2012. Also in relation to this hearing, the staff of the Joint Committee on Taxation prepared a discussion of tax reform issues related to Native American tribes entitled Overview of Federal Tax Provisions and Analysis of Selected Issues Relating to Native American Tribes and Their Members (JCX-40-12), May 14, 2012. Both documents can be found on the Internet at www.jct.gov.

2 The source of information about the territories included in this paragraph and the paragraph that follows is the website of the Office of Insular Affairs of the Department of the Interior: http://www.doi.gov/oia/index.html.

2

The economies of the U.S. territories differ from one another and from the economy of the United States as a whole. The territories are generally poorer than the United States as a whole. Per-capita Gross Domestic Product (“GDP”) in each of American Samoa, Guam, the Northern Mariana Islands, and Puerto Rico is below per-capita GDP in any of the U.S. states.3 As is illustrated in more detail in Table 2 below, the patterns of business activity in the territories vary both from one territory to another and from the United States as a whole.

The application of the Federal tax rules to the territories varies from one possession to another. Three territories, Guam, the Northern Mariana Islands, and the U.S. Virgin Islands, are referred to as mirror Code possessions because the Internal Revenue Code of 1986, as amended (the “Code”)4 serves as the internal tax law of those territories (substituting the particular territory for the United States wherever the Code refers to the United States). A resident of one of those territories generally files a single tax return only with the territory of which the individual is a resident, and not with the United States. American Samoa and Puerto Rico, by contrast, are non-mirror Code possessions. These two territories have their own internal tax laws, and a resident of either American Samoa or Puerto Rico may be required to file income tax returns with both the territory of residence and the United States.

Federal tax rules apply to the territories in a manner that is different from their application in relation to both the States and foreign countries. Broadly, an individual resident of a territory is exempt from U.S. tax on income that has a source in that territory but is subject to U.S. tax on U.S.-source and non-possession-source income. A corporation that is organized in a territory is generally treated as a foreign corporation for U.S. tax purposes. On the other hand, a number of Code provisions have effect in one or all of the territories as if the territories were States. For example, the tax credit for research and experimentation has been available for research conducted in a territory. Historically, the Federal tax rules also have included preferences for territory activities. Until its expiration in 2006, the section 936 possession tax credit permitted qualifying U.S. corporations a credit against their U.S. tax liability in respect of possession-source income. After section 936 expired, a similar, temporary provision was enacted for American Samoa activities, and the section 199 domestic production activities deduction was expanded temporarily to include production activities conducted in Puerto Rico. These special rules for American Samoa and Puerto Rico expired at the end of last year.

Questions related to the Federal tax rules’ application to the territories include whether the application should be uniform across the territories; whether the application should be based on a single principle such as State treatment or foreign country treatment; and whether U.S. bilateral income treaties should in any cases include the territories in their scope.

3 The 50 states of the United States and the District of Columbia are referred to in this document as the

“States.”

4 Unless otherwise noted, section numbers in this document are sections of the Code.

3

I. ECONOMIC CONDITIONS OF U.S. TERRITORIES

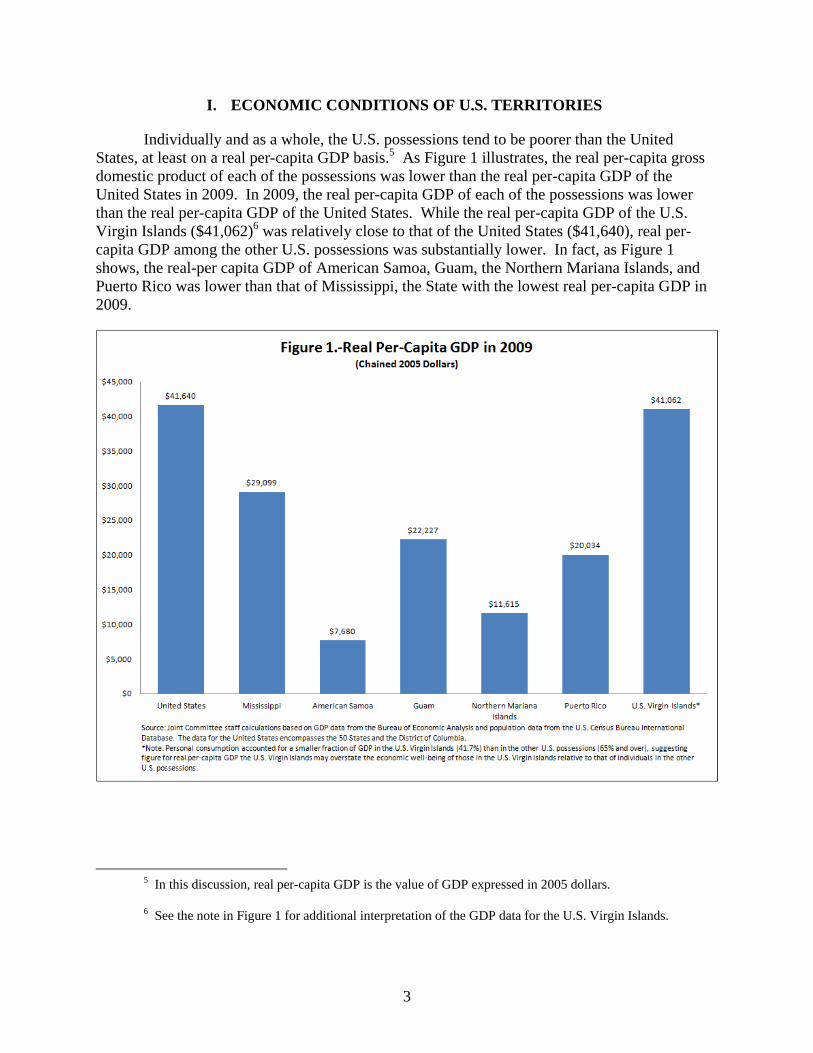

Individually and as a whole, the U.S. possessions tend to be poorer than the United States, at least on a real per-capita GDP basis.5 As Figure 1 illustrates, the real per-capita gross domestic product of each of the possessions was lower than the real per-capita GDP of the United States in 2009. In 2009, the real per-capita GDP of each of the possessions was lower than the real per-capita GDP of the United States. While the real per-capita GDP of the U.S. Virgin Islands ($41,062)6 was relatively close to that of the United States ($41,640), real per-capita GDP among the other U.S. possessions was substantially lower. In fact, as Figure 1 shows, the real-per capita GDP of American Samoa, Guam, the Northern Mariana Islands, and Puerto Rico was lower than that of Mississippi, the State with the lowest real per-capita GDP in 2009.

5 In this discussion, real per-capita GDP is the value of GDP expressed in 2005 dollars.

6 See the note in Figure 1 for additional interpretation of the GDP data for the U.S. Virgin Islands.

4

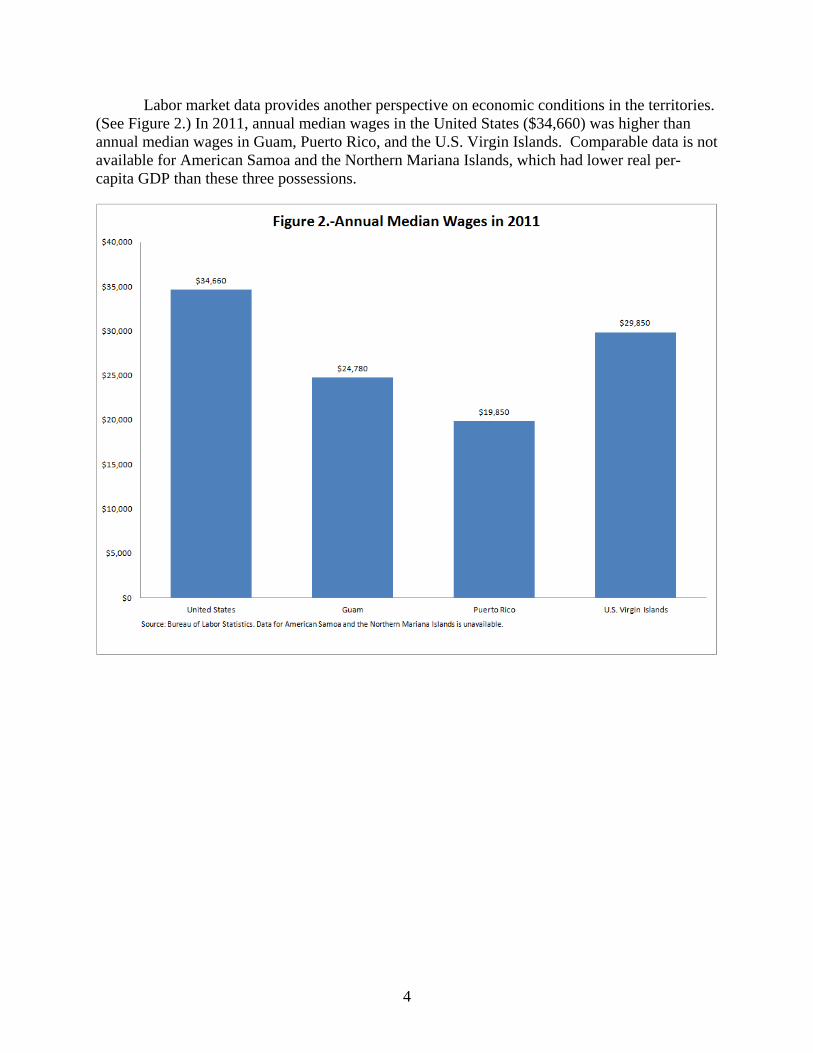

Labor market data provides another perspective on economic conditions in the territories. (See Figure 2.) In 2011, annual median wages in the United States ($34,660) was higher than annual median wages in Guam, Puerto Rico, and the U.S. Virgin Islands. Comparable data is not available for American Samoa and the Northern Mariana Islands, which had lower real per-capita GDP than these three possessions.

5

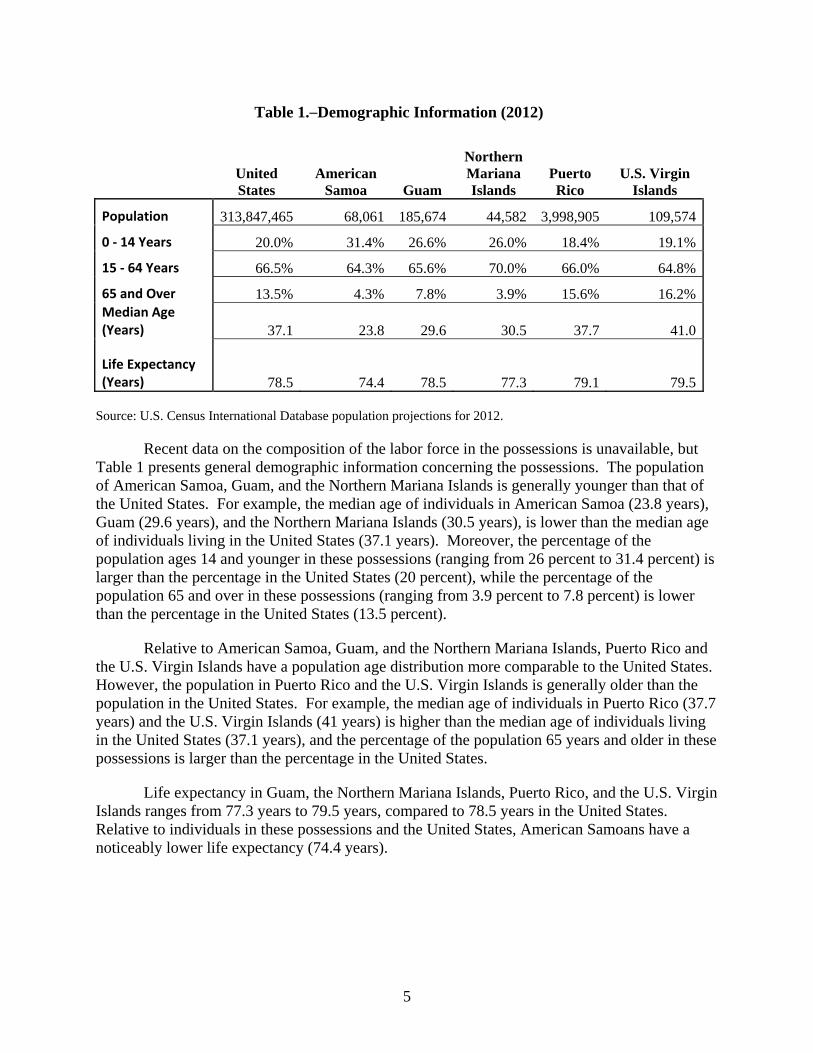

Table 1.─Demographic Information (2012)

United States

American Samoa Guam

Northern Mariana Islands

Puerto Rico

U.S. Virgin Islands

Population 313,847,465 68,061 185,674 44,582 3,998,905 109,574

0 ‐ 14 Years 20.0% 31.4% 26.6% 26.0% 18.4% 19.1%

15 ‐ 64 Years 66.5% 64.3% 65.6% 70.0% 66.0% 64.8%

65 and Over 13.5% 4.3% 7.8% 3.9% 15.6% 16.2%Median Age (Years) 37.1 23.8 29.6 30.5 37.7 41.0

Life Expectancy (Years) 78.5 74.4 78.5 77.3 79.1 79.5

Source: U.S. Census International Database population projections for 2012.

Recent data on the composition of the labor force in the possessions is unavailable, but Table 1 presents general demographic information concerning the possessions. The population of American Samoa, Guam, and the Northern Mariana Islands is generally younger than that of the United States. For example, the median age of individuals in American Samoa (23.8 years), Guam (29.6 years), and the Northern Mariana Islands (30.5 years), is lower than the median age of individuals living in the United States (37.1 years). Moreover, the percentage of the population ages 14 and younger in these possessions (ranging from 26 percent to 31.4 percent) is larger than the percentage in the United States (20 percent), while the percentage of the population 65 and over in these possessions (ranging from 3.9 percent to 7.8 percent) is lower than the percentage in the United States (13.5 percent).

Relative to American Samoa, Guam, and the Northern Mariana Islands, Puerto Rico and the U.S. Virgin Islands have a population age distribution more comparable to the United States. However, the population in Puerto Rico and the U.S. Virgin Islands is generally older than the population in the United States. For example, the median age of individuals in Puerto Rico (37.7 years) and the U.S. Virgin Islands (41 years) is higher than the median age of individuals living in the United States (37.1 years), and the percentage of the population 65 years and older in these possessions is larger than the percentage in the United States.

Life expectancy in Guam, the Northern Mariana Islands, Puerto Rico, and the U.S. Virgin Islands ranges from 77.3 years to 79.5 years, compared to 78.5 years in the United States. Relative to individuals in these possessions and the United States, American Samoans have a noticeably lower life expectancy (74.4 years).

6

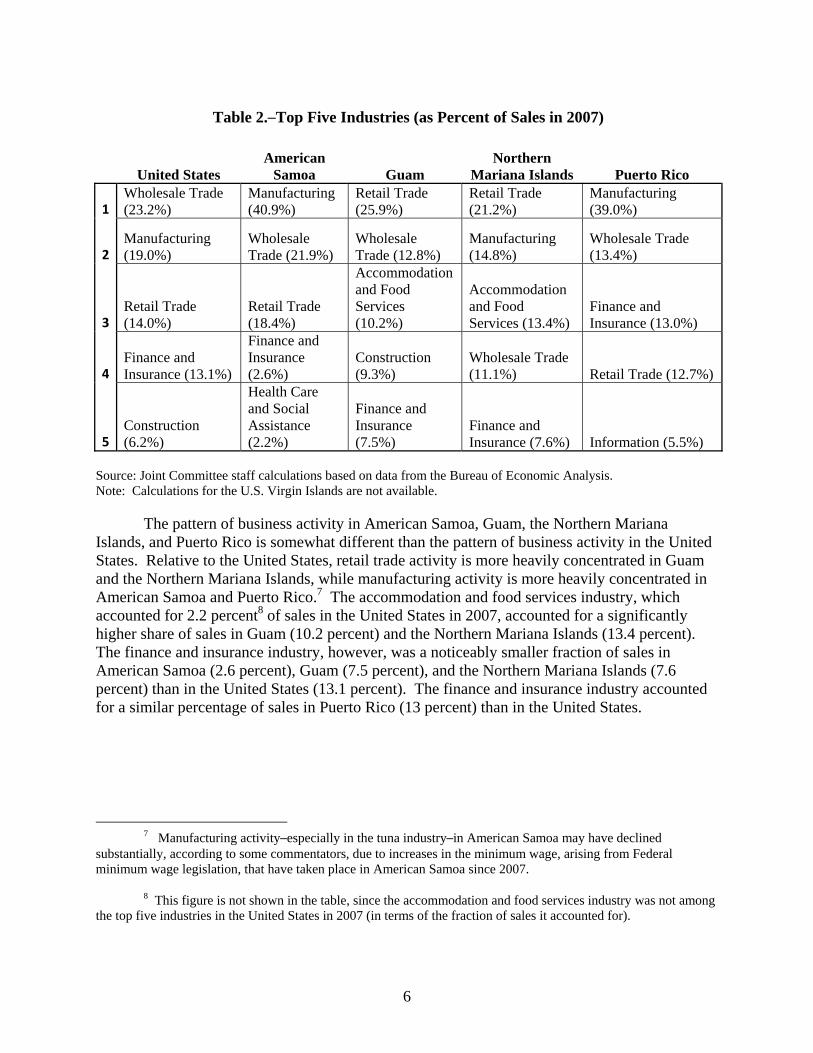

Table 2.─Top Five Industries (as Percent of Sales in 2007)

United States American

Samoa Guam Northern

Mariana Islands Puerto Rico

1 Wholesale Trade (23.2%)

Manufacturing (40.9%)

Retail Trade (25.9%)

Retail Trade (21.2%)

Manufacturing (39.0%)

2 Manufacturing (19.0%)

Wholesale Trade (21.9%)

Wholesale Trade (12.8%)

Manufacturing (14.8%)

Wholesale Trade (13.4%)

3 Retail Trade (14.0%)

Retail Trade (18.4%)

Accommodation and Food Services (10.2%)

Accommodation and Food Services (13.4%)

Finance and Insurance (13.0%)

4 Finance and Insurance (13.1%)

Finance and Insurance (2.6%)

Construction (9.3%)

Wholesale Trade (11.1%) Retail Trade (12.7%)

5 Construction (6.2%)

Health Care and Social Assistance (2.2%)

Finance and Insurance (7.5%)

Finance and Insurance (7.6%) Information (5.5%)

Source: Joint Committee staff calculations based on data from the Bureau of Economic Analysis. Note: Calculations for the U.S. Virgin Islands are not available.

The pattern of business activity in American Samoa, Guam, the Northern Mariana Islands, and Puerto Rico is somewhat different than the pattern of business activity in the United States. Relative to the United States, retail trade activity is more heavily concentrated in Guam and the Northern Mariana Islands, while manufacturing activity is more heavily concentrated in American Samoa and Puerto Rico.7 The accommodation and food services industry, which accounted for 2.2 percent8 of sales in the United States in 2007, accounted for a significantly higher share of sales in Guam (10.2 percent) and the Northern Mariana Islands (13.4 percent). The finance and insurance industry, however, was a noticeably smaller fraction of sales in American Samoa (2.6 percent), Guam (7.5 percent), and the Northern Mariana Islands (7.6 percent) than in the United States (13.1 percent). The finance and insurance industry accounted for a similar percentage of sales in Puerto Rico (13 percent) than in the United States.

7 Manufacturing activity─especially in the tuna industry─in American Samoa may have declined

substantially, according to some commentators, due to increases in the minimum wage, arising from Federal minimum wage legislation, that have taken place in American Samoa since 2007.

8 This figure is not shown in the table, since the accommodation and food services industry was not among the top five industries in the United States in 2007 (in terms of the fraction of sales it accounted for).

7

II. PRESENT LAW U.S. TAX PROVISIONS RELATED TO U.S. TERRITORIES

A. Overview of the U.S. Tax Provisions Related to U.S. Territories

1. In general

While U.S. statutory laws apply to the U.S. possessions, and natives of U.S. possessions are U.S. citizens or nationals, for tax purposes the Code generally treats the U.S. possessions as foreign countries. When the Code uses the term in a geographical sense, the “United States” includes only the 50 States and the District of Columbia.9

The meaning of the term possession is not uniform throughout the Code, and is not among the defined terms in section 7701. For purposes of assessment and collection of Federal taxes, the possessions are generally treated the same as the States, except as provided in the Revised Organic Act of the Virgin Islands and the Organic Act of Guam with respect to certain taxes covered over to the treasuries of the U.S. Virgin Islands and Guam.10 Taxes imposed by the Code in any possession are collected under the direction of the Secretary. Taxes with respect to any individual to whom section 931 or 932(c) applies are covered into the Treasury of the specific possession of which the individual is a bona fide resident.11

Income derived from U.S. possessions is ordinarily treated as foreign-source income. Entities organized in U.S. possessions are generally treated as foreign persons. Of the various trust territories and possessions of the United States, only those with local taxing authorities that have entered into a tax coordination agreement with the United States, that is, American Samoa, Guam, the Northern Mariana Islands, Puerto Rico, and the U.S. Virgin Islands, are provided special treatment in the Code and are the focus of this pamphlet.12

Three of the possessions employ a “mirror system” of taxation. In Guam,13 the Commonwealth of Northern Mariana Islands14 and the U.S. Virgin Islands,15 the United States

9 Sec. 7701(a)(9).

10 Sec. 7651.

11 Sec. 7654.

12 See Rev. Proc. 2006-23, 2007-1 C.B. 900. In addition to these five jurisdictions, other territories may be considered possessions of the United States for political purposes but are not generally accorded special status under the Code or by Treasury. But see, e.g., section 274(h)(3)(A) (defines “North American area” to include the United States, its possessions and the Trust Territory of the Pacific Islands, as well as Canada and Mexico) and Rev. Rul. 2011-26, 2011-1 C.B. 803 (explains the current status of the entities that were part of the Trust Territory when 274(h) was enacted, and rules that “possessions” includes, in addition to the five discussed in this pamphlet, Baker Island, Howland Island, Jarvis Island, Johnston Island, Kingman Reef, the Midway Islands, Palmyra Atoll, Wake Island, and any other United States islands, cays, and reefs that are not part of the fifty states or the District of Columbia).

13 The 1950 Organic Act of Guam, 48 U.S.C. sec. 1421i(h) (2012).

8

Federal income tax laws are in effect (or “mirrored”) as the local territorial income tax. Proceeds of the mirror codes are generally paid to the treasuries of the possessions. Not all of the Code is mirrored; generally, only the income tax provisions of the Code are mirrored.16 In the tax statutes as in effect in each of these possessions, the name of the possession is substituted for “United States,” and vice-versa. Although the reverse substitution is not explicitly described in any of the operative statutes for the possessions, two-way mirroring has been required to give effect to the intent of the mirroring requirement. To the extent that mirroring would produce a result manifestly incompatible with the Code or other provisions of the United States Code, mirroring is not required.17

The Tax Reform Act of 1986 (the “1986 Act”) granted authority to Guam, the Commonwealth of Northern Mariana Islands and American Samoa to cease use of the mirror system, and authorized the U.S. Virgin Islands to impose local taxes at variance from the rates in the Code as mirrored. It repealed the relevant rules that provide coordination between the Federal statutes and the statutes as mirrored in Guam, American Samoa and the Northern Mariana Islands and amended the coordination rules for the U.S. Virgin Islands. The changes are not yet in effect for Guam or the Northern Mariana Islands, because the effective date is contingent upon the existence of an implementation agreement, and the contingency has not been met.18

2. Income taxation of individuals

The United States generally imposes income tax on the worldwide income of U.S. citizens and residents. Thus, all income earned by a U.S. citizen or resident, whether from

14 Covenant to Establish a Commonwealth of the Northern Mariana Islands in Political Union with the

United States of America (“Covenant”), Act of March 24, 1976, Pub. L. No. 94-241, 48 U.S.C. sec. 1801 (note) (2012); President Ronald Reagan, “Placing Into Full Force and Effect the Covenant With the Commonwealth of the Northern Mariana Islands, and the Compacts of Free Association With the Federated States of Micronesia and the Republic of the Marshall Islands,” Proclamation No. 5564, 51 Fed. Reg. 40,399-400 (Nov. 3, 1986).

15 Act July 12, 1921, ch 44, 42 Stat. 123, popularly known as the Naval Service Appropriation Act, 1922, codified at 48 U.S.C. sec. 1397 (2012).

16 For example, 48USC 1421i(d) specified that for Guam, the mirrored sections include most of subtitle A (income tax), chapters 24 and 25 (withholding tax), and subtitle F (administrative) as applicable to the income tax.

17 Gumataotao v. Director of Revenue and Taxation of Guam, 236 F.3d 1077 (9th Cir. 2001) [“Only those provisions of the I.R.C. that are “manifestly inapplicable or incompatible with the intent of [the Income Tax Section]” do not apply to Guam taxpayers. 48 U.S.C. § 1421i(d); see Sayre & Co. v. Riddell, 395 F.2d 407, 410 (9th Cir. 1968) (en banc) (“Sayre”) (G.T.I.T. “mirrors” the I.R.C., except where “manifestly inapplicable or incompatible”).”]

18 The special effective date for the revision of section 931 and repeal of section 935 is provided in section 1277(b) of the 1986 Act, stating “The amendments made by this subtitle shall apply with respect to Guam, American Samoa, or the Northern Mariana Islands (and to residents thereof and corporations created or organized therein) only if (and so long as) an implementing agreement under section 1271 is in effect between the United States and such possession.” Tax Reform Act of 1986, Pub. L. No. 99-514, sec. 1277(a), (b), 100 Stat. 2085, 2600 (1986).

9

sources inside or outside the United States, is taxable whether or not the individual lives within the United States. All U.S. citizens and residents whose gross income for a taxable year is not less than the sum of the personal exemption amount and the basic standard deduction are required to file an annual U.S. individual income tax return.

The taxable income of a U.S. citizen or resident is equal to the taxpayer’s total worldwide income less certain exclusions, exemptions, and deductions. A foreign tax credit, with limitations, may be claimed for foreign income taxes paid or accrued, or, alternatively, foreign taxes may be treated as a deduction. Income taxes paid in a U.S. possession are generally creditable taxes for these purposes.

Generally, special U.S. income tax rules apply with respect to U.S. persons who are bona fide residents of U.S. possessions and who have possession source income or income effectively connected with the conduct of a trade or business within a possession.19 The term bona fide resident means a person who meets a two-part test with respect to American Samoa, Guam, the U.S. Virgin Islands, Puerto Rico, or the Northern Mariana Islands as the case may be, for the taxable year. First, an individual must be present in the U.S. possession for at least 183 days in the taxable year.20 Second, an individual must (1) not have a tax home outside such possession during the taxable year and (2) not have a closer connection to the United States or a foreign country during such year.

Individual residents living in U.S. possessions generally are subject to either a single- or double-filing system with respect to their income. Individual residents subject to section 931 or 933 (that is, bona-fide residents of American Samoa and Puerto Rico) operate under a double-filing system. Under a double-filing system, income that is not exempt from U.S. tax under section 931 or 933, and meets certain filing thresholds, must be reported to the United States on a U.S. return. Thus, an individual operating under a double-filing system that has income from sources outside the U.S. possession where the individual is resident (e.g., a Puerto Rico individual with non-Puerto Rico-source income) must file a tax return in the United States and in the U.S. possession where the individual is a bona-fide resident if such income is subject to reporting. Income reported on a U.S. return by a bona-fide resident of a U.S. possession is generally subject to the same U.S. tax treatment that applies to individuals resident in the United States.

In contrast, individual residents subject to section 932(c) or 935 (that is, bona fide residents of the U.S. Virgin Islands, as well as the Northern Mariana Islands and Guam21)

19 For more detail about these special rules, see generally, Joel D. Kuntz and Robert J. Peroni, U.S.

International Taxation, “U.S. Taxation Relating to Possessions” (Warren Gorman and Lamont-RIA, 2005), Part D.

20 Sec. 937(a). Treasury regulations provide guidance related to meeting the presence test, including exceptions for certain extended absences from the possession. Treas. Reg. sec. 1.937-1.

21 The repeal of section 935 is not yet effective for Guam or the Northern Marianas, due to failure to meet the condition in the special effective date provided in section 1277(b) of the 1986 Act, which states, “The amendments made by this subtitle shall apply with respect to Guam, American Samoa, or the Northern Mariana Islands (and to residents thereof and corporations created or organized therein) only if (and so long as) an

10

generally operate under a single-filing system. Under a single-filing system, income is only reported in one jurisdiction, based on bona-fide residency. Thus, an individual operating under a single-filing system generally does not have to file a tax return with the United States. In a single-filing system, income is often allocated between the U.S. possession and the United States through a cover over22 mechanism.

As a general rule, the principles for determining whether income is U.S. source are applicable for purposes of determining whether income is possession source. In addition, the principles for determining whether income is effectively connected with the conduct of a U.S. trade or business are applicable for purposes of determining whether income is effectively connected to the conduct of a possession trade or business. However, except as provided in regulations, any income treated as U.S. source income or as effectively connected with the conduct of a U.S. trade or business is not treated as income from within any possession or as effectively connected with a trade or business within any such possession.23

For purposes of the foreign earned income exclusion, the U.S. possessions are not treated as foreign countries. Thus, residents of U.S. possessions do not qualify for the foreign earned income or housing exclusion under section 911 of the Code because they are not considered resident abroad.24

U.S. citizens who relinquish their citizenship and U.S. residents who terminate their long-term residency may be subject to special tax rules intended to limit any tax benefits from expatriation. Certain persons expatriating before June 17, 2008 are subject to an alternative tax regime for a period of 10 years if they meet certain income and net-worth thresholds or they fail to comply with certain U.S. Federal tax obligations.25 Certain persons expatriating after June 16, 2008, are treated as if all property was sold on the day before their expatriation date for its fair market value.26 U.S. citizens and lawful permanent residents who leave the United States and establish residency in one of the possessions are generally not considered to have either relinquished their U.S. citizenship or terminated their U.S. residency; however, the special source rules may apply to U.S. citizens and residents that leave the United States and establish

implementing agreement under section 1271 is in effect between the United States and such possession.” Tax Reform Act of 1986, Pub. L. No. 99-514, sec. 1277(a), (b), 100 Stat. 2085, 2600 (1986).

22 Cover over refers to the collection of certain taxes and fees by the U.S. Treasury and subsequent payment of such taxes and fees to the governments of the territories as specified.

23 Sec. 937(b).

24 Treas. Reg. secs. 1.911-2(g),(h).

25 Sec. 877.

26 Sec. 877A.

11

residency in American Samoa, the Northern Mariana Islands, or Guam during the 10-year period beginning when the person first becomes a resident.27

3. Income taxation of corporations

U.S. corporations

U.S. corporations are subject to U.S. income tax on their worldwide income, whether derived in the United States or abroad. Income earned by a domestic parent corporation from foreign operations conducted by foreign corporate subsidiaries generally is subject to U.S. tax when the income is distributed as a dividend to the domestic corporation. Until such repatriation, the U.S. tax on such income is generally deferred. However, certain anti-deferral regimes may cause the domestic parent corporation to be taxed on a current basis in the United States with respect to certain categories of passive or highly mobile income earned by its foreign subsidiaries. The main anti-deferral regimes in this context are the controlled foreign corporation rules of subpart F28 and the passive foreign investment company rules.29 A foreign tax credit is generally available to offset, in whole or in part, the U.S. tax owed on this foreign-source income, whether earned directly by the domestic corporation, repatriated as a dividend, or included under one of the anti-deferral regimes, subject to certain limitations.

Foreign corporations

Foreign corporations with U.S. source income are generally subject to U.S. tax on a net basis at graduated rates on income effectively connected to a U.S. trade or business. U.S.-source passive income paid to a foreign corporation is generally taxed on a gross basis at a withholding rate of 30 percent. Income earned by a foreign corporation from its foreign operations generally is subject to U.S. tax only when such income is distributed to any U.S. persons that hold stock in such corporation. However, several sets of anti-deferral rules impose current U.S. tax on certain income earned by a U.S. person through a foreign corporation.

Corporations formed in the U.S. possessions are generally treated as foreign corporations for U.S. tax purposes. Thus, the foreign status of entities formed in a U.S. possession means that the shareholders of such entities may be subject to U.S. anti deferral regimes, such as the controlled foreign corporation regime (subpart F), and the shareholders of such entities may have to pay current U.S. tax on their foreign source income.

However, notwithstanding the general rule that companies organized in a U.S. possession are treated as foreign corporations, certain qualifying corporations are deemed not to be foreign corporations for purposes of withholding taxes on passive income. Corporations organized in

27 See section 1277(e) of the 1986 Act. Under this special source rule, gains from dispositions of certain property held by a U.S. person prior to becoming a resident in American Samoa, the Northern Mariana Islands, or Guam are treated as income from sources within the United States for all purposes of the Code.

28 Secs. 951-964.

29 Secs. 1291-1298.

12

American Samoa, Guam, the U.S. Virgin Islands, or the Northern Mariana Islands are not subject to withholding tax on payments from corporations organized in the United States, provided that certain local ownership and activity requirements are met.30 In turn, each of those possessions have adopted local internal revenue codes that provide a zero rate of withholding tax on payments made by corporations organized in such possession to corporations organized in the United States. Thus, certain corporations organized in American Samoa, Guam, the U.S. Virgin Islands, or the Northern Mariana Islands can receive dividend payments from a U.S. subsidiary at a zero rate of withholding.

4. Estate and gift taxation

U.S. citizens and residents

U.S. citizens and residents are subject to estate tax on the transfer of their worldwide estate at the time of death. The taxable estate is equal to the decedent’s worldwide gross estate, less allowable deductions (including the marital deduction). Certain credits are allowed, including the unified credit, which directly reduce the amount of the estate tax.31

U.S. citizens and residents are subject to gift tax on transfers of property by gift made directly or indirectly, in trust or otherwise. Thus, the gift tax applies to transfers of property, regardless of where such property is situated. The amount of a taxable gift is determined by the fair market value of the property on the date of the gift. An annual exclusion (adjusted periodically for inflation)32 applies to gift given in a calendar year.33

A U.S. citizen residing in a U.S. possession is treated as a citizen for estate and gift tax purposes unless he acquired U.S. citizenship solely by reason of birth or residence within the possession.34

Nonresident aliens

The estate of a nonresident alien generally is taxed at the same estate tax rates applicable to U.S. citizens, but the taxable estate includes only property situated within the United States

30 Sec. 881(b).

31 The unified credit amount is the tax computed on the applicable exclusion amount or $5.12 million for 2012 (indexed for inflation). In 2012, the maximum estate tax rate is 35 percent. The applicable exclusion amount and maximum rates currently sunset for estates of decedents dying after 2012. The applicable exclusion amount for decedents dying after 2012 reverts to $1million and the maximum estate tax rate reverts to 55 percent.

32 Sec. 2503(b). The annual gift tax exclusion amount for 2012 is $13,000.

33 An applicable amount applies for computing the gift tax on lifetime transfers ($5.12 million for 2012) and for 2012 the maximum gift tax rate is 35 percent. The applicable amount and 35-percent tax rate is currently scheduled to sunset for gifts made after 2012 when the maximum rate reverts to 55 percent and the applicable exclusion amount is $1 million.

34 Secs. 2208 (estate tax) and 2501(b) (gift tax).

13

that is owned by the decedent at death (and certain property transferred during life subject to reserved interests or powers). This estate generally includes the value at death of all real and personal tangible property situated in the United States and certain intangible property, such as stock of a domestic corporation, considered to be situated in the United States.35 The estate of a nonresident alien is allowed a unified credit of $13,00036 and under treaty may instead be allowed a pro rata portion of the generally applicable unified credit.

Nonresident alien individuals are subject to gift tax with respect to certain transfers by gift of U.S.-situated property under the same tax rate schedule applicable to U.S. citizens. The tax applies only where the value of the transfer exceeds the annual exclusion amount.37 Such property includes real estate and tangible property located within the United States. Nonresident aliens generally are not subject to U.S. gift tax on the transfer of intangibles, such as stock or securities, regardless of where such property is situated.

A U.S. citizen residing in a possession is treated as a nonresident alien for estate and gift tax purposes if the individual’s U.S. citizenship was acquired solely by reason of birth or residence within the possession.38 Estates of decedents who are treated as nonresident aliens for purposes of this rule are allowed a credit against the estate tax equal to the greater of $13,000 or that proportion of $46,800 which the value the decedent’s gross estate situated in the United States bears to the value of the entire gross estate wherever situated.39

5. Payroll taxes

Employees and employers in the United States are subject to payroll taxes for the Federal Insurance Contributions Act (“FICA”) that fund Social Security and certain Medicare benefits, Federal unemployment insurance payroll tax (“FUTA”), and the withholding tax for Federal income tax.40 FICA imposes tax on employers based on the amount of wages paid to an employee during the year. The tax imposed is composed of two parts: (1) the old age, survivors, and disability insurance (“OASDI”) tax as a percentage of covered wages; and (2) the Medicare hospital insurance (“HI”) tax amount, also a percentage of covered wages. In addition to the tax on employers, each employee is subject to FICA taxes equal to the amount of tax imposed on the employer. The employee level tax generally must be withheld and remitted to the Federal government by the employer. Certain categories of services and employment are often exempt from FICA, including foreign agricultural workers with appropriate visas.

35 For these purposes the United States means the 50 States and the District of Columbia.

36 Sec. 2102(b). This credit essentially acts to shelter the first $60,000 of the taxable estate from Federal estate tax.

37 The annual exclusion amount is $13,000 for 2012 (indexed for inflation).

38 Sec. 2209 (estate tax) and 2501(c) (gift tax).

39 Sec. 2102(b)(2).

40 Secs. 3121(a) and 3402(a).

14

Similar FICA payroll tax obligations generally apply to persons in any of the U.S. possessions.41 In contrast, employees and employers in the possessions are generally not subject to the withholding at source for Federal income tax, although they are subject to withholding for local taxes.42 These payroll obligations of the employers are generally applicable to Federal agencies with personnel in the possession. Finally, only Puerto Rico and the U.S. Virgin Islands are within the scope of the FUTA obligations.43 Wages paid to persons employed in Puerto Rico or the U.S. Virgin Islands are subject to FUTA on wages for each calendar year paid by a covered employer to each employee. Federal unemployment insurance payroll taxes are used to fund programs maintained by the local jurisdictions for the benefit of unemployed workers. Employers in such jurisdictions with programs approved by the Federal government may qualify for a credit of 5.4 percentage points against the 6.0 percent tax rate, making the minimum, net Federal unemployment tax rate 0.6 percent.44

6. Excise tax

U.S. excise taxes generally do not apply within the U.S. possessions. However, U.S. excise taxes equal to the taxes on domestically produced articles are imposed on articles of manufacture brought into the United States from Puerto Rico and the Virgin Islands and withdrawn for consumption or sale.45 These taxes are generally covered over to the respective treasuries. Articles imported from the United States into Puerto Rico, the Virgin Islands, Guam, and American Samoa are generally exempt from U.S. excise tax; however articles imported from the United States into Puerto Rico and the Virgin Islands are subject to a local excise tax equal to the tax imposed under the revenue laws of the United States.46 Provisions related to the allowance of drawback47 on excise tax on articles exported from the Unites States are extended

41 Internal Revenue Service, Federal Tax Guide for Employers in the U.S. Virgin Islands, Guam, American

Samoa, and the Commonwealth of the Northern Mariana Islands (Publication 80 Circular SS), 2012.

42 Under section 3401(a)(8), most wages paid to U.S. persons for services performed in one of the possessions are excluded if the payments are subject to withholding by the possession, or, in the case of Puerto Rico, the payee is a bona fide resident of the possession for the full year.

43 Section 3306(j) provides that for purposes of the FUTA tax, the term State includes both Puerto Rico and the Virgin Islands.

44 While the gross FUTA tax rate was 6.2 percent (until July 2011), the net rate was 0.8 percent. The credit is not available to employers who are delinquent in repaying a Federal loan.

45 Sec. 7652.

46 Sec. 7653.

47 A drawback is a refund of certain duties, taxes and fees paid by the importer of record and granted to a drawback claimant upon the exportation, or destruction of eligible articles upon which the duties, taxes and fees have been paid. The purpose of drawback is to place U.S. exporters on equal footing with foreign competitors by refunding most of the duties, taxes and fees paid on imports used in domestic manufacturing intended for export.

15

to like articles when shipped from the United States to Puerto Rico, the Virgin Islands, Guam, or American Samoa.48

7. Tax incentives

The Code contains other provisions that provide incentives for certain activities. Some of the provisions expand the incentives provided for State and local jurisdictions to the U.S. possessions while others are specifically targeted at certain activities within a specific U.S. possession. Examples of State and local incentives that apply to U.S. possessions include the exclusion of interest on State and local bonds,49 the credit for research and experimentation,50 and the low-income housing credit.51 Other incentives are described in the discussion of the individual possessions below.

8. Tax treaties

In addition to the U.S. and foreign statutory rules for the taxation of foreign income of U.S. persons and U.S. income of foreign persons, bilateral income tax treaties limit the amount of income tax that may be imposed by one treaty partner on residents of the other treaty partner. For example, treaties often reduce or eliminate withholding taxes imposed by a treaty country on certain types of income, such as dividends, interest, and royalties paid to residents of the other treaty country. Treaties also include provisions governing the creditability of taxes imposed by the treaty country in which income is earned in computing the amount of tax owed to the other country by its residents with respect to that income.

There are no bilateral tax treaties between any of the possession and any foreign country. In addition, U.S. treaties typically do not include the possessions in the definition of United States for treaty purposes. However, for purposes of identifying the scope of exchange of information agreements, the possessions are included.52 Treaties further provide procedures under which inconsistent positions taken by the treaty countries on a single item of income or deduction may be mutually resolved by the two countries. To the extent that inconsistent positions are taken by the Internal Revenue Service (“IRS”) and the taxing authority of one of the possessions, relief from double taxation may be available by negotiation between the two taxing agencies. Each of the U.S. possessions has an agreement (variously styled as

48 Sec. 7653(c).

49 Sec. 103. Section 103(c)(2) defines State to include any possession of the United States.

50 Sec. 41. The credit is generally not available to foreign research; however, section 41(d)(4)(F) defines foreign research to be research conducted outside the United States, the Commonwealth of Puerto Rico, or any possession of the United States.

51 Sec. 42. Section 42(h)(8)(B) defines State to include a possession of the United States.

52 See, e.g., Agreement between the Government of the United State of America and the Government of the Republic of Panama for Tax Cooperation and the Exchange of Information Relating to Taxes Tax Information Agreement between United States and Panama, entered into force April 18, 2011.

16

coordination, exchange of information, or implementation agreements) that permits entry into a memorandum of understanding to resolve such conflicts. The process for seeking such relief is similar to that available under competent authority procedures.53

53 See section 1.02 of Rev. Proc. 2006-23, 2007-1 C.B. 900.

17

B. Overview of U.S. Tax Provisions Related to American Samoa

1. In general

Unlike the other U.S. possessions, individuals born in American Samoa are U.S. nationals, not U.S. citizens.54 However, all residents of American Samoa are subject to tax as U.S. citizens, with an exclusion provided for American Samoa-sourced income. Samoans are also subject to local income tax in American Samoa. Also, unlike the U.S. Virgin Islands, Guam, and the Northern Mariana Islands, the Code does not include a provision similar to section 932 or 935 that provides for relief from a double filing requirement. Thus, residents of American Samoa potentially have to file with both the United States and the American Samoa government.

The Code was not imposed on American Samoa as it was with the other mirror Code possessions. American Samoa adopted its own income tax system and chose the Code as its local income tax in 1963. The 1986 Act allowed American Samoa to continue with its own local income tax system, but conditioned such authority on the existence of a tax implementation agreement between American Samoa and the United States. Such agreement was signed in 1988, but declared effective January 1, 1987, to prevent a gap in American Samoa’s authority to impose its income tax. The American Samoa tax system is similar to a mirror system in that the words American Samoa are substituted for United States, where appropriate. However, the American Samoa income tax does not replace U.S. Federal tax, it creates instead a territorial income tax modeled after the federal tax. Instead of provisions like section 932 or 935 that create a single filing requirement, bona fide residents of American Samoa are granted an exclusion from U.S. gross income on all American Samoan-source income and income effectively connected to an American Samoa trade or business (similar to the operation of section 933 for Puerto Rico residents).55

2. Taxation of individuals

Individual residents of American Samoa are taxed on their worldwide income pursuant to the local tax imposed by American Samoa. A foreign tax credit is allowed for taxes paid to the United States, a foreign country, or another U.S. possession. Nonresident aliens are only subject to tax on their American-Samoa source income.

Under section 931, U.S. citizens or aliens who are bona fide residents of American Samoa for the entire tax year are allowed an exclusion from U.S. gross income for income derived from sources within American Samoa and income effectively connected with the conduct of a trade or business by such individual within American Samoa. As mentioned above, the foreign earned income exclusion under section 911 is not available to individuals residing in

54 U.S. nationals may live in the United States without restriction and naturalize as U.S. citizens under the

same rules as other resident aliens. The distinction between a U.S. national and a U.S. citizen is that a U.S. national cannot vote or hold elected office.

55 Sec. 931.

18

a U.S. possession; however in comparing the foreign earned income exclusion to the exclusion under section 931, the section 931 exclusion is more generous because it is unlimited in its amount. The exclusion for possession source income, however, does not apply to compensation paid to employees of the United States and its agencies. An individual with compensation from a U.S. government employer must file a U.S. return.

3. Taxation of corporations

In general, a corporation organized under the laws of American Samoa is a foreign corporation for U.S. tax purposes. The United States taxes foreign corporations only on income that has a sufficient nexus to the United States. Generally, this would include a 30 percent tax on the gross amount of its fixed, determinable, annual or periodic income from U.S. sources and a net basis tax at regular rates on income effectively connected with the conduct of a U.S. trade or business.

The 30-percent gross-basis withholding tax does not apply to payments made to a corporation organized in American Samoa so long as the corporation satisfies certain requirements intended to ensure a sufficient connection to American Samoa.56

For American Samoa tax purposes, corporations chartered in American Samoa are domestic corporations. Corporations formed outside American Samoa are regarded as foreign corporations. For American Samoa tax purposes, the taxable income of a corporation is calculated the same as for U.S. corporations under the U.S. Code. Foreign taxes paid by American Samoa corporate taxpayers are creditable towards their American Samoa income tax.

4. Excise tax

U.S. excise taxes generally do not apply within the U.S. possessions. Articles imported from the United States into American Samoa are generally exempt from U.S. excise tax; additionally, provisions related to the allowance of drawback on tax on articles exported from the Unites States are extended to like articles when shipped from the United States to American Samoa.57

5. Tax incentives

A domestic corporation that was an existing credit claimant with respect to American Samoa and that elected the application of the section 936 possession tax credit58 for its last

56 Sec. 881(b)(1).

57 Sec. 7653.

58 Certain domestic corporations with business operations in the U.S. possessions were eligible for a possession tax credit. Secs. 27(b), 936. This credit offset the U.S. tax imposed on certain income related to operations in the U.S. possessions. Subject to certain limitations (including, as one of two alternatives, the economic activity-based limitation), the amount of the possession tax credit allowed to any domestic corporation equaled the portion of that corporation’s U.S. tax that was attributable to the corporation’s non-U.S. source taxable income from (1) the active conduct of a trade or business within a U.S. possession, (2) the sale or exchange of

19

taxable year beginning before January 1, 2006 was temporarily allowed a credit based on the corporation’s economic activity-based limitation with respect to the corporation’s activities in American Samoa, except that no credit is allowed for the amount of any American Samoa income taxes.59

The corporation’s economic activity-based limitation with respect to American Samoa, was equal to the sum of (1) 60 percent of the corporation’s qualified American Samoa wages and allocable employee fringe benefit expenses and (2) 15 percent of the corporation’s depreciation allowances with respect to short-life qualified American Samoa tangible property, plus 40 percent of the corporation’s depreciation allowances with respect to medium-life qualified American Samoa tangible property, plus 65 percent of the corporation’s depreciation allowances with respect to long-life qualified American Samoa tangible property.

The credit was allowed for the first six taxable years of a corporation that begin after December 31, 2005, and before January 1, 2012.

substantially all of the assets that were used in such a trade or business, or (3) certain possessions investment. No deduction or foreign tax credit was allowed for any possessions or foreign tax paid or accrued with respect to taxable income that was taken into account in computing the credit under section 936.

To qualify for the possession tax credit for a taxable year, a domestic corporation was required to satisfy two conditions. First, the corporation was required to derive at least 80 percent of its gross income for the three-year period immediately preceding the close of the taxable year from sources within a possession. Second, the corporation was required to derive at least 75 percent of its gross income for that same period from the active conduct of a possession business. Sec. 936(a)(2). The section 936 credit generally expired for taxable years beginning after December 31, 2005.

59 The credit was not part of the Code but was computed based on the rules of sections 30A and 936.

20

C. Overview of U.S. Tax Provisions Related to Guam

1. In general

Guam employs a mirror system of taxation. The rules for coordination of U.S. and Guam income taxes are found in section 935. Although that section was repealed by the 1986 Act, which also authorized Guam to enact its own system of taxation, the 1986 Act changes are not yet in effect, because the effective date of the repeal was contingent upon the existence of an implementation agreement in effect between Guam and the United States.60 The United States and Guam executed a tax implementation agreement in 1989, expected to enter into force on January 1, 1991. However, such agreement was amended in December, 1990, and the effective date was postponed indefinitely. Thus, without an implementation agreement, pre-1986 law, including an earlier coordination agreement, remains in effect.61

2. Taxation of individuals

Under section 935, individual residents of the United States or Guam are required to file only one tax return with respect to their income tax liability. In general, U.S. residents file only with the United States, Guamanian residents file only with Guam, and those individuals subject to Guamanian or U.S. income tax who are not residents of either Guam or the United States generally file with the United States. Bona fide residence is determined based on the entire taxable year, as opposed to the close of the taxable year, and joint filers file based on the spouse who has the greater adjusted gross income for the taxable year. In addition, with respect to taxation of U.S. and Guamanian citizens and resident individuals, the United States is treated as part of Guam for purposes of Guamanian taxation and Guam is treated as part of the United States for purposes of U.S. taxation. The United States generally covers over to (that is, pays) the Guamanian Treasury certain taxes collected from individuals on Guamanian source income and withholding tax on U.S. Federal personnel employed or stationed in Guam. Similarly, Guam covers over to the U.S. Treasury certain taxes collected from individuals on U.S. source income.

3. Taxation of corporations

In general, a corporation chartered in Guam is treated as a domestic corporation for Guamanian tax purposes and a foreign corporation for U.S. tax purposes. A Guamanian corporation that receives U.S. source income (other than certain passive income) or income

60 The special effective date for the revision of section 931 and repeal of section 935 is provided in section

1277(b) of the 1986 Act, stating “The amendments made by this subtitle shall apply with respect to Guam, American Samoa, or the Northern Mariana Islands (and to residents thereof and corporations created or organized therein) only if (and so long as) an implementing agreement under section 1271 is in effect between the United States and such possession.” Tax Reform Act of 1986, Pub. L. No. 99-514, sec. 1277(a), (b), 100 Stat. 2085, 2600 (1986).

61 See section 1.02 of Rev. Proc. 2006-23, 2007-1 C.B. 900. (In explaining how to apply for relief from potential double taxation as a result of conflicts between Federal income tax and position of the taxing authorities in one of the possessions, the IRS identifies a tax coordination agreement executed with Guam in 1977 as the only agreement with Guam that is in effect.)

21

effectively connected to a trade or business in the United States has to file a U.S. return and pay U.S. tax on that income. Guamanian taxpayers are generally entitled to a foreign tax credit for taxes paid to the United States, a foreign country, or another U.S. possession. Other tax credits are also allowed, as mirrored by Guam.

Mirroring the U.S. Code, Guam imposes a 30 percent withholding tax on dividends and other payments made to corporations who are foreign for Guamanian tax purposes. However, the Guam Foreign Investment Equity Act (the “GFIE Act”) reduced withholding rates on both individuals and corporations with respect to Guam-source income by deeming Guam to be part of the United States for purposes of U.S. income tax treaties and thus the same rates agreed to in U.S. income tax treaties shall apply to Guam.62 For example, under the GFIE Act, the reduced withholding rates under the U.S.-Japan treaty apply to dividend payments from a Guamanian corporation to a Japanese shareholder. According to legislative history, the high statutory withholding rates were considered an impediment to foreign investment in Guam, which accounts for approximately 75 percent of all investment in that territory.63

4. Payroll taxes

Although FICA payroll tax obligations generally apply to employers and employees in Guam, a special exception from the definition of employment is provided for services performed by residents of the Philippines who enter Guam on a nonresident basis.64 Employers in Guam are not subject to FUTA or the withholding at source for Federal income tax. They are subject to withholding for Guamanian taxes.

5. Excise taxes

U.S. excise taxes generally do not apply within the U.S. possessions. Articles imported from the United States into Guam are generally exempt from U.S. excise tax; additionally, provisions related to the allowance of drawback on tax on articles exported from the United States are extended to like articles when shipped from the United States to Guam.65

62 Pub. L. No. 107-211, 116 Stat. 1051, August 6, 2002, amending 48 USC sec. 1421(i).

63 Hon. Robert A. Underwood, 147 Cong. Rec. E40, Jan. 30, 2001.

64 Sec. 3121(b)(18).

65 Sec. 7653.

22

D. Overview of U.S. Tax Provisions Related to Commonwealth of the Northern Mariana Islands

1. In general

The Commonwealth of the Northern Mariana Islands (“Northern Mariana Islands” or “Northern Marianas”) employs a mirror system of taxation. Although adopted from the systems used in both U.S. Virgin Islands and Guam, it has several significant differences. First, references in the Code to Guam are deemed to also refer to the Northern Mariana Islands.66 Thus, the mirror Code of the Northern Marianas is linked to the Guamanian mirror code. Second, the Northern Mariana Islands has the authority to rebate the tax imposed by its mirror code with respect to Northern Marianas-source income. The Northern Mariana Islands rebate a significant amount of this tax, but impose three separate taxes that cover most of the same types of income at lower rates.67

The 1986 Act authorized The Northern Mariana Islands to continue with its mirror system of taxation without regard to whether Guam enacts its own tax laws. It also authorized the Northern Marianas to impose its own additional taxes contingent on a tax implementation agreement between the United States and Northern Marianas. The application of new Code provisions (section 931) and the repeal of section 935, set forth in the 1986 Act, are contingent on the entry into force of a tax implementation agreement.68 At this time, no tax agreement between Northern Marianas and the United States has been reached, nor has the agreement between Guam and the United States entered into force.

2. Taxation of individuals

As mentioned above, the Northern Marianas’ tax system consists of the same tax laws that apply to Guam. Thus, the filing rules for the Northern Marianas are the same as for Guam, including the single filing rule under section 935. Like other U.S. possessions, bona fide residency is determined based on a two-part test that requires an individual to be present in the U.S. possession for at least 183 days in the taxable year, while precluding such individual from having a tax home outside the Northern Marianas or having a closer connection to the United States or a foreign country. The major difference between the tax structure of Northern Marianas and Guam is that Northern Marianas taxpayers may claim a nonrefundable credit against their Northern Marianas tax liability with respect to Northern Marianas source income. Rebate rates can range from 50 to 90 percent.

66 Covenant, sec. 601, Act of March 24, 1976, Pub. L. No. 94-241, 48 U.S.C. sec. 1801 (note) (2012).

67 Covenant, sec. 602, Act of March 24, 1976, Pub. L. No. 94-241, 48 U.S.C. sec. 1801 (note) (2012).

68 The special effective date for the revision of section 931 and the repeal of section 935 is provided in section 1277(b) of the 1986 Act, stating “The amendments made by this subtitle shall apply with respect to Guam, American Samoa, or the Northern Mariana Islands (and to residents thereof and corporations created or organized therein) only if (and so long as) an implementing agreement under section 1271 is in effect between the United States and such possession.” Tax Reform Act of 1986, Pub. L. No. 99-514, sec. 1277(a), (b), 100 Stat. 2085, 2600 (1986).

23

3. Taxation of corporations

For the Northern Mariana Islands tax purposes, domestic corporations are those formed in the Northern Marianas. Foreign corporations are all corporations formed elsewhere, including the 50 United States and the District of Columbia. Northern Marianas corporations are subject to tax on their worldwide income and a foreign tax credit is allowed for income taxes paid to the United States, a foreign country, or another U.S. possession. As with other U.S. possessions, corporations in the Northern Marianas that meet certain income and ownership requirements may be subject to a zero withholding tax rate on passive income from sources within the United States. Other U.S. source income will generally be taxed on a net basis at U.S. graduated rates.

The full amount of corporate income tax liability must be paid to the Northern Marianas government, but as with individuals, a certain percentage is generally rebated to the taxpayer. The rebate rates are the same for corporations as individuals. Corporations with a tax liability of $20,000 or less are entitled to a 90 percent rebate, a tax liability of $100,000 receives a 70 percent rebate, and for tax liabilities over $100,000 a 50 percent rebate is granted.

4. Payroll taxes

Certain categories of services and employment are often exempt from FICA, including foreign agricultural workers with appropriate visas. The Northern Marianas grants a Commonwealth Only Transitional Worker (CW) visa classification, which is available only for work in Northern Marianas. Persons admitted to Northern Marianas on such a visa are not exempt from social security and Medicare taxes unless they also satisfy the requirements for an exemption on some other basis (for example, a temporary worker may hold a valid U.S. H-2 visa in addition to the CW visa). Absent such an exemption, employers are required to withhold and pay social security and Medicare taxes.69

Although similar FICA payroll tax obligations generally apply to persons in any of the possessions, employees and employers in the Northern Marianas are not subject to FUTA or the withholding at source for Federal income tax. They are subject to withholding for Northern Marianas taxes. The payroll obligations of the employers are applicable to Federal agencies with personnel in the possession. By agreement with the Northern Marianas, all Federal employers with personnel resident in Northern Marianas (including the Department of Defense) are required to withhold Northern Marianas income taxes (rather than Federal income taxes) and deposit the Northern Marianas taxes with the Northern Marianas Treasury.

69 Internal Revenue Service, Federal Tax Guide for Employers in the U.S. Virgin Islands, Guam, American

Samoa, and the Commonwealth of the Northern Mariana Islands (Publication 80 Circular SS), 2012.

24

E. Overview of U.S. Tax Provisions Related to Puerto Rico

1. In general

Although Puerto Rico is generally treated as a foreign country for U.S. tax purposes, a person born in Puerto Rico is typically treated as a U.S. citizen for U.S. tax purposes. As a result of the hybrid foreign-domestic treatment, the general principles of U.S. taxation are qualified by many special rules applicable to U.S. citizens and residents of, and U.S. persons doing business in, Puerto Rico. In many cases, these special rules have the effect of dividing tax authority between the U.S. Federal government and the government of Puerto Rico. Other rules are designed to prevent U.S. Federal tax laws from negating tax incentives used by Puerto Rico to attract investors. The United States has also used tax incentives to assist Puerto Rico in obtaining economic development through investments by U.S. companies. The argued need for these special tax incentives has been attributed, in part, to what some observers contend are the additional costs imposed on investing in Puerto Rico because of its status as a U.S. possession.70

2. Income taxation of individuals

Under the Jones Act,71 Puerto Rico is deemed to be a part of the United States for purposes of acquiring U.S. citizenship by place of birth. Thus, a person born in Puerto Rico is typically a U.S. citizen for U.S. tax purposes. However, section 933 of the Code provides that income derived from sources within Puerto Rico by an individual who is a bona fide resident of Puerto Rico for an entire taxable year generally is excludable from U.S. gross income and thus exempt from U.S. taxation, even if such resident is a U.S. citizen.

Income excludible from U.S. gross income under section 933 is generally subject to taxation by Puerto Rico. Items of income earned from sources outside of Puerto Rico by U.S. citizens who reside in Puerto Rico generally are subject to U.S. taxation. The principles that generally apply for determining income from sources within and without the United States also generally apply in determining income from sources within and without a possession. In addition, the principles for determining whether income is effectively connected with the conduct of a U.S. trade or business are applicable for purposes of determining whether income is effectively connected to the conduct of a possession trade or business. However, except as provided in regulations, any income treated as U.S. source income or as effectively connected with the conduct of a U.S. trade or business is not treated as income from within any possession or as effectively connected with a trade or business within any such possession.72

A bona fide resident of Puerto Rico is an individual that meets a two-part test for the taxable year. First, the individual must be present in Puerto Rico for at least 183 days in the

70 Joint Committee on Taxation, General Explanation of the Tax Reform Act of 1986 (JCS-10-87), May 4,

1987, pp. 999-1000, available at http://www.jct.gov/jcs-10-87.pdf.

71 39 Stat. 951 (1917).

72 Sec. 937(b).

25

taxable year. Second, the individual must (1) not have a tax home73 outside Puerto Rico during the taxable year and (2) not have a closer connection74 to the United States or a foreign country during such year.75

3. Income taxation of corporations

In general, a corporation organized under the laws of Puerto Rico is a foreign corporation for U.S. tax purposes. The United States taxes foreign corporations only on income that has a sufficient nexus to the United States. Generally, this would include a 30-percent tax on the gross amount of its fixed, determinable, annual, or periodic income from U.S. sources and a net basis tax at regular rates on income effectively connected with the conduct of a U.S. trade or business.

The withholding tax rate on U.S. source dividends paid to a corporation created or organized in Puerto Rico is lowered from 30 percent to 10 percent, to create parity with the generally applicable 10-percent withholding tax imposed by Puerto Rico on Puerto Rico-source dividends paid to U.S. corporations.76 The lower rate applies only if the same local ownership and activity requirements are met that are applicable to corporations organized in other possessions receiving dividends from corporations organized in the United States. If Puerto Rico increases its 10-percent withholding tax imposed on dividends paid to U.S. corporations, the U.S. income tax withholding rate on dividends paid to Puerto Rico corporations will be increased to 30 percent.

4. Payroll taxes

Employers and employees in Puerto Rico are subject to FICA and FUTA.77 Certain statutory exceptions from the definition of wages for FICA and FUTA purposes do not apply in the case of employers and employees in Puerto Rico. For example, the exceptions from the definition of wages for amounts under an educational assistance program or a dependent care assistance program78 do not apply because the exceptions are by reason of specific Code sections (i.e., sections 127 and 129) that are not applicable in the case of Puerto Rico employers and employees.

73 Determined under the principles of sec. 911(d)(3).

74 Determined under the principles of sec. 7701(b)(3)(B)(ii).

75 Sec. 937(a).

76 Sec. 881(b)(2).

77 Secs. 3121(e) and 3306(j).

78 Secs. 3121(a)(18) and 3306(b)(13).

26

5. Excise taxes

In general

U.S. excise taxes generally do not apply within the U.S. possessions. However, U.S. excise taxes equal to the taxes on domestically produced articles are imposed on articles of manufacture brought into the United States from Puerto Rico and withdrawn for consumption or sale.79 These taxes are generally covered over to the Treasury of Puerto Rico. A special excise tax rule also applies when articles manufactured in the United States are shipped to Puerto Rico. In such cases, the articles are exempt from Federal excise taxes and, upon being entered in Puerto Rico, are subject to a tax equal in rate and amount to the excise tax imposed in Puerto Rico upon similar articles of Puerto Rico manufacture. 80

Cover over of excise taxes on Puerto Rico products

Revenues collected by the United States from the excise taxes imposed on certain articles coming into the United States from Puerto Rico generally are covered over to the Puerto Rico Treasury.81 With respect to otherwise eligible excise taxes imposed on articles not containing distilled spirits, revenues are covered over to Puerto Rico only if the cost or value of materials produced in Puerto Rico plus the direct costs of processing operations performed in Puerto Rico equal at least 50 percent of the value of the article at the time it is brought into the United States. Moreover, no cover over is permitted on such articles if Puerto Rico provides a direct or indirect subsidy with respect to the article which is of a different kind or in an amount greater than the subsidies which Puerto Rico generally offers to industries producing articles not subject to Federal excise tax.

With respect to Federal excise taxes imposed on articles containing distilled spirits that are manufactured in Puerto Rico and shipped into the United States, revenues are covered over to the Puerto Rico Treasury only if at least 92 percent of the alcoholic content of such articles is attributable to rum. The amount of excise taxes covered over to Puerto Rico from such articles cannot exceed $10.50 per proof gallon. This limitation was temporarily increased to $13.25 for articles brought into the United States after June 30, 1999, however the increase in the limitation does not apply to articles brought into the United States after December 31, 2011.

Cover over of excise taxes on rum imported from other countries

A provision of the Code added by the Caribbean Basin Economic Recovery Act82 provides a special rule for excise taxes collected on rum imported into the United States from any country. Such excise taxes are covered over to the treasuries of Puerto Rico and the U.S.

79 Sec. 7652.

80 Sec. 7653.

81 Sec. 7652(a).

82 Pub. L. No. 98-67, August, 5, 1983.

27

Virgin Islands, under a formula prescribed by the Treasury Department for the division of such tax collections between Puerto Rico and the U.S. Virgin Islands. The formula for division of excise tax collected from other countries is roughly based on the relative market share of rum produced in Puerto Rico and the U.S. Virgin Islands. The law stipulates that the Puerto Rico share not exceed 87.626889 percent and not fall below 51 percent. This formula resulted in approximately 88 percent of revenues from rum excise taxes being covered over to Puerto Rico in fiscal year 2009.83

6. Tax incentives

The generally applicable section 199 deduction for income from domestic production activities was expanded temporarily to include production activities conducted in Puerto Rico.84 For purposes of computing the wage limitation for the deduction, wages include wages paid for services performed in Puerto Rico. This provision is not applicable to tax years beginning after December 31, 2011.

83 Steven Maquire, Congressional Research Service, The Rum Excise Tax Cover-Over: Legislative History

and Current Issues (Report R41028), October 27, 2011, p. 4, available at http://www.crs.gov/Products/R/PDF/R41028.pdf.

84 Sec. 199(d)(8).

28

F. Overview of U.S. Tax Provisions Related to U.S. Virgin Islands

1. In general

The U.S. Virgin Islands has an income tax system that “mirrors” the U.S. Code. The U.S. Virgin Islands may also impose certain local income taxes in addition to taxes imposed by the mirror Code. The Code provides rules for coordination of United States and U.S. Virgin Islands taxation.85 It permits the U.S. Virgin Islands to reduce or remit tax otherwise imposed by the mirror code if the tax is attributable to U.S. Virgin Islands source income or income effectively connected to the conduct of a trade or business in U.S. Virgin Islands.86 The U.S. Virgin Islands has exercised that authority to provide development incentives for certain types of businesses operating within its borders. Under such initiatives, companies can receive a 90 percent reduction in their tax liability on certain income.

2. Taxation of individuals

Under the mirror Code, U.S. Virgin Islands citizens and residents are taxable on their worldwide income. A foreign tax credit is allowed for income taxes paid to the United States, foreign countries, and other possessions of the United States. In general, a bona fide resident of the U.S. Virgin Islands is required to file and pay tax only to the possession; compliance with that obligation satisfies any Federal income tax filing obligation. All other U.S. residents or citizens with income from U.S. Virgin Island sources are subject to a dual filing requirement.